One box on your DMC form decides if your 300‑cow herd keeps a $15,000 cheque—or donates it to Washington. Tier 1 isn’t 5M anymore.

Executive Summary: For 2026, DMC’s Tier 1 cap quietly jumped from 5 million to 6 million pounds, and that one change is worth roughly $15,000–$18,000 a year in premium savings for a lot of 300‑cow herds that actually use it. USDA also reset the rules so everyone enrolling this year has to rebuild production history off the best of their 2021–2023 milk and can lock coverage through 2031 for a 25% discount, which is why “same as last year” at FSA has suddenly become a very expensive reflex. The sting is in the premium gap: Tier 1 at $9.50 still runs about $0.15/cwt, while Tier 2 at $8.00 is around $1.81/cwt, so every hundredweight you move into Tier 1 is swapping a $1.81 bill for $0.15 instead. What’s encouraging is that risk‑management analysts at Ever.Ag and NMPF both expect DMC to throw off real payments in early 2026, and today’s feed costs and milk futures back that up. From there, the article walks you through a simple “runway test”—how many months of fixed costs your current cash covers—to right‑size Tier 2 and decide if that six‑year, 25% discount fits your herd plans or if annual flexibility matters more. For many Midwest 200–500 cow freestall herds, maxing Tier 1 at $9.50 is almost automatic, while Western and Northeast operations still pair DMC with Dairy Revenue Protection or LGM‑Dairy to deal with basis and local feed quirks. In the end, one DMC checkbox now decides whether your farm keeps a five‑figure cheque the new Tier 1 rules already put on the table—or quietly gives it back.

The Tier 1 cap just jumped to 6 million pounds. If you sign the “same as last year” form, you’re essentially handing the government a five‑figure donation.

You know how it goes. It’s January, you’re juggling fresh cow management, frozen lines, butterfat levels that always seem to slide when it turns cold, and a lender review that’s been sitting on the corner of your desk for a little too long. Somewhere between a transition cow that’s not quite right and a scraper that breaks at the worst time, you duck into the FSA office and say, “Let’s just renew what we had last year so I can get back to the barn.”

In a lot of years, that’s been fine. This year, it really isn’t. The way 2026 Dairy Margin Coverage is set up, that “autopilot” answer can quietly cost a typical 300‑cow herd somewhere in the fifteen‑ to twenty‑thousand‑dollar range in extra premiums over the year, based on USDA’s new Tier 1 rules and the official premium schedule that land‑grant universities use in their decision tools.

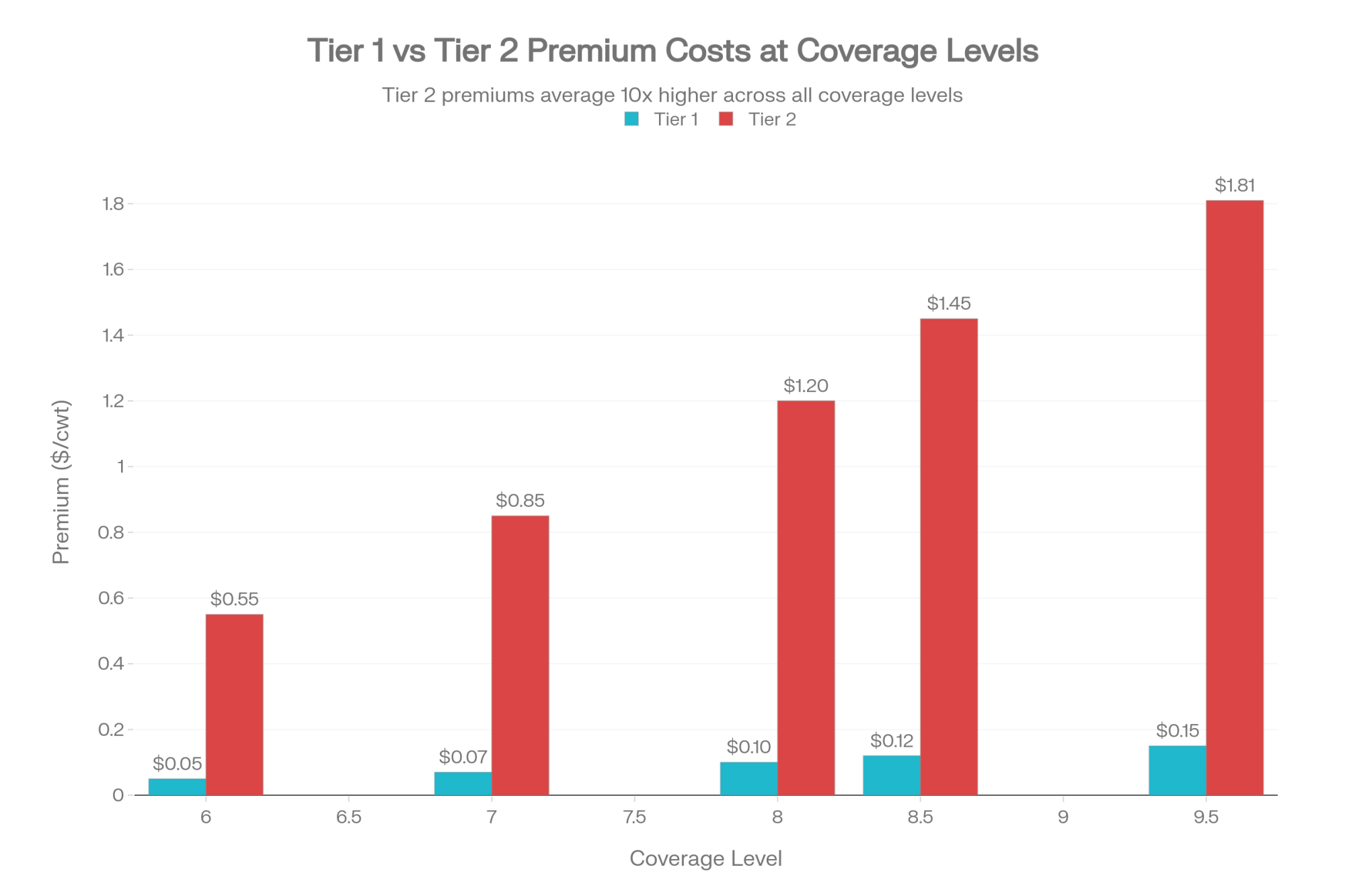

| Coverage Level | Tier 1 Premium ($/cwt) | Tier 2 Premium ($/cwt) | Difference ($/cwt) |

|---|---|---|---|

| $9.50 Coverage | 0.15 | 1.81 | 1.66 |

| $8.50 Coverage | 0.12 | 1.45 | 1.33 |

| $8.00 Coverage | 0.10 | 1.20 | 1.10 |

| $7.00 Coverage | 0.07 | 0.85 | 0.78 |

| $6.00 Coverage | 0.05 | 0.55 | 0.50 |

Here’s what’s interesting about 2026: USDA has actually been very clear about what changed. At the American Farm Bureau convention, Agriculture Secretary Brooke Rollins walked through how the One Big Beautiful Bill Act—signed on July 4, 2025—extended DMC through 2031, increased Tier 1 coverage from 5 million to 6 million pounds, required every operation enrolling in 2026 to set a fresh production history using the highest of its 2021, 2022, or 2023 milk marketings, and created the option to lock coverage in for 2026–2031 with a 25% premium discount.

So let’s sit down, as if we were at the kitchen table with a pot of coffee, and walk through what that actually means on your farm—because the numbers are big enough that it’s worth slowing down for.

