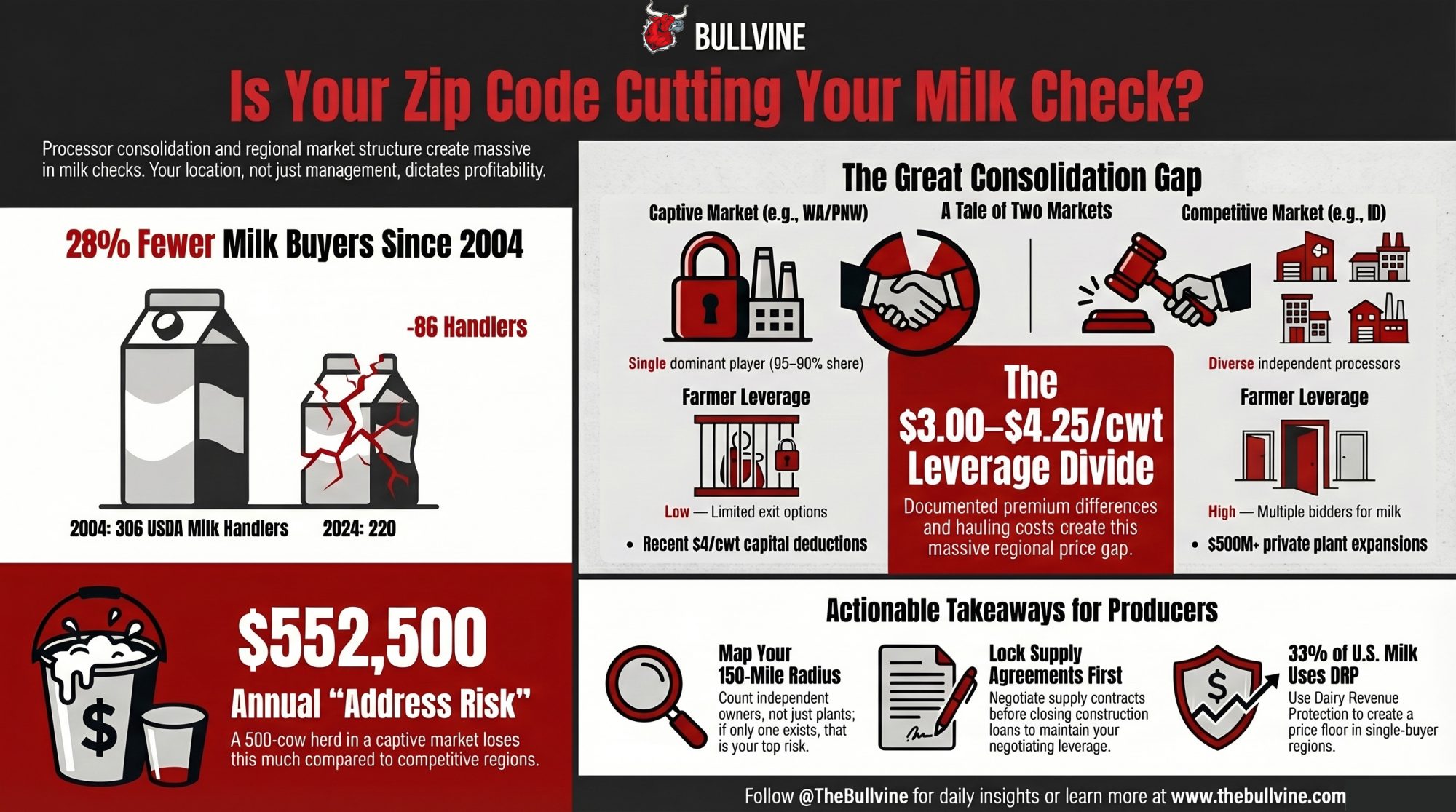

Processor consolidation has cut U.S. milk handlers by 28% in two decades. The gap between competitive and captive markets now runs $3–4/cwt — and your address determines which side of that line you’re milking on.

Krista Stauffer’s family has shipped milk to Darigold for years, building equity in the cooperative, as generations of Pacific Northwest dairy families have. She shared that they now have “quite a bit of equity sitting there” — with a real chance that only her kids ever see it come back. Her situation isn’t a one-off grievance. It’s what happens when processor consolidation narrows your options to one real buyer. And the financial distance between farming where processors compete for your milk and farming where a single handler calls the shots is wider than most people think.

