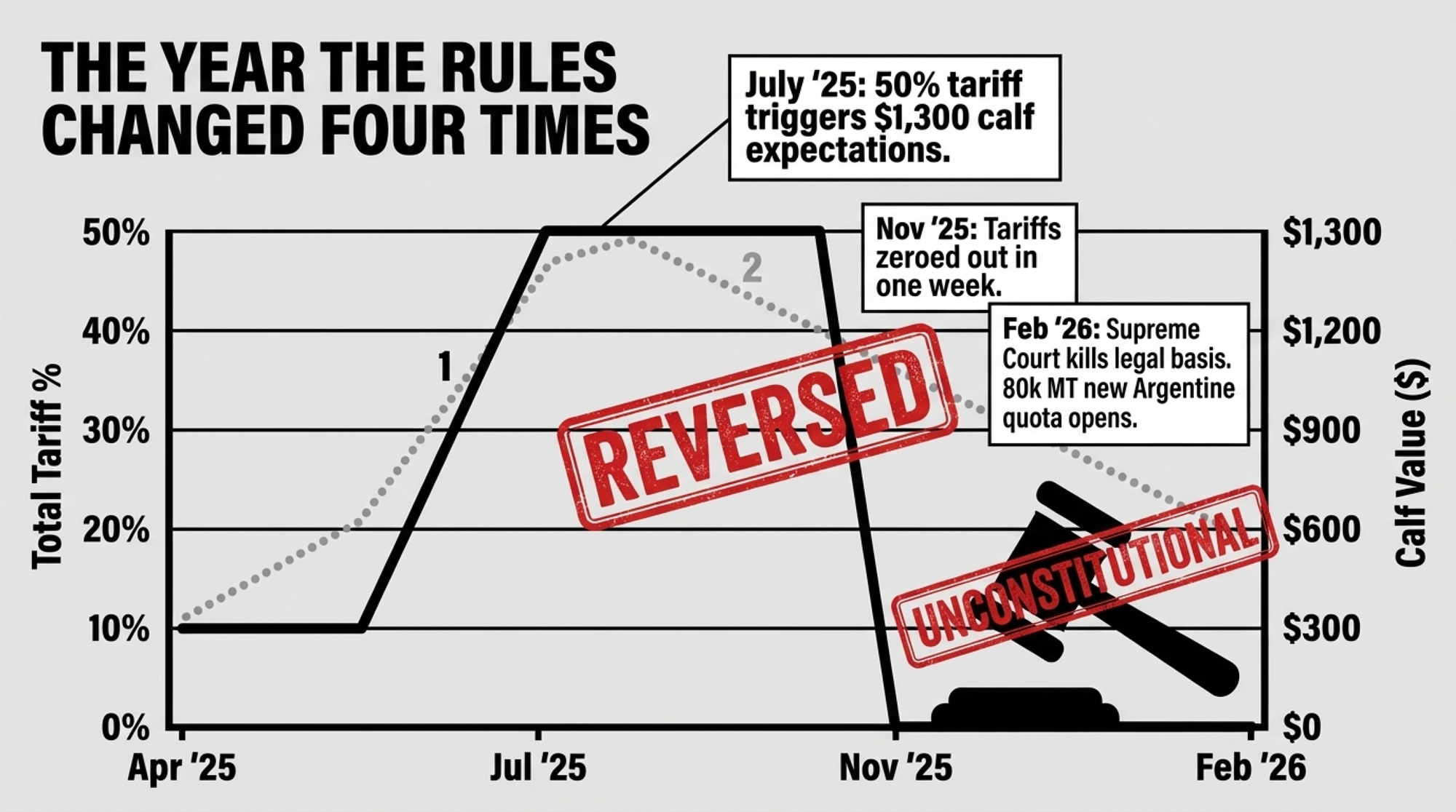

A 50% tariff on Brazil lasted a few months. The White House rolled it back within a week, the Supreme Court struck down the law behind it, and then the administration opened 80,000 more metric tons of quota for Argentina. Your calf plan didn’t get a vote any of those times.

