Inside the import-substitution playbook, processors run across every dairy market — and the barn math that shows whether your contract is next.

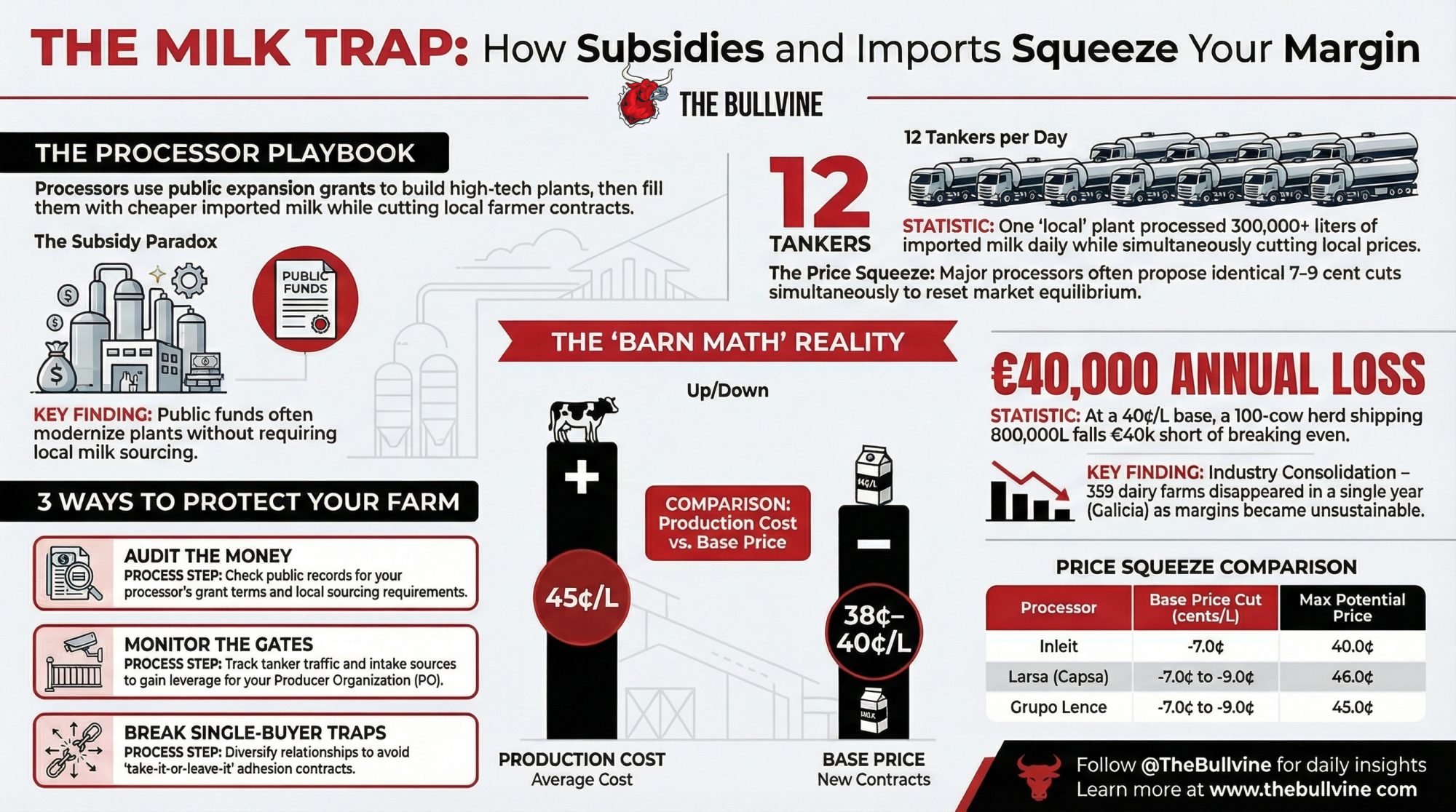

Executive Summary: Galician farmers proved their processor took €14 million in public subsidies, then filled a “local” plant with 12 Portuguese milk tankers a day and still tried to cut contracts 7–9 cents per litre. At Inleit’s proposed 40¢/L base, a 100‑cow herd shipping 800,000 L a year is roughly €40,000 under water against a 45¢/L cost of production, and other big processors in the region landed on almost identical cut ranges. Spain’s Food Chain Law technically bans below‑cost contracts, but AICA’s fines have been tiny, and courts have thrown out sanctions against buyers like Mercadona and Lactalis on procedural grounds, even as a Barcelona court ordered Capsa, Puleva, and Danone to compensate farmers 2% for a proven 2000–2013 milk cartel. The same playbook shows up in North America when subsidized plant expansions, FMMO make‑allowance changes, and TRQ usage quietly move hundreds of millions from the milk pool to processors without an obvious “price cut” on your statement. The article walks through simple checks you can run in 30 days — pulling your processor’s grant files, watching tanker traffic, stress‑testing your breakeven against current offers, and figuring out how exposed you are to a single buyer. If you’re wondering whether your own “local” plant is using foreign milk and regulatory tweaks to set up the next contract squeeze, this is worth a full read.

Roberto García made it official on Monday, March 30, 2026. The General Secretary of Unións Agrarias — Galicia’s largest agricultural union — met with FENIL, the national dairy processor federation, in Madrid. By the end of the session, he’d declared relations “broken with the industry until this situation changes”.

Three days earlier, his members had intercepted a Portuguese tanker truck in the industrial park at Teixeiro, in the municipality of Curtis, A Coruña. They dumped 15,000 liters of milk onto the pavement. Not because they’d lost their minds. Because they’d done the math.

The tanker was headed to Inleit Ingredients — a high-tech protein fractionation plant that received €14 million in Galician public subsidies to process local milk. That’s not a union estimate. Xunta President Alfonso Rueda himself cited that figure during a March 2023 visit to the factory, describing the funds as aid “for the expansion and improvement of Inleit’s facilities since it began its operations”. Óscar Pose, the dairy sector head of Unións Agrarias, told Campo Galego his team had been counting: an average of 12 Portuguese tankers per day — more than 300,000 litres daily — rolling into that same facility in the weeks before the protest. And on the negotiating table? A proposed 15% base price cut — from 47 cents to 40 cents per litre — for the Galician farms that were supposed to be Inleit’s reason for existing.

