July milk per-cow jumped to 2,081 lb in the 24 big states—while corn’s pegged at a record 188.8 bpa. Margins? Tight… unless planned.

Executive Summary: Here’s the quick read over coffee. Milk output is running hot—per-cow hit 2,081 lb in July across the 24 major states—while butter’s been slipping on the board even though cold storage isn’t bloated. USDA’s August WASDE prints a record 188.8 bpa corn yield and a 16.7-billion-bu crop, which screams “cheap feed”… if it holds. But field scouts aren’t buying it—Pro Farmer’s final at 182.7 bpa points to disease shaving kernel weight, and that’s exactly the kind of shift that can add 20–40 cents/bu fast on a short-covering pop. Meanwhile, the butter spot around $2.235/lb and a firmer whey tone keep Class III steadier than Class IV—so checks tied to butter/powder feel more pressure. The big move right now isn’t fancy: lock about two‑thirds of feed through early 2026 while the curve is friendly, and set a reasonable floor on milk revenue—then lean into butterfat and protein to keep IOFC intact. Plants coming online in Dodge City and Lubbock will help basis, but not in time to save September spot loads—so plan hedges around the plant’s utilization, not a national average. The bottom line is to get coverage on the books while there’s room, and don’t wait for the market to force the hand.

Key Takeaways

Lock feed while it’s offered: with USDA at 188.8 bpa vs. Pro Farmer 182.7, pre‑commit ~66% of Q4’25–H1’26 rations; that cushions a 20–40c/bu corn jump that could hit IOFC $0.20–$0.40/cwt.

Use DRP as a true hedge tool: quote it in real time with an agent—the premium and coverage change daily with futures; set a floor that matches the plant’s utilization mix.

Aim components for ROI: pushing ~4.2% butterfat and ~3.3–3.4% true protein typically offsets Class IV weakness and stabilizes income-over-feed when whey props Class III.

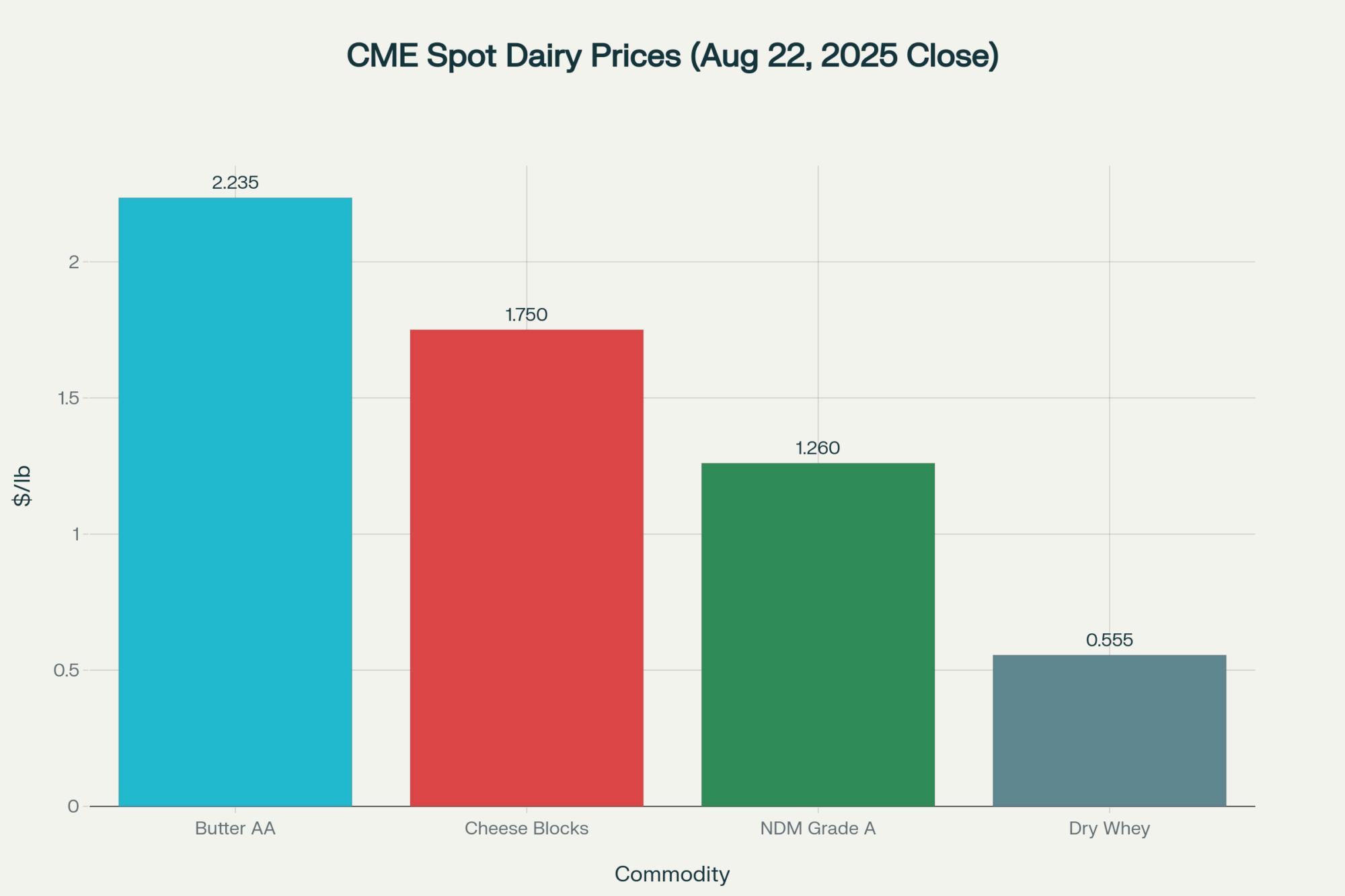

Watch butter vs. stocks: butter around $2.235/lb despite July stocks down ~6% YOY says the market’s pricing future cream; don’t overbuild inventory if processing.

Expect basis relief later, not now: Dodge City is online and Lubbock ramps in 2026—help is coming, but September milk still travels; hedge the haul and basis accordingly.

The U.S. dairy industry is heading for a collision. That isn’t hyperbole. July data shows milk production is running significantly higher year over year, while feed market risk is anything but settled, setting up a classic margin squeeze if timing goes the wrong way for producers selling milk daily and buying feed in chunks. USDA NASS Milk Production | USDA ERS LDP Outlook

More Than a Milk Price: Why Supply and Basis Are Driving Your Check

What’s striking this summer is a tricky mix for producers planning Q4 coverage and cash flow: stronger per‑cow output in key dairy states combined with unusually wide spreads in feed market signals that amplify basis and logistics risk on the ground. USDA Dairy Market News

Scope

Per‑cow (lb)

Notes

24 major states (July)

2,081

+36 lb YoY; higher output corridor

National (July)

2,063

Lower than 24‑state average

According to the USDA’s July Milk Production report, production per cow in the 24 major states averaged 2,081 pounds, up 36 pounds year over year; the national July average was 2,063 pounds, and that difference matters when estimating loads and component tons per month under tight plant schedules.

The growth corridors across the South‑Central and Plains keep adding milk and steel, but line time and trucking don’t appear out of thin air—when plants prioritize nearby milk, basis penalties can hit loads that have to move farther even if headline prices look fine. USDA Dairy Market News

Butter, Classes, and Why Inventory Isn’t the Whole Story

Butter told the market story in August as spot Grade AA settled around $2.2350 per pound on August 22, looking cheap versus global values but largely discounting what’s coming more than what’s currently in storage. CME butter prices

Cold Storage shows July butter stocks down about 6% year over year—tight enough today—yet prices softened anyway, signaling traders are pricing future cream flows and churn time rather than present availability. USDA Cold Storage – July 2025

This development has a fascinating effect on Class dynamics. When butter and powder soften while whey holds firm, Class III can look relatively better than Class IV. In certain months, this translates into weaker Producer Price Differentials (PPDs) in markets with a butter/powder‑heavy utilization mix. Class spreads and pricing context

Feed Risk: Why the USDA and Field Scouts Disagree on Your Corn Bill

According to the August WASDE, the first survey‑based national corn yield printed a record 188.8 bushels per acre with production at 16.7 billion bushels if realized—an undeniably feed‑friendly deck if it stands. DTN/Progressive Farmer summary

But the view from the field tells a different story: Pro Farmer’s final tour estimate pegs yield at 182.7 and flags widespread late‑season disease pressure across parts of the Belt, which is big enough to tighten carryout and nudge basis and futures higher into winter.

Positioning raises the stakes—CFTC data show managed money carrying sizable net shorts in corn ahead of harvest, the exact fuel that can power a fast short‑covering rally if the crop underperforms.

What to Do Now (Before the Market Makes the Choice for You)

Action

What to do now

Why it pays

Lock feed (~66% Q4–H1’26)

Pre‑commit while USDA’s high yield is priced

Cushions a 20–40c/bu corn pop; protects IOFC $0.20–$0.40/cwt

Price DRP in real time

Quote with an agent; align to plant utilization mix

Sets floor against Class IV softness, matches actual pooling

Push components (BF/TP)

Aim ~4.2% butterfat; ~3.3–3.4% true protein

Lifts pay price when cheese/whey support Class III

Based on market signals and risk calendars, producers should consider these three strategic actions now:

Lock In Feed Costs: Pre‑commit to roughly two‑thirds of feed needs for Q4 2025 and early 2026 while the forward curve still reflects the USDA’s high yield scenario, leaving room to average if field‑driven numbers prevail and basis firms. USDA WASDE

Evaluate Dairy Revenue Protection (DRP): Work with an agent to price DRP in real time—premiums and terms change daily with futures and endorsements, so it’s a tool to manage actively, not guess at. USDA RMA DRP policy

Maximize Component Pay: For component‑based pay, push butterfat toward 4.2% and true protein into the 3.3–3.4% range to lift IOFC even when class prices wobble—especially if feed conversion efficiency holds under current diets. Milk check and pooling dynamics

Capacity and Basis: Help Is on the Way, Just Not for September

Capacity growth is real but won’t solve September’s milk; it matters for anyone with spot loads and a long haul to a dryer or churn while plants juggle maintenance, staffing, and qualifications. USDA ERS LDP Outlook

Hilmar’s new Dodge City facility—an investment north of $600 million—anchors the emerging milk map from western Kansas into the Panhandle and should help rebalance line time and haul distance over the next 12–18 months.

Leprino’s Lubbock facility is staged toward early 2026 for a full ramp, so relief is coming, but not fast enough to erase basis pressure for milk still looking for a closer home this fall and winter.

Global Pull and Why U.S. Butterfat Still Matters

U.S. butterfat remained globally competitive in early 2025, and USDEC highlighted strong mid‑year export momentum that helped keep domestic butter stocks tighter even as milk rose—one reason current weakness is more about forward cream supplies than a freezer problem.