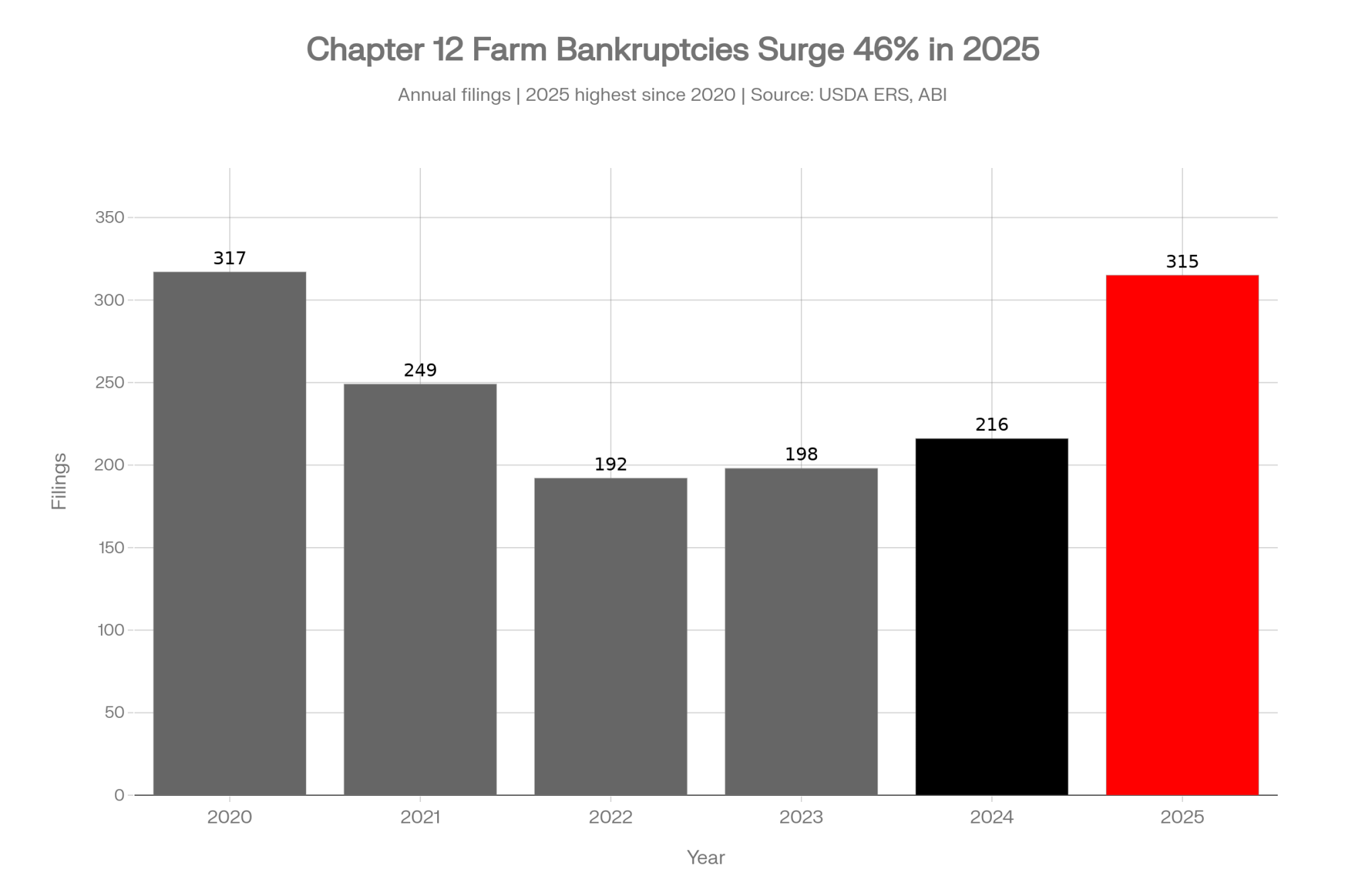

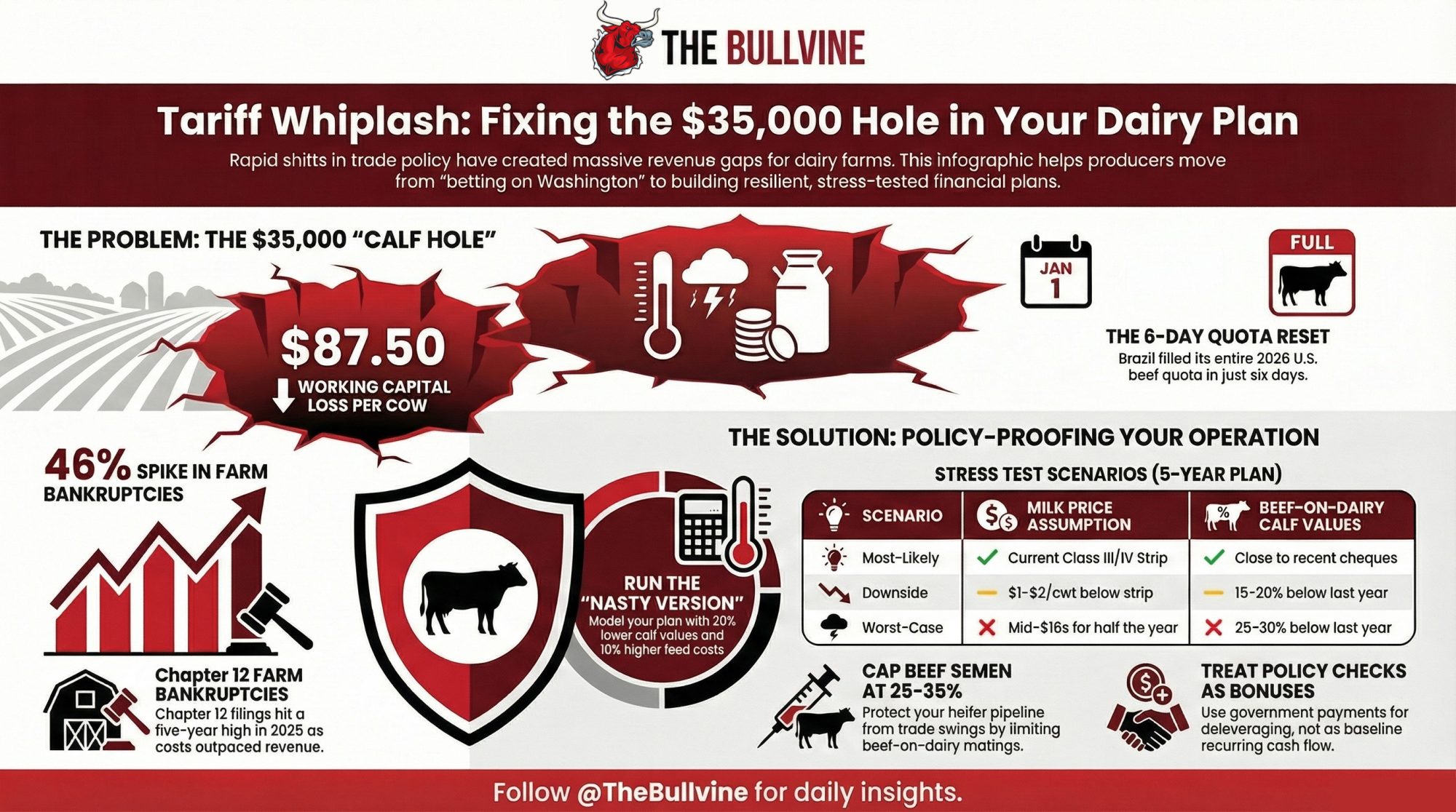

Executive Summary: A 50% tariff on Brazilian beef lasted from July to November 2025 — then both layers vanished in a single week, the Supreme Court ruled the legal basis unconstitutional, and the White House responded by opening 80,000 metric tons of new duty-free Argentine beef quota. For a 400-cow dairy running 35% beef-on-dairy breedings, that whiplash opened a $35,000 hole in annual calf revenue — $87.50 per cow in working capital your lender won’t ignore. Brazil filled its entire 2026 U.S. quota in six days. The domestic herd sits at 94.2 million head, the lowest mid-year count since 1973, and Chapter 12 farm bankruptcies hit 315 last year — up 46%. JBS co-owner Joesley Batista got a private White House meeting weeks before the exemptions; your banker got a stress test that no longer assumes any tariff protection will return. If your five-year plan only works at last year’s calf prices, you don’t have a plan — you have a bet that Washington will keep a promise it’s already broken three times in eight months.

On a humid July night in 2025, a 400‑cow dairy in central Wisconsin sat at the kitchen table with the banker and finally saw a little daylight.

Trump had just stacked a 40% emergency tariff on top of an existing 10% reciprocal duty on Brazilian imports — beef included — bringing the total tariff on Brazilian beef to 50%. Calf buyers were talking about tight supplies. Four‑figure beef‑on‑dairy cheques didn’t feel like lottery tickets anymore. They felt like something you could cautiously build a plan around.

So the yellow pad on the table assumed about 140 beef‑cross calves at roughly 1,300 dollars a head — somewhere around 182,000 dollars a year in gross calf revenue. That kind of number is plausible in a market where 600‑ to 650‑pound beef‑on‑dairy steers were bringing 269–272 dollars per hundredweight in 2024 video auction data, and 2025 feeder calf prices were running about 15% higher than the year before.

The new barn note looked tight, but doable, as long as those calf numbers held.

By November, both tariff layers were gone. By February 2026, the Supreme Court made sure they couldn’t come back the same way — and the White House responded by opening even more duty‑free quotas for imported beef. That same producer is back at the kitchen table, explaining why the math no longer works.

The Year the Rules Changed Four Times

Here’s how fast the ground beneath your calf cheque moved.

- April 2, 2025: Executive Order 14257 slaps a 10% reciprocal tariff on most imports into the U.S., including beef, while exempting Canada and Mexico under USMCA.

- May 11, 2025: USDA halts all cattle imports from Mexico after detecting New World screwworm — a parasitic fly that kills livestock by feeding on living tissue. The ban further squeezes domestic feedlot supply.

- June 12, 2025: JBS — the Brazilian meat giant that already processes a big share of U.S. beef — completes a dual listing on the NYSE and Brazil’s B3.

- July 1, 2025 context: USDA reports the U.S. cattle inventory at 94.2 million head — the lowest mid‑year count on record in data going back to 1973, down 8 million head from 2020. The 2025 calf crop comes in at 32.9 million head, a record low for the second straight year.

- July 30, 2025: Executive Order 14323 uses national‑emergency powers to add a 40% tariff on Brazilian goods, including beef. Total duty on Brazilian beef: 50%. The move is sold as a way to protect American agriculture.

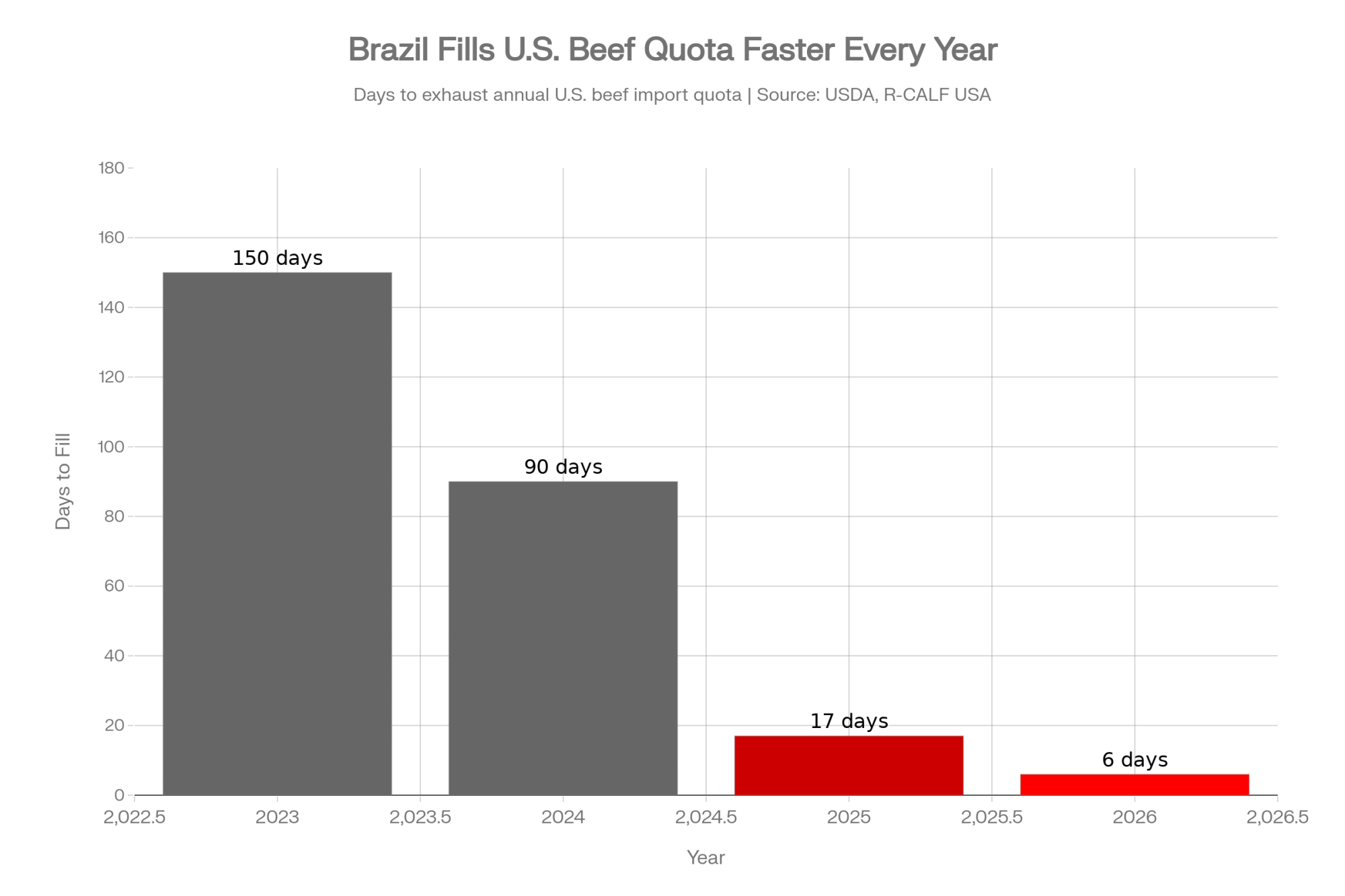

- August 2025: R‑CALF USA urges Washington to suspend Brazilian beef imports entirely, pointing to Brazil filling its entire 65,000‑ton “other countries” quota in just 17 days at the start of the year.

