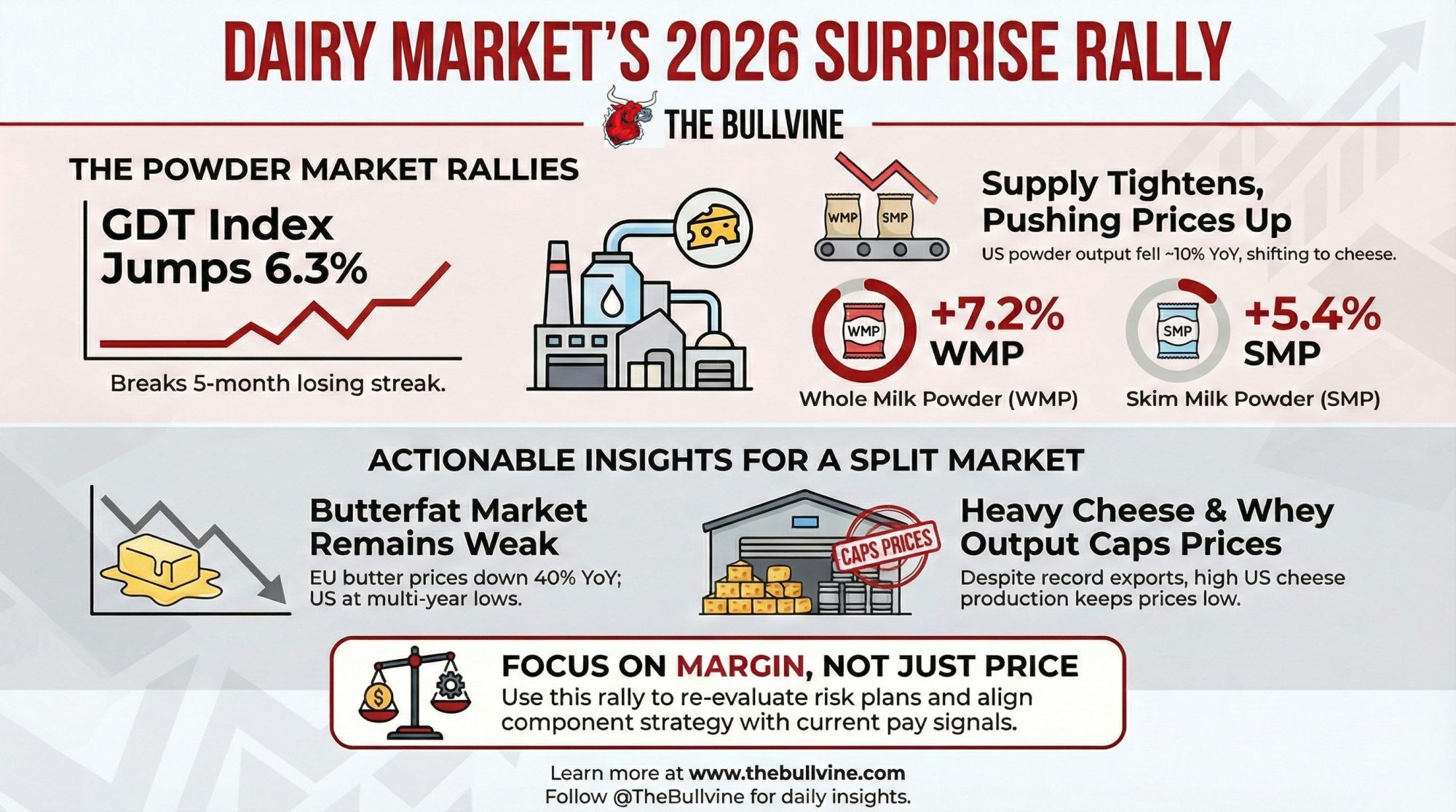

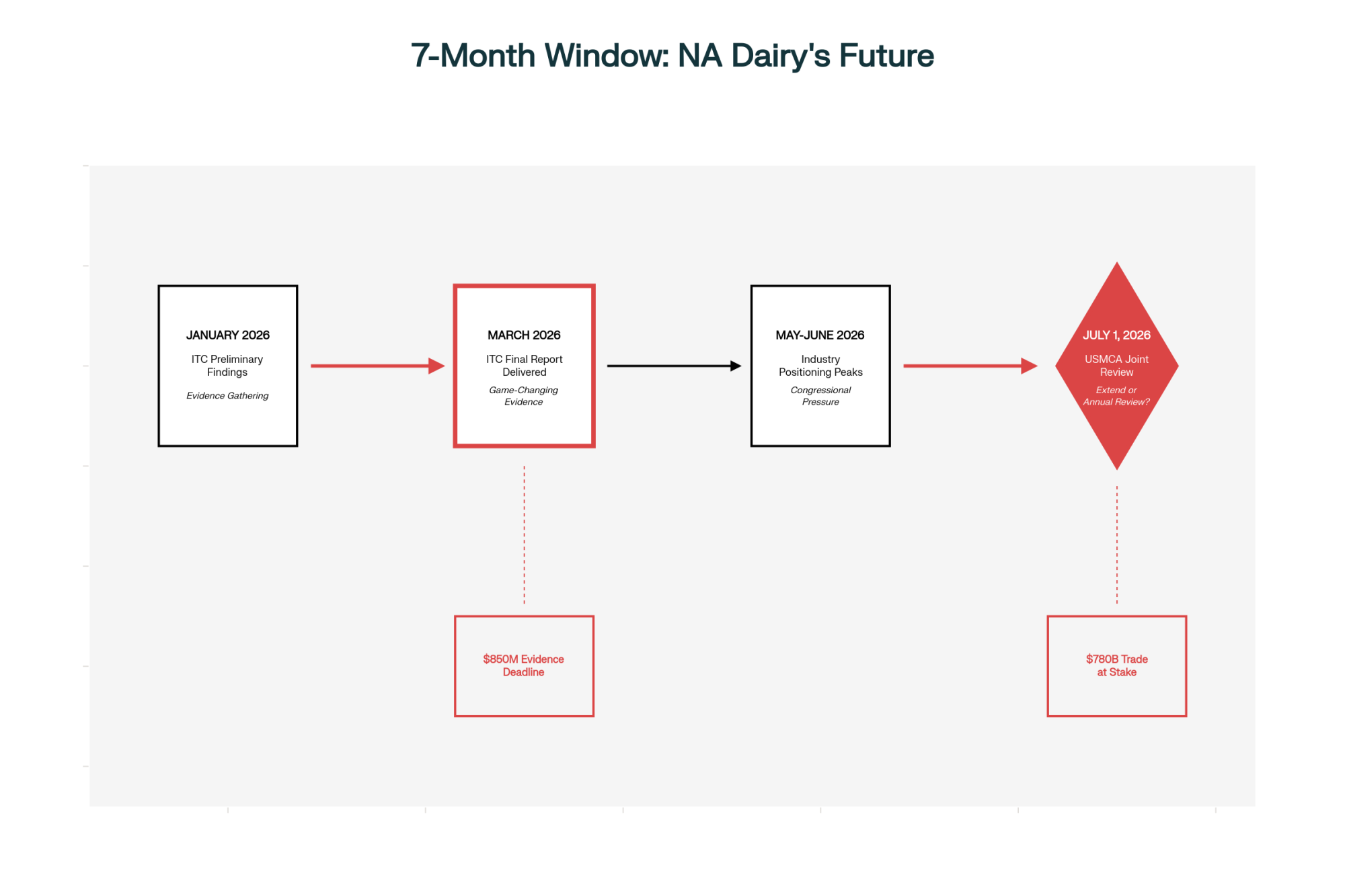

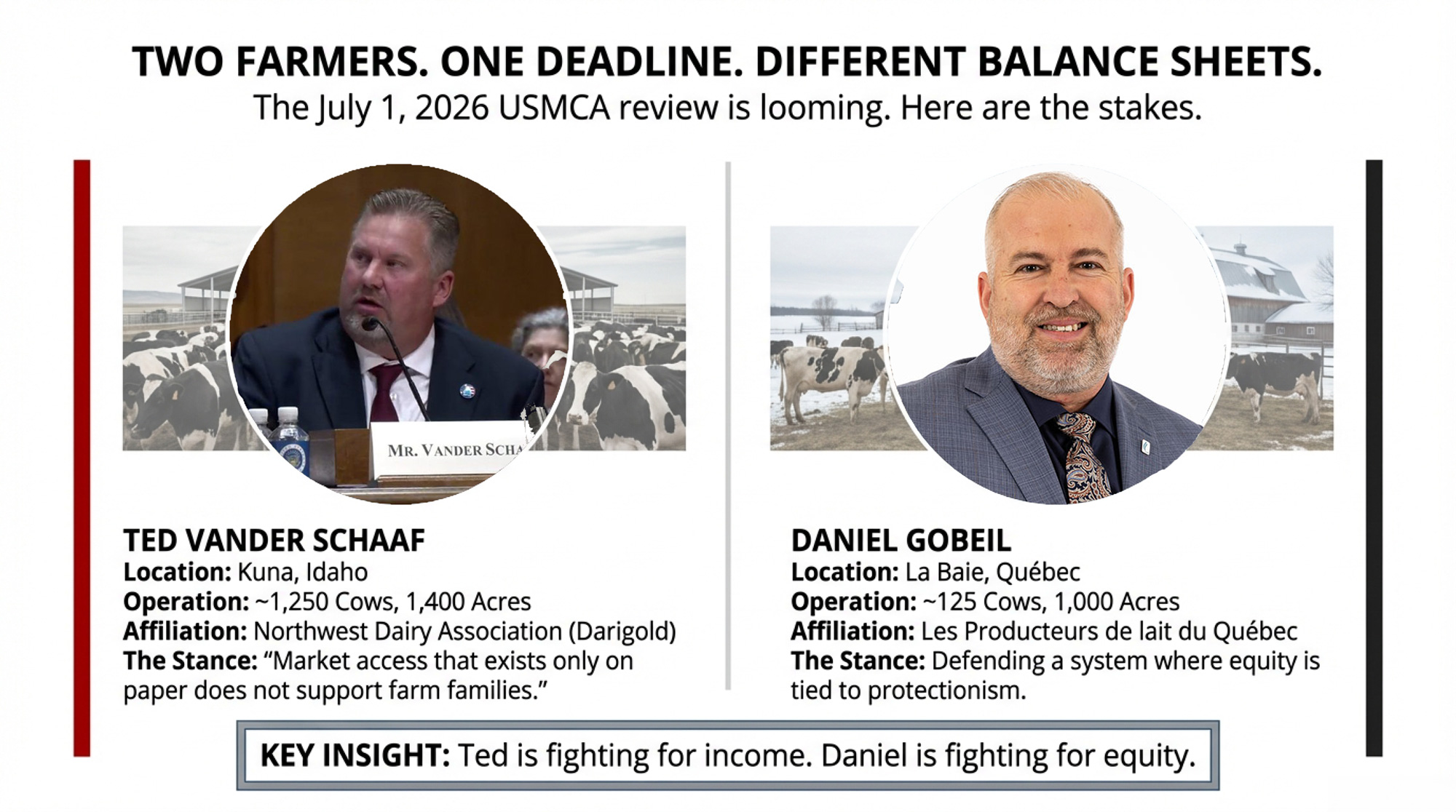

The USMCA review hits July 1. Two dairy farmers — one in Idaho, one in Québec — are watching the same deadline with completely different balance sheets at stake. Here’s the barn math for both sides of the border.

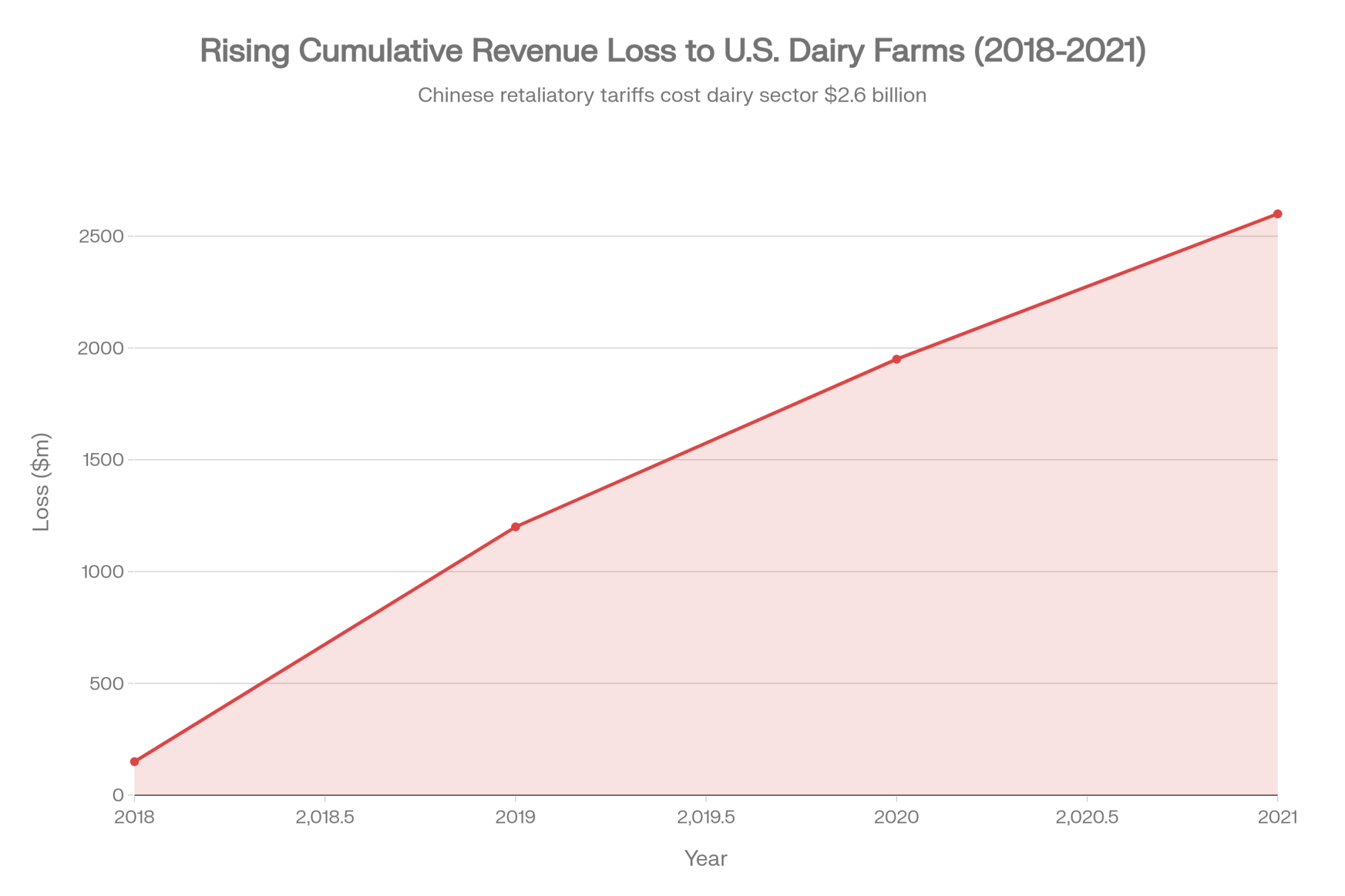

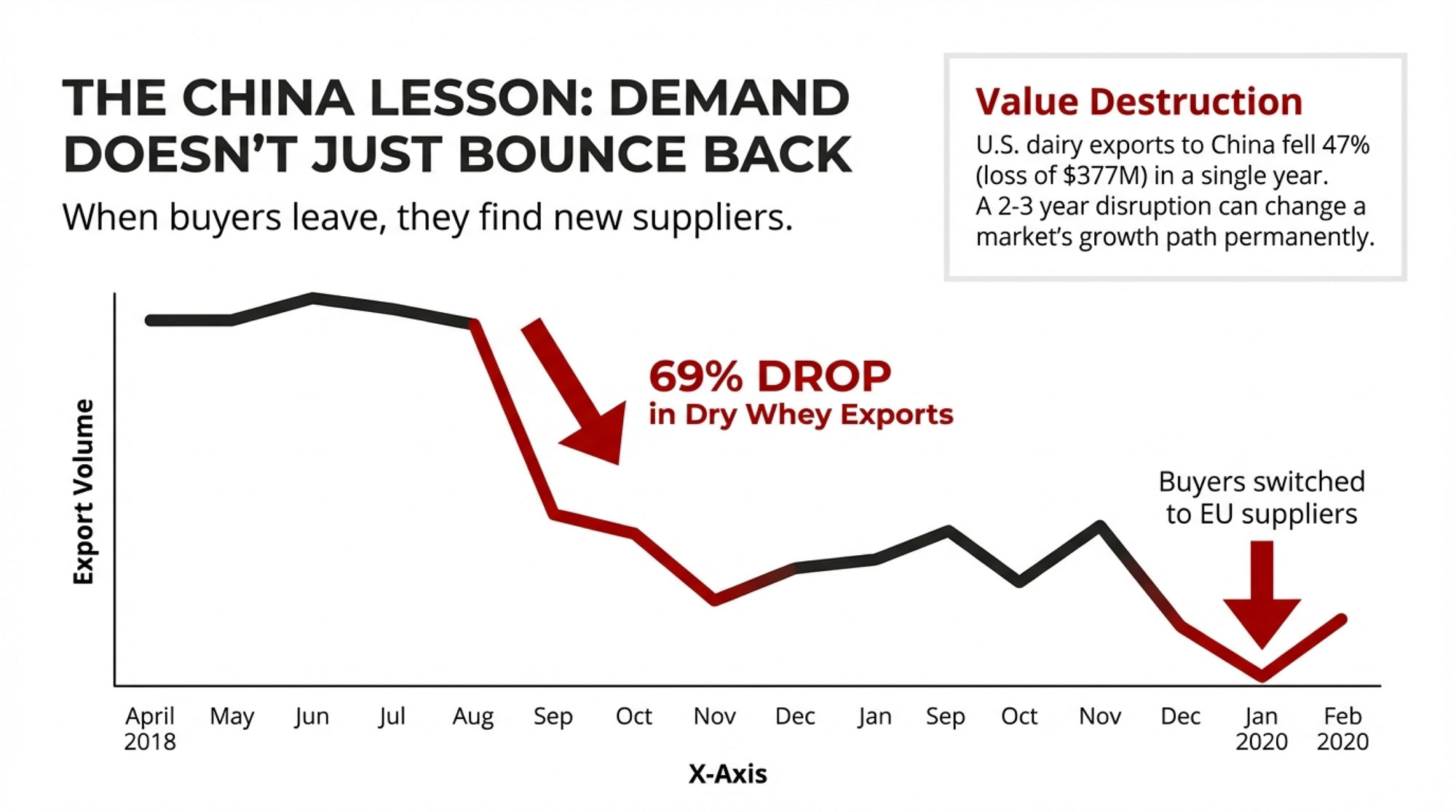

The U.S. dairy industry told the Senate this week that Canada is blocking roughly $200 million per year in dairy market access it promised under the USMCA — called CUSMA in Canada. Spread that number across American production, and the farm-level impact lands around five cents per hundredweight. Before Congress approved this deal, the U.S. International Trade Commission projected it would boost dairy exports to Canada by 43.8% — about $227 million once fully implemented (USITC Publication 4889, April 2019). Both countries are spending enormous political capital on a fight where the per-farm stakes are far smaller than either side’s press releases suggest.

On February 12, Ted Vander Schaaf delivered that case to the Senate Finance Committee. Vander Schaaf milks approximately 1,250 Holsteins near Kuna, Idaho, on 1,400 acres of forage, is a third-generation member-owner of the Northwest Dairy Association (the co-op behind Darigold), and board member of the Idaho Dairymen’s Association. “Market access that exists only on paper does not support farm families, pay employees, or justify new investment,” he told the Committee. And then the line that landed: “A firm base depends on Canada upholding their end of the bargain”.

About 1,500 kilometres northeast, Daniel Gobeil runs Ferme du Fjord in La Baie, Québec — deep in Saguenay-Lac-Saint-Jean — with about 125 lactating cows across more than 1,000 acres of barley, oats, and soybeans (DFC). Gobeil is Vice-President of Dairy Farmers of Canada and President of Les Producteurs de lait du Québec. When Vander Schaaf told the Senate that Canada isn’t upholding its end of the bargain, the implications land directly on operations like his.”

What’s Actually on the Table This July

The USMCA hits its first mandatory joint review by July 1, 2026, as required by Article 34.7. All three countries decide: extend the agreement for 16 years (to 2042), continue with annual reviews until the 2036 expiration, or walk away. U.S. Trade Representative Jamieson Greer left no ambiguity in December 2025: “Could it be exited? Yes, it could be exited. Could it be revised? Yes. Could it be renegotiated? Yes. That is the purpose of that clause, and all of those things are on the table”.

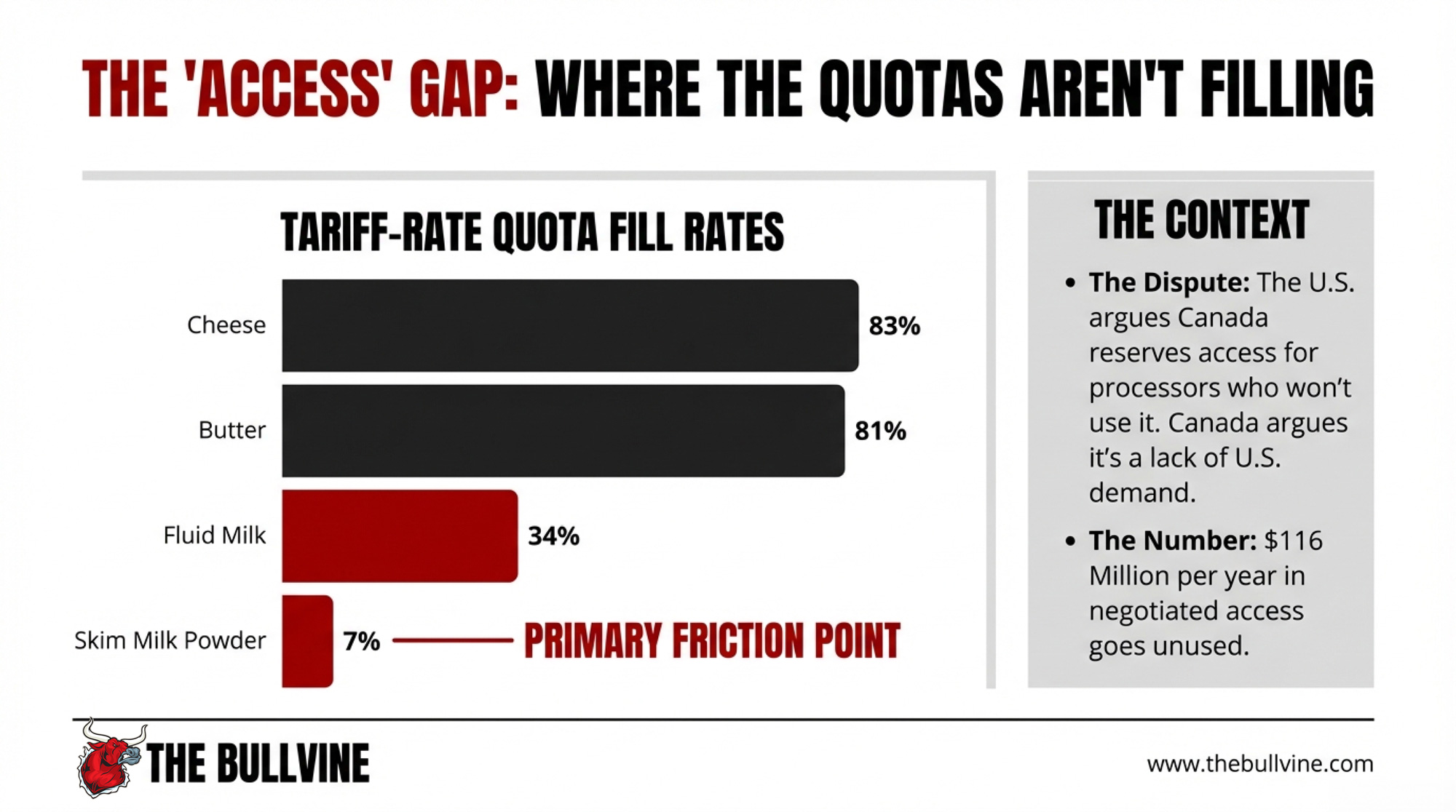

Dairy is the loudest file in the room—and the most organized. On February 4, NMPF and USDEC co-launched the Agricultural Coalition for USMCA, an industry-wide push to strengthen and renew the agreement. When the deal was signed, it opened about 3.6% of Canada’s dairy market as tariff-rate quota access — roughly US$200 million per year across 14 product categories. But those quotas aren’t filling. The overall average fill rate was just 42% in 2022/23, with 9 of 14 TRQs below half the negotiated value. More current data tells a split story:

Product

Fill Rate

Period

Cheese (all types)

83%

2024 calendar year

Butter & cream powder

81%

2023/24 dairy year

Industrial cheese

59%

2024

Milk powders

57%

2024

Fluid milk

34%

Cumulative

Skim milk powder

7%

Cumulative

Note: Globe & Mail figures reflect CUSMA-specific TRQs. USDA FAS data may include quotas across all trade agreements (WTO, CETA, CPTPP), which explains the variance in cheese fill rates between sources. Both are accurate within their reported scope.

Cheese and butter fill reasonably well. It’s the fluid milk and powder categories dragging the average, and those are the categories where the allocation system faces the strongest U.S. criticism. Canada argues some TRQs go unfilled because American exporters haven’t generated sufficient demand — a demand problem, not an allocation barrier. The U.S. counters that the allocation system suppresses demand by restricting who can import. A Texas Tech University causal impact study found the actual USMCA boost came in at 34% ($519 million cumulatively) — real growth, but below the USITC’s 43.8% projection, partly because “Canada’s allocation of these quotas mostly favors its own processors over U.S. exporters”.

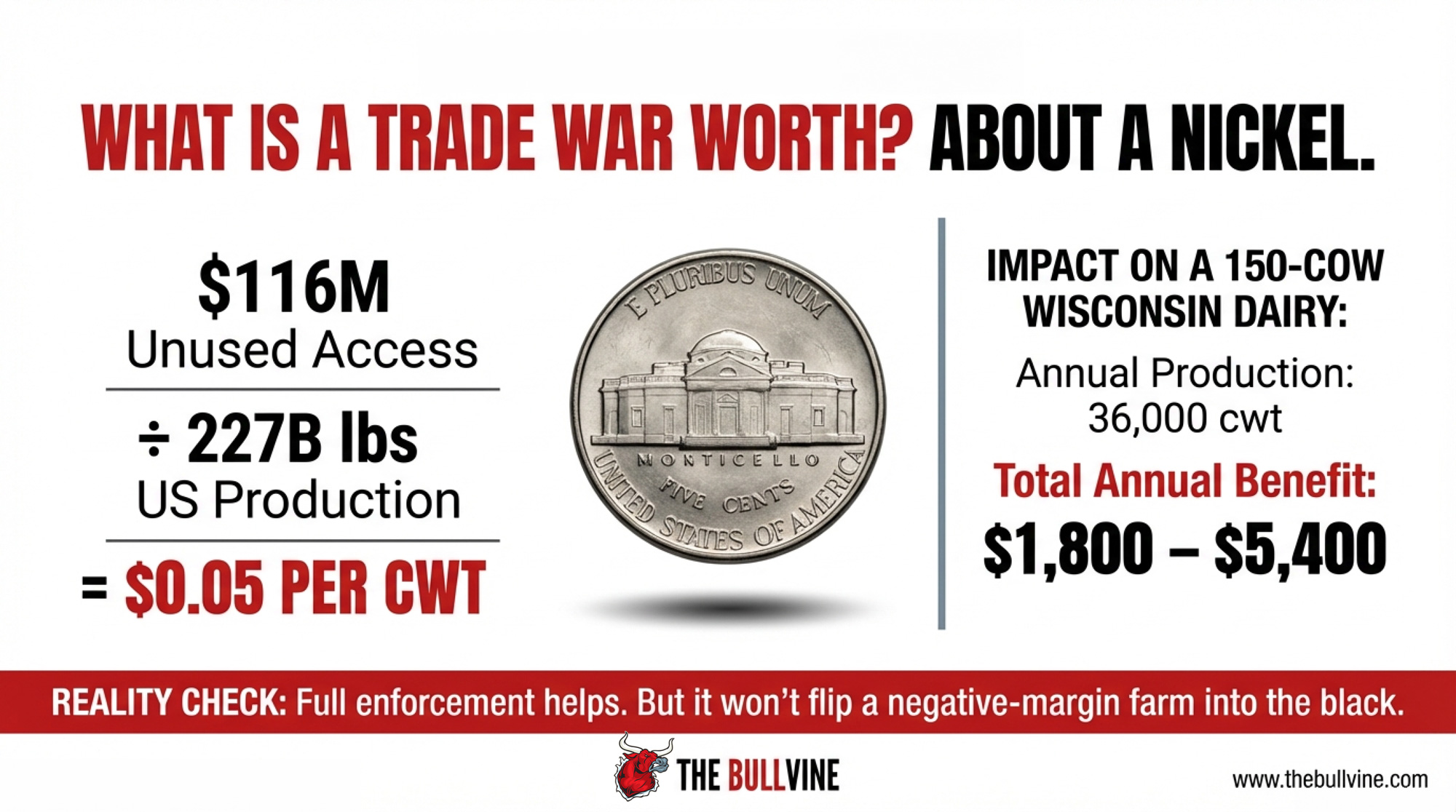

By our math, $200 million in annual TRQ access times the 42% fill rate — roughly $116 million per year in negotiated access goes unused. That’s a lot of money from the lobby’s podium. It’s a different number from the barn.

Metric

Lobby Number

Barn Number

Total annual unused TRQ access

$200M (promised) / $116M (unused at 42% fill)

—

Spread across 227B lbs U.S. production

—

$0.05/cwt

Impact on 150-cow farm (36,000 cwt/yr)

—

$1,800/year

Impact on 500-cow farm (120,000 cwt/yr)

—

$6,000/year

Impact if export lift adds $0.10–0.15/cwt

“Game-changer” (NMPF)

$3,600–$5,400/year (150-cow)

Average U.S. dairy cost of production

—

$19–23/cwt (USDA)

February 2026 all-milk forecast

—

$18.95/cwt (WASDE)

Who’s Pushing — and Who’s Pushing Back

The U.S. says Canada designed its allocation system to block imports by reserving 80–85% of many TRQs for domestic processors who had little incentive to use them. A USMCA dispute panel ruled in the U.S.’s favour in January 2022 and ordered changes. Canada rewrote the rules. A second panel, reporting on November 24, 2023, found, by a two-to-one decision, that Canada’s revised system didn’t technically breach USMCA. The dissenting panelist argued Canada’s narrow eligibility rules “significantly limit a large number of other Canadian importers who would be eager to bring U.S. dairy products to Canada”.

On December 2, 2025, 74 bipartisan House members from dairy states, including New York, Washington, Wisconsin, and California, wrote to Greer urging him to use the 2026 review for enforcement. “NMPF and USDEC — led by President and CEO Gregg Doud, the former Chief Agricultural Negotiator at USTR — have described Canada’s TRQ policies as ‘manipulative’ and accused Ottawa of ‘circumvention’ of USMCA’s dairy export disciplines.” Vander Schaaf told senators the U.S. exported approximately $9 billion in dairy products in 2025, including a record 559,000 metric tons of cheese through November. The trajectory is up. The frustration is that Canada isn’t absorbing its share.

On the Canadian side, Prime Minister Mark Carney responded directly in December 2025. Supply management is “not on the table,” — and he answered the English-language question in French. That’s a message aimed squarely at Québec.

DFC President David Wiens — who milks about 240 cows with his brother Charles near Grunthal, Manitoba — told MPs the combined impact of CUSMA, CETA, and CPTPP means roughly 18% of Canada’s domestic dairy demand is now met by imports. When CUSMA was signed, DFC projected that cumulative concessions would displace one in five Canadian dairy products — amounting to $1.3 billion in annual farm-gate losses once fully phased in. Both sides believe they’re defending survival — $1.14 billion in U.S. dairy exports to Canada in 2024, a record, and part of a $3.6 billion flow to Mexico and Canada that accounts for 44 percent of total U.S. dairy export value. On the other side: CA$4.8 billion in federal compensation flowing to supply-managed sectors.

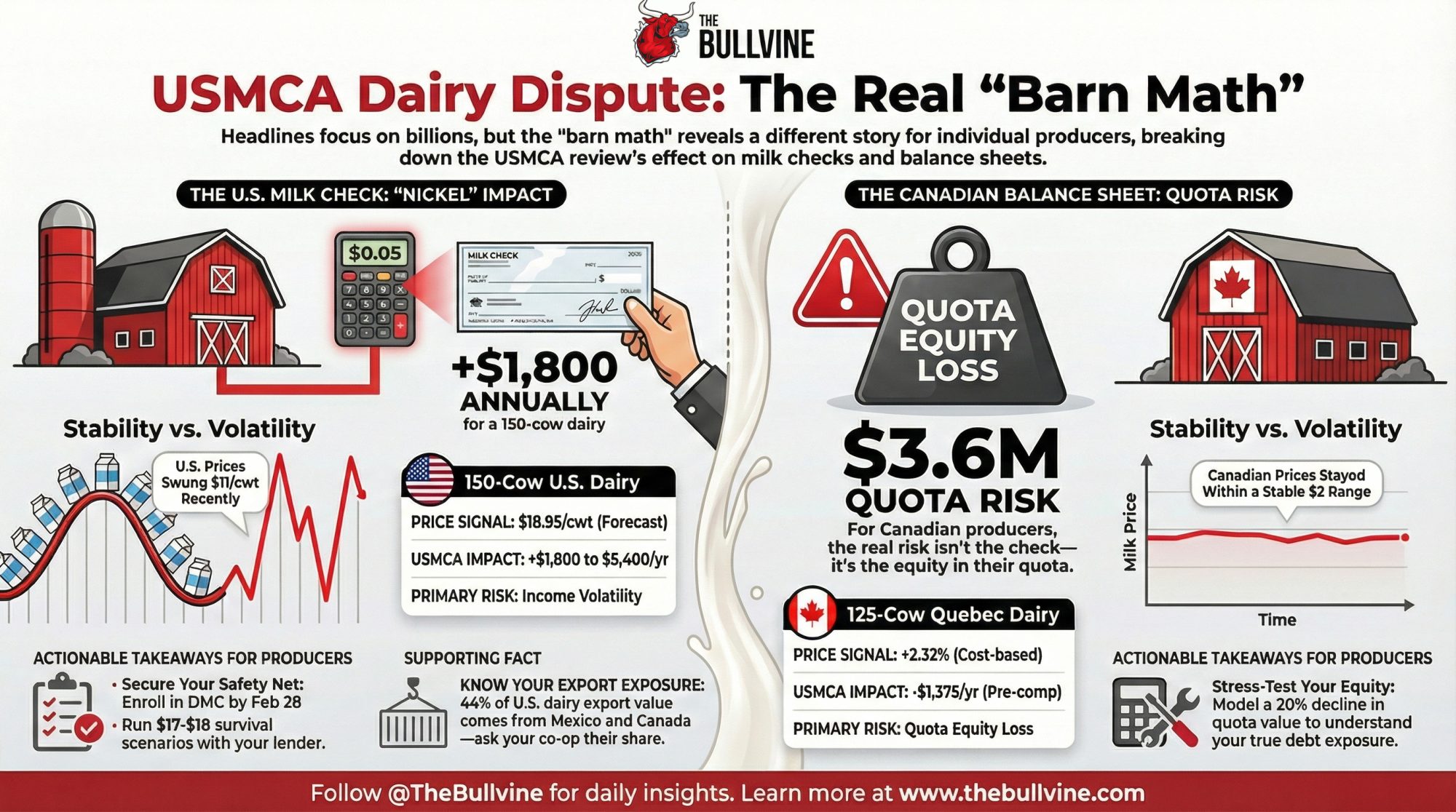

Why the Same Commodity Pays Two Different Mortgages

The single biggest difference between Vander Schaaf’s milk check and Gobeil’s: how the price gets set.