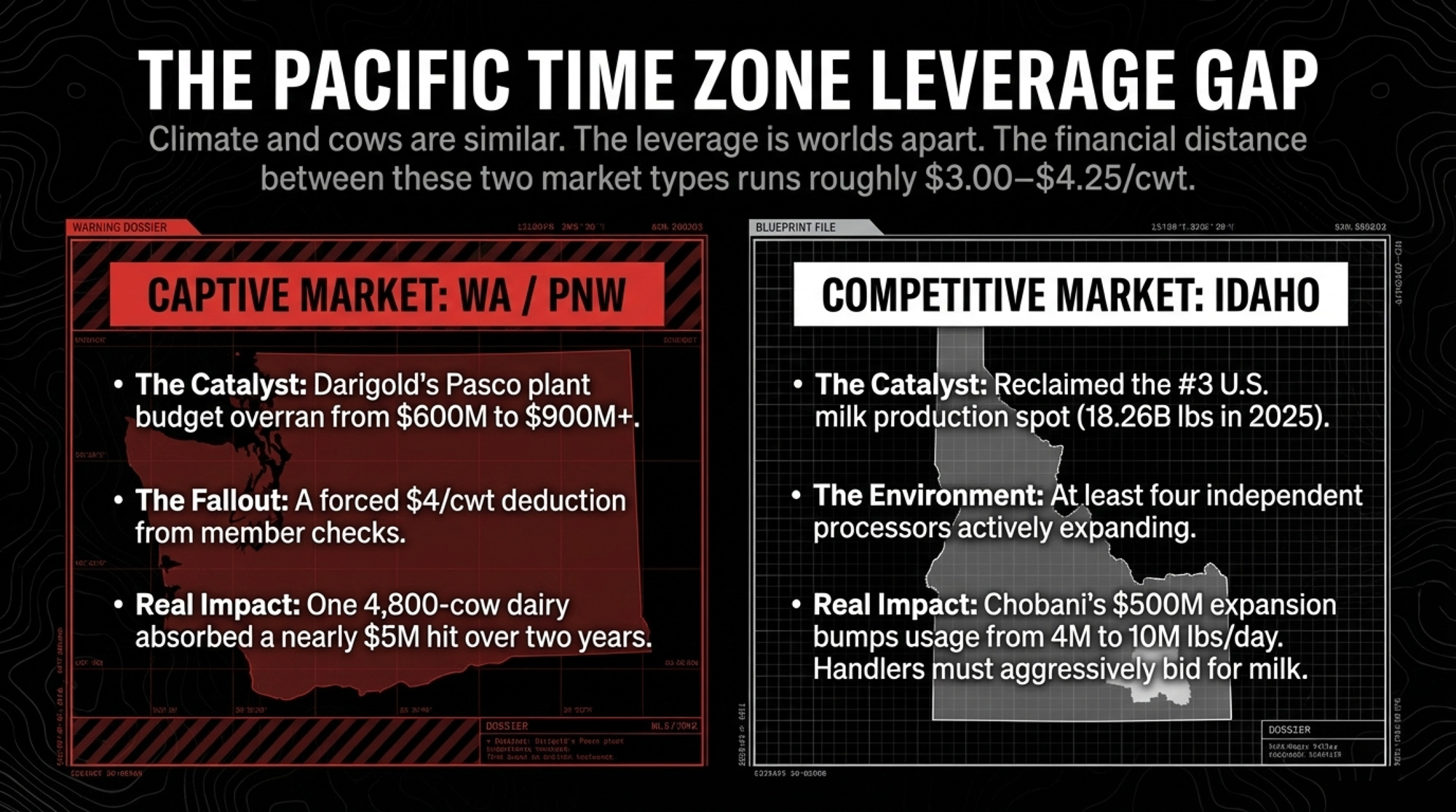

When you stack documented premium differences, structural hauling costs, and the 2025 make-allowance hit together, the gap between the best and worst regions runs roughly $3.00–$4.25/cwt on your milk check. On a 500-cow herd, that’s $390,000–$552,500 a year, driven by your zip code, not your TMR.

From 306 Buyers to 220

Twenty years ago, the USDA counted 306 handlers pooling milk across the federal orders. By 2024, that number had dropped to 220 — a 28% decline (USDA AMS, 2024). Pooled producers fell from 52,853 to 20,168 over the same stretch. Fewer farms are shipping to fewer buyers. That’s the whole structural picture in one sentence.

But it doesn’t look the same everywhere. In Wisconsin’s Upper Midwest order, multiple cooperatives and proprietary processors still overlap routes and counties, so they’re forced to bid for milk. In the Pacific Northwest, Darigold operates 11 production facilities and handles the vast majority of pooled milk in the order — processing up to 8 million pounds per day at its new Pasco plant alone (Northwest Dairy Association annual report; FMMO-124 data). In the Southeast, DFA and its affiliates manage supply for essentially every regulated fluid plant in the Florida order. All three regions are “orderly markets” on paper. On your milk check, they’re completely different worlds.

The $11 Billion Build-Out — and Who It Actually Helps

Processors are in the middle of an $11 billion processing build-out — more than 50 new or expanded plants announced between 2025 and 2028 (Dairy Foods, 2025). Texas, Idaho, New York, and South Dakota are picking up the lion’s share. Pennsylvania, parts of the Northeast, and Washington are losing plants as older facilities shutter or consolidate.

That looks like capital investment on a press release. On the farm, it means some regions are getting more bidders for your milk — and others are getting fewer. The question isn’t whether new capacity is coming. It’s whether any of it lands within your hauling radius.

Same Time Zone, Different Reality: Idaho vs. Washington

The sharpest contrast in American dairying right now sits inside the Pacific time zone. Same climate band. Very different leverage.

Idaho just reclaimed the No. 3 spot in U.S. milk production. According to USDA data released in February 2026, the state’s roughly 350 dairy operations produced 18.26 billion pounds of milk in 2025 — narrowly edging Texas at 18.21 billion (USDA NASS, Feb. 2026). In the Magic Valley, at least four independent processors are actively adding capacity. Chobani broke ground on a $500 million expansion in Twin Falls — its largest capital investment ever — bumping milk usage from about 4 million pounds per day to over 10 million (Chobani, 2025; Twin Falls Times-News). Idaho Milk Products is building in Jerome. High Desert Milk has invested tens of millions in its own operation. Newer players like Suntado have come online. Every one of those plants needs milk. Everyone competes for it. Idaho Dairymen’s Association CEO Rick Naerebout told Dairy Herd Management: “Idaho dairymen, for the most part, are fairly well situated financially right now.”

