Dairy success isn’t about better farming anymore—here’s the real force changing who survives and who sells out.

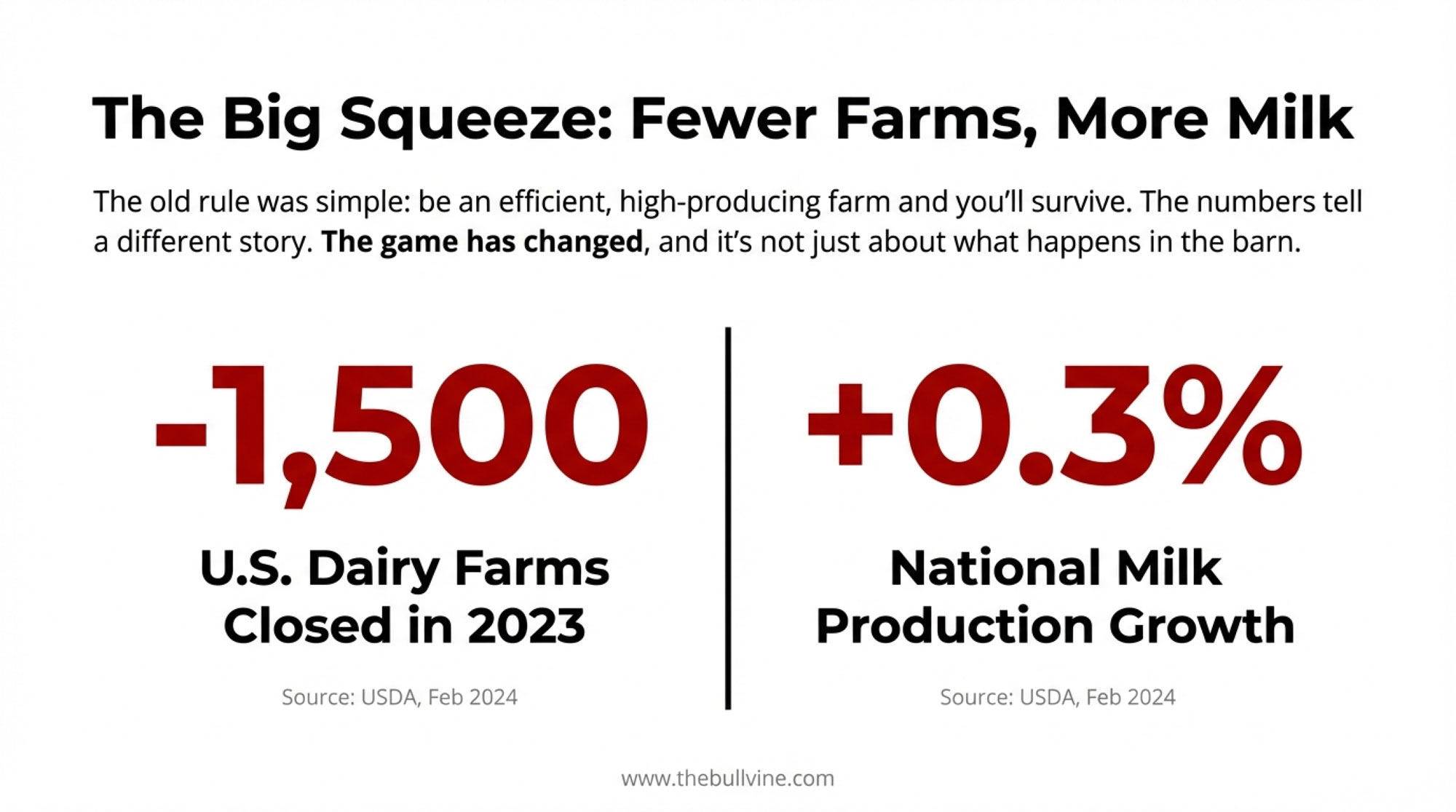

The February 2024 USDA report had a number that’s stuck with me: about 1,500 U.S. dairy farms closed in 2023, yet national milk production ticked higher. That’s not just abstract data—it’s what drives our conversations at kitchen tables and farm meetings across the country. Let’s talk through what’s really happening and what it means for the future.

