At $18.95 stress‑test milk and repriced debt, the gap between a viable farm transition and a slow‑motion exit is narrower than most families think — and your lender already knows which side you’re on.

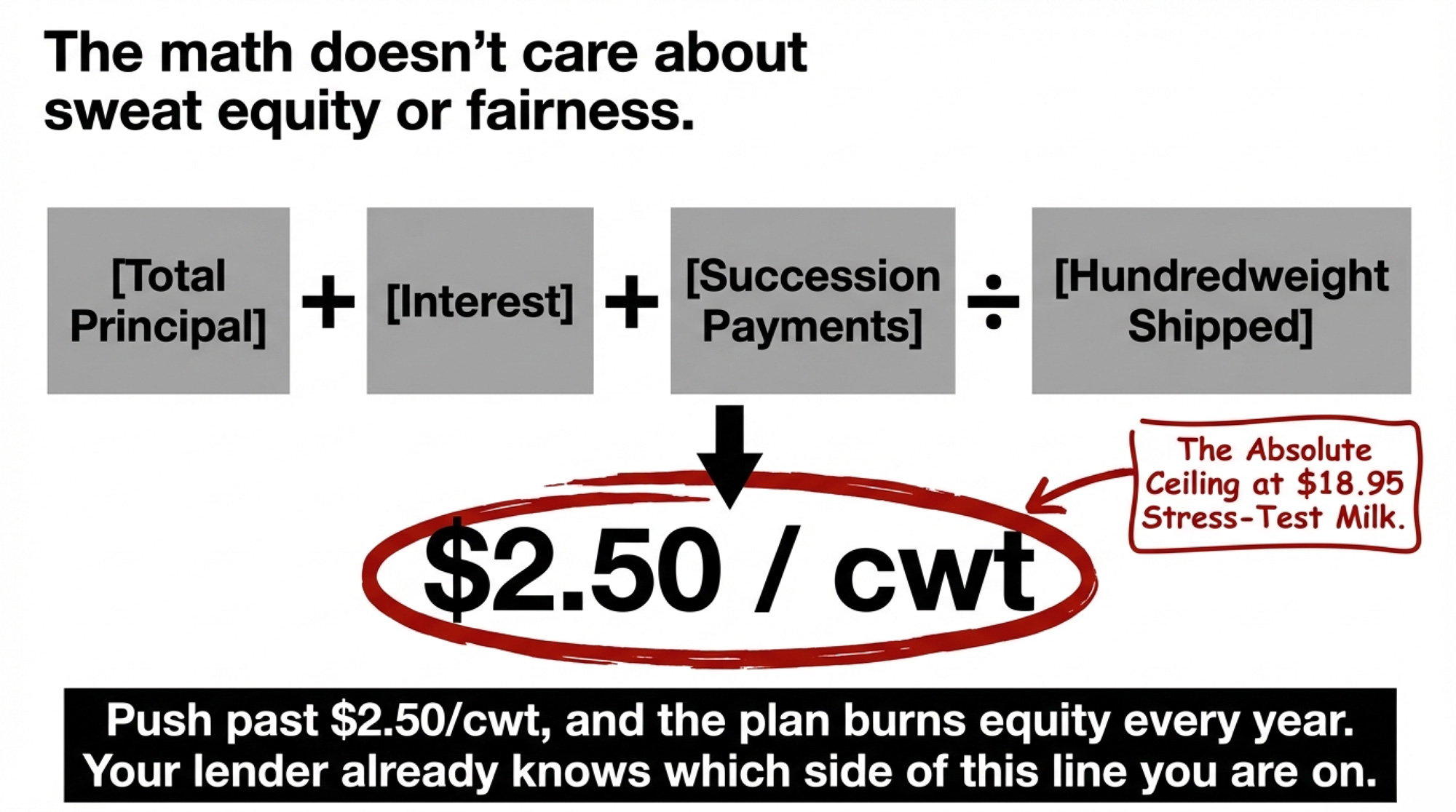

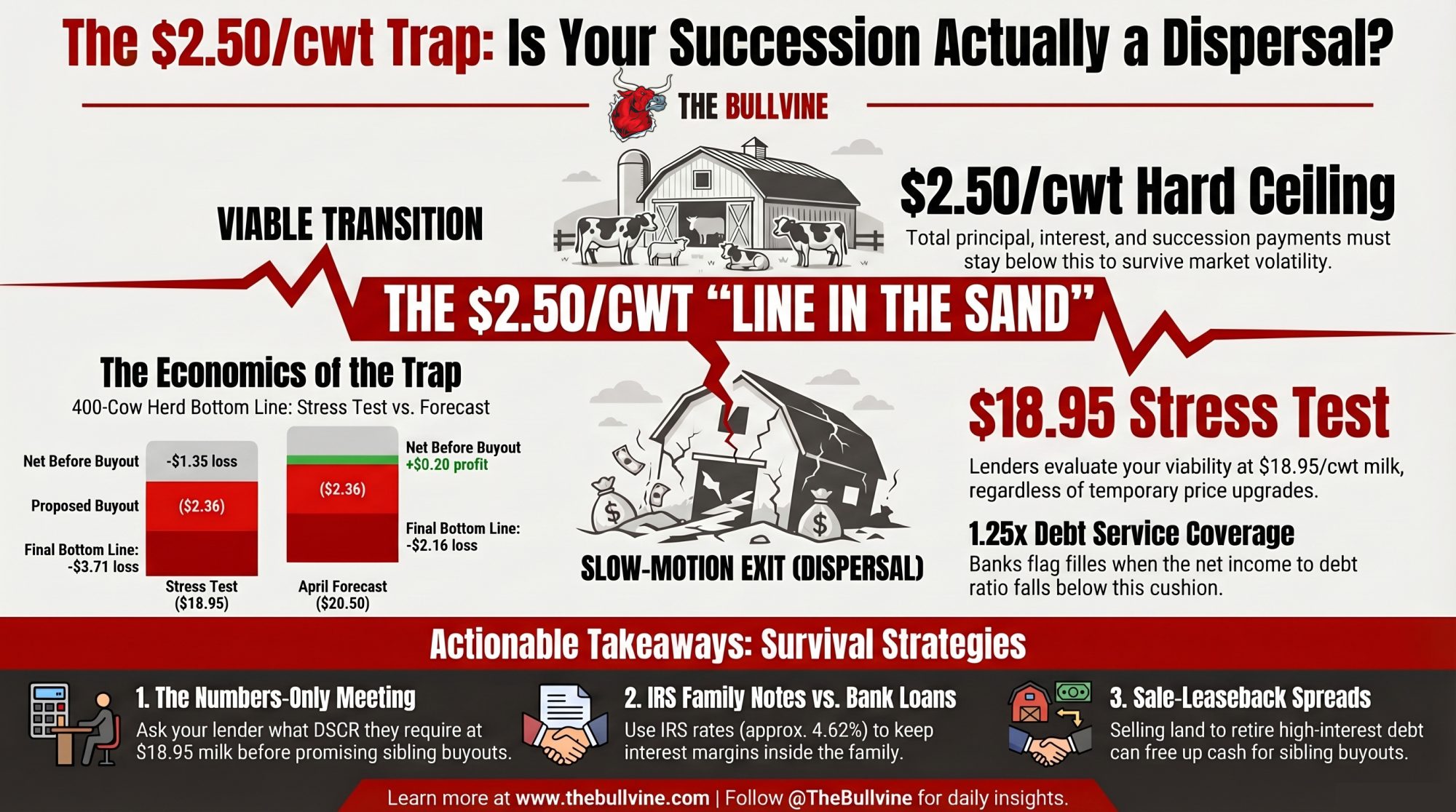

Steve Bodart runs a dairy financial consulting firm called AgriGrowth Solutions out of Elk Mound, Wisconsin. Speaking on the Uplevel Dairy podcast, he described spending his days at kitchen tables with farm families in Wisconsin and Minnesota, trying to answer one blunt question: can this dairy actually afford its own succession plan at today’s prices and interest costs? His first move isn’t a values talk. It’s a calculator. Add up every dollar of principal, interest, and proposed transition payments. Divide by hundredweight shipped. If that number clears about $2.50/cwt, the plan doesn’t survive contact with a stress‑test milk price.

As Bodart highlighted on the Uplevel Dairy podcast, that single number is the line this article keeps coming back to. Not feelings. Not “fair market value.” Just whether your milk check can carry the math — and what your options are when it can’t.

2026 Economics: Milk Price “Upgrades” and Rising Interest Bills

Two big forces are colliding under mid‑size herds right now.

On the revenue side, USDA’s February 2026 WASDE pegged the all‑milk price at $18.95/cwt. March bumped it to $19.70, and the April 9 update pushed it to $20.50 again. That looks like good news in the headline. But you still do your stress test at $18.95, because that’s the price band lenders and analysts are using to see who survives when the air goes out of the market. And it’s not a fantasy number. Bullvine’s earlier work showed USDA’s 2026 all‑milk “upgrade” only lifted projected