Drive west, and the story flips. Darigold’s Pasco, Washington, plant — originally budgeted at around $600 million — exceeded $900 million by the time it opened in June 2025 (Capital Press; Reuters, 2025). The cooperative approved the project back in 2021. CEO Stan Ryan pointed to labor shortages and equipment procurement as the main cost drivers. To cover the gap, the cooperative pulled a $4/cwt deduction from member checks (eDairyNews, May 2025). Yakima County producer Dan DeRuyter, milking about 4,800 cows, told reporters the hit amounted to nearly $5 million taken from his operation over two years. He didn’t sign the construction contract. He didn’t pick the procurement strategy. He had no practical alternative buyer for his milk. He just absorbed the deduction.

That’s the governance structure on paper. Here’s how it played out on the milk check: one buyer, one deduction, limited alternatives.

The Leverage Gap at a Glance

| “Captive” Market (WA / PNW) | “Competitive” Market (ID / Magic Valley) | |

| Dominant Player | Darigold (~85–90% of pooled milk) | Diverse: Chobani, Idaho Milk Products, High Desert Milk, Suntado, Glanbia |

| Farmer Leverage | Low — limited exit options, retained equity as anchor | High — multiple independent bidders for milk |

| Recent Trend | $4/cwt capital deduction from member checks | $500M+ in private processor expansions |

| Risk Profile | High “address risk” — geography controls your basis | Dynamic growth — processors competing for supply |

| 2025 Milk Production | ~10 billion lbs (NDA members, WA/OR/ID/MT) | 18.26 billion lbs (Idaho alone, USDA NASS) |

Here’s the barn math that connects those two columns. Take a 300-cow herd shipping about 78,000 cwt a year. In a region with multiple handlers fighting for milk — over-order premiums, quality bonuses, and hauling competition all working in your favor — it’s reasonable to see at least 50-100¢/cwt more in total value than the same herd in a single-buyer region. That’s $58,500 a year. Or roughly $195/cow — pushed or pulled entirely by how many processors are in range, not how well you bed stalls.