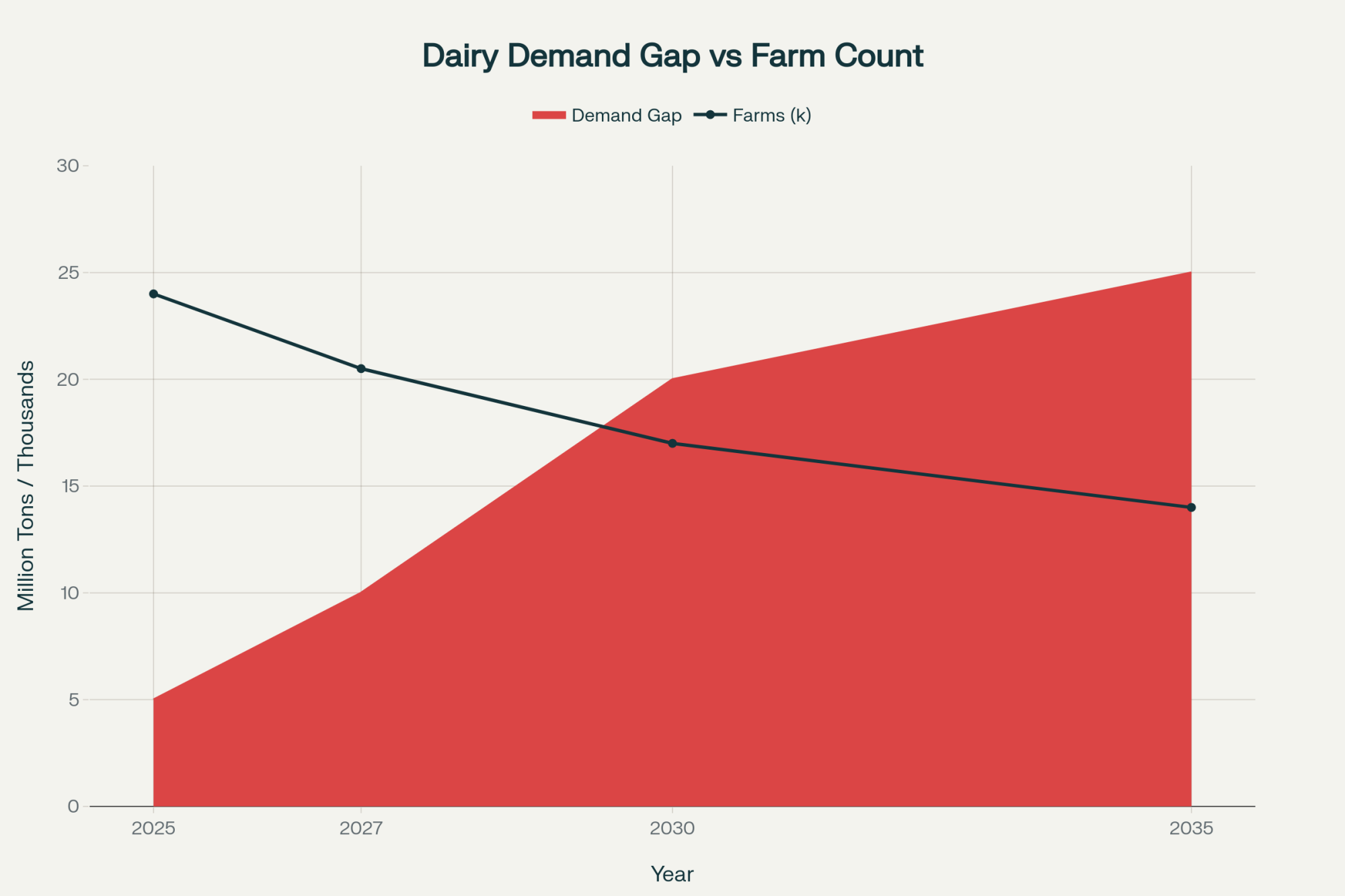

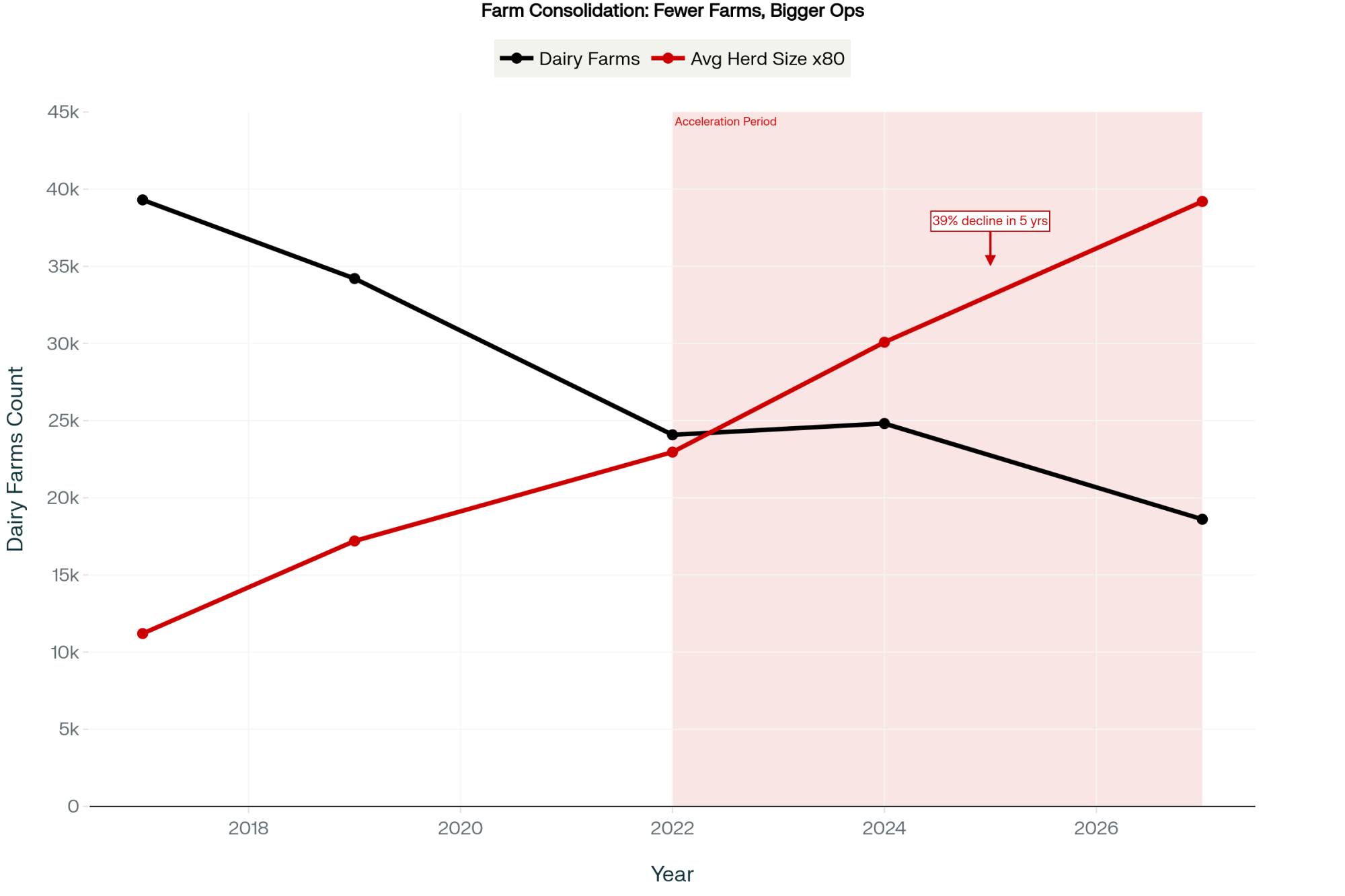

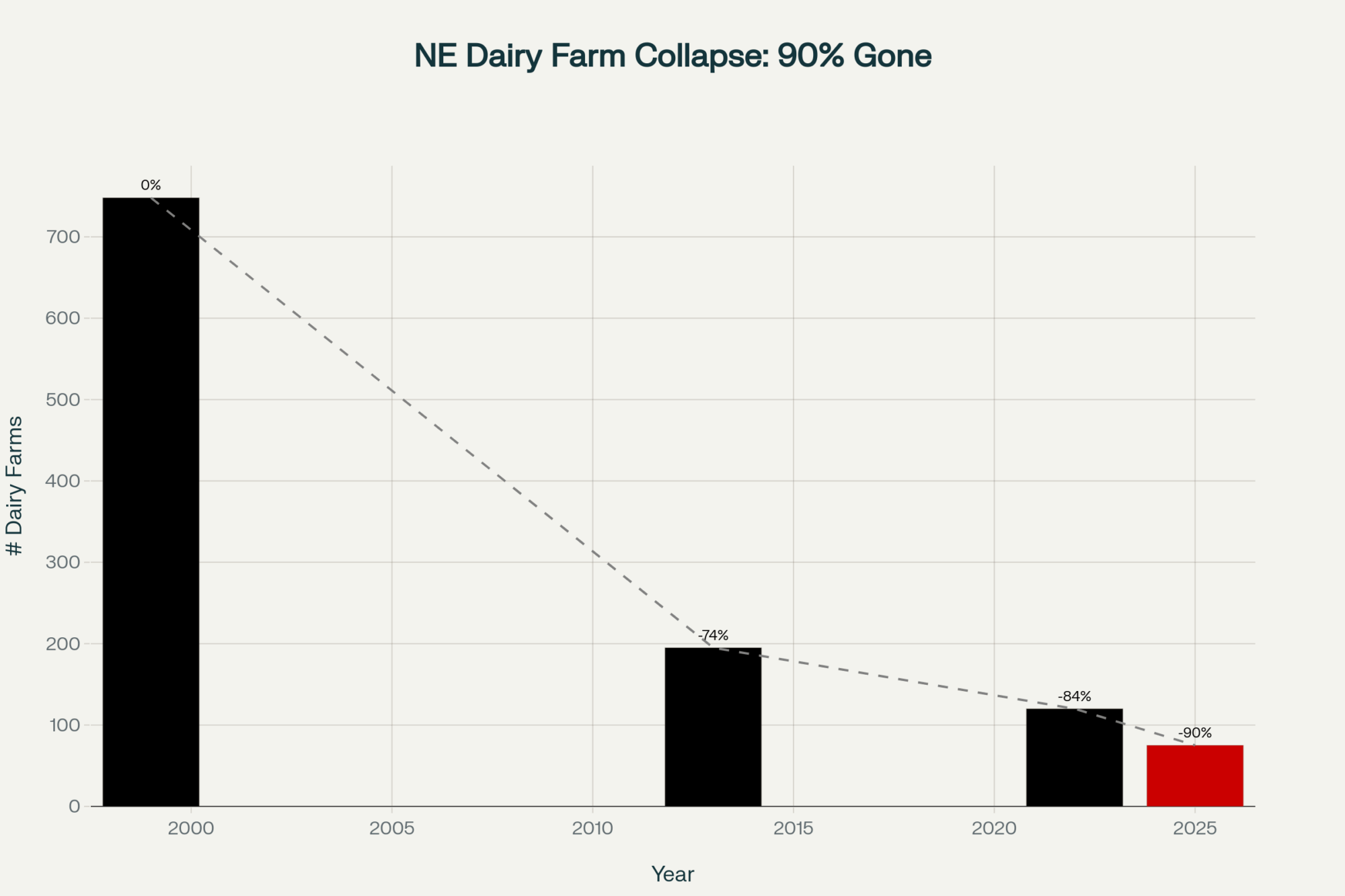

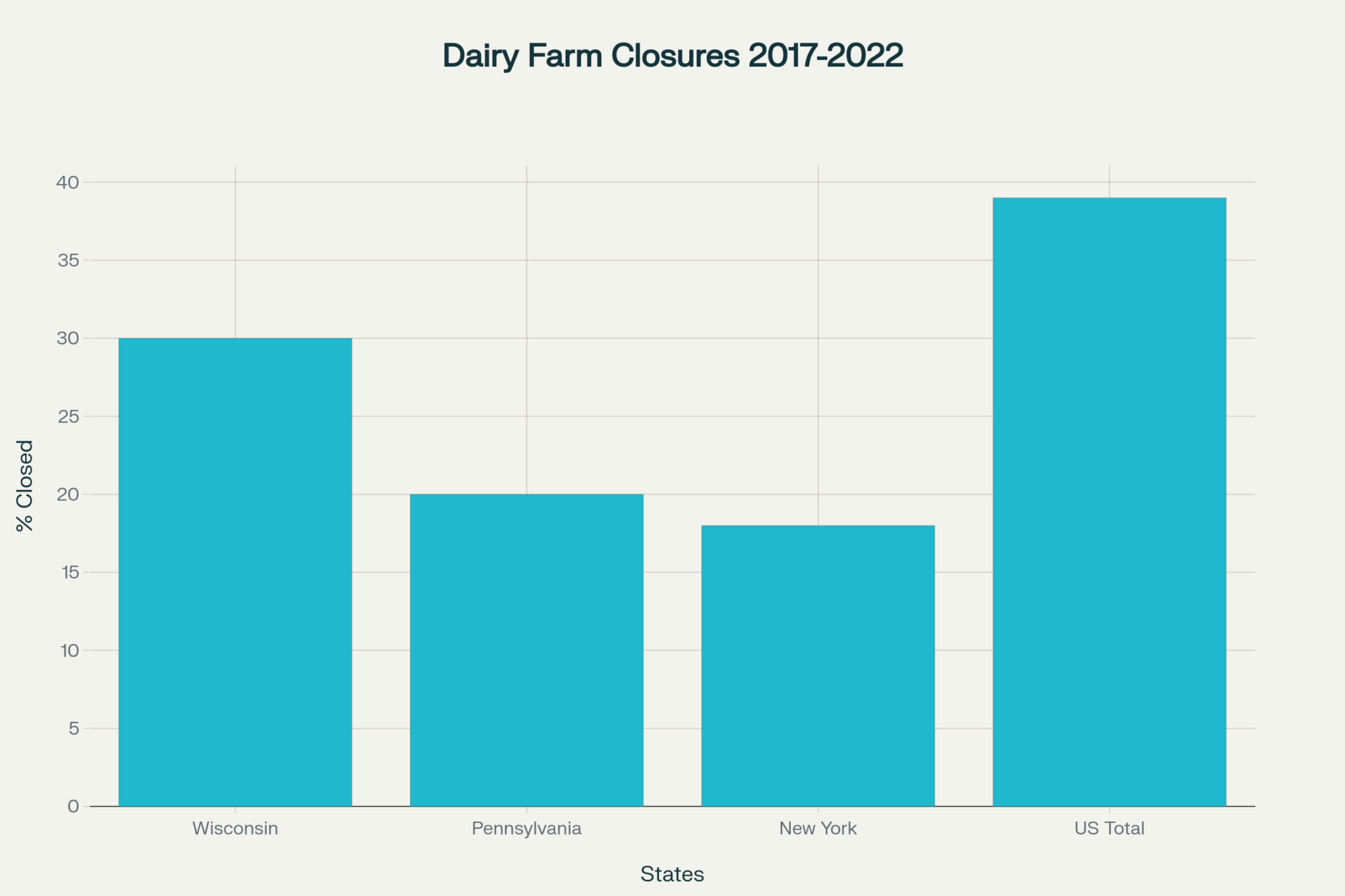

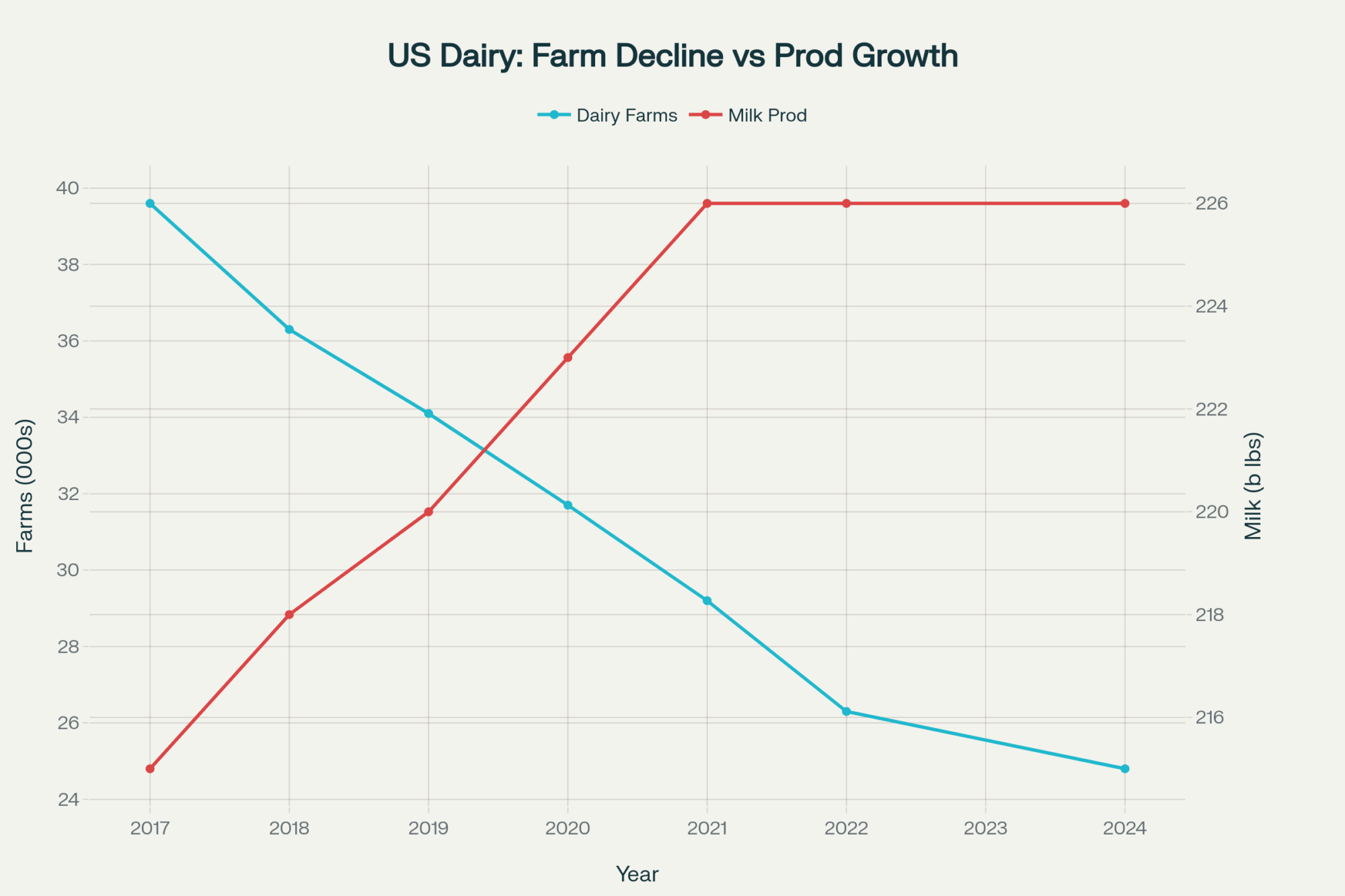

U.S. dairy farming faces an existential consolidation crisis, with farm numbers plummeting from 39,300 operations in 2017 to a projected 10,500 by 2040—a 73% reduction driven by systematic structural advantages favoring mega-operations over traditional family farms, with 1,420 farms disappearing annually as of 2024.

Looking at How the Structure Has Shifted

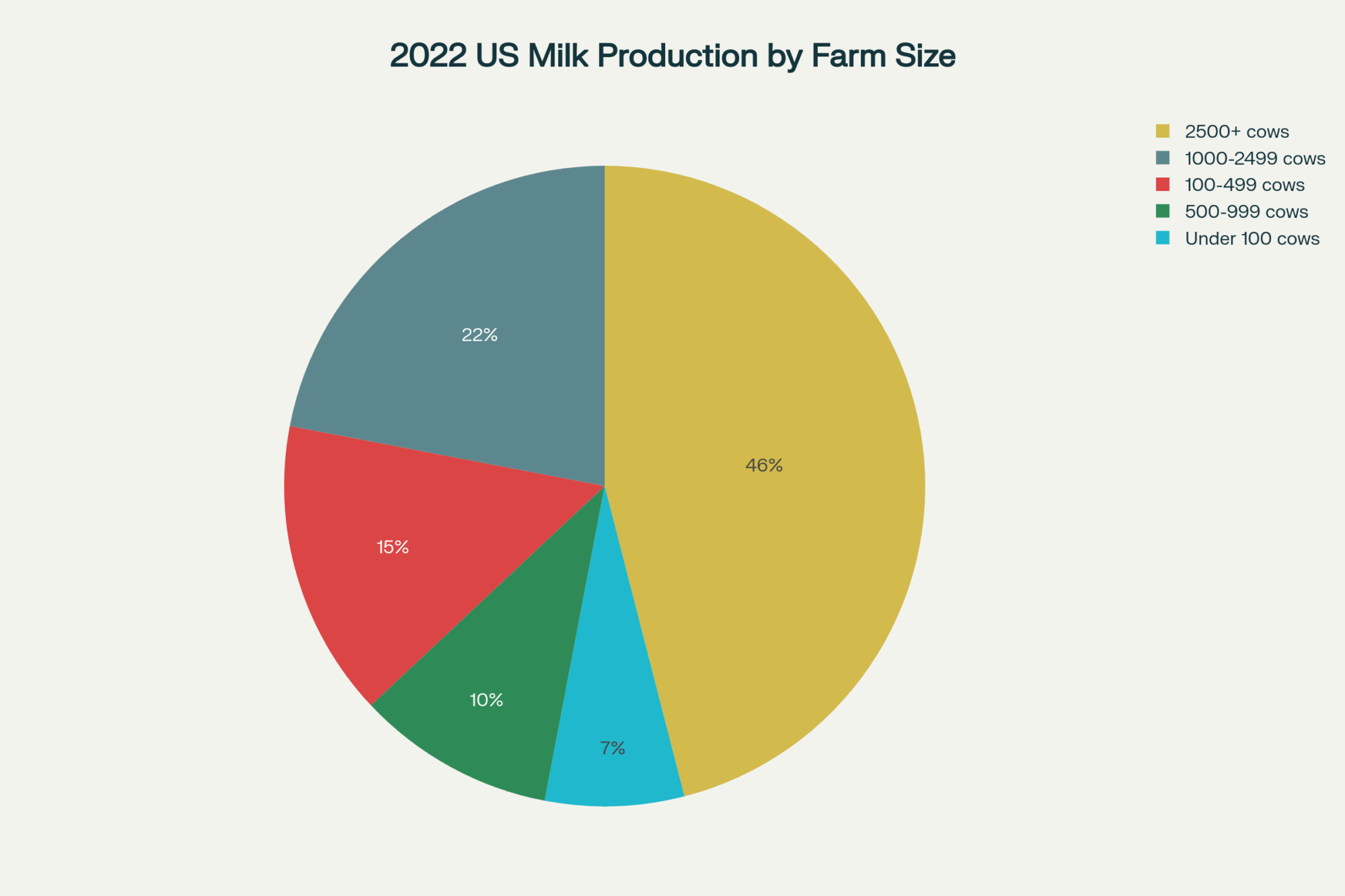

Start with the numbers, because they’re telling: The 2022 Census of Agriculture shows about 65% of American milk now comes from just 8% of herds—those with over 1,000 cows. Meanwhile, nearly 9 out of 10 farms (the 100–500 cow group) account for only 22% of the supply. In the Northeast and Midwest, that’s still the “standard” size, but the playing field keeps tilting.

As one third-generation Wisconsin farmer shared, “I remember 13 dairies on our road, but now it’s just us. Plenty of the folks who exited were younger managers, not retirees. They just couldn’t get the numbers to work.”

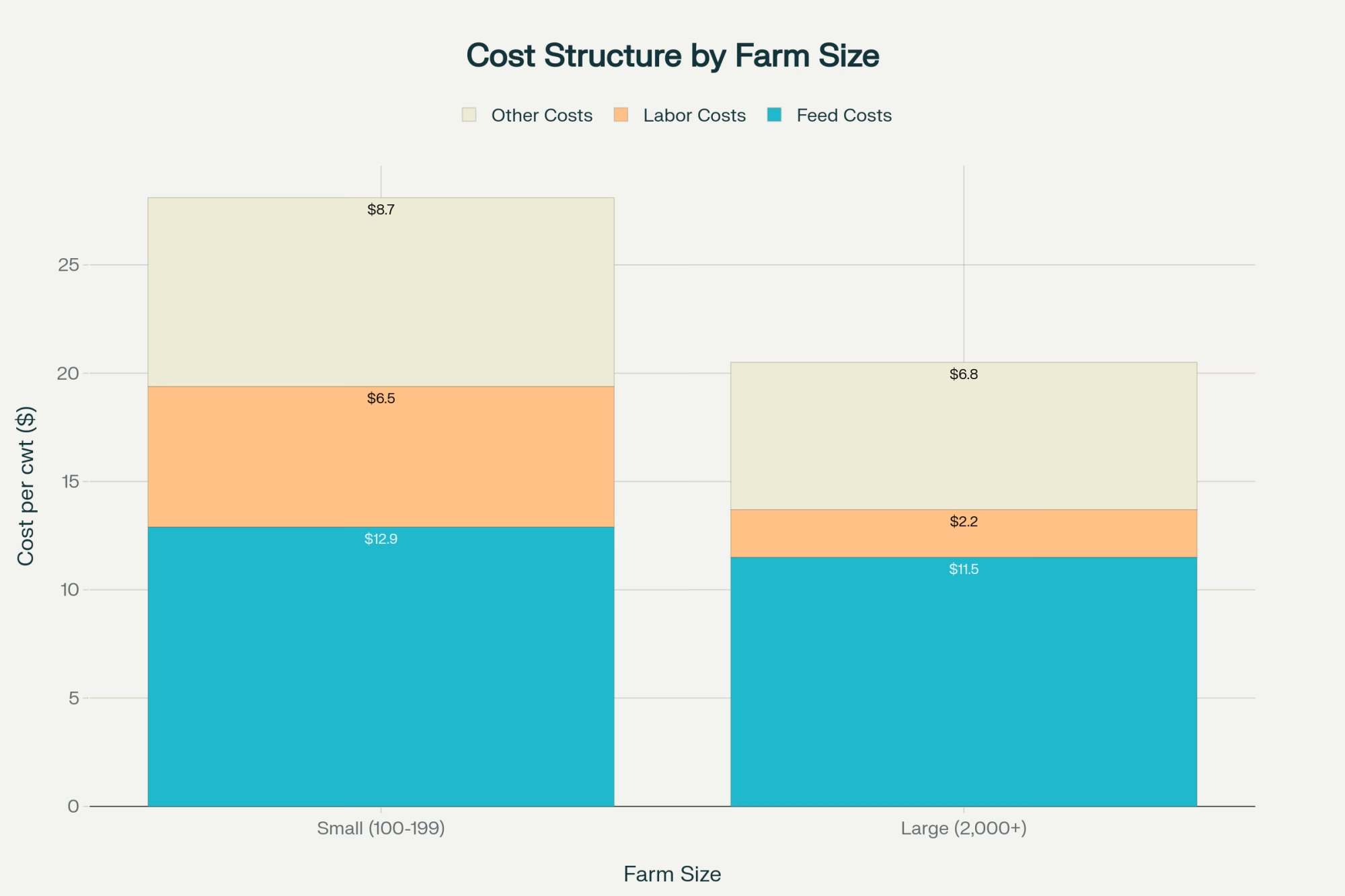

Cost of production varies dramatically by herd size, with the smallest operations facing a devastating $9/cwt disadvantage that translates to $250,000 in annual losses for a typical 600-cow farm—a gap driven by scale advantages in feed purchasing, financing, and regulatory compliance rather than management quality.

Cornell’s Dairy Farm Business Summary for 2022 has it in black and white: the biggest herds report $22–$24/cwt cost of production. For 100–199 cow operations, the range is $31–$33/cwt. In a market where the base price is set by regional blend or federal order, that gap eats margin and equity fast.

Beyond Raw Efficiency: What’s Really Behind Cost Gaps

What’s interesting here is how much of the “efficiency” story isn’t really about cow management or even genetics anymore. I talked to a Central Valley manager running 5,000 cows who summed it up: “We buy grain by the unit train—110 railcars. Our delivered price is CBOT minus basis, sometimes 15 cents lower. My neighbor with 300 cows pays elevator price, plus haul; that’s 40, 50 cents more per bushel.”

It’s not just West Coast operations seeing this. In the Upper Midwest, neighbors share similar experiences. Volume buyers get priority and save dollars, not because they feed cows better, but because they can buy enough at once to command a discount.

Bring in finance, and the gap widens. Published rates show 2,000-cow herds receiving prime plus 0.5%. A 200-cow farm might see prime plus two. On a $1 million note, that’s more than $15,000 a year in extra interest just for being smaller.

Then consider environmental compliance. The latest Wisconsin Department of Ag reports—which many of us turned to during the farm planning season—show the cost of nutrient management, methane compliance, and water permits comes out to 50 cents/cwt for the largest herds, but easily $15/cwt or more for the smallest. It’s the same paperwork, same inspector fee—just spread over far fewer cows and pounds.

The scale advantage isn’t about better farming—it’s about systematic structural advantages that give large operations a $4/cwt cost edge through volume discounts on feed, preferential financing rates, amortized regulatory compliance costs, and labor efficiency, creating a $100,000 annual penalty for a 500-cow farm that has nothing to do with management quality.

The Co-op/Processor Crossover: Facing Up to the Math

Now, here’s where a lot of dinner-table talk turns pointed. Vertical integration with co-ops, especially after big moves like DFA’s $425 million purchase of Dean Foods’ 44 plants, changes the dynamic. Industry estimates now indicate that more than half of DFA members’ milk flows through DFA plants.

