Your neighbors will bring casseroles and cattle trailers for the first 48 hours. They won’t write a $519,000 check in month 13. Only a correctly written policy does – and most mid-size dairies don’t carry one.

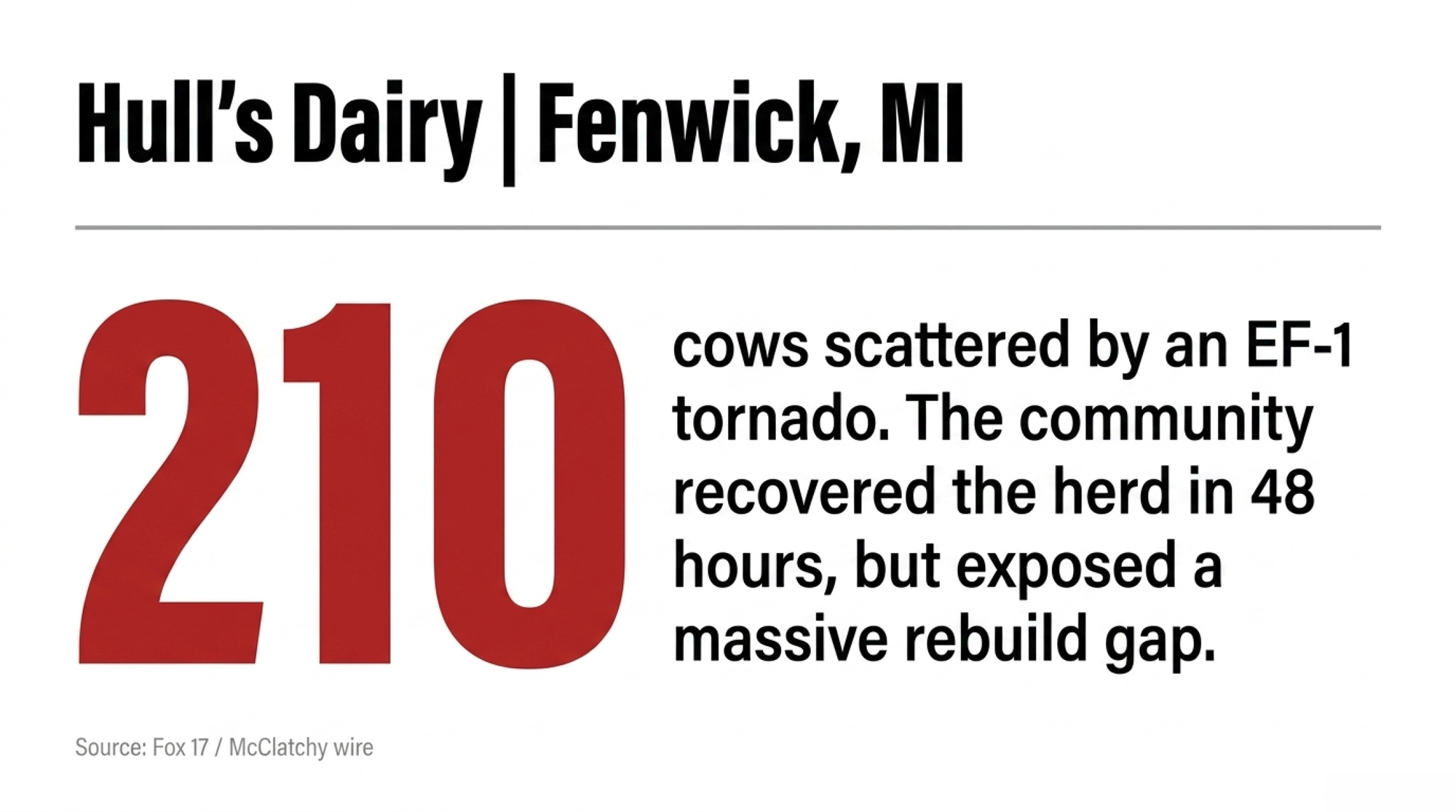

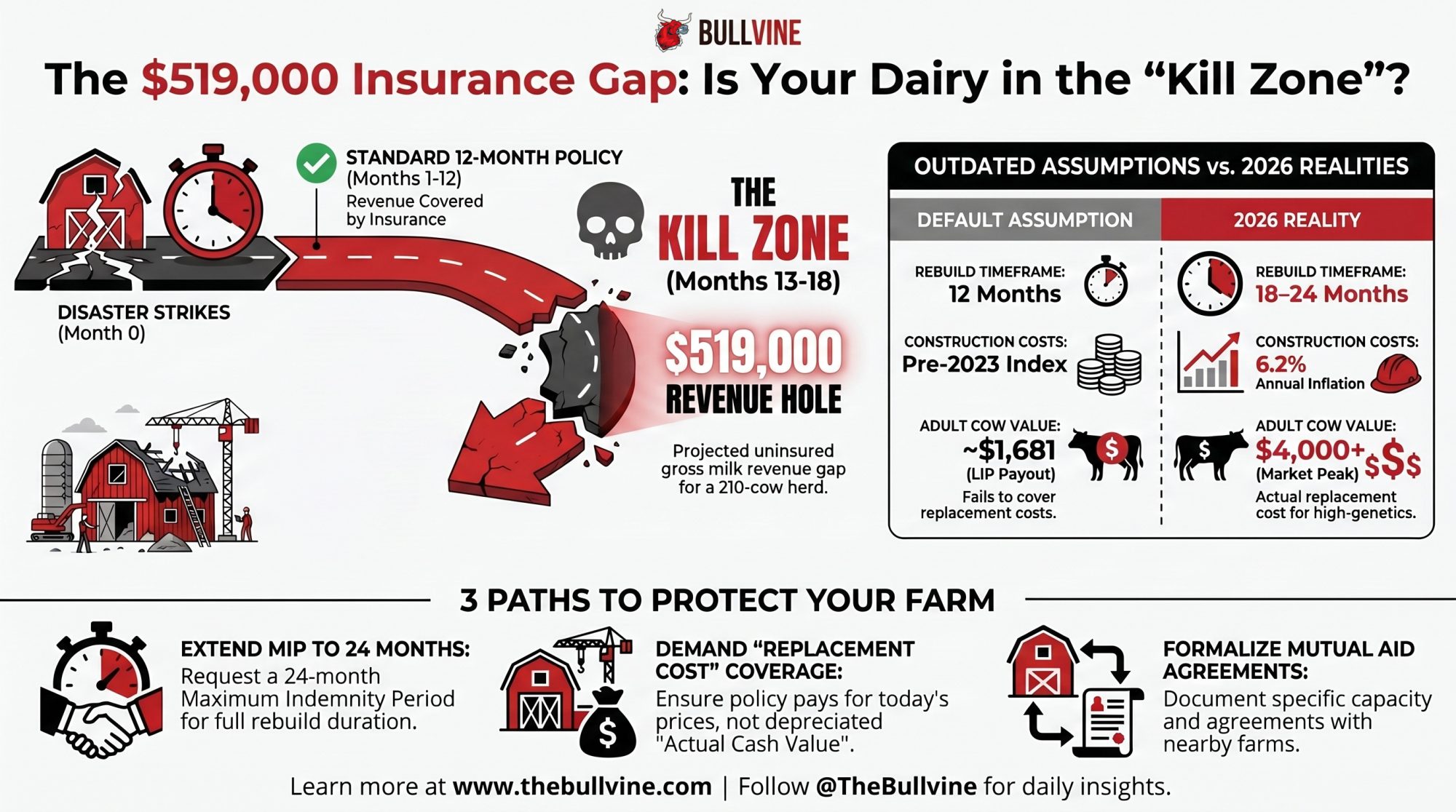

Executive Summary: An EF-1 tornado leveled Hull’s Dairy in Fenwick, Michigan at 10:58 PM on April 14, scattering 210 cows across Montcalm County — and exposing a six-figure coverage hole sitting in most mid-size dairy policies. Default farm policies run 12-month business interruption periods, but industry ag claims guidance — including from Sedgwick — puts complex dairy rebuilds at 18–24 months, leaving roughly $519,000 in uninsured gross milk revenue on a 210-cow herd at March 2026’s $16.16/cwt Class III. Construction costs make it worse: BLS PPI put 2025 materials inflation at 6.2%, and Lactanet’s 2023 survey pegs insulated dairy barns at $18,160 per head all-in, $7,100 per cow in equipment alone. Your LIP payment isn’t a recovery mechanism either — $1,681.88 per adult cow pays about 42 cents on the dollar against a $4,000+ springer, and as little as 12 cents on a VG-88 with real genetic merit. Blanket livestock coverage doesn’t distinguish a +2800 GTPI two-year-old from a GP-83 off a truck. The community brought cattle trailers for the Hulls within hours; they won’t cover month 13 of a rebuild. The 30-day move: call your agent, confirm Replacement Cost (not ACV) coverage, and price a 24-month MIP before renewal.

Janet Hull was in her basement at 10:58 PM on April 14, 2026, when the EF-1 hit her family’s farm in Fenwick, Michigan. She told Fox 17 it sounded like a train coming through the barns above her. By morning, the freestall that housed 80 of her cows was gone, two head were confirmed dead, and more than 200 animals were scattered across miles of dark Montcalm County countryside.

The community response was the kind dairy country still does better than anywhere else. Noah Heckman pulled in at sunrise with a cattle trailer, per Fox 17. Stephanie Schafer of Jem-Lot Dairy — a Michigan Farm Bureau District 5 director — drove her own truck over, per McClatchy wire reporting. Lane Grieser with Farm Bureau was on the phone. By Wednesday night, nearly the entire 210-cow herd had been recovered and relocated to a neighbor farm in North Ionia.

Every local outlet ran that story. None of them ran the math.

