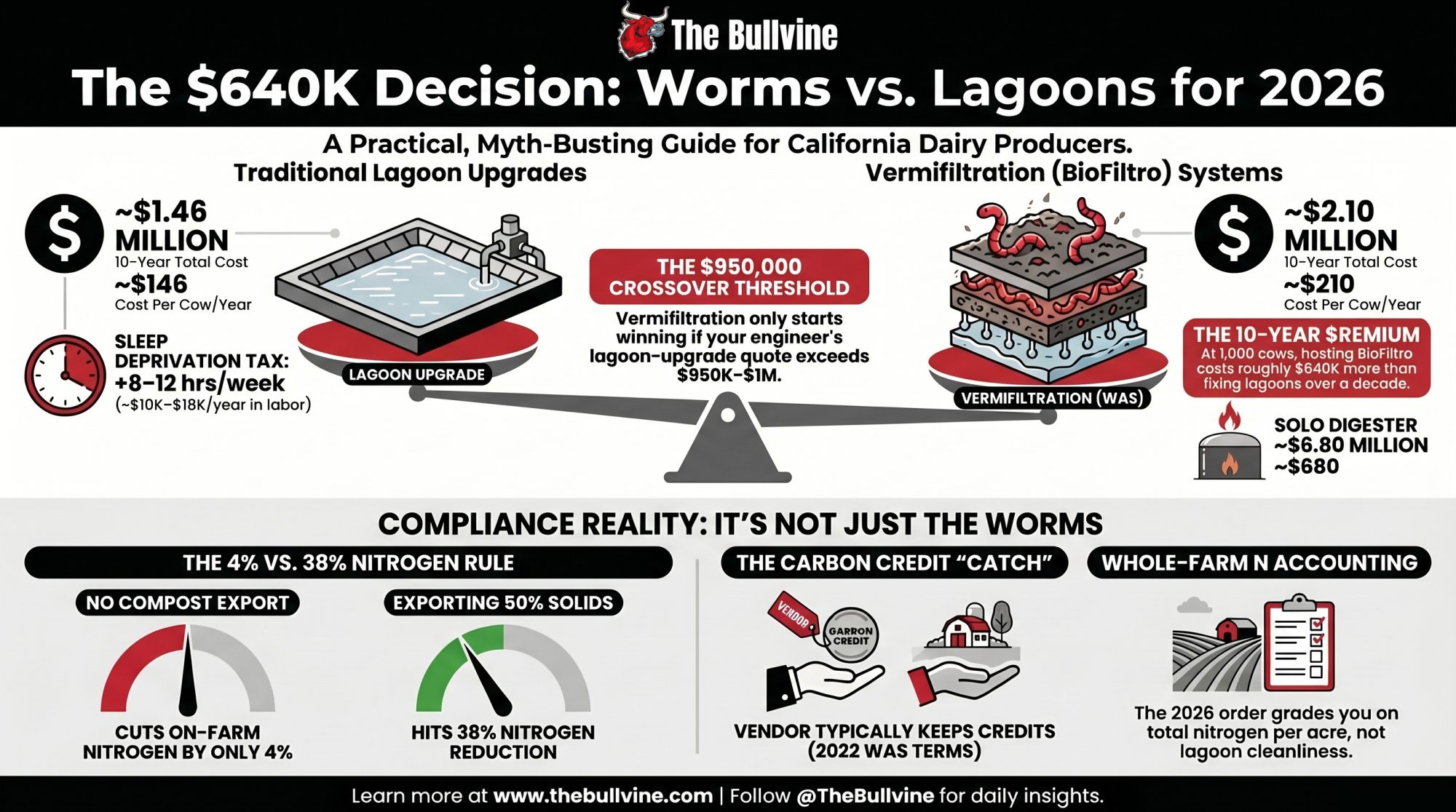

At 1,000 cows, the 10-year gap between fixing your lagoons and hosting BioFiltro runs near $640K. The term sheet says the vendor keeps the carbon. What does yours say?

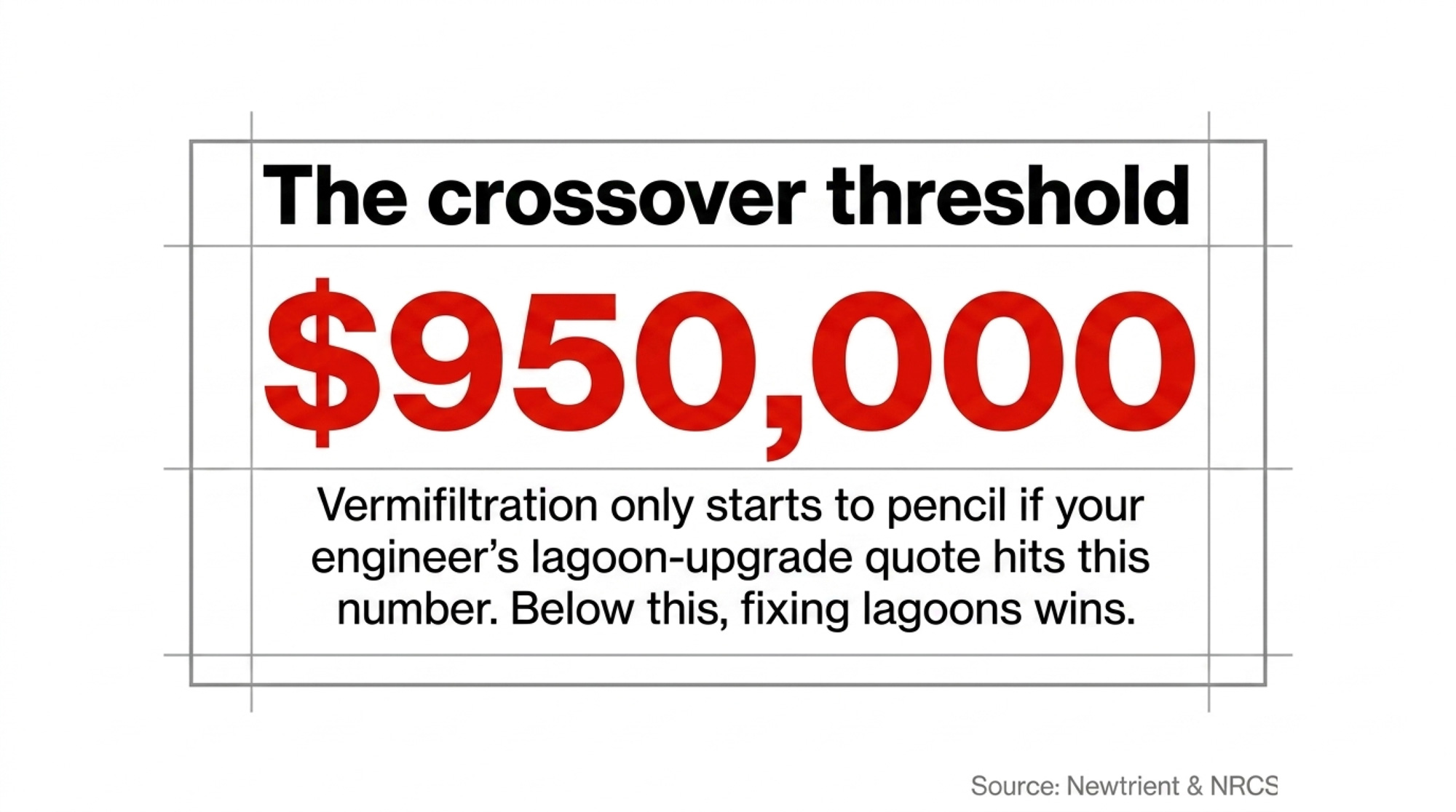

Executive Summary: The 10-year cost gap at 1,000 cows runs near $640K, and the crossover where vermifiltration starts to pencil is a lagoon-upgrade quote around $950K. Alberto Dairy near Hickman is hosting one of California’s largest vermi installs — six beds on roughly eight acres, handling up to 1.7 million gallons of manure water a day. Here’s the catch most pitches don’t lead with: BioFiltro’s publicly filed 2022 investor summary describes the vendor and its equity partners as holding the climate attributes on WAS systems, so the farm avoids the capex and the vendor captures the carbon economics. The 2026 Central Valley nitrogen order will grade you on whole-farm N balance, not lagoon cleanliness — which means without a signed compost-export contract, vermifiltration cuts your on-farm N loading by just ~4%; with 50% of solids moving off-farm, it drops ~38%. Add 8–12 operator hours a week and a Sleep Deprivation Tax of roughly $10–18K/yr, and the realistic vermi-vs-lagoon gap at 1,000 cows climbs closer to $780K over a decade. For 800–1,200 cow operators: fix the lagoons, run the worm deal, go solo-digester, or right-size — but decide against your engineer’s written quote and your term sheet, not the vendor’s model.