There’s no way around it: when your co-op is both your “agent” and your buyer, it faces a built-in conflict. The original co-op job—fight for a fair farm price—collides with the processor’s goal: keep input costs as low and steady as possible.

A Cornell ag econ professor put it bluntly at last year’s co-op leadership workshop: “Co-ops owning plants face incentives that are tough to align. You can’t maximize both farmer pay price and processing margin.” And I’ve seen the evidence myself; the research shows co-ops often have lower stated deductions, but within the co-op group, “other deductions” can vary wildly. As one board member told us, “Transparency on this stuff is hard for everyone, even when we want it.”

Think about it: if your co-op owns the plant, is the negotiation about pay price truly across the table or just across the hallway?

Canadian Lessons: Costs and the Future

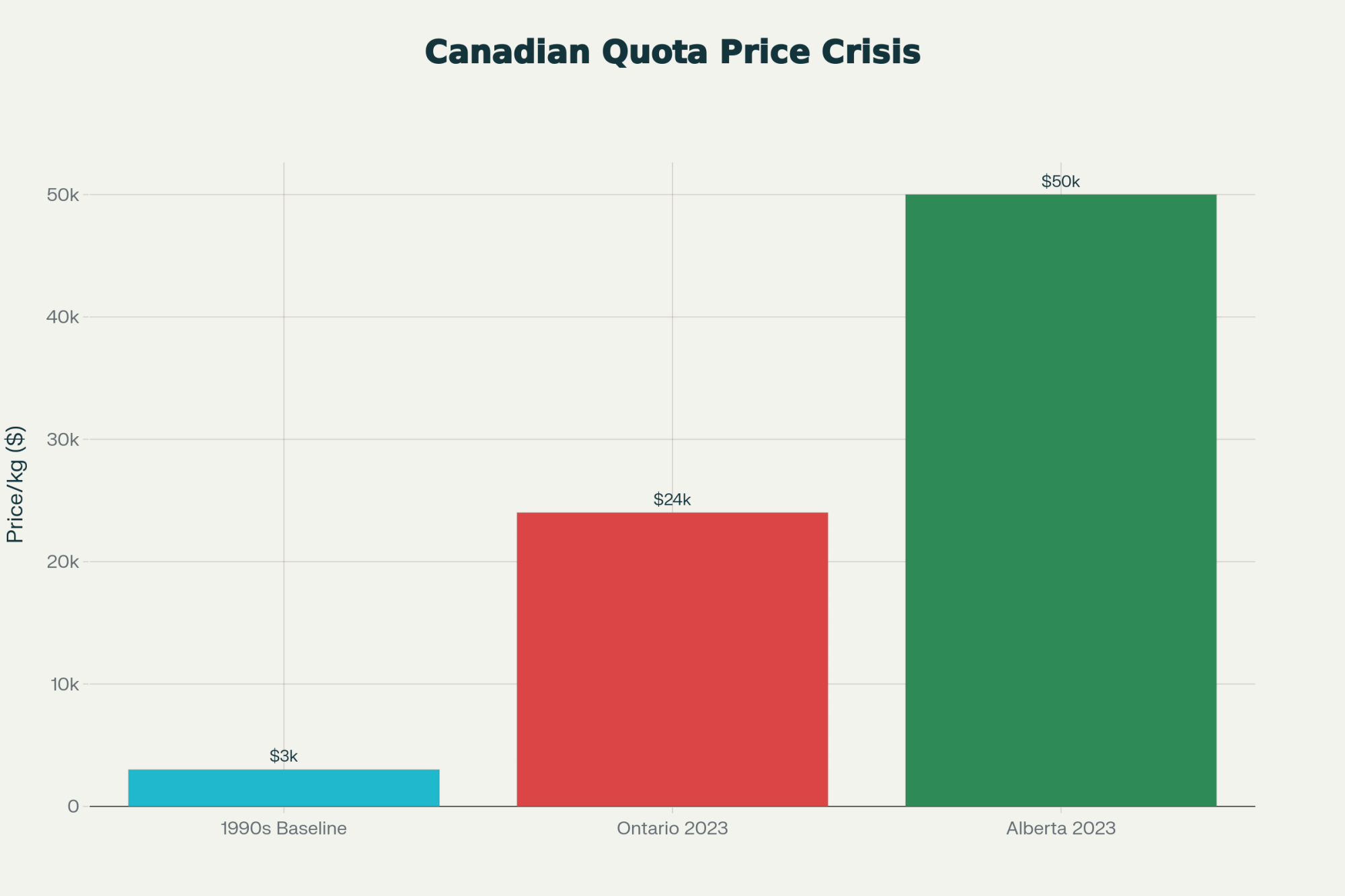

Now, Canadian friends watching these trends aren’t immune either. The Canadian Dairy Information Centre’s latest data puts the last decade’s dairy farm reduction at over 2,700, even under supply management. And quota levels are a choke point: In Ontario, with a strict cap, quota changes hands around $24,000 per kilo of butterfat; Alberta’s uncapped market runs up past $50,000.

A young producer near Guelph explained it best: “We want to keep the farm in the family, but the math now is about buying quota at market rate from Dad—he paid $3,000/kilo in the ’90s. I pay $24,000/kilo or more, and start so far behind on cash flow it feels impossible.”

Canadian dairy quota prices have exploded from $3,000 per kilogram in the 1990s to $24,000 in Ontario and $50,000 in Alberta by 2023—a 1,567% increase that creates an impossible generational wealth transfer barrier, forcing young farmers to begin their careers hundreds of thousands of dollars in debt simply to acquire the right to produce milk their parents obtained for a fraction of the cost.

Producers Team Up—and Win

We should all pay attention to how producers abroad have responded. In Ireland, Dairygold tried to drop prices, but farmers quickly networked on WhatsApp. Once they started comparing pay stubs, they discovered inconsistencies—same pickup, same composition, different pay. They organized: “If 200 show up with real data, will you join?” The answer was yes. Six weeks, 600 farmers, and the transparency improved, the price cut was rescinded.

That lesson isn’t just for Ireland. That’s modern farm business—facts and solidarity over rumors and grumbling.

U.S. Adaptation Tactics: What’s Working

Across the U.S., I’ve watched farmers embrace savvy but straightforward approaches. Central Valley producers doubled back to their milk checks and truck bills and found that some paid 20 cents/cwt more for identical hauls. As a group, they pressed for change—and got it.

Midwesterners have started bottling their own milk—Wisconsin’s extension reports show farmgate price benefits of $2 to $4 a gallon, though yeah, getting there takes $75,000 to $100,000 and some serious compliance stamina.

Debt is a fresh challenge in its own right in cow management. Now’s the time to renegotiate any credit above prime plus one. Dropping even one percent on a $2 million note brings $20,000–$25,000 savings straight to the P&L.

Environmental Law: A Sea Change

California’s methane digester rules, fully phased in over the past two years, are a classic case of “scale wins again.” For big operations, $4 million-plus digesters can become a profit center—especially if you trade renewable natural gas credits north of $1 million a year. Small farms? They can’t justify the capital, so the compliance cost splits unevenly—UC Davis economists show $2/cwt for small farms, under 50 cents for the largest.

It’s not about better manure management; it’s about who can amortize the cost.

The Path Ahead: What’s Next in Dairy Consolidation

The USDA’s Economic Research Service expects U.S. dairy farm numbers to dip below 10,000 by the mid-2030s, with Canadian farm numbers also dropping to around 4,000–5,000. That’s the math if nobody changes the model or the market.

But honestly, what gives me hope are examples of when perseverance, innovation, and strategic shifts pay off. In Wisconsin, several smaller herds now sell directly into grass-fed cheese contracts, pulling in a $4/cwt premium (more than make-allotment size, less fight for line space). “We stopped competing with 5,000-cow barns by beating them at their game,” one farmer told me. “We get paid for our story and our butterfat.”

Where To Focus Now

Calculate Your Position Honestly. Know your true cost—family living included—against hard local benchmarks. If the numbers don’t lie, accept what you see and plan accordingly.

Don’t Go It Alone. From paycheck audits to volume negotiations, the farms that win increasingly do so together.

Strategic Awareness Beats Production Alone. The future belongs to those who know how pricing, processing, and consumer trends intersect—and find their “crack” in the system instead of just producing more.

As Tom Vilsack put it at a dairy business roundtable: “We love to say we’re saving family farms, but policy and business choices keep rewarding bigness and consistency.” No matter your model—organic, conventional, something in between—the goal is to find your margin, your allies, and your leverage.

The numbers will keep changing, but one reality holds—those who adapt, share, and innovate stand the best chance. Old rules are being rewritten, and it’s worth being part of that conversation. For deep dives on industry economics, co-op strategy, and farm resilience, visit www.thebullvine.com.

KEY TAKEAWAYS

Butterfat numbers and raw efficiency don’t guarantee survival—market scale, price leverage, and transparency do.

Question every deduction and demand clarity from your co-op or processor—internal conflicts don’t have to shortchange you.

Benchmark your costs with neighboring farms and negotiate together—solo producers rarely win against consolidated buyers.

The farms thriving today are adapting: going direct-to-consumer, value-adding, or finding specialized markets to earn more per cwt.

Success in modern dairy comes from forward planning, embracing new models, and building your own leverage—not waiting for the system to “fix itself.”

EXECUTIVE SUMMARY:

Dairy’s old rules—“be efficient and you survive”—no longer hold. Drawing on real farm stories and national data, this investigation exposes why scale, access, and co-op consolidation matter more than top cow performance. You’ll see how market power and processor influence—not just farm management—decide who survives and who sells out. With insights from producers challenging these trends, along with practical strategies and benchmarks, this article is a must-read for anyone rewriting their playbook. Get the facts, the framework, and a clear-eyed look at what real success in dairy now demands.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Your 2025 Dairy Gameplan: Three Critical Areas Separating Profit from Loss – Reveals specific operational adjustments—from silage density to amino acid balancing—that can generate $500+ per cow in additional net income, offering a tactical way to combat the structural cost disadvantages highlighted in the main article.

Decide or Decline: 2025 and the Future of Mid-Size Dairies – Delivers a strategic ultimatum for the “squeezed” mid-sized herds discussed above, analyzing why standing still drains 6-8% of equity annually and outlining two viable survival models: specialized optimization or calculated expansion.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

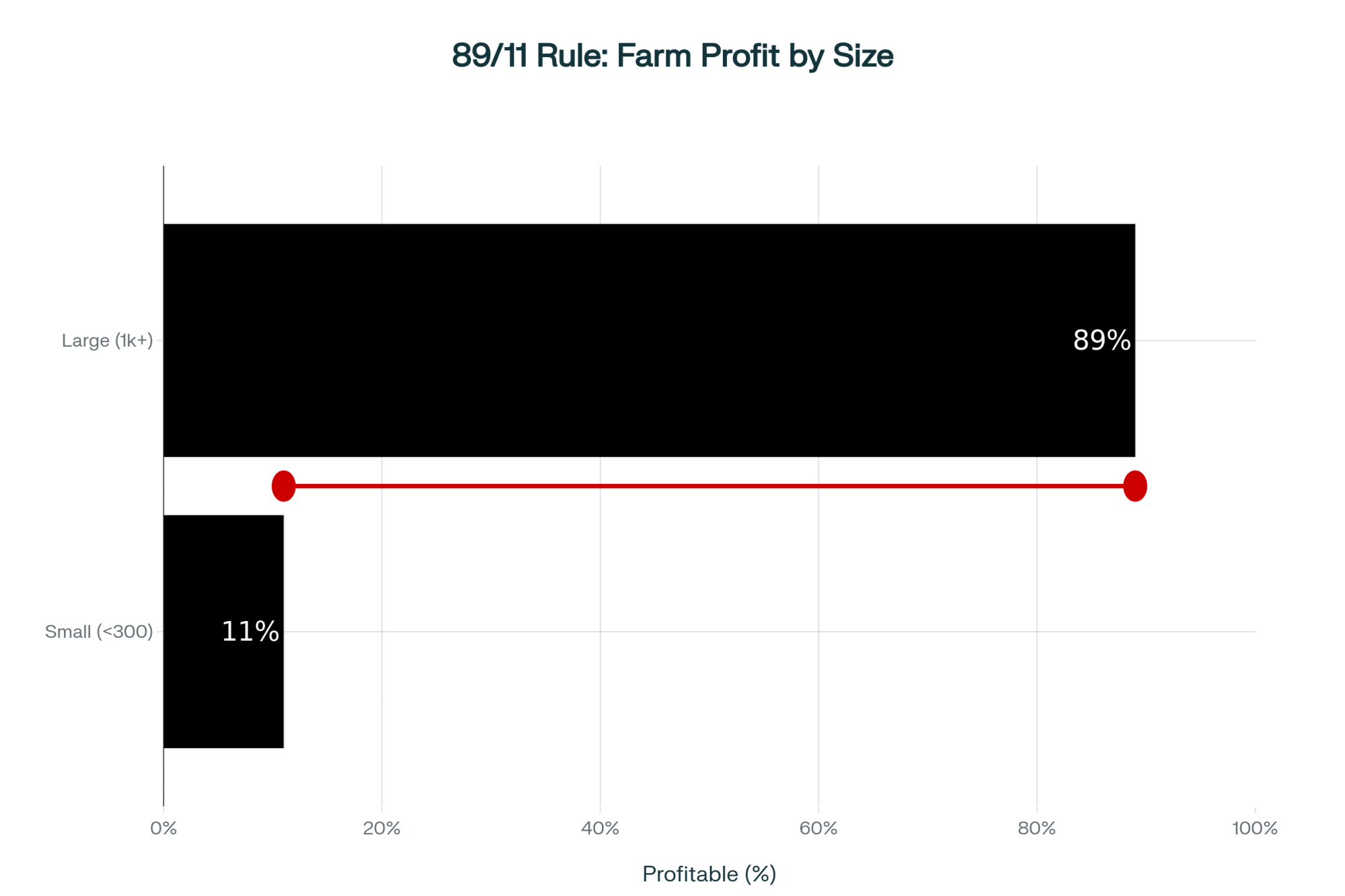

Only 11% of dairies under 300 cows are profitable. But three paths still work—if you move in the next 18 months.

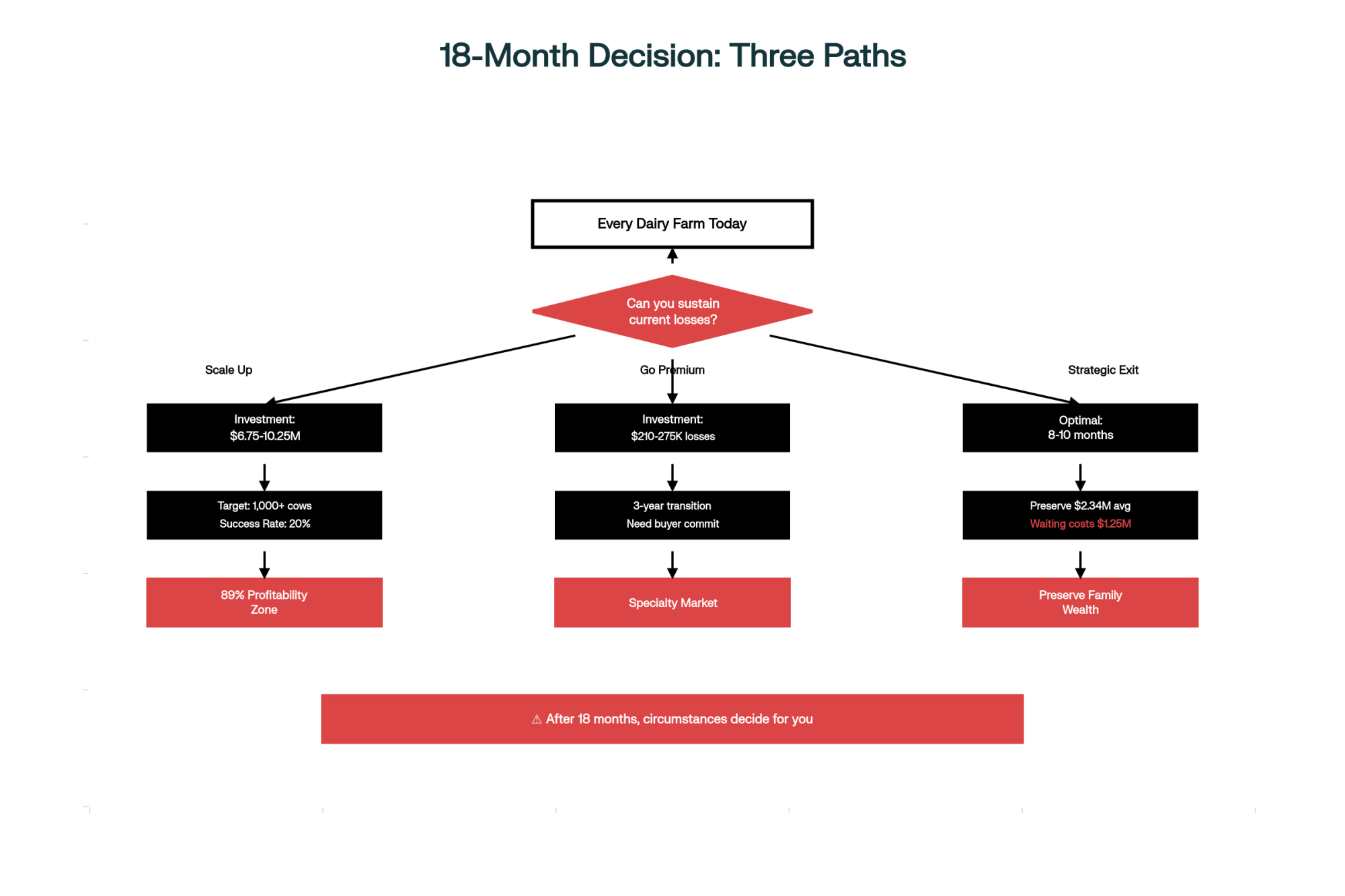

EXECUTIVE SUMMARY: Lactalis cutting 270 dairy farms while investing $11 billion in processing isn’t a contradiction—it’s the clearest signal yet that commodity milk is finished and component quality now rules everything. The stark reality: 89% of dairies over 1,000 cows are profitable while only 11% under 300 cows make money, and this isn’t about management skill—it’s structural economics you can’t overcome with hard work alone. Three converging crises (interest rates doubling to 8%, heifer inventory at 20-year lows, and labor costs up 73%) have compressed what was once a gradual 5-year industry shift into an urgent 18-month decision window. Every dairy faces three paths: invest $6.75-10.25 million to scale beyond 1,000 cows, transition to premium markets (organic/specialty) despite 3-year losses, or exit strategically while you can still preserve family wealth. Real farmers are already choosing—a Minnesota couple successfully scaled to 1,100 cows, Vermont neighbors transitioned to organic, and a Wisconsin family preserved $2.1 million through strategic sale. The difference between 3.6% and 4.2% butterfat is now worth $529,000 annually for a 500-cow operation, making component performance literally the difference between survival and closure. Your window to control this decision closes in 18 months—after that, circumstances decide for you.

