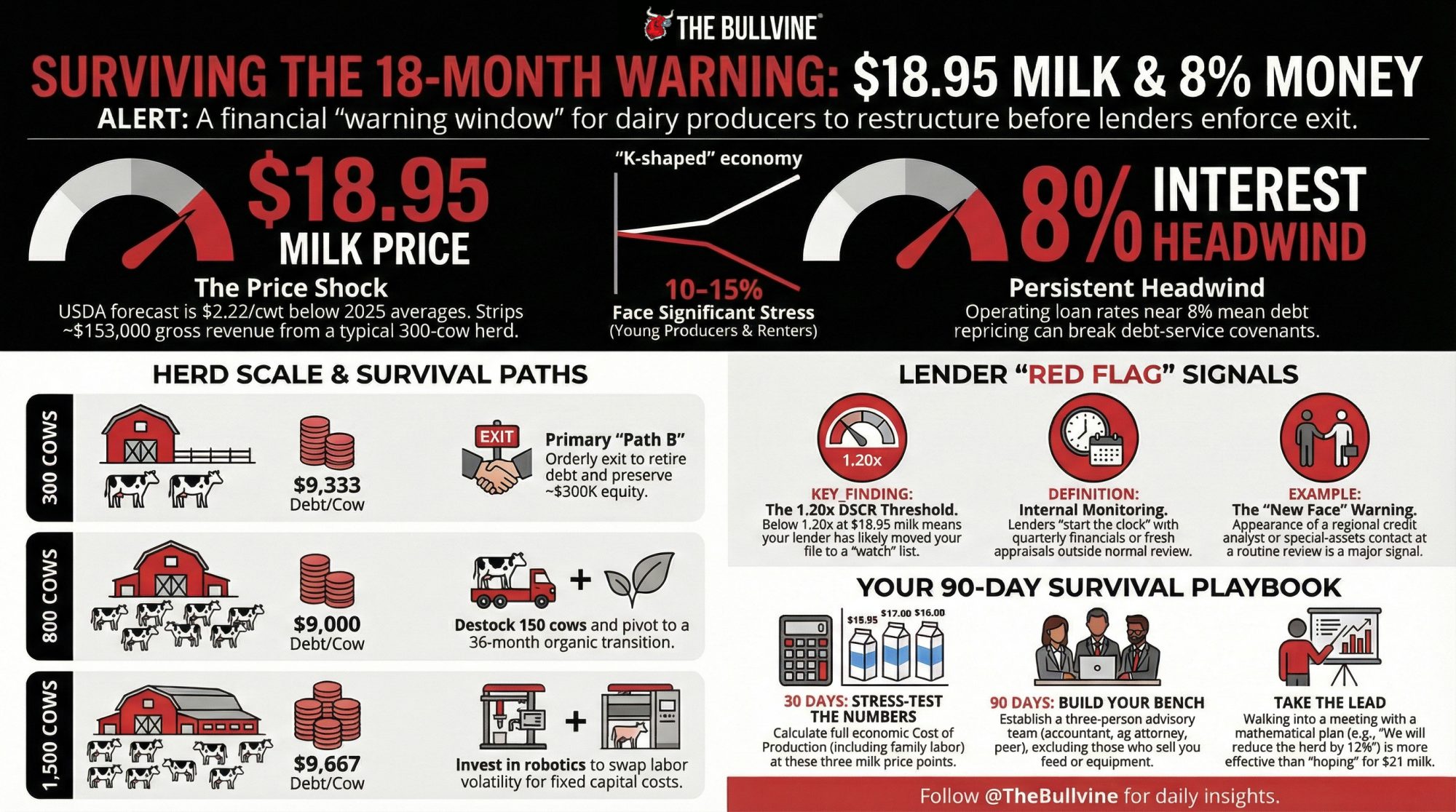

Cornell’s bottom‑quartile dairies sit at 0.36× DSCR. At 7% money on $4.5M of repriced debt, that’s about $118,000 more a year — and the reason your loan officer opened the laptop instead of the yellow pad.

Executive Summary: Commercial ag operating rates sat in the mid‑7% range through late 2025 and early 2026, and Cornell’s 2023 DFBS shows the lowest‑profit quartile of New York dairies running a 0.36× DSCR — the exact number sending “good customer” files to the watch list. On $4.5M of repriced debt spread across real estate, equipment, and an operating line, the jump from 3.5–4% money to 7–8% adds roughly $118,000 a year in required payments, or about $1.07/cwt on a 400‑cow herd shipping 110,000 cwt. At USDA’s early‑2026 all‑milk forecast of $18.95/cwt, that same herd barely clears 1.0× DSCR; you need $20+ milk to breathe. Re‑amortizing a $1.8M parlor note from 14 to 25 years at 7.25% frees about $47,000 a year in cash flow — enough to pull a file out of the red, at the cost of more lifetime interest. Lenders aren’t firing bad customers; their models are. The farms getting flexibility walk in with a rolling 12‑month cost per cwt, their own DSCR math, a stress test at $17 milk, and at least one non‑correlated revenue line — beef‑on‑dairy, custom heifers, crop sales — that the dashboard can see. If your DSCR sits below 1.15× today and you can’t list every note and index on one page, your loan officer has more clarity on your risk than you do — and the next 30 days are when that changes.

Picture a gray February morning in central Wisconsin. A third‑generation dairyman walks into his Farm Credit office carrying 30 years of loan statements and the quiet confidence of a guy who’s never missed a payment.

He’s expecting a handshake. A quick renewal. Maybe a short gripe about milk prices over bad coffee.

Instead, the loan officer — younger, laptop already open — pulls up a screen. The numbers don’t work the way they used to. Red on debt service coverage. Yellow on working capital. A projected breakeven that has jumped nearly two bucks a hundredweight after a batch of loans repriced. For a 380‑cow herd, that’s not an abstract “dairy lending 2026” headline. That’s the morning the computer says no — and a family decides whether to catch up to the bank’s math or let the bank decide their future.

A note on these stories: The three dairies described below are illustrative composites, not real operations. They’re built from 2023–2026 industry patterns in Cornell’s Dairy Farm Business Summary, Chicago and Kansas City Fed ag credit surveys, and Bullvine case work. The math and thresholds are real. The names, scenes, and dialogue are not attributed to any specific producer. Real named sources — Nathan Kauffman at the Kansas City Fed and David Oppedahl at the Chicago Fed — are quoted or paraphrased only from their own published commentary and reporting by outlets like Brownfield Ag News. If you’re a producer willing to share your DSCR restructure story on the record, reach out — future “Dairy Lender Files” installments will feature real named operations.

The Day the Screen Replaced the Yellow Pad

For a long time, your dairy loan ran on three things: reputation, collateral, and whether your lender thought you kept a tight ship. You’d sit across from someone who knew your family and your fields. They’d scribble on a yellow pad, ask how the year went, and if you’d always paid your bills, the renewal slid through.

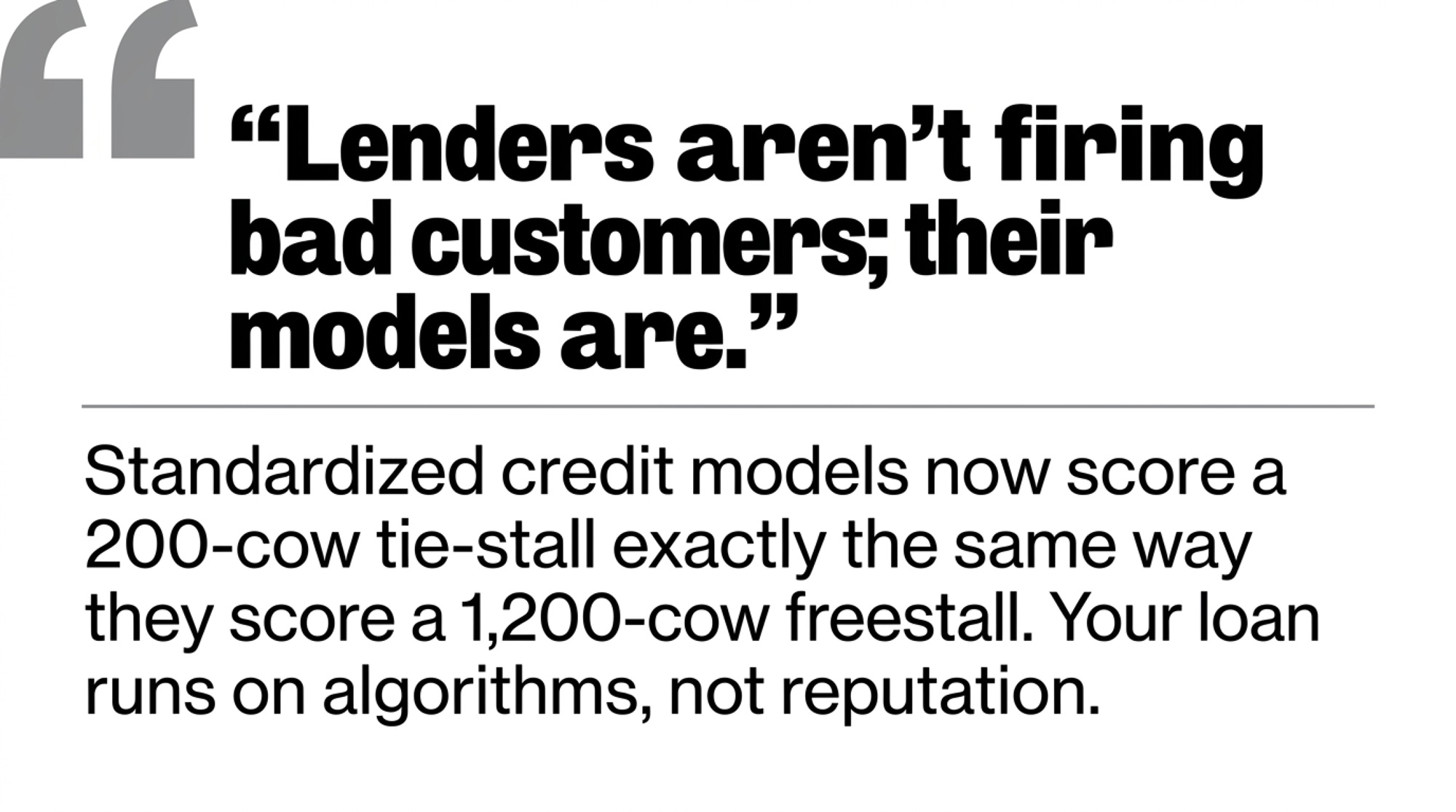

That world hasn’t vanished. It now sits underneath something colder — standardized credit models that score a 200‑cow tie‑stall in Minnesota the same way they score a 1,200‑cow freestall in New York.

