A 400‑cow herd can be $584,000 in the hole even after “sustainability” premiums. The math isn’t a scare tactic — it’s what happens when credits don’t hit your milk check.

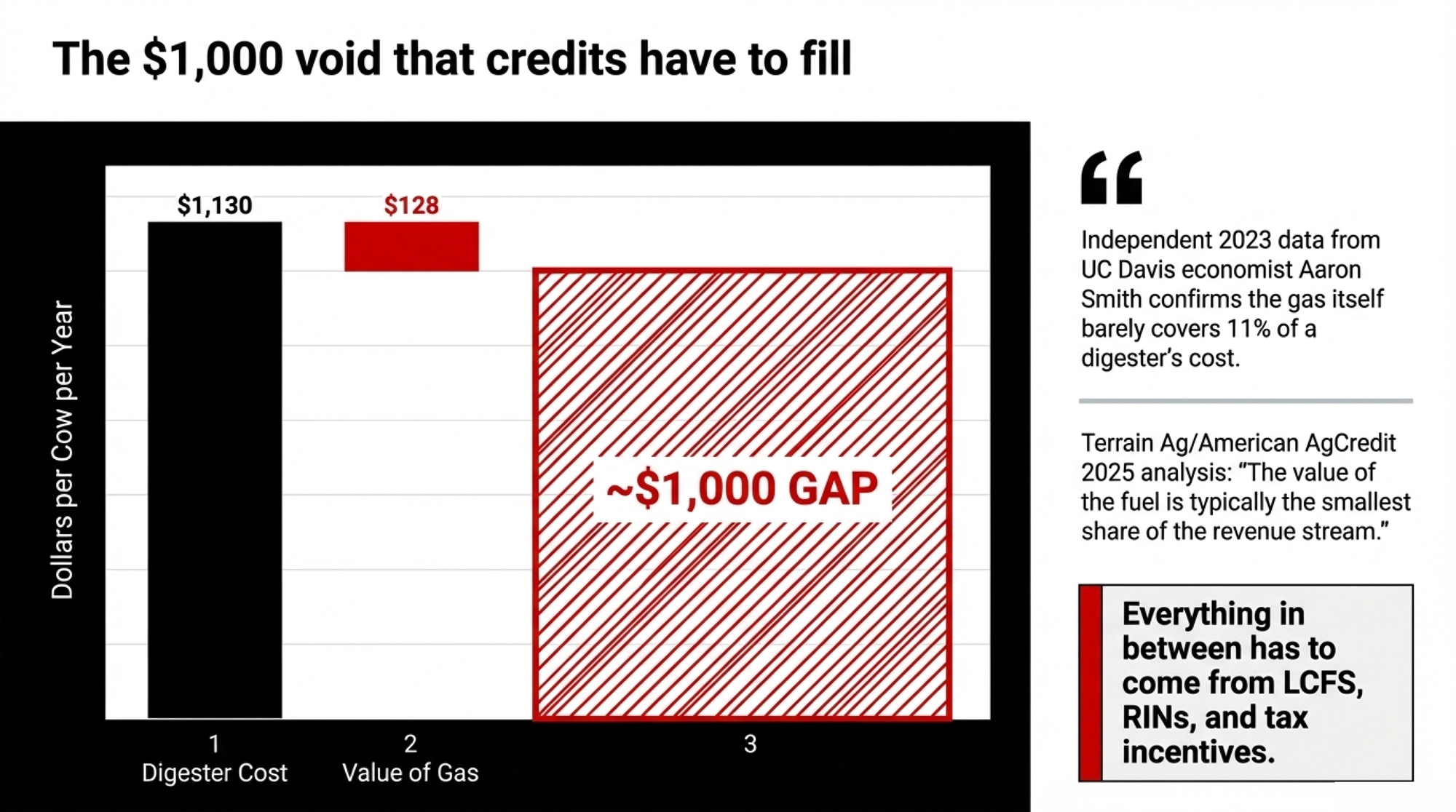

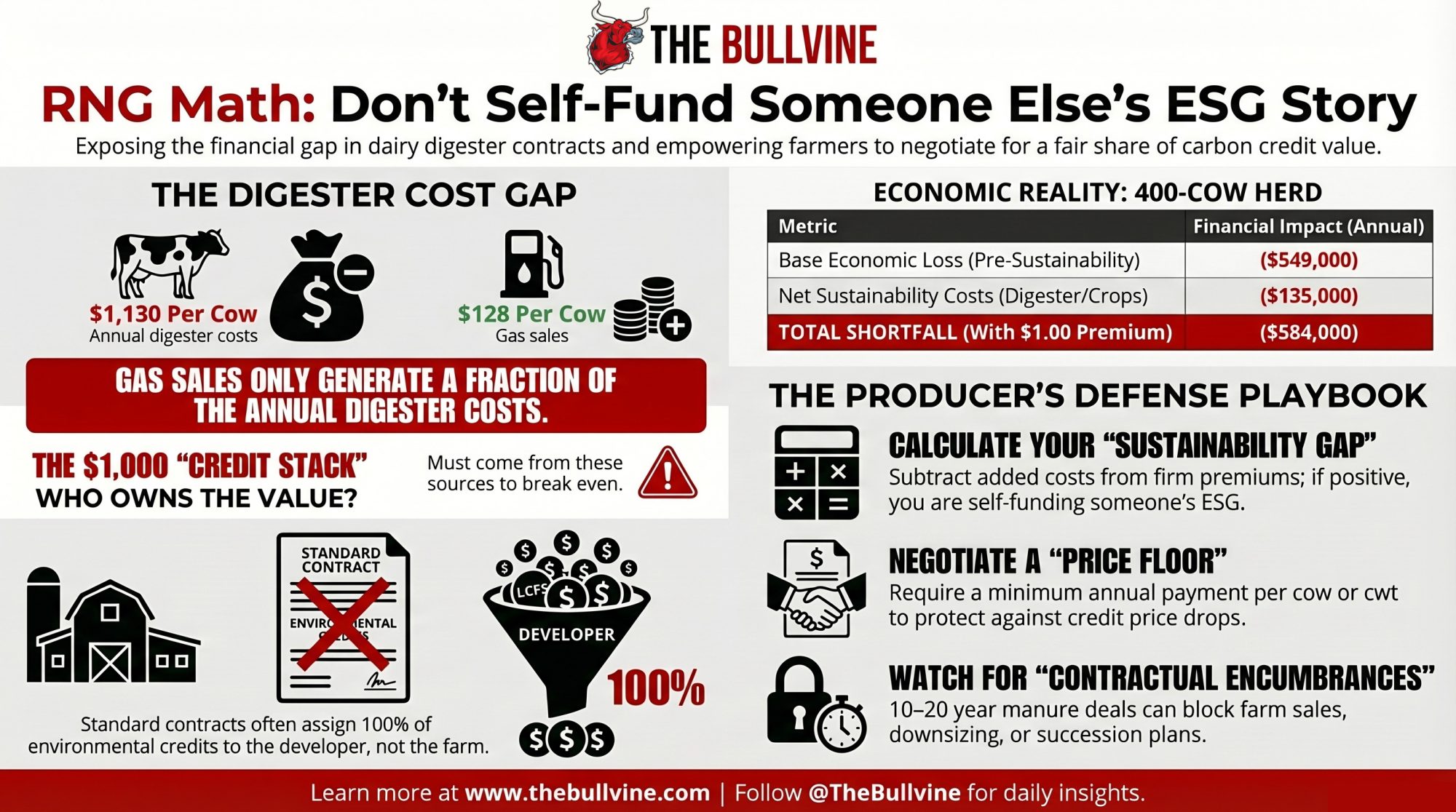

Executive Summary: A UC Davis analysis shows that a typical dairy digester costs about $1,130 per cow per year,while the gas is worth only $128 per cow, so nearly $1,000 has to come from credits, incentives, and premiums. Standard RNG contracts and lender requirements usually assign those LCFS credits, RINs, tax breaks, and Scope 3 “wins” to the project and processor, not the farm, which means the climate value created in your lagoon often lands on someone else’s balance sheet first. Using 2022 Illinois cost data and a modeled 400‑cow herd shipping 100,000 cwt, the article walks through how a farm already losing $5.49/cwt on full cost can end up $5.84/cwt in the hole — $584,000/year — even after a $1.00/cwt sustainability premium. It shows how 10‑ to 20‑year manure deals can behave like an encumbrance on your land and succession plan, tying you to minimum volumes and lender‑friendly terms long after the RNG hype cycle or policy incentives shift. For herds in the 300–1,200‑cow band looking at digesters, feed additives, or “climate‑smart” bundles, the risk is quietly self‑funding someone else’s ESG story out of your equity if the premium per cwt never catches up to the true sustainability bill. The piece gives you a 30/90/365‑day playbook to calculate your own sustainability gap, read the fine print on environmental credit ownership, and push for a milk price floor plus a defined share of the credit stack before you sign.

When a 1,000‑cow producer in Virginia, we’ll call Ben Smith, finally sat down with the numbers on his new digester, one line item stopped him cold. Independent 2023 work by UC Davis economist Aaron Smith estimated that a dairy digester on a 2,500‑cow covered‑lagoon project costs about $1,130 per cow per year, while the gas itself is worth only about $128 per cow per year. Everything in between — almost $1,000 per cow — has to come from somewhere other than the gas.

A 2025 Terrain Ag/American AgCredit analysis of digester economics confirmed the same thing in plain language: “The value of the fuel is typically the smallest share of the revenue stream.” The real money sits in LCFS credits, RIN credits, and tax incentives. And standard RNG contracts are designed to keep most of that value on the developer’s side of the ledger.

Ben Smith is a composite of several 800–1,200‑cow dairies we’ve spoken with over the past 18 months. His name isn’t real. The math and the contract patterns are.