revenue to $18.95 against about $19.14 in fully loaded costs — still upside down once you count unpaid family labor and realistic depreciation. Cash costs vary widely — a low-debt, 600-cow freestall with owned feed might run $16/cwt, while a 350-cow herd buying all feed could be north of $20. Use your actual number, not this one.

On the cost‑of‑money side, the numbers have shifted just as hard. A 2025 review of USDA Farm Service Agency loans showed average first‑year interest expense on operating loans more than doubled between 2005 and 2024 — from roughly $18,000 to $40,000. Farm ownership loan interest went from about $28,000 to $50,000 over the same window. Even with headline rates similar to 2007, producers are now paying 50–62% more in first‑year interest and 72–89% more in total first‑year payments because they borrowed a lot more principal.

Land and heifer costs piled on. Wisconsin cropland averaged $6,800/acre in 2024 (USDA NASS) and climbed to $7,250 in 2025, according to Wisconsin DATCP. That looks great on a balance sheet, but it pushes expectations for sibling buyouts higher. CoBank’s 2025 heifer report warned that U.S. dairy heifer inventories could fall by around 800,000 head through 2025–2026, dropping to the lowest levels since the late 1970s before any rebound in 2027. In that environment, bred heifers in the Upper Midwest pushed into the $3,000‑plus range for quality animals.

You see it in your own decisions. Maybe you bought springers at $1,600 five years ago. Now they’re $2,800–$3,200 when you can find them. CoBank dairy economist Corey Geiger summed it up this way: “Heifer values have reached record highs and could climb well above $3,000 per head.” That doesn’t just hurt when you sign the check. It shows up quietly in your per-cwt debt.

