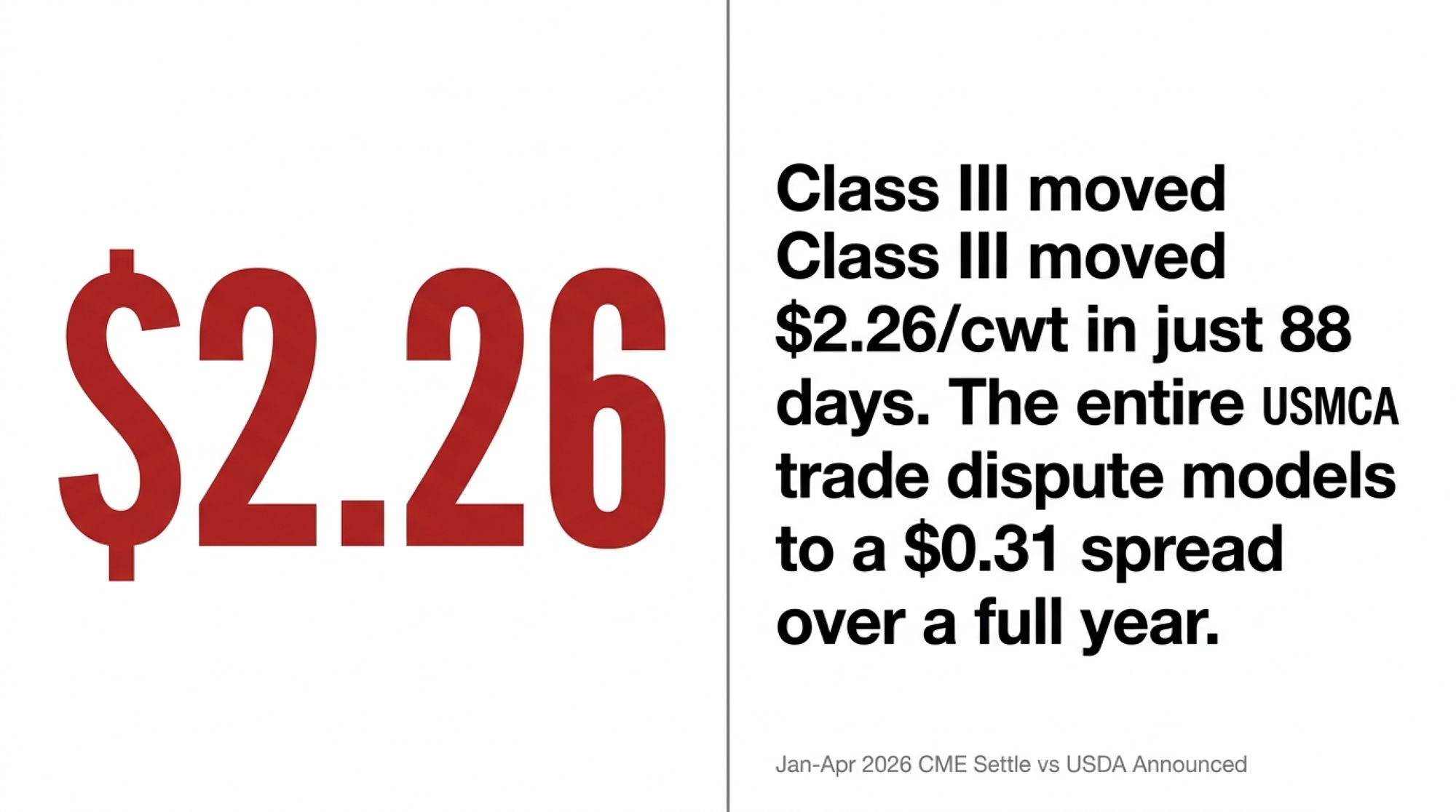

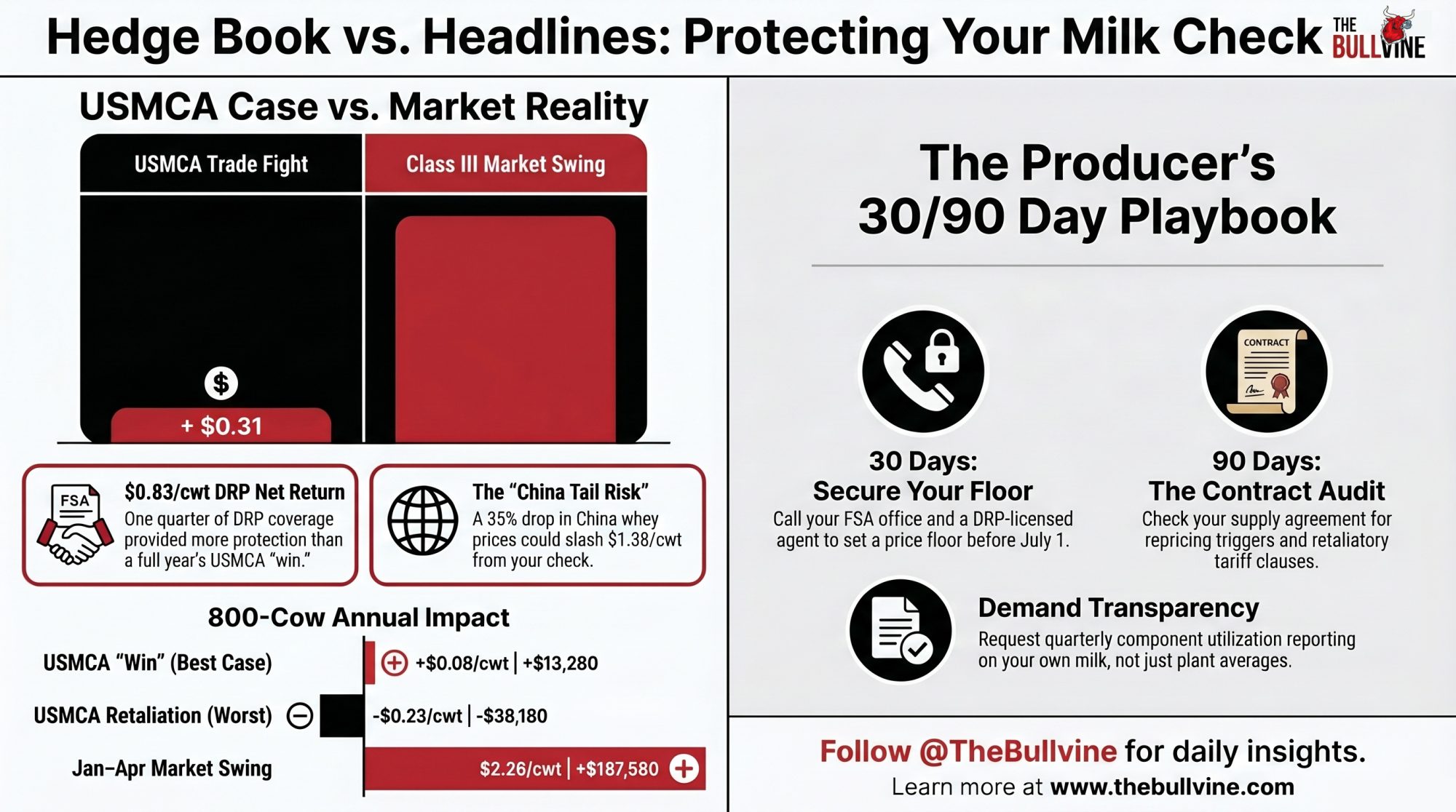

Class III moved $2.26/cwt in 88 days. The entire USMCA enforcement case Morris is running models to $0.31/cwt over 12 months. Guess which one clears your September check.

Executive Summary: Class III moved $2.26/cwt between January’s $14.59 announced price and the April 28, 2026, CME settle near $16.85 — roughly $187,580 of revenue swing on an 800-cow Northeast cheese herd’s Q3–Q4 book, no diplomats required. The entire NMPF/USDEC enforcement case Shawna Morris is running into the July 1 USMCA Joint Review models to a $0.31/cwt total scenario spread over 12 months: +$0.08 best case, -$0.23 worst case, author-modeled off published transmission coefficients and 2024 FAS GATS volumes. HighGround Dairy’s April 22 print shows Q1 2026 DRP netted $0.83/cwt — one quarter of coverage delivered more protection than the maximum USMCA “win” scenario delivers in a year. The real tail risk nobody’s pricing sits in Other Solids: a 35% China whey-price drop runs -$1.38/cwt on Class III, and it stacks on top of Scenario C, not instead of it. Producers with Q3–Q4 2026 contract renewals and unhedged milk are carrying the highest exposure — the 30/90/365 playbook inside starts with an FSA call today and a Contract Audit checklist for the September repricing clause you may not have read. The diplomats control the headline. Your hedge book controls the revenue.

Class III moved $2.26/cwt between the $14.59/cwt January 2026 USDA AMS announced price and the April 28, 2026, CME April-contract settle near $16.85/cwt. On an 800-cow Northeast cheese-oriented operation shipping roughly 83,000 cwt across Q3 and Q4, that’s 7,580 of revenue swing on half a year’s production — a volatility reference point, not a forecast. The market doing what markets do, no diplomats required.

In the 63 days between today and the July 1, 2026, USMCA Joint Review required under Article 34.7, the NMPF and USDEC enforcement push Shawna Morris has led is worth, on the barn math below, about $0.31/cwt of total scenario spread over 12 months.

The USMCA dairy 2026 fight is real. It’s also not the number that determines whether you make your debt service this fall.

Ted Vander Schaaf, an Idaho producer and Northwest Dairy Association member-owner, made the institutional case on February 12, 2026, before the Senate Finance Committee on behalf of USDEC, asking Congress to treat July 1 as the window to fix what USMCA promised American producers. The case is real. The September milk check is a separate timeline.