Between 2015 and 2021, a lot of dairy debt went on the books at roughly 3.5–4.5% for conventional ag loans. Some FSA‑backed notes sat even lower. Then cheap money disappeared. The Chicago Fed’s 7th District AgLetter has pegged operating‑loan rates in the mid‑7% range and farm real‑estate loans in the high‑6% range through late 2025 and into early 2026 — still about double what many dairies locked in during their last expansion.

Those are effective rates on recently booked loans reported by participating banks — a blend of fixed and variable product. New paper is increasingly written as variable, typically priced as a spread over Prime or a term SOFR benchmark. Ask your lender which index your next renewal tracks. On a $3M loan, a 100‑basis‑point drift is roughly $30,000 a year in added interest; closer to $50,000 on $5M.

As of early 2026, USDA direct FSA operating loans sat in the mid‑4% range and ownership loans in the mid‑5% range — well below the commercial market, but only for borrowers who qualify. Check the current month’s FSA rate notice before you assume you’re priced in.

Kansas City Fed economist Nathan Kauffman told Brownfield Ag News in late 2025 that most producers can still service existing debt, helped by strong land values, but working capital is tight and some have already restructured heading into 2026. Chicago Fed policy advisor David Oppedahl has been more pointed in recent AgLetter commentary: repayment rates on non‑real‑estate loans are slipping, problem loans are creeping up, and roughly half of surveyed ag bankers expect more forced liquidations ahead.

At the system level, it’s “stress, not crisis.” At your kitchen table, sitting at 1.0× DSCR with repriced loans, that distinction feels academic.

What Your Lender’s Dashboard Actually Sees

When your lender opens your file, the model behind the screen scores you on ratios that sound cold but boil down to barn math once you cut the jargon. Every farm should be able to pull this snapshot in under five minutes.

The Dashboard Cheat Sheet

| Metric | Target (Strong) | Danger Zone | Where the Numbers Come From |

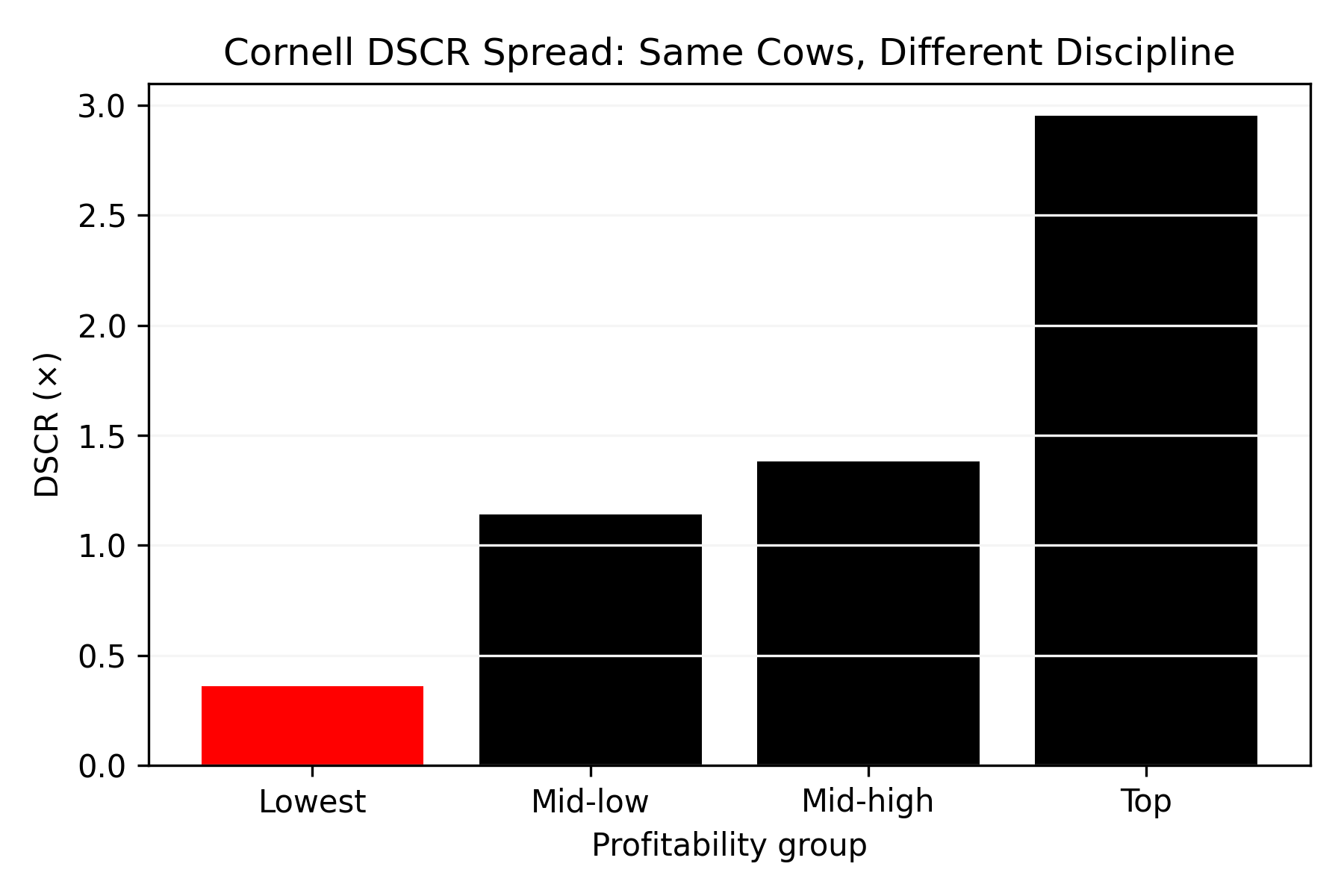

| DSCR | > 1.25× | < 1.0× | Cornell DFBS 2023: top group 2.95×, bottom 0.36× |

| Debt per Cow | < $3,500 | > $7,000 | Progressive Dairy “Dairy Dozen” benchmarks |

| Working Capital | > 25% of gross revenue | < 10% | OSU “15 Measures of Dairy Farm Competitiveness” |

| Debt‑to‑Asset | < 0.25 | > 0.40 | DFBS 2023 average 0.29; top group 0.21 |

Now the barn‑math version of each.

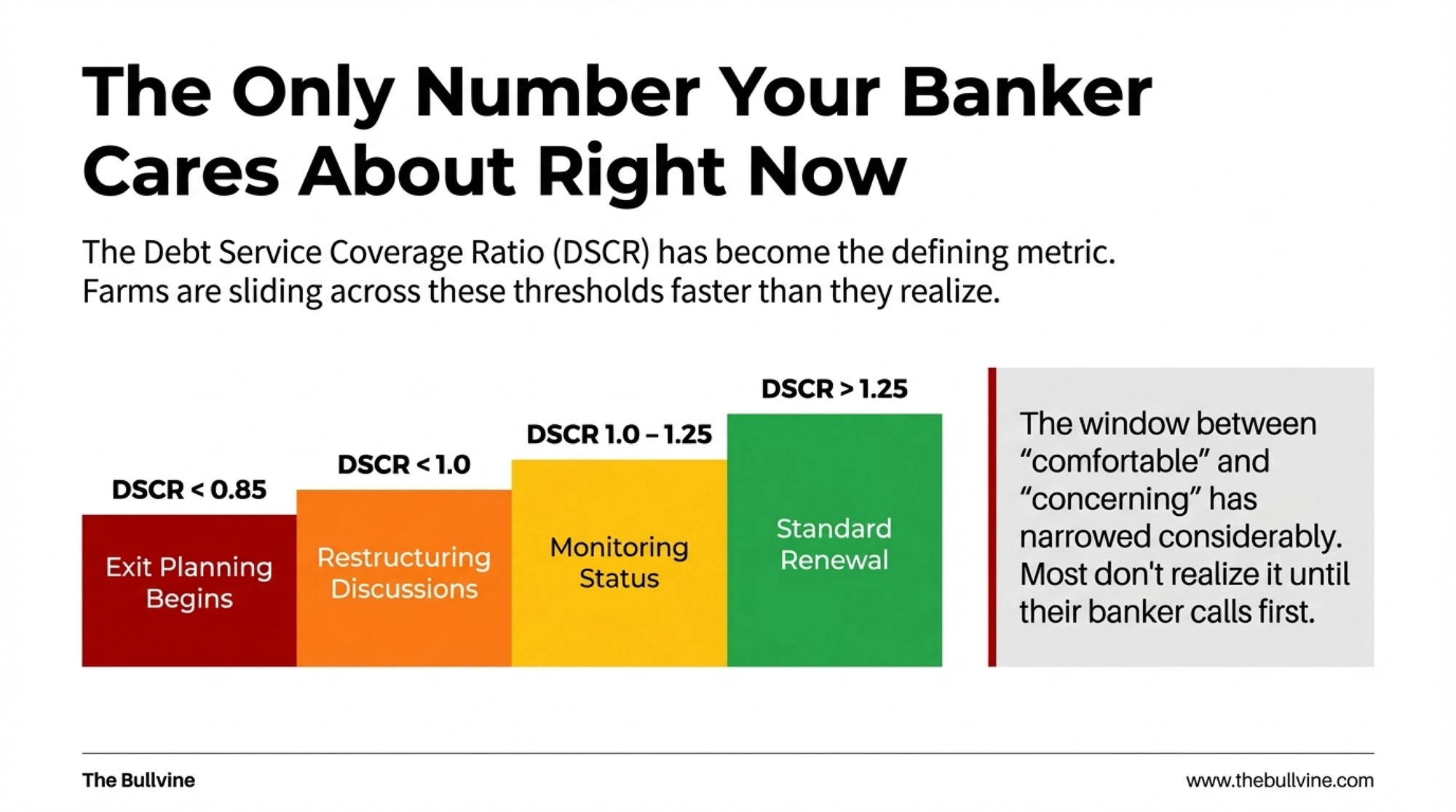

Debt service coverage ratio (DSCR). Net cash available for debt service divided by total annual principal and interest. A lot of lenders quietly target at least 1.25× as a comfort line. Cornell’s 2023 DFBS profitability comparison across 129 New York herds makes the spread vivid: the lowest‑profit group averaged just 0.36×, mid‑low hit 1.14×, mid‑high reached 1.38×, and the most profitable group sat at 2.95×. Below 1.0×, you’re not generating enough cash to cover your own debt.

| Profitability Group | DSCR (×) |

|---|---|

| Lowest | 0.36 |

| Mid‑low | 1.14 |

| Mid‑high | 1.38 |

| Top | 2.95 |

Working capital. Current assets minus current liabilities. Ohio State’s “15 Measures of Dairy Farm Competitiveness” calls anything above 25% of gross revenue competitive. In Brownfield’s 2025 coverage, Kauffman flagged working capital as the metric lenders are watching closest heading into 2026.