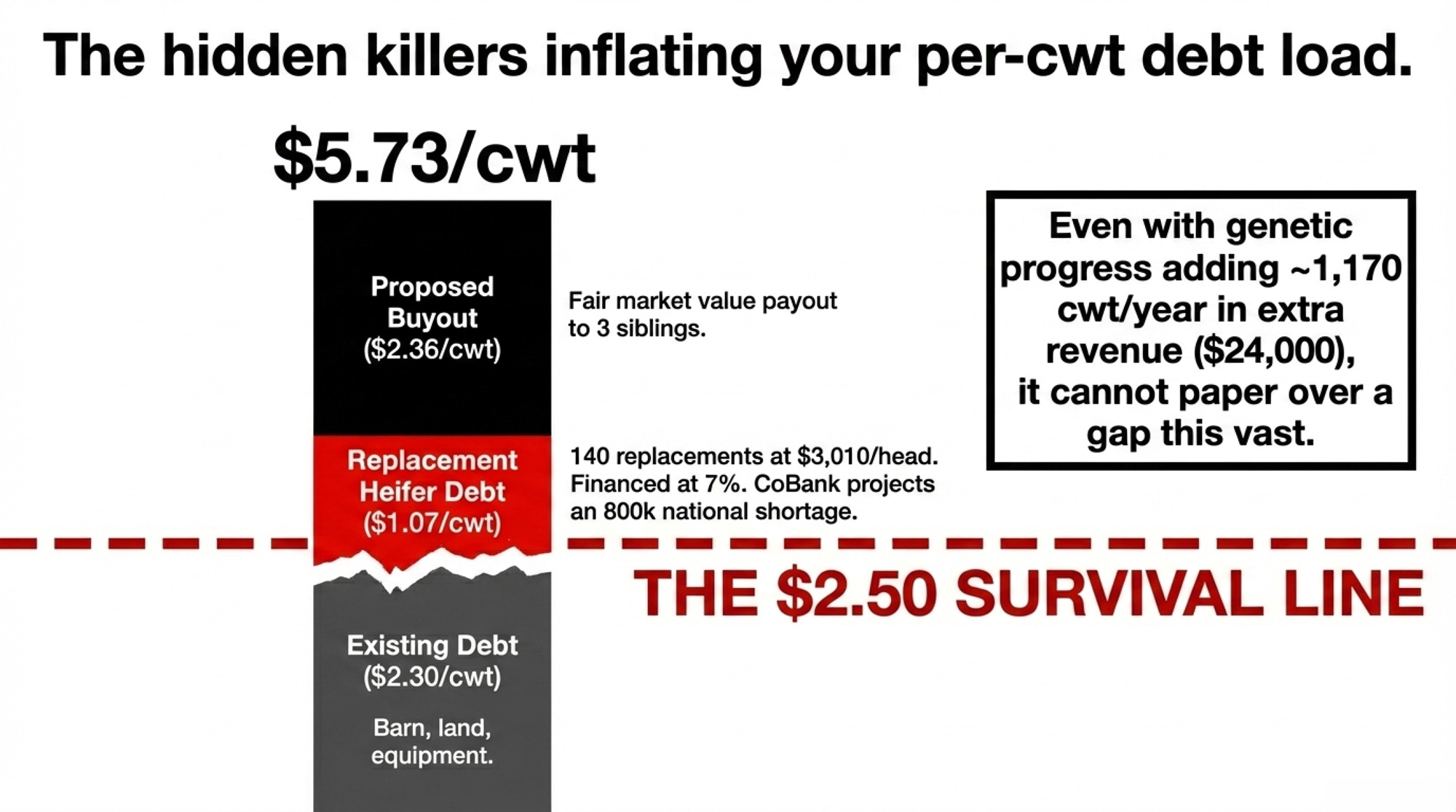

A 400‑cow herd turning over 35% of the milking string each year needs about 140 replacements. At $3,010 per head — CoBank’s 2025 average — that’s about $421,400 in capital tied up in replacements. Finance that at 7% over five years, and you’re looking at just under $103,000 a year in payments. Spread across 96,000 cwt, you’ve added roughly $1.07/cwt in debt service. Your cow count didn’t change. Your per‑cwt debt load did.

When you stack all this — thinner milk margins, higher interest, more expensive land, $3,000 heifers — on top of an already leveraged 400‑cow operation, you can see why Bodart starts with $/cwt instead of dreams about passing the farm on.

How This Plays Out on Real Farms

Across Wisconsin and Minnesota, the pattern Bodart describes on the Uplevel Dairy Farm Forward episode is uncomfortably familiar.

You’ve got a 400‑cow freestall, maybe 450 if you’re counting high pens and hospital strings. Mom and Dad still sign the checks. The next generation is already working there — maybe as the herdsman or managing cropping — drawing a modest wage that everyone silently treats as “sweat equity.” Off‑farm siblings are teachers, nurses, tradespeople, or run their own businesses in town. The expectation is that someday, when everyone’s ready, the farming child will “buy the farm” and the others will be treated “fairly.”

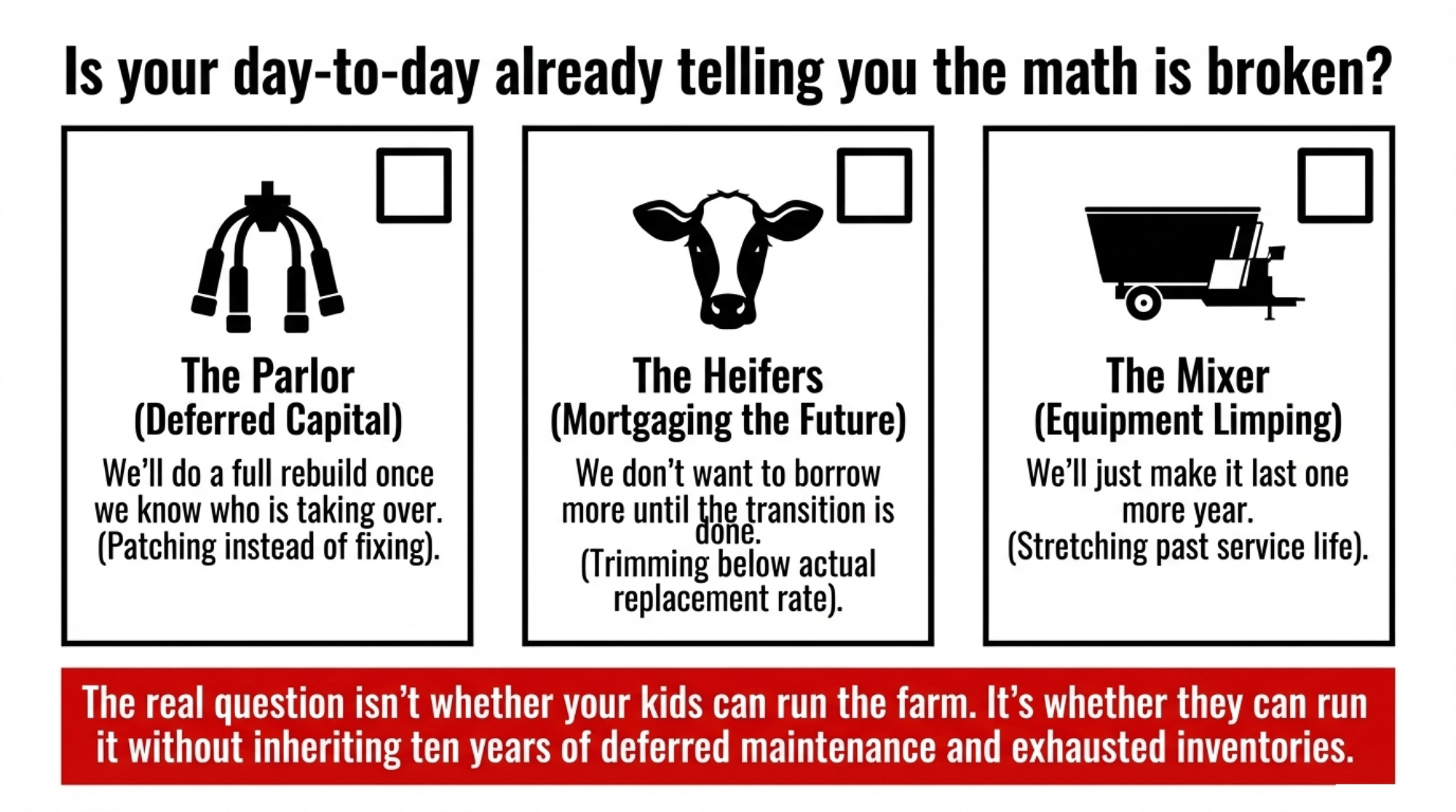

The first warning sign isn’t a missed payment. It’s a string of deferred decisions. A parlor repair gets patched instead of fully rebuilt because “we’ll fix it once we know who’s taking over.” Heifer numbers get trimmed because “we don’t want to borrow more until the transition is done.” A worn mixer keeps limping along one more year.

