Your lender is already running the Q3 margin math. Here’s how to beat them to it.

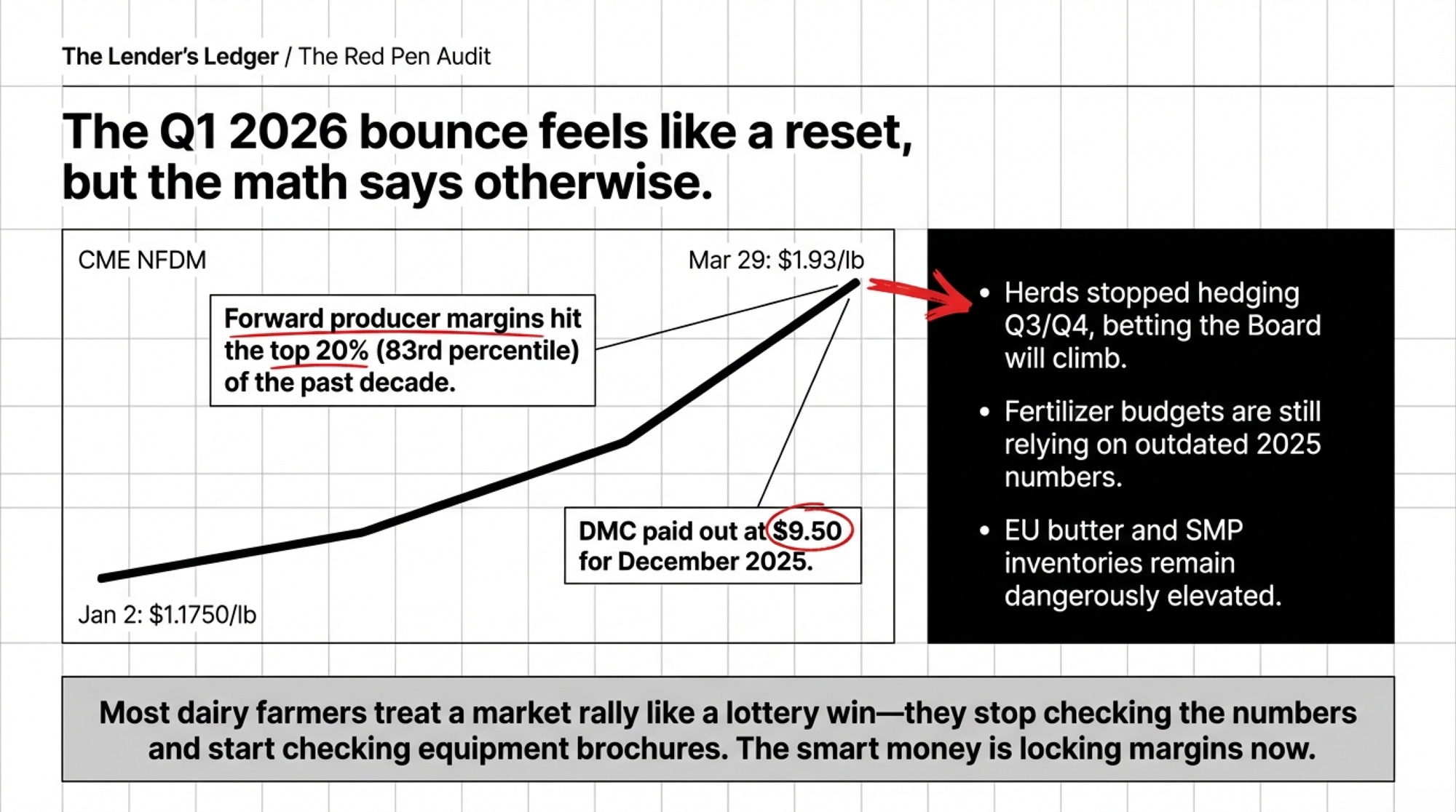

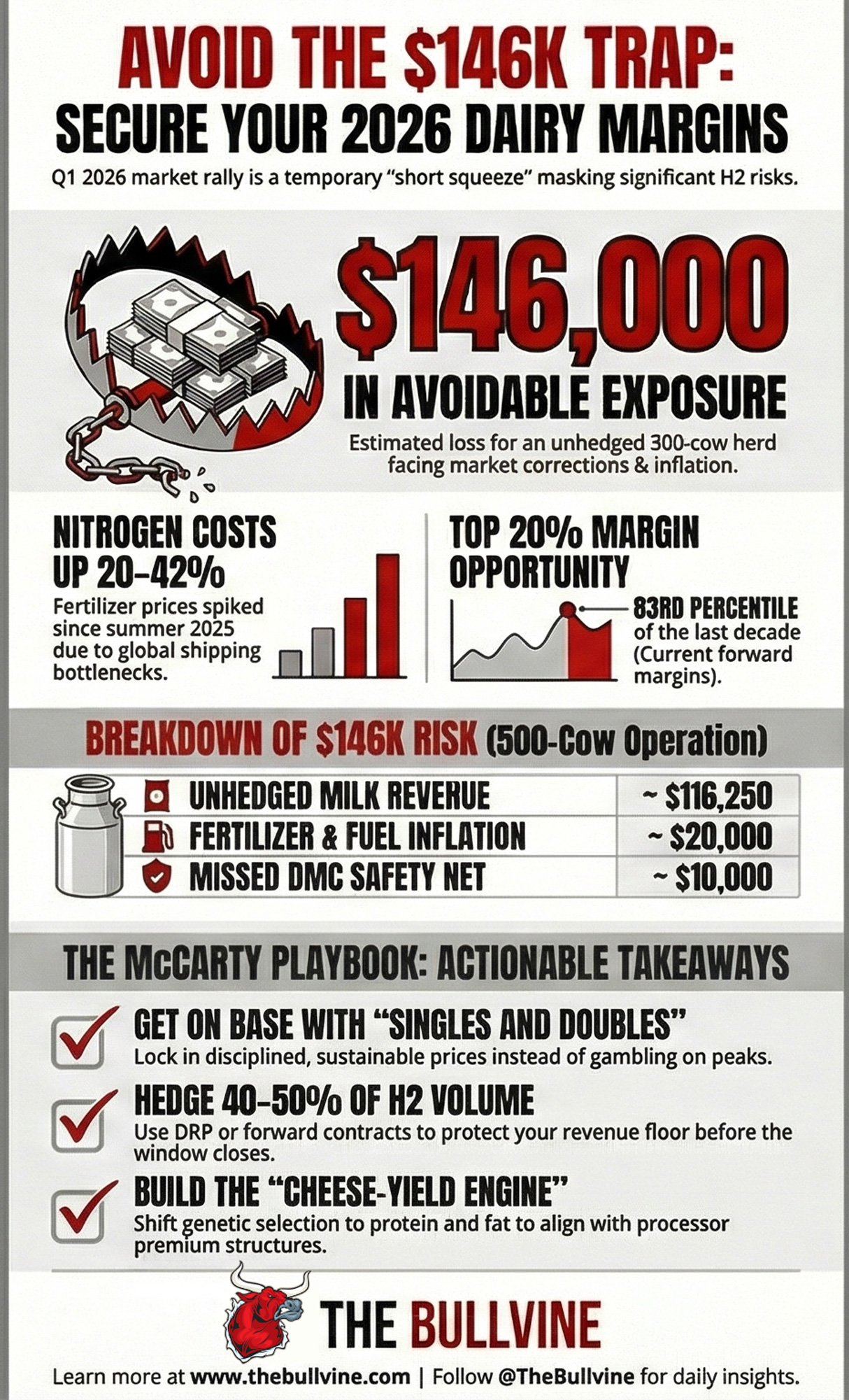

Executive Summary: Forward dairy margins from March 2026 onward sit above the 83rd percentile of the past decade — and most herds haven’t locked a pound of H2 milk. The Q1 rally that pushed CME NFDM from $1.1750 to $1.93 in under three months wasn’t a fundamental demand reset — it was a short squeeze layered on Hormuz-related double-ordering, and both forces are already fading. On a 500-cow herd, leaving H2 unhedged while running 2025 input numbers creates roughly $146,000 in avoidable exposure: $116,250 in unprotected milk revenue plus $20,000-plus in fertilizer and fuel inflation most budgets haven’t absorbed yet. Central Illinois nitrogen alone is up 20–42% since last summer, depending on source. EU butter and SMP stocks remain heavy, and the late-March GDT Pulse auction already softened. Inside: the full barn math on that $146K, a three-sentence lender script for your Q2 review, and a 30/90/365-day playbook for buying floors while the window’s still open. If your stress-case H2 DSCR sits below 1.2x, read this before your next lender meeting — not after.

Most dairy farmers treat a market rally like a lottery win — they stop checking the numbers and start checking the equipment brochures. Ken McCarty isn’t most farmers. While the rest of the industry basks in the glow of the Q1 2026 bounce, the smart money is already bracing for the $146,000 trap waiting in the H2 tall grass. If you aren’t mathing your margin right now, your lender is about to do it for you — and you won’t like their answer.