Debt per cow. Cornell’s lowest‑profit quartile carried about $5,007 of debt per cow versus roughly $3,097 for the top group — a gap of almost $1,900 per cow. Progressive Dairy’s “Dairy Dozen” benchmarks peg $3,000–$5,000 as manageable and flag $7,000 per cow as the point where servicing gets difficult.

Debt‑to‑asset ratio. The Cornell all‑farm DFBS average was 0.29 in 2023. Top‑profit farms ran about 0.21; the lowest‑profit group sat at 0.34. OSU flags anything above 0.30 as moving into higher‑risk territory.

Your grandfather knew these ratios. The difference? He had a year to fix them. You have a quarter.

The model pulls your numbers quarterly — sometimes monthly — and benchmarks them against thousands of farms in the bank’s footprint. Chicago Fed surveys through 2025 showed a rising share of 7th District banks reporting tighter collateral demands. If you’re not running these ratios yourself, your lender still is. You’re just not seeing the same screen.

Three Composite Farms, Three Outcomes

What follows are three composite dairy families — patterns, not people — built from 2023–2026 data in Wisconsin, New York, and Minnesota. Same industry, same rate environment. Very different results, depending on how they showed up at the bank.

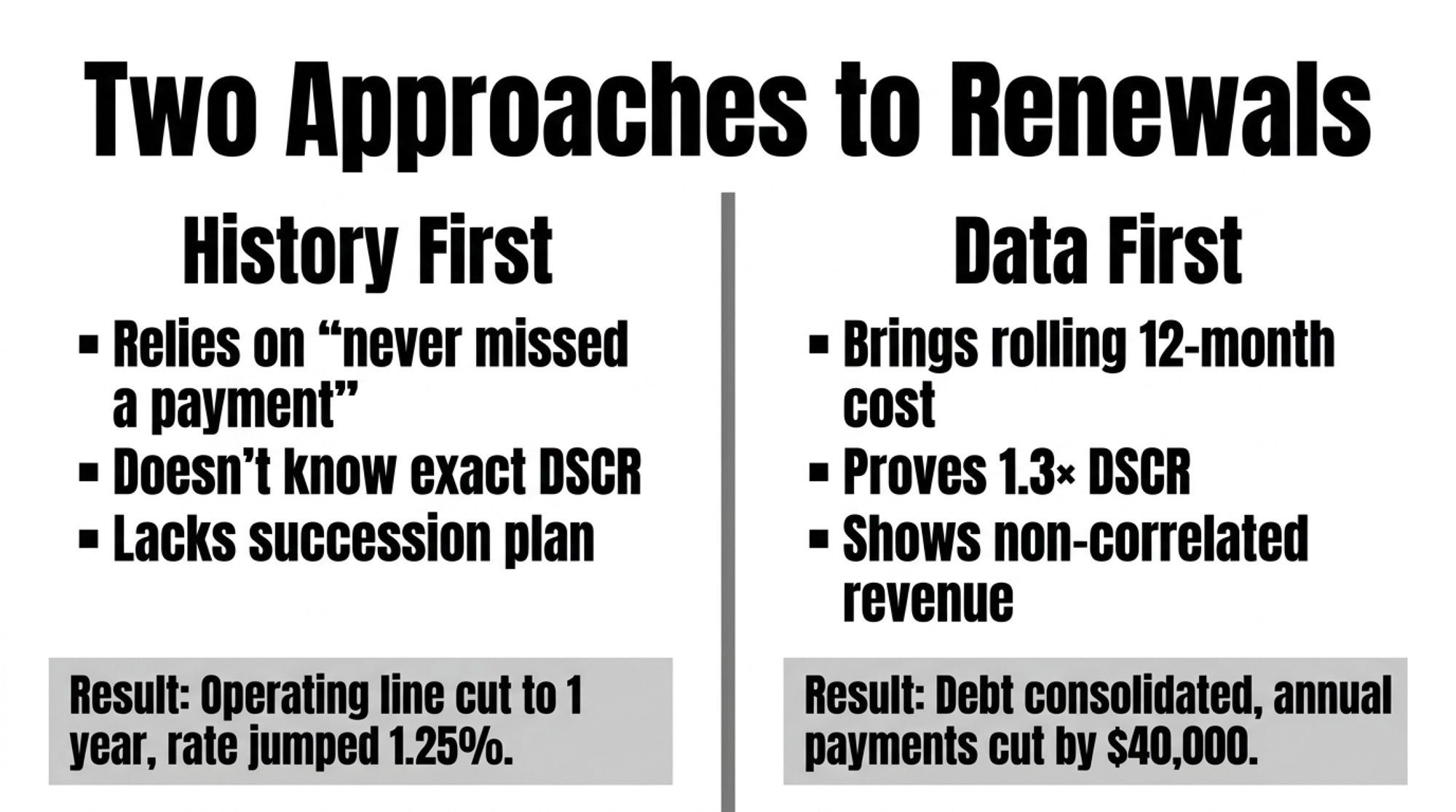

A 380‑Cow Wisconsin Dairy: “Good Customer” Meets New Math

Call this composite a 380‑cow Holstein herd in a sand‑bedded freestall in central Wisconsin. Rolling herd average in the high 70s. In 2019, a farm with this profile might have expanded the parlor and housing, taking on roughly $1.8 million in new term debt at around 3.75%. Payments fit fine at the time.

Those loans repriced in late 2025 to just over 7%, right in line with Chicago Fed survey rates. Bullvine’s own rate analysis suggests repricing typical mid‑size dairy debt from the mid‑3s to the mid‑7s can add more than $100,000 a year in debt service on $3–4M of repriced debt. For a 380‑cow herd on this trajectory, breakeven jumps from the high‑$17s into the low‑$19s per cwt.

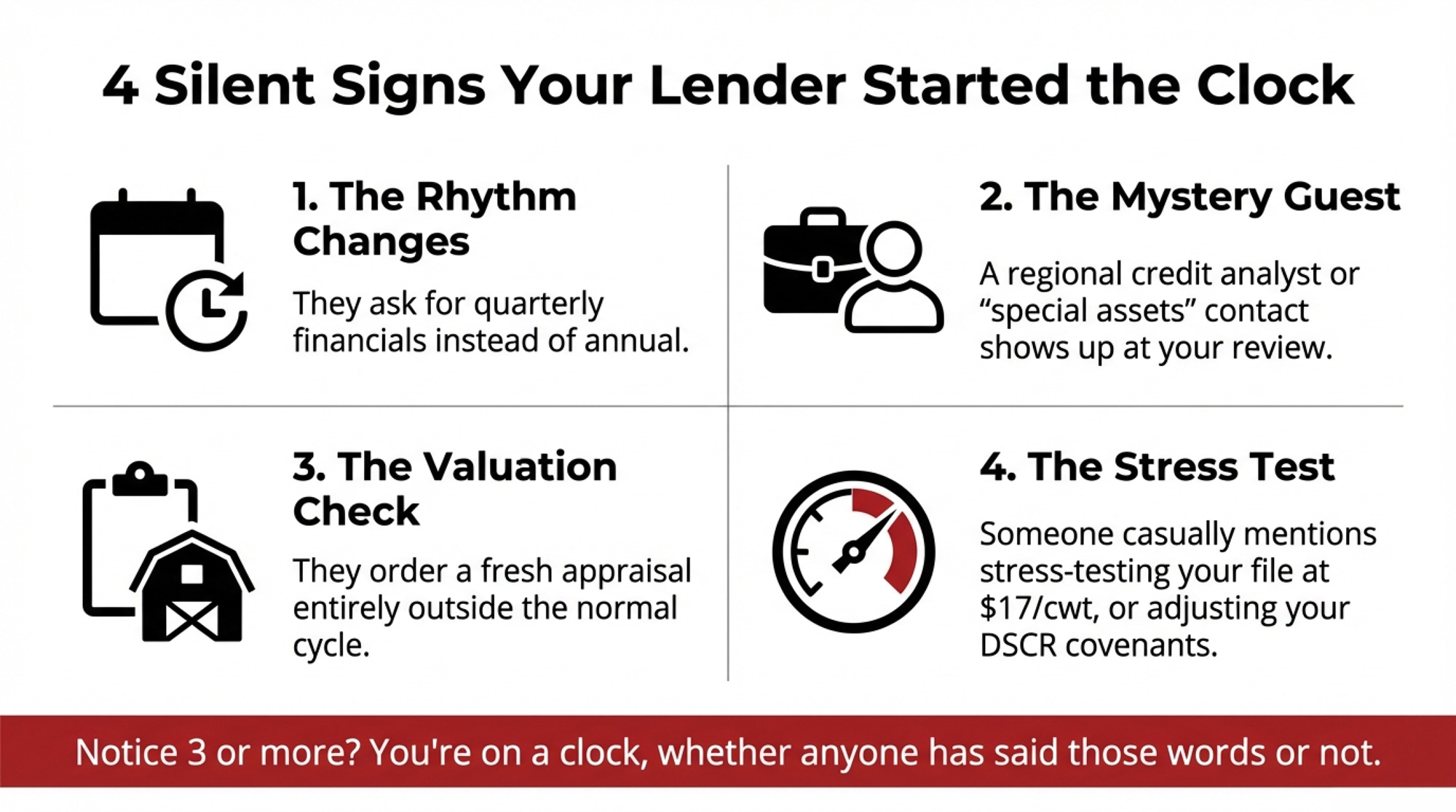

A herd like this often has never missed a payment. Land still pencils as strong collateral — Oppedahl has noted in the Chicago Fed AgLetter that rising 7th District land values give some stressed farmers the option to sell off a portion of land to support operations. Even so, this kind of file typically shows DSCR sliding from above 1.4× to around 1.1×. That moves it off autopilot and onto the watch list.