What Changed—and Why That Extra Million Pounds Is “Cheaper,” Not Just “More”

Looking at this trend in the 2026 rules, the headline change is pretty straightforward: Tier 1 DMC coverage now runs up to 6 million pounds per year instead of stopping at 5 million. But the real story isn’t just that you can cover more milk. It’s that the extra milk can be covered at a much lower premium.

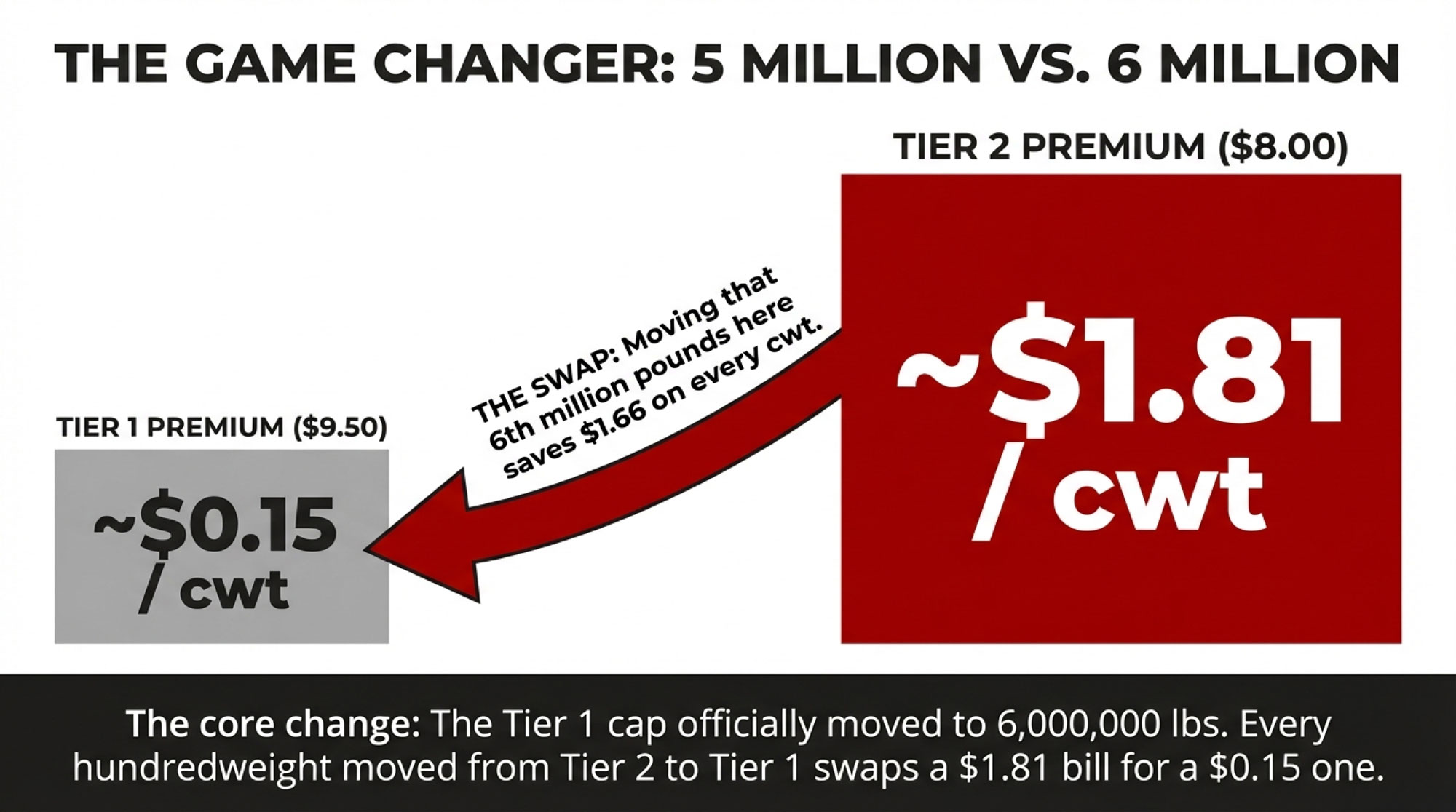

If you pull up the current DMC premium tables on FSA’s website—the same table the University of Wisconsin’s 2025 DMC update uses and that Hoard’s Dairyman has referenced in their coverage analysis—you see that Tier 1 coverage at the top $9.50 margin level carries a premium of about $0.15 per hundredweight, while Tier 2 coverage at $8.00 carries a premium of about $1.81 per hundredweight. Extension economists in Wisconsin and other land‑grant universities are using those exact numbers in their DMC decision tools.

So the spread you’re working with is roughly $1.66 per hundredweight between Tier 1 at $9.50 and Tier 2 at $8.00.

Now, here’s where it starts to matter. At 95% coverage, one million pounds of milk equals 9,500 hundredweight. Move those 9,500 hundredweight from Tier 2 at $1.81 to Tier 1 at $0.15, and you cut your premium bill by about $15,700 for the year. Dairy‑focused accounting firms like Adams Brown have shared examples in their late‑2025 DMC brief that land in that same ballpark.