The Price Gap Before Sustainability Even Enters the Room

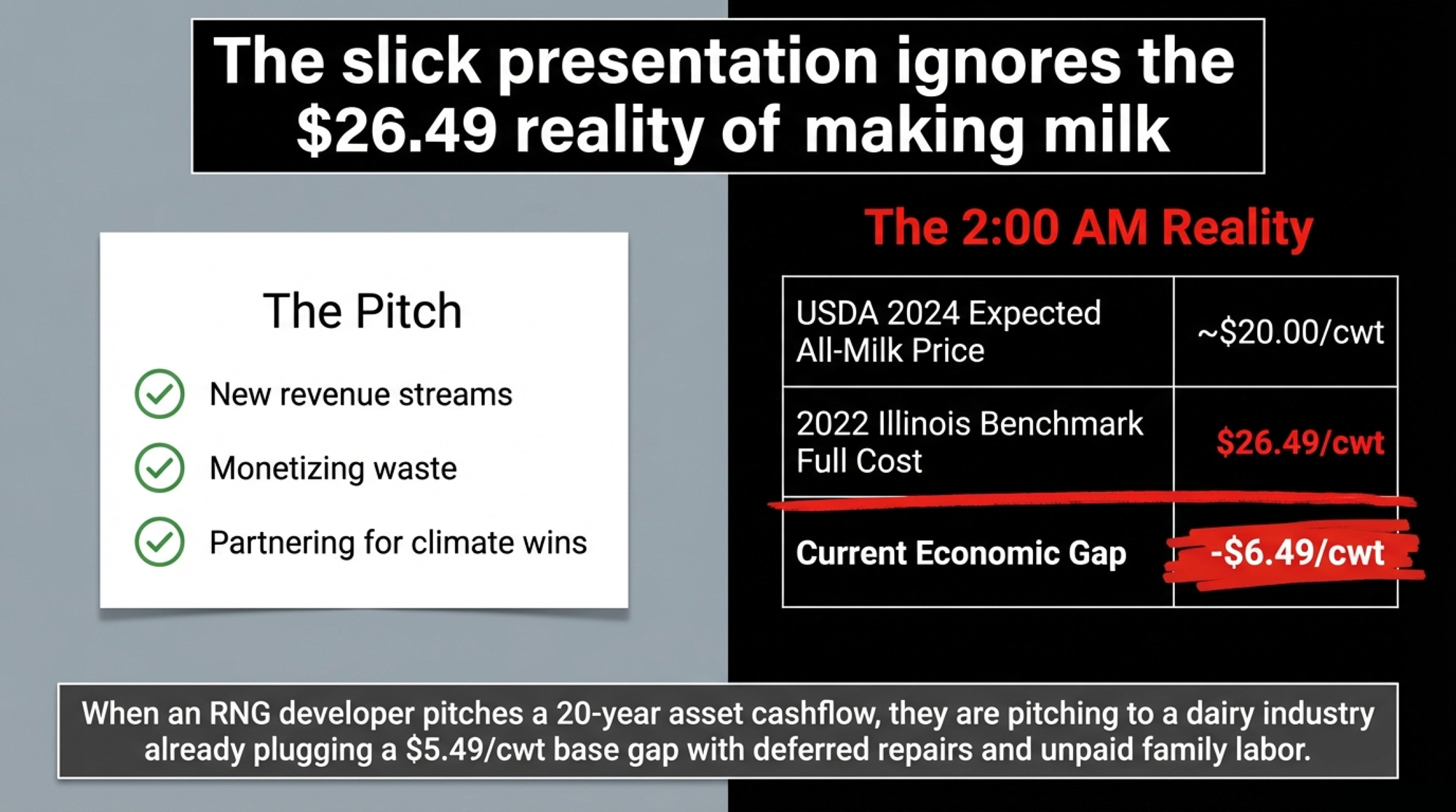

Ben’s herd operates in the same economic band that 2022 Illinois data spelled out: full economic costs around $26.49 per cwt, average net price at $25.36 per cwt, a gap of about $1.13 per cwt in economic losses for the average herd in that dataset.

Set that against USDA’s expectation of a roughly $20.00 per cwt national all‑milk price for 2024, and you see the backdrop when an RNG developer pulls into your yard with a slick deck.

They roll through slides about “new revenue streams,” “monetizing waste,” and “partnering for climate wins.” You picture a stronger milk check. On the other side of the table, the pitch is built around 20‑year asset cashflows, LCFS credit strips, and tax incentives layered on top.

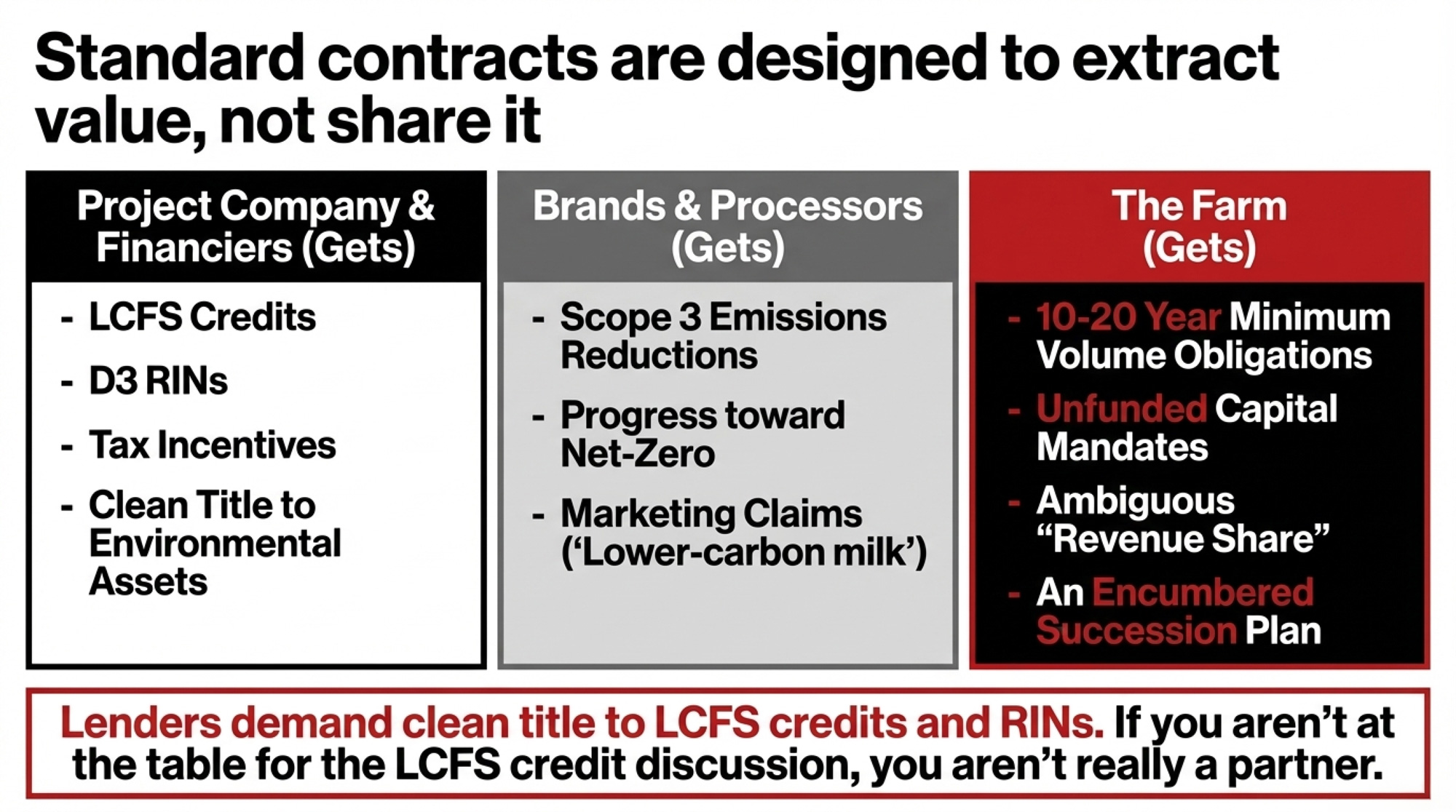

If you aren’t at the table for the LCFS credit discussion, you’re not really a partner in how that value gets split.