At annual review, instead of a quick signature, the conditions now look like this: monthly financials instead of quarterly, a cap on new capital spending, and a clear ask to show a path back to at least 1.25× DSCR inside 18 months.

The common turning point on farms like this: somebody — often a younger family member — pulls 12 months of milk checks and expense reports, sits down with an Extension farm business educator, and builds a cash‑flow projection with three paths. Hold steady and hope for $20+ milk. Trim tail‑enders and push extra cash into principal — exactly the kind of move Kauffman has pointed to as risk reduction. Or lean harder into components and beef‑on‑dairy genetics.

That last path matters more to the bank than many producers realize. Lenders reward revenue that isn’t tied to the Class III/IV roller coaster. Beef‑on‑dairy calves sell into the fed‑cattle market, not the milk market, so they’re effectively non‑correlated revenue — cash that keeps flowing when milk prices tank. On a working balance sheet, a pen of high‑value crossbred calves and short‑bred heifers carries more weight than straight Holstein bull calves, strengthening the working‑capital line the model pulls every quarter. That kind of balance‑sheet signal often translates into more flexibility at renewal.

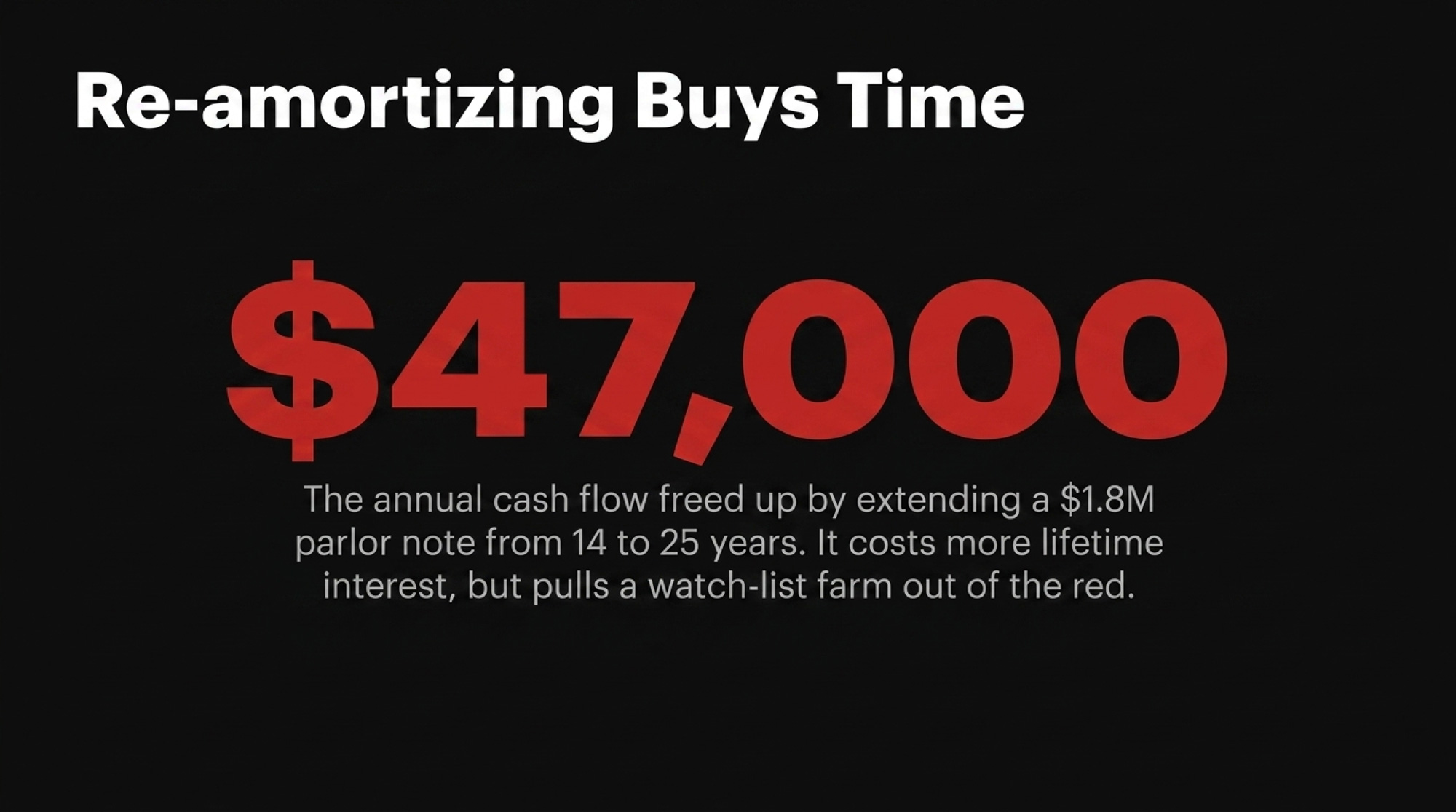

💡 The $47,000 Payment Gap On a $1.8M parlor note at ~7.25%, re‑amortizing from a 14‑year remaining term to a new 25‑year term drops annual P&I from roughly $203,000 to $156,000 — a gap of ~$47,000 per year. That’s the number in the headline. It’s also what often moves a watch‑list farm back into the “renewed” column. The trade‑off: more total interest over the life of the loan.

When a composite farm like this comes back to its lender with the same cows, same ground, same total debt, but a sharper story, the outcome typically shifts. A $47,000/yr payment drop nudges projected DSCR from about 1.14× into the low‑1.2× range. Not cushy. Out of the danger zone.

The relationship doesn’t carry farms like this. The data does.

Go deeper: “Profitable but Drowning: The Interest Rate Crisis Reshaping Mid‑Size Dairy” walks through the full repricing breakdown on herds in this exact position.

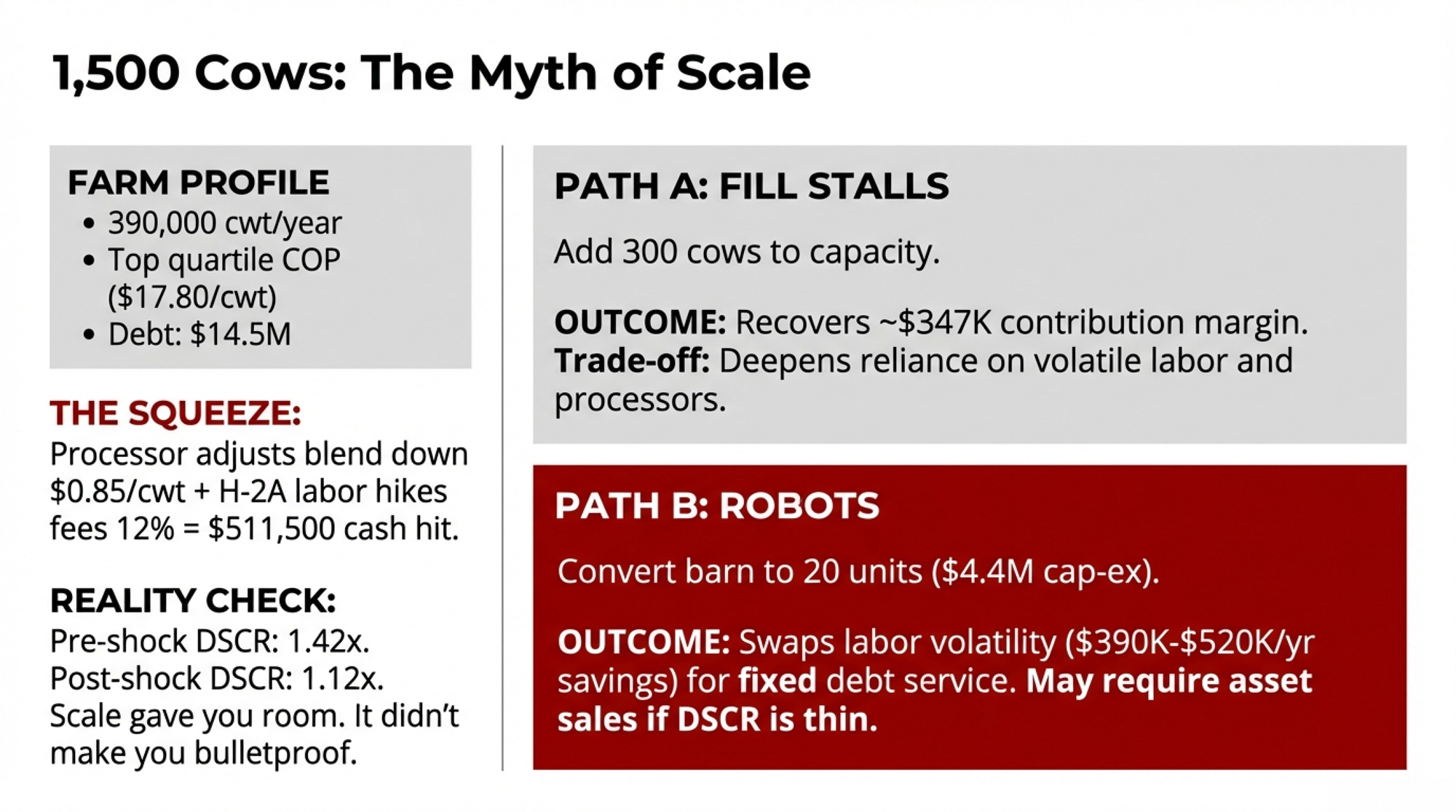

A 620‑Cow New York Dairy: Data Buys Better Terms

The second composite: a 620‑cow western New York dairy built from 200 over a decade by reinvesting profits and timing land buys around local retirements. Total debt near $6.8 million across a Farm Credit real‑estate package, a local bank equipment note, and an FSA‑guaranteed operating line. On paper, that leverage could make any lender twitch in a 7% rate world.