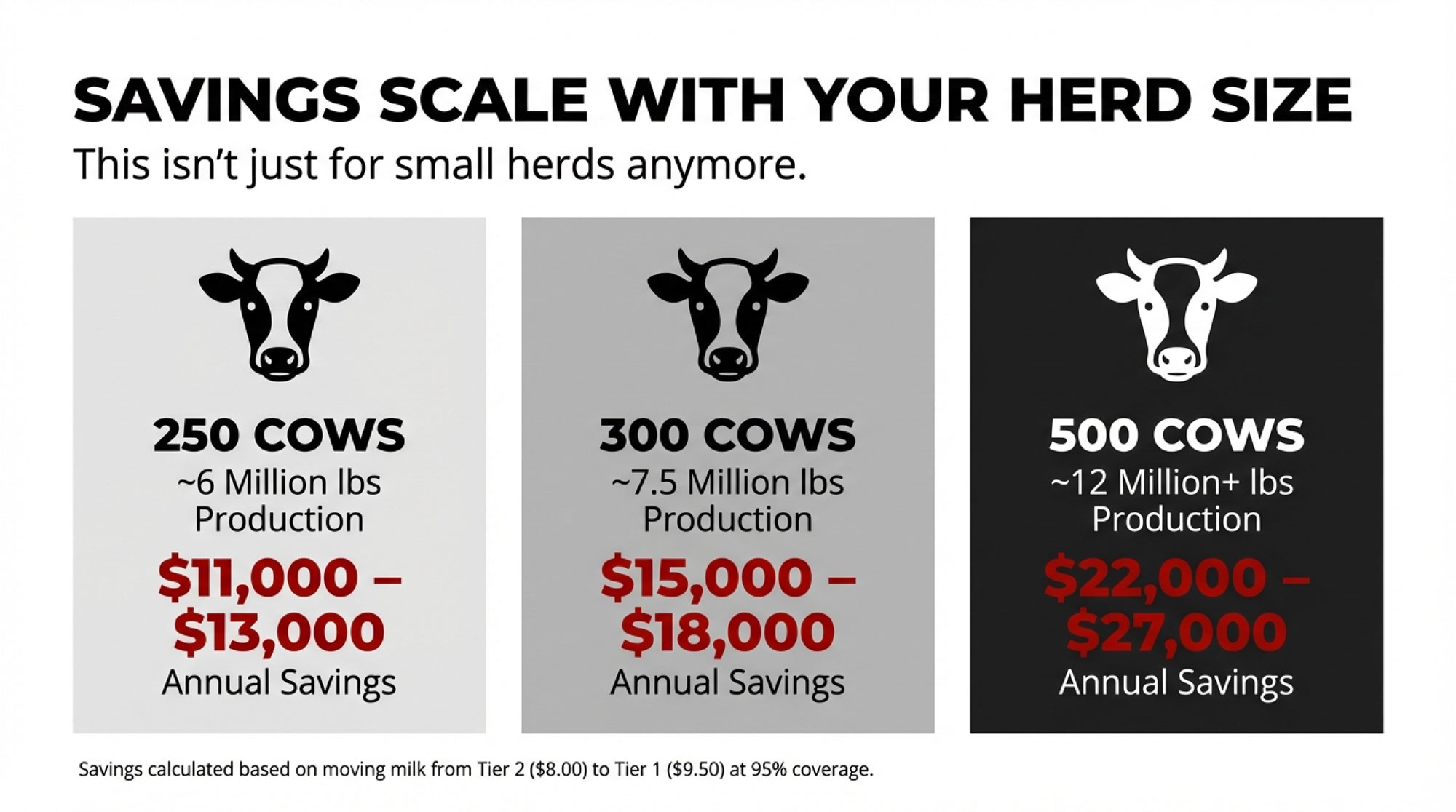

When you scale that up to realistic herd sizes, using commonly reported production levels:

| Approx. Herd Size | Annual Milk (lbs) | Estimated Annual Premium Savings* |

| 250 cows | ~6 million | $11,000–$13,000 |

| 300 cows | ~7–7.5 million | $15,000–$18,000 |

| 500 cows | ~12 million+ | $22,000–$27,000 |

*Based on FSA’s published premiums (Tier 1 at $9.50 ≈ $0.15/cwt; Tier 2 at $8.00 ≈ $1.81/cwt) with 95% coverage, using the same method as USDA‑endorsed DMC tools.

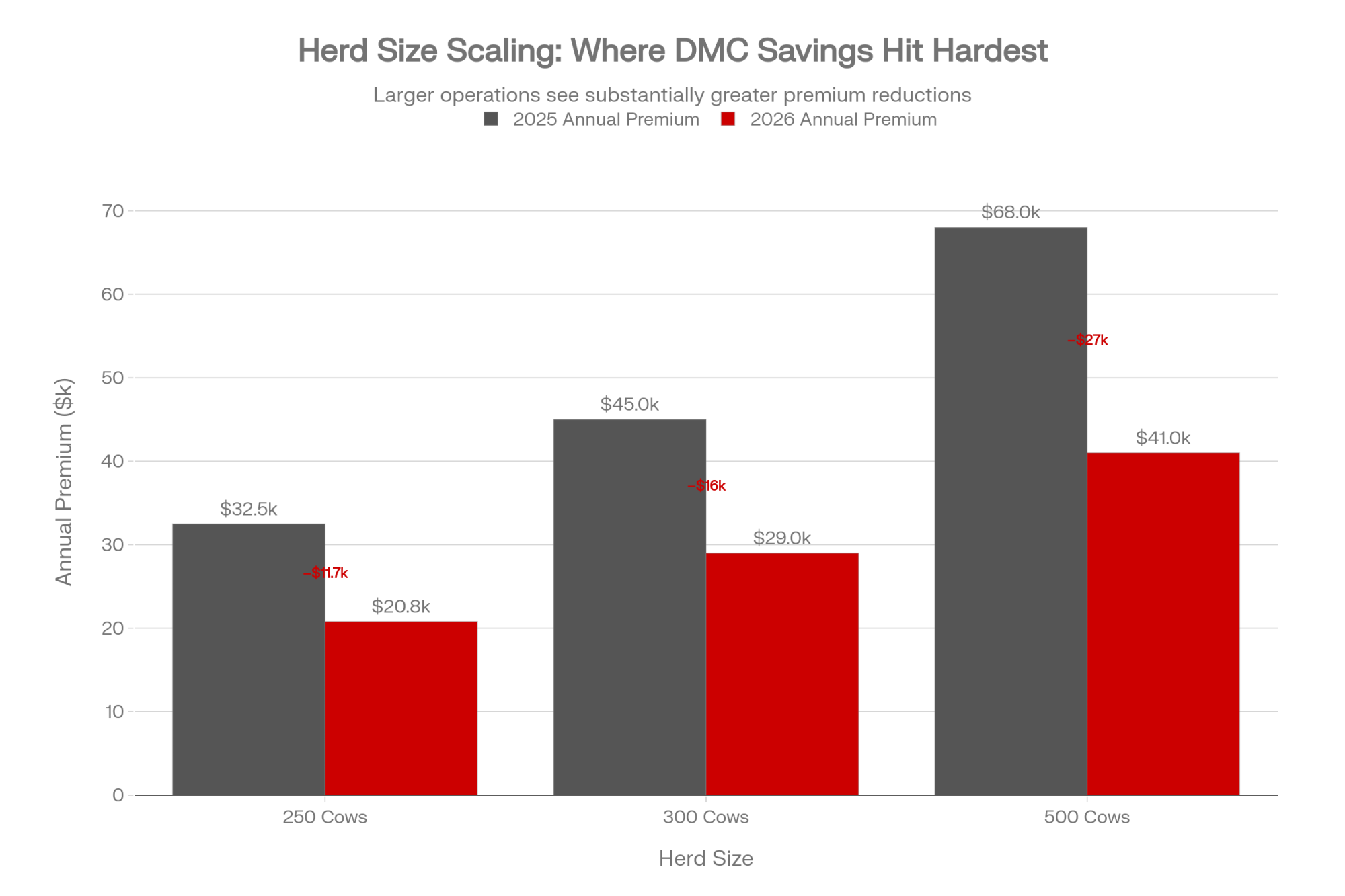

Look at those numbers and tell me DMC is “just for small herds.” That old myth doesn’t hold up when you run the Tier 1 math on 300‑ to 500‑cow operations. The premium gap is real, and it scales.

| Herd Size (Cows) | Annual Production (lbs) | 2025 Annual Premium | 2026 Annual Premium | Annual Savings |

|---|---|---|---|---|

| 250 | ~6M | ~$32,500 | ~$20,800 | ~$11,700 |

| 300 | ~7.2M | ~$45,000 | ~$29,000 | ~$16,000 |

| 500 | ~12M+ | ~$68,000 | ~$41,000 | ~$27,000 |

What I’ve noticed is that when producers see those numbers in winter meetings, the first reaction is often, “That can’t be right.” But then someone pulls up the FSA table or the University of Wisconsin DMC calculator on their phone, lays in their own production history, and the savings that pop out look very similar.

