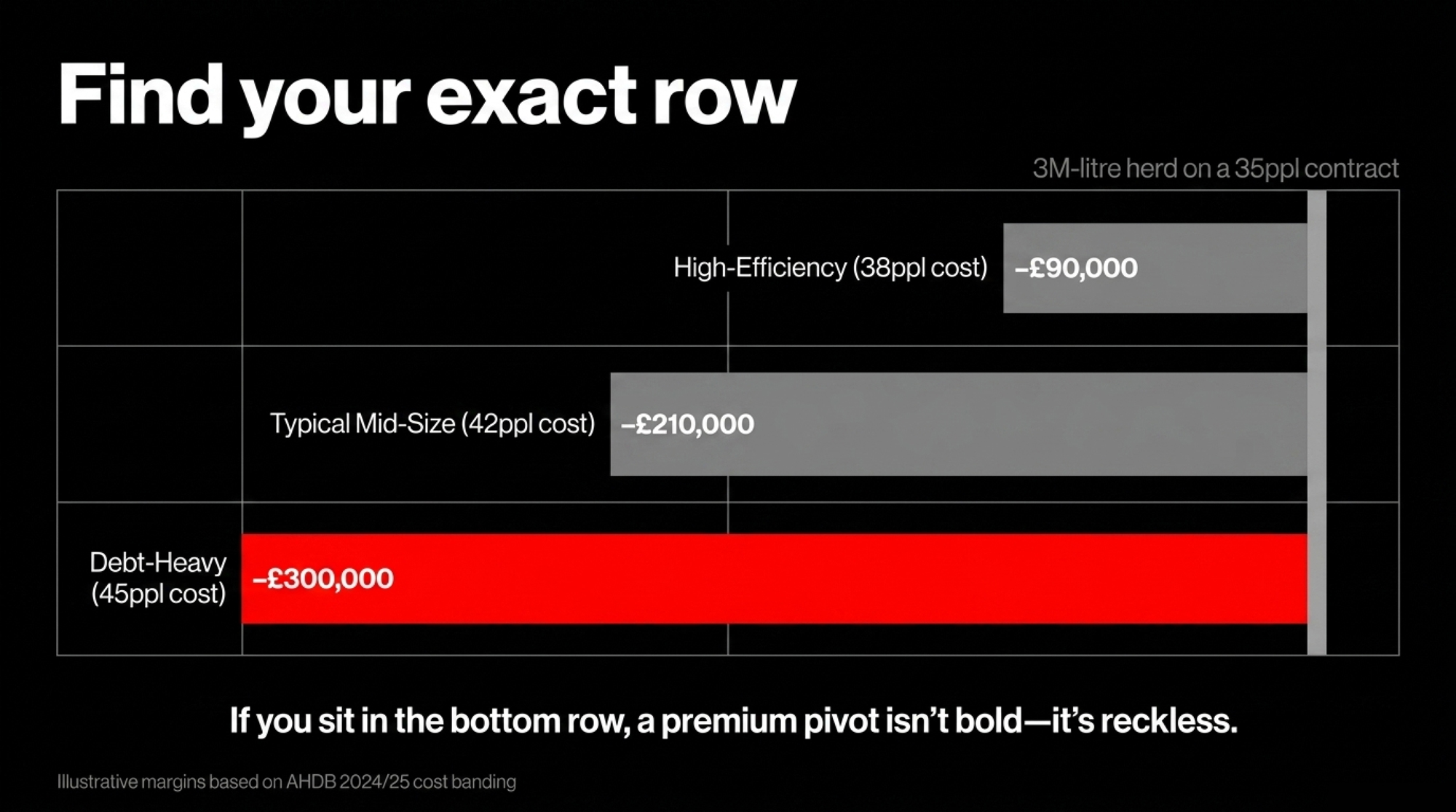

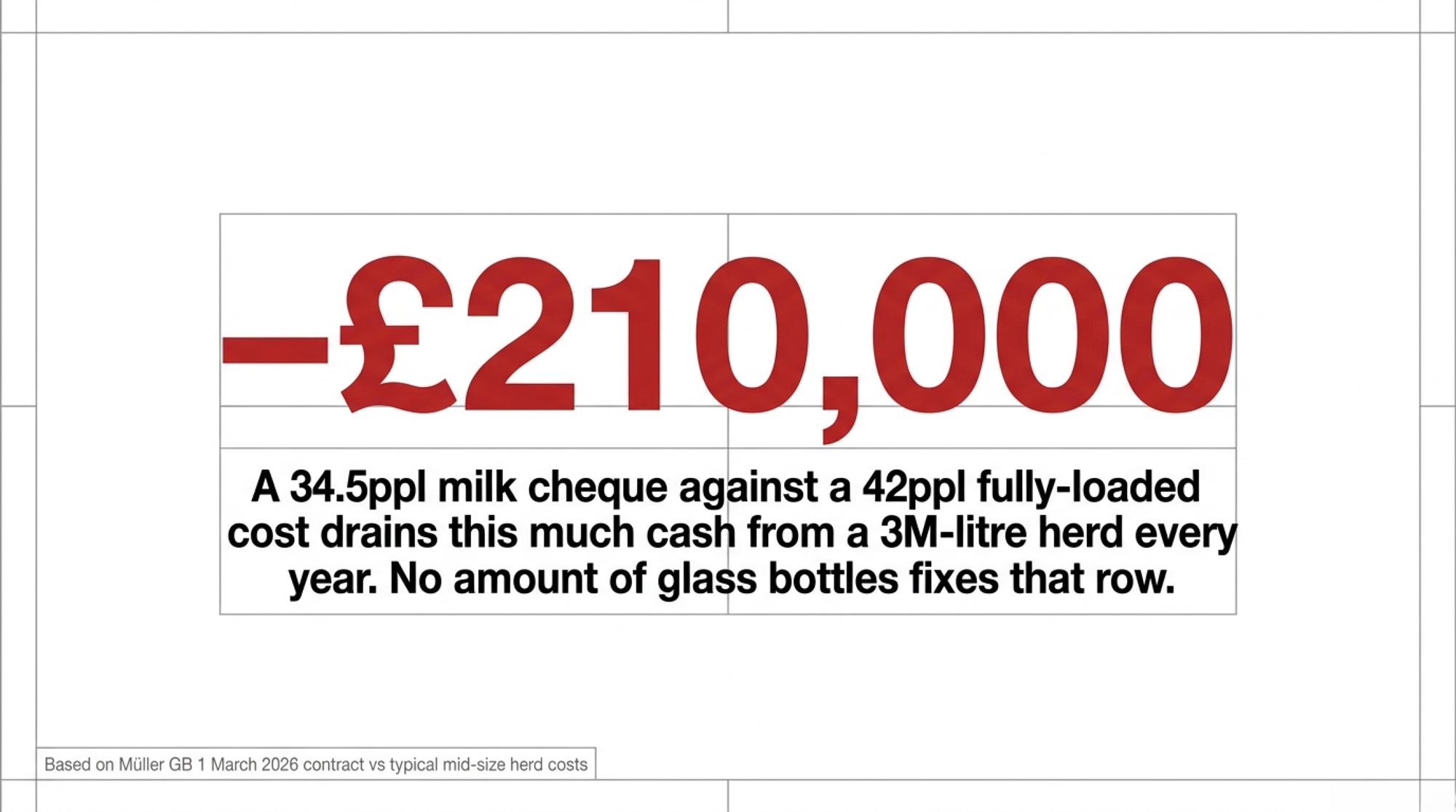

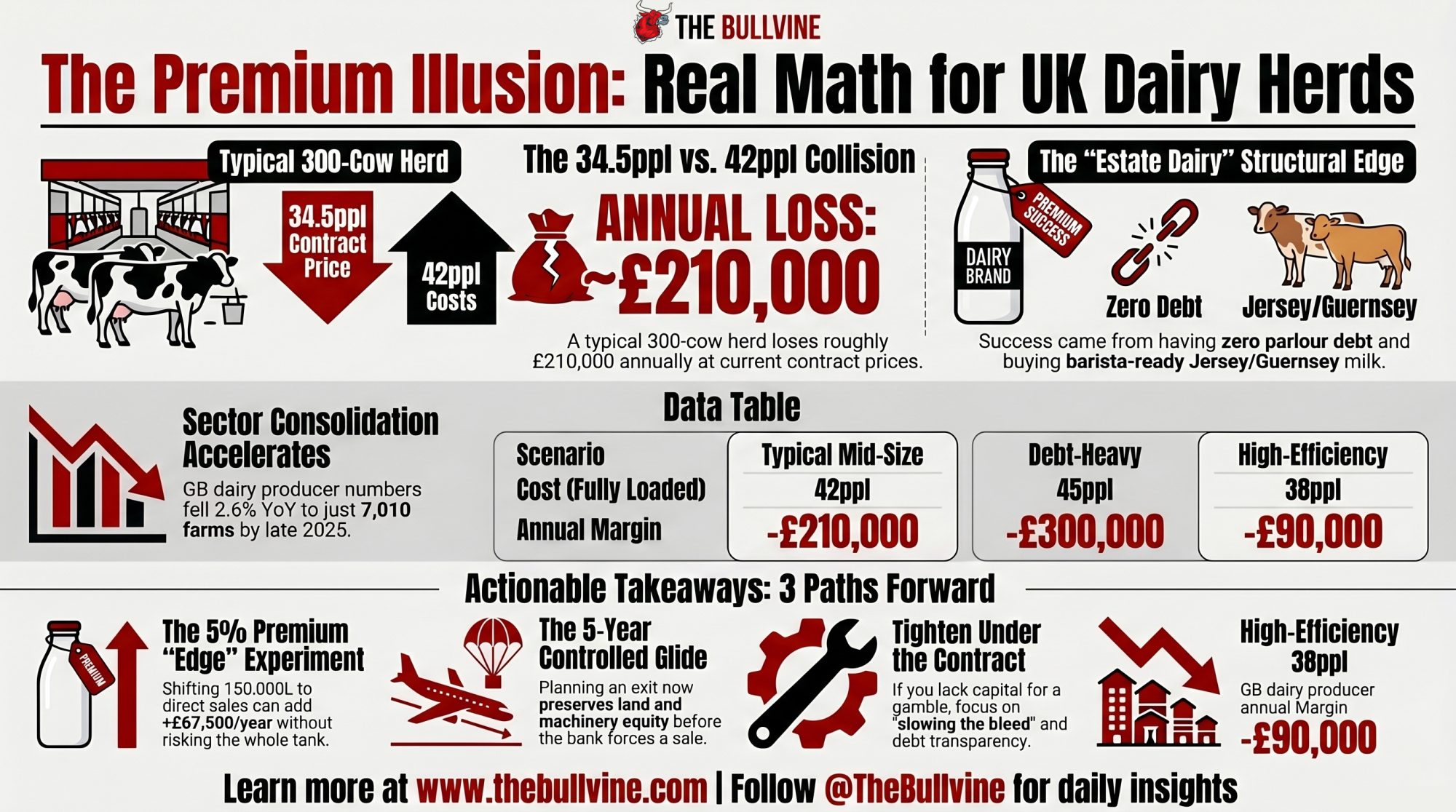

Müller’s cheque cleared at 34.5ppl on 1 March. Your fully-loaded cost sits near 42ppl. On 3 million litres that’s –£210,000 a year — and no amount of glass bottles fixes that row.

Executive Summary: Müller GB cut its Advantage contract price to 34.5ppl from 1 March 2026, while Estate Dairy — the asset-light London brand that started with £5,000, a borrowed catering van and no cows of its own — just reported turnover of about £26M on Claridge’s, Ritz and Savoy tables. For a 300-cow Holstein herd shipping around 3M litres a year, that cheque at 34.5ppl against a typical fully-loaded cost of roughly 42ppl pencils out at –£210,000 annually, and at 45ppl it widens to –£300,000. AHDB’s October 2025 survey puts GB down to 7,010 producers (–2.6% YoY), so the pressure to “do an Estate Dairy” is real — but the Youngs’ edge was starting with no parlour debt and buying Jersey and Guernsey milk already suited to baristas, not flipping a Holstein herd. A disciplined 5%-of-the-tank premium experiment (150,000 L at a net 80ppl) could add about +£67,500 a year, enough to close the gap on the High-Efficiency row but nowhere near the Debt-Heavy row. The four paths worth costing this month: tighten under the contract, run a bounded 12-month premium edge experiment, plan a 3–5 year glide exit, or go big on premium only if most debt is secured against land. Read the full piece if you want the row-by-row barn math and the 30-day actions before the next Müller price letter lands.

Shaun and Rebecca Young built UK’s Estate Dairy from £5,000, a borrowed catering van and no cows of their own, and turned it over at about £26 million in its most recently reported financial year, with hospitality names like Claridge’s, The Ritz and the Savoy on the customer list, according to reporting in The Times. If you’re milking 300 cows in 2026, carrying more kit finance than you’d like and staring at a 34.5ppl Müller cheque from 1 March, that headline lands differently at your kitchen table than it does in a London Sunday supplement.

Estate Dairy is a real business with real cows’ worth of milk moving through it. The mirage isn’t whether the Youngs did it — it’s whether a 300-cow Holstein herd carrying parlour and shed finance can copy it. Let’s put the glossy version next to the one that actually matters — yours — and ask the quiet question nobody in the farm press wants to say out loud: are you really failing if you stay on the contract?

