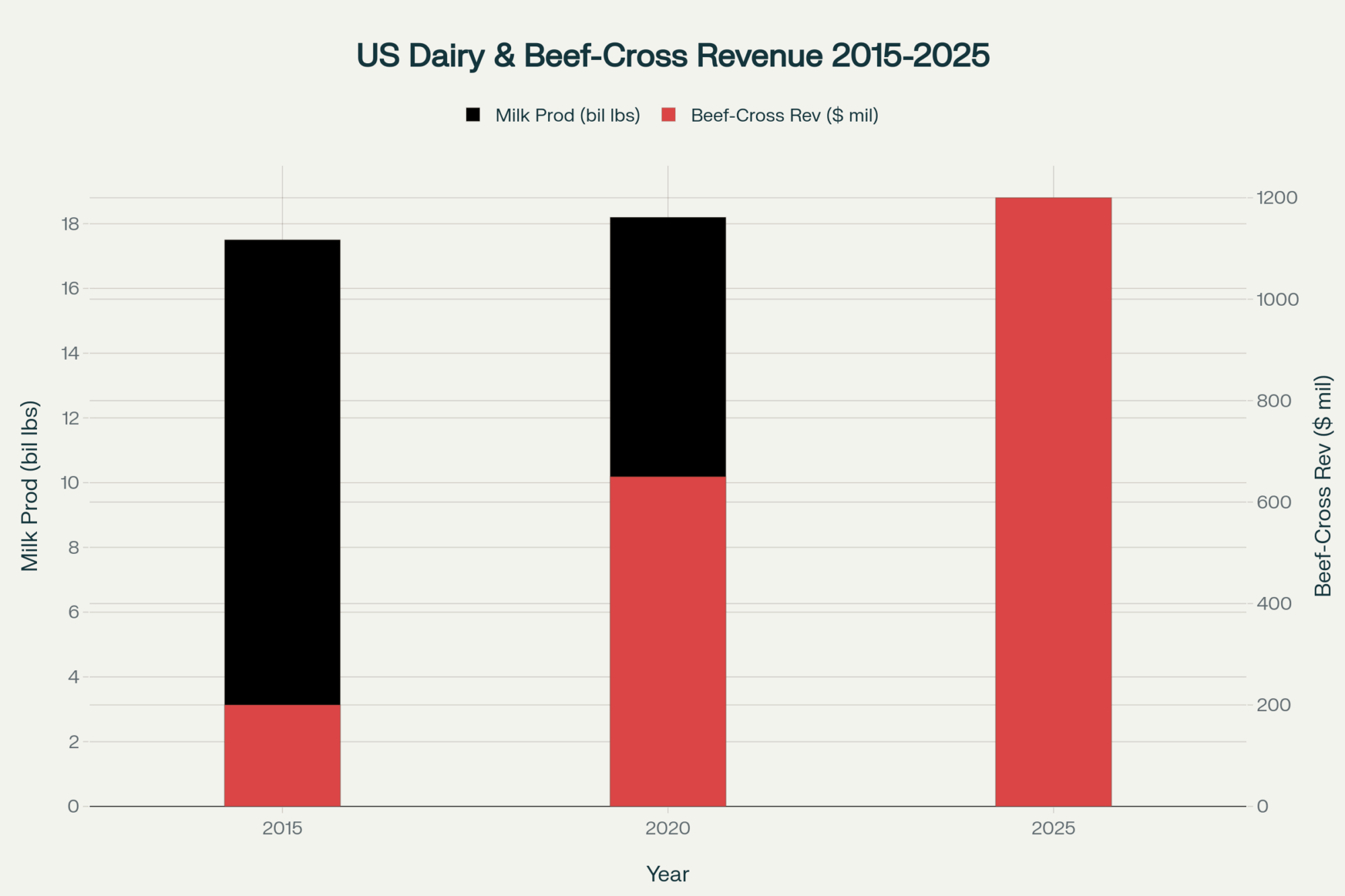

What happens when processors start paying farmers NOT to produce milk? We’re finding out right now