Here’s what they missed — and it’s not about Hull’s specific policy, which isn’t public. It’s about the default farm insurance structure a typical 200-cow family dairy carries. That structure likely sits on roughly $519,000 in uninsured gross revenue exposure between what a 12-month business interruption policy pays and what a complex rebuild costs when it runs to the midpoint of an 18–24 month range. No claim here about the Hulls’ individual coverage. This is about what the default structure does to a farm at that scale — and where the real risk hides in most dairy farm tornado damage recovery scenarios.

What’s Changed — and Why Your Policy Hasn’t Kept Up

Three things have shifted in the last few years that quietly made most farm insurance policies inadequate. Most producers didn’t notice. Carriers don’t send a letter when the math stops working.

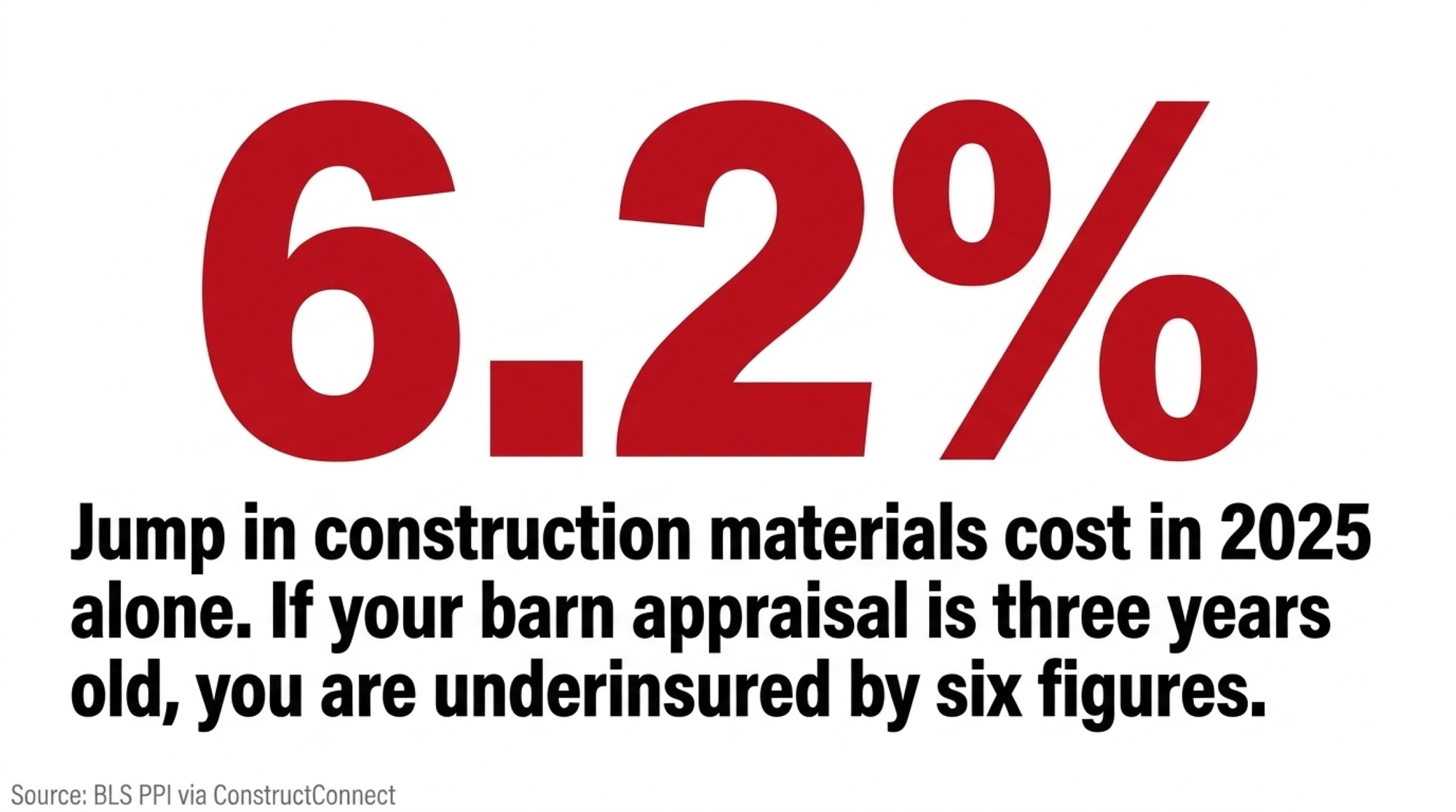

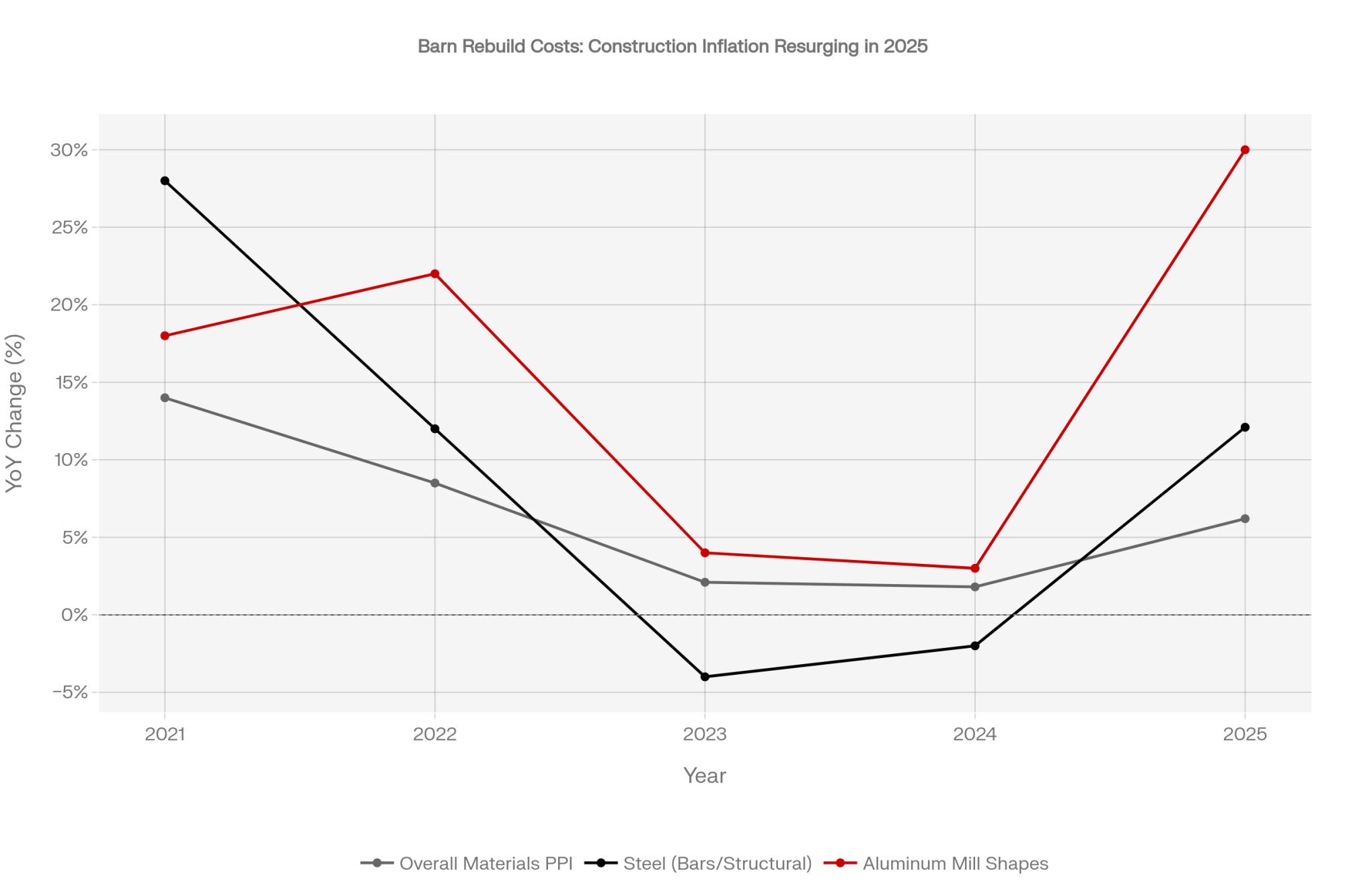

Construction costs are the first. Construction material prices rose 6.2% across 2025 — the largest single-year increase since the post-Covid spike in 2021 — according to Bureau of Labor Statistics Producer Price Index data reported by ConstructConnect. Steel bars, plates, and structural shapes climbed 12.1%. Aluminum mill shapes jumped more than 30% on tariff pressure. The Dairy Challenge 2022 benchmark pegged a basic freestall at roughly $3,500–$7,000 per milking stall depending on parlor and equipment build-out. Lactanet’s 2023 survey of 29 insulated dairy barns in Quebec put median costs at $101 per square foot total, $60.10 per square foot building only, $18,160 per head all-in, and $7,100 per cow in equipment alone. Layer the 2025 materials escalation onto that 2022–2023 baseline and rebuild numbers are running well above what most policies were priced to cover.

The replacement heifer market is the second. CoBank’s Knowledge Exchange reported in August 2025 that U.S. dairy heifer inventories have already hit a 20-year low and will shrink by an estimated 800,000 head over the next two years before any rebound in 2027. CoBank’s Corey Geiger flagged that heifer prices had already reached record highs and “could climb well above $3,000 per head.” Trade-media reporting through spring 2025 puts peak-market Holstein springer prices at $4,000–$4,200. If you have to replace cows fast after a disaster, “average” isn’t the number you pay. The market is. And the market is expensive.

The third shift is the quiet one. Farm policies don’t automatically update to either of those realities. Per-building replacement values are set at underwriting and only move when you proactively ask for a reappraisal. Some policies carry inflation-guard or auto-adjust endorsements, but most standard farm packages don’t include them by default — which is why the audit call matters. Maximum indemnity periods on business interruption coverage default to 12 months, a number calibrated back when a standard dairy rebuild fit inside that window. The gap shows up when the adjuster does.