Underneath those deferrals is simple barn math. A 550‑cow Wisconsin dairy that sat down with a financial advisor earlier this year put cash operating costs at about $17.25/cwt and fully loaded economic costs (including unpaid labor and real depreciation) at $18.75/cwt. UW dairy budgets numbers put many mid‑size Upper Midwest herds in a similar ballpark. If you’re running cash costs around $18/cwt, here’s what your stress test really looks like on 400 cows.

How Much Does Saying “Yes” to the Succession Buyout Really Cost?

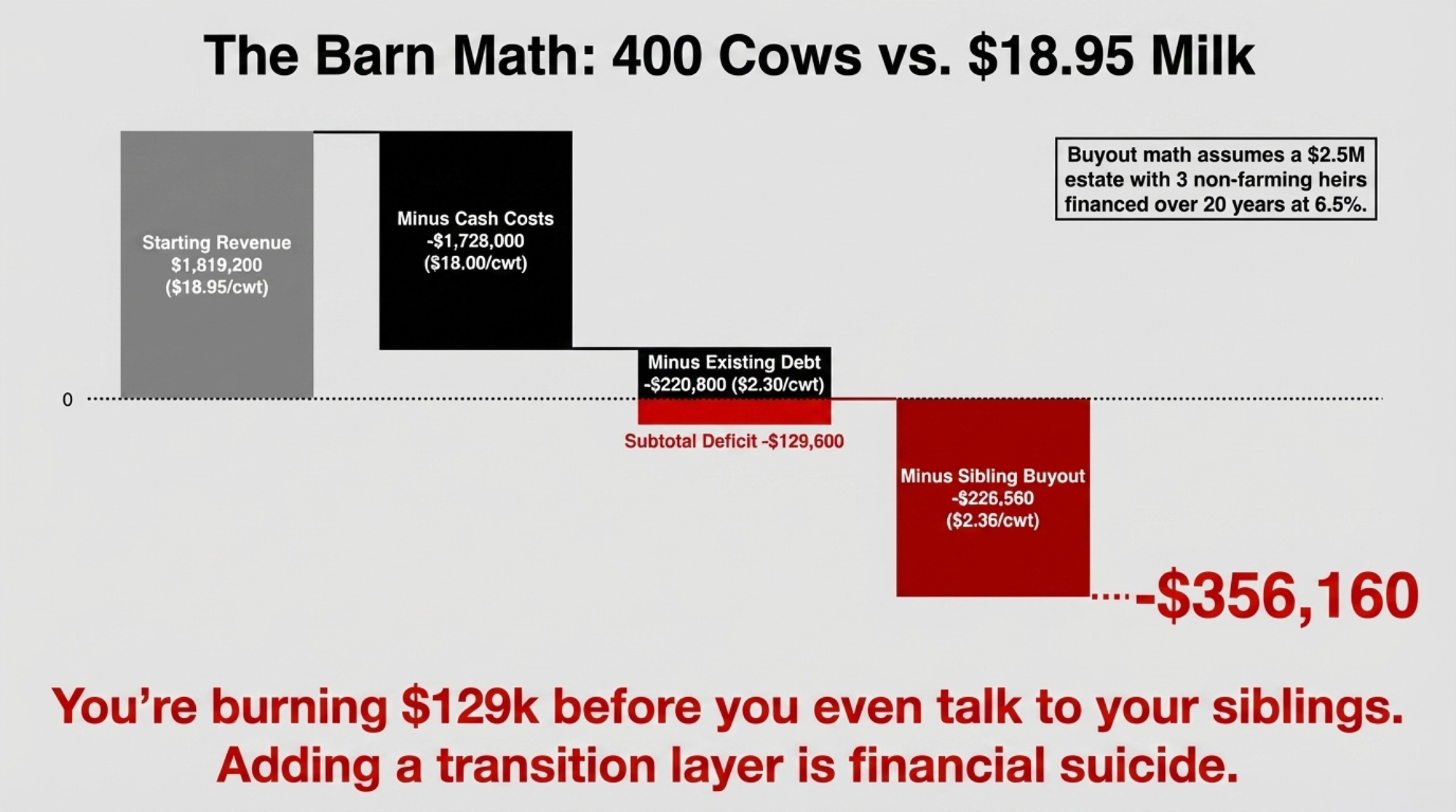

Let’s take that 400‑cow herd shipping 96,000 cwt a year. You’re in Wisconsin. Cash costs run about $18/cwt. You’re already servicing about $2.30/cwt in principal and interest across barn, land, and equipment loans.

Here’s the barn-math table Bodart described walking clients through on the podcast.

| Metric | Stress Test ($18.95/cwt) | April Forecast ($20.50/cwt) |

| Gross Income (96,000 cwt) | $1,819,200 | $1,968,000 |

| Cash Operating Costs ($18/cwt) | ($1,728,000) | ($1,728,000) |

| Existing Debt Service ($2.30/cwt) | ($220,800) | ($220,800) |

| Net Before Buyout | −$129,600 | $19,200 |

| Proposed Buyout ($2.36/cwt) | ($226,560) | ($226,560) |

| Final Bottom Line | −$356,160 | −$207,360 |

Those buyout payments don’t come from a random number. A 400‑acre Wisconsin farm at $7,250/acre has about $2.9 million in land value. Add buildings, cows, and iron, and you’re probably north of $3.5 million in total equity. With three non‑farming siblings, the farming heir could be staring at around $2.5 million in expected buyout obligations.

Finance $2.5 million over 20 years at 6.5% and you’re looking at roughly $227,000 per year in payments — about $2.36/cwt on 96,000 cwt. Stack that on top of the existing $2.30/cwt, and you’re north of $4.60/cwt in total annual debt service. Even with USDA’s April forecast of $20.50 milk, this 400‑cow herd has just $19,200 left after cash costs and current debt — and the buyout wants $227,000.

At $18.95 stress‑test milk, there’s no wiggle room at all. You’re burning more than $129,000 before you even talk about siblings — and more than $350,000 once you do. That’s not a succession plan. That’s a slow‑motion dispersal that just hasn’t been named yet.