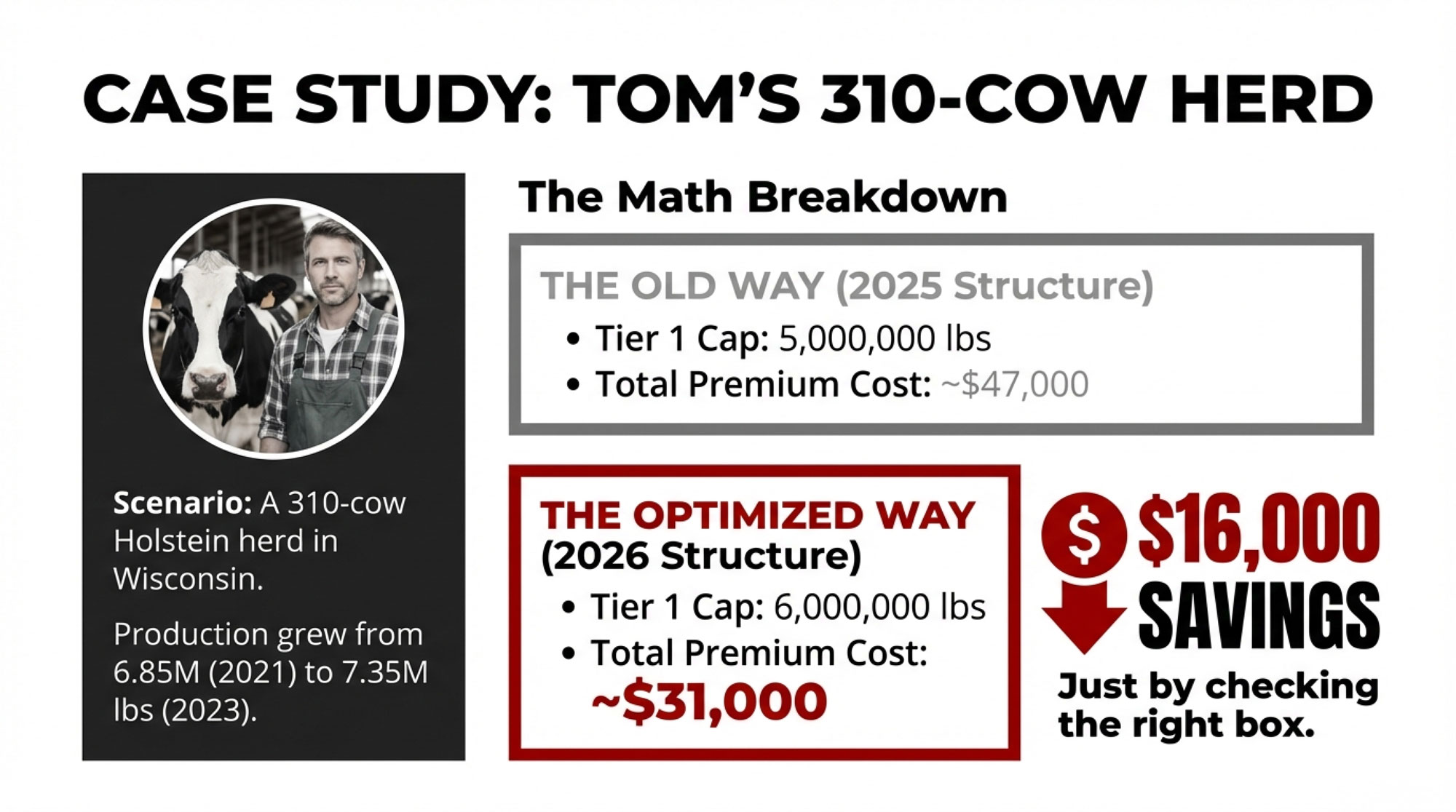

A “Tom in Wisconsin” Example: Putting the Math on a Real‑World Herd

Let’s walk through a scenario that looks a lot like many operations in the Upper Midwest.

Tom milks about 310 Holsteins in central Wisconsin. His cows are in sand‑bedded freestalls, he raises his own replacements, and he uses a dry lot system for bred heifers. Over the last few years he’s focused hard on the transition period—fresh cow checks, pre‑fresh diets, keeping stalls well‑bedded—because he saw what transition problems were doing to his cull rate and vet bills, which lines up with what Wisconsin extension has been emphasizing in herd case studies.

His co‑op milk statements show roughly:

- 2021: about 6.85 million pounds

- 2022: about 7.10 million pounds

- 2023: about 7.35 million pounds

Under the updated DMC rules USDA and FSA laid out for 2026, his DMC production history must be set to the highest of those three years, which would be about 7.35 million pounds. USDA and state Farm Bureaus have been repeating that “highest of 2021–2023” requirement in their DMC explainer pieces.

Now think about how Tom’s 2025 DMC coverage looked, which fits a lot of herds his size:

- Tier 1: 5,000,000 pounds at $9.50, 95% coverage.

- Tier 2: 2,350,000 pounds at $8.00, 95% coverage.

Using the FSA premium schedule, that structure puts his Tier 1 premiums at roughly $7,100 and his Tier 2 premiums just over $40,000, for a combined DMC premium total in the $47,000–$48,000 range.

For 2026, using the same coverage levels but with the new Tier 1 cap, Tom could set:

- Tier 1: 6,000,000 pounds at $9.50, 95% coverage.

- Tier 2: 1,350,000 pounds at $8.00, 95% coverage.

Run that through the same FSA table and his total premium drops into the $31,000–$32,000 range, which is a reduction of roughly $15,000 for the year. Consultants and extension economists using USDA‑supported DMC calculators have shown similar results in examples with 280‑cow New York herds and 400‑ to 450‑cow Idaho herds, so Tom’s case isn’t a unicorn.

It’s worth noting that Tom isn’t doing anything exotic here. He’s just using the extra million pounds of Tier 1 that Congress and USDA have already given him.

| DMC Tier & Coverage | 2025 (Autopilot) | 2026 (Optimized) | Change / Savings |

|---|---|---|---|

| Tier 1 (@ $9.50, 95% coverage) | 5.0M lbs @ $0.15/cwt = $7,100 | 6.0M lbs @ $0.15/cwt = $8,500 | +$1,400 |

| Tier 2 (@ $8.00, 95% coverage) | 2.2M lbs @ $1.81/cwt = $38,000 | 1.2M lbs @ $1.81/cwt = $20,700 | –$17,300 |

| Total Annual DMC Premium | $45,100 | $29,200 | SAVES $15,900 |

| 6-Year Lock-In Discount (25%) | N/A | $7,380 avg. annual savings | Extra $44,280 over 6 years |

Why So Many Good Managers Could Still Miss This

What farmers are finding is that the biggest risk here isn’t that producers don’t care about DMC. It’s that the timing and process make it way too easy to default to “just renew it.”

USDA’s January 2026 announcements make it clear that DMC enrollment for the 2026 coverage year runs from January 12 through February 26. For most herds, that window lands right on top of:

- Winter headaches in the Midwest and Northeast: frozen lanes and waterers, tough calvings, ration adjustments to protect milk and butterfat, and fresh cow issues that demand attention.

- Weather swings and mud out West and in the Southwest: keeping cows comfortable in open housing and dry lot systems when conditions aren’t ideal.

- Financial review season everywhere: lender meetings, tax prep, feed and seed contracting, and labor scheduling.

On the FSA side, county offices are juggling ARC/PLC, CRP, disaster assistance, and DMC at the same time. Their software is designed to pull up your previous DMC elections and ask if you want to make changes. It doesn’t automatically flash a message that says, “Your Tier 1 cap just went from 5 million to 6 million pounds and your production history has been recalculated.”

So you get conversations like this:

- FSA: “Last year you had 5 million pounds in Tier 1 and 2.35 million in Tier 2 at these coverage levels. Do you want to keep that?”

- Producer, thinking about getting back to the barn: “Yeah, that worked. Let’s renew it.”

Extension economists in Wisconsin, Pennsylvania, and Kentucky have all used some version of the phrase, “2026 is not the year to just renew last year’s DMC structure,” precisely because the Tier 1 cap and production histories have changed.

