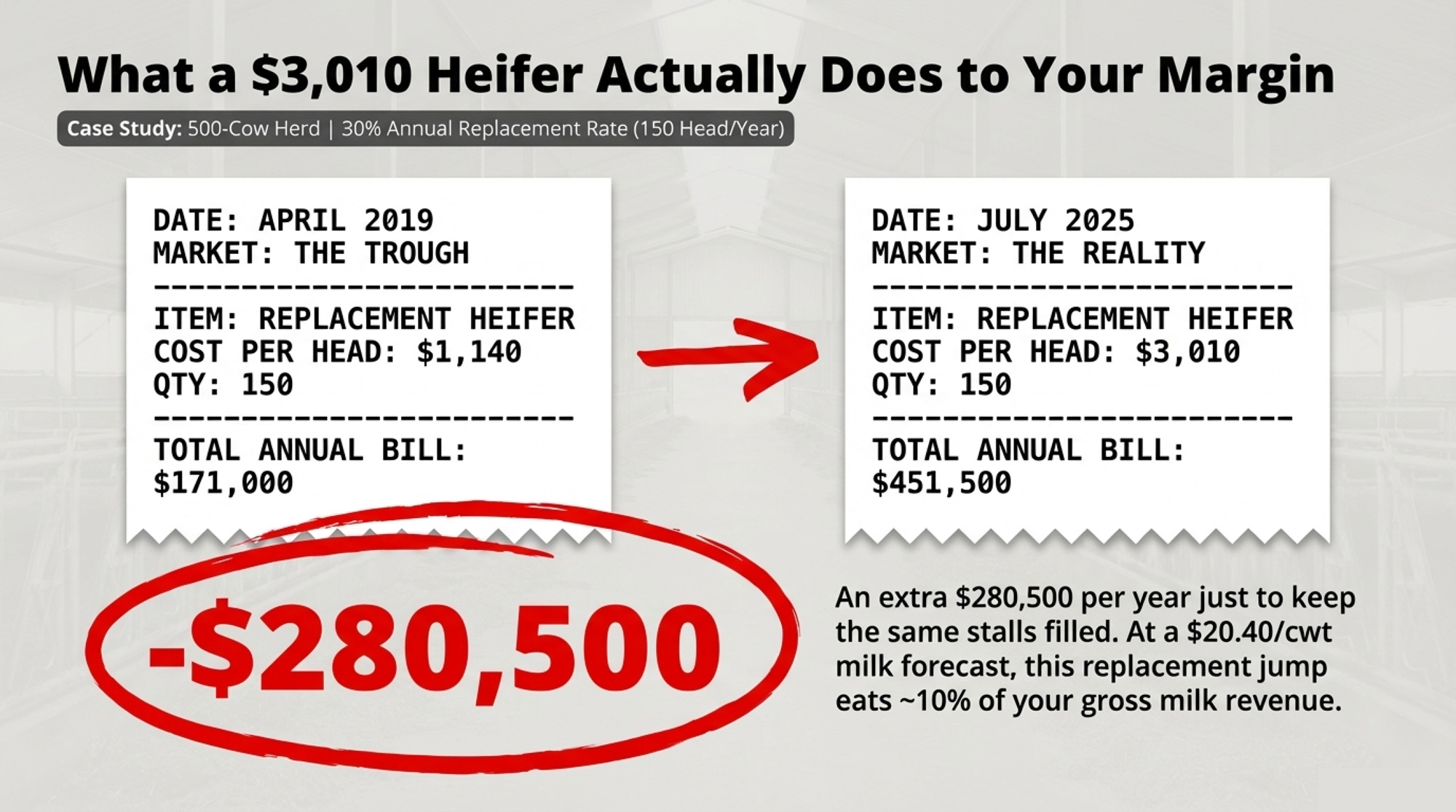

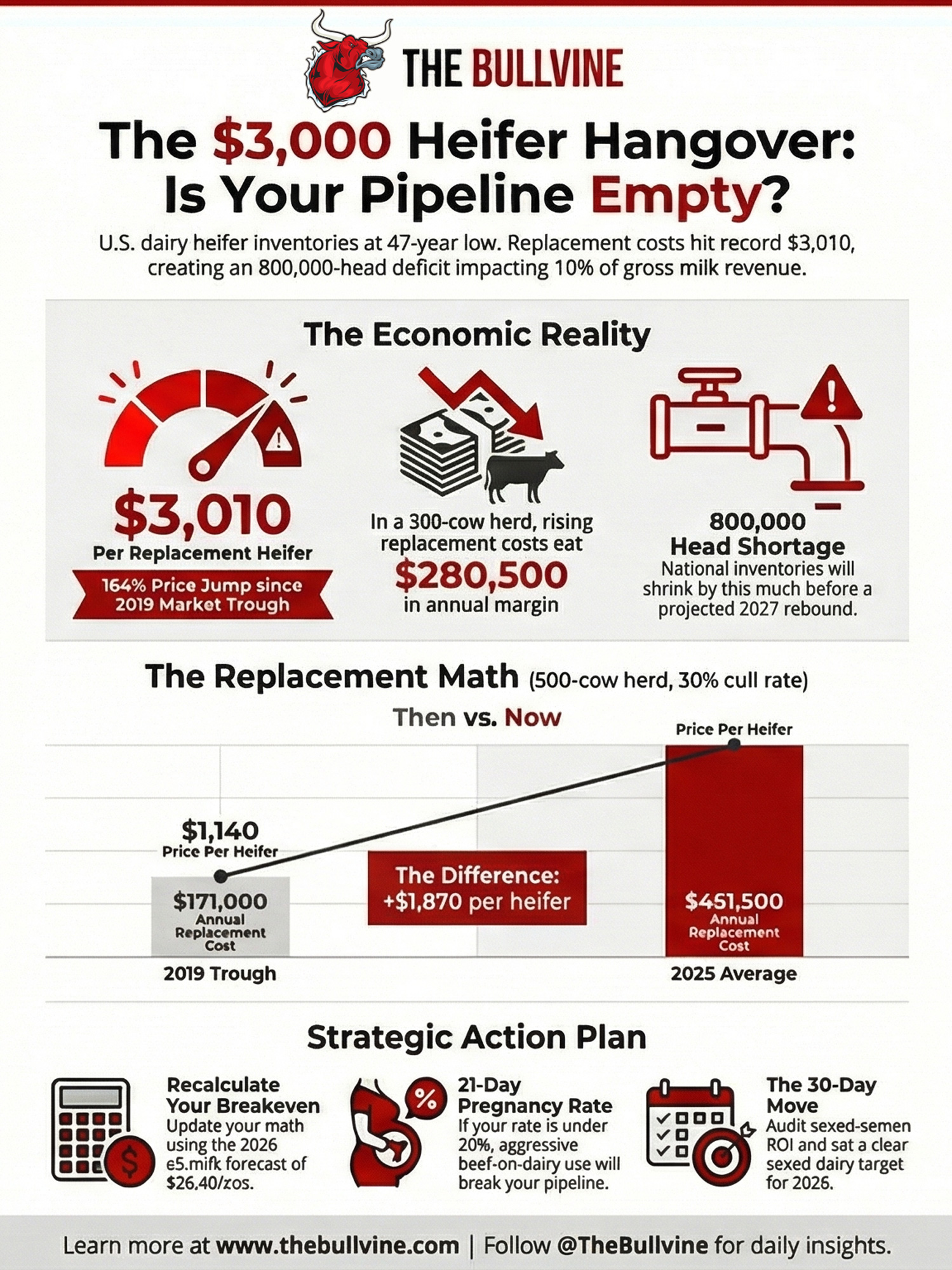

On a 500‑cow herd, the jump from $1,140 to $3,010 per replacement eats $280,500 a year — roughly 10% of your gross. Have you recalculated your breakeven yet?

