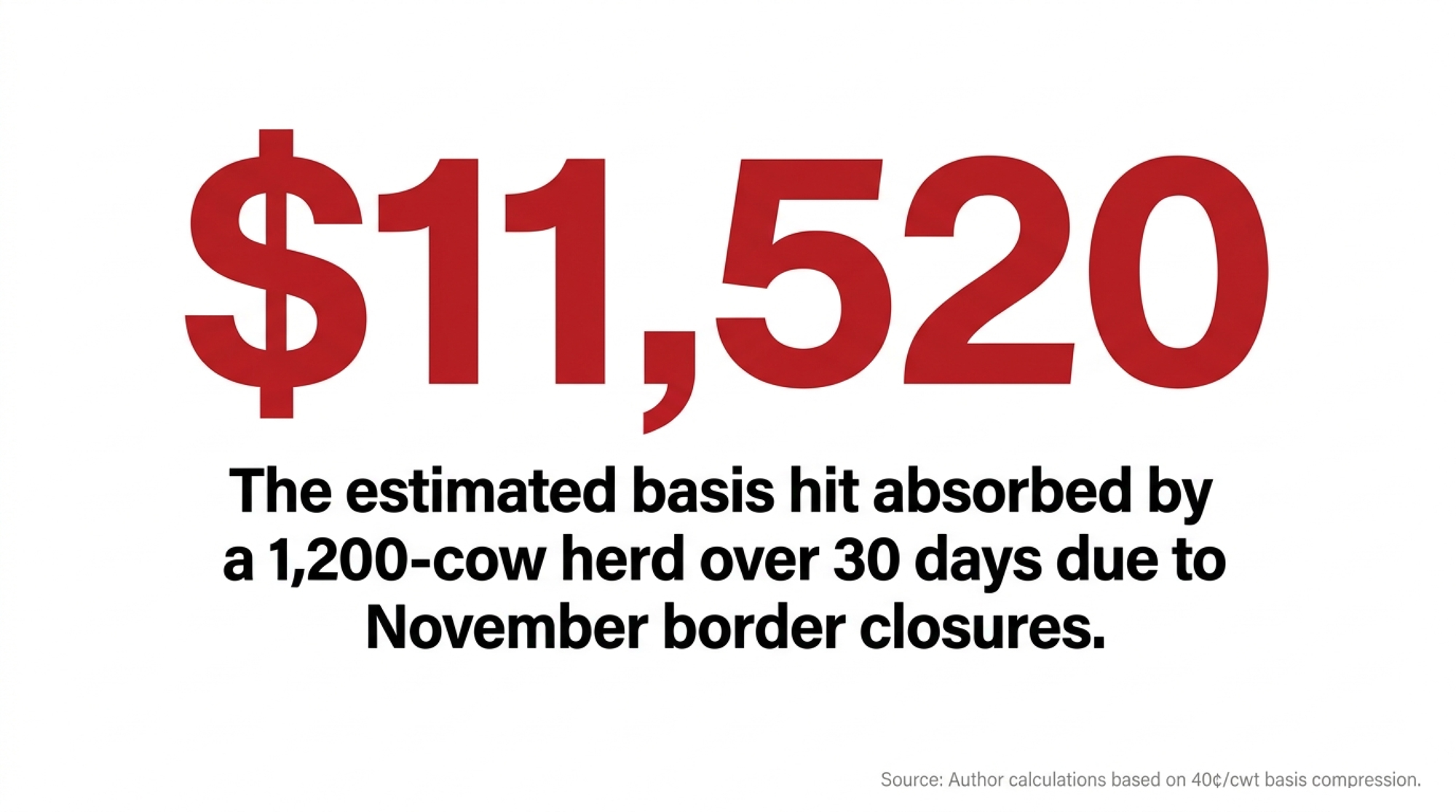

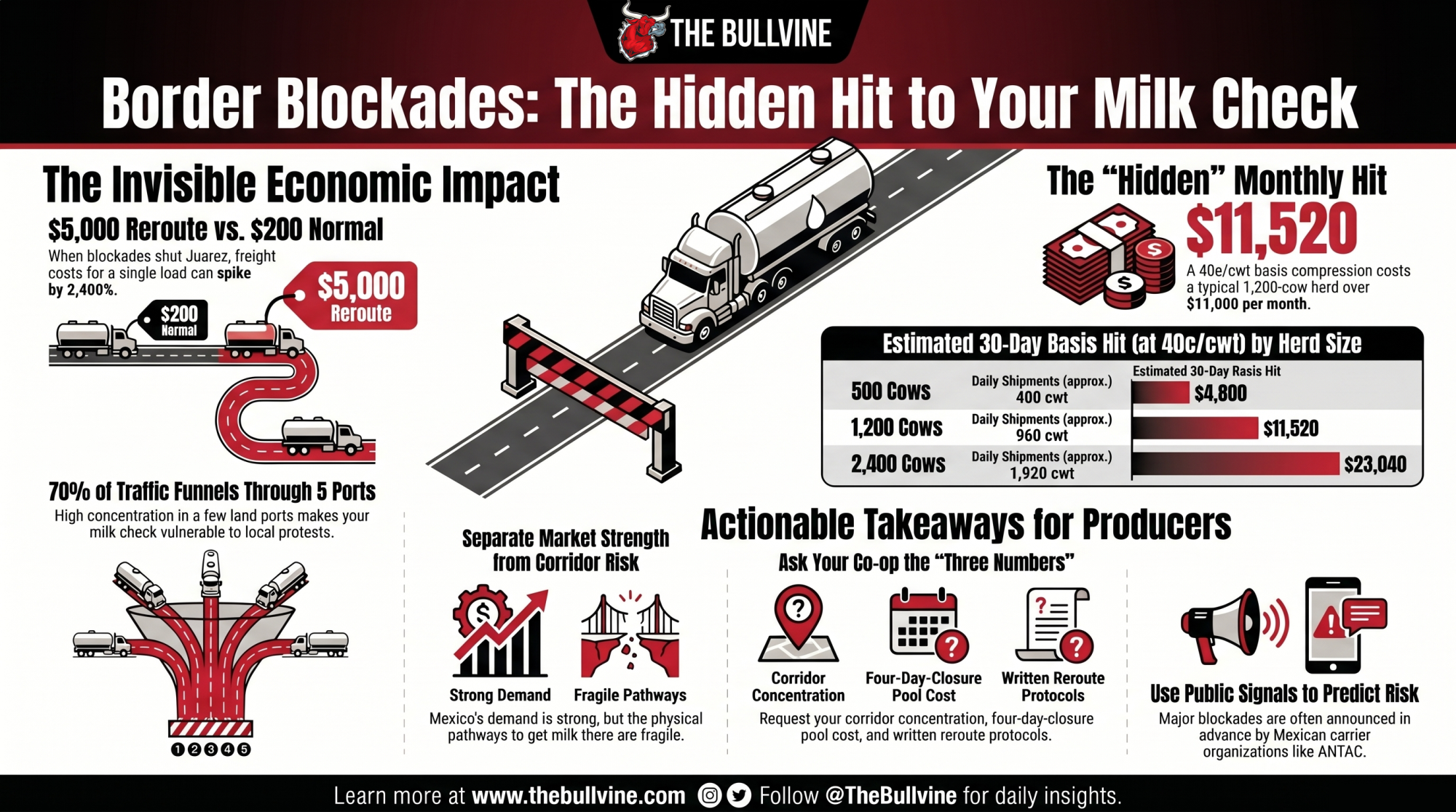

Four days of closed bridges. About $5,000 per reroute versus $200. On a 1,200-cow herd, ~40¢/cwt of compression for a month is roughly $11,520 — and your field rep can’t tell you why.