The Mechanics Behind the Numbers

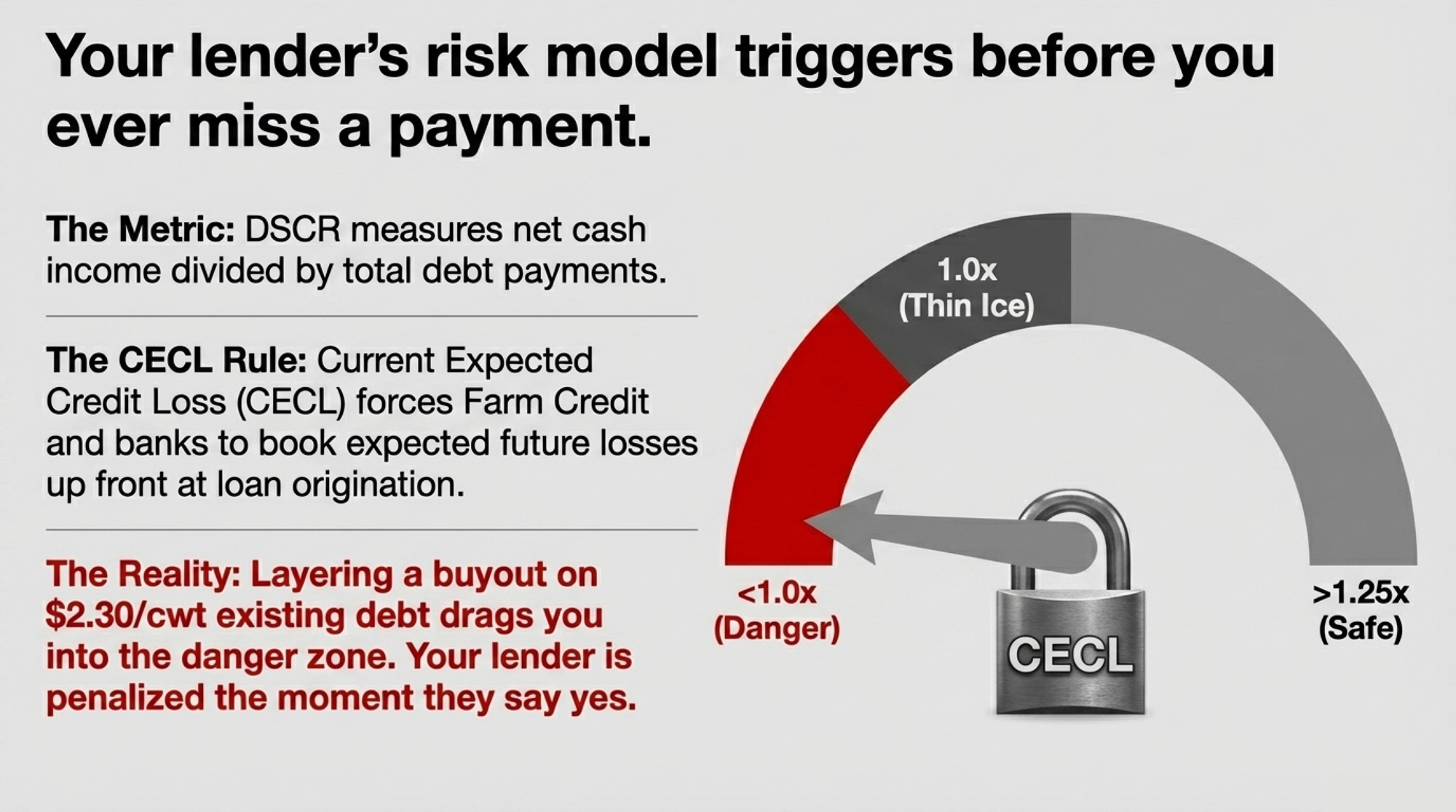

Two metrics drive almost every decision your lender makes: debt service per cwt and debt‑service coverage ratio (DSCR).

Debt service per cwt is straightforward. Add up every dollar of principal and interest you pay in a year — operating, term, land, equipment, everything — and divide by hundredweight shipped. Bodart’s rule of thumb out of Elk Mound is that total principal + interest + succession payments combined shouldn’t exceed about $2.50/cwt at today’s prices. Go above that, and you’re relying on either unusually strong milk, unusually low costs, or unusually patient creditors.

DSCR is the ratio your lender stares at: net cash income before debt service divided by total annual debt payments. A DSCR of 1.25× means you’re generating 25% more cash than needed to cover your obligations. Many Farm Credit associations and ag banks treat 1.25× as a comfortable cushion, 1.0× as thin ice, and anything below 1.0× as a “we need to talk” situation. When you’re layering a buyout on top of $2.30/cwt in existing debt, you’re not just asking if you can pay another bill. You’re asking your lender to underwrite a plan that could drag your DSCR down into the danger zone for a decade.

The CECL rules (Current Expected Credit Loss) changed how that feels on their side of the desk. Under CECL, Farm Credit and banks now have to book expected future credit losses up front — at origination and at renewal — rather than waiting until loans go bad. CoBank’s 2025 annual report showed a $77 million provision for credit losses in Q1 2025, compared to a $37 million reversal a year earlier — a swing driven partly by CECL models reacting to rising risk in ag portfolios. That means every new transition note doesn’t just affect your family. It affects their capital requirements.

There is one piece of the puzzle that works in your favor: genetic progress. USDA ERS data shows U.S. milk per cow reached 24,391 pounds in 2025, up 1.2% year‑over‑year. The April 2025 CDCB base change captured that cumulative progress across milk, fat, and protein. On a 400‑cow herd, that 1.2% gain adds around 117,000 pounds, or about 1,170 cwt, without a single new stall. At $20.50/cwt, it’s roughly $24,000 in extra revenue. That helps spread your fixed debt across more hundredweight. It does not paper over a $200,000‑plus annual gap between “what you have” and “what the buyout wants.”

Is Your Day‑to‑Day Already Telling You the Answer?

You don’t always need another spreadsheet to know that the plan doesn’t pencil out.

If you’re already stretching equipment past its service life because “we’ll replace it after the transition,” your day‑to‑day decisions are quietly telling you there isn’t room in the cash flow for both capital and buyouts. If you’ve trimmed heifer numbers below your real replacement rate because “we don’t want to add more debt,” you’re mortgaging future production to keep today’s principal and interest manageable.

Sometimes the stress‑test is sitting right in front of you: you’re carrying $2.30/cwt in existing term debt, and you’re still deferring basic maintenance. That’s with one household. What happens when two households expect to make a living off that same check?