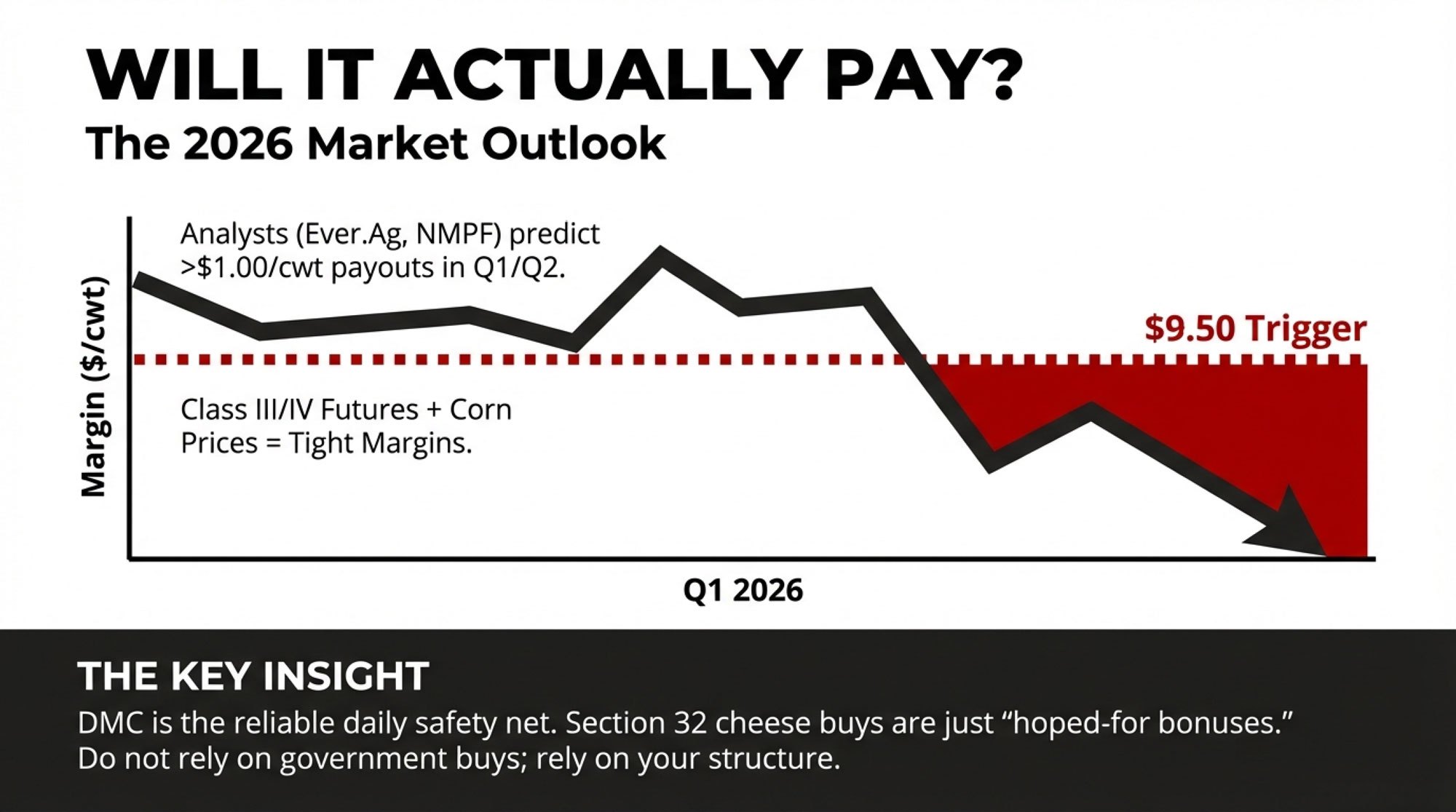

So… Is DMC Actually Likely to Pay in 2026?

The next question that usually comes up—and it’s a fair one—is, “If I take the time to optimize Tier 1, is DMC even going to pay, or am I just rearranging premiums?”

If you look at the recent track record and the early 2026 outlook, the program looks likely to pay at the $9.50 level in at least part of the year.

In 2023, DMC triggered payments in most months at $9.50 coverage. Dairy Herd reported that eligible producers enrolled in DMC received indemnity payments 11 out of 12 months that year, averaging about $2.80 per cwt per month. Farmers in Tier 1 who chose $9.50 coverage paid a premium of $0.15 per cwt over the last six years and received average annual payments of $1.17 per cwt—meaning that taking full coverage from DMC was clearly beneficial.

| Month | 2023 Actual | 2024 Actual | 2025 Forecast | 2026 Forecast | Tier 1 Trigger @ $9.50 |

|---|---|---|---|---|---|

| January | 8.20 | 8.48 | 9.85 | 7.80 | 9.50 |

| February | 8.50 | 9.12 | 10.20 | 8.20 | 9.50 |

| March | 8.75 | 9.50 | 10.50 | 8.50 | 9.50 |

| April | 9.10 | 9.75 | 10.80 | 9.00 | 9.50 |

| May | 9.40 | 10.00 | 11.00 | 9.50 | 9.50 |

| June | 9.80 | 10.20 | 11.10 | 10.00 | 9.50 |

In 2024, DMC delivered its first strong payment when the January margin dropped to $8.48 per hundredweight, resulting in payments of about $761 for each one million pounds enrolled at the $9.50 level.

Moving into late 2025, USDA’s DMC margin updates and industry commentary show the November 2025 margin sitting just over $10 per hundredweight—down from earlier in the year, but still above the $9.50 trigger. USDA’s decision tool and extension economists using it were projecting that the December 2025 margin would fall below $9.50, which would trigger a DMC payment for December milk at the $9.50 coverage level.

Katie Burgess, director of risk management at Ever.Ag, in January 13, 2026 said their model was showing DMC payouts of more than $1 per hundredweight for January through April at $9.50 coverage, with smaller payouts likely for May through July. In the same article, William Loux, senior vice president of global economic affairs for the National Milk Producers Federation, said he would “certainly expect to see some DMC payments here through the first quarter and probably through the first half of the year,” and that a payment for December 2025 milk was “fairly well assured” based on projected margins and futures.

The data suggests they’re not just guessing. They’re looking at the same mix of milk prices and feed costs producers are.

| Month | 2023 Actual | 2024 Actual | 2025 Forecast | 2026 Forecast | Tier 1 Trigger @ $9.50 |

|---|---|---|---|---|---|

| January | 8.20 | 8.48 | 9.85 | 7.80 | 9.50 |

| February | 8.50 | 9.12 | 10.20 | 8.20 | 9.50 |

| March | 8.75 | 9.50 | 10.50 | 8.50 | 9.50 |

| April | 9.10 | 9.75 | 10.80 | 9.00 | 9.50 |

| May | 9.40 | 10.00 | 11.00 | 9.50 | 9.50 |

| June | 9.80 | 10.20 | 11.10 | 10.00 | 9.50 |

Overlay that with current market signals:

- Class III and Class IV futures for early 2026 have been trading in the mid‑teens, which most economists describe as a tight‑margin environment when paired with today’s costs.

- USDA and industry analyses suggest corn is generally in the mid‑$4 per bushel range, soybean meal in the mid‑$300 per ton range, and high‑quality hay still elevated in several dairy regions.

Put those feed prices into the DMC formula and the margin projections coming from NMPF, USDA’s tools, and independent risk advisers line up with what Burgess and Loux are talking about: DMC payments are quite likely for at least some of the first half of 2026 at $9.50.

So this isn’t just about tidying up premiums for a program that doesn’t pay. The odds are good that DMC will actually do its job this year.

Section 32: What USDA’s Buying Tells You About the Safety Net

Looking at USDA’s recent Section 32 moves adds one more signal about where the real support lives now—and it’s a pretty important pivot.

At that same Farm Bureau convention, USDA announced a new round of commodity purchases using Section 32 funds—up to $80 million worth of specialty crops, split equally between almonds, grape products, pistachios, and raisins, as Dairy Reporter detailed in their January coverage. There’s no dairy in that particular package.

In past downturns like 2009 and 2016, USDA did use cheese and other dairy purchases under similar authorities, and both NMPF and dairy economists have said those interventions mattered.