McCarty’s family had key energy costs locked years in advance as part of a long‑term risk strategy with their processor and partners. Boring. Disciplined. And worth serious money on a multi‑site family dairy of their size. His philosophy boils down to one line: get on base. Lock in a price you can live with before the market hands you something you can’t.

HighGround Dairy’s Q1 2026 Producer Market Update pegs forward producer margins from March 2026 onward above the 83rd percentile of the past decade — top‑20% territory. At the same time, nitrogen costs have climbed 20–40%from late‑summer 2025 levels, European butter and SMP stocks are heavy, and most 2026 fertilizer invoices haven’t fully landed in cash‑flow plans yet. For a 500‑cow operation that rides the rally, changes nothing, and walks into Q3 unhedged, the math points to roughly $146,000 in avoidable exposure over the next twelve months.

That’s the number your lender is going to circle in red.

Why the Q1 Bounce Feels Safe — and Isn’t

Through late 2025, the consensus called for a “tsunami of milk” in 2026. EU production ran well above year‑earlier levels in Q3 and Q4, with Germany and France driving much of the growth. USDA kept nudging U.S. production forecasts higher. Simple story: too much milk, weaker Mailbox Prices ahead.

Then Q1 didn’t follow the script.

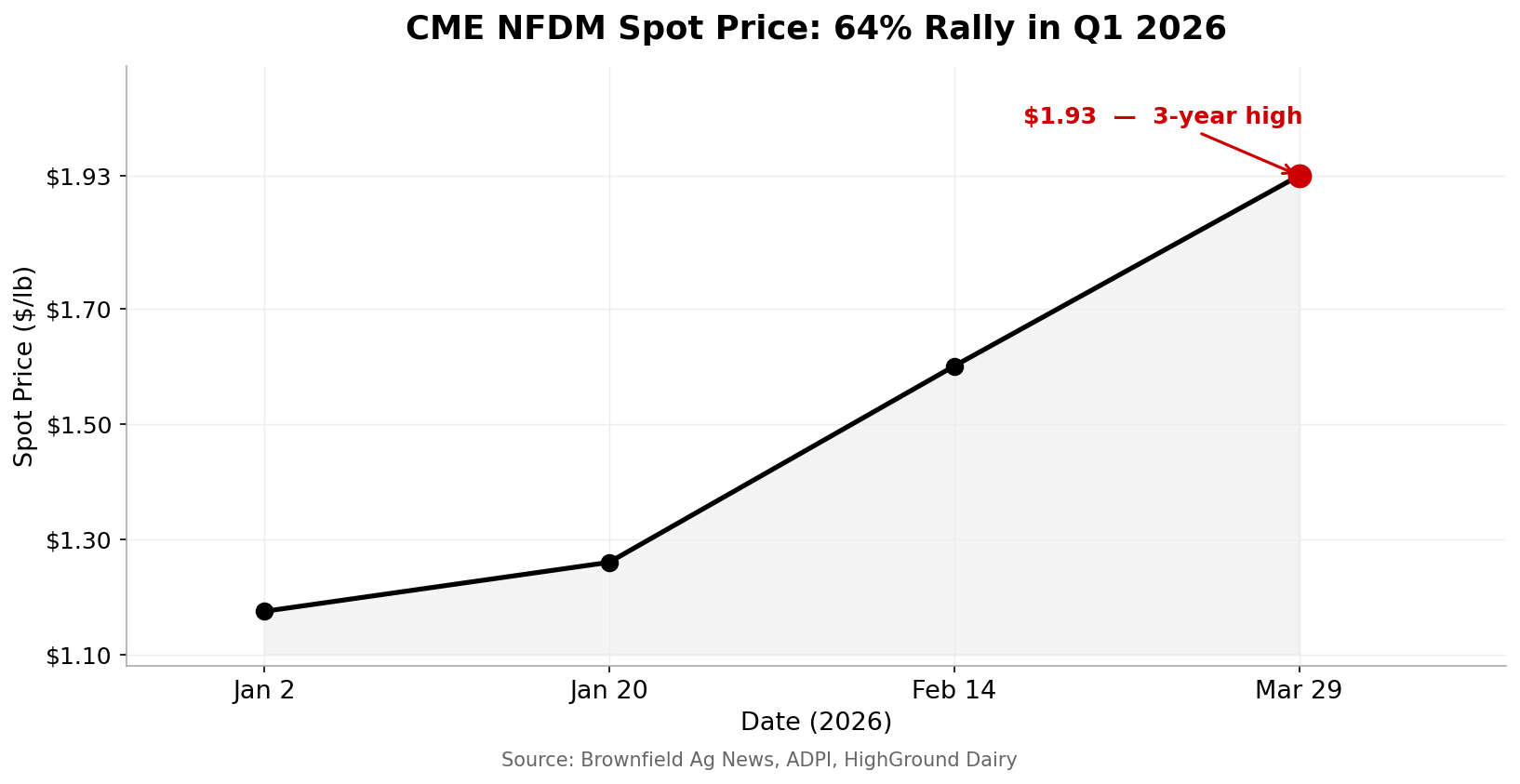

At the first 2026 Global Dairy Trade auction (Event 395), the GDT Price Index jumped 6.3% — snapping a string of declines stretching back to August 2025. A February auction posted another strong gain, driven by whole and skim milk powder. On the Board, CME spot nonfat dry milk opened the year at exactly $1.1750/lb on January 2, according to Brownfield Ag News. By January 20, Federal Order 30 data had it at $1.26/lb. ADPI’s January Dairy Economist Ingredient Outlook confirmed CME NFDM rallied to the mid‑$1.40s by month’s end. By early February, HighGround pegged it at $1.60/lb — a gain of nearly 40% in a matter of weeks. And by March 29, Brownfield had it at $1.93/lb, the highest level since mid‑2022. That kind of move makes you forget what’s sitting on the other side of summer.

On the farm, it finally felt like a break. USDA’s Dairy Margin Coverage program paid out for December 2025 at the $9.50 coverage level — the first and only DMC payment for all of 2025. Cheques improved. Beef calf revenue stayed solid. After a rough 2023–24 stretch, you could almost breathe.

And that’s exactly when the trap tends to spring. The same Q1 that boosted your mailbox also:

- Encouraged some operations to treat 2026 DMC coverage as optional because “things were turning around.”

- Tempted herds to leave Q3 and Q4 completely unhedged, betting the Board would keep climbing.

- Buried the fertilizer bomb — nitrogen climbing 20–40% on the back of the Iran–Hormuz conflict.

- Masked the reality that EU butter and SMP inventories were still elevated, and European weekly milk intakes remained strong.

The market handed you a chance to lock in margins in the top fifth of the last decade, whether you treat that like McCarty did with energy — or like a feel‑good moment that looks great on a Q1 statement and ugly by October — is the question this piece is built around.