That 0K gap is the defining number in California dairy manure management 2026. It’s the premium an operator pays to hand lagoon capex risk to a vendor and buy regulatory peace on the way into the new Central Valley nitrogen order. Alberto Dairy near Hickman in Stanislaus County, a third-generation family operation reported as founded in 1981 in Dairy Herd Management’s 2024 California coverage, is hosting the BioFiltro install: six vermifiltration beds on roughly eight acres, handling up to 1.7 million gallons of manure water per day. BioFiltro has described the installation as among California’s largest dairy vermifiltration systems.

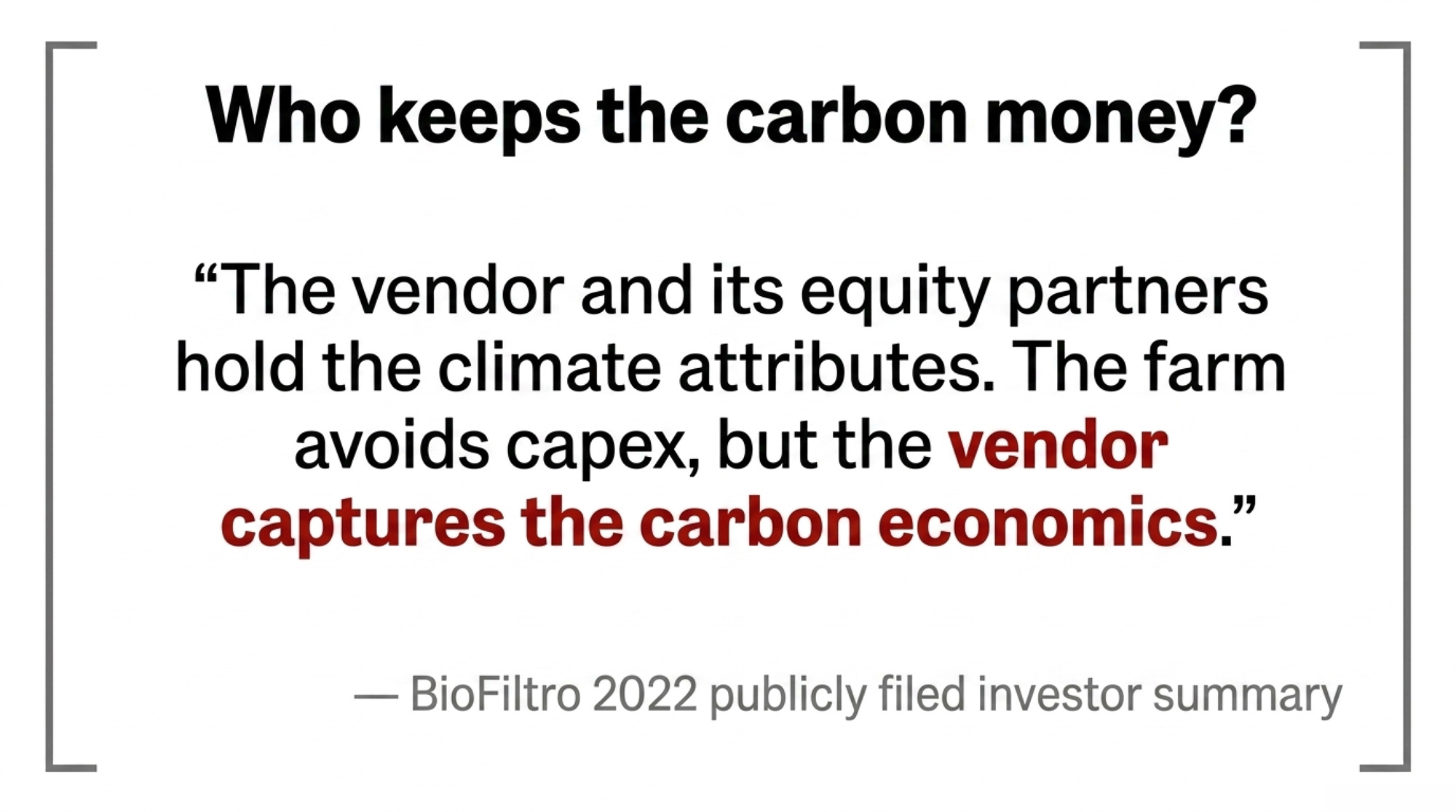

Here’s the structural question most readers miss. BioFiltro’s publicly filed 2022 investor summary describes the vendor and its equity partners as holders of the climate attributes on its “Wastewater as a Service” systems. Under that described structure, dairies pay a service fee and receive treated effluent; farms hosting WAS systems wouldn’t directly receive the associated carbon or water credits unless individual contracts provide otherwise. The Bullvine requested confirmation from BioFiltro on whether the 2022 structure remains current in 2026 WAS contracts. As of publication, no response had been received, and current contract terms aren’t independently verified.

Bullvine editorial analysis: That’s not a scandal. It’s a term sheet.

Stress-test that term sheet against your own lagoon exposure before the 2026 Central Valley nitrogen order takes effect. Alberto’s confirmed cow count, exact WAS fee, grant stack, and contract term aren’t public. The model below uses 1,000 cows because it roughly matches the reported scale — and because it’s the size band where the decision actually matters.

Why Did California Dairy Manure Management 2026 Just Get More Expensive?

The State Water Board’s October 2024 directive told the Central Valley Regional Board to align its dairy orders with the 10 mg/L drinking water nitrate standard and move dairies toward whole-farm nitrogen accounting. Central Valley Regional Board staff analysis attributes roughly 94% of nitrogen reaching affected aquifers to land application of manure, not lagoon leakage.

Read that twice. The order won’t grade you primarily on how clean your ponds are. It’ll grade you on pounds of nitrogen per acre, sustained across a ten-year whole-farm balance.

Stanislaus County sits in the Modesto Subbasin — a medium-priority SGMA basin under DWR’s 2024 prioritization, with a groundwater sustainability plan already adopted. Stack that on California’s 40% dairy and livestock methane reduction target under SB 1383, the AMMP and Dairy Plus grant cycles, and Nestlé’s dairy sustainability program. “Do nothing” stopped being an option a couple of years ago. The question is which path costs the least — and who captures any upside along the way.

A Central Valley ag lender, asked informally what’s driving 2025–2026 capex conversations with mid-size dairy clients, put it plainly to The Bullvine: lagoon reline quotes have gotten uglier, not prettier, and the quote is now the conversation starter. The per-client range isn’t for publication. The direction of travel isn’t in dispute. Readers with a better number from their own engineer are invited to send it in for the “Lagoon Inflation” tracker described at the end of this piece.

What the Worm System Actually Does (and Doesn’t)

Vermifiltration routes liquid manure across beds of wood chips and red wiggler worms. Worms and the associated microbial community break down organic load, strip nitrogen from the liquid stream, and immobilize nutrients in the bed media. Per Dairy Herd Management’s 2024 reporting and BioFiltro’s public site documentation, the Alberto system runs six beds on roughly eight acres with approximately four-hour retention. Treated water cycles back to barn flush and parlor cleaning. Bed media is eventually harvested as vermicompost.

The California Dairy Research Foundation cites 40–80% nitrogen removal from the liquid fraction in dairy vermifiltration systems, depending on design and operating conditions. LPELC and Washington State University extension research confirm the range at the concentration level. BioFiltro has reported 97–98% methane reduction compared with conventional lagoon storage, based on pilot data from Fanelli Dairy in Tulare County.