For operators reading the tea leaves, watch the spread between U.S. and EU/NZ butter values alongside Cold Storage—if the U.S. discount narrows as milk stays high, export pull can fade and leave more butterfat at home right into seasonal cream recovery. USDA ERS LDP Outlook

If exports hold, inventories won’t spike quickly; if they wobble, Class IV bears the brunt first, and it shows up in the milk check. Class IV and utilization context

Your Milk Check Explained: How Class Spreads and PPDs Impact Your Bottom Line

When whey resilience props up Class III while butter/powder softness drags Class IV, checks in cheese‑heavy utilization areas can look materially different than those tied more heavily to churns and dryers, and that matters for how DRP or options are layered over already‑contracted milk. Class spreads and pricing context

Weak Class IV tends to pull PPDs lower and reduce the final pay price in orders where Class IV utilization spikes, so re‑read the plant’s pay formula and align hedges with the utilization reality—not a national average that won’t match the load on the truck. Milk check and pooling dynamics

The cheapest penny is the one not lost to a mismatch between pooling math and hedges, especially in a fall when spreads can move faster than loads can be re‑routed. USDA Dairy Market News

Bottom Line: Before the Collision, Not After

If USDA’s big yield verifies, feed stays friendly and margin math gets breathing room, but if Pro Farmer is closer to right and disease pulled kernel weight, the short‑covering bid can meet softening milk and turn the screws on IOFC unless protections are already in place. USDA WASDE | Pro Farmer final

The smartest move is the one made before the market forces your hand—lock in feed and revenue floors while the opportunity exists, don’t wait for the market to dictate terms, and let new capacity in Dodge City and Lubbock ease basis and haul pressure as it ramps over the next few quarters. Hilmar Dodge City | Leprino Lubbock

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Maximizing Milk Components: The Key to Higher Milk Checks – This article provides tactical, in-the-barn strategies for ration balancing and herd management to achieve higher butterfat and protein, demonstrating how to translate market signals into feeding decisions that directly boost your income-over-feed-cost (IOFC).

Beyond the Bulk Tank: How Global Dairy Demand is Reshaping the US Market – Shifting focus to the broader economic landscape, this piece analyzes long-term consumer trends and export dynamics. It provides a strategic framework for understanding how international demand will impact future U.S. milk prices and processor investments.

From Theory to Reality: How Genomic Testing is Delivering ROI in Commercial Herds – This forward-looking piece reveals how top producers are using genomic data to build more resilient and efficient herds. It offers a practical look at leveraging this technology to increase profitability and navigate the market volatility discussed in the main article.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Where should you really be milking in 2025? Hint: It’s not where you think.

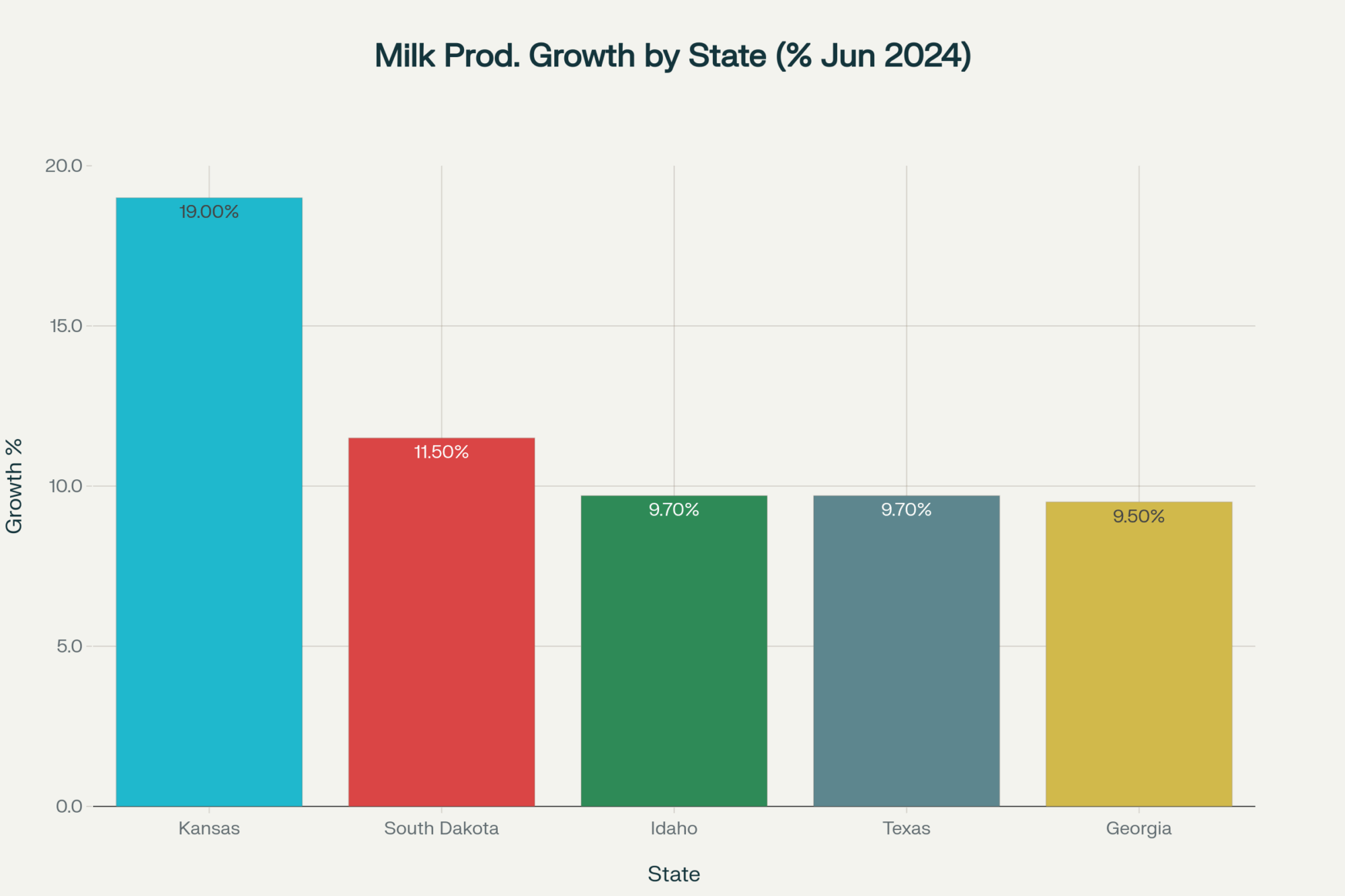

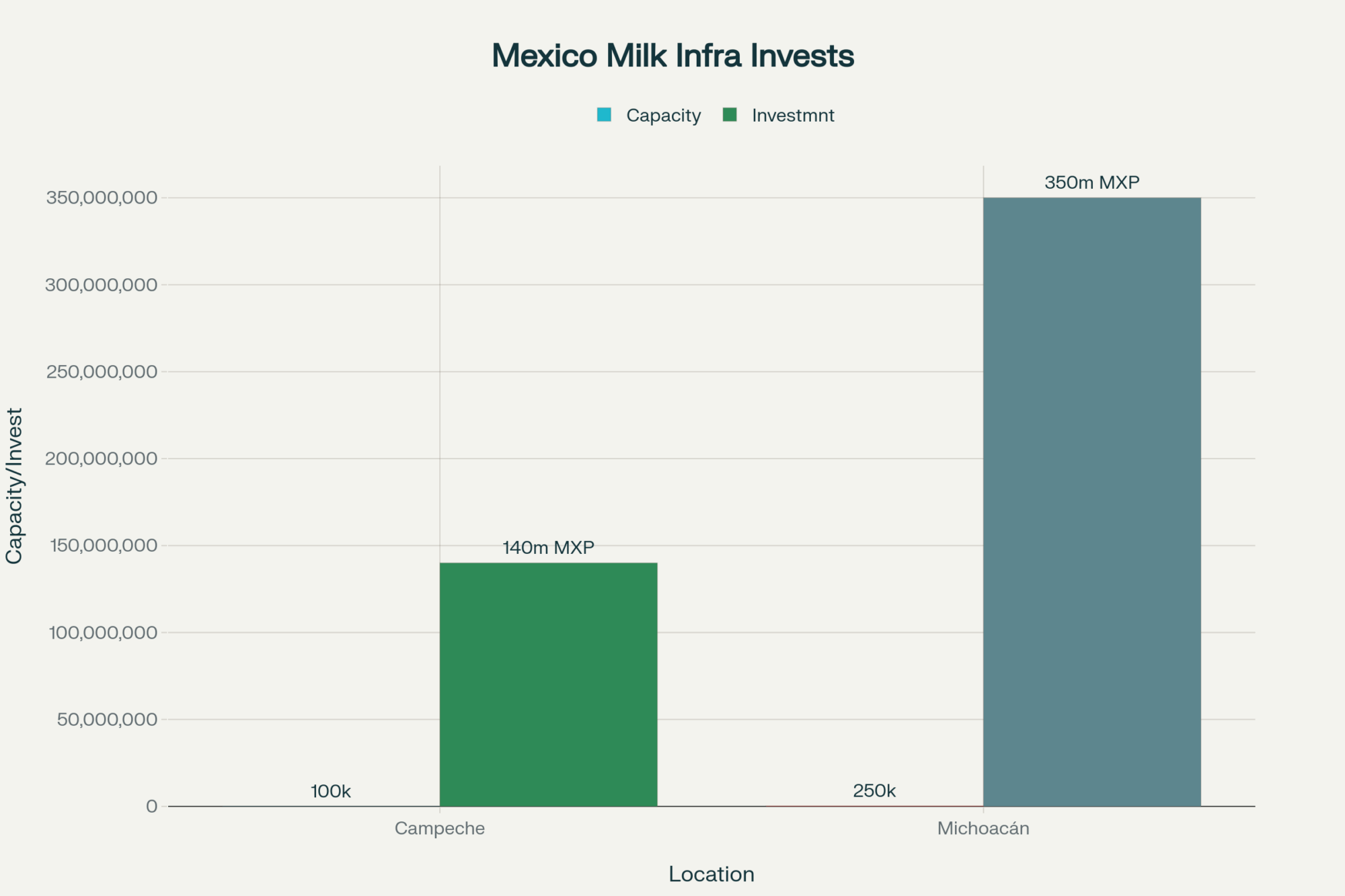

EXECUTIVE SUMMARY: Here’s the deal: dairy’s economic heart is shifting to the Plains, fast. Kansas milk production jumped 18.64%, South Dakota’s rose 10.64%, and the combined investment in processing has topped $2 billion since 2020. Those numbers aren’t just stats—they mean smaller hauling costs, stronger margins, and better feed efficiency according to Kansas State’s latest research. Meanwhile, Wisconsin lost over 300 farms, but milk production’s holding steady by consolidating on bigger, more efficient farms. Globally, efficiency and cost advantages drive production shifts—and the US Plains are no exception. If you’re considering where to grow or reinvest, it’s time to examine the economics, from water reliability to mailbox prices. This isn’t about tradition—it’s about profitability. You should be watching these trends closely and adapting now.

KEY TAKEAWAYS:

Kansas and South Dakota reported milk production gains of over 10% in 2025, driven by infrastructure investments. Producers should evaluate nearby processing plants to reduce hauling costs and boost margins in today’s volatile market.

Feed conversion improvements in new Plains dairies give a measurable cost advantage—start tracking feed efficiency with DairyComp and compare to regional benchmarks for better ROI.

California faces high regulatory costs (~$245/cow) but offsets some with digester and LCFS credits—producers should assess environmental programs’ ROI and explore similar revenue streams.