What Shawna Morris’s USMCA Enforcement Case Is Actually Asking For

Morris, EVP of Trade Policy and Global Affairs at NMPF, has pressed the enforcement case publicly for three years. The joint comments NMPF and USDEC submitted on October 31, 2025, for the USMCA Review lay out the mechanism: Canada’s TRQ architecture awards most of the quota in each of 14 dairy categories to Canadian producers of the product in question, forcing US exporters to sell largely to their own Canadian competitors. Morris escalated the same case at the USTR USMCA operation hearing on December 3, 2025, backed the same day by a bipartisan letter from 74 US House members to USTR Jamieson Greer.

The NMPF/USDEC filing documents fill rates as low as 3% on skim milk powder (TRQ-CA3), 8% on milk protein concentrates (TRQ-CA12), 12% on yogurt and buttermilk (TRQ-CA7), 21% on whey powder (TRQ-CA8), 51% on cream (TRQ-CA2), and 59% on industrial cheese (TRQ-CA5). A 20-to-30-point fill-rate gain — moving under-utilized TRQs toward a 70–80% band — is the volume recovery the filing targets.

Dairy Farmers of Canada has pushed back hard. In a March 8, 2025, statement, DFC President David Wiens argued the US “secured substantial tariff-free access to the Canadian dairy market” under USMCA and that the US “enjoys a significant dairy trade surplus with Canada, exporting 7.5 million CAD in dairy products while importing 7.9 million CAD in return.” The June 2025 passage of Bill C-202 further limits Canada’s ability to offer supply-managed concessions in future trade negotiations. The access exists. The access isn’t being fully used. Both positions hold.

Neither one pays your September note.

What Does a $0.31/cwt USMCA Dairy 2026 Spread Actually Mean for Your 800-Cow Herd?

The $0.31/cwt figure is load-bearing for every hedge decision downstream, so it has to hold up.

Published dairy price-transmission literature supports a working coefficient in the low-single-digit cents/cwt range for each 1% of incremental US dairy export volume. Apply that to the TRQ-recovery volume and a Class III discount — cheese-and-whey routes transmit tighter than all-milk because butter and powder share less of the Class III formula — and the midpoint on a US enforcement win lands near +$0.08/cwt. That is author modeling, not a published coefficient, and the methodology note at the end of this piece spells out every assumption behind it.

A failed-talks and retaliation scenario lands near -$0.23/cwt on the same framework, modeled on a 15–25% reduction in 2024 US-to-Canada dairy exports (C$877.5M; roughly US$640M in 2024 annual-average exchange rates per Bank of Canada). Canada retained meaningful counter-tariff authority from the C$30 billion March 4, 2025, list of US goods subject to 25% tariffs, with the updated list effective September 1, 2025.

Total scenario spread: $0.31/cwt, best case to worst case, over 12 months. Author modeling. Not a projection.

