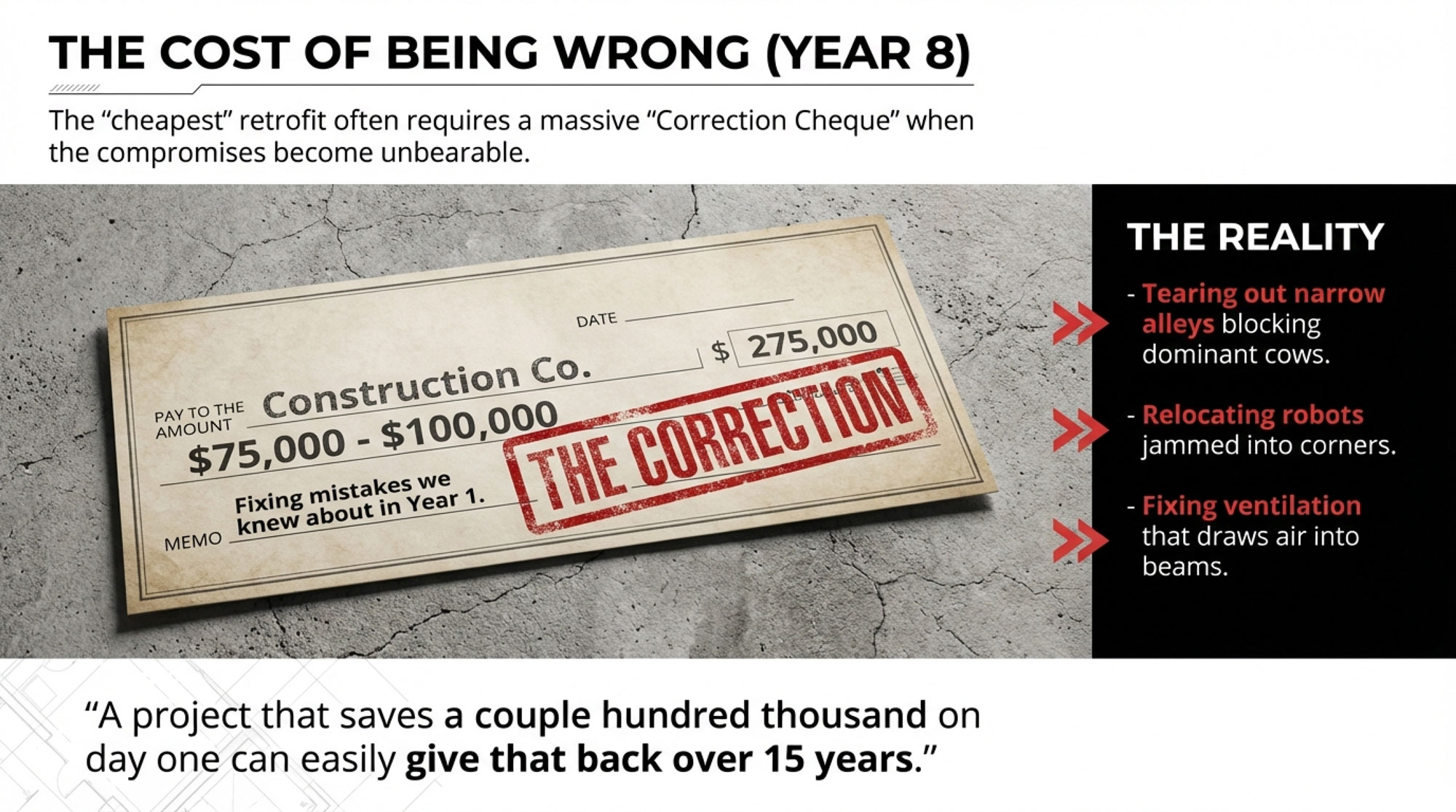

Here’s the cash flow math the dealer didn’t show you — and the one number that predicts whether your robots will pay

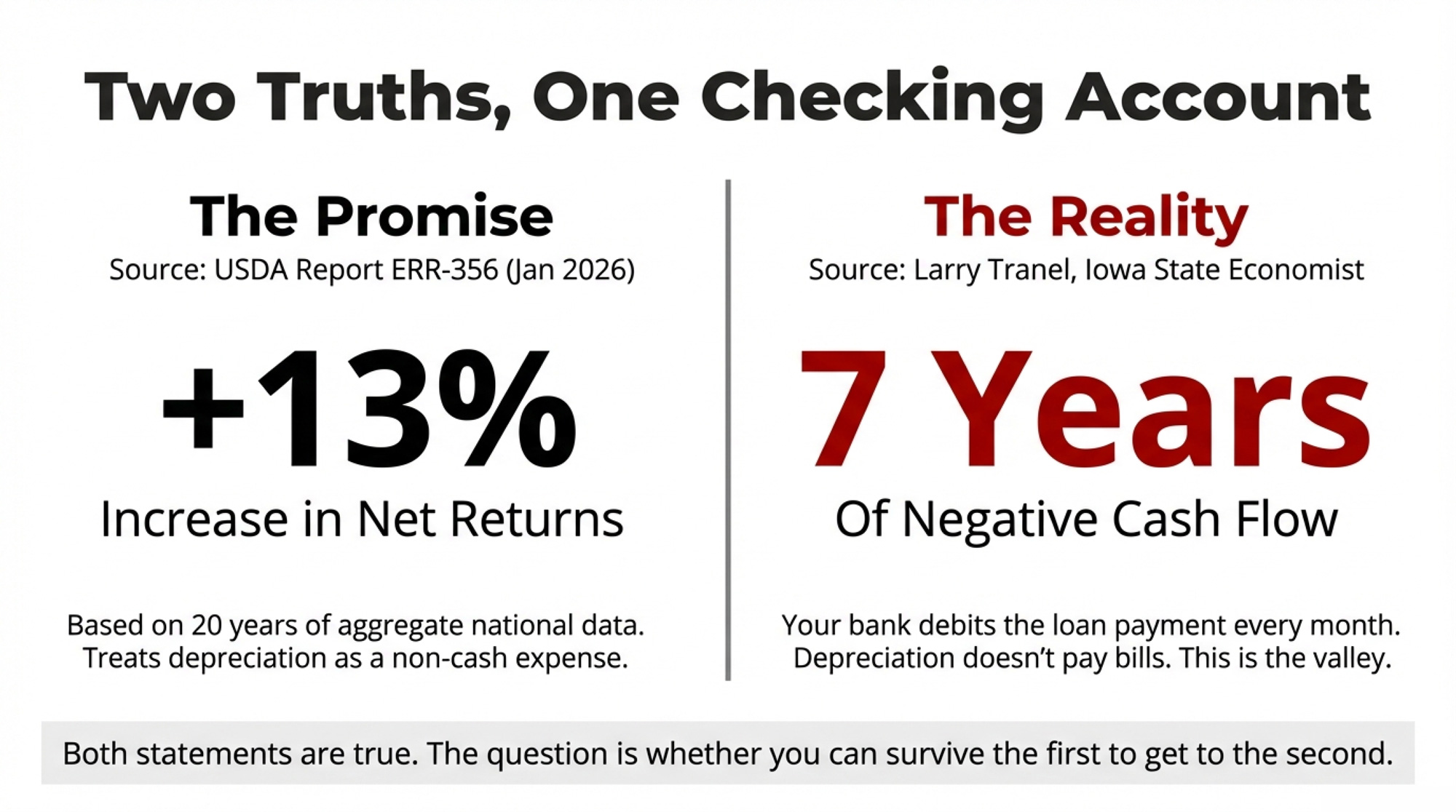

A brand-new USDA Economic Research Service report — Precision Dairy Farming, Robotic Milking, and Profitability in the United States (ERR-356, January 22, 2026) — finds that robotic milking increases U.S. dairy net returns by 13 percent on average. The researchers drew on five waves of USDA Agricultural Resource Management Survey data spanning 2000 through 2021, and they controlled for the fact that stronger managers tend to adopt first. That 13% is an adjusted treatment effect. It’s the strongest national evidence yet that AMS profitability is real.

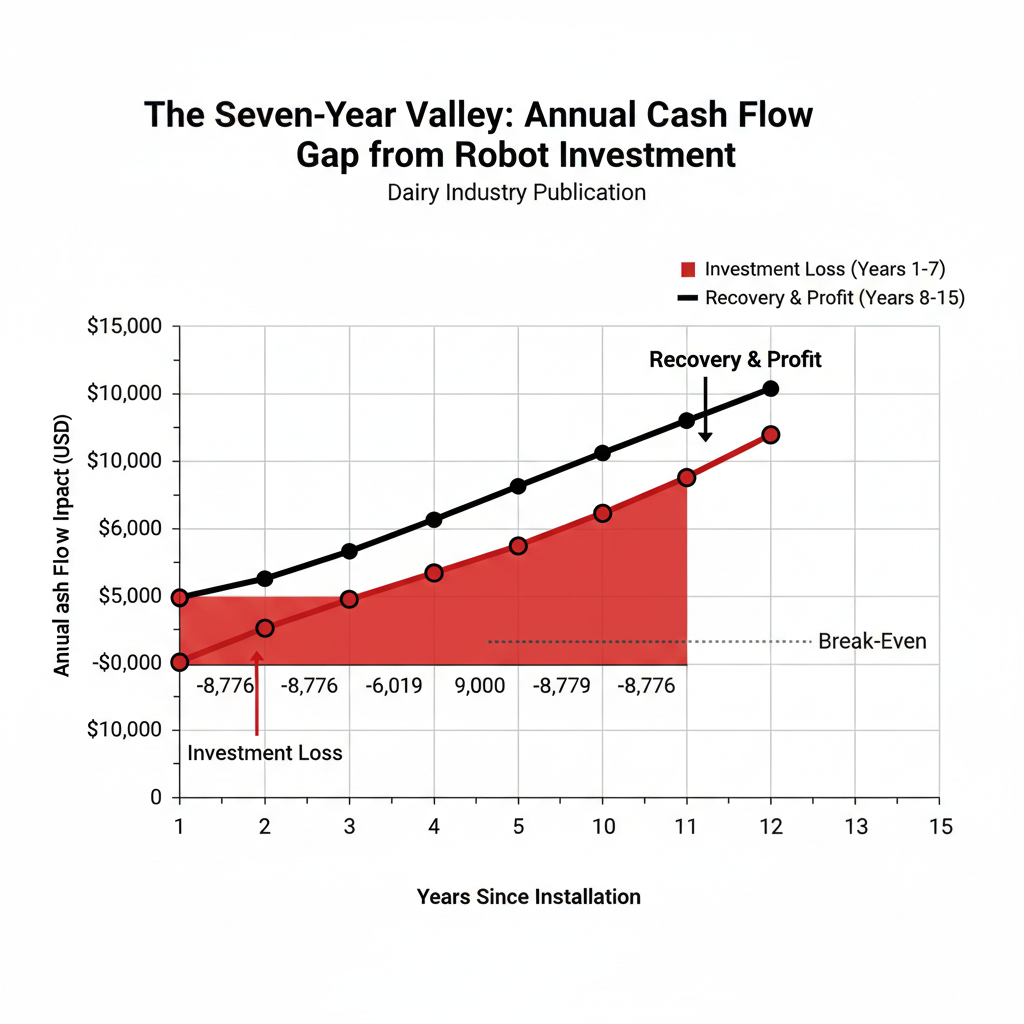

And yet. Iowa State dairy economist Larry Tranel — the guy who’s been running AMS economics since before most dealers had a demo unit — puts it this way: “Cash flow of a robot tends to be very negative in the first seven years, then pretty positive for rest of the life of the AMS, but that is dependent on many variables, especially repair costs across the whole life of the robot.”

Both things are true. The question is whether your operation can survive seven years on the wrong side of the ledger to reach the right one.