How This Plays Out on Real Farms

Run the numbers on a 210-cow herd. A well-managed Holstein herd producing at 85 lbs/day puts roughly 17,850 pounds of milk in the tank daily — a pace above USDA NASS’s national average of about 65 lbs/cow/day across all breeds, which is why we’re calling it well-managed, not average. At USDA AMS’s March 2026 Class III price of $16.16/cwt, that’s $2,885 in daily gross milk revenue. Weekly, call it $20,200. Monthly, about $86,500. April 2026 Class III futures were trading around $16.84 as of mid-April; the USDA final print follows at month-end.

Now layer in the disruption math. Standard farm BI kicks in after a 48–72 hour waiting period and runs for a 12-month maximum indemnity period on most policies. In Sedgwick’s February 2024 publication “Maximum Indemnity Period: Is 12 months long enough?”, the firm’s major loss specialists make the case explicitly: policyholders “should work on the assumption of a total loss” and factor in a full recovery period, because rebuilding the physical asset is only phase one — winning back revenue or customers is phase two, and the phases compound. Farmers Weekly’s Business Clinic makes the dairy-specific version of the same point bluntly: “For larger, more complex dairy units 24 months may be needed to rebuild and re-establish a herd.” Those extensions have to be proactively bought. Unless you raise it, many policies renew at the default 12-month MIP out of habit.

What Your Policy Probably Says vs. What the Rebuild Actually Costs

| Coverage element | Default policy assumption | 2026 reality | Gap |

| Freestall replacement (80-stall unit) | Indexed to pre-2023 build figures | Per Lactanet 2023: median $18,160/head all-in on insulated barns; equipment alone at $7,100/cow | Scales with cumulative 2023–2026 escalation |

| Construction input escalation | Locked at last appraisal | 6.2% materials increase in 2025 alone per BLS PPI | Tens of thousands to six figures depending on appraisal age |

| Business interruption period | 12 months MIP | 18–24 months per Sedgwick and Farmers Weekly guidance for complex dairies | 6–12 months uncovered |

| Livestock indemnity per adult cow | $1,681.88 via USDA FSA LIP (2025 schedule) | $3,000+ per head per CoBank; $4,000–$4,200 peak spring 2025 | ~$1,300–$2,500+ per head |

| Gross milk revenue at risk, months 13–18 | Not covered | ~$519,000 on a 210-cow herd | ~$519,000 ← The Kill Zone |

If a rebuild runs past the 12-month mark, the missing months 13 through 18 represent roughly $519,000 in uninsured gross milk revenue on a herd this size. One caveat worth naming up front: BI policies typically pay gross revenue minus saved expenses, so the actual out-of-pocket shortfall moves with feed, labor, and repair savings during the disruption. The $519,000 is the top-line revenue hole, not the net gap. Even so, the net still lands in six figures on a herd this size. Call it the kill zone: the window where no program, no neighbor, and no GoFundMe covers the difference. Only a correctly written policy does.

And this math scales. A 500-cow operation running the same 85 lbs/day at $16.16/cwt is putting about $206,000 in monthly gross revenue through the parlor — double the exposure per month the default MIP leaves uncovered. Scale doesn’t protect you here. It widens the gap.