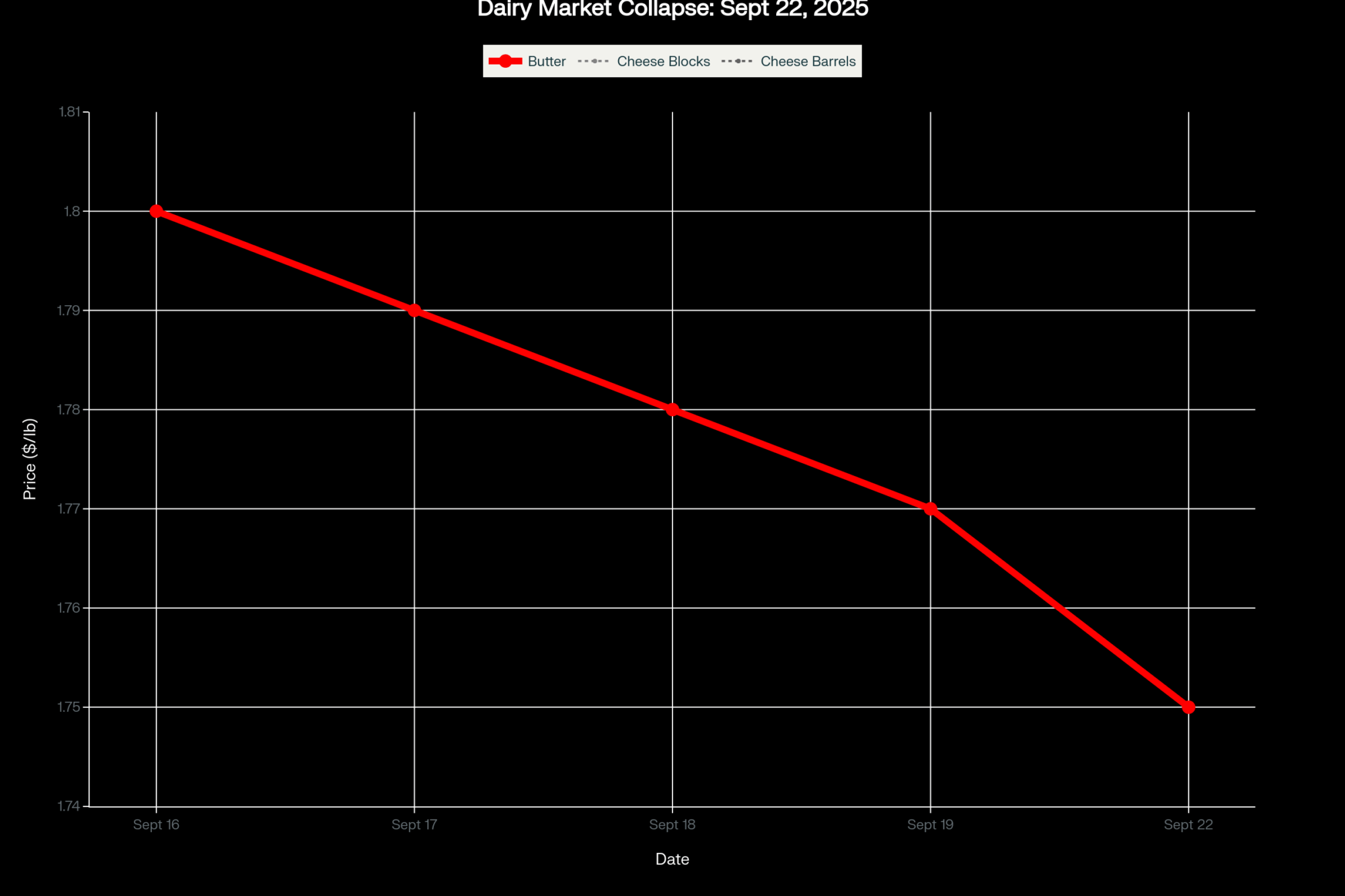

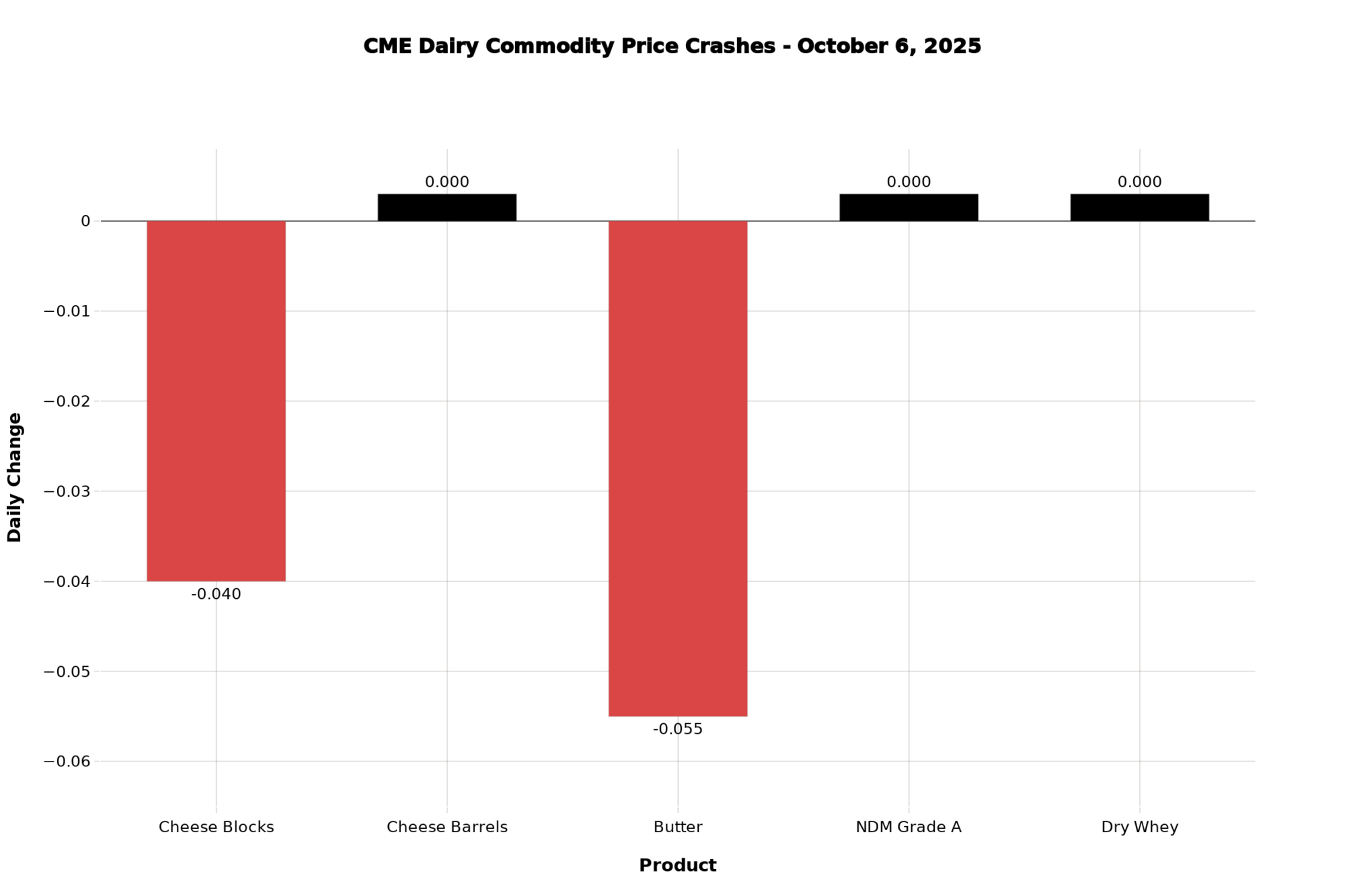

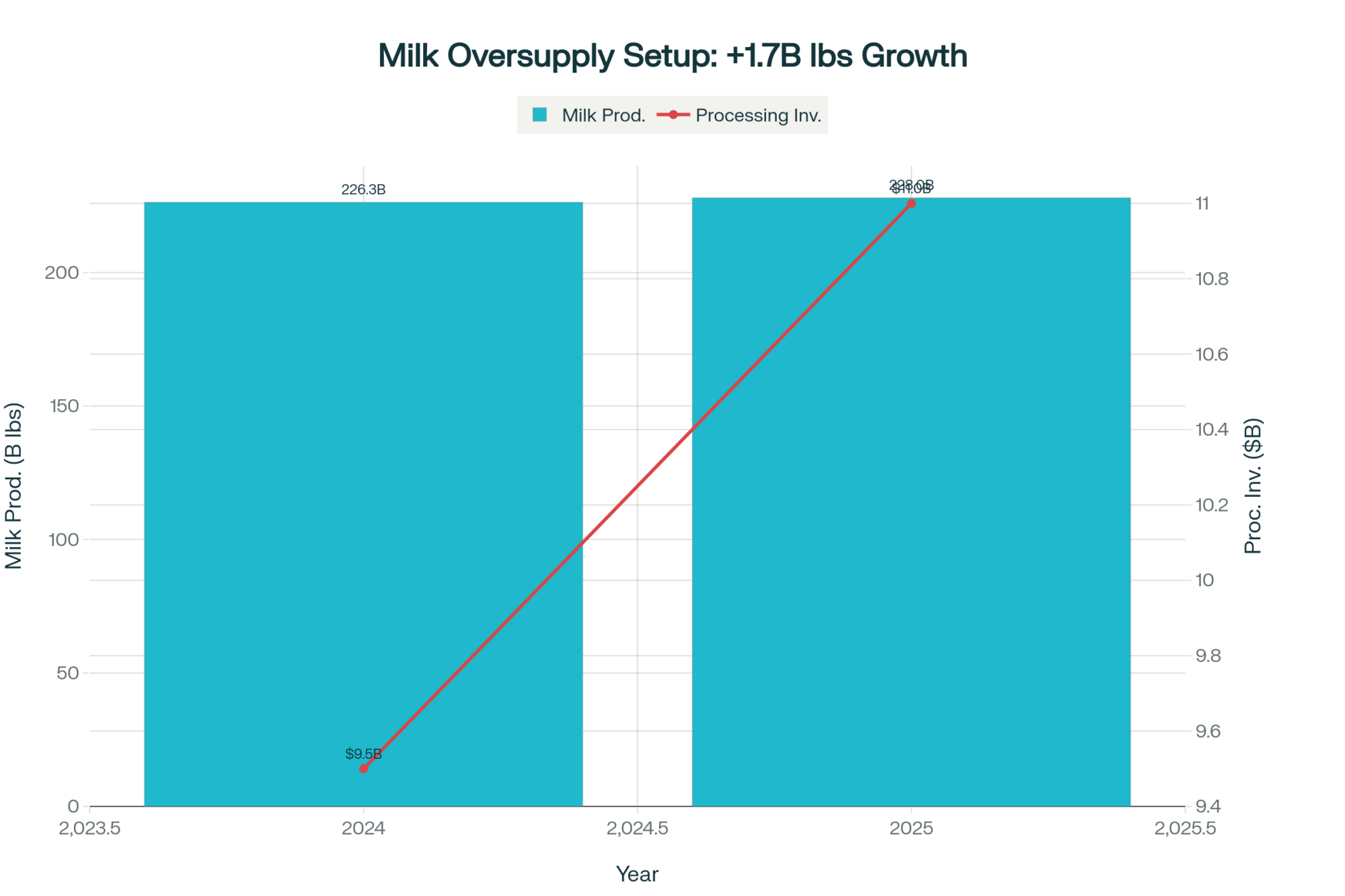

EXECUTIVE SUMMARY: Today’s CME action revealed what many producers have been suspecting—the September rally was built on hope rather than fundamentals, with cheese blocks plummeting 4 cents to $1.75/lb and butter crashing 5.5 cents to $1.6950/lb. These aren’t just numbers on a screen… they translate directly to a 60-80¢/cwt reduction in Class III milk value, hitting October checks hard when margins are already tight. Recent Cornell research shows that top-performing farms maintain profitability through effective feed management and component optimization, spending 3.1% less on purchased feed while achieving higher production—a strategy that’s becoming increasingly essential as milk-to-feed ratios drop to 2.35 from August’s 2.51. With 228 billion pounds of milk forecast for 2025 (up from 226.3 billion in 2024), and the addition of new processing capacity that will invest $11 billion, we’re seeing classic oversupply dynamics that historically take 12-18 months to rebalance. Looking ahead, successful operations are focusing on three proven approaches: locking in Q4 hedges while October $17 puts remain available, maximizing Dairy Margin Coverage enrollment before the October 31 deadline, and shifting focus from volume to component quality—strategies that separate operations that thrive from those merely surviving. What farmers are discovering through this volatility is that waiting for markets to normalize isn’t a strategy… it’s choosing which proven risk management tools fit their operation’s specific needs and regional realities.

Well, here we go again. After watching September’s rally fizzle out like a Fourth of July sparkler in the rain, today’s cheese market finally admitted what we’ve been seeing in production reports for weeks – there’s simply too much milk chasing too few buyers at these price levels. Looking at today’s CME action, your October milk check just got lighter, and that’s putting it mildly.

The Numbers Tell a Brutal Story

Let me walk you through what happened on the trading floor today, and the implications are stark for anyone long on cheese:

Product

Price

Today’s Move

Weekly Average

What This Actually Means

Cheese Blocks

$1.7500/lb

-4.00¢

Down to $1.75 from $1.79

Class III drops 60-80¢/cwt

Cheese Barrels

$1.7700/lb

No change

Holding at $1.77

Barrels are steady, but can’t prop up the market

Butter

$1.6950/lb

-5.50¢

Crashed from $1.75

Butterfat premiums evaporating

NDM Grade A

$1.1600/lb

No change

Steady at $1.16

Powder markets holding

Dry Whey

$0.6300/lb

No change

Slight weekly decline

Protein values are stable but trending softer

CME Dairy Commodity Price Crashes – October 6, 2025: Cheese blocks plummet 4¢ and butter crashes 5.5¢ in brutal trading session that signals fundamental market reset.

What’s particularly telling is how these moves played out. Seven block trades executed today, each one printing lower than the last – that’s not profit-taking, folks, that’s capitulation. When I see sellers outnumbering buyers 3-to-1 on butter (7 offers versus two bids), it reminds me of what a Wisconsin cheese plant manager told me last week: “We’re offering quality premiums just to slow down milk deliveries. That’s code for ‘please stop sending us so much milk.'”

The Trading Floor Speaks Volumes

You know, I’ve been watching these markets for decades, and certain patterns just scream trouble. Today’s bid-ask spreads told the whole story. Zero bids on cheese blocks against three offers? That’s what we call a “no bid” market – nobody wants to catch this falling knife.

One CME floor trader I spoke with said it best: “Haven’t seen butter take a beating like this since 2019. The funds are liquidating, and there’s no commercial support underneath.” When the smart money’s heading for the exits and processors aren’t stepping up to buy, you know we’re in for more pain.

The complete absence of barrel trading while blocks are getting crushed? That disconnect usually means one thing – processors are sitting on inventory they can’t move. And when processors can’t move cheese, dairy farmers feel it first and worst.

Where We Stand Globally

Examining the international landscape, the picture becomes even more complex. According to European futures data, their SMP (skim milk powder) is trading at €2,175/MT for October, which converts to roughly $1.05/lb, keeping them competitive with our NDM at $1.16. Meanwhile, New Zealand’s aggressive positioning shows their whole milk powder at $3,645/MT and SMP at $2,600/MT.

Ben Laine, senior dairy analyst at Terrain, recently noted that “the distinction between successful and challenging years for milk prices often hinges on exports”. Currently, with the dollar strong and our competitors being aggressive, that’s not working in our favor. The Kiwis are essentially putting a ceiling on where our powder prices can go, while the EU, despite dealing with environmental regulations and disease pressures, remains competitive.

Feed Costs: The Squeeze Gets Tighter

Here’s where the margin pressure really starts to bite. December corn futures closed at $4.6125/bushel today, up from $4.19 last week. Soybean meal is sitting at $277.10/ton. For those keeping score, that milk-to-feed ratio we all watch? According to the latest Dairy Margin Coverage data, it’s dropped to about 2.35 from 2.51 in August.

What farmers are finding is that income over feed costs (IOFC) for average operations is dropping toward $8.50/cwt. If you’re running efficiently, you may be holding at $9.50. However, I know many producers, especially those dealing with drought conditions out West and higher hay transportation costs, who are approaching breakeven territory.

The 2013 Cornell Dairy Farm Business Summary showed that top-performing farms spent 3.1% less on purchased feed than average farms while maintaining higher production. That efficiency gap is about to separate survivors from casualties.

Production Reality Check

The Oversupply Setup: More Milk + More Processing = Lower Prices – 1.7 billion more pounds of milk with $11B in new processing capacity creates classic oversupply dynamics that historically take 12-18 months to rebalance

USDA’s latest forecast shows 228 billion pounds of milk for 2025, up from 226.3 billion in 2024. We have 9.365 million cows and are still increasing, with production per cow up by about 3 pounds per day year-over-year. That’s a lot of milk looking for a home.

What’s really caught my attention is the regional variation. Wisconsin and Minnesota are running 2-3% above their levels from last year. New York alone has seen $2.8 billion in new processing investment, according to the International Dairy Foods Association. Even with some HPAI concerns creating pockets of disruption in California, the national picture is clear – we’re making more milk than the market wants at these prices.

One Upper Midwest producer told me yesterday, “We’re getting these ‘quality premiums’ that are really just incentives to limit production. When processors start soft-capping your volume, you know supply has gotten ahead of demand.”

What’s Really Driving These Price Drops

Let’s be honest about domestic demand. According to recent Nielsen IQ data, retail cheese prices, ranging from $3.49 to $4.39 per pound/pound have finally reached the consumer’s price ceiling. Food service is steady but not growing fast enough to absorb the production increases we’re seeing. Supply isn’t the primary driver here – consumer behavior is. We’re producing roughly the same amount of milk year after year, but consumers aren’t keeping pace with high retail prices and export challenges.

On the export front, the situation’s equally concerning. Mexico – our biggest customer at $2.32 billion annually – is down 10% year-to-date according to USDA data. Political uncertainty and peso weakness aren’t helping. China? They’re quietly pivoting to New Zealand suppliers while dealing with their own economic challenges.