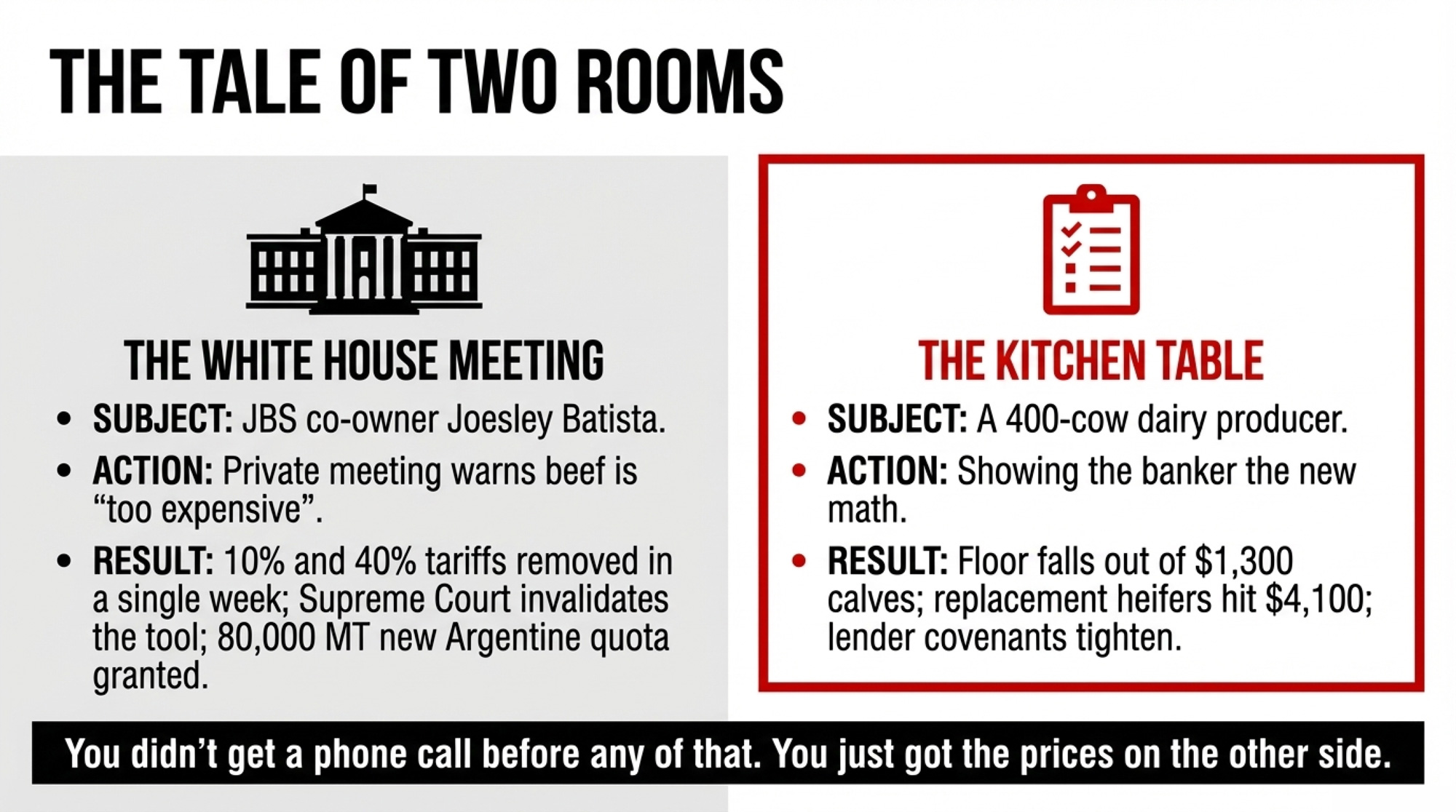

- Late September 2025: Reuters reports that JBS co‑owner Joesley Batista — whose company admitted in Brazilian plea deals to bribing roughly 1,800 politicians — gets a private meeting with President Trump. Sources familiar with the meeting say Batista warned the tariffs were making beef “too expensive” for consumers.

- ~November 14, 2025: An executive action removes reciprocal tariffs on 200‑plus agricultural products not deemed sufficiently produced in the U.S., including beef.

- November 20, 2025: A second order removes the remaining 40% Brazil‑specific duty on beef and other ag goods, retroactive to November 13, with refunds available on duties collected in between. In less than a week, Brazilian beef goes from a 50% combined tariff to zero additional duty beyond the normal quota structure.

- February 6, 2026: Trump signs a proclamation titled “Ensuring Affordable Beef for the American Consumer,” temporarily increasing the U.S. beef tariff‑rate quota by 80,000 metric tons for calendar year 2026 — allocated entirely to Argentina, in four quarterly tranches of 20,000 MT each starting February 13. The proclamation cites ground beef hitting $6.69 per pound in December 2025, the highest since the BLS started tracking beef prices in the 1980s.

- February 20, 2026: The U.S. Supreme Court rules in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose tariffs, invalidating the legal basis for both the 10% reciprocal and 40% Brazil‑specific tariffs entirely. The same day, Trump issued an executive order ending the collection of all IEEPA duties.

- February 24, 2026: A new 10% global surcharge under Section 122 of the Trade Act of 1974 takes effect as a stopgap — but beef is explicitly exempted via the Annex II exceptions list, along with other agricultural products. Section 122 is capped at 150 days and expires July 24, 2026, unless Congress extends it.

R‑CALF CEO Bill Bullard didn’t hide his frustration. In a November 2025 statement, he called U.S. cattle producers “beleaguered” and said decades of failed trade policy had “driven hundreds of thousands” of ranchers out of business. He argued that the 10% reciprocal tariff plus the 40% Brazil‑specific duty were “important first steps” toward fixing that imbalance.

Both steps got wiped out in a week. A few months later, the court took the whole tool off the table — and the White House added 80,000 metric tons of Argentine beef quota on top of it.

What Happened After the Exemptions Tells You Everything

The ink on the November exemptions was barely dry before Brazilian exporters moved. Authorized Brazilian meatpackers quickly resumed full shipments. According to Valor International, November exports hit about 12,600 tonnes despite only around ten tariff‑free days on the calendar. Volumes were projected at 35,000 tonnes for December and 50,000 tonnes for January as the duty‑free quota reset. Brazil exported 244,500 tonnes to the U.S. from January through November 2025, already surpassing full‑year 2024 totals.

Brazil then filled its 2026 U.S. beef quota within six days of the start of the new trading year. By the USDA weekly report ending January 12, Brazil had already used 73% of its 2026 allocation. For comparison: in 2025, the quota lasted 17 days. In 2024, March. In 2023, May. Each year faster.

On the calf side, the market told a loud story too. Feedlot Magazine reported that from January 2025 to January 2026, the beef‑cross‑dairy calf market increased by 176 dollars per hundredweight — about 1,056 dollars per head on a 600‑pound feeder. Beef‑cross calves out of Holstein dams averaged 26.83 dollars per hundredweight higher than those from non‑Holstein dairy females. Strong, yes. But that strength was built during a period when tariffs theoretically constrained supply and screwworm shut down the Mexican cattle border. With the tariffs gone, the legal basis ruled unconstitutional, and 80,000 MT of new Argentine quota on the books, the floor under those calf prices is thinner than it looked when you and your banker sharpened your pencils in July.

It’s not just the U.S. border that’s opening wider. Mexico announced a new tariff‑free quota for 2026 — up to 70,000 tonnes of beef and 51,000 tonnes of pork from Brazil and other exporters. China set its first formal beef import quota for Brazil at 1.106 million tons for 2026, with an additional 55% tariff on volumes exceeding the cap — a measure that could redirect excess to the U.S. and other markets if Chinese demand softens or the quota binds.