The Comparison That Actually Matters

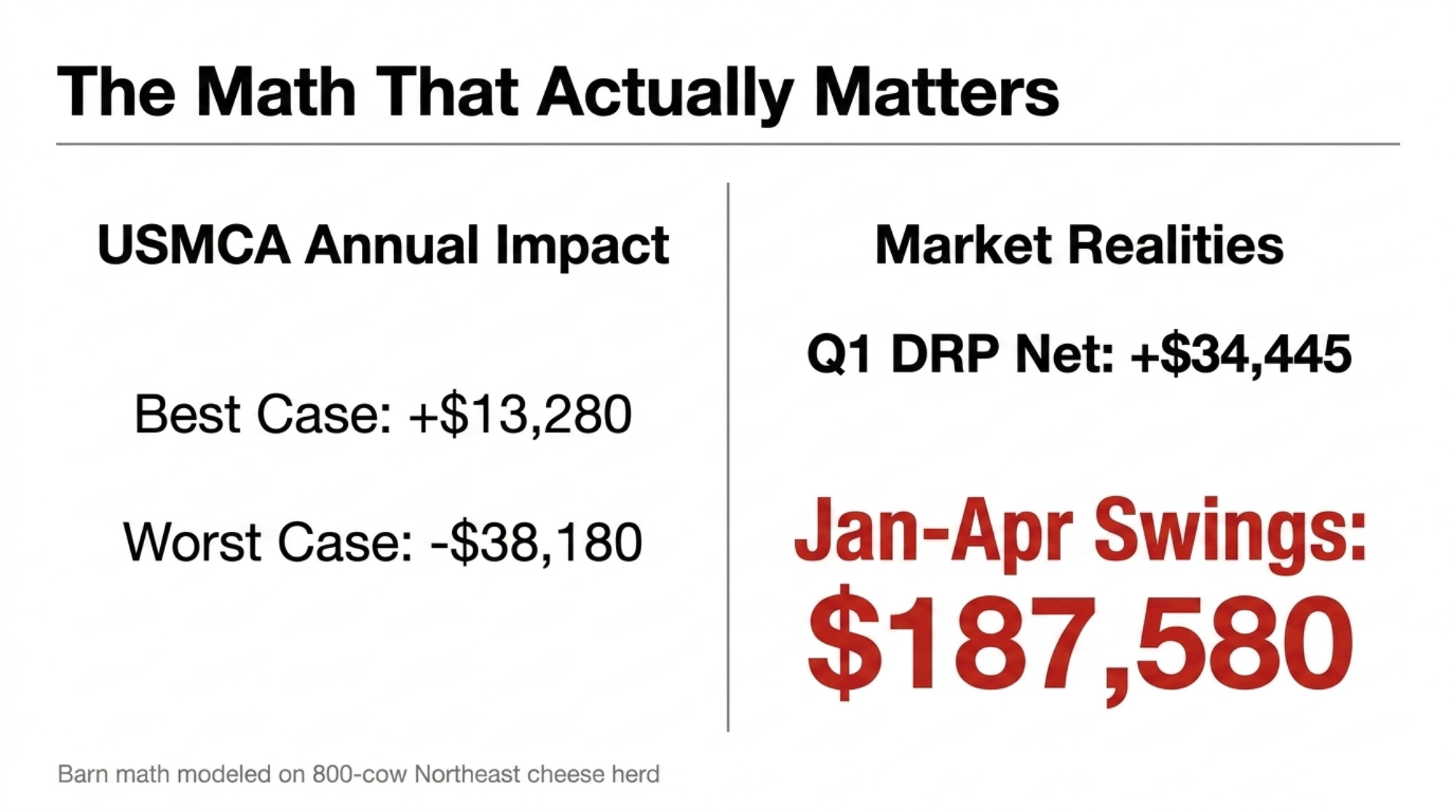

| Scenario | Per cwt Impact | 800-Cow Annual Impact |

| USMCA Win (Best Case) | +$0.08 | +$13,280 |

| USMCA Retaliation (Worst Case) | -$0.23 | -$38,180 |

| Total USMCA Scenario Spread | $0.31 | $51,460 |

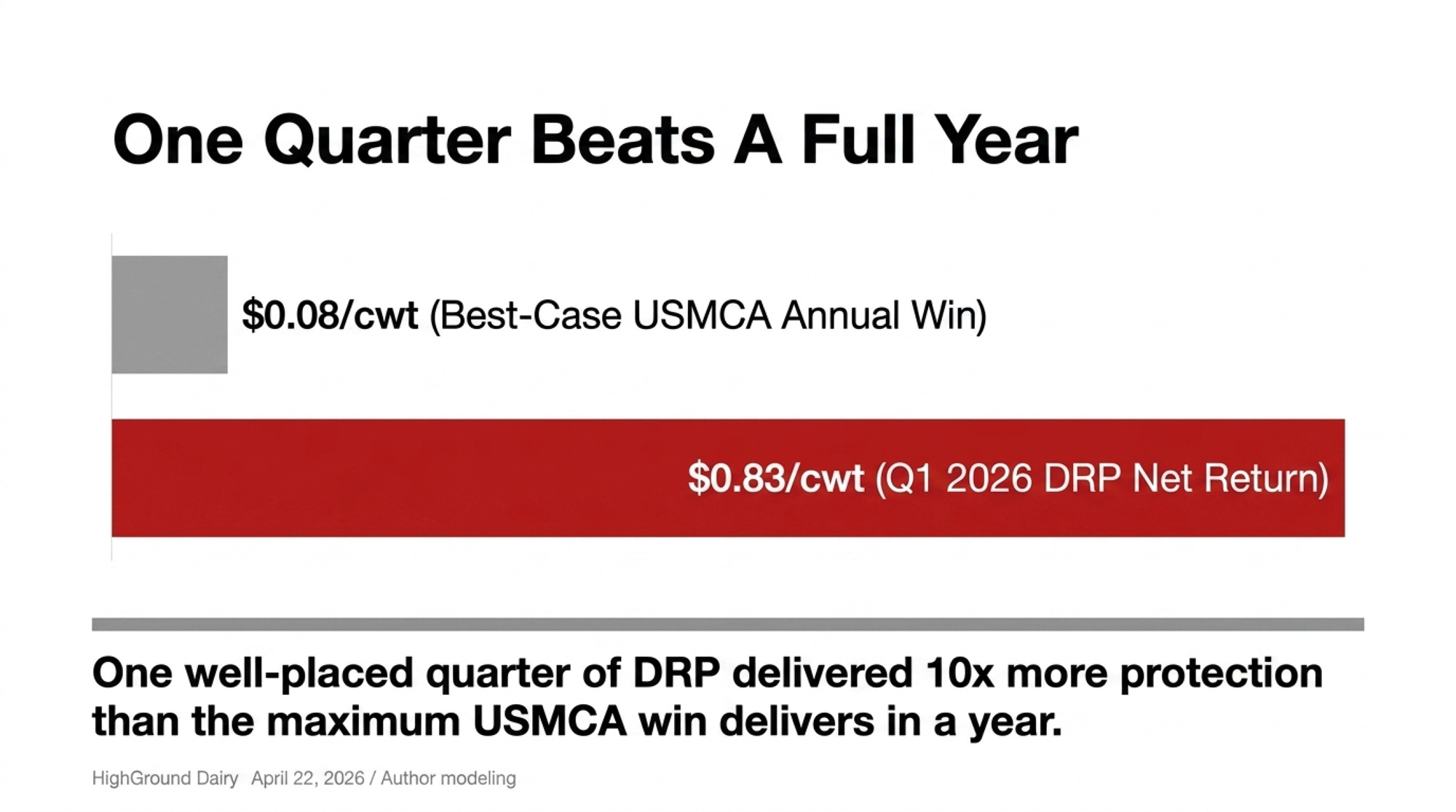

| Q1 2026 DRP Net Return | +$0.83 | +$34,445 (one quarter) |

| Jan–Apr 2026 Class III Movement | $2.26 | $187,580 (half year) |

Bottom line: one well-placed quarter of DRP delivered more protection than the entire USMCA “win” scenario delivers in a year. HighGround Dairy’s Q1 2026 DRP results, published April 22, 2026, report estimated indemnities averaging $1.12/cwt against premium costs of $0.28/cwt. HighGround’s five-year review (2019–2023) shows DRP averaged $0.30/cwt in premiums and $0.53/cwt in indemnities, a net gain of $0.23/cwt and a $1.78 return on every $1 of premium.

Running the Numbers

Barn math: 800-cow Northeast cheese-oriented operation, 12 months ending Q4 2026

Production inputs (illustrative Northeast anchor — substitute your own cwt/cow):

- 57 lbs/cow/day working anchor (USDA NASS Milk Production 03/20/2026 reports January 2026 U.S. 24-state average at 2,068 lbs/cow/month, or ~68 lbs/day; PA January 2026 production totaled 817 million lbs with an 11,000-head cow decline year-over-year)

- 57 × 365 ÷ 100 = 208.05 cwt/cow/year

- 800 cows × 208 cwt = ~166,000 cwt/year

- Q3 + Q4 combined: ~83,000 cwt

Volatility reference (Jan–Apr 2026 actual):

- Class III Jan 2026 announced ($14.59/cwt) → April 28, 2026, front-month (~$16.85/cwt): $2.26/cwt over 88 days

- Applied to 83,000 cwt: $187,580 revenue swing — reference, not a prediction

DRP reference (Q1 2026 actual per HighGround):

- Net return $0.83/cwt × Q1 production (~41,500 cwt) = +$34,445 in one quarter for covered producers

Scaling the 12-month USMCA scenario spread at $0.31/cwt to your herd:

| Herd Size | Annual cwt | USMCA Scenario Spread |

| 400 cows | 83,200 | $25,792 |

| 800 cows | 166,000 | $51,460 |

| 1,200 cows | 249,600 | $77,376 |

Pull your last three milk checks, calculate your actual cwt shipped per cow, apply the +$0.08 upside and the -$0.23 downside, and compare the result to what your Q1 2026 DRP coverage paid — or would have paid.

Why Vander Schaaf’s Testimony and a Hedge Book Aren’t the Same Argument

The split between institutional timelines and individual hedge timelines isn’t something trade-group messaging usually spells out.

Vander Schaaf’s Senate Finance testimony addressed a 10-year structural question about USMCA’s enforcement architecture. That question is real. A producer in his position still faces the same 63-day hedge window every other US producer is sitting in. Q3 milk that needs to be priced. A Q4 contract that’s either hedged or isn’t. Cheese markets moving week to week.

NMPF’s enforcement case runs on a 10-year structural horizon. A US dairy producer’s Q3 check clears in September. Both things are true at once.

The processor conflict inside the TRQ system sharpens the split further. The TRQ architecture gives any processor with cross-border manufacturing options sourcing flexibility domestic-only competitors don’t have. Saputo — one of the top three US cheese producers, with US plants spanning Wisconsin, New Mexico, and beyond — Agropur (operating 39 North American plants and moving 6.1 billion litres/year), and Lactalis sit among the cross-border manufacturers whose bilateral US–Canada footprints create material Scenario C retaliation exposure. The question for a producer is whether your own processor’s public position on enforcement aligns with where your milk actually earns.

The Second Front: China Tail Risk Nobody Is Pricing

If the USMCA is the “known” variable producers are watching, the China tail risk is the “unknown” that could swallow the USMCA spread three times over.