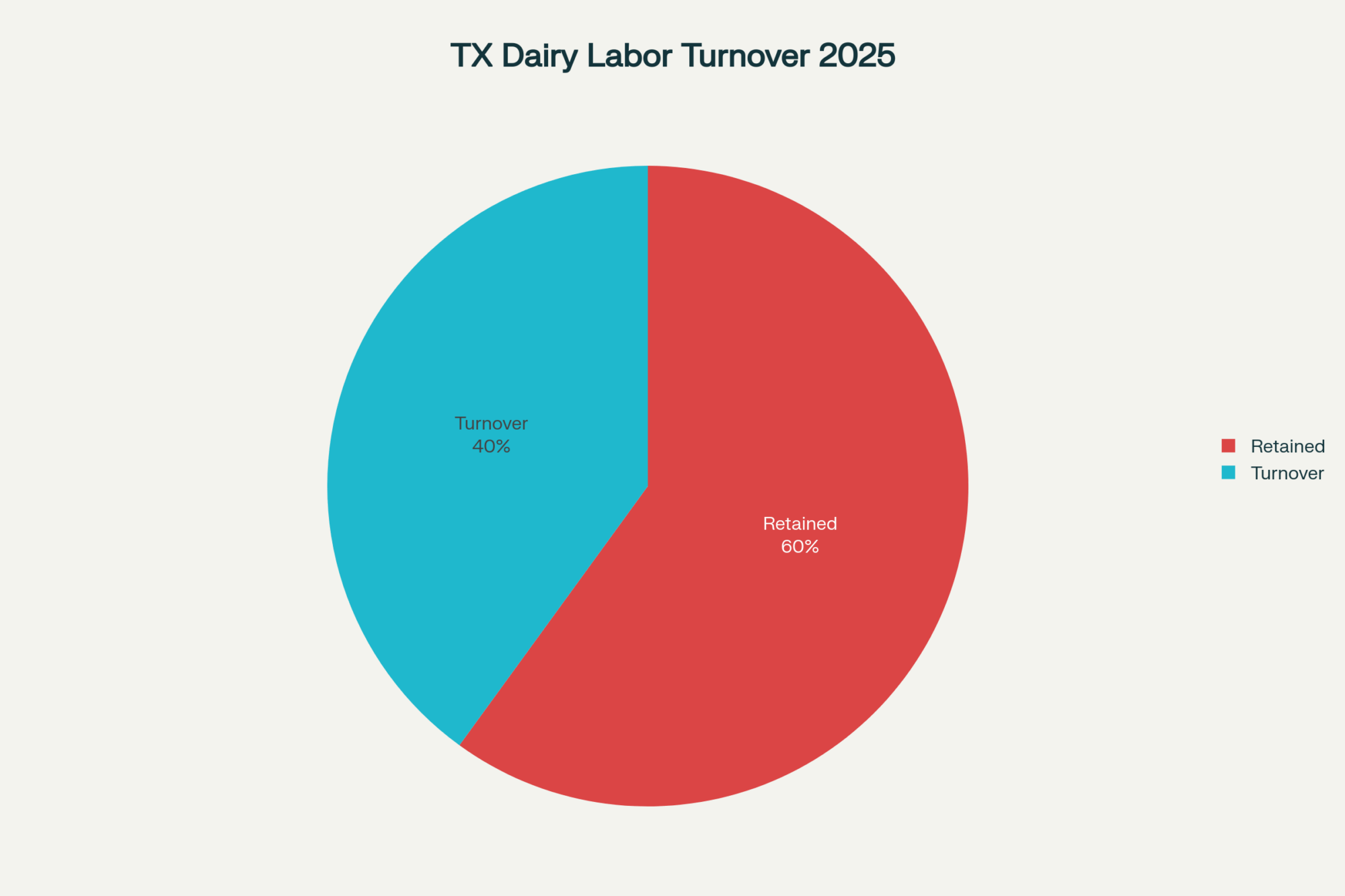

Labor turnover exceeds 40% in parts of Texas; implementing effective retention practices can help stabilize operations, reduce costs, and improve herd performance in the 2025 tight labor market.

Land values in key Plains expansion areas jumped 22%, so timing land purchases carefully and monitoring cropland prices are vital for strategic growth and profitability.

While traditional dairy states grapple with rising costs and regulatory pressures, a new economic reality takes hold in America’s heartland. According to August 2025 data from USDA-NASS, Kansas posted an 18.64% jump in milk production from the previous year, with South Dakota following at 10.64%. Since 2020, milk output has grown the fastest in Texas, South Dakota, and Kansas, while legacy states like Wisconsin and California have maintained their volume through consolidation, rather than by adding farms. The net effect is more milk being produced closer to new processing plants — and farther from some older ones.

The Data Driving the Shift

The numbers from Kansas are striking, with the state delivering an 18.64% increase in milk production from the previous year, followed closely by South Dakota at 10.64%. Texas continues to cement its position, producing 1.51 billion pounds in July while steadily expanding its herds.

What really stands out is how these newer Plains dairies are improving feed conversion. Agricultural economists at Kansas State University reported meaningful efficiency gains, meaning these farms get more milk from every pound of feed compared to older operations — a critical advantage when feed costs remain stubbornly high.

South Dakota’s growth is similarly well-founded. Herd numbers are up, and the state has seen substantial investment in infrastructure and feed supply, supporting sustained expansion.

Meanwhile, Wisconsin faced the closure of 313 dairy farms in 2024, highlighting the pressure on producers in traditional regions. However, production has remained resilient as dairy cows are consolidated on fewer, more efficient farms, helping maintain output and profitability.

California faces similar challenges — but with key advantages. California dairy producers benefit from proximity to major processors, higher milk solids, and revenue streams from digester-generated energy and Low Carbon Fuel Standard (LCFS) credits, which can offset some regulatory costs.

The Core Economics: Water, Labor, and Regulation

Water adds considerable complexity. Parts of the High Plains, particularly western Kansas and the Texas Panhandle, rely heavily on the Ogallala Aquifer, where water levels are declining rapidly. However, other regions, like eastern South Dakota and Nebraska, experience more stable groundwater supplies. For long-term investments, reliability and costs — including heat stress-related cooling — must factor heavily into planning.

California producers face strict water regulations, which drive up costs and incentivize innovative solutions. Regulatory costs are high, but partly offset by additional revenue from environmental credits and proximity to processing facilities.

Labor is another hurdle. Automation and efficient facility design help newer Plains dairies reduce labor per hundredweight of milk. Wisconsin and California are adapting—but the learning curves and capital needs remain significant.

Regulatory compliance costs in California are among the highest in the country — estimated at roughly $245 per cow annually, compared with $70 per cow in Plains regions. But environmental credits help some producers offset these expenses. Still, overall operational costs remain a significant factor in expansion decisions.

Where the Smart Money Is Flowing

Since 2020, investors have poured over $2 billion into dairy processing infrastructure across Kansas, Texas, and South Dakota, including expansions at the Hilmar Cheese plant in Kansas, Leprino Foods facilities in Texas and Colorado, and Valley Queen Cheese’s plant in South Dakota. These investments support and attract growing milk supplies in the region.

One 1,800-cow Plains dairy operator, speaking on the condition of anonymity, said, “The cost advantages out here allow us to reinvest and grow in ways that weren’t possible back East.”

Access to favorable financing tends to favor larger operations, though exact rates vary and are often proprietary.

Automation investments, such as milking systems, typically pay back in 18-24 months on average in these growth areas, driven by increased production and labor savings.

Proximity to processing plants is also a game-changer. The Plains benefit from facilities like Hilmar Cheese in Kansas, Leprino’s operations in Texas and Colorado, and Valley Queen in South Dakota. Herds delivering milk over shorter distances avoid the margin erosion caused by long-distance hauling.

Growth Pains: Risks to Watch

The National Weather Service highlights increasing weather variability in the Plains, posing risks to feed costs and cow comfort management.

Labor challenges persist, with turnover rates exceeding 40% at Texas dairies, according to the Texas Association of Dairymen.

Export demand appears promising, with the USDA projecting 4-6% growth for 2025; however, trade policies pose risks to maintaining this momentum.

Land prices are climbing rapidly. The Kansas City Fed reports a 22% increase in cropland values in Western Missouri over the past year, restricting the window for affordable expansion.

Disease outbreaks, animal movement restrictions, and gaps in insurance coverage for extreme weather add additional risk layers.

Why Scale Matters

Research by Cornell University confirms that dairies running more than 2,000 cows achieve significant economic advantages across geographies.

Your Strategic Takeaways

Monitor mailbox pricing and basis differences carefully, as these swings impact profitability more than volume changes. Track feed and forage costs, including sourcing silage and alfalfa locally versus transporting feed into expanding regions. Factor hauling distances and processing capacity availability into your cost analysis.

Consider potential impacts from upcoming federal milk marketing order reforms, which may alter class price relationships and influence regional payouts.

Test the sensitivity of your operation to 15% variations in feed costs, $1 modifications in milk prices, and additional cooling hours due to heat stress to refine strategic plans.

Look, I know change isn’t easy in this business. But the numbers don’t lie—and neither do your margins. Whether you’re considering expansion, exploring new technology, or simply trying to stay competitive, these shifts are happening whether we like it or not.

What do you think? Are you witnessing any of this unfold in your area?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

The Unseen Costs of Employee Turnover on Your Dairy – Our analysis flags the 40% turnover in Texas as a major risk. This article breaks down the hidden financial drain of that churn and provides practical strategies for improving employee retention to cut costs and stabilize your workforce.

Is Your Dairy Ready for the AI Revolution? – We’ve established efficiency as a key driver for growth. This piece explores the next frontier: artificial intelligence. It demonstrates how to leverage predictive analytics for superior herd health, reproductive performance, and enhanced profitability in a competitive future.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Milk prices held steadier than expected last week — but the underlying pressures are real. Here’s what smart producers are doing.

EXECUTIVE SUMMARY: Listen up — there’s some serious turbulence brewing in dairy markets right now. The Global Dairy Trade auction saw just a 0.3% price dip, but don’t let that fool you — U.S. cheese prices plummeted nearly 4% in one week, and China’s still pulling back hard from imports while Europe floods the market with surplus milk. Here’s what caught my attention… the producers who are thriving right now aren’t the ones with the most cows — they’re the ones milking smarter, not harder. We’re talking about farms that can break even at $17/cwt, while others are scrambling at $20. The difference? They’ve got their feed costs locked down, they’re culling strategically, and they’re using risk management tools that most farmers ignore. This isn’t just a rough patch — it’s a fundamental shift separating the wheat from the chaff.

KEY TAKEAWAYS:

Lock in your downside with Dairy Revenue Protection — it’s not just insurance, it’s profit protection when milk hits $16-17/cwt (and with current trends, that’s not fantasy anymore)

Feed strategy wins are real money — producers locking soybean meal contracts now are saving $30-50 per cow monthly compared to spot pricing

Strategic culling delivers 5-12% efficiency gains — removing the bottom 20% performers can boost your per-cow average by 200+ pounds monthly

Lender relationships matter more than ever — proactive communication about cash flow keeps credit lines open when markets get ugly (and they’re getting ugly)

Market intelligence pays — tracking Global Dairy Trade auctions and China’s import data gives you a 2-3 week advance warning on price moves that can make or break your quarter

We get it. You see those market signals, and it makes your stomach drop.

Let’s sit down with a coffee and unpack what’s really going on with the dairy market in 2025—and what you can do on your farm to face these times head-on.

The Numbers Don’t Lie — And They’re Talking

Here’s what the latest data tells us:

U.S. milk production in July 2025 hit 19.23 billion pounds, up 3.3% from last year, with nearly 9.47 million cows and average milk per cow climbing about 1.7% to over 2,000 pounds monthly. What’s particularly noteworthy is that producers across the Midwest are crediting better herd management and refined feeding programs with driving these gains.