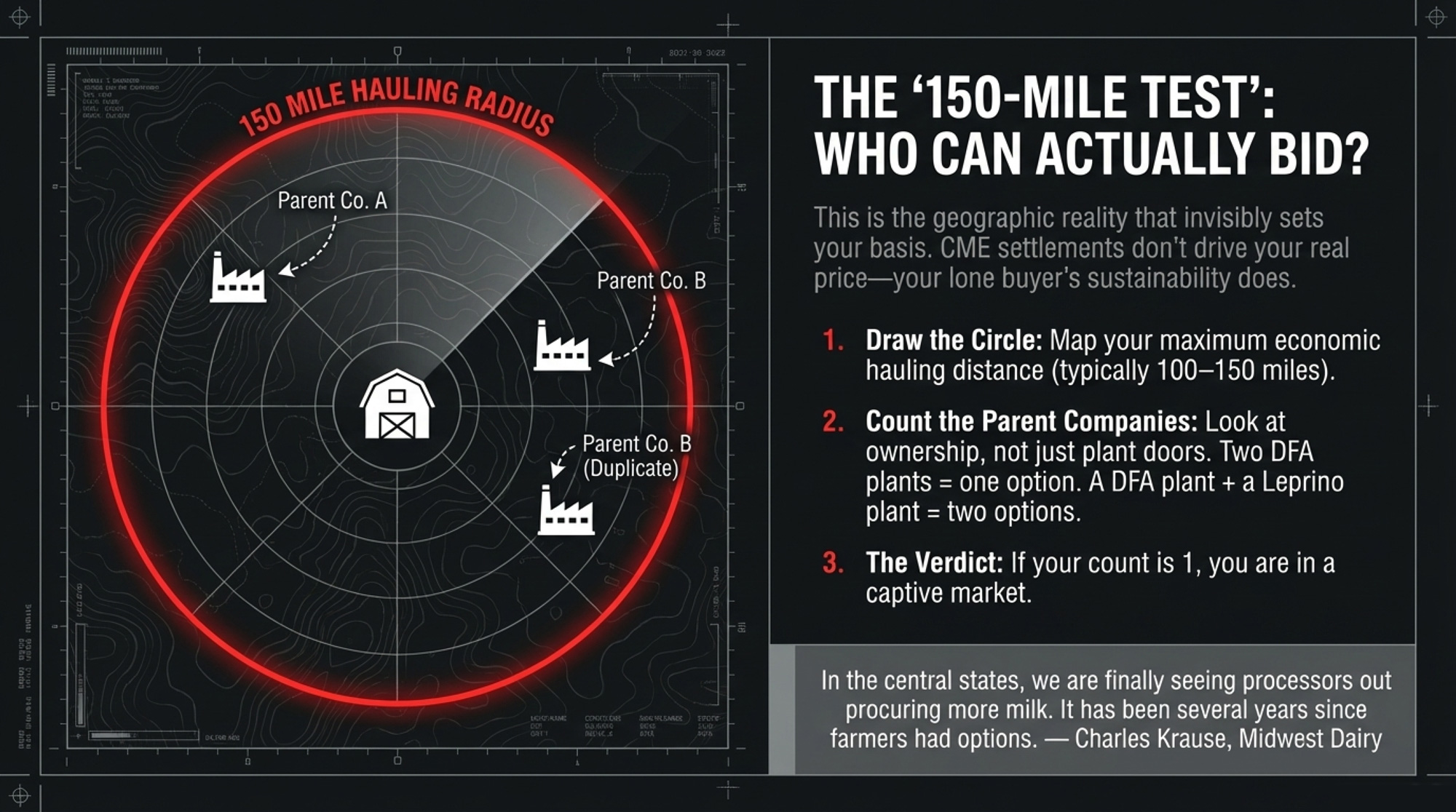

How Many Buyers Can Actually Bid on Your Milk Right Now?

This is the question that invisibly sets your basis.

Pull up a map. Draw a circle with your maximum economic hauling distance — for most outfits, that’s 100–150 miles, depending on roads and fuel. Count the plants inside that circle. Then ask the harder follow-up: how many of those plants are controlled by different companies?

Two DFA plants don’t equal two buyers. A DFA plant and a Leprino plant do.

If you count four or more independent buyers, you’re in rare air. Much of Wisconsin, eastern Minnesota, and chunks of Idaho’s Magic Valley still look like this — multiple co-ops, proprietary cheese plants, and specialty processors overlapping territories. Charles Krause, chair of Midwest Dairy’s board and a sixth-generation dairy producer running a 350-cow operation in Buffalo, Minnesota, told Progressive Dairy: “In the central states, we are finally seeing processors out procuring more milk. It has been several years since farmers had options.”

If the count is one, you’re in a captive market. CME settlements or national mailbox averages don’t drive your real price. It’s set by whatever your lone buyer decides is sustainable — for them.

Where Does the Money Go Before It Reaches Your Statement?

Two pieces of plumbing turn consolidation into smaller milk checks. Neither one shows up as a tidy line item.

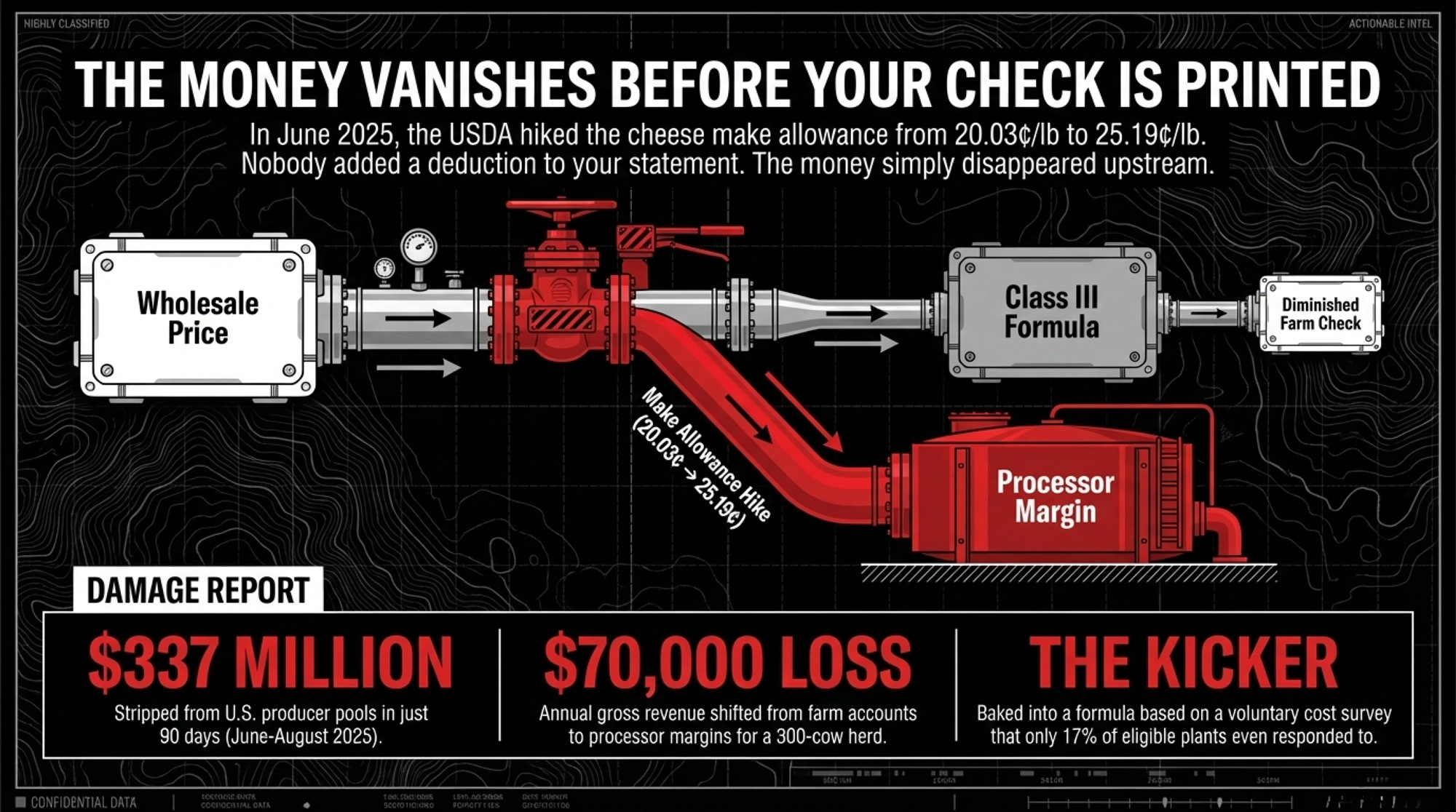

Make allowances move money upstream before your check is even printed.