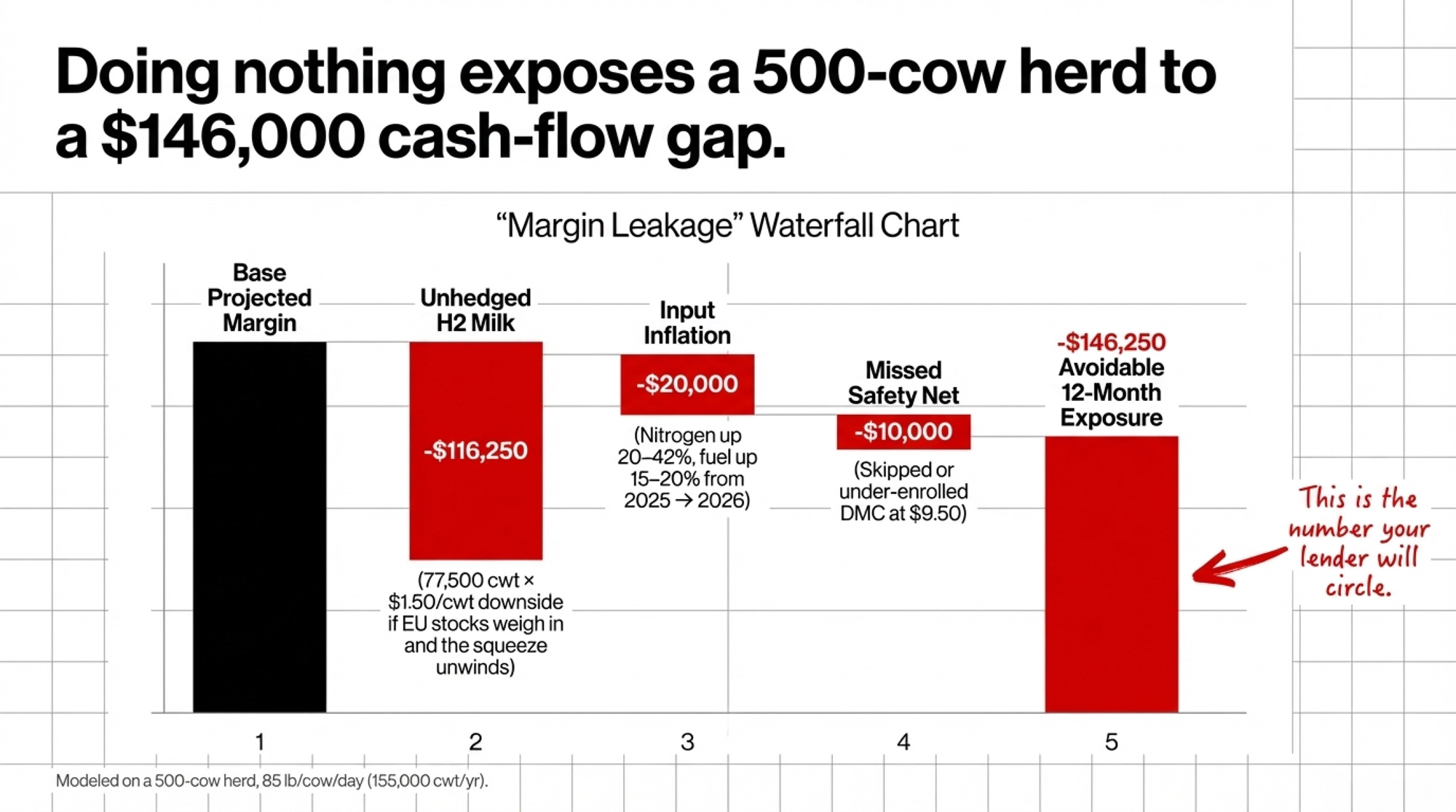

The Quick Math: Where $146,000 Disappears on a 500‑Cow Herd

Here’s the summary for the barn‑aisle scroll. This is a 500‑cow herd, 85 lb/cow/day, roughly 155,000 cwt per year.

| Risk Category | Inputs | Exposure |

| H2 milk revenue left unhedged | 77,500 cwt × $1.50/cwt downside | ≈ $116,250 |

| Fertilizer + fuel inflation (2025 → 2026) | N up 20–40%; fuel up ~15–20% | ≈ $20,000 (illustrative, based on central IL prices) |

| Missed DMC safety net | Skipped or under‑enrolled at $9.50 | ≈ $10,000 (illustrative) |

| Total avoidable 12‑month exposure | ≈ $146,000 |

That’s the gap between “we bought a floor when the math was there” and “we rode it and hoped.” Now let’s walk through the arithmetic.

How Much H2 2026 Milk Should You Lock?

Take that 500‑cow herd. At 85 lb/cow/day, you ship roughly 155,000 cwt per year. The second half alone:

155,000 cwt ÷ 2 ≈ 77,500 cwt in H2.

HighGround’s Q1 update shows forward margins from March onward sitting above the 83rd percentile of the last ten years. That’s the window your risk advisor is waving their arms about. You don’t have to lock every pound — but leaving them all uncovered is a choice with a price tag.

Stay conservative. Assume you could lock an H2 Class III/all‑milk equivalent $1.50/cwt higher than a plausible Q3 downside if EU inventories weigh in and the squeeze unwinds:

77,500 cwt × $1.50/cwt = $116,250

That’s $116,250 of Mailbox Price you could have “on base,” as McCarty would say, if you’d bought a floor while margins were rich. And $1.50/cwt isn’t an edge case. The Board has moved more than that inside a single year, more than once.

[Pro‑Tip] Don’t wait for your DRP agent to call. Pull your own H2 cwt number this week. Multiply by $1.50. Write it down. That’s what you’re wagering by doing nothing.

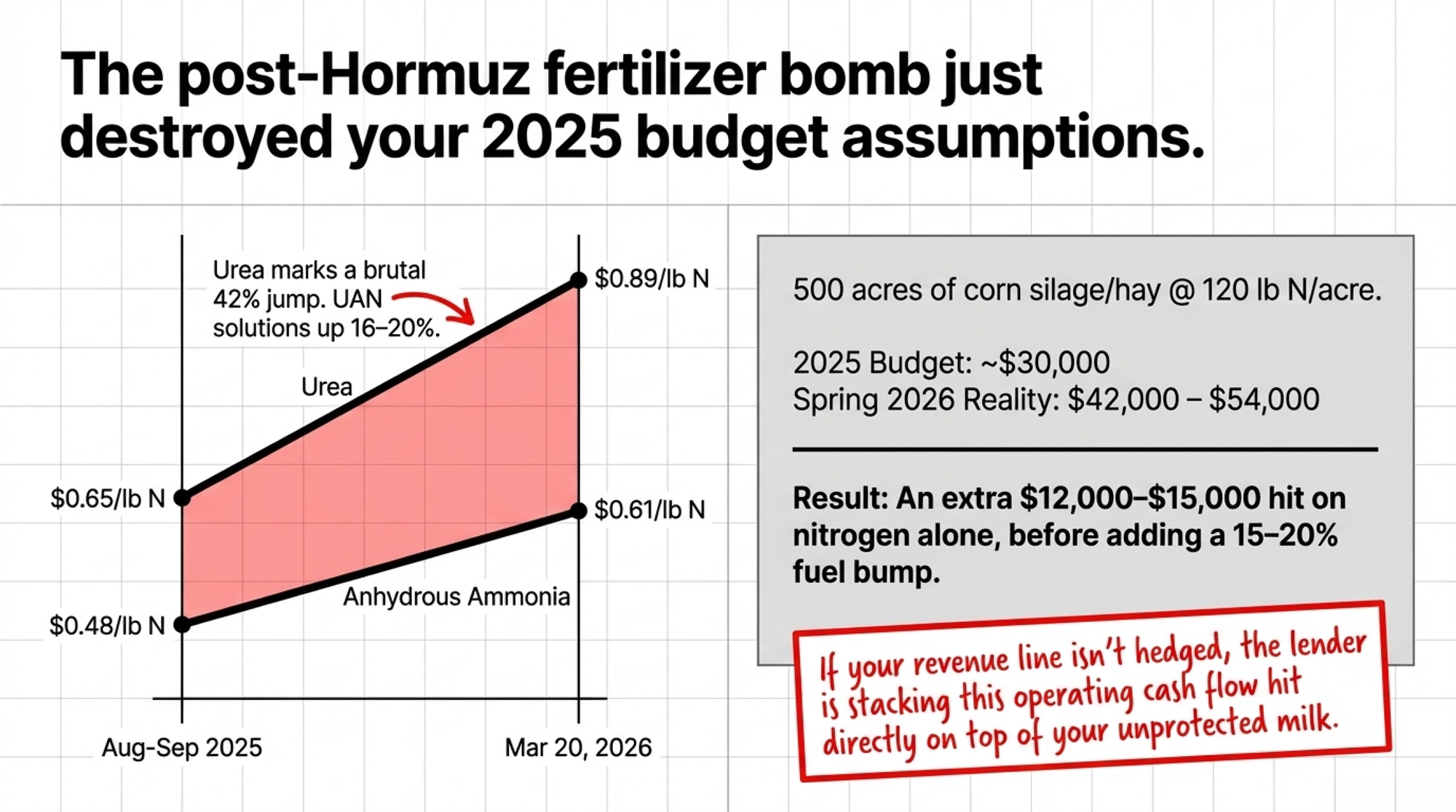

The Fertilizer Bomb After Hormuz

Now stack that revenue risk against your 2026 input reality.