What the Estate Dairy UK Growth Story Really Proved

| Factor | Estate Dairy (Youngs) | Your 300-Cow Holstein Herd |

|---|---|---|

| Starting capital | £5,000 + borrowed van | £800k–£2M in parlour, shed & kit finance |

| Herd ownership | None — bought milk from others | Owned; replacement costs ~20–25%/yr |

| Milk breed | Jersey / Guernsey (high fat, high protein) | Holstein (high yield, lower fat/protein) |

| Parlour debt | £0 legacy debt | Typically £200k–£600k outstanding |

| Annual turnover | ~£26M (FY 2025 reported) | ~£1.05M at 35ppl on 3M litres |

| Pre-tax profit | ~£1M (reported) | –£90k to –£300k depending on cost tier |

| Customer base | Claridge’s, Ritz, Savoy, M&S, Ocado | Single processor contract (e.g., Müller) |

| Route to market | Built coffee/hospitality channels first | Processor sets price; no direct market |

| Genetic pivot timeline | N/A — sourced milk already suited to premium | 4–7 years to shift bulk tank profile via crossbreeding |

| Key replicable element | Brand building, channel relationships | Cost discipline, premium edge experiment (5% of tank) |

Before the brand, the Youngs worked in London’s specialty coffee scene, not a parlour. Around 2015 they scraped together £5,000, sold a car, borrowed Rebecca’s mum’s catering van, and used a friend’s cold store as a first “plant.” They spent roughly a year driving between farms and cafés, looking for milk that would actually perform in a barista’s hands.

A few hard facts about that journey:

- Founded 2016. The Estate Dairy brand launched that year.

- Asset-light entry. No parlour, no robot, no slurry store, not an acre of their own — and no legacy dairy debt. That structural difference matters more than any branding lesson you could copy off them.

- Bought the milk, didn’t breed it. Suppliers reported in Estate Dairy’s public origin story have included Brades Farm’s Jerseys in Lancashire’s Lune Valley and Bickfield Farm’s Guernseys in Somerset — higher fat, higher protein, that “gold top” look in a glass.

- High-end customer base. As reported in early 2026, the customer list has included Claridge’s, The Ritz, the Savoy, plus retailers such as Sainsbury’s, Marks & Spencer, Ocado and Waitrose.

- Profitable from the start. The Times reported turnover in the most recently reported financial year at around £26 million, with just under £1 million pre-tax profit.

Strip the Instagram glow off that and the proof is narrower than the headline suggests. Start with no herd and no farm debt. Buy milk already suited to premium channels. Build the coffee and hospitality relationships before you spend big on plant. Do those things in that order and you can build a profitable premium dairy brand that never lives or dies by a processor contract. None of that is the same as saying a 300-cow Holstein herd with parlour finance, shed loans and machinery leases should try to become The Estate Dairy 2.0.

What’s Actually Changing for Mid-Size UK Herds

Step away from Shoreditch cafés for a moment and look at the picture most readers are standing inside.

A fairly typical GB mid-size setup in 2026:

- Around 300 Holstein-type cows in a higher-yield system.

- Roughly 2.4–3.0 million litres/year, depending on litres per cow and days in milk — comfortably above the UK all-cow average of about 8,148 litres/cow/year in the 2023/24 milk year. [VERIFY: confirm exact litres/cow/year figure from latest Defra/AHDB milk utilisation release at sub-edit.]

- A processor contract — say Müller — paying 34.5ppl for Advantage-eligible milk from 1 March 2026, down 1ppl from the 35.5ppl paid from 1 February, according to Müller GB’s own published 1 February 2026 and 1 March 2026 price announcements.