The $8,776 Gap Your Checking Account Feels Every Year

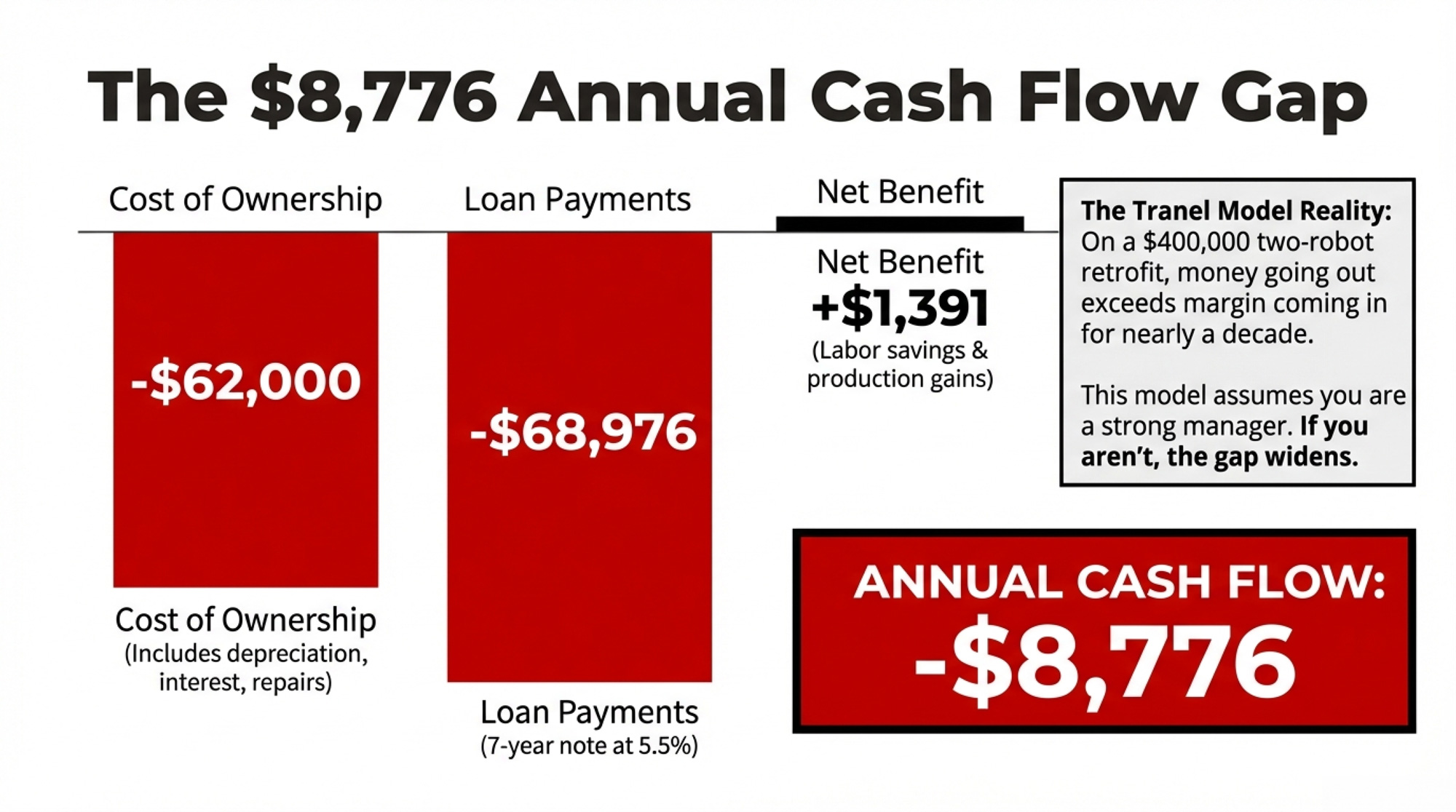

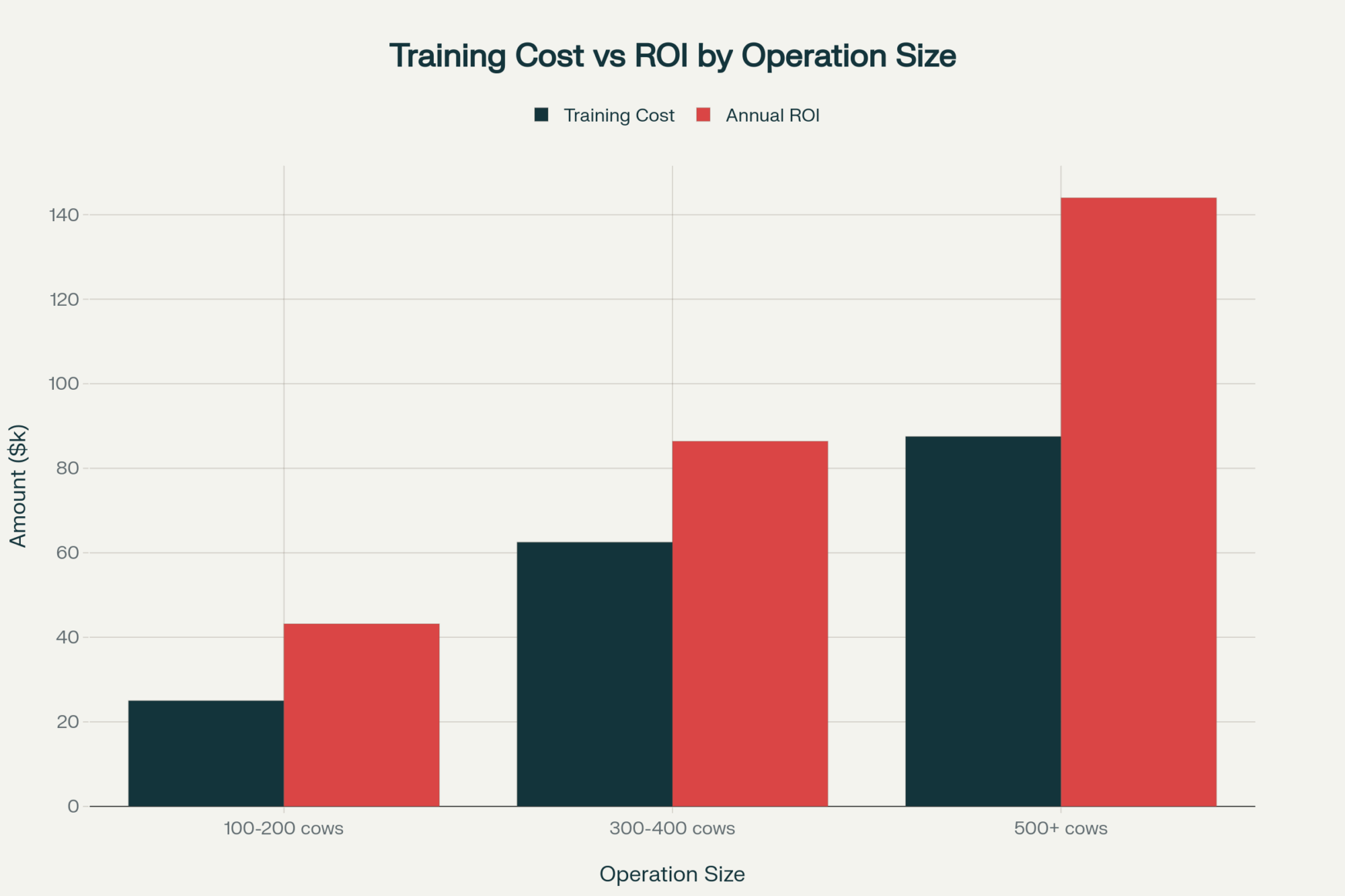

Here’s how the math works in Tranel’s partial budget model for a two-robot retrofit with a total investment of $400,000. Annual ownership costs — depreciation, interest, repairs, insurance — run roughly $62,000. Against that, the net financial benefit from labor savings, production gains, and reduced hired help comes to just $1,391 per year before you assign a single dollar to quality of life.

Now layer on the loan. A 7-year note at 5.5% means an annual payment of $68,976. The capital recovery cost for a 10-year useful life is $60,200. The gap: negative $8,776 per year in cash flow — and that’s before you account for any labor you didn’t actually eliminate.

Why does the USDA aggregate picture look so much rosier? Depreciation. In the national profitability calculation, it’s a non-cash expense spread over the equipment’s useful life. In your checking account, the loan payment is debited every month. For seven years, money going out exceeds the margin improvement coming in. That’s the valley.

Worth noting: the USDA report says only 6% of U.S. milk came from cows milked via box robots as of 2021. AMS remains the minority, meaning the profitability data reflects a population skewed toward early adopters who tend to be stronger managers to begin with.

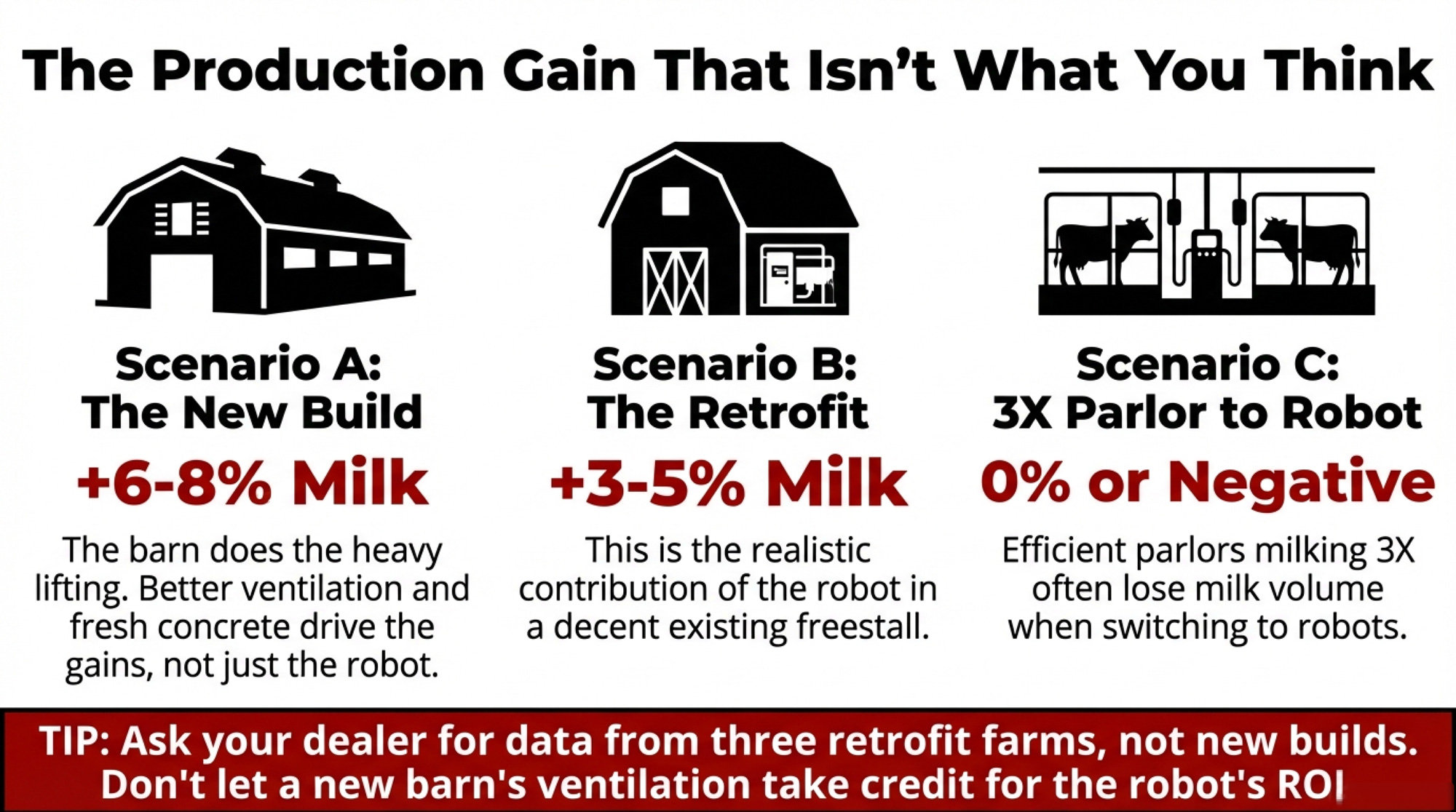

The Production Gain That Isn’t What You Think

Tranel puts the typical production bump at 3 to 5 percent for herds switching from twice-daily milking. Some farms hit 10% or more. But here’s what gets glossed over at the open house: “Often, much of the increase reported on AMS is due to the new cow housing facility, not just the AMS, as new facilities often increase production 6 to 8 percent over old, worn-out facilities. This is an important point often overlooked.”

That 10% jump your neighbor reported? Maybe 3–5 points came from the robot. The rest came from the new barn. Better ventilation. Fresh concrete.

Already milking 3X in an efficient parlor? Tranel doesn’t sugarcoat it: “Producers currently milking 3X may experience a decrease in milk production.”

Where You’re Starting

Realistic Gain

2X in older tie-stall or worn-out freestall

6–8% (new barn + robot combined)

2X in decent existing freestall (retrofit)

3–5% (robot contribution)

3X in an efficient parlor

0% or potentially negative

Source: Tranel, Iowa State Extension (2018)

💡 The Bullvine Tip: Before you sign an AMS contract, ask the dealer for production data from three retrofit farms — not new-builds. If the big gains only show up where somebody also poured a new barn, the robot isn’t the hero. The ventilation and stall comfort are doing the heavy lifting. Purina Canada’s 2025 analysis of Canadian retrofit herds found a trending average of +3 liters/cow/day — about C$2.70/cow/day at a Canadian milk price of roughly 90 cents/liter. A useful reference point, but Canadian pricing doesn’t translate directly to U.S. operations.

At Tranel’s benchmark of 4,500 lb of milk per robot per day, AMS milking costs run about $2.13/cwt (range: $1.77–$3.00). A well-run swing-12 parlor? Roughly $1.08/cwt. That’s a dollar-plus gap you have to close with production gains, labor savings, and management value. Every month.

Cost Component

AMS ($/cwt)

Swing-12 Parlor ($/cwt)

Ownership (depreciation, interest, insurance)

$1.05

$0.38

Maintenance & Repairs

$0.54

$0.22

Labor (net after savings)