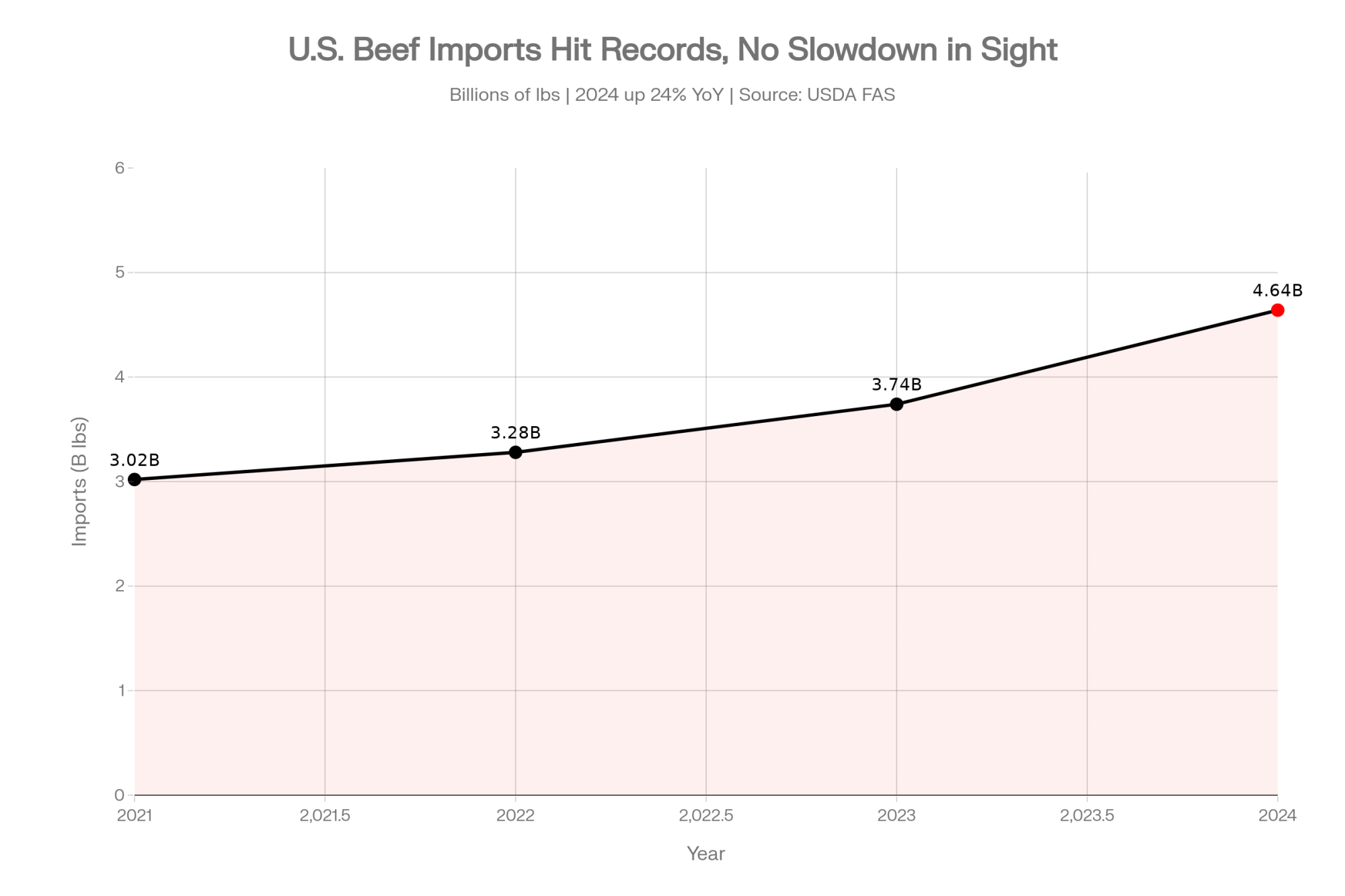

Meanwhile, total U.S. beef imports jumped 17% through November 2025 compared to the same period in 2024, hitting 1.76 million metric tons. The U.S. imported a record 4.64 billion pounds of beef in 2024 alone — a 24% leap from 2023.

You didn’t get a phone call before any of that. You just got the prices on the other side.

How Does a Policy Flip Turn Into a $35,000 Problem at Your Place?

Now put some barn math to what that whiplash does to a 400‑cow dairy that’s leaned into beef‑on‑dairy.

Iowa State Extension livestock economist Lee Schulz documented beef‑on‑dairy steers averaging roughly 269–272 dollars per hundredweight at 650 pounds in Superior and video auction data, meaning a 650‑pound beef‑on‑dairy feeder was worth around 1,750 dollars in that 2024 market. Iowa Beef Center forecasts show 2024–2025 feeder calf prices at historically high levels, keeping four‑figure values common for 550‑ to 650‑pound steers.

On the front end, Midwest Farm Report highlighted baby beef and beef‑cross calves “selling to 1,000 dollars a head” at Wisconsin auctions to start 2025. Wisconsin DATCP summaries showed beef‑on‑dairy cross calves bringing roughly 480 dollars per head against about 110 dollars for straight Holstein bull calves — a 370‑dollar premium in spring 2025.

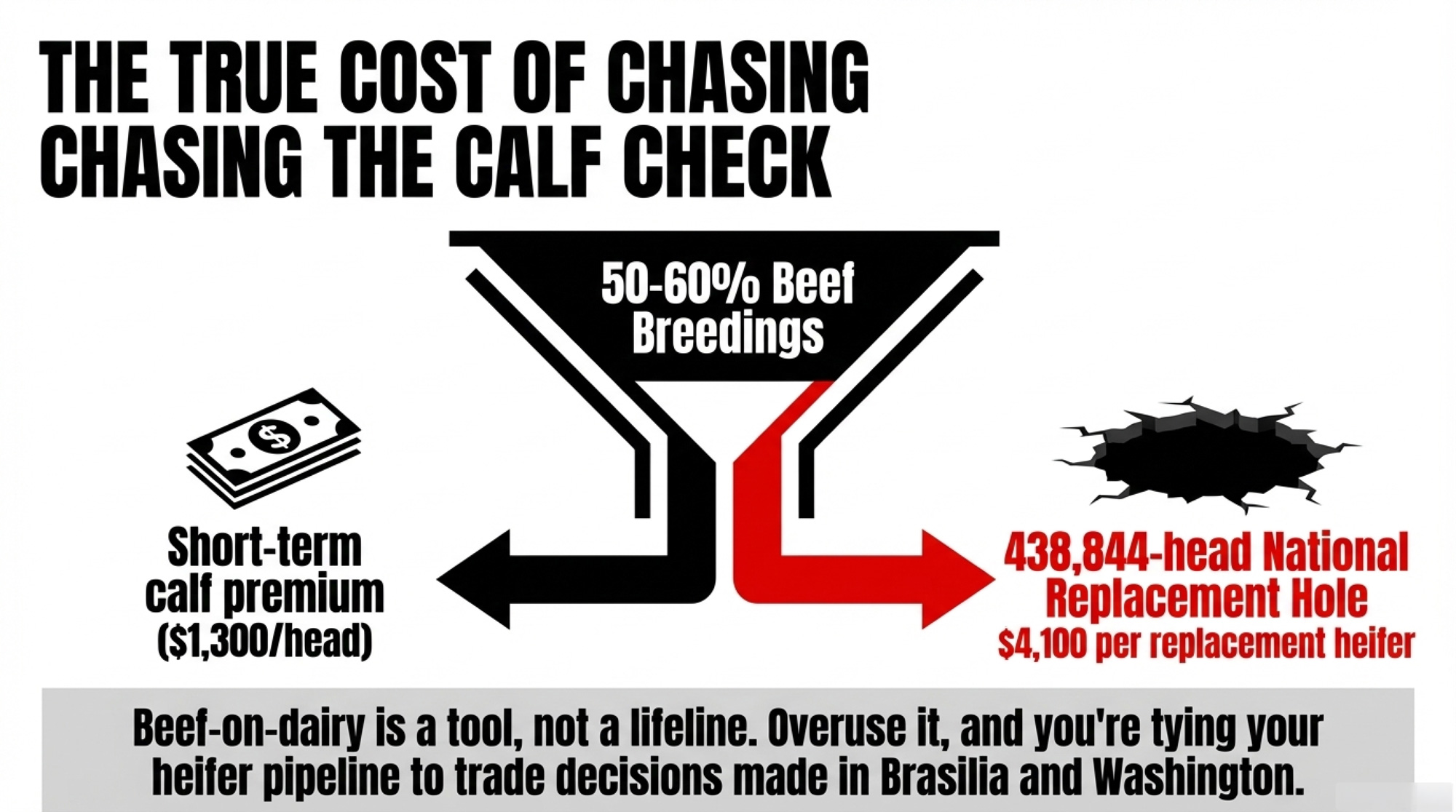

The Bullvine’s heifer analysis piled on another layer: replacement heifers moving from roughly 1,700 dollars to over 4,100 dollars, leaving a 438,844‑head hole in the national heifer pipeline.