Files like this one earn the opposite reaction.

Operators on this trajectory track cost of production by month. Not just “feed, labor, other” — purchased feed per cow per day, hired labor per cwt, interest expense per cwt, repairs as a percent of gross. A rolling 12‑month cost around $16.80/cwt is plausible for a tightly run herd of this size. A 2023 Northeast Dairy Farm Summary reported a net cost of production of $22.64/cwt across member farms, so this composite would run well below the regional average. Cornell’s DFBS profitability comparison confirms the pattern from another angle: the highest‑profit group carried a debt coverage ratio of 2.95× versus 0.36× at the bottom.

A herd like this seeking $400,000 to upgrade manure storage under state rules would typically show DSCR holding in the high‑1.3× range even under a modeled $17 all‑milk year. Working capital comfortably positive. A simple written succession outline bringing a family member in over the next decade.

Rather than tightening terms, a lender looking for a reason to keep this file often goes the other direction — consolidating higher‑rate equipment debt into a longer real‑estate package. On the $1.2M chunk modeled here, stretching the term and picking up a better rate can cut annual debt service by roughly $40,000 (illustrative; exact savings depend on term and rate selected). That cash goes straight to working capital and strategic repairs.

The farm that walks in with a clear cost‑of‑production story gets the best tools when things get tight.

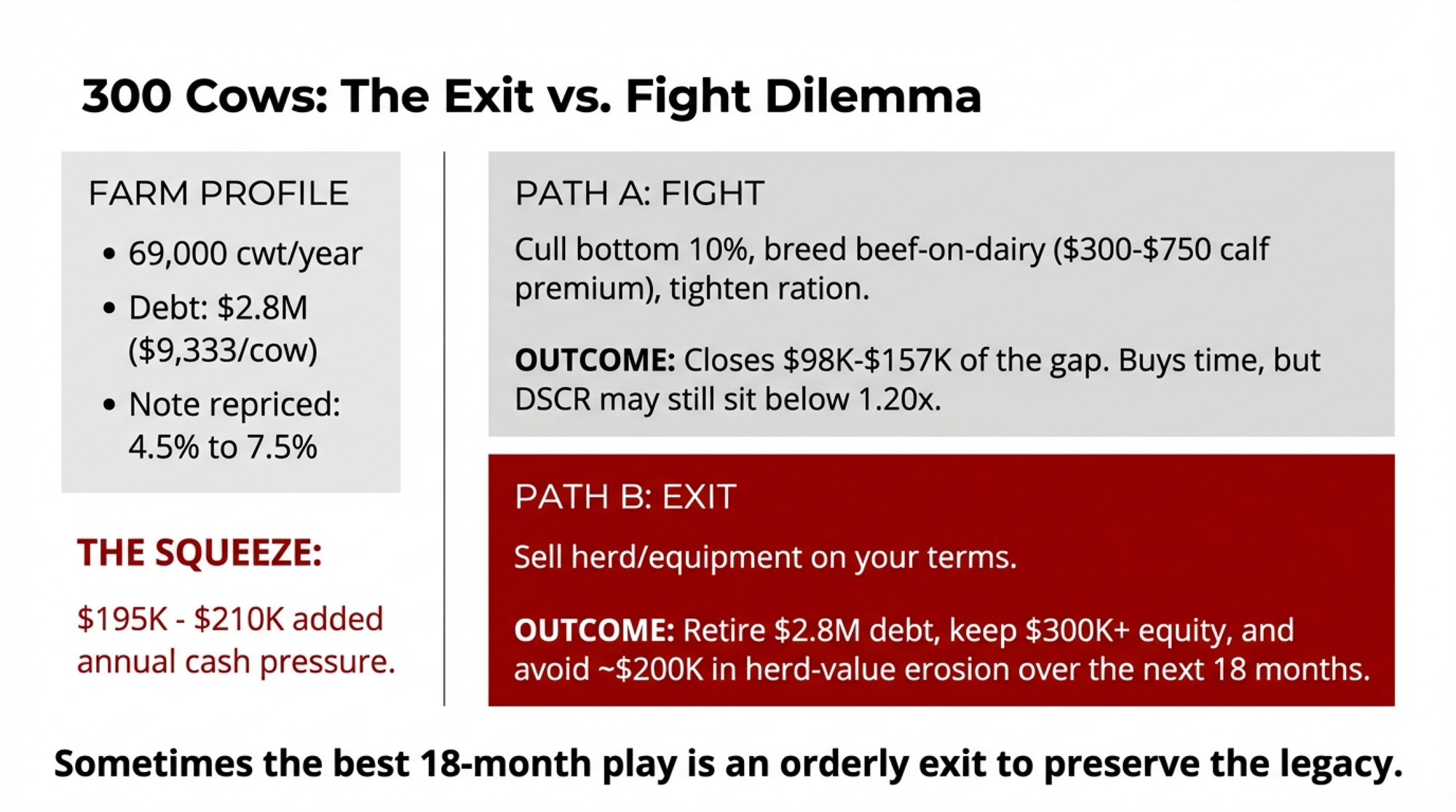

A 280‑Cow Minnesota Dairy: When “Good Customer” Isn’t Enough

The third composite: a 280‑cow tie‑stall in east‑central Minnesota. The cows do fine. The concrete, not so much.

No parlor, no robots, no big value‑added sideline. Total debt around $1.9 million, mostly land and building mortgages. A family farm like this often works with the same locally owned community bank for decades. The lender knows them by name and quietly rolls the operating line year after year.

Then, in 2024, that bank gets absorbed into a larger regional system — part of the wave of Midwest community‑bank consolidations over the last decade. When the file hits the new centralized risk model, three things flag: DSCR under 1.0× on recent tax returns (well below the Cornell all‑farm average of 1.84×), debt‑to‑asset ratio pushing 0.40 (versus the DFBS average of 0.29), and no documented succession plan. Kids with careers off‑farm.

That’s almost exactly the profile Kauffman has flagged in KC Fed commentary as most at risk — a producer who hasn’t built much land equity and carries heavier leverage on machinery or buildings.

Doors don’t slam on farms like this. The rules change. Operating line renewed for one year instead of three. Rate jumps about 1.25 percentage points, adding roughly $7,500 a year in added interest on a $600,000 line — on top of tighter covenants and a shorter renewal window. The bank asks for a formal transition or exit plan inside 12 months.

The typical next step on these files is a Minnesota Farm Business Management instructor — not to plan expansion, but to map an orderly wind‑down. A realistic three‑year exit: timing cow and equipment sales to avoid fire‑sale discounts, using Dairy Margin Coverage payouts and safety‑net checks to bridge cash flow, and listing land at current comparable values instead of waiting for a sheriff’s notice.

Bullvine’s own case work across several Midwest exits suggests families who planned 7–18 months ahead preserved roughly $400,000–$680,000 more equity than those pushed into forced liquidation. It isn’t the ending anyone dreams of. It beats letting the dashboard pick the date and the price.

▶ Next Step for Farms in This Position: Read “The 45‑Day Survival Guide for Mid‑Sized Dairy Operations” — the most logical playbook for operators whose DSCR is already under 1.0×.

What Happens to Your Milk Check When Your Interest Rate Jumps 1%?

Strip away the banker language and a big part of this shift is brutally simple: the same debt costs you a lot more than when you signed for it.

Take $2.5 million of term debt on a 20‑year amortization. At 6.5%, annual principal and interest runs about $223,700. Ship 100,000 cwt a year, and that’s roughly $2.24/cwt just to service that debt. At 7.5%, the payment climbs to about $241,700 — roughly $2.42/cwt. That’s about $18,000 more per year, or $1,500 less cash per month. (Standard amortization estimates; your exact number depends on payment structure and compounding.)

| Interest Rate | Annual P&I (US$) |

|---|---|

| 6.5% | 223,700 |

| 7.5% | 241,700 |

Now look at how that moves DSCR:

- Net cash for debt service at $300,000 and a 6.5% payment: DSCR ≈ 1.34×.

- Same cash, 7.5% payment: DSCR drops to about 1.24×.

- If milk slides and net cash falls to $200,000 at the higher rate: DSCR ≈ 0.83×.

One percentage point of interest. One dollar of milk price. That’s the gap between “renewed with conditions” and “we need to talk about restructuring.”

How Much Does a Full Repricing Really Move Your Breakeven?