Those are real, repeatable numbers in the liquid stream. What they don’t change is total nitrogen excretion from the herd. And they don’t change the whole-farm accounting the 2026 order will apply.

Running the Numbers: Three Lanes for a 1,000-Cow Central Valley Dairy

Inputs: 1,000 milking cows, 600 acres for manure application (~1.67 cows/acre, typical for a mid-size Central Valley dairy), 10-year horizon, 7% cost of capital (capital recovery factor ≈ 0.1424). Benchmarks drawn from Newtrient and NRCS capex ranges, UCCE dairy lagoon cost studies, BioFiltro’s publicly reported Fanelli WAS figure, and standard Central Valley operating data. Scope: California Central Valley, 2026–2035 planning window. Illustrative — not an accounting of any specific operation’s books.

Crossover Threshold (Read This First)

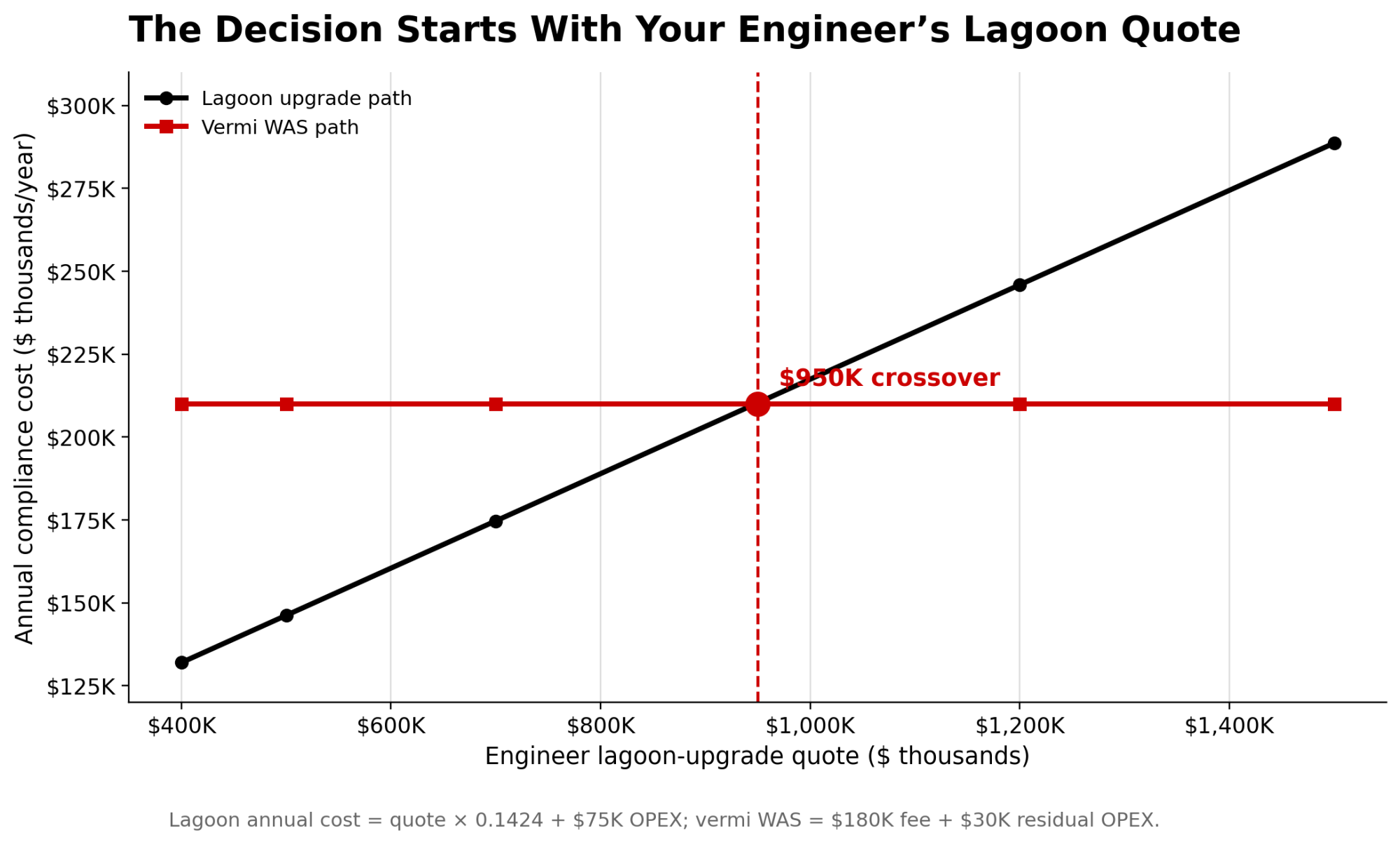

At 1,000 cows with the modeled inputs, vermifiltration under WAS starts penciling when your engineer’s lagoon-upgrade capex quote hits roughly $950,000–$1.0M. Below that, fixing lagoons is less expensive. Above it, vermi starts winning — before grant stack, carbon carve-outs, or labor adjustments.

That one number is the most actionable data point in this article. If your engineer’s memo lands below $950K, Lane 2 probably isn’t your path, regardless of how the pitch reads.