$0.34

$0.38

Throughput & Efficiency

$0.20

$0.10

Total Milking Cost

$2.13

$1.08

Gap You Must Close

+$1.05/cwt

—

Where the Maintenance Money Goes

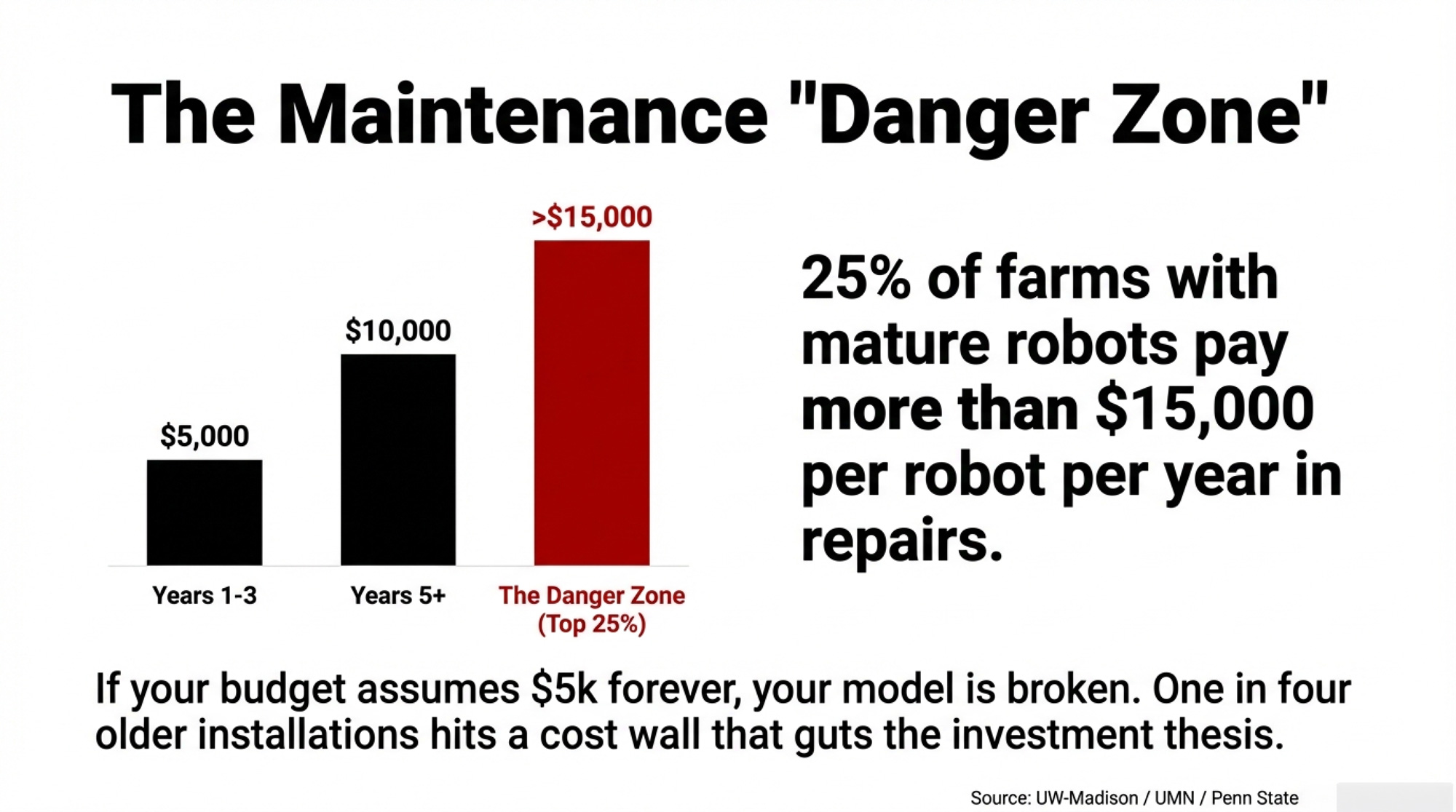

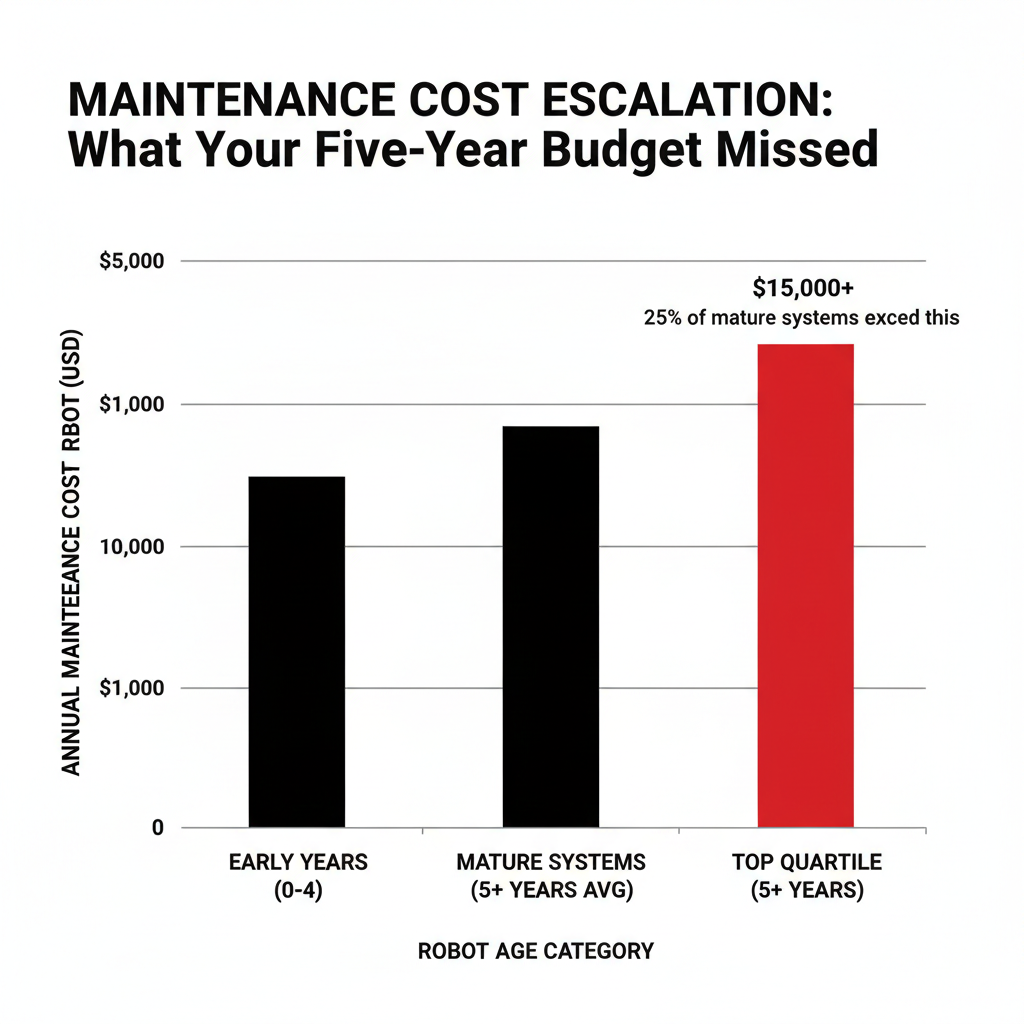

The 2019 joint survey by Extension educators at UW-Madison, the University of Minnesota, and Penn State — with more than 50 complete responses — tracked how costs change as robots age.

Early years: repairs and maintenance average around $5,000 per robot per year. As units get older, those costs climb to roughly $10,000, driven mainly by bigger repair bills while routine maintenance stays fairly steady.

But averages mask the danger zone. Among farms running robots for 5 years or more, 25% reported maintenance costs exceeding $15,000 per robot per year. A few blew past $25,000. Those producers, in their written comments, “made it clear that adaptation to AMS didn’t go well for them and that they were transitioning back to conventional milking systems or exiting the dairy sector.”

One in four older installations is hitting a cost wall that guts the investment thesis. That’s not a tail risk. That’s a quartile.

One bright spot from the same survey: 45% said dealer service had improved since they first adopted. When your robot goes down, how fast the technician arrives is the difference between a hiccup and days of lost production.

The Labor Savings Are Real. The Mental Load Is the Surprise.

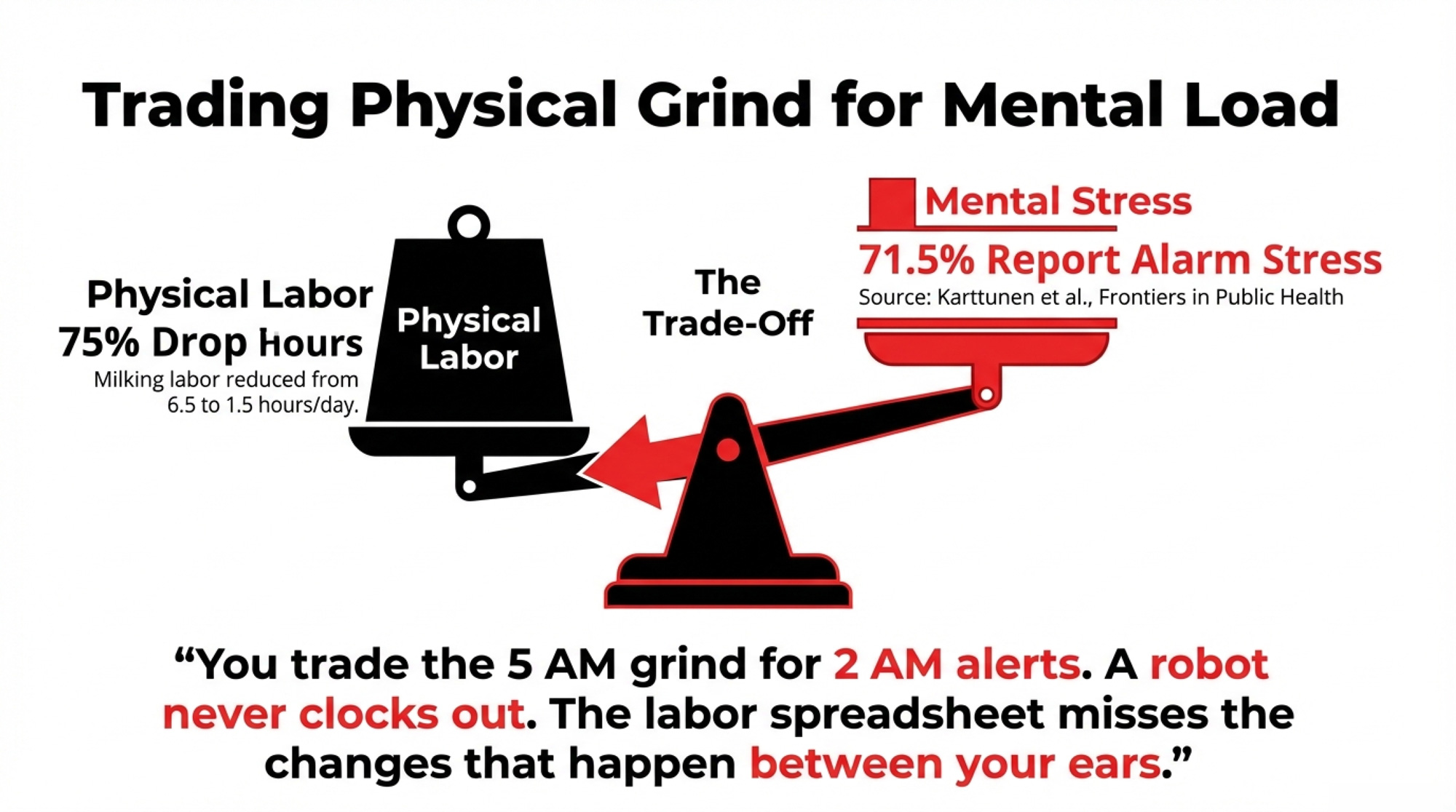

Tranel’s data show a 75% decrease in milking labor hours — from 6.5 hours/day to 1.5 on a typical two-robot farm. The UW–UMN–Penn State survey confirmed average savings of 38% per cow and 43% per hundredweight. At $15/hour, that works out to about $1.50/cwt in labor savings. Top-quartile farms saved $2.40/cwt or more.

But 8% of respondents reported no labor savings at all — mostly because maintenance demands ate the hours right back.

And the labor spreadsheet misses the changes that happen between your ears. A 2014 survey of 228 Finnish AMS farmers — published in 2016 by Karttunen, Rautiainen, and Lunner-Kolstrup in Frontiers in Public Health — found 71.5% reported mental stress from nightly AMS alarms and 51.7% experienced stress from the 24/7 standby. Overall, 93.4% mentioned at least one AMS-related issue causing mental strain.

That survey is now a dozen years old, and alarm management tech has improved. But the underlying reality hasn’t changed — a robot never clocks out. Christina Lunner Kolstrup of the Swedish University of Agricultural Sciences, a co-author on the Finnish study, put it plainly in a summary of her qualitative research reported by Dairy Global in 2021: “Previously, with conventional milking, the working day had a clear and natural ‘start’ and ‘end’, but with the AMS, there are no specific working hours. The informants claimed that they are working longer hours now than before. They are never really done after a working day, as there is always something more to be done in the dairy barn.”

One Wisconsin producer in the Extension survey nailed it: “AMS is not stress free. Physically, it is easier. Mentally stressful.” Another said: “Anyone considering robotics should understand that there is still plenty of daily work involved in milking, robots just give you more flexibility with your time.”

You trade the 5 AM and 5 PM grind for 2 AM alerts. If you run a family operation, that trade-off deserves a kitchen-table conversation before it deserves a dealer quote.

Factor

The Financial Gain (Quantified)

The Mental Load Reality (Survey Data)

Milking Labor Hours

75% reduction (6.5 hrs/day → 1.5 hrs/day)

51.7% report stress from 24/7 standby requirement

Labor Cost Savings

38–43% per cow; $1.50–$2.40/cwt

71.5% report stress from nightly AMS alarms

Top-Quartile Labor Savings

$2.40/cwt or higher

Workdays no longer have clear “start” or “end”

Zero Labor Savings

8% of adopters (maintenance ate the hours back)

93.4% report at least one AMS-related mental strain

Physical Demand

Significantly easier (no 5 AM/5 PM milking)

“Mentally stressful… never really done after a working day”