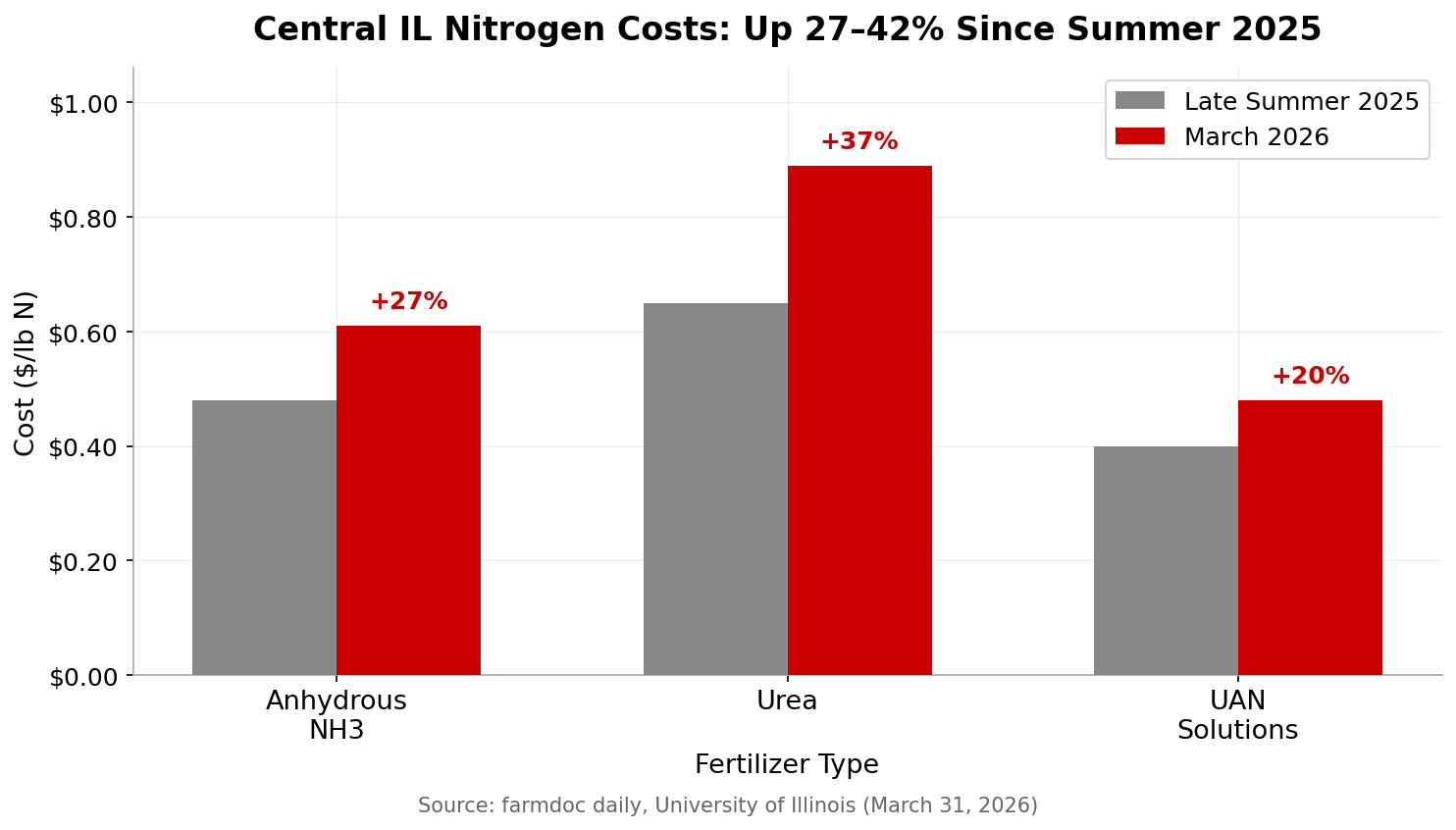

The Iran–Hormuz conflict bottlenecked nitrogen exports from a major urea and ammonia‑producing region. Sulfur shipments — a key feedstock for phosphate fertilizers — snarled, too. University of Illinois’ farmdoc daily analysis (March 31, 2026) tracked how fast that hammered central Illinois prices:

- Anhydrous ammonia: roughly $0.48/lb N in Aug–Sep 2025 → $0.51 in February → $0.61/lb N by March 20, 2026.

- Urea: around $0.65/lb N in late summer 2025 → $0.89/lb N by March 20 — about a 42% jump, the steepest of any major N source.

- UAN solutions: up roughly 16–20% over the same stretch.

For that same 500‑cow herd farming 500 acres of corn silage and hay at ~120 lb N/acre:

2025 N budget: 500 ac × 120 lb N × $0.50/lb N ≈ $30,000

Spring 2026 reality: 500 ac × 120 lb N × $0.70–$0.90/lb N ≈ $42,000–$54,000

An extra $12,000–$15,000 on nitrogen alone. Layer on phosphate, potash, and a 15–20% fuel bump on a dairy burning 6,000+ gallons per month, and you’re conservatively in the $20,000 neighbourhood of additional 2026 cash cost. Those N numbers are central Illinois; your local market may differ, but the direction has looked similar across most U.S. regions.

[Lender’s View] Your lender sees that ,000 fertilizer gap as a direct hit to operating cash flow — and if your revenue line isn’t hedged, they’re stacking it on top of the unprotected milk. That’s how a “good year” turns into a covenant conversation.

The Safety Net You May Have Skipped

Brownfield reported on February 23 that 2026 DMC enrollment would close on February 26. Dairy Herd’s “11th‑Hour Trigger” coverage confirmed that December 2025’s margin triggered a payment at the .50 level — the lone DMC cheque for all of 2025. Producers who’d locked coverage when things looked worst saw real money early in 2026.

Those who watched the Q1 rally and figured “maybe we don’t need this” risked missing the only meaningful safety‑net payment of the year. On a 500‑cow herd, even a modest DMC payout reaches into five figures once you multiply per‑cwt across shipped volume. We’ll use roughly $10,000 as an illustrative figure — your actual number depends on your coverage tier and pounds.

What Actually Drove the Board — and Why It Probably Won’t Drive Q3

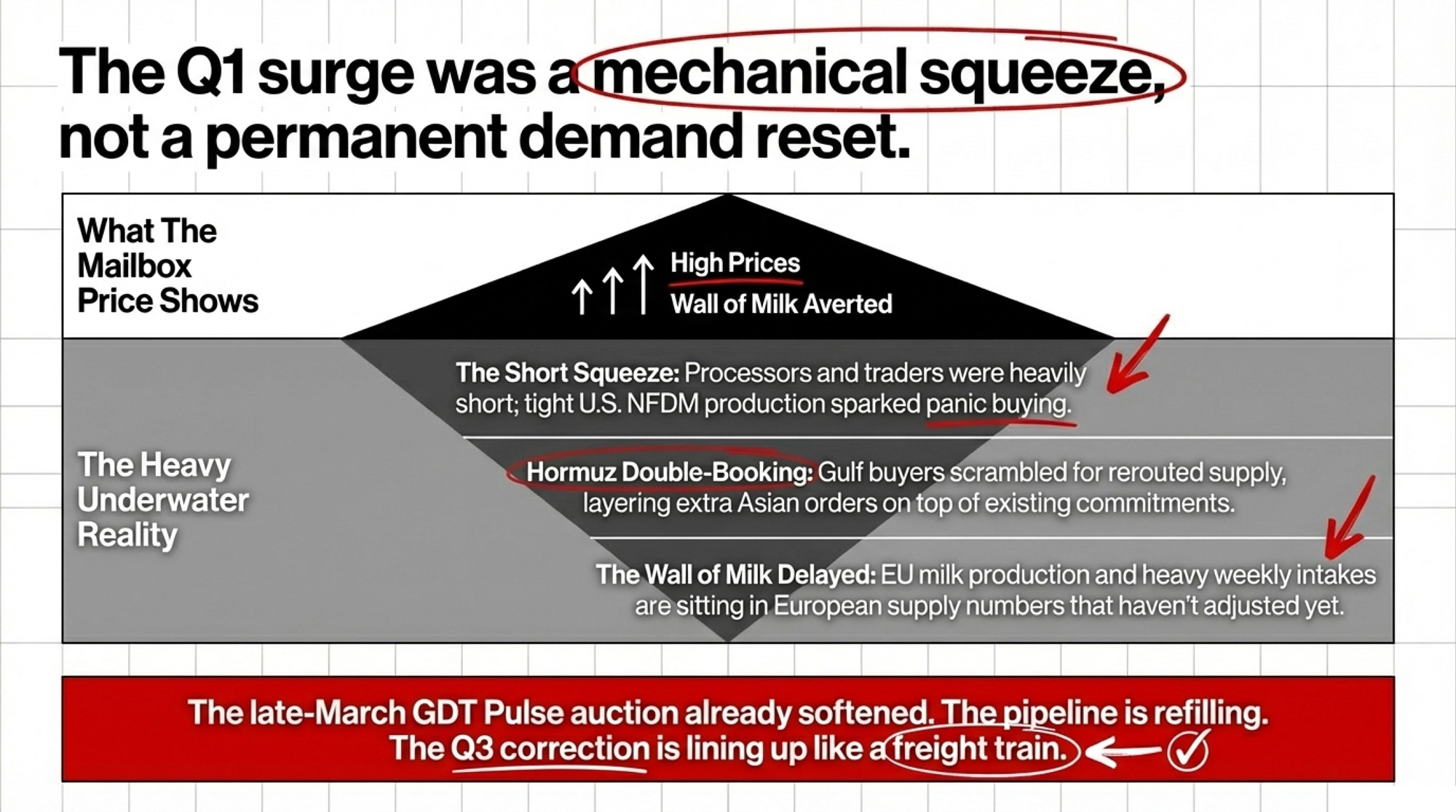

The Q1 surge wasn’t “strong demand” in the way a rising Mailbox Price implies. There were too many shorts and too many late buyers crammed into the wrong side of the trade at the same time.

Coming into 2026, processors and traders were heavily short, counting on the wall‑of‑milk story to keep the Board pinned. End users had taken minimal forward coverage. Non‑China importers had already stepped up powder purchases in late 2025 when prices were weak. When tight U.S. NFDM production — after two years of milk shifting toward cheese and high‑protein ingredients — left less powder available than anyone had modeled, shorts scrambled. Buyers scrambled. Short‑covering stacked on top of real demand pushed prices higher.

Then Hormuz blew up. Gulf buyers scrambled for rerouted supply. Analysts report that some Asian buyers waiting on delayed European products turned to the U.S. and New Zealand to avoid running short, effectively layering extra orders on top of existing commitments. That double‑booking created a temporary demand bulge on top of the short squeeze — the kind of pattern that lifts a GDT index 6–7% in one event and then fades once the pipeline refills.