That’s the story the headlines gave you. But if you think it’s just a Spanish problem, look at your own processor’s recent expansion grants. The playbook is the same. Here’s how it works.

The Subsidy Paradox

The Inleit plant in Teixeiro isn’t a traditional bottling operation. It produces micellar casein, milk permeate powders, and specialized protein isolates — high-margin functional ingredients for sports nutrition, cheese manufacturing, and clinical products. It holds FDA registration and GFSI audit certifications. Exactly the kind of value-added facility that regional governments love to fund.

And the Xunta de Galicia funded it heavily. Rueda’s own March 2023 announcement put the total at €14 million — public money intended to modernize the sector and add value to local production. That language matters. It’s the justification for every euro of taxpayer money. Pose, for his part, told Campo Galego: “It’s not exactly normal for the Galician government to give more than 10 million euros to this company for them to do this”.

But here’s what those subsidy terms apparently didn’t lock down: sourcing requirements. If Inleit can withachieve the same protein density from Portuguese milk at a lower landed cost, the industrial logic points toward importing. How much lower? Unións Agrarias told the Consellería do Medio Rural that imported milk was arriving at processing plants for as little as 20 cents per kilogram — while Portuguese farmgate prices sat at 40 cents and French at 44. As García put it to Campo Galego: “Buying milk in Portugal at 40 cents or in France at 44 and selling it here at 20 cents is unfair competition”.

By December 2025, Unións Agrarias estimated that imported milk flowing into Galician plants exceeded 600,000 kg per day — roughly 7% of the region’s entire output. Pose was blunt about the strategy: “The industry is sorting out its bottom line for the whole of 2026,” he said. “This isn’t just about the next four months of contracts”. In the union’s view, a plant built with Galician public money now functions as a hub for processing cheaper Iberian imports. Inleit has not publicly addressed its intake sourcing relative to subsidy terms.

You’ve seen this movie before. The names change. The pattern doesn’t.