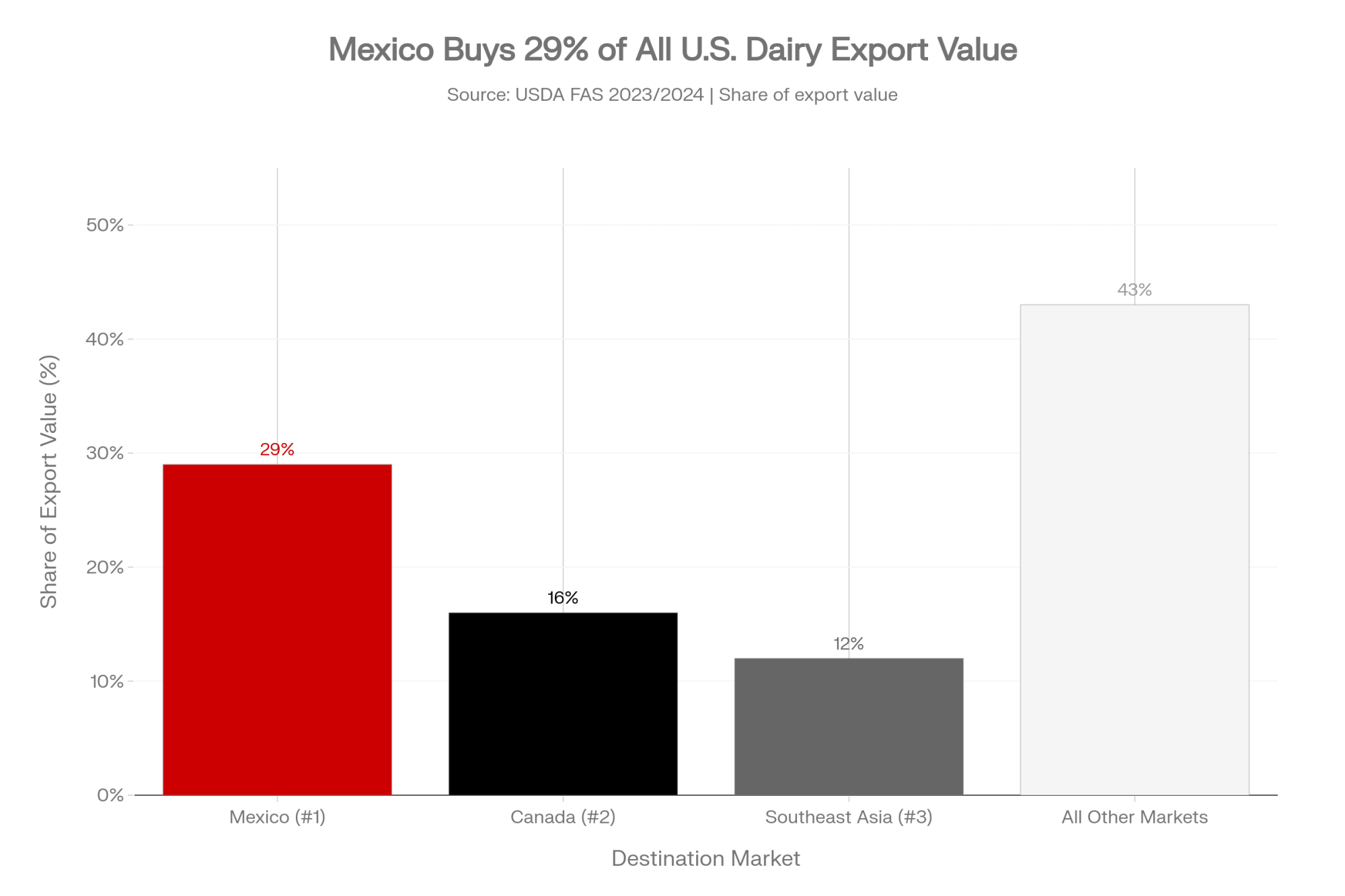

Executive Summary: Three coordinated farmer-and-trucker blockades in five months — November 24–28, December 17, and April 6–8 — shut down the Juárez–El Paso corridor that moves the highest commercial volume of any land border on earth, staging 38,000 trucks during the November round alone. Mexico now buys roughly 29% of U.S. dairy export value, about $2.32 billion in 2023 per USDA FAS, and more than 70% of that traffic funnels through five land ports. When co-op export desks rerouted through Nogales, costs jumped from $150–$200 a load to roughly $5,000 — and that compression got pooled and showed up as a soft export month, not a line item. On a 1,200-cow herd shipping 80 lbs/cow/day, a 40¢/cwt basis hit over 30 days runs about $11,520, and most producers can’t tell you whether November cost them that, double, or half. The wrinkle: December 2025 exports still finished +13% YoY, the strongest since 2022, so the aggregate headline and your co-op’s actual routing reality may be telling very different stories on the same milk check. With the USMCA review deadline July 1, 2026 and three blockade dates already announced publicly before they hit, the highest-leverage move is asking your co-op — this week — what percentage of your Mexico volume runs through Juárez and what a four-day closure costs the pool. If the field rep can’t answer, that’s the answer.

By the time Manuel Sotelo spoke to El Paso reporters during the November 24–28, 2025 closure, the standard freight workarounds had stopped working.

Sotelo serves as vice president of the Mexican Chamber of Cargo Transportation for Northern Mexico, the trade association representing northern Mexican freight carriers. According to the Chamber’s public materials, he’s logged roughly two decades in cross-border logistics across the Juárez–El Paso corridor — the highest-volume commercial land border on earth.