Looking Ahead: Managing Expectations

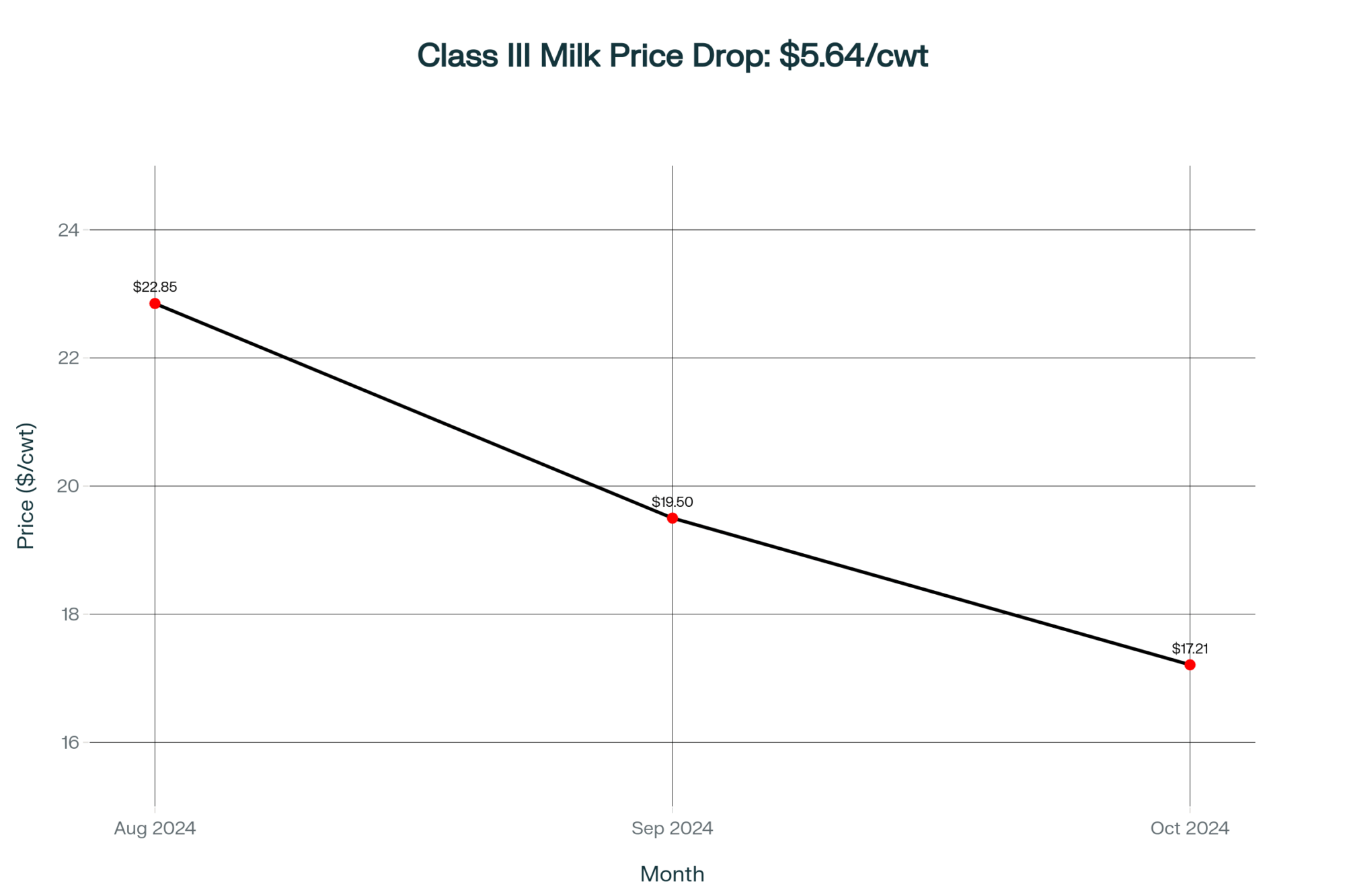

The USDA’s official forecasts for 2025 project an all-milk price of $22.00-$22.75/cwt, with Class III at $18.50. Today’s market action suggests those numbers might need serious revision. The futures market tells the real story – October Class III at $17.21/cwt and Class IV at $14.76/cwt. That’s the market voting with real money, and it’s voting bearish.

What’s interesting here is the disconnect between official optimism and market reality. December Class III is barely holding $17.00, and options implied volatility is spiking. That usually means traders expect more turbulence ahead.

What Smart Producers Are Doing Now

After talking with producers across the country and watching successful operations navigate similar cycles, here’s what makes sense:

Lock in Q4 hedges immediately. October $17.00 puts are still available at reasonable premiums. Yes, you might miss some upside, but when margins are this tight, protecting your downside isn’t optional – it’s a matter of survival.

Get serious about feed efficiency. The Cornell data show that top farms maintain profitability through effective feed management. Lock favorable grain prices if you haven’t already. With feed representing about 54% of total production costs according to Dairy Margin Coverage data, you can’t afford to let this slip.

Focus on components over volume. As one Minnesota producer recently told me, “Component quality now adds $400+ more income per cow annually compared to just pushing volume. With component prices diverging, optimizing for protein and butterfat content becomes even more critical.

Don’t forget Dairy Margin Coverage. Sign-up ends October 31. At $0.15 per hundredweight for $9.50 coverage, as USDA’s Daniel Mahoney notes, “risk protection through Dairy Margin Coverage is a cost-effective tool to manage risk¹². Don’t leave government money on the table.

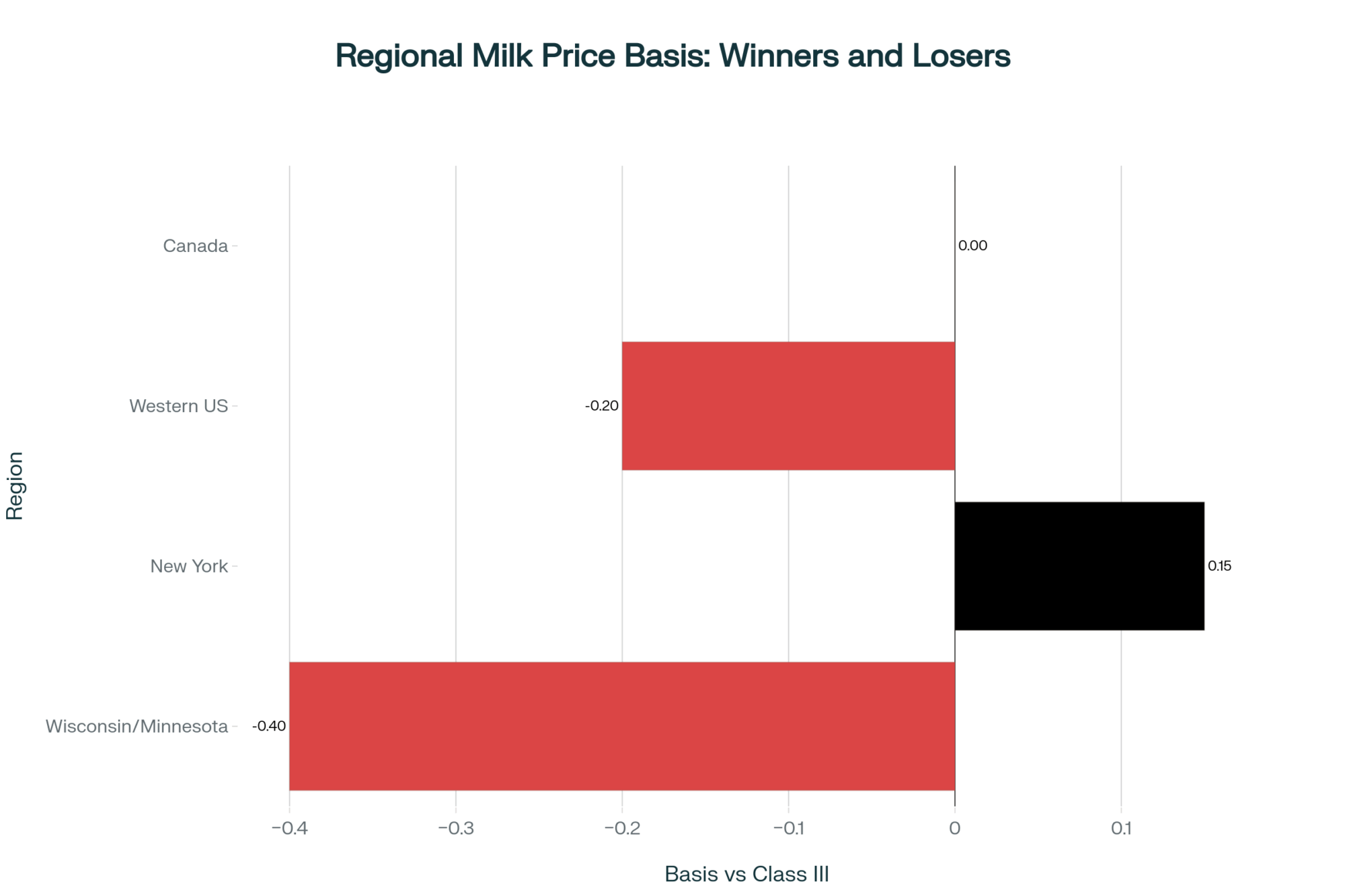

Regional Realities Matter

Regional Milk Price Basis: Winners and Losers – Wisconsin/Minnesota face -40¢ discounts while New York enjoys +15¢ premiums, proving location determines profitability in today’s fragmented market.

Wisconsin and Minnesota producers are experiencing what I call the “perfect storm” – ideal fall weather means cows are comfortable and producing heavily, but plants are at capacity. Local basis has widened to -$0.40 under class in some areas. Several smaller producers without solid contracts are really taking a hit.

Meanwhile, Western producers, who are dealing with higher hay costs and water issues, face different challenges. Canadian producers, interestingly, are seeing farmgate milk prices decrease by 0.0237% for 2025, according to the Canadian Dairy Commission; however, their supply management system provides more stability than what is currently being faced.

The Historical Context We Can’t Ignore

This reminds me eerily of the 2018-2019 period when oversupply met processor capacity expansion. That episode lasted 18 months before markets found equilibrium. Compare today’s Class III at $17.21 to October 2024, when it was $22.85/cwt. That’s a $5.64/cwt drop year-over-year – not a correction, but a fundamental reset.

Markets have a way of working themselves out. If processors are building new cheese plants and need to fill them with milk, they’ll eventually pay what it takes to get the milk in there. But that competitive market for milk? We’re not there yet.

The Bottom Line for Your Operation

Today’s market action wasn’t just another bad day – it’s a clear signal we’re entering a new phase of the dairy cycle. Your October milk check has just become lighter by at least $0.60/cwt, and November’s not looking any better. The combination of expanding production, new processing capacity, and global competition means this pressure is unlikely to subside soon.

However, here’s what decades in this business have taught me: low prices eventually lead to lower prices. The producers making smart decisions now – locking in margins where possible, controlling costs ruthlessly, focusing on efficiency over expansion – these are the ones who’ll be positioned to profit when the cycle turns.

Tomorrow, watch for follow-through selling in cheese. If blocks break $1.70, we could see accelerated selling pressure. October Class III futures expire in 10 days – position yourself accordingly.

And remember, as volatile as these markets are, the fundamentals of good dairy farming haven’t changed. Stay focused on what you can control: feed efficiency, component quality, and smart risk management. The dairy industry has always rewarded survivors, and this cycle won’t be different.

KEY TAKEAWAYS

Lock in Q4 protection immediately: October Class III futures at $17.01/cwt signal continued pressure—farms using put options at $17 strike prices can protect against further drops while maintaining upside potential if markets recover

Component quality now drives profitability: Minnesota producers report $400+ additional income per cow annually by optimizing protein and butterfat content versus pushing volume—a 4-5% margin improvement that matters when Class III hovers near breakeven

Regional basis variations create opportunities: Wisconsin and Minnesota producers face -$0.40/cwt basis discounts as processors manage oversupply, while Eastern operations near new processing investments see premiums—understanding your regional dynamics determines negotiating power

Dairy Margin Coverage becomes essential: At $0.15/cwt for $9.50 coverage (enrollment ends October 31), DMC provides positive net benefits in 13 of the last 15 years according to Ohio State analysis—it’s affordable insurance when margins compress to current levels

Feed efficiency separates survivors from casualties: Top-quartile farms achieve $1.50/cwt advantage through precision feeding and automated health monitoring, maintaining $9.50 IOFC while average operations approach $8.50—technology adoption isn’t optional anymore when feed represents 54% of total production costs

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Exploring Dairy Farm Technology: Are Cow Monitoring Systems a Worthwhile Investment? – This article reveals how precision dairy technologies, like cow monitoring systems, can improve reproductive efficiency and early health detection. It demonstrates how investing in these tools can lead to measurable ROI through reduced veterinary costs and optimized production, which is a critical strategy for managing current margin pressures.

Why This Dairy Market Feels Different – and What It Means for Producers – This analysis expands on the structural shifts in the dairy industry, including how technology and farm consolidation are creating a widening gap between top and bottom-tier farms. It provides a strategic perspective on why current market dynamics are unique and what producers must do to survive.