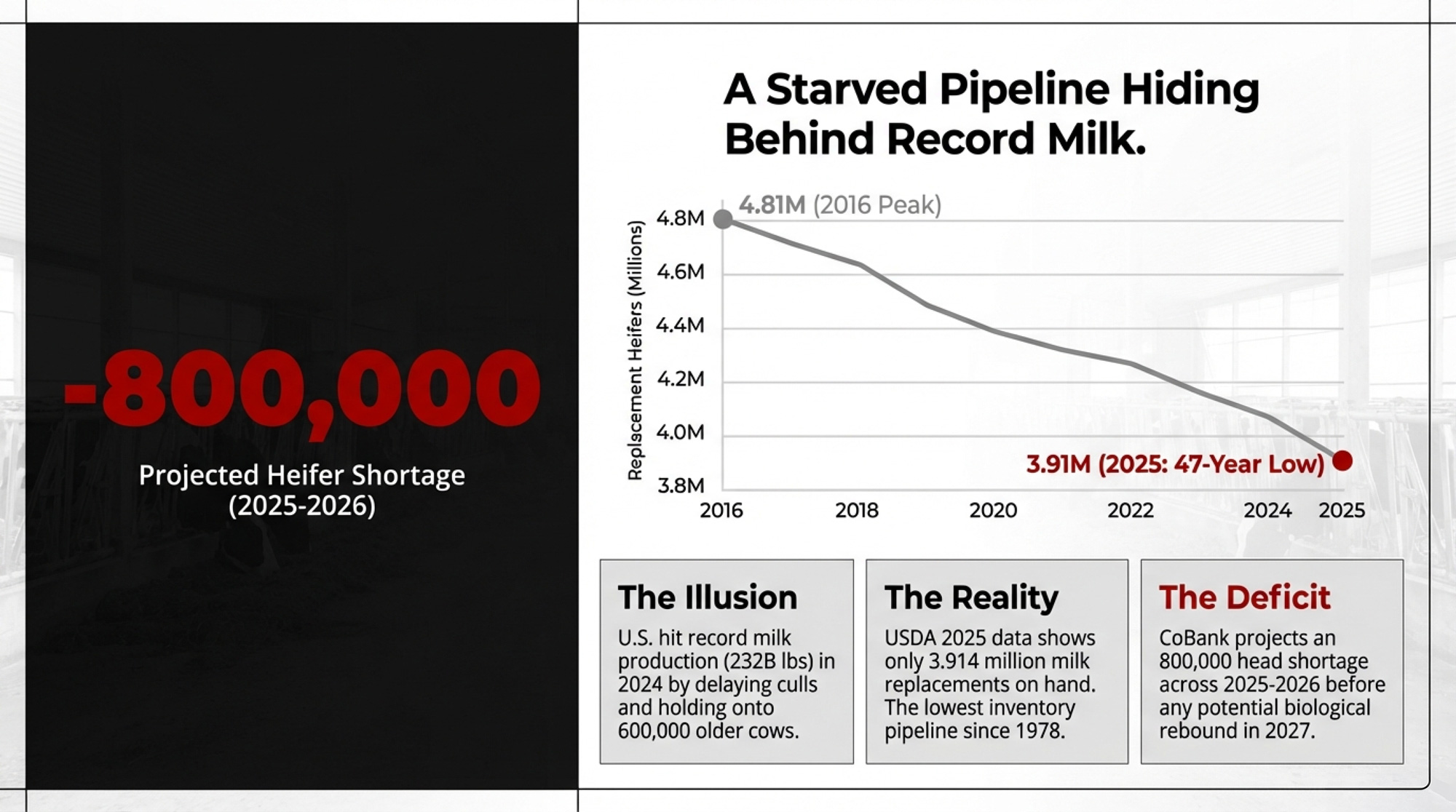

Executive Summary: Average U.S. replacement heifers just hit about $3,010 per head, and CoBank says the national pipeline will shrink by roughly 800,000 heifers before any rebound in 2027. USDA’s 2025 data shows 3.914 million milk replacements on hand — the lowest since 1978 — even as total milk climbed to 232 billion pounds on 9.50 million cows averaging 24,390 pounds each. For a 500‑cow herd replacing 30% annually, the jump from $1,140 to $3,010 per heifer adds about $280,500 a year in replacement cost, which is close to 10% of gross milk revenue at $20.40/cwt. Beef‑on‑dairy and heavy use of beef semen (7.9 million units on dairy in 2024) filled calf pens but quietly drained the heifer pipeline, especially in fast‑growing states like Kansas, South Dakota, Idaho, and Texas. The article walks through JDS modelling, NAAB semen data, and real farm examples to show when beef‑on‑dairy works, when it backfires, and how your 21‑day preg rate and semen mix determine whether you’ll have enough 2028 replacements. You’ll see three clear paths — lock the pipeline, choose margin over size, or push expansion — each with a 30‑day move you can take now so $3,000 heifers don’t quietly eat what’s left of your margin.

Record 2025 milk production was built on one of the thinnest heifer pipelines in decades — and over the next 12–18 months, herds from Kansas to the Upper Midwest will find out if their replacement math holds or breaks.

Ken McCarty of McCarty Family Farms still remembers trying to sell Holstein bull calves: “Two for $5” — with no takers. That kind of market teaches you not to count on calf checks to save the milk check. Fast‑forward to 2024–25, and beef‑on‑dairy calves are bringing $600, $1,000, even $1,400 a head in some barns. It feels like someone finally turned on a faucet that’d been stuck dry for years. (Read more: The McCarty Magic: How a Family Farm Became the Dairy Industry’s Brightest Star) But there’s a bill attached, and it’s landing in the form of four‑figure replacement heifers and a national heifer pipeline CoBank says will be roughly 800,000 head short of where it needs to be before a hoped‑for rebound in 2027.

If you milk cows in the U.S. right now — 150 stalls in Wisconsin, 1,500 in western Kansas, anything in between — your future herd is being shaped by the replacement math you run (or don’t run) in the next 90 days.

We traded our future for a quick calf check. Now the bill is coming due in empty stalls. That’s what the $3,000 hangover feels like when your heifer string is thin, and the sale barn is picked over.