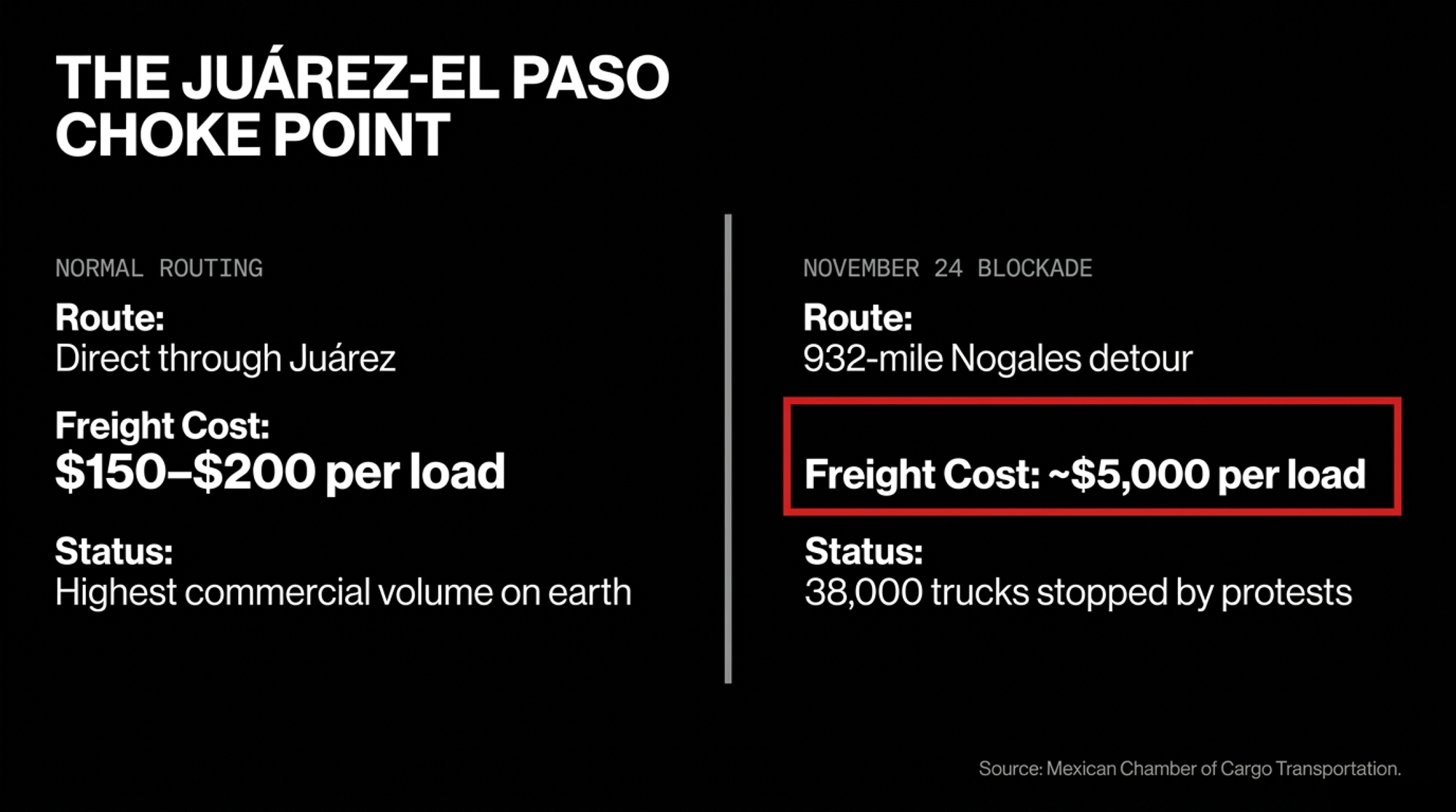

“There was no possibility on Tuesday or Wednesday to cross anything,” he told KFOX/ABC-7 in El Paso during the closure. The Ysleta–Zaragoza bridge: closed. The Córdova–Las Américas bridge: closed after protesters broke into the customs facility. The Colombia bridge to the north: barely functional. An estimated 38,000 trucks were staged at the Juárez–El Paso crossing alone — not delayed, not rerouted, but stopped. Nogales and Nuevo Laredo had already absorbed the overflow and hit their own ceilings. Gas stations across the Juárez region began running dry because the region itself couldn’t receive product from the south.