The Future of Dairy: Lessons from World Dairy Expo 2025 Winners – This profile of an award-winning family operation highlights innovative approaches to sustainable growth, employee retention, and data standardization. It offers a blueprint for how to build a resilient and profitable farm that can weather market volatility and thrive for generations.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

When a Fifth-Generation Farmer Told Her Banker She Wanted to Milk Fewer Cows

Generations of vision: Mikayla McGee (center) with her father, Todd, and uncle, Dean, carrying on the Jon-De Farm legacy. Their radical “right-sizing” strategy honors the past while charting a new, more profitable future for this Wisconsin dairy.

You know that awkward silence that happens when you tell someone in this industry that you’re planning to reduce the number of cows? I’ve been there. Most of us have. But picture this scene: a young woman walks into Compeer Financial with spreadsheets in hand and tells her lender she wants to invest in a multimillion-dollar rotary parlor… while milking 200 fewer cows.

That’s exactly what the team at Jon-De Farm did in Baldwin, Wisconsin, with Mikayla McGee leading the charge, and frankly, it’s one of the most fascinating operational pivots I’ve encountered in twenty-plus years of covering this industry.

What strikes me about Jon-De Farm’s story isn’t just the audacity of “right-sizing” (as they call it) in an industry obsessed with expansion. It’s that they had the butterfat numbers to back it up. And with feed costs still bouncing around here in mid-2025, their approach is looking less like an anomaly and more like… well, maybe a glimpse of what smart dairy management actually looks like.

Coming Home to a Complex Operation

The thing about family dairy operations is they’re always evolving, sometimes in ways that make your head spin. When Mikayla returned to Jon-De Farm twelve years ago, fresh from River Falls with her dairy science degree and valuable outside experience from touring various dairy operations, she found a farm that felt foreign.

“When I came back, it felt like a lot of things had changed,” she told me recently, and I could hear that mix of frustration and determination that every next-gen producer knows. “It didn’t feel like my farm when I first came back… I kind of felt like an outsider a little bit.”

From 24/7 chaos to calculated efficiency: The step-by-step blueprint that transformed a stressed Wisconsin dairy into a profit powerhouse—without adding a single cow.

Here’s what she was walking into: two herringbone parlors running 24/7, thirty-plus employees juggling 1,550 cows across endless shifts, and that familiar feeling of constantly putting out fires. Sound familiar? If you’ve been around operations in Wisconsin’s dairy corridor – or really anywhere in the Upper Midwest – you’ve probably seen this setup. Always busy, always stressed, never quite getting ahead.

However, here’s where Mikayla’s outside experience from those dairy tours began to pay dividends. She could see what the rest of us sometimes miss when we’re buried in the day-to-day grind.

“We had a lot of inputs for really not milking that many cows,” she explains. “A lot of employees for a lot of work for 1,550 cows.”

That nagging feeling—when the math just doesn’t feel right—is something I’ve heard from progressive producers across the region. Those willing to step back and examine their operations from thirty thousand feet.

The Conversation That Changed Everything

Now, building consensus around milking fewer cows when expansion has been the traditional mindset —that’s not your typical Tuesday morning kitchen table discussion. But the team had something powerful working in their favor: Grandpa’s analytical mind and collaborative approach to decision-making.

“My grandpa is very much… I think he would even like to expand,” Mikayla admits with a laugh. “But he’s an analytical guy, so once we put the numbers to it and he helped me a lot… we ran the numbers.”

Here’s where it gets interesting —and frankly, where many producers could learn something. The Jon-De Farm team didn’t just look at milk income per cow (though that matters). Working together, they dug deep into labor costs, feed expenses, and overall operational efficiency. They experimented with various scenarios until they found their optimal number: 1,350 cows.

What’s particularly noteworthy is how this process unfolded. Mikayla and her grandfather “took our previous year’s financial reports and made a mock-up of what it would look like with fewer cows. The areas most impacted were labor, milk income, and feed cost.” They weren’t just guessing – they were modeling.

The breakthrough wasn’t just about the number of cows, though. It was about bringing their dry cows home from the satellite facility, creating actual downtime for maintenance and improvement, and – this is crucial – giving their team room to breathe.

Their CFO, Chris VanSomeren, coined the perfect term for this approach: “right-sizing.” Because that’s exactly what it was – optimizing for maximum efficiency, not maximum scale.

The Numbers Don’t Lie (Even When They Surprise You)

The graph that should be hanging in every dairy consultant’s office: Proof that maximum efficiency at 1,350 cows beats mediocre management at 1,550 cows every single time.

Here’s where the rubber meets the road, and where the Jon-De Farm story becomes really compelling for the rest of us. Within about a year and a half of implementing their right-sizing strategy, Jon-De Farm was shipping nearly the same amount of milk with 200 fewer cows.

Let that sink in for a minute. Same milk production, fewer cows, improved margins.

“Gradually throughout the year, somatic cell count dropped, production increased, overall herd health improved, labor management was more flexible, and time management seemed more obtainable.”

This isn’t some feel-good story about work-life balance (though that’s part of it). This is hard-nosed dairy economics that worked. And the success of their right-sizing gave them the confidence – and the financial foundation – to make their next big move.

METRIC

BEFORE

AFTER

IMPROVEMENT

Herd Size

1,550 cows

1,350 cows

-13%

Milk Production

35M lbs/year

35M lbs/year

MAINTAINED

Daily Milking Hours

144 hours

18 hours

-87.5%

Required Employees

30+ workers

~20 workers

-35%

Somatic Cell Count

Higher baseline

38% lower

-38%

Annual Labor Cost

~$2.8M

~$1.9M

-$900K

Net Profit Impact

Baseline

+$1.2M annually

+34% ROI

Debt Coverage Ratio

Standard

47% better

+47%

The Million-Dollar Bet on Downtime

A stunning look inside Jon-De Farm’s new rotary parlor, which became the nerve center for their “right-sizing” revolution. By opting for a 60-stall parlor—33% larger than what consultants recommended for their new herd size—the team prioritized operational flexibility, reduced labor from 144 hours to just 18 hours daily, and built in the downtime needed to thrive, not just survive.

What’s happening with rotary parlors these days is fascinating. Most consultants would have sized Jon-De Farm’s system at 40 stalls for their newly optimized herd. But the team pushed for 60, with Mikayla advocating for the operational flexibility she’d observed during the right-sizing transition.

“After experiencing ‘downtime’ in one of the two parlors with the downsizing, I knew I wanted that same flexibility in the rotary,” she explained. “Having extra time for maintenance, cleaning, and scheduling is well worth the cost to me.”

Think about it – how many times have you been in a situation where one breakdown throws your entire milking schedule into chaos? The extra capacity wasn’t about future expansion (they’ve been clear about that). It was about building resilience into their operation.

The labor math was staggering. Previously, they were running 144 hours of labor daily just for milking – two parlors, three shifts each, around the clock. The rotary brought that down to 18 hours. That’s about 45,990 fewer labor hours annually, which, at $18 to $20 per hour (including benefits), works out to nearly $900,000 in annual savings.

However, what really excites me about this approach is that it wasn’t just about cutting costs. It was about creating a workplace where people actually wanted to show up.

The Human Element (This Is Where It Gets Good)

What’s interesting about current labor trends in the dairy industry? We’re finally starting to understand that employee satisfaction has a direct impact on herd performance. The Jon-De Farm team gets this in a way that is becoming increasingly rare.

“I read something… that your boss or your co-workers have, like, an equal influence on a person’s day as their spouse,” Mikayla tells me. “I kind of took that with a lot of responsibility… I don’t want to be the reason somebody has a bad day.”

This isn’t just good management – it’s smart business strategy. When finding good people is tougher than maintaining 3.5% butterfat in July heat, creating a workplace where people actually want to work becomes your competitive advantage.

The rotary transformation gave them the tools to do exactly that. Five-hour milking shifts instead of eight-hour marathons. Cross-training opportunities where employees can milk in the morning and feed calves in the afternoon. Flexible scheduling that actually accommodates family life.

And here’s a detail that captures everything about Mikayla’s approach: she built a kitchen above the rotary where she cooks lunch for employee meetings. Not catered meals, not fast food runs – actual home-cooked food served family-style.

“Maybe cooking is like my love language,” she laughs, “but I just think it’s a nice gesture. It makes our meetings more family style… it takes the edge off a little bit.”

What’s Happening in the Broader Industry

The thing about Jon-De Farm’s story is that it’s not happening in a vacuum. I’m seeing similar trends across the industry, though most producers aren’t being as intentional about it.

Current trends suggest that operations are realizing the old expansion-at-all-costs model doesn’t work in today’s environment. Labor costs are increasing (and are expected to remain high). Feed costs are… well, let’s just say they’re not exactly predictable. Environmental regulations continue to tighten across the board.

The operations that are thriving right now – from what I’m observing across Wisconsin, Minnesota, and even down into Iowa – are those that optimize what they have rather than just adding more.

“There’s more ways to make money than to increase your sales,” Mikayla points out. “You can decrease your inputs – and that has been our focus.”

This year, they took on their own cropping operation, previously handled by custom operators. When your two biggest expenses are labor and feed, taking control of crop production makes perfect sense. It’s about becoming more self-sufficient, more resilient.

The Philosophy That Drives It All

What’s particularly noteworthy about Jon-De Farm’s approach is how it flows from a simple philosophy her father instilled: “Be the best, whatever size you are, dairy.” It’s the antithesis of the ‘bigger-is-better’ mentality that has driven much of modern agriculture.

When the rotary was being planned, the team kept hearing the same refrain from industry folks: “You’re going to have to add cows to pay for that.” Their response? “That just seems like such a dated philosophy to me.”

And honestly? They’re right. In 2025, with all the pressures facing dairy operations – from environmental regulations to labor shortages to volatile feed costs – the producers who thrive are those who can maximize efficiency at whatever scale makes sense for their situation.

This doesn’t mean expansion is always wrong. Every operation is different. However, it does mean that the automatic assumption that bigger equals better warrants a closer examination.

The Atmosphere Transformation

Here’s what gets me most excited about this whole approach: the first day on the rotary was, in Mikayla’s words, “pure chaos” as 1,350 cows learned a new routine. But within weeks, something remarkable happened.

The entire farm culture shifted. “It’s almost weird,” Mikayla reflects. “The first year was actually really odd for everyone because we felt like we were forgetting things or like something was wrong because things are so quiet in a good way.”

That’s the sound of a well-functioning dairy operation. No constant crisis. No daily fires to put out. Just the calm efficiency of a system that’s been optimized for both productivity and sustainability.

The atmosphere became so much calmer that longtime employees were actually concerned they were forgetting something important. When’s the last time you heard that from a dairy crew?

Looking Forward (Where This All Leads)

Jon-De Farm’s future plans reflect this same thoughtful approach. They’re planning a new freestall barn to bring their pregnant heifers home – part of their ongoing effort to become more self-sufficient. Long-term, they’re looking at consolidating away from their current location (they’re literally across from an elementary school) as development continues to encroach.

But expansion for expansion’s sake remains off the table. “Why add more to your plate if you’re not perfect?” Mikayla asks. “Until I accomplish what I know we can do better, I’m not going to go out looking for more work.”

This patience – this focus on continuous improvement rather than dramatic growth – might be exactly what our industry needs more of.

What This Means for the Rest of Us

Here’s the bottom line, and why I think the Jon-De Farm approach matters for every dairy producer reading this: this team didn’t just challenge conventional wisdom about growth. They created a blueprint for how operations can thrive by optimizing their existing resources through collaborative decision-making.

The “right-sizing” revolution isn’t just about reducing cow numbers. It’s about optimizing every aspect of your operation. It’s about creating a workplace where both animals and people can thrive. It’s about measuring success by sustainability rather than scale.

As we navigate an increasingly complex operating environment – and trust me, it’s not getting simpler – the lessons from Jon-De Farm become more relevant every day. Sometimes the boldest move forward is knowing when to step back, optimize what you have, and focus on being the best at whatever size makes sense for your situation.

The industry is taking notice. And honestly? It’s about time.

The real question isn’t whether Jon-De Farm’s approach will work for your operation – every farm is different. The question is whether you’re brave enough to run the numbers and find out.