Meanwhile, European producers aren’t sitting idle. EU milk production reached 160.8 million tonnes in 2023, marking steady growth driven by favorable weather conditions and lower feed costs.

Now here’s the kicker: China, our longtime dairy superconsumer, has pulled back hard. Multiple industry reports confirm that they’ve dramatically scaled back imports due to high inventories sitting in warehouses, as well as economic headwinds that aren’t expected to subside anytime soon.

Look at the Global Dairy Trade auction on August 19—prices declined just 0.3%, suggesting some market stabilization after months of volatility. To put that in perspective, Fonterra’s benchmark unsalted butter sold for $7,175 per tonne, while their key Whole Milk Powder product fetched $4,025 per tonne.

But closer to home? CME cheese prices tell a different story.

Block cheddar dropped from $1.83 to $1.76 per pound (a 3.8% decline), while barrel prices took a 5% hit over the week ending August 22. Meanwhile, the European Mild Cheddar index is holding firmer at €4,435 per tonne, showing some regional price differences. That’s your classic foodservice demand warning signal right there.

What You Need to Do Right Now

If you can’t break even with milk around $17/cwt, it’s time for a hard look at your cost structure. Here’s what smart producers are focusing on:

Get serious about risk management. Tools like Dairy Revenue Protection aren’t just government programs—they’re lifelines when markets get nasty.

Optimize your feed strategy. With grain markets looking somewhat friendlier than last year, this might be your chance to lock in favorable contracts, especially on soybean meal. But don’t get greedy—flexibility has value too.

Make tactical culling decisions. I know it’s painful, but removing your lower-performing cows earlier can save serious feed costs and help you right-size production for market realities.

Don’t ghost your lender. Keep that relationship strong. Share your numbers, explain your plan, and show them you’re thinking ahead.

The Big Picture — Supply, Demand, and Reality

Here’s what’s fascinating about this cycle:

Europe’s creating what everyone’s calling a “wall of milk,” with massive volumes getting processed into skim powder. The U.S. is steadier but still quietly adding volume through those productivity gains I mentioned.

Add in the Southern Hemisphere’s seasonal flush—New Zealand’s spring milk is just starting to ramp up—and you’ve got a supply picture that’s, frankly, overwhelming.

But demand? That’s where things get interesting.

China’s absence has left this massive hole that nobody else can fill. This is creating some interesting trade shifts. For example, with European products needing a home, recent shipments of EU butter to the U.S. surged by over 80%. At the same time, China has been taking advantage of lower tariffs to buy huge volumes of whey from the U.S., even while shunning milk powder.

Southeast Asia and the Middle East are buying, sure, but they’re opportunistic and price-sensitive. They’ll nibble at the edges, but they can’t absorb the surplus.

Technology in Tough Times

What strikes me is how many producers continue to invest in automation, despite tight margins.

Robotic milking systems are now operating on about 20% of Canadian farms, and I get why—better consistency, reduced labor headaches, more detailed cow monitoring.

But let’s be real: these aren’t magic bullets. Recent industry analysis indicates that while efficiency improvements can be substantial, success ultimately depends on how effectively you manage both the technology and your operations. In this market, you’d better have rock-solid numbers before making that kind of investment.

Eyes on the Horizon

Mark your calendars for a few key dates:

The next Global Dairy Trade auction, scheduled for September 2, will reveal whether the price stabilization holds. China’s August import data (due in mid-September) could be a real game-changer if it signals a resumption of buying. Europe’s production report in late September will tell us if their supply surge is finally moderating.

And here’s something most folks miss: keep an eye on the U.S. Restaurant Performance Index. It’s your early warning system for foodservice demand, which drives a huge chunk of cheese consumption.

Bottom Line — Tough Times, Tougher Farmers

This industry has weathered brutal cycles before, and this time will be no different.

The producers who stay sharp on their numbers, utilize available safety nets, and make tough decisions now will be the ones who emerge stronger. This downturn won’t last forever, but the choices you make today will define your operation tomorrow.

The bottom line? While everyone else is complaining about prices, savvy operators are positioning themselves to emerge from this downturn stronger than when they entered.

What strategies are working on your farm to weather this storm? Share your insights in the comments below.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Dairy Farming’s Brutal Reality: The Cold Hard Truth About the Cost of Production – This article provides a tactical masterclass in cost management. It reveals practical methods for analyzing your true cost of production, helping you identify immediate opportunities for efficiency gains that are crucial for profitability in a down market.

The ROI of Dairy Automation: Is It Worth the Investment? – This piece examines the real-world return on investment for the technologies mentioned in the main article. It demonstrates how to evaluate if automation is the right fit for your operation, ensuring your capital investments directly translate into measurable cost savings.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Trade barriers are dropping rapidly—and those who act now stand to gain significantly in the long run.