How RNG Contracts Turn Your Manure Into Someone Else’s Climate Asset

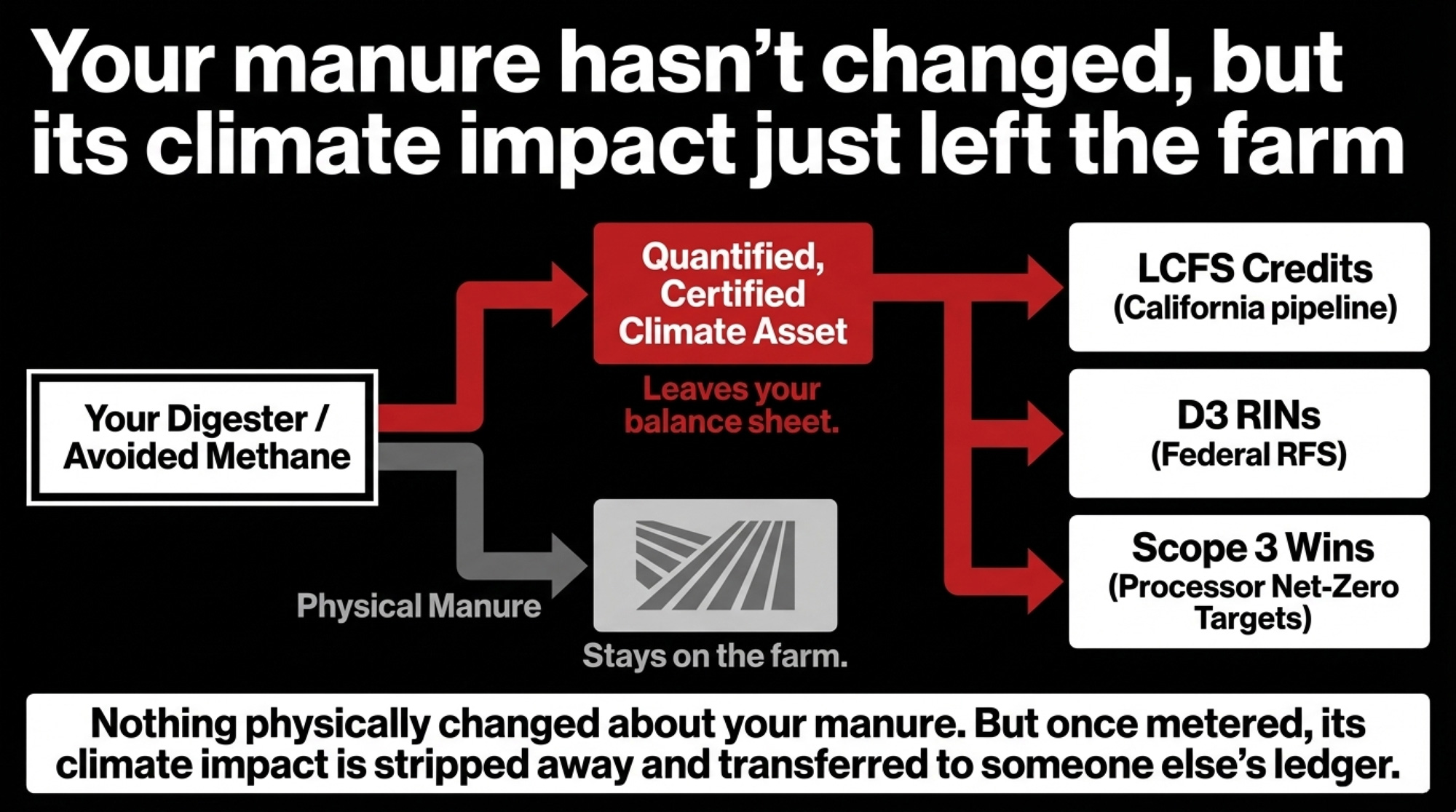

The standard story is that sustainability programs are here to help you transition. In practice, these deals also turn your manure and management into tradable climate value — and that value is usually booked somewhere other than your milk check.

Your digester makes methane a measurable commodity. Protocols like the Climate Action Reserve’s U.S. Livestock standard treat the difference between your old lagoon and your new digester as avoided methane emissions. Those avoided tonnes of CO₂e become:

- LCFS credits are awarded when RNG with very low or negative carbon intensity hits a California pipeline.

- D3 RINs under the federal Renewable Fuel Standard.

- In some cases, additional voluntary carbon credits are layered on top.

| Scenario | Environmental credit ownership | Contract term & volume obligations | Impact on milk check per cwt |

|---|---|---|---|

| Typical developer template | Developer owns LCFS, RINs, tax credits <span style=”color:#FF0000;”>(farmer: 0%)</span> | 10–20 years, strict minimum manure volume <span style=”color:#FF0000;”>locked in</span> | Small fixed payment, no defined share of credit value |

| Producer assumes “50/50 partnership” | Shared in theory, but no explicit credit split in contract | Long term, volumes loosely defined, lender rights unclear | Revenue share only after costs recovered; payout highly variable |

| Contract with defined credit‑share clause | Developer holds title; farmer guaranteed <span style=”color:#FF0000;”>10–30%</span> of LCFS/RIN revenue | 10–15 years, minimum volumes tied to realistic herd size | Per‑cwt formula ties credit value directly to milk check |

| Producer‑led negotiation with floor | Jointly structured entity or royalty on all climate value | Term aligned with lender horizon; flexible volumes on downsizing | Milk price floor plus per‑cwt climate bonus; downside risk reduced |

Nothing about the manure changed physically. But once the system is metered and verified, its climate impact becomes quantified, certified, and tradable.

Standard RNG contracts push that value upstream. Guidance written for developers is blunt about who’s supposed to own those credits. A 2022 Biomass Magazine article on manure‑supply agreements advises developers that the contract should “clearly state that the developer owns all rights to the environmental credits, tax credits, and similar benefits arising from the project.”

Lenders and offtakers want the project entity to have a clean title to LCFS credits, RINs, and tax incentives — not shared or ambiguous ownership. Compeer Financial’s 2025 guidance to producers echoed the same concern from the farmer’s side: “Understanding the fine print is crucial to ensure a successful and sustainable partnership.”