The real operational question isn’t “can my son or daughter run this farm?” It’s “can they run this farm under this debt load, at this milk price, without inheriting ten years of deferred maintenance and exhausted heifer inventories?”

The legal system has already started answering that question in painful ways. In a 2025 Ontario case covered in Bullvine’s “Only 12% of Dairy Farms Reach Generation Three” feature, a family kept an informal succession arrangement going for six extra years after a lender determined the proposed buyout note couldn’t be serviced on a 10‑year schedule. When the matter finally hit court, the lack of formal structure and the disconnect between expectations and cash flow turned a farm‑succession discussion into a litigation file.

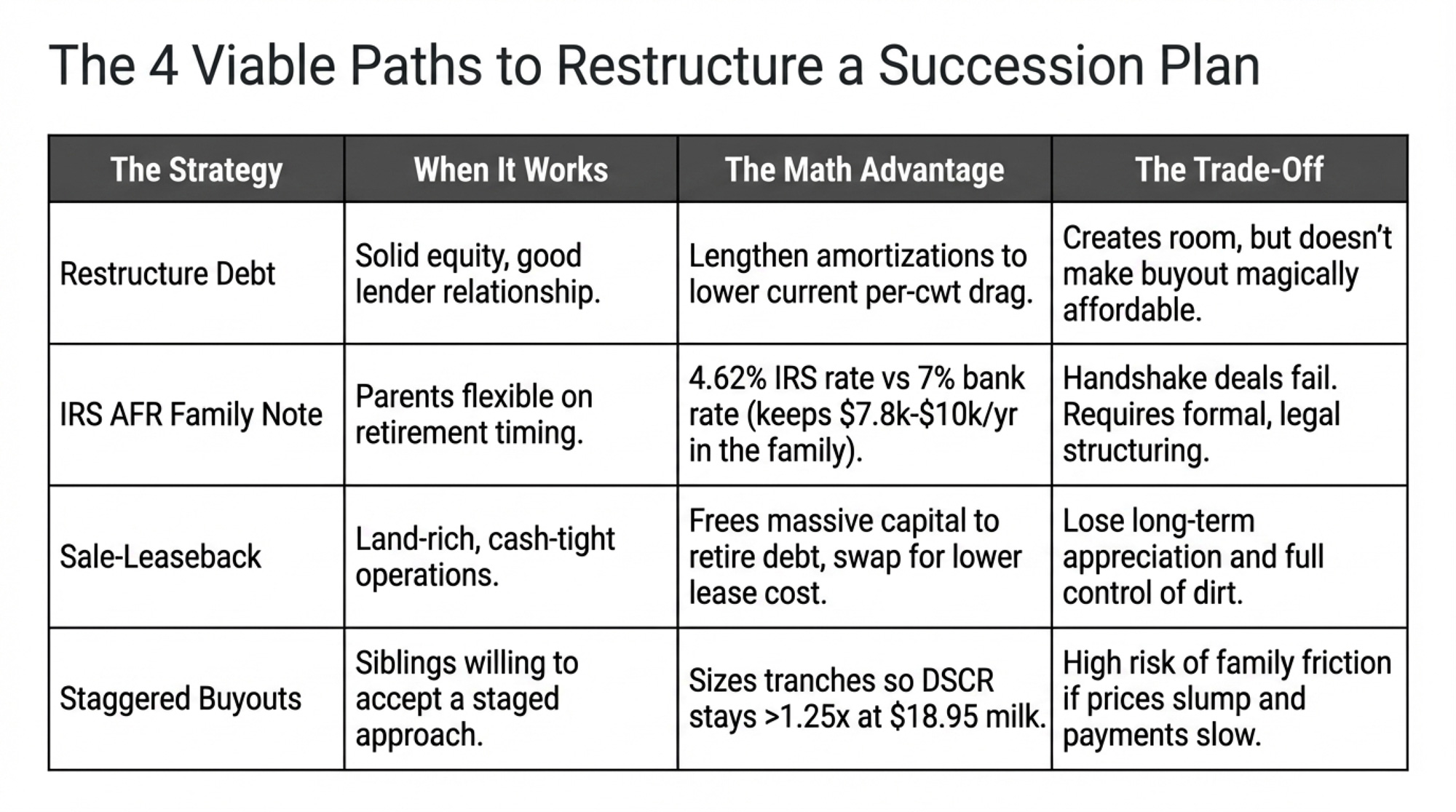

Options and Trade‑Offs for Farmers

If you’re that 400‑cow Upper Midwest dairy — $2.30/cwt in existing debt, three siblings, next generation already on the payroll — you still have choices. None is painless. Some are still better than drifting along, hoping $22 milk comes back and fixes everything.

1. Restructure debt before you restructure ownership

When it makes sense: You’ve got equity left, your relationship with the lender is still solid, and you’re not already in arrears.

What it requires: A numbers‑only meeting with your Farm Credit or bank officer. Bring three things: total term debt, total annual principal and interest, and last year’s hundredweight shipped. Ask them to model your DSCR and per‑cwt debt service at $18.95, not just last year’s average price. Then ask them to layer in the proposed buyout payments over 20 years and show you what your DSCR looks like.

You’re not arguing for sympathy. You’re asking for structure: longer amortizations on some notes, rate adjustments where possible, or moving certain assets into lower‑risk categories that are easier for them to carry under CECL. If you’ve had one or two good years recently and used them to pay down principal instead of buying iron, this is where that discipline pays off.

Risks/limits: Restructuring doesn’t make your buyout magically affordable. It creates room. If your DSCR is already wobbling near 1.0×, there may not be enough room left to get post‑transition coverage back up into that 1.25× comfort zone. You’ll know after that meeting — not in another five years.

30‑day action: Book that meeting this month. Ask three direct questions:

- What is our DSCR at $18.95 per cwt of milk today?

- What would it be if we added the proposed buyout payments?

- What DSCR and total payment per cwt do you need to see to be comfortable saying yes?