And here’s the pull‑quote version of what this all adds up to:

DMC is now the day‑in, day‑out safety net for dairy margins, while Section 32 purchases are targeted and episodic. The most reliable protection is the one you structure yourself.

For your operation, that means the program you can count on is the one you enroll in and shape—not a hoped‑for cheese buy that may or may not come when margins tighten.

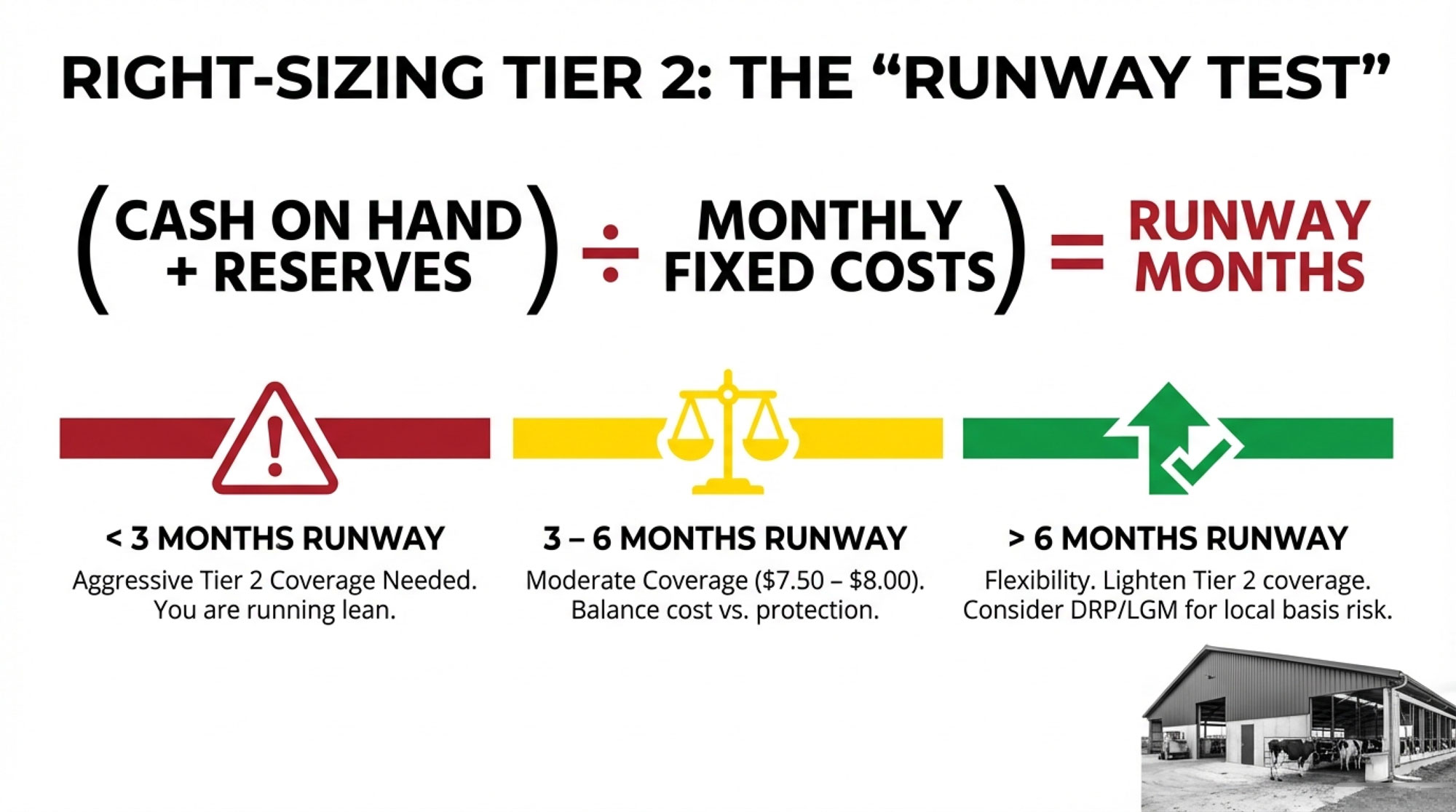

A Simple Way to Right‑Size Tier 2: The Runway Test

Once you’re committed to taking full advantage of the 6‑million‑pound Tier 1 cap (if your production allows it), you’ve still got two big questions left:

- How aggressive should your Tier 2 coverage be?

- Does the six‑year lock‑in with a 25% discount make sense for your farm?

What I’ve found, and what many lenders and farm‑business consultants are using, is a simple “runway” test that keeps those decisions grounded in your actual cash position.

Here’s the basic idea, which lines up closely with how Farm Credit and several university farm‑management programs talk about resilience:

- Add up how much cash you can realistically access in the next 30 days—operating account plus short‑term reserves that you’d actually tap if you needed to.

- Add up your true monthly fixed costs—scheduled debt payments, essential payroll, insurance, property taxes, and core utilities.

- Divide cash by monthly fixed costs. That’s your runway in months.

| Farm Scenario | Monthly Fixed Costs | Accessible Cash | Runway (Months) | Recommended Tier 2 Level |

|---|---|---|---|---|

| Lean (Under 3 months) | $35,000 | $75,000 | 2.1 months | $8.00 (High Coverage %) |

| Middle (3–6 months) | $40,000 | $180,000 | 4.5 months | $7.50–$8.00 (Moderate Coverage %) |

| Strong (Over 6 months) | $38,000 | $250,000 | 6.6 months | $7.00–$7.50 (Lower Coverage %) |

Then you match Tier 2 to that runway:

- If your runway is under about three months, you’re running fairly lean. In that case, a stronger Tier 2 position—often around the $8.00 level at a high coverage percentage—can be justified, because you don’t have much cushion if margins go south.

- If you’re in the three‑ to six‑month range, you’re in more of a middle ground. Many advisers in extension and lending suggest Tier 2 coverage somewhere between $7.50 and $8.00 there, adjusted to your comfort level and your local milk and feed market.

- If your runway is more than six months, you’ve earned some flexibility. Some producers in that position lighten up Tier 2 coverage and rely more on working capital and other tools, like Dairy Revenue Protection, to target specific risks, especially in regions where basis and local feed costs don’t track the national DMC formula as closely.

The nice thing about this approach is that it uses a metric your lender already cares about—months of coverage—and translates it into DMC choices, instead of guessing based on “how nervous you feel” in a given year.