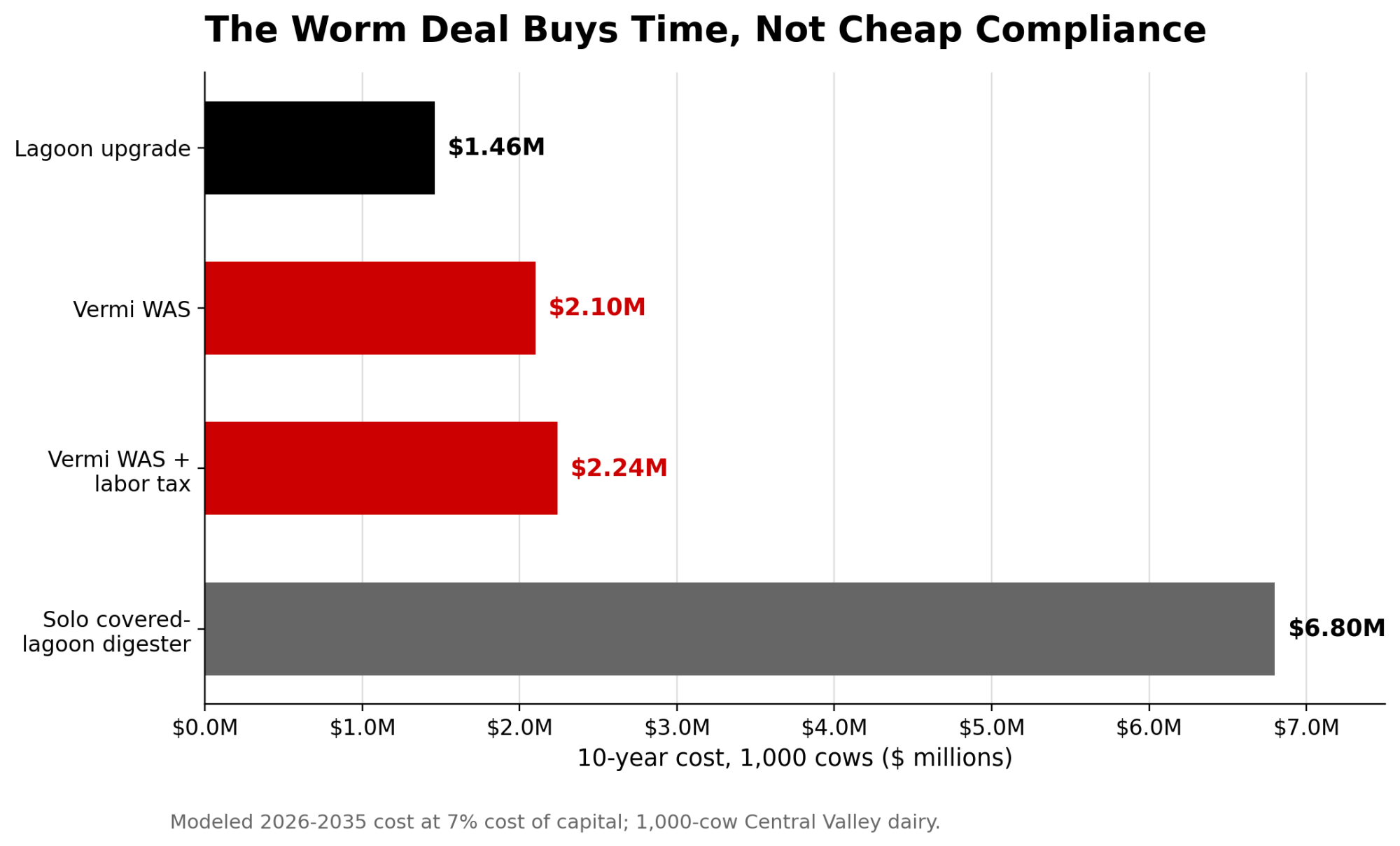

Lane 1 — Lagoon Upgrade Path

| Input | Value |

| Capex (mid-range reline/expansion, Newtrient/NRCS benchmarks) | ~$500,000 |

| Annualized at 7% over 10 yrs (× 0.1424) | ~$71,200/yr |

| Lagoon OPEX (UCCE benchmark, inclusive of baseline labor) | ~$75/cow/yr × 1,000 = $75,000/yr |

| Total annual cost | ~$146,200/yr |

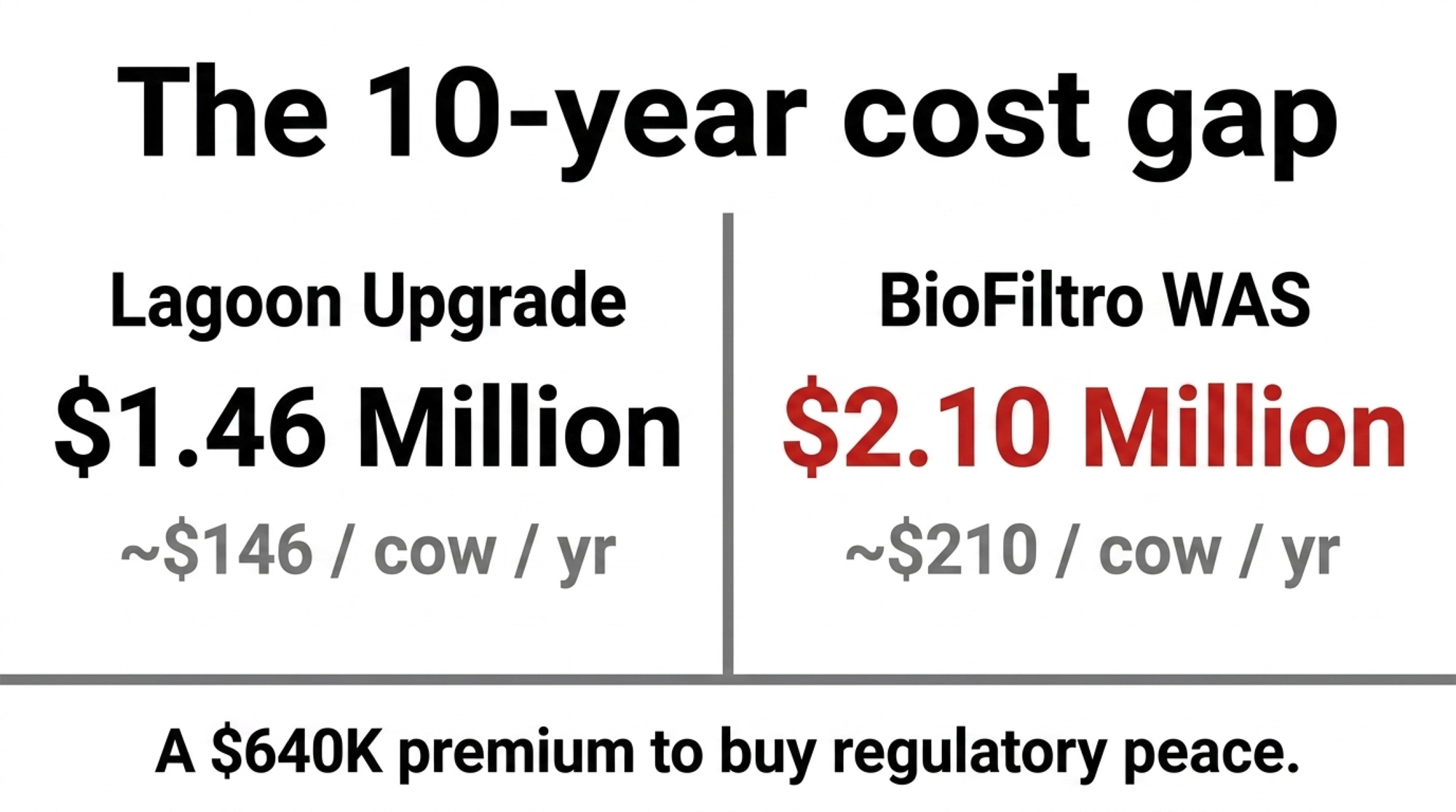

| 10-year total | ~$1.46 million (~$146/cow/yr) |

Lane 2 — Vermifiltration Under BioFiltro WAS

| Input | Value |

| WAS service fee (Fanelli benchmark near $162/cow/yr per vendor disclosure; modeled at $180/cow/yr for conservatism) | $180,000/yr |

| Residual lagoon OPEX | $30/cow/yr × 1,000 = $30,000/yr |

| Total annual cost | $210,000/yr |

| 10-year total | $2.10 million ($210/cow/yr) |

Lane 3 — Solo Covered-Lagoon Digester

| Input | Value |

| Post-grant capex (1,000-cow solo project, directional; CDFA DDRDP and Newtrient benchmarks — solo capex varies widely by site and grant stack) | ~$4,000,000 |

| Annualized at 7% over 10 yrs | ~$569,600/yr |

| Added OPEX (digester + residual lagoon) | ~$110/cow/yr × 1,000 = $110,000/yr |

| Total annual cost | ~$679,600/yr |

| 10-year total | ~$6.80 million (~$680/cow/yr) |

The Lane 2 vs Lane 1 gap at these inputs: ~$638,000 over 10 years — the “~$640K” in the headline.

One labor-symmetry note: the $75/cow/yr Lane 1 OPEX benchmark already rolls in baseline conventional lagoon management labor. The 8–12 additional operator hours per week associated with vermifiltration are incremental to that baseline, not a replacement for it.

Plug Your Operation In (Phone-in-the-Barn Version)

Define your variables: C = your milking cow count F = your vendor’s WAS fee, in $/cow/year (ask for it in writing) R= residual lagoon OPEX, modeled at $30/cow/year L = your current lagoon OPEX, modeled at $75/cow/year K = your engineer’s lagoon-upgrade capex quote, in whole dollars A = 0.1424 (annualization factor: 7% cost of capital, 10-year horizon)

Your annual vermi cost = (C × F) + (C × R) Your annual lagoon cost = (K × A) + (C × L)

Worked at C=500, F=$180, R=$30, L=$75, K=$300,000: Lane 2 = (500 × $180) + (500 × $30) = $90K + $15K = $105K/yr (~$1.05M over 10 years) Lane 1 = ($300,000 × 0.1424) + (500 × $75) = $42.7K + $37.5K = $80.2K/yr(~$802K over 10 years) Lane 2 premium at 500 cows: ~$24.8K/yr × 10 = ~$248K over a decade.

If your vendor’s WAS quote (F) lands materially above or below $180/cow/year, Lane 2 narrows or widens accordingly. Get that number in writing before you model anything.

What the Alberto Dairy Case Actually Shows Mid-Size Operators

Dairy Herd Management’s 2024 reporting places Alberto Dairy in its third generation, founded in 1981. Per Ag Alert’s California coverage, the operation is among the California sites BioFiltro features when presenting the WAS model to prospective dairy operators. The system is installed and operating under the WAS structure. The 2026 Central Valley order will apply regardless of when the installation decision was made.