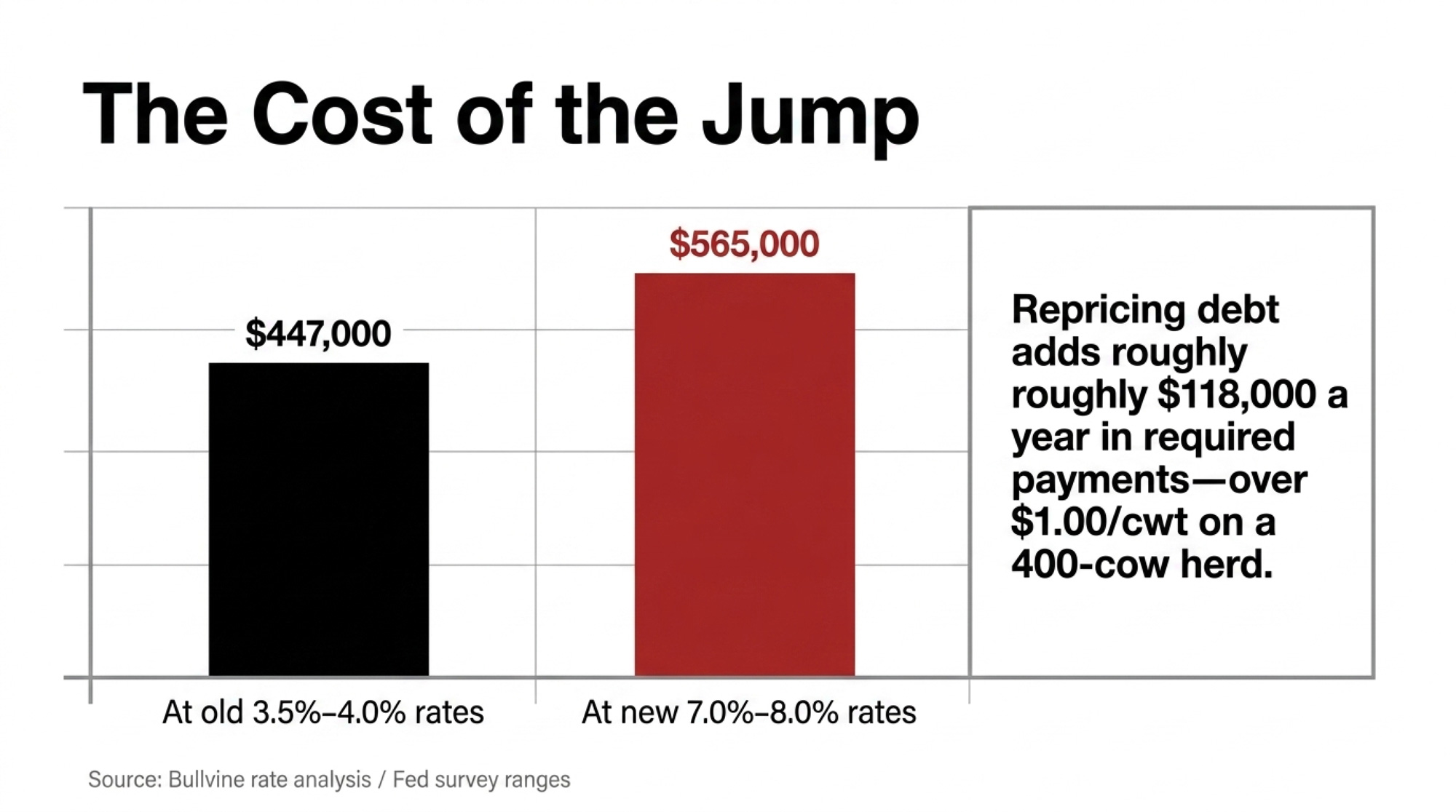

If you’re sitting on around $4.5 million in total debt, here’s what the repricing wave looks like using realistic chunks drawn from Fed survey ranges (standard amortization math, rounded for presentation):

| Debt Type | Amount | Old Rate | New Rate | Old Annual P&I | New Annual P&I |

| Real estate (15‑yr) | $2.7M | 3.5% | 7.5% | ~$232,000 | ~$300,000 |

| Equipment (7‑yr) | $1.2M | 4.0% | 7.0% | ~$197,000 | ~$217,000 |

| Operating line (interest‑only) | $600K | 3.0% | 8.0% | $18,000 | $48,000 |

| Total | $4.5M | ~$447,000 | ~$565,000 |

That’s about $118,000 more per year in required payments.

Spread across different herd sizes shipping milk:

| Approximate Herd Size | Cwt Shipped | Added Cost (US$/cwt) |

|---|---|---|

| 200 cows | 55,000 | 2.15 |

| 280 cows | 80,000 | 1.48 |

| 400 cows | 110,000 | 1.07 |

The smaller you are, the bigger the per‑unit hit. And if your margin was only $0.50–$1.00/cwt to start with, that’s the whole ballgame.