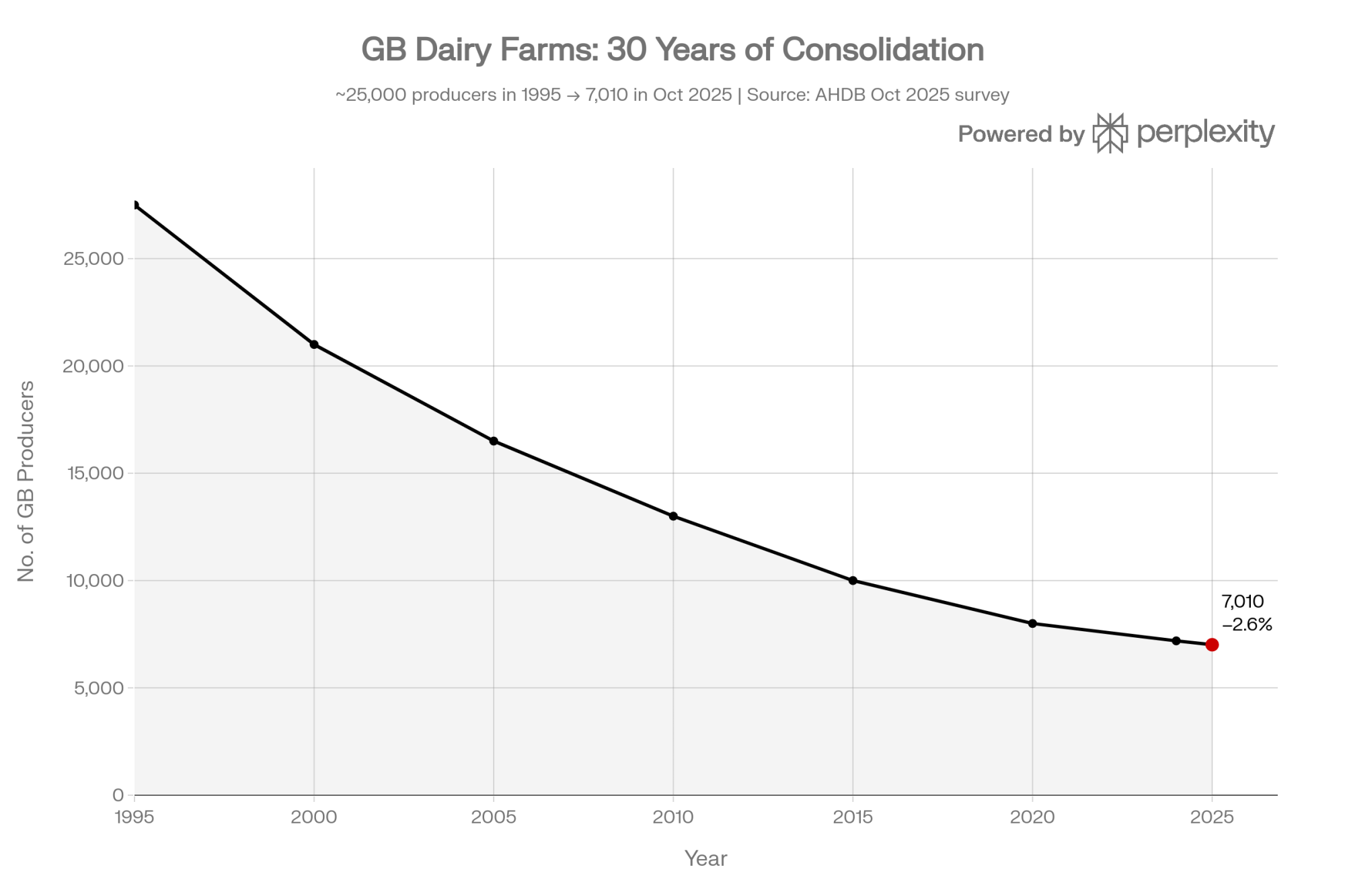

AHDB’s October 2025 milk buyer survey counted 7,010 GB dairy producers, down 2.6% year-on-year, and structural work on the industry shows GB farm numbers were roughly 25,000–30,000 in the mid-1990s. The sector has consolidated hard. Major GB processors have restructured supply pools over the past year, and UK farm trade press has reported termination or restructure notices involving cases at Müller and other buyers. Müller GB was approached for comment on this piece; any response received post-publication will be added as an update.

AHDB’s recent cost-of-production work shows dairy costs have climbed sharply since 2019, with feed, energy and finance squeezing margins even where milk prices lifted. Fully-loaded costs in many higher-input, debt-heavy systems can end up above 40ppl. AHDB’s 2024/25 cost banding places a meaningful minority of GB producers in the high-cost tier where contract price alone cannot close the gap.

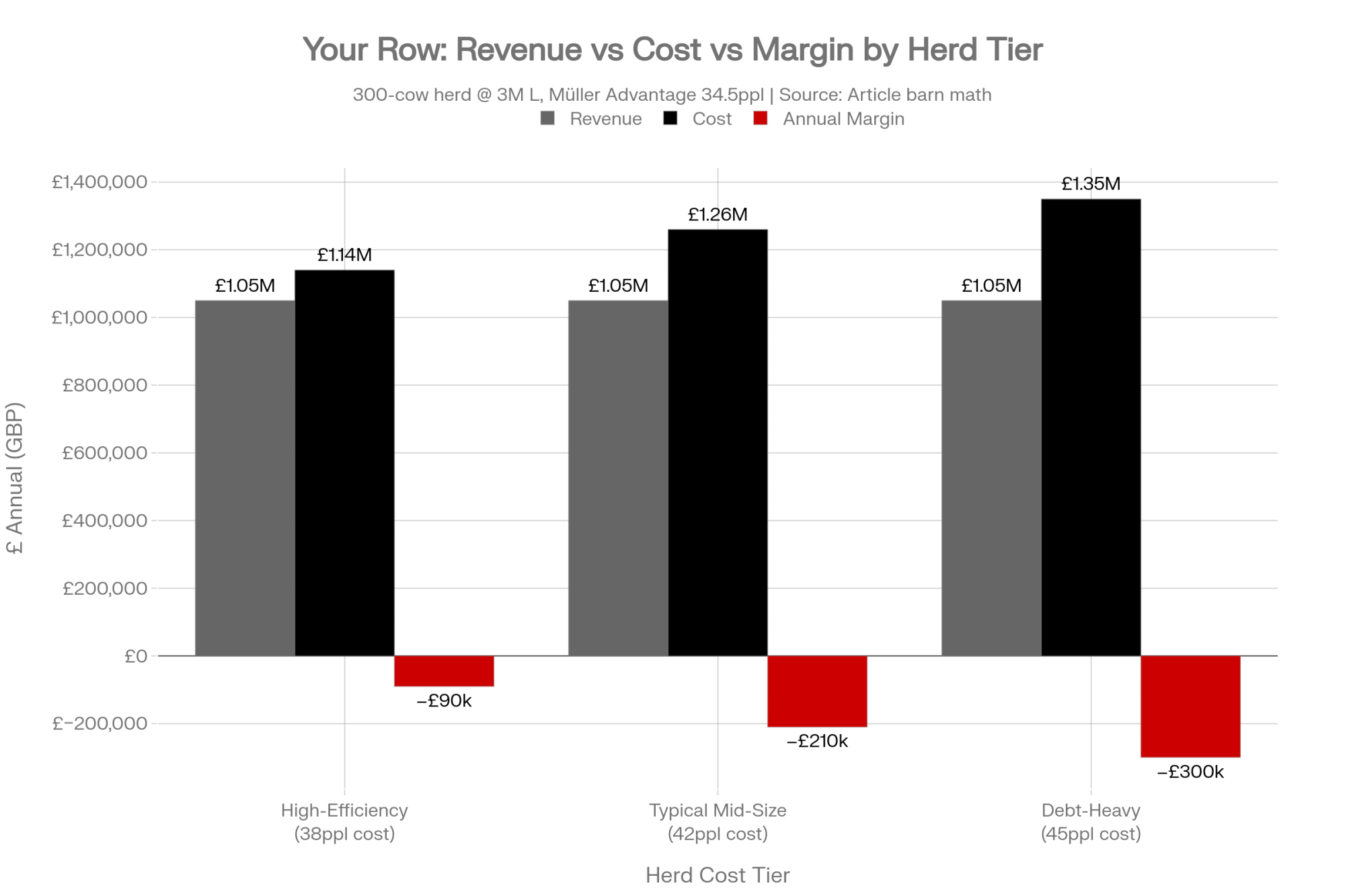

Find Your Tier on One Page

Three illustrative scenarios, same 3.0M-litre herd, same 35ppl contract price. Find the cost band closest to your own books and read down.

Illustrative only — not a benchmark for any named farm. Before you scroll further, decide which of these three rows your last milk cheque actually puts you in.

| Scenario | Revenue (3M L @ 35ppl) | Cost (fully loaded) | Annual Margin |

| High-Efficiency (38ppl cost, 3.0M L baseline) | £1,050,000 | £1,140,000 | –£90,000 |

| Typical Mid-Size (42ppl cost) | £1,050,000 | £1,260,000 | –£210,000 |

| Debt-Heavy (45ppl cost) | £1,050,000 | £1,350,000 | –£300,000 |

The shape holds. The size changes. Higher-yielding 300-cow herds pushing 3.2–3.3M L should re-run the High-Efficiency row on their own litres before drawing conclusions. When you read the £26M Estate Dairy headline after looking at your own bank statement, the emotional math can feel worse than the financial math — and the first honest move is knowing which row you’re standing in.

How Does a 12-Month Premium “Experiment” Actually Hit Your Cashflow?

On paper, “go premium” almost always looks better than “stay commodity.” That’s what makes it dangerous.