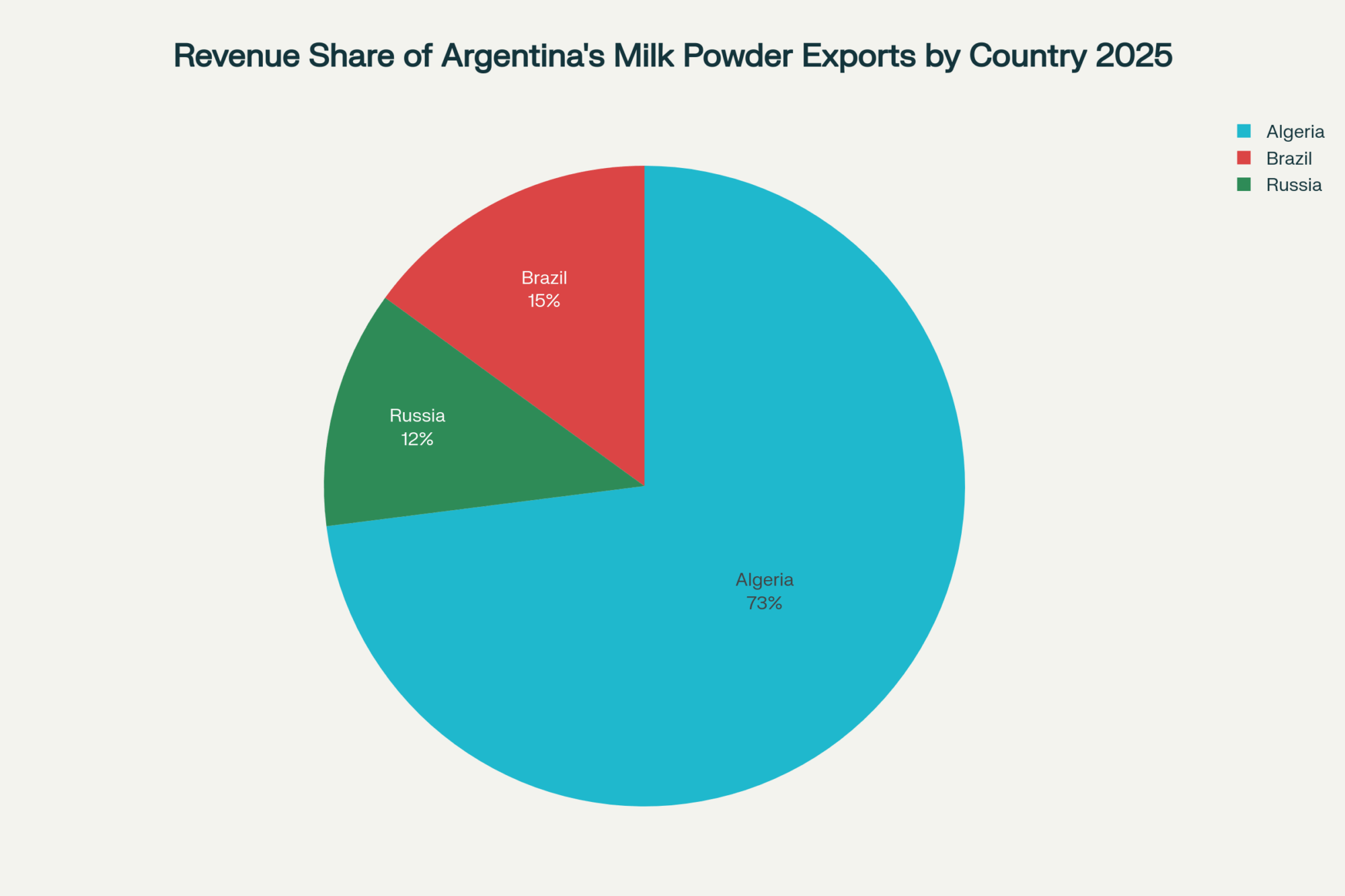

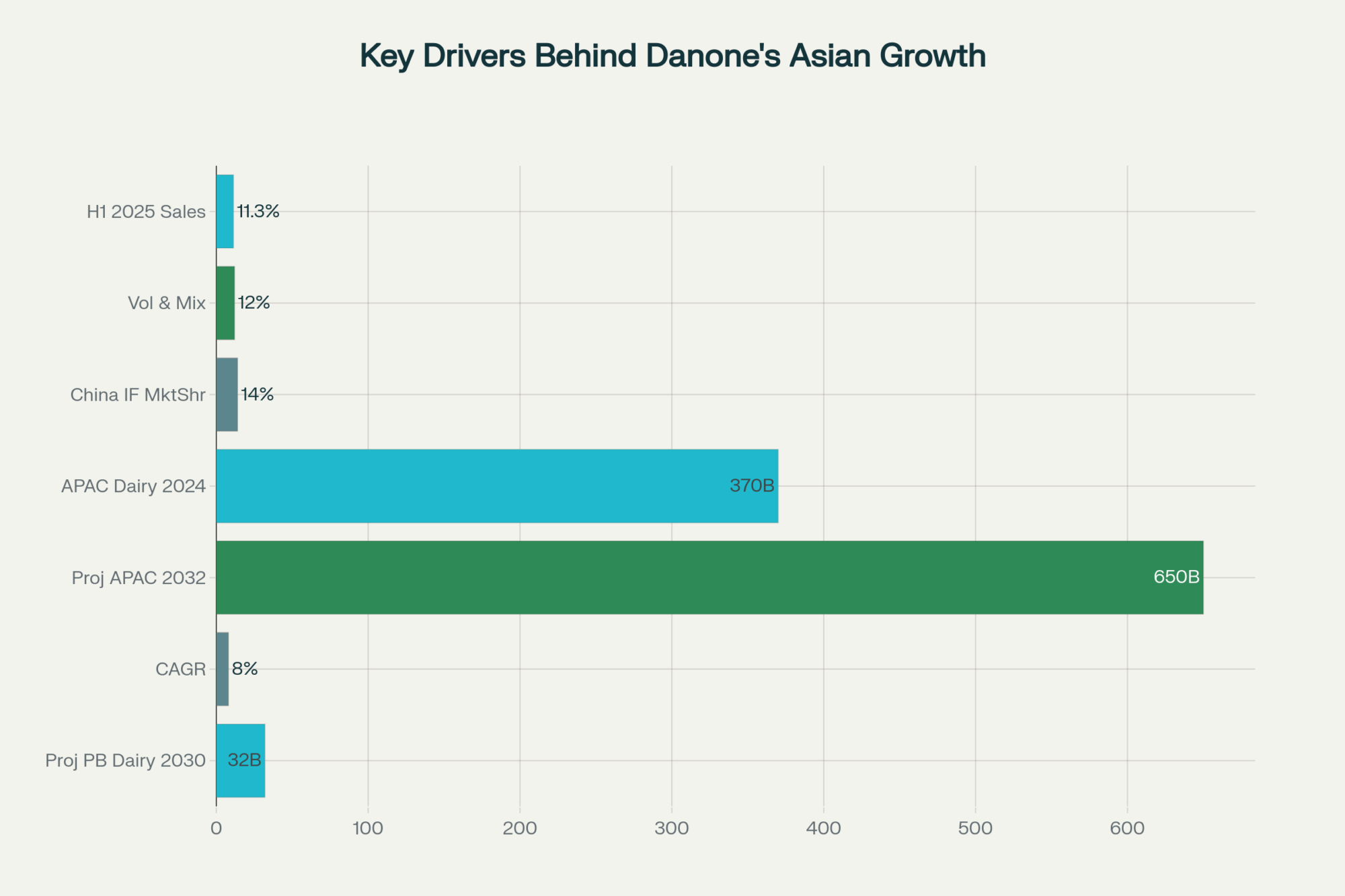

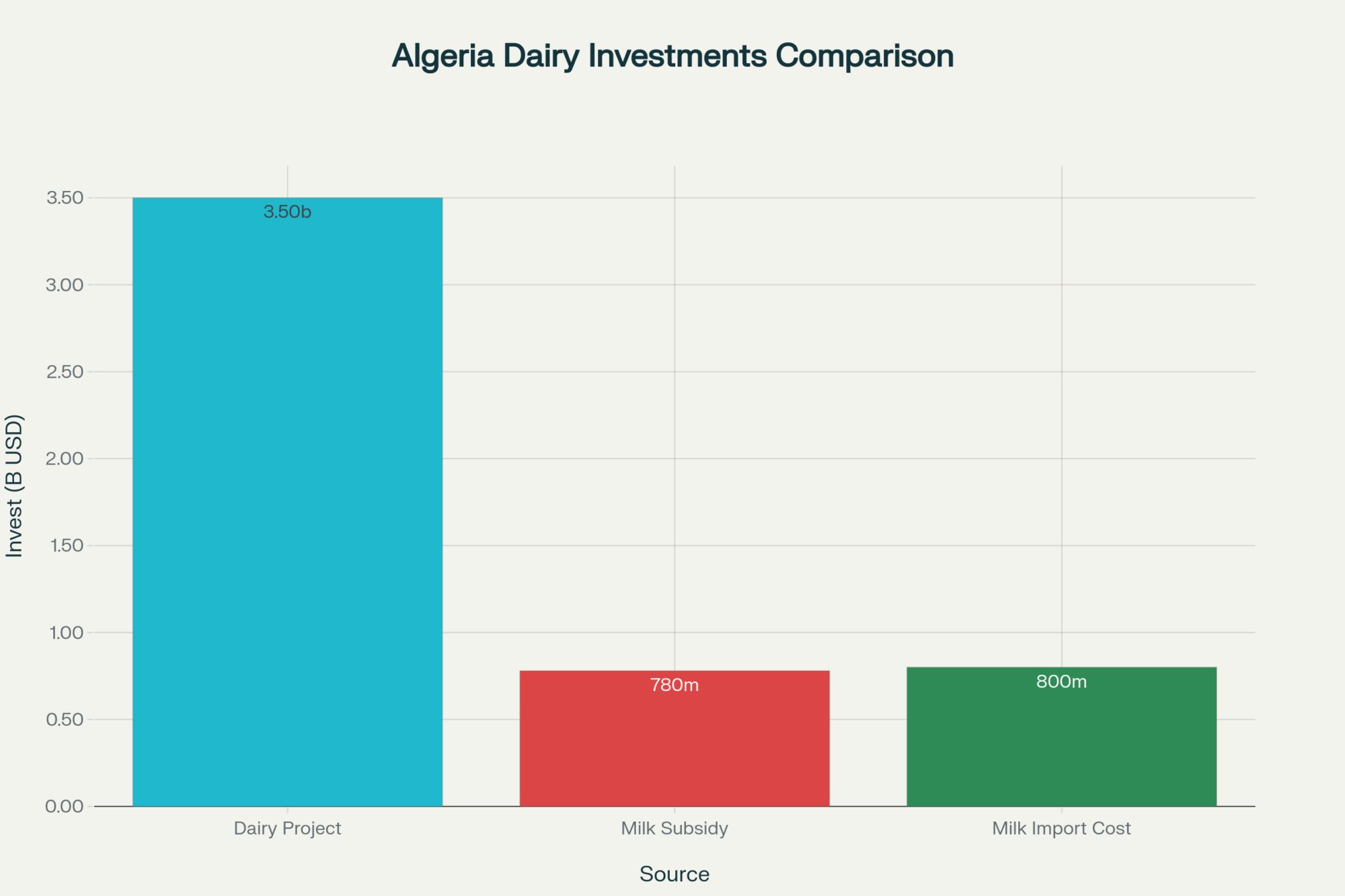

EXECUTIVE SUMMARY: I understand — with milk prices hovering around $17.30 and feed costs rising, thinking beyond your local market may seem like a luxury. However, what caught my attention is that Asia’s dairy market isn’t only growing, but also expanding rapidly, from $333 billion in 2024 to a projected $616 billion by 2033. We’re talking about consumers who’ll pay 50% premiums for quality products, especially in places like China, where the infant formula market alone saw a 4.2% increase in premium share from 32.8% to 37% in just one year. Sure, the entry costs aren’t pocket change — you’re looking at $ 300,000+ for compliance and cold chain setup, with a minimum of 2,000 cows required to make the math work. But those trade deals with Indonesia, Japan, and Korea? They’re opening doors that’ve been locked for decades. This isn’t about quick fixes — it’s about positioning your operation for the next decade while others are still figuring out domestic margins.

KEY TAKEAWAYS

Market premiums of $2.50-$4.00 per cwt are realistic within 3 years — focus on lactose-free products, high-protein whey, and specialty lines that Asian consumers actually want and will pay for

Minimum scale matters: 2,000 cows to absorb the $300K+ entry costs — but trade deals with Japan (80% tariff cuts) and Korea (16,000 tons tariff-free) make the investment worthwhile for serious players

Digital traceability isn’t optional anymore — 78% of Asian dairy companies have it — start building your systems now because it’s your ticket to premium pricing and market access

Currency swings can eat 8-12% of your margins overnight — hedge smart, keep domestic operations strong, and don’t bet the farm on export revenues until they’re proven

Timeline reality check: 12 months for compliance, 2-3 years to profitability — start your regulatory paperwork today because the window for first-mover advantage won’t stay open forever

Let’s talk about dairy margins. With Class III futures still around $17.32/cwt in July 2025 and feed pushing costs higher, many producers are knee-deep in short-term survival mode. Meanwhile, currency volatility and regulatory curveballs have shifted from being surprises to being central features of the export landscape.

However, what’s fascinating is that while we’re focused on domestic pressures, Asia’s dairy market is opening doors that could reshape your operation’s future. The U.S.-Indonesia deal, which eliminates tariffs on 99% of dairy exports, was signed this year, instantly changing marketplace dynamics. China’s recent approval of whey permeate imports signals another long-awaited shift.

From Bulk Buys to Premium Brands: How Asian Consumer Tastes Are Evolving

Asia’s dairy market was valued at $333.00 billion in 2024, with forecasts indicating a rise to $616.45 billion by 2033. That kind of growth demands serious consideration of how your operation fits into the picture.

Premium positioning is paying off. China’s premium infant formula segment expanded from a 32.8% to a 37% market share in 2024, with consumers paying 50% premiums for products backed by science and health claims. That premium trend is spilling into other dairy categories.

Southeast Asia offers the most explosive potential. Per capita dairy consumption sits at less than 20kg annually compared to 300kg in developed markets, according to industry data. Thailand alone achieved 11.5% export growth to $582.62 million in 2024, reflecting rapid market expansion.

Infrastructure and regulatory compliance carry eye-opening costs. Industry experts estimate that the annual cost for facility registration and certification processes ranges from $50,000 to $200,000. Cold chain logistics investments typically range from $500,000 in mature markets, such as Japan, to $2 million in markets where infrastructure requires development, like Vietnam.

Legal compliance and quality certifications add another $25,000 to $75,000, while partnership due diligence can cost up to $500,000. You’re looking at six-figure commitments before shipping your first gallon.

Currency fluctuations have already eroded export margins this year due to the strength of the USD against Asian currencies. Competitors fiercely defend their market share, meaning new entrants face considerable pricing and relationship pressures.

China’s dairy imports strengthened in April 2025, marking five consecutive months of year-on-year growth, with sweet whey powder imports up 30% year-to-date. The U.S. maintained its position as the primary supplier, accounting for 43% of China’s total imports of sweet whey powder.

The regulatory momentum is building, but timing matters.

Your Go-To-Market Timeline: From Paperwork to Profitability

You’ll generally need a 2,000-cow equivalent operation to handle export compliance and logistics costs effectively. China’s projected increases in dairy imports, particularly whole milk powder, create specific opportunities where the U.S. already holds established market positions.

Industry data indicate that successful operators typically achieve premiums of $2.50-$4.00 per hundredweight over domestic pricing within 24-36 months—but this requires sustained marketing investment averaging $150,000-$300,000 annually for brand development and regulatory maintenance.

Real talk: export ventures are fraught with risk. Currency swings bite margins, competitors push back hard, and partnerships can fracture unexpectedly. The best strategy? Maintain strong domestic operations while young export markets mature.

Compliance and market development typically require a minimum of 12 months, with brand and distribution establishment demanding another 1-3 years. Expect full profitability in 3-5 years, though some operators achieve positive cash flow by years 2-3.

Focus on market-relevant products: lactose-free items aligned with regional preferences, high-protein whey concentrates where U.S. technology excels, premium products that leverage the North American quality reputation, and strategic joint ventures rather than commodity exports.

The takeaway is clear: engage now or risk being locked out of the market.

Bottom Line: Your Herd’s Strategic Decision Point

Producers positioning themselves for leadership in Asia’s dairy markets by 2030 are investing today—in both infrastructure and partnerships. This isn’t about chasing spot commodity prices when U.S. demand softens; it’s about building durable market share where growth is real.

With domestic milk prices steady near $17.32/cwt amid rising feed costs, diversifying through Asia plays both an offensive and defensive role in margin management. The barriers to market access are falling, but the window to act is closing quickly.

Action Plan for the Ready:

Phase 0 (Right Now): Evaluate your finances rigorously with the help of your advisors. Can your operation withstand a 2-3 year wait for returns? If not, scaling export efforts may need to wait.

Phase 1 (Next 6 Months): Launch comprehensive regulatory registrations and certifications—FDA facility registration, HACCP compliance, and relevant export documentation.

Phase 2 (6-18 Months): Attend trade shows, meet distribution partners in target countries, and immerse yourself in evolving consumer trends.

Phase 3 (Years 2-3): Implement traceability and quality control systems aligned to Asian import standards. Test your brand with trusted local partners.

Those ready to move early will build lasting market power. Those waiting may miss the opportunity entirely.

This strategy isn’t a quick fix for a volatile U.S. market; it’s a long-haul, capital-intensive investment in your herd’s future. The regulatory doors are now opening, but they require both vision and courage to walk through.