Record Milk on a Starved Heifer Pipeline

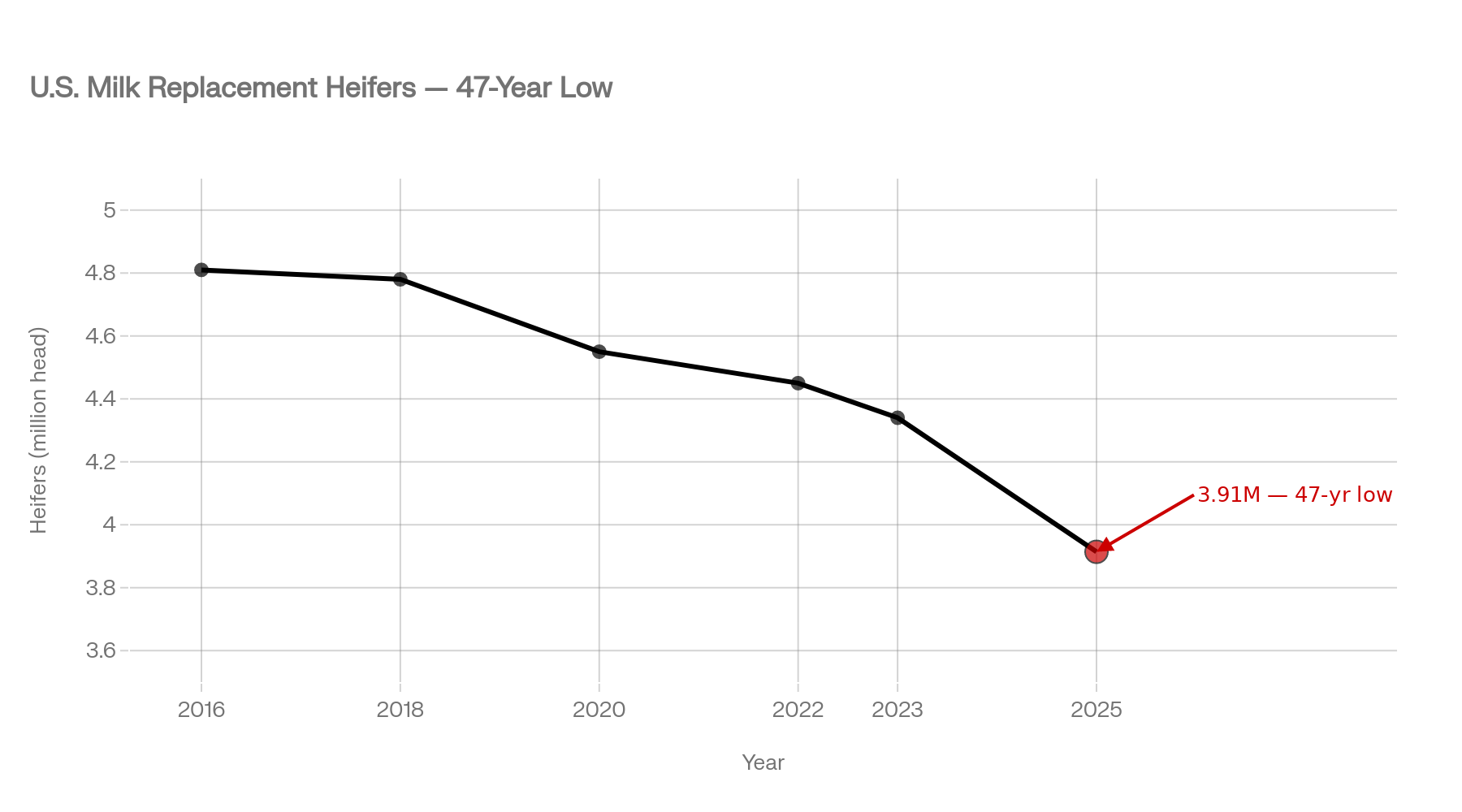

USDA’s January 2025 Cattle report shows where the real squeeze is. On Jan. 1, 2025, there were 3.914 million milk replacement heifers, down from 4.34 million just two years earlier and roughly 4.78 million in 2018, and well below the 2016 peak of 4.81 million. Farm Progress put it plainly: dairy replacement heifers have tumbled to a 47‑year low.

CoBank’s August 2025 heifer report, built on those USDA inventories, projects the gap at 357,490 fewer dairy heifers in 2025 and another 438,844 fewer in 2026 — roughly 800,000 missing replacements across a two‑year window — before inventories begin to rebound sometime in 2027. As CoBank economist Corey Geiger put it: “We don’t see a rebound until 2027, and that will be up 285 thousand, but you’ve got to remember, that’s going to be after 800 thousand fewer heifers.”

Meanwhile, the top‑line production numbers look deceptively strong. USDA’s annual Milk Production summary, released February 20, 2026, puts 2025 U.S. milk production at 232.0 billion pounds, up 2.6% from 226.1 billion in 2024. The national milking herd averaged 9.50 million head for the year — up 153,000 from 2024. Milk per cow hit 24,390 pounds, up 218 pounds from 2024’s 24,172. Since 2016, total milk has climbed about 9%, while per‑cow output has risen roughly 7%.

Those extra pounds didn’t come from a lush crop of young cows behind the string. They came from hanging onto cows that, in any other cycle, would’ve been on a truck. CoBank’s analysis and slaughter data note dairy producers sent over 600,000 fewer cows to slaughter from late 2023 through 2024 as they tried to cover plant needs without the replacements to support normal culling. You bought time with older cows because the young stock to replace them either wasn’t there or wouldn’t pencil at current prices.

The industry celebrated record milk. It should’ve been counting heifers.