In many of the digester and RNG project templates and legal guides The Bullvine has reviewed, the pattern looks like this:

- You sign a 10‑ to 20‑year manure‑supply agreement with minimum daily volumes keyed to your current herd size.

- They — the project company and its financiers — own the LCFS credits, RINs, and tax incentives.

- Your processor or brand counts the resulting emissions reduction toward its Scope 3 targets.

The climate asset your farm creates doesn’t vanish. Under most current contract and policy setups, it’s usually recognized first on the developer’s or buyer’s balance sheet, not on your milk check.

Processors book Scope 3 wins off your barn. Under the Greenhouse Gas Protocol, processors report supply‑chain emissions from purchased milk under Scope 3 Category 1. If they can show that milk from farms like yours carries less embedded CO₂e — because of digesters, feed additives, or manure practices — they can claim progress toward net‑zero targets and market “lower‑carbon milk” to retailers.

Those wins are real. But they don’t automatically show up in your mailbox price unless the contract forces them to.

The Premiums Are Real — But Thin

Brands and co‑ops are right to say they’re not asking for all this for free. There are real premiums out there, especially in Europe and New Zealand.

- ING’s 2024 work on dairy companies’ path to net zero notes that a “couple of cents per liter” is the sort of sustainability premium discussed in parts of Western Europe — and that dairy companies struggle to pass even that level on to end customers.

- Fonterra’s 2025/26 incentives include a new Emissions Excellence payment of 1–5 cents per kgMS, plus an Emissions Incentive of 10–25 cents/kgMS for the roughly 300–350 farms (out of ~10,000 suppliers) with the very lowest emissions intensity. A separate Fonterra–Nestlé partnership adds 1–2 cents/kgMS for farmers hitting certain sustainability levels.

Convert those kgMS figures into U.S. units, and you’re usually in the sub‑$1 to low‑$2 per cwt range for top‑performing farms, depending on solids and exchange rates. Real dollars. But not unlimited — and not guaranteed across every herd.

| Region or program | Premium per cwt (USD, est.) | Added sustainability cost per cwt (USD, est.) | Net effect on margin per cwt |

| Western Europe “couple of cents/liter” | ~1.50–2.00 | 1.00–2.50 (manure, feed, verification) | Often near zero; can slip negative in high‑cost years |

| Fonterra top‑tier incentives (NZ) | ~1.00–2.00 | 0.75–1.75 (emissions, auditing, practice changes) | Small positive spread for elite low‑emission herds |

| USDA climate‑smart pilots (U.S.) | 0.25–0.75 | 0.75–1.50 (cover crops, data, management time) | Many farms underwater on true full cost |

| Modeled 400‑cow herd in article example | 1.00 | 1.35 (digester, cover crops, grazing shifts) | –0.35 per cwt; $35,000/year gap |

In North America, published premium examples are thinner. USDA’s climate‑smart commodities projects describe incentives in modest terms, not major price shifts. And while the developer’s PowerPoint always looks clean, nobody’s putting the 2:00 a.m. frozen‑pump repair on a slide.

What Does $21 Milk Plus RNG Costs Mean for a 400‑Cow Herd?

Here’s where it stops being theory and becomes barn math you can run on a legal pad. These numbers are a modeled example — not a specific farm — so you can plug in your own herd size and cost structure.

Take a 400‑cow conventional herd shipping roughly 10 million pounds of milk per year — about 100,000 cwt.