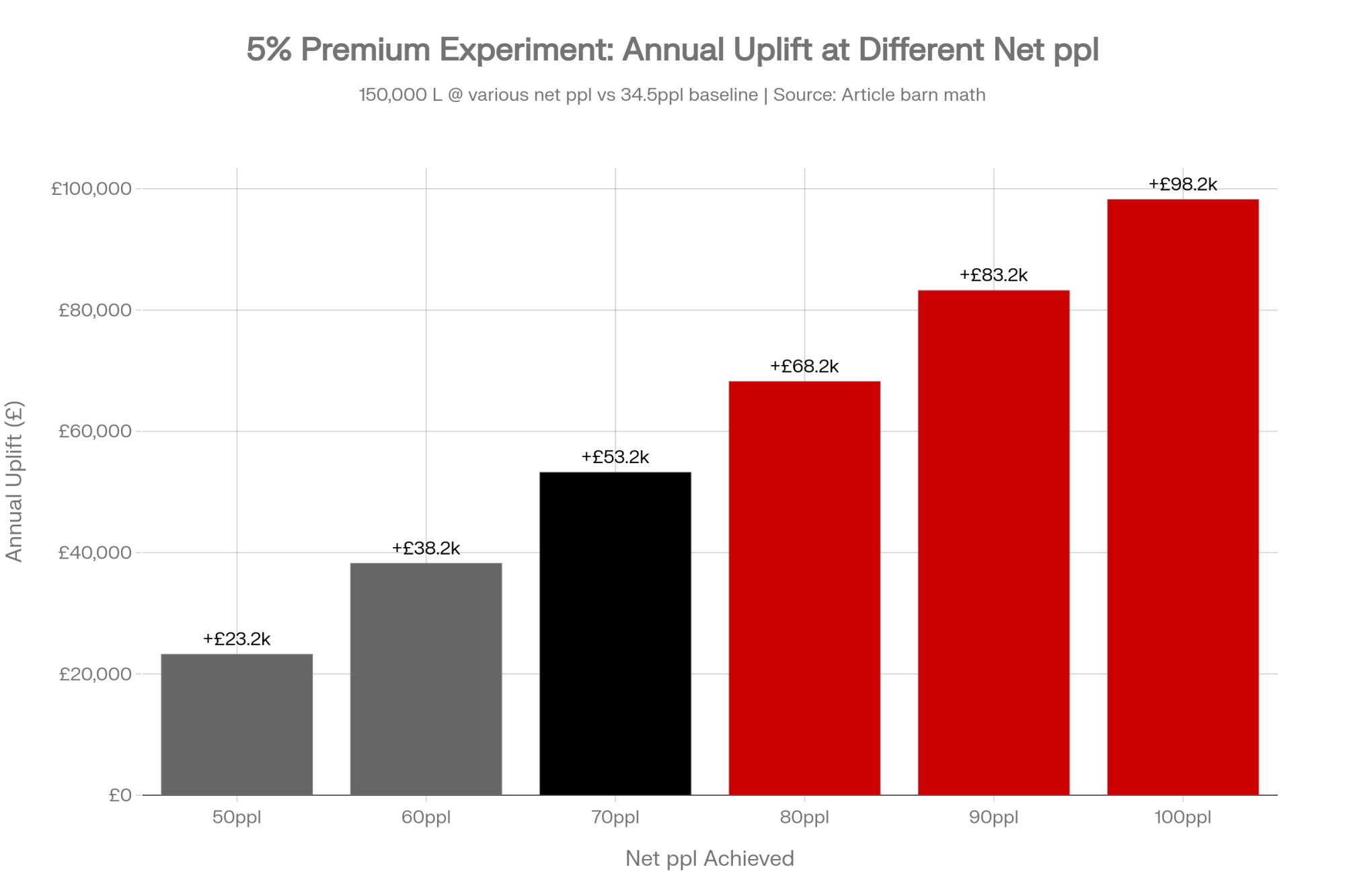

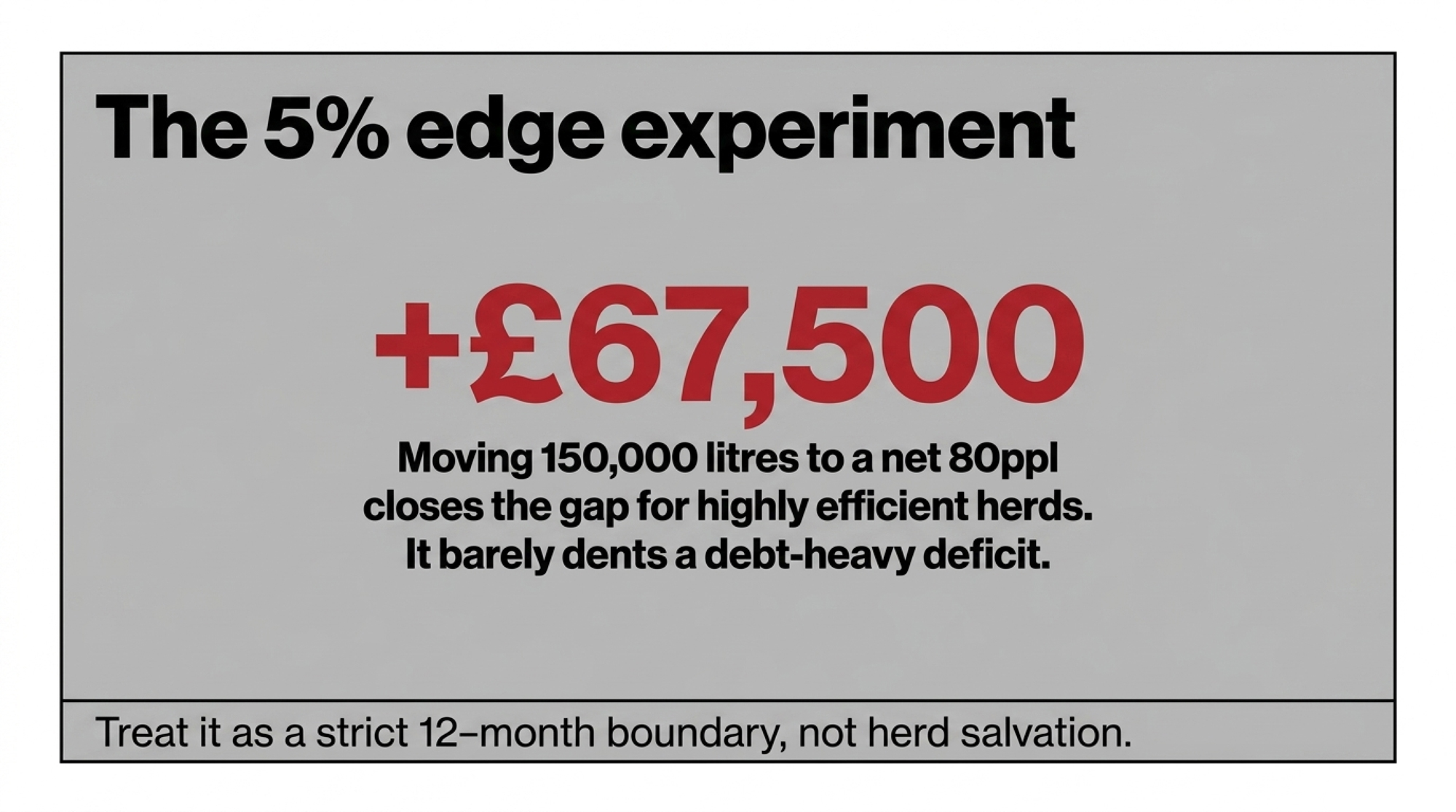

Say your herd is in that 3.0M-litre zone and you decide not to go all-in. You’ll test the waters with 5% of your milk.

- 5% of 3,000,000 L = 150,000 litres.

- At contract, 150,000 × 35ppl = £52,500.

- If you can move those 150,000 L at a net 80ppl after packaging, labour, fuel and extras — the kind of margin some UK glass-bottled premium lines report achieving, though published per-litre net margins from GB direct-sales operators remain thin and this figure should be read as illustrative — it brings in around £120,000.

- Upside: roughly +£67,500/year on 5% of your milk.

The upside is real. The road to it isn’t free. You’re buying bottles, labels and crates, maybe a vending unit. You’re building delivery routes or paying someone to run them. And it all lands on top of the deficit rows in the table above.

The Soft Cost Nobody Puts on the Spreadsheet

Every direct-sales plan underestimates the same line item: your time. If even a day a week of your time goes to chasing café invoices and fixing the vending machine, who’s walking fresh cows? A premium margin can be eaten alive by a measurable drop in pregnancy rates — even a couple of percentage points — because the boss was busy being a delivery driver instead of managing the transition pen.