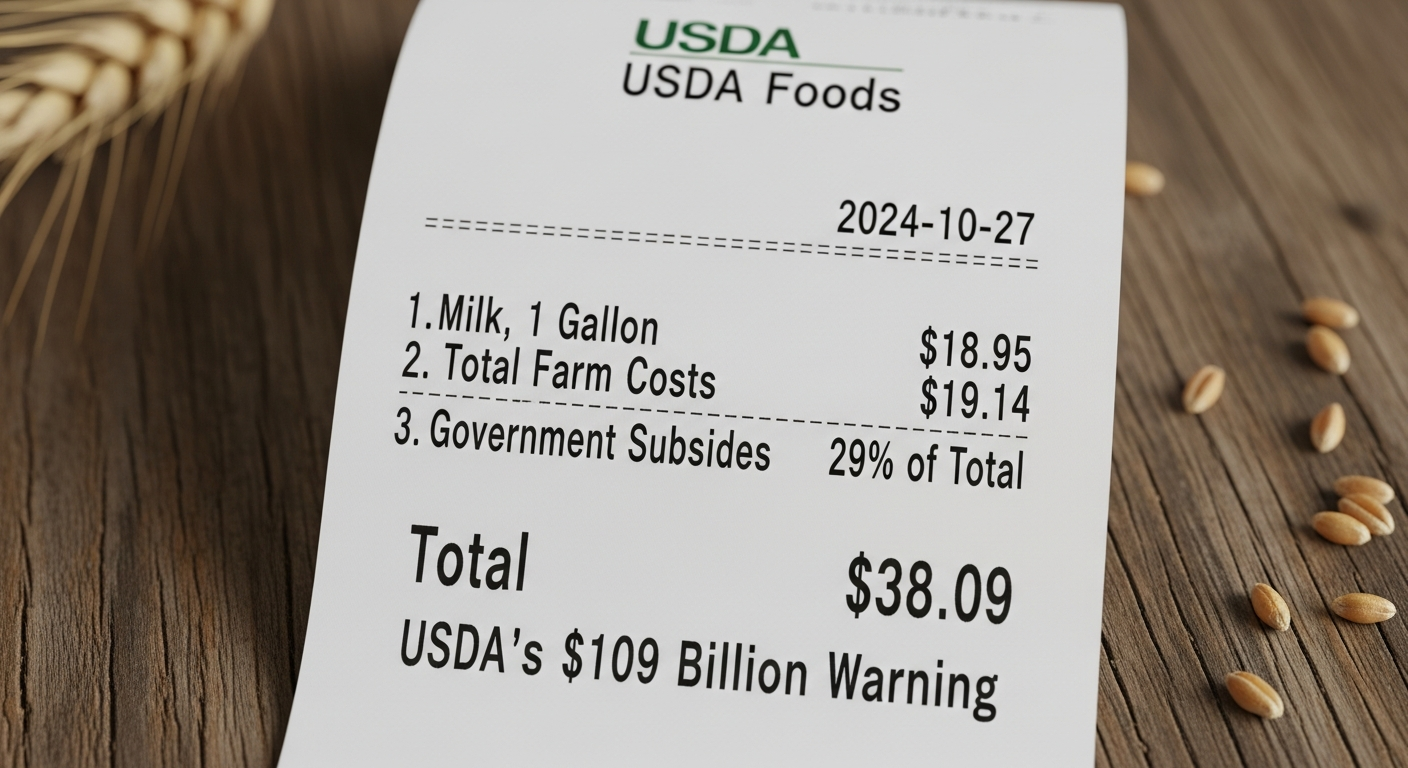

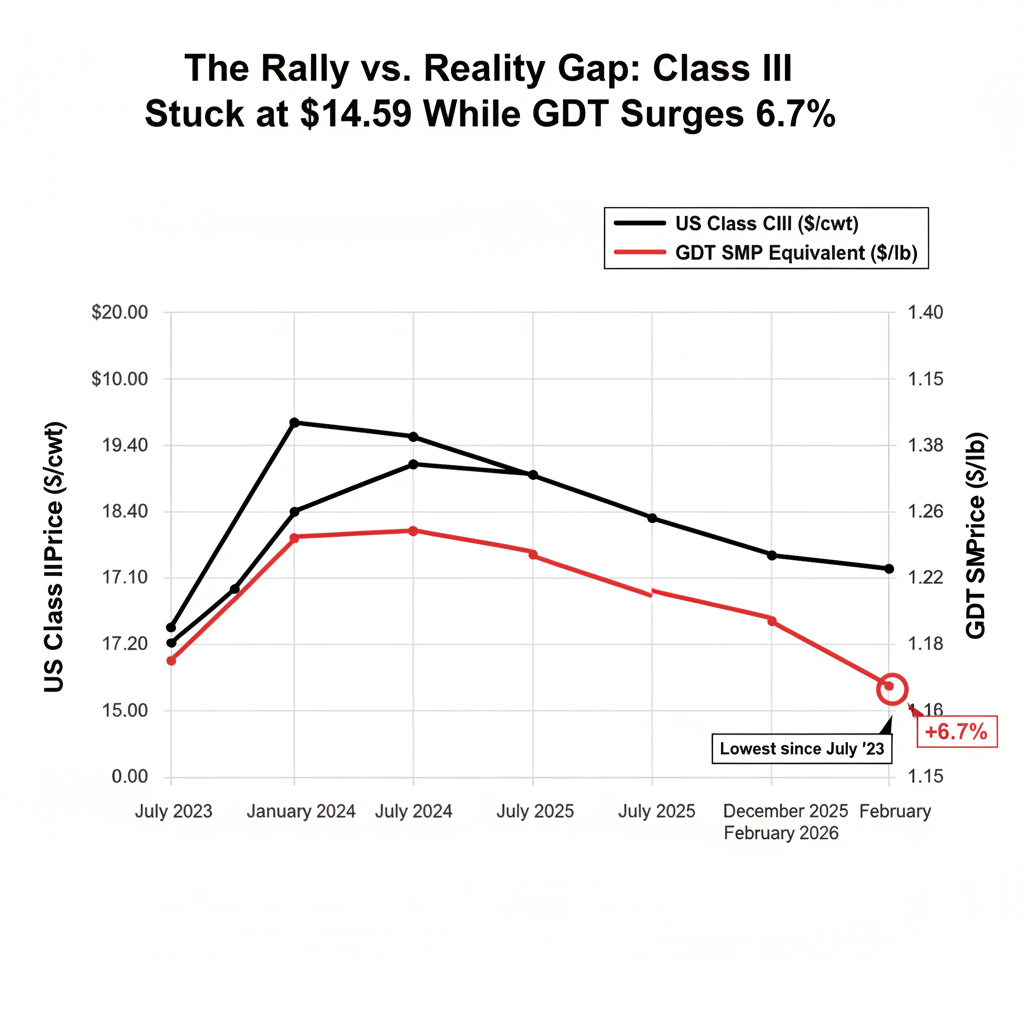

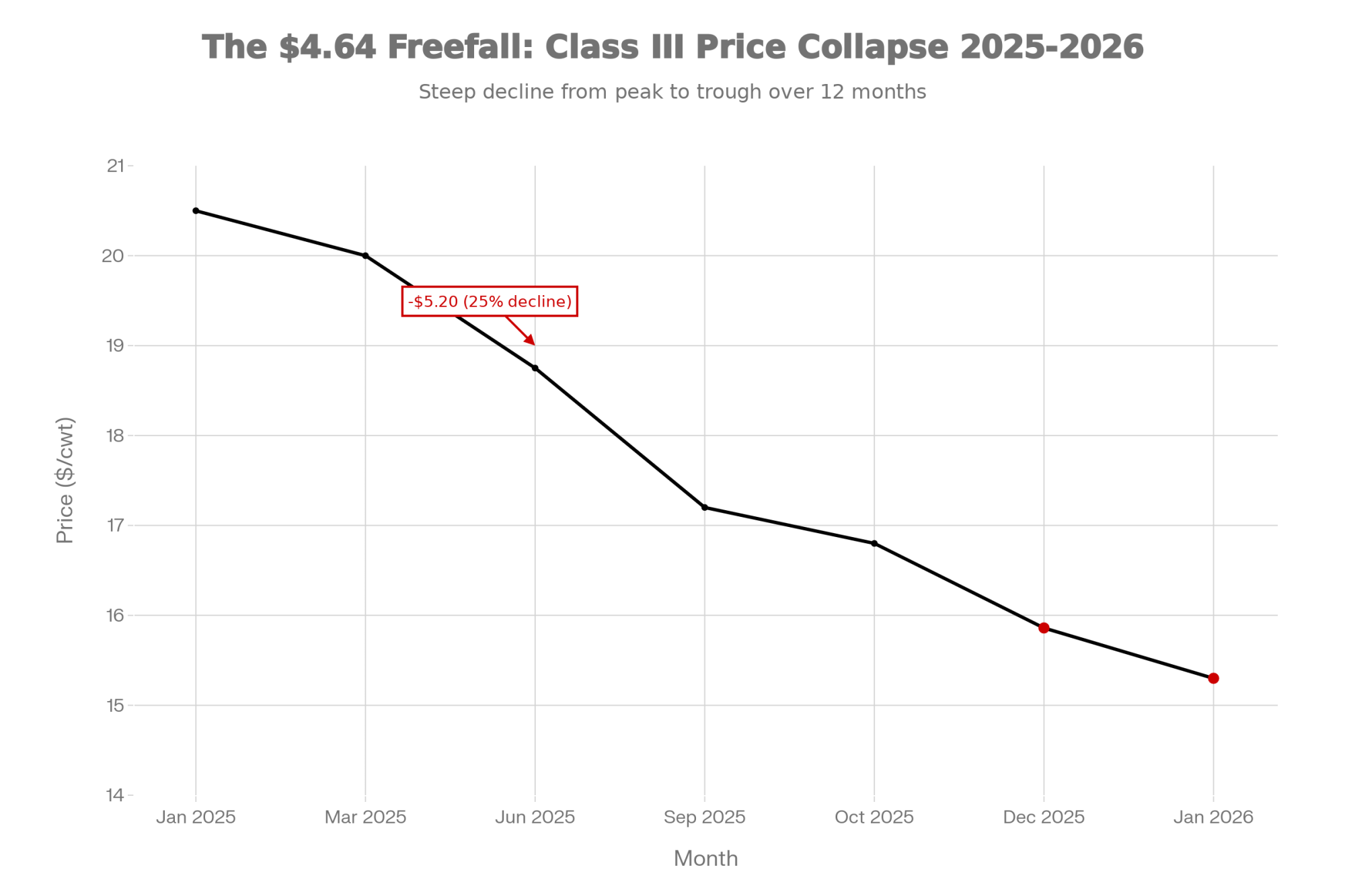

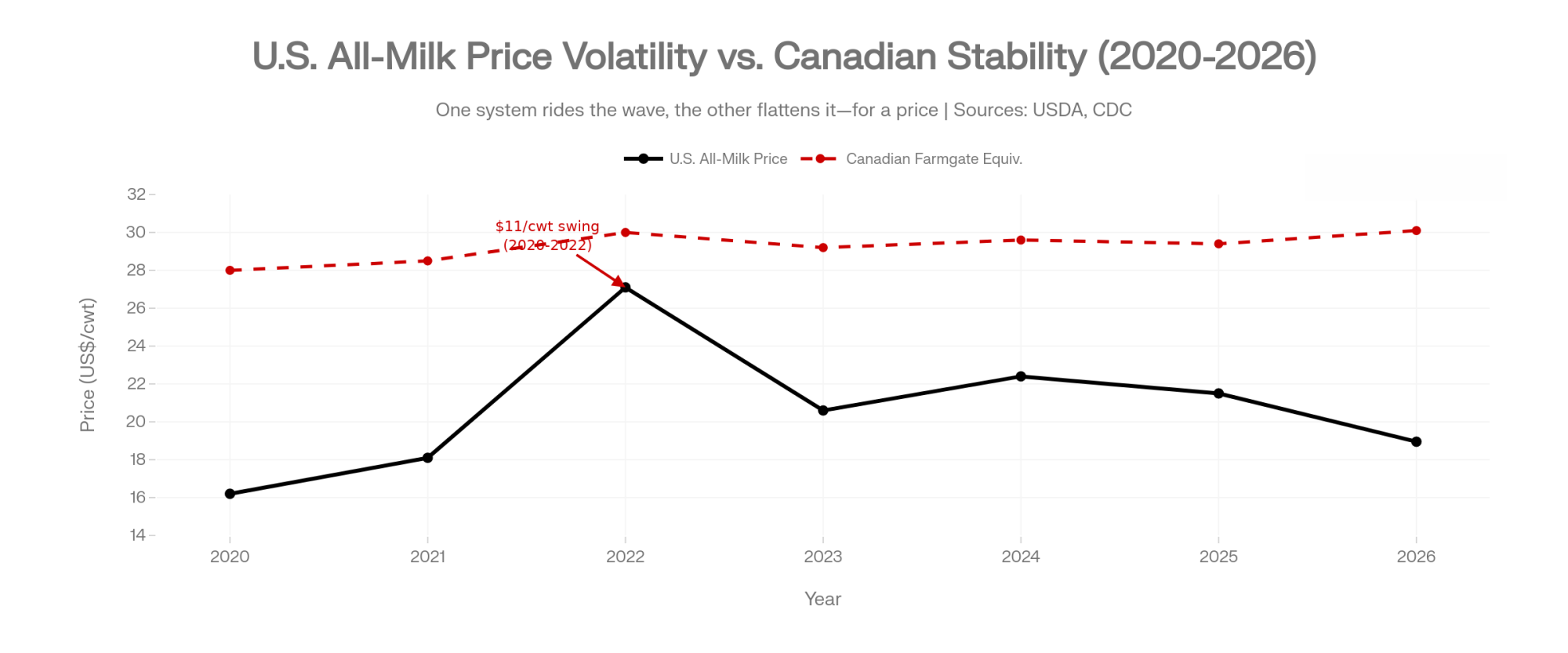

In the U.S., the base price flows from Class III/IV futures and commodity markets. USDA’s February 2026 WASDE projects the all-milk annual average at US$18.95/cwt — but January’s Class III came in at just $14.59/cwt. The back half of the year has to do heavy lifting to hit that average. The safety net is Dairy Margin Coverage: insurance, not a guaranteed price. Over the last five years, U.S. all-milk prices swung from roughly $16.20 in 2020 to $27.10 in 2022 — an $11/cwt range.

Year

U.S. All-Milk Price (US$/cwt)

Canadian Equivalent (US$/cwt)

2020

$16.20

$28.00

2021

$18.10

$28.50

2022

$27.10

$30.00

2023

$20.60

$29.20

2024

$22.40

$29.60

2025

$21.50 (est.)

$29.40

2026

$18.95 (forecast)

$30.10 (forecast w/ 2.3% increase)

In Québec, the Canadian Dairy Commission surveys actual production costs each year and adjusts the farmgate price to cover them. The formula: 50% of the change in the indexed cost of production, 50% of the change in the consumer price index. That produced the 2.3255% farmgate increase effective February 1, 2026 — tied to input costs and inflation, not commodity markets in Chicago. Canadian farmgate prices move in a narrow band, roughly US$28–30/cwt equivalent at the 2025 average exchange rate, against that $11 U.S. swing.

But that stability comes stapled to a different kind of risk. In the P5 provinces — Ontario, Québec, New Brunswick, Nova Scotia, and PEI — quota trades at a cap of CA$24,000 per kilogram of butterfat per day. A cow producing 1.2–1.3 kg BF/day means a per-cow quota value around CA$28,800–$31,200. In western Canada, it’s higher — Alberta’s quota traded at CA$56,495/kg BF/day in January 2025, and Manitoba’s at CA$44,000. On Gobeil’s 125-cow Québec farm, that’s roughly CA$3.6–3.9 million in quota value — an asset that exists only as long as Ottawa keeps defending it.

One system charges you in income volatility. The other charges you in political risk locked inside your balance sheet.

What Does the USMCA Review Mean for a 150-Cow Wisconsin Dairy?

Here’s where the barn math gets humbling. Spread across 227 billion pounds of annual U.S. production, the raw math on $116 million in unused TRQ access works out to about $0.05/cwt nationally. Five cents.

Take a 150-cow Wisconsin dairy producing 24,000 lbs per cow. That’s 36,000 cwt per year. At $0.05/cwt, full TRQ enforcement is worth roughly $1,800 annually. Scale to a 500-cow operation producing 120,000 cwt, and it’s $6,000 — still not survival money.

But trade access lifts demand signals across the domestic market. Cornell dairy economist Charles Nicholson, working with Wisconsin’s Mark Stephenson, estimated that each additional 1% of U.S. dairy components exported lifts the all-milk price by about $0.12/cwt (95% CI: half a cent to $0.24/cwt). Their own conclusion: “it would be appropriate to be cautious in estimating the magnitude of price impacts from US dairy exports.” As exports grow, supply grows roughly in step.

Herd Size

Annual Production (cwt)

Direct TRQ Impact ($0.05/cwt)

Optimistic Export Lift ($0.10–0.15/cwt)

Total Potential Gain

Cost of Production ($/cwt)

2026 Forecast ($/cwt)

Margin Gap

150 cows

36,000 cwt

$1,800/yr

$3,600–$5,400/yr

$5,400–$7,200/yr

$19–23

$18.95

−$0.05 to −$4.05

500 cows

120,000 cwt

$6,000/yr

$12,000–$18,000/yr

$18,000–$24,000/yr

$19–21 (scale advantage)

$18.95

−$0.05 to −$2.05

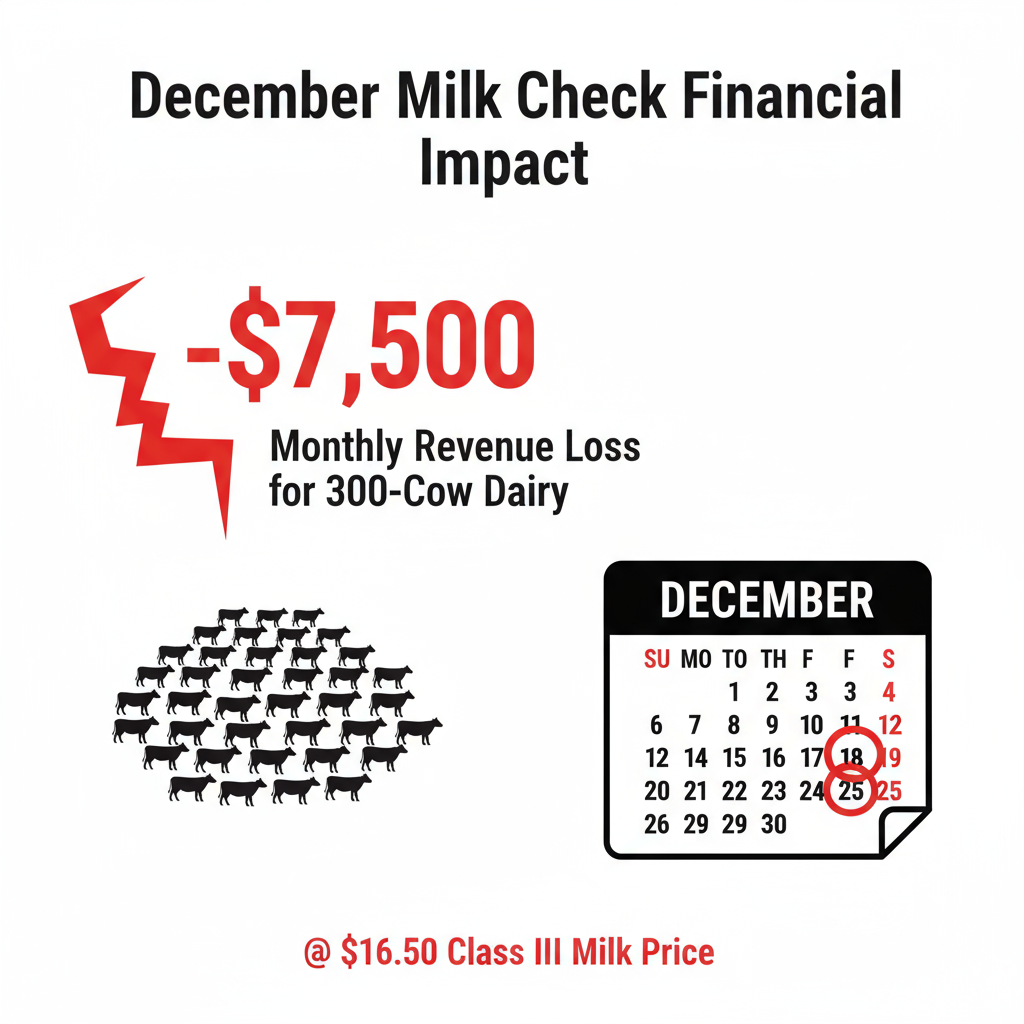

1,250 cows(Vander Schaaf)

150,000 cwt

$7,500/yr

$15,000–$22,500/yr

$22,500–$30,000/yr

~$19 (scale advantage)

$18.95

−$0.05

Apply that framework. Filling the remaining $116 million wouldn’t move the export needle by a full percentage point. Even at the generous end of Nicholson’s range, you’re looking at $0.10–$0.15/cwt in total price lift. On 36,000 cwt, that’s $3,600 to $5,400 per year for our 150-cow Wisconsin dairy.

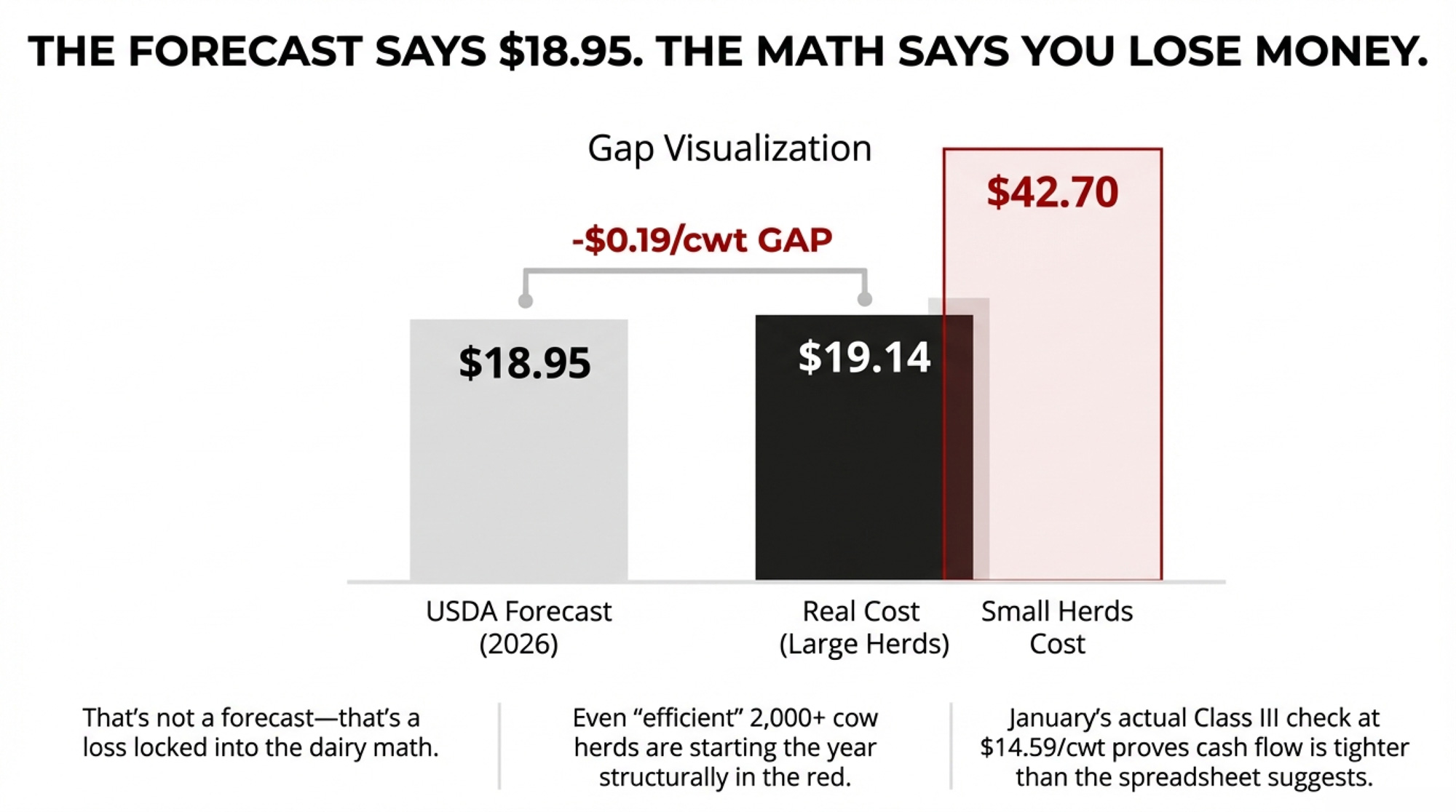

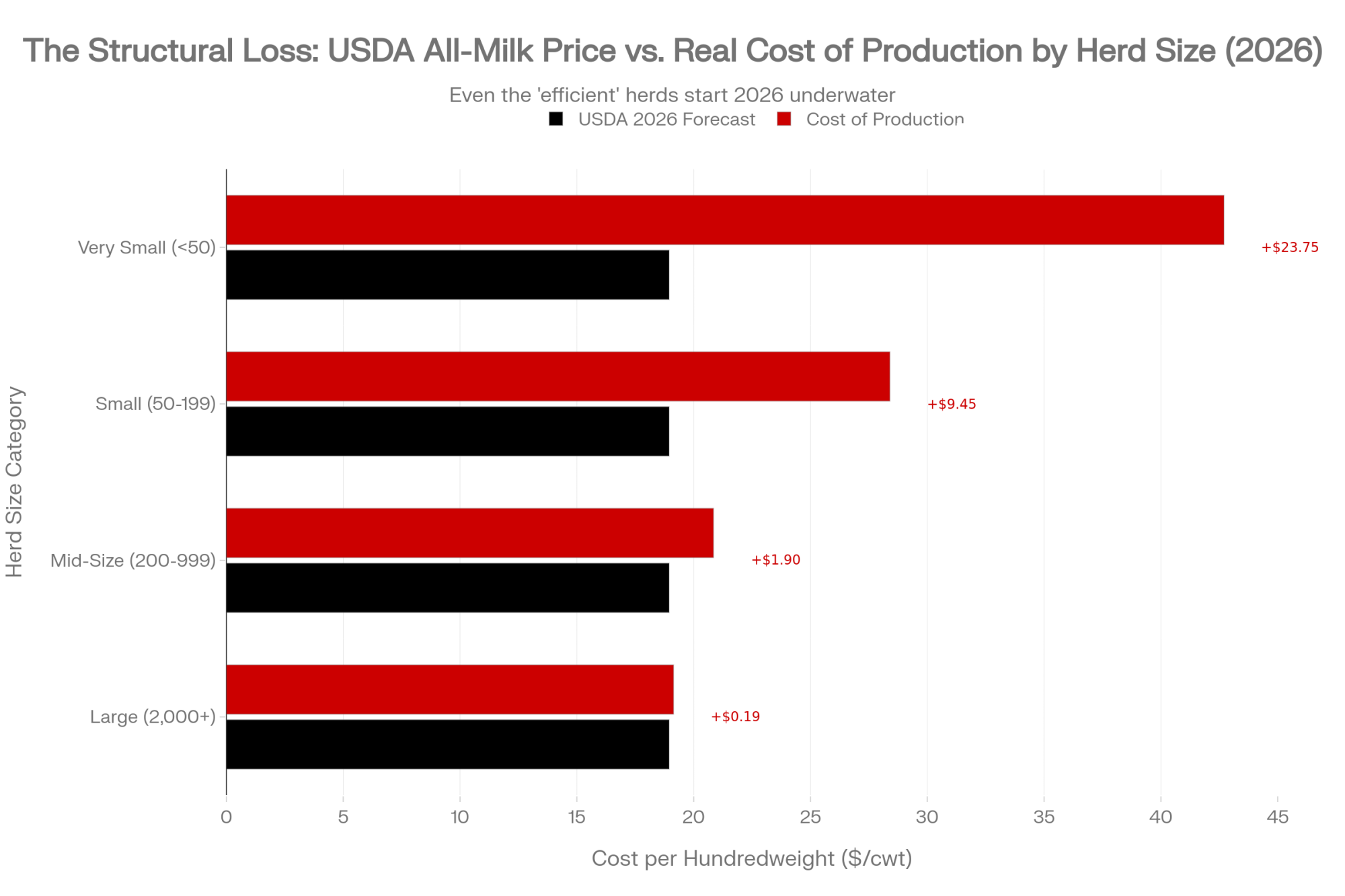

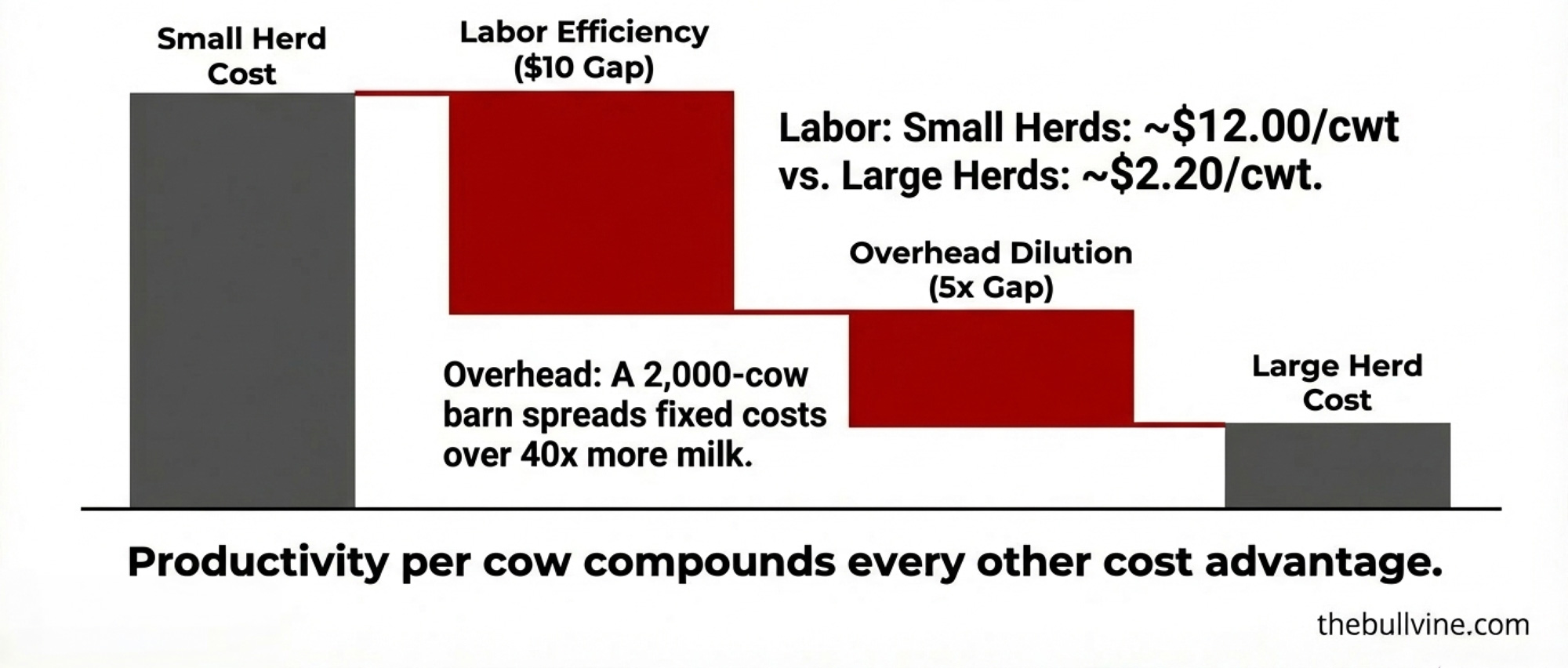

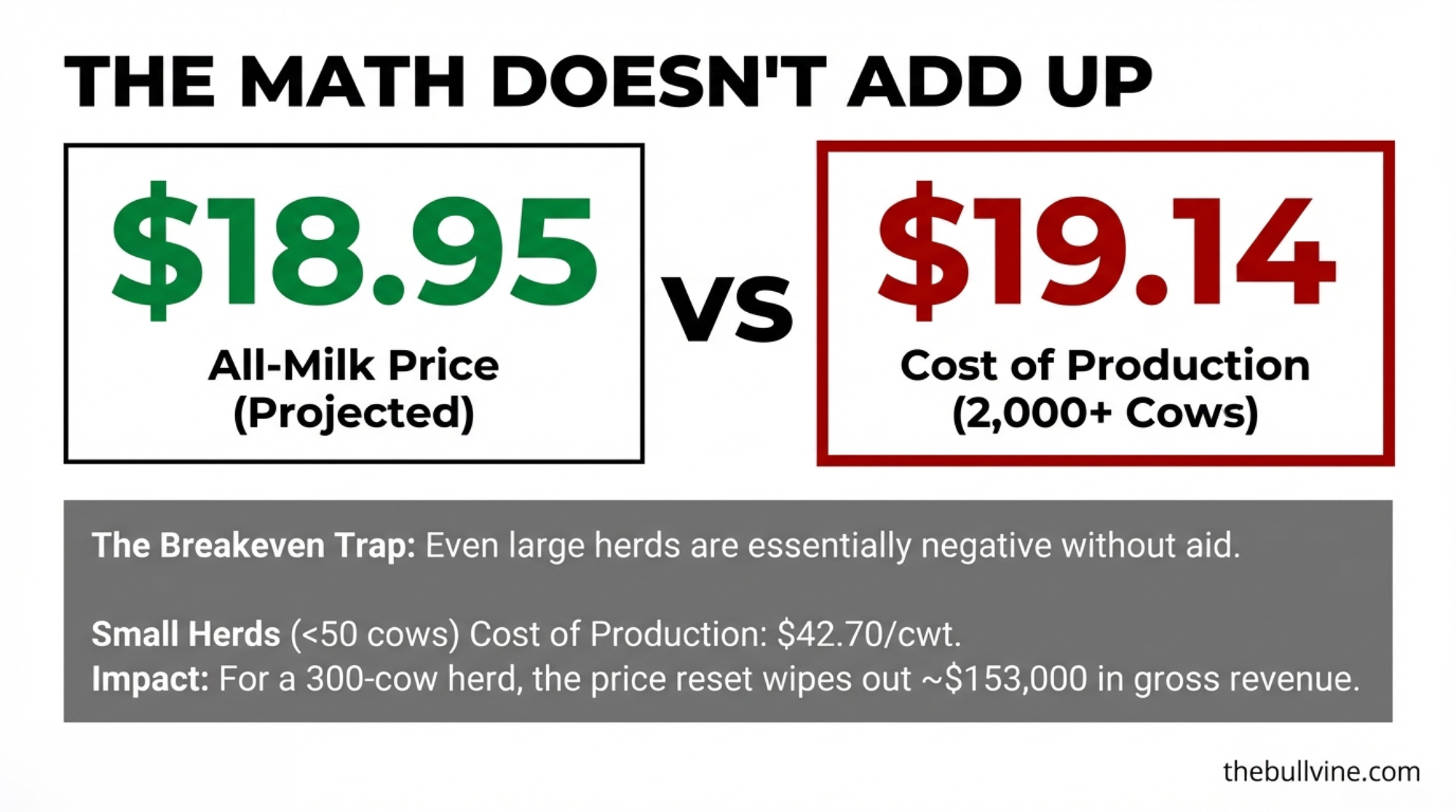

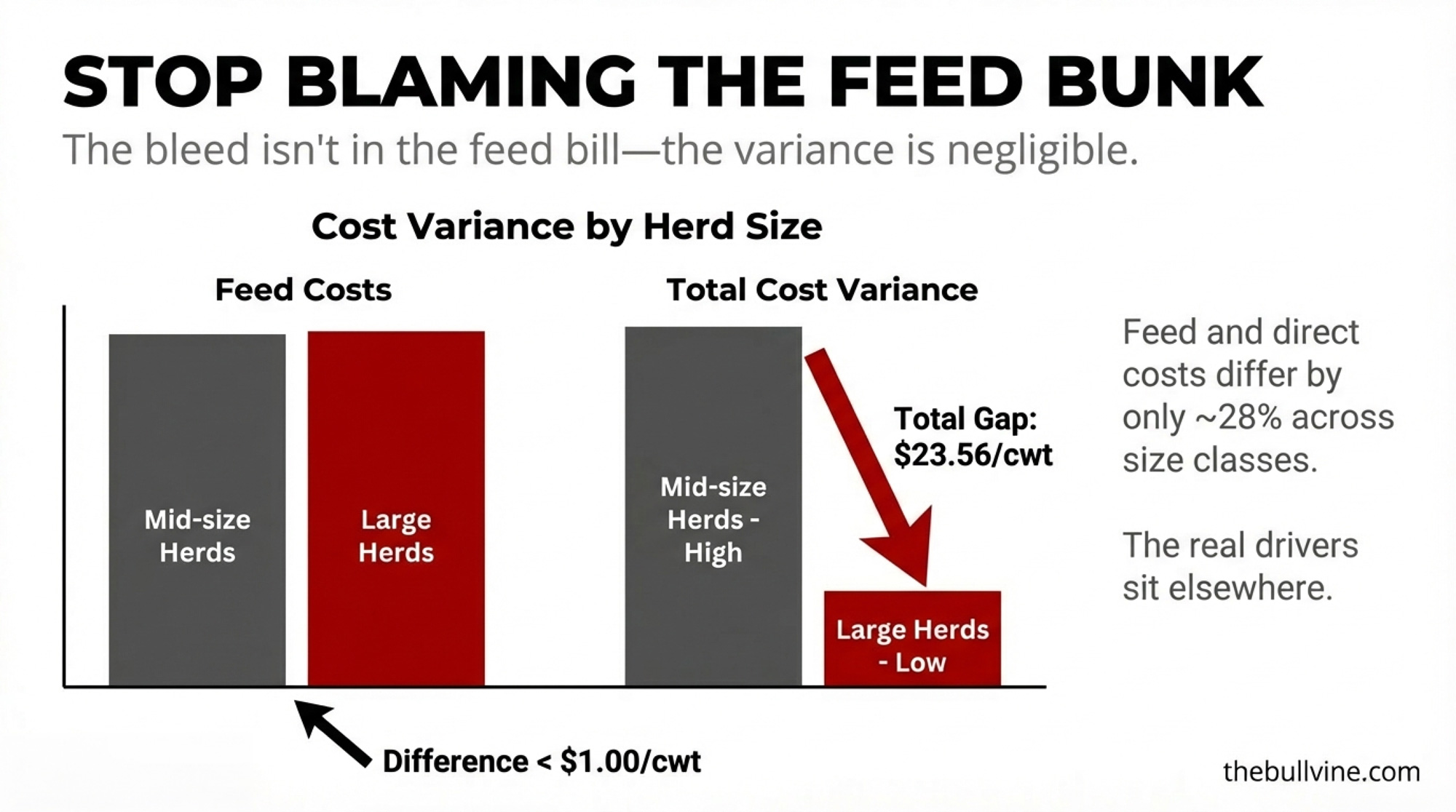

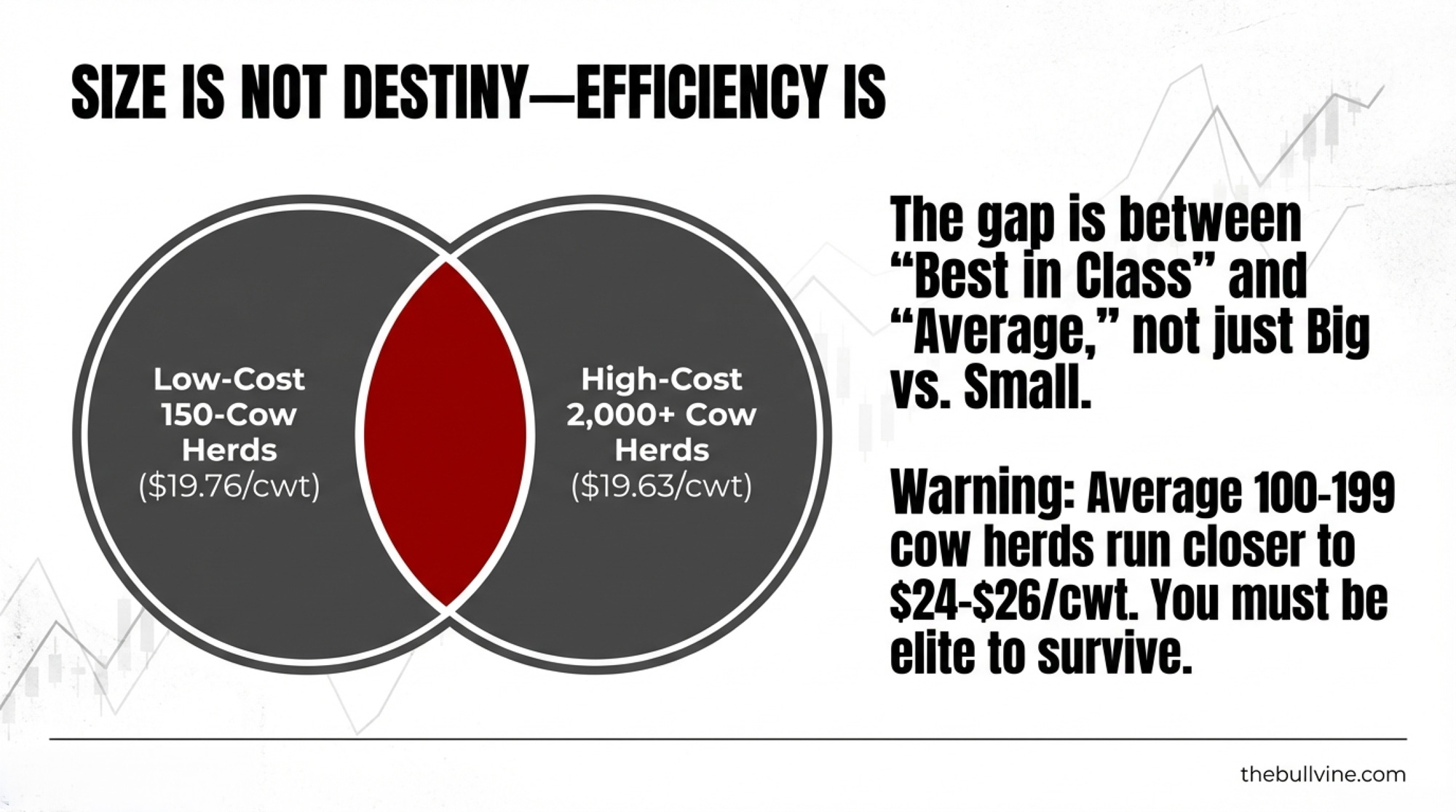

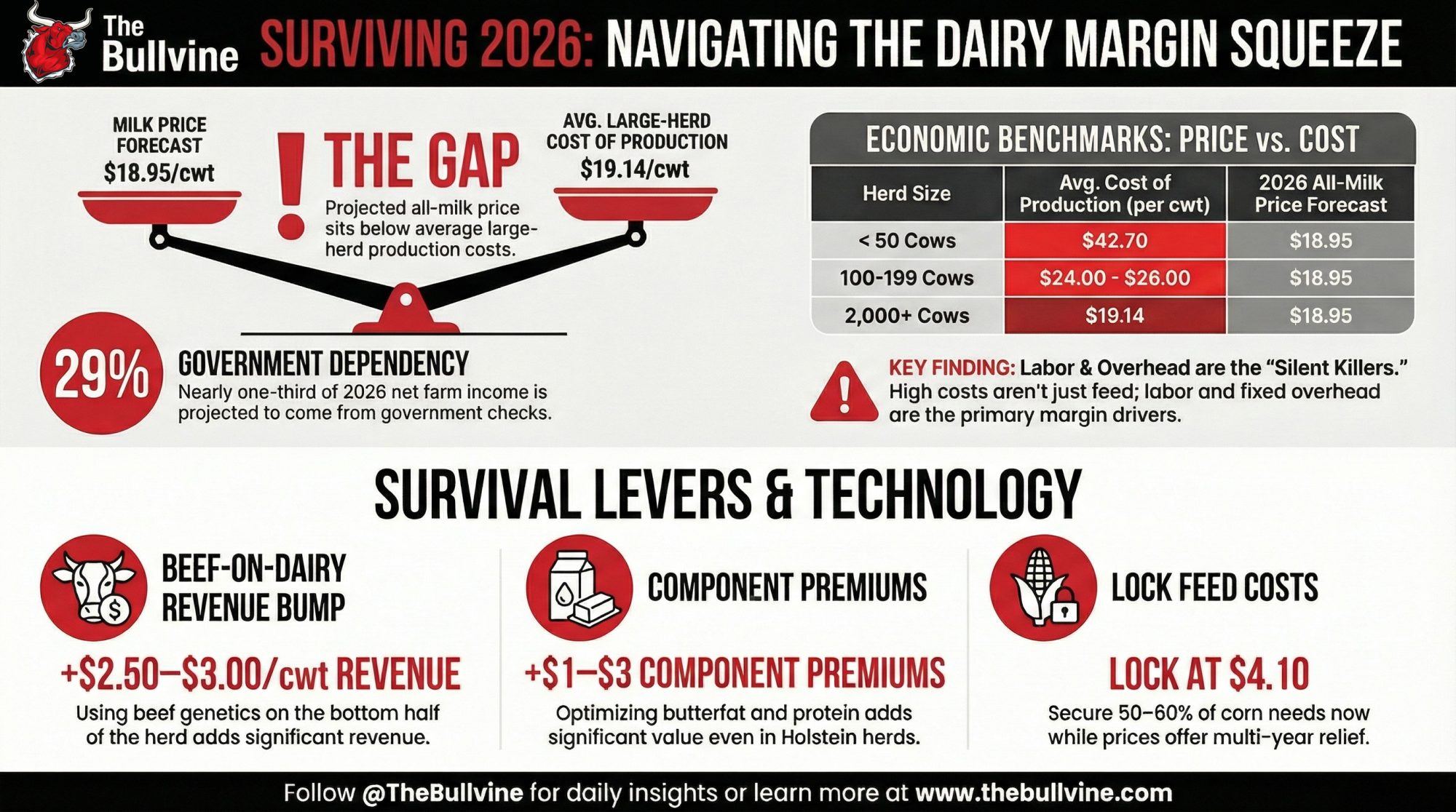

Set that against cost reality. USDA ERS data (2021 ARMS survey, published July 2024) shows farms with 2,000+ cows averaging $19.14/cwt in full economic cost, while herds under 50 cows hit $42.70/cwt. Analysts pegged mid-size net cost of production at $22.64/cwt. A 150-cow operation in that $19–23/cwt range — receiving a forecast of $18.95 — is treading water or running red before trade even enters the picture. An extra $1,800 to $5,400 helps. It won’t flip a negative-margin farm into a positive one.