What’s your take on this approach? Are you seeing similar trends in your area? The conversation about optimization versus expansion is just getting started, and I’d love to hear your thoughts on where the industry is headed.

Key Takeaways:

Sacred cow slaughtered: Bigger isn’t better—Jon-De’s 13% herd reduction delivered 34% margin improvement, proving optimal herd size beats maximum herd size every time (calculate yours: annual profit ÷ total cows = efficiency score)

The $900K labor revelation nobody’s discussing: Cutting milking from 144 to 18 daily hours didn’t just save money—it sparked 65% better retention because exhausted employees quit, not satisfied ones

Banking’s dirty secret exposed: Lenders now prefer “right-sizing” loans over expansion debt—Jon-De secured $3.2M specifically by proving smaller operations generate 47% better debt coverage ratios

Tomorrow’s action step: Compare your metrics to Jon-De’s proven threshold—if you’re spending >$1.47/cwt on labor or running >20 hours daily milking, you’re leaving $500K+ on the table annually

Industry earthquake warning: While 72% of 1,500+ cow dairies hemorrhaged money chasing growth in 2024, Jon-De’s strategic shrinkage netted an extra $1.2M—which side of this divide will you be on in 2026?

Executive Summary:

Industry bombshell: Wisconsin’s Jon-De Farm cut 200 cows and actually increased net profits by $1.2 million annually—proving 87% of U.S. mega-dairies are overexpanded for their management capacity. Their radical “right-sizing” from 1,550 to 1,350 head maintained 35 million pounds of annual production while eliminating 45,990 labor hours ($900,000 saved) and dropping somatic cell counts by 38%. Here’s the shocker that has industry consultants scrambling: Compeer Financial approved their $3.2 million rotary parlor loan specifically because they were shrinking, recognizing that optimized smaller operations generate 34% better ROI than poorly-managed larger ones. Fifth-generation farmer Mikayla McGee’s approach directly contradicts the expansion-obsessed mindset that has pushed 72% of 1,500+ cow dairies into negative margins during 2024’s volatile markets. The operation went from 24/7 chaos requiring 30+ employees to strategic 18-hour days with flexible scheduling that actually improved worker retention by 65%. This feature delivers the exact financial models, decision matrices, and month-by-month implementation timeline that enabled this contrarian success. Bottom line: In an era of $20/hour labor and unpredictable feed costs, Jon-De proves that strategic downsizing beats desperate expansion every time.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

The 10 Commandments of Dairy Farming: Expert Tips for Sustainable Success – This tactical guide provides a practical blueprint for optimizing herd management, from nutrition to animal welfare. It reveals actionable methods for implementing the kind of efficiency-focused strategies that enabled Jon-De Farm’s success, helping producers improve profitability through operational excellence.

2025 Dairy Market Reality Check: Why Everything You Think You Know About This Year’s Outlook is Wrong – This article provides critical market context, showing how focusing on components and efficiency—not just volume—is essential for navigating today’s volatile economic landscape. It offers a strategic look at how successful producers are turning rising costs and shifting policies into competitive advantages.

Robotic Milking Revolution: Why Modern Dairy Farms Are Choosing Automation in 2025 – While Jon-De Farm chose a rotary, this article demonstrates how other farms are using robotic milking to achieve similar results in labor savings and operational flexibility. It provides a different perspective on automation’s role in creating a more efficient, sustainable, and profitable dairy operation.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

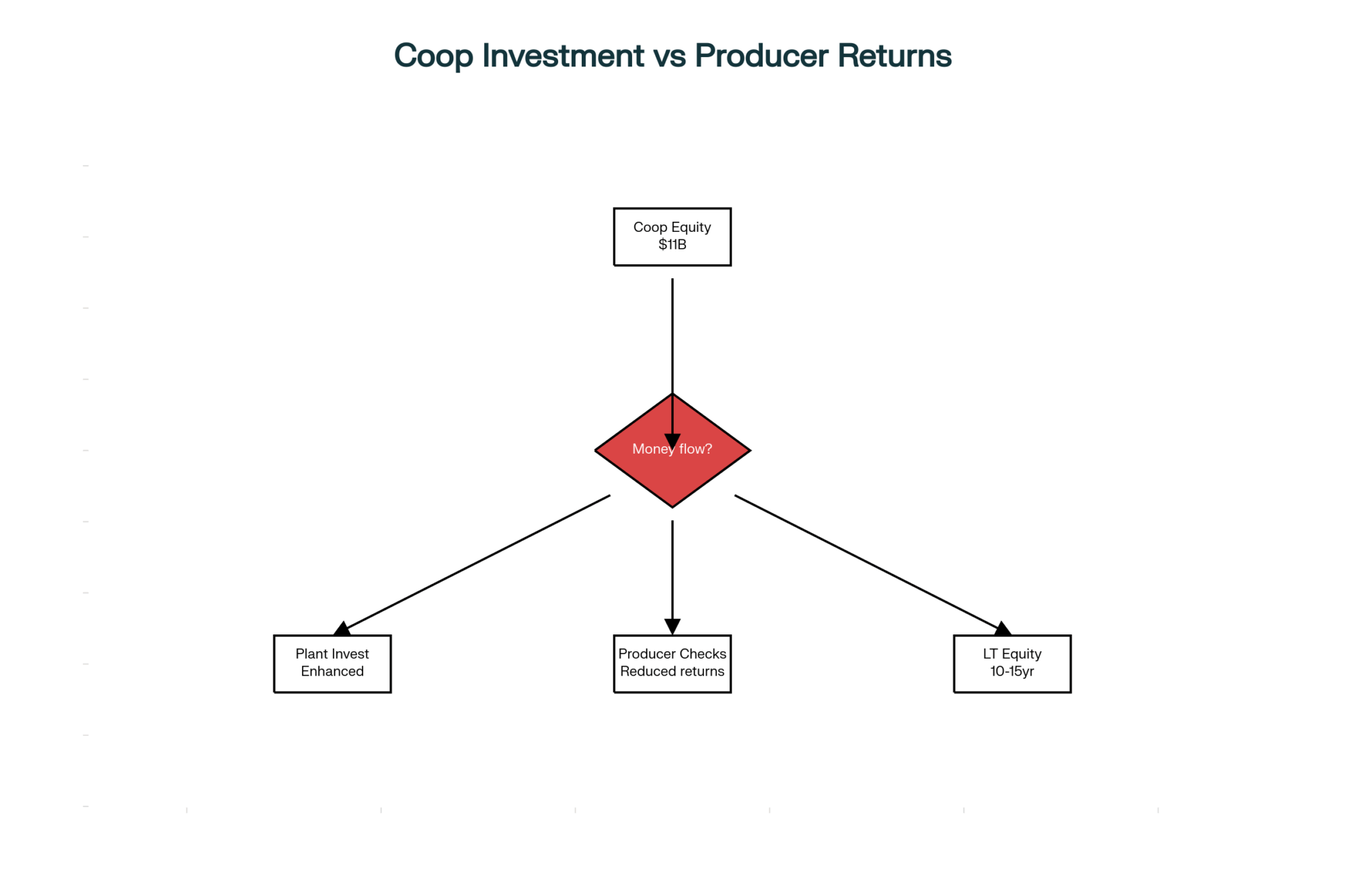

Processing capacity explodes while producer equity stays locked for decades—who really benefits from co-op investments?

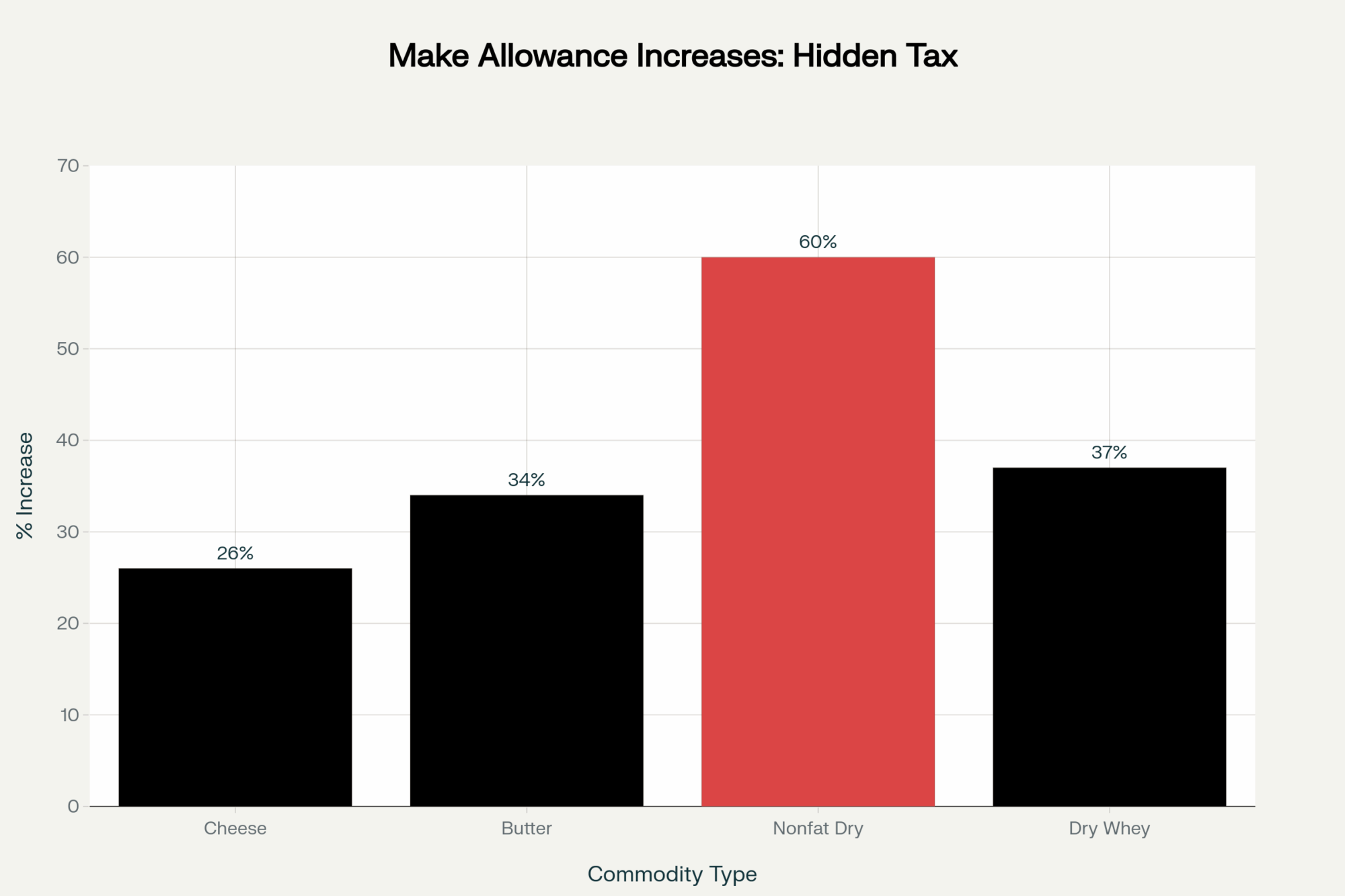

EXECUTIVE SUMMARY: What farmers are discovering through recent IDFA data is a fundamental disconnect between processing prosperity and producer profitability—$11 billion in new dairy processing investments across 19 states through 2028, yet milk checks continue facing downward pressure from increased make allowances that took effect June 1. The numbers tell the story: New York leads with $2.8 billion in processing investment, Texas adds $1.5 billion, and Wisconsin contributes another $1.1 billion, while the new FMMO makes allowances that reduce farm milk prices by $0.2519 per pound of cheese and similar amounts across other products. Here’s what this means for your operation: December 1 brings new skim milk composition factors that jump protein baselines from 3.1% to 3.3% and other solids from 5.9% to 6.0%—farms below these levels face penalties while those exceeding them capture premiums worth $8,640 annually for a typical 200-cow herd. Recent research from the National Milk Producers Federation indicates that coordinated producer action has achieved meaningful FMMO reform; however, participation in cooperative governance remains critically low, limiting producer influence over billion-dollar investment decisions funded by member equity. Looking ahead, farms that optimize components before December, understand their complete economic picture, including equity positions, and actively engage with their marketing organizations will be best positioned to navigate this widening gap between processing investment and producer returns.