How Beef‑on‑Dairy Helped Create an 800,000‑Head Hole

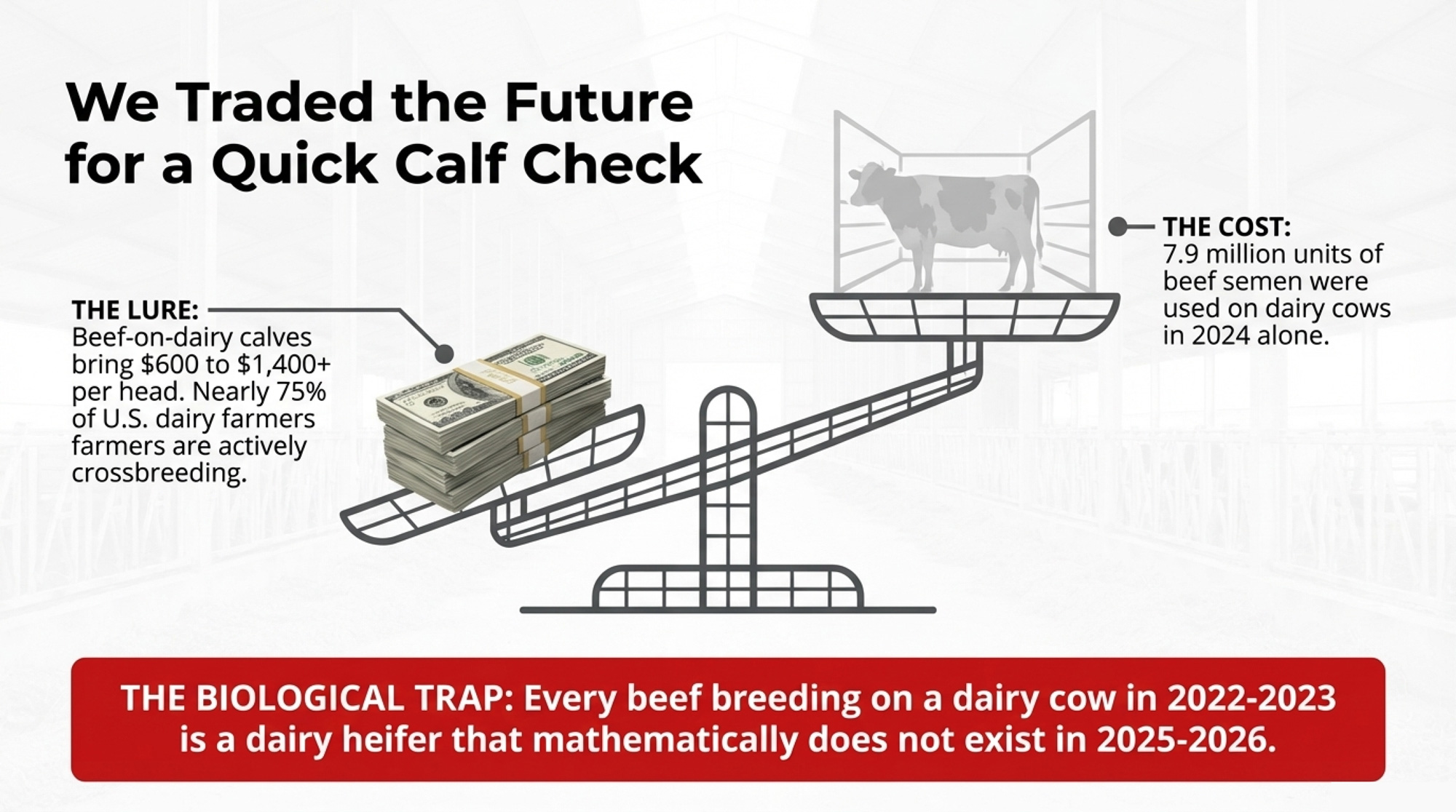

The flip side of McCarty’s “two for five” story is the beef‑on‑dairy boom that followed. When Holstein bull calves couldn’t draw a bid, it made perfect sense to chase a calf check that finally moved the needle. By 2024–25, sale reports around the country had beef‑on‑dairy calves bringing $800, $1,100, even $1,400 — with some two‑ and three‑day‑old calves fetching about $1,000 in the Northwest, as Ever.Ag’s Mike North told Brownfield. That kind of money is hard to say no to when milk margins are thin.

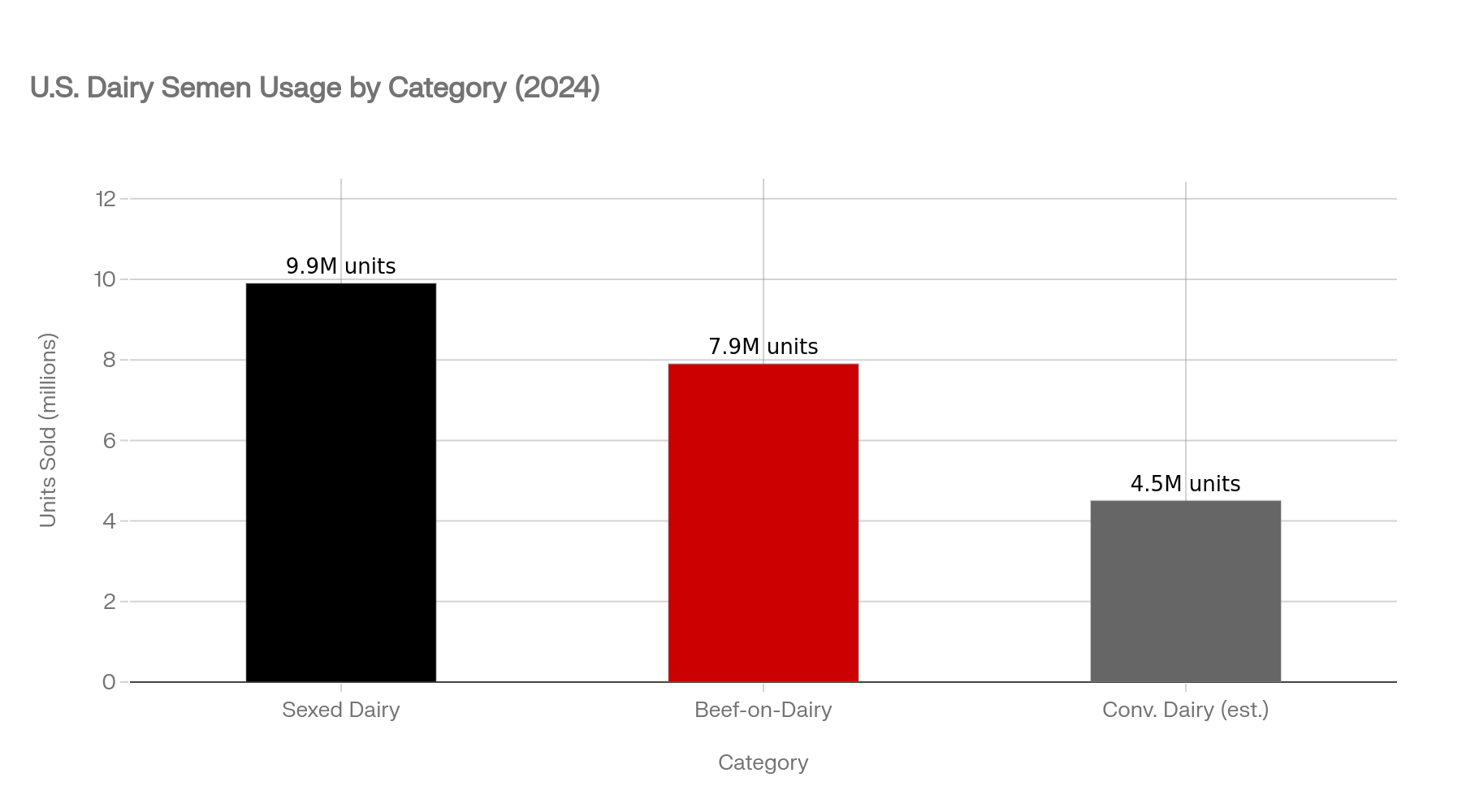

A 2024 Purina survey found that almost three‑fourths of U.S. dairy farmers now actively crossbreed dairy cows or heifers with beef cattle, with another 16% considering it. NAAB’s 2024 year‑end semen report shows just how far the shift has gone: gender‑selected dairy semen hit about 9.9 million units, up roughly 1.5 million from the year before, while beef semen sales reached 9.7 million units, with 7.9 million of those used on dairy cows and heifers. Sexed dairy is now the largest semen category — and beef‑on‑dairy is firmly entrenched alongside it.

On paper, the strategy looks balanced: more sexed dairy on your best females, beef on the bottom end. On the national ledger, it didn’t balance out. CoBank’s “Dairy Heifer Inventories to Shrink Further Before Rebounding in 2027” lays it out: even with more sexed dairy semen in the mix, three straight years of aggressive beef‑on‑dairy use shrank the replacement pipeline heading into 2026.