China was the US dairy sector’s second-largest export destination outside Mexico in 2024, with dry whey products and lactose the dominant lanes, per USDA FAS Beijing’s Dairy and Products Annual (October 22, 2024) and FAS PSD World Markets and Trade circulars. In April 2025, China’s retaliatory tariffs on US dairy reached 84%, explicitly including whey and lactose — covered in The Bullvine’s April 10, 2025, analysis. FAS Beijing’s May 20, 2025, semi-annual reported China’s whey imports would decline in 2025 “due to China’s retaliatory tariffs on U.S. origin product.” “China takes a lot of US whey products — dry whey, whey protein concentrates, permeate, lactose,” Phil Plourd of Ever.ag said in the April 2025 cycle. “Today, we’re up to 84%, making things more challenging.”

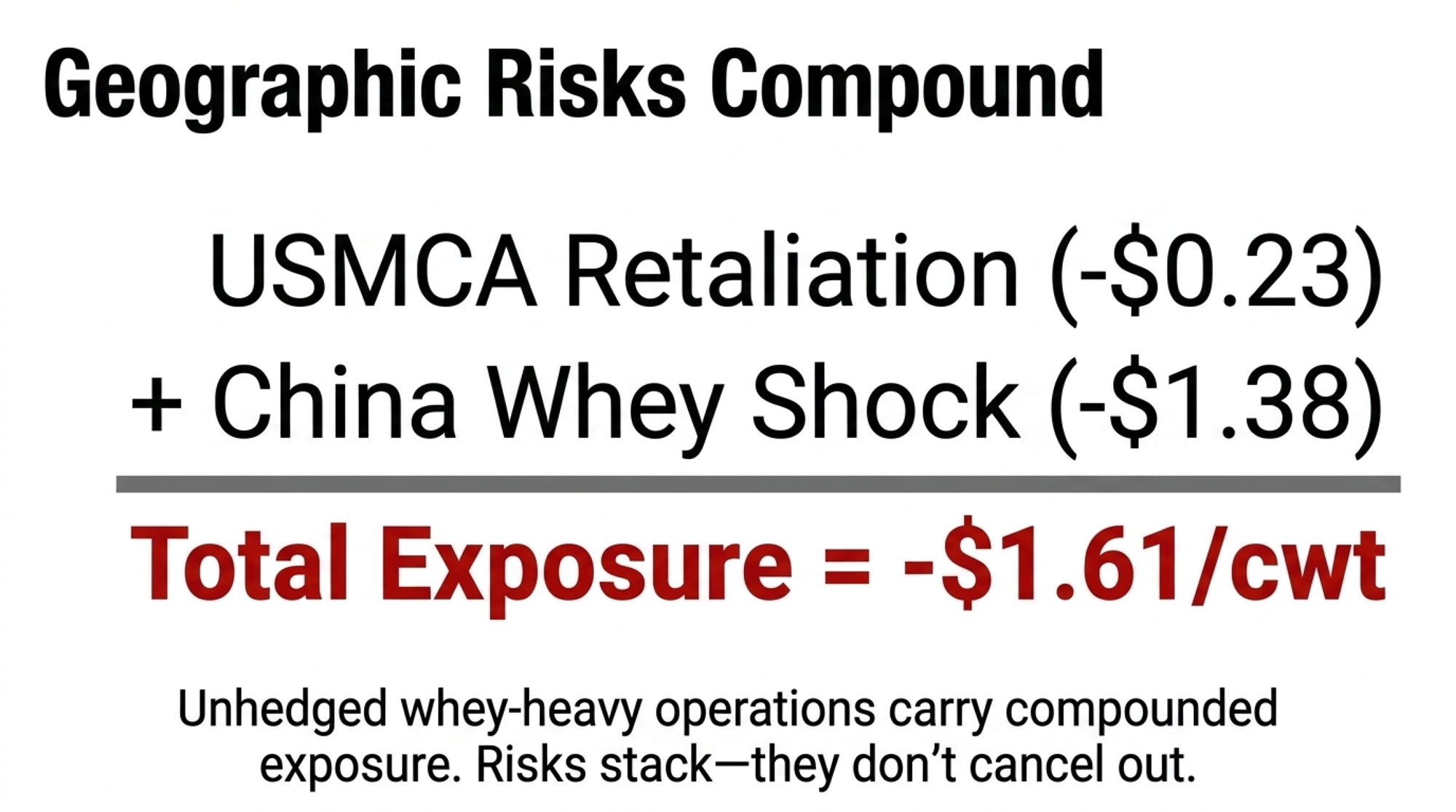

Apply a working model — not a prediction — to April 2026 dry whey pricing near $0.649/lb (USDA AMS Dairy Products Sales Report, week ending April 18, 2026). The Federal Order Class III Other Solids formula runs (dry whey price − $0.2668) × 1.03. At $0.649/lb, Other Solids prices at $0.3939/lb; at $0.4219/lb after a 35% whey drop, Other Solids drops to $0.1596/lb. The delta of $0.2343/lb applied to 5.9 lbs of other solids per cwt (Federal Order standardized factor, USDA AMS FMMO) equals roughly -$1.38/cwt Class III. On a 1,000-cow Midwest whey-heavy operation at 208 cwt/cow (~208,000 cwt/year), that’s -$287,040 annualized.