By late March, the GDT Pulse auction had already softened. EU butter prices eased. Reports across Europe described butter and SMP stocks as significantly higher year‑over‑year. Rabobank’s Q1 2026 Global Dairy Quarterly, summarized by AHDB, suggested EU milk production may contract about 0.9% in the second half — but emphasized the lag between lower farmgate prices and actual volume response.

The Q3 correction is lining up like a freight train, and a lot of herds are standing on the tracks with a Q1 smile. The wall of milk didn’t crash into Q1 the way early bears predicted. But it didn’t vanish, either. It’s sitting in European supply numbers that haven’t adjusted yet. If panic buying fades, Gulf shipping normalizes, and EU intake stays firmer than models expect, the mechanical rally that saved your Q1 Mailbox Price sets you up for an H2 where Class III and IV give back part of the gains.

The only part of your revenue that holds up is the part you already took off the table. That’s the setup McCarty’s risk plan was built for. Not market timing. Just getting on base before the pitch changes.

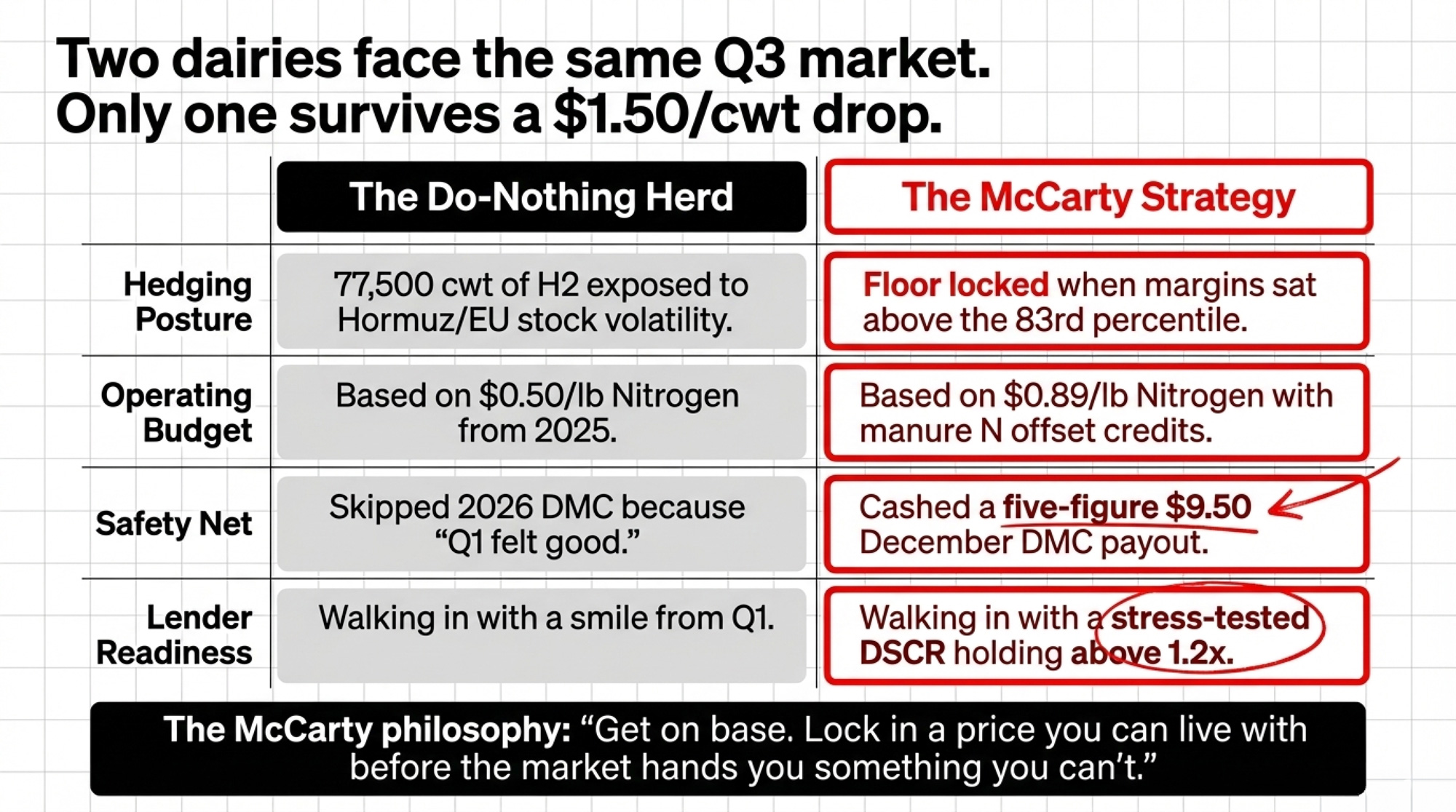

McCarty’s Singles and Doubles vs. the “Do Nothing” Herd

McCarty’s approach isn’t clever. It’s a risk philosophy that survives cycles. His family took a long‑term view with their processor to stabilize key costs — energy, feed, equipment — years in advance. Not flashy. Deliberate. When diesel blew up in 2022, they weren’t scrambling. They were executing a plan they’d already paid for.

Right now, a lot of 500‑cow operations are in the opposite position:

- Q1 felt good, so 2026 DMC got treated as a “maybe.”

- DRP and forward contracts are sitting on the “we really should call our agent” list.

- Fertilizer and fuel are budgeted off 2025 numbers, not current March 2026 quotes.

One operation walks into their lender meeting with DRP confirmations, and a fertilizer pre‑buy that proves H2 floor revenue covers term debt even in a stress case. Another walks in with a smile from Q1, a budget using last year’s N prices, and 77,500 cwt of H2 production exposed to whatever EU butter stocks and Hormuz do next.

Same rally. Very different December.

| Metric | Hedged Operation (McCarty Model) | Unhedged Operation (“Do Nothing”) |

|---|---|---|

| H2 2026 Milk Floor ($/cwt) | Locked ~$19.50–$20.00 via DRP floors at 83rd-pct margins | Riding spot — exposure to $1.50+/cwt downside if Board corrects |

| Q3/Q4 Volume Protected | 40–60% of 77,500 cwt (~31,000–46,500 cwt) | 0 cwt — fully exposed to market move |

| 2026 Nitrogen Budget ($/lb N) | Current quotes: $0.70–$0.89/lb (anhydrous/urea blend) | 2025 budget: ~$0.50/lb — understated by 40%+ |

| Fertilizer Cash-Flow Gap | ~$0 — pre-bought or properly budgeted | ~$12,000–$15,000 underfunded on N alone |

| DMC Enrollment Status | $9.50 coverage confirmed before Feb 26 deadline | Skipped — “things were turning around” |

| H2 DSCR (Stress Case) | Holds at 1.2x+ even if Board gives back $1.50/cwt | May fall below 1.2x — covenant conversation risk |

| Lender Meeting Posture | Walks in with DRP confirmations + updated budget | Walks in with Q1 smile and 2025 numbers |

| December 2026 Outcome | Stable margins; singles and doubles locked in | Six-figure exposure if Q3 correction materializes |