Schedule Flexibility

More control over daily timing

Trade 5 AM/5 PM grind for 2 AM alerts; alarms wake you at night

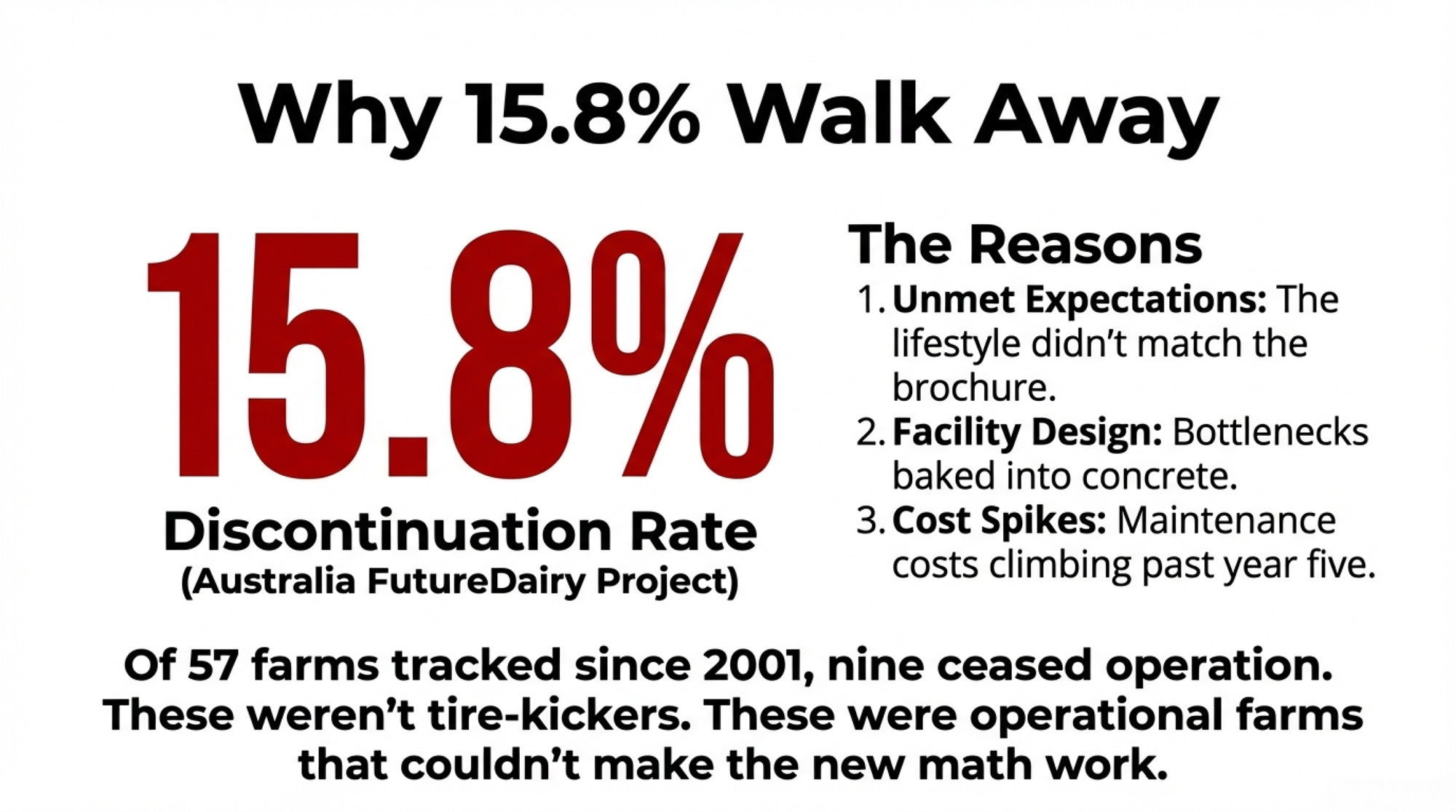

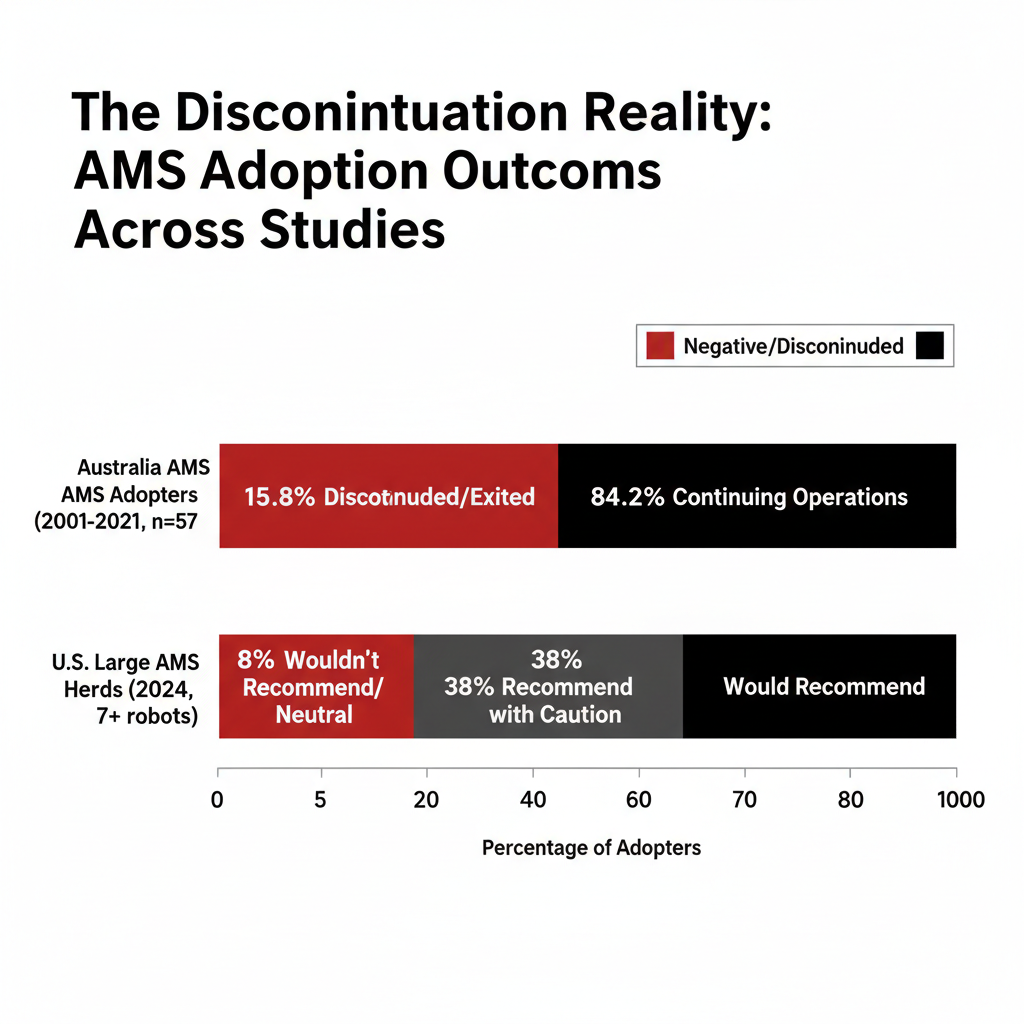

The 15.8% Who Stopped

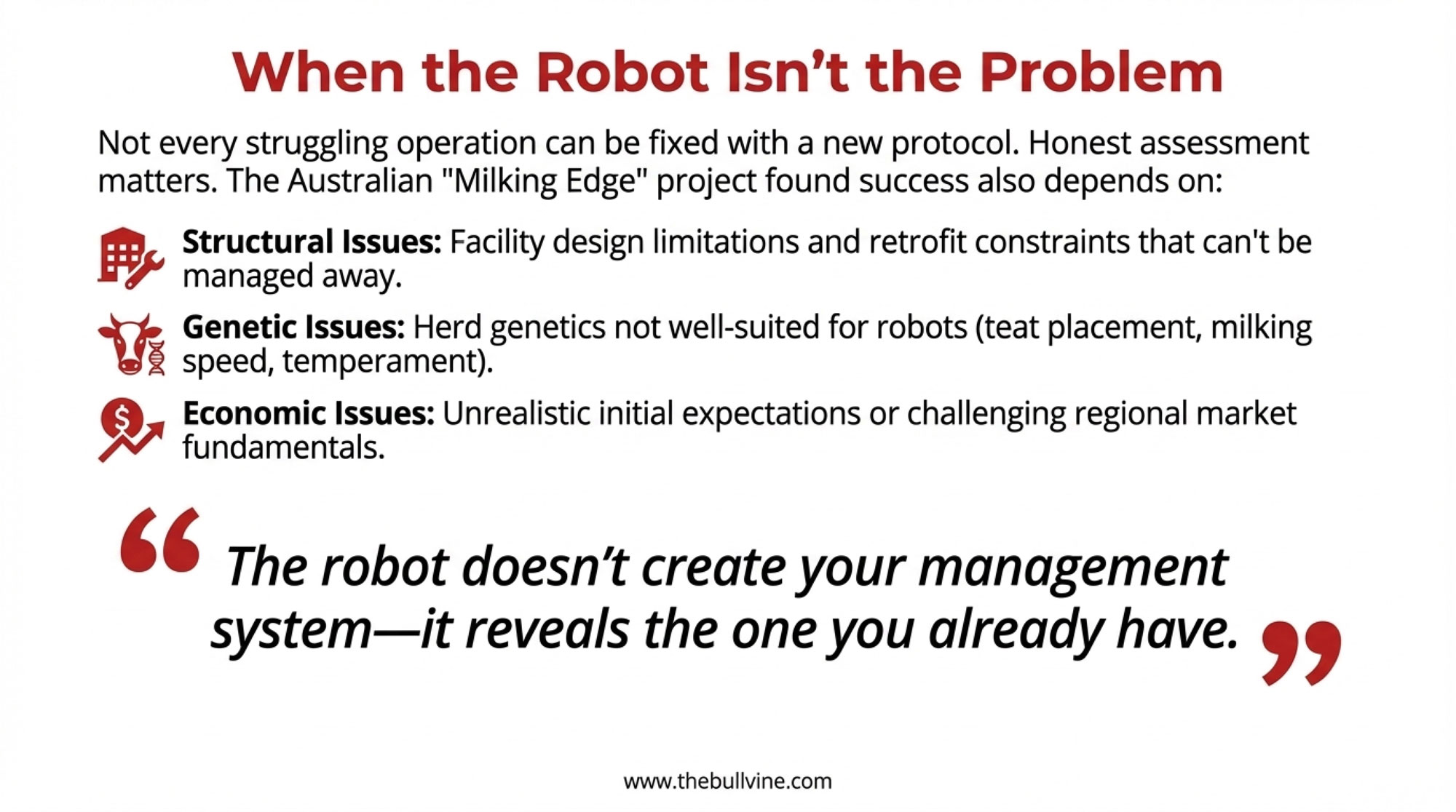

Dr. Nicolas Lyons, dairy technology leader at NSW Department of Primary Industries and a key researcher on Australia’s FutureDairy project, tracked the country’s entire AMS adoption history: “Of the 57 farms that commissioned robots since 2001, now there were only 48 operating. We had nine cease — some went back to a conventional dairy, and some left the industry entirely.”

Nine of 57. A 15.8% discontinuation rate — not among tire-kickers, but among farms that installed robots, ran them, and walked away.

Lyons didn’t dodge the reasons: “It basically comes down to things like expectations weren’t met; some couldn’t make it work; some didn’t have a good relationship with the equipment provider; and some didn’t achieve what they had hoped.”

The pattern usually starts with facility design — cow traffic bottlenecks baked into concrete you can’t move. It compounds when maintenance costs climb past year five. And it breaks open when the promised lifestyle improvement collides with the grind of 24/7 systems management.