Even when the premium slice eventually works, total cashflow often gets worse before it gets better. If your real monthly gap is already around £17,500 (Typical Mid-Size row) or £25,000 (Debt-Heavy row), extra capex and learning curves can push that wider for a few months while new channels settle. The honest question isn’t “should you try premium?” It’s whether your balance sheet and your management bandwidth can fund 6–12 months of worse-before-better on top of the gap you already carry, without your lender losing patience or your herd losing performance.

Is Your Herd’s Milk Even What Premium Buyers Want?

Estate Dairy didn’t invent its supply story. It bought into one that already existed. Brades Farm’s Jerseys in Lancashire’s Lune Valley are known for rich, high-fat milk and barista-focused work, and Bickfield Farm’s Guernsey herd in Somerset produces the classic “gold top” milk that behaves differently in a glass or a flat white.

Those herds came with fat and protein that make better foam, butter and yoghurt — plus a story buyers can tell: long-established herds, grass-based systems, heritage breeds tied to a specific region. A lot of GB 300-cow herds are built on a different model: Holstein-heavy, often chasing 8,000–10,000+ litres/cow/year, with regular beef-on-dairy use to add calf and cull value, which limits dairy heifers if you suddenly want to pivot the whole herd.

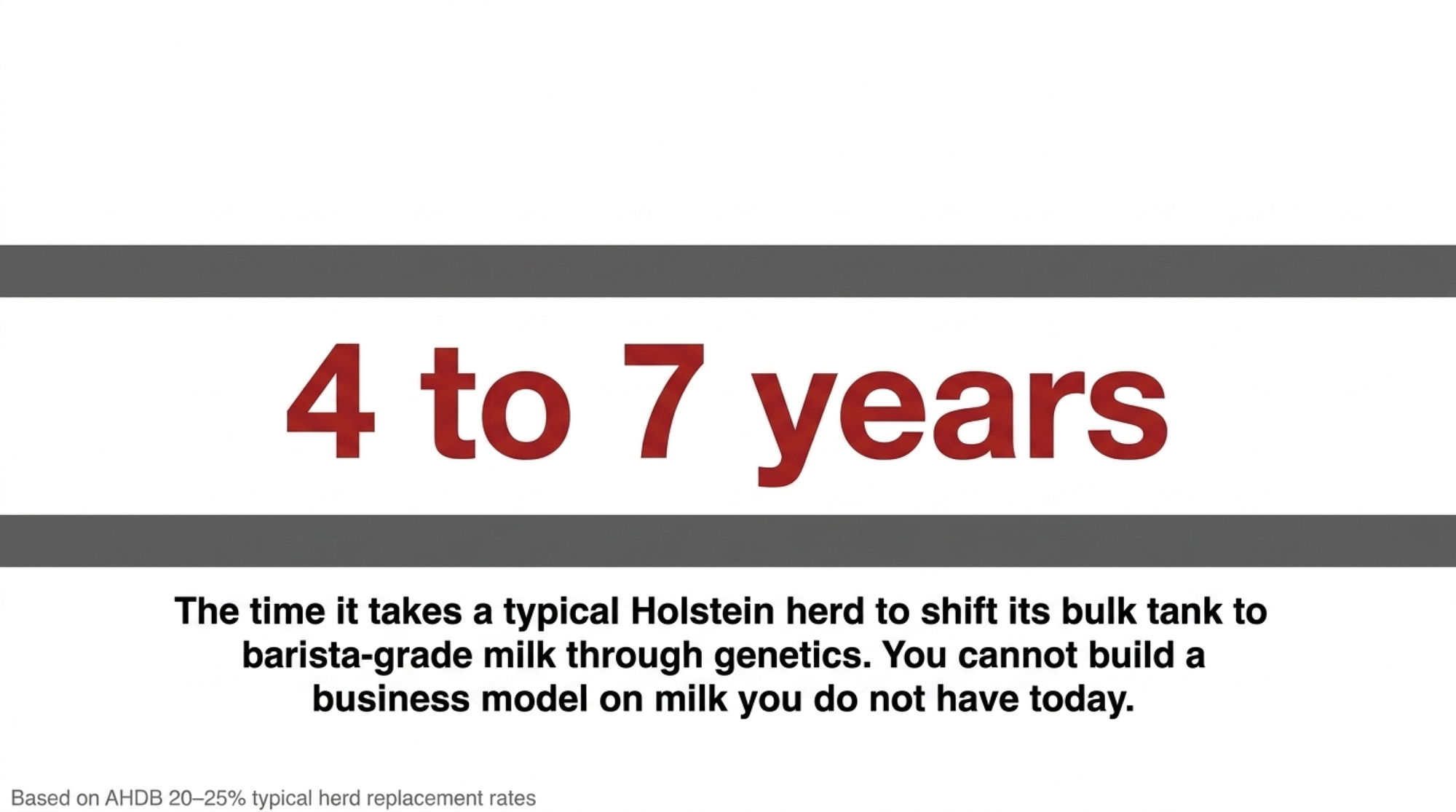

You can shift the profile of your tank — crossbreeding, selection for fat and protein, changing feeding strategy. But with a GB replacement rate typically in the 20–25% range reported in AHDB benchmarking, you’re usually looking at 4–7 years before a new genetic strategy really shows up in the bulk tank.