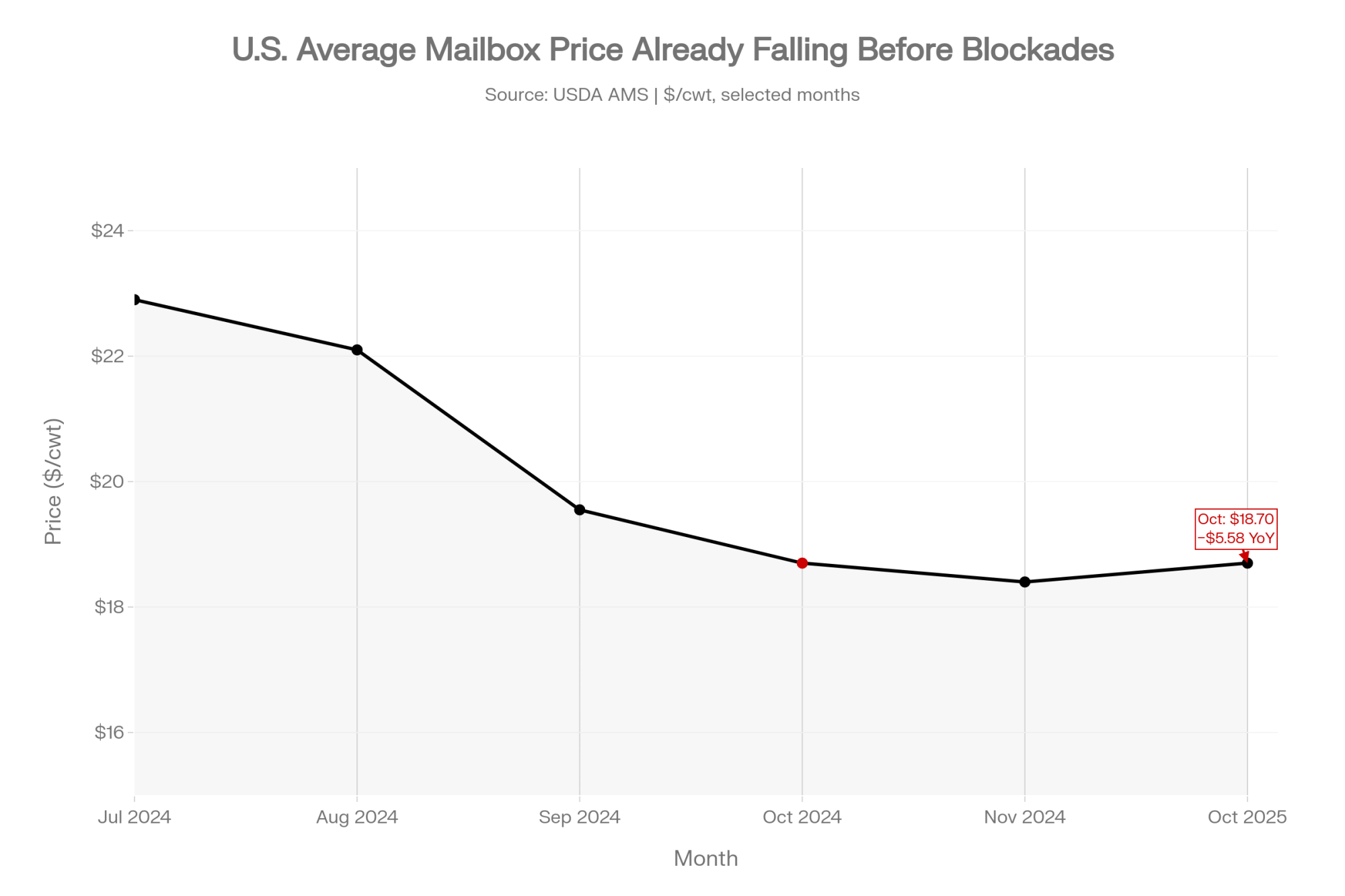

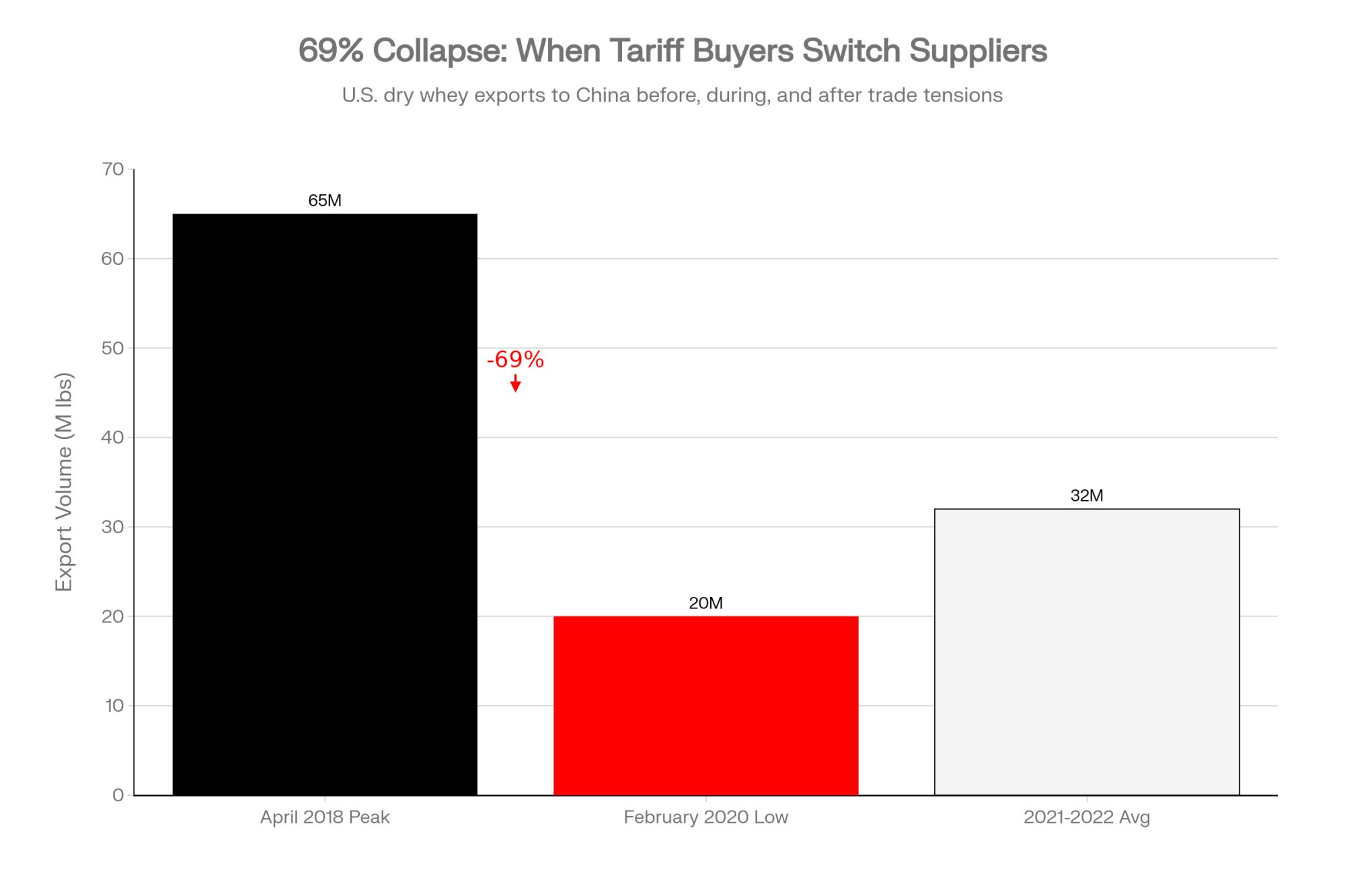

Six hundred miles north, in dairy country across the Upper Midwest and California, you were probably reading milk statements that didn’t quite reconcile. October’s U.S. average mailbox price had already dropped 85 cents in a single month to $18.70/cwt — $5.58 below the same month a year prior, according to USDA AMS. Then November and December came and went. For most producers, no one from the co-op called to explain what role the corridor closures played in the basis you’d just absorbed.

That gap — between what Sotelo’s industry was managing in real time and what generally surfaced on producer milk checks weeks later — is the part of this story that hasn’t been written yet. It’s also the part that matters most for what happens next.

The Blockade That Wasn’t a One-Off

The November 2025 mobilization didn’t surprise the organizations that launched it. The National Front for the Rescue of Mexican Farmland (FNRCM) and the National Association of Carriers (ANTAC) had been escalating since October, when a wave of highway closures across 17 Mexican states forced the federal government to the table. Mexico City offered a 25% increase in corn payments and a 950 peso per tonne subsidy. FNRCM said it wasn’t enough. They were demanding 7,200 pesos per tonne for white corn while receiving 5,050 to 5,200.

By the time the November 24 mobilization hit, 29 separate blockade sites were active across 25 states. The Confederation of National Chambers of Commerce, Services and Tourism (Concanaco-Servytur) estimated accumulated losses of 3 to 6 billion pesos — roughly $150 to $300 million USD at prevailing exchange rates — by day four. The National Confederation of Mexican Transporters (Conatram) pegged daily losses in excess of 100 million pesos, around $5 million USD, in fuel waste and contractual penalties alone. The first product to run short on shelves in northern Mexico wasn’t electronics or auto parts. It was dairy.

Here’s why that matters to anyone shipping into a co-op with Mexico exposure. Mexico has grown to roughly 29% of all U.S. dairy product export value, according to USDA Foreign Agricultural Service data through 2024 — making it the single largest customer by a wide margin. In 2023, Mexico imported roughly $2.32 billion in U.S. dairy products. Volume reached 1.38 billion pounds on a milk-solids basis, up 42% over the prior decade.

But more than 70% of that commercial traffic crosses through five land ports. The Juárez–El Paso cluster — Ysleta, Córdova, and Zaragoza — handles the highest commercial throughput of any land border crossing on earth. Organized groups proved in November that they can close it in hours.

What Your Co-op Was Doing While You Watched the News

The co-op export desk knew what was happening in real time. When C.H. Robinson — one of the largest freight brokers in North America — issued an emergency client advisory on the morning of November 24, the operative guidance came down to this: monitor local traffic authorities for resolution updates. That isn’t evasion. It’s the honest ceiling of what professional logistics infrastructure can offer when public protests are negotiating directly with their own federal government over corn prices.

What the export desks did next was rational, and largely invisible to producers. They rerouted loads through Nogales — 466 miles in one direction on the Mexican side, 466 miles back on the U.S. side, to reach the same El Paso destination. Sotelo’s company made that move. “It cost us over 100,000 Mexican pesos per shipment,” he told KVIA in December. That’s roughly $5,000 per load versus $150 to $200 through Juárez. Some product moved through domestic spot channels at prices nobody had modeled. Some sat in staging. The export premium that Mexico-market volume supports began compressing.

That compression settled into pool pricing, got averaged across member volume, and eventually appeared on milk statements as softer export conditions. Picture what that meant on the ground at three operation scales:

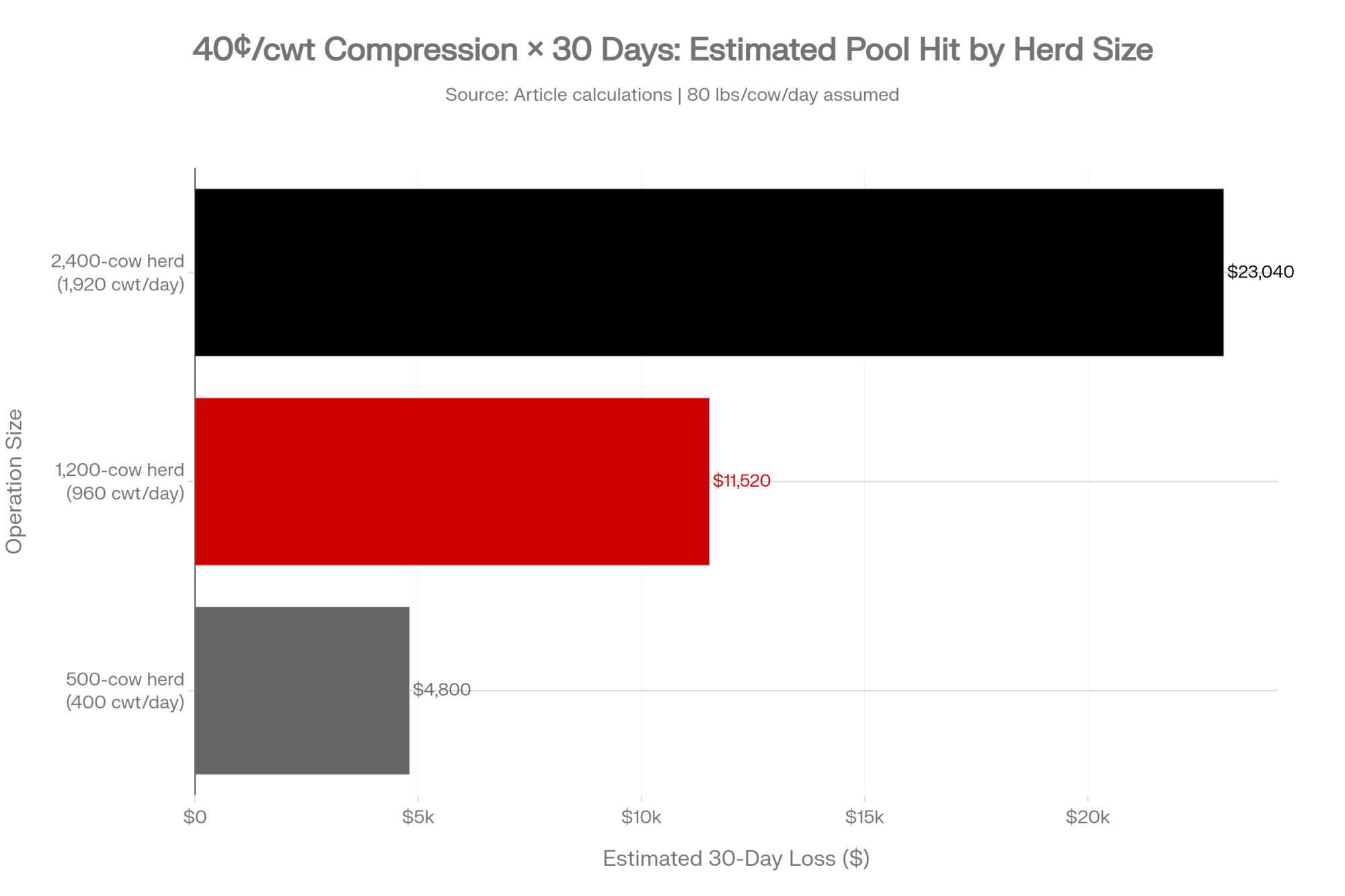

- On a 500-cow operation shipping 400 cwt per day (roughly 80 lbs/cow/day), a 40 cent/cwt basis compression over 30 days works out to roughly $4,800 — about a month of one full-time labor cost.