When USDA raised the cheese make allowance to 25.19¢/lb in June 2025 — up from 20.03¢ where it had sat since 2008 — nobody added a “make allowance” deduction to your statement (USDA AMS, Final Decision on FMMO Amendments, 2025). The money vanishes earlier than that. USDA subtracts the allowance from the wholesale commodity price before calculating protein and butterfat values for Class III. The processor keeps the allowance as an operating margin. What’s left becomes your component price.

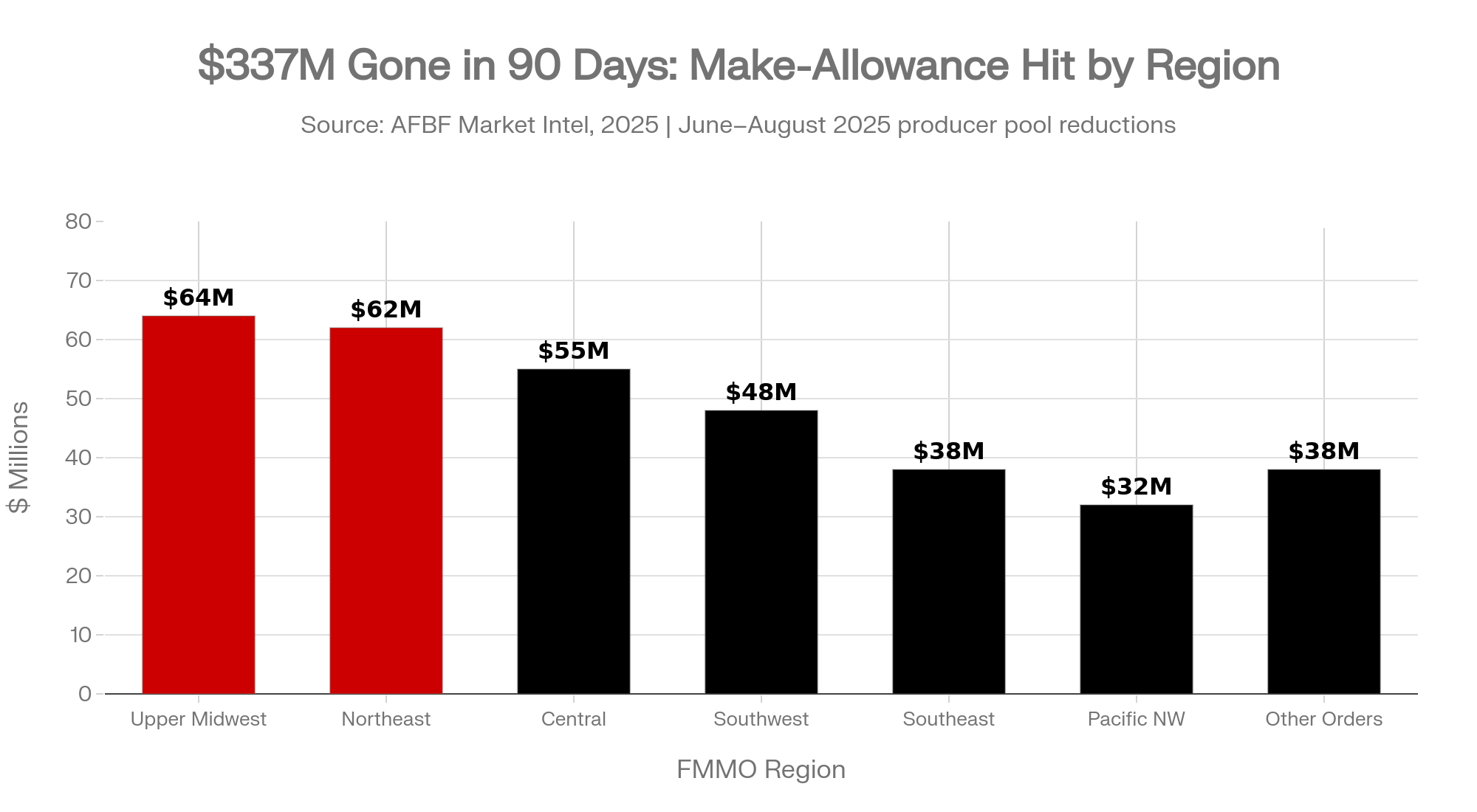

Danny Munch at AFBF did the math. The new make allowances stripped $337 million from producer pools in just 90 days — June through August 2025 (AFBF Market Intel, 2025). That included about $64 million from the Upper Midwest and $62 million from the Northeast. Class price reductions ranged from 85 to 93 cents per hundredweight. Terrain Ag’s analysis was blunt: “Increased make allowances will have the most clear-cut negative effect on component values and milk prices.”