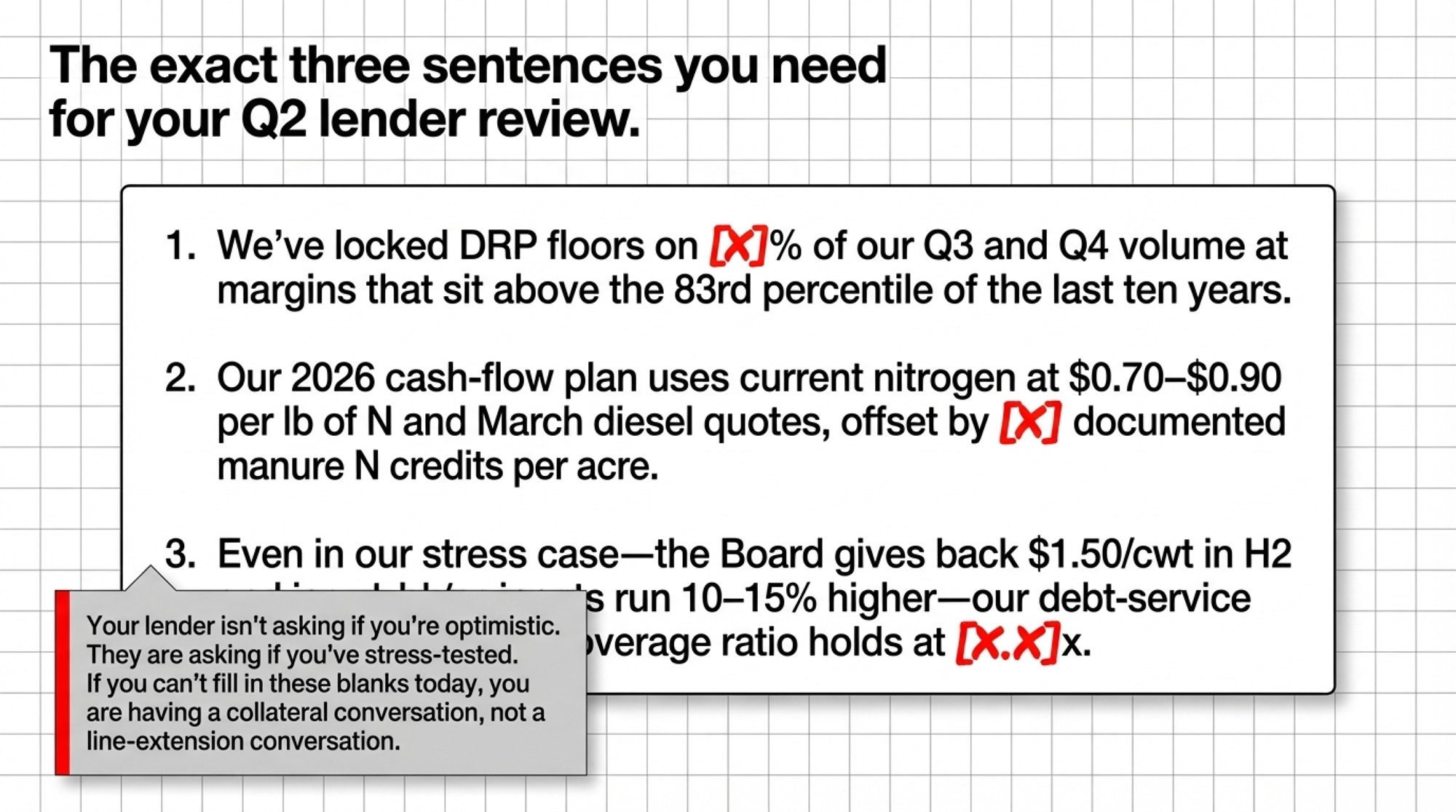

Three Sentences to Bring to Your Lender

The headline promises lender math. Here’s how to deliver it in your Q2 review. Walk in with your numbers already run and say:

Sentence 1: “We’ve locked DRP floors on [X]% of our Q3 and Q4 volume at margins that sit above the 83rd percentile of the last ten years, based on HighGround’s Q1 producer update.”

Sentence 2: “Our 2026 cash‑flow plan uses current nitrogen at $0.70–$0.90 per lb of N and March diesel quotes — not 2025 numbers — and we’ve offset part of that with documented manure N credits per acre.”

Sentence 3: “Even in our stress case — the Board gives back $1.50/cwt in H2 and inputs run another 10–15% above current — our debt‑service coverage ratio holds at [X.X]x.”

[Lender’s View] Your lender isn’t asking whether you’re optimistic. They’re asking whether you’ve stress‑tested. These three sentences — backed by actual confirmations and an updated budget — tell them you have. That’s the difference between “extending your line” and “let’s talk about your collateral.”

If you can’t fill in those blanks today, that’s the problem this article is about.

The 30/90/365‑Day Playbook

| Action Item | Deadline/Window | Risk if Skipped | Priority |

|---|---|---|---|

| Buy DRP floors on 40–50% of H2 volume | Next 30 days (while margins at 83rd pct) | $116,250 unprotected milk revenue (500-cow herd) | 🔴 Critical |

| Rebuild 2026 input budget with current quotes | Next 30 days | $12–15k+ fertilizer gap; lender sees 2025 numbers | 🔴 Critical |

| Run manure N credits with agronomist | Next 30 days | Miss $30–45/acre savings (up to $13,500 on 300 ac) | 🟠 High |

| Build base + stress H2 margin sheet (DSCR) | Next 90 days | Don’t know if stress DSCR < 1.2x until lender flags it | 🟠 High |

| Ask processor 3 blunt questions (milk end-use) | Next 90 days | Shipping into a plan you don’t understand | 🟠 High |

| Drop bottom-protein bulls; tighten sire stack | Next 90 days | Calving volume-heavy heifers into 2028 component market | 🟠 High |

| Cull by protein yield; deploy beef semen on tail | Next 365 days | Herd drifts away from cheese-yield premium | 🟡 Medium |

| Align risk calendar to DRP sales/DMC deadlines | Ongoing | Buy protection when desperate, not when optimal | 🟡 Medium |

| Basis + alternatives review before contract renewal | Next 365 days | Miss co-op leverage window or consolidation shift | 🟡 Medium |

You won’t fix all of this in one phone call. But you can move from “hoping” to “protecting” over the next year.

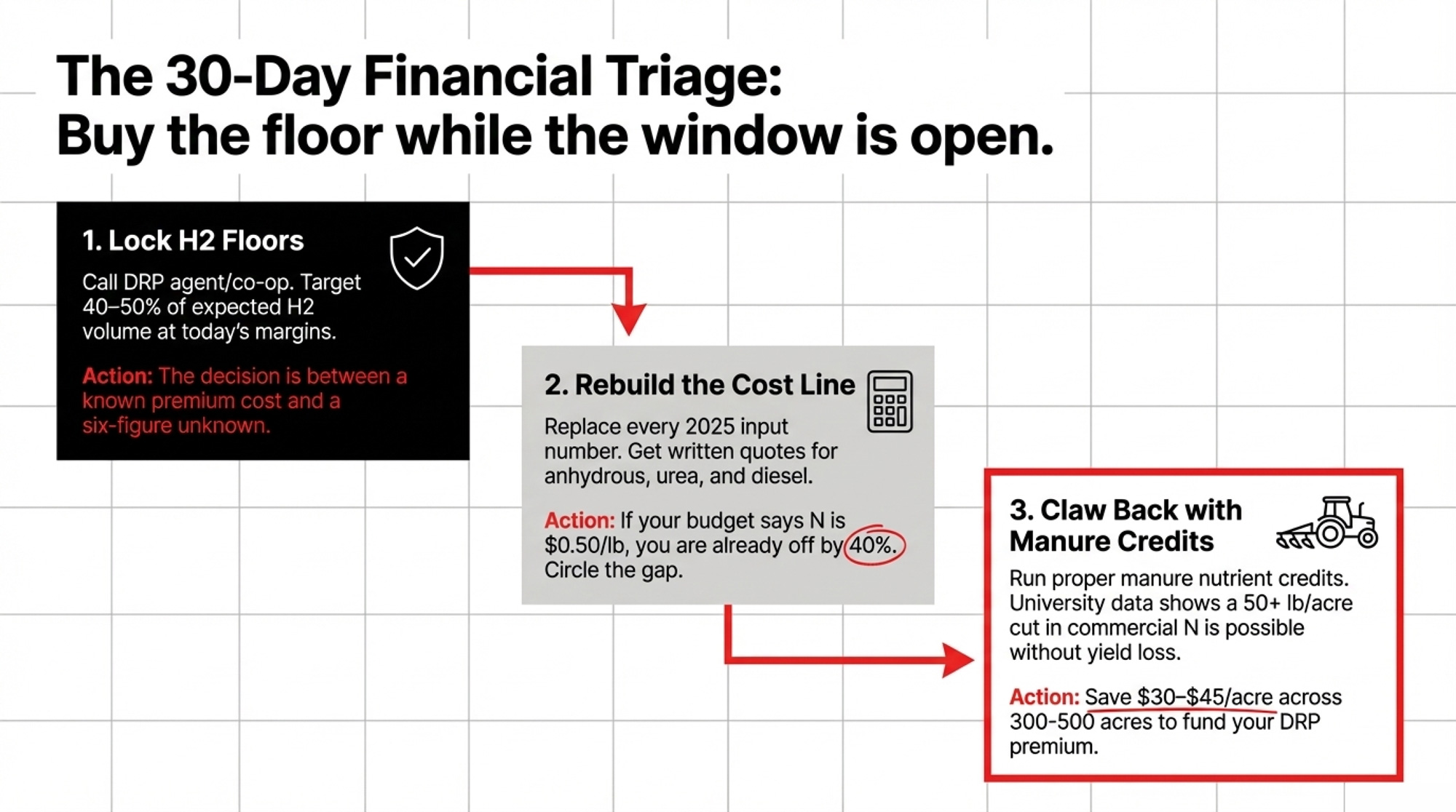

Next 30 Days

1. Buy a floor under a meaningful chunk of your H2 milk. Call your DRP agent or co‑op risk advisor and get Q3/Q4 quotes. Target at least 40–50% of expected H2 volume at today’s margins. If your cheque is heavily component‑based, look at the component blend option so your hedge matches your actual milk. DRP isn’t free — you’re paying a premium or giving up upside. But the decision right now is between a known cost and a six‑figure unknown.

2. Rebuild your 2026 cost line with current quotes. Get written nitrogen quotes for anhydrous, urea, and UAN at current $/lb N. Pull current diesel offers. Replace every 2025 input number in your cash‑flow plan. Circle the gap. If your 2026 budget still shows N at $0.50/lb, you’re already off by 20–40%.

3. Use manure N to claw back some of that increase. Have your agronomist run a proper manure nutrient credit for each field getting manure. University and extension work show farms with real nutrient management plans can cut commercial N by 50+ lb/acre on some fields without losing yield, which at current N prices saves $30–$45/acre. Across 300–500 acres, that’s enough to fund a chunk of your DRP premium.