- On a 1,200-cow operation shipping 960 cwt per day (same per-cow assumption): roughly $11,520.

- On a 2,400-cow operation: approximately $23,040.

Those figures are illustrative. Actual basis impact depends on your co-op’s specific Mexico exposure and routing. But the pattern is the point. Every operation shipping into a co-op with meaningful Mexico volume absorbed something in November and December. Most producers couldn’t tell you how much, because the information needed to calculate it lives inside co-op logistics departments — not in producer communications.

Why the Field Rep Didn’t Have Your Answer

A co-op’s pooling structure protects you from single-market volatility. It also obscures the specific source of disruption when something goes wrong. When the export desk absorbs rerouting costs and spot-channel discounts, those losses get averaged across total pool volume. They don’t appear on a milk statement as: the Juárez corridor was closed for four days and cost you X cents per cwt. They appear as a soft export month.

The field rep isn’t withholding information. They’re communicating at the resolution the system produces. Their training covers milk pricing, component premiums, and program updates — not cross-border freight logistics or corridor risk stratification by port of entry. That gap was never a problem when disruptions to the Mexico corridor were short and infrequent.

Because co-ops blend these logistics costs directly into pool pricing, isolating the exact pennies lost per hundredweight remains nearly impossible from the outside looking in. It requires a level of corridor-specific disclosure that isn’t currently standard practice in producer communications — but should be.

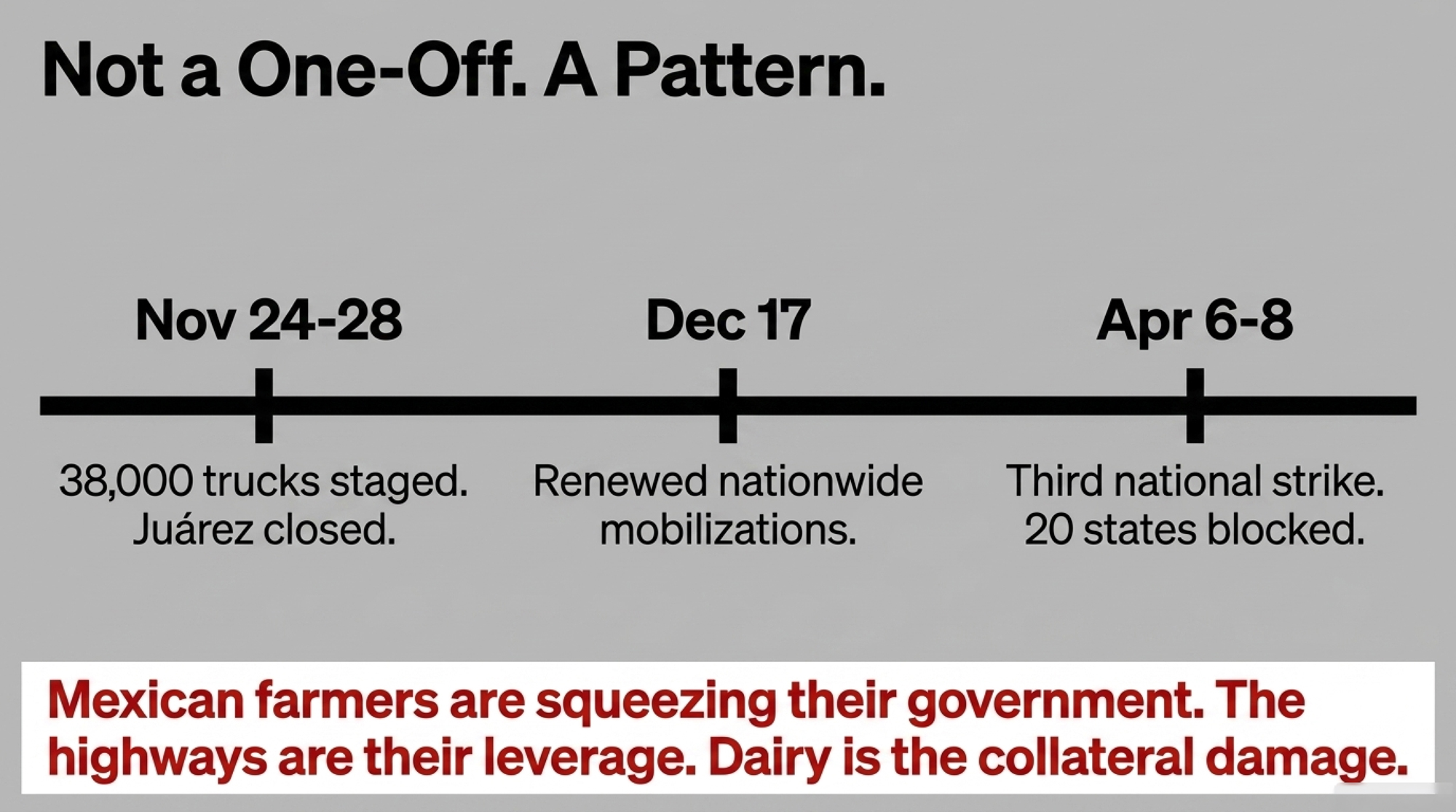

That changed in November. And the resolution wasn’t a resolution. When Interior Minister Rosa Icela Rodríguez announced the November deal on day four, Mexican media reported FNRCM and ANTAC framing the agreement as a truce rather than a settlement. The pattern that followed proved that framing accurate:

- December 17, 2025: Renewed nationwide mobilizations launched by FNRCM and freight transport organizations. December 18 negotiations produced another truce — government commitments on highway security, escort programs, and a roadmap for price-support mechanisms (pignoración) for corn, beans, sorghum, wheat, barley, and soy. Sotelo’s December warning about the limits of contingency planning came in the middle of this round.

- April 6–8, 2026: A third nationwide strike led by the National Transport Association (ANT) and FNRCM blocked routes in at least 20 states, including Mexico–Querétaro, Mexico–Puebla, the Culiacán–Mazatlán corridor, and access routes to Tijuana, Mexicali, and Ciudad Juárez. Protesters cited cargo crime, soaring diesel costs from Strait of Hormuz disruption, and stagnant grain prices.

| Blockade Event | Dates | Lead Organizations | Primary Trigger | Juárez Corridor Status | Estimated Economic Loss |

|---|---|---|---|---|---|

| Mobilization #1 | Nov 24–28, 2025 | FNRCM, ANTAC | Corn price (demand: 7,200 vs. 5,050–5,200 MXN/tonne) | Fully closed — Ysleta, Córdova, Zaragoza bridges shut | 3–6 billion MXN (~$150–$300M USD) |

| Mobilization #2 | Dec 17–18, 2025 | FNRCM, freight orgs | Nov truce violations; price-support commitments unmet | Partial closure — routes disrupted nationwide | 100M+ MXN/day (~$5M USD/day) in fuel waste & penalties |

| Mobilization #3 | Apr 6–8, 2026 | ANT, FNRCM | Cargo crime + diesel costs (Hormuz) + stagnant grain prices | Partial closure — 20+ states, Juárez access routes blocked | Not yet formally estimated |

| All Three Events | 5-month window | Multiple national coalitions | Structural: water law, grain prices, cargo security, fuel costs | Pattern established— corridors closed on avg every ~6 weeks | ~$11,520 est. basis hit on a 1,200-cow herd over 30 days |

Three coordinated, politically-driven national mobilizations in five months. The pattern is established.