So, what’s your move?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Breeding for a Balanced Herd: The Unsung Value of Components – This article provides practical genetic strategies for increasing milk fat and protein. It reveals how to breed for the high-value components that are essential for creating the premium export products Asian markets are demanding, directly impacting your potential margins.

The Dairy Industry’s Crossroads: Navigating the Top 5 Economic Headwinds of 2025 – While the main article focuses on the “pull” of Asian markets, this piece details the “push” from domestic pressures. It offers a strategic analysis of market volatility, helping you frame an export strategy as a crucial long-term risk management tool.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

US dairy exporters only fill 42% of the Canadian quota—that’s leaving millions on the table while you’re fighting for every cent.

EXECUTIVE SUMMARY: Listen, Canada’s “unbreakable” dairy fortress is showing serious cracks — and smart producers are already positioning for what’s coming. We’re talking about a system where US exporters can’t even fill 42% of their allocated quota because Canada hands the keys to their own processors. Meanwhile, Canadian farmers are paying around $41,500 per cow just for quota rights — that’s working capital that could be improving operations instead. With feed costs potentially spiking 8-15% from China’s canola mess and Class III hovering at $18.80/cwt, margins are tighter than ever. The 2026 USMCA review isn’t some distant policy debate — it’s a business reality that’ll reshape how we all operate. If you’re not hedging feed costs and building cross-border relationships now, you’re missing a significant opportunity.

KEY TAKEAWAYS

Lock in your feed costs today — CME futures can protect against that 8-15% protein spike; cover at least 50% of your next six months’ needs for around $50-100 per contract

Audit your cost structure now — with milk at $18.80/cwt, every efficiency gain matters; benchmark against your region’s top performers using extension data

Get border-ready with HACCP certification — takes 90-120 days and $3,000-5,000, but positions you for expanded market access when quotas open up

Start processor conversations — relationships built today could be worth millions when trade barriers fall, especially critical for operations within 200 miles of the border

Watch that 65% quota threshold — when US utilization hits this level, it signals real market shifts and your window to capitalize

The Canadian supply management system—that seemingly unshakeable foundation of the Canadian dairy sector—is facing coordinated pressure unlike any we’ve seen before. Between Trump’s August tariff escalation, New Zealand’s legal victory, and China’s retaliatory action against canola, the 2026 USMCA review is shaping up to be a pivotal moment for every dairy operation in North America.

What strikes me about this moment is how synchronized it’s all become. We’re no longer looking at isolated trade spats; this is systematic pressure that’s already changing how astute producers think about their operations.

The real bottleneck isn’t tariffs—it’s the quota game. Canada predominantly hands import licenses to its own processors rather than to American exporters. According to 2024 year-end data from the USDA’s Foreign Agricultural Service, US dairy exporters are using only about 42% of their allocated quotas.

I was speaking with a Wisconsin cheese producer last week, who summed it up perfectly: “They give us permission to knock on the door, then they give the key to our competition.”

The Kiwi Playbook That’s Got Everyone’s Attention

New Zealand’s approach has been brilliant. Instead of fighting tariff battles, they challenged Canada’s administrative processes under CPTPP and won. The result? $157 million annually in additional dairy access by forcing changes to how quotas actually work.

This isn’t just a New Zealand story—US trade lawyers are studying every detail of their strategy for the 2026 review.

Why China’s Canola Move Hits Your Feed Bill

China’s 75.8% tariff on Canadian canola has effectively eliminated a $5 billion export market. Canadian farmers are scrambling to reallocate acres, while US soybean producers are positioned to capture displaced Chinese demand.

Here’s where it gets interesting for dairy operations… According to a recent analysis from Iowa State University agricultural economists, these types of oilseed disruptions typically increase protein feed costs by 8-15% within six months. A feed supplier I know in Iowa mentioned they’re already adjusting September contracts—protein meal prices are creeping up as the supply picture tightens.

With Class III milk prices averaging $18.80 per cwt, that’s margin pressure we can’t ignore.

What the Numbers Tell Us

Here’s some perspective on what we’re dealing with: Based on recent industry data, quota values in key Canadian provinces now average around $41,500 per cow equivalent—that’s a massive amount of working capital tied up solely for the right to produce milk. Compare that to the flexibility US producers have to respond to market signals.

The political math is shifting as well. Canada has roughly 9,000 dairy farmers, representing less than 0.5% of its workforce, who defend this system against pressure from its three largest trading partners.

The Canadian Counter-Move

While US producers focus on hedging and export positioning, Canadian producers are taking different strategic approaches. Forward-thinking Canadian operations are focusing relentlessly on operational efficiency, benchmarking against top provincial performers to stay competitive amid growing pressure.

Many are exploring value-added routes—think organic, A2, or grass-fed—that leverage supply management’s stability for brand development. The predictable pricing structure becomes a platform to build premium market positions that aren’t easily disrupted by trade disputes.

Engagement with provincial boards and the Dairy Farmers of Canada is intensifying, pushing for a modernization narrative that strikes a balance between protection and evolution. Getting involved with policy discussions isn’t optional anymore—producers need to be part of shaping what comes next, not just defending what exists.

What Proactive Producers Are Doing

While policy will unfold over the next 18 months, savvy producers on both sides of the border are taking targeted steps to mitigate risk and prepare for opportunities. Here’s the playbook they’re using:

This month (For All Producers): Lock in feed costs for the next six months using CME futures. Even covering 30-50% of your protein needs gives you protection against these supply disruptions. Contract costs run $50-100, but that beats getting blindsided by a 15% feed spike.

Next 90 days (For U.S. Border-State Producers): If you’re within 200 miles of the Canadian border, get your HACCP certification current. The process takes 90-120 days and costs around $3,000-$ 5,000, but it positions you for opportunities when access becomes available.

Strategic positioning (For All Producers): Start conversations with processors on both sides of the border. A dairy operation near the Quebec border told me they’re already exploring partnerships with Canadian co-ops. When rules change, relationships matter more than paperwork.

Risk Management (For US Producers): The USDA Market Access Program provides up to 50% cost-sharing for export development, offering good financing for positioning investments.

Ongoing (For Canadian Producers): Focus on operational efficiency, benchmarking production costs against top provincial performers to maintain competitiveness as external pressures mount.

Exploration (For Canadian Producers): Pursue value-added niches such as organic, A2, or grass-fed products that leverage supply management’s stability for premium positioning.

Advocacy (For Canadian Producers): Engage with provincial boards and Dairy Farmers of Canada to support modernization efforts that preserve farmer viability while reducing trade friction.

What to Watch For

Industry analysts are tracking three key signals: quota utilization rates climbing above 65% (we are currently at 42%), Canadian industry messaging shifting from “protection” to “modernization” language, and protein meal basis levels widening in your region.

Research from the University of Guelph suggests that even partial Canadian market opening could generate hundreds of millions annually in additional US dairy exports, supporting domestic milk prices through expanded demand.

The 2026 Moment We’re All Preparing For

The USMCA review next summer represents the biggest structural opportunity for North American dairy integration since NAFTA. US dairy organizations are systematically building their case, with New Zealand’s victory providing both precedent and tactical guidance.

Keeping Perspective

Canada’s supply management system has provided real benefits—income stability, supply predictability, and rural economic support that shouldn’t be dismissed. The challenge isn’t destroying what works for Canadian farmers, but finding evolution that reduces trade friction while preserving viability.

The pressure we’re seeing suggests change is coming, but how it unfolds depends on finding solutions that work for everyone.

The Bottom Line Strategy

Immediate (All Producers): Hedge feed costs through futures contracts to manage price volatility from supply chain disruptions

Short-term (All Producers): Audit production efficiency against regional benchmarks and update relevant certifications

Near-term (Border-Area Producers): Build cross-border relationships with processors and distributors for partnership opportunities

Long-term (All Producers): Monitor quarterly TRQ reports and policy signals while developing financial flexibility for rapid opportunity capture

The Canadian fortress isn’t falling overnight, but the foundation is definitely shifting. Producers who prepare strategically now—through operational excellence, risk management, and relationship building—will be positioned to benefit when market access expands.

In this business, being ready beats being right. The 2026 review is coming, whether we’re prepared or not.

The bottom line? This isn’t about politics — it’s about your farm’s future profitability. The producers preparing now will be the ones cashing in when the walls come down.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

The 7 Key Performance Indicators Every Dairy Farmer Should Be Tracking – This article provides a tactical guide to benchmarking your herd’s performance. It reveals the essential metrics you need to monitor for improving operational efficiency, controlling costs, and making data-driven decisions to boost your bottom line.

A2 Milk: Is it the answer for the dairy industry? – Explore the strategic market potential of value-added dairy. This piece examines the A2 milk trend, offering insights into changing consumer preferences and helping you evaluate whether niche markets could build a more resilient revenue stream for your operation.

Dairy Genetics 101: A Producer’s Guide to Profitable Breeding – A forward-looking guide on how to leverage genetics as a competitive advantage. It breaks down how strategic breeding decisions can drive long-term profitability by creating a more efficient, healthy, and productive herd ready for future market demands.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

China’s dairy dropped 2.8%—but they doubled down on efficiency over volume. Game changer.

EXECUTIVE SUMMARY: Here’s what’s happening: China’s milk production hit 40.8 million tonnes in 2024, down 2.8% from last year, but don’t let that fool you. They’ve systematically shifted from chasing volume to maximizing efficiency per cow—we’re talking 9,600 kg annually on average, with elite operations pushing 12+ tonnes. That’s putting them toe-to-toe with Wisconsin and New Zealand’s best. Their self-sufficiency jumped from 70% to 85% in four years while imports surged 16% in February alone, but here’s the kicker—they’re buying premium cheese and whey, not commodity powder. Feed conversion ratios are now reaching 1.4:1, compared to traditional systems at 1.8:1, which translates to real cost savings of approximately $340 per cow annually, based on current feed prices. New Zealand’s cashing in big with duty-free access, while U.S. exporters are getting hammered by tariffs. Bottom line? If you’re not tracking feed efficiency, product differentiation, and shifting buyer preferences, you’re leaving serious money on the table.

KEY TAKEAWAYS:

Benchmark your feed conversion ratio immediately—Chinese mega-dairies are hitting 1.4:1, saving roughly $340 per cow annually on feed costs compared to traditional 1.8:1 ratios

Pivot to premium product positioning now—buyers are abandoning commodity powder for cheese, whey proteins, and specialty ingredients that command higher margins

Track Chinese import data monthly through GACC reports—early indicators of product category shifts can help you adjust marketing strategy before pricing impacts hit

Evaluate financing options with agricultural lending rates—China’s effective 3% rates are driving their technology investments, so secure competitive financing for your own efficiency upgrades

Focus on supply chain transparency and traceability systems—Chinese buyers increasingly demand full documentation, creating competitive advantages for operations that can deliver verified quality

The Chinese dairy market is changing—not in the dramatic way headlines suggest, but through calculated moves that savvy producers and exporters need to understand.

The Production Reality

Let me start with what we actually know. According to the Chinese Ministry of Agriculture’s latest sector report, China’s raw milk production reached 40.8 million tonnes in 2024. That represents a modest 2.8% decline from 2023—the first drop since 2018.