[Pro‑Tip] Run all three before your Q2 lender review. Walking in with DRP confirmations, updated N quotes, and a manure credit plan is the difference between asking for patience and proving a plan.

Next 90 Days

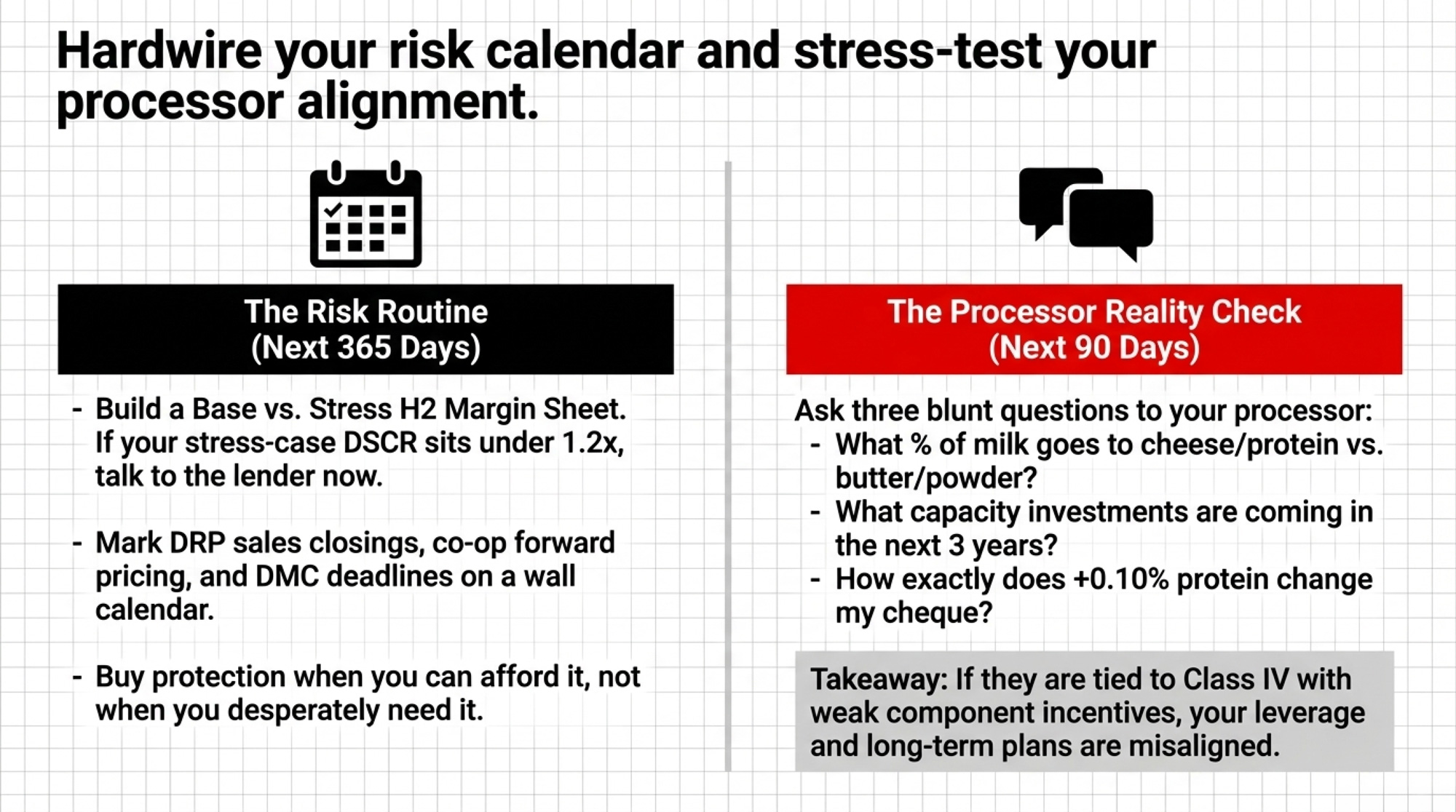

4. Build a base vs. stress H2 margin sheet. July–December, two columns: base case (hedged floor + updated 2026 inputs) and stress case (same floors + another 10–15% on feed/fertilizer/fuel). Calculate a rough debt‑service coverage ratio in both. If your stress‑case DSCR sits under about 1.2x, have that conversation with your lender before numbers tighten — not after.

5. Ask your processor three blunt questions. What percentage of your milk ends up in cheese and protein ingredients versus butter and powder? What cheese and high‑protein capacity investments are they making over the next three years? If you bring them milk that’s +0.10% protein and +0.15% fat, what does that do to your cheque? If the answers show they’re structurally tied to Class IV butter/powder with weak component incentives, you’ve learned your long‑term plans, and theirs may not be aligned — and that’s a conversation you can’t keep deferring.

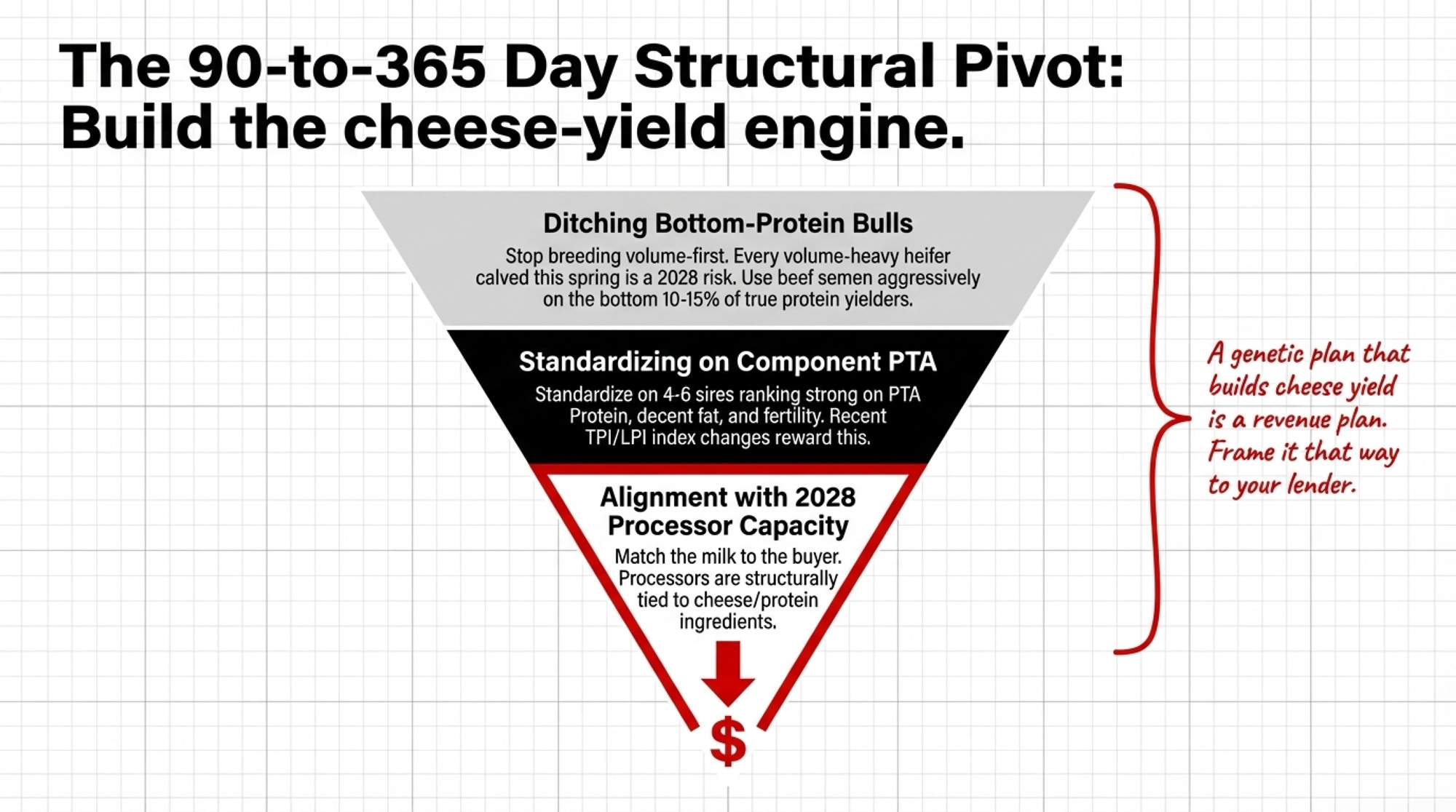

6. Build the cheese‑yield engine — starting with your sire stack. If your herd isn’t building the cheese‑yield engine of 2028, you’re breeding further out of line with a market that’s paying for protein and cheese yield, not liters. Every volume‑only heifer you calve this spring pushes you in the wrong direction in a Q3 2026 market that rewards components. Drop the bottom protein bulls. Standardize on 4–6 sires that rank strong on PTA Protein, decent fat, and good fertility. Recent TPI and Canadian LPI index changes increased the protein’s weight because processors and pricing structures are doing the same.