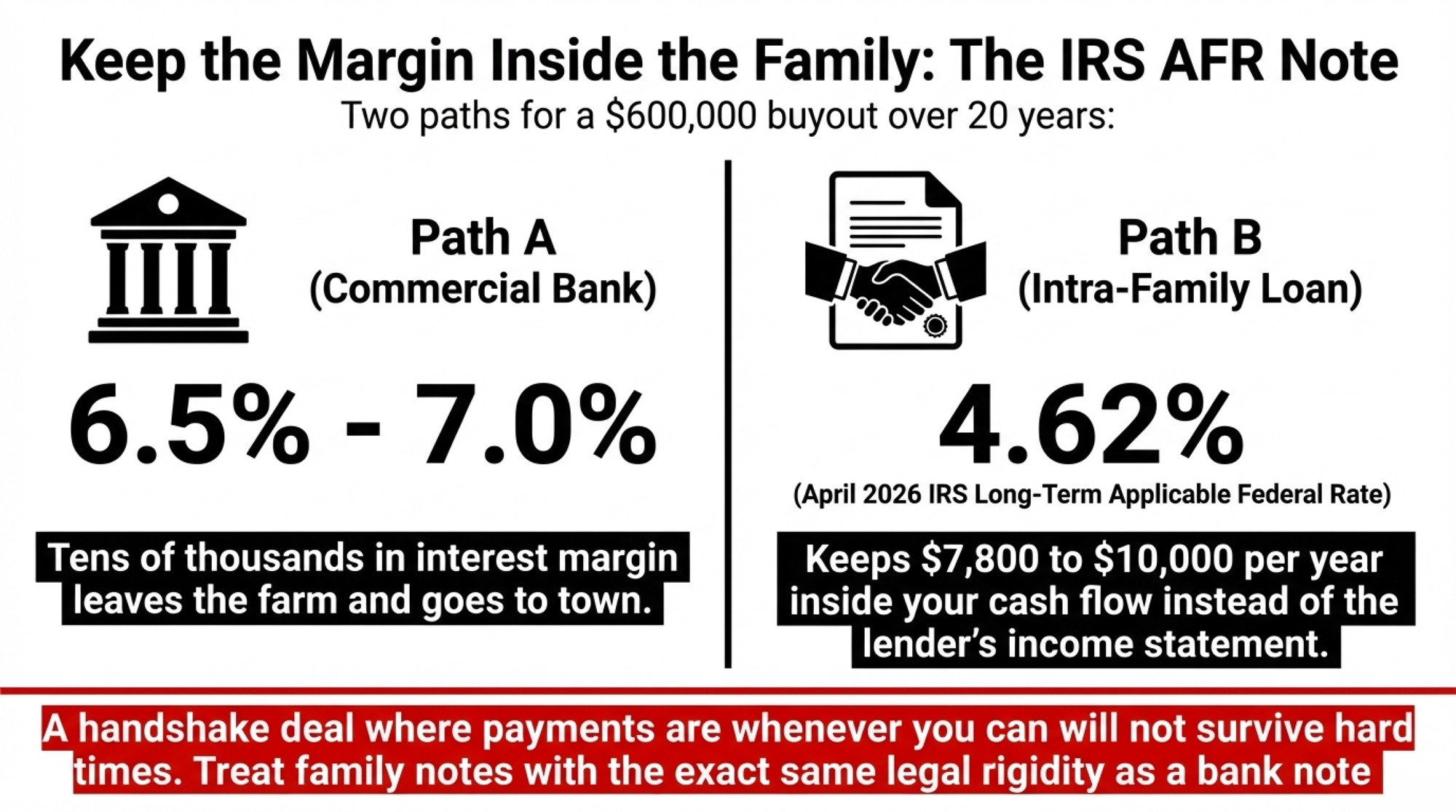

2. Swap a bank‑financed buyout for an IRS AFR family note

When it makes sense, parents have some flexibility in the timing of retirement income and trust the farming heir to make steady payments. Siblings would rather get paid in full over time than risk a forced sale later.

What it requires: A formal intra‑family loan at the IRS Applicable Federal Rate instead of a commercial 6.5–7% note. The long‑term AFR for April 2026 is 4.62% (IRS Rev. Rul. 2026‑07). On a $600,000 buyout over 20 years, that spread versus a 7% bank loan keeps roughly $7,800–$10,000 per year in your cash flow instead of in the lender’s income statement, depending on the exact commercial rate.

You still do the paperwork: promissory note, security, repayment schedule, and reported interest income on the parents’ or siblings’ side. You move the interest margin inside the family instead of sending it to town.

Risks/limits: A handshake deal where payments are “whenever you can” doesn’t survive hard times. The Ontario case shows what happens when expectations and reality aren’t documented. You will still need an accountant or attorney to structure it properly — and you’ll still need a plan for what happens if the farm can’t make those payments someday.