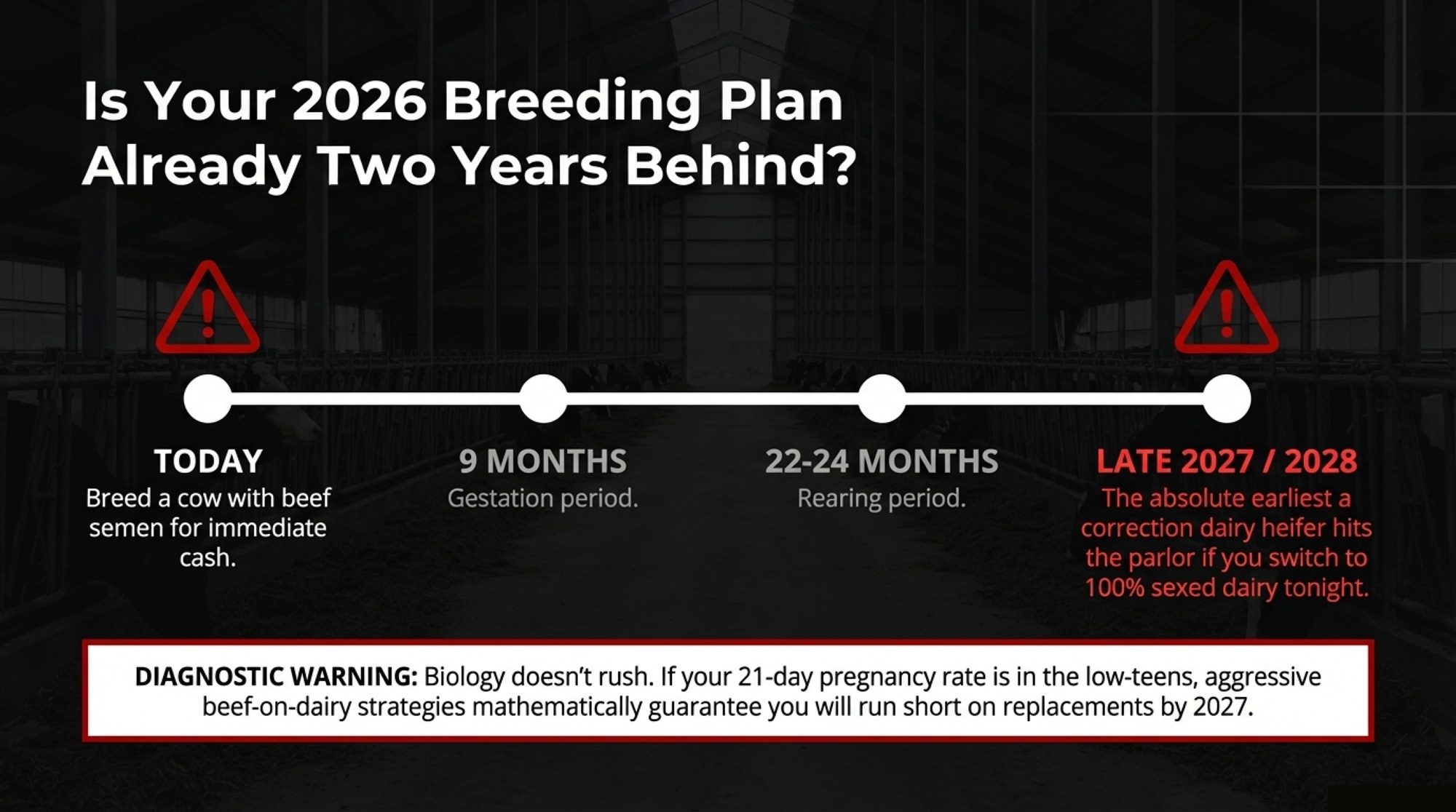

And biology doesn’t rush. You’ve got conception, nine months of gestation, then roughly 22–24 months of rearingbefore a heifer freshens. Even if every dairy flipped to all‑dairy semen tonight, the first real wave of “correction” heifers wouldn’t be hitting parlors in bulk until late 2027 and into 2028 — right around the time CoBank expects inventories to begin rebounding.

Every beef breeding on a dairy cow in 2022–23 was a dairy heifer that doesn’t exist in 2025–26. You can’t dodge that math now.

What Does a $3,000 Heifer Actually Do to Your Check?

Here’s where the hangover shows up in plain numbers.

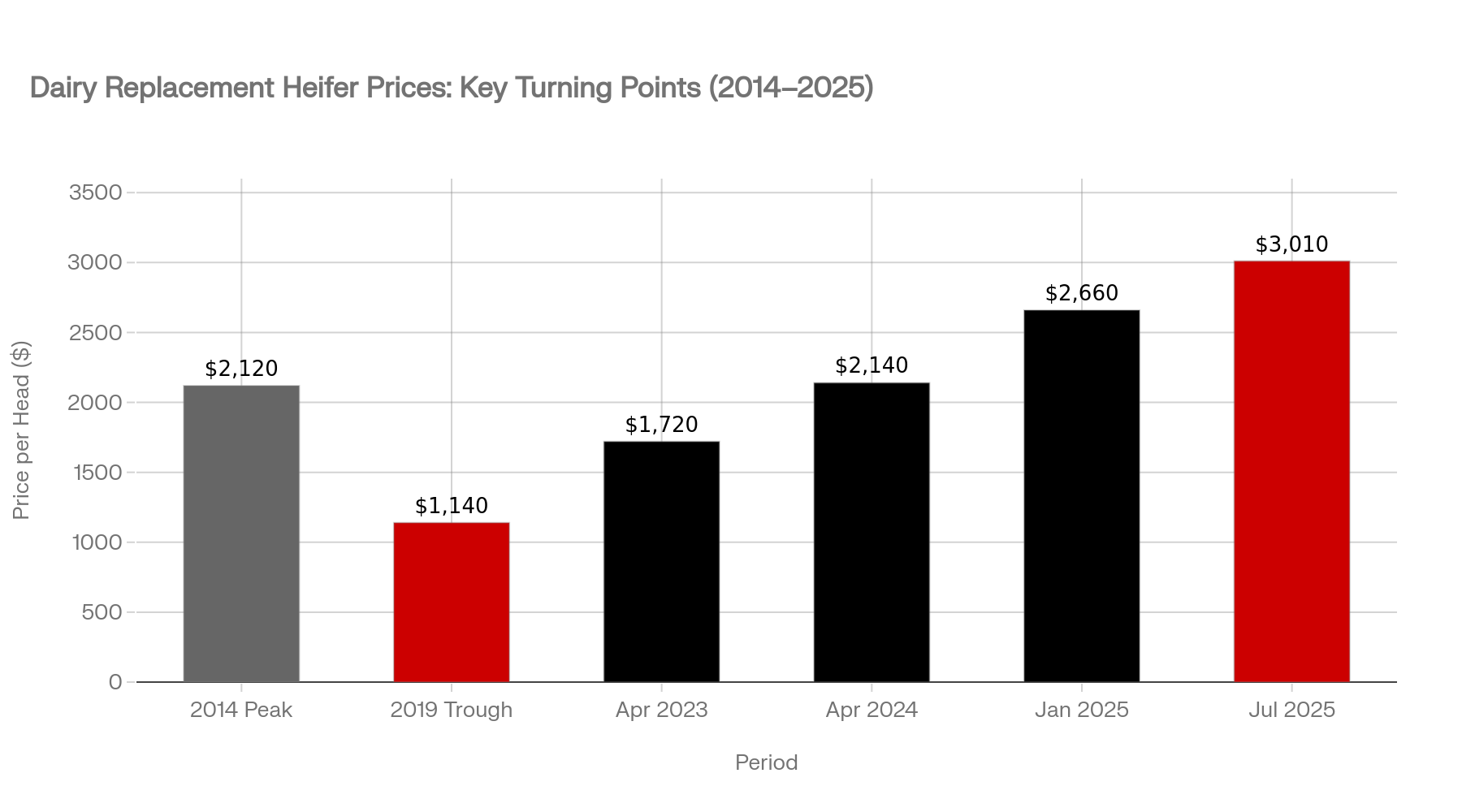

CoBank’s Geiger, using USDA Agricultural Prices data, traced the replacement arc across a decade. Dairy replacement values peaked at $2,120 per head in October 2014, then fell nearly $1,000 over five years to settle at $1,140 by April 2019 — a price so low that those heifers were arguably worth more as beef than as future milk cows. It took almost a decade for prices to claw back. By April 2024, values had climbed to $2,140 — the same level as the 2014 peak — then pushed higher to $2,660 by January 2025 as tight inventories, not windfall milk margins, drove the move. By July 2025, Geiger says values hit an “unforeseen threshold” of $3,010 per head — a 164% jump from the 2019 trough and about 75% higher than the $1,720 reading in April 2023.