[Lender’s View] Your lender may not care which bull you use. But they absolutely care whether your revenue per cwt is trending toward or away from what your processor actually pays premiums for. A genetic plan that builds cheese yield is a revenue plan — frame it that way.

Next 365 Days

7. Cull with composition in mind. Use 12‑month test‑day data to flag cows in the bottom 10–15% for true protein yield. Let low protein be the tiebreaker when you’re on the fence. Use beef semen aggressively on genetic bottom‑end cows. You’re ratcheting the herd toward the milk your best buyers pay best for — one breeding decision at a time.

8. Align your risk calendar to your cash‑flow pinch points. Mark DRP quarterly sales closing dates, co‑op forward pricing windows, and DMC enrollment deadlines on a wall calendar — with your own “two weeks before” internal target for each. Buy protection when you can afford it, not when you desperately need it and can’t.

9. Run a basis and alternatives review before your next contract renewal. Have an advisor compare what you’ve actually received — net of hauling and premiums — versus what you’d get from a more component‑friendly buyer within realistic hauling distance. Part of that review: understand where the consolidation window is heading for your region and your processor. The leverage you have today isn’t guaranteed tomorrow.

What This Means for Your Operation

- If you’re running 400–600 cows and haven’t locked any Q3/Q4 milk, roughly half your H2 volume is exposed to the kind of $1.50/cwt downside this article walked through. Pull your own H2 cwt, multiply by $1.50, and decide if you can absorb that hit without changing plans.

- If your 2026 budget still uses 2025 nitrogen and fuel prices, you’re planning with the wrong year. Update those line items this month. If the gap exceeds one good month of milk cheques, your cash‑flow plan needs surgery — not a Band‑Aid.

- If your co‑op can’t clearly explain how your milk fits their cheese and high‑protein strategy, you’re shipping into a plan you don’t fully understand. You don’t have to jump ship — but you need to know how much of your 2028 Mailbox Price depends on their capacity bets, not yours.

- If your stress‑case H2 DSCR comes in under ~1.2x, your lender sees you as tight. Walk in with proof you’ve acted — DRP floors, updated budgets, manure credits — not just a good attitude.

- If you’re still breeding volume‑first and protein‑second, every volume‑heavy heifer you calve this spring is a 2028 risk. Changing bulls and tightening culling is the cheapest way to start building the cheese‑yield engine. Low‑debt operations with strong cost structures may have more room to stay partially uncovered — but even they should be running the stress case, not just assuming the Q1 rally is the new normal.

- Your 30‑day check: Pull your projected H2 2026 milk volume (cwt). Multiply by $1.50/cwt. Write that number next to your updated 2026 fertilizer + fuel increase. That spread is what you’re betting on if you do nothing. Now try filling in the three blanks from the lender script above.

Key Takeaways

- Unhedged H2 milk plus outdated input budgets is a six‑figure bet that the Q1 rally was more than a mechanical squeeze. Very few 500‑cow herds can afford to be wrong on that bet twice.

- DRP and DMC are the difference between having a floor under your Mailbox Price when Q3 softens and hoping the Board doesn’t move too fast. Skipping them in 2026 is a cash‑flow decision, not a paperwork decision.

- Aligning genetics toward protein isn’t optional anymore. The herds that start building for cheese yield now see it in 2027–2028 cheques. The herds that don’t stay aligned with a slower‑growing, lower‑value part of the market.

- Your lender’s question six months from now won’t be “Did you enjoy the rally?” It’ll be: “What floors did you buy, how does your DSCR hold in a stress case, and what’s your plan if the Board gives back $1.50 by October?”

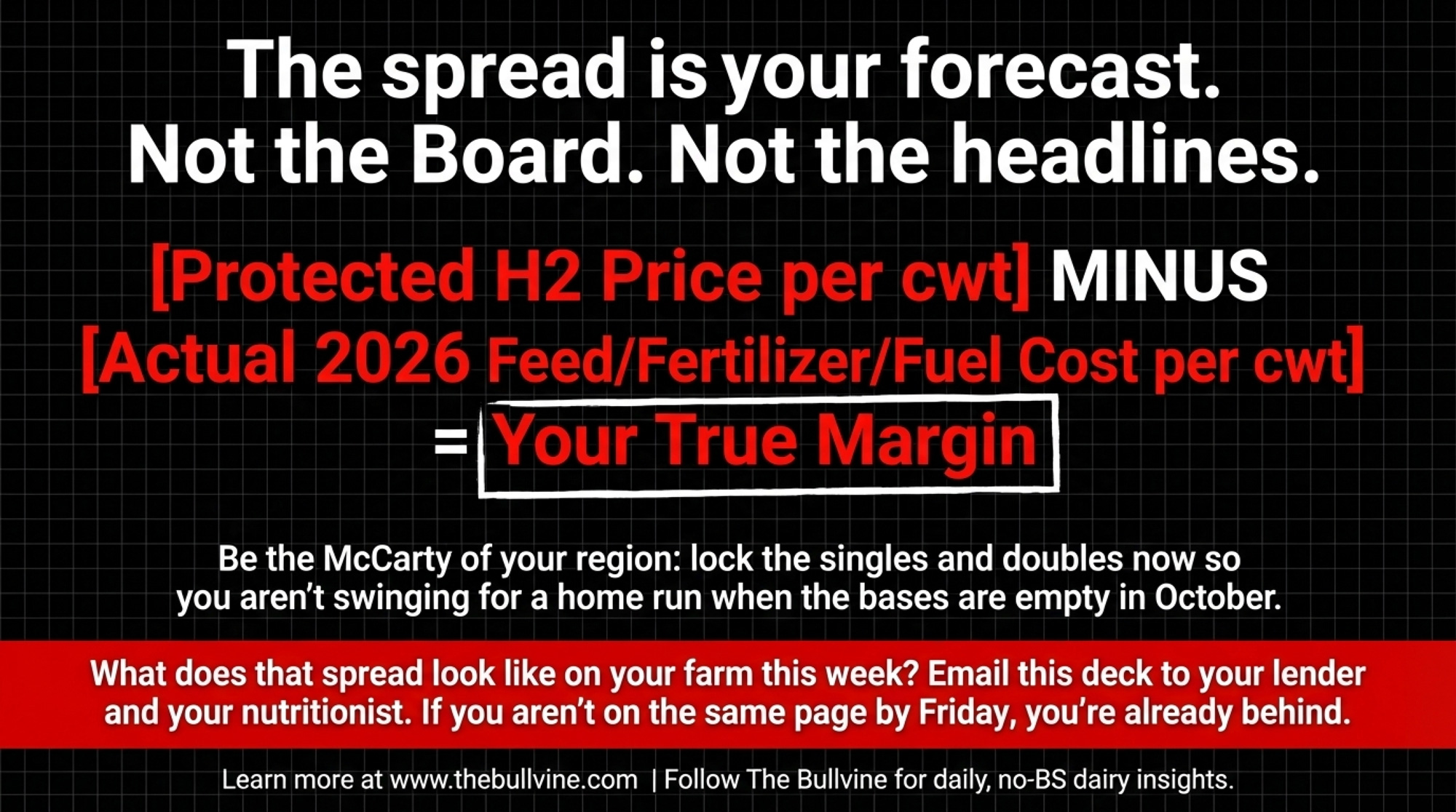

The Q1 2026 rally gave you something real — not just better cheques, but a window to lock H2 margins at top‑20% levels while everyone else was still smiling at the Board.

Before that window closes, pull two numbers: your protected H2 milk price per cwt and your actual 2026 feed + fertilizer + fuel cost per cwt based on this month’s quotes — not last year’s. Put them side by side. That gap is your forecast. Not the Board. Not the headlines. Not the feeling you got when that Q1 cheque hit.

Be the McCarty of your region: lock the singles and doubles now so you aren’t swinging for a home run when the bases are empty in October.

What does that spread look like on your farm this week?

Email this to your lender and your nutritionist. If you aren’t all on the same page by Friday, you’re already behind.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $15,800 DMC Wake-Up Call: Tier 1 Just Jumped to 6 Million Pounds. Don’t Sign ‘Same as Last Year’ – Arms you with a high-impact checklist to exploit the new 6-million-pound Tier 1 cap. Reveals how simple structural shifts in your DMC enrollment can trigger five-figure premium savings while maximizing your 2026 safety net payments.

- 2026 Dairy Rally Or Dead-Cat Bounce? The Risk and Margin Math Behind Today’s Wall of Milk – Exposes theunderlying global supply pressure that threatens to collapse current price gains. Delivers the strategic foresight needed to distinguish between a fundamental market reset and a temporary short squeeze, securing your operation’s long-term positioning.

- Bred for $3 Butterfat, Selling at $2.50: Inside the 5-Year Gap That’s Reshaping Genetic Strategy – Breaks down the critical ROI disconnect between today’s breeding decisions and future mailbox prices. Reveals why shifting to a “cheese-yield engine” is mandatory to outpace the 2025 Net Merit formula changes and protect your 2028 checks.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.