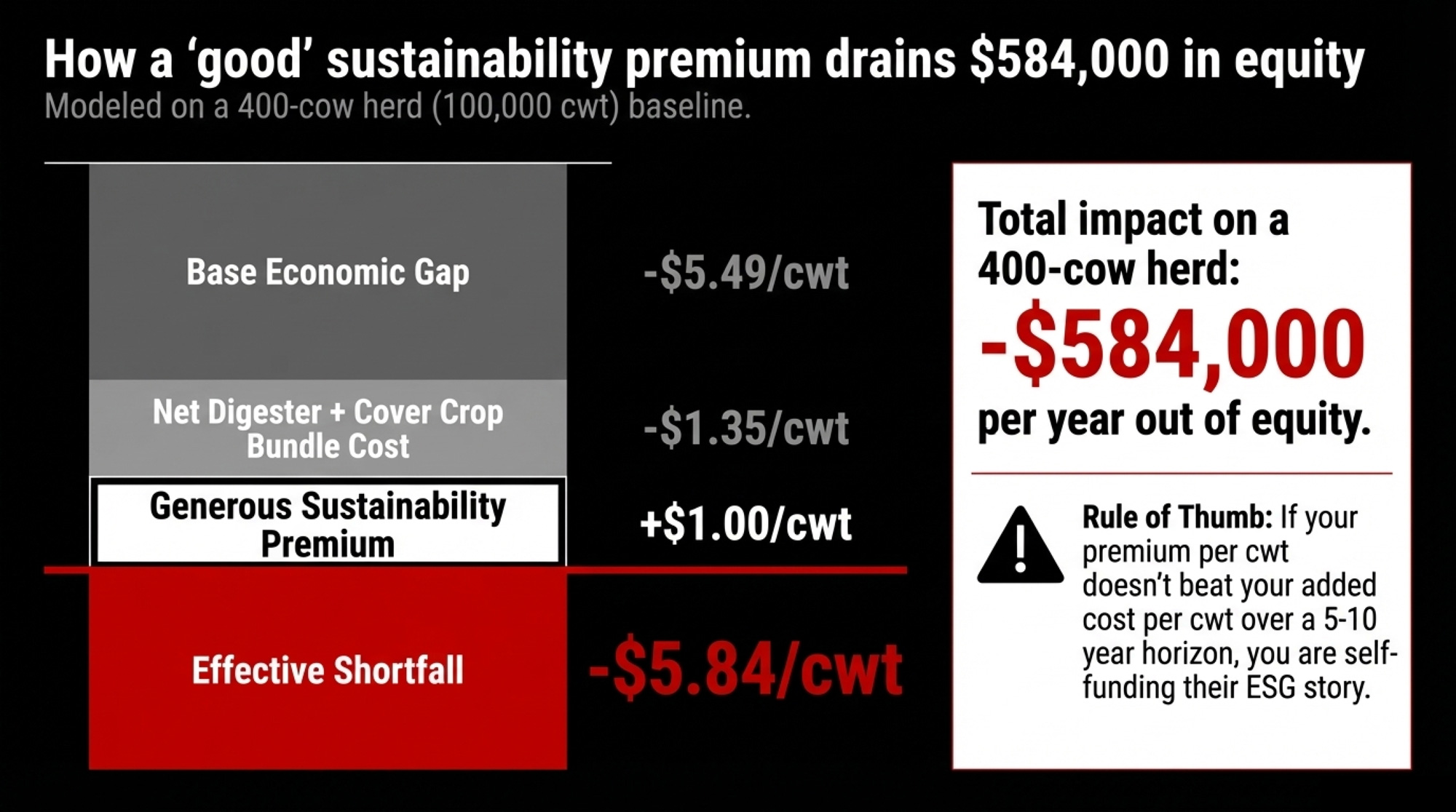

Step 1: Your base gap before sustainability.

Say your average milk check over the last year sat around $21 per cwt. Stack that against a full‑cost level like the Illinois benchmark at $26.49 per cwt:

- Gap: $5.49 per cwt.

- On 100,000 cwt: $549,000 per year.

If your full cost beats your price, you’re already plugging a hole with deferred repairs, restructured loans, or unpaid family labor. This is the hole many “sustainability” deals are quietly being asked to fill.

Step 2: Add a reasonable sustainability bundle.

Working from digester economics and extension budgets:

- Digesters: ~$0.75–$1.25 per cwt in net required margin after gas revenue, based on the $1,130/$128 per‑cow gap scaled to a mid‑sized herd.

- Cover crops: ~$0.15–$0.30 per cwt.

- Grazing/forage shifts: ~$0.10–$0.25 per cwt in early years.

Pick mid‑points: $1.00 + $0.20 + $0.15 = $1.35 per cwt, or $135,000 per year.

Step 3: Add a strong sustainability premium.

Assume a relatively generous $ 1.00-per-cwt premium on all your milk, above what many North American programs currently pay.

- Extra revenue: $100,000.

- Sustainability costs: $135,000.

- Net sustainability gap: $35,000 per year, or $0.35 per cwt.

Whole‑farm picture:

- Base economic gap: $5.49 per cwt.

- Plus net sustainability gap: $0.35 per cwt.

- Effective economic shortfall: about $5.84 per cwt, or $584,000 per year.

Here’s the breakeven rule of thumb: if your sustainability premium per cwt is lower than your added sustainability costs per cwt over a 5‑ to 10‑year horizon, you’re self‑funding the program out of equity.

Remember — this is a modeled 400‑cow herd, not a specific farm. Your numbers will shift depending on the cost structure and premiums you can actually lock in.

The Turn: When Ben Read His Own Contract

For Ben, the moment things clicked wasn’t a bad milk check. It was a Scope 3 slide deck.

His main buyer laid out how it planned to cut Scope 3 supply‑chain emissions by about 30% by 2030 using “value‑chain interventions” — digesters, feed additives, manure upgrades — on farms that supply it. Ben sat there looking at the tonnes of CO₂e on the screen and thinking about the $1,130/$128 per‑cow math and his own cost per cwt.