You know, when Lactalis—the world’s largest dairy processor—announces they’re cutting 450 million liters and ending contracts with 270 French farmers, we should probably pay attention. I’ve been digging into this, talking with producers, looking at the numbers… and what’s interesting is this isn’t just another market cycle. We’re seeing something bigger here, something that’s going to affect all of us, whether we’re milking 50 cows or 5,000.

What I’ve found is that the traditional commodity dairy model—you know, the one most of us grew up with—it’s changing faster than anyone expected. And the timeline to adapt? Well, that’s gotten surprisingly short.

The 89/11 Rule reveals the stark reality: structural economics, not management quality, determines survival in modern dairy

Understanding Why Processors Are Making These Moves

So here’s what caught my attention in Lactalis’s 2024 financials: €30.3 billion in revenue, but only 1.2% net profit margins. That’s down from 1.45% the year before. Now compare that to their premium products—the yogurt division they bought from General Mills is generating 15-20% operating margins. Premium cheese? Consistently 8-12% margins.

Lactalis’s supply director explained in their October statement that the valuation of excess milk is often very low and subject to market volatility—language that really reflects how processors are viewing commodity markets these days. When a processor that size essentially says commodity milk isn’t worth the trouble… well, that’s not just complaining, is it?

FrieslandCampina’s been going through similar challenges. They’ve talked about timing mismatches—buying milk at one price, processing it, then having to sell into a lower market. That kind of volatility makes it really tough to plan, and shareholders don’t like uncertainty.

The Component Game Has Changed Everything

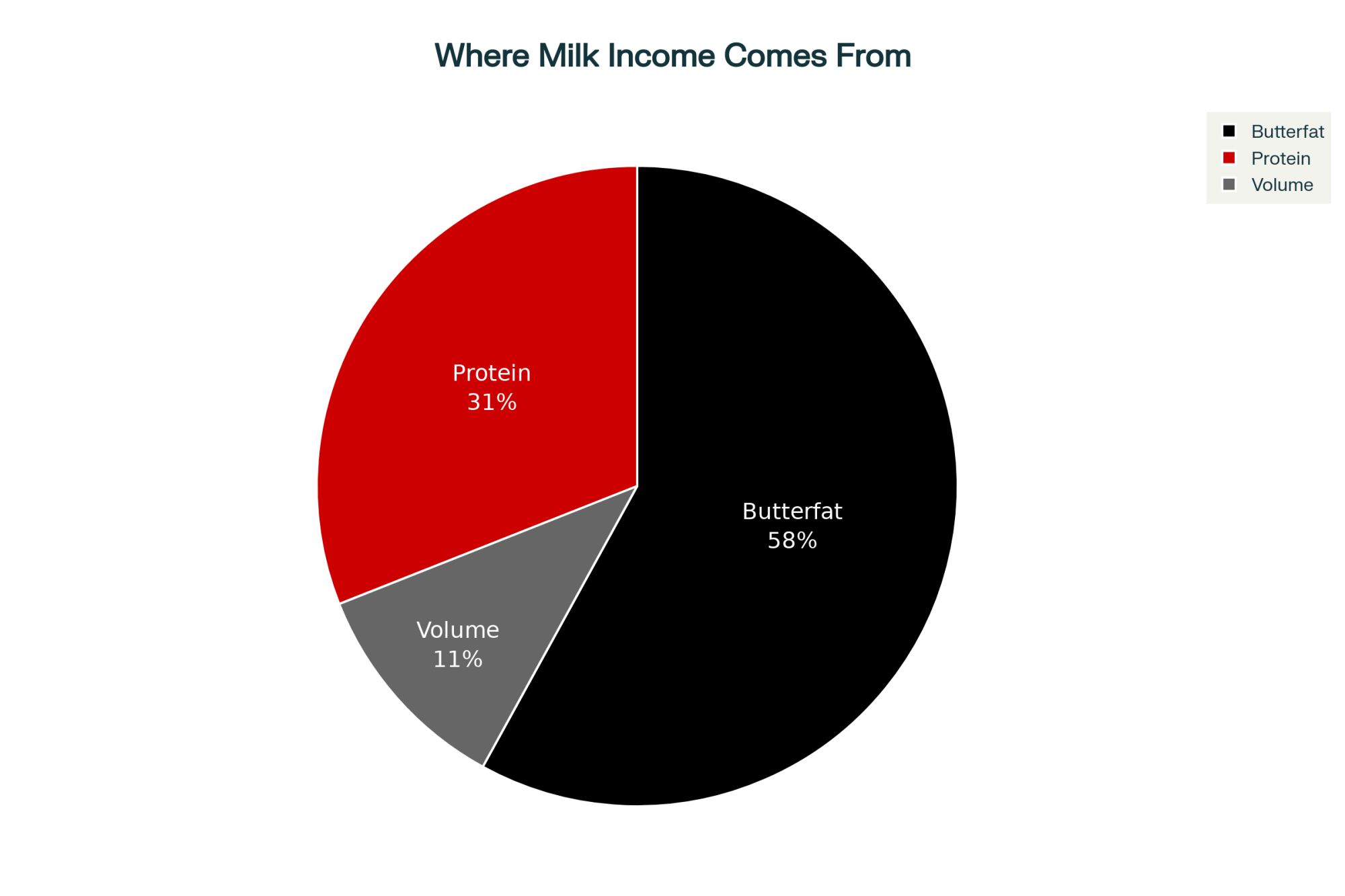

Component performance is now non-negotiable—volume alone won’t pay the bills anymore

I was talking with a Wisconsin producer last week—he’s running 650 cows near Fond du Lac—and he helped me understand just how much components have shifted the whole economics of dairy farming. USDA data from November shows butterfat now represents 58% of your milk check value, and protein adds another 31%. Think about that… 89% of your income comes from components, not volume.

His neighbors who consistently hit 4.23% butterfat compared to the regional average of 3.69%? They’re capturing about $4.60 more per hundredweight. For a 500-cow operation producing 23,000 pounds per cow annually, that works out to roughly $529,000 in additional revenue—though your actual numbers will vary with production levels and regional premiums, of course.

Cornell’s latest farm business data shows some interesting patterns:

The big operations—1,000+ cows—they’re hitting 4.0-4.3% butterfat with 3.3-3.5% protein pretty consistently

Mid-sized farms, say 300-500 cows, generally average 3.6-3.8% butterfat, 3.0-3.1% protein

And here’s what’s telling: large farms maintain about 2% daily variation in components while smaller operations see 5-10% swings

Now, getting those high components isn’t just about genetics. You need systematic management—a good nutritionist runs $80,000 to $120,000 a year, based on what I’m hearing. Feed testing programs add another $15,000 to $25,000. Those precision feeding systems? Dealers are quoting $250,000 to $500,000, depending on what you need.

The math gets tough for smaller operations. When you spread the combined cost of nutritionist, vet services, and consultants across a thousand-cow operation, it might come to $0.08-0.12 per hundredweight. But for a 200-cow farm? You’re looking at $0.40-$0.60 per hundredweight for the same level of professional support. That’s a huge competitive disadvantage.

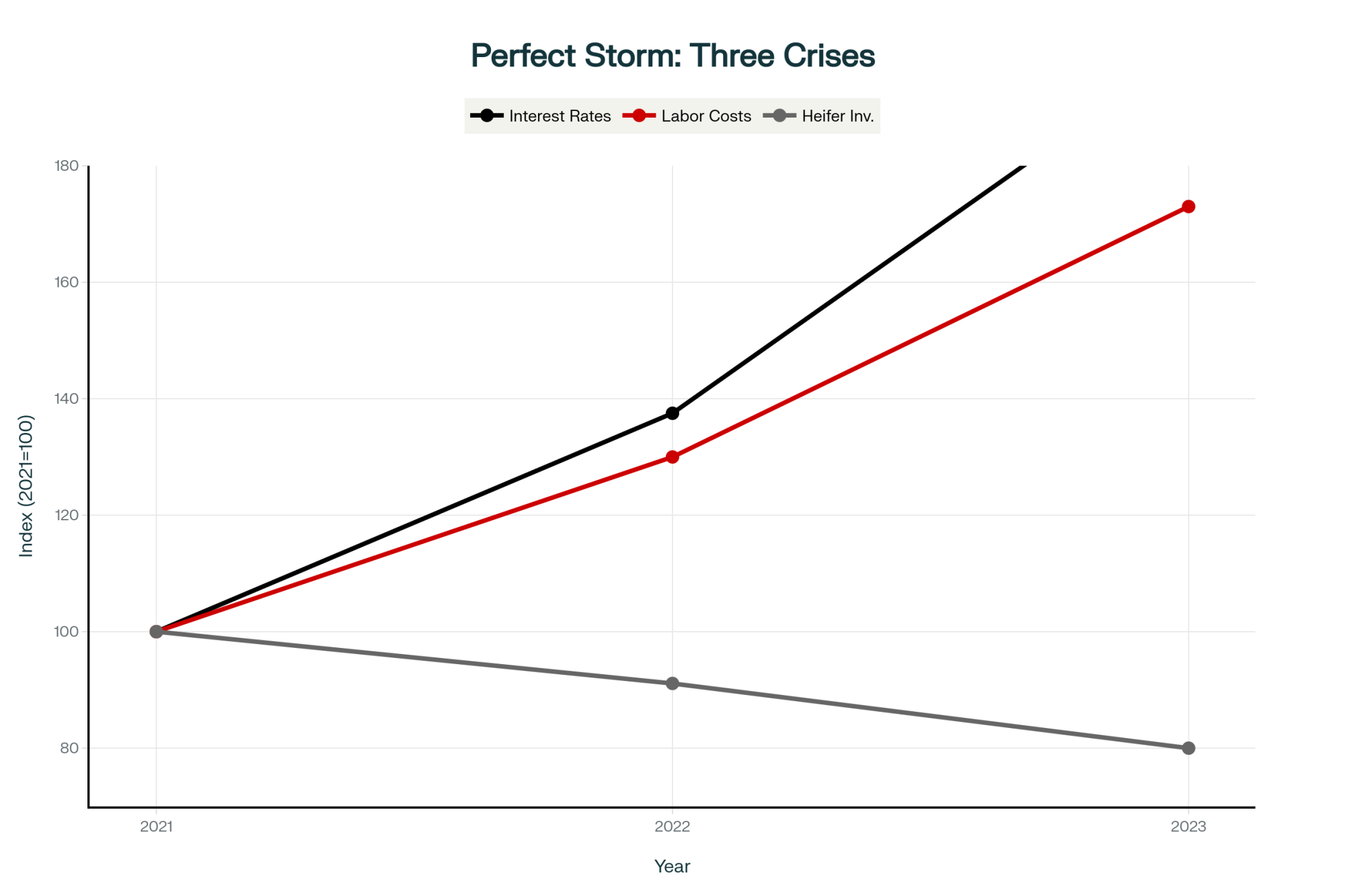

Three Things Hitting Us All at Once

Cornell’s dairy economics team has been documenting what they’re calling a compressed decision timeline, and I think they’re onto something. Three things have converged, forcing us to make decisions faster than we’re used to.

Three converging crises compressed a gradual 5-year industry shift into an urgent 18-month decision window

Interest Rates Hit Like a Hammer

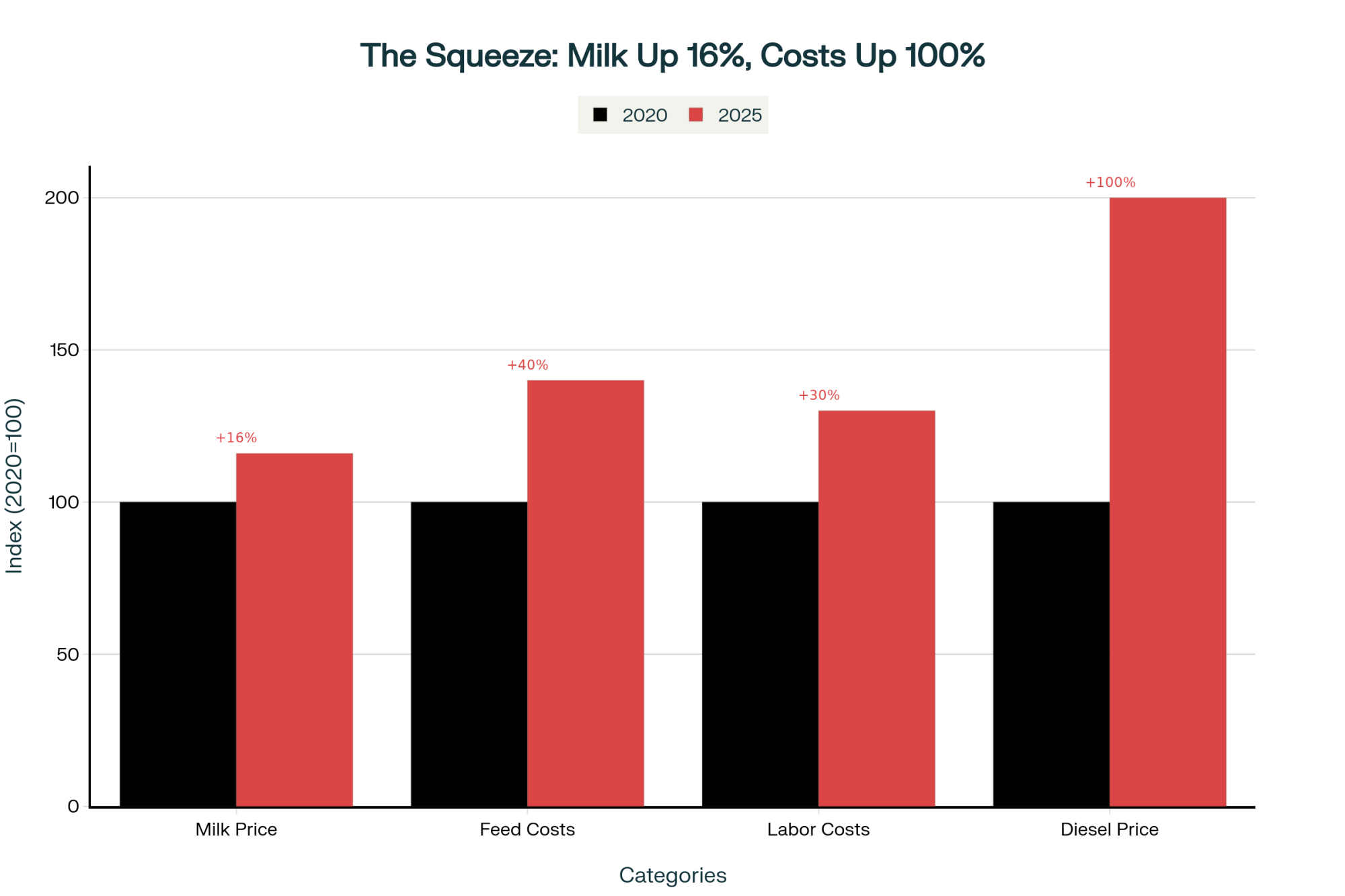

Federal Reserve data shows operating loan rates doubled—went from about 4% in 2021 to over 8% by late 2023. Haven’t seen rates like that in 20 years. A lender in Pennsylvania told me that operations that were barely profitable at 4% are now losing $3,000 to $5,000 monthly.