Those USDA averages still lag what some barns are seeing. Geiger notes “high‑quality Holstein replacement heifers have routinely fetched over $3,000 per head, with some premium heifers receiving over $4,000 per head in California and Minnesota auctions.” North told Brownfield that “some animals moving in the northwest last week were north of $4,000 an animal.” That’s not theory. That’s the check producers are writing today.

Now drop that onto a herd you can actually picture. Take a 500‑cow operation replacing 30% of its string annually — that’s 150 head a year. At the 2019 trough of $1,140 per head, your replacement bill sat around $171,000. At $3,010, it jumps to $451,500. That’s an extra $280,500 per year to keep the same number of stalls filled.

If you’re shipping about 75 pounds per cow per day, that 500‑cow herd moves roughly 13.7 million pounds of milk a year — about 136,900 cwt. At USDA’s 2026 all‑milk forecast of $20.40/cwt, gross milk revenue lands around $2.8 million. That replacement‑cost jump alone chews up roughly 10% of your gross.

USDA‑ERS cost‑of‑production benchmarks Bullvine has highlighted put full‑cost numbers for efficient large herds near $19.14/cwt. Against a $20.40 forecast, that’s about $1.26/cwt of breathing room — before replacements even enter the picture. You don’t have to be a spreadsheet person to see how fast $3,000 heifers chew through that.

Here’s the simple check you can run with your own numbers:

Replacement cost per cwt = (annual replacements × price per head) ÷ total cwt shipped.

If that number has more than doubled since 2019 and you haven’t updated your breakeven, your cash‑flow story and your actual economics are already out of sync.

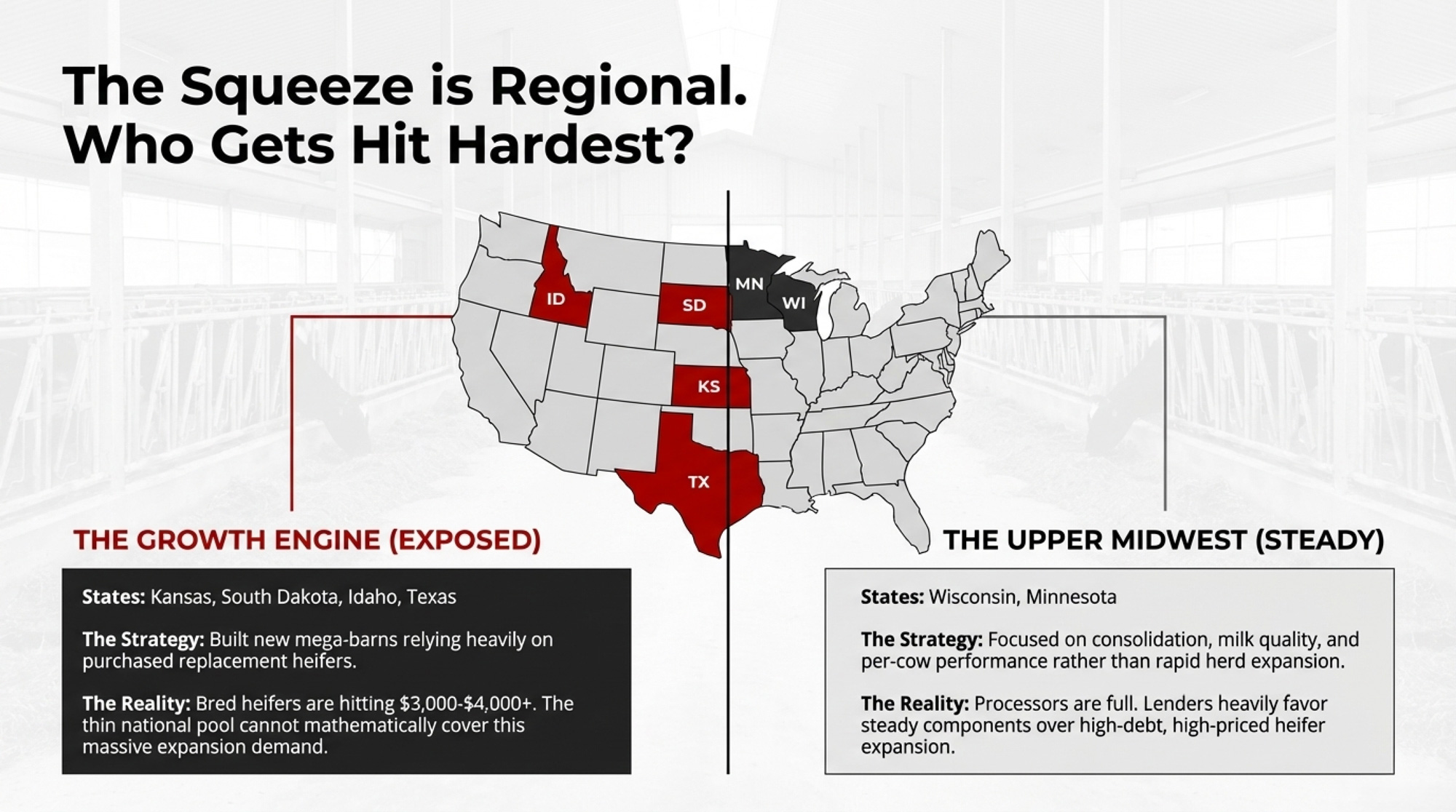

Why Are Heifers So Scarce in the Growth States?

The heifer crunch isn’t spread evenly across the map. It’s piled up hardest in the same places that pushed U.S. milk to new highs.

| State/Region | Cow Count Trend | Heifer Inventory Direction | Replacement Strategy | Risk Level |

|---|---|---|---|---|

| Kansas | Strong multi-yr growth | Shrinking — drawing from national pool | Primarily purchased heifers | 🔴 High |

| South Dakota | +117% over 10 yrs (~215K head by 2025) | Under pressure from rapid expansion | Mixed raised/purchased | 🔴 High |

| Idaho | Large gains — now #3 milk state | Tight; competes with Western demand | Primarily purchased | 🔴 High |

| Texas | Rapid growth then cooling | Lost 10K heifers YoY (USDA data) | Purchased-heavy, margin-squeezed | 🟠 Elevated |

| Wisconsin | Consolidation-led, steady output | Gained 10K heifers YoY | Raised, disciplined culling | 🟢 Lower |

| Minnesota | Efficiency-led, steady | Stable — processor relationships strong | Raised, component-focused | 🟢 Lower |

Kansas has been one of the big growth engines. CoBank and regional coverage point to strong multi‑year expansion in Kansas milk output, driven by new barns and new processing plants in the southwest part of the state. Those cows have to come from somewhere, and more of them are being purchased rather than raised.