The structural drivers aren’t going away. Mexico’s new General Water Law removed the ability for agricultural users to transfer water concessions during land sales and granted CONAGUA broad discretionary authority to reduce existing water volumes during drought. Farmers describe the change as an existential threat to long-term land values and credit access. Cargo theft on Mexican federal highways has remained a persistent operational risk over recent years according to publicly reported industry tracking, and now diesel cost pressure from Middle East disruption compounds the squeeze. Corn prices remain well below break-even demands. The pressure for future mobilizations is intact.

If the highways close again, not just the customs facilities, Sotelo told KVIA the only fallback is air freight. “They don’t have as many planes as we do with ground transportation.” The infrastructure ceiling of the backup plan is the cargo capacity of Juárez International Airport. Against thousands of daily commercial export crossings averaging tens of thousands of dollars in value each, that ceiling closes fast.

How Much Did the November Blockade Actually Cost Your Milk Check?

The honest answer: it depends on your co-op’s Mexico exposure, and most producers haven’t been given enough information to calculate it.

Here’s what’s documented. The four-day November closure plus a roughly ten-day recovery backlog created about two weeks of compressed export throughput for co-ops routing significant volume through Juárez. During that window, loads moved at reroute cost or spot-channel discount. Those costs got pooled. October’s mailbox had already dropped 85 cents in a single month to $18.70/cwt — $5.58 below October 2024. September had been $19.55, $5.23 below the prior year. The November and December disruptions hit inside an already-deteriorating pricing environment, which is part of why their specific contribution is hard to isolate from your vantage point.

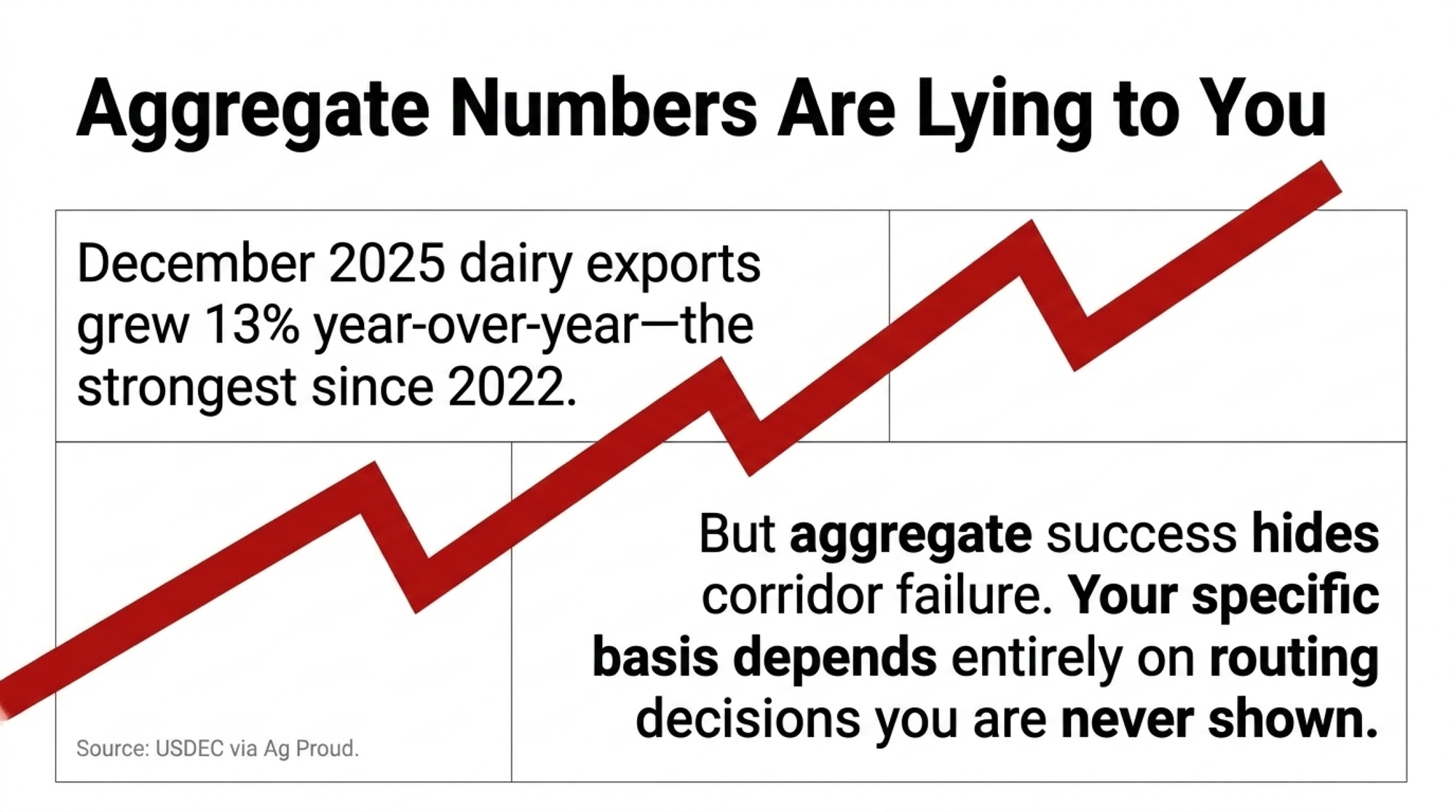

And here’s the wrinkle that complicates everything. Year-end U.S. dairy export volumes actually finished strong — December 2025 dairy product exports grew 13% year-over-year, reaching levels not seen since 2022, according to USDEC via Ag Proud. The aggregate story was good. The corridor-specific story was something else. Whether your co-op’s December basis reflected the strong aggregate or the disrupted corridor depends on routing decisions you almost certainly weren’t shown.

That’s the gap. Not a cover-up. A structural mismatch between where the information lives and who needs it.

Is Your Co-op’s Mexico Program Built for the Risk Environment That Actually Exists Now?

The USMCA review deadline arrives July 1, 2026 — 39 days from this writing. Mexican farm organizations have explicitly stated they want basic grains removed from the agreement. U.S. dairy groups want stronger market access enforcement. The December 18 government settlement with FNRCM included the creation of a formal institutional channel under Mexico’s Ministry of Economy specifically to analyze USMCA-related issues from the Mexican producer side.

Whatever the review produces, it won’t create an obligation for Mexican bridges to stay open during domestic protests. That gap — between what a trade agreement governs and what actually controls your load’s ability to move — exists regardless of the review outcome.

The co-ops best positioned for the next disruption aren’t necessarily the ones with the strongest Mexico buyer relationships. They’re the ones that have pre-negotiated reroute capacity at Nogales and Nuevo Laredo, modeled corridor-specific exposure for their member base, and have a communication protocol ready before the next mobilization date circulates — not after the bridges close. Those aren’t complex systems. They’re the difference between managing an event and being surprised by it.

For broader context on how trade policy is reshaping the export environment, see how the broader trade war is reshaping dairy export economics.