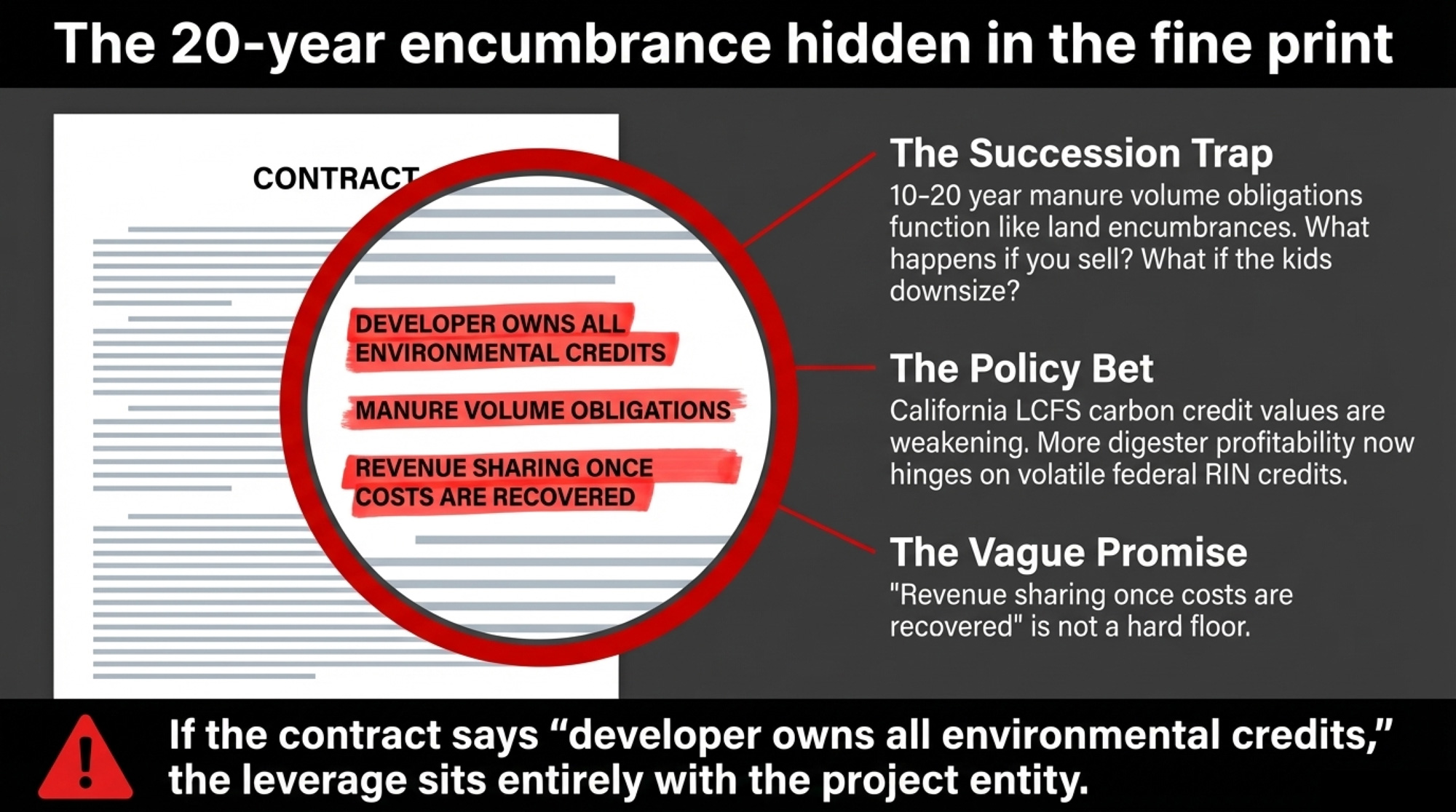

Then he re‑read his manure supply agreement. The developer had a long‑term commitment (10–20 years), minimum-volume obligations, environmental and tax-credit ownership, and lender protections upon termination. Ben had a promise of revenue sharing once costs were recovered — payments tied to project performance and policy, not a hard floor.

His wife asked the question that changed the conversation: What happens to this contract if we want to sell or if the kids want to downsize? The answer wasn’t simple. Legal and project guidance on RNG deals makes clear that lenders want long terms and enforceable feedstock commitments. A 10‑ or 20‑year manure obligation can function like an encumbrance — something a bank, buyer, or lawyer must clear before a sale, retirement, or transition.

A May 2025 Brownfield Ag News report underlined the policy risk: one dairy analyst noted that “the future of dairy digester projects is contingent on federal and state incentive programs continuing” and that “a larger portion of profitability hinges on RIN credits as the value of California’s carbon credit weakens.”

Ben’s takeaway is blunt: “Sustainability wasn’t just about practices anymore. It felt like a financial product. And from where I sat, I was the only one who didn’t have a clearly defined share written into the deal.”

That’s the assumption this piece pushes on. Not that digesters or climate‑smart programs are automatically bad — but that they’re structured financial assets, and as a producer, you need to negotiate like you’re part of that asset, not just a convenient source of manure and data.

Your 30 / 90 / 365‑Day RNG & Sustainability Playbook

You can’t control the LCFS market or your buyer’s ESG strategy. You can control how you show up in the next conversation.

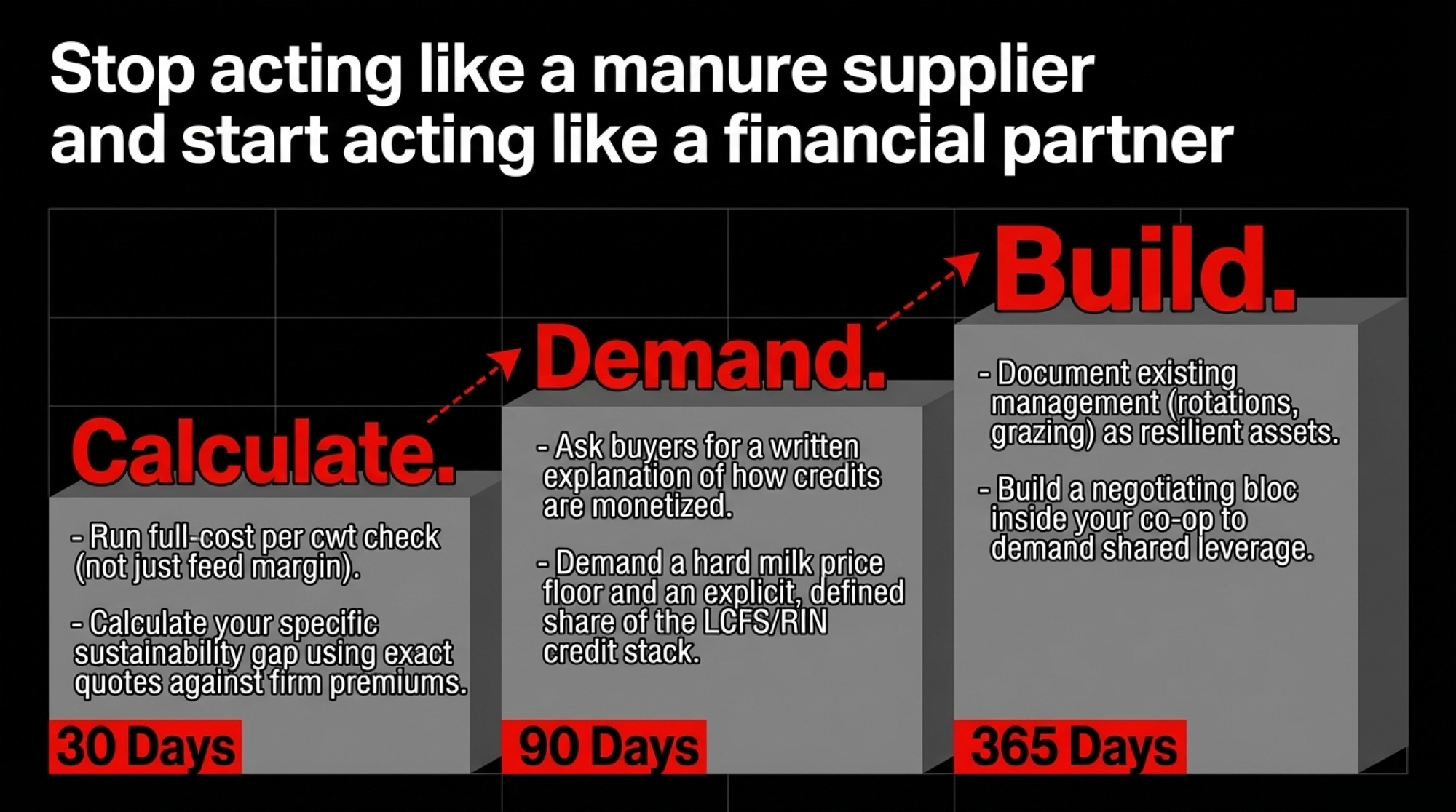

Next 30 days: put real numbers on your own sheet.