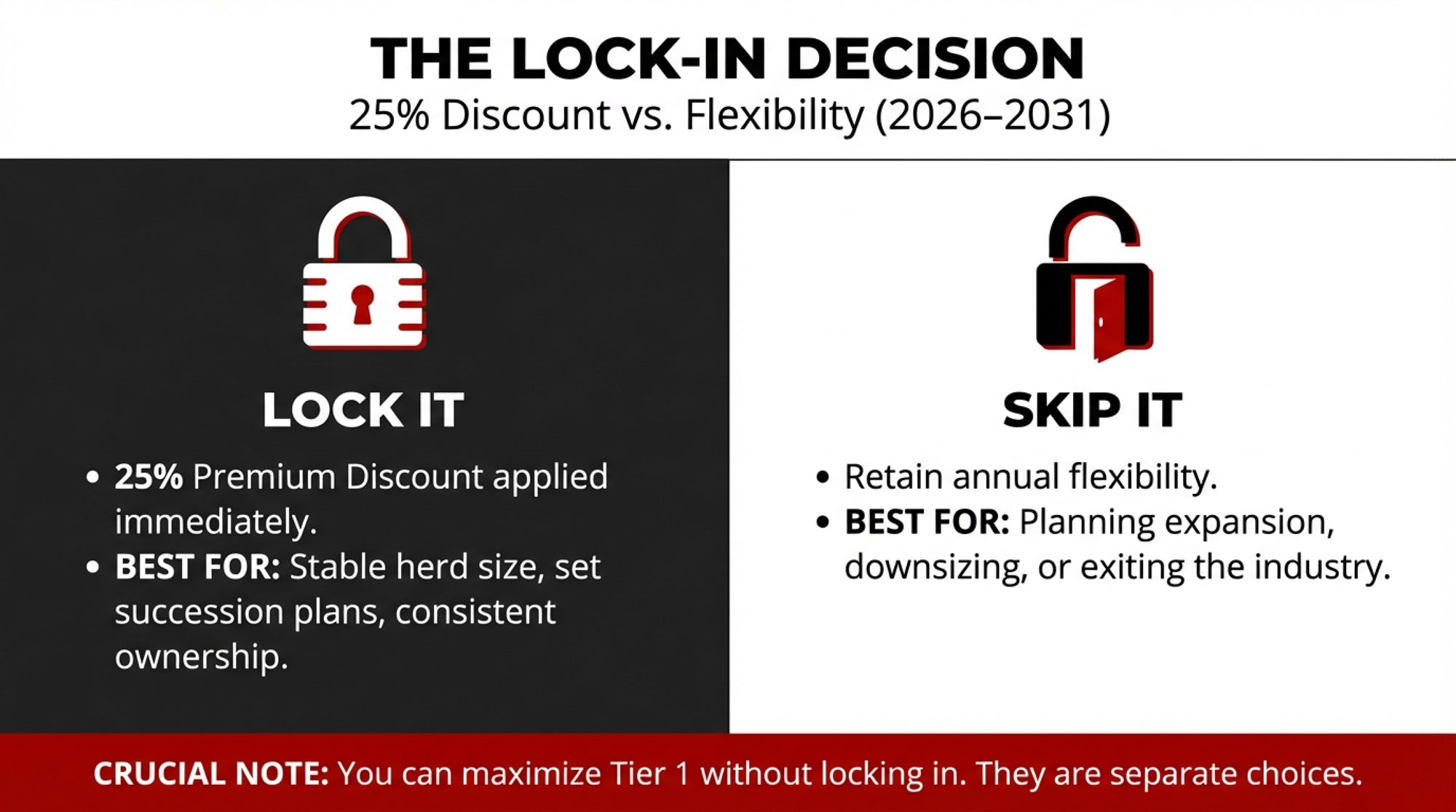

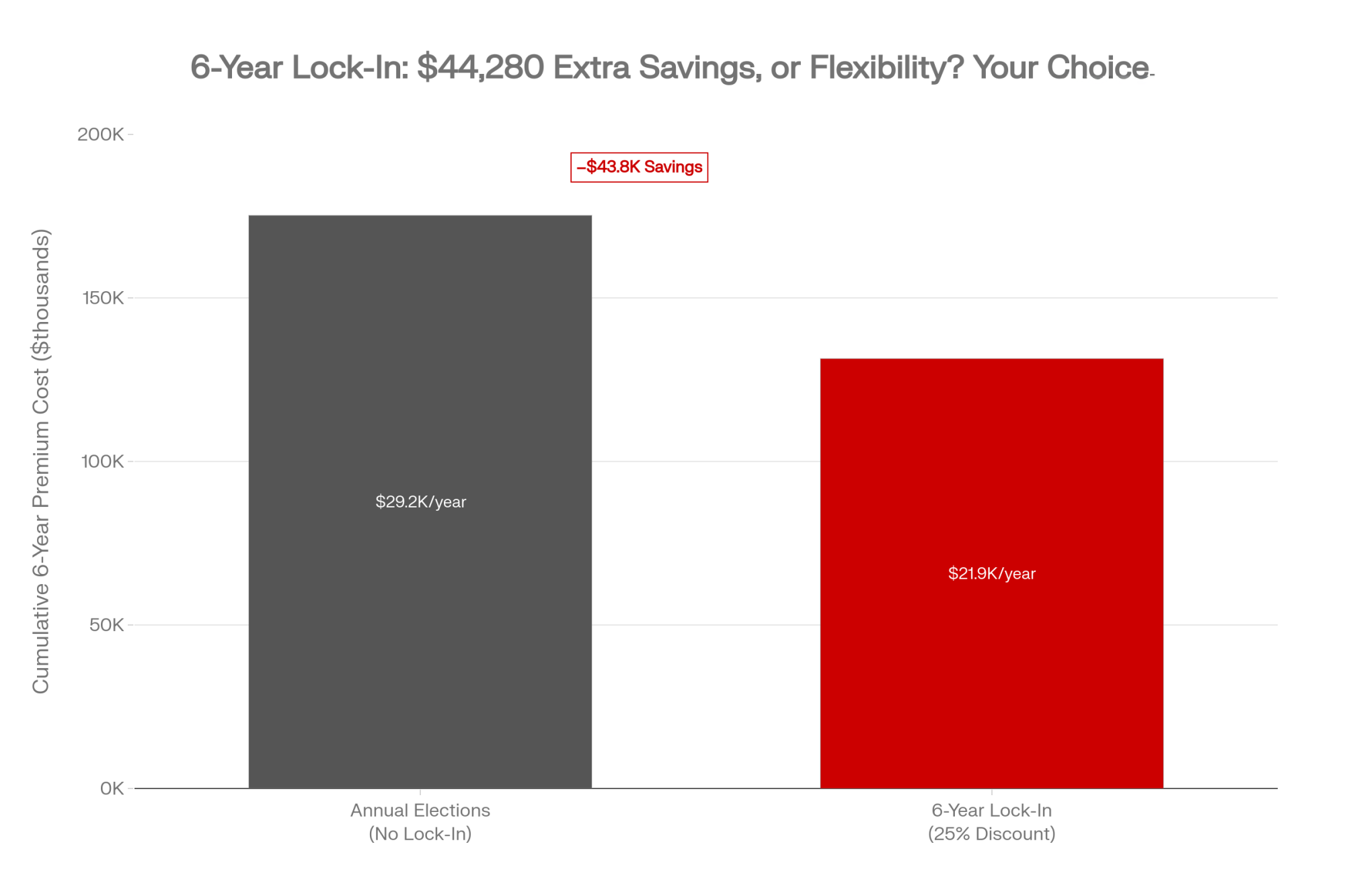

The Six‑Year Lock‑In: When That 25% Discount Fits—and When It Doesn’t

The other new lever on the DMC dashboard is the six‑year lock‑in. Under OBBBA and the updated USDA rules, you can choose to lock in your DMC coverage structure from 2026 through 2031 and receive a 25% discount on your premiums every year you stay in that lock‑in.

For a herd like Tom’s, once he’s got Tier 1 maxed out and a sensible Tier 2 level in place, that discount could easily shave $7,000–$8,000 off his annual premium bill—something in the $40,000–$50,000 range over the full six‑year run. For larger operations, the savings are even bigger.

But it’s not free money. You’re committing to that structure for six years.

| Scenario | Year 1 Premium | Years 2–6 Premium (each) | Total 6-Year Cost | Premium Discount | Net 6-Year Savings |

|---|---|---|---|---|---|

| Annual Elections (No Lock-In) | $29,200 | $29,200 | $175,200 | $0 | — |

| 6-Year Lock-In (25% Discount) | $21,900* | $21,900* (each) | $131,400 | Yes | –$43,800 |

What extension specialists and lender panels tend to say is:

- If you’re not planning major changes in herd size, and your succession plan is already fairly clear and in motion, the lock‑in can make a lot of sense. It lowers your annual costs and provides a stable risk‑management framework for you and your lender.