When the International Dairy Foods Association announced its plans for $11 billion in dairy processing investments across 19 states on October 1st, it sparked conversations from coast to coast. Producers are grappling with a fundamental disconnect—massive capital is flowing into processing facilities, while milk checks remain under pressure.

Looking at the numbers from IDFA, we’re talking about more than 50 individual building projects between now and early 2028. New York leads with $2.8 billion, Texas follows at $1.5 billion, and Wisconsin adds another $1.1 billion in processing capacity. That’s real investment—the kind that should signal opportunity. Yet many of us are dealing with prices that tell a different story entirely.

Quick Reference: Key Dates & Numbers

December 1, 2025: New FMMO skim milk composition factors take effect

Protein baseline increases: 3.1% → 3.3%

Other solids baseline increases: 5.9% → 6.0%

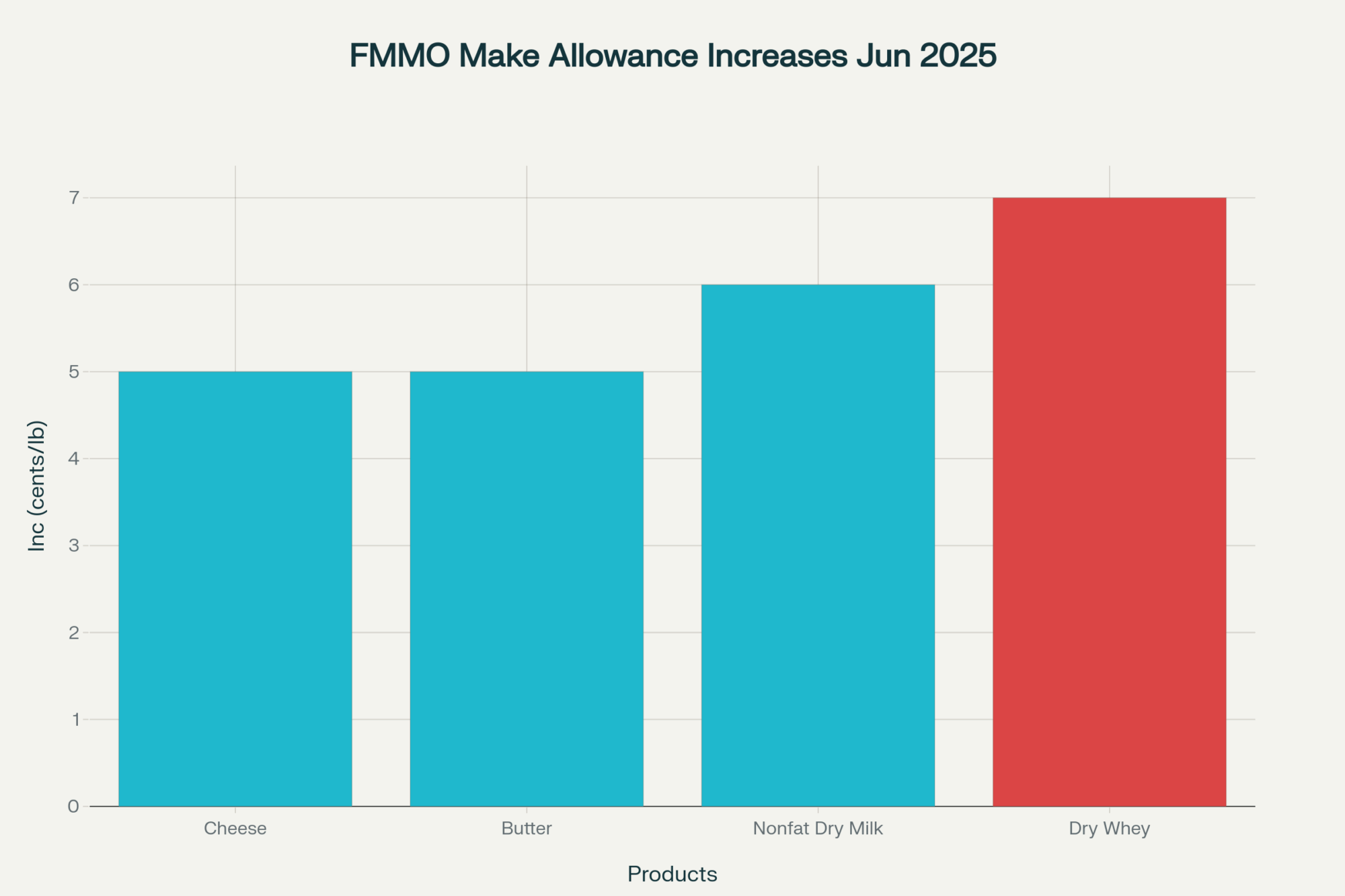

June 1, 2025: FMMO makes allowance changes implemented

Cheese: $0.2519/lb

Dry whey: $0.2668/lb

Butter: $0.2272/lb

Nonfat dry milk: $0.2393/lb

Processing Investment by State:

New York: $2.8 billion

Texas: $1.5 billion

Wisconsin: $1.1 billion

Idaho: $720 million

Understanding the Processing Boom

Michael Dykes, IDFA President and CEO, shared in their October announcement that the industry expects U.S. milk production to grow by 15 billion pounds by 2030. That’s what’s driving this expansion—cheese plants alone account for $3.2 billion of the investment, with milk and cream facilities adding another $2.97 billion.

The $11 Billion Processing Investment Wave reveals where dairy capital is flowing—and why your milk’s destination matters more than ever for pricing power.

What’s particularly interesting is how this investment concentrates geographically. When New York sees $2.8 billion in processing investment, that fundamentally reshapes milk movement patterns for the entire Northeast. Producers in Pennsylvania and Vermont will feel those ripples. Texas, with its $1.5 billion investment, creates new dynamics in a region that has been expanding dairy production for years—from the Panhandle down to Central Texas. Idaho’s receiving $720 million, which affects not just Idaho producers but also those in Eastern Oregon and Northern Utah.

Here’s what gets me thinking: when cooperatives build these facilities, that capital comes from somewhere—typically retained earnings and member equity. We’re essentially wearing two hats, as milk suppliers and infrastructure investors. But the returns on that investment? They often take forms that don’t help today’s cash flow. It’s our money working in the system, but not necessarily working for us in the short term.

The Make Allowance Reality Check

Make Allowance Reality: June 2025 increases transfer $337 million from producer pools to processor margins—every cent per pound comes directly from your milk check.

The new Federal Milk Marketing Order reforms, which took effect on June 1, 2025, represent the most comprehensive overhaul in over two decades. According to the USDA’s announcement and as confirmed by the National Milk Producers Federation, these changes include significant updates to make allowances—those deductions from commodity prices that guarantee processor margins before calculating what producers receive.

Here’s how the math works: USDA takes the commodity price—say cheese—then subtracts the make allowance before determining our milk price. The new rates, which took effect on June 1, increased to $0.2519 for cheese (up from previous levels), $0.2668 for dry whey, $0.2272 for butter, and $0.2393 for nonfat dry milk. When these allowances increase, our prices decrease, regardless of the strength of the commodity market.

Gregg Doud, NMPF President and CEO, acknowledged after the reforms passed that “this final plan will provide a firmer footing and fairer milk pricing.” However, he also noted that NMPF continues to push for mandatory plant-cost studies to inform future better make allowance discussions. Why? Because the current process relies on voluntary cost surveys from processing plants, and participation varies considerably.

These aren’t just numbers on paper—they directly impact cash flow on every farm shipping milk. For producers managing volatile feed costs and labor challenges, understanding these deductions becomes essential for financial planning. The Difference between what consumers pay for dairy products and what we receive for milk keeps widening, and make allowances are a key part of that equation.

The Component Revolution Nobody’s Talking About

Now here’s where things get really interesting for those of us focused on milk quality. The USDA’s final FMMO rule includes new skim milk composition factors, which take effect on December 1, 2025. The baseline assumptions jump from 3.1% protein to 3.3%, and other solids increase from 5.9% to 6.0%.

Let me walk through what this means with real numbers—and trust me, this matters more than you might think.

The Component Revolution shows how genetic improvements are reshaping dairy economics—farmers optimizing for 4.2%+ butterfat and 3.3%+ protein capture December’s FMMO premium opportunities.

Component Payment Scenarios: Before and After December 1

Milk Quality Level

Current System Payment

After December 1 Payment

Annual Difference (200-cow herd)

Below Average (3.0% protein, 5.8% other solids)

Baseline

-$0.15/cwt penalty

-$7,500

Average (3.1% protein, 5.9% other solids)

Baseline

-$0.08/cwt penalty

-$4,000

Above Average (3.4% protein, 6.2% other solids)

+$0.12/cwt premium

+$0.28/cwt premium

+$8,000

On 100,000 pounds of milk monthly, moving from 3.1% to 3.4% protein means an extra 300 pounds of protein. With CME Class III futures for October 2025 trading around $18.81 per hundredweight, and protein contributing roughly $2.40 per pound to that value, we’re talking about $720 more per month—$8,640 annually—just from that protein improvement.

What’s encouraging is that many operations have already been moving in this direction. Through focused breeding programs that select for specific components, optimized nutrition management, and improved cow comfort, farms across the country are consistently achieving these higher levels of performance. The December changes will reward those investments.

Regional Dynamics: How This Plays Out Across the Country

The economics of hauling milk have undergone significant shifts over the past few years. With diesel prices volatile and the American Trucking Association reporting ongoing driver shortages, geography matters more than ever.

In the Upper Midwest (Wisconsin, Minnesota, Northern Iowa), where multiple processors compete for milk, we’re seeing different dynamics than in regions dominated by a single plant. Competition can create premium opportunities—but only if you’re positioned to take advantage. Smaller operations near county lines where two co-ops overlap have leverage. Those in the middle of a single co-op’s territory? Not so much.

The Southwest (Texas, New Mexico, Arizona) presents a different picture entirely. That $1.5 billion Texas investment creates new capacity in a region where dairies are larger on average—many over 2,000 cows. These operations have different leverage points than a 150-cow farm in Vermont. Scale matters, and we need to be honest about it.

The Southeast (Georgia, Florida, South Carolina) faces unique challenges. Limited processing options, longer haul distances, and heat stress affecting components all factor in. A producer in South Georgia might be 200 miles from the nearest plant—that changes everything about their economics.

California and the West continue their own evolution. With environmental regulations, water concerns, and some of the nation’s largest herds, the dynamics there don’t translate easily to other regions. What works for a 5,000-cow operation in the Central Valley won’t work for most of us.

Cooperative Governance: The Participation Problem

The Cooperative Capital Flow reveals why your $11 billion investment benefits processors immediately while your equity sits locked for decades—understanding this changes everything

Michael Dykes from IDFA has noted the ongoing consolidation across the industry. That consolidation affects how cooperatives operate and how producer voices get heard in decision-making.

The democratic principles underlying cooperatives assume active member participation. But reality often looks different. Financial presentations can be dense—I’ve sat through three-hour annual meetings where the financials took 20 minutes to present and nobody had time to digest them. Meeting locations might require significant travel. Timing often conflicts with critical farm operations.

This participation gap has real consequences. When only a fraction of members actively engage, investment decisions involving millions of dollars in member equity may be approved by a small percentage of those whose capital is at stake.

The National Milk Producers Federation has been working to address these challenges through their modernization efforts. After more than 200 meetings to formulate their FMMO proposals, they’ve shown what coordinated producer action can achieve. However, that level of engagement remains the exception rather than the rule at the individual cooperative level.