What Every Processor Offers — and What It Actually Means

The Teixeiro dump wasn’t about one plant. All six major Galician processors proposed base-price cuts for April 2026 contracts. The uniformity is what caught the union’s attention.

| Processor | Previous Base (cents/L) | New Base (cents/L) | Cut | Max w/ Premiums | Context |

| Inleit | 47.0 | 40.0 | −7.0 | 40.0 | Aggressive base cut, no premium above base |

| Lactalis | ~42.5 | 38.0 | −4.5 | 45.0 | Targeted drops for high-volume suppliers |

| Larsa (Capsa) | 46.0–48.0 | 39.0 | −7.0 to −9.0 | 46.0 | Welfare and volume premiums layered on top |

| Grupo Lence | 47.0–49.0 | 40.0 | −7.0 to −9.0 | 45.0 | Volume and hygiene quality tiers |

| Naturleite | 48.5–50.5 | 41.5 | −7.0 to −9.0 | 45.0 | Environmental and welfare premium integration |

| Reny Picot | 47.0–49.0 | 40.0 | −7.0 to −9.0 | 45.0 | Aligned to Grupo Lence tier structure |

Source: Unións Agrarias contract analysis, confirmed by Campo Galego (March 18, 2026).

Look at the Inleit line. A 7-cent base cut — and the maximum potential price, even with every premium, is the same 40 cents as the base. No quality tier, no welfare bonus, no volume incentive. Just a flat number that sits well below what it costs to produce the milk.

Unións Agrarias called the pattern across all six processors an “orchestrated maneuver” to reset the entire market at a lower equilibrium. Six processors are landing on the same 7-to-9-cent cut range during the same contract window. And this comes on the heels of an existing legal finding: Spain’s CNMC (competition authority) already established that major dairy companies colluded on milk pricing between 2000 and 2013. On February 2, 2026, the Audiencia Provincial de Barcelona ordered Capsa — owner of Larsa, one of the six processors in the table above — along with Puleva Food (a Lactalis subsidiary) and Danone, to pay 2% compensation on milk purchased from producers during those cartel years. The court reversed a lower ruling that had dismissed the farmers’ claims as time-barred. Coordination isn’t hypothetical in Spanish dairy. It has a court record.

Can a 100-Cow Galician Dairy Survive These Numbers?

Now put those contract offers into barn language.

Take a family operation in Lugo or Pontevedra province: 100 cows producing roughly 800,000 litres per year. That’s well above the regional average — FEGA data showed the typical Galician herd averaging about 44.9 cows in recent years, though the number climbs every year as smaller farms fold. And they’re folding fast. FEGA’s January 2025 report counted 5,212 active dairy farms in Galicia, already down from approximately 5,571 at the start of 2024 — a loss of 359 operations in a single year. Another 92 disappeared between January and April 2025 alone. At that rate, Galicia has almost certainly dropped 5,000 active dairy farms by now.

At Inleit’s proposed base of €0.40/litre, that 100-cow farm generates €320,000 in annual milk revenue.

Noelia Rodríguez, president of Agromuralla — a separate Galician farm union — told Cadena SER’s Radio Lugo on March 24, 2026 that current production costs for a farm without excessive debt sit at around 45 cents per litre. On 800,000 litres, that’s €360,000.

The gap: €40,000 per year in the red. Not a tight margin. A loss.

Whether that 45-cent figure fully captures the 7-cent cost spike Unións Agrarias documented for early 2026 is unclear. The spike is driven by diesel, fertilizer, and energy costs tied to Middle East instability and disruptions in the Strait of Hormuz. Rodríguez said “right now,” which suggests current conditions — but if the full spike isn’t baked in, the real gap is wider. And for most Galician farms, the March-to-June window represents 60–80% of annual operational spending as they prepare fodder and manage peak biological cycles. A price cut during this specific period is the worst possible timing.

Three separate sources — Rodríguez (Agromuralla), Pose (Unións Agrarias), and the union’s formal input-cost analysis — all point at the same threshold. This isn’t one organization’s negotiating posture. It’s the math.

Even farms hitting the maximum premium tier at Grupo Lence or Naturleite — 45 cents — are just scraping breakeven. Those premiums require hitting quality, welfare, and volume benchmarks that add their own costs.

Why Doesn’t Spain’s Food Chain Law Stop This?

Spain has a law for exactly this situation. The Ley de la Cadena Alimentaria (Law 12/2013, amended by Law 16/2021) explicitly prohibits purchasing agricultural products at prices below the effective cost of production. Unións Agrarias asserts that by proposing prices as low as 38 or 39 cents per litre while costs exceed 45 cents, the industry is in systematic breach.