What LIP Doesn’t Cover: The Genetic Premium Your Policy Ignores

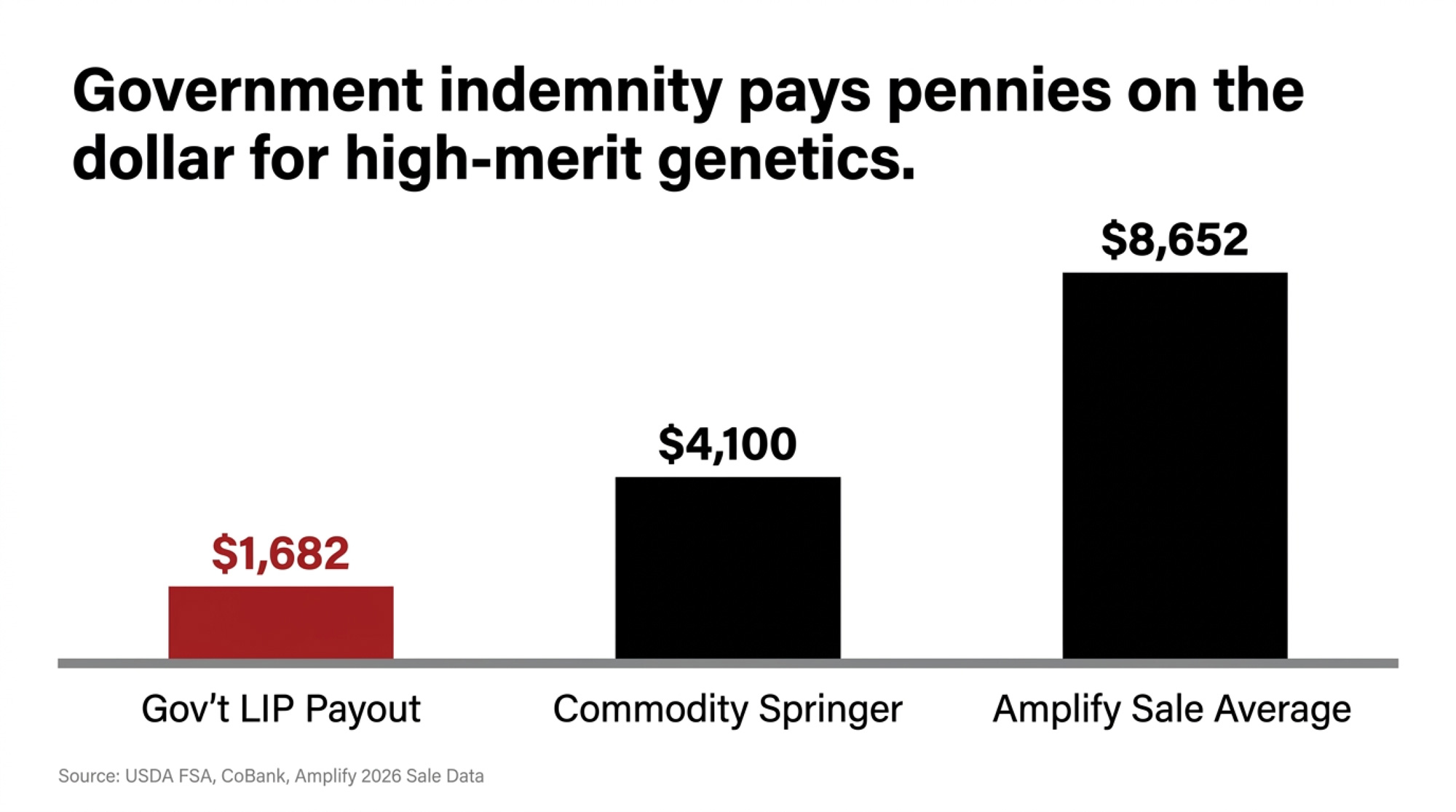

Now the second gap — and this one hits Bullvine readers harder than most. The USDA Livestock Indemnity Program pays $1,681.88 per adult dairy cow lost to a qualifying disaster under the 2025 rate schedule. The 2026 table hadn’t been released as of publication; historically, LIP rates update mid-year based on prior-year fair market values.

That $1,681.88 is calculated on an industry-average market value for a generic adult dairy cow. It doesn’t distinguish between a GP-83 first-calver you bought off a truck and a VG-88 two-year-old carrying a +2800 GTPI that you’ve spent three generations building toward. If you lose that animal in a tornado, LIP pays $1,681.88. Period. The pedigree, the classification score, the genomic premium, the flush potential — none of it exists in the indemnity formula.

Market replacement springers are running $4,000–$4,200 for average genetics at peak, per spring 2025 trade-media reporting. But if you’re rebuilding a herd with above-average genetic merit, the replacement cost per head isn’t $4,000. For genomic-tested, classified cows — the kind many Bullvine readers are building — market replacement routinely runs two to four times the commodity springer price, and for the top end of the market, much higher. The Amplify 2026 sale averaged $8,652 across 124 lots — roughly double commodity springer pricing. Move up one tier and the 2024 World Classic Holstein Sale at World Dairy Expo averaged $30,245 across 55 lots, with a $205,000 IVF session topping the board. Best of Triple-T & Friends in May 2025 hit $78,500 on Ms Milksource Sunday-ET, an All-American class winner Tattoo daughter. That makes LIP not a recovery mechanism but roughly 42 cents on the dollar at commodity replacement, and materially less — potentially 12–21 cents on the dollar — for a genetically invested herd. For every cow lost and replaced, the farm eats the rest.

Standard farm insurance livestock coverage doesn’t typically distinguish by genetic merit either — not unless you’ve specifically scheduled individual high-value animals, which most 200-cow operations haven’t done. If you’ve never asked your agent whether your livestock coverage is blanket or scheduled, and whether it pays market value or a flat sublimit, this is the week to find out.

The Mechanics Behind the Outcomes

It’s not random. It’s how the system was built.

Farm insurance is priced against historical average losses. Reinsurance models, per-building sublimits, and MIP caps were calibrated against a decade of claims data from an era when construction costs were flatter and ag contractors more available. Those assumptions haven’t updated at the pace the underlying economics have. The policy you signed three years ago is protecting a farm that no longer exists at those numbers.

Federal disaster programs, meanwhile, run in isolation. LIP, FSA Emergency Loans, SBA EIDL, and crop insurance — four different agencies, four different timelines, four different sets of eligibility rules, and no coordinated intake. USDA’s One Farmer, One File initiative launched at 2026 Commodity Classic is working to streamline digital services across FSA, NRCS, and RMA, but completion is targeted for 2028. A producer in active recovery today still has to navigate all four programs independently while managing a displaced herd, a construction project, and a cash-flow hole. The system rewards sophistication at exactly the moment operators have the least capacity for it.