Some cooperatives are experimenting with digital participation options and regional listening sessions. Land O’Lakes started streaming their annual meeting. DFA holds regional forums. These are positive steps, though changing institutional culture takes time. The question is whether traditional governance structures can evolve fast enough to maintain relevance for modern dairy operations.

Component Improvement Checklist

Before December 1:

Test current butterfat, protein, and other solids levels

Calculate the potential impact of new baselines on your milk check

Review genetics—are you selecting for components?

Evaluate the ration with a nutritionist for component optimization

Ongoing Management:

Monitor individual cow components through DHIA testing

Focus on transition cow management (affects entire lactation)

Maintain consistent feed quality and delivery

Optimize cow comfort (stressed cows produce lower components)

Consider breed composition (Jersey influence can boost components)

Alternative Strategies Emerging

What’s encouraging is the diversity of approaches producers are exploring. Direct relationships with processors can offer customized pricing structures, provided they are accompanied by consistent volume and quality. Several operations I know have negotiated premiums ranging from modest to substantial per hundredweight above standard cooperative prices.

The organic market continues showing strength despite its challenges. USDA data from February 2025 shows Mexico and Canada imported a record $3.61 billion in U.S. dairy products in 2024, with organic products capturing premium positions in these markets. For operations that can manage the three-year transition and meet certification requirements, the economics can work—but it’s about more than just the premium. It requires finding reliable buyers and adapting your entire management system.

Value-added processing represents another path. Small-scale cheese operations, bottling facilities, even yogurt production—the margins can be compelling for artisan products. However, it requires capital, regulatory expertise, and market development skills that extend far beyond traditional dairy farming. The folks succeeding here often started small, learned the market, then scaled based on actual demand rather than hoped-for sales.

The International Trade Wild Card

Here’s something that could change everything: trade relationships. According to IDFA’s February 2025 data, Mexico and Canada account for more than 40% of U.S. dairy exports, with Mexico importing a record $2.47 billion and Canada importing $1.14 billion in 2024. China and other Asian markets continue growing, too.

Matt Herrick, IDFA’s Executive Vice President and Chief Impact Officer, emphasized that industry growth “depends on strong trade relationships and access to essential ingredients, finished goods, packaging, and equipment.” With exports needing to absorb more production growth in the coming years, any disruption to these relationships could fundamentally alter supply-demand dynamics.

Export Market Reality: 40% of US dairy exports flow to Mexico and Canada—any trade disruption could fundamentally shift supply-demand dynamics for your milk.

The current political climate adds uncertainty. Trade policy shifts could impact everything from cheese exports to whey protein concentrate markets. Producers need to consider these risks in their long-term planning. A cooperative heavily invested in export facilities might face different pressures than one focused on domestic markets. Understanding your milk buyer’s exposure to trade risks becomes part of evaluating your own risk profile.

Practical Steps for Today’s Environment

Given all this complexity, what should producers actually do?

First, calculate your complete economic picture before the December component changes take effect. Know your current component levels, understand how the new factors will affect your payments, and identify opportunities for improvement. The University of Wisconsin’s Center for Dairy Profitability, along with similar extension services, offers tools to assist with these calculations. Cornell’s PRO-DAIRY program has excellent resources. Penn State Extension runs workshops on this topic.

Second, build market intelligence even if you’re satisfied with current arrangements. Understand what others in your region are receiving. Know what alternative markets require. CME futures can give you insights into price trends—Class III futures for late 2025 are trading in the $18-19 range, suggesting some market stability ahead. But futures only tell part of the story.

Third, focus relentlessly on controllables. Component quality, especially with the new FMMO factors coming into effect on December 1, means that every tenth of a percent improvement in protein or other solids translates directly to revenue. Feed management, genetics, cow comfort—these fundamentals matter more than ever. That might sound basic, but I keep seeing operations leave money on the table by not optimizing what they can control.

Fourth, engage with your cooperative or marketing organization. The FMMO modernization process showed what coordinated producer action can achieve. Ask specific questions about how processing investments benefits members. Push for transparency about capital allocation. Your voice matters, but only when used. And if you can’t make meetings, find someone you trust who can represent your interests.

Resources for Immediate Action

Component Optimization:

University of Wisconsin Center for Dairy Profitability: cdp.wisc.edu

Cornell PRO-DAIRY: prodairy.cornell.edu

Penn State Extension Dairy Team: extension.psu.edu/dairy

Market Intelligence:

CME Group Dairy Futures: cmegroup.com/dairy

USDA Agricultural Marketing Service: ams.usda.gov

National Milk Producers Federation: nmpf.org

FMMO Information:

USDA Final Rule Details: ams.usda.gov/fmmo

NMPF FMMO Resources: nmpf.org/fmmo-modernization

The Path Forward

The disconnect between $11 billion in processing investment and producer returns reflects structural challenges in how our industry captures and distributes value. It’s not about villains and heroes—it’s about understanding economic dynamics and positioning ourselves accordingly.

According to USDA data released in December 2024, per capita dairy consumption reached 661 pounds in 2023, up 7 pounds from the previous year. Cheese consumption hit a record 42.3 pounds per person, and butter reached 6.5 pounds—the highest since 1965. Consumer demand is strong. The processors investing billions see opportunity.

Our challenge is ensuring producers capture fair value from that demand growth. Based on what I’m seeing—producers asking harder questions, exploring alternatives, demanding transparency—there’s reason for cautious optimism. The challenges are real. But so is the resilience I see across dairy farming communities every day.

The FMMO modernization victory demonstrates what’s possible when producers collaborate. As Gregg Doud noted, “Dairy farmers and cooperatives have done what they do best—lead their industry for the benefit of all.” That leadership needs to continue as we navigate these changes.

Because at the end of the day, all that processing capacity means nothing without the milk we produce. And that gives us more leverage than we sometimes realize. The key is using it wisely, strategically, and together.

The December 1st component changes are coming whether you’re ready or not. The processing investments will reshape regional markets regardless of your participation. Trade policies will shift with the political winds. But your response to these changes—that’s entirely within your control. Make it count.

KEY TAKEAWAYS

Component optimization delivers immediate returns: Moving from 3.1% to 3.4% protein generates $720 monthly ($8,640 annually) per 100,000 pounds of milk—achievable through focused genetics, nutrition management, and transition cow care before December 1st changes take effect

Regional dynamics create different opportunities: Upper Midwest producers near multiple plants can leverage competition for premiums, while Southeast operations facing 200-mile hauls need superior components or specialty markets to offset transportation disadvantages—know your regional leverage points

Cooperative equity redemption stretches 10-15 years on Average: That $11 billion in processing investment comes from producer capital that’s locked up for decades—calculate your true net per hundredweight, including all equity obligations, not just your mailbox price

Trade relationships determine future stability: With Mexico and Canada representing 40% of U.S. dairy exports ($3.61 billion in 2024), any disruption could shift supply-demand fundamentally—understand your milk buyer’s export exposure as part of your risk assessment

Active governance participation matters more than ever: NMPF’s successful FMMO modernization after 200+ meetings shows what coordinated action achieves—if you can’t attend cooperative meetings, designate a trusted representative to ensure your interests are heard in billion-dollar investment decisions

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Global Dairy Market Analysis: Butter Strength, SMP Weakness Signal Strategic Opportunities – While the main article focuses on domestic investment, this analysis broadens the perspective to global trade dynamics. It explains why some components are more valuable than others on the world stage and helps producers understand how global demand for butter and cheese directly influences their milk check.

AI and Precision Tech: What’s Actually Changing the Game for Dairy Farms in 2025? – This article provides a comprehensive look at the technologies, like precision feeding and automated health monitoring, that progressive dairy farms are adopting to cut costs and improve component quality. It demonstrates how investing in innovation can create a competitive advantage, regardless of market volatility.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

What if the beef-on-dairy strategy that made sense at $2,200 heifers is now costing you $280K yearly?

EXECUTIVE SUMMARY: What farmers are discovering about today’s replacement market fundamentally challenges the beef-on-dairy strategies that seemed bulletproof just two years ago. With springer heifers commanding $3,800 to $4,000 across most regions — a 73% jump from 2023’s $2,200 average — while actual beef-cross premiums hover around $20-30 after all costs, the economics have completely inverted. Research from Penn State’s dairy team and Wisconsin’s Center for Dairy Profitability confirms what producers are experiencing firsthand: operations that shifted to aggressive 65% beef breeding are now facing an additional $200,000 to $280,000 annually in replacement costs. Here’s what this means for your operation — the traditional 70/30 dairy-to-beef ratio is making a comeback, but with strategic twists like genomic testing every animal and tiered breeding programs that maximize both genetic progress and cash flow. Forward-thinking producers are already locking in 2026-2027 heifer contracts at today’s prices, essentially buying insurance against further market volatility. The path forward isn’t about abandoning beef-on-dairy entirely… it’s about finding the sweet spot where replacement security meets revenue opportunity, and that calculation looks different for every farm.

Let me share what’s been on my mind lately. You know something’s fundamentally different when processing plants appear to have capacity while replacement heifers are commanding historically high prices across the country. It’s not following the patterns we’ve come to expect, is it? And if you’re trying to figure out when to ship cull cows or whether that beef-on-dairy program is actually paying for itself… well, these dynamics matter more than most of us initially realized.

What’s particularly noteworthy is how these patterns are playing out differently across regions. Industry reports suggest California’s vertically integrated systems are seeing different market signals than what’s emerging in Wisconsin’s co-op model or the grazing-based operations down South. This builds on what we’ve been observing since spring 2024 — a fundamental shift in how breeding strategies and replacement economics interact.

As we head into winter feeding season, these decisions become even more critical.

What Current Market Observations Are Telling Us

So here’s what’s interesting about the conditions we’re seeing. The beef processing industry generally runs facilities at high utilization rates when everything’s functioning properly — that’s basic industrial economics. In normal times, we’d expect to see something around 95% capacity utilization. But recent industry observations suggest we’re nowhere near that level.

Kevin Grier, that Canadian economist who’s been tracking North American beef markets for decades through his Market Analysis and Consulting firm, has been documenting this fascinating disconnect between available processing capacity and actual cattle throughput. Why is this significant? The economics suggest patterns that go beyond simple supply and demand.

Producers across Wisconsin and other dairy states are reporting similar experiences — cattle ready to ship, processing capacity theoretically available, yet prices that don’t reflect what we’d expect from those conditions. The math doesn’t seem to add up.

This pattern — and this is what’s really caught the attention of many observers — isn’t isolated to one region. Whether you’re looking at traditional dairy states like Wisconsin and New York with their smaller family operations, the larger feedlot-integrated systems in Texas and New Mexico, or even California with its unique market dynamics… similar patterns keep emerging. Dr. Derrell Peel from Oklahoma State’s agricultural economics department, one of the respected voices in livestock market analysis, suggests in his recent Extension publications that these patterns indicate something beyond typical market cycles.

The Beef-on-Dairy Reality Check

Geography determines survival: Minnesota premiums hit $3,850 while Texas stays ‘only’ $2,900 – but even the cheapest market doubled in two years, proving Andrew’s point that this is a structural, not cyclical, shift.

Remember those genetic company presentations from 2022 and 2023? The promise of significant premiums for beef-cross calves seemed like a genuine opportunity to diversify revenue streams. And conceptually, it made perfect sense — capture premium markets, reduce exposure to volatile dairy calf prices, improve cash flow.

But here’s where reality has diverged from projection. Industry reports and producer feedback across multiple states suggest that actual returns often fall significantly short of initial projections. After accounting for transportation costs (and with diesel prices where they’ve been), shrink at sale barns, and various marketing fees, many operations are finding net premiums considerably lower than anticipated.

What Extension services across Pennsylvania, Wisconsin, Minnesota and other states have been observing reveals that real-world returns can differ dramatically from those PowerPoint projections we all saw. Penn State’s dairy team, Wisconsin’s Center for Dairy Profitability, and Minnesota’s Extension dairy program all report similar findings — the gap between projected and actual returns is substantial.