What the Satisfied Farms Actually Said

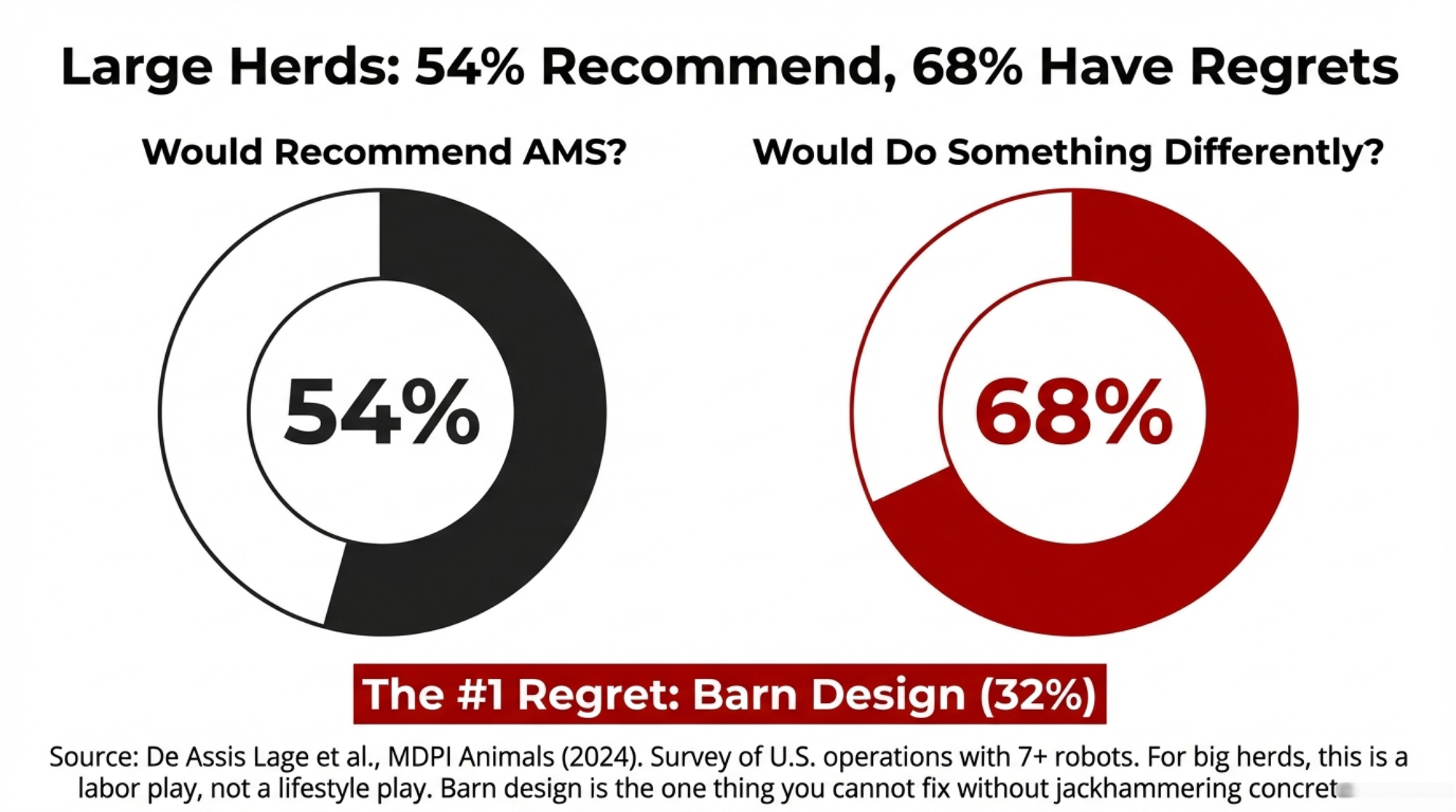

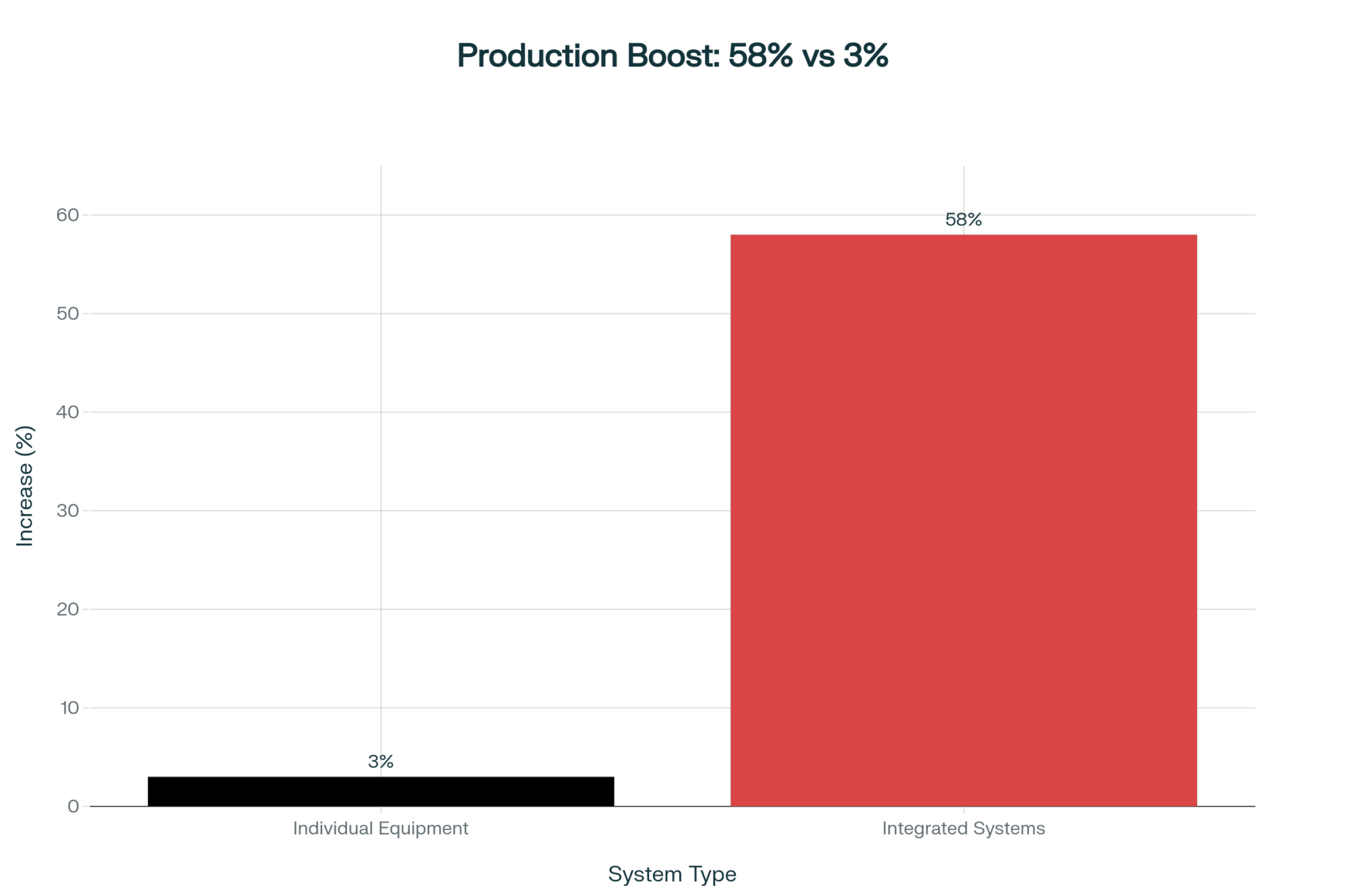

De Assis Lage and colleagues surveyed large U.S. AMS operations — farms running 7 or more milking boxes, median herd around 940 lactating cows — in a 2024 study published in MDPI Animals. The results: 54% would recommend AMS. Another 38% advised careful consideration before adopting. Just 8% were neutral or wouldn’t recommend.

That 38% isn’t a rejection. It’s producers who know it works—and exactly what it costs to get there.

Production results: 58% reported increases, and 32% saw higher fat and protein content. Top adoption motivations for these large herds: labor costs (81%), cow welfare (78%), herd performance (74%). Quality of life came in fourth at 44%. For big U.S. operations, AMS is a labor and performance investment first. The lifestyle argument carries more weight on smaller Canadian and European farms, where it consistently ranks as the top driver.

The regret data matters most: 68% would do something differently. Barn design modifications topped the list (32%), followed by improvements to cow flow (16%). Two-thirds wished they’d planned their facility better — the one thing you absolutely cannot fix without jackhammering concrete.

What Your Lender Sees

Brad Guse, Senior Vice President of Agriculture at BMO Harris Bank, frames the question the way your banker will: “Given the significant capital outlay for robotic dairy equipment, how are you going to repay the debt?”

Tranel’s model answers that bluntly. On a $400,000 investment at 7 years and 5.5%, the payment is $68,976/year. Capital recovery is $60,200/year. The cash squeeze starts on day one.

Guse warns specifically against balloon payments — you’re deferring principal at exactly the point maintenance costs start climbing.

And Tranel raises a timeline question that rarely comes up at the dealer’s table: “If you will be farming for at least another 13 to 17 years, that increases the propensity to put in robotics, but if you are only planning on farming about seven years, then it might not make sense.” Looking at 20 more years? “You need to consider needing to make a second investment of money in 15 years when the equipment wears out.”

The One Number That Predicts Your Return

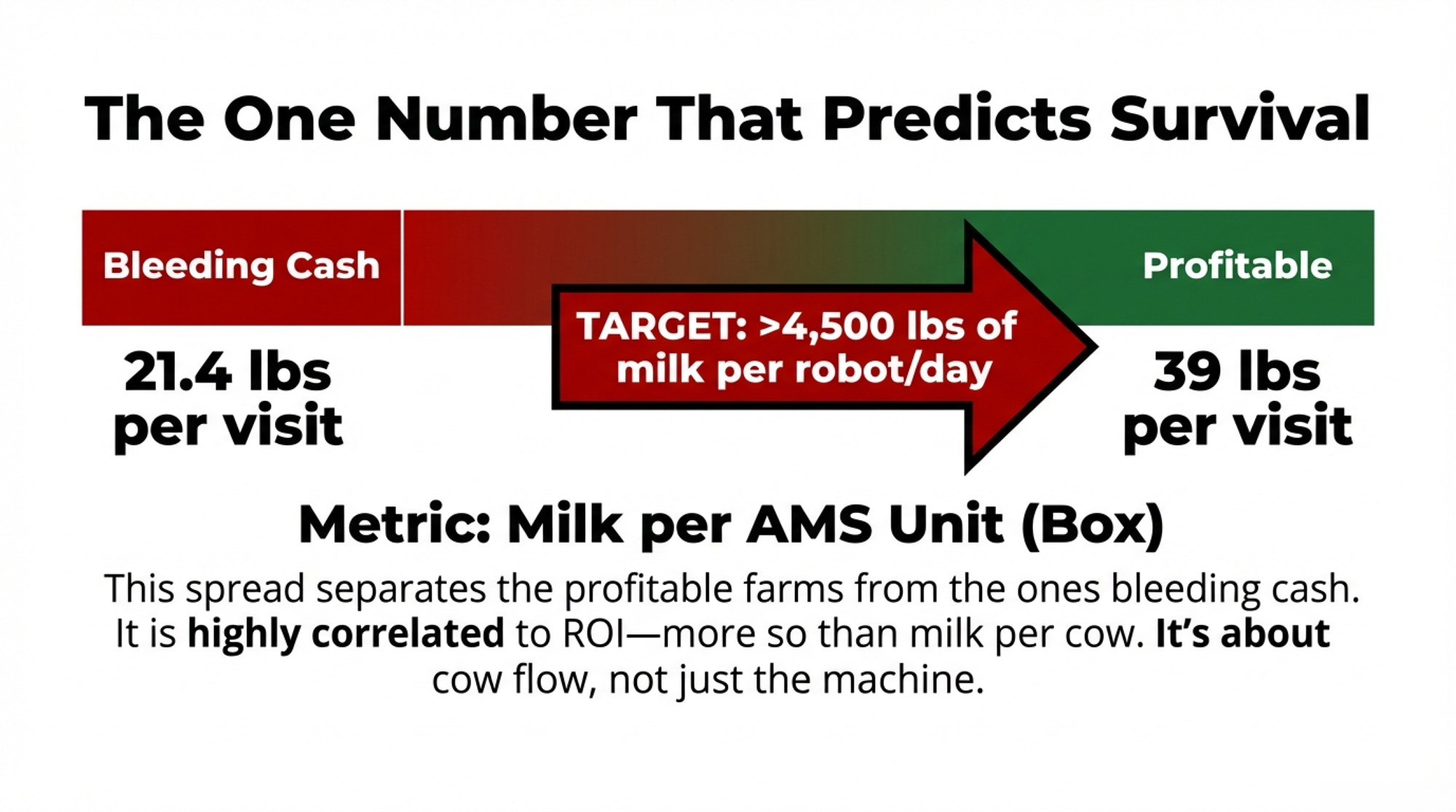

Tranel is clear: milk per AMS unit is “very highly correlated” to AMS profitability — more so than milk per cow. The 2019 survey data showed robot visits ranging from 2.4 to 3.1 per cow per day, and milk per visit ranging from 21.4 to 39 lb.

That spread — 21.4 to 39 lb per visit — separates the robots that pay from the ones that bleed you dry. And the gap isn’t about the machine. It’s cow flow, feed management, lameness protocols, stall comfort, and whether you run the data like a systems manager or treat the robot as a very expensive hired hand.

What This Means for Your Operation

Budget AMS milking at $2.00–$2.50/cwt against roughly $1.08/cwt for a good parlor. Your labor savings, production bump, and management-software value have to clear that gap. Monthly.

Plan for maintenance to roughly double by year five — and for the real possibility you land in the top quartile at $15,000+ per robot. If your cash flow model assumes $5,000/year in perpetuity, it’s wrong.

If you’re milking 3X in an efficient parlor, don’t model production gains from AMS. Tranel’s data says you may lose ground. Be honest about your starting point before you model the finish.

Run Tranel’s spreadsheet — search “Iowa State Extension dairy team milking systems” for the free download. [Verify URL is current before publication.] Stress-test your numbers at $17 milk, not just $22. If the math only works at high prices, you’re making a bet, not an investment.

Facility design is the regret you can’t undo. Visit retrofits, not just new-builds. Walk through at peak milking time. Ask every operator the same thing: “What would you do differently?”

Know your timeline. Less than 10 years to exit? The valley may outlast your career. Twenty years out? Budget for a full equipment replacement at year 15.

Have the family conversation about mental load before you have the dealer conversation about price. The Finnish data is clear: 71.5% of AMS farmers reported stress from nightly alarms. Alarm tech has improved since that 2014 survey, but the 24/7 nature of robot management hasn’t changed.

Key Takeaways

The January 2026 USDA report (ERR-356) confirms that AMS boosts net returns 13% on average. But Tranel’s cash flow model shows seven years of red ink before you reach the payoff. Both are true. The difference is what you measure.

Production gains of 3–5% are realistic for 2X herds. Much of any larger gain comes from new facilities—not from the robot itself. Ask for retrofit data before you sign.

AMS milking costs roughly double a good parlor — $2.13/cwt vs. $1.08/cwt in Tranel’s model.

54% of large U.S. AMS farms recommend the technology, but 38% say do your homework first. And 68% wish they’d planned their barn differently.

Maintenance costs nearly double as robots age. One in four older installations tops $15,000/robot/year.

Of Australia’s 57 AMS adopters since 2001, nine stopped entirely — a 15.8% discontinuation rate driven by unmet expectations and poor dealer relationships.

The Bottom Line

The producers who recommend AMS without hesitation didn’t just buy different equipment. They became different managers — relentless about the gap between 21.4 and 39 lb per visit, obsessed with cow flow, and brutally honest about what the investment demands.

Where does your operation actually sit in that picture? Answer with a spreadsheet — not a brochure — before you pour the concrete.

Executive Summary:

USDA’s 2026 ERR-356 report says robotic milking and precision tech boost U.S. dairy net returns by about 13% on average, but Iowa State economist Larry Tranel’s cash flow work shows that a typical two-robot install often spends roughly seven years in the red before that upside appears. In his model, a $400,000 system carries about $62,000 in annual ownership costs and nearly $69,000 in loan payments, with only around $1,400 in net financial benefit — leaving an estimated $8,776/year cash flow gap in the early years. Extension surveys echo that pressure, finding that maintenance and repair costs commonly rise from about $5,000 to $10,000 per robot as units age, and that roughly one-quarter of mature AMS herds pay more than $15,000 per robot per year. On the positive side, those same data sets show 3–5% milk increases in most 2X herds that adopt robots, 38–43% labor savings, and better components in many large U.S. dairies, especially when upgrades include new barns. Mental health research from Finland and Sweden then adds a human price tag, with more than 70% of AMS farmers reporting stress from nightly alarms and describing workdays that no longer have a clear start or finish. The full article combines these numbers into a clear playbook — from cost per cwt and milk per robot box to maintenance risk and farming timeline — so you can decide, with eyes open, whether robotic milking fits your herd and your life.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Dairy Tech ROI: The Questions That Separate $50K Wins from $200K Mistakes – Gain a definitive roadmap for tech upgrades by identifying the robot profitability “sweet spot.” This breakdown exposes the infrastructure failures that sink 62% of investments and arms you with the labor-wage thresholds required for a positive return.

More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Secure your operation against 2026’s projected margin compression by mastering the “more milk, fewer farms” math. This strategic briefing reveals the $250,000 revenue gap facing mid-sized dairies and delivers actionable culling and hedging tactics to protect your bottom line.

The Next Frontier: What’s Really Coming for Dairy Cattle Breeding (2025-2030) – Capture an additional $3,000 per cow in annual revenue by positioning your herd for the gene-editing revolution. This forward-looking analysis breaks down how designer milk and genomic health markers will fundamentally reshape your competitive advantage and profit potential by 2030.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Under 500 cows and eyeing robots? Before you sign a $1M note, answer this: Who shows up your lane when the barn goes dark?