What a Nickel Means for a 125-Cow Québec Quota Farm

Now flip the border. If those TRQs fill completely, cheese is already at 81–83%, so the real incremental pressure comes from powder and fluid categories. On 125 cows producing roughly 27,500 cwt per year, a nickel-per-hundredweight hit works out to about $1,375 annually. Ottawa cushions that — CA$1.2 billion over six years through the Dairy Direct Payment Program alone for CUSMA. Minister Bibeau confirmed in November 2022 that the combined package across three trade deals reaches CA$4.8 billion.

But every round of “access goes up, Ottawa writes a bigger cheque” adds weight to a political question. That CA$4.8 billion comes from general federal revenue — Canadian taxpayers. FCC’s 2026 dairy outlook advises producers to “continue focusing on what they can control on the farm” until the details of the CUSMA review are known. Sensible. It’s also what you say when you don’t know how the politics will break.

The bigger exposure isn’t the milk cheque. It’s the balance sheet. A 20% decline in quota value on Gobeil’s 125-cow operation at the P5 cap means roughly CA$720,000–$780,000 in equity gone. If you’re running 500+ cows in Alberta at CA$56,495/kg BF/day, your exposure is roughly double the P5 math. Your stress test looks different.

Are These Farmers Actually on Opposite Sides?

The easy version — American dairy vs. Canadian dairy, free market vs. supply management — misses what’s happening to both of them.

Vander Schaaf’s 1,250-cow Idaho operation and Gobeil’s 125-cow Québec farm are both getting squeezed by the same forces — processors, retailers, global commodity traders — and dealing with it through completely different systems. The American system absorbs that pressure through farmer income. The Canadian system absorbs it through government spending and quota valuation. Neither pushes the pressure back up the chain to the players who actually control pricing power.

If both sides “win” their version of the 2026 review — full TRQ enforcement for the U.S., intact supply management plus compensation for Canada — it doesn’t fix either farmer’s structural problem. It determines who bleeds a little slower.

The Border Math, Side by Side

Metric

150-Cow Wisconsin Dairy

125-Cow Québec Dairy

Price mechanism

Class III/IV futures + commodity markets

CDC formula (50% COP + 50% CPI)

Farmgate price (5-year range)

~US$16.20–$27.10/cwt (2020–2022)

~US$28–30/cwt equivalent

2026 price signal

$18.95/cwt forecast (WASDE Feb 2026)

2.3255% increase eff. Feb 1, 2026

Annual production

~36,000 cwt

~27,500 cwt

USMCA impact (full TRQ enforcement)

+$1,800–$5,400/yr

−$1,375/yr (before compensation)

5-year price volatility

~$11/cwt swing

~$2–4/cwt swing

Safety net

DMC + crop insurance

Supply management + CA$4.8B federal compensation

Balance-sheet risk

Land + cows + equipment

Land + cows + equipment + ~CA$3.6–3.9M quota

The math doesn’t pick a winner. It shows two different bills for the same thing: stability.

What You Can Do Before July

If you’re milking in the U.S.:

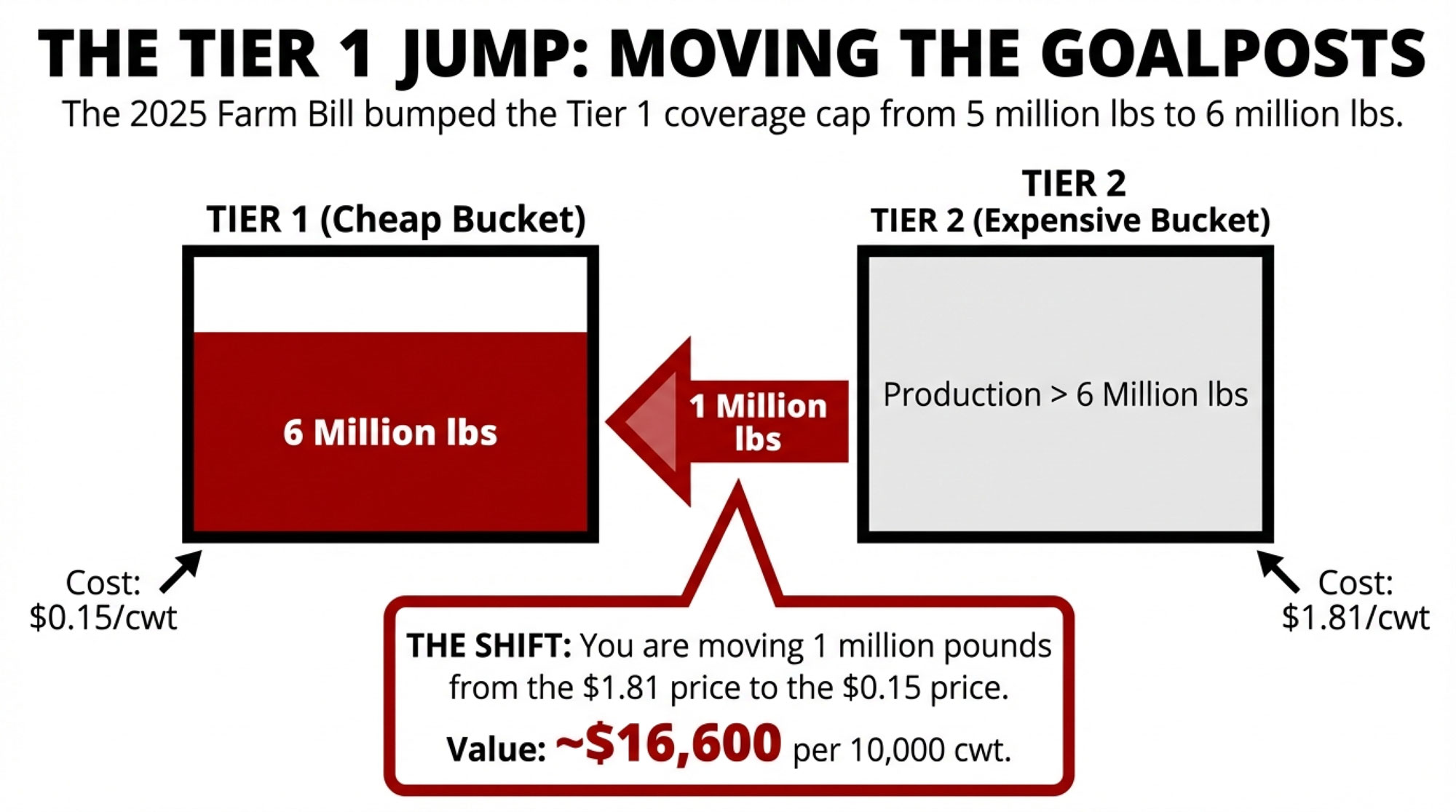

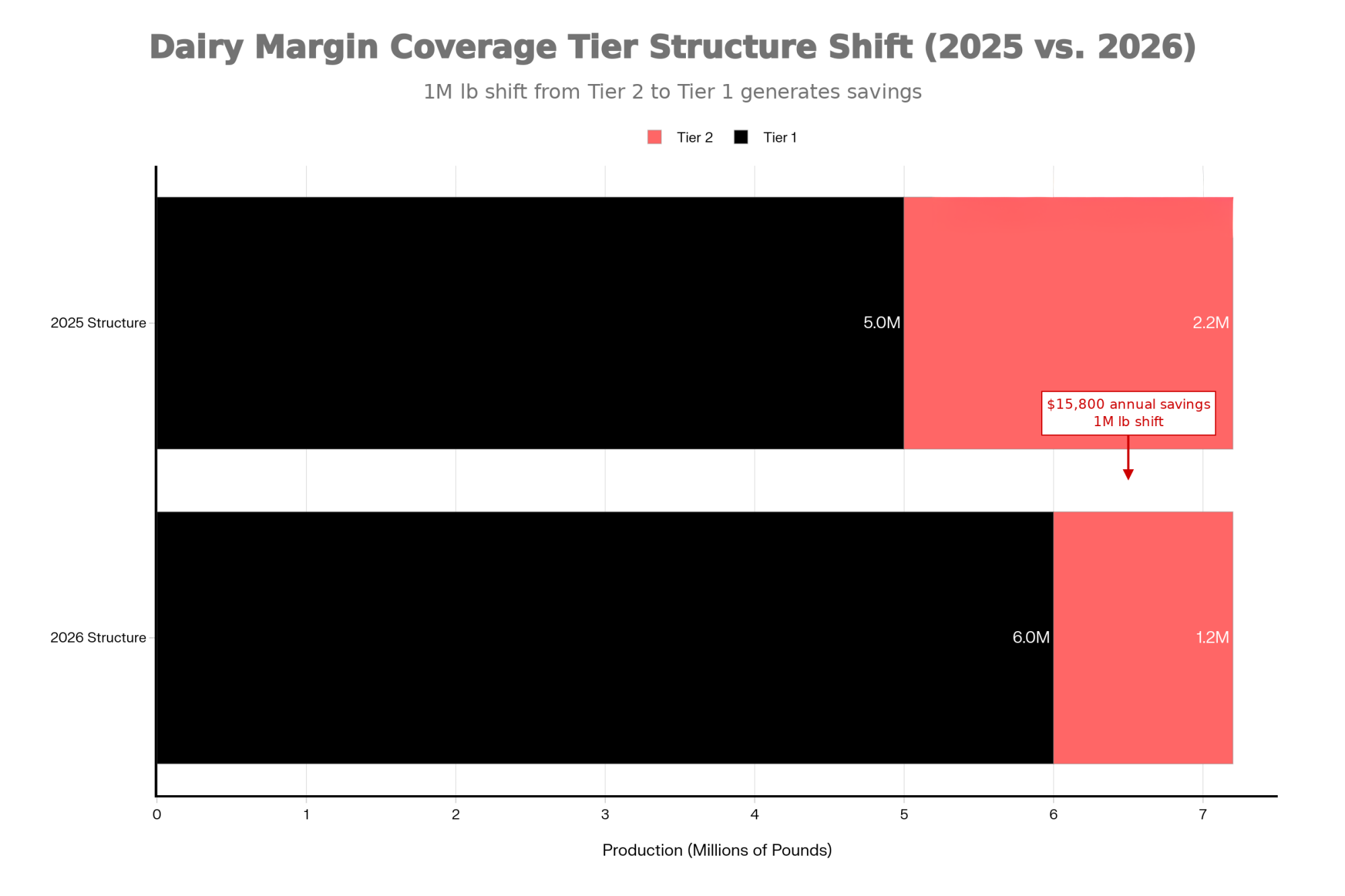

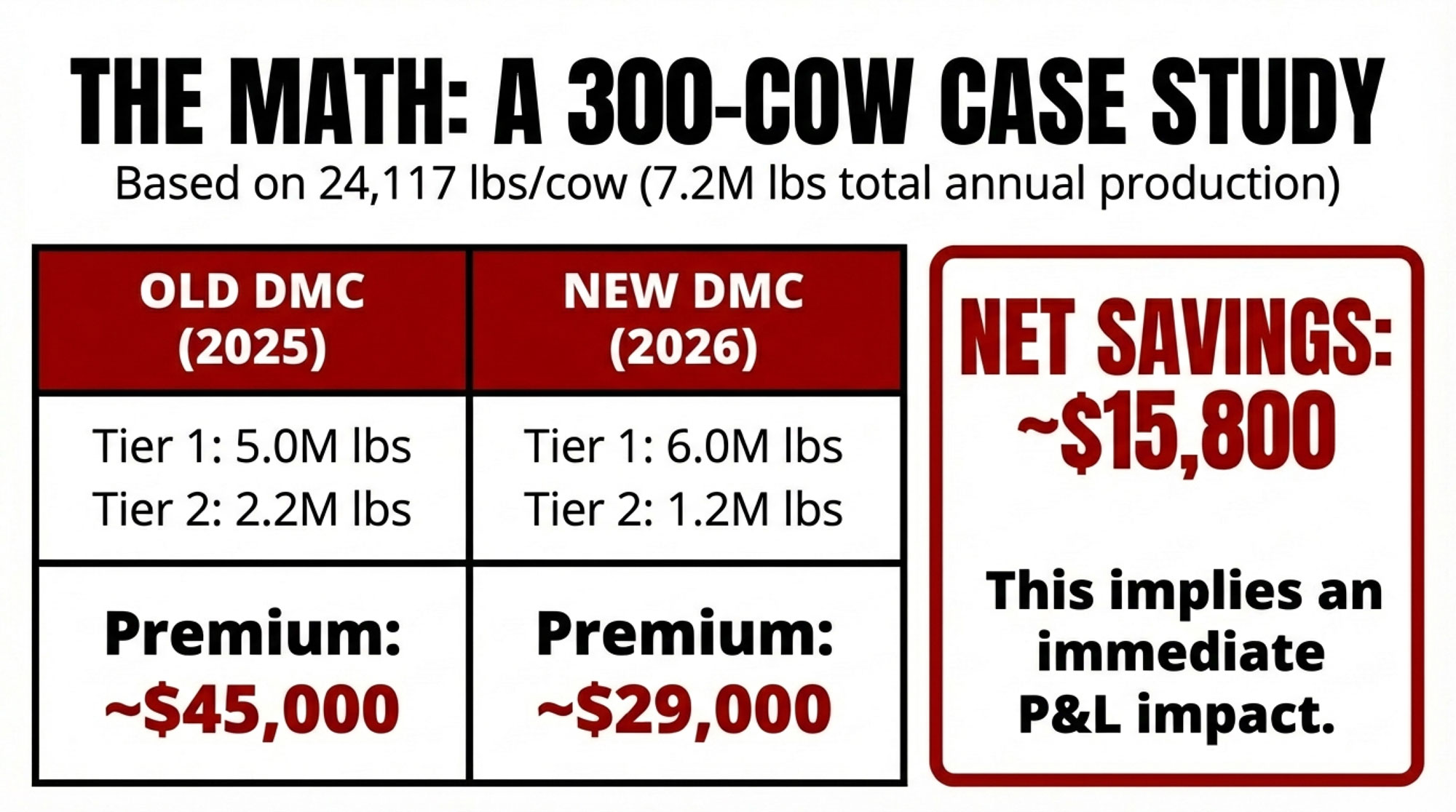

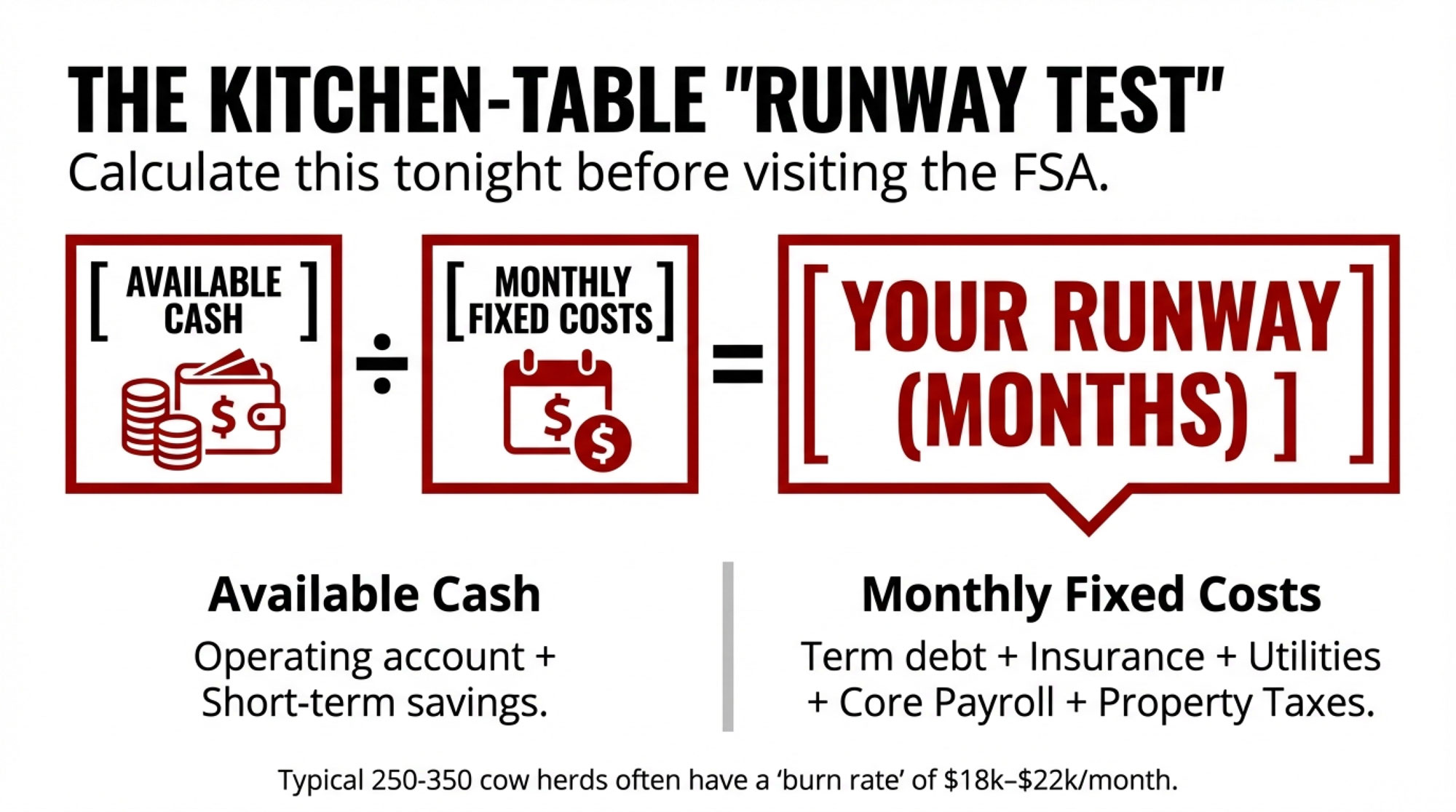

Enroll in DMC before February 28. Tier 1 coverage expanded from 5 million to 6 million pounds under the One Big Beautiful Bill Act (signed July 4, 2025). At $9.50 coverage, you’re paying $0.15/cwt in premium. Lock in for six years (2026–2031) at a 25% premium discount — but that means you can’t adjust if your herd grows or margins recover. If you’re above 6 million lbs (roughly 275+ cows at the national average production), Tier 1 covers only a fraction. Talk to your risk management advisor about Dairy Revenue Protection or Livestock Gross Margin for the rest.

By spring: Run a survival scenario at US$17–18/cwt with your lender. If your breakeven sits above $18, work the restructuring math before margins compress — not after.

Before July: Ask your co-op: “What percentage of our milk ends up in Canada or Mexico, and what’s our contingency if USMCA stalls?” Mexico and Canada purchased $3.6 billion in U.S. dairy products in 2024, accounting for 44 percent of total U.S. dairy exports.

If you’re milking in Canada:

Pull your own cost-of-production numbers and compare them against the CDC’s national average. If you’re not participating in COP surveys, you’re relying on your neighbours’ data while your livelihood depends on the results.

Watch the protein shift. FCC’s 2026 dairy outlook flags that both P5 and WMP are restructuring producer pay to incentivize more protein and less butterfat. If your herd tests 4.5% BF and 3.4% protein, you’re roughly neutral. Push butterfat higher without matching protein, and your gross revenue could drop by 1.2% under the new WMP structure. Factor that into breeding and ration planning alongside trade uncertainty.

By spring, model a 20% decline in the quota value with your lender. Not because that’s likely — but because you should know the answer before you need it. If you’re carrying debt against quota collateral, ask what their haircut assumptions are. FCC’s 2026 dairy outlook is worth reading alongside your balance sheet.

Before July: Watch two signals. First, CDC pricing bulletins — are they still citing cost of production and CPI as drivers, or are words like “affordability” or “competitiveness” creeping in? That language shift is your early-warning system. Second, provincial quota exchange reports. In January 2025, Ontario moved 405.98 kg BF/day at the CA$24,000 cap. Firm volume at the cap means the market believes the system holds. Watch for softening.

Both sides: Don’t let the trade conversation be somebody else’s problem. Your milk check is already a trade document.

Key Takeaways:

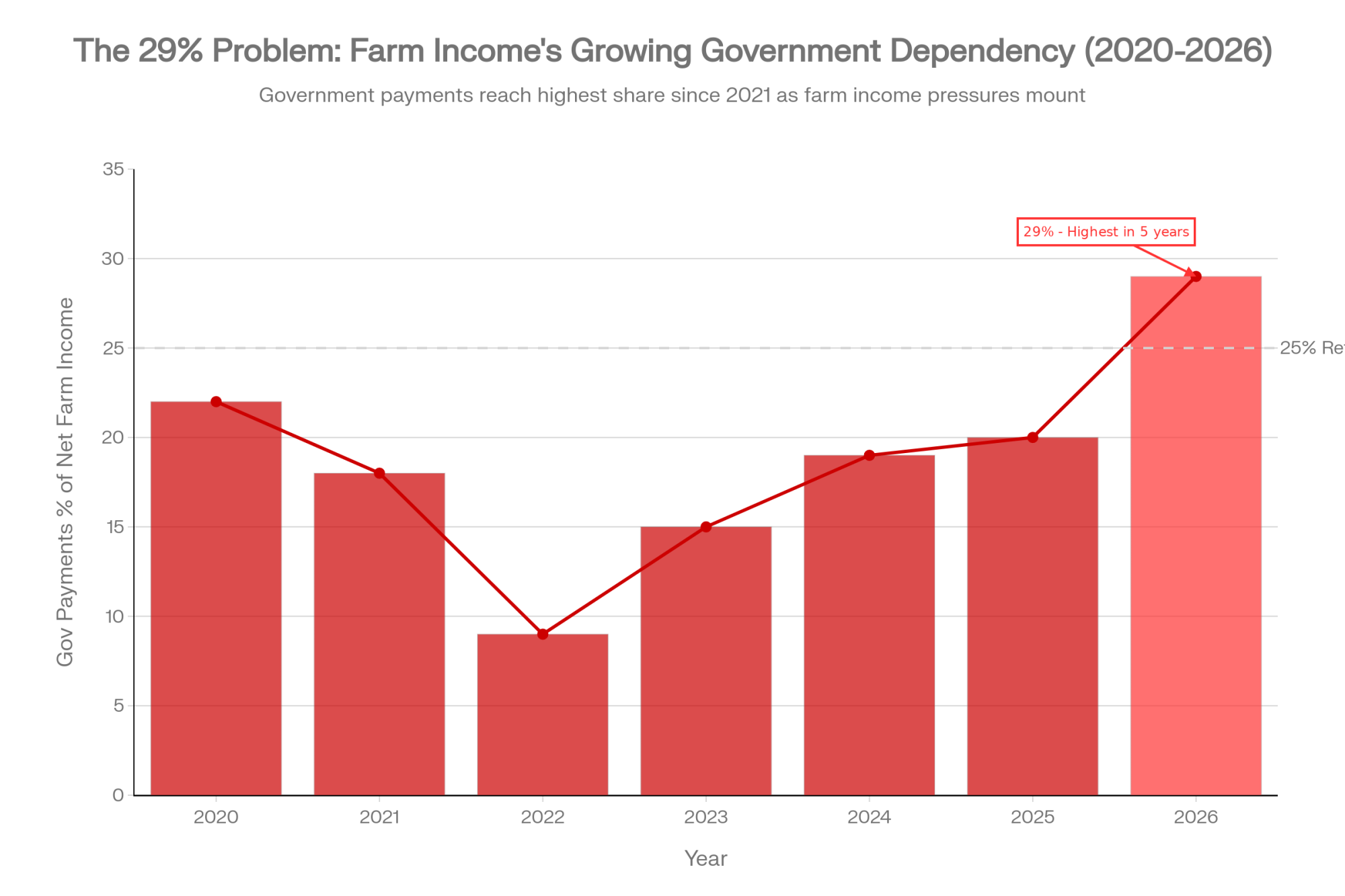

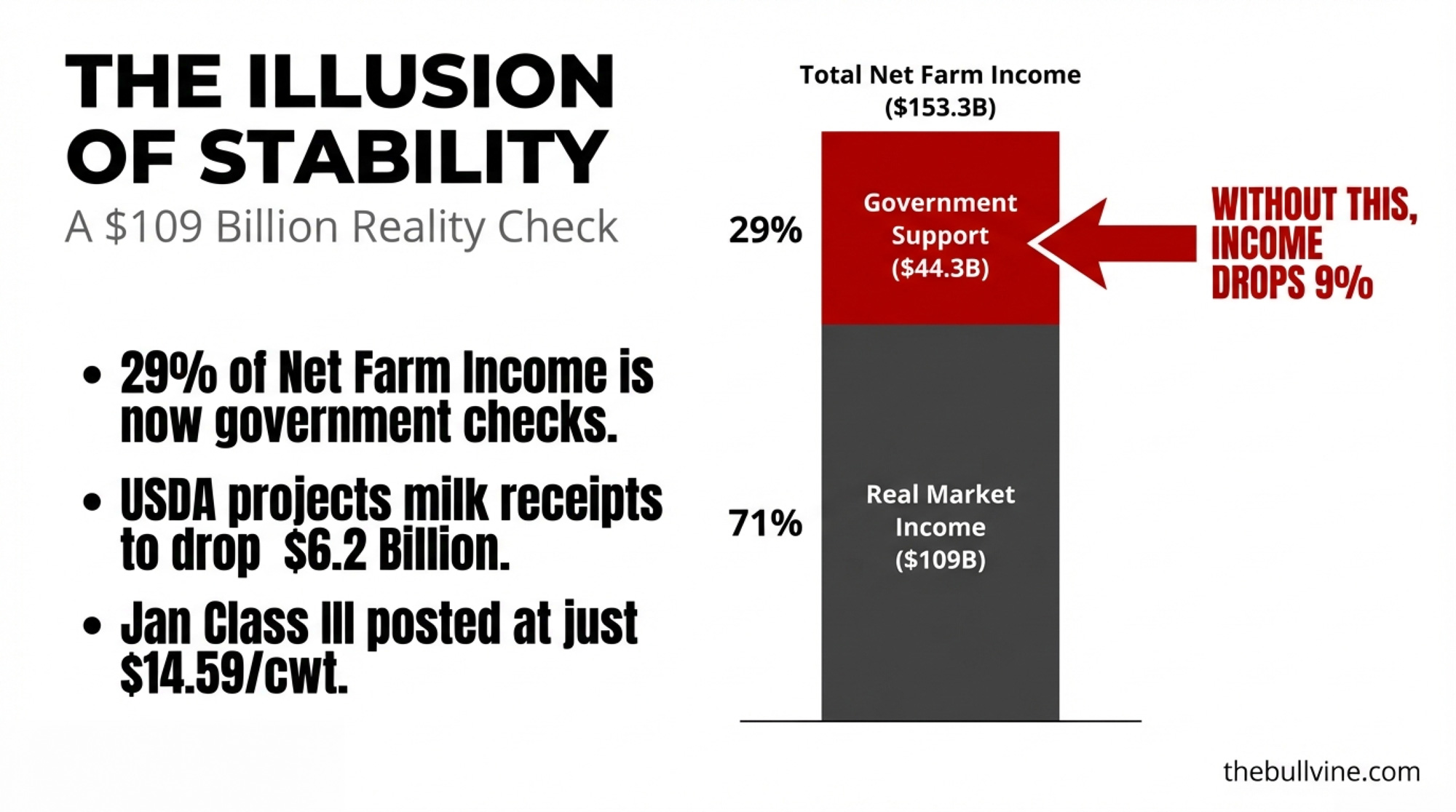

The USMCA dairy fight is huge in headlines ($200M–$1.14B), but the farm‑level effect is small: roughly 5¢/cwt or $1,800–$5,400/year for a 150‑cow U.S. herd.

Canadian supply management trades income stability for political and balance‑sheet risk: US$28–30/cwtstability on the milk cheque, but CA$3.6–3.9M in quota equity exposed to Ottawa’s trade decisions.

Full TRQ enforcement and a “win” for U.S. dairy won’t rescue a negative‑margin farm; survival still comes down to cost control, risk management (DMC/DRP/LGM), and co‑op strategy.

For Canadian producers, the real USMCA/CUSMA risk isn’t this year’s milk price; it’s possible quota repricing, so you need to stress‑test a 20% equity hit with your lender.

If you don’t know your co‑op’s export exposure, your breakeven, or your quota‑value stress line, you’re flying blind into the 2026 review — your milk cheque is already a trade document.

The Bottom Line

Vander Schaaf delivered his testimony and returned to his Idaho operation. Gobeil, 1,500 kilometres north, leads the organization representing every Québec dairy farmer who’ll feel whatever the July review decides. Both face the same July deadline. Both will judge the outcome by the deposit on their next milk cheque. The question for you isn’t which system is better — it’s whether you know your own numbers well enough to plan around whatever comes out of that review.

When the USMCA review panel reports this summer, we’ll re-run the barn math for both sides of the border in our Border Math series. What does your co-op’s export breakdown look like? What’s your breakeven?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

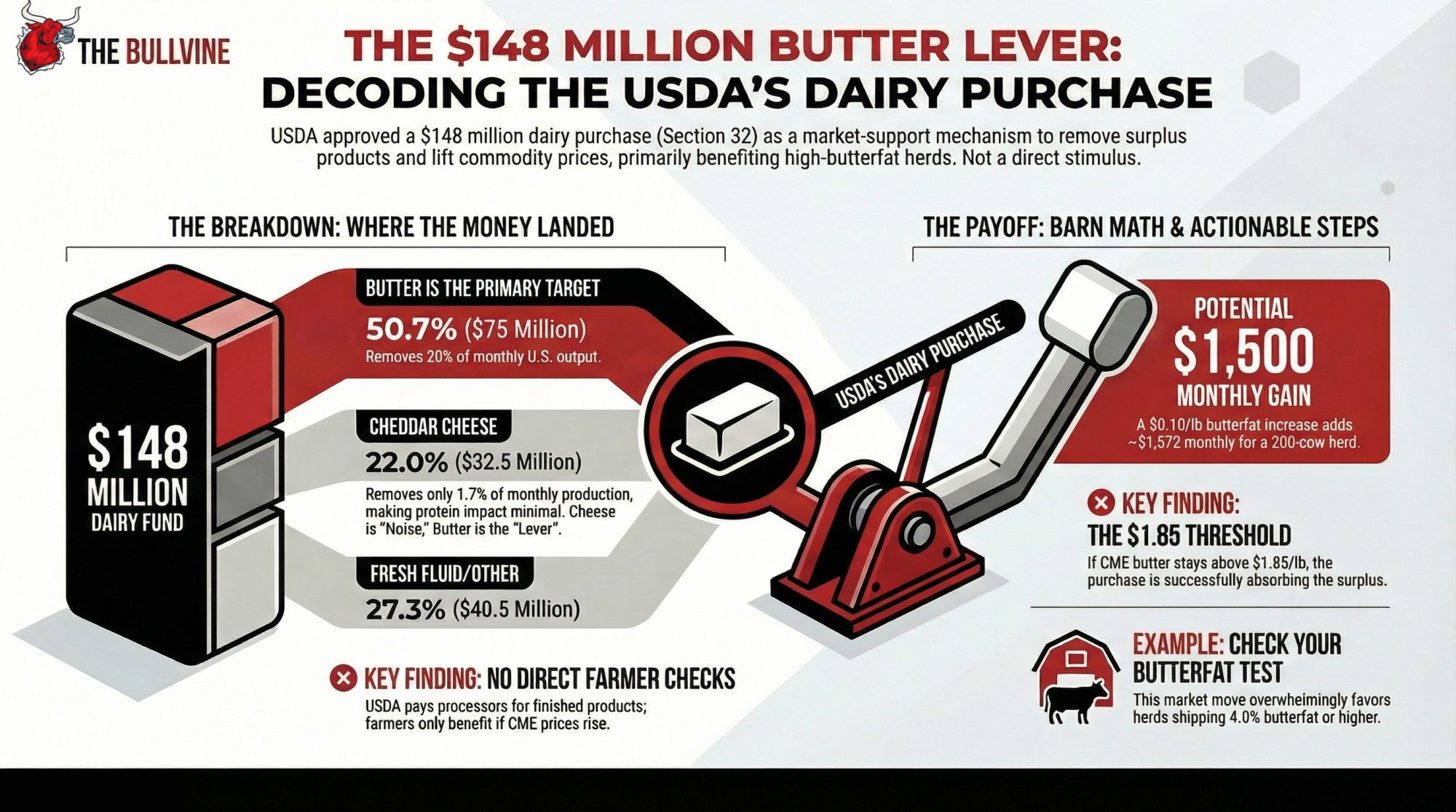

NMPF asked USDA for exactly $148 million in dairy purchases last November. On February 19, USDA delivered — to the dollar. That’s not luck. That’s the advocacy pipeline working. Who benefits?

Executive Summary: USDA has approved $263 million in Section 32 food purchases, including $148 million for dairy — the exact figure NMPF asked for last November and the largest dairy round since the COVID programs. That money goes to processors for butter, cheese, and milk, not directly to farms, so any benefit shows up only if it lifts CME prices enough to move FMMO component values on your milk check. Butter is the main story: $75 million at current prices pulls roughly 40 million pounds — about 20% of a typical month of U.S. butter output — out of the commercial market, and CME butter already jumped $0.165/lb during the announcement week. The $32.5 million cheddar buy, by comparison, removes only about 1.7% of a month’s cheese production, so it’s unlikely to change protein checks on its own materially. For high‑butterfat herds, a sustained $0.10/lb increase in butterfat value can add more than $1,500/month per 200 cows, but only if the rally holds and your co‑op’s component premiums pass that value through. The article breaks down that barn math, compares this purchase to earlier Section 32 and COVID‑era interventions, and provides a 30/90/365‑day playbook so you can track CME butter, scrutinize your component statement, and adjust your risk‑management strategy in response to this one‑time demand boost.

$148 million. That’s the dairy industry’s share of USDA’s $263 million Section 32 purchase announced on February 19, 2026 — and it’s the exact figure the National Milk Producers Federation requested in a letter to USDA last November. Not one dollar more. Not one dollar less.

Every ag newswire ran the number. Secretary Brooke Rollins called it “delivering wholesome, real food to Americans while injecting critical dollars into local economies”. NMPF President and CEO Gregg Doud said the purchases “will provide important relief to producers who will benefit from the additional demand”. The International Dairy Foods Association applauded. Headlines everywhere.