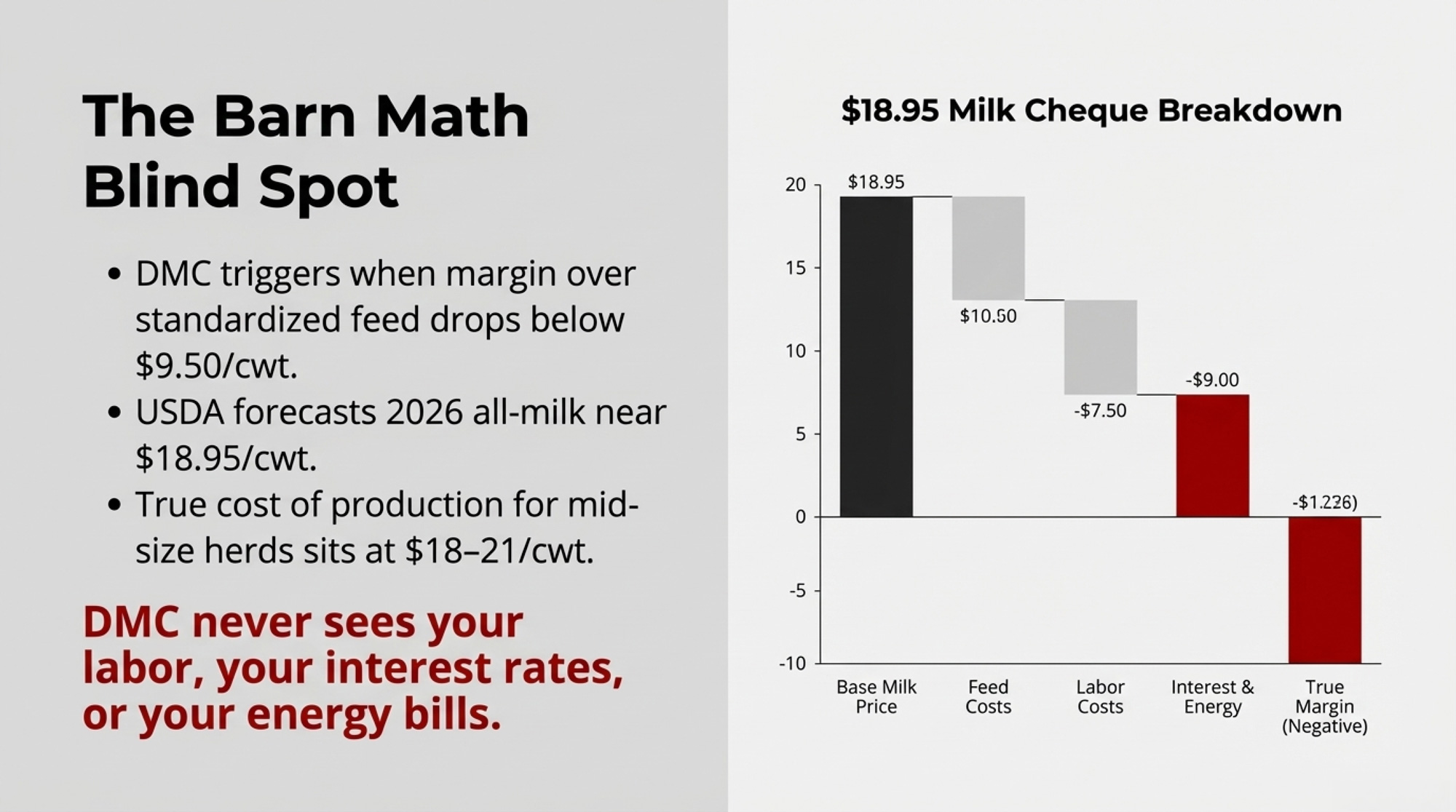

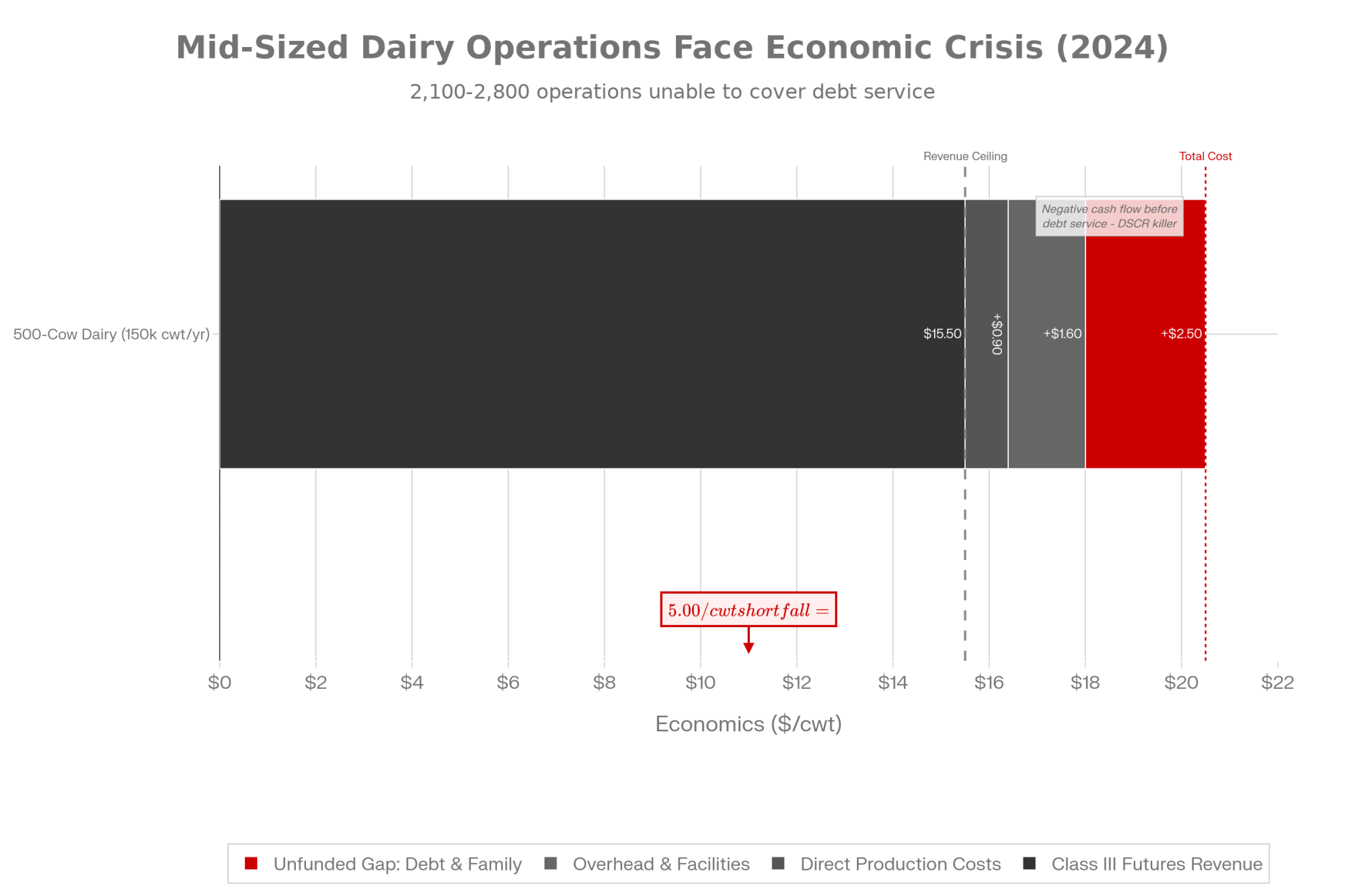

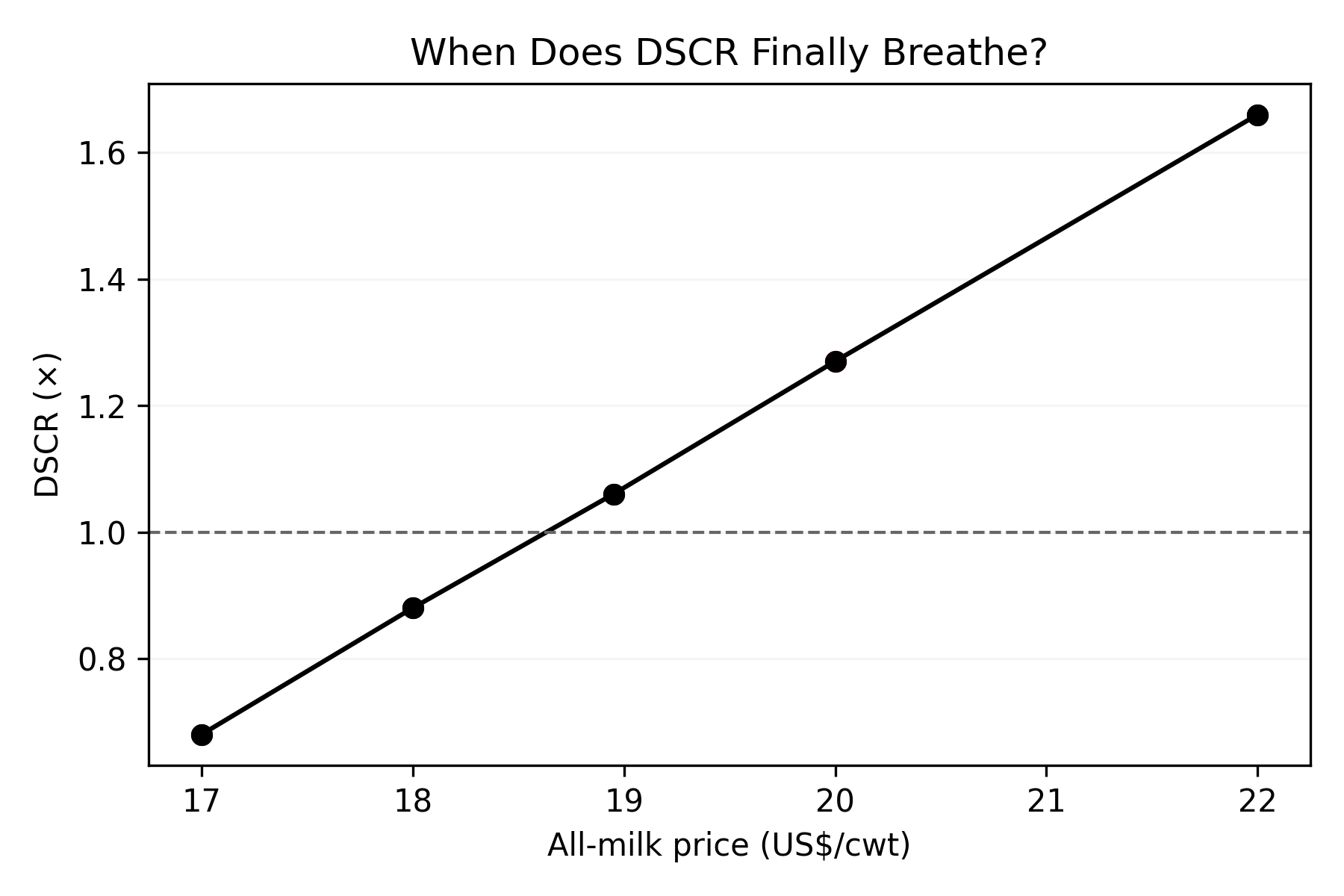

Now stress‑test DSCR for that 400‑cow, $4.5M‑debt scenario. Assume 110,000 cwt shipped and non‑debt cash operating costs around .50/cwt — efficient by Cornell’s standards, given that DFBS profitability data shows far higher averages across most farms. USDA’s early‑2026 WASDE pegged the all‑milk forecast at $18.95/cwt, down from a revised $21.17 for 2025.

WASDE updates monthly. If a newer report has landed between filing and publication, refresh both the all‑milk row and the DSCR column below.

| All‑Milk Price | Gross Revenue (110k cwt) | Cash Costs (@ $13.50) | Net Cash for Debt | DSCR vs ~$565K P&I | How Your Lender Reads It |

| $17.00 | $1,870,000 | $1,485,000 | $385,000 | ~0.68× | “We have a problem.” |

| $18.00 | $1,980,000 | $1,485,000 | $495,000 | ~0.88× | Below 1.0× threshold |

| $18.95 | $2,084,500 | $1,485,000 | $599,500 | ~1.06× | Barely above water |

| $20.00 | $2,200,000 | $1,485,000 | $715,000 | ~1.27× | Comfort zone |

| $22.00 | $2,420,000 | $1,485,000 | $935,000 | ~1.66× | Strong |

At $18.95 milk, you barely clear 1.0×. You need $20+ to breathe.

And that $13.50/cwt cost assumption is efficient. A 2023 Northeast summary reported a net cost of production of $22.64/cwt across member farms. If your cost base runs closer to $16–$17, the DSCR in this table deteriorates fast.

Go deeper: “$18.95 Milk, $19.14 Costs: USDA’s 2026 Milk Price ‘Upgrade’ Still Leaves Your Dairy in the Red” runs the full margin math band by band.

What DSCR Do Banks Really Want from Dairy Farms?

You can’t control your lender’s internal model. You can understand the target it’s aiming at.

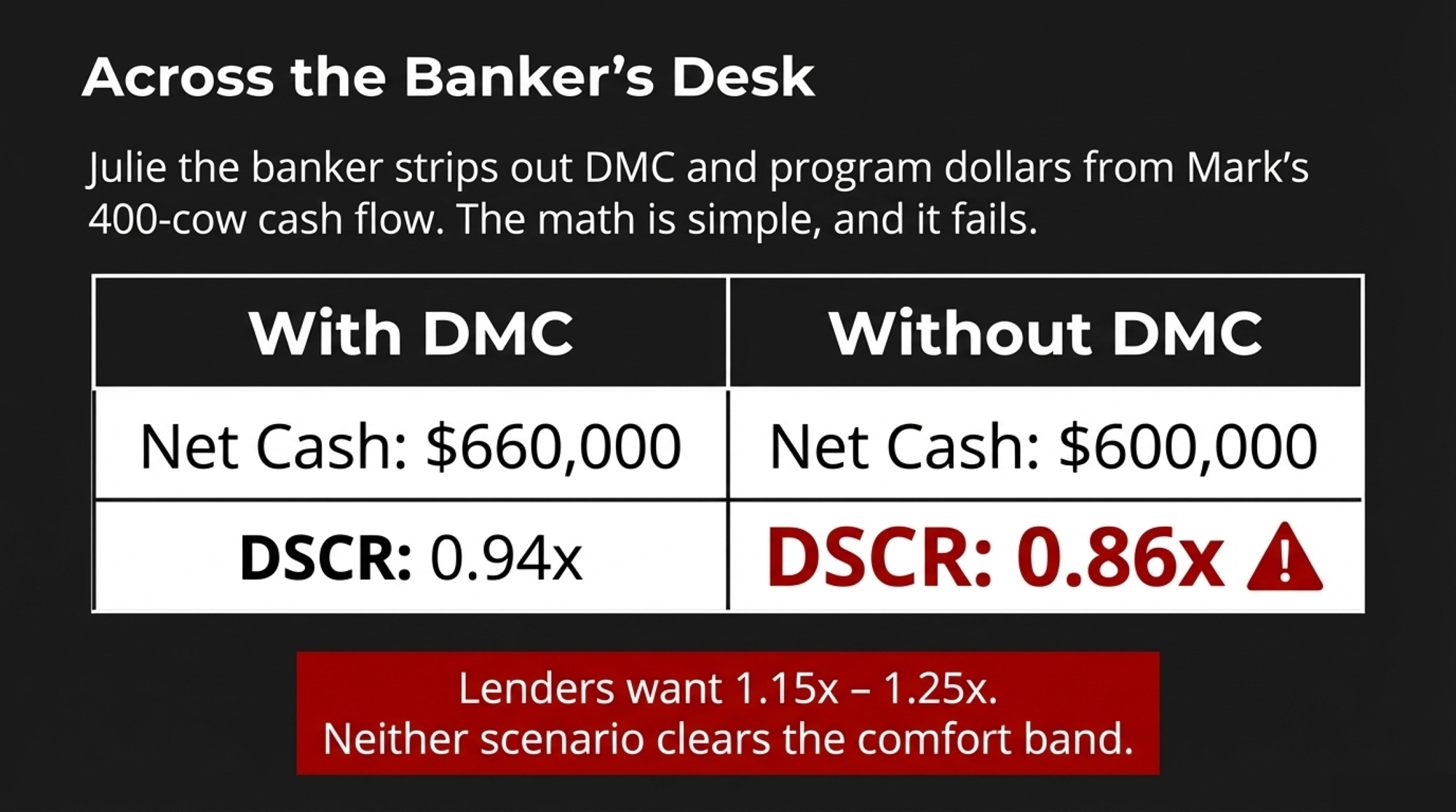

At its simplest: DSCR = net cash available for debt service ÷ total annual principal and interest. If your net cash is $400,000 and total payments are $320,000, your DSCR is 1.25× — the farm generates 25% more cash than it needs to make debt payments.

| DSCR Band | Typical Bank View | What It Feels Like on Farm | Lender Response |

| Below 1.0× | Not covering debt from cash flow | Scrambling to make payments, no buffer | Conditions, collateral pressure, restructure or exit talks |

| 1.0–1.15× | Thin, one bad month from trouble | Every breakdown or milk dip hurts | Short‑term tolerance only with a written plan |

| 1.15–1.30× | “Okay, not great” | Can sleep, but watch weather and milk price | Floor for flexible terms, new money around 1.25× |

| > 1.30× | Strong performer | Can invest and handle volatility | More freedom on terms, structure, and covenants |

Pulling from Cornell’s 2023 DFBS profitability comparison (129 New York herds):

- Below 1.0×. Not generating enough cash to cover debt. The lowest‑profit group averaged 0.36×. Expect conditions, collateral calls, or hard conversations.