The harder question for any third-generation California family dairy isn’t whether vermifiltration works technically. Published data show it does. It’s whether entering a long-term service contract for vendor-owned treatment infrastructure is the right structural choice for an independent family operation, given current credit-ownership terms and the coming regulatory framework.

As an industry pattern for dairies in this size band, WAS installations can function as a defensive capital decision — hedging a large near-term lagoon capex against a long-term service fee. The Bullvine isn’t characterizing the specific financial reasoning at Alberto Dairy, which isn’t public. Whether that’s the calculus at any given farm is a question only the operator can answer.

For readers weighing the same decision right now, the operator’s question isn’t “is this the future of dairy?” It’s “which lane does my actual operation survive?” That’s the lens this piece is written in.

The Nitrogen Trap Most Sustainability Stories Don’t Tell

The common assumption was that 40–80% nitrogen removal in treated effluent would translate directly into smaller regulatory exposure under the 2026 order. It mostly doesn’t — because the order is built around whole-farm nitrogen balance, not lagoon concentration readings.

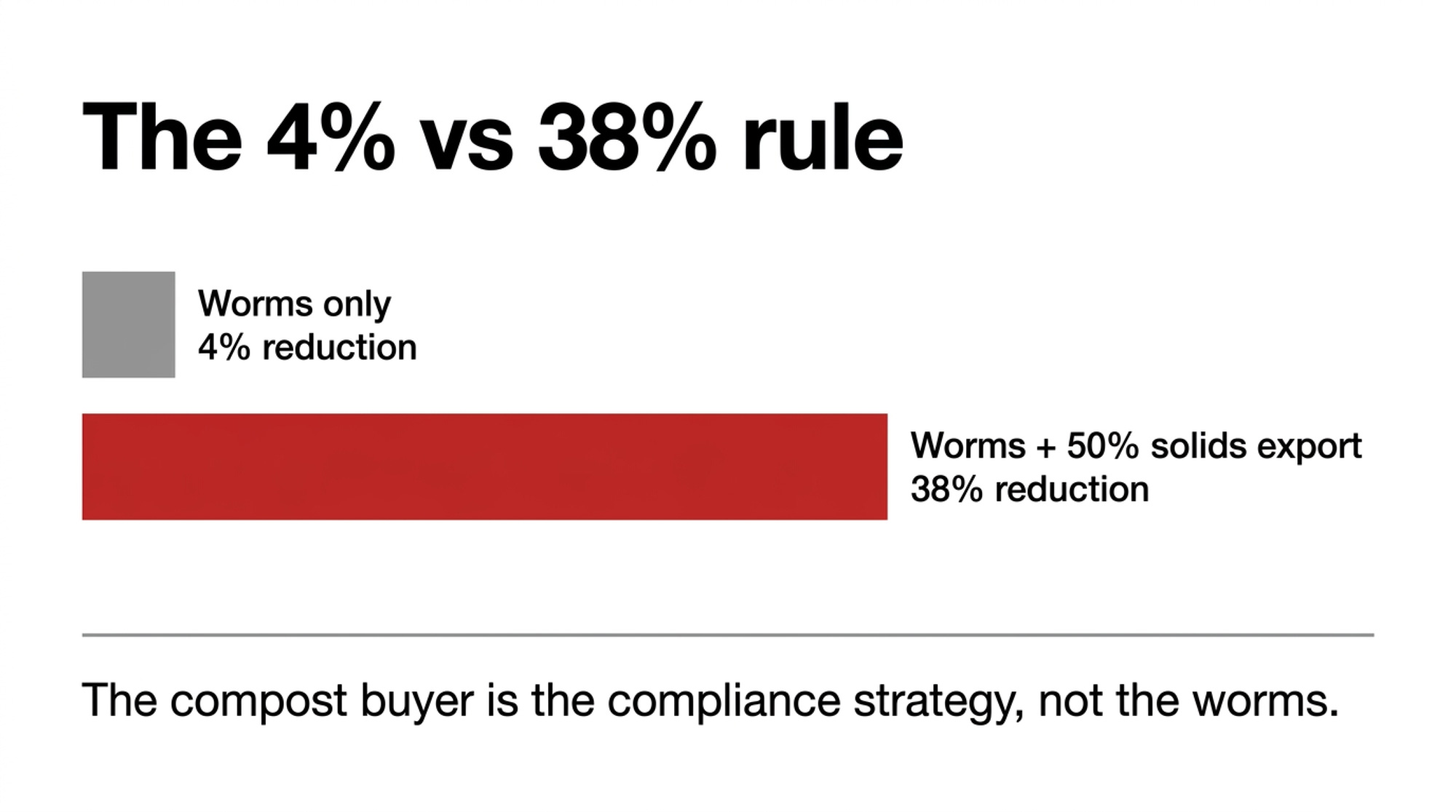

🔑 Key Takeaway — The 4% vs. 38% Rule

Without a compost export contract, vermifiltration cuts your whole-farm nitrogen loading by just ~4%. With 50% of solids moving off-farm, loading drops ~38%.

To survive the 2026 order, vermi without an export contract is a capital expense without a compliance outcome. The compost buyer is the compliance strategy — not the worms.