The Illinois farm management folks found that farms carrying significant debt saw interest costs per tillable acre jump from $33 to $60 in three years. That’s 82% more in fixed costs, and you can’t pass that along to your milk buyer.

What really concerns me is the Q3 2024 ag lending data—operating loan volumes are up over 30% for the third quarter in a row. A Wisconsin banker friend put it best: “This isn’t growth borrowing, it’s survival borrowing.”

The Heifer Shortage Nobody Saw Coming

CoBank’s August report lays out a fascinating situation—dairy heifer inventory’s at a 20-year low just when we need expansion for all this new processing capacity.

Here’s how we got here: the breeding data shows beef semen sales to dairy farms tripled from 2.5 million units in 2017 to 7.2 million by 2020. Last year? 7.9 million of the 9.7 million total units were beef semen.

Can’t blame anyone really. When beef calves were bringing $1,000 to $1,500 last October, while it costs $2,200 to $2,500 to raise a heifer worth maybe $1,600… the math was obvious. Problem is, we all did the same math at the same time.

CoBank thinks we’ll lose another 800,000 head before things turn around in 2027. An Idaho producer told me he’s been offered $3,200 for breeding-age heifers—if he had any. “Five years ago at $1,400, I had too many,” he said. “Now I can’t find them at any price.”

Labor Is Getting Impossible

Texas A&M’s 2024 research shows that immigrant workers make up 51% of dairy labor and milk 79% of our cows. Their models suggest losing that workforce would cut U.S. milk production by 48.4 billion pounds annually. That’s not a typo.

And it’s not just finding workers—it’s affording them. USDA data shows dairy wages went from $11.54 an hour in 2015 to $18-20 by 2024. A large operations manager in New Mexico told me they’re at $28 an hour when you factor in housing, benefits, and recruitment. “And we still can’t stay fully staffed,” he added.

Three Producers Who Found Their Way Through

Despite all these challenges, I’ve met several operations that have successfully navigating this transition. Let me share what they did differently.

Smart Scaling in Minnesota

There’s a couple in central Minnesota who expanded from 350 to 1,100 cows between 2019 and 2023. They saw their co-op’s base program would limit growth for mid-sized farms, so they moved early. Got financing at 3.5% before rates spiked, used sexed semen exclusively for three years to build internally, and partnered with an experienced Venezuelan family.

What’s smart is they expanded in phases over four years—each phase had to cash flow before they moved to the next. They’re now shipping butterfat at 4.1% consistently and have signed a five-year contract with a cheese plant 40 miles away. Their breakeven’s around $17.50 per hundredweight, so they’ve got a cushion even when markets get tough.

Going Organic in Vermont

A Vermont family with 480 cows went organic in 2021—right when everyone said that market was full. Key thing? They got Organic Valley’s commitment in writing before starting the transition. They lost $210,000 over three years, but off-farm income and some timber sales bridged the gap.

Today, they’re netting $3.80 per hundredweight after all costs. “We focused on keeping cows healthy and production steady rather than trying to expand during transition,” the son told me. They maintained 92% of conventional production throughout the transition—well above the 85% average.

Making the Tough Call in Wisconsin

This one’s harder to talk about. A couple near Eau Claire sold their 280-cow operation in March 2024 after recognizing they were in what economists call the 18-month window—sustained losses with limited options. At 58, with kids established off-farm, expanding to a competitive scale meant $6 million in new debt.

They sold into a strong cull market, leased the cropland to a neighbor, and kept the house and 40 acres. The husband’s now using his 30 years of experience as a co-op field rep. “I sleep better, my wife’s happier, and financially we’re ahead,” he told me. They preserved about $2.1 million in equity that probably would’ve disappeared if they’d hung on another year.

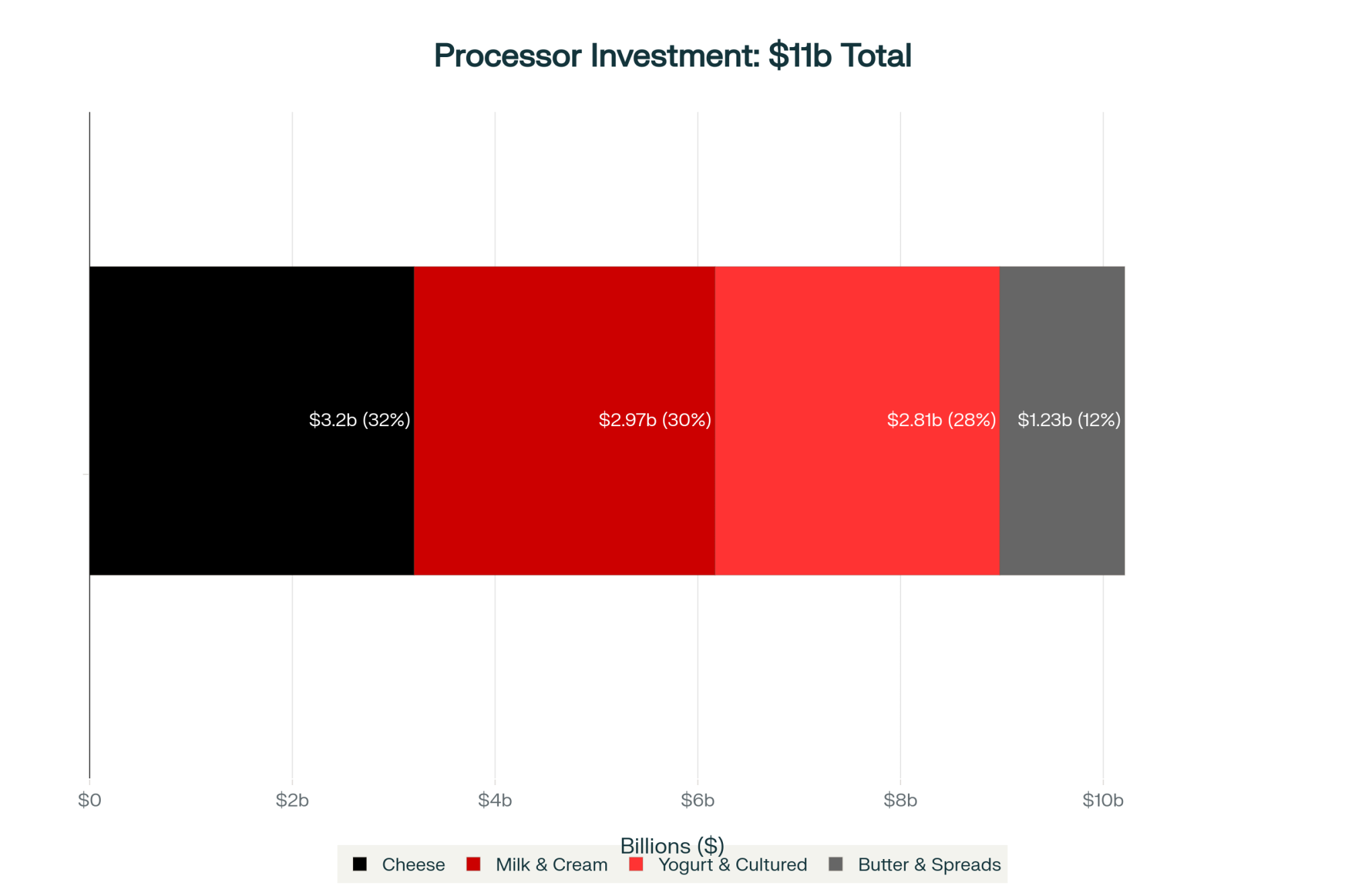

Where All This New Processing Investment Is Going

Processors already chose their future—understand their strategy to predict yours

IDFA announced $11 billion in new processing capacity, and where that money’s going tells you everything about industry direction. Their October breakdown shows:

Cheese gets $3.2 billion—32% of everything

Milk and cream processing: $2.97 billion—30%

Yogurt and cultured products: $2.81 billion—28%

Butter and spreads: $1.23 billion—12%

Three new cheese plants in the Texas Panhandle need 20 million pounds of milk daily by mid-2025. But these aren’t commodity operations—they’re component extraction facilities making mozzarella for export while capturing valuable whey proteins.

What they’re NOT building? Commodity powder plants or basic fluid bottling. A processing engineer in Wisconsin explained it well: “We’re maximizing value from every component now. Just removing water to make powder doesn’t cut it anymore.”

And here’s something else—up in the Northeast, a couple of smaller specialty cheese operations just expanded. They’re not huge, but they’re finding success focusing on local markets and agritourism. Different model entirely from the big Texas plants, but it shows there’s more than one way forward. Out in California’s Central Valley, I’m seeing similar patterns with artisan operations carving out niches even as the big players consolidate.

The Cooperative Evolution We Need to Talk About

This is uncomfortable for many of us, but cooperatives have changed dramatically since DFA was formed in 1998 through regional mergers. They now control 30% of U.S. milk production, and after buying 44 Dean Foods plants in 2020, they’re both the biggest milk marketer AND processor.

A former board member explained how this creates tension: “When your co-op owns processing plants, optimizing those facilities becomes as important as your milk check—sometimes more important.”

Base-excess programs show this complexity. Cornell’s research indicates these programs typically use your best three consecutive months over three years as “base.” Milk over that? You might pay penalties of $5 to $13.30 per hundredweight.

A Vermont producer shared his frustration: “We wanted to add 50 cows to get more efficient, but overbase penalties would’ve killed any benefit. We’re locked at the current size.”

Meanwhile, operations that were already large when base programs started? They’re fine. It’s the 300-cow farms trying to grow to 500 that get squeezed.

Your Three Paths Forward—Let’s Look at Real Numbers

Path Comparison at a Glance

Factor

Scale Up

Go Premium

Strategic Exit

Investment

$6.75-10.25M

$210-275K losses

Preserve equity

Timeline

4-5 years

3-year transition

8-10 months optimal

Success Rate

~20%

Varies by market

100% if timed right

Key Risk

Debt burden

Market saturation

Waiting too long

Extension economists from Cornell and Wisconsin show that farms with sustained losses typically face critical decisions within 12-18 months. So what are your actual options?

Path 1: Scale Up to Compete

Investment Required: $6.75-10.25 million total

Buildings and infrastructure: $3.5-5.0 million

Cattle at current prices: $2.25-3.0 million

Feed base expansion: $500,000-1.5 million

Working capital: $500,000-750,000

Success Rate: According to lending industry estimates, about 20% achieve projected returns. Key Factor: Usually need family money for unexpected challenges. Financing Options: USDA FSA offers beginning farmer programs and guaranteed operating loans through participating lenders, though eligibility and terms vary by operation and region. Some states also have specific dairy expansion programs worth exploring.

Path 2: Find Your Premium Market

Organic Transition Example:

Typical losses: $210,000-275,000 over 3 years

Pay organic feed prices (30-50% higher) while getting conventional prices

Need written buyer commitment before starting

Must maintain 85%+ production through transition

Potential Returns: $2.45/cwt net (vs. -$5.29 for conventional, based on USDA 2023 data). Reality Check: Most regions aren’t currently seeking new organic production. Alternative Options: Consider grassfed certification, A2A2 markets, or local/regional branding

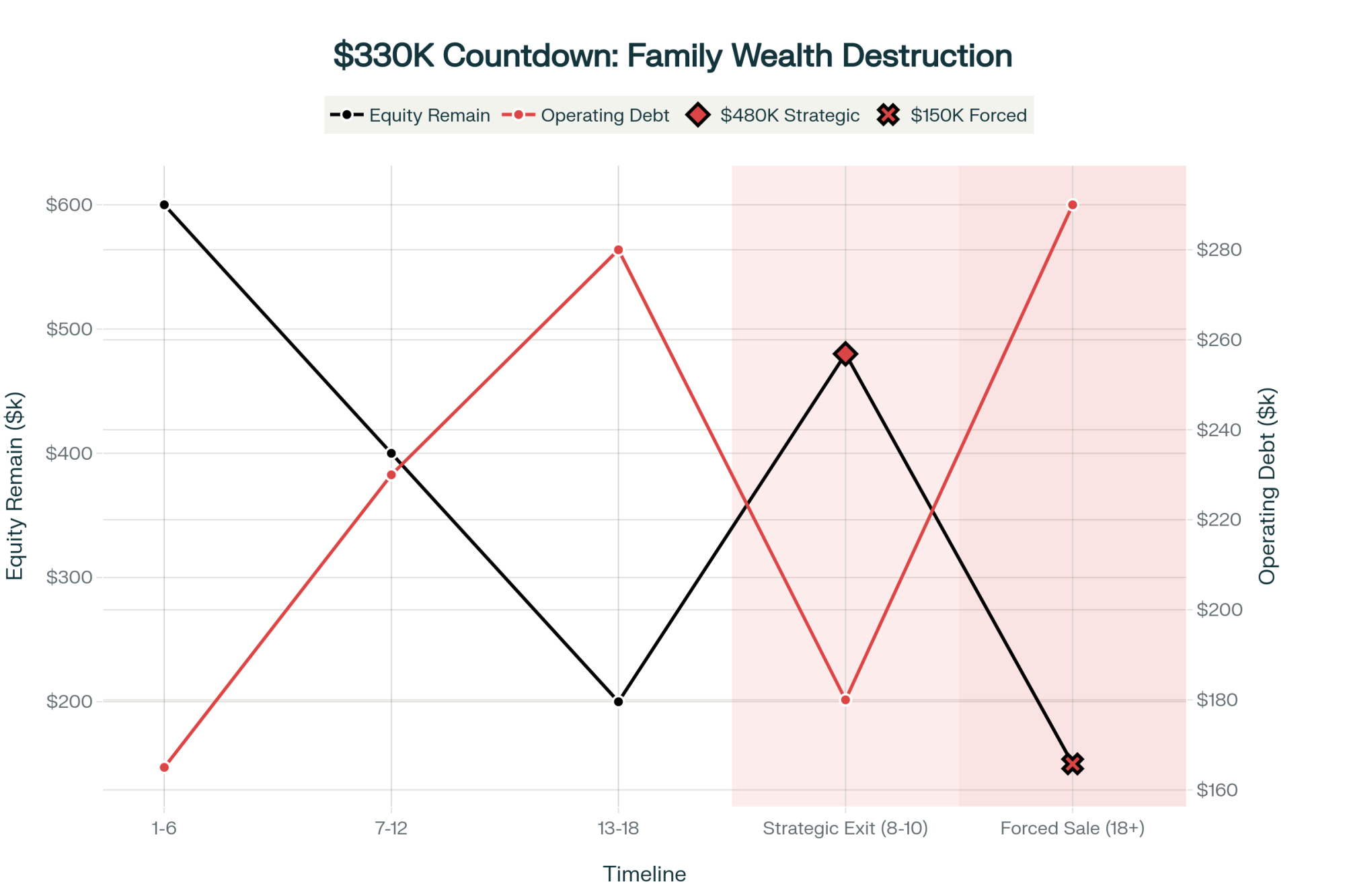

Path 3: Strategic Exit While You Can

Timing Matters—Example for 300-cow operation with $2M debt:

Exit at 8-10 months:

Assets bring ~$4.65 million

After $2M debt and costs ($230,000-390,000): $2.26-2.42 million preserved

Forced sale at 16-18 months:

Assets bring ~$3.4 million (discounted)

After everything: $650,000-970,000 retained

The difference: Over $1.4 million in family wealth

Three paths still work—but only if you move in the next 18 months. After that, circumstances decide for you

The Technology Wave is Coming Fast

I attended the Protein Industries Summit in Chicago last month, and what I heard was eye-opening. McKinsey’s early 2025 biotech analysis shows precision fermentation has already hit cost parity for certain dairy proteins. Boston Consulting thinks these proteins will be five times cheaper than ours by 2030.

Here’s what’s already happening—Perfect Day’s animal-free whey is in Ben & Jerry’s ice cream right now. Not someday. Today. Fonterra’s partnerships with Superbrewed Food and Nourish Ingredients show where big players are heading. Fonterra indicated in its August 2024 announcements that ingredients from these technologies can be used alongside traditional dairy products. Translation: they’re building systems that can use proteins from cows or fermentation tanks—whatever’s cheaper.

And it’s not just startups anymore. I’m seeing major food companies quietly building fermentation capacity. They’re hedging their bets, preparing for a world where they can source proteins from multiple streams.

How This Hits Different Regions

This transformation affects regions differently, and understanding your local dynamics matters.

California: UC Davis research shows farms with less than 22% quota coverage pay more into the system than they get back. “We’re subsidizing the big quota holders,” a Tulare County producer told me.