The enforcement agency, AICA, has been busy — over €703,000 in sanctions in the first three months of 2026 alone for food chain infractions, including non-compliance with payment terms, missing written contracts, and unilateral contract modifications. But the fines are small relative to processor margins, and the courts keep gutting them.

Here’s what that looks like: Mercadona was fined just €66,000 for allegedly buying cow’s milk below cost from Covap — a major dairy cooperative that supplies the Hacendado brand through Naturleite in Galicia. Lactalis faced similar AICA sanctions. Both companies convinced Spain’s National Court to annul the fines — not on the merits, but on procedural defects that left the companies in “a position of legal defenselessness,” according to the court. The law exists. The enforcement exists. And the outcomes still favour the processors.

Agricultural organizations publicly warned processors as recently as March 12, 2026, that reducing milk prices without accounting for new costs from the Middle East conflict could breach the Chain Law. Nothing changed. The proposals went out anyway.

FENIL’s defence? Spanish farmgate prices — averaging €0.495/liter nationally in January 2025, according to FEGA data — have remained above the EU average. FENIL argues this creates a competitiveness gap, making Spain a target for cheaper imports. But that comparison ignores higher Spanish energy and logistics costs — and it ignores that Galicia consistently trails the national average. FEGA’s own January 2025 data puts Galicia at €0.473/liter, a 2.2-cent-per-liter gap below the national figure, making it the cheapest milk-producing region in Spain despite producing the most.

Does This Pattern Show Up in North American Contracts?

Yes. And you don’t have to squint to see it.

In the United States, federal and state subsidies for processing plant construction have accelerated since 2020. New capacity goes online, processors gain intake flexibility across wider geographies, and contract leverage shifts. The USDA’s Federal Milk Marketing Order reform that took effect January 1, 2026, was supposed to help, but an American Farm Bureau Market Intel analysis found the make-allowance increases transferred an estimated $337 million in annual pool revenue from producers to processors in just the first three months. For a 300-cow herd producing roughly 23,000 lbs per cow annually, that kind of systemic revenue shift means thousands of dollars disappearing from each monthly check — money that moved from the barn to the plant through regulatory mechanics, not market forces.

Canada’s supply management system provides more structural protection than anything in the EU or the US. But it’s not immune. Tariff-rate quotas under CUSMA allow a growing volume of US and international dairy to enter the Canadian market at reduced duties. The Canadian Dairy Commission’s pricing formula adjusts with a lag — sometimes a significant one — which means cost spikes on-farm can outrun the administered price for months. And provincial allocation rules determine which processors get quota access, creating their own version of the leverage asymmetry Galician farmers face.

The mechanism is the same everywhere: subsidized capacity expansion → intake geography diversification → contract leverage → price compression. The rulebooks change from country to country. The outcome for your milk cheque doesn’t.

How Would You Know If Your Processor Is Running This Playbook?

You probably wouldn’t — not from the information most producers have access to. That’s the point. The whole setup depends on you not having the numbers.

But there are signals worth watching:

- Capital investment without new local supply contracts. When your processor announces a plant expansion funded partly by public grants, and your contract terms don’t improve or lock in volume, that capacity isn’t being built for you. Rueda announced Inleit’s €14 million in March 2023. Three years later, Galician farmers got a 7-cent price cut. Connect the dots.

- Subtle shifts in intake policy. New quality tiers, changed testing protocols, or volume-flexibility clauses that weren’t in the last contract can signal that your processor is blending your milk with cheaper imported inputs. Pose’s team documented 12 Portuguese tankers a day arriving at a plant that markets itself as processing Galician milk.

- Contract language that eliminates collective bargaining. García described the current proposals as “adhesion contracts where the farmer’s only option is to sign or dump the milk”. The EU’s March 2026 CMO reform specifically targets this tactic by preventing buyers from contacting individual PO members to undercut collective negotiations.

- Regional pricing that diverges from national trends. Galicia’s FEGA-reported farmgate price was €0.473/litre in January 2025 — the lowest of any Spanish region, despite producing more milk than any other. When your region’s price falls further behind while your processor’s margins hold, that’s not the market. That’s leverage.

Options and Trade-Offs for Farmers

Play 1: Audit the money — this month. Did your processor receive public funding? Those grant terms are often public record. Pull them. Look for local-sourcing requirements, employment commitments, or production targets. The Galician case is a blueprint: Rueda publicly announced €14 million in Inleit subsidies in March 2023. Three years later, producers caught a dozen Portuguese tankers a day rolling through the gates. If the subsidy terms include sourcing obligations that aren’t being met, that’s leverage — for your PO, your elected representative, or the media. Cost is time, not cash. Risk is low.