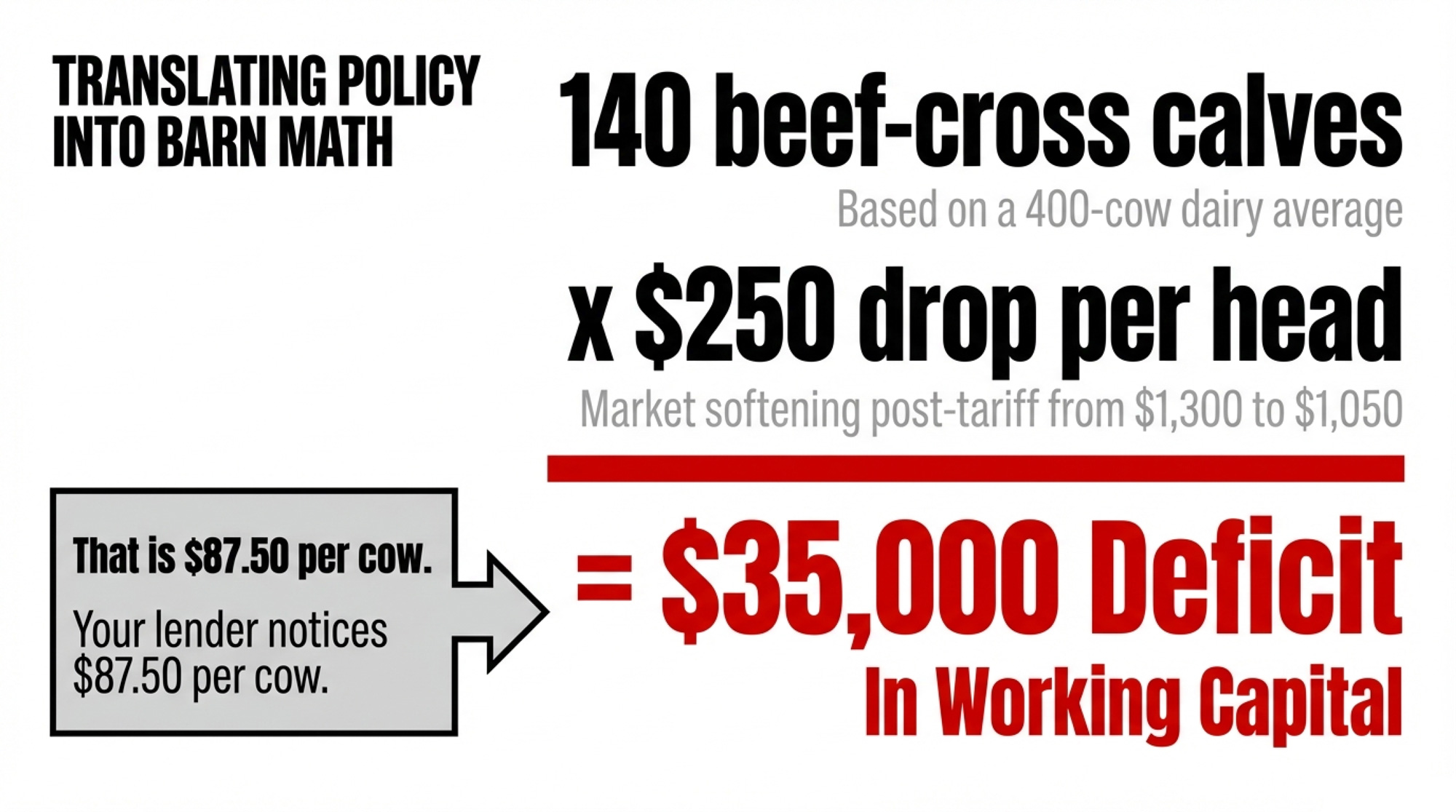

Now run the numbers on your 400‑cow herd:

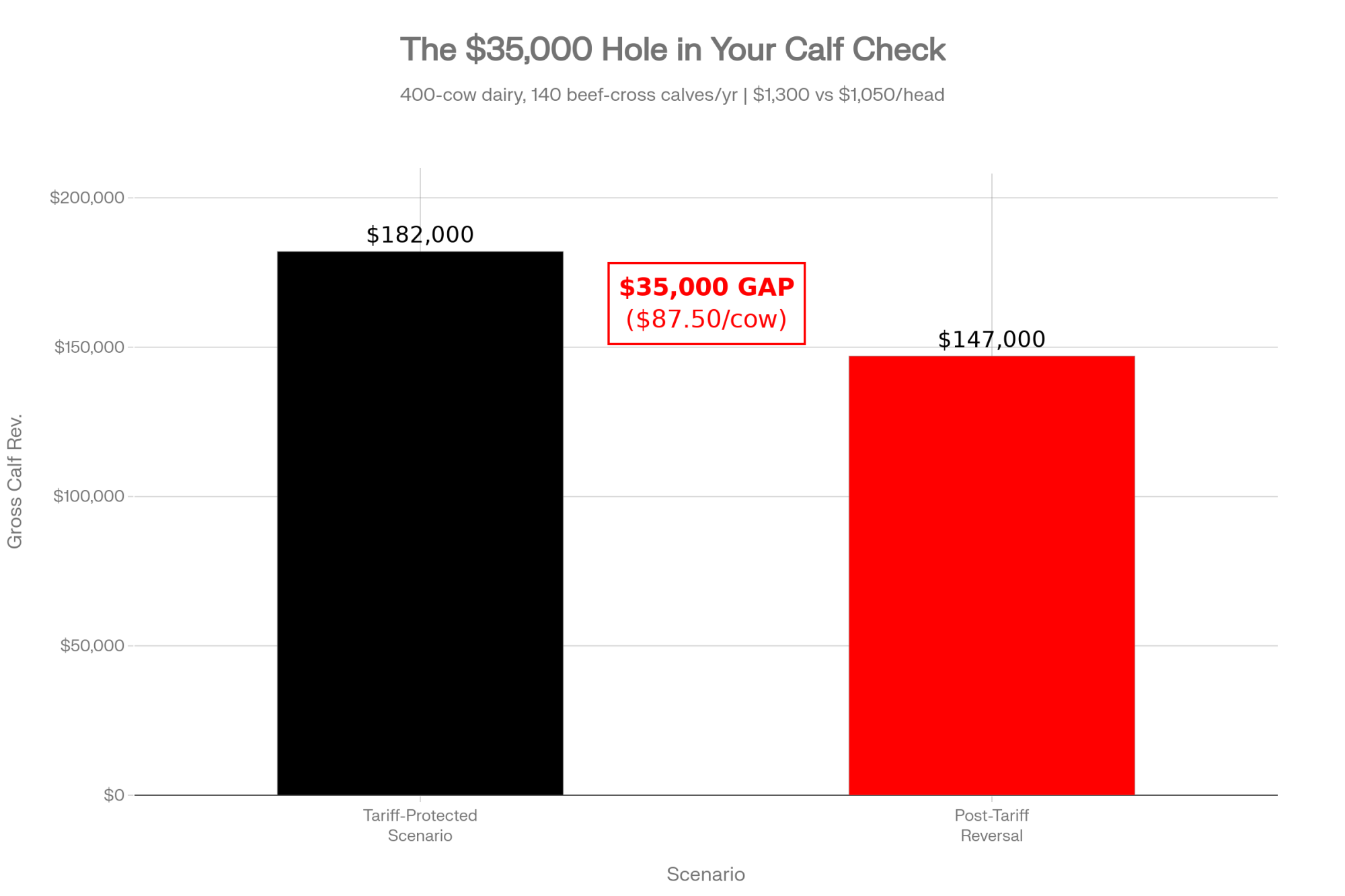

- 35% of breedings to beef = roughly 140 beef‑cross calves per year

- At 1,300 dollars each — realistic for a solid 600‑ to 650‑pound beef‑on‑dairy feeder in this price environment — that’s about 182,000 dollars in gross calf revenue.

- If markets soften by about 20% after the tariff and court whiplash, and those calves fall to roughly 1,050 dollars, you’re at 147,000 dollars.

- Gap: $35,000, or $87.50 per cow in working capital

That $87.50 per cow is the kind of number your lender zeros in on. It’s not “extra.” It’s a robot payment. Or a nutrition upgrade. Or the difference between paying principal versus just servicing interest.

What Does Your Lender Actually See When Policy Is Part of Your Repayment Story?

From your side of the table, “tariff whiplash” sounds like a fair explanation for why the numbers don’t pencil anymore.

From your lender’s side, it’s a reminder they can’t afford to build your future on Washington’s promises — especially when the Supreme Court just ruled the legal tool unconstitutional, and the White House responded by opening moreimport access, not less.