Run that through the barn. A 300-cow herd shipping 78,000 cwt a year sees about $70,000 in annual gross revenue shift from farm accounts to processor margins because of a single rule change. You can’t negotiate it back in a premium. It’s baked into the formula — based on a voluntary cost survey that, according to the hearing record, only about 17% of eligible plants bothered to respond to.

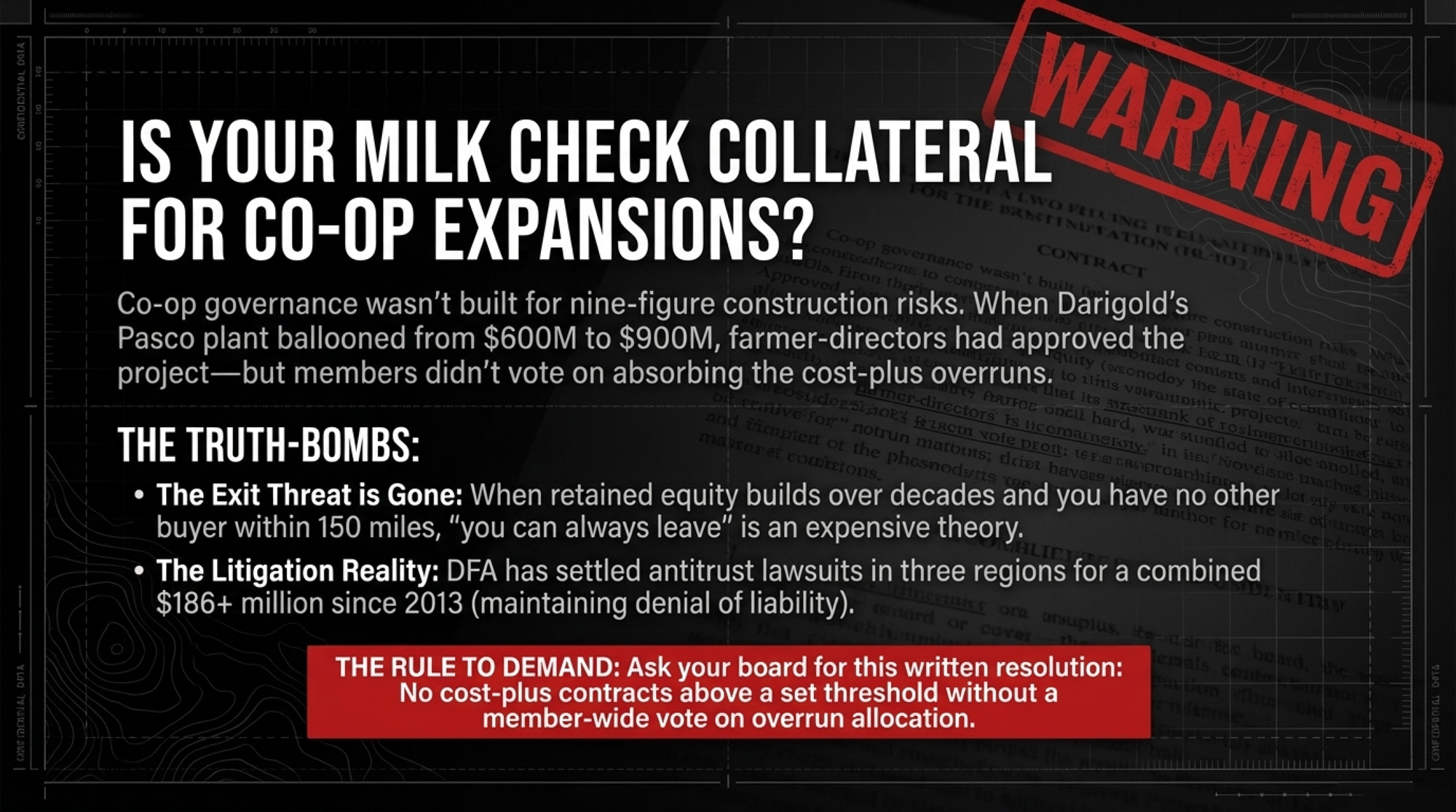

Co-op governance wasn’t built for nine-figure construction risks.

On paper, farmer-directors run cooperatives. Members often report that management holds significantly more information than individual directors — and in a complex construction project, that asymmetry can matter enormously. When Darigold says “farmer-owners approved the Pasco project,” that’s technically true. The board voted in 2021. But members did not vote on which contractors to use, whether the job was fixed-price or cost-plus, or who would absorb cost overruns. Those three decisions are exactly what turned a $600M project into a $900M one — and a $4/cwt deduction.

Co-op law gives you formal authority. Consolidation takes away your exit threat. When retained equity builds up over decades, notice periods stretch out, and there’s no other buyer within economic hauling distance, “you can always leave” becomes an expensive theory. That’s how Krista Stauffer ends up with equity sitting in a co-op she may never meaningfully cash out of.

The transparency metric worth demanding: Before your co-op board approves any capital project over $100 million, it’s worth asking in writing whether the construction contract is fixed-price or cost-plus — and what the member-approved cost cap is. If there’s no cap, your future milk checks are the cap. A simple resolution — “No cost-plus contracts above a set threshold without a member-wide vote on overrun allocation” — would have changed the math for DeRuyter and Stauffer.