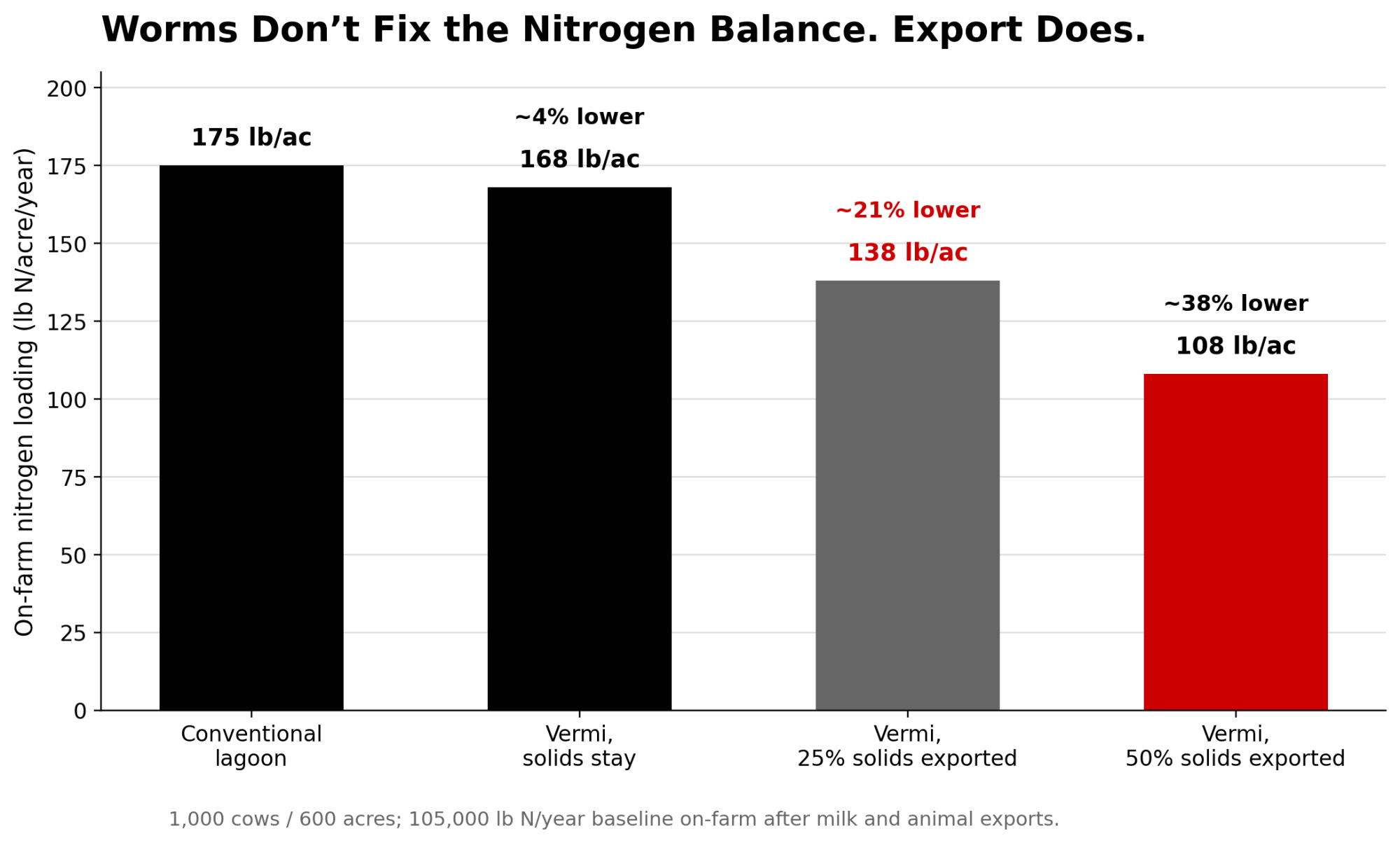

A 1,000-cow Central Valley dairy excretes roughly 140,000 lb N/year at the 140 lb N/cow benchmark from UC Davis nutrient-balance work. Milk and animal exports carry off around 25%, the midpoint of the 20–30% band in published California herd studies, leaving ~105,000 lb N on the farm to manage. On 600 acres, three scenarios.

Nitrogen per acre, three management approaches (1,000 cows / 600 acres, illustrative)

| Scenario | Total N on farm (lb/yr) | Per-acre N (lb/acre/yr) |

| Conventional lagoon, all N applied on-farm | 105,000 | 175 |

| Vermifiltration WAS, all solids applied on-farm | 100,590 | 168 |

| Vermifiltration WAS, 50% of solids exported off-farm | 64,995 | 108 |

Assumptions: 70/30 liquid/solids split under conventional; 60% N removal from liquid (mid-range of the published 40–80% band) under vermi; 90% of removed N immobilized in bed media, 10% lost via gaseous pathways; half the vermi solids exported represents ~900 dry tons/year ≈ 1,800 as-is tons at 50% moisture, at 2% N dry basis.

One honest caveat on that 10% gaseous loss line. Volatilization is a double-edged sword: it reduces N on the balance sheet, but ammonia and nitrous oxide are increasingly tracked under California air-quality mandates and under SB 1383. Treat gaseous loss as a temporary regulatory loophole — one that closes the moment air-side accounting catches up with water-side accounting.

Compost-buyer relationships at the 900 dry tons/year scale aren’t a given for individual dairies at this size. This step, not the worms themselves, is where the model earns its premium or doesn’t.

Moving that volume off-farm isn’t a passive win. It’s a logistics program — reliable buyer, consistent hauling, pricing that doesn’t turn a nitrogen strategy into a cost center. Using regional rates consistent with CalRecycle and UCCE compost pricing work (sale near $15/ton, trucking near $10/ton), best-case compost revenue on 1,800 as-is tons lands near +$9,000/year net after haul. For conservatism, the Lane 2 model above holds that revenue out; netted in, Lane 2 would move to ~$201K/yr and ~$2.01M over a decade. The value isn’t the check. It’s the acres you don’t rent and the cows you don’t cull to stay under the N cap.

Who Actually Gets the Carbon Money on California Dairy Projects?

| Project / funding lane | Credit or funding pathway | Realistic value signal | Who likely captures upside | Farm-level question before signing |

| Vermifiltration WAS | Voluntary carbon / climate attributes | Lower than LCFS; contract-dependent | Vendor/equity partners under described 2022 WAS structure | Does the current term sheet assign climate attributes to the farm or vendor? |

| Covered-lagoon digester | LCFS / RNG economics | $91–$548/cow/year gross range in published project economics | Split varies by operator/developer contract | What is the farm’s written gross and net revenue share? |

| AMMP / Dairy Plus support | California grant stack | Can reduce upfront project burden materially | Farm benefit depends on grant pass-through and fee structure | Does the grant lower the service fee, or only improve vendor economics? |

| Compost export | Vermicompost sales and N-balance relief | About +$9K/year net in modeled best case | Farm, if buyer/haul terms are real | Is there a signed buyer for 800–1,000 dry tons/year, not just a handshake? |

In the pitch deck, the California climate premium flows back to dairies. For covered-lagoon digesters participating in the Low Carbon Fuel Standard, there is real revenue — published analyses of California dairy consolidation and LCFS economics covering the 2020–2024 window place LCFS value in the range of $91–$548 per cow per year gross on qualifying projects, with material variance driven by LCFS credit price and project vintage.

Revenue-share arrangements between dairies and third-party digester operators vary widely. Published contract analyses have reported farm share sometimes running a minority of gross. Individual contracts vary. Request your split in writing before assuming a number.

Vermifiltration sits in the voluntary carbon market, which has historically paid less per ton than LCFS. BioFiltro’s publicly filed 2022 investor summary states that the vendor and its equity partners hold the climate attributes generated under its WAS structure. Unless individual contracts provide otherwise, farms hosting WAS systems under that described structure wouldn’t directly receive carbon credit revenue.

AMMP, Dairy Plus, CPG climate funding, and the vendor’s own credit revenue are the three pillars the pitch stands on. The farm avoids capex and gains regulatory cover. The vendor captures the climate economics over the life of the contract.

Bullvine editorial analysis: That arrangement can be rational. Operators entering WAS agreements expecting direct carbon revenue should request the current credit-ownership clause in writing before assuming otherwise.

Can Your Family Actually Run a Small Wastewater Plant?