Southeast: Maintains higher Class I fluid use—over 60% according to Federal Orders—which provides some buffer since processors need consistent daily deliveries. But even there, consolidation pressure is building.

Upper Midwest: All about cheese, so components rule everything. Wisconsin processors consistently tell me 4% butterfat is their practical minimum for preferred suppliers.

Plains States: Seeing aggressive expansion with new processing, but these plants want a minimum of 50,000+ pounds daily per farm. Can’t deliver that volume? You won’t get a contract.

Pacific Northwest: Interesting developments with smaller operations finding niches in farmstead cheese and direct marketing. Not for everyone, but it’s working for some.

Northeast: Beyond the specialty cheese operations, there’s also growth in agritourism and on-farm processing. Entirely different economics, but viable for the right location.

Western States: Water rights and environmental regulations adding another layer of complexity to expansion decisions.

Questions to Ask Yourself Right Now

Before you make any big decisions, honestly assess:

Are you covering all costs, including family living?

Can you achieve 4%+ butterfat consistently?

Do you have succession lined up?

What’s your debt-to-asset ratio?

Could you survive another year like 2023?

What would happen if you lost two key employees tomorrow?

Is your processor investing in commodity or specialty capacity?

Are there emerging environmental regulations that could affect you?

What This All Means for Your Planning

After looking at all this, here’s what I think matters most:

Component performance isn’t negotiable anymore. The difference between 3.6% and 4.2% butterfat can mean hundreds of thousands annually for a 500-cow operation. That fundamentally changes farm economics.

That 12-18 month window Cornell documented? It’s real. Interest rates, heifer availability, and labor costs compressed what used to be a multi-year adjustment into a much shorter period. Within the next 12-18 months—essentially by mid-2026, based on the timeline Cornell economists have documented—many operations will have made their choice, voluntarily or not.

Scale economics show clear breaks. USDA data showing 89% profitability for 1,000+ cow operations versus 11% for under 300 cows… that’s not about who’s a better manager. It’s structural advantages smaller operations can’t overcome.

Your processor’s strategy matters more than ever. If they’re investing in commodity powder, you’ve got time. If they’re building component extraction or specialty facilities, that tells you something different.

Technology adoption keeps accelerating. The Good Food Institute tracked $840 million in precision fermentation investment last year. Alternative proteins are moving from the experimental to the commercial stage faster than most of us expected.

Risk management tools—like Dairy Margin Coverage and Dairy Revenue Protection—might buy you time but won’t change the fundamental economics. They’re Band-Aids, not cures.

The Bottom Line

What Lactalis is doing—cutting 450 million liters while investing in premium capacity—makes sense when you understand their strategy. They’re consolidating relationships with farms that can deliver consistent, high-component milk at scale while preparing for fermentation-derived proteins.

The Minnesota couple who scaled smart, the Vermont family succeeding in organic, the Wisconsin couple who preserved wealth through planned exit—they all made different choices. But they shared a realistic assessment of where things are heading and made decisions accordingly.

For those of us still figuring out our path, an honest assessment of where we fit in this evolving structure is critical. Whether that means pursuing scale, finding premium markets, or planning transition, the key is making informed decisions while we still have options.

And if you’re wondering about the next generation—I talked with several young farmers recently. The ones succeeding are incredibly sharp, using technology in ways we never imagined, and they’re not afraid to try completely different models. That gives me hope, even as things change.

The dairy industry will keep producing milk—consumers guarantee that. But who produces it, how it’s valued, and what matters most? That’s changing fundamentally. Understanding where your operation fits in that transformation might be the most important analysis you do this year.

Because waiting for things to “go back to normal”? Well, I think we all know that ship has sailed.

The Bullvine provides ongoing analysis and resources at www.thebullvine.com. Cornell’s Dairy Markets and Policy program and Wisconsin’s Center for Dairy Profitability offer valuable planning tools. The producer experiences shared here reflect confidential discussions, with identifying details modified for privacy.

KEY TAKEAWAYS

You Have 18 Months to Decide: Cornell economists confirm sustained losses trigger forced decisions within this window—control your choice now or lose that option forever

Three Paths Still Work: Scale to 1,000+ cows ($6.75-10.25M investment, 20% success rate) | Go premium (organic/A2/grassfed, 3-year transition) | Exit strategically (preserves $1.4M more than waiting)

Components = Survival: The 0.6% butterfat difference between average and top herds is worth $529,000/year, and processors are making this gap the entry requirement

The 89/11 Rule: 89% of 1,000+ cow dairies profit while only 11% under 300 cows survive—this is structural economics, not management quality

Processors Already Chose: They’re investing $11B in component extraction while cutting commodity suppliers—understand their strategy to predict your future

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Seizing the Moment: Maximizing Milk Solids Output Through Strategic Nutrition and Genetics – This guide provides the tactical “how-to” for the main article’s “what.” It details precise nutritional strategies, feed supplements, and grazing management techniques for maximizing butterfat and protein, directly linking daily management to component-driven profits.

Genetic Revolution: How Record-Breaking Milk Components Are Reshaping Dairy’s Future – This piece explains the why behind the component surge: genomics. It details how millions of cattle tests have revolutionized breeding, permanently shifting the industry’s genetic base and enabling the high-component cows that processors now demand.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Your banker knows. Your co-op won’t say it. China’s birth crisis means your 300-cow dairy has 90 days to decide its fate. Here’s how.

EXECUTIVE SUMMARY: China’s 42 million tonne milk mountain isn’t temporary—it’s the product of a 48% birth rate collapse that permanently eliminates demand for 5% of global milk production. If you’re running a 200-500 cow dairy, this structural shift means you’re losing $359,609 annually compared to 2,000-cow operations, a gap that superior management cannot close. With milk prices locked at $16.50-18.00/cwt through 2027, you have exactly three viable options: borrow $8-15 million to scale beyond 1,500 cows, pivot to premium markets with guaranteed contracts (organic, A2, grass-fed), or execute a strategic exit that preserves your equity. The difference between acting now and waiting is stark—strategic exit today nets 70-85% of equity ($1.5M), while forced liquidation in 12 months recovers just 30-50% ($700K). Every month of indecision bleeds $23,000-55,000 through operating losses and accelerating asset depreciation. Your Q1 2026 decision isn’t about whether you’re a good farmer—it’s about whether you’ll control your family’s financial future or let market forces decide for you.

Let me share something that’s been on my mind lately—and I think it deserves careful attention from every dairy farmer reading this. China’s sitting on 42 million tonnes of surplus milk, based on their agriculture ministry’s September reports. That’s roughly 5% of global production, just… sitting there. And here’s what’s interesting: this isn’t your typical market cycle that we’ve all weathered before.

You know, I’ve been digging through the data, talking with economists at Cornell and Wisconsin’s dairy programs, and what’s emerging is a picture that’s fundamentally different from anything we’ve navigated since—well, probably since we all switched from hand milking to mechanical systems. Understanding why this time really is different —and knowing what steps to take right now —could make all the difference for your operation over the next 24 months.

Why This Crisis Breaks All the Old Patterns

So I was looking back at my notes from the 2009 downturn the other day. Remember that one? USDA data shows all-milk prices bottomed out at $11.30 per hundredweight in July 2009, then bounced right back within 12 months. The 2016 slump—you remember, when Russia imposed an embargo and the EU eliminated quotas—that stabilized within 18-24 months, according to the dairy network analysis I’ve been reviewing. Even COVID, for all its disruption, saw our sector adapt remarkably well within months. There’s actually some fascinating research in the Journal of Dairy Science from 2021 documenting how quickly we pivoted.

But China? This is something else entirely.

What farmers are discovering—and China’s National Bureau of Statistics backs this—is that we’re dealing with a demographic reality nobody can fix. Their birth rate collapsed from 12.43 per 1,000 people in 2016 to just 6.39 in 2023. That’s a 48% decline, folks. The population of kids aged 0-3… you know, the ones drinking all that infant formula? Down from 47 million to 28 million in just five years. Those babies don’t exist and won’t magically appear if milk prices recover.

The numbers don’t lie: China lost 19 million formula consumers (40% decline) while birth rates crashed 48%. This isn’t a cycle—it’s permanent demand destruction that eliminates 5% of global milk consumption. Your 2027 milk price depends on markets that will never return.

Here’s what happened: After that horrific 2008 melamine scandal—six babies died, 300,000 were hospitalized according to World Health Organization reports—Beijing went all-in on dairy self-sufficiency. The Chinese began importing hundreds of thousands of Holstein cattle in 2019, according to the customs data I’ve been reviewing. Average herd sizes grew 40% year-over-year through late 2023, if you can believe it. They hit 85% self-sufficiency, up from about 70%—exactly what they wanted. Problem is, they built all this capacity assuming demand would keep growing.

Now here’s where it gets really unusual. Chinese raw milk prices have been underwater for over two years—sitting at 2.6 yuan per kilogram against production costs of 3.8 yuan, based on China Dairy Industry Association data from October. Farmers there are literally paying to produce milk. Yet production continues, propped up by government subsidies, soft loans from state banks, and political imperatives that… well, they just don’t follow normal market rules.

The Hard Math Behind Mid-Size Dairy Challenges

USDA’s Agricultural Resource Management Survey data reveal a stark cost differential across farm sizes. And this isn’t about who’s a better farmer—it’s about structural economics that management alone can’t overcome.

Looking at production costs per hundredweight from the USDA’s dairy cost and returns estimates:

Farms with fewer than 200 cows: generally running $23.68-33.54/cwt

200-499 cows: around $20.85/cwt

500-999 cows: typically $18.93/cwt

1,000-1,999 cows: averaging $17.39/cwt

2,000+ cows: down to $16.16/cwt

The brutal economics of scale: Mid-size operations face an automatic $4.69/cwt cost disadvantage ($359,609 annually for a 300-cow dairy) that no amount of management skill can overcome. Market prices lock them into structural losses through 2027.

With USDA’s World Agricultural Supply and Demand Estimates showing milk prices at $16.50-18.00/cwt through 2026-2027, you can see the problem pretty clearly. A 300-cow operation faces production costs about $4.69/cwt higherthan a 2,000-cow operation. On annual production of, say, 76,650 cwt, that’s a $359,609 competitive disadvantagebefore you even wake up in the morning.

What’s really interesting is research by agricultural economists at Wisconsin showing that management quality accounts for only about 22% of the variance in profitability. The other 78%? That comes from herd size and the resulting cost structure. Labor costs alone create roughly a $2.60/cwt difference between mid-size and large operations. Fixed overhead adds another $3.33/cwt disadvantage. Even feed costs—where you’d think everyone’s buying the same corn—show about a $1.40/cwt advantage for large operations through volume purchasing and precision nutrition programs.

You just can’t manage your way out of that kind of structural disadvantage, no matter how good you are. And believe me, I’ve seen some excellent managers struggle with this reality.

Three Paths Forward: Finding Your Best Option

After talking with farm management specialists at Penn State Extension and Farm Credit consultants across the Midwest, three viable paths keep emerging for dairy operations facing this transformation. Each has specific requirements that need honest evaluation.

Path 1: Scale to Competitive Size (1,500-2,500+ cows)

I’ve noticed that farmers considering expansion need to tick quite a few boxes before this makes sense. Agricultural lenders at CoBank and Farm Credit are generally looking for:

Debt-to-asset ratio below 40% before you even start

At least $300,000-600,000 in working capital reserves (expansion disrupts cash flow for 12-24 months, as many of us have learned the hard way)

Access to $8-15 million in financing

Another 500-800 acres of land are available

Confirmation from your processor that they can handle the additional volume

As consultants like Tom Villenga in Wisconsin often explain, it typically takes 18-24 months from groundbreaking to positive cash flow. And farmers need to understand—you’re not really farming at that scale anymore. You’re managing 8-15 employees and running a business. It’s a completely different skill set.

Path 2: Pivot to Premium Markets

This development suggests a real opportunity for the right operations. Organic milk premiums are running $8-12/cwt over conventional, based on CROPP Cooperative’s October market reports. But location matters enormously here.

Economists at Cornell’s Dyson School have documented that you need to be within 75 miles of a metro area with a population of 250,000+ to make premium markets work. The affluent consumers who pay those premiums are concentrated in specific geographic areas—that’s just the reality of it.

What farmers are finding crucial: secure your premium buyer contracts before beginning any conversion. I keep hearing stories—you probably have too—of operations that completed expensive organic transitions only to discover no premium buyers existed in their region. That’s a tough spot to be in.

The conversion timeline’s no joke either. It’s a full three years before you see those organic premiums, based on USDA’s National Organic Program guidelines. During that time, you’re incurring organic costs while still selling at conventional prices. Budget $50,000-100,000 for a 300-cow operation to make that transition, based on case studies from Vermont’s sustainable agriculture program.

Path 3: Strategic Exit While Preserving Equity

Nobody likes talking about this option, but sometimes it’s the smartest move. Industry consultants like Gary Sipiorski at Vita Plus, who’s been working with dairy operations for decades, often point out that strategic exit while you’re solvent preserves 70-85% of equity. Forced liquidation after covenant violations? You’re looking at 30-50% if you’re lucky.

Here’s something most farmers don’t know about: Section 1232 of the bankruptcy code can save substantial capital gains taxes for farmers with highly appreciated land. Agricultural bankruptcy attorneys who specialize in this area explain that if appropriately executed before selling assets, farmers can save $200,000-500,000 in capital gains taxes through a strategic Chapter 12 filing. It’s worth understanding these provisions even if you hope never to use them.

The indicators suggesting this path include working capital trending below 6 months of operating expenses, being 55+ without a committed next generation, or simply having no viable path to profitability at forecast milk prices.

The Asset Value Reality Nobody Discusses

What’s particularly concerning—and I don’t hear this discussed nearly enough at co-op meetings—is how quickly farm asset values deteriorate when a region’s dairy sector struggles.

Mark Stephenson at Wisconsin’s Center for Dairy Profitability has done extensive work on this. When dairy becomes structurally unprofitable in a region and multiple farms exit simultaneously, those anticipated liquidation values farmers count on for retirement… they simply evaporate.

Think about it. Land you believe is worth $9,000 per acre based on that sale down the road last year? When 8-12 dairy farms in your county hit the market simultaneously with no qualified buyers, you might see $6,000-6,500. I’ve watched it happen in several Wisconsin counties over the past three years, and it’s heartbreaking.

Equipment values face the same compression. That 2018 John Deere you figure is worth $75,000? When six similar tractors are at auction within 50 miles, you might get $48,000. And dairy-specific infrastructure—milking parlors, freestall barns—they become nearly worthless without other dairy farmers to buy them.

Based on Farm Financial Standards Council accounting principles, farms in declining dairy regions face combined monthly wealth destruction of $23,000- $ 55,000 from operating losses and asset depreciation. Your farm’s value isn’t static—it’s changing every month based on regional dynamics.

Time destroys wealth faster than you think. A 300-cow operation valued at $1.5M today becomes $322K in 12 months—78% wealth destruction. Strategic exit today preserves $1.16M (77.5%). Forced liquidation after covenant violations leaves you with $323K (21.5%). That’s a $839,700 difference for waiting one year.

What Co-ops Are Saying vs. Market Reality

Comparing cooperative messaging against actual market data reveals… well, let’s call it a disconnect.

When co-ops say “market conditions will stabilize by late 2026,” they’re technically correct—USDA projects Class III prices around $18-19/cwt. But here’s what they’re not emphasizing: that’s still below breakeven for operations under 1,000 cows while remaining profitable for 2,000+ cow operations. In other words, “stabilization” actually accelerates consolidation rather than providing relief.

This disconnect partly stems from structural conflicts within the cooperative model itself. Market analysts like Phil Plourd at Blimling and Associates have documented how co-ops need maximum milk volume to spread fixed processing costs. They have an incentive to keep members producing, even at a loss—it’s just the nature of the cooperative structure.

What really caught my attention was data from the National Milk Producers Federation showing that DFA lost over 500 member farms in 2023. They’re anticipating shrinking from current levels to around 5,100 farms by 2030. That’s roughly a 9-10% annual attrition rate among their membership. If co-ops are successfully supporting family farms, why are 280+ farms leaving each year?

Looking Ahead: The 2028 Dairy Landscape

Based on consolidation trends documented by Rabobank’s dairy research group and factoring in China’s sustained market pressure, here’s what I think we’re looking at:

Total U.S. dairy farms will likely decline from today’s roughly 31,000 to somewhere around 20,000-22,000 by 2028—that’s a 29-35% reduction. But the distribution shift is even more dramatic.

Operations with 2,000+ cows, currently about 800 farms producing 46% of U.S. milk, will probably expand to 1,200-1,400 farms producing 60-65%. Meanwhile, that middle tier—200-999 cow operations in commodity production—faces a 75-85% reduction. It’s stark, but that’s what the data suggests.

What’s emerging are essentially three viable farm types:

Industrial-scale operations (2,000-5,000+ cows) competing on efficiency

Lifestyle farms (<100 cows) subsidized by off-farm income

The middle? It’s disappearing. And that’s a huge change for our industry.