And the pattern isn’t limited to the Pacific Northwest. DFA has settled antitrust lawsuits in three separate regions: $50 million in the Northeast, $140 million in the Southeast, and $34.4 million in the Southwest — a combined $186+ million since 2013 (court records; Cheese Reporter, multiple years). Settling litigation is standard practice and doesn’t constitute an admission of wrongdoing — DFA has made that point explicitly in each case, stating it “steadfastly denied liability and mounted a vigorous defense.” But somebody still wrote a check.

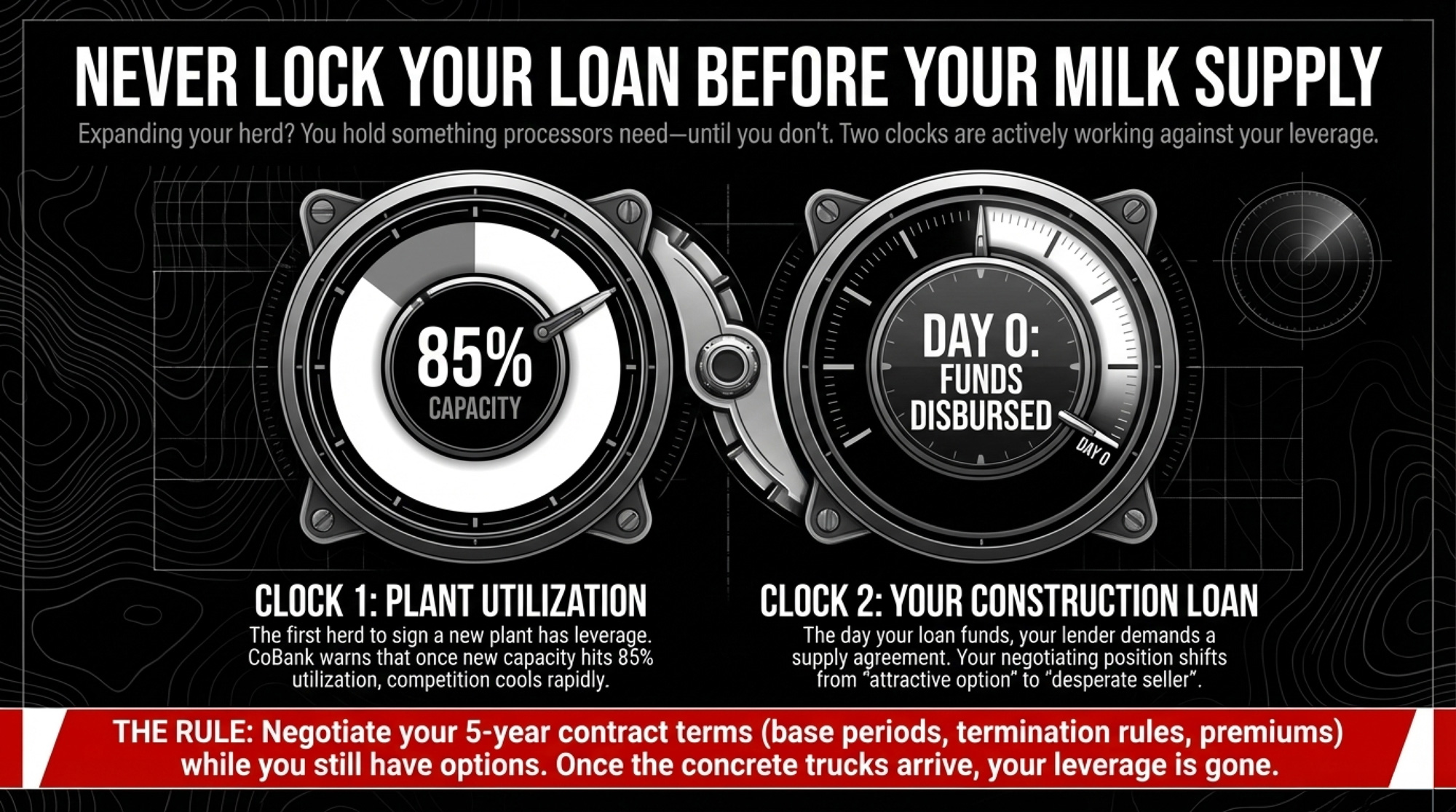

Should You Lock Your Supply Agreement Before or After Your Construction Loan?

Before. Always before.

A 300-cow dairy looking at 1,000 cows has something processors need: roughly 18 million pounds of additional annual supply. Right now, that’s the story around places like Leprino’s new Lubbock cheese plant in Texas, Hilmar’s Dodge City facility in Kansas, and Chobani’s Twin Falls expansion — which alone will need an additional 6 million pounds of milk per day once it’s fully running.

But two clocks are running against you.

Plant utilization. Once those new plants reach roughly 85% capacity, the tone changes. CoBank has warned that as new cheese capacity in the Southern Plains fills by around 2027, competition for milk will cool and product prices will come under pressure. The first herd to sign has more leverage than the last.

Your loan closing. The day your construction loan funds, your lender expects a signed supply agreement. At that point, your processor knows you must have a buyer. Your negotiating position shifts from “we’re one of several attractive options” to “we can’t close this loan without you.”

The contract you’ll live under for five years — base period, over-base penalties, premiums, termination rules — should be negotiated while both clocks are still in your favor. Not as a rushed afterthought once the concrete trucks have come and gone.