- Run a full‑cost per cwt check, not just margin over feed. Pull your last 12 months of books — feed, labor at a realistic rate, vet/med, fuel, repairs, insurance, interest, depreciation, overheads — and divide by cwt shipped.

- Compare that to a benchmark like $26.49 per cwt from Illinois, and your actual average milk price is around $20–$21 per cwt. If your price falls below your full cost, any unfunded sustainability obligation will come out of your equity.

- List every sustainability ask on the table — from co‑ops, developers, and lenders — and mark whether each one has a firm per‑cwt premium, a duration, and capital support.

- Use your own quotes and the ranges above to calculate your sustainability gap per cwt. If that number is positive, you’re paying to make someone else’s emissions profile look better.

Next 90 days: change the conversation with your co‑op and developers.

- Take your numbers to the next co‑op or processor meeting. Frame it: “This bundle costs us $X per cwt. Your sustainability premium is $Y per cwt. Who’s funding the X–Y gap?”

- Ask for a written explanation of how they value emissions reductions from your farm, how those reductions are monetized (credits, brand claims, Scope 3 targets), and how that value gets back to producers in predictable per‑cwt terms.

- Before signing or renewing any RNG contract, push for:

- A clear formula for your share of total project revenue, including LCFS, RIN, and carbon credit value — not just gas sales.

- A minimum annual payment per cow or per cwt, indexed over time, so your return doesn’t disappear if credit prices sag.

- Either partial ownership of environmental credits or a defined share of the revenue they generate, spelled out in dollars.

- Exit and assignment terms that define what happens if you sell or retire before the term ends, including who pays what to unwind the obligations.

If the contract instead says “developer owns all environmental and tax credits” and only describes “revenue sharing” in broad terms, it’s very likely that most of the formal credit ownership — and the leverage over how it’s used — sits with the project entity, not your farm.

Next 365 days: build leverage instead of just compliance.

- Turn your existing management into a documented sustainability asset. Many mid‑size dairies already use rotations, grazing, and manure cycling that soil and climate researchers describe as resilient. Write it down: rotations, grazing plans, soil tests, input changes.

- Add someone to your advisory circle for protocols and policy: LCFS/RFS updates, Scope 3 guidance, Farm Bill debates. Their job is simple — translate each change into dollars per cwt on your farm.

- Build a bloc inside your co‑op. A group of producers who’ve done their own sustainability‑gap math and are asking for a contractual price floor plus a share of the credit stack is harder to ignore than one lone voice.

What This Means for Your Operation

- Calculate your sustainability gap per cwt in the next 30 days. Use your own quotes for digesters, cover crops, and grazing shifts, plus the ranges above, to calculate added costs per cwt; subtract firm premiums and project payments. If the result is positive, you’re self‑funding someone else’s climate target.

- Read your contracts for where the climate value sits. Look for language that assigns all environmental and tax credits to the project entity and locks in long-term commitments with minimum volumes and lender rights. Bring those clauses to your advisor or lawyer before you sign.

- Tie your “yes” to a floor and a formula. Before agreeing to any new sustainability requirement or label, ask for a written milk price floor for participating farms and a simple per‑cwt formula showing your share of any climate‑related value — credits, premiums, or brand payments.

- Factor manure contracts into your succession plan. If you’re planning a transition in the next 10–20 years, treat long‑term manure and RNG deals like major debt instruments. Your lender, lawyer, and kids need to understand what their limits are before anyone signs.

- Watch RIN and LCFS credit prices, not just milk futures. Brownfield’s coverage and energy‑market analysis make it clear that more digester profitability is tied to RINs as LCFS weakens. If incentives shift, your developer’s ability — and willingness — to share revenue shifts too.

- Ask one blunt question in every sustainability pitch. “Over the life of this deal, in dollars per cwt, how much of the climate value created on my farm comes back to my milk check, and how much stays on your balance sheet?” If nobody answers plainly, you’re not looking at a partnership yet.

Key Takeaways

- Standard RNG contracts assign LCFS credits, RINs, tax incentives, and Scope 3 reductions to developers and processors, not farms — by design, to satisfy lenders and offtakers.

- Aaron Smith’s analysis puts digester costs at ~$1,130/cow/year and gas value at ~$128/cow/year, a gap backed up by the 2025 Terrain Ag report’s finding that fuel is “the smallest share of the revenue stream.”

- If your sustainability premium per cwt doesn’t match your added sustainability costs per cwt over a realistic timeframe, you’re financing climate goals out of equity — and the $584,000 modeled gap on a 400‑cow herd shows how fast that adds up.

- Policy risk is real: with LCFS values weakening and more profitability tied to RINs and federal incentives, any long‑term manure contract that assumes today’s credit value is exposing you to someone else’s policy bet.

- Your best defense is to treat sustainability as a financial product and negotiate for a contractual milk price floor, a defined share of the climate value stack in dollars per cwt, and exit terms that don’t trap the next generation.

Before you sign the next “climate‑smart” agreement, pull your last year of milk checks and your cost‑of‑production worksheet. What’s your actual full cost per cwt — and how many dollars per cwt of the climate value created on your farm are guaranteed to come back to you in writing?

That spread is the only sustainability metric that really decides what happens to your operation.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Three Dairy Producers Just Transformed $2.5 Million in Manure Costs into Million-Dollar Revenue Streams – Reveals the operational blueprints three pioneering producers used to flip a $306-per-cow liability into a massive asset. It delivers the specific math on biochar and nutrient recovery that can bridge your farm’s sustainability gap today.

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Arms you with the brutal market data needed to survive the 2026 margin squeeze. It exposes the $250,000 annual shortfall facing mid-sized herds and provides a systematic risk management plan to protect your equity.

- 400 of 1,600 Danish Farms Report Bovaer‑Linked Health Issues: EFSA’s 2026 Review and the 3 Methane‑Contract Clauses to Read Twice – Breaks down the catastrophic “hidden” costs of methane mandates that marketing brochures ignore. You’ll gain a critical understanding of the three non-negotiable contract clauses that protect your herd’s health and your bottom line.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.