Your Action Plan: Practical Steps for Right Now

For farmers reading this in late 2025, your window for strategic decision-making is measured in months, not years. Here’s what I’d suggest doing immediately:

This week: Calculate your true working capital per cow. Take current assets minus current liabilities, divide by cow count. If you’re below $800 per cow, you need to act fast.

Schedule a frank conversation with your banker about exactly where you stand relative to loan covenants. Don’t wait for them to call you—be proactive about it.

Have an honest family discussion about the farm’s actual financial position. I know these conversations are tough, but they’re essential.

And listen, if stress is affecting your sleep, relationships, or wellbeing, please reach out for help. The National Suicide Prevention Lifeline at 988, Farm Aid at 1-800-FARM-AID, and Iowa Concern at 1-800-447-1985 all have counselors who understand what you’re going through. There’s no shame in needing support—we all do sometimes.

Within 30 days: Engage an independent agricultural consultant—not your co-op field rep—for an honest viability assessment. Yes, it’ll cost $2,000-5,000, but it could save you hundreds of thousands in the long run.

Meet with an agricultural attorney who understands Section 1232 provisions and strategic options. Get real liquidation values for your assets from agricultural appraisers, not optimistic book values.

Develop three scenarios with your family: scale up, premium pivot, or strategic exit. Run the numbers on each. Be honest about what’s realistic for your situation.

The Success Story: Learning from Those Who’ve Navigated Change

Let me share a story about a family I’ll call the Johnsons—they represent what I’m seeing across eastern Iowa and similar situations throughout the Midwest. Third-generation dairy farmers with 380 cows faced this exact decision in early 2024, when working capital started to dwindle.

After careful analysis with their consultant, they executed a strategic exit in May 2024, using Section 1232 provisions to preserve an additional $180,000 in capital gains taxes. Today? They’re debt-free. The husband works as a herd manager for a 2,500-cow operation nearby. They kept their house and 40 acres. Their adult daughter started veterinary school this fall.

But let me be honest about something—when he talked with me about it, he said it was the hardest year of his life. “Watching that auction… seeing our cows loaded on someone else’s trailer… I couldn’t watch. Had to walk away.” His voice caught a bit. “Four generations of Johnsons milked those cows. Four generations.”

The identity crisis is real. The sense of failure—even when you’re making the smart financial decision—it’s overwhelming. He told me he didn’t go to the coffee shop for three months because he couldn’t face the questions. Couldn’t face being “the Johnson who lost the farm,” even though he’d actually saved his family’s financial future.

“But you know what?” he continued, “Looking at our grandkids playing in the yard, knowing they’ll have college funds, knowing we can sleep at night without worrying about milk prices… we made the right call. Hardest thing I ever did. Also, the smartest.”

That’s the kind of brutal honesty we need right now. Strategic exit isn’t failure—it’s protecting what matters most. But that doesn’t make it easy.

Key Takeaways for Your Decision

What this all boils down to is understanding that we’re experiencing a structural transformation, not a typical cyclical downturn. China’s demographic shift and production surplus represent permanent changes to global dairy demand—at least for the foreseeable future.

The $3-5/cwt cost advantage that 2,000+ cow operations enjoy over 200-500 cow farms simply can’t be overcome through better management. It’s structural, and we need to accept that reality.

Every month of delay in stressed markets costs not just operating losses but also substantial asset-value deterioration—that hidden wealth destruction that nobody talks about at the coffee shop.

Three paths remain viable for most operations: scaling to 1,500+ cows if you have the resources, pivoting to premium markets with guaranteed contracts, or executing a strategic exit while preserving equity.

The window for making these decisions strategically rather than under duress is closing. Industry dynamics suggest farmers need to commit to their chosen path by the end of Q1 2026.

And please, remember this: with farmer suicide rates running 3.5 times the national average according to CDC data, no amount of farm equity is worth sacrificing your wellbeing or family relationships. Your family needs you more than they need the farm.

The dairy industry’s undergoing its most significant transformation in generations. Like that shift from hand milking to mechanical systems, this change will determine which farms exist in 2028 and which become memories. The farmers who acknowledge this reality and act decisively—whether scaling up, pivoting to premium, or strategically exiting—will be the ones sharing stories of resilience rather than regret.

The choice, and the timeline, are yours. But that window for making the choice? It’s closing faster than most of us realize. What matters now is making an informed decision while you still have options.

KEY TAKEAWAYS:

This is structural, not cyclical: China’s 42 million tonne surplus reflects permanent demand loss from a 48% birth rate collapse—recovery isn’t coming

Your management can’t fix physics: 300-cow dairies face an automatic $359,609 annual disadvantage versus 2,000-cow operations at any skill level

Three paths remain viable: Scale past 1,500 cows ($8-15M investment), pivot to premium markets with secured contracts, or execute strategic exit today at 70-85% equity (vs. 30-50% in forced liquidation)

Every month costs $23,000-55,000: Operating losses plus hidden asset depreciation are turning $1.5M farms into $700K distressed sales

Control your exit or it controls you: Make your decision by Q1 2026 while you have options—after that, loan covenants decide your fate

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

WARNING: Your 2026 dairy contract has unlimited liability clauses. 500-cow farms face $55K in new costs. Check these three things before signing →

EXECUTIVE SUMMARY: Dairy farmers signing 2026 contracts now are discovering unlimited liability clauses that hold them responsible for allergen incidents—even those that occur at the processor. These new terms, triggered by California’s July 2026 allergen law, could cost a typical 500-cow operation between $15,000 and $55,000 annually in testing, infrastructure, and insurance. That’s up to 44% of net profit gone. With December 31 deadlines approaching, farmers face three paths: scale up to 1,500+ cows for efficiency, pivot to premium markets with $5-10/cwt premiums, or exit strategically while preserving wealth. The harsh reality is that 500-cow commodity dairies are becoming economically obsolete—caught between mega-farms operating at $3/cwt lower costs and premium producers capturing higher margins. Your decision in the next 90 days isn’t just about a contract; it’s about whether your farm exists in 2030.

You know, I’ve been talking with a lot of dairy farmers lately—folks running anywhere from 300 to 800 head—and the same topic keeps coming up over coffee.

These new contracts are landing on kitchen tables across the country right now? They’re different.

And I don’t mean different like when they tweaked the somatic cell premiums a few years back. I mean, fundamentally different.

One Wisconsin producer I know pretty well—let’s call him Tom to keep things simple—he runs about 500 Holsteins outside Eau Claire. Last Tuesday, he opens his December 2025 contract renewal expecting the usual adjustments. Maybe a change in butterfat differential or a new hauling schedule.

Instead, he finds himself staring at 15 extra pages of allergen management requirements. Language about “unlimited liability.” Clauses saying he has to defend his processor against claims he didn’t even cause.

“The efficiency gains are real—our cost per hundredweight dropped by nearly three dollars. But this wasn’t just about surviving allergen costs. We saw where the industry was heading and decided to get ahead of it.” — A Wisconsin dairy producer who expanded from 600 to 1,800 cows last year

And here’s what’s interesting—Tom’s not alone. From the Texas Panhandle to Vermont’s Northeast Kingdom, down through the Georgia dairy belt and out to Idaho’s Magic Valley, producers are discovering their 2026 contracts contain terms nobody’s ever seen before.

Now, California’s allergen labeling law takes effect on July 1, 2026—that’s the official reason. But what I’ve found is that processors are using this regulatory change as the mechanism for something much bigger.

They’re fundamentally restructuring how risk flows through the dairy supply chain.

Let me walk you through what’s actually happening, because once you understand the pieces, the decisions you need to make become a lot clearer.

What Is California’s Allergen Law?

Starting July 1, 2026, California requires restaurant chains with 20+ locations nationwide to label major food allergens on menus. While this sounds limited to restaurants, processors are using it to justify comprehensive supply chain allergen controls—pushing liability and costs upstream to dairy farms through new contract requirements.

Why These Contract Changes Hit Different

I’ve been looking at dairy contracts for going on two decades now, and what’s landing on farm desks this quarter is genuinely unprecedented.

You probably saw the FDA’s recent data from their Reportable Food Registry—dairy products accounted for nearly 30% of all food recalls in the first quarter of 2025. That’s almost 400 recalls from our industry alone.

And when you dig into those numbers, undeclared allergens are driving a huge chunk of them, with milk proteins topping the list.

The Grocery Manufacturers Association conducted research in 2022 that showed food recalls average around $10 million in direct costs. And that’s just pulling product, investigating, notifying regulators.

Doesn’t even touch brand damage, lost sales, or legal fees. You’re looking at exposure that could bankrupt a mid-sized processor, which is why they’re scrambling to push that risk elsewhere.

What’s the target? Your farm.

What I’m hearing from agricultural attorneys who specialize in dairy contracts—and there aren’t that many of them, as you probably know—is that processors aren’t just updating compliance language.

They’re fundamentally restructuring who bears risk when something goes wrong. California’s July 1, 2026, deadline? It’s the perfect justification.

Here’s the really clever part, or concerning part, depending on where you sit. Most dairy contracts run calendar year, right? So farms need to sign their 2026 agreements right now, in Q4 2025.

By the time California’s law kicks in and everyone understands what these terms really mean, you’ll already be locked into a 12-month commitment.

Timing’s not an accident.

What Your Contract Might Look Like Now

Here’s what producers from Pennsylvania to Idaho to the Florida Panhandle—even down in Mississippi, where my cousin runs 400 head—are finding buried in their contracts:

Testing requirements where the processor decides frequency, but farmers pay 100% of costs—we’re talking $55 to $80 per sample for standard allergen tests, based on what companies like Neogen are charging these days.

Infrastructure modifications requiring capital investments of $50,000 to $250,000. Cornell Extension’s been helping farmers price this out, and those are real numbers.

Insurance minimums are jumping from your typical $2 million general liability to $5-10 million specifically for allergen incidents. I’ve talked to insurance agents we work with—Nationwide, American National, some of the bigger ag insurers—and they’re all saying premiums are up 30 to 50 percent for this coverage.

And then there’s the real kicker: unlimited indemnification clauses that make farmers liable for downstream incidents “regardless of origin.” Think about that. Even if contamination happens at the processor, you could be on the hook.

The Real Numbers for Your Operation

Let’s talk specifics for a typical 500-cow dairy producing around 10 million pounds annually—that describes a lot of operations in the Upper Midwest and down through Oklahoma and Arkansas.

I’ve been running these numbers with farm financial consultants, and here’s what the math looks like.

Compliance Level

Annual Testing

Infrastructure

Insurance Increase

Documentation/Training

Total New Costs

Profit Impact

Minimal(2¢/cwt)

$1,700

$5,000

$4,000

$2,500

$15,000

12%

Mid-Level(8¢/cwt)

$7,000

$10,000

$8,000

$9,500

$34,000

28%

High (15¢/cwt)

$13,000

$15,000

$12,000

$15,500

$55,000

44%

That’s a 12% hit to your bottom line if you’re running decent margins on the minimal path. Not great, but manageable for efficient operations.

Mid-level? That’s 28% of your profit gone. The difference between paying bills on time and stretching payables, as many of us know all too well.

At the high end? 44% of the net income was lost. For a lot of 500-cow operations, that’s the difference between viable and not.

The Cost Gap That’s Already There

What makes this particularly challenging is the existing cost structure gap. USDA’s Economic Research Service published their cost of production data in March 2024, and here’s the reality:

Farm Size

Average Cost per cwt

2,000+ cows

$17

100-500 cows

$20+

That’s more than a three-dollar disadvantage before you add a penny of allergen compliance costs.

Already Behind Before Allergen Costs: 500-cow dairies face $3.37/cwt higher costs than 1000-cow operations and $8.48/cwt higher than mega-dairies—BEFORE adding $0.02-0.15/cwt allergen compliance. On 10 million lbs annually, that’s $337,000-$848,000 structural disadvantage you can’t manage away

Understanding the Bigger Picture

Here’s where things get really interesting—and by interesting, I mean concerning if you’re a mid-sized dairy like most of us.

The consolidation trends were already stark before these contract changes. The 2022 Census of Agriculture, released in February 2024, shows that we lost 39% of U.S. dairy farms between 2017 and 2022.

Dropped from over 39,000 to about 24,000 operations. Yet—and here’s the kicker—milk production actually increased 5% over that same period according to the USDA’s National Agricultural Statistics Service.

Think about that for a minute. Fewer farms, more milk. The math only works one way, doesn’t it?

Today, according to the same Census, 65% of the U.S. dairy herd lives on farms with 1,000 or more cows. The 834 largest dairies—those with 2,500 or more head—they control 46% of production by value.

These aren’t future projections, folks. This is where we are right now.

I was talking with a senior ag lender recently—manages a portfolio north of $400 million in dairy loans—and he was remarkably candid about it.

“We’re not trying to prevent consolidation. We’re positioning our portfolio to be on the right side of it. Managing 50 medium-sized dairy loans requires far more oversight than five large ones with professional CFOs and management teams.” — Senior agricultural lender with $400M+ dairy portfolio

The September 2025 lending data from agricultural finance institutions shows that smaller ag lenders—those under $500 million in loans—they absorbed 75% of the increase in farm lending during 2024.

Meanwhile, the big players with over a billion in ag loans? They contributed just 10% to that increase.

The sophisticated lenders they’re already pulling back from medium-sized operations. Makes you think, doesn’t it?

The Numbers Don’t Lie: Since 2017, America lost 15,000 dairy farms (39%) while milk production INCREASED 5%. By 2030, another 7,000 operations will disappear. This isn’t a downturn—it’s systematic elimination of mid-size dairies. Where does YOUR farm fit?

Three Paths Forward (And Why You Need to Choose Now)

After talking with dozens of farmers facing these decisions and running scenarios with financial advisors, I’m seeing three viable strategies emerge.

The key is picking the right one for your specific situation—not what worked for your neighbor, not what your grandfather would’ve done.

Path 1: Scale Up to Survive

Who should consider this path? Well, if you’re under 45 with kids who genuinely want to farm—and I mean really want it, not just feel obligated—this might be your route.

You need a debt-to-equity ratio under 2.0, preferably lower. You should already be in the top 25% for efficiency, meaning your cost of production is under $19 per hundredweight.

You’ve got to have the land base or be able to acquire it. And honestly? You need to actually enjoy the business side of dairy, not just working with the cows.

What’s it take? University of Wisconsin Extension’s been helping folks price out expansions, and you’re looking at $3.5 to $5 million in capital investment.

That’s an 18 to 24-month timeline just for permits and construction. You’ll be managing employees, not just family labor. And you need the stomach for significant debt and risk.

The payoff? Production costs drop two to three dollars per hundredweight at scale—USDA data’s pretty clear on this—which more than covers new allergen compliance costs.

You become the type of operation processors want to work with long-term. But it’s a big leap, no doubt about it.

Path 2: Exit Commodity, Enter Premium

What’s encouraging is that producers from North Carolina to Kansas to New Mexico are finding similar success with premium markets.

This path works if you’re within 60 miles of a decent-sized population center—100,000 people or more. You or your spouse actually has to enjoy marketing and talking to customers. Can’t stress that enough.

You’ll be working farmers markets, doing farm tours, and managing social media. As you’ve probably experienced yourself, it’s exhausting but can be rewarding.

Your location needs affluent consumers who value local food. And you’ve got to handle the three-year organic transition financially—that’s no small feat.

What’s it take? Organic certification under the USDA’s National Organic Program is a 36-month process, as you probably know.

If you’re adding processing, budget $150,000 to $300,000 for a small facility—USDA Rural Development has some grant programs that can help with this.

Plan on 15 to 20 hours per week just on marketing. It’s a completely different mindset about what you’re selling.

The payoff? Premium markets can deliver five to ten dollars per hundredweight above commodity prices—USDA tracks these premiums pretty consistently.

“We realized we couldn’t compete with mega-dairies on cost. But we could compete on story, quality, and customer connection. Our milk price went from $21 to $28 per hundredweight, and our yogurt adds another eight to ten dollars per hundredweight equivalent.” — Vermont dairy family who transitioned to organic with on-farm processing

But more importantly, you’re building direct relationships that give you control over your price. You’re not just waiting for the monthly milk check to see what you got.

Path 3: Strategic Exit While You Can

This is the path nobody wants to talk about, but research on farm transitions suggests that strategic exits can preserve significantly more wealth than distressed sales.

Sometimes 25 to 40 percent more.

Who should consider this? If you’re over 55 without a successor who’s passionate about dairy—and I mean passionate, not just willing—this might be your reality.

If your debt-to-equity exceeds 2.5, if your cost of production is over $21 per hundredweight, if you’re emotionally exhausted from the volatility… well, it’s worth considering.

Especially if you have other interests or opportunities.

What’s it take? Good transition planning, starting 12 to 18 months out. Realistic asset valuations—don’t kid yourself about what things are worth.

Emotional readiness to close this chapter. And a clear plan for what comes next.

The payoff? Preserving capital while land values remain strong—and they won’t forever, we all know that.