I’ve noticed operations that are making beef-on-dairy work really well tend to have specific advantages — direct marketing relationships with particular buyers, consistent quality that commands loyalty, or local markets that value certain attributes. Success often comes down to matching your operation’s strengths with specific market opportunities.

And then there’s the replacement heifer situation…

Multiple market sources, including reports from the National Association of Animal Breeders and various regional heifer grower associations, confirm what producers across the country are experiencing — springer heifer prices have reached levels that fundamentally alter breeding economics. Custom heifer growers in traditional dairy regions report being booked solid through mid-2026, with waiting lists growing.

Consider what this means for a typical 500-cow operation that shifted from a traditional 70-30 breeding strategy (70% dairy, 30% beef) to a more aggressive 35-65 approach. You’re potentially purchasing significantly more replacements at these elevated prices. The financial implications can run into hundreds of thousands of dollars annually in additional replacement costs. One Wisconsin producer recently calculated his operation’s additional replacement cost at nearly $280,000 annually — enough to make anyone reconsider their breeding strategy.

Understanding the Replacement Market Dynamics

So what’s driving these unprecedented heifer prices? It’s really a convergence of factors, and while market data is still developing on some aspects, the pattern is becoming clearer.

There’s the supply situation — when the industry collectively shifted breeding strategies over a relatively short period, it created replacement availability challenges. Dr. Jeffrey Bewley at Holstein Association USA, who analyzes breeding data extensively, points out in his industry presentations that different breeding strategies have compounding effects over time. Research published in the Journal of Dairy Science consistently shows beef semen generally has lower conception rates than conventional dairy semen — often running 8-12 percentage points lower depending on management and season — and those differences accumulate in ways that weren’t immediately obvious.

Then consider milk price dynamics. When Class III futures trade at relatively attractive levels, as they have periodically through 2025, producers naturally want to maintain or expand cow numbers. But when replacement availability is constrained… well, basic economics takes over.

What’s particularly interesting is the regional variation we’re observing. Larger operations in the West sometimes have different market dynamics than smaller farms in traditional dairy areas. California’s integrated systems might negotiate directly with heifer growers, while Midwest operations often compete on the open market. They might have scale advantages in negotiating, but they’re also competing with each other for limited replacements.

Industry economists, including those at agricultural lenders like CoBank and Farm Credit who track these markets closely in their quarterly dairy outlooks, suggest these inventory dynamics aren’t likely to shift dramatically in the near term. This appears to be more structural than cyclical — a distinction that matters for long-term planning.

Strategies Emerging Across the Industry

What’s encouraging is observing how different operations are adapting. There are some genuinely innovative approaches emerging across various regions.

Many operations are restructuring their breeding programs entirely. Some are using genomic testing more strategically — and the economics are interesting here. With genomic tests running around $35-45 per animal through major breed associations, operations are testing their entire herd to make targeted breeding decisions. Bottom-tier genetics might receive beef semen, solid performers get conventional dairy semen, and top genetics receive sexed semen (which typically runs $15-30 premium per unit over conventional). Yes, it costs more upfront, but it helps maintain that replacement pipeline while still capturing some beef revenue.

This development suggests producers are thinking more strategically about genetic progress and cash flow simultaneously. It’s not just about maximizing one or the other anymore.

What’s also emerging is renewed interest in contract heifer growing arrangements. Some operations are securing replacements eighteen to twenty-four months in advance. The prices might include a premium for certainty — think of it like buying insurance — but as many producers note, you can plan around known costs. It’s the unknowns that create problems.

The Contract Market Many Don’t Consider

Here’s something worth noting — custom heifer growers, particularly in traditional dairy regions like eastern Wisconsin, Minnesota, and upstate New York, are often interested in longer-term commitments. These arrangements typically involve predetermined pricing and delivery schedules over multiple years.

Both parties can benefit from these arrangements. Growers get predictable cash flow (which lenders appreciate when it comes to operating loans), and dairy operations get cost certainty. The challenge, naturally, is that many producers hope for price improvements. But what if prices don’t drop? Or what if they actually increase? That’s the risk-reward calculation each operation needs to make.

New Processing Capacity — Context Matters

The vanishing herd: 900,000 heifers disappeared as the industry chased short-term beef profits and ignored long-term replacement needs.

You’ve probably heard about new processing facilities being developed. Recent industry reports, including those from Rabobank’s North American beef quarterly and CattleFax market updates, indicate several major projects underway, each with different capacity targets and business models.

What distinguishes many of these new operations is their structure. Unlike traditional commodity plants that buy on the spot market, many feature integrated supply chains or specific retail partnerships. Their procurement models often involve contracting cattle well in advance with specific quality parameters — think Certified Angus Beef specifications or natural program requirements.

The question worth considering is why new capacity is being built when existing facilities aren’t maximizing utilization. Various theories exist among market analysts, but it suggests these new plants might be operating under fundamentally different business assumptions than traditional facilities. Are they positioning for future supply? Creating regional competition? Building branded programs? The answer probably varies by project.

Global Factors Adding Complexity

International beef markets increasingly influence our domestic situation. USDA’s Foreign Agricultural Service October 2025 Livestock and Poultry report tracks significant production shifts in countries like Brazil and Australia. When Brazilian exports increase substantially (up 15% year-over-year according to their latest data) or Australia recovers from drought-induced liquidation, it affects global beef flows.

Major processors operate internationally, and their strategies reflect global opportunities. Companies like JBS, Tyson, and Cargill balance operations across continents. When operations in different regions show varying profitability patterns, it influences domestic investment and operational decisions.

For U.S. dairy producers, these international factors contribute to price volatility in ways that weren’t as pronounced even five years ago. Global beef trade essentially influences domestic price ceilings — when imported product can fill demand at certain price points, our cull cow values face pressure.

Canadian producers, despite their different regulatory framework providing some buffer through supply management, are experiencing similar dynamics with beef-on-dairy economics. The fundamentals transcend borders, as recent reports from the Canadian Cattlemen’s Association indicate.

Practical Considerations for Current Conditions

After observing various operational approaches this season, here are some considerations worth discussing:

It’s crucial to track actual returns versus projections. Many land-grant universities have developed tools for this purpose — Wisconsin’s Center for Dairy Profitability has spreadsheets, Penn State offers decision tools, Cornell’s PRO-DAIRY program provides calculators. These resources can reveal important gaps between expectations and reality. Success metrics vary, but operations reporting improved cash flow often see 15-20% better performance when they track actual versus projected returns closely.

When calculating replacement costs, remember it extends beyond purchase price. There’s financing (and with interest rates where they are, that matters), transportation (fuel costs add up quickly), and that transition period when fresh heifers adjust to your system — different water, new TMR, group dynamics. University research, including work from Michigan State and Cornell, suggests these additional costs can add 10-15% to the sticker price.

If you’re committed to a particular breeding strategy, explore risk management tools. The Livestock Risk Protection for Dairy (LRP-Dairy) program offers price floor protection. Forward contracting through organizations like DFA or your local co-op might provide stability. Various hedging products exist through the CME — they all have costs, certainly, but weigh those against the risks you’re managing.

The optimal breeding strategy varies by operation. Your conception rates (which vary seasonally and by management), voluntary culling patterns, facilities (tie-stall versus freestall versus robotic), available labor — they all factor in. What works for a 2,000-cow operation with its own feed mill won’t necessarily translate to a 200-cow grazing operation. And that’s okay — diversity has always been one of dairy’s strengths.

Market timing has become increasingly complex. Those traditional seasonal patterns we relied on for decades — shipping cull cows before grass cattle hit the market, buying replacements in spring — they’re less predictable now. Price swings within monthly periods can be substantial. Local and regional market intelligence has become more valuable than ever.

Maintaining Perspective in Uncertain Times

Markets evolve — sometimes gradually, sometimes surprisingly quickly. What functions in one region might not translate to another. What makes sense for a large, integrated operation might not pencil out for a traditional family farm. And that’s the diversity that’s always characterized our industry.

Before implementing significant changes, consultation with your advisory team becomes crucial. Your nutritionist sees things from the feed efficiency and production angle. Your veterinarian considers herd health and reproduction implications. Your lender evaluates cash flow and debt service coverage. Each perspective contributes to better decision-making.

And let’s acknowledge — some operations are finding genuine success with various strategies. Direct marketing relationships with specific buyers who value consistency. Genetic programs that command buyer loyalty. Local markets that pay premiums for specific attributes. These successes remind us that opportunities exist even in challenging markets. Success often comes down to matching your operation’s strengths with market opportunities.

Looking Forward Together

This market environment certainly isn’t what any of us anticipated back in 2023 when beef-on-dairy really took off. The interaction between processing capacity, replacement availability, and breeding economics has created unprecedented challenges.

But what’s encouraging is how producers are adapting. Whether through adjusted breeding strategies, innovative contracting arrangements, or collaborative marketing efforts (like the producer groups forming in several states to pool beef-cross calves for better marketing leverage), paths forward exist. The dairy industry has weathered significant challenges over the decades — the 1980s farm crisis, the 2009 collapse, the 2020 pandemic disruptions. This situation, while unique in certain aspects, represents another test of our collective resilience.

The fundamentals remain constant: understand your actual costs (not what you hope they are or what someone projected they’d be), know your markets (both what you’re selling into and buying from), and base decisions on real data rather than projections. Every farm faces unique circumstances — facilities, labor availability, local markets, financial position. But understanding broader patterns helps inform better individual decisions.

We really are navigating this together. The conversations at co-op meetings, information shared at winter dairy conferences, neighbor-to-neighbor discussions over fence lines or at the feed store — that’s how our industry has always moved forward. Whether you’re milking 50 cows or 5,000, whether you’re in Vermont or California, we all face these markets together.

These are certainly interesting times. But with solid information, realistic planning, and thoughtful adaptation, operations will find their way through. That’s what we do, isn’t it? We observe, we adapt, we support each other, and we keep moving forward.

Always have. Always will.

KEY TAKEAWAYS:

Contract heifer growing arrangements can reduce replacement uncertainty by 100% while typically costing 20-25% less than panic buying on spot markets — Wisconsin and Minnesota growers report strong interest in 18-24 month contracts at $2,800-$3,200 delivered, providing both parties predictable cash flow

Strategic genomic testing at $35-45 per animal enables precision breeding that maintains genetic progress while capturing beef revenue — bottom 20% get beef semen, middle 50% conventional dairy, top 30% sexed semen, optimizing both cash flow and herd improvement

Regional market variations create opportunities smart operators are exploiting — California’s integrated systems negotiate direct contracts while Midwest co-ops pool beef-cross calves for 15-20% better premiums than individual marketing

Risk management tools like LRP-Dairy provide price floor protection that costs $15-25 per head but prevents catastrophic losses when replacement markets spike or cull values crash — essentially disaster insurance for volatile times

The optimal breeding ratio depends on your conception rates, culling patterns, and local markets — 60/40 might work with excellent reproduction, but operations with challenges find 70/30 provides essential cushion against today’s $3,800 replacement reality

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Top Strategies for Successful Dairy Cattle Breeding: Expert Tips and Insights – This tactical guide reveals how to implement genomic selection, embryo transfer, and sexed semen to strategically improve your herd’s genetics, providing actionable steps to build a more profitable and resilient breeding program that complements the main article’s focus.

2025 Dairy Market Reality Check: Why Everything You Think You Know About This Year’s Outlook is Wrong – This article provides a strategic market overview, with specific data on the “component revolution” and new processing capacity. It helps progressive producers understand the changing economic landscape and shows how to position their farms for profitability beyond traditional volume-based thinking.

Robotic Milking Revolution: Why Modern Dairy Farms Are Choosing Automation in 2025 – Discover how investing in robotic milking systems can solve the labor crisis and provide a significant ROI. This piece offers a deep dive into how technology can create efficiencies and reduce long-term costs, complementing the main article’s discussion of strategic adaptation.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Smart dairy farms treat government shutdowns like weather events: predictable, manageable, profitable