And there’s a piece nobody talks about at the Farm Bureau meeting: your lender isn’t your friend when the barn is flat. They’re a risk manager. Ag lenders use internal risk classification systems, and a disaster-recovery loan can quietly move to a watch list or “Special Assets” classification. Disclosure timing varies by lender. Borrowers who ask directly typically get straightforward answers. Borrowers who don’t ask often don’t find out until their loan terms change underneath them — interest rate, reporting requirements, and collateral scrutiny can all shift once the file moves to a different desk. The bridge-financing conversation that could’ve happened easily in month 2 gets noticeably harder in month 10.

None of this is rocket science. It’s just the work nobody does until the wind hits.

How Much Does the 20-Minute Phone Call Actually Save?

Depends where your current coverage sits relative to your real exposure. But the order of magnitude is consistent across most mid-size dairies that haven’t reviewed their policies in three or more years.

On the structure side, a construction cost gap against a $300,000 barn scales directly with the cumulative escalation since your last appraisal — likely in the tens of thousands on a barn that size, potentially six figures if the appraisal is five-plus years old. BLS PPI put 2025 materials inflation at 6.2%. On the MIP side, stretching from 12 to 24 months on a 210-cow operation protects roughly the same six-figure range as the $519,000 gap walked through earlier — the back half of a slow rebuild where the default policy has already tapped out. Combined, the phone call plus a modest premium adjustment closes a six-figure exposure currently sitting on your balance sheet as unacknowledged risk. That’s a better ROI than most decisions you’ll make this quarter.

Is Your Mutual-Aid Network Real, or Is It a Hope?

Every producer in tornado country has a mental list of neighbors they’d call. Fewer have actually confirmed those neighbors have the capacity, the facility space, and the willingness to absorb 50–100 head on 12 hours’ notice. Fewer still have had the conversation explicitly enough that the neighbor knows to pick up the phone at 11 PM on a Tuesday.

Per public reporting, the Hulls had Noah Heckman, Stephanie Schafer, Lane Grieser, and a neighbor in North Ionia who could house the entire 210-cow herd. Real network. It showed up. For most producers, the answer to “who boards my herd for 6 months if the barn’s gone tomorrow” is a name, not an agreement. Those aren’t the same thing. Write down the agreement. Exchange numbers. Document the capacity. After the siren, you can’t build the relationship fast enough.

| Element | “I Have a Name” | A Real Agreement |

|---|---|---|

| Contact confirmed? | Maybe — you assume they’d answer | Cell number in your phone, verified in last 6 months |

| Capacity confirmed? | Assumed based on farm size | Explicit: “I can take 50 head in the freestall for up to 90 days” |

| Timing confirmed? | “They’d come if I called” | Explicitly agreed: picks up at 11 PM on a Tuesday |

| Herd biosecurity discussed? | ❌ Never | ✅ Health status, vaccination protocols exchanged |

| Feed/labor cost arrangement? | Assumed informal | Written: cost-sharing or reciprocal commitment documented |

| Lender/insurance notified? | ❌ Unknown | ✅ Listed as contingency in your insurance file |

| Michigan AgMediation contact? | ❌ Unknown | 📞 800-616-7863 on file |

Options and Trade-Offs for Farmers

Four practical paths for producers who want to close these gaps before they turn into active problems.

Path 1 — The 20-minute coverage audit (do this within 30 days). Call your ag insurance agent this week and ask three specific questions: (1) What is the replacement cost per building on my policy, and when was it last updated? (2) What is my maximum indemnity period for business interruption? (3) What does a livestock loss claim actually pay on cows that are unrecovered versus confirmed dead?

Pro Tip: Ask your agent one more question: “If I have a total loss today, do I have a Replacement Cost or Actual Cash Value policy?” If they say ACV, start shopping. An ACV policy insures depreciated value — the farm as it existed in 2018, not the farm you’d have to rebuild in 2026. That single distinction can be the difference between a six-figure gap and a manageable rebuild. Replacement Cost coverage pays what it actually costs to rebuild at today’s prices. ACV pays what your barn was worth minus years of wear. You don’t want to find out which one you have after the adjuster shows up.

Path 2 — Request a replacement cost appraisal. If your last appraisal is more than three years old, construction escalation has likely opened a meaningful gap between insured value and rebuild cost. BLS PPI data — via ConstructConnect — puts 2025 construction materials inflation at 6.2%, the fastest single-year rise since 2021, with specific items like steel and aluminum running well higher. Makes sense for any farm with meaningful capital infrastructure. Requires a formal appraisal request and possibly a premium adjustment. The limit: ask for the quote before committing. Premium increases may be modest or meaningful depending on how much coverage you actually need to expand.

Path 3 — Extend your MIP to 24 months. Sedgwick’s major loss team and Farmers Weekly’s Business Clinic both make the case that 18–24 months is the realistic indemnity window for complex dairy rebuilds. Makes sense for any farm with specialized ventilation, robotic or parallel milking systems, or multi-structure exposure. Requires a proactive ask at renewal. The premium increase is usually modest. The coverage difference can run into six figures.