South Dakota is the poster child. Over the past decade, its dairy cow population has increased by about 117%, reaching roughly 215,000 head by 2025, fueled by expansions at processors like Valley Queen Cheese and Agropur and a concerted state‑level push to become a dairy corridor. Idaho added tens of thousands of cows and overtook Texas to become the No. 3 milk state, while Texas itself surged before weather and margin pressure cooled its growth.

Geiger warns that this draws on a thin heifer pool and, combined with roughly $10 billion in new U.S. dairy processing investments expected to come online through 2027, creates a looming pinch point for both farms and plants. Regions like Kansas, Texas, Idaho, and the I‑29 corridor are leaning hardest on a national heifer pool that’s at one of its lowest levels in nearly five decades. In some of those markets, bred heifers are bringing $3,000–$4,000 and still not covering all the demand.

The Upper Midwest has quietly taken a different path. USDA state numbers show Wisconsin and Minnesota together contributing a major share of national milk output, with growth coming mostly through consolidation and better performance per cow, not a rash of brand‑new mega‑barns. Wisconsin’s heifer inventory actually gained 10,000 headyear‑over‑year, while Texas lost 10,000, according to USDA data cited in Bullvine’s $3,010 analysis. That divergence comes down to processor relationships and infrastructure, not just breeding decisions.

In that Upper Midwest milkshed, processors and lenders talk constantly about quality and consistency. Compeer Financial’s Curtis Gerrits told Brownfield that Upper Midwest processors “are at a point where their farmers are doing such a great job and getting great high‑quality milk and a good amount of milk out of those animals that our processors are relatively full.” In a tight replacement market, those steady herds — strong components, disciplined culling, controlled expansion — often look better to lenders and plants than operations that depend heavily on debt‑financed growth and high‑priced purchased heifers.

Growth states chased cow numbers just as the replacement pipeline was thinning. Steady regions tightened up and let efficiency do more of the work.

What Does a $3,000 Heifer Do to Your 2028 Herd?

This is where your breeding sheet and the calendar slam into each other.

Every service you write this spring won’t show up in the parlor until late 2028 at the earliest. The heifers that will freshen in 2027 were mostly conceived in 2024–25, when beef‑on‑dairy was hottest and sexed semen use was still catching up. If your 2026–27 heifer crop already looks thin, you’re staring at decisions you made a couple of breeding seasons ago.

Economic modelling in the Journal of Dairy Science backs up what a lot of you can feel without a calculator. In one simulation of a 1,000‑cow Holstein herd, beef semen made the most economic sense when two things were true: beef‑cross calves were worth significantly more than dairy bull calves, and the herd’s reproductive performance stayed strong with targeted use of sexed dairy semen — 21‑day pregnancy rates in the 20–30% range, not in the low‑teens. When repro performance sagged, or sexed semen wasn’t used strategically, the more aggressive beef programs ran short on replacements, even though the calf income looked good on paper.

In Bullvine’s earlier coverage, one Minnesota producer’s allocation illustrated the hedging strategy many herds have adopted: 10% of cows bred to sexed Holstein and 90% to beef; for heifers, a 50/50 split between sexed dairy and beef. On the page, that sounds like a reasonable hedge — some calf revenue, some replacements. In the barn, that kind of allocation can leave one 300‑cow group with extra heifers and another group 20–30 heifers short. At $3,000 per head, that’s a $60,000–$90,000 swing in purchased replacements just from how you’re lining up semen today.

So the question isn’t “Is beef‑on‑dairy good or bad?” It’s “Does your current repro reality and semen strategy actually deliver the heifers you’ll need in 2028 — or are you penciling in daughters that don’t exist?”

Is Your 2026 Breeding Plan Already Two Years Behind?

If you spread your 2026 breeding sheet on the kitchen table tonight, would it set you up with more replacement options in 2028 — or fewer?

If your 21‑day pregnancy rate lives in the high‑teens or lower, that JDS modelling suggests you need to be very cautious about how much beef semen you’re putting on cows — especially if you’re not aggressive with sexed dairy on the right animals. You gain margin from beef‑cross calves today, but you give up flexibility down the road, particularly if you’re in a growth region where every neighbor is trying to buy heifers from the same thin pool.

The herds that will still have room to maneuver in 2028 are making deliberate choices right now:

- Sexed dairy semen on the best animals — cows and heifers — where you actually want daughters.

- Beef is reserved for the bottom end, or strictly for animals you’ve already decided won’t contribute replacements.

- A hard count of how many home‑raised heifers that strategy should deliver each year — and how that compares to your real replacement needs over the next three years.

North told Brownfield he’s already seeing the inflection: “Some animals moving in the northwest last week were north of $4,000 an animal. That’s a pretty tall price, and so now, guess what? We’re seeing people starting to switch some of their breeding back to that replacement animal.” McCarty’s whiteboard this spring looks different from it did when his calves were going two‑for‑five. His family lived the downside of relying on calf checks to backstop the milk check — and at $3,000‑plus per replacement, the stakes on getting that breeding plan wrong have never been higher.

Three Paths — and the 30‑Day Move for Each

Let’s be blunt. You’re probably living one of these strategies already.

| Strategy | Best For… | Key Risk | The “Must‑Do” Now |

| Path 1: Lock the Pipeline | Herds that want steady or modest growth and are willing to carry more youngstock | High heifer‑rearing cost and capital tied up in replacements if prices cool | Audit your sexed‑semen and heifer‑raising ROI at today’s $3,000‑plus values and set a clear sexed‑dairy target for 2026. |

| Path 2: Margin over Size | Stable or mid‑size herds in mature markets with solid processors | Missing upside if milk and premiums improve and plants chase volume | Push components and quality hard enough to be at the top of your plant’s sheet, and put a real ceiling on herd size in your plan. |

| Path 3: Push Expansion | New or expanding facilities tied to fresh processing capacity | Over‑leveraging debt into a market with $3,000–$4,000 heifers and export risk | Stress‑test your 3‑year plan at $19–$19.50 milk, $3,000 heifers, and tighter premiums before you pour more concrete. |

Each column is a gut check. Where you land in that table matters more than what you tell your banker.

For Path 1, you’re choosing control over your replacement pipeline. That means more sexed dairy on your best females, a tighter culling list, and either an in‑house heifer program or a long‑term grower relationship that pencils at current feed and interest levels. The 30‑day move here is simple: sit down with your repro team and lender and decide how many sexed‑dairy pregnancies you actually need in the next 12 months to cover your 2028 replacement needs — then lock in how you’ll raise or contract those heifers at something close to today’s true cost.

For Path 2, you’re accepting a ceiling on cow numbers and choosing to compete on margin. That’s the path many Upper Midwest herds are already on — Compeer’s Gerrits described processors in that region as “relatively full” with high‑quality milk from their existing base. The key risks are missing upside if milk or premiums jump and plants start rewarding volume again, or getting sidelined if processors concentrate on a smaller number of mega‑suppliers. Your 30‑day move: update your breakeven and cash‑flow projections with current replacement and interest numbers — not 2022 figures — and sit down with your processor and lender to explain that holding or slowly shrinking cow numbers is a conscious survival strategy built around components and reliability.