Options and Trade-Offs for Producers

The goal here isn’t alarm. It’s calibration. A few practical paths worth considering now:

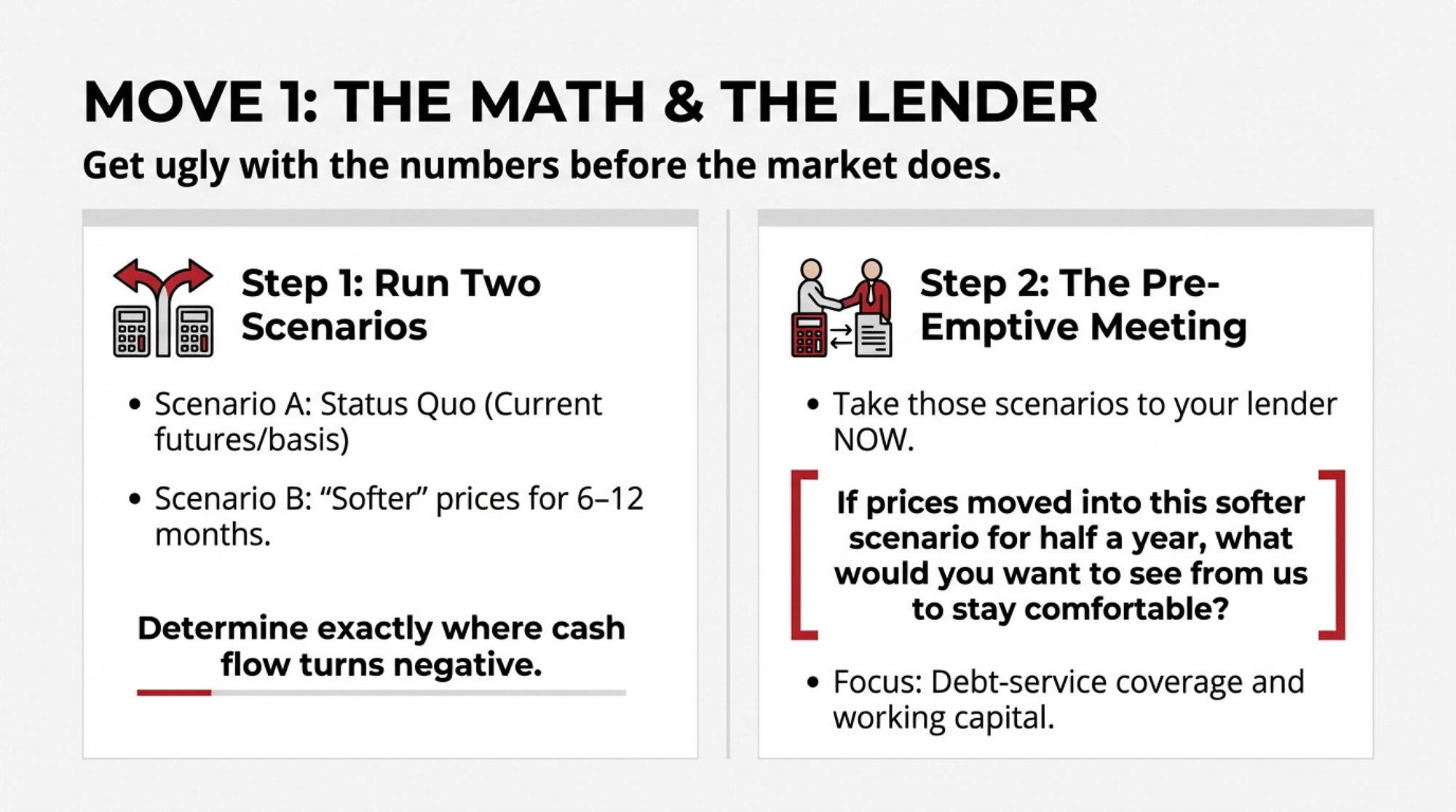

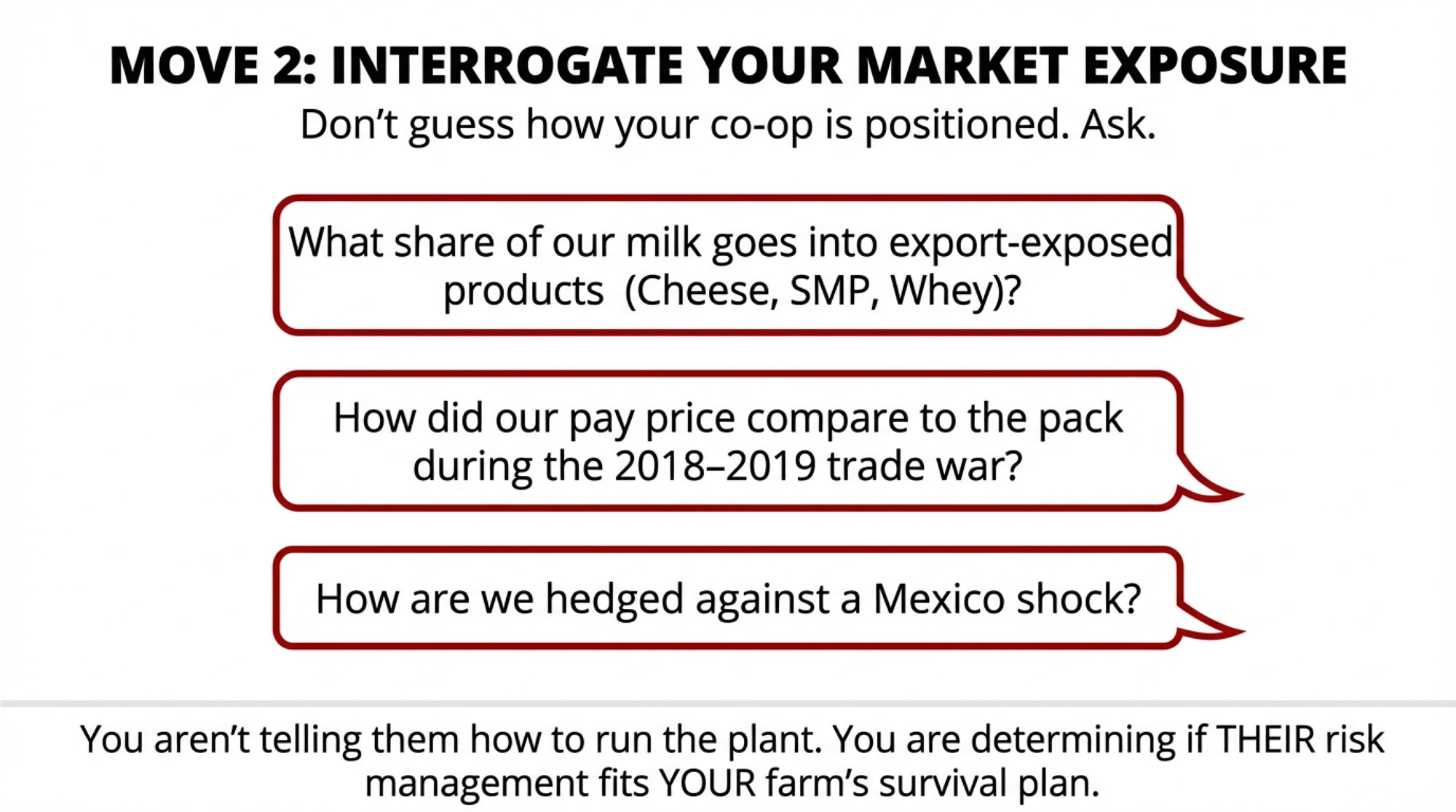

1. Ask your co-op for corridor-specific exposure information — within 30 days. Your co-op’s export desk knows which crossings carry the majority of your Mexico-bound volume. Asking for that breakdown, even a rough percentage by corridor, is a legitimate member inquiry. You don’t need their full routing database. You need enough to understand whether a four-day Juárez closure is a minor inconvenience or a real basis risk for your operation. If the field rep can’t answer, ask them to escalate.

When it makes sense: Any operation whose co-op does meaningful Mexico export volume. What it requires: A direct, polite ask — email is fine. Key limit: Co-ops vary in how they handle governance-level member inquiries. Some have this conversation readily. Others route you through layers before anyone with the data responds. The response itself often tells you something useful about the institution.