Critical framing: this -$1.38/cwt China whey shock is additive to any USMCA losses, not alternative to them. A producer modeling the worst case stacks Scenario C’s -$0.23/cwt on top of a -$1.38/cwt whey shock for a combined -$1.61/cwt exposure. These risks can and do compound.

Sensitivity the other way: a 20% whey-price drop lands closer to -$0.79/cwt; a 50% drop pushes past -$1.97/cwt. The 35% draw is a midpoint sensitivity, not a ceiling.

That’s not the USMCA fight. That’s the USMCA fight plus the tail nobody in the current trade press coverage is pricing.

The Cooperative “Wait and See” Conversation

Before any hedge decision works, name the advice pattern that can block it. “Wait and see on Q3 coverage because things might improve after the review” is advice worth examining.

Co-ops and their field representatives balance multiple interests — member retention, logistics, plant utilization, and member margins. Independent DRP agents and ag lenders often point out that those interests don’t always line up one-to-one with a single producer’s hedge economics. That doesn’t make co-op advice bad. It makes it one input among several worth weighing.

Cooperative pooling delivers real benefits individual risk management can’t: spread risk, logistics leverage, steadier pay timing. The point isn’t that pooling is bad. The point is that pool-level price optimism isn’t the same as your farm-level risk management.

Run the asymmetry. HighGround’s five-year review shows DRP premiums averaged $0.30/cwt, with Q1 2026 running lighter at $0.28/cwt. The cost of being wrong on an unhedged 83,000 cwt Q3+Q4 book, against a $1.00/cwt market correction, is $83,000. The $2.26/cwt move that already happened between January and late April 2026 would have been $187,580 on half-year production. Producers who carried DRP coverage into Q1 2026 netted $0.83/cwt after premiums, per HighGround. Producers without coverage didn’t capture that return.

The numbers tell you to carry coverage and stop watching the diplomatic calendar for hedge signals.

The 30/90/365-Day Playbook for 800-Cow Herds Heading Into July 1

30-Day Actions (before May 29, 2026)

- Call your FSA county office today. Get the exact Q3 2026 DRP enrollment deadline in writing or with an RMA confirmation reference. The window closes before July 1 — the same date as the USMCA Joint Review required under Article 34.7.

- Call a DRP-licensed insurance agent from the USDA RMA Agent Locator, not your co-op field rep. Ask for three specific numbers at 95% coverage: net premium per cwt after subsidy, effective price floor, and total cost on your declared Q3 production. Premium benchmarks land near the $0.28–$0.30/cwt HighGround five-year range; use that as a sanity check on the quote.

- Pull your Class III utilization percentage from co-op member services. Not your field rep — member services. A 75%+ Class III operation runs different coverage economics than a 55/30/15 blended one.

Red-flag trigger: If CME cheddar blocks break below your risk advisor’s established reassessment threshold, add coverage the same day.

Where it backfires: If your DSCR has been under 1.2 for three consecutive months on your lender’s covenant method, premium dollars compete with operating line headroom. Call your lender before the insurance agent.

90-Day Actions (through late July 2026)

The Contract Audit — pull your supply agreement and check:

- [ ] Does it address retaliatory tariffs (US-imposed or Canada-imposed) and is there a pricing-review trigger?

- [ ] What is the notice period for non-renewal?

- [ ] Is the repricing mechanism spot, formula, or blend?

- [ ] Is the over-order premium fixed, variable, or floored?

- [ ] Does it guarantee quarterly component utilization reporting on your own milk?

- [ ] What is the effective date of the current terms and when does the next window open?

Other 90-day moves:

- Draft a trade-outcome review clause for the renewal. Suggested language: “If the United States imposes retaliatory tariffs on Canadian dairy products, or Canada imposes retaliatory tariffs on US dairy products, either party may request a pricing review within 30 days.” It doesn’t guarantee outcomes. It guarantees a seat at the table if Scenario C activates.

- Request quarterly component utilization reporting on your own milk. Not plant economics — your own payment breakdown by component. The ask is legitimate under Federal Order component pricing transparency.

What this requires: A copy of your current contract, your co-op member services contact, and — if the conversation gets serious — an ag contract attorney who works on dairy supply agreements.

Where it backfires: Going in without Q3 hedging in place. Processors know renewal deadlines. Negotiating a 2027 extension with uncovered Q3 milk is negotiating from need, not from position.

365-Day Moves (positioning for the next cycle)

- Build a Q3–Q4 2027 hedge ladder now, not in May 2027. HighGround’s research finds DRP coverage secured three quarters out delivered the highest average net return in Q1 2026 at $1.53/cwt — four and five quarters out returned $1.37 and $1.28 respectively. Laddered DRP or Class III put coverage through Q4 2027 costs premium dollars but caps tail risk and historically pays for itself.