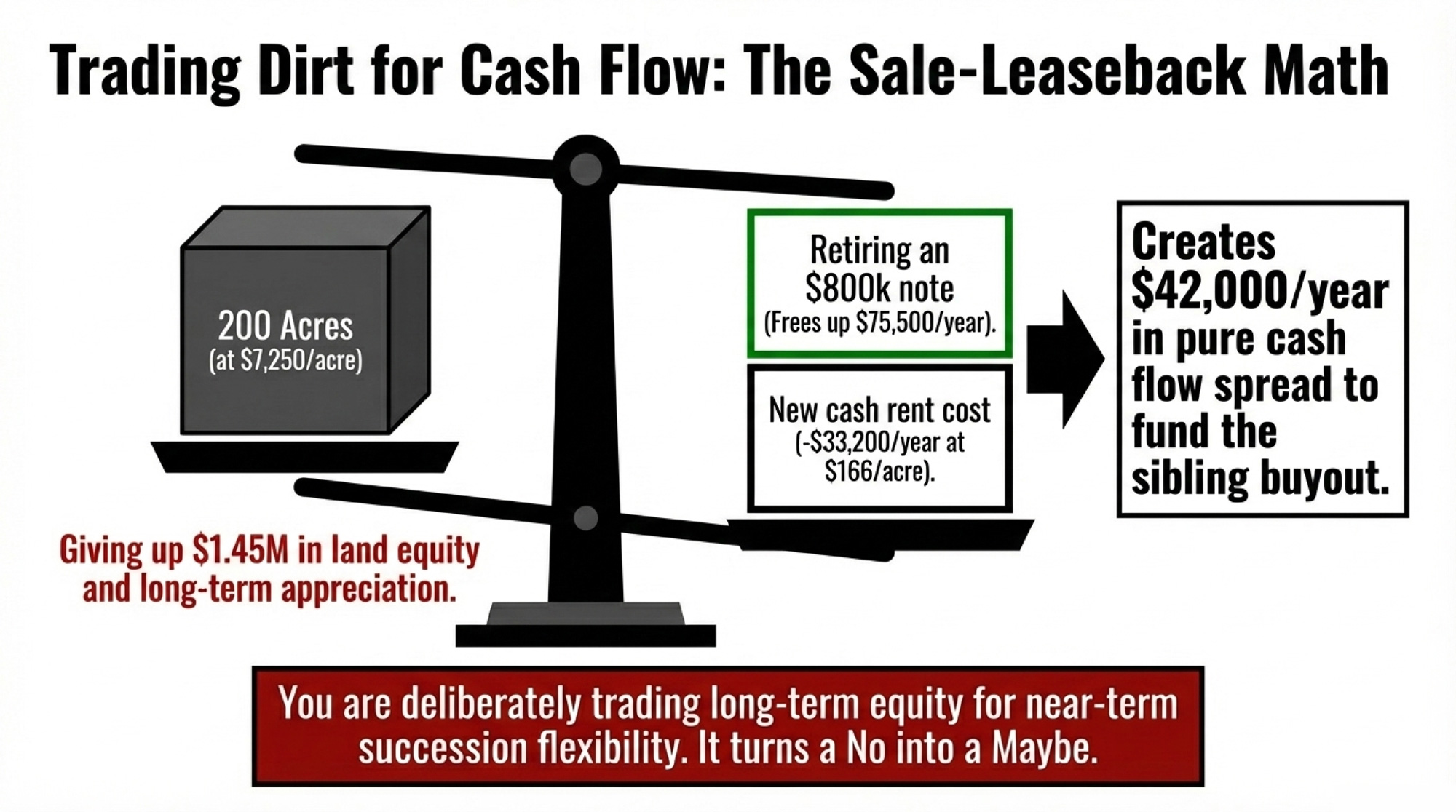

3. Sell land, lease it back, and use the spread to fund part of the buyout

When it makes sense: You’re land‑rich, cash‑tight, and serious about the next generation running cows, even if they don’t own every acre from day one.

What it requires: A deliberate sale‑leaseback. Wisconsin cropland averaged $7,250/acre in 2025. USDA NASS reported an average cash rent of around $166/acre. If you sell 200 acres at $7,250, you free up about $1.45 million in cash. Use that to retire an $800,000 barn or land note at 7% over 20 years, and you’ll cut roughly $75,500/year in payments. Leasing those 200 acres back at $166 costs about $33,200/year.

That spread — roughly $42,000/year — can go toward a sibling buyout without further tightening your operational cash flow. It won’t cover $227,000 by itself. It does make a partial buyout more realistic.

Risks/limits: Once you sell land, you’ve given up long‑term appreciation and full control. The buyer, lease terms, and any right of first refusal matter. You’re trading long‑term equity for near‑term cash flow and succession flexibility. Some families will take that trade. Others won’t.

4. Stagger sibling buyouts instead of doing them all at once

When it makes sense: You have multiple non‑farming heirs who want to be treated fairly but are open to a staged approach.

What it requires: A written plan that lines up with what the milk check can carry. Maybe sibling one gets bought out in years 1–7, sibling two in years 8–14, and the third receives a mix of partial buyout and estate allocation. You size each tranche so post‑buyout DSCR stays above 1.25× at $18.95 milk. You also make it very clear what happens if prices slump and payments need to slow down — before that slump hits.

Risks/limits: This isn’t just math. It’s family dynamics. If one sibling feels their payout was riskier or delayed, the transition can sour relationships, even if everyone eventually reaches the same dollar amount. An outside facilitator — an accountant, attorney, or advisor — helps keep the conversation focused on the numbers rather than old grievances.

Key Takeaways

- If your total principal, interest, and proposed succession payments push you past about $2.50/cwt, you’re not talking about a viable two‑household plan at $18.95 stress‑test milk — you’re talking about a managed drawdown of equity. The sooner you name that, the more options you still have.

- If your post‑transition DSCR falls below 1.25× at $18.95 milk, your lender’s CECL models have already flagged your file as higher risk, even if nobody has said it out loud yet. Pushing ahead with a full “fair market value” buyout under those conditions is a bet that prices and interest will both break your way.

- If your family expects full appraised value at commercial interest rates without changing anything else, do the barn math before you write that number on the whiteboard. On a $2.5 million estate with three non‑farming heirs, the annual payment at 6.5% over 20 years runs about $227,000 — more than many 400‑cow herds clear in net cash at today’s projected prices.

- If you haven’t had a hard‑numbers meeting with your lender before you sit down with siblings, you’re building promises on someone else’s risk limits. Get their line in the sand first. Then fit your family plan inside the space your milk check and DSCR actually give you.

- If the honest math says “no” to full succession under your current structure, treat that not as failure but as information. A planned, equity‑preserving exit, where cows and land are sold on your terms and parents and heirs are clear on who gets what, usually beats five years of grinding toward a lender‑driven restructuring where everyone walks away with less.

So here’s the kitchen‑table question worth answering this month: does your milk check actually have room for a transition layer, or are you already rationing cash to keep the wheels on? At $18.95 stress‑test milk, a 400‑cow Wisconsin dairy with $18/cwt cash costs and $2.30/cwt in existing debt has a negative margin before paying a single dollar to siblings. Even at USDA’s upgraded $20.50 forecast, that herd has $19,200 left after cash costs and current debt — and the buyout needs $227,000. The price moved. The math didn’t.

If you want to stop guessing, put your own numbers through the same stress test.

Methodology Note: Cost-of-production data draws on USDA ERS and UW Extension dairy enterprise budgets. WASDE all-milk prices from February, March, and April 2026 reports. Wisconsin land values from USDA NASS (2024) and Wisconsin DATCP (2025). Heifer pricing from CoBank’s 2025 dairy sector outlook. All dollar figures are USD. National and state averages may not reflect your specific herd size, management system, or debt structure. We welcome producer feedback and corrections.

Learn More

- 438,000 Missing Heifers. $4,100 Price Tags. Beef-on-Dairy’s Reckoning Has Arrived. – Explains the tactical breeding shifts and extended lactation protocols you need right now to slash replacement costs. It arms you with a management roadmap to survive the $4,100 heifer market without tanking your 2028 cash flow.

- Only 12% of Dairy Farms Reach Generation Three – A 2025 Court Ruling Exposes Why Succession Fails and How to Fix It – Exposes the legal landmines that blow up multi-generational transfers when math and paperwork don’t match. It delivers a strategic entity-separation blueprint to protect family equity from the “informal agreement” trap that sinks most dairies.

- Is Feed Efficiency Measurement Finally Worth It? (New Research Says Yes) – Breaks down the emerging ROI on genetic feed efficiency as the ultimate margin-builder in high-interest environments. It reveals how capturing a $30,000 annual advantage through precision selection can bridge the gap between dispersal and success.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.