- If you’re seriously considering expansion, downsizing, exiting, or still wrestling with how succession will play out, then keeping the flexibility of annual DMC elections can be more valuable than the 25% discount.

Either way, the Tier 1 optimization—using all 6 million pounds you’re entitled to—is a separate decision. You can and should do that whether you lock in or enroll year‑by‑year.

Why This Program Feels Different in Wisconsin, California, and the Northeast

As many of us have seen over the years, national programs like DMC land very differently depending on where you milk cows and how you sell your milk.

In Wisconsin and much of the Upper Midwest, a lot of producers ship to cooperatives where their mailbox price tends to track the national all‑milk price reasonably well, and feed costs for corn and soybean meal often move with national markets. University of Wisconsin economists have shown that for many Wisconsin herds, the national DMC margin formula is a decent approximation of their own “income over feed cost,” especially around corn‑and‑alfalfa based rations. For 200‑ to 500‑cow freestall herds in that region, fully using the 6‑million‑pound Tier 1 cap at $9.50 is about as close to a slam‑dunk as risk management gets.

In California’s Central Valley, Idaho, New Mexico, and parts of Texas, the story is different. Local basis can pull mailbox prices down well below national averages, and key feeds—especially high‑quality alfalfa and some silages—are more expensive because of water, land, and freight. Western dairy coverage and interviews with leaders like Rick Naerebout of the Idaho Dairymen’s Association highlight how these economics have “dampened” growth and turned the screws on mid‑size and large herds. In those regions, many operations still enroll in DMC for Tier 1 but lean heavily on Dairy Revenue Protection or LGM‑Dairy to tailor coverage to their actual prices and feed base.

In the Northeast—Vermont, upstate New York, parts of Pennsylvania—you see more small and mid‑size family herds, some of them shipping less than 5–6 million pounds a year. Cornell and Penn State DMC outreach has shown that for those herds, every pound is already in Tier 1, and $9.50 coverage has historically offered a strong return in low‑margin years because premiums are so heavily subsidized relative to potential payouts. Their main DMC questions revolve less around Tier 2 and more around “Do we stay at $9.50?” and “Does this six‑year lock‑in fit where our family and farm are headed?”

For Canadian readers, DMC doesn’t apply under supply management and quota, but the logic around runway, premium cost, and matching risk tools to financial resilience still holds true when you’re evaluating other tools or bigger strategic decisions.

So while the core message—don’t leave Tier 1 stuck at 5 million pounds when it can be 6—applies across the board, the rest of the plan deserves to be tuned to your region, your buyer, and your long‑term strategy.

A Simple Checklist Before You Head to FSA

Let’s pull this all together into a straightforward checklist you can use before that February 26 deadline.

- Gather your production history. Print or download your total milk marketings for 2021, 2022, and 2023 from your co‑op or buyer. Under the current rules, FSA must use the highest of those three years to set your 2026 DMC production history.

- Review your 2025 DMC structure. Look at how many pounds you had in Tier 1 and Tier 2, your coverage levels, and your total annual premium. That’s your baseline.

- Run your runway test. Calculate how many months of fixed costs your readily accessible cash would cover. Use that to decide how strong Tier 2 needs to be.

- Sketch your 2026 coverage plan. At a minimum:

- Move Tier 1 up to the lesser of 6 million pounds or your new production history at the $9.50 level, ideally at a high coverage percentage.

- Put remaining pounds into Tier 2 at a margin level and coverage percentage that match your runway and your comfort with risk.

If you’d like a second opinion on the math, plug your numbers into a DMC calculator from a trusted university, such as Wisconsin or Cornell, which are designed precisely for this kind of scenario testing.

- Decide on the six‑year lock‑in. Talk with your lender and your family about whether the 25% premium discount for locking in 2026–2031 coverage fits your herd‑size plans and generational timing, or whether annual flexibility is more important.

- Book your FSA appointment early. Don’t leave it for the last week of February. Give yourself time to fix any data or coverage issues if something looks off.

- Be explicit at the appointment. When the FSA technician opens your file, say something like:

“I want to restructure my 2026 DMC coverage to make full use of the six‑million‑pound Tier 1 cap at $9.50. I don’t want to just renew last year’s structure.”

Then watch the screen and confirm that Tier 1 is at 6 million pounds (or at your full production history if it’s lower), Tier 2 matches the plan you worked out at home, and the total premium is in the range you expect from your own calculations or the DMC tool.

If you don’t say you want to change it, the system is perfectly happy to keep charging Tier 2 premiums on milk that could be under Tier 1. And once you’re out of the enrollment window, there’s no fixing it until next year.

Key Takeaways for 2026 DMC

- Use the new 6‑million‑pound Tier 1 cap at $9.50 if your production allows it; the premium gap with Tier 2 can easily reach five figures per year for mid‑size herds.

- Run a simple runway test—months of fixed costs you can cover with accessible cash—and let that guide how strong your Tier 2 coverage needs to be.

- Think carefully about the six‑year, 25% premium discount; it’s a powerful tool if your herd size and succession plans are stable, but annual elections may suit operations in transition better.

- Don’t let DMC renew on autopilot at FSA. Go in with your own numbers and a clear plan to restructure coverage for 2026.

The Bottom Line

Stepping back, what’s happening with DMC in 2026 is a good snapshot of the bigger shift we’ve all felt over the last decade. We’ve gone from relying mainly on ad‑hoc price supports and occasional government cheese purchases to a world where structured, margin‑based tools—DMC at the core, with DRP and other options on the side—are the backbone of dairy risk management.

What I’ve noticed, across different regions and herd sizes, is that the operations that treat DMC like a tool they understand and deliberately shape tend to come through rough stretches with more options. They still feel the squeeze when Class III prices and feed costs move against them, but they’re more likely to keep investing in the things that truly move the needle: cow comfort in the transition period, better ventilation, milking systems that fit their labor pool, genetics tuned to their market, and feeding strategies that protect income over feed cost when grain and forage prices spike.

You can’t set the Class III price. You can’t decide how much milk Europe or New Zealand puts on the world market. You can’t tell USDA exactly when and where to use Section 32 next.

You can decide how you structure your DMC coverage in a year when Tier 1 just got more generous and margins are expected to be tight.

So if there’s one government form you don’t want to autopilot before February 26, it’s this one. Run your numbers. Max out Tier 1 at 6 million pounds if your production allows it. Let your runway guide Tier 2. Walk into FSA ready to say, “We’re restructuring, not just renewing.” That extra half hour of planning might be the difference between keeping—or quietly leaving on the table—a five‑figure check this year.

Learn More

- Record Corn Won’t Save You: The $100K Margin Hit Coming for Mid-Size Dairies in 2026 – This breakdown arms you with a realistic 2026 budgeting framework, exposing why dropping feed costs can’t offset falling milk prices. It delivers a “Monday morning” checklist to benchmark your true cost of production against critical survival thresholds.

- Why Dairy Markets Can’t Self-Correct Anymore: The Hidden Forces Reshaping the Dairy Industry’s Future – This analysis reveals the structural shifts moving the industry toward multi-revenue economics. It breaks down how adding beef-on-dairy or energy contracts creates a $3–$4/cwt competitive advantage, insulating your operation from the traditional boom-bust cycles that once dictated profitability.

- 5 Technologies That Will Make or Break Your Dairy Farm in 2025 – This field report exposes the “innovation gap” and delivers high-ROI tactics for genomic testing and advanced sensor adoption. It reveals how catching health issues 72 hours early and optimizing forages weekly can slash treatment costs and protect your peak milk.