What You Can Actually Do About This

Here’s where the data stops and your decisions start. Not every move fits every operation, but each one has a clear trigger, a trade-off, and a timeline.

Next 30 Days: Map your processor options and take the map to your lender.

Set aside an afternoon. Pull a map and mark every plant within your realistic hauling radius: who owns it, what it makes, whether it’s expanding or shrinking. Count independent buyers, not just plant dots. If it’s one, that’s your biggest business risk — bigger than any single feed line. Lenders are starting to stress-test processor dependency alongside debt coverage, especially after 2025’s make-allowance shock and the Darigold overrun.

Walking into a loan review with a processor map signals that you understand your exposure. Suppose you’ve got two or three real options, which gives you room to negotiate. If you don’t, it justifies tighter risk management and more conservative debt.

The Lender Stress-Test Cheat Sheet

Bring these four questions to your next lender meeting:

- “How much of our debt coverage depends on over-order premiums that could vanish if our buyer consolidates or restructures?”

- “What is our Plan B if our primary plant issues a 12-month termination notice?”

- “Based on the 2025 make-allowance shifts, what is our new break-even cost per hundredweight?”

- “If our co-op levies a $2–4/cwt capital assessment — like Darigold did — for how many months can we service debt at that reduced pay price?”

Next 90 Days: If you’re expanding, lock your supply agreement before your construction loan closes.

Your leverage window is the 60–120-day period when new plants are still filling capacity, and you haven’t yet signed the building loan. Use it. Ask for a base period that moves with herd size, a clear over-base penalty cap, a symmetric termination notice, and a quality premium schedule fixed for at least 24–36 months. Farms that treat this like a formality end up signing whatever’s in front of them. Farms that treat it like a one-time leverage point can carve out terms that matter the next time prices roll over.

This Year: In single-buyer regions, treat DRP as a core defense.

If you can’t change your processor, you can still change your exposure. HighGround Dairy’s quarterly analysis shows DRP (Dairy Revenue Protection) covered about 32–33% of the U.S. milk supply in Q3–Q4 2024 (HighGround Dairy, 2024). In a competitive market, DRP is one more tool. In a captive market, it might be the only way to put a price floor under part of your check that doesn’t depend on your buyer’s goodwill. The key is to run DRP against your actual butterfat and protein, not a generic blend. A 20-minute meeting with a good agent can show you what 10–20% of protected revenue looks like compared to rolling the dice entirely on your local basis.

You gain a price floor, but you give up premium dollars and take on basis risk between the futures price and the DRP you cover. In a one-buyer region, that trade-off usually pencils. In a region with three competitive buyers already bidding up your premiums, it’s less clear-cut.

Ongoing: Push components that keep paying even when formulas shift.

Make allowances hit everyone, but high-component herds still come out ahead. Herds consistently above about 4.2% butterfat and 3.3% protein are seeing 50¢–$1.50/cwt in premiums that help offset structural hits they can’t control. That doesn’t fix consolidation. But your breeding and feeding decisions can either leave money on the table or claw some of it back.

Key Takeaways

- If your processor map shows only one independent buyer within 100–150 miles, treat that as your top business risk. Everything else in your plan should assume that the buyer controls your basis.

- If new deductions — hauling surcharges, co-op assessments, base-excess penalties — add up to more than $1/cwt compared to your 2023 statements, that’s a structural change, not a bad month. Revisit expansion plans and debt levels accordingly.

- If you’re expanding and your supply agreement is being negotiated after your construction loan closes, you’ve already given up your best leverage. Flip the order.

- If you’re in a single-buyer region and not using DRP on at least part of your volume, you’re carrying all the downside your buyer doesn’t want. Run the numbers on one or two coverage levels before your next quarterly enrollment.

- If your co-op can approve nine-figure plant projects without a member vote on cost-control terms, assume your future milk checks are potential collateral. Ask for fixed-price contract disclosure and a written cost cap before the next build — not after the overrun.

- If your 3-to-5-year plan only works at $22–23/cwt with healthy premiums, it’s not a plan. Model your numbers at $18–21/cwt with no over-order premiums and see if the pencils still sharpen.

Where does your farm sit on this leverage map — competitive, moderate, or captive? That’s not an abstract policy question. It’s whether your next expansion, your next loan renewal, and your next contract negotiation assume you have options or admit you don’t.

The make-allowance drag, the co-op capital calls, and the processor build-out aren’t going away. The real question is whether your numbers, contracts, and risk tools align with the reality of who can actually bid on your milk.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- GT Thompson’s 2026 Farm Bill Math: DMC Pays Your 200‑Cow Dairy $1800, Make Allowances Cut $42240 – a 23 to 1 Hit – Arm yourself with a 90-day financial survival roadmap to calculate your specific make-allowance exposure. This audit guide reveals how to leverage actual statement data to strengthen negotiations with lenders and co-op boards.

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Secure a long-term competitive advantage by mastering the “more milk, fewer farms” era. This strategic breakdown delivers essential margin-protection tactics, helping you choose a profitable path before market consolidation decides your future for you.

- The Robot Revolution: Transforming Organic Dairy Farms with Smart Tech in 2025 – Gain a disruptive edge by integrating robotic milking and AI-driven feeding systems into your operation. This analysis exposes how smart technology can reduce waste by 30%, driving efficiency gains that offset narrowing processor margins.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.