Play 2: Count the tankers — this quarter. The Galician farmers who monitored tanker arrivals at Inleit did basic supply-chain surveillance that changed the public conversation. Your PO doesn’t track your processor’s total intake sources? You’re negotiating blind. Under the new EU CMO rules, processors can’t bypass your PO to deal with individual members — but that only works if your PO has data to bargain with. In North America, equivalent information is harder to get but not impossible through FOIA requests and provincial regulatory filings. Trade-off: time and organization now versus better leverage in the next contract round.

Play 3: Break the single-buyer trap. The most vulnerable farms in Galicia ship 100% to one buyer with no alternative outlet. Sound familiar? Start exploring whether a second relationship — even for a small percentage of your volume — changes your risk profile. Splitting volume may cost a tier premium short-term. But single-buyer dependency is exactly what gives processors the confidence to present take-it-or-leave-it contracts. On January 29, 2026, roughly 25,000 Spanish farmers brought 15,000 tractors into city streets for the “Super Thursday” protest against the EU-Mercosur deal. García has called for a dairy-specific mobilization later in April — and that kind of turnout happens when producers feel they’ve run out of options at the negotiating table.

Play 4: Demand indexed contracts — next negotiation cycle. Unións Agrarias has called for contracts that automatically adjust based on official production-cost indices. If your market doesn’t have such indices, advocate for their creation through your national dairy association. The risk: indexation cuts both ways if input costs fall. But the Galician experience shows what happens when there’s no floor at all.

Key Takeaways

- If your processor received public subsidies for plant construction but your contract doesn’t include sourcing guarantees, pull the grant terms this month — those obligations may already exist and go unenforced. Xunta President Rueda publicly confirmed Inleit’s €14 million. Three years later, there’s no visible sourcing accountability.

- If all processors in your region propose similar price cuts within the same contract window, your producer organization should ask the competition authorities whether the uniformity warrants an investigation. Six Galician processors landing on the same 7-to-9-cent cut isn’t a coincidence in the union’s view — and Spain’s Audiencia Provincial de Barcelona has already ordered Capsa, Puleva, and Danone to compensate farmers at 2% of milk purchased during a proven 2000–2013 cartel.

- If your production cost exceeds your contracted base price, you’re operating below the threshold where food chain laws are supposed to protect you. Document your costs in writing, formally, every quarter. Enforcement agencies need paper trails they’re not getting — and when they do act, courts are throwing sanctions out on procedural technicalities.

- If you can’t answer the question “where does my processor’s other milk come from,” that gap in your information is the gap in your leverage. Close it before your next co©ntract negotiation, not after.

The Bottom Line

García told FENIL on March 30 that the industry is “acting unilaterally, trampling the most basic rules of collective negotiation” and imposing “adhesion contracts where the farmer’s only option is to sign or dump the milk”. The contract deadline for the April terms was March 31. Pose summed it up plainly to Campo Galego: “The industry is sorting out its bottom line for the whole of 2026”. If the January “Super Thursday” protest, which drew 25,000 farmers across Spain, is any guide, the processors should pay attention to what comes next.

The Portuguese tankers keep rolling. The question isn’t whether your processor could run this playbook — it’s whether you’ve looked at the numbers closely enough to know if it’s already happening. If you want the full economic model behind processor import-substitution mechanics, we’re building it out for a deeper piece later this month.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The Hidden Contract Clause That Could Cost Your Dairy $55,000 in 2026 – Arms you with a 30-day action plan to dodge massive liability shifts in new milk contracts. This guide exposes the hidden costs of regulatory compliance and delivers the specific negotiation leverage you need to protect your 2026 net profit.

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Reveals the brutal $250,000 margin gap currently threatening mid-sized operations and breaks down the “more milk, fewer farms” era. It provides the long-term economic benchmarks required to position your herd’s equity before the market decides for you.

- Butterfat vs. Powder: What the Great Dairy Divide Really Means for Your Bottom Line – Discovers how to pivot your genetic strategy toward the high-margin components that processors actually value. This analysis exposes why volume is a losing game and shows how precision breeding adds $2.00/cwt to your check without adding a single cow.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.