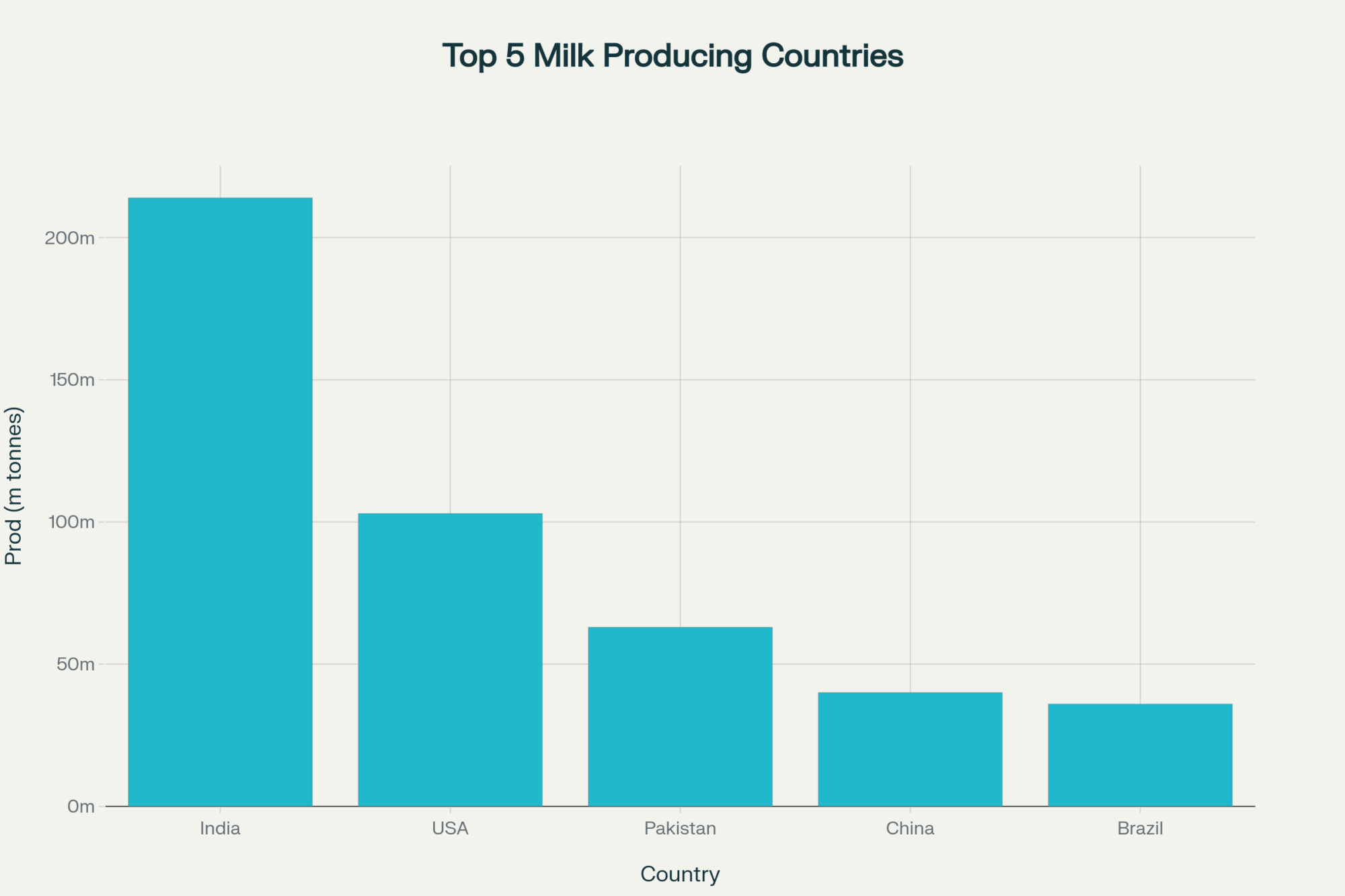

But here’s what that number doesn’t tell you. Chinese farms have been systematically culling less productive animals while increasing per-cow yields. We’re seeing average production climb toward 9,600 kg per cow annually, with top operations reaching 12 tonnes or more per cow per year. That puts their elite herds right alongside what we’re seeing in Wisconsin’s best farms or Canterbury’s most efficient operations.

The bigger shift? China’s dairy self-sufficiency has increased from around 70% to approximately 85% over the past four years, according to official agricultural policy documents. They’re producing less milk overall but depending less on imports—that’s strategic, not accidental.

What’s particularly striking is how they’ve approached this transition. Instead of the boom-bust cycles we’ve seen in other markets, Chinese policymakers have implemented what amounts to controlled market rebalancing. Feed conversion improvements are real—operations are reporting ratios approaching 1.4:1 compared to 1.8:1 for traditional systems, according to recent dairy efficiency research.

Import Patterns Are Shifting

Now, here’s where it gets interesting for those of us watching export markets. China’s General Administration of Customs reported dairy imports rose in early 2025 compared to the previous year. But they’re not buying the same products.

The shift is away from commodity milk powder toward specialty items, such as cheese, whey proteins, and functional ingredients. Think premium rather than volume. New Zealand is significantly benefiting from its duty-free access arrangements, while U.S. exporters face substantial tariffs that have effectively closed major market segments.

Recent trade analysis indicates that sweet whey powder imports have reached 237,000 tonnes year-to-date in 2025, a 30% increase year-over-year. The driver? China’s recovering swine sector needs high-quality protein sources. The U.S. maintained 43% market share, followed by the EU at 30%.

“We’re seeing Chinese buyers bypass traditional tenders for long-term partnerships focused on quality and traceability,” notes Michael Harvey, a trade analyst at Rabobank. “The message is clear: if you’re competing on price alone, you’ve already lost.”

What’s driving this product mix evolution? Chinese consumers are willing to pay premiums for quality, traceability, and health benefits. The days of competing purely on price are ending—something every exporter needs to understand.

The Consolidation Story

The scale transformation happening in China is worth paying attention to, especially if you’re trying to benchmark your own operation’s efficiency. Large operations—farms with 1,000+ head—now account for nearly 56% of the national herd, up from 24% just five years ago.

These aren’t just larger farms; they’re entirely different operations. Take the mega-dairies in Inner Mongolia—some managing 80,000+ cows with automated milking systems, integrated feed programs, and genetic optimization. Companies like Yili, which reported 115.8 billion yuan in revenue for 2024, are investing heavily in R&D and processing technology, positioning them to compete globally.

Here’s what really gets my attention, though—the operational metrics these Chinese mega-farms are achieving. Recent industry reports describe milking carousel systems completing rotations in 2 minutes 45 seconds with 99%+ uptime. That’s not just impressive technology; it’s setting new competitive benchmarks.

Financial Realities and Regional Variations

The financing environment creates both opportunities and constraints. While China’s Loan Prime Rate sits at 3.00%, actual agricultural lending rates vary significantly by region and farm size. Most producers are seeing rates between 4% and 6% for expansion capital, according to data from the Agricultural Bank of China’s sector.

Feed Conversion Ratio

Feed Cost per Cow/Year

Savings vs 1.8 FCR

1.8 (Traditional)

$2,840

Baseline

1.6 (Improved)

$2,650

$190

1.4 (Chinese Elite)

$2,500

$340

Feed costs, labor availability, and local policy support vary dramatically by province. Inner Mongolia and Heilongjiang possess natural advantages, including better forage production, established infrastructure, and proximity to processing facilities. But other regions are struggling with the transition to larger, more efficient operations.

What strikes me about the regional differences is how stark they are. Ningxia province, for instance, had 920,000 dairy cows producing 4.3 million tonnes of fresh milk in 2023, with plans to reach 1.1 million cows and 5.5 million tonnes by 2025. Meanwhile, southern provinces are experiencing farm consolidation and exits as producers struggle to compete with the efficiency levels of their northern counterparts.

The human aspect of this transformation is also significant. USDA reports indicate that over 90% of dairy farms are operating at a loss with raw milk prices near 3 RMB (€0.36) per kg. That’s forcing smaller operations out while rewarding those who can achieve scale efficiency.

What This Means for Your Operation

For exporters: Commodity approaches are no longer effective. The buyers I talk to want consistency and innovation, not just competitive pricing. Focus on differentiation—quality specifications, supply chain transparency, products that deliver demonstrable value.

Think about it this way: if Chinese operations can achieve 12+ tonnes per cow with automated systems running at exceptional uptimes, what does that mean for your cost structure? For your technology investment priorities?

For domestic producers: These efficiency benchmarks aren’t just interesting statistics—they’re becoming global competitive standards. Whether you’re in California, Ontario, or Canterbury, these are the metrics against which your products compete in international markets.

For strategists: This represents calculated market evolution, not emergency response. China’s approach to managing oversupply through structural adjustment rather than emergency intervention offers lessons for other markets facing similar challenges.

Here’s what you need to track and act on:

Monitor Chinese trade data monthly through GACC reports to identify product category shifts before they affect global pricing

Benchmark feed conversion efficiency against the documented performance of 1.4:1 achieved by top Chinese operations

Evaluate export product positioning for premium segments rather than commodity competition

Assess supply chain transparency requirements as Chinese buyers increasingly demand full traceability

The Chinese dairy story isn’t about dramatic overnight changes—it’s about systematic improvements in efficiency, quality, and market positioning executed with impressive consistency. Those who understand this evolution will find opportunities. Those who don’t may find themselves competing for markets that no longer exist.

What impresses me most about this transformation is how methodically it’s been executed. Rather than reacting to market pressures, Chinese producers and policymakers have implemented structural changes aimed at creating sustainable competitive advantages. The question for the rest of us isn’t whether this transformation will continue—the evidence suggests it will. The question is whether we can adapt our strategies to compete effectively in this evolving market environment, because, ready or not, the global dairy landscape has undergone a fundamental change.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Maximize Dairy Farm Efficiency: How Robots Can Cut Costs When Managed Properly – This article provides a tactical guide for implementing robotics to reduce labor costs and boost productivity, offering a practical “how-to” that complements the main article’s strategic overview of Chinese operational efficiency and automation.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Think the market’s stable? Think again — this plateau might be a trap!

EXECUTIVE SUMMARY: Look, I’ve been watching this industry long enough to know when something doesn’t smell right. Everyone’s talking about market “balance,” but history shows these calm periods usually end badly. Debt levels are climbing — many producers are sitting above 40% debt-to-asset ratios — while replacement heifers have skyrocketed from $1,600 to over $4,000 in just 18 months. Meanwhile, processing capacity is expanding faster than the milk supply can keep up, creating pockets of oversupply that could drive down local prices. Dr. Nicholson’s economic models at Wisconsin aren’t pretty — they show potential milk price drops of $1.90 per hundredweight and export losses hitting $22 billion. Here’s the thing: smart producers aren’t waiting around to see what happens. They’re tightening their belts, building cash reserves, and hedging their bets right now.

KEY TAKEAWAYS:

Debt management is critical — keep your debt-to-asset ratio below 35% to avoid getting squeezed when markets turn

Build liquidity like your business depends on it — aim for six months of operating reserves because cash creates options when others are forced into crisis decisions

Start hedging now while you can — use Class III futures or feed cost hedging to lock in margins before volatility hits

Diversify your buyer relationships — don’t put all your eggs in one processor’s basket, especially with new capacity coming online everywhere

Focus on operational efficiency ruthlessly — every dollar you save on feed conversion or labor costs today becomes margin protection when prices drop

The chatter in the dairy industry is all about “market balance.” Prices have plateaued, and many believe this stability will last. But here’s the thing — this perceived comfort might just be setting you up for a devastating fall.