Executive Summary: If you milk under 500 cows and you’re eyeing robots, this piece shows why a USD $1 million AMS note won’t automatically fix your labor problem—and might bury you if the math and the people aren’t there. It breaks down current immigrant‑labor dependence, Wisconsin’s drop from 16,000+ herds to just over 5,300, and what real AMS budgets and labor‑savings studies say about when robotic milking ROI actually pencils out. You’ll see a side‑by‑side look at parlor‑only, hybrid “parlor + tech,” and full AMS paths, with clear thresholds—like whether you can truly staff milking for around USD $200,000 a year—that help you decide if you should upgrade, automate, or plan a clean exit. The article also ties genomics and proofs straight to robot performance, showing why milking speed, udder traits, health, and beef‑on‑dairy decisions are now core to your AMS payback, not just nice extras. Alongside the math, it tackles storms, backup power, mental health, and the 4‑H kid with a calf who might be your next key employee or successor. You’ll walk away with a 30‑day checklist, practical questions to take to your lender and family, and one blunt test that matters more than any sales pitch: when the barn goes dark, who actually turns up your lane?

The trucks in the lane usually tell the truth before any robot ever will.

They’re strung along the driveway at a small robot barn in central Wisconsin—feed company pickups, a neighbor’s welding rig, the vet’s SUV, a church friend’s minivan. Inside, the old parlor is half‑gutted, and three new robotic milking systems sit on concrete that still looks damp. If you’re running a small or mid‑sized herd in 2024–2026 and even thinking about robots, this is your world: broken labor, big capital decisions, and a hard choice between AMS, a hybrid setup, or an exit while you’re still ahead.

This piece walks straight through that choice—the math, the decision rules, and the people around you who decide whether you’re still milking in five years or reading your own dispersal catalog.

Editor’s note: This is a composite story built from real 2023–2025 data and patterns on robot herds across Wisconsin and the Midwest—not a blow‑by‑blow profile of one specific farm. The economics and pressures are real; the names and scenes are representative.

The Labor Bomb Under a 200‑Cow Dairy

Let’s start where you actually live—at the kitchen table with a calculator and a coffee that went cold an hour ago.

By late 2023, a typical 180‑cow herd in central Wisconsin looked a lot like yours might. Margins tight. Kids in school. Parents still doing more 4 a.m. milkings than they’ll admit. And a labor situation that quietly shifted from “hard” to “not sustainable.”

A lot of herds have walked this path:

Starting milkers at USD $16/hour with housing.

Bumping to $18, then $20–22 with more flexible hours.

Edging toward $24 with a decent bunkhouse and still watching people leave for climate‑controlled warehouse jobs with weekends off and no risk of a frozen yard.

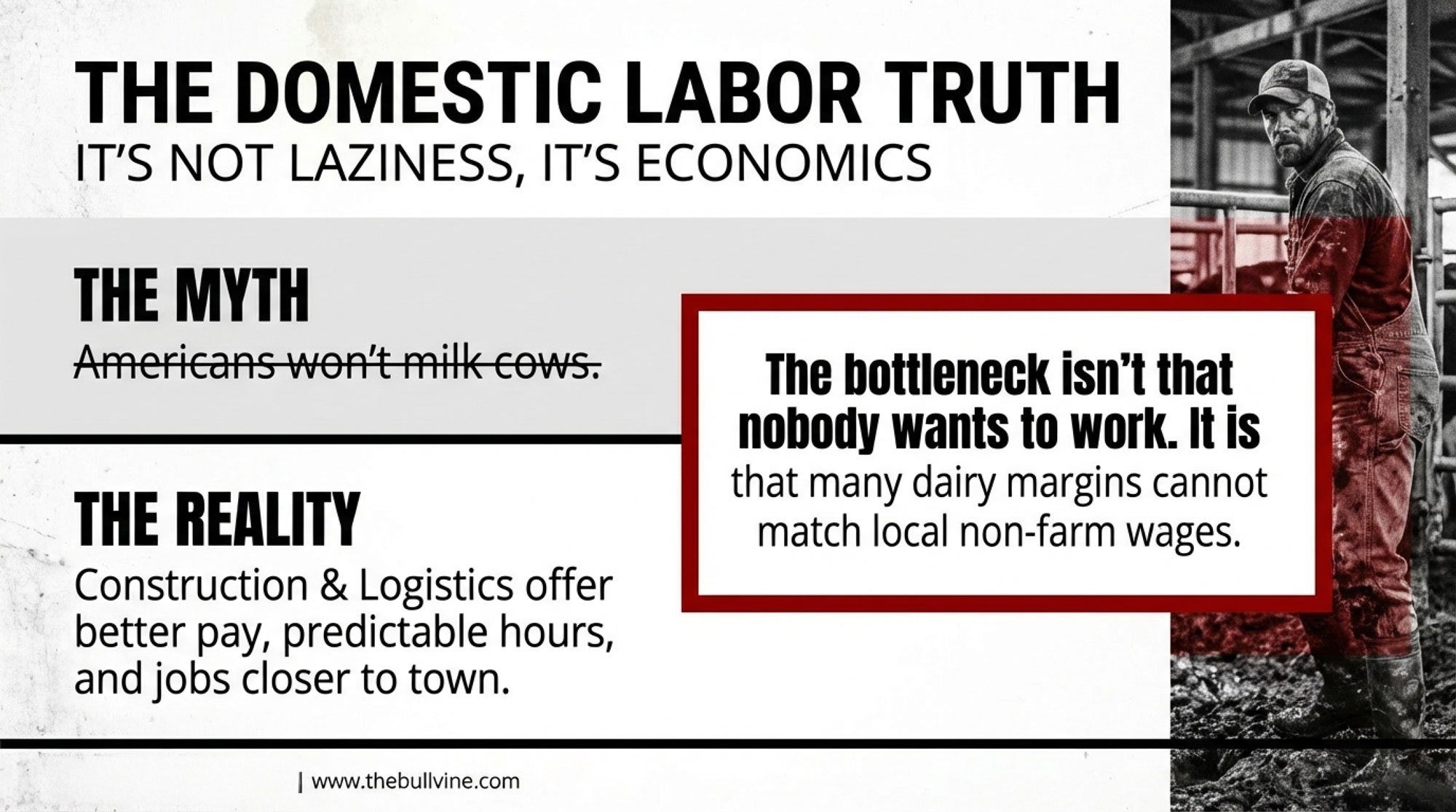

That’s not just bad luck. A National Milk Producers Federation study with Texas A&M found that immigrant workers make up about 51% of all hired U.S. dairy labor, and that farms employing them produce roughly 79% of the nation’s milk. In that same modeling work, if that immigrant workforce disappeared, more than 7,000 dairies would shut down, and retail milk prices would jump nearly 90%.

In Wisconsin, a UW–Madison School for Workers analysis—summarized in recent industry coverage—estimated more than 10,000 undocumented workers doing around 70% of the state’s dairy labor, with researchers warning that without them, Wisconsin’s dairy industry would be at serious risk of rapid collapse.

Lay that on top of herd numbers. USDA‑NASS and state data show:

16,264 licensed dairy herds in Wisconsin in 2003.

Around 6,140 herds by late 2022.

Just over 5,300 by early 2025, with cow numbers and total milk roughly holding.

Same or more milk. Fewer families. More ground to cover with fewer people.

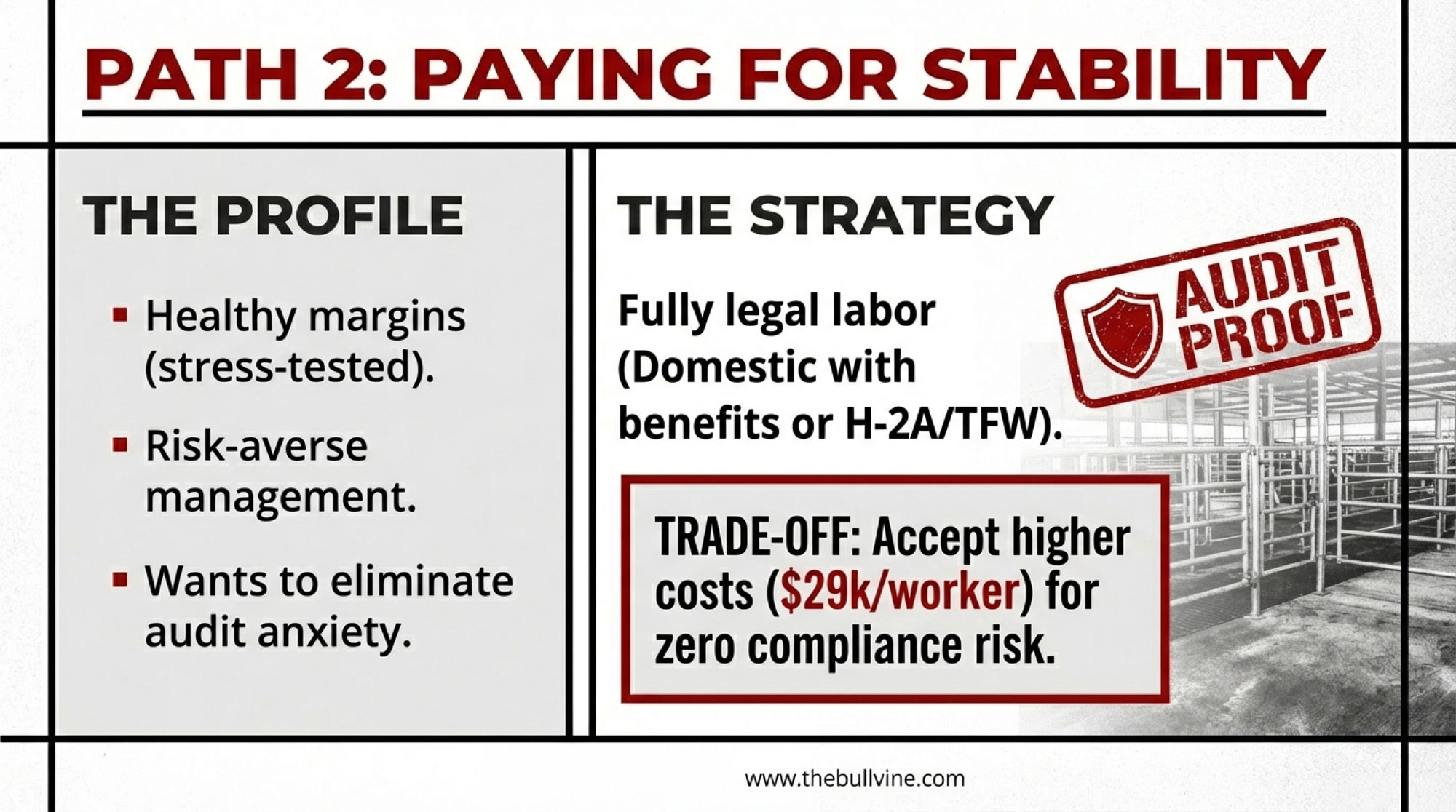

At some point, you’re down to three real options: pay legal labor what it actually costs and design your system around that, automate the hardest work, or plan a clean exit while you still have equity and energy.

Everything else is creative stalling.

The Night You Finally Say “We Can’t Keep Going Like This”

On the farms that are still breathing a few years later, the turning point is almost never a glossy robot brochure.

It’s the night someone at the table finally says, “We can’t keep going like this.”

On too many farms, that sentence dies in the kitchen. On the ones that make it, it doesn’t stay inside the house.

The smarter move we’re seeing more often now is simple but not easy: before signing an automatic milking system contract, you call the people who’ll actually be in your lane when things go sideways.

Picture a scene you’ve probably lived:

One neighbor has toured a robot barn a county over.

Another has a cousin on AMS in Ontario.

A younger dairyman down the road is “robot‑curious” but still in a double‑8.

The 4‑H leader knows half your heifers by name.

They pile into your kitchen with chili, kids, and opinions.

“We’re not sure we can do this,” you admit. “But we’re sure we can’t keep doing what we’re doing.”

On the barns that survive, that’s the moment it stops being your problem and becomes our barn.

You hear real commitments, not just sympathy:

“I’ll cover morning feeding if construction runs long.”

“We’ll shuffle concrete work so your robot pad gets poured before frost.”

“When it’s time to train cows, I’ll bring the 4‑H kids—they’re not going to forget it.”

Robots stop being a lonely, high‑risk hardware purchase. They become a community project.

You’ll hear some version of this line:

“What keeps us going isn’t just the cows—it’s the people around us.”

And that’s before a single robot milks a single cow.

The $1.2 Million Question

Now we get to the part most sales pitches slide past: the actual ROI of robotic milking.