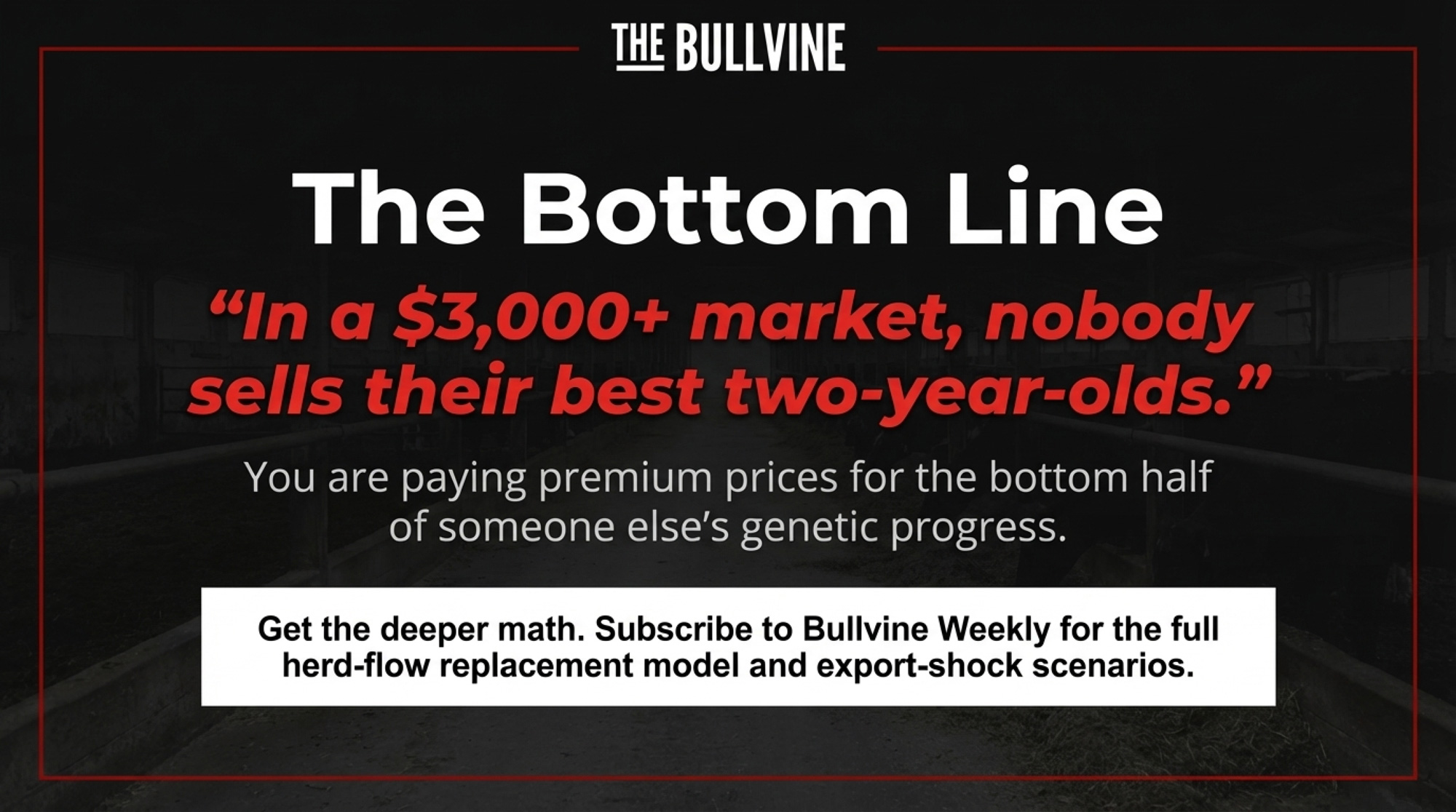

For Path 3, you’re betting that your cost structure, processor relationship, and export demand can carry you through the heifer squeeze. Geiger points to roughly $10 billion in new U.S. dairy processing investments expected through 2027. U.S. dairy exports hit about $8.2 billion in 2024, one of the strongest years on record. That combination only works if export buyers keep writing checks, and your plant still needs every pound you can ship. Your 30‑day move is to run an honest stress test with your lender: what happens to your principal and interest coverage if all‑milk settles closer to $19–$19.50/cwt, replacement prices hold near $3,000 per head, and your base or premiums tighten by 10–15%? If those numbers don’t work on paper, they won’t work in the barn. In a $3,000+ market, remember: nobody sells their best two-year-olds. You are paying premium prices for the bottom half of someone else’s genetic progress.

Key Takeaways

- If your replacement cost per cwt has more than doubled since 2019, recalculate your breakeven using today’s heifer values and the 2026 all‑milk forecast of $20.40/cwt — then take that updated math to your lender before the next renewal meeting.

- If your 21‑day pregnancy rate is stuck in the high‑teens or lower, be cautious about how much beef semen you’re putting on cows; JDS modelling makes it clear that with weaker repro, aggressive beef strategies run short on replacements even when calf prices are strong.

- If you’re buying replacements at $3,000‑plus and your total replacement cost per cwt is drifting toward $4.00 or more, you can’t stay on autopilot. Pick a path — pipeline, margin, or deliberate expansion — in the next 30 days instead of letting replacements “just happen.”

- If you’ve already decided to hold herd size steady or shrink slightly, call your processor and lender within 90 days to explain that this is a strategy built around margin and reliability, not a slow slide — it changes how they look at your risk.

- If your 2026 breeding sheet still looks like 2023, sit down this month and pencil out how many heifers it actually delivers by 2028. If the number comes up short of what you’ll need, adjust your sexed‑dairy vs beef allocation before this spring’s breeding season is in full swing.

The Bottom Line

The question worth putting on the whiteboard in your office this week isn’t “How much milk did we ship last year?” It’s “Where are our 2028 replacements coming from — and what happens to our cash flow if each one costs $3,000 or more?”

For some herds — especially the Upper Midwest operations that quietly tightened up while their neighbors chased growth — the answer is already baked in. For others in Kansas, South Dakota, Idaho, or Texas who built new capacity on the back of beef‑on‑dairy, the hardest conversations with bankers and processors may be right around the corner.

Which side of that line do you want to be on when CoBank’s projected 2027 rebound finally shows up — and how many stalls will you have to fill before it gets here?

If you want the deeper math — by herd size, region, and debt profile — Bullvine Weekly and an upcoming Tier 3 economics feature will break down the full herd‑flow replacement model. That’s where you’ll see per‑cwt cost curves and export‑shock scenarios. But the fork in the road starts here, with the numbers on your own whiteboard.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – This breakdown reveals the exact 21-day pregnancy rate thresholds that make or break your beef-calf income. It delivers a concrete, performance-tiered roadmap to ensure your breeding mix actually adds to the bottom line without starving your future pipeline.

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – This strategic deep dive exposes the structural reset currently hitting the industry, where $11 billion in new processing capacity meets record-low heifer inventories. It arms you with long-term positioning strategies to protect equity before the next market shift.

- Bred for $3 Butterfat, Selling at $2.50: Inside the 5-Year Gap That’s Reshaping Genetic Strategy – You’ll gain a decisive advantage by understanding how to outrun the “lag effect” of your breeding choices. This article breaks down how to align current genetic selection with future component demand, securing your spot as a preferred processor partner.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.