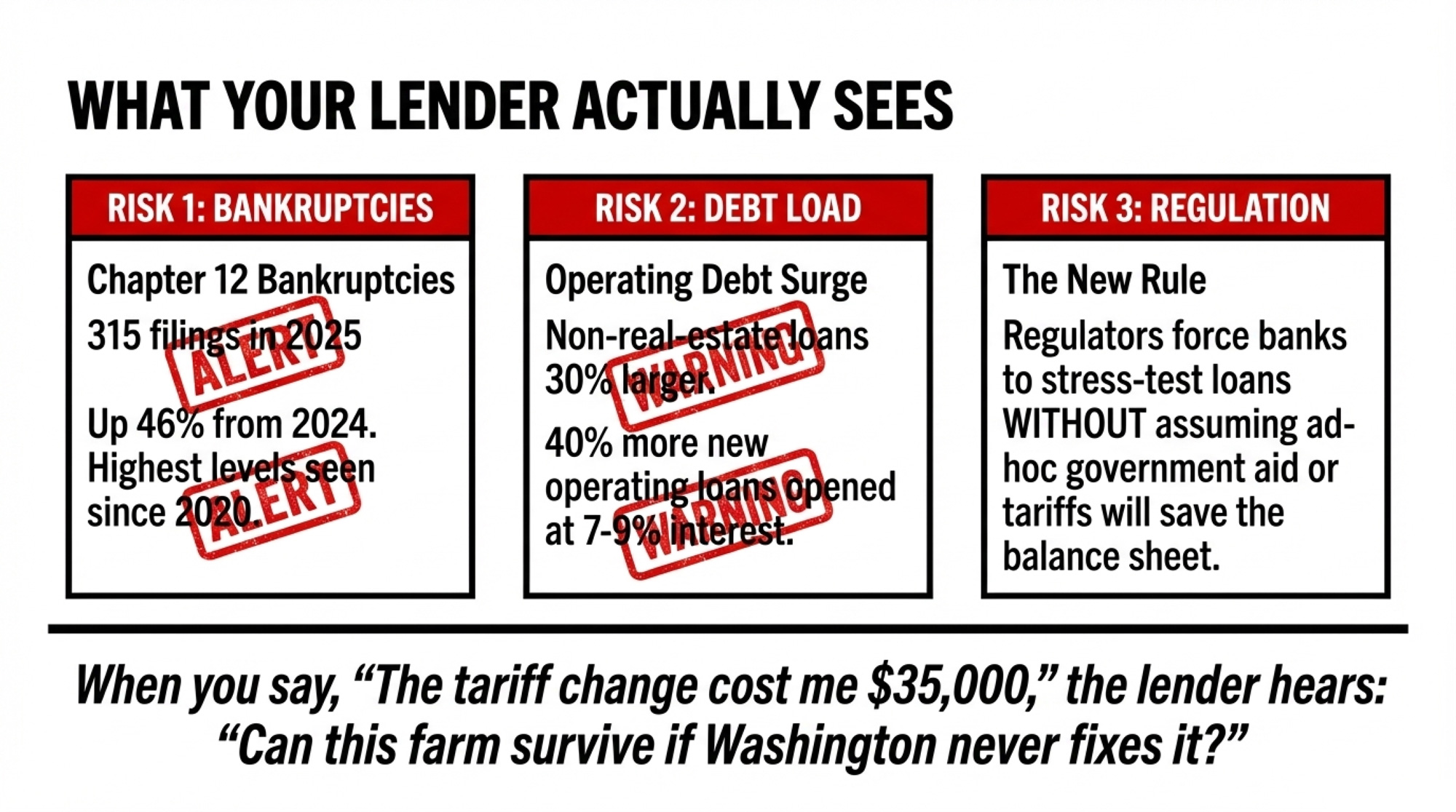

After the MFP cycle, regulators pushed banks and Farm Credit to stress‑test loans without assuming ad‑hoc government aid will show up again. A loan that only works if DC sends a cheque isn’t good.

So today, most ag lenders will:

- Run your plan without counting any future tariff relief, MFP‑style programs, or emergency cheques

- Model what happens if your milk check drops 1–2 dollars per hundredweight, feed jumps 10%, and beef‑on‑dairy calf values fall 15–20%

- Watch working capital and total debt per cow closely, especially with many new operating loans at 7–9%.

A Kansas City Fed review found average non‑real‑estate farm loan sizes roughly 30% higher in late 2024 and early 2025 than a year earlier as producers borrowed more to cover higher input costs. In 2025, nearly 40% more new farm operating loans were opened than in the prior year.

At the same time, Chapter 12 farm bankruptcy filings hit 315 in calendar year 2025 — up 46% from 216 in 2024 and the highest count since 2020. Arkansas led the nation with 33 filings (more than double its prior-year total), followed by Georgia at 27, Iowa at 18, Nebraska at 17, and Wisconsin and Missouri at 16 each. The Midwest and Southeast together accounted for 226 of the 315 cases.

When you tell your lender, “The tariff change took 35,000 dollars out of our calf plan,” they don’t argue. They ask:

- If calves never reach 1,300 dollars, can this farm still make full payments?

- How close are we to breaking covenants if we have one more bad year?

- Is it smarter to restructure now, while equity is still there?

If you don’t have your own answers ready before they ask, you’re already behind.

Can You Build a Five‑Year Plan When the Rules Keep Changing Under Your Feet?

You’re making choices right now that will shape the next decade of your operation:

- A new barn sized for 550 head when you’re milking 400

- A robot system that only pencils if labor stays tight and cull prices hold

- A breeding lineup that leans harder into beef‑on‑dairy on the bottom half of the herd

- Genomic bets you won’t fully cash for four or five years

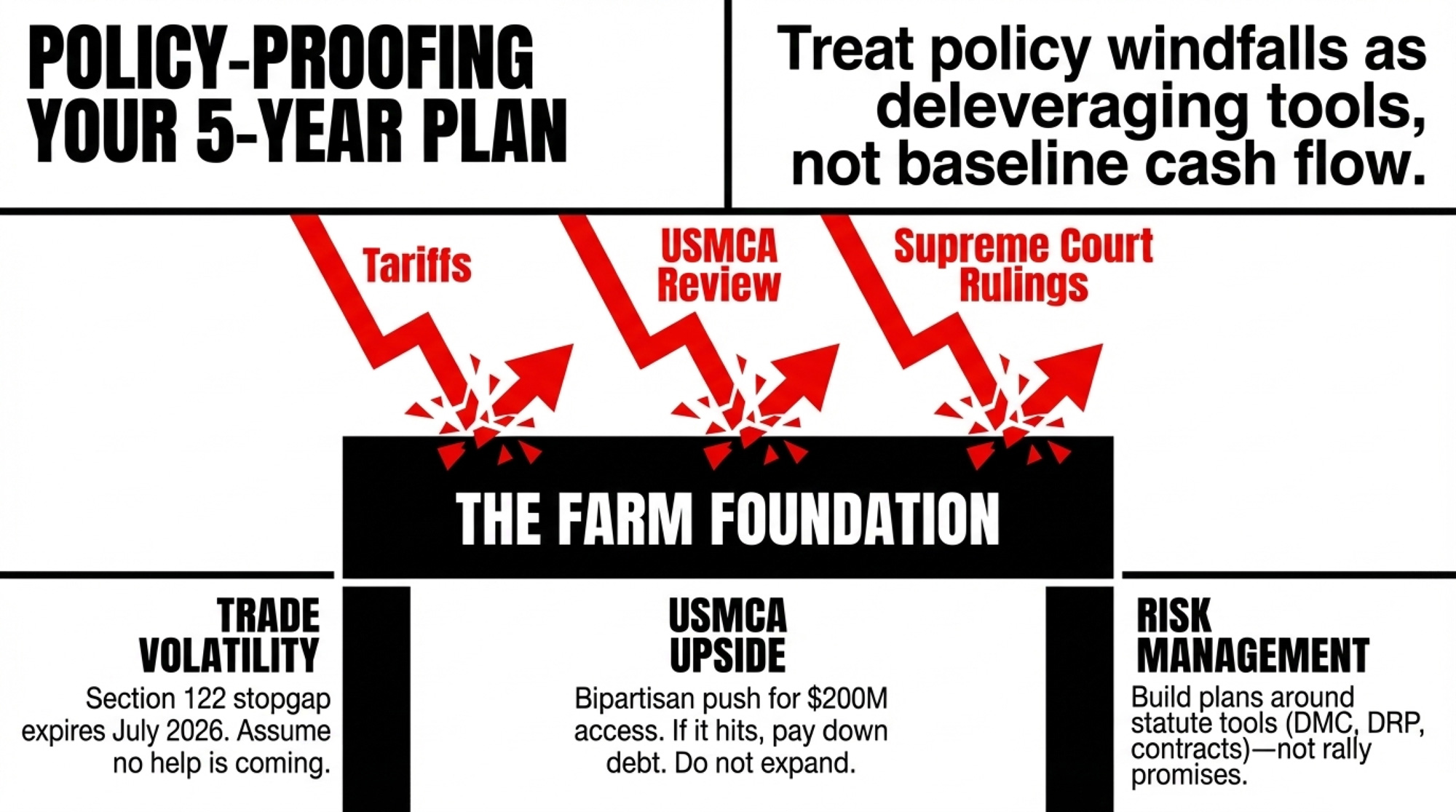

Meanwhile, the tools Washington used — reciprocal tariffs, national emergency orders, retroactive exemptions — just had their legal foundation pulled out from under them by the Supreme Court. The 10% Section 122 stopgap expires July 24, 2026, and beef is already exempt from it anyway. The administration’s next move is Section 301 investigations that USTR says will “cover most major trading partners” — but those take months to conclude and years to implement.