- Evaluate processor optionality. If your operation runs 75%+ Class III and your co-op’s over-order premium structure doesn’t reflect that concentration, a specialty processor relationship may align your milk more cleanly with your hedge strategy. The trade-off: you lose pooling diversification and take on concentration risk against a single processor.

- Track China dairy tariff status monthly. USDA FAS Beijing publishes updates. The signal to watch is whether Chinese importers continue the cost-sharing arrangement absorbing partial tariff pass-through. When that breaks down, whey volume drops within 60–90 days.

Opportunity signal: If your co-op’s over-order premium widens by $0.20/cwt or more in the second half of 2026 while your feed-cost basis holds within $0.40/cwt of current levels, you have room to renegotiate contract term length from 12 months to 24 months at better component premiums.

What Does Your Current Contract Say About the 63 Days You Can’t See Yet?

NMPF’s enforcement push continues through July 1. The testimony is on the record. On April 22, 2026, the Globe and Mail reported Prime Minister Mark Carney rejecting the notion the US “dictates the terms” of USMCA talks, with Finance Minister Dominic LeBlanc telling the paper: “We’re not going to reopen supply management and have a discussion around quotas in the supply managed sector.” That same morning, USTR Jamieson Greer told the House Ways and Means Committee that Canada has made no commitments to alter its largely closed dairy market and that the dispute will be resolved through USMCA negotiations or through enforcement actions. Bill C-202, passed in June 2025, further narrowed Canada’s ability to concede on supply-managed goods. All of that is real. None of it changes what your Q3 milk ships at.

The trade fight is worth $0.31/cwt in total scenario spread over 12 months. Your hedge book is managing a revenue stream that moved $2.26/cwt in the first 88 days of 2026 alone. Both deserve your attention. They don’t deserve equal attention.

Pull your contract today. Find the clause that governs how your September repricing actually works. Call FSA this afternoon. Call a DRP-licensed agent tomorrow morning. Call member services by Friday.

What does your current contract say about what happens to your over-order premium if retaliatory dairy tariffs get imposed between now and your September renewal date? If the answer is nothing — or if you don’t know — that’s the line item worth more attention this week than any USTR press release.

Your hedge book controls your revenue. The diplomats control the headline. Know the difference.

Methodology sidebar: Scenario B and Scenario C midpoints are author modeling informed by published dairy price-transmission literature and USDA FAS GATS 2024 trade data. The +$0.08/cwt Scenario B midpoint reflects a Class III discount applied to a working all-milk export-transmission coefficient and a ~1.2% export-volume recovery drawn from TRQ fill-rate gains on cream and industrial cheese. The -$0.23/cwt Scenario C midpoint is drawn on a 15–25% reduction in 2024 US-to-Canada dairy exports. Neither midpoint is a published figure. Outcomes are not predictions. All dollar figures scale linearly with herd-level cwt shipped; substitute your own production inputs for a farm-specific result. A Q2 2026 follow-up in The Bullvine’s “Hedge Book vs the Headline” series will revisit these scenarios against the post-July-1 review record.

Key Takeaways

- The entire NMPF/USDEC enforcement push Morris is running into July 1 models to $0.31/cwt of scenario spread over 12 months. Class III has already moved $2.26/cwt this year. Don’t confuse the headline with the hedge.

- One quarter of Q1 2026 DRP netted $0.83/cwt per HighGround — more protection than the maximum USMCA “win” scenario delivers in a full year. If you’re unhedged on Q3–Q4, call a DRP-licensed agent before you call anyone else.

- The real tail sits in Other Solids. A 35% China whey-price drop runs -$1.38/cwt on Class III, and it stacks on top of Scenario C, not instead of it — whey-heavy Midwest operations carry the compounded exposure.

- If your Q3 or Q4 2026 contract is up for renewal, run the Contract Audit before July 1: repricing mechanism, over-order premium structure, and a trade-outcome review clause that gives you a seat at the table if tariffs land.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- 84% Chinese Tariffs Slam US Dairy: Why Whey & Lactose Exports Face Crisis — Arms you with a survival strategy for the “Second Front” of the trade war. This analysis reveals how 84% tariffs make U.S. whey uncompetitive overnight, risking $584 million in annual exports and crashing Class III prices.

- USMCA 2026: The $200M Question – Why Only 42% of U.S. Dairy Access to Canada Gets Used — Exposes the loophole Canada uses to design allocation rules that favor domestic processors over American exporters. It delivers a 3-year roadmap for turning paper-only access into real orders during the formal 2026 review.

- $146,000: The Trapdoor Under the 2026 U.S. Dairy Rally — Dismantles the “wait and see” approach by modeling a $146,000 avoidable exposure for unhedged 500-cow herds. It follows the money on fuel and fertilizer inflation, proving that outdated input budgets hit harder than trade headlines.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.