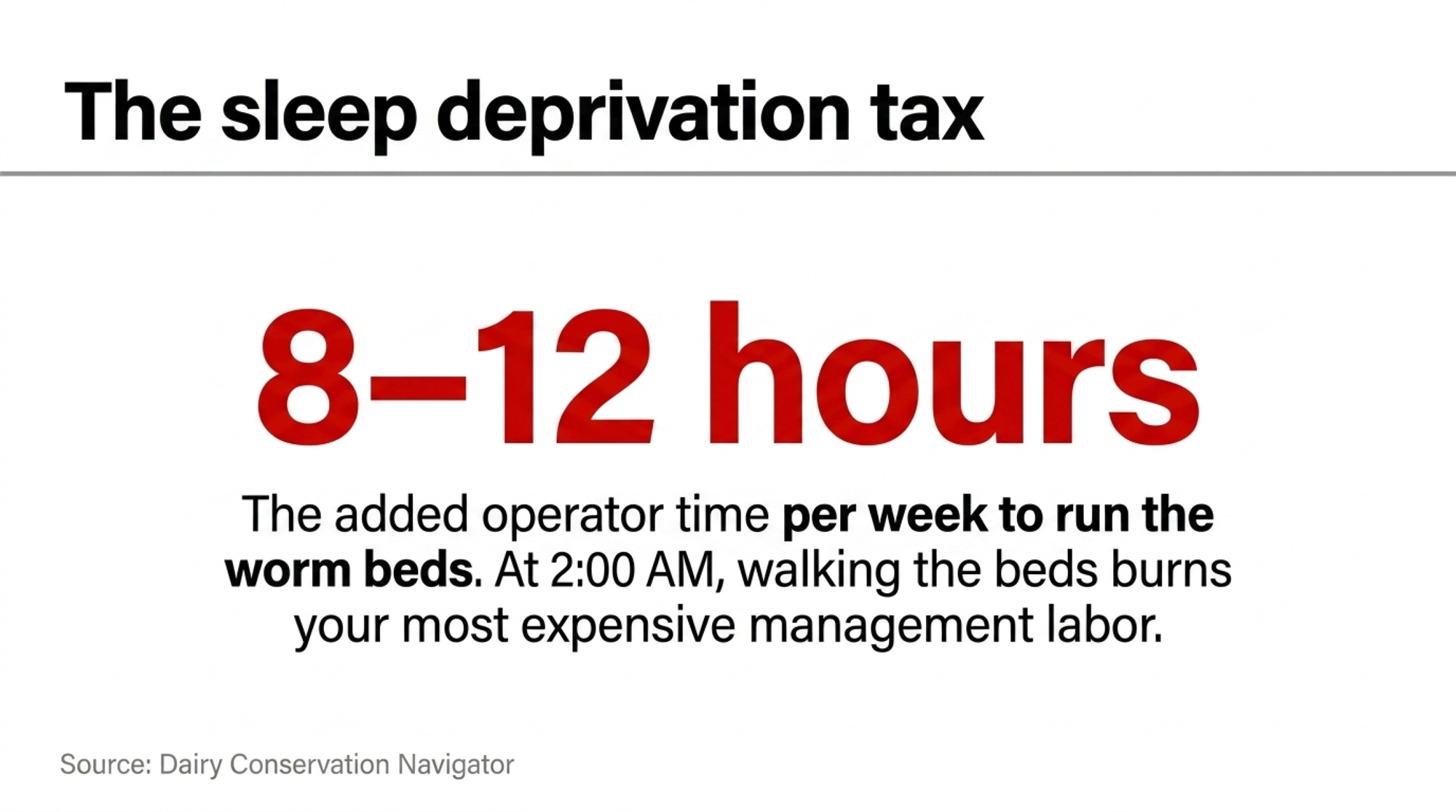

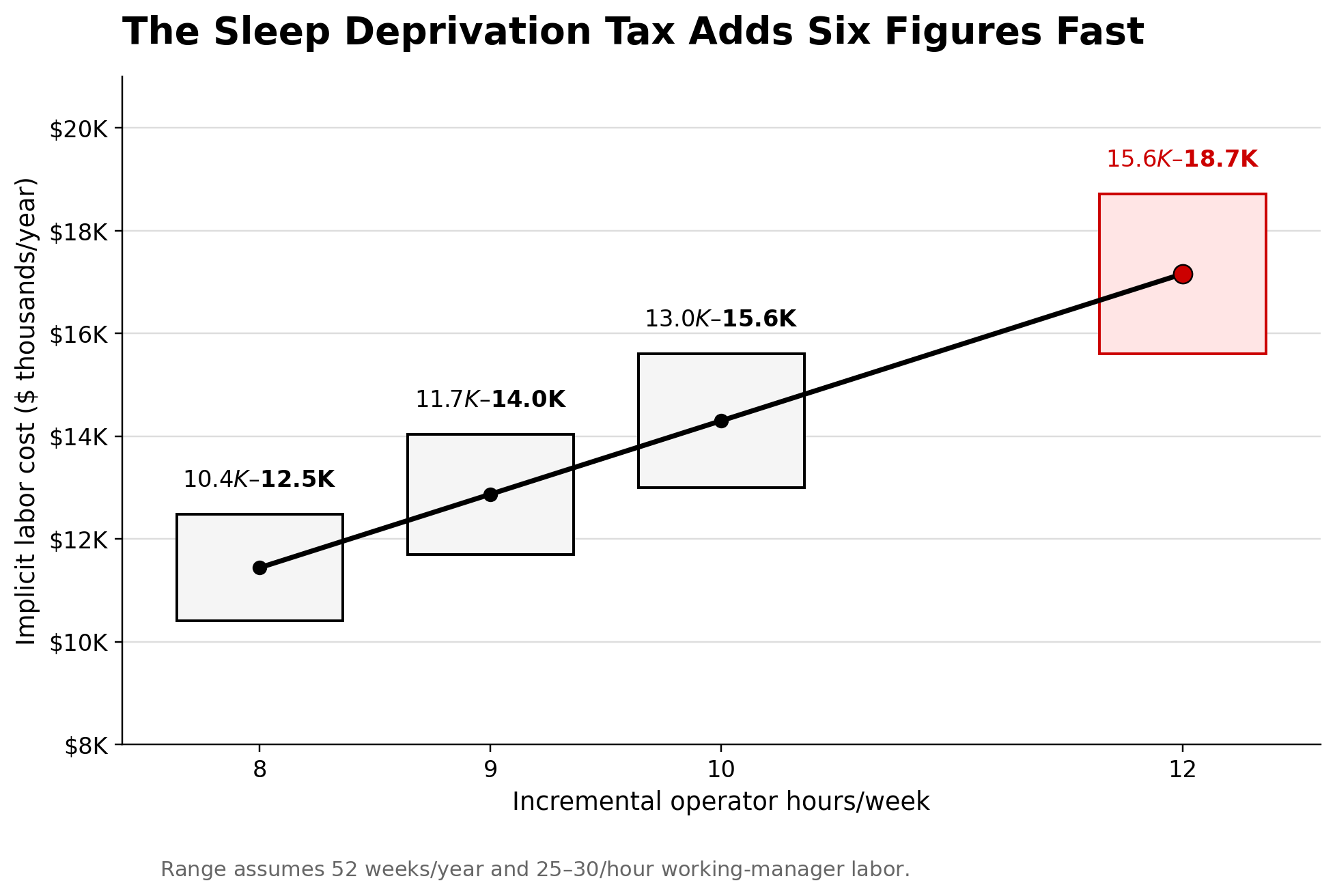

Dairy Conservation Navigator is direct: vermifiltration requires trained operators, daily and weekly inspections, and media replacement every 18–24 months. For an 8-acre system at the scale of the Alberto install, realistic routine labor runs roughly 8–12 additional operator hours per week above conventional lagoon management — about 416–624 additional hours per year. Priced at working-manager rates around $25–$30/hr, that’s roughly $10,000–$18,000/yearin implicit labor cost, or $100,000–$180,000 over the decade. Add the midpoint (~$14K/yr) to Lane 2 and the vermi-vs-lagoon gap for a 1,000-cow modeled operation moves toward ~$780K over ten years.

Call that line what it actually is: the Sleep Deprivation Tax. For operations that rely on owner-operator labor to backfill when a relief manager calls in sick, walking the worm beds at 2:00 AM burns the most expensive labor on the farm at roughly /hr — while the cows and the parlor crew still need that same owner sharp at 4:00 AM. Those hours come out of the one manager already watching pregnancy rates, feed shrink, and parlor labor. If that attention slips, the indirect hit to production can exceed the explicit labor line several times over. Decide which person absorbs those hours before you sign a long-term contract.

Royal Dairy in Washington has been publicly associated with BioFiltro for years through trade press and vendor case-study material. Fanelli has published pilot case-study data. Both are specific operations with specific management bandwidth — not proof the model travels automatically.

Does California Vermifiltration Pencil? Four Honest Lanes

For an 800–1,200 cow Central Valley operator facing the 2026 order, four paths. Each with when it makes sense and where it breaks down.

| Lane | Best-fit operation | 10-year modeled cost | Decision trigger | Where it breaks |

| Lagoon upgrade | 800–1,200 cows with workable acres and disciplined NMP records | $1.46M at 1,000 cows | Engineer quote below $950K | If added storage/reline climbs toward $1.0M–$1.5M, the advantage narrows fast |

| Vermifiltration WAS | Mid-size dairy with ugly lagoon exposure, grant eligibility, and compost outlet | $2.10M before labor; $2.24M with midpoint labor | Engineer quote near or above $950K | No compost export contract means only ~4% N-loading reduction |

| Solo covered-lagoon digester | Larger or cluster-scale operation with deep grant/LCFS stack | $6.80M at 1,000 cows | Strong gas volume, grants, and revenue-share terms | Small solo projects rarely carry debt service without outside economics |

| Right-size or structured exit | Tight acres, weak DSCR, unclear succession, high basin pressure | Variable, but avoids forced capex spiral | DSCR below 1.2 for repeated quarters | Waiting too long lets the buyer or lender set the terms |

Lane 1 — Fix the lagoons, tighten nitrogen management. Makes sense when your engineer’s 10-year compliance estimate is in the $400–700K range, your acres-per-cow ratio is workable, and your NMP execution is disciplined. Requires a current lagoon integrity assessment against Central Valley Regional Board seepage standards, added storage planning, and honest per-acre N accounting. Risk: if the 2026 order requires partial covers or significant added storage, a $500K estimate can climb toward $1.0–1.5M, and this lane narrows against Lane 2.