History is littered with periods where seemingly stable prices plunged unexpectedly, catching producers completely off guard. Think back to the early 2000s and the 2014-2015 cycles — long stretches of steady pricing that lulled producers into aggressive expansion and debt accumulation. When the market suddenly shifted, those who had leveraged too heavily saw their equity vanish overnight.

Current Warning Signs Are Flashing Red

Today, multiple vulnerability indicators are blinking simultaneously, and frankly, they’re being ignored by too many operators who’ve bought into the “balanced market” narrative.

Debt levels are rising across the industry, with many producers carrying debt-to-asset ratios exceeding 40% — a historically critical stress marker that has preceded major financial casualties in previous downturns. Cash flows are being squeezed by stubbornly high feed and input costs that refuse to come down despite commodity corrections.

Interest rates are hovering near 5% for qualified operations, making expansion financing and debt refinancing particularly costly propositions. Add persistent policy uncertainties — from potential trade disruptions to shifting immigration and labor regulations — and you’ve got a perfect storm brewing beneath the surface calm.

The Economic Modeling Says It All

Crucially, recent economic modeling from Dr. Charles Nicholson at the University of Wisconsin-Madison isn’t speculative forecasting — it’s hard data analysis. His research reveals specific scenarios where various trade and policy shifts could result in milk price reductions of up to $1.90 per hundredweight and cumulative U.S. dairy export value decreases of $22 billion over a four-year period.

That’s not a theoretical risk — that’s economic modeling based on current market structure and realistic policy trajectories.

The replacement cattle market tells an even more dramatic story. Replacement heifers have surged from around $1,600 per head in mid-2023 to over $4,000 by late 2024 — a 150% spike driven by inventory scarcity and the beef-on-dairy trend. When input costs are exploding while revenue streams remain stagnant, that’s a classic vulnerability setup.

Meanwhile, dairy processing capacity has been expanding aggressively, with new mega-plants coming online across multiple regions. But milk production growth isn’t keeping pace uniformly, creating potential pockets of oversupply that could hammer local pricing.

Are You on This List? Identifying the Most Vulnerable Operations

Are the operations walking the tightrope right now? Those who expanded aggressively during recent favorable periods, especially in high-cost regions where water, feed, and regulatory pressures add operational complexity. Small to mid-size operations with thin margins and limited cash reserves are particularly exposed.

The highest-risk profiles include:

Operations with debt-to-asset ratios above 40% and debt service coverage below 1.25

Producers dependent on single-buyer relationships or concentrated market exposure

Facilities in regions facing water restrictions, increased regulatory pressure, or limited processing alternatives

Operations that banked on continued export market stability without downside protection

Here’s what really concerns me: the early warning signs I’m seeing mirror patterns from previous market corrections. The disconnect between soaring replacement costs and stagnant milk premiums? That’s a classic vulnerability indicator that preceded past crashes.

Your Defensive Playbook: Strategic Protection Plan

Market turbulence isn’t a question of if — it’s when. Smart operators aren’t sitting around hoping this plateau continues. They’re actively building defensive positions while opportunities still exist.

Diversification isn’t optional anymore. Don’t put your operation’s future on a single buyer or market channel. I’m seeing forward-thinking producers develop relationships with multiple processors, exploring emerging opportunities in specialty markets and value-added product streams.

Risk management tools deserve serious consideration. Whether through Class III milk futures, options contracts, or cross-hedging strategies for feed costs, you need downside protection. Recent analysis shows that effective hedging strategies can significantly manage margin risk during volatile periods.

Cash reserves aren’t a luxury — they’re survival insurance. Target at least six months of operating reserves. Operations with strong liquidity positions will have options when others are forced into crisis decisions.

Financial discipline matters more than ever. Aim for debt-to-asset ratios below 35% and debt service coverage ratios above 1.25. These aren’t arbitrary benchmarks — they’re financial stress indicators that historically separate survivors from casualties.

Take Action Now — Your 4-Step Priority Plan

If I were making decisions on your operation tomorrow, here’s my immediate action checklist:

1. Get a Real-Time Financial Snapshot. Immediately calculate your actual debt-to-asset ratio and debt service coverage. If you’re above 40% and below 1.25, respectively, you need a deleveraging plan now, while milk prices still provide some flexibility.

2. Lock In Your Risk Management. Don’t gamble with your operation’s future. Whether it’s forward pricing a portion of your production, establishing feed cost hedges, or negotiating flexible supply agreements with multiple buyers, your goal is to minimize as much uncertainty as possible from your profit and loss (P&L) statement.

3. Hunt for Efficiencies Ruthlessly. Every dollar you save in feed conversion, labor productivity, or operational costs today becomes a dollar of margin protection when the market turns. This requires disciplined focus on measurable improvements.

4. Hoard Cash Like Your Business Depends on It. If that means pausing expansion plans or selling non-core assets to build liquidity reserves, do it. In a downturn, cash creates options, and options are the difference between survival and failure.

The Bottom Line

Don’t be lulled into complacency by the current price plateau. This “market balance” narrative is dangerous precisely because it breeds the kind of strategic inaction that destroys operations when cycles inevitably turn.

The dairy industry’s current stability might be real, but it’s also fragile. External shocks — whether from trade policy changes, weather events, disease outbreaks, or broader economic disruption — could unravel today’s equilibrium faster than most producers realize.

The next market cycle isn’t coming someday — it’s building momentum right now, beneath the surface of this apparent calm. The question isn’t whether it will arrive, but whether your operation will be positioned to weather it when it does.

Will you be ready?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Profit and Planning: 5 Key Trends Shaping Dairy Farms in 2025 – While the main article advises hunting for efficiencies, this piece provides a tactical roadmap. It details five specific areas, from data integration to sustainability, where you can find cost savings and boost operational resilience against market volatility.

USDA’s 2025 Dairy Outlook: Market Shifts and Strategic Opportunities for Producers – This article provides the official market analysis to balance the main piece’s warning. It breaks down the USDA’s forecasts on milk production, pricing, and exports, giving you the hard data needed to assess opportunities and validate your risk management strategy.

The $8 Billion Infrastructure Trap: Why America’s Dairy Boom Could Become Its Biggest Bust – For a deeper dive into the processing capacity risk mentioned in the main article, this piece is essential. It explores how the massive infrastructure buildout could create regional oversupply and price pressure, revealing the mechanics behind the potential market trap.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Milk prices drop 4.1% but your feed bill’s the same—here’s how smart producers are still making money

EXECUTIVE SUMMARY: Look, here’s what’s really happening out there—the old “more cows, more money” playbook is broken. I’m talking to producers from Ontario to Idaho, and the ones still making decent money aren’t the guys with the biggest herds. They’re the ones pushing butterfat above 4.1% and protein over 3.3%, which can mean an extra $2 per hundredweight when milk prices are getting hammered.The Global Dairy Trade took a 4.1% hit in July, and powder prices dropped 5.1% to $3,859 per metric ton—but here’s the thing. Feed costs are actually holding steady around $4.50 for corn and $350 for soybean meal, so if you’re smart about efficiency, your margins don’t have to tank.China’s cutting back on imports by 12-15%, Europe’s drowning in €850 per cow compliance costs, and everyone’s scrambling to figure out what’s next. Meanwhile, the producers who maintain 60-90 days of operating cash and hedge 40-60% of their production are sleeping soundly at night. Stop chasing volume and start chasing components—that’s where the money is in 2025.

KEY TAKEAWAYS

Lock in Feed Cost Savings: Target feed costs under $9.50/cwt by tracking your receipts against USDA data on a monthly basis. Every dollar you save here goes straight to your bottom line when milk prices are soft.

Component Premium Strategy: Push for butterfat over 4.1% and protein above 3.3%—this can net you an extra $2/cwt in premiums. Pull your latest DHIA report and see where you stand right now.

Smart Risk Management: Hedge 40-60% of your milk production through DMC or forward contracts. With China backing out and market volatility hitting hard, unprotected milk is a gamble you can’t afford to take.

Cash Flow Defense: Build and maintain 60-90 days of operating cash reserves. Call your lender this week and ask for their benchmark data on what successful operations are keeping liquid.

Strategic Market Timing: Use 2025’s feed cost stability (corn near $4.50/bu) to improve feed conversion ratios. Wisconsin Extension trials show 4-6% improvements are realistic with better TMR protocols.

The thing about this market? It feels like watching fresh cows trickling into a dry lot on a chilly morning—uneasy, unpredictable, and every farmer feeling it a bit differently. I’ve received quite a few calls lately from folks in Ontario to Idaho, and the question is always the same: how do we handle falling milk prices amid rising input costs?

At the July 15, 2025, Global Dairy Trade event, the index slid 4.1%, with whole milk powder easing 5.1% to $3,859 per metric ton. For those of you in cooler climes like the northern U.S. or Canada, this slump echoes in your contracts too—European futures have their own skirmishes with skim milk powder and butter prices wavering, though sometimes not as sharply as headlines might suggest.

However, here’s the thing—if your nutritionist isn’t providing you with data, ask for it. Wisconsin Extension trials showed that herds implementing TMR protocols saw a 4–6% improvement in feed conversion ratio. That’s real fuel for boosting milk production without breaking the bank. With feed costs holding steady—corn is hovering near $4.50 per bushel and soybean meal is under $350 per ton, according to the USDA’s June 2025 Feed Grains Outlook—your margins depend heavily on capturing these efficiencies.

Herd Growth: More Cows, But Are We Making More Money?

However, let’s be clear about what the headlines often overlook: more milk doesn’t automatically translate to higher margins. Yes, U.S. dairies increased cow numbers by more than 45,000 head since July 2024, with rolling averages inching up—some hitting 24,000 pounds per cow or better. However, sharp operators I know keep a close eye on component checks, pushing to keep butterfat above 4.1% and proteins above 3.3%. That’s becoming a critical tactic, especially as risk management becomes a staple, not an option.

And what about the Australians and Kiwis? While Fonterra reports a 1.5% increase in collections, places like Gippsland in Australia actually saw a 2% drop in production year-over-year, due to dry weather. The growth we’re seeing isn’t universal—it’s pockets of efficiency, careful grazing, and smart tech upgrades keeping some farms afloat.

China’s Changing Game—Buying Less Powder, Investing More at Home

One of the game-changers in this market is China. Market analysts project a 12-15% decline in China’s whole milk powder imports for the latter half of 2025, driven by an estimated $5 billion state-backed investment in domestic processing capacity—including robotics, new plants, and larger herds—which is reshaping global trade.

This is why you’re hearing about hedging at every co-op meeting. If your risk advisor suggests hedging half of your production, don’t just nod—ask them for the Rabobank or USDA FAS data they’re using. Tools like the Dairy Margin Coverage (DMC) program are experiencing unprecedented use.

Europe’s Compliance Crunch and Margin Squeeze

For European producers, the mountain to climb looks steeper. The European Agricultural Fund for Rural Development recently estimated that environmental compliance costs could reach as high as €850 per cow, and the European Dairy Farmers’ Association confirms that margins have dipped below 3%. The price per hundred kilos may hover near EUR53, but when you factor in growing paperwork and strict audits, chasing component premiums is the real strategy to keep things running.

Herd managers across northern Europe are doubling down on ration tweaks just to eke out extra euro per tank, especially on butterfat numbers, which remain the shining stars in this squeeze.

The Bottom Line: Managing Break-Even and Cash Flow in Bumpy Markets