But here’s what nobody’s explaining: Section 32 doesn’t write checks to dairy farmers. It buys finished products from processors. Between that $148 million announcement and your milk check, there are five steps, at least three middlemen, and zero guaranteed dollars. Let’s walk through what this purchase actually buys, who actually gets paid, and what it could — could — mean for the price of your milk.

What USDA Is Actually Buying

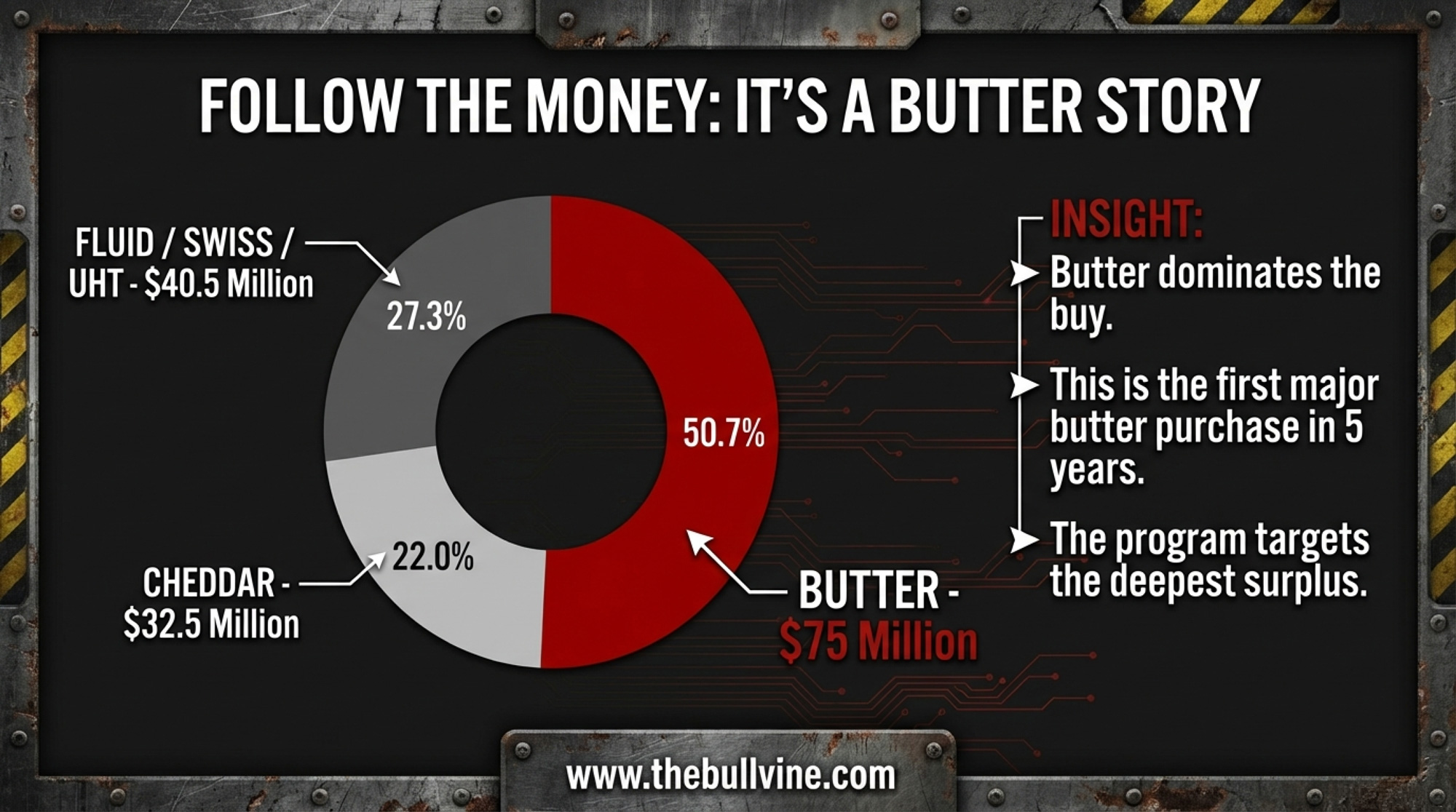

The $148 million breaks down into five commodity categories, and the allocation tells you exactly where USDA sees the deepest surplus problem:

Butter: $75 million (50.7% of dairy total)

Cheddar cheese: $32.5 million (22.0%)

Fresh fluid milk: $20.5 million (13.9%)

Swiss cheese: $10 million (6.8%)

UHT (shelf-stable) milk: $10 million (6.8%)

Butter dominates. That’s not random — it’s where the price crash has been worst. NMPF specifically noted that these are “the first major butter purchases in five years.” The remaining $115 million in the broader announcement covers non-dairy commodities: dried beans ($25 million), split peas ($24 million), fresh pears ($15 million), walnuts ($15 million), lentils ($14 million), chickpeas ($12 million), and pecans ($10 million).

Dairy got the single largest allocation of any category. That matters.

How $148 Million Became the Number

This wasn’t a surprise. NMPF sent USDA a letter last November requesting exactly $148 million in dairy purchases. What followed, in NMPF’s own words, were “extensive conversations and further official communication with USDA”. When the announcement dropped on February 19, it matched the request to the dollar.

Gregg Doud — NMPF’s president and CEO since September 2023, a former Chief Agricultural Negotiator under President Trump’s first term, and a Kansas farm kid who still runs cattle — framed it as demand support: “Dairy farmers have shared in the struggles faced throughout the agricultural economy.”

That’s the advocacy pipeline working. NMPF identified the surplus problem, built the case with USDA, and delivered a specific ask. Whether you’re an NMPF member co-op shipper or not, this is what organized lobbying looks like when it produces results. The question is whether those results reach your bulk tank.

If you ship to an NMPF member co‑op, this is your dues at work; if you don’t, you’re still riding the same CME prices, just without the direct contract upside.

What Is a Section 32 Purchase and How Does It Work?

Section 32 of the Agricultural Adjustment Act of 1935 authorizes the USDA to buy surplus U.S.-produced agricultural products for two purposes: stabilize farm markets and supply food to federal nutrition assistance programs.

Here’s the mechanism, step by step:

USDA’s Agricultural Marketing Service issues Purchase Program Announcements.

Approved vendors — processors, not farmers — submit bids.

USDA awards contracts to winning bidders.

Processors deliver products to food banks and nutrition programs.

The purchased volume exits the commercial market, reducing available supply.

That fifth step is where farm‑level impact starts, in theory. Removing surplus from the market tightens supply, which supports commodity prices on the CME, which flows through FMMO formulas into component pricing, which eventually — weeks to months later — appears on your milk check.

Five steps. None of them is “USDA writes a check to a dairy farmer.” This is a market-support mechanism, not a direct payment. That distinction matters.

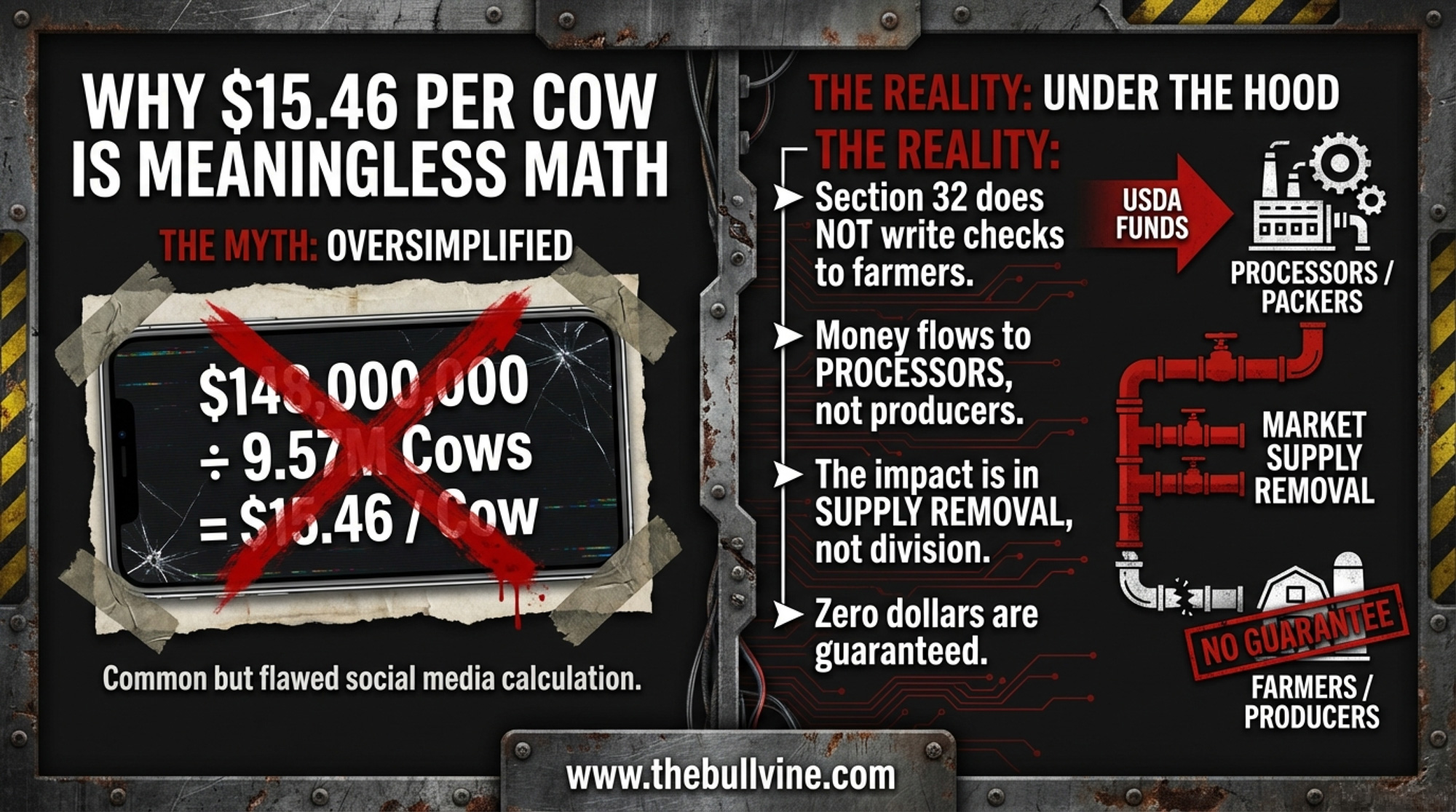

The Per-Cow Reality Check: Why $15.46 Is a Meaningless Number

You’ll see this math on social media: $148 million ÷ 9.57 million U.S. dairy cows = $15.46 per cow. Sounds underwhelming, right?

It’s also completely irrelevant. Section 32 doesn’t distribute money per cow. It removes the product from the market. The $15.46 figure tells you nothing about the actual price-support effect, which depends on how much volume gets pulled, from which markets, at what prices, and how CME traders respond.

The per-cow math is a useful headline killer, though. And that’s the point: $148 million sounds massive until you spread it across the national herd. The real impact isn’t in the division. It’s in the market math.

Butter vs. Cheese: One Big Lever, One Tiny One

This is where the numbers get interesting. The $75 million butter purchase is the headline within the headline. Here’s why.

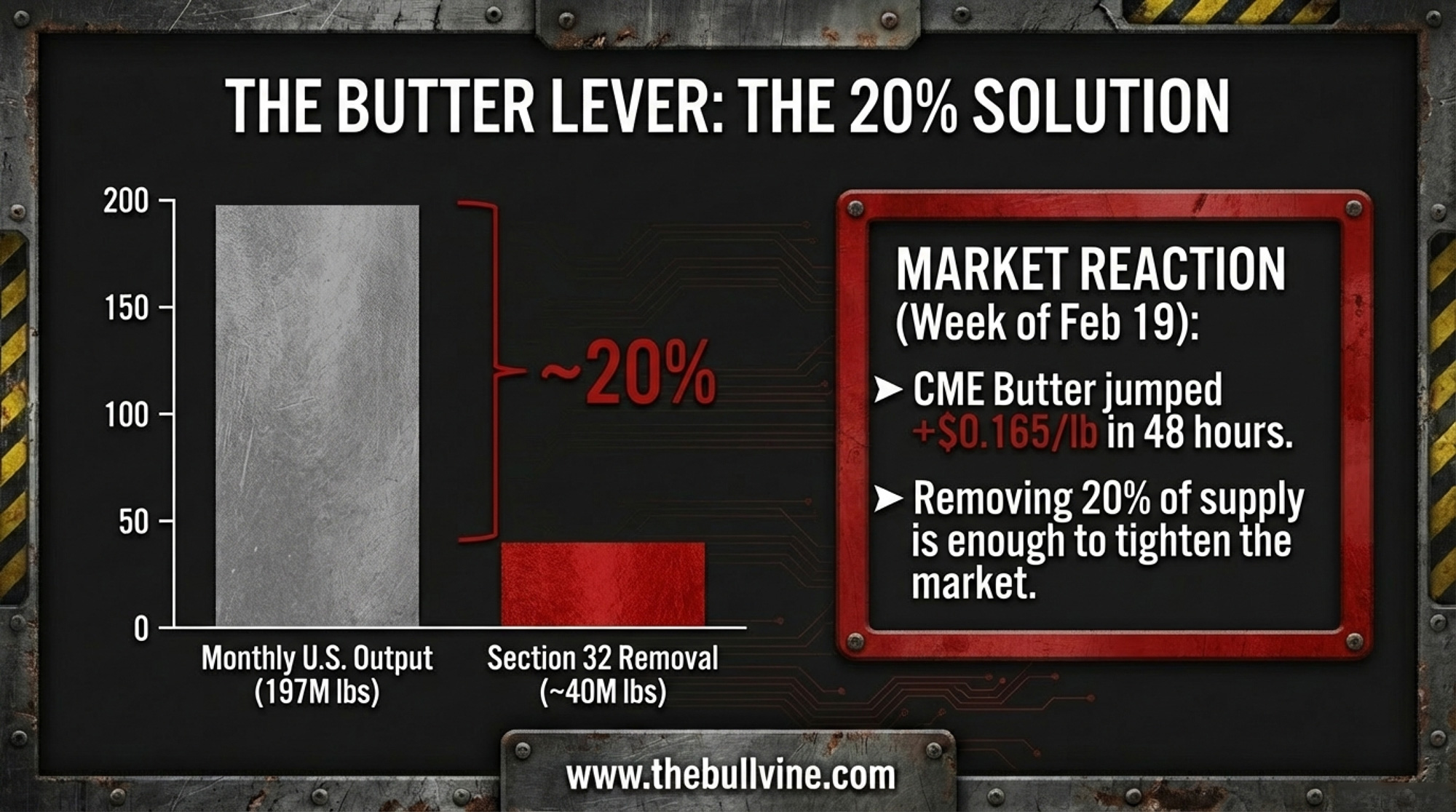

Butter math: At CME cash butter prices of $1.8700/lb on Friday, February 20, 2026, $75 million buys roughly 40 million pounds of butter. December 2025 U.S. butter production was 204 million pounds, according to USDA NASS’s Dairy Products report released on February 5, 2026. Full-year 2025 butter output hit 2.36 billion pounds — an average of about 197 million pounds per month. That $75 million purchase removes roughly 20% of one month’s productionfrom the commercial market.

Metric

Butter

Cheddar Cheese

Purchase Amount

$75 million

$32.5 million

Pounds Purchased

~40 million lbs

~21.7 million lbs

Typical Monthly Production

~197 million lbs

~1.28 billion lbs

% of Monthly Output Removed

20.3%

1.7%

Likely CME Price Impact

$0.10–0.15/lb

$0.01–0.02/lb

Twenty percent is significant. It’s not catastrophic-surplus territory, but it’s enough to tighten the market meaningfully — especially with butter already climbing. CME cash butter opened the announcement week at $1.7050 on Tuesday and closed Friday at $1.8700, a $0.165/lb gain in four trading sessions. That’s not all Section 32 — other factors are in play — but the timing is hard to ignore.

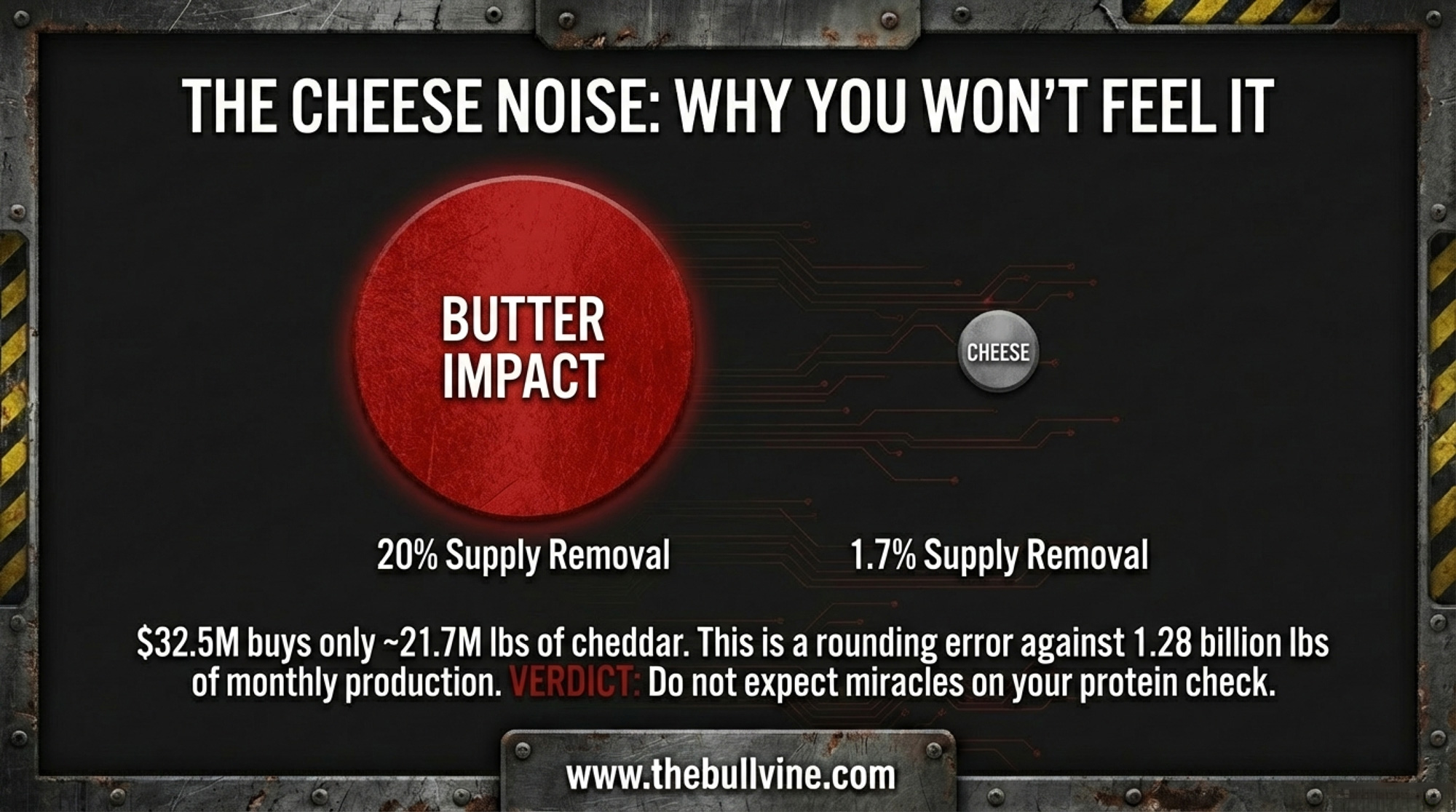

Cheese math: The $32.5 million cheddar purchase at roughly $1.50/lb buys about 21.7 million pounds. December 2025 total cheese production was 1.28 billion pounds. That’s barely 1.7% of one month’s output. Meaningful for cheddar specifically, but a rounding error for the broader cheese market.

The takeaway: If you’re a high-butterfat herd, this purchase tilts in your favor. If your income depends more on protein and cheese prices, the direct effect is minimal. Butter is the big lever here. Cheese is noise.

How Much Will This Actually Affect Milk Prices?

Now for the barn math that connects the announcement to your component statement.

Start with butter. If the Section 32 purchase contributes even $0.10/lb to sustained butter price support — and the $0.165/lb rally this week suggests that’s conservative — here’s what it means at the farm level:

The Class IV butterfat price is derived directly from CME butter. A $0.10/lb butter increase translates to roughly $0.10/lb on your butterfat component price. For a 200-cow herd shipping 23,000 lbs/cow/year at 4.1% butterfat:

Monthly milk shipped: ~383,333 lbs

Monthly butterfat lbs: ~15,717 lbs

Value of $0.10/lb BF increase: ~$1,572/month, or $18,860 annualized

For a 400-cow herd at the same test? Double it: roughly $3,144/month.

That’s real money — if the butter rally holds and if your co-op’s component premiums reflect it. Two big ifs.

Now cheese. A $32.5 million purchase removing 1.7% of monthly production might support block prices by $0.01–0.02/lb at best. On your protein check, that’s almost invisible.

Bottom line: This purchase is a butterfat story. Your Class IV components — butterfat specifically — are where the action is. If your herd tests 3.6% fat, the impact is noticeably smaller than at 4.2%. Run it with your own numbers.

Why Now — and How Does This Compare?

Butter prices crashed from roughly $2.50/lb in mid-2025 to around $1.50/lb by January 2026 — a 40% decline in six months. CME cheese blocks were sitting at $1.45/lb before the announcement week. Global milk production — what analysts have called the “wall of milk” — has been pressuring commodity prices across the board.

NMPF called this the first major butter purchase in five years. That’s significant context. For comparison:

2020 COVID-era: USDA purchased roughly $1.33 billion in dairy products across multiple programs, including about $100 million/month in Section 32 alone. That removed an estimated 238 million pounds of cheese and 64 million pounds of butter over the year.

2020 Section 32 specifically: A $120 million cheese-and-butter purchase removed about 23 million pounds of cheese and 3.6 million pounds of butter per month.

January 2026: USDA bought $80 million in specialty crops under Section 32 — no dairy in that round.

At $148 million, this is the largest single-round Section 32 dairy purchase outside of COVID emergency spending. It’s substantial. It’s also one-time, not recurring. The 2020 program ran for months. This is a single injection.

The Market Already Moved

Here’s what happened on the CME the week of the announcement:

Commodity

Tue 2/17

Wed 2/18

Thu 2/19 (Announcement)

Fri 2/20

Weekly Change

Butter ($/lb)

$1.7050

$1.7050

$1.7800

$1.8700

+$0.1650

Blocks ($/lb)

$1.4500

$1.5000

$1.5100

$1.4975

+$0.0475

Barrels ($/lb)

$1.4500

$1.4700

$1.4700

$1.4900

+$0.0400

NFDM ($/lb)

$1.5900

$1.5975

$1.6225

$1.6850

+$0.0950

Butter jumped $0.075/lb on announcement day alone and added another $0.09 on Friday. That’s a two-day move of $0.165/lb — the kind of swing that moves component checks. Blocks and barrels gained modestly. NFDM surged nearly a dime on the week.

The market is pricing in the volume removal. Whether it holds through March and April — when the actual Purchase Program Announcements are issued, and contracts are awarded — is the open question.

What $148 Million in Section 32 Purchases Means for Your Component Check

Check your butterfat test. This purchase overwhelmingly favors high-BF herds. At 4.0%+ test, the butter rally has meaningful upside for your Class IV components. At 3.5%, the effect is roughly half as large.

Watch CME butter through March. If butter sustains above $1.85/lb through mid-March, the Section 32 volume removal is working as intended. If it fades back below $1.70, the purchase wasn’t enough to absorb the surplus.

Don’t expect cheese miracles. The $32.5 million cheddar purchase is too small relative to monthly production (1.28 billion pounds in December alone ) to meaningfully move block or barrel prices. Your protein check won’t feel this.

Know the timeline. USDA hasn’t issued the Purchase Program Announcements yet. Approved vendors still need to bid. Contracts need awarding. Product needs to ship. The actual volume won’t leave the commercial market for weeks, possibly months.

Ask your co-op. Does your cooperative supply USDA commodity programs? If so, this purchase directly increases demand for your co-op’s output. If not, you’re relying entirely on the indirect price-support effect.

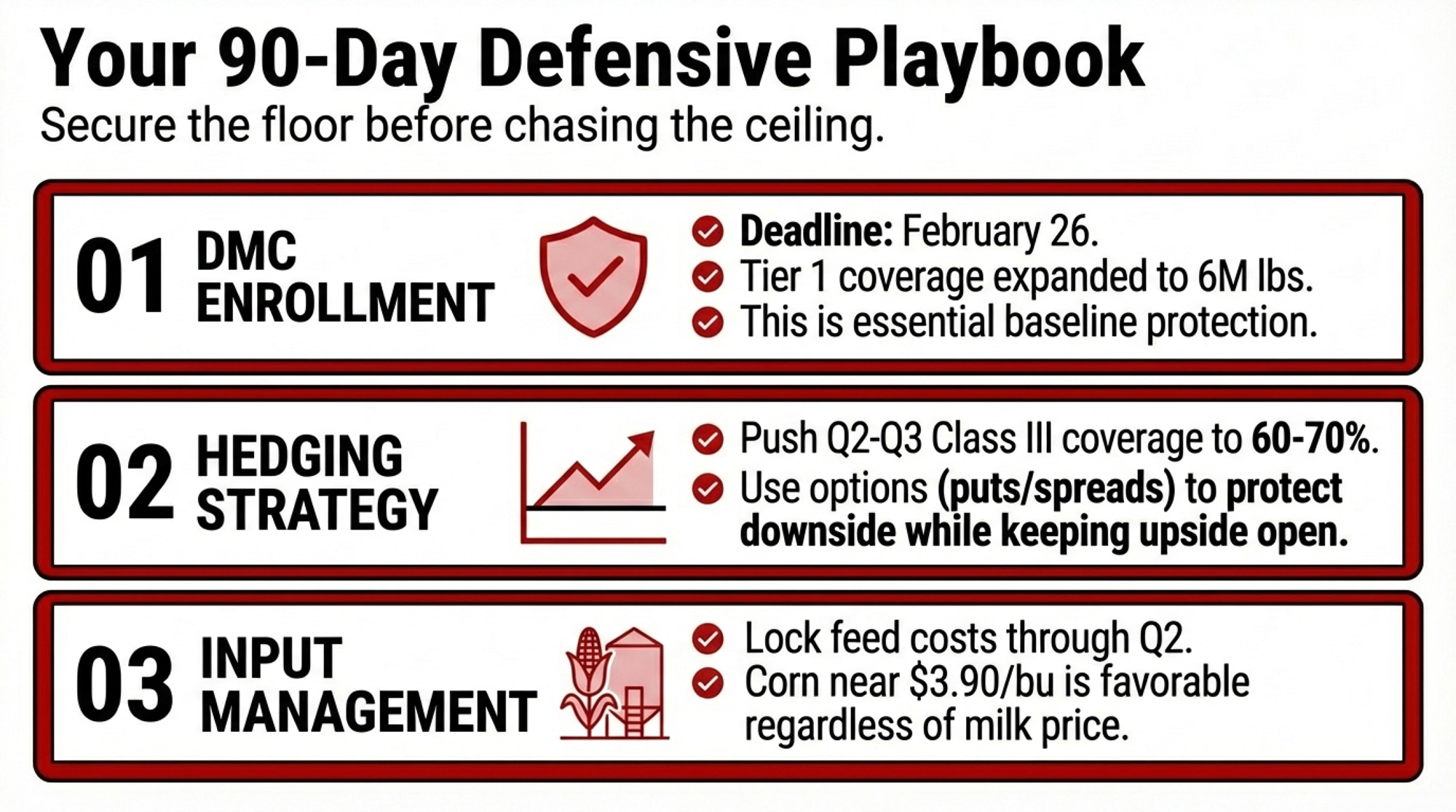

Review your risk coverage. DRP (Dairy Revenue Protection) is available for purchase on any business day when prices are published on RMA’s website — there’s no fixed quarterly enrollment window. If butter holds its rally, Class IV DRP coverage premiums will rise as expected revenue increases. Locking in current premium levels sooner rather than later may make sense for Q2 and Q3 2026 quarters. Separately, DMC enrollment for 2026 closed February 26 — if you missed it, DRP is your remaining federal safety-net option.

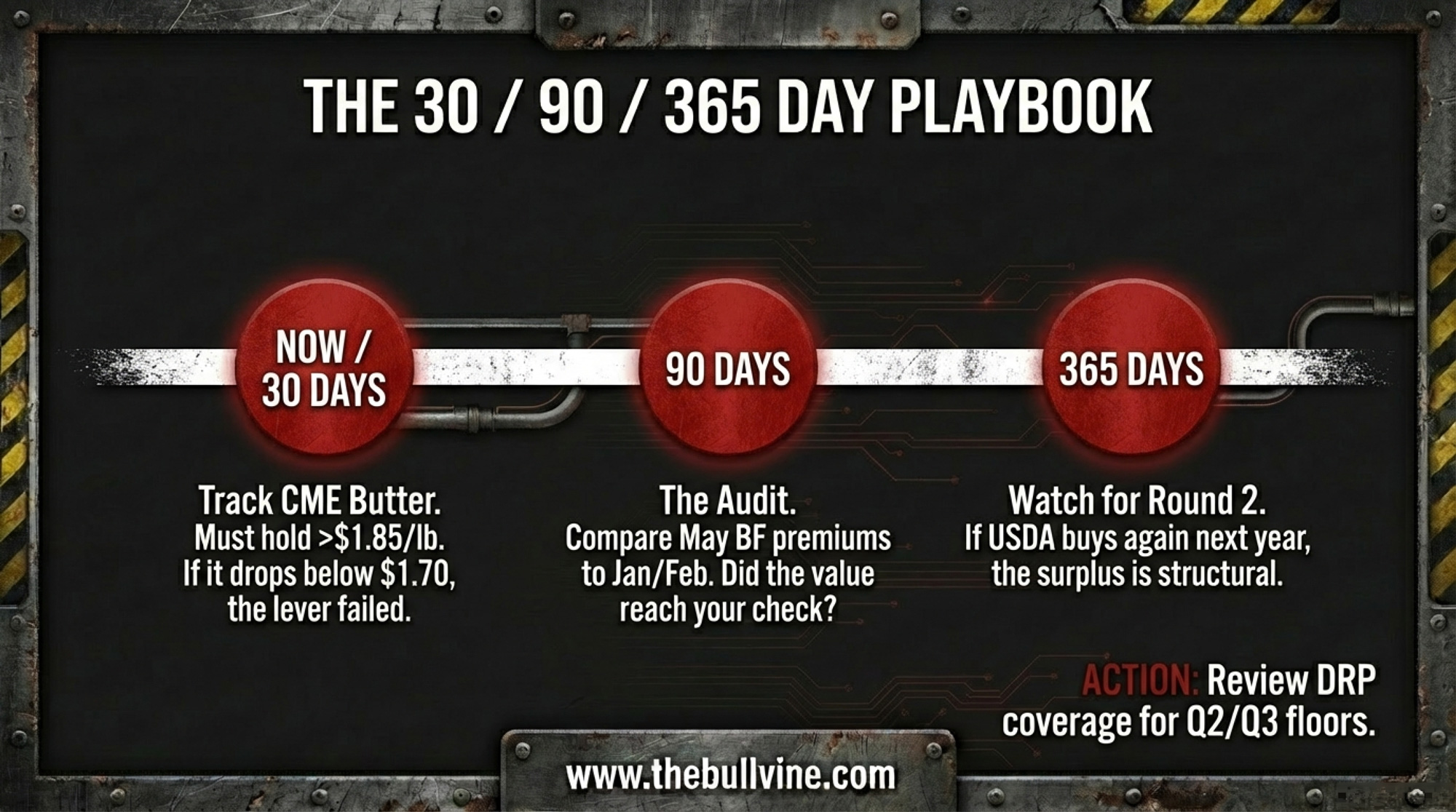

Your 30/90/365-Day Playbook

Timeline

What to Track

Key Threshold

Action If Threshold Met/Missed

This Week

USDA AMS Purchase Program Announcement

Announcement posted

Read for delivery windows, product specs, quantity breakdowns

30 Days

CME butter & cheese block prices

Butter holds above $1.85/lb

Price support working; below = surplus bigger than $75M can fix

90 Days

Your co-op component statement (April/May)

BF premium reflects butter rally

If butter held but BF premium flat = question for co-op field rep

365 Days

Total 2026 Section 32 dairy purchases vs. 2024/2025

Second round announced

Signals structural surplus, not seasonal—NMPF pipeline now recurring

This week: Read the USDA AMS Purchase Program Announcement when it posts. It will specify exact product forms, quantities, and delivery windows. That’s when you’ll know whether this is a 60-day buy or a 6-month program.

30 days: Track CME butter and cheese block prices. The $1.85/lb butter threshold is your marker. Above it, the purchase is supporting prices. Below it, the surplus is bigger than $75 million can fix.

90 days: Pull your co-op component statement for April or May. Compare your butterfat premium to January and February. If butter held above $1.85 through March and your BF premium didn’t move, that’s a question for your co-op field rep.

365 days: Compare the total 2026 Section 32 dairy purchases to 2025 and 2024. If USDA comes back for a second round, it signals the surplus problem is structural, not seasonal — and that NMPF’s advocacy pipeline is becoming a recurring feature of dairy price support.

Key Takeaways

USDA’s $148 million dairy allocation under Section 32 is exactly what NMPF asked for last November and marks the largest non‑COVID dairy purchase in five years.

None of that money arrives as a farm check — it pays processors, and the only way you see it is if it pushes CME prices high enough to lift FMMO component values on your milk check.

Butter is where it bites: $75 million pulls roughly 40 million pounds — about 20% of a typical month of U.S. butter output —, and CME butter already moved $0.165/lb higher during the announcement week.

The cheddar piece is small by comparison: $32.5 million removes only about 1.7% of a month’s cheese production, so don’t expect a big protein or Class III bump from this round alone.

If your herd ships 4%‑plus butterfat, a sustained $0.10/lb increase in butterfat value can add more than $1,500/month per 200 cows, which makes watching butter hold above roughly $1.85/lb and checking how your co‑op adjusts component premiums a key decision point.

The Bottom Line

$148 million isn’t a rescue. It’s a market lever—and specifically, a butter lever. NMPF asked for it, USDA delivered it, and the CME responded with a $0.165/lb butter rally in 48 hours. Whether that holds depends on what happens when the actual contracts hit and the product starts moving.