Lane 2 — Vermifiltration under a vendor-owned WAS deal. Makes sense when expected lagoon capex is heading toward $950K+, you’re a competitive AMMP/Dairy Plus candidate in the current cycle, you have a real outlet for 800–1,000 dry tons of compost per year, and your management team has bandwidth for roughly 8–12 additional operator hours per week. Risk: under structures like the one BioFiltro’s 2022 investor summary describes, you don’t capture carbon revenue, you’re locked into a long-term service contract, you still carry residual lagoon OPEX, and your compliance story depends on keeping compost moving off-farm.

Lane 3 — Covered-lagoon digester, solo project. At 1,000 cows, the 10-year model runs near $6.8M. Requires deep grant and LCFS revenue to pencil, and typically makes sense only at consolidated or cluster scale. Smaller solo projects rarely generate enough biogas volume to cover debt service without a co-digestion partner.

Lane 4 — Right-size or plan a structured exit. Makes sense when basin math is ugly, acres-per-cow is already tight, succession is unclear, and any capex path above would strain what your lender will refinance. Risk: waiting too long lets a forced sale set the terms. Requires an advisor without a sales agenda and a willingness to look at the numbers without attachment to headcount.

The 30/90/365-Day Playbook for Herds Facing This Decision

Print this section. Take it to your lender.

30-Day Actions — Pull These Before Any Vendor Meeting

- ☐ Get a written, independent lagoon assessment. Commission a current lagoon integrity and storage-capacity review from your ag engineer, referenced to Central Valley Regional Board seepage standards. Use an engineer with no commercial relationship to the system vendor. Red-flag trigger: if the 10-year compliance estimate comes back above $950K in today’s dollars, Lane 2 becomes a legitimate conversation. Where it backfires: a vendor-funded assessment isn’t the same thing.

- ☐ Check your AMMP/Dairy Plus eligibility. Ask your NRCS technical service provider for an updated eligibility review before the next grant cycle opens. Red-flag trigger: if you don’t qualify for either program as currently structured, the WAS economics don’t work without CPG or third-party funding.

- ☐ Test the compost market. Call the nearest bulk compost buyer and request a price and volume quote for 500–1,000 tons/year of dairy vermicompost, plus a haul estimate for your location. Red-flag trigger: if no buyer within 50 miles quotes you a price, Lane 2’s nitrogen benefit disappears.

90-Day Actions — Structural Decisions That Need Planning

- ☐ Run the three-lane model for your actual operation. Use your real cow count, real acres, and your lender’s honest 10-year debt service view. Requires your CPA, your lender, and one independent ag engineer — not the vendor’s financial model. Red-flag trigger: if your DSCR has been below 1.2 for three or more consecutive quarters under your lender’s method, any capital-intensive path is secondary to fixing cash position.

- ☐ Get a written WAS term sheet. Request a written quote including per-gallon or per-cow fee, carbon credit ownership clause, contract term and exit conditions, and what happens if you sell or right-size. Red-flag trigger: any clause that bars decommissioning if the system fails to meet your agronomic or regulatory targets.

- ☐ Run your actual per-acre N balance. Pull the last three years of NMP records and calculate real lb N/acre/year by field. Red-flag trigger: if you’re already above 175 lb/acre on a meaningful portion of your acreage, you have a nitrogen problem vermi alone won’t solve without a parallel export strategy.

365-Day Moves — Strategic Positioning for the Rule You’re Going to Get

- ☐ Make a binary lane decision. Indecision has a cost. Each lane is defensible with clear eyes; none is defensible as a permanent maybe. Opportunity signal: if AMMP and Dairy Plus together can cover 60%+ of a verified vermi project AND your lagoon bullet is at the $950K+ end, Lane 2 may pencil. Document the analysis and take it to your lender before the order finalizes.

- ☐ Lock in your compost export relationship in writing. Treat the compost outlet like a feed contract. An informal agreement isn’t a nitrogen compliance strategy. Requires a signed annual purchase agreement with a buyer who can absorb consistent volume, plus a backup if that buyer exits.

- ☐ Position for the rule as written, not as hoped. Whole-farm N accounting is coming to the Central Valley whether or not you own worms. Operators with the most flexibility in 2027 and 2028 will be the ones who ran the N balance honestly this year and made a structural decision — more acres, verified export, precision feeding, or a lane choice above.

What This Means for Your Operation

Vermifiltration is a legitimate survival tool for a narrow band of California dairies where the lagoon bullet is genuinely ugly, the grant stack is real, the compost outlet exists, and management has bandwidth to run a small wastewater plant alongside a large dairy. For that specific combination, Lane 2 is a rational hedge against regulatory and capital risk. For everyone else, the math still favors fixing your lagoons, running your N balance honestly, and making a hard call about whether your acreage and cost structure survive what the 2026 order is about to demand.

The trade-off at the heart of this case isn’t worms versus lagoons. It’s whether paying a premium to host infrastructure that generates climate revenue for the vendor — in exchange for regulatory goodwill and avoided lagoon capex — is worth it for your balance sheet, your management bandwidth, and your basin’s specific water pressure.

What does your engineer’s most recent lagoon memo actually say your 10-year compliance path costs — and does any clause in your current processor sustainability agreement change which lane you’re really in?

Are you seeing lagoon upgrade quotes in the $1M range in your basin? Drop a comment or email us — we’re tracking the “Lagoon Inflation” across the Central Valley and will publish an aggregated quote range in a follow-up within 60 days.

Key Takeaways

- The deciding number isn’t $640K — it’s your engineer’s lagoon-upgrade quote. Below roughly $950K at 1,000 cows, fixing lagoons still wins; above it, a BioFiltro deal starts to pencil before labor and carbon carve-outs.

- Under the 2022 WAS structure, the vendor holds the climate attributes. Before you sign, get the current credit-ownership clause in writing — don’t assume carbon revenue flows back to the farm.

- Worms don’t solve a whole-farm N balance. Without a signed compost-export contract moving 50% of solids off-farm, your on-farm loading drops only ~4%; with that contract, it drops ~38%.

- Four honest lanes: fix lagoons, sign a WAS deal, build a solo digester, or right-size. Pick one against your actual engineer’s memo, your NMP records, and your lender’s DSCR view — not the vendor’s financial model.

Methodology & Sourcing Note

This piece analyzes publicly reported information about Alberto Dairy and BioFiltro. Contract descriptions reflect BioFiltro’s publicly filed 2022 investor summary and may not match specific Alberto Dairy contract provisions, which aren’t public. All barn math is modeled and illustrative — not an accounting of any specific operation’s actual books. Regulatory references include the State Water Board’s October 2024 directive to the Central Valley Regional Board and the Central Valley Regional Board’s staff analysis of nitrogen pathways to affected aquifers. Trade-media references include Dairy Herd Management’s 2024 Alberto Dairy feature and Ag Alert’s California coverage. The lender characterization reflects an informal, off-the-record industry conversation and is included as directional context only; no client-specific numbers are attributed. Financial modeling inputs are drawn from Newtrient, NRCS, UCCE dairy cost studies, the California Dairy Research Foundation, LPELC, Washington State University Extension, CalRecycle, CDFA’s Dairy Digester Research & Development Program, and BioFiltro public disclosures. Lane cost ranges reflect a 2026–2035 planning window at 7% cost of capital; individual operations should model their own inputs with their CPA, lender, and an independent ag engineer.

Learn More

- The Carbon Credit Programs Every Dairy Should Join Before 2026 — Arms you with a vetted checklist to avoid the “$100,000 mistake” when vetting climate programs. Lists funding levels for REAP and LCFS multipliers, delivering the exact ROI benchmarks needed to verify any sustainability pitch.

- The $100 Springer Gap: Dairy Farm Relocation Is Moving America’s Milk Map to I-29 — Delivers a 10-year financial map of the friction between staying in California and relocating to the I-29 corridor. Breaks down the specific $0.75/cwt basis trigger and 7–10 year payback window that forces the move-or-adapt decision.

- $1130 Per Cow, $128 Back: Where the Rest of Your RNG Money Really Goes — Exposes the “50/50 partnership” myth by following the money on RNG credit splits. Reveals how the $1,130-per-cow gross value shrinks to $128 for the producer, identifying the hidden contract clauses that decide who gets paid.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.