Avoiding slow wealth erosion. Maybe transitioning to less-stressful agricultural enterprises, such as cash crops or custom work.

It’s not giving up; it’s making a strategic business decision.

The Supply Chain Dynamics You Need to Understand

To negotiate effectively, you need to understand what’s driving processor behavior. From their perspective, this isn’t about hurting family farms—it’s about survival in a world where one allergen incident can trigger catastrophic losses.

RaboResearch’s food industry analysis from this past summer suggests processors face an impossible situation. Their insurance companies are demanding comprehensive allergen controls.

Regulators are increasing scrutiny. Consumer lawsuits are proliferating. They’re pushing liability upstream because they genuinely don’t see another option.

What’s particularly telling is that processors actually prefer consolidation. Think about it from their shoes: Managing 200 large suppliers instead of 2,000 small ones.

Professional management teams they can work with. Sophisticated quality systems and documentation. Resources to implement new requirements properly. Lower transaction costs across the board.

This isn’t a conspiracy—it’s economics. And understanding these dynamics helps you negotiate more effectively because you know what processors actually value.

Worth noting, too, that some processors are working with their farmers through this transition. A couple of the smaller regional processors in Ohio and Pennsylvania have offered 40-60% cost-sharing arrangements with phased implementation schedules over 18 months.

They’re the exception, not the rule, but it shows there’s some recognition of the burden these changes create.

Regional Factors That Change Everything

Geography’s becoming destiny in dairy. What I’m seeing is a real divergence driven by water availability and the regulatory environment.

Water-secure regions—the Upper Midwest, Northeast, and parts of the Southeast, like northern Georgia—are seeing renewed interest from both expanding local operations and relocating Western dairies.

Dairy site selection consultants tell me they’ve never been busier. Every conversation starts with “Where can we find reliable water for the next 30 years?”

Water-stressed areas—the Southwest, parts of California—that’s a different story. University of Arizona research on aquifer depletion shows that some dairy-intensive areas are experiencing annual water-table drops of several feet. Water costs in these regions have doubled or tripled in the past decade.

That’s not sustainable, and everyone knows it. These operations face a double whammy—new allergen costs plus rising water expenses.

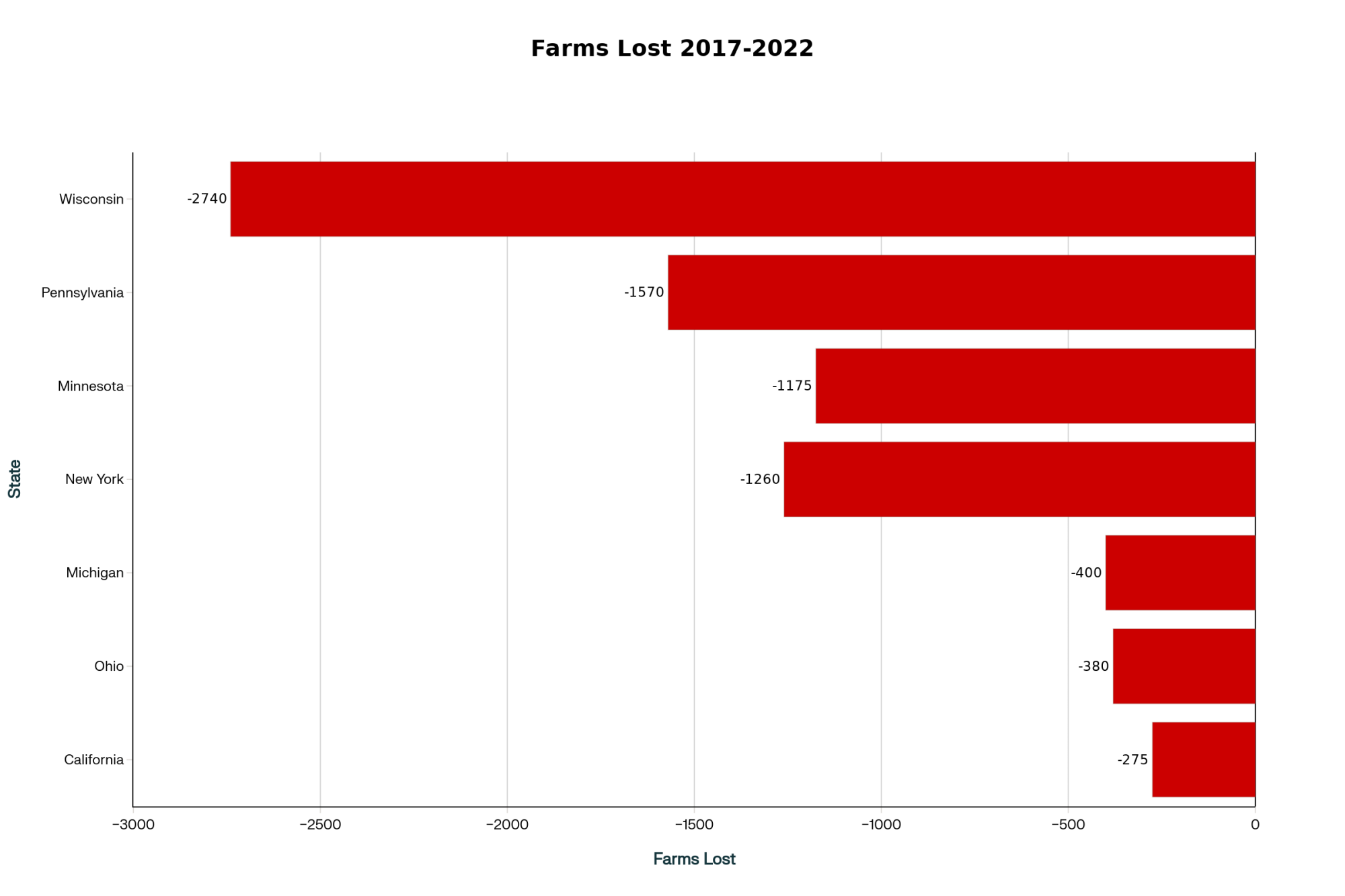

This Isn’t Happening Everywhere Equally: Wisconsin hemorrhaged 2,740 farms—more than the next three states combined. Pennsylvania, Minnesota, and New York each lost 1,000+ operations. Meanwhile, California (the largest dairy state) lost just 275. Geography matters, but the trend is universal

Negotiation Strategies That Actually Work

After watching dozens of these negotiations, here’s what’s actually effective:

Form an informal buying group. You don’t need a formal cooperative structure—just five to ten neighbors agreeing to push for the same contract terms. When six farms representing 3,000 cows approach a processor together, they listen differently than when you come alone.

Use professional help strategically. Yes, agricultural attorneys cost money. But spending $5,000 on contract review could save you $50,000 annually in bad terms. Frame it as the bad cop: “I’d love to sign this, but my attorney insists on liability caps…”

Offer trades, not just demands. “I’ll implement comprehensive testing protocols if you’ll split the costs 50/50 and cap my liability at one year’s gross revenue.” Processors respond better to negotiation than ultimatums.

Know your walkaway point. If you have alternative buyers—even if they’re 50 miles further—that knowledge changes how you negotiate. Do the math beforehand: What’s the worst deal you can accept and still stay viable?

Technology as a Survival Tool

The farms that are successfully adapting aren’t doing so through willpower alone. They’re leveraging technology to make compliance manageable.

What’s encouraging is that agricultural technology providers report dairy operations implementing digital documentation systems are seeing significant reductions in administrative burden.

Automated testing protocols are lowering sampling costs. Real-time environmental monitoring can prevent contamination incidents before they become recalls.

For example, farms using systems like DairyComp 305’s newer modules or Valley Ag Software’s compliance-tracking are finding the documentation requirements much more manageable than those trying to handle them with spreadsheets.

The upfront cost—usually $5,000 to $15,000 for implementation—pays for itself in reduced labor and avoided compliance violations. One Kansas operation told me they cut documentation time by 60% after implementing digital tracking, saving nearly $20,000 annually in labor costs alone.

Technology isn’t optional anymore. What is the difference between farms crushing under compliance costs and those managing them? Usually comes down to whether they’ve invested in the right systems.

What Dairy Looks Like in 2030

Based on everything I’m seeing, here’s my best projection for where we’re heading:

We’ll probably have 15,000 to 20,000 dairy farms by 2030, down from today’s 24,000. But—and this is important—they won’t all be mega-dairies.

I’m expecting maybe 12,000 to 15,000 large-scale commodity operations, another 3,000 to 5,000 premium or specialty farms serving local and niche markets, and 2,000 to 3,000 transitional operations finding unique market positions.

Agricultural economists analyzing dairy consolidation trends suggest we’re not witnessing the death of dairy farming. We’re seeing differentiation.

The 500-cow commodity model is becoming obsolete, yes. But opportunities are emerging for farms willing to adapt strategically.

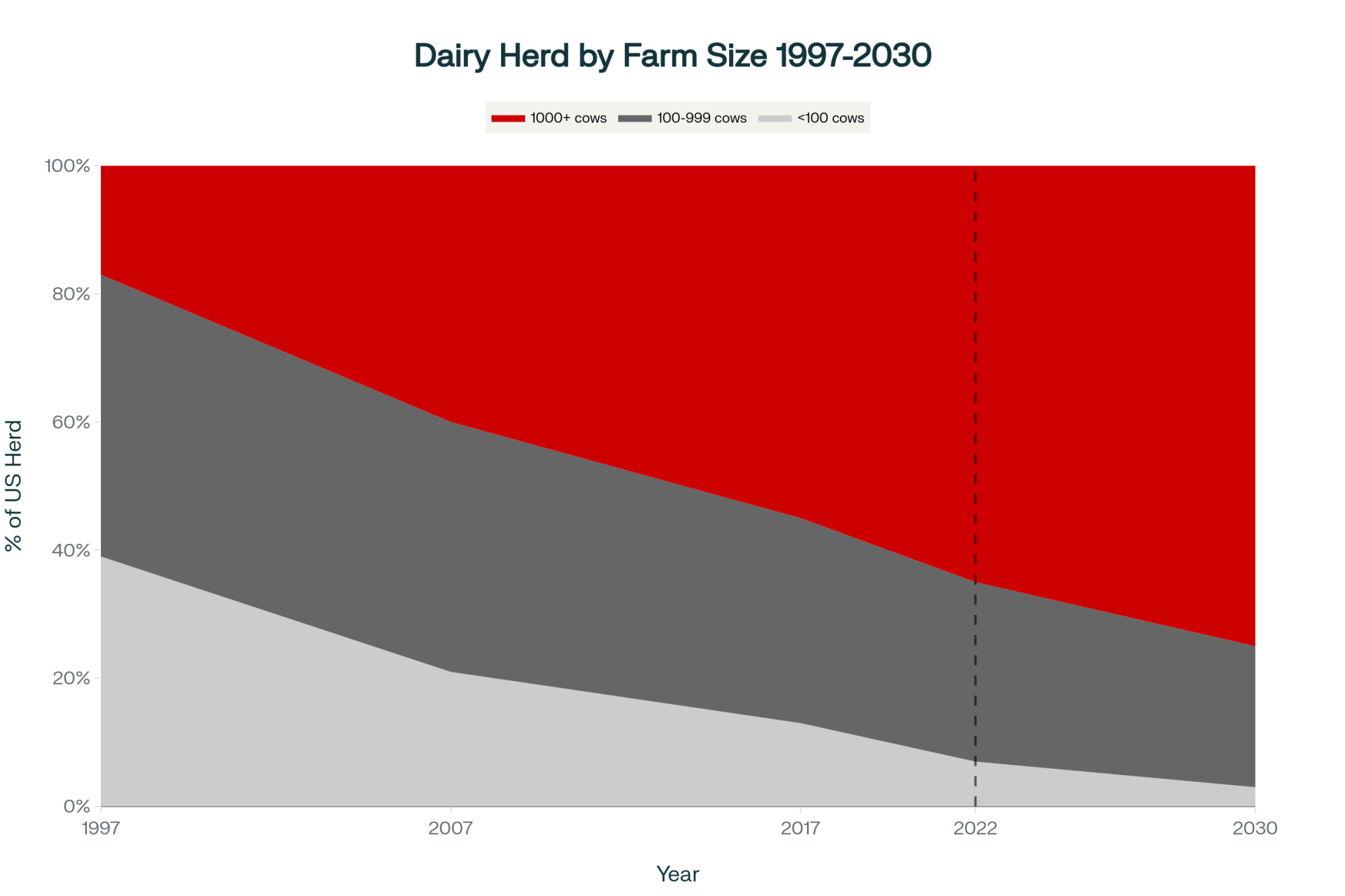

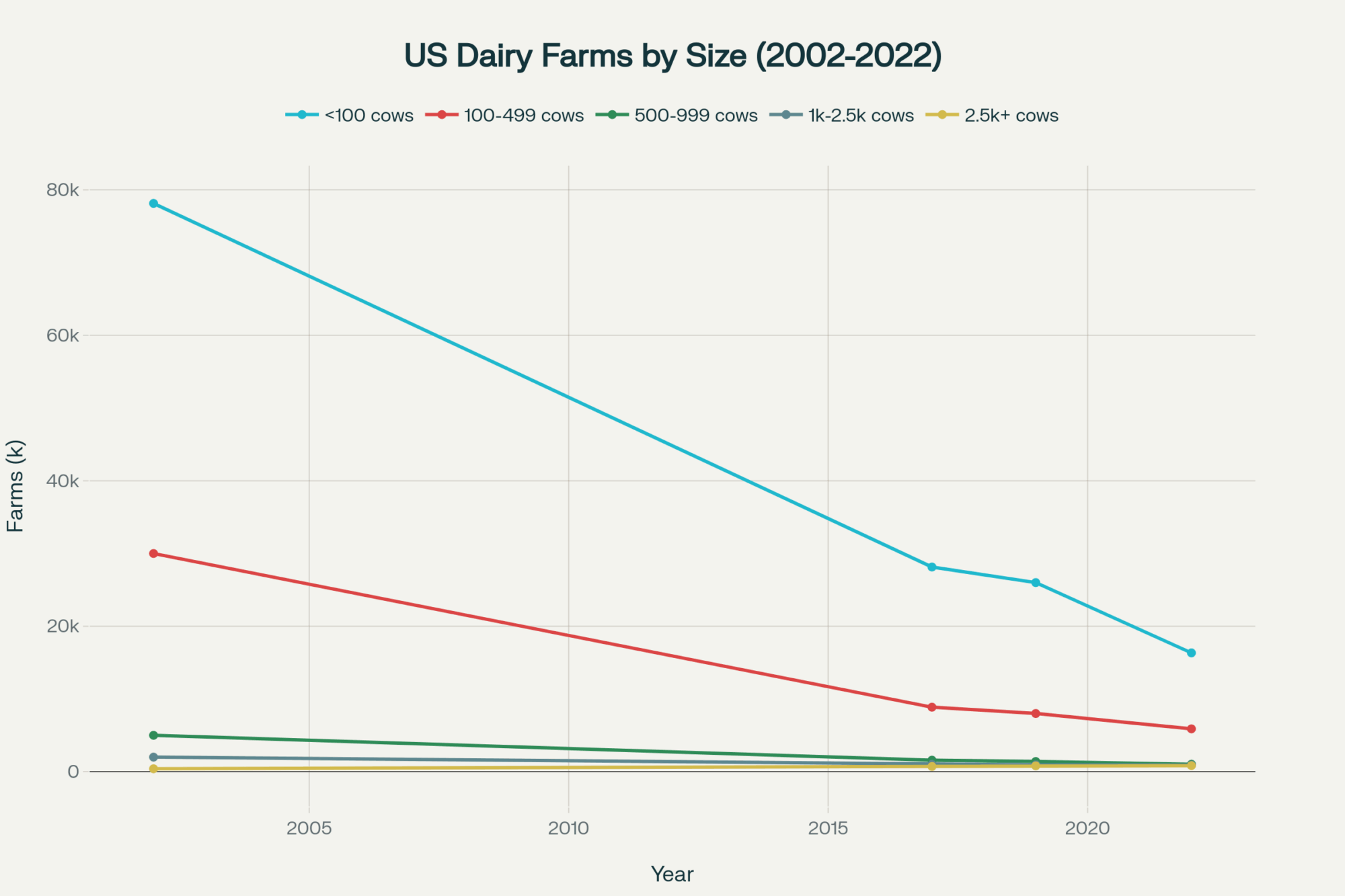

The 25-Year Transformation: In 1997, just 17% of dairy cows lived on 1,000+ cow farms. Today? 65%. By 2030? Projected 75%. Meanwhile, farms under 100 cows dropped from 39% to 7% and are heading toward extinction. This isn’t gradual change—it’s systematic restructuring

Making Your Decision: A Practical Framework

So what should you actually do? Here’s the framework I’m suggesting to farmers facing these contracts:

Your 30-Day Action Plan

Calculate your true cost of production—don’t guess, know it

Review your current contract for existing allergen language

Get insurance quotes for the new liability levels

Talk honestly with family about succession plans

Research premium market opportunities in your area

Key Decision Factors