Pull your last component statement. Find the butterfat line. Now add $0.10/lb and multiply by your monthly butterfat pounds. That’s the upside scenario from this purchase — not $148 million divided by your herd size, but butter price × your components × time.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

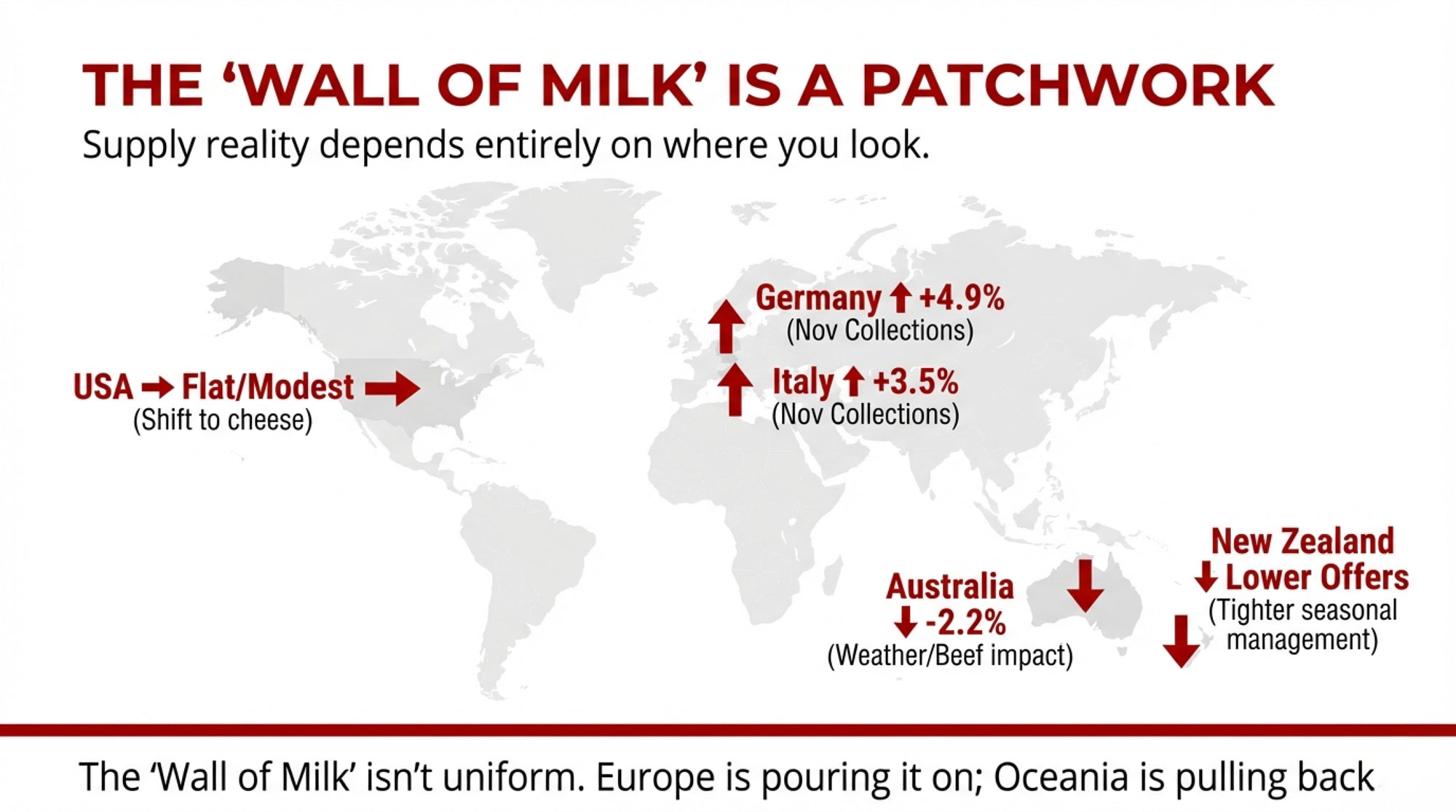

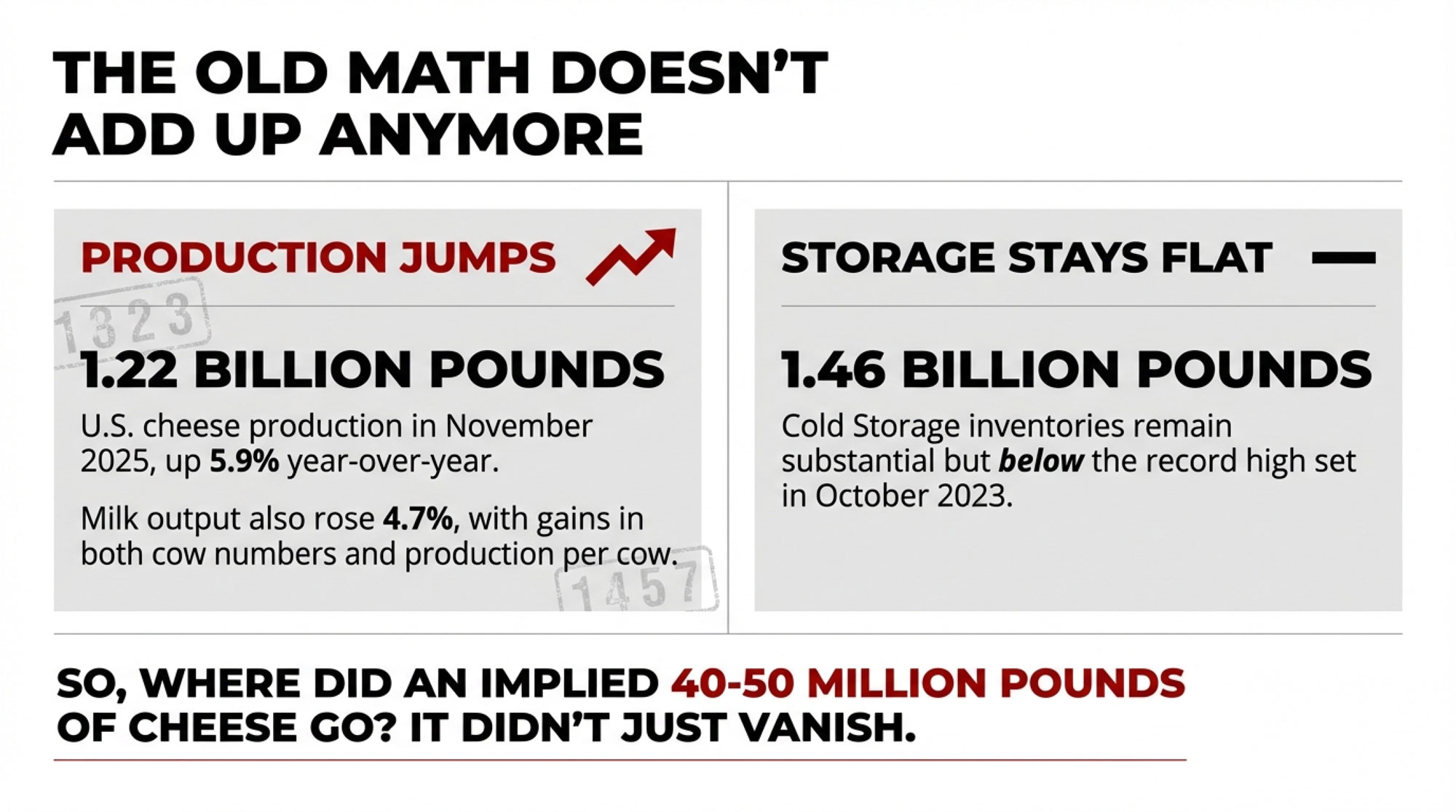

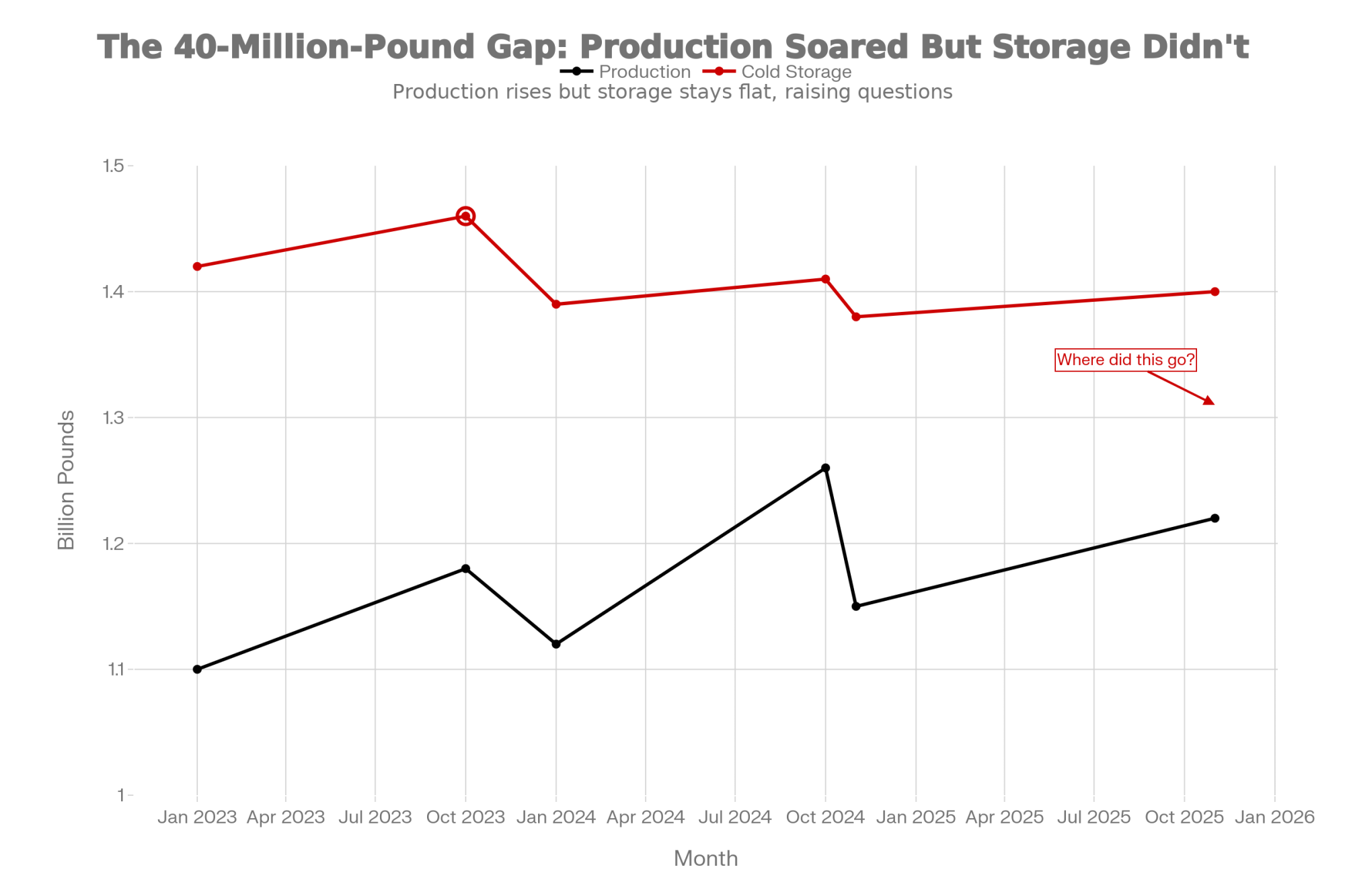

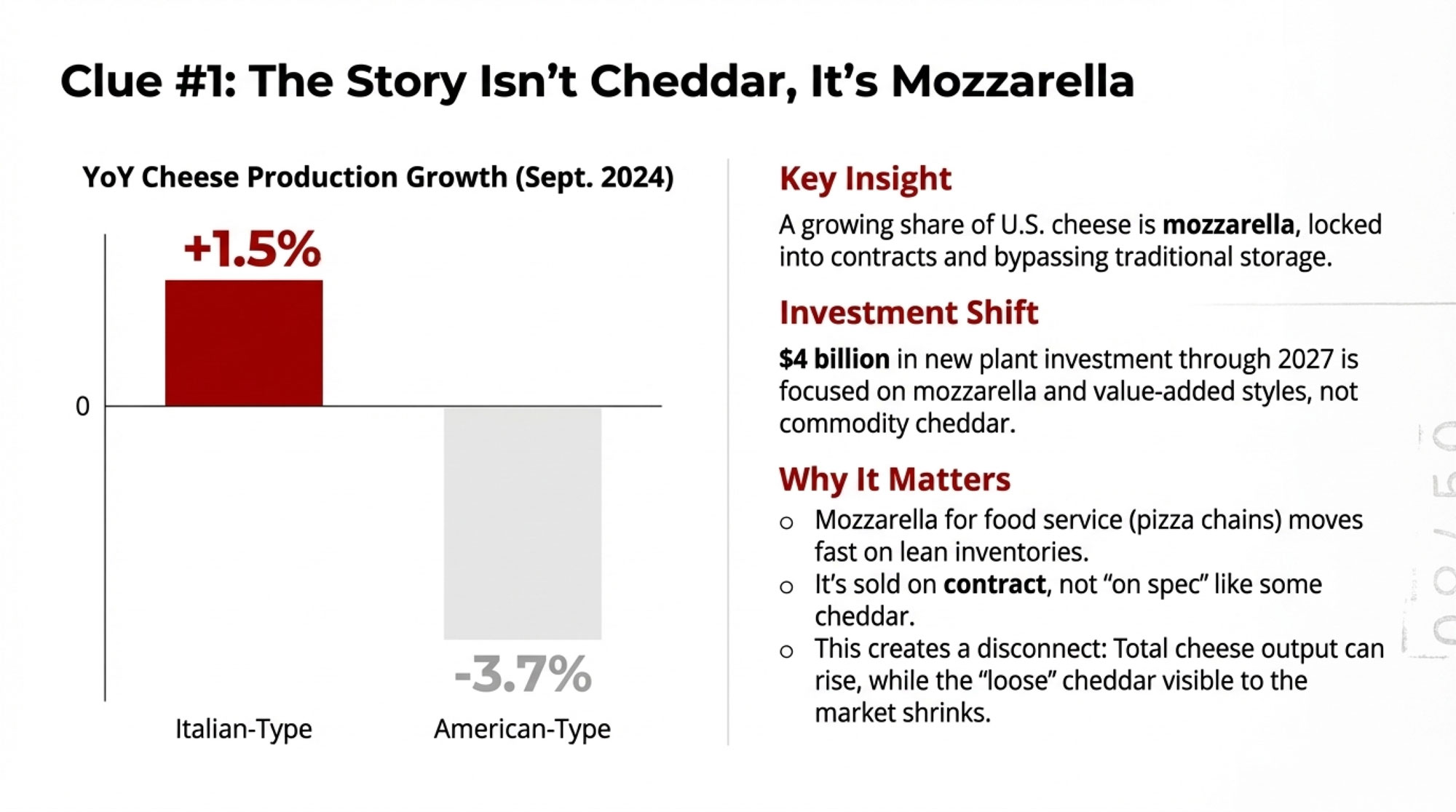

The Wall of Milk: Making Sense of 2025’s Global Dairy Crunch – Reveals the structural supply collision between the U.S., EU, and New Zealand that is currently capping your upside. This strategic analysis exposes the “biological trap” of beef-on-dairy and helps you position your operation for the next three years.

Genetic Revolution: How Record-Breaking Milk Components Are Reshaping Dairy’s Future – Delivers a deep dive into the genomic surge that “pre-loaded” the national herd for record butterfat. It identifies the emerging genetic traits—from feed efficiency to methane indexes—that will determine which dairies remain competitive through the 2030s.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

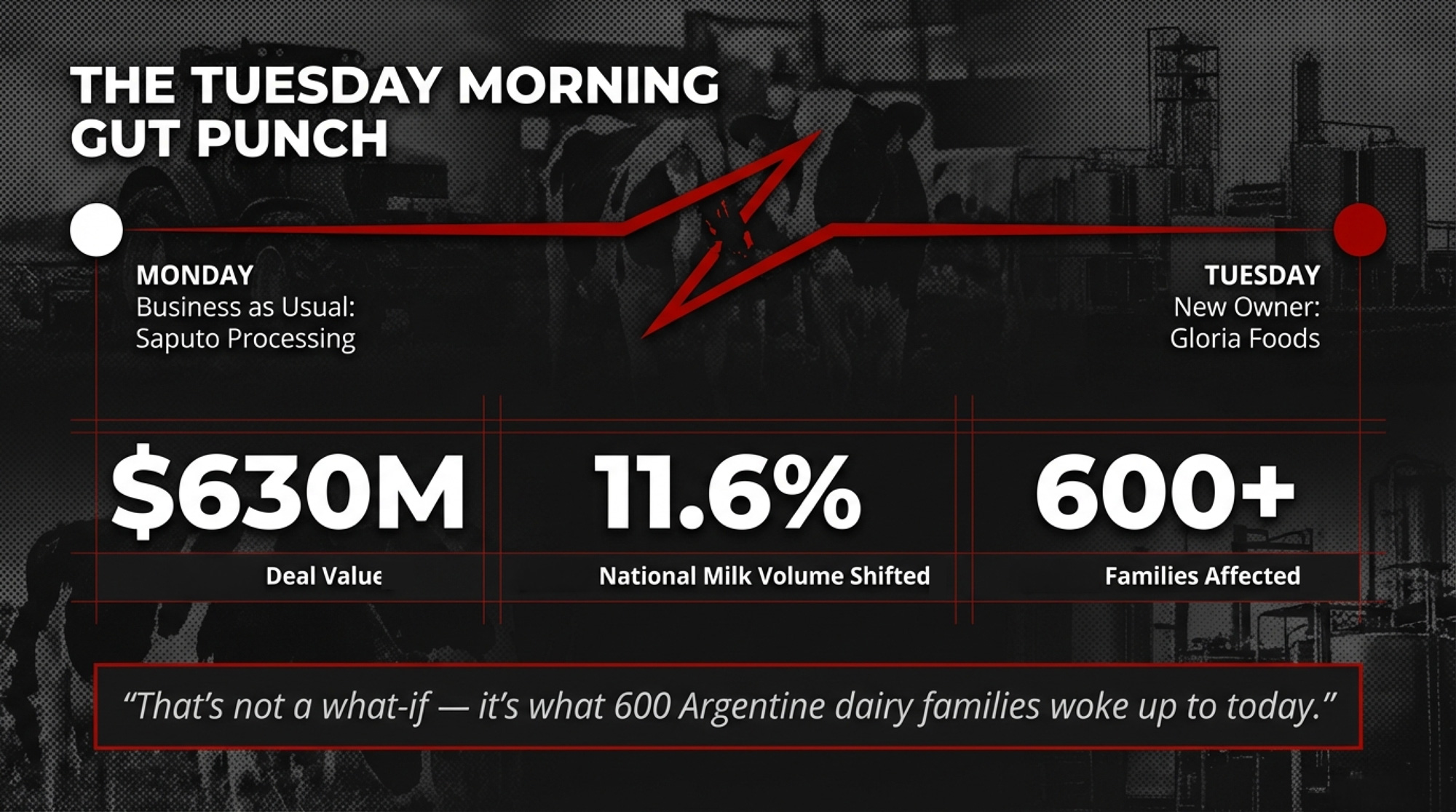

Your milk goes to one processor. Overnight, they sell 80% to a stranger. That’s not a what‑if — it’s what 600 Argentine dairy families woke up to today.

Executive Summary: Saputo is selling 80% of its Argentine dairy division to Peru’s Gloria Foods in a deal that values the business at C$855 million (about US$630 million), while keeping a 20% stake. Overnight, control of Argentina’s largest milk processor — 11.6% of the nation’s industrial milk and collections from more than 600 farms — shifts to a buyer that’s been sued for abusing its power with producers in Chile, fined in Colombia for adding whey to “whole” milk, and accused of monopolistic practices in Peru. Farmers shipping to Saputo’s Rafaela and Tío Pujio plants learned about the deal from a press release instead of a phone call, and they still don’t know if Gloria will keep their contracts, prices, and pickup schedules intact. They’re dealing with that gut punch in a sector where SanCor has just entered creditor protection and co‑ops’ share of Argentina’s milk has collapsed from roughly 34% to about 3%, leaving most producers tied closely to a single processor. Add in Gloria’s aggressive acquisition run and rising debt‑service costs at its Peruvian holding company, and you have a new owner that’s highly motivated to manage margins hard once the ink dries. This article walks you through what’s happening to those 600 Argentine dairy families — and gives you a concrete playbook to check whether your own processor contract would protect you if the company you ship to sold tomorrow without warning.

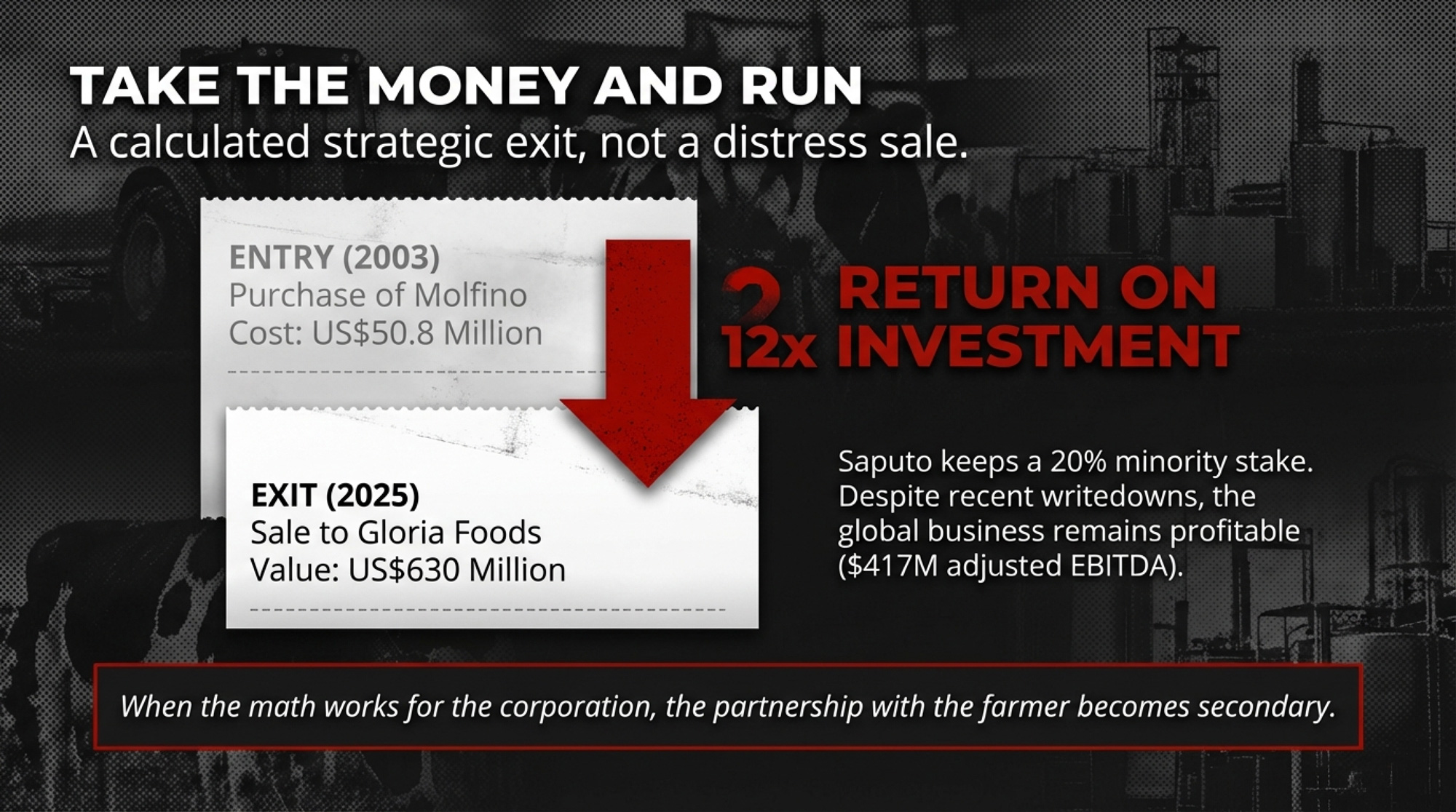

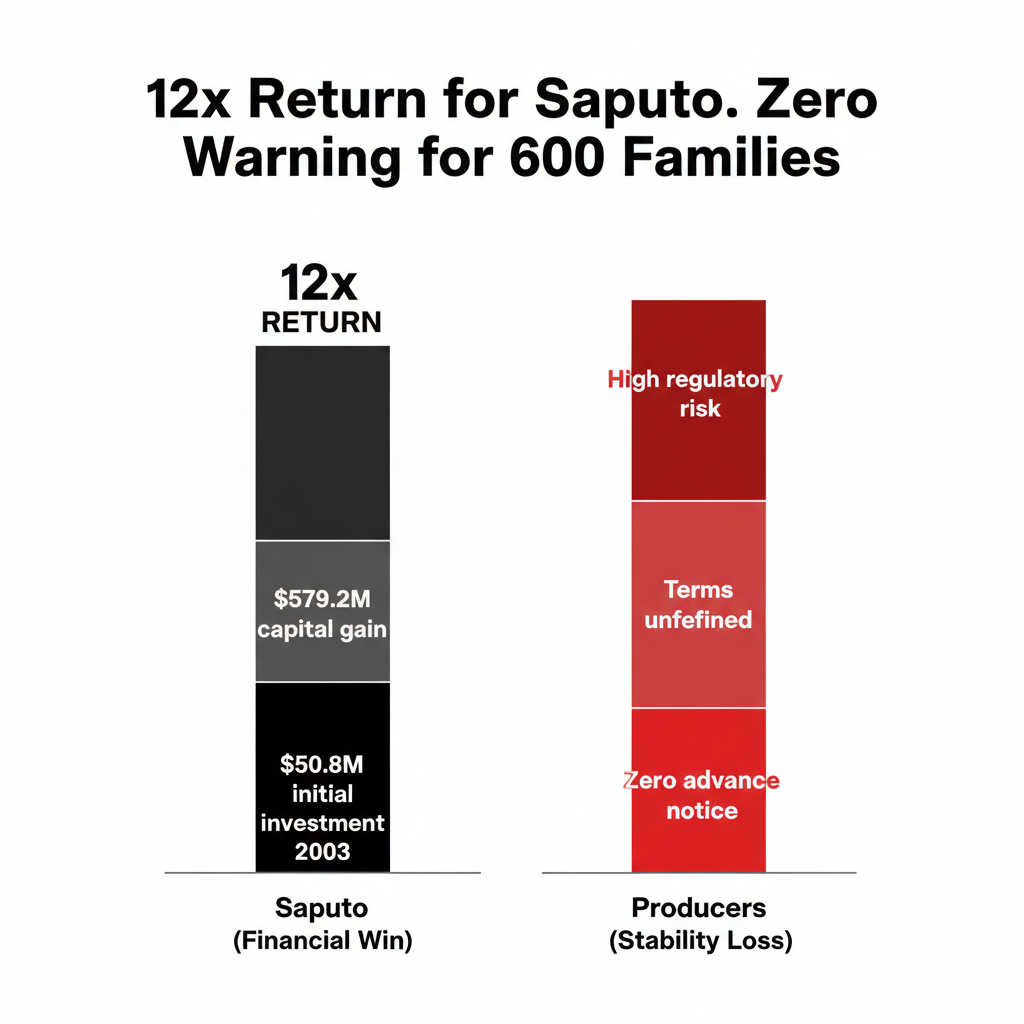

Saputo Inc. announced today that it’s selling 80% of its Argentine dairy division to Gloria Foods — the dairy arm of Peru’s Grupo Gloria — for an enterprise value of C$855 million. That works out to roughly US$630 million, including assumed debt, though Peruvian business media report the equity purchase price closer to US$500 million. Saputo expects net proceeds after tax of approximately C$543 million (US$400 million). The company keeps a 20% minority stake. The deal covers two processing plants, the La Paulina, Ricrem, and Molfino brands, and a milk collection network serving more than 600 dairy farms across Santa Fe and Córdoba provinces, according to Argentine agricultural media, including LA17 and Bichos de Campo.

This is what dairy processor consolidation risk looks like in practice. Those 600 families weren’t part of the conversation — and the company taking over has a record across Latin America that every producer, Argentine or not, ought to understand before this deal closes around mid-2026.

If you read nothing else this month, pair this with our recent piece on the four questions every dairy producer should ask about processor dependency. What’s happening in Argentina right now is a textbook case of what that audit is designed to prevent.

How Saputo Built Argentina’s Top Dairy Operation — Then Walked Away

Saputo entered Argentina in November 2003 by acquiring Molfino Hermanos S.A. from Molinos Río de la Plata for US$50.8 million. At the time, Molfino was the country’s third-largest processor — two plants, roughly 850 employees, about US$90 million in annual revenue. Over 23 years, Saputo turned that into the country’s number-one operation.

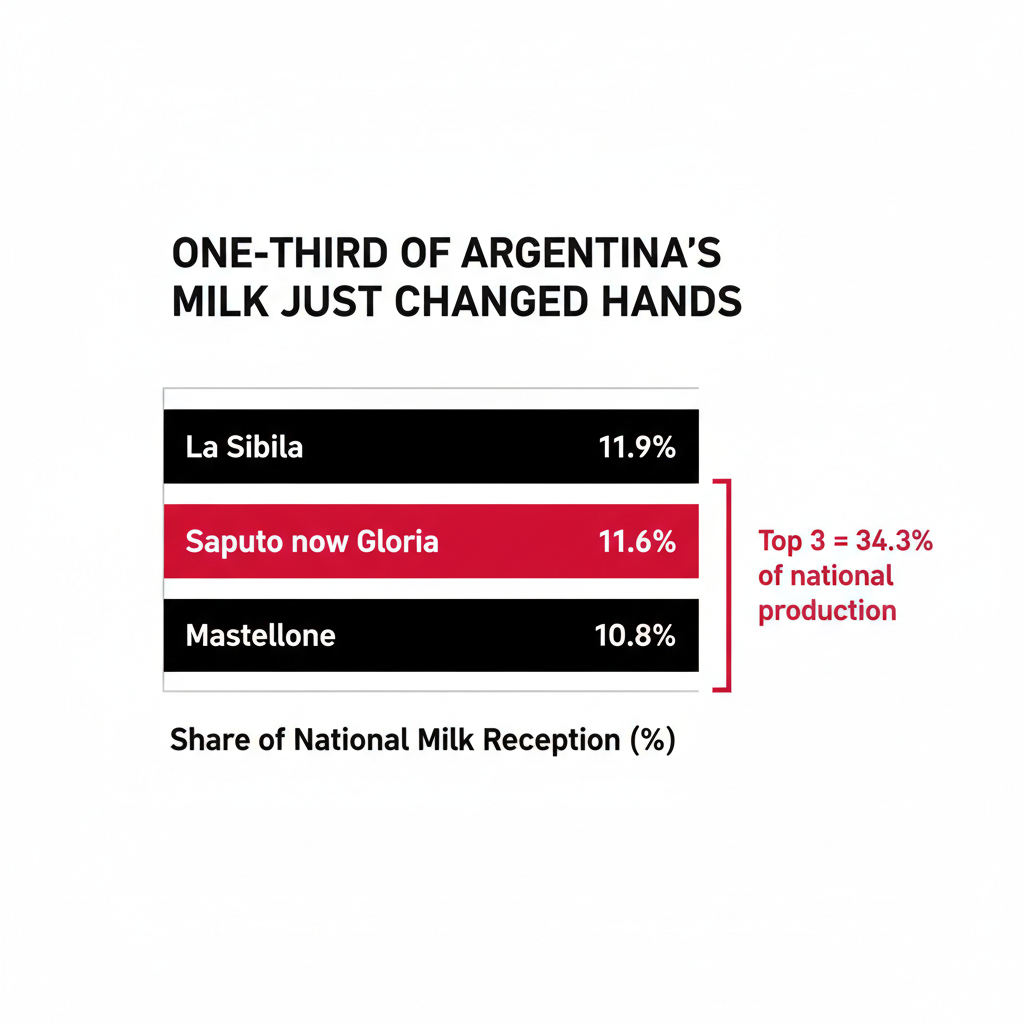

The OCLA 2023/24 industry ranking — based on reported and estimated daily milk reception by industrial processors, published annually — had Saputo processing an average of 3,650,288 liters per day, or 12.5% of national industrial milk volume. By the most recent OCLA 2024/25 ranking (published July 2025), that figure had dropped to 3.53 million liters daily, or 11.6% of the national total. Still number one, ahead of Mastellone (La Serenísima) at 3.15 million liters and 10.8%, but the decline hints at the pressures behind Saputo’s decision to sell. In the last four quarters, the Argentine operation generated approximately C$1.2 billion in revenue — about 7% of Saputo’s consolidated total.

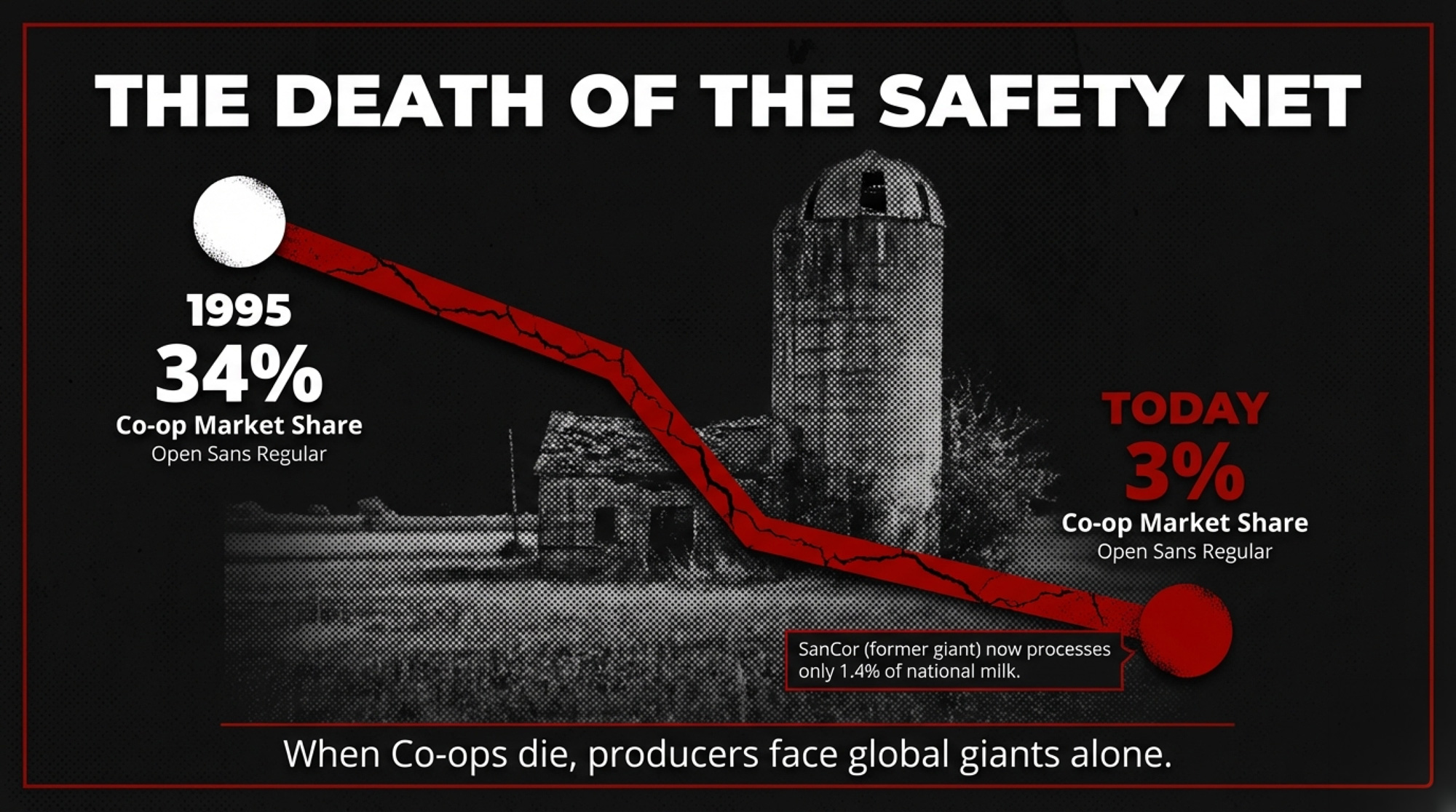

When SanCor — once Argentina’s cooperative giant — entered a deep financial crisis beginning in 2017 (as SanCor put it in its February 2025 court filing), Saputo moved quickly. The company absorbed the freed-up milk supply and routinely offered prices better than competitors’. Producers followed the money. You would have too.

And then SanCor’s story got worse. On February 2, 2025 — just ten days before today’s Gloria announcement — SanCor formally filed for concurso preventivo de acreedores (creditor protection proceedings) at the Commercial Court in Rafaela, Santa Fe, carrying approximately US$400 million in debt. SanCor now processes just 409,163 liters daily, barely 1.4% of national production, down from its peak of 1.2 million. The region’s dairy infrastructure isn’t just shifting; it’s transforming. It’s being completely restructured.

Saputo’s dominance also created structural dependency. The practical effect was that Saputo’s price signals shaped the broader regional market — when the biggest buyer in the milkshed moved, everyone else followed. That arrangement works fine. Right up until the company at the center decides to leave.

CEO Carl Colizza’s press release language was corporate but clear: “This divestiture enhances our financial flexibility and supports targeted reinvestment in platforms that offer the highest growth opportunities.” Translation: take a roughly 12-fold return on a 23-year investment (US$630M enterprise value on a US$50.8M entry) and redeploy capital somewhere with fewer currency crises.

600 Families, No Advance Notice

Here’s what we know about how this landed on the ground. As of publication — hours after the announcement — there’s been no reported communication from Gloria Foods to Argentine producers. No new contract terms. No timeline for meetings. No word on whether existing payment schedules, quality premiums, or pickup logistics will change. Infocampo described the news as a “sacudón” — a jolt — to the Argentine dairy chain.

Several cooperatives sit squarely in Saputo’s milkshed. Cooperativa Tambera Central Unida in San Guillermo, Santa Fe — managed by Javier Clemente — delivers milk to five processing companies, including Saputo. Clemente has spoken publicly about producer autonomy in the region: “The one who decides where their production goes is the member, because the milk belongs to whoever produces it.” He made those remarks before the Gloria deal was announced. His cooperative is now directly affected, and whether that principle holds when a Peruvian conglomerate replaces a Canadian one is the question nobody can answer yet.

Cooperativa Agrícola Santa Rosa, also near San Guillermo and managed by Martín Guruceaga, works with approximately 60 farms across a 40-kilometer radius. Guruceaga has described the area simply as “una zona tambera” — a dairy zone where the community and the industry are one and the same. UNCOGA, a federation of nine cooperatives spanning central-west Santa Fe and central-east Córdoba, operates across the heart of Saputo’s collection territory.

These cooperatives are the closest thing to a collective voice that affected producers have. But the cooperative system itself has been hollowed out. Cooperative share of Argentine milk reception dropped from 34% in 1995 to roughly 3%today, according to the OCLA 2024/25 industry ranking. That means most of those 600-plus farms negotiate individually with their processor. When that processor changes without warning, individual leverage is essentially zero.

“The dairy sector and the country will only grow when the producer grows, because the producer is the one who carries the activity in their blood.” — Daniel Oggero, APLA executive committee, El Litoral, July 2015

Oggero made that statement during a blockade of Saputo’s Rafaela plant by western Santa Fe dairy farmers protesting milk price cuts. Those words land differently today, when the producer’s voice in the transaction was exactly zero.

Why Saputo Sold — And What Gloria’s Track Record Shows

Understanding both sides of this deal matters if you’re trying to figure out what comes next.

Why Saputo left: This isn’t a distressed sale. Through FY26, Saputo’s efficiency program has been delivering: Q1 operating cash flow hit C$317 million (up 66% year-over-year), adjusted EBITDA reached C$417 million (up 12.7%), and the company has been buying back shares aggressively. Saputo reported net losses of C$250 million through the nine months ended December 2024, driven largely by writedowns and hyperinflation accounting adjustments tied to Argentina — but the underlying business is profitable and improving. Saputo chose to leave. That tells you how the company views Argentine risk-reward going forward.

Who Gloria is: Gloria Foods is the dairy platform of Grupo Gloria, a Peruvian conglomerate with more than 7,000 employees across Peru, Chile, Bolivia, Argentina, Colombia, and Ecuador. President Claudio Rodriguez called the Saputo acquisition “a milestone within the strategy of sustained growth in Latin America.” The expansion has been rapid: Soprole in Chile from Fonterra for approximately US$644 million (completed April 2023), Ecuajugos from Nestlé in Ecuador (2024), and now Saputo Argentina.

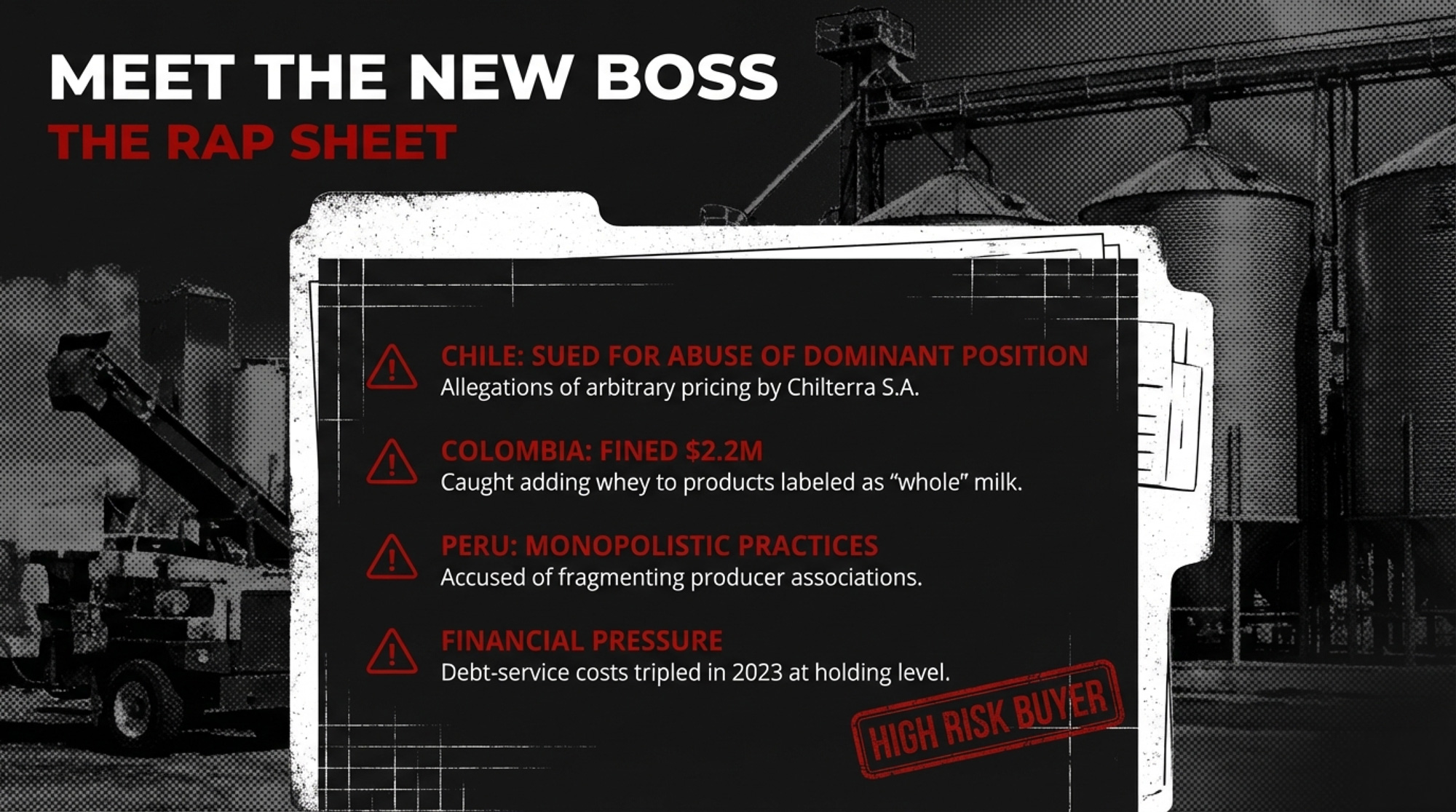

But that growth has come with a trail of regulatory actions and producer-relations disputes. Not one-offs. A pattern across multiple countries.