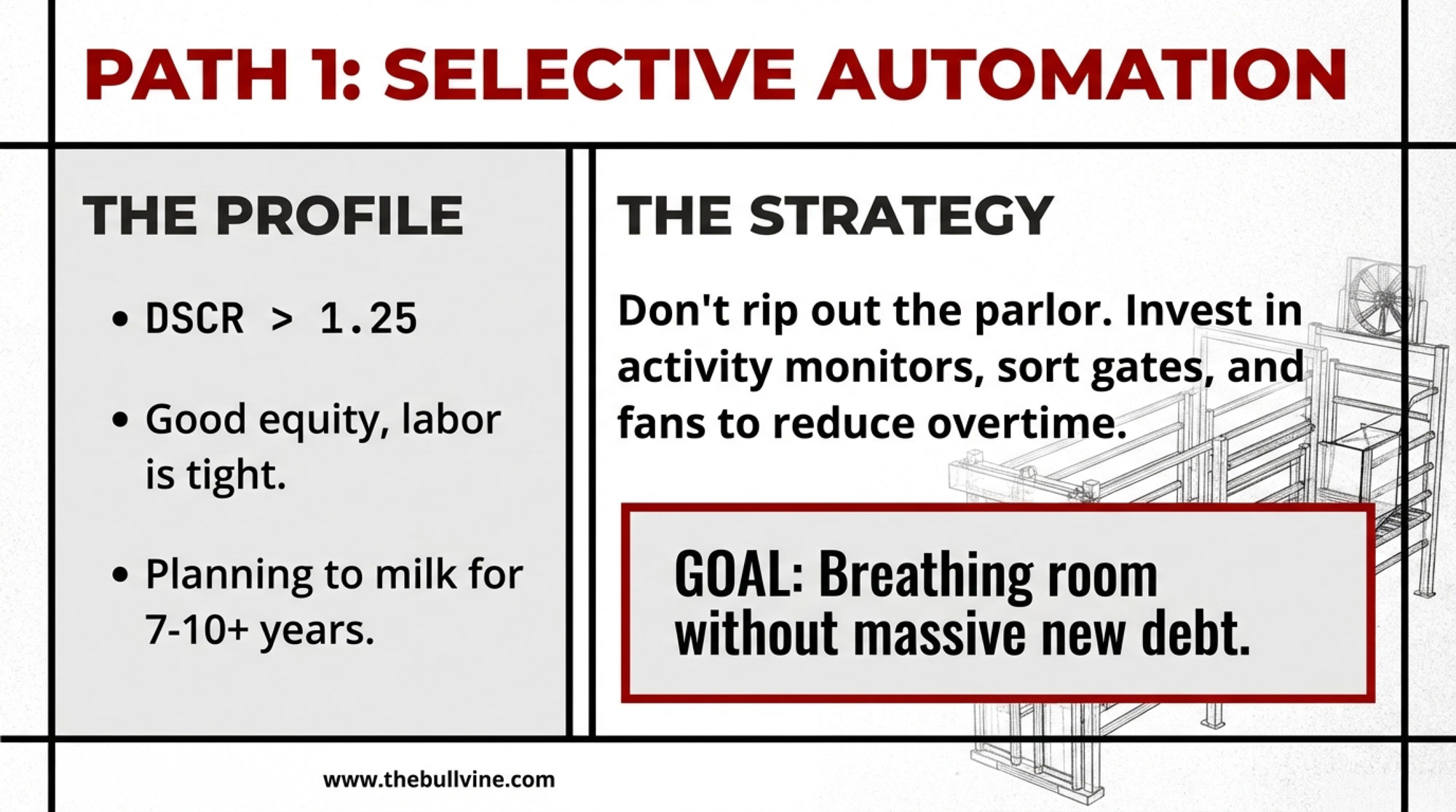

The Bullvine’s own robotics position is blunt: every robot sold under 500 cows in the U.S. is at best a dangerous luxury and at worst malpractice—unless your labor cost is insane or you literally can’t hire. That doesn’t mean no herd under 500 cows should ever go robotic. It means the automatic “yes” is gone. The default answer is “no” until your local numbers force you to “maybe.”

Here’s what typical AMS budgets look like when you strip away the sales pitch.

Capital and service costs

On small and mid‑sized herds in the Upper Midwest, 2023–2025 manufacturer quotes and independent budgets commonly put a three‑box install covering roughly 180–210 cows in the following ballpark:

Robotic milking systems + installation: roughly USD $180,000–250,000 per box, including software and accessories.

Barn modifications: often another USD $100,000–300,000, depending on how “robot‑ready” your layout is.

Put that together, and many 3‑box projects end up somewhere in the USD $800,000–1,200,000 range once the dust settles. Analysis notes that each automatic milking system can reasonably be assumed to cost about USD $200,000, including USD $15,000–20,000 in facility renovation per unit, numbers that align with these ranges.

Service doesn’t disappear either:

On many farms, service contracts, parts, and callouts can cost tens of thousands of dollars per box per yearover the life of the system, totaling hundreds of thousands of dollars over a decade.

Labor savings and milk flow

On the other side of the ledger:

University of Wisconsin–Madison Extension reports AMS herds in their sample saving around 0.06 hr/cow/day, which worked out to about a 38% drop in labor per cow and 43% per cwt—roughly USD $1.50 per cwt in labor savings at a USD $15/hour wage, with some farms reporting savings closer to USD $2.40 per cwt.

A Cornell‑led multi‑state study, cited in Bullvine’s own AMS analysis, found AMS herds cutting overall labor costs by about 21%, raising milk output 3–5 lb/cow/day, and improving milk quality metrics in roughly 32% of barns surveyed. Results weren’t universal: some herds did very well, some were neutral, and a minority struggled.

This is where your robotic milking ROI either holds or falls apart.

Here’s the hard truth on that:

If you’re paying USD $15–18/hour, and you can still hire decent milkers, robots are a tough sell on dollars alone.

Once your real, legal, fully loaded milking labor cost creeps toward USD $28–35/hour, and you’re burning out trying to keep staff, AMS stops being a toy and starts looking like a survival tool.

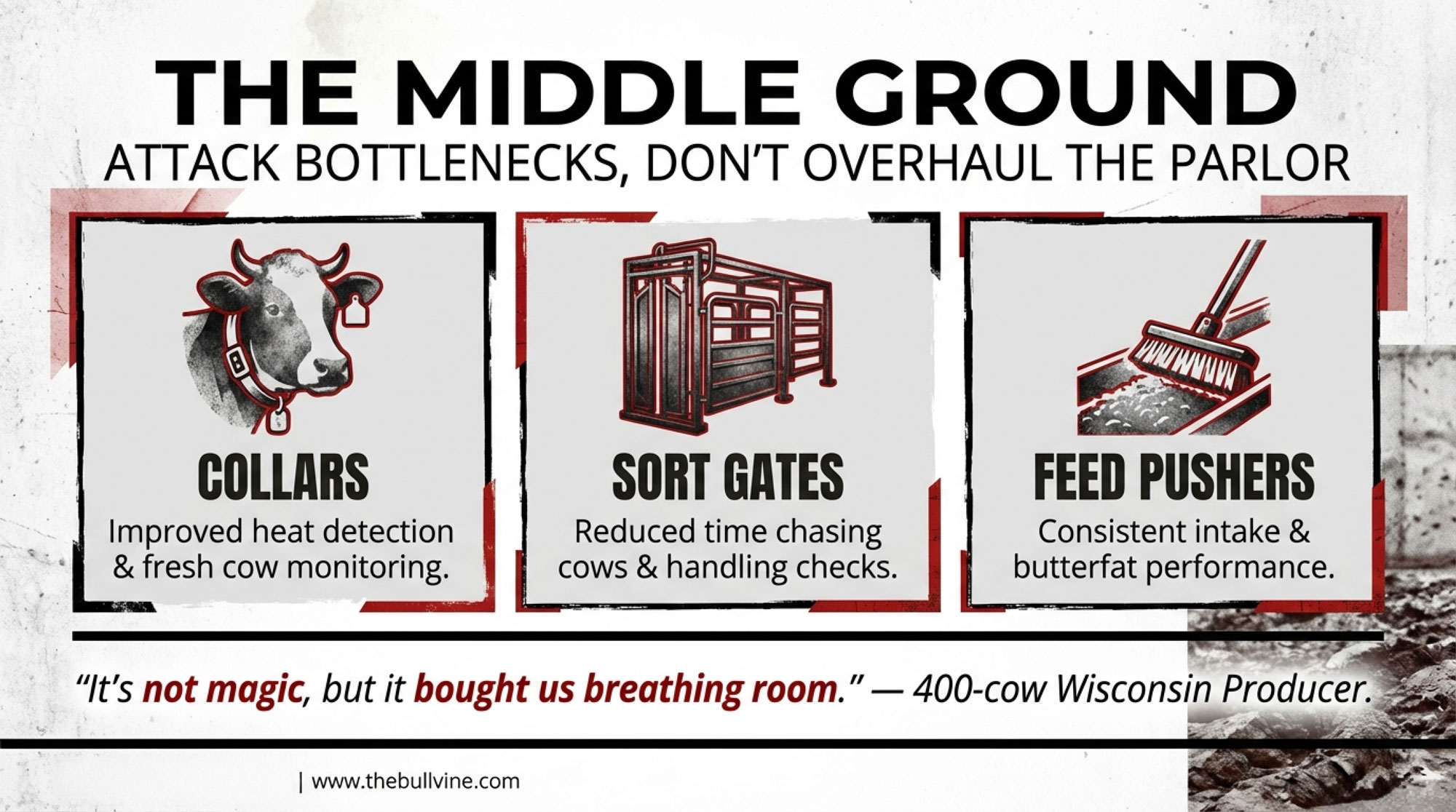

If you’re under 250–300 cows, and you haven’t squeezed the cheap levers—activity monitors, sort gates, and feed pushers—you should be very nervous about skipping straight to robots.

A simple comparison looks like this:

Option

10‑Year Capital Outlook (typical)

Labor Impact

Management Stress

Best Fit

Keep parlor, no tech

Lowest capital, rising repair cost

High, fixed shifts

High physical, high mental

Areas with relatively cheap, reliable labor

Parlor + sensors + sort gates + feed pusher

Medium capital (tens of thousands for ~180 cows, not hundreds of thousands)

20–40% labor efficiency gain

Medium (more tech, same cows)

Herds <300 cows, labor ~USD $18–25/hr

Full AMS (3 boxes, 180–210 cows)

Very high capital (USD $800,000–1,200,000 + ongoing service)

30–40% labor savings, more flexibility

Less physical, more tech and mental load

Labor USD $28+/hr or no reliable hire pool; strong management bench

That hybrid package matters. For a lot of herds in older parlors, a mix of activity monitors, a sort gate, and a feed pusher is a tens‑of‑thousands‑of‑dollars investment instead of a million‑dollar note. On herds that actually use the data and gates, that kind of setup can free up substantial milking‑related labor and tighten up heat detection and health monitoring. It won’t take you out of the pit, but it can move your labor efficiency significantly closer to AMS levels at a fraction of the capital cost—and it buys you time to decide whether you truly need robots or just a better‑designed system.

If you’re in Canada under quota with component pricing and a more stable milk cheque, the AMS payback can look different than on a volatile U.S. Class III cheque. The same basic math still applies, but your revenue line won’t whip around as hard. You still need to plug your own numbers into a milk board or advisory cost‑of‑production sheet before you buy anybody’s ROI pitch.

Here’s a test worth running quietly with your lender and accountant:

Can you hire and keep three reliable people to cover milking for USD $200,000/year or less total cost?

If the honest answer is yes, humans probably still beat robots on pure economics for most sub‑500‑cow herds.

If the answer is “no chance” and you’ve already tried, then you’re in the “AMS or exit” conversation, whether you like it or not.

And for some small or heavily leveraged herds, the most profitable move might still be an orderly dispersal while there’s equity left—not taking on a million‑dollar note because a dealer says “everyone is going robotic.”

Mentorship, Genomics, and Cow Sense in a Robot Barn

Robotic milking doesn’t change the fact that fresh cow management still makes or breaks your month, SCC still hits your milk cheque, and components still pay the bills.

It does change who is watching what.

On the best AMS herds, you see a familiar pattern with new tools:

An older generation walks pens and spots the fresh cow whose eyes are a bit dull or whose cud is slow.

The next generation pulls up the robot dashboard and shows that same cow’s milk visits, milking speed, conductivity, and rumination trend.

They argue a little, walk out together, and usually both end up half right.

A 2024 U.S. AMS study reported that many owners reported labor cost reductions of 20% or more, and many reported better control of mastitis, lameness, and reproductive problems on their farms. Many of those same farmers also said robots improved their quality of life by changing when, not just how much, they worked.

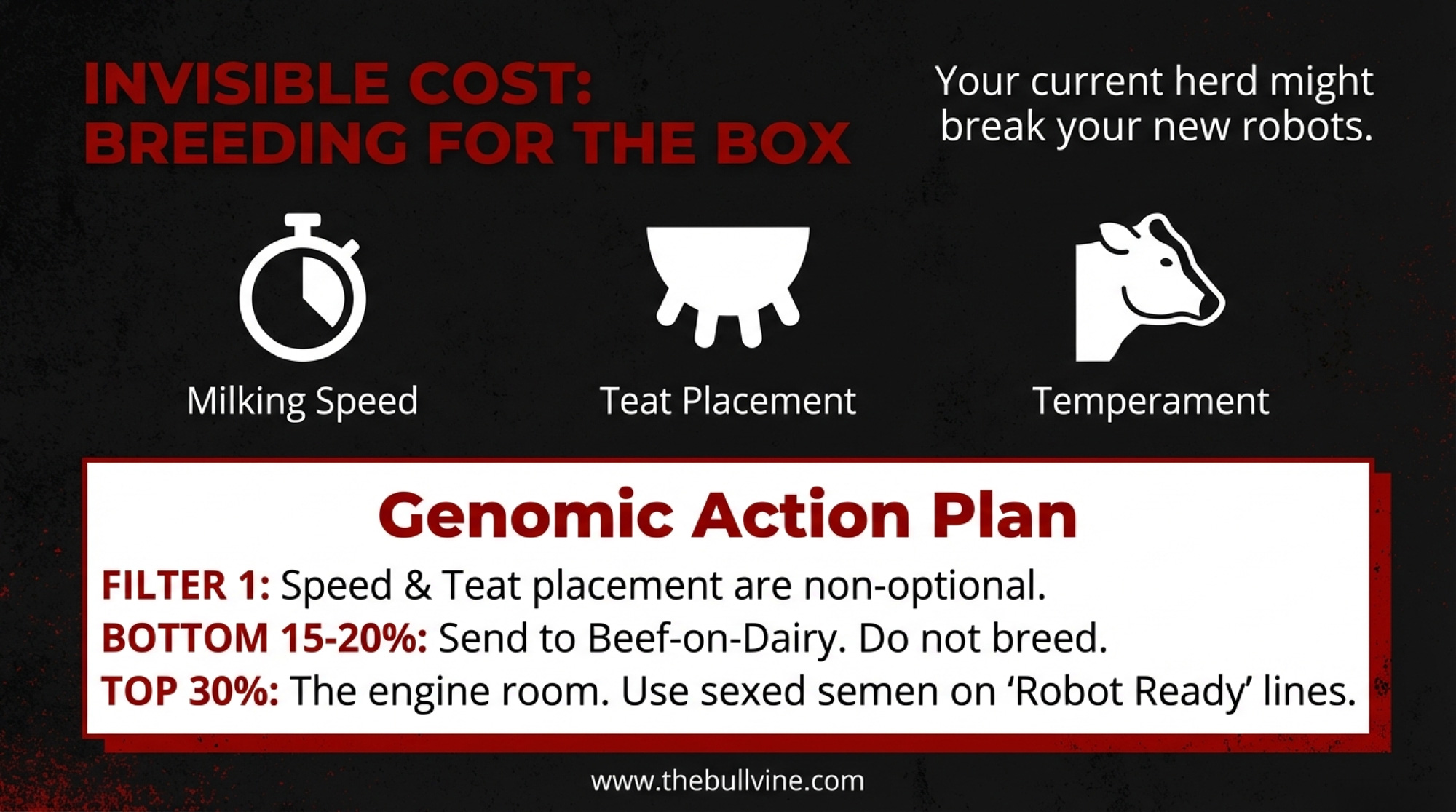

This is where genomic proofs and sire lists quietly make or break your AMS ROI.