If the story in your head is, “We’ll flip our Holstein herd into Jersey-type milk in a couple of years and then go premium,” you’re stacking two big bets. Bet one: you can fund the genetic transition while you’re still paid mostly on litres. Bet two: a premium buyer who cares about that new profile will be there at scale when you’re ready. Estate Dairy didn’t wait for genetics. They went and found the milk they needed. That difference matters when you decide how much of their path is even available to you.

Options and Trade-Offs for Farmers

Stop measuring yourself against someone else’s starting line and your choices sharpen. None of these paths are glamorous. All of them are real.

1. Tighten Under the Contract — and Drop the Guilt

When it makes sense:

- You’re already losing money at today’s milk price.

- You’re 12–24 months from contract renewal.

- You don’t have six figures of spare cash for a gamble.

What it requires:

- A blunt look at the books: which row of the table above you actually sit in, and which kit upgrades are habit rather than need.

- A frank talk with your lender: “Here’s cost per litre. Here’s the gap. Here’s what we’re doing about it.”

Risks and limits:

- You’re still exposed to processor cuts.

- This is a “slow the bleed” strategy, not a growth story.

30-day action: print the last 12 months of bank statements and milk cheques. On a single sheet of paper, write down your average monthly gap at today’s price. If you can’t do that in an hour, that’s your first job.

Go deeper: our Tier 3 piece on what happened to GB farms that tried to ride out Müller’s 1ppl cut without changing anything else picks up where this path ends.

2. Try Premium at the Edges, Not the Whole Tank

When it makes sense:

- You can name at least three realistic local buyers — a farm shop, a cluster of cafés, a gelato maker, a small cheese plant — who might pay more for what you already produce.

- You have labour or capital you can risk without missing loan payments.

What it requires:

- Treat it as a bounded experiment, not salvation. “We’ll put 5–10% of our milk and £X of capital into this. In 12–18 months we either have a clear profit or we shut it down.”

- Honest costing of the soft stuff: bottling, cleaning, deliveries, invoice chasing — and whose attention shifts away from fertility, transition and feed while that happens.

Risks and limits:

- Side projects creep. 5% can quietly become 20% if you don’t watch it.

- A vending-machine side business that trims a couple of points off your pregnancy rate isn’t a win — it’s a distraction with a logo.

Barn-math example: shift 150,000 L (5% of 3.0M) from 35ppl to a net 80ppl after extra costs. That’s roughly +£67,500/year. On its own, it won’t fill the Typical Mid-Size –£210,000 row or the Debt-Heavy –£300,000 row. Paired with tight cost control, it can close most of the gap on the High-Efficiency row.

30-day action: write a short list of who within 30 miles would pick up the phone if you offered something different. If you can’t fill that list with real names, you’re not ready to spend on stainless.

Go deeper: our case study on how one GB farm kept 95% of its milk on contract and still made a vending machine pay in 12 months shows what a disciplined edge experiment actually looks like.

3. Plan a Controlled Glide Path Instead of a Crash

When it makes sense:

- Age and family plans make a 10-year turnaround unlikely.

- You care more about protecting equity and health than about the size of the herd on your funeral card.

What it requires:

- A 3–5 year plan with your bank and your family: freeze non-essential capex, keep the unit tidy and saleable, pay down what you can, and pick a window to sell cows and machinery while they still hold value.

- The guts to say “enough” before the lender says it for you.

Risks and limits:

- Emotionally brutal. It can feel like walking away from generations of work.

- Resist jumping back in when milk blips up for a few months.

Reframe what “winning” looks like. Exiting with your land, machinery and cow values substantially intact is not losing — it’s walking away with capital in hand. A forced liquidation by an administrator or a fire-sale dispersal under bank pressure typically turns far less equity into cash than a planned, well-timed exit on your own calendar. One path ends with something left to pass on. The other doesn’t.

Talk to enough GB 300-cow operators and you hear the same thing: hard work doesn’t scare them. Betting the kids’ future on a shiny new bottling line that may or may not pay? That’s what really weighs on them.

30-day action: book a two-hour session with your accountant and your bank manager in the same room. Walk them through your land vs kit-finance split, your cull and machinery values, and ask one question out loud: “If we chose to glide out over five years starting this autumn, what does the best-case exit balance sheet look like?”

4. Go Big on Premium — Only If the Runway Is Real

When it makes sense:

- Most of your debt is secured against land, not short-term kit finance.

- You have strong reserves or credible outside backing.

- You can name specific buyers who need what you could produce — not a vague sense that “people will pay more.”

What it requires:

- A phased plan, not a leap. Secure one or two anchor customers first — a cluster of independent cafés, a regional foodservice wholesaler. Size your first processing kit to those customers, not your entire herd. Consider retail only once you can move product consistently and stay on top of compliance.

Risks and limits:

- Specialist coffee and high-end hospitality already have suppliers like Estate Dairy. You’re not filling an empty niche — you’re asking someone to switch.

- A mis-timed plant investment can sink a business faster than a bad milk cheque.

30-day action: map your existing relationships — chefs, retailers, wholesalers — and ask, quietly: “If we built this, would you sign a contract, and for how much volume?” If the answers are vague, hit pause.

Key Takeaways

- If your fully-loaded cost puts you in the Debt-Heavy row (–£300,000/year), a big premium pivot isn’t “bold” — it’s reckless. Tighten under the contract or plan a controlled exit instead.

- If you’re in the High-Efficiency row (–£90,000/year), a +£67,500 edge experiment can credibly close most of the gap when paired with cost discipline — but only with hard limits on volume, capital and timeframe set before you start.

- If most of your debt is tied to parlour, robots and sheds rather than land, your runway for a 6–12 month “worse-before-better” transition is short. The more repayments depend on today’s litres, the less room you have for a bet that temporarily reduces them.

- If you can’t name three realistic local buyers within driving distance who would pay more for what you already produce, you’re not “behind” on premium — you just don’t have a market yet.

- If your breeding and replacement plan means 4–7 years to shift your tank’s profile, don’t build a business model that assumes Jersey-style milk is two winters away.