In Peru, former AGALEP (national dairy farmers’ association) president Javier Valera publicly described Gloria’s market behavior as monopolistic. His successor, Nivia Vargas, accused the company of offering infrastructure only to larger-volume farms — deliberately fragmenting producer associations and undermining collective bargaining. Gloria has also fought a Peruvian government decree requiring evaporated milk be made from fresh milk. AGALEP leadership says that regulation underpins demand from an estimated 450,000 Peruvian dairy farmers.

In Chile, Gloria’s subsidiary Prolesur faces a lawsuit admitted by the national competition tribunal (TDLC) on January 30, 2025. Plaintiff Chilterra S.A. alleged abuse of dominant position, specifically that Prolesur imposed “unjustified prices through arbitrary and unverifiable criteria”—a system plaintiff Ricardo Ríos described as designed to create total producer dependence.

In Colombia, the Superintendencia de Industria y Comercio fined Gloria, along with Lactalis, Hacienda San Mateo, and Sabanalac in February 2025 for adding whey protein (lactosuero) to products labeled as whole pasteurized milk. The basis: INVIMA laboratory studies from 2019–2020 detected elevated caseinomacropeptide levels — a marker indicating whey protein had been added to a product labeled as pure milk. Gloria’s penalty was US$2.2 million. The company has appealed.

Country

Action / Dispute

Year

Status / Penalty

Peru

Former AGALEP president accused Gloria of monopolistic behavior; producers claim infrastructure access limited to large farms, fragmenting associations

Ongoing

No formal penalty; producer relations remain strained

Chile

Prolesur (Gloria subsidiary) sued for abuse of dominant position—”unjustified prices through arbitrary criteria” designed to create producer dependence

2025

Lawsuit admitted by TDLC competition tribunal Jan 2025; pending resolution

Colombia

Fined for adding whey protein to “whole” milk; INVIMA labs detected elevated caseinomacropeptide (adulteration marker)

2025

US$2.2 million fine; Gloria appealed

Puerto Rico

Exited market entirely after regulatory challenges made operations “unworkable”

2025–26

Complete market withdrawal

Gloria reports investing approximately S/718 million — roughly US$190 million (S/ refers to Peruvian soles) — between 2012 and 2023 in a farmer development program. That figure comes from Gloria itself and hasn’t been independently audited, but the investment claim is on the record. In Puerto Rico, the company exited the market entirely in 2025–2026 after what it described as regulatory challenges that made operations unworkable.

Does any of this predict what happens in Argentina? Not necessarily. Different market, different regulations, different competitive dynamics. But the holding-level financial picture adds context. Holding Alimentario del Perú reported net losses of S/124.9 million (roughly US$33 million) in 2023 and S/62.2 million (~US$16 million) through nine months of 2024, according to Peruvian securities filings. Financial expenses surged from S/123.7 million in 2022 to S/399.5 million in 2023. A company whose debt-service costs tripled in one year is under pressure, even if the core dairy business is profitable.

Nobody’s saying assume the worst. But you’d be wise to ask very specific questions before closing day.

What This Means for Your Operation

This section is about dairy processor risk — and it applies whether you’re milking cows in Córdoba or Ontario or Wisconsin.

Contract Protection

What It Does

Argentine Status

Your Action This Week

Ownership-change clause

Requires new buyer to honor existing contract terms or provides renegotiation window

Missing for most producers

Pull your supply agreement; search for “assignment,” “change of control,” or “transfer” clauses

Minimum notice period

Guarantees 30–90 days’ written notice before contract termination or major changes

Missing for most producers

Check termination section; if absent, negotiate 60-day minimum before any ownership transfer

Unknown—producers waiting for Gloria communication

Verify whether your agreement specifies payment continuity; if not, add it

Secondary buyer relationship

Diversifies risk by routing 10–30% of production to alternative processor

Not common in concentrated markets

Identify regional cheese makers or co-ops; formalize even small-volume backup contract

Collective bargaining vehicle

Cooperative or producer association negotiates on behalf of group

Exists (UNCOGA, cooperatives) but weakened by 3% co-op market share

Join or re-engage with local co-op; coordinate questions for new buyer through group

Regulatory review trigger

Large acquisitions require competition-authority approval, sometimes with producer-protection conditions

Pending—Argentine CNDC reviewing deal

Monitor CNDC decision; if conditions imposed, ensure enforcement mechanisms exist

If you’re in Saputo’s Argentine collection zone: Your contract is the document that matters now. Does it include an ownership-change clause? A minimum notice period? A payment guarantee? If yes, those terms should carry over. If not — or if you don’t have a written agreement at all — you’re negotiating from scratch with a company you’ve never dealt with. Contact your cooperative this week. The latest SIGLEA data (December 2025) shows Argentine farm-gate milk prices averaging AR$476.60 per liter — up only about 8% year-over-year in nominal terms, while costs have continued to rise, putting margins under pressure. Any disruption in payment terms during a processor transition hits harder when margins are already thin.

If you’re a North American Saputo supplier: This looks like an emerging-market exit, not a signal about Saputo’s core North American business. The company is investing in U.S. capacity and showing improving domestic margins. Your situation is structurally different. But the underlying lesson is universal — if your supply agreement doesn’t survive a processor sale, you’re carrying the same risk these Argentine families just discovered. You just haven’t been tested yet.

If you sell to any dominant processor, anywhere: Here’s the math that matters. If one company handles more than 60% of your milk and your agreement has no ownership-change clause, you’re structurally identical to those 600 Argentine families. Geography doesn’t change that equation. What changes it is your contract.

The trend behind this deal — processor consolidation reshaping producer relationships globally — isn’t slowing down. In the past three years, Fonterra sold Soprole to Gloria, Nestlé sold Ecuador operations to Gloria, Savencia acquired Williner in Argentina, and Lactalis bought Dairy Partners Americas. Every transaction meant producers discovering, after the fact, that their buyer had changed.

Four Moves Before Closing Day

1. Pull your supply agreement and read it this week. Look for three things: the termination notice period, the ownership-change transfer provision, and the payment guarantee. If any are missing, that’s your negotiating priority before the new owner takes over. Not after.

2. Engage through your cooperative — and accept the trade-off. UNCOGA, Productores Unidos de Rafaela, and the San Guillermo cooperatives are the existing vehicles for collective action. A unified set of questions to Gloria about contracts, payment terms, and collection schedules carries more weight than 600 separate phone calls. Yes, coordinated engagement could be perceived as adversarial before the relationship starts. Move forward anyway. Silence is worse than friction.

3. Explore a second buyer relationship. Around Córdoba and Santa Fe, small and medium cheese makers (PyMEs queseras) have historically offered competitive raw-milk prices. Diversifying even a portion of production reduces concentration risk. The trade-off is real: approaching alternative buyers pre-closing could signal distrust to Gloria, and logistics with smaller processors are more complex. But having options is always the right strategy. And here’s your trigger — if Gloria hasn’t communicated directly with producers within 60 days of closing, that’s your signal to formalize a secondary buyer relationship. Not explore one. Formalize it.

4. Watch Gloria’s first 90 days after closing. Do they communicate directly with producers? Honor existing terms? Provide timeline certainty? Those are positive signals. Prolonged silence — producers still waiting for a phone call weeks after operational control transfers — tells a different story. What Gloria actually does will matter more than anything in a press release.

Three Signals Between Now and Mid-2026

Argentine regulatory review. This deal requires approval from Argentine authorities. At 11.6% of the national industrial milk volume, the competition authority (CNDC) could attach conditions. Any requirements imposed on Gloria regarding producer terms or pricing would be of enormous importance.

Gloria’s outreach to producers. The single most revealing signal. The company knows 600-plus families are waiting. Whether Gloria reaches out proactively or waits for producers to come to them will tell you which version of Gloria is showing up in Argentina.

Payment performance. SIGLEA reported Argentine farm-gate milk prices at AR$476.60 per liter in December 2025 — up only about 8% year-over-year in nominal terms, while production costs have continued climbing, according to OCLA. Gloria’s ability and willingness to maintain competitive pricing after closing will be the metric that matters most to every producer in the collection zone. Everything else is words on paper.

The broader context here — what processor consolidation means for producer survival — was one of the defining themes of 2025 dairy coverage.

Your Processor Risk Checklist

Audit your contract this week. No ownership-change clause, no defined termination notice, no payment guarantee means you’re carrying processor risk whether you’re in Córdoba or Ontario, or Wisconsin.

Know your single-buyer number. Over 60% of your milk to one processor without contractual protections? You’re in the same structural position as those Argentine families. The difference is timing — you can fix it before the press release drops.

Research your processor’s parent company. Financial pressure at the holding level — like debt-service costs tripling in a year — eventually filters down to producer terms. This applies to your processor too.

Don’t wait for the phone call. If you’re in Saputo’s Argentine collection zone: contact UNCOGA, your regional cooperative, or APLA (headquartered in Suardi, Santa Fe) this week. Ask collectively about contract continuity, payment schedules, and collection logistics. A coordinated ask is harder to ignore.

For North American Saputo suppliers wondering if you’re next: The evidence points to an emerging-market exit driven by Argentine macro conditions, not a systemic pullback. Saputo’s domestic numbers are moving in the right direction. But read your contract. Know what survives a sale.

If you know Argentine producers, share this. If you’ve toured dairy operations in Santa Fe or met producers from the Rafaela corridor at genetics events, connect them with this information. The more that circulates, the better everyone’s decisions get.

The Bottom Line

Guruceaga calls his part of Santa Fe “una zona tambera.” A dairy zone. It sounds simple until you sit with what it means: the cows and the community are the same thing. When the processor changes, the community changes with it.

The hardest part of what happened today isn’t the deal. It’s the sequence. A press release in Montreal. A wire story picked up in Lima. A notification on a phone in a milking parlor somewhere between Rafaela and Tío Pujio. And then the question that 600-plus families are asking right now — the same question every producer who depends on a single buyer should be asking before their turn comes:

Does my contract survive this?

If you don’t know the answer, you already know what to do this week.

Key Takeaways

Saputo is selling 80% of its Argentine dairy division to Gloria Foods for a C$855 million (≈US$630 million) enterprise value, keeping a 20% minority stake.

That puts Argentina’s largest processor — 11.6% of industrial milk and collections from 600‑plus farms — in the hands of a buyer that’s been sued for abuse of dominance in Chile, fined in Colombia over adulterated “whole” milk, and accused of monopolistic behavior in Peru.

Farmers supplying Saputo’s Rafaela and Tío Pujio plants learned of the sale from the media, not from their processor, and, as of today, have no firm answer on whether Gloria will honor their current contracts, prices, or pickup schedules.

With SanCor in creditor protection and co‑ops’ share of Argentina’s milk shrinking from roughly 34% to about 3%, most producers are now highly dependent on a single buyer when decisions like this drop.

If more than 60% of your milk goes to one processor and your contract is silent on ownership changes, you’re carrying the same processor‑risk those 600 Argentine families just discovered — and you should be auditing that agreement this week, before your own “press‑release moment” arrives.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

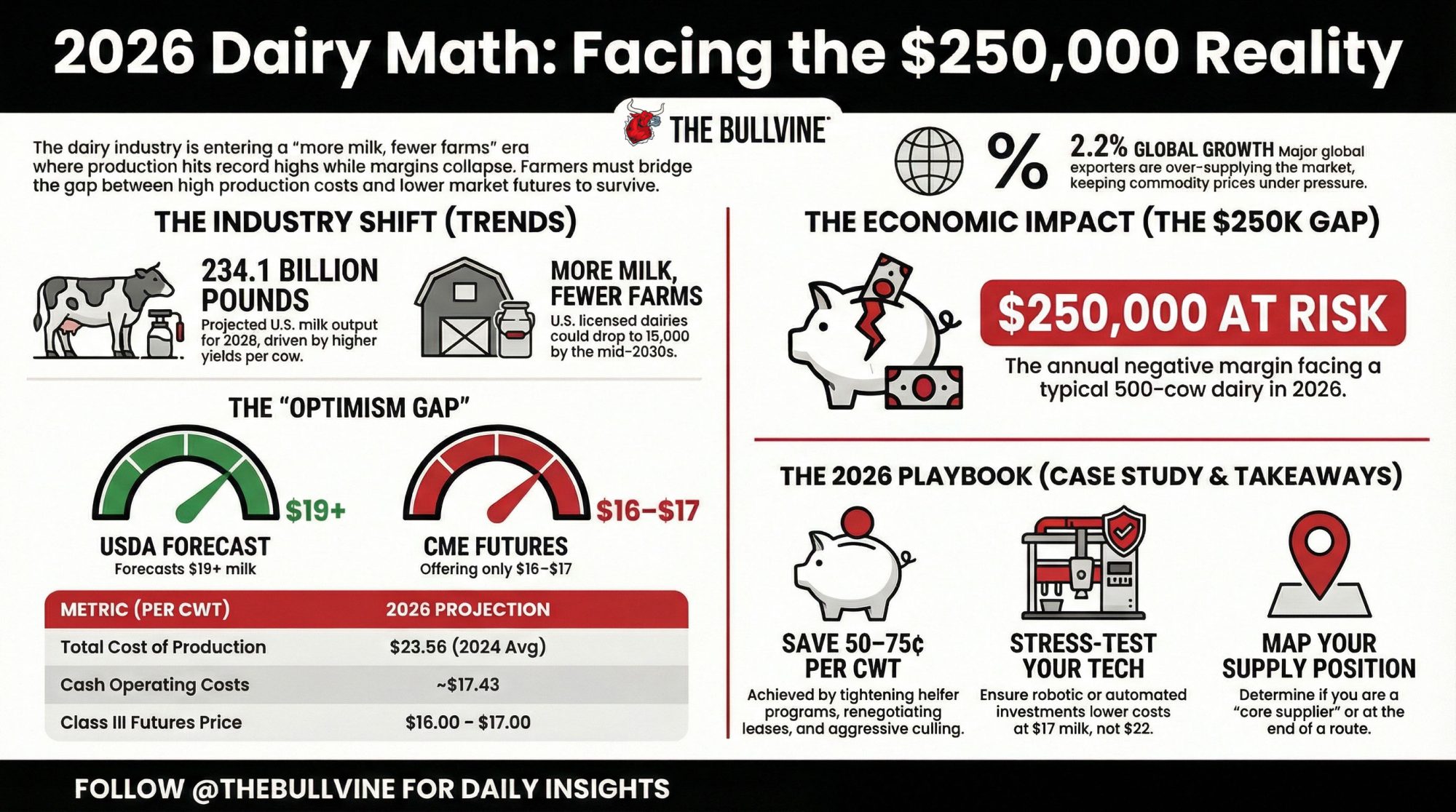

More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Exposes the $250,000 annual margin gap facing mid-sized dairies and reveals how to position your operation for 2026’s “more milk, fewer farms” reality. This strategic analysis identifies the specific leverage points needed to survive increasing processor consolidation.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

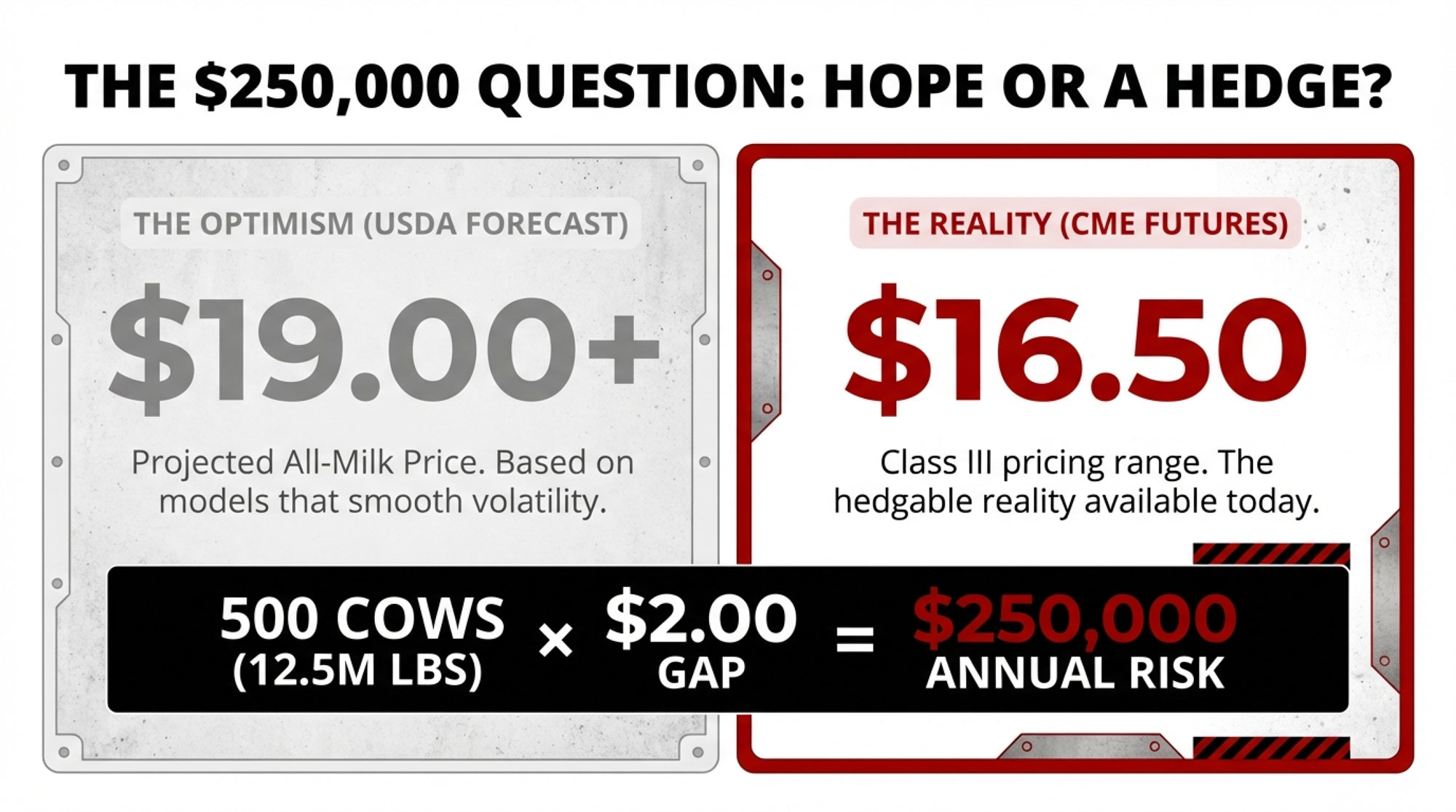

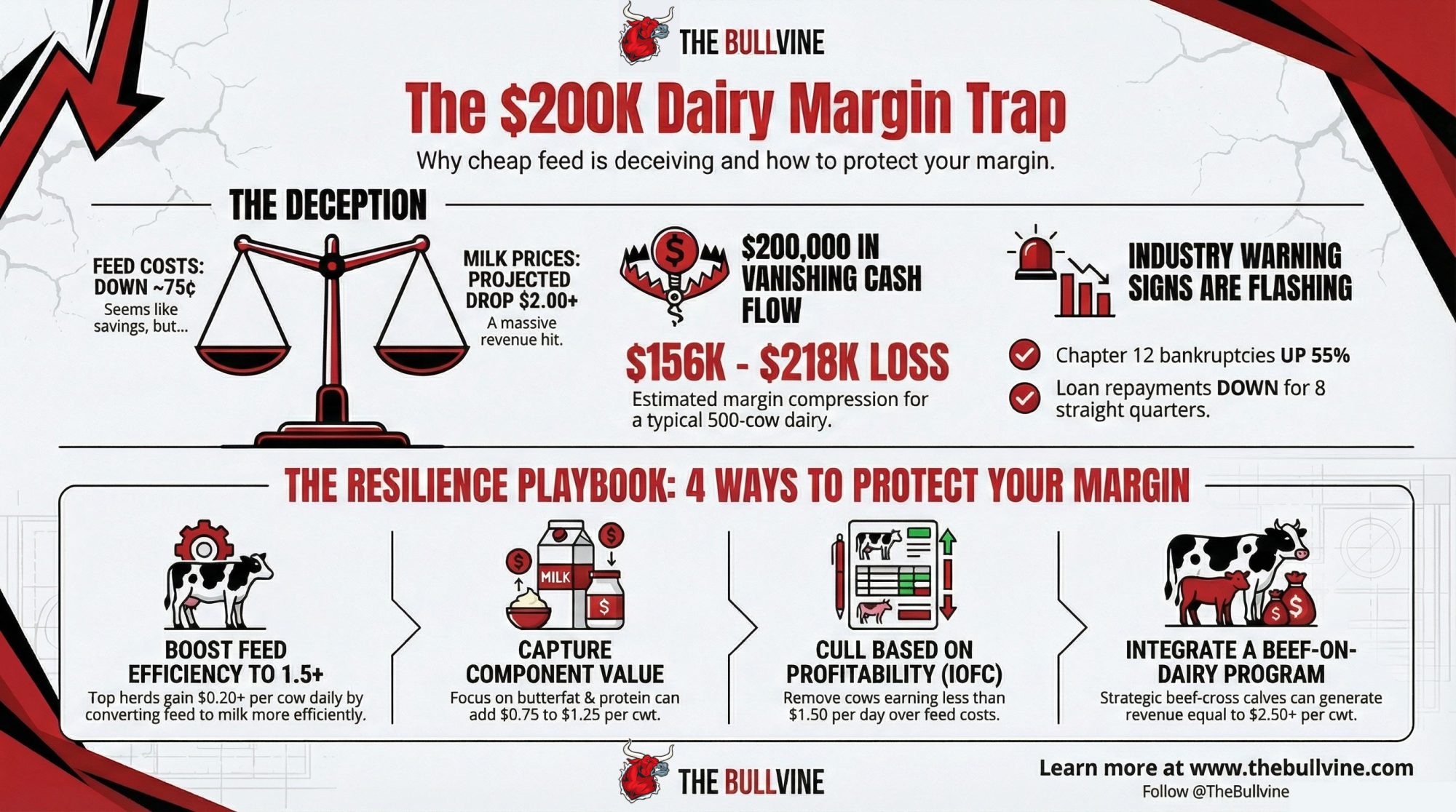

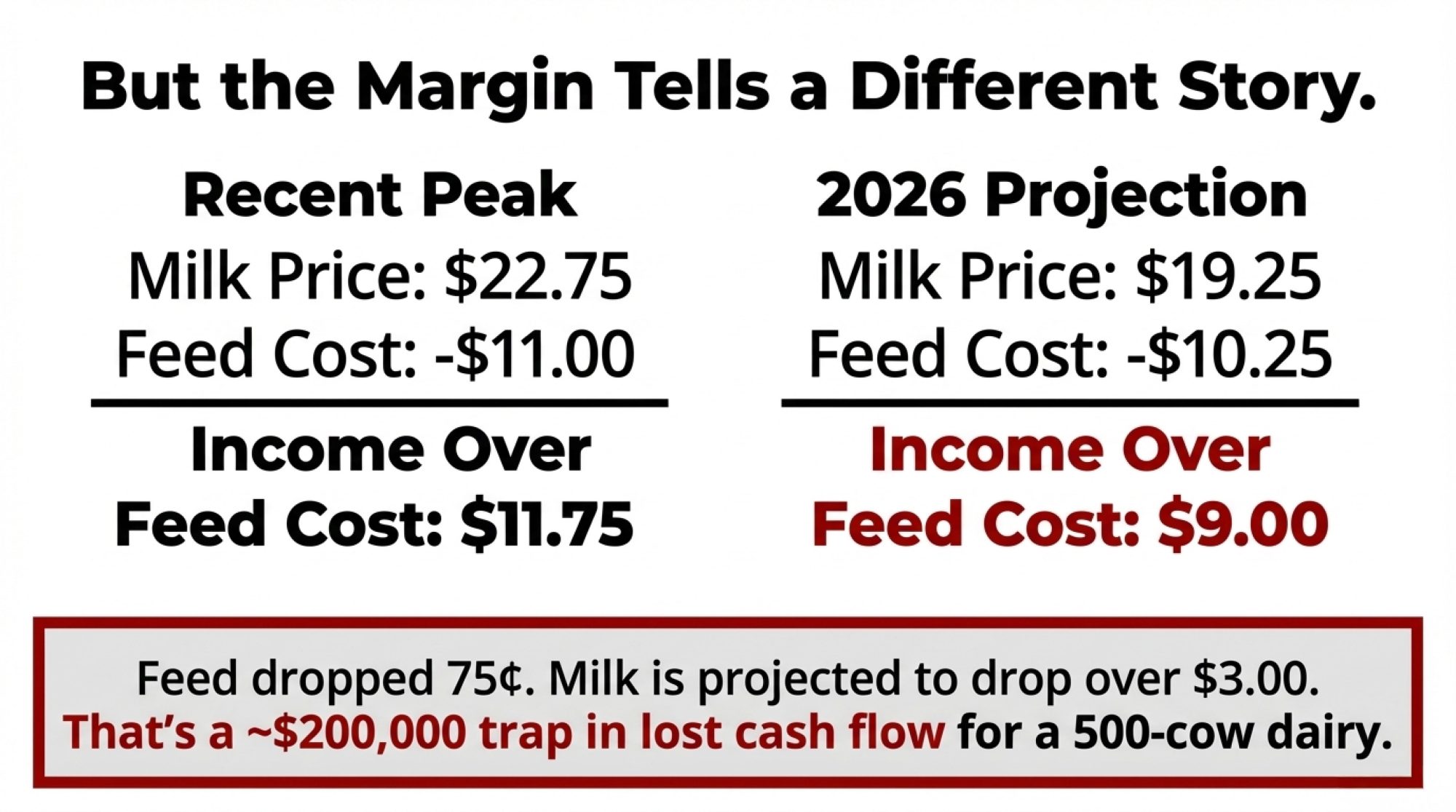

USDA says 2026 milk is $18.95. ERS says your costs are $19.14. That’s not a forecast — that’s a loss locked into the dairy math.

Executive Summary: USDA’s February WASDE now projects $18.95/cwt all‑milk for 2026, but ERS cost‑of‑production numbers still put average 2,000‑plus cow herds at $19.14/cwt and the smallest herds near $42.70/cwt, so a lot of dairies are starting the year structurally in the red. January’s actual Class III check at $14.59/cwt explains why your cash flow feels even tighter than the forecast suggests. At retail, a gallon of whole milk still sits around $4.05, with farmers getting only 25¢ of the dairy dollar and an opaque $2.40–$2.80 slice going to processing and retail that the Gillibrand‑Collins Fair Milk Pricing for Farmers Act tries to drag into the light. For many herds, beef‑on‑dairy calf and cull checks worth about $4.50/cwt are what plug the hole, even as they drain the replacement pipeline and push heifer prices over $3,000/head. The article uses a 550‑cow Wisconsin dairy to show how an honest cost‑of‑production run, fast culling decisions, and debt restructuring turned an 11‑week runway into something survivable. Then it hands you a four‑lane playbook — tighten components, lock in DMC/DRP, get in front of your lender, or consider exiting while asset values hold — with clear thresholds and stress‑tests so you can see, in dollars, which path actually fits your operation.