Path 4 — Document your mutual-aid network in writing. Identify two neighbor farms willing to take 50–100 head on 12 hours’ notice. Get their cell numbers in your phone. Exchange basic herd inventories so confirmations move fast. Makes sense for every farm in tornado, flood, or fire country. Requires a real conversation, not an assumption. The limit: goodwill and capacity aren’t the same thing — confirm both. Michigan producers can also loop in the state’s Agricultural Mediation Program (800-616-7863) for any disaster-related lender or neighbor-aid dispute that can’t be resolved at the kitchen table.

Key Takeaways

- If your policy’s per-building replacement value hasn’t been updated in three years, assume a meaningful construction gap and request a reappraisal this month. BLS PPI alone put 2025 materials inflation at 6.2%.

- If your business interruption MIP is still 12 months, get a quote on 24. Sedgwick and Farmers Weekly both point to 18–24 months as the realistic rebuild window for complex dairies.

- If you don’t know whether you carry Replacement Cost or Actual Cash Value coverage, find out before your next renewal. ACV protects a depreciated barn, not the one you’d have to build.

- If your livestock coverage is blanket rather than scheduled, high-value genetics typically aren’t protected — a VG-88 cow and a GP-83 cow often pay out the same under standard farm policies. Confirm with your agent before assuming your genetic investment is covered.

- If you don’t know that LIP pays $1,681.88 per adult dairy cow, you can’t model the out-of-pocket gap against CoBank’s $3,000+ heifer forecast — let alone replacement for an Amplify 2026-tier lineup averaging $8,652 or a World Classic-tier lineup averaging $30,245.

- If your mutual-aid network is a list of names rather than a set of confirmed agreements, treat it as a hope, not a plan.

- If you haven’t asked your commercial lender how your loan classification changes in a disaster-recovery scenario, you’re flying blind on a conversation that happens quietly around month 8.

- If you can’t name an operator in your region who has completed a full post-disaster dairy rebuild, find one through Farm Bureau or your co-op before you need them. Their pattern recognition is worth more than any program brochure.

The community that showed up for Janet Hull on April 15 was extraordinary. But here’s the part nobody says out loud: your neighbors will bring casseroles and cattle trailers for the first 48 hours. They aren’t writing a $519,000 check in month 13. Only you — and a correctly written policy — can do that. Find out your number before your neighbor finds out theirs.

Next week in Bullvine Weekly: the full replacement cost audit framework by herd size and structure type — the exact questions to bring to your agent, the documents to request, and the thresholds that tell you whether your policy is keeping pace with 2026 construction costs. That’s where the real numbers live.

Sourcing note: This article is based on public reporting from Fox 17, WKAR, WWMT, and the McClatchy wire (Kansas City Star). Class III price per USDA AMS Announcement of Class and Component Prices (March 2026). LIP rate per USDA FSA 2025 Livestock Indemnity Program fact sheet. Construction cost data per Bureau of Labor Statistics Producer Price Index (2025) as reported by ConstructConnect (February 2026). Dairy barn construction cost benchmarks per Lactanet 2023 survey of 29 insulated Quebec dairy barns and Dairy Challenge 2022 building cost estimates. Heifer market data per CoBank Knowledge Exchange, “Dairy Heifer Inventories to Shrink Further Before Rebounding in 2027” (August 27, 2025). Business interruption guidance per Sedgwick, “Maximum Indemnity Period: Is 12 months long enough?” (February 11, 2024) and Farmers Weekly Business Clinic (March 28, 2022). Sale averages per Amplify 2026 (February 27, 2026), 2024 World Classic Holstein Sale at World Dairy Expo, and The Best of Triple-T & Friends 2025. Milk production context per USDA NASS. The Bullvine has not spoken directly with the Hull family. If Janet, Bryan, Ryan, or Drew would like to share their perspective for follow-up coverage — or request a correction on anything in this piece — we welcome the conversation.

Learn More

- The Hidden Contract Clause That Could Cost Your Dairy $55,000 in 2026 — Warns against unlimited liability clauses in 2026 processor contracts that could drain $55,000 from a 500-cow operation. This breakdown dismantles the new allergen regulatory shift and delivers a buying-group strategy to cap risk before year-end.

- 4.23% Butterfat, $187,000 Gone: The Margin Math That Broke 2025 – And Shapes Your 2028 — Exposes the invisible equity erosion costing operations $187,000 annually by following the money on national component records and regional pain points. Alignment strategies for 2028 export market realities deliver a framework to protect your long-term equity.

- Bred for Fat, Paying for Protein: The $180,000 Trap Locked into Western Cheese Herds Until 2029 — Dismantles the NM$ index myth and delivers a custom, protein-weighted breeding strategy to capture cheese-market premiums. This analysis follows the money on a structural margin gap of $182,000 per year for mismatched herds.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.