- If a planned 3–5 year glide path preserves more land, cow and machinery equity than a forced liquidation would, that’s a win in cash terms — not a defeat in identity terms.

| Strategic Path | Best-fit scenario | 12-month cash requirement | Biggest hidden risk | 30-day action |

|---|---|---|---|---|

| Tighten under the contract | Cost sits near 38–40ppl; within 12–24 months of renewal | Minimal capex; focus on cost cuts | Still exposed to processor cuts; no upside | Print 12 months of bank statements + milk cheques onto one sheet |

| Premium edge experiment (5% of tank) | Can name ≥3 local buyers; 150,000 L available | £15,000–£40,000 upfront (bottles, crates, labour) | Management time drag drops pregnancy rates; side project creeps to 20% | List real buyer names within 30 miles; no list = not ready |

| Controlled glide exit (3–5 yr) | Age/succession makes 10-yr turnaround unlikely; land equity intact | Freeze non-essential capex; no new debt | Emotional — hardest path to hold when milk ticks up for a season | Two-hour session: accountant + bank manager, same room, exit balance sheet |

| Go big on premium | Most debt secured against land; credible outside backing; anchor customer committed | £100,000–£300,000+ for processing kit and working capital | Niche already occupied by Estate Dairy et al.; mis-timed plant investment is terminal | Map existing chef/retailer relationships; ask for a volume commitment in writing |

You can’t control which dairy stories the business pages choose to spotlight. The Youngs’ £5,000-to-£26M arc was always going to make headlines. You can control which game you’re actually playing.

Pull the 12-month milk cheque total, the average ppl and your best estimate of fully-loaded cost, and put them on one page before the end of the week. Find your row in the table above. Then answer the question out loud, in front of the person whose name is also on the loan:

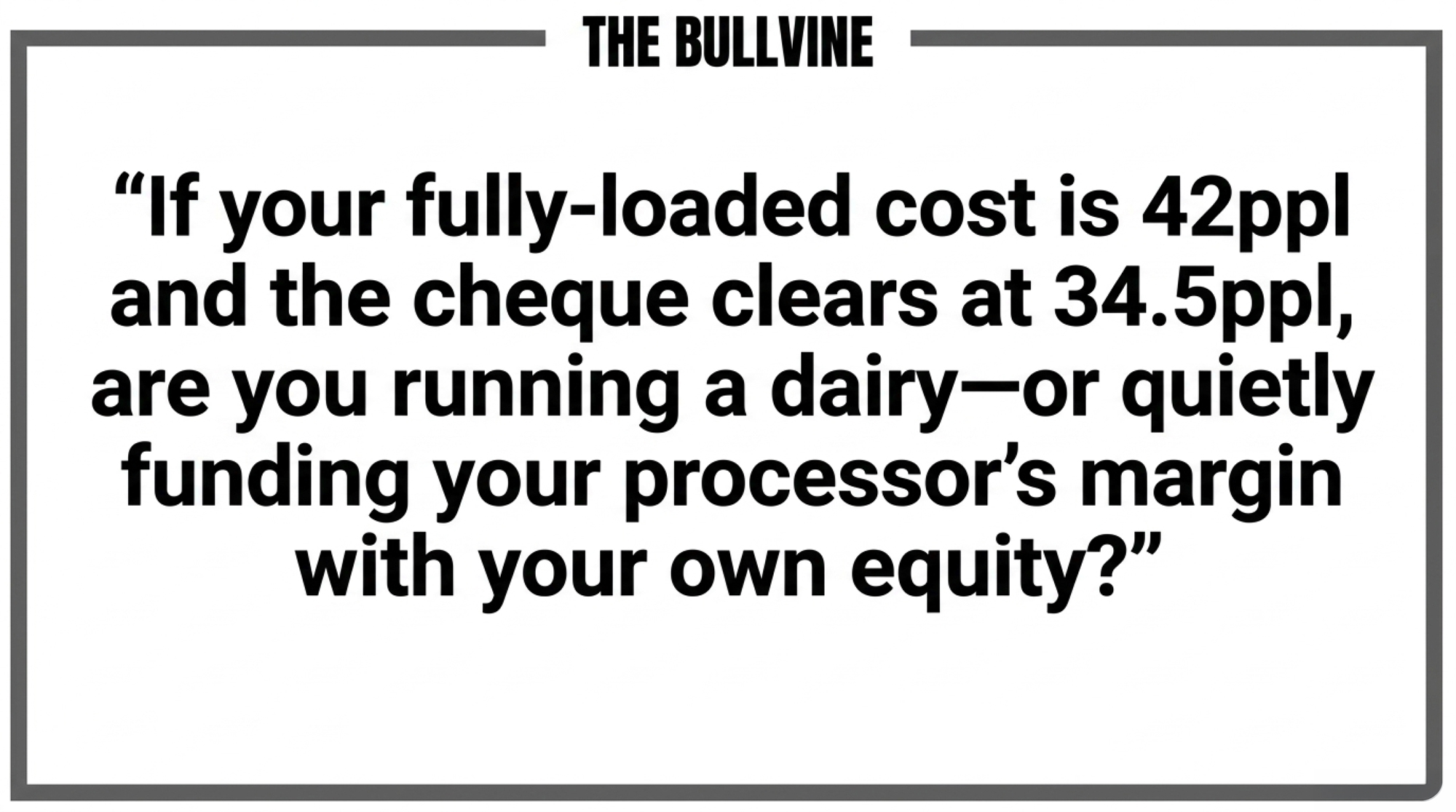

If your fully-loaded cost is 42ppl and the cheque clears at 34.5ppl, are you running a dairy — or quietly funding your processor’s margin with your own equity?

Run Your Numbers

Farm Benchmark Snap Check — Drop in your herd’s litres, ppl, and fully-loaded cost per litre and see which row you’re actually standing in — High-Efficiency, Typical Mid-Size, or Debt-Heavy — before you decide whether to tighten under the contract, experiment at the edges, glide out, or bet on premium.

Learn More

- £187500 Apart: The Contract Clause Deciding Which UK Dairies Survive 2026 — Arms you with the specific contract math that separates survivors from those bleeding cash. Reveals how a 14ppl gap between aligned and non-aligned deals strips £187,500 from your margin while costs hover near 49ppl.

- £368m, Arla, Müller and 6.8% More Milk: Which UK Herds Are They Really Betting On? — Dismantles the myth that more milk fixes low margins. Exposes why processors are betting £368 million on new capacity while mid-sized herds face a structural squeeze, forcing a choice between scale, repositioning, or exit.

- After 75 Years and 850 Doorsteps, One Number Forced Cooil’s Dairy to Choose – How Close Are You? — Delivers a raw reality check on direct-to-consumer sales. Follows the money on vending machines versus cooperative supply, proving that even a 75-year doorstep legacy can’t outrun a retail channel that no longer pays its way.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.