And there’s another pressure point already on the books. The formal USMCA joint review is scheduled for July 2026, and NMPF and USDEC testified before USTR on December 3, 2025, urging the administration to fix Canada’s dairy quota implementation. A bipartisan group of 74 House members — led by Representatives DelBene, Tenney, Wied, and Costa — sent a letter to USTR Jamieson Greer the same day, calling out Canada’s unfair TRQ allocation and global dairy protein dumping practices.

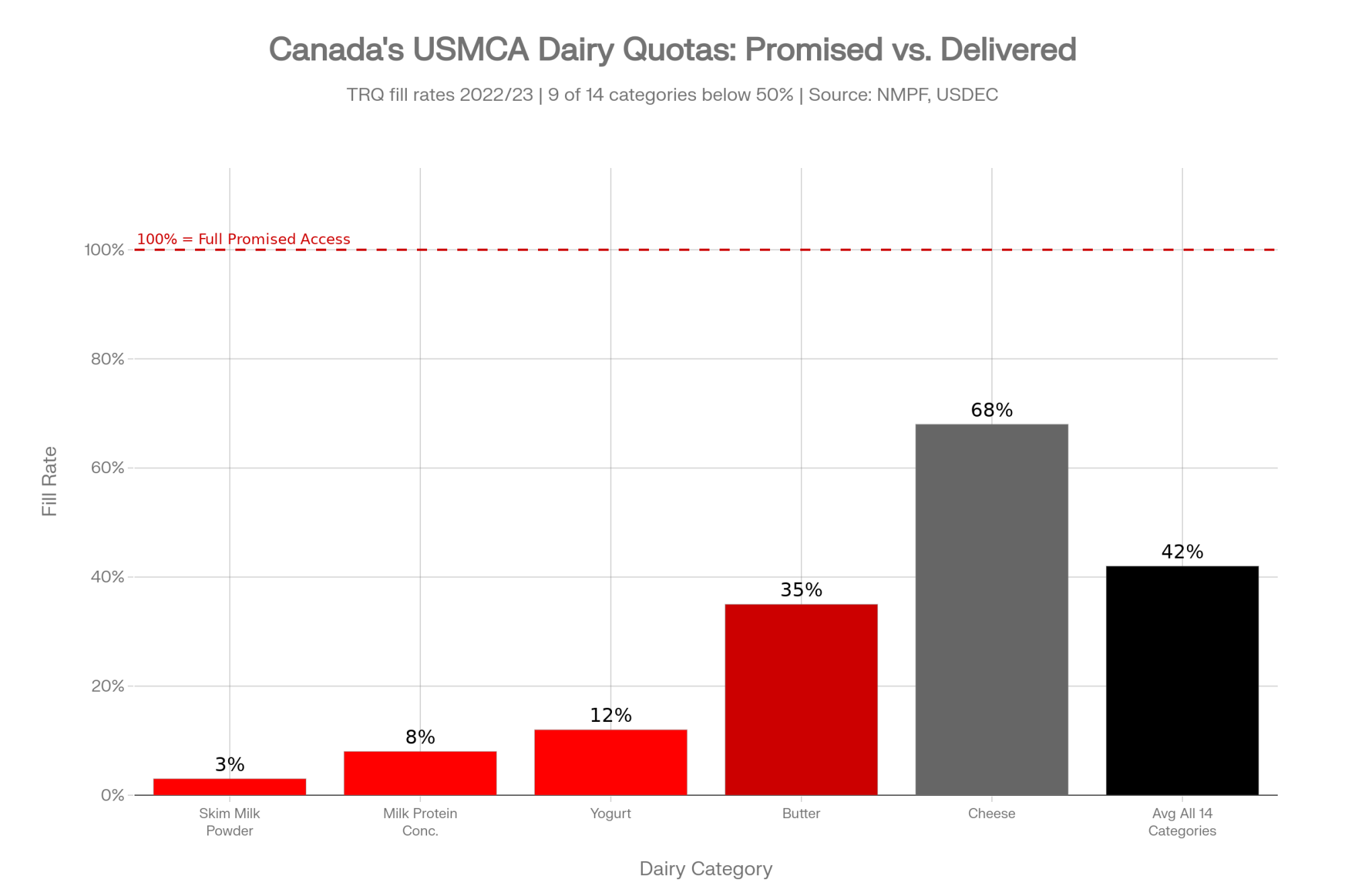

That push matters because the numbers are damning. TRQ fill rates averaged just 42% across all 14 dairy categories in 2022/23, with 9 of 14 quotas below 50%. Some categories were barely touched: 3% for skim milk powder, 8% for milk protein concentrates, 12% for yogurt. That’s not weak demand — it’s Canada’s allocation system channeling most quota to domestic processors who don’t use it, exactly as two dispute panels have already confirmed.

USMCA promised roughly $200 million in new annual access to Canada’s dairy market. If U.S. exporters could actually ship the full 100% of what was promised instead of getting stuck at 42%, as NMPF and USDEC have argued in their 2025 testimony, that’s the kind of money that would more than plug a $35,000 calf hole on a 400‑cow dairy.

The U.S. Dairy Export Council estimates Mexico and Canada at about $3.6 billion, or roughly 44% of total U.S. dairy export value. If those markets see new tariffs, quotas, or retaliation because dairy becomes a bargaining chip again, your check feels it — even if you never sell a pound of cheese directly across a border.

So the only way to build a five‑year plan you can sleep on is to assume tariffs and trade deals won’t sit still, policy help is a bonus rather than a baseline, and your numbers have to survive ugly scenarios — not just the best‑case breakout.

What Does a Real Stress Test Look Like Before You Sign?

Before you sign for a barn, a robot, or a major breeding push, you need more than “should work” and a rosy spreadsheet. You need to see what happens when things get ugly.

Your Three‑Case Stress Test at a Glance

Drop in your own numbers. But they should look at least as nasty as this.

| Scenario | Milk price assumption* | Feed cost assumption | Beef‑on‑dairy calf values | Interest rate assumption |

| Most‑likely | Around current Class III/IV strip (e.g., high‑18 to low‑19 dollars/cwt) | 3–5% higher than today | Close to recent cheques | Current rates on operating + term debt |

| Downside | 1–2 dollars/cwt below that range | At least 10% higher | 15–20% below last year’s cheques | +1 percentage point on variable‑rate debt |

| Worst‑case | Mid‑16s for roughly half the year | 15–20% higher | 25–30% below last year’s cheques | +2–3 percentage points on vulnerable loans |

*Use the actual futures curve and your co‑op’s basis, not a guess.

Then ask the same questions your lender is already asking:

- In the downside case, does this project still cover the full debt service?

- Do you have enough working capital and operating line to survive the worst‑case year without missing payments or blowing covenants?

If you can’t answer “yes” to both, you’re not stretching — you’re betting that policy and markets will behave. Given that the legal basis for the original tariffs got struck down by the Supreme Court and the administration added 80,000 more metric tons of imported beef quota on top of that, that bet looks worse today than it did a year ago.

How Do You Keep Beef‑on‑Dairy From Owning Your Future?

Beef‑on‑dairy has been a lifeline for a lot of barns. It’s also a quiet way trade policy can reach right into your calf pen.

When beef semen is going on half your cows because the cheques looked great last year, you’re not just chasing a premium. You’re tying both your heifer pipeline and your loan plan to decisions made in Washington, Brasilia, Ottawa, Mexico City, and Beijing. And now add Buenos Aires, thanks to the February 6 proclamation.

A more survivable approach:

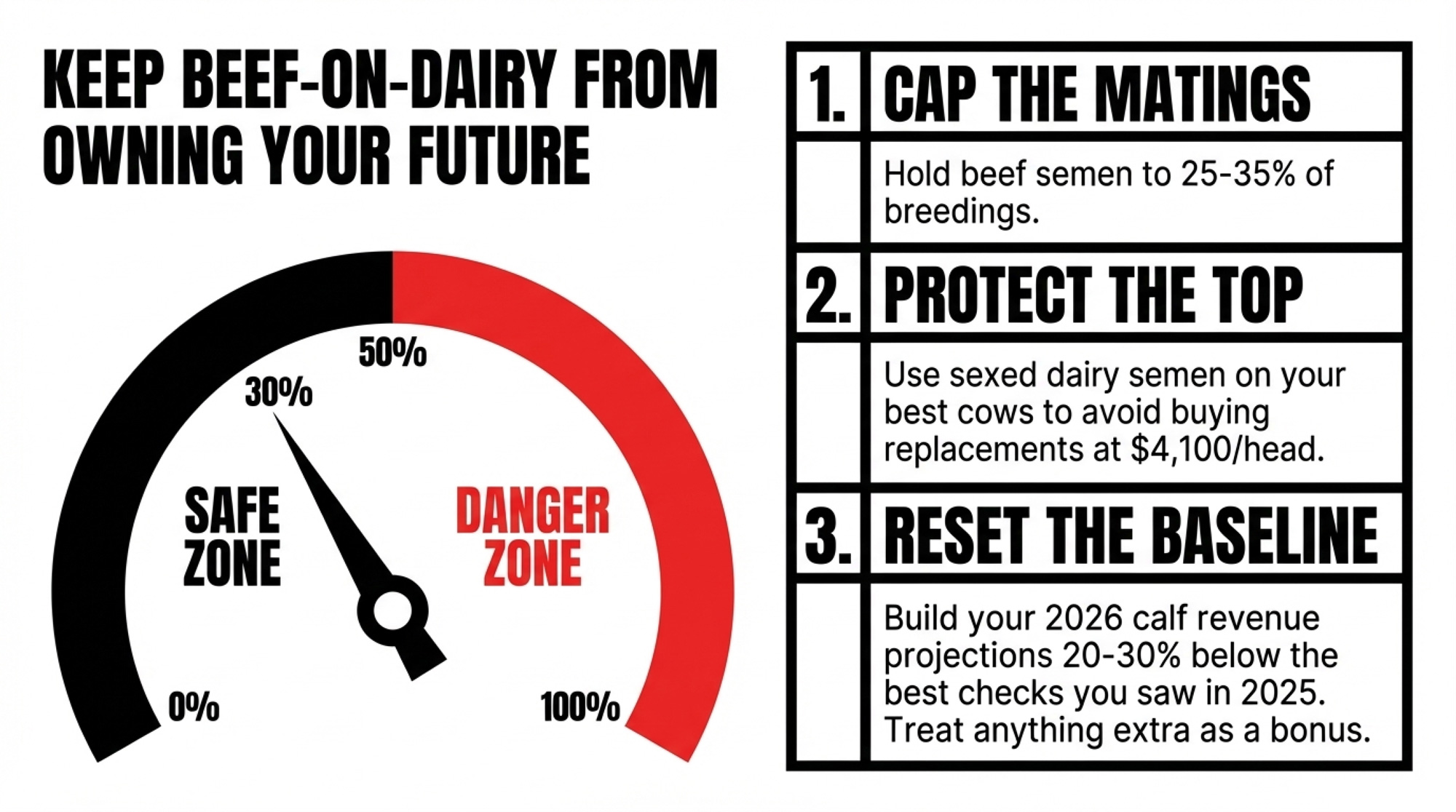

- Treat beef‑on‑dairy as a tool, not a lifeline

- Keep beef semen around 25–35% of breedings and protect the top of your herd with sexed dairy semen so you don’t wake up with a replacement hole you can’t fill at 4,100 dollars a head.

- Build calf revenue in your plan at prices 20–30% below the best cheques you’ve seen, and treat anything better as upside.

Suppose that sounds conservative, good. Your banker already thinks this way.

Options and Trade‑Offs for Farmers

You can’t control who gets a White House meeting. You can control how exposed your farm is when tariffs swing — or when courts wipe them out entirely.

Build for Margin, Not for Milk Price

When it makes sense: You’re planning to keep milking 300–600 cows in the commodity stream, and you know “waiting for 20‑dollar milk and a good government” isn’t a strategy.

What it requires:

- A current breakeven that includes today’s interest, realistic replacement heifer costs in the 3,000–4,100‑dollarrange, and full family living, not 2022 numbers

- A path to pull 1–2 dollars per hundredweight out of your cost via better repro, tighter heifer programs, fewer transition wrecks, and real labor efficiency

- The guts to cut non‑essentials that don’t move cost per hundredweight

Where it can bite you: If you’re already carrying high fixed costs — big facility notes, heavy land debt — you may not be able to get cheap enough to play this game.

30‑day action: Before your next lender visit, rerun your breakeven with current loan rates, replacement heifers at 3,000–4,100 dollars, and a calf price 20% below last year’s cheques. If the result makes your stomach flip, that’s the first thing to attack. That 2026 cost‑per‑cwt math is worth running beside these numbers.

Treat Beef‑on‑Dairy as a Tool, Not a Lifeline

When it makes sense: You’re in that 300–1,000‑cow window where beef‑cross calves are real money, but you don’t want a trade decision in Brasilia or Buenos Aires to decide whether you keep the farm.

What it requires:

- Capping beef semen at about 25–35% of breedings, not 50–60%, and keeping sexed dairy semen on the top of your genetic stack so your heifer pipeline doesn’t disappear

- Monthly heifer inventory checks that look two years ahead

- Calf revenue assumptions built 20–30% under the best prices you’ve seen, with upside treated as a bonus

Where it can bite you: If you have already sold too many dairy heifers and dug a big hole, unwinding takes time and discipline. It means saying “no” to the next round of crazy beef prices.

Premium or Differentiated

When it makes sense: You’ve got a genuine premium channel — organic, A2, grass‑fed, on‑farm processing — in a market that can pay for it, and a story people will actually pay extra for.

What it requires:

- Knowing the full math of the premium: pay price, cert and testing costs, labor, shrink, rejected loads risk

- A plan to protect the margin if premiums shrink or competition crowds in

- A clearer brand than “we’re local and we work hard.”

Where it can bite you: Premiums erode. Specs tighten. Consumer fads move. You swap commodity risk for brand and channel risk. This isn’t a soft landing for a weak commodity business — it’s a different business. What Clark Farms learned about on‑farm creamery ROI is a useful reality check before you go down this road.

Policy‑Proofing Your Plan

When it makes sense: Always, this is the base layer under every other layer.

What it requires:

- Treating any policy‑driven cheque — MFP, ad‑hoc disaster, tariff‑driven payments — as deleveraging money, not recurring cash flow

- Building risk management around tools that are in statute and contracts — DMC, DRP, forward contracts — not around what was said at the last rally

- Running the “no help for five years” scenario once a year and asking if the farm still survives

The Supreme Court just made this advice more concrete than ever. The legal basis for the tariffs that were supposedly protecting you was ruled unconstitutional. The 10% Section 122 stopgap expires July 24, 2026; beef is exempt from it anyway, and the Section 301 investigations that follow will take months to conclude. Meanwhile, the July 2026 USMCA review is less than three months away, with 74 House members already pushing USTR Jamieson Greer to fix the 42% dairy fill rate in Canada. If that USMCA $200 million dairy access problem gets fixed, treat the upside as a chance to pay down debt — not add more.

Your lender is already thinking this way. Here’s what they’re calculating before you walk in.

Key Takeaways

- If your five‑year plan only works at last year’s calf prices, you don’t have a plan — you have a bet. Run your numbers at 20–30% lower beef‑on‑dairy calf values and see if the debt still pencils.

- If beef semen is going on more than a third of your breedings, your heifer pipeline is tied to trade decisions you’ll never be in the room for. Cap beef matings and protect the top of your herd for replacements.

- If a barn, robot, or big upgrade only looks “smart” at 19‑dollar milk and interest rates from two years ago, walk away. The right projects still pay in a 17‑dollar milk, +10% feed, −20% calf world.

- If you catch yourself saying, “It’ll be fine once they fix trade,” stop and grab a pencil. The Supreme Court just struck down the legal basis for the tariffs. The White House added 80,000 MT to the Argentine beef quota in the same month. Rebuild the plan assuming nobody fixes anything — and treat any policy win, including a fixed USMCA TRQ, as a chance to deleverage.

- If your lender seems more nervous than you are, listen. They’re already stress‑testing your numbers without counting on tariffs, bailouts, or emergency cheques. You should be, too.

The Bottom Line

The picture that sticks from this whole episode isn’t a chart or a tariff code. It’s two people affected by the same decision sitting in very different rooms.

One is Joesley Batista, walking into a private White House meeting and, weeks later, watching both the 10% reciprocal and the 40% emergency tariffs on beef disappear fully inside a single week. Then, watching the Supreme Court make sure the tool behind them can’t be used the same way again. Then, the administration opened 80,000 more metric tons of duty‑free beef quota for good measure.

The other is a 400‑cow producer at a kitchen table, explaining to a lender why a $35,000 calf‑revenue hole — $87.50 per cow in working capital — just opened in a plan built around a “national emergency” tariff that lasted a few months.

The system will keep getting sold as “protecting American agriculture. The question is whether your own numbers treat that as a promise, or as whether you’ve got to farm through.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The 90-Day Dairy Pivot: Converting Beef Windfalls into Next Year’s Survival – Reveals the high-speed math needed to turn fleeting beef premiums into a 2026 resilience plan. Breaks down the \$26,600 revenue opportunity for 100-cow herds, arming you with the breakeven benchmarks to survive flat milk checks.

- USMCA 2026: The \$200M Question – Why Only 42% of U.S. Dairy Access to Canada Gets Used – Exposes the structural loopholes costing U.S. producers \$200 million in annual trade value. Delivers the strategic intelligence required to navigate the 2026 USMCA review, ensuring your operation is positioned to capture real orders, not just paper access.

- Genetic Revolution: How Record-Breaking Milk Components Are Reshaping Dairy’s Future – Breaks down the DNA-driven shift toward 3.7% protein and record butterfat. Reveals how the 2025 genetic evaluation reset prioritizes feed efficiency, arming you with the genomic tools to build a high-value protein factory for the next decade.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.