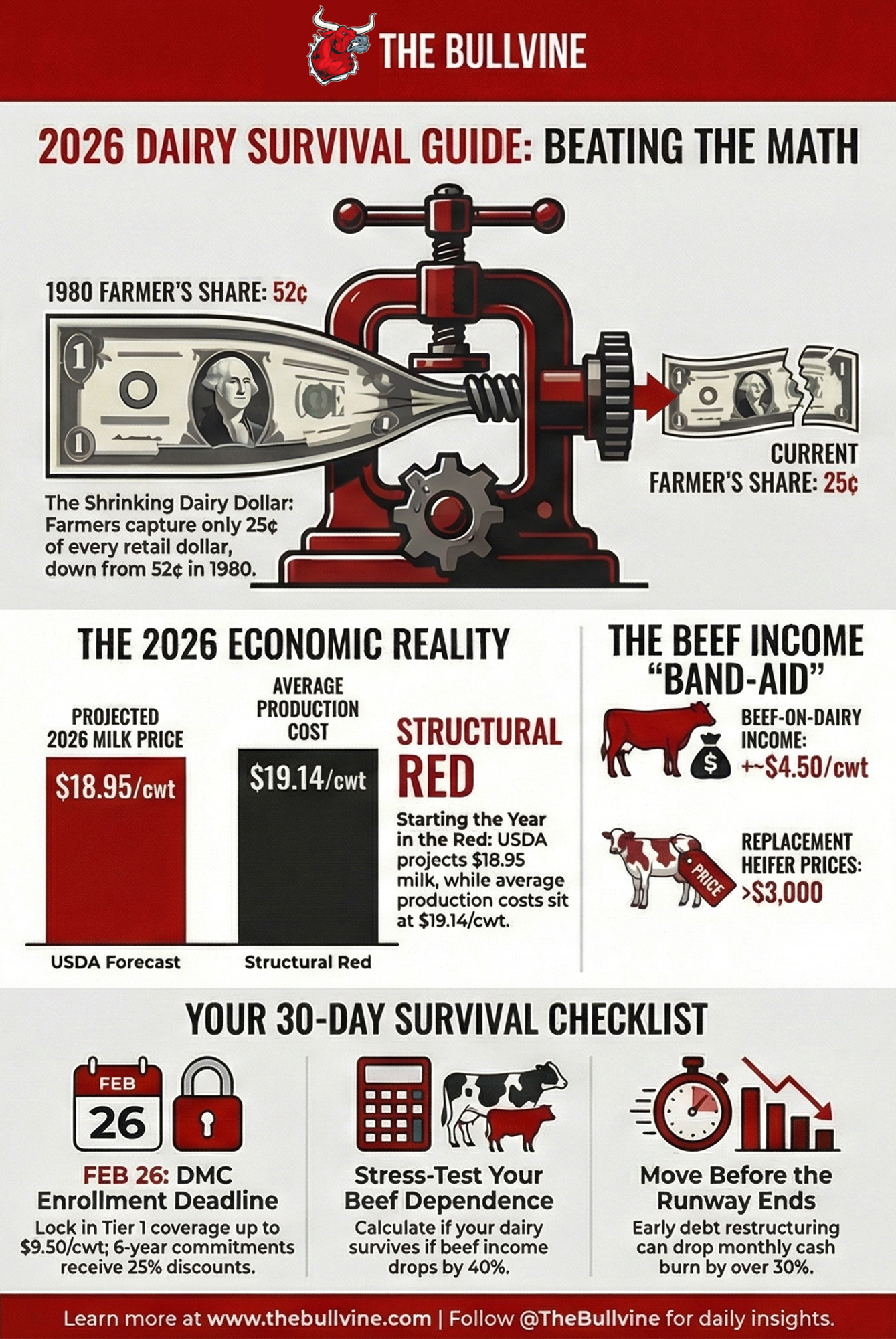

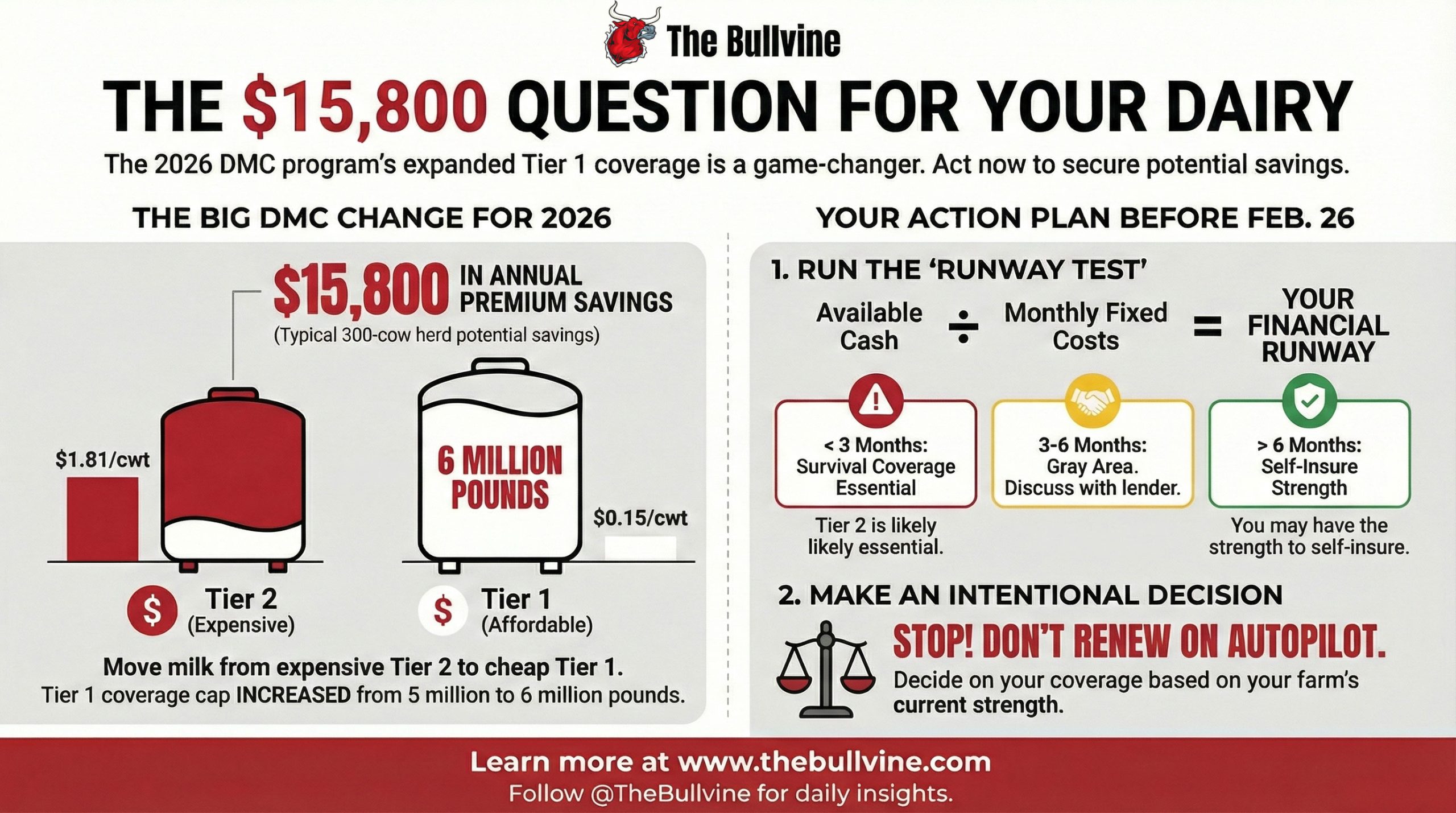

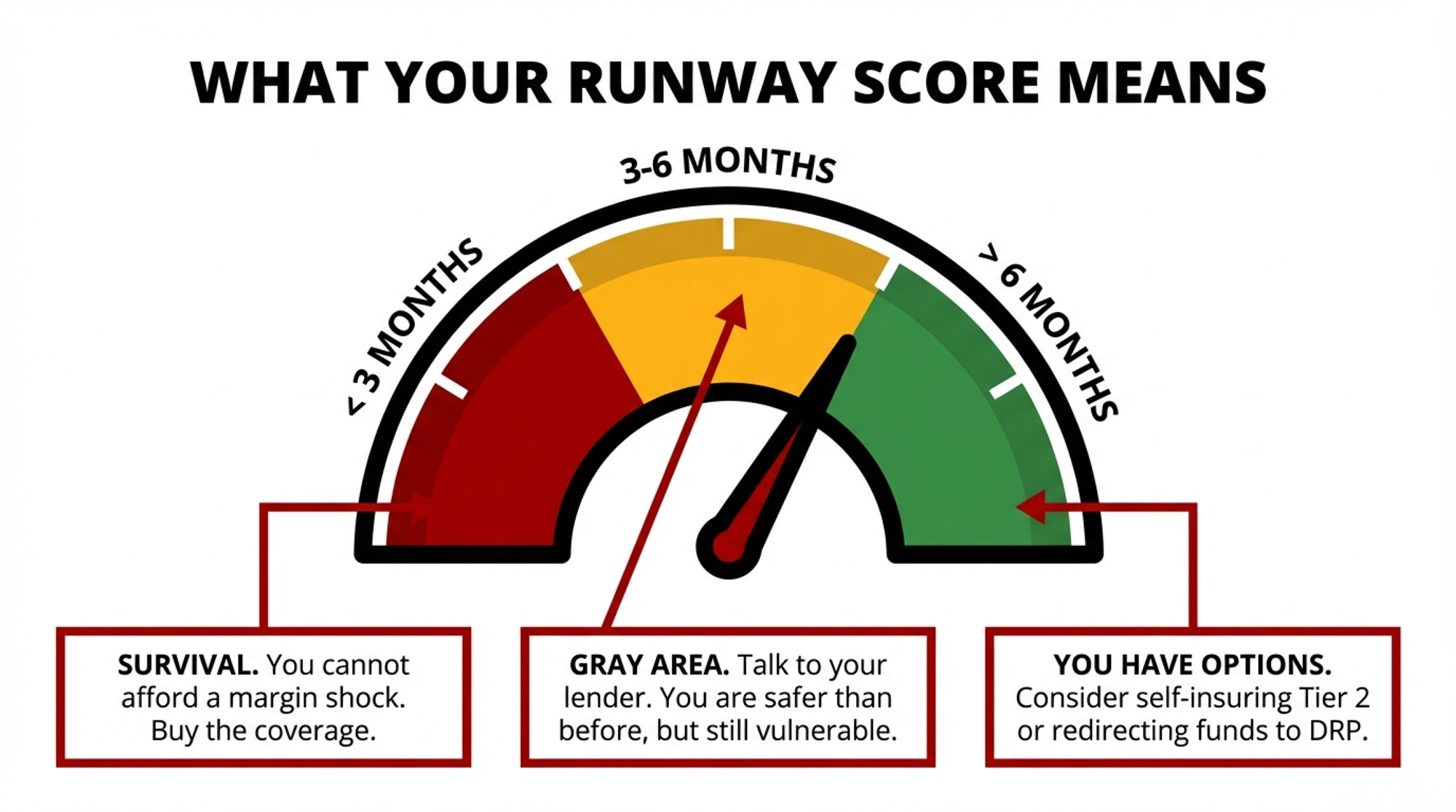

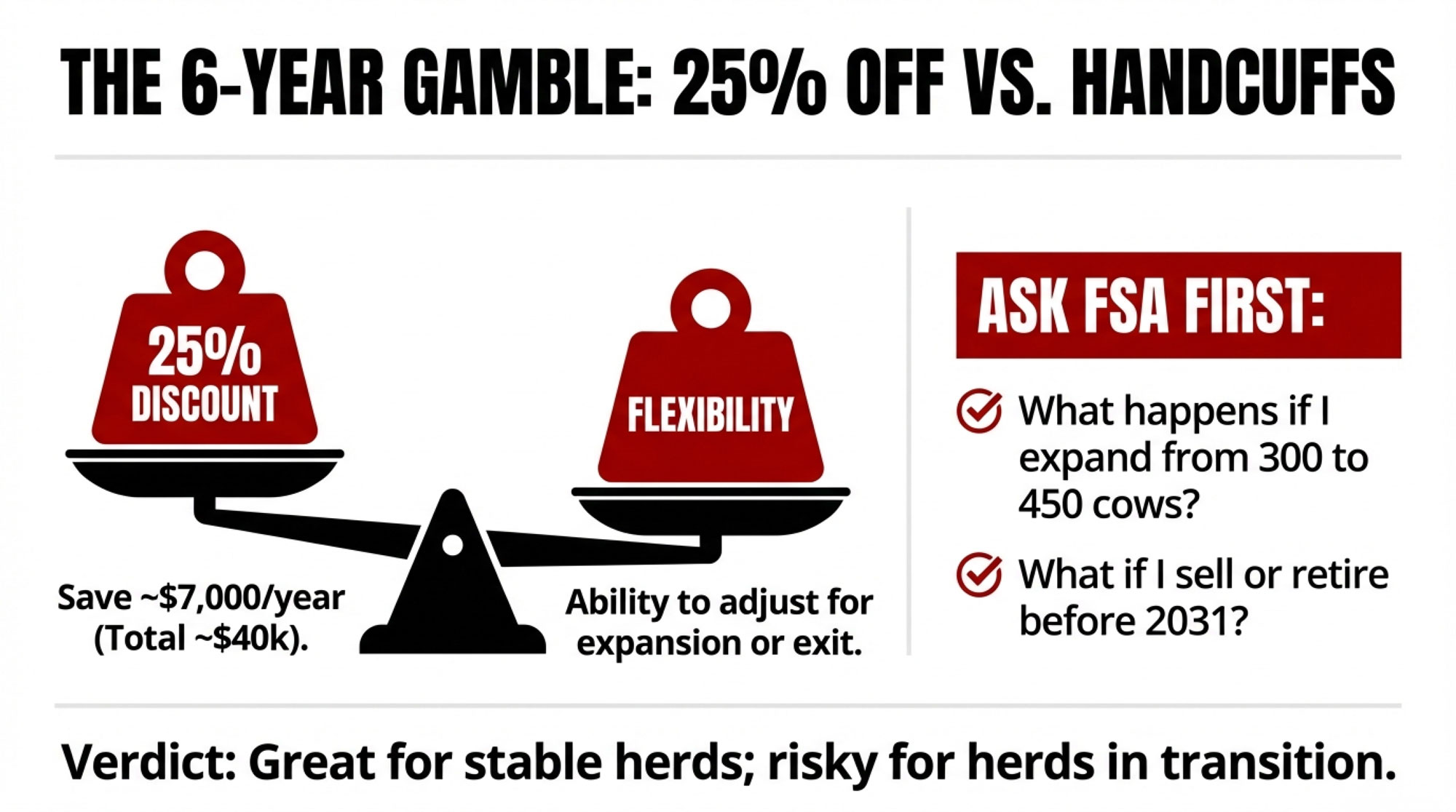

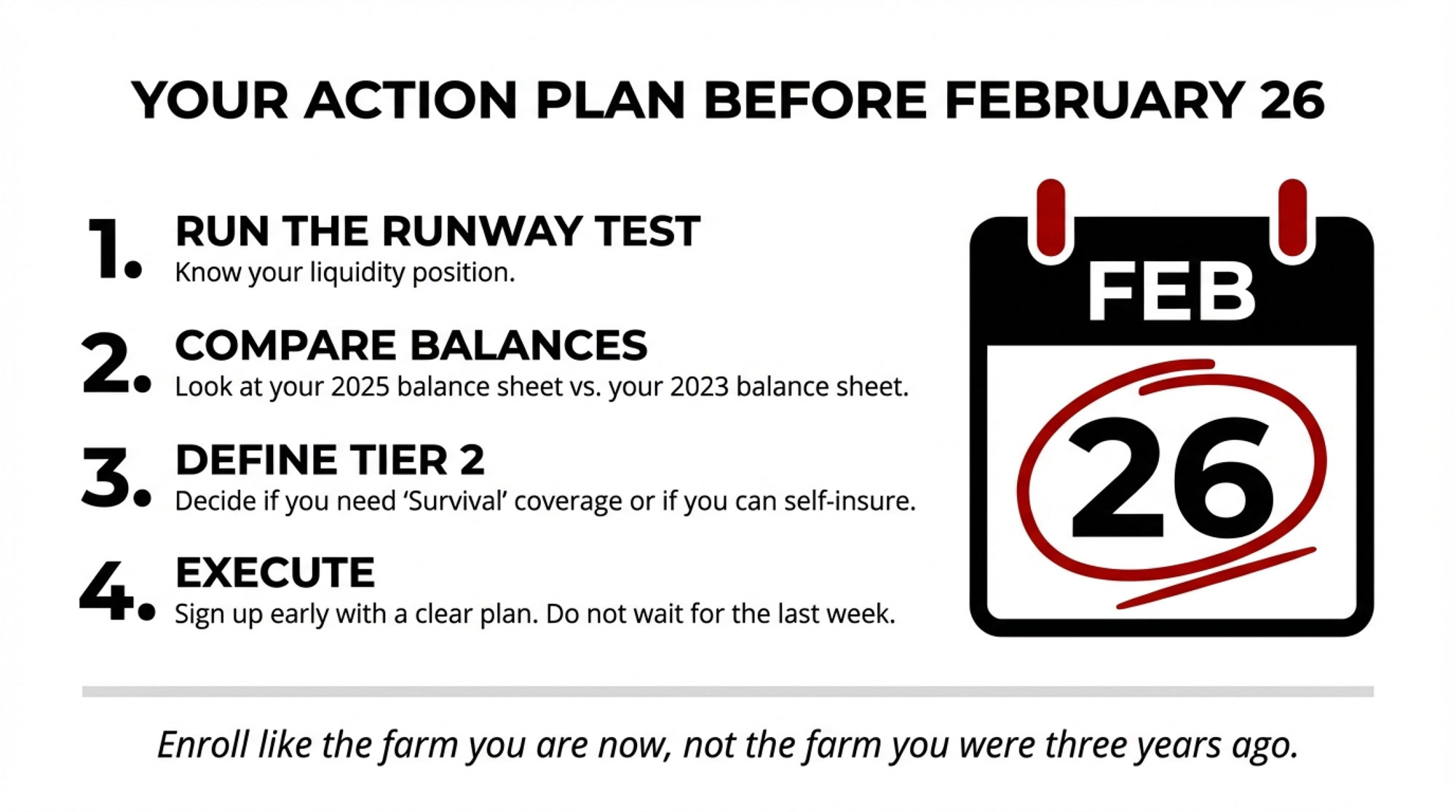

⚠️ DMC ENROLLMENT CLOSES FEBRUARY 26 — 15 DAYS FROM TODAY Tier 1 coverage is now available up to 6 million pounds at $9.50/cwt. A six‑year commitment (2026–2031) under the One Big Beautiful Bill Act (OBBBA) cuts your premiums by 25%. That cap covers roughly a 270‑cow herd at 22,000 lbs/cow. If you’re eligible and not enrolled yet, you’re on the clock. Source: USDA Farm Service Agency, Secretary Rollins’ Jan. 12 announcement, farms.com, and Penn State/Extension enrollment summaries.

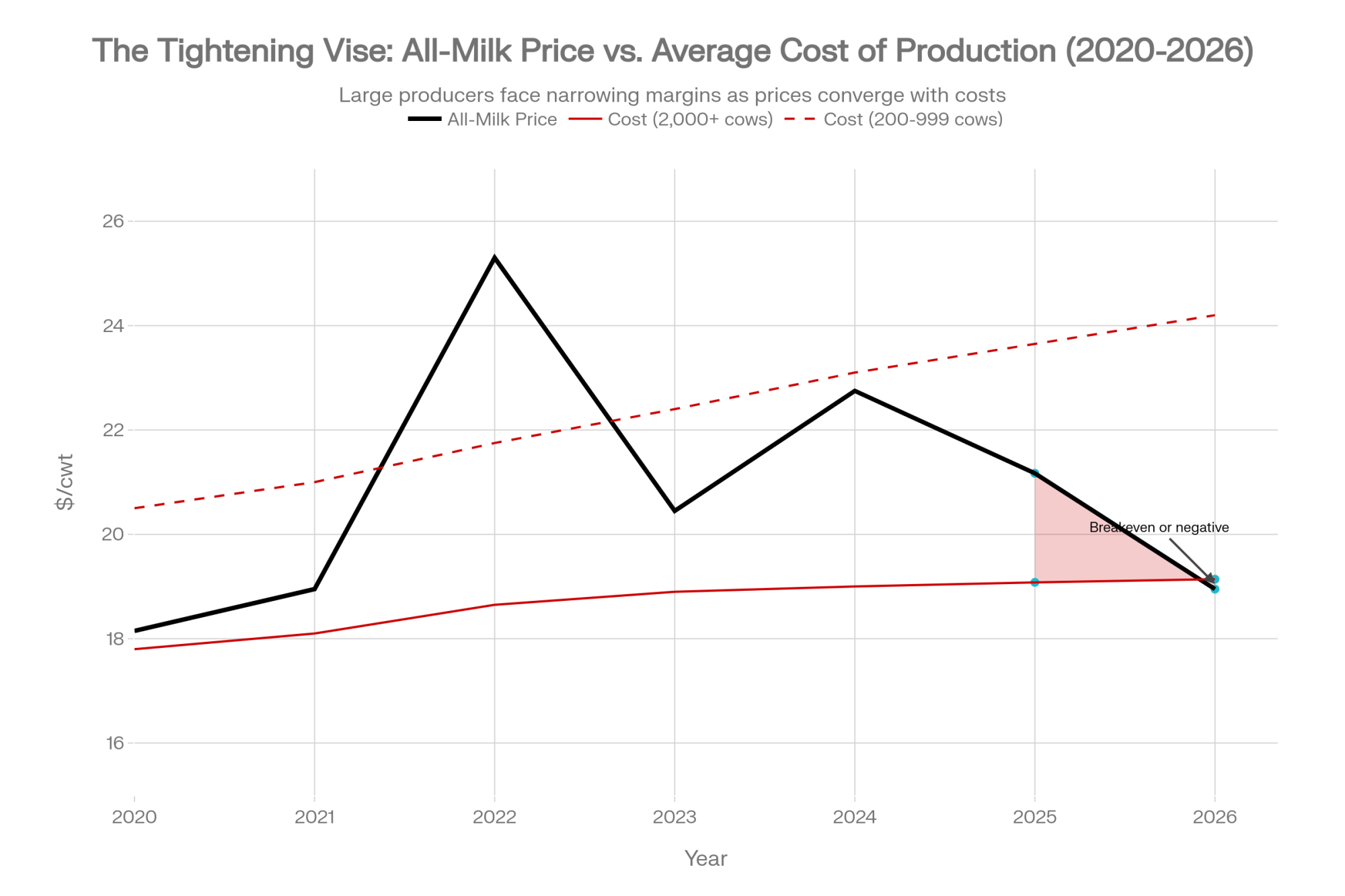

USDA’s February 10 WASDE briefing shows the 2026 all‑milk price at $18.95/cwt, down $2.22/cwt from the revised 2025 average of $21.17/cwt. That’s roughly $153,000 in lost gross milk revenue for a 300‑cow herd shipping 69,000 cwt a year. The same USDA‑ERS data behind that WASDE also say this: on a full‑cost basis, even the biggest, “efficient” herds average 19¢/cwt above the new all‑milk price, while sub‑50‑cow herds sit more than $23/cwt higher than that $18.95.

The $4.05 Gallon and the Broken Price Signal

Here’s the number that should make you stop and stare for a second.

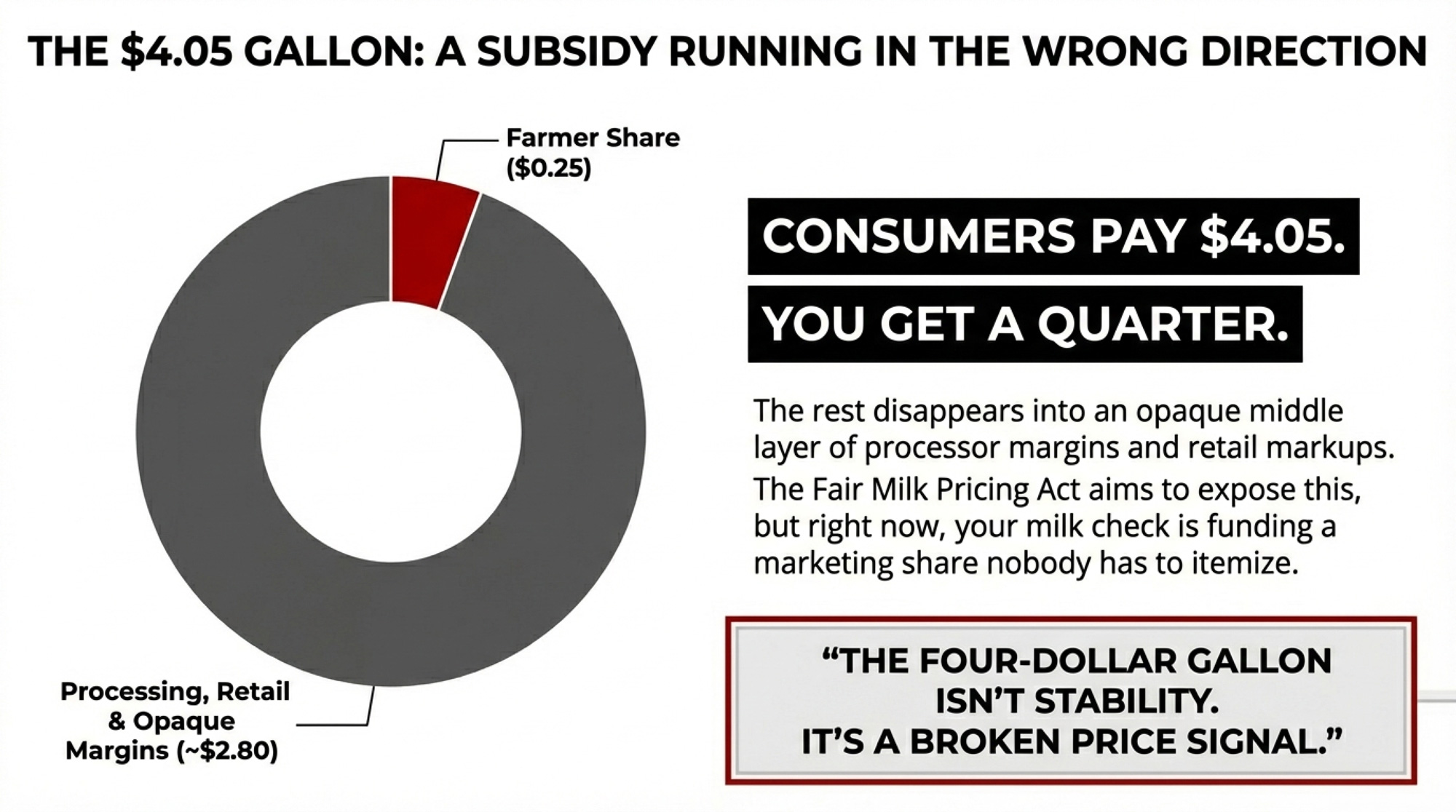

The national average price of a gallon of whole milk in December 2025 was $4.05, essentially unchanged from four years earlier. Over that same period, food‑at‑home prices climbed about 23%, according to BLS CPI data. Eggs jumped. Beef jumped. Milk stayed pinned. Consumers got a better deal on your product than on almost anything else in the grocery store.

USDA’s Economic Research Service tracks how that retail dollar gets split. In 2024, dairy farmers captured 25¢ of every retail dairy dollar, up a bit from 23¢ in 2023 but down from 28¢ in 2022. Back in 1980, the farm share sat near 52¢; by 1999, it was around 32¢. For fluid milk specifically, ERS pegs the 2024 farm share at 49%. With the 2026 all‑milk forecast now at $18.95, that share is drifting toward the low 40s.

Here’s how your slice of that $4.05 gallon changes at three price points:

Your share of the $4.05 gallon (fluid milk)

Price Scenario

Farm Value per Gallon

Your Share

Goes to Processing & Retail

2025 all-milk avg ($21.17/cwt)

$1.82

44.9%

$2.23

2026 all-milk forecast ($18.95/cwt)

$1.63

40.2%

$2.42

Jan 2026 Class III actual ($14.59/cwt)*

$1.25

31.0%

$2.80

*Class III is always lower than the all‑milk blend, which includes Class I & II. January’s all‑milk will be higher than $14.59, but the direction is the same. Farm values converted at 1 gallon ≈ 8.6 lbs; all‑milk and Class III from USDA WASDE/AMS, retail from BLS.

That bottom row is the punch in the gut. At January’s actual Class III, $2.80 of every $4.05 gallon goes to processing and retail. And here’s the part that should bother you: ERS only tells you the farm share versus “marketing share” — it doesn’t break that $2.80 into processor margins, retail markups, transportation, or packaging. It’s one big opaque slice.

2025 will be remembered as a year of “margin capture through arbitrage in the middle of the supply chain. Dairy markets worked—just not for dairy farmers. Senators Kirsten Gillibrand (D‑NY) and Susan Collins (R‑ME) responded by introducing the Fair Milk Pricing for Farmers Act (S.581) in February 2025, which would require audited dairy processor cost surveys every two years under the Agricultural Marketing Act of 1946. Until something like that passes, your milk check is funding a mid‑chain marketing share nobody has to itemize.

That’s not a neutral market adjustment. It’s a price discovery system that keeps the shelf price stable, preserves every margin between your bulk tank and the dairy case, and hands the entire “flex” to your end of the deal. The four‑dollar gallon isn’t stability. It’s a subsidy running in the wrong direction.

The 234.5‑Billion‑Pound Elephant in the Room

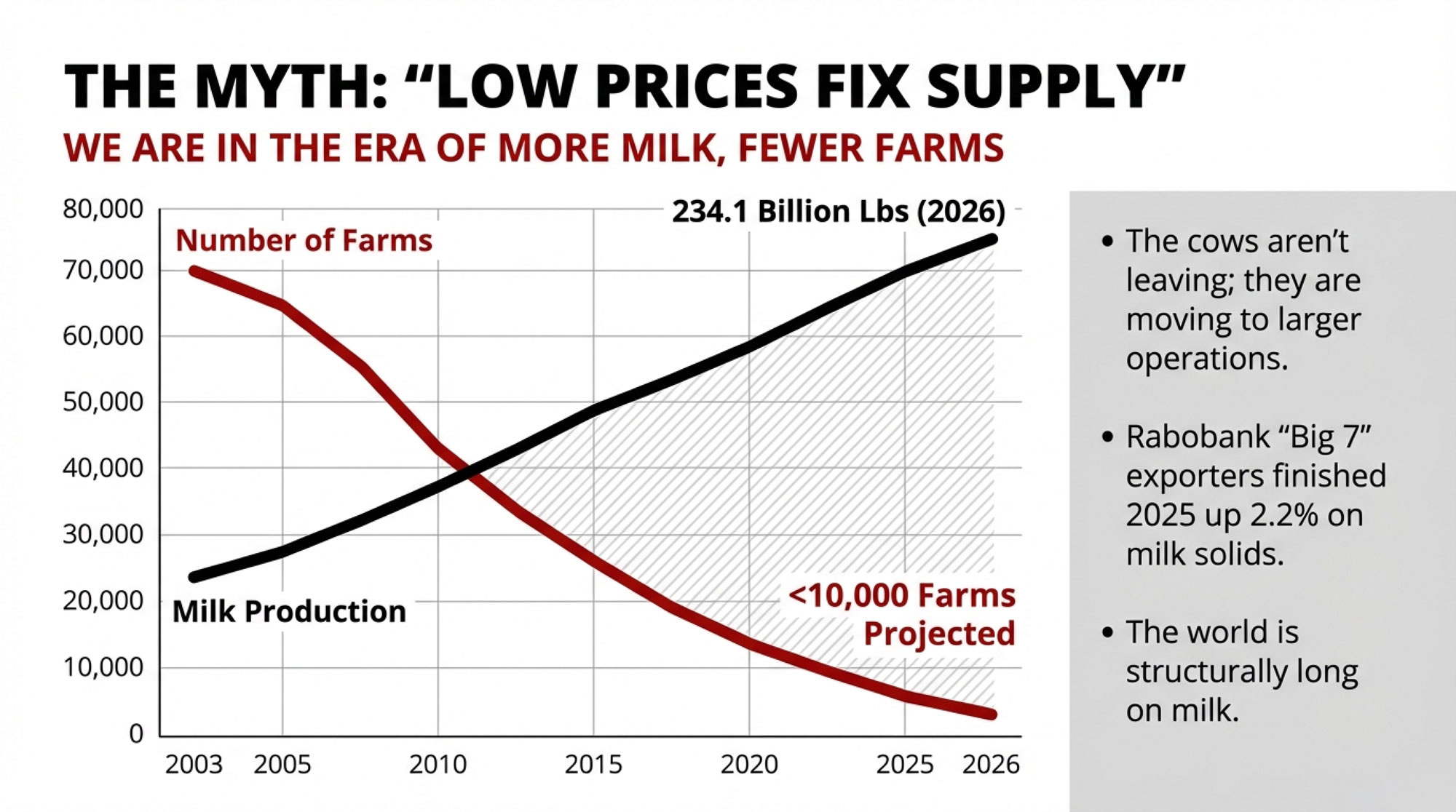

So if the money’s not showing up in your milk check, where is all this milk coming from?

USDA’s January Livestock, Dairy, and Poultry Outlook had 2026 milk output at 234.3 billion pounds on 9.555 million head, averaging 24,520 lbs/cow. The February WASDE nudged that up to 234.5 billion pounds, citing a slightly larger herd and continued productivity gains. November 2025 production was already running 4.5% above the prior year, with 211,000 more cows on feed and per‑cow output up 2.1%.

On the consumer side, that $4.05 national average hides a range from roughly $3.50/gallon in parts of the Midwest to more than $4.80 in some Northeast urban markets. The 2022 annual average peaked closer to $4.20 after mid‑year spikes above $4.30, then slid back and basically flat‑lined. And as we outlined in “USDA Says $18, Futures Say $16: The $150K Gap That’s Rewriting 2026 Dairy Budgets,” spot and futures markets have consistently priced a weaker Class III than USDA’s annual averages suggest.

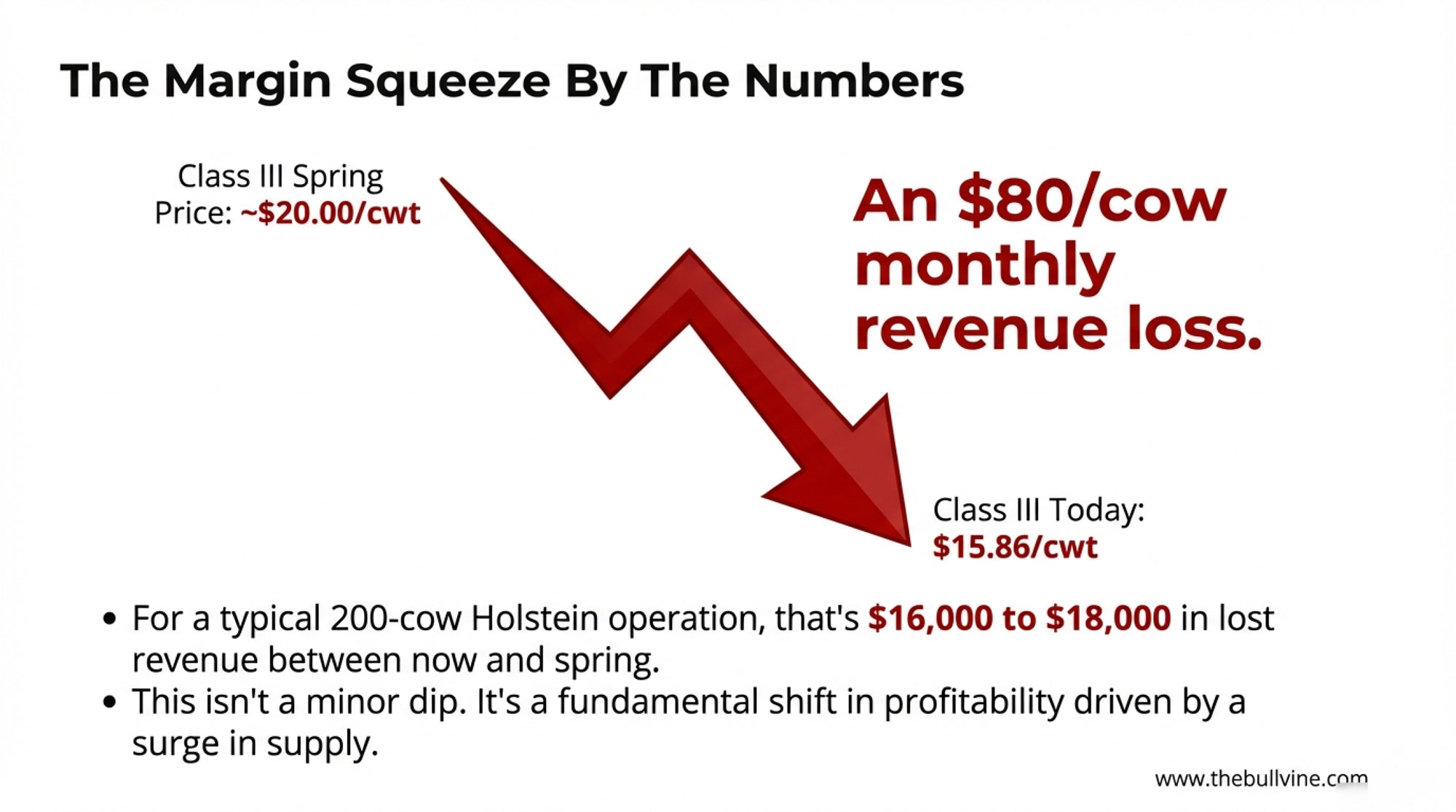

The February WASDE bumped all‑milk to $18.95 and Class III to $16.65/cwt, up 30¢ from January’s $16.35 forecast. But January’s actual Class III was still $14.59, and December’s was $15.86. That means the back half of 2026 has to do a lot of heavy lifting to deliver the annual average USDA now has in its spreadsheet.

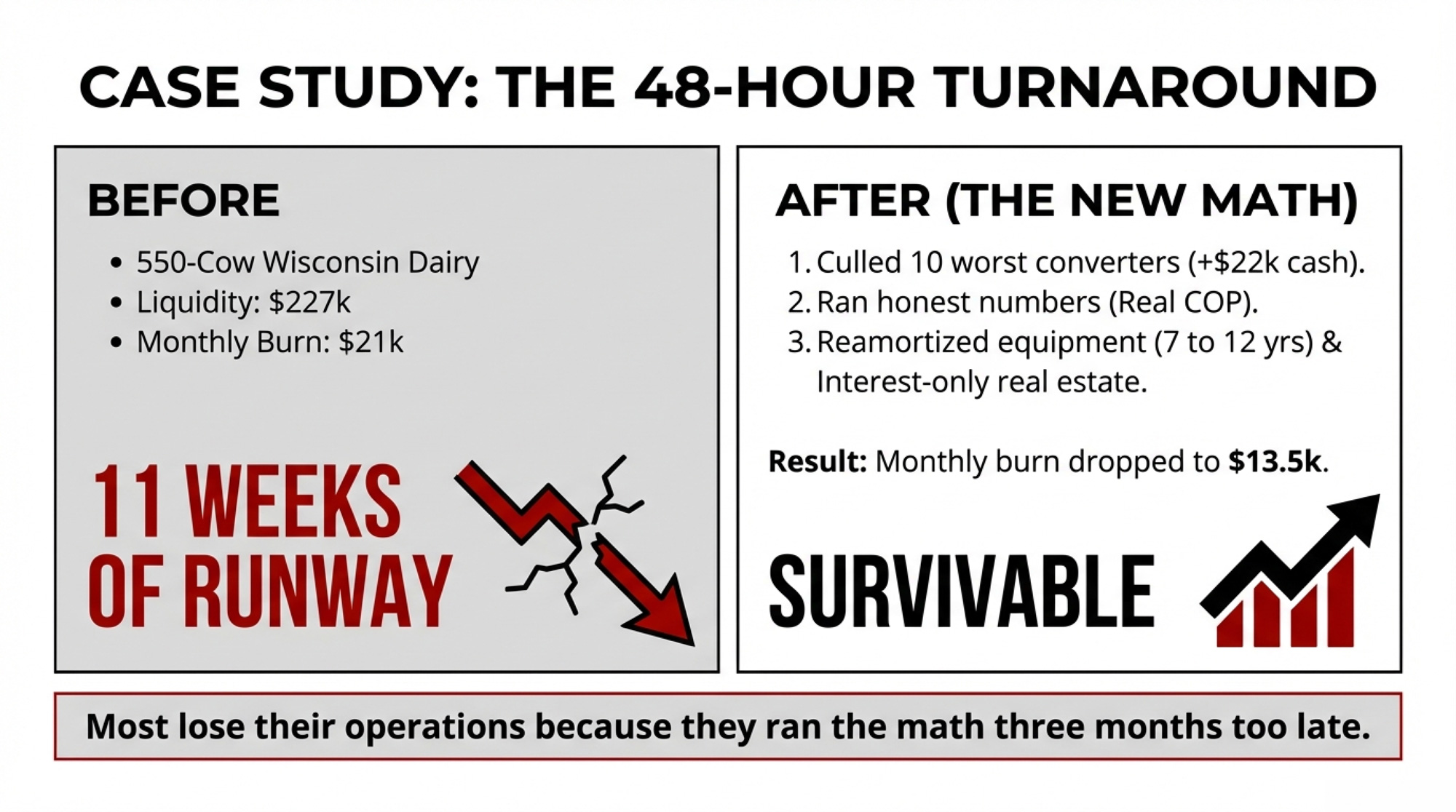

How This Lands on a Real Operation

Let’s bring this down to barn level.

A 550‑cow Wisconsin dairy recently sat down with a farm financial counselor through an Extension‑affiliated program and pulled a full cost‑of‑production analysis. The producer thought his all‑in cost was about $17.25/cwt. When the spreadsheet included market‑rate family labor, real depreciation, current interest on all repriced debt, and health insurance, the true number came back at $18.75/cwt — right in line with UW Extension’s $18–$19/cwt benchmarks for mid‑size herds in the region. That $1.50 gap represented roughly $200,000 in annual losses he hadn’t really accounted for.

The cash‑flow picture was worse. Total liquidity: $227,000. Monthly burn at current prices: about $21,000. That’s eleven weeks of runway, not the five or six months he’d been carrying in his head.

Here’s what changed everything. Within 48 hours, he:

Culled his 10 worst feed‑to‑milk converters, bringing in roughly $22,000 in cash and cutting daily feed cost by about $85.

Walked into his lender’s office with a 12‑month projection at $18/cwt and a real cost‑of‑production sheet.

Negotiated reamortization on equipment debt (from seven years to twelve) and four months of interest‑only on real estate.

The lender said yes. Monthly burn dropped from $21,000 to roughly $13,500. Same cows. Same parlour. New math.

That 48‑hour response is the difference between survival and bankruptcy in this kind of year. Not new genetics. Not a magic ration. Not a unicorn contract. Just running the real numbers, believing what they tell you, and moving beforethe runway disappears.

Most producers who lose their operations in a down cycle don’t lose them because the math was impossible. They lose them because they ran the math three months too late. The difference between “tight but okay” and “weeks from the wall” is often just one honest accounting exercise.

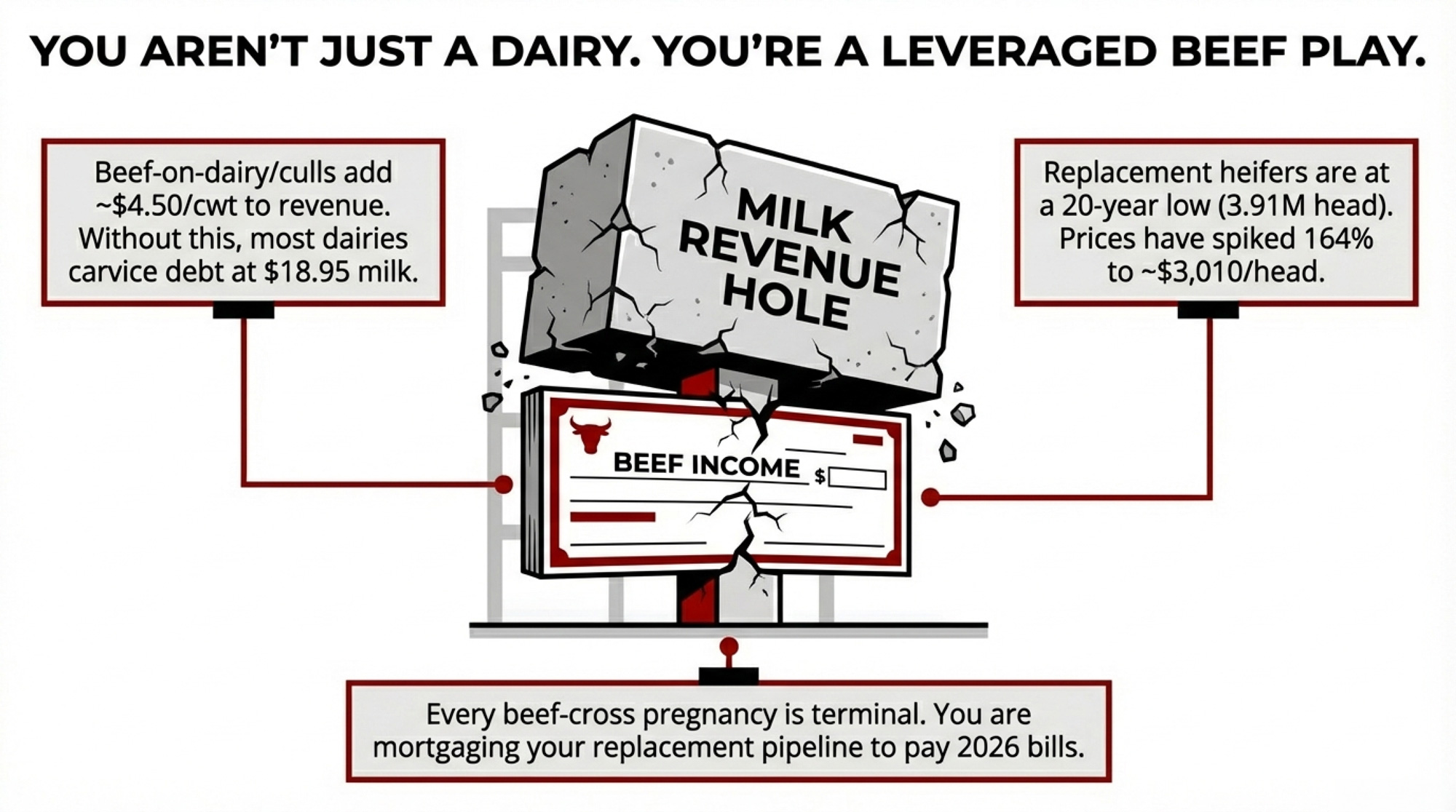

The Beef Check Holding It All Together

On a growing number of dairies, the milk margin alone isn’t keeping the lights on. Beef is.

High Ground Dairy’s October 2025 analysis — based on a representative 1,000‑cow model — estimates beef‑related income north of $4.50/cwt of milk shipped, with seven of the next twelve months projected above $5.00/cwt. Those forward numbers are modeled, not guaranteed, but they reflect what you’ve seen in your own calf checks and cull slips.

On that 300‑cow herd shipping 69,000 cwt, $4.50/cwt in beef income adds up to about $310,000 a year — coming from the cattle market, not the milk market. Strip it out and ask honestly whether your milk margin alone services your current debt with all‑milk at $18.95 and Class III at $16.65.

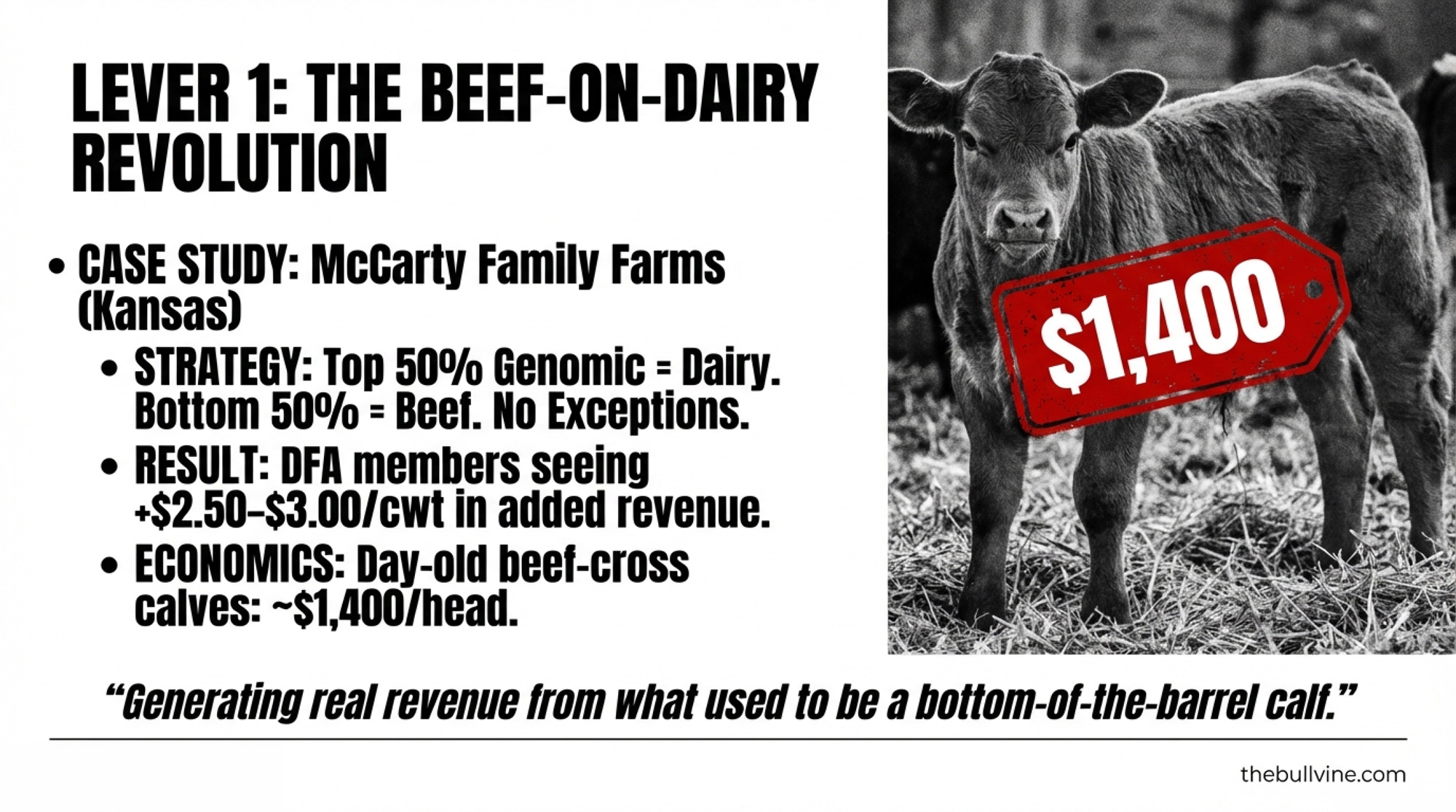

That beef check didn’t come free. CoBank’s August 2025 Knowledge Exchange report, authored by Corey Geiger and drawing on NAAB data, notes that beef semen sales into dairy nearly tripled from 2.5 million units in 2017 to 7.9 million in 2024. Conventional dairy semen sales fell hard over the same period.