- 1.0–1.15×. One bad month of milk, a feed mistake, or a breakdown can push you under. Some lenders will sit here short‑term, but only with a written plan to climb out.

- 1.15–1.30×. Where a lot of mid‑size herds land when things are “okay, not great.” Many lenders treat 1.25× as the floor for new money or flexible terms. Cornell’s mid‑high profit group averaged 1.38×.

- Above 1.3×. Strong. The top‑profit group ran at 2.95×. These farms tend to get more freedom on amortization schedules and covenant structures because the numbers back the story.

Here’s the catch. Your lender isn’t just running DSCR at today’s mailbox price. Chicago Fed data confirm that extensions and renewals on non‑real‑estate lending are increasing — a sign more borrowers are asking for extra time and banks are testing harder before granting it. If you walk in having only looked at your best‑case price, and the dashboard is staring at your worst‑case, you’re not even arguing over the same math.

Are You Giving Your Lender Enough Data to Fight for You?

A lot of good operators will quietly admit they’ve never walked into the bank with a real data packet. The lender knew them. The cows looked fine. Bills got paid.

In a dashboard world, being a good operator still matters — but mostly after the numbers clear the first screen. If you want your lender to push for you with a credit committee that’s never set foot in your parlor, you’ve got to hand them ammunition.

The Minimum Data Packet (200–1,500‑Cow Dairy)

For your next scheduled meeting — not an emergency — walk in with:

- Last three years of financials. Tax returns (Schedule F), year‑end balance sheets, depreciation schedules.

- Rolling 12‑month cost per cwt. At least broken into feed, labor, and “all other” operating costs.

- Your current DSCR. Today’s loan balances, current interest rates, total annual payments.

- Working capital snapshot. Current assets minus current liabilities — the metric Kauffman has specifically flagged as the one lenders are watching closest.

- Leverage snapshot. Total debt divided by total assets. The DFBS average was 0.29 in 2023; know where you sit.

That alone puts you ahead of more farms than you’d guess.

What Actually Earns Better Terms

- Three forward scenarios. Base case, a “$2/cwt lower milk” stress case, and a slightly better‑than‑today case.

- A simple succession plan. Even a one‑page outline of who’s likely running the place in 5–10 years. Farm Credit and Extension communications increasingly treat succession as a formal credit factor, not just a family story.

- Real‑time production data. Rolling herd average, butterfat/protein trends, voluntary cull rate — anything that shows you manage cows, not just cash.

- A non‑correlated revenue story. Beef‑on‑dairy receipts, custom heifer raising, crop sales, on‑farm processing. Anything not priced off the milk check strengthens your current‑asset picture in the bank’s model.

- Rate‑index awareness. Know whether your current notes are fixed, variable over Prime, or tied to term SOFR. If you can’t tell the loan officer which index prices your operating line, you’re arguing blind.

- FSA awareness. Know whether you qualify for USDA direct loans — well below commercial markets — and whether FSA‑guaranteed lending could improve terms with your current bank.

Red Flags That Trip Wires Fast

Patterns that, from lender and Extension farm‑management conversations, tend to push files straight into the risk bucket:

- No updated personal financial statement after the lender asked for one.

- No honest cost‑of‑production number.

- No forward cash‑flow projection, even a simple one‑pager.

- Farm and household expenses so tangled the lender can’t separate them.

- A flat refusal to discuss succession.

- No idea whether your rate is fixed or floating — or over what index.

When your dashboard numbers are already thin, any one of these pushes a lender toward higher rates, tighter covenants, or a quiet “no.”

Options and Trade‑Offs for Farmers

You don’t control interest rates. You control how you show up in front of the dashboard over the next 12 months.

1. Upgrade Your Data Game (30‑Day Action)

Start here if you plan to keep milking at least 3–5 years, you’re not insolvent, but you honestly don’t know your DSCR or cost per cwt.

This month: Pull 12 months of milk checks and main expense categories. Build a rolling 12‑month cost per cwt using a simple spreadsheet or FINPACK template from Extension. Calculate your DSCR. Then book a meeting with your lender specifically to review your data — not to ask for money.

You walk in knowing where you stand instead of hoping. Your lender sees someone running toward the problem, not hiding.

The risk: You may not like that first DSCR number. But you can’t fix a ratio you won’t look at.

2. Restructure Before You’re Forced To

Move here if your DSCR is hovering near or just below 1.0×, you still have land equity, and your next big renewal is 6–24 months out.

What it takes: Map every loan on one page — balance, rate, index (fixed, Prime‑based, SOFR‑based), remaining term, payment. Model what happens if milk averages $2/cwt less than last year. Be open to extending terms on some debt or selling a non‑core asset. Oppedahl has pointed out in recent AgLetter commentary that some farms will need to sell land to help fund operations — it goes better if you initiate that conversation.

What you gain: Breathing room. A lender looking for a reason to keep you often will stretch a major note from 14 to 25 years, saving about $47,000 a year in payments on $1.8M at roughly 7.25% — enough to move DSCR out of the red.

What you give up: More total interest over the life of the loan. You’re buying flexibility today with future dollars. Move early and you help design the restructure. Wait, and somebody else does it for you.

3. Double Down on Margin, Not Size

This is the right path when you’re not set up to add cows cheaply, but there’s room to improve component premiums, beef‑on‑dairy revenue, or trim operating costs.

What it takes: Honest benchmarking of feed, labor, and machinery cost per cwt against peers. A focused 12‑month plan to raise butterfat/protein, add beef‑cross value, or shave specific costs. Cornell’s DFBS tells the story bluntly: the spread in debt coverage between the lowest‑profit group (0.36×) and highest (2.95×) wasn’t mainly about herd size or premiums — it was about cost discipline that drops straight to the DSCR line.

On a 600‑cow herd shipping 170,000 cwt, a $1.00/cwt cost reduction is worth $170,000 a year. Premiums help. Cost discipline changes your DSCR. A solid beef‑on‑dairy program gives the bank a revenue line that isn’t riding the Class III roller coaster.

The risk: Chasing premiums with extra labor or purchased feed can backfire if costs rise faster than the bonus. Measure tightly.

4. Plan an Exit While You Still Have Leverage

Consider this one when you’re past 60, heirs aren’t coming back, DSCR is under 1.0×, and you’re tired of wondering which letter from the bank is “the one.”

What it takes: A farm transition specialist or attorney. Early, blunt conversations with your lender about what a cooperative exit looks like. The willingness to say, “We might be better off leaving on our own terms.”

Across several Midwest cases, Bullvine’s analysis suggests strategic exits with 7–18 months of planning preserve roughly $400,000–$680,000 more family equity than forced sales — a margin close to the $480,000 equity gap between strategic exit and forced sale we’ve documented in prior case work. The difference between “retire with options” and “start over in town.”

The risk: Emotionally brutal. Some relationships fray. But the math usually gets worse, not better, if you delay.

Go deeper: “Only 12% of Dairy Farms Make It to Generation Three — Here’s What’s Different About the Ones That Do” is the companion read for families wrestling with this path.

Key Takeaways

- If your DSCR sits below 1.15× today, treat it as a yellow light. Cornell’s lowest‑profit group averaged 0.36× — they didn’t get there in one quarter. Run your own stress test at $17 milk and talk with your lender before you drift under 1.0×.

- If you can’t list your total annual debt payments on one sheet of paper, your lender has more clarity on your risk than you do. Within 30 days: list every note and operating line, add up annual P&I, calculate your DSCR.

- If your plan assumes rates “go back to normal,” it’s not a plan. Commercial operating rates sat in the mid‑7% range through late 2025 and early 2026, and new paper is increasingly variable over Prime or term SOFR. Model your next two years at today’s rates and one notch higher.

- If more than 90% of your revenue comes off the milk check, your balance sheet is more fragile than your lender’s model likes. Beef‑on‑dairy, custom work, or crop sales aren’t just extra cash — they’re non‑correlated revenue that strengthens how the dashboard reads your farm.

- If you want your lender to fight for you in the credit committee room, hand them a story their dashboard can tell. A real cost‑of‑production number, a forward cash‑flow, and at least a rough succession outline.

The next time you sit across from your loan officer, the screen between you will quietly shape how hard they can push on your behalf.

You don’t control that dashboard. You do control whether it shows a fuzzy picture or a sharp one. For the deeper math — DSCR across five milk‑price bands, how Dairy Margin Coverage and FMMO changes interact with lender risk scoring, and the full cost‑of‑production playbook — watch for the next “Dairy Lender Files” installments in The Bullvine Weekly.

If the numbers are weighing on you, don’t carry it alone. Call or text 988 for the Suicide & Crisis Lifeline. For dairy‑specific support, reach out to Farm Aid at 1‑800‑FARM‑AID, your state farm‑mediation service, or your Extension farm management program.

Do you know your DSCR today? If not, the computer does. It’s time to see the same screen.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $19 Milk Trap: How 2026 Prices Quietly Drain a 400‑Cow Dairy’s Equity — Exposes the $144,000 annual equity drain facing mid-sized herds and delivers a high-stakes playbook to protect your balance sheet. Breaks down full-cost breakeven targets while providing the “action signals” needed to survive a $19.00 milk market.

- Dairy farm economics 2026: pricing and margins — Reveals the structural reset hitting North American producers through FMMO modernization and the Canadian protein pivot. Arms you with the market intelligence to navigate the “higher-of” formula and identify the quiet margin leaks threatening long-term profitability.

- Beef-on-Dairy’s $3,000 Trap: 800,000 Missing Heifers and Who Pays the Bill — Dismantles the “cash-flow hero” myth of beef-on-dairy by exposing the looming 800,000-head heifer shortage. Follows the money on $3,000 replacement costs, revealing why high-reproduction herds are the only ones winning the genetic revenue gamble.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.