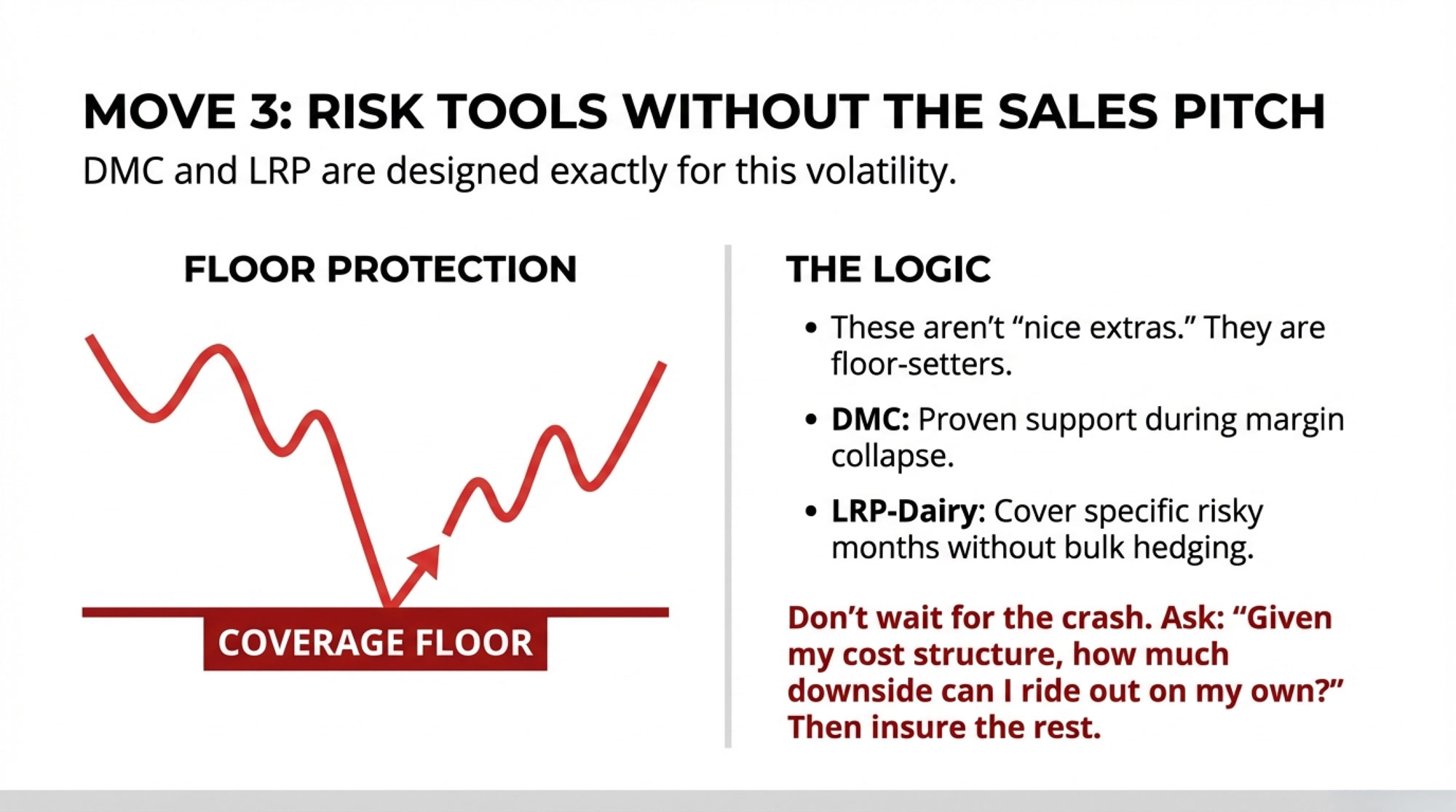

2. Separate “market reliability” from “corridor reliability” in your risk thinking. These are different things, and the industry has communicated them as one. Mexico as a dairy market is genuinely strong — demand fundamentals, volume, and buyer relationships are real. But Mexico as a logistics corridor runs through infrastructure that organized domestic groups have demonstrated they can close in hours. Building both into your mental model doesn’t mean abandoning the export program. It means hedging differently. If you’re scenario-planning for milk price downside, add a 30-day corridor disruption scenario alongside your standard price sensitivity analysis.

When it makes sense: Larger operations where basis variance moves real dollars. What it requires: About 30 minutes with your accountant or risk manager. Key limit: Without corridor-specific exposure data from your co-op, you’re estimating. An estimate still beats nothing.

3. Track ANTAC, ANT, and FNRCM mobilization signals — they announce dates publicly. All three organizations communicated their dates in advance. The November 24 date circulated for weeks. The December 17 date was set within days of the November truce. The April 6 mobilization was announced openly. A Google Alert on “ANTAC blockade,” “FNRCM huelga,” or “Mexico carriers strike” gives you more lead time than most co-op communications currently provide. That lead time isn’t a trading signal. It’s context for timing decisions about forward sales and export-dependent premium months.

When it makes sense: Any producer who wants a more complete picture of export risk. What it requires: Five minutes of setup. Key limit: Knowing a date is circulating doesn’t tell you whether it’ll escalate to full closure. That depends on whether the Mexican government makes meaningful concessions in the interim.

4. If you sit on a co-op board or advisory committee, bring the governance question. The three numbers every producer with Mexico export exposure should have access to — percentage of volume through each corridor, estimated cost of a four-day closure to the pool, and the written reroute protocol — aren’t proprietary. They’re basic operational transparency. With the USMCA review deadline arriving July 1, the timing for raising those questions formally is now.

When it makes sense: Anyone with governance-level standing in their co-op. What it requires: A written request before the next board or delegate meeting. Key limit: Some boards receive this kind of question as constructive. Others read it as a confidence challenge. Knowing which culture you’re in is its own useful data.

Key Takeaways

- If your co-op exports to Mexico and you haven’t asked which crossings carry your volume, send the email this week. That’s the single highest-leverage move available before July 1.

- If your risk model treats market access and corridor access as one thing, fix it. They’ve been communicated as one. They aren’t.

- If the next mobilization date is circulating in Mexican press and your co-op hasn’t flagged it, your information lag is the problem worth solving. ANTAC, ANT, and FNRCM announce publicly. Google Alerts close the gap.

- If you sit on a board or advisory committee, ask the three numbers before the next meeting. Corridor concentration, four-day-closure pool cost, written reroute protocol. None are proprietary.

- If the strong aggregate export number is reassuring you past the corridor question, you’re reading the wrong signal. The headline figure and your co-op’s routing reality can tell different stories on the same milk check.

The question isn’t whether your co-op’s Mexico relationship is valuable. It is, and the export numbers support that — December 2025 closed with the strongest year-over-year export growth since 2022. The question is whether the risk picture you’ve been given matches the risk you’re actually carrying. For most producers, those two pictures haven’t been the same since November 24.

Worth knowing before the next date circulates.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Surviving the $0.94/cwt Dairy Make Allowance Hit – The Bullvine — Arms you with a blueprint to reconcile state-announced milk prices against your actual statement. Exposes how a fixed multi-dollar deduction permanently suppresses Class III and Class IV minimum regulated values.

- Decode Mexico’s Dairy Protectionism: Your Export Strategy Survival Guide | The Bullvine — Delivers an essential strategic forecast on how regional water scarcity and aggressive multi-billion-dollar domestic subsidies reshape commodity demand. Explains the structural trade realities you must navigate over the next 3–5 years.

- The 400-Cow Margin Trap: When $14.59 Milk Bleeds $425K in 2026 – The Bullvine — Dismantles the danger of anchoring capital budgets to volatile monthly government estimates. Reveals a strict 90-day action plan to insulate your operational margins from severe cash-flow whiplash and equity erosion.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Join the Revolution!

Join the Revolution!