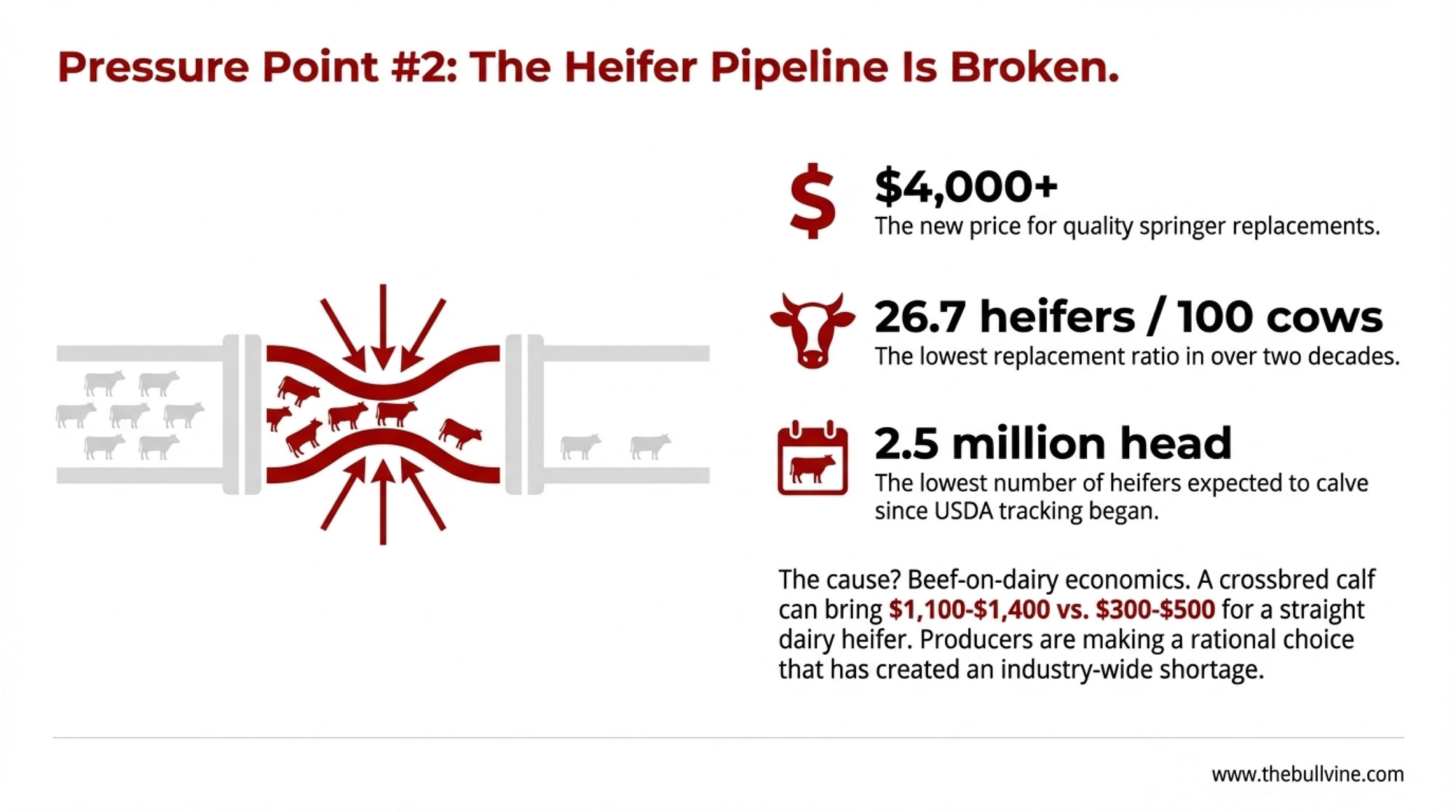

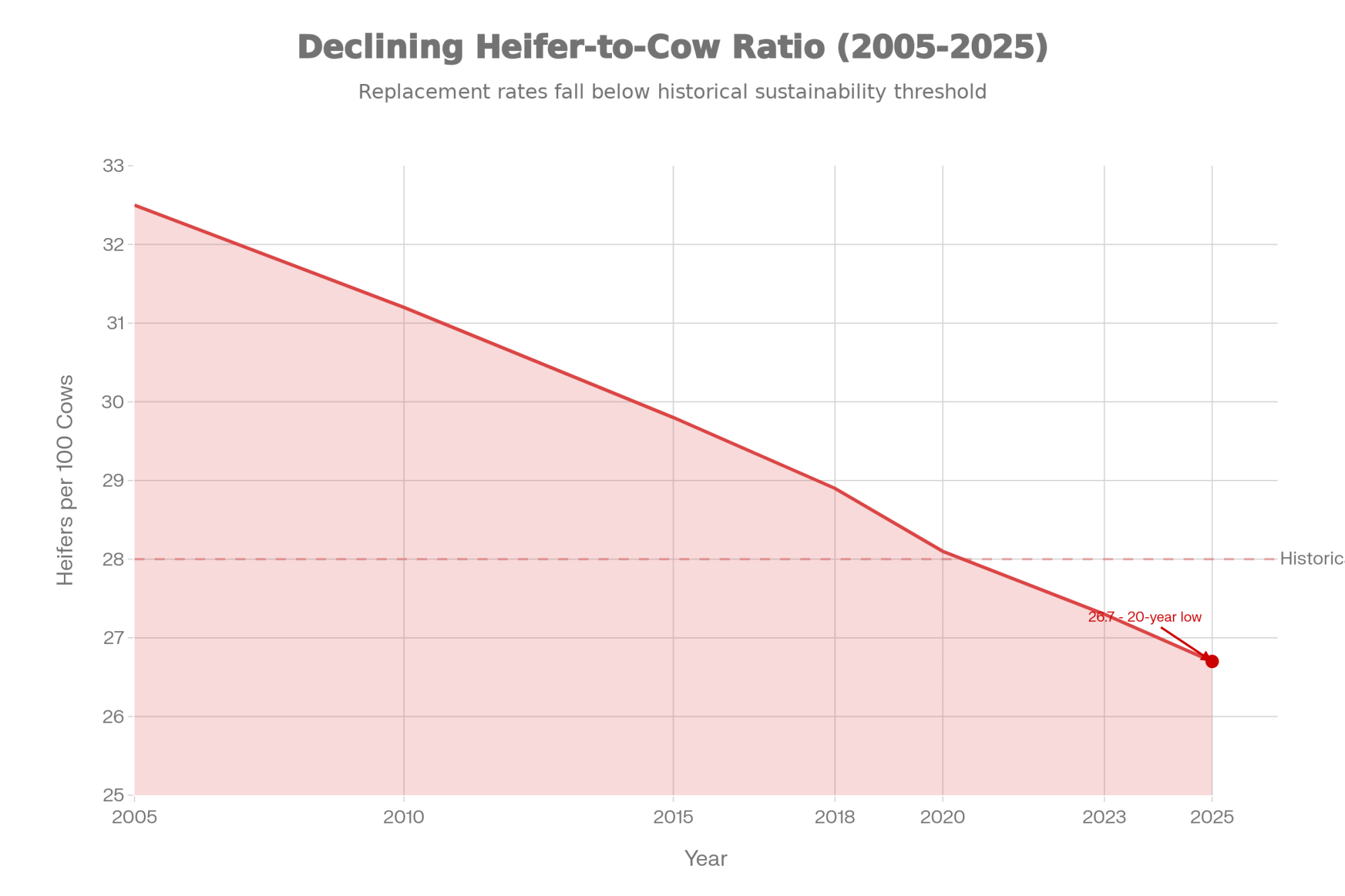

Every beef‑cross pregnancy is terminal. No heifer behind it.

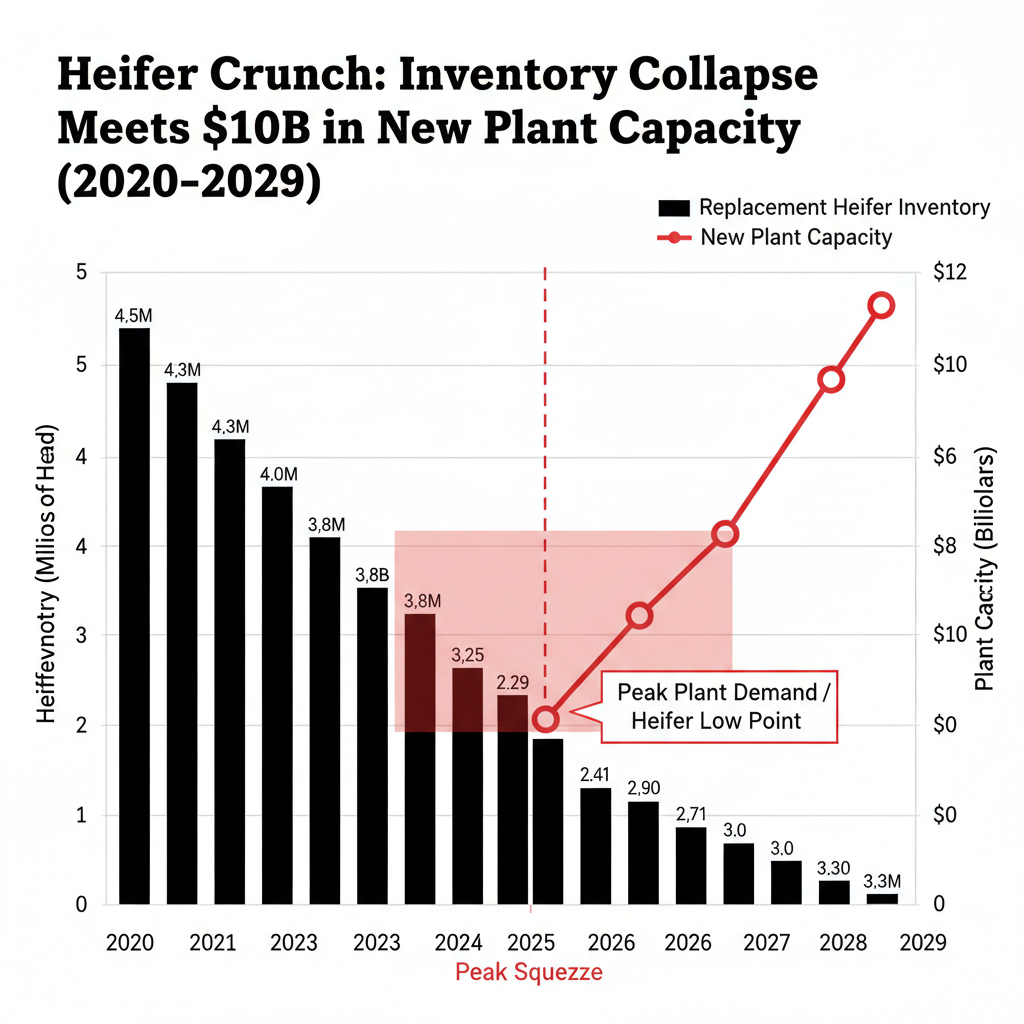

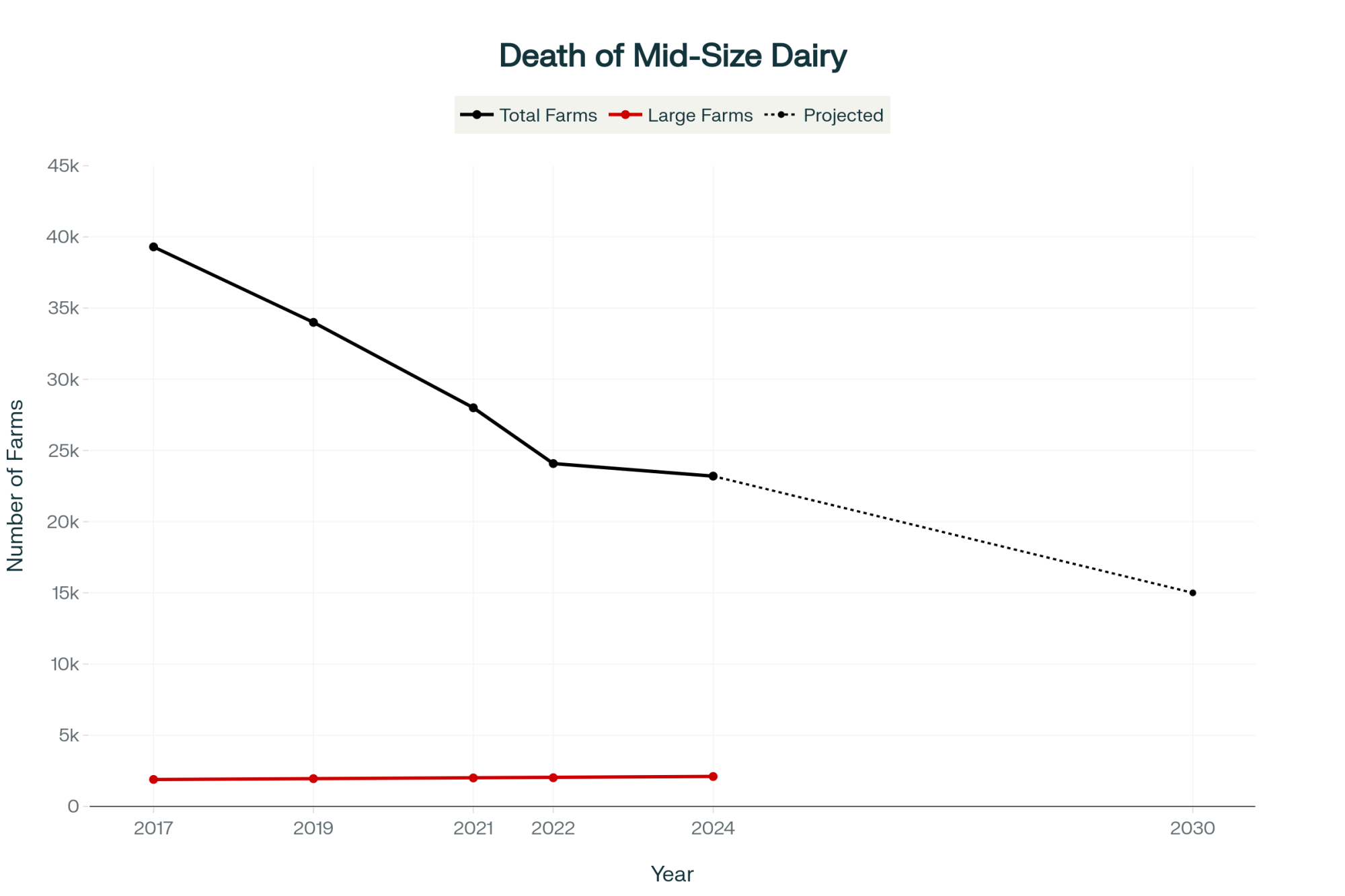

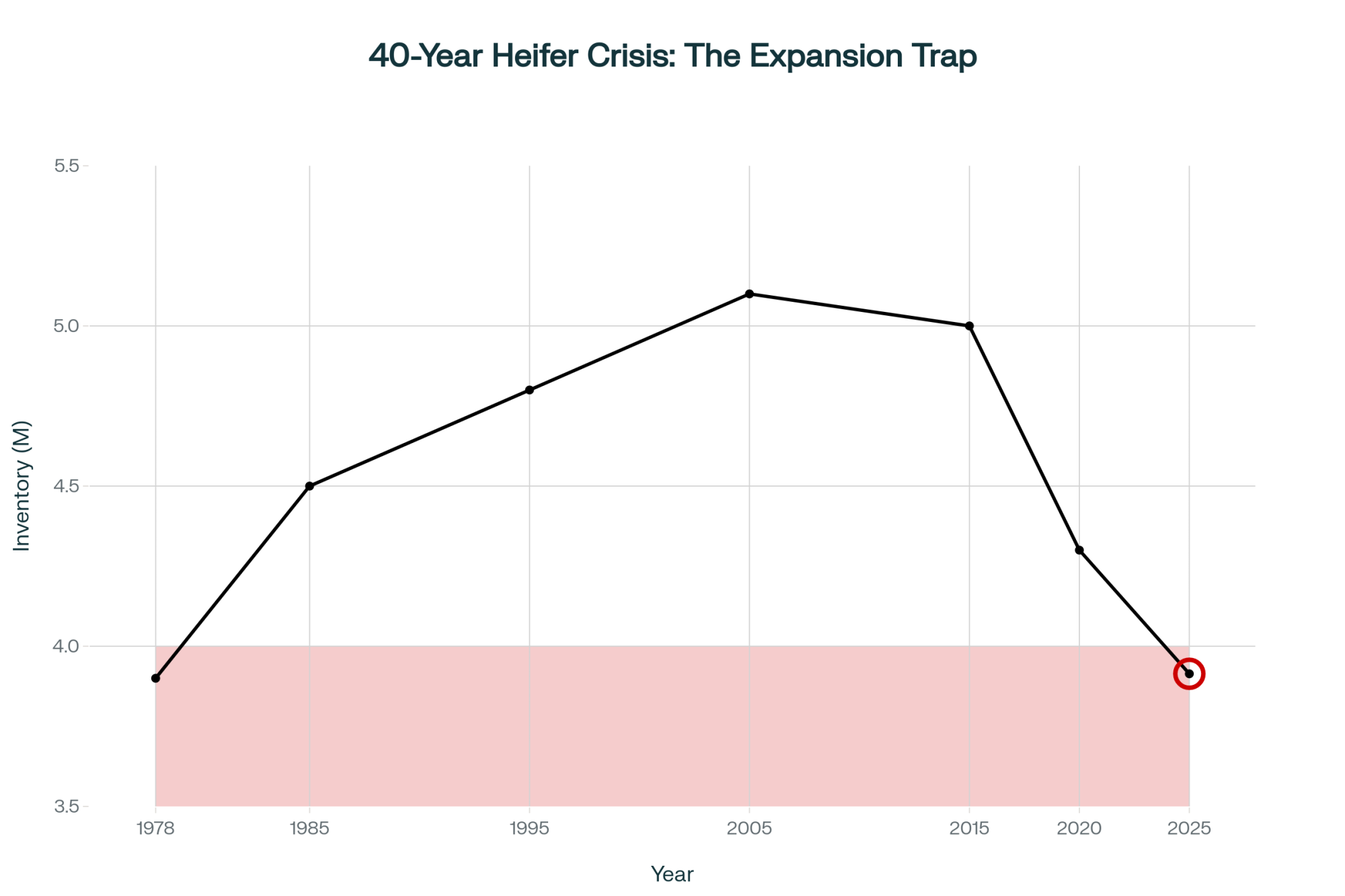

USDA’s January 2025 Cattle report shows dairy replacement heifers at a 20‑year low of 3.91 million head, down 18% from 2018. Geiger’s analysis highlights how that shortage shows up in prices: average dairy heifer values of $3,010/head in July 2025, up 164% from $1,140 in April 2019, with top sales in California and Minnesota clearing above $4,000/head. CoBank projects the heifer inventory will shrink by another 800,000 head over the next two years before stabilizing.

So yes, the beef check is saving a lot of balance sheets in 2026. It’s also mortgaging your replacement pipeline for the next three to four years.

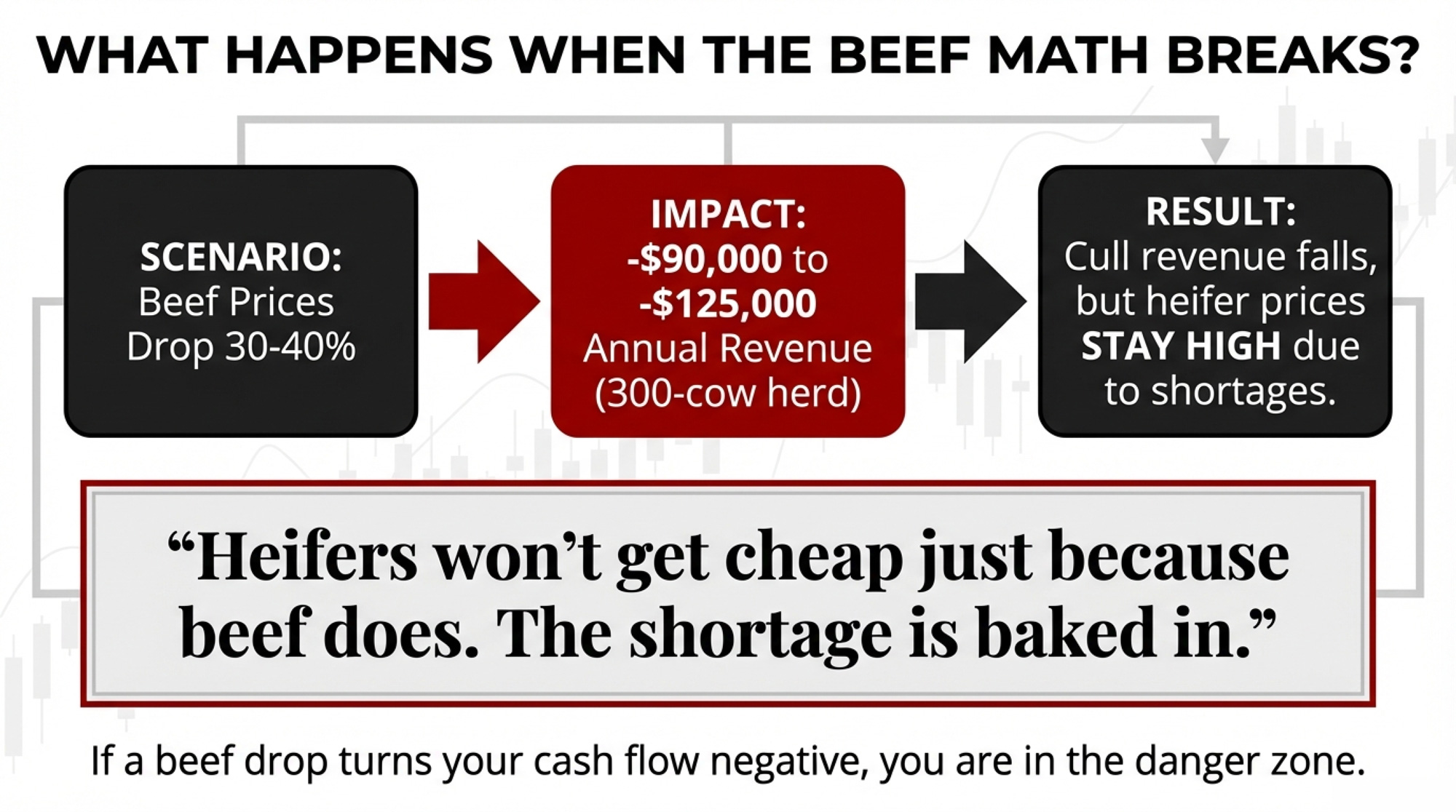

When Beef Softens—Stress‑Testing the Safety Net

Cattle markets move in cycles. CattleFax’s outlook at CattleCon 2026 in Nashville earlier this month put the average 2026 fed steer price at $224/cwt, roughly steady with 2025, and cull cows around $155/cwt. COO Mike Murphy called current levels “near cyclical highs” and described a slow, measured expansion phase, as high input costs and producer demographics cap herd rebuilding.

That suggests beef could stay supportive through 2026. But that’s not an excuse to skip the stress test.

A 30–40% drop in beef prices — well within range for a down cycle — would shave roughly $90,000–$125,000 off that $310,000 in annual beef revenue on a 300‑cow herd. You’d feel it on both sides: beef‑on‑dairy calf checks shrink, and cull revenue falls, while replacement heifers remain tight and expensive. Heifers won’t suddenly get cheap just because beef does; the structural shortage is baked in.

CoBank’s August 2025 work also points out that dairy producers have effectively “hoarded” about 611,600 cows from slaughter since Labor Day 2023, compared to the trend. If beef softens enough that everyone starts shipping at once, those cows hit the rail together — and the cull market falls harder. That’s how a softening beef market can turn from a warning sign into a full‑on margin squeeze.

The Canada Contrast

North of the border, the Canadian Dairy Commission boosted the farm‑gate milk price 2.3255% effective February 1, 2026. The CDC’s formula is straightforward: half the change in indexed cost of production (up 2.7%) plus half the change in CPI (up 1.9%).

Two pieces of that matter if you’re milking cows in the U.S.:

When beef revenue is strong, it flows into Canada’s COP index as an offset, dampening their milk price increases. When beef weakens, the formula moves in the other direction. The system self‑corrects.

The CDC cost formula includes feed, labor, and energy. DMC only looks at feed. Every non‑feed cost that’s blown out since 2022 — labor, interest, insurance, repairs — is invisible in your U.S. safety net.

Of course, Canada’s stability comes at a high price. Ontario quota traded above $24,000 per kilogram of butterfat per day in 2025. That locks out new entrants and caps growth. But if the question is whether you can make a five‑year investment decision without guessing where Class III will land next January, the Canadian model offers something the U.S. structure doesn’t: a rulebook.

Four Paths—and What Each One Costs

Strategy

Upfront Cost / Action

Monthly Cash Impact

Long-Term Trade-off

Best Fit If…

Component Optimization

Ration/genetics adjustment

+$0.58/cwt (down from +$0.98 in 2025)

Feed cost now, fat revenue later—only if BF price recovers

Your plant pays component premiums & you can wait for BF rebound

DMC/DRP Enrollment (by Feb 26)

Premium ~$1,500–$3,000/yr for $9.50 Tier 1 (25% discount if 6-yr commit)

+$0.30–$0.60/cwt margin support (feed only)

Doesn’t cover labor, debt, energy squeeze

You’re ≤270 cows, feed is your main cost pressure, & you’re not enrolled

Lender Restructuring

Time + full COP analysis

−$2,390/mo (example: $500k note, 7→12 yr)

+$115,600 extra interest over loan life

Cash flow is tight (<6 mo runway) but operation is viable at $18–$19 milk

Strategic Exit

Appraisal, auction, legal fees

Lump-sum: cull/heifer/land at current highs

You’re out of dairy

3-yr projection at $18.95 milk leaves you with less equity than exiting now

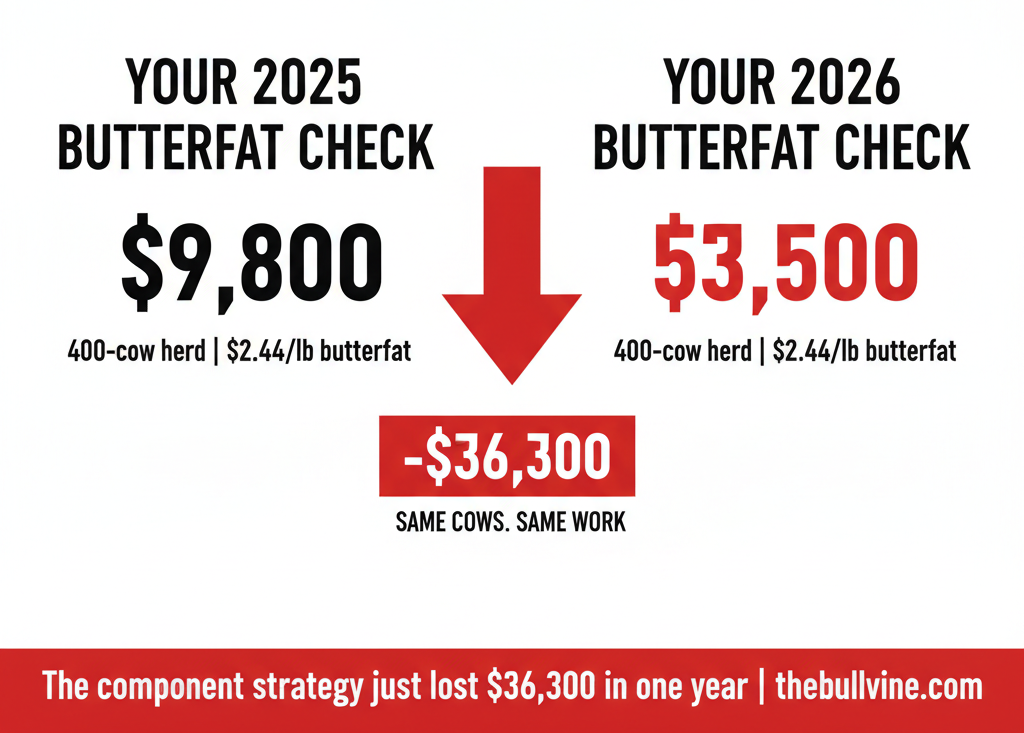

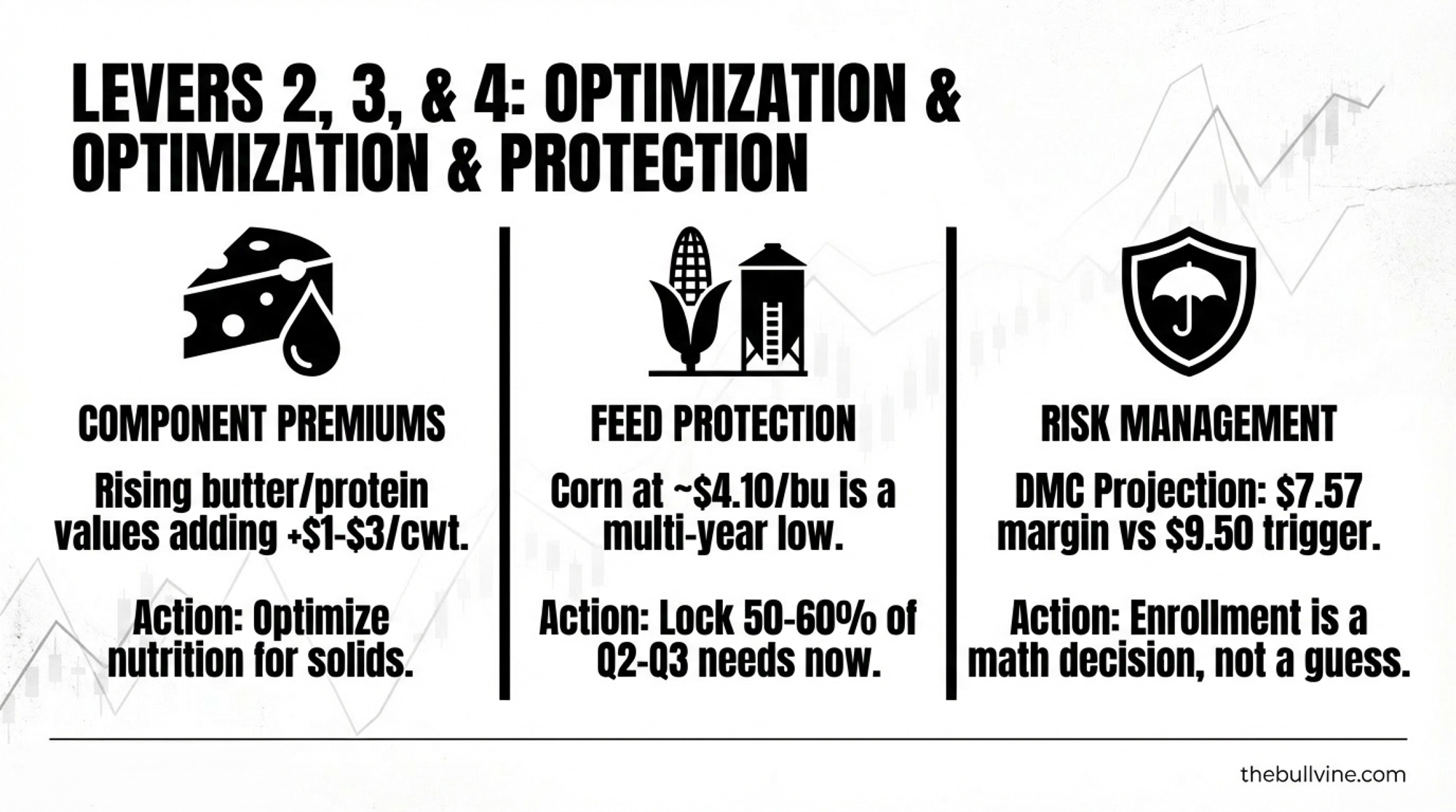

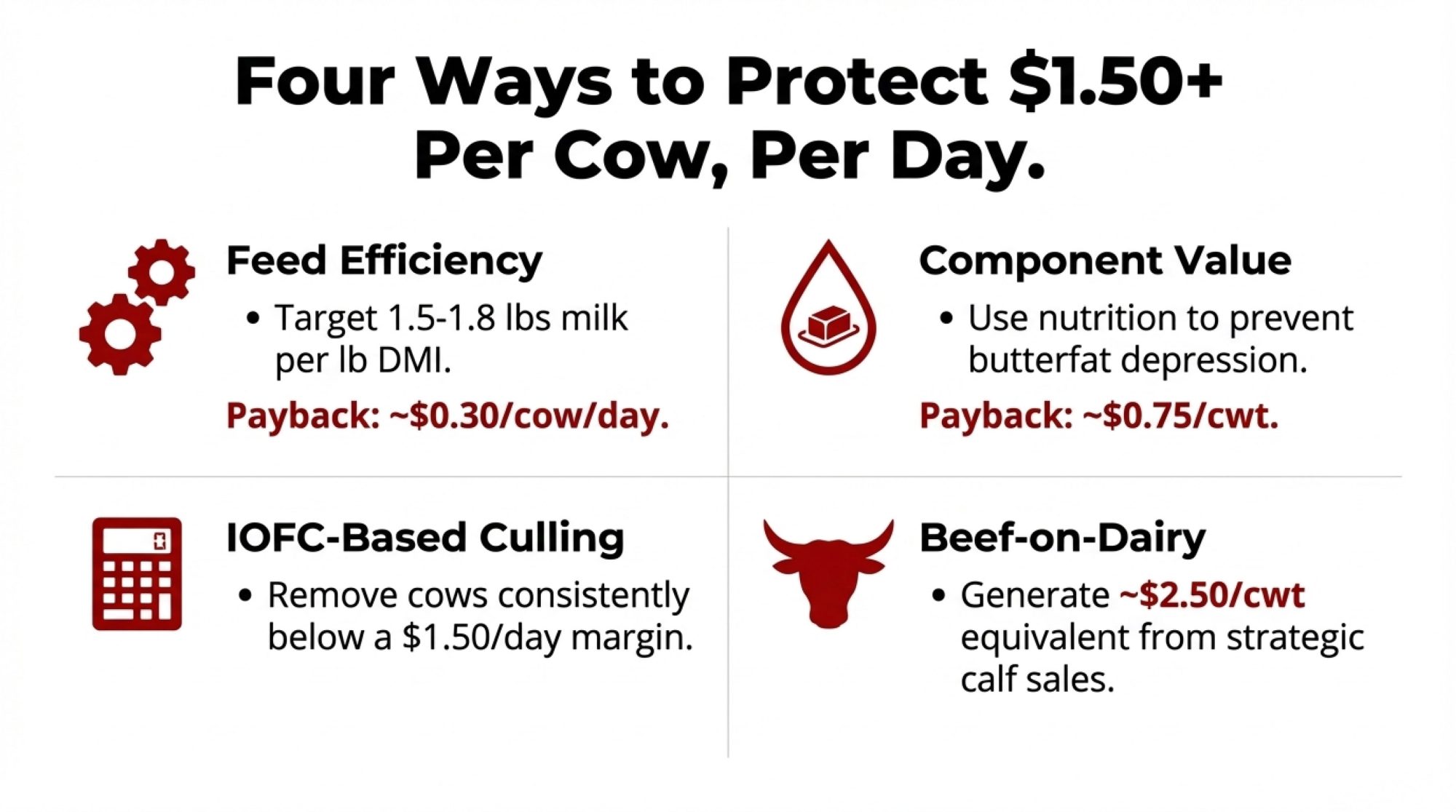

1. Component Optimization

Breeding and feeding for butterfat has been the go‑to growth lane. But the payoff depends entirely on when you’re selling that fat.

Butterfat premium: same herd, two prices (400‑cow herd, 23,000 lbs/cow, 3.8% → 4.2% BF = 36,800 extra lbs fat/year)

If you’re still budgeting on 2025 butterfat prices, you’re overstating your 2026 margin by about $0.40/cwt before you even start the mixer. If your plant pays on straight hundredweight with no component bonus, the math is even uglier—you’re carrying the extra feed cost without seeing the fat check.

Trade‑off: Components still matter, but the days of butterfat bailing out every hole in the budget are on pause until that $/lb recovers.

2. Risk Management Enrollment—Before February 26

This one’s on a hard deadline.

The One Big Beautiful Bill Act (OBBBA) reinstated the Dairy Margin Coverage program for 2026–2031 and expanded Tier 1 coverage to 6 million pounds of production history at up to $9.50/cwt margin coverage. Producers who lock in all six years get a 25% premium discount, according to the University of Minnesota Extension’s January 27 enrollment guide. Production history is based on your highest marketings from 2021, 2022, or 2023.

Six million pounds covers roughly a 270‑cow herd at 22,000 lbs/cow. Everything above that needs to be managed with DRP, futures, or options. LRP can backstop your calf and cull revenue.

Trade‑off: DMC only sees feed costs. If your margin squeeze is coming from debt service, labor, or energy, DMC checks help the feed side, but don’t fix the whole picture. Minnesota producers should also look hard at the state’s DAIRI program, which ties about $3 million in state funds to DMC participation.

3. Lender Engagement—Early, With Real Numbers

The Wisconsin producer’s experience is the template.

Showing up with a full cost‑of‑production sheet, a 12‑month cash flow at $18–$19 milk, and a specific restructuring ask is a completely different conversation than showing up after you’ve bounced a check.

Reamortization math: $500,000 note at 7.5%

Metric

7-Year Term

12-Year Term

Difference

Monthly payment

$7,670

$5,280

−$2,390/mo (−31%)

Annual debt service

$92,040

$63,360

−$28,680/yr

Total interest paid

$144,200

$259,800

+$115,600