In a robot barn, you suddenly care a lot more about:

Milking speed and temperament—slow, jumpy cows choke box capacity.

Udder attachment and teat placement—functional PTAT, not just show‑ring pretty.

Health and hoof traits that keep cows sound and productive long enough to pay off your capital.

Genomic Trait

Importance in Parlor Herd

Importance in AMS Herd

Why It Matters for Robots

Milking Speed

Medium

CRITICAL

Slow cows choke box throughput; every extra minute per cow = fewer total milkings per box per day

Still critical in AMS, but conductivity sensors catch problems faster than twice-a-day visual checks

Components (Fat/Protein %)

High (market pays you)

HIGH (market still pays you)

Higher frequency can dilute components slightly; select bulls that hold % under 3x milking

If your sire list doesn’t reflect that, you’re breeding for the wrong barn.

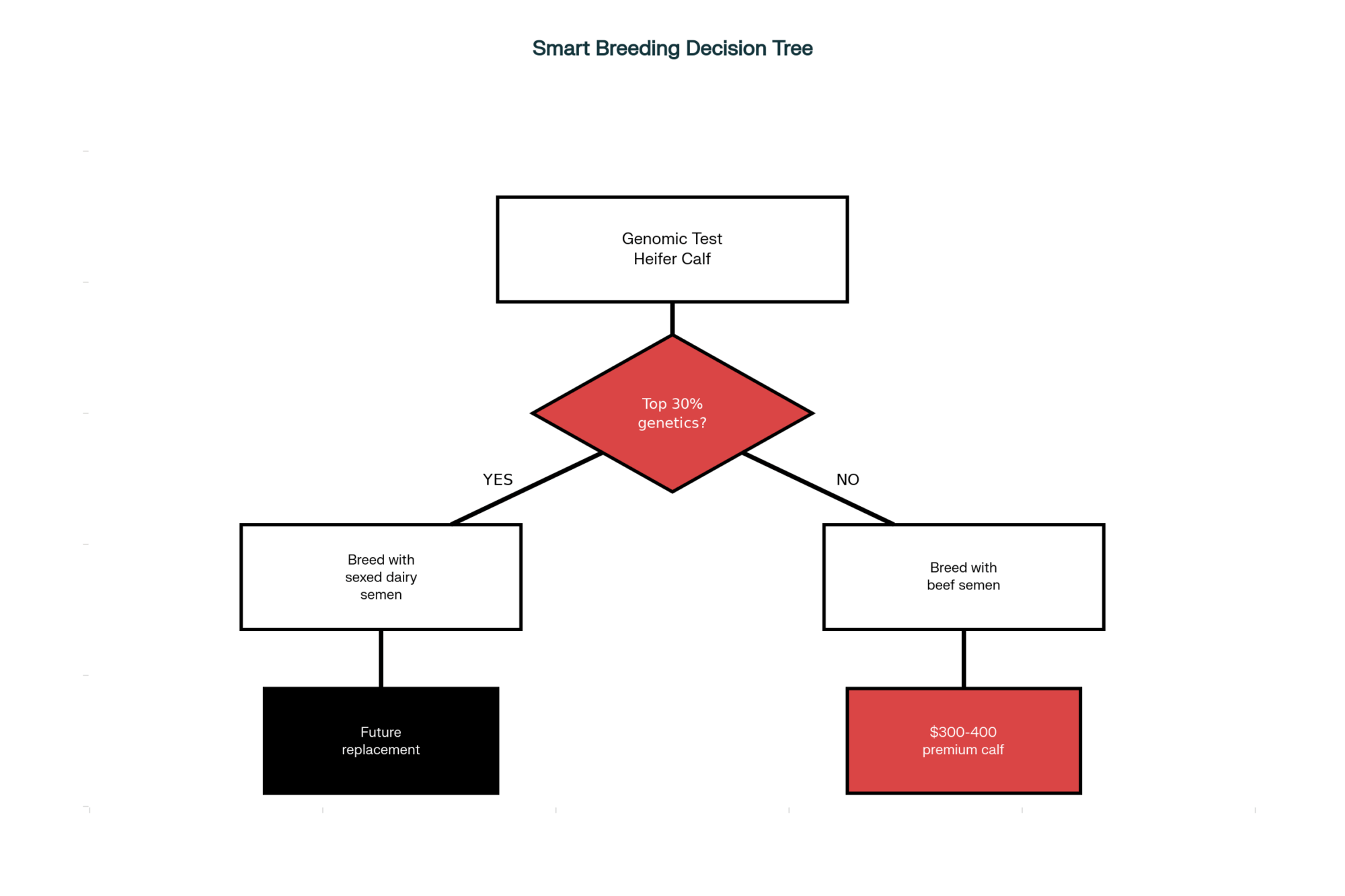

Practical steps:

Screen bulls for robot‑relevant traits—milking speed, udder depth, teat position, daughter behavior—alongside Net Merit, Pro$, or LPI, depending on where you ship.

Use genomic testing to push the bottom 15–20% of heifers straight into beef‑on‑dairy or terminal matings, not into your replacement pool.

Treat your top 30% as the engine room: sexed semen, targeted embryo work, and matings that stack components and longevity with robot‑friendly udders.

When you look at proof sheets, treat milking speed and udder traits as non‑optional filters for AMS herds, not “nice extras.”

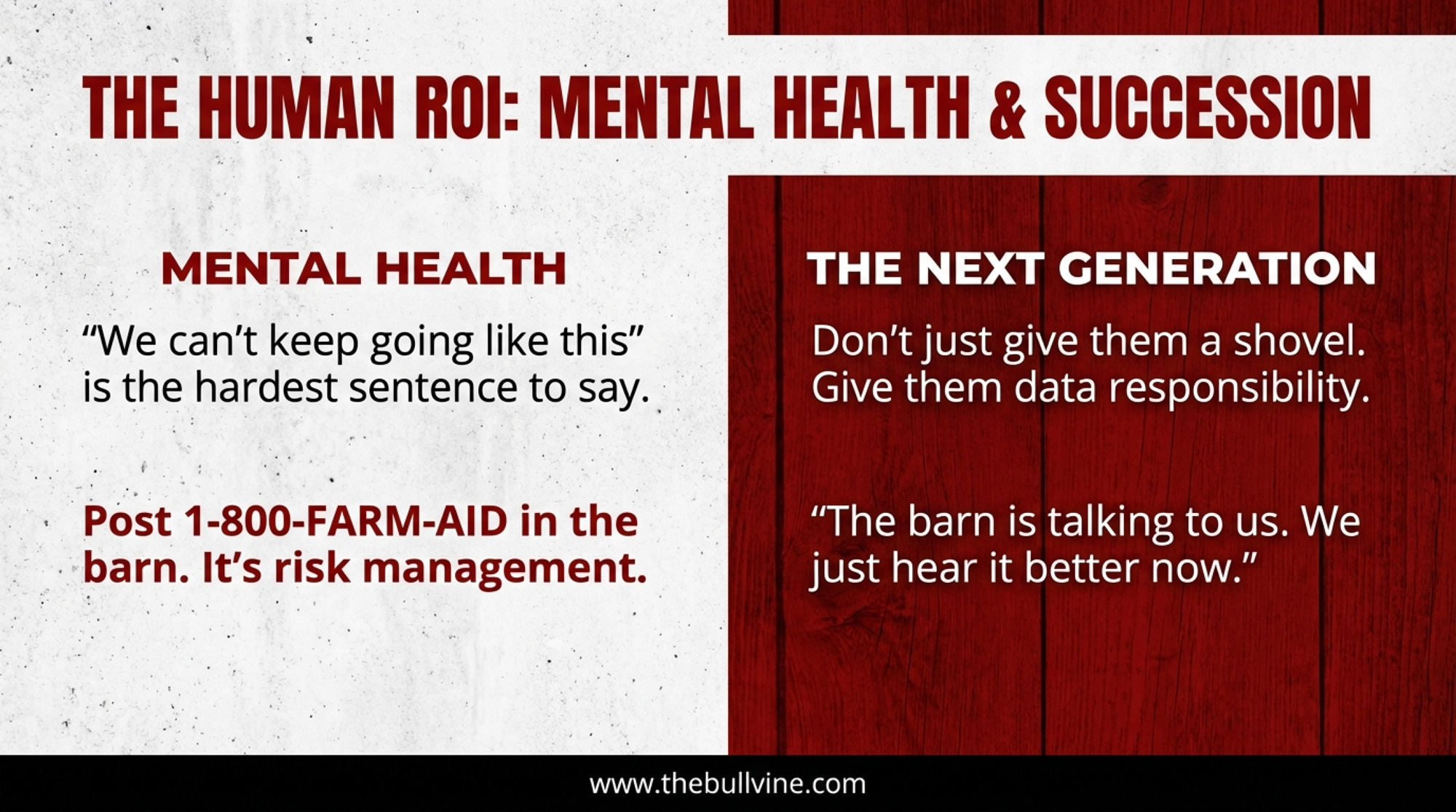

If you want the next generation actually to want the keys one day, they need more than a shovel in their hands.

Give them real responsibility:

Make a teenager or young adult responsible for one metric on the AMS or herd‑management software—SCC alerts, “red cows,” abnormal visits.

Let them sit in on breeding and culling meetings where AMS performance, genomic proofs, and fat/protein kilos actually shape decisions.

Ask what they see in the data that you’ve been feeling in the barn.

One young producer on an AMS herd put it this way to her grandfather: “The barn’s talking to us all day now.” His reply was simple: “It always was. We just hear it better now.”

Storms, Blackouts, and Who Backs a Tractor Up to Your Panel

Six months after startup, the real test on a lot of robot barns isn’t software.

It’s a thunderstorm.

A fast‑moving cell rips across the township. Trees down. Lines down. One minute, the robot room hums; the next, it’s dead. Vent fans are silent. Lights gone. Cows are mid‑cycle and starting to wonder what’s wrong.

This is where you find out if you bought machines or built a support system.

On the barns that get through nights like this without permanent damage to cows, people, or cashflow, you see the same pattern:

Within fifteen minutes, headlights swing into the yard.

One neighbor backs a tractor‑driven generator up to the panel like he’s done it twenty times.

Another shows up with portable lights and coffee.

A cousin‑electrician arrives with a headlamp and a coil of wire.

By the time the power company truck finally grinds in, the robots are already milking again. Cows are agitated but under control. Everyone is wiped. But nobody is arguing about whether automation “was the right call” anymore—because the real question was never robots vs parlor.

It was: “When the barn goes dark, who turns up your lane?”

If you can’t answer, right now, whose tractor is backing up to your panel, who milks if you land in the hospital, and who you call first in a disease outbreak or barn fire, that’s not a theoretical risk.

That’s a hole in your survival plan.

The Hardest Sentence in the Barn: “We Can’t Keep Going Like This”

We’ve all seen the mental‑health headlines. Too many of us know the families behind them.

Farmer stress and mental health aren’t side topics anymore. They sit right in the middle of whether your barn is still lit five years from now.

It’s bad enough that national and regional groups have put serious resources behind it. The Farm Aid Hotline (1‑800‑FARM‑AID) provides confidential assistance to farmers in distress or crisis, connecting them to financial, legal, and mental‑health resources. States and provinces now maintain ag‑specific counsellor lists and crisis lines. Farm organizations quietly slip those numbers into meetings and newsletters.

Robots don’t fix that. A USD $1 million AMS note and a constant stream of alerts can make your head even louder.

On the farms that actually get healthier, there’s almost always a moment before anyone signs a contract when someone finally says:

“We can’t keep going like this.”

Short‑staffed. Watching neighbors sell out. Lying awake, wondering whether your kids will resent you more for selling now or handing them a mess in ten years. Afraid that saying it out loud means you’ve failed.

On the barns that make it through, people around them don’t accept “we’re fine” as an answer.

Common patterns:

A neighbor couple shows up most Sunday evenings during the transition, not to critique cows but to ask, “What went a little better this week? What’s still chewing on you?”

Vets and nutritionists leave mental‑health resource cards by the computer and say plainly, “These are here for anyone on this farm. Including you.”

Pastors, teachers, and coaches with farm roots stop by during chores, not to preach, just to sit at the table and listen.

When those farmers look back, the line that sticks isn’t about robots.

It’s some version of:

“The moment that changed everything wasn’t when the robots started. It was when we realized we didn’t have to pretend we were fine anymore.”

If you’re serious about staying in dairy, this isn’t fluff. It’s risk management. Cows don’t care how tough you are. Your family and your lenders care very much that you’re still here.

The 4‑H Calf That Keeps a Kid – and a Farm – Connected to Dairy

Every county has a story that quietly explains why community still matters.

A quiet kid drifts into a 4‑H dairy club meeting. No farm background. New boots, still clean. Home life? Let’s just call it complicated.

A local dairyman offers him a calf from his herd for the summer. Nothing out of the World Dairy Expo showstring. Just a decent heifer with a kind eye and a shot at VG down the road if things line up.

All summer, that calf gives him a reason to get up and go somewhere safe twice a day. He learns to halter, to brush, to read her moods. When she walks into the robot for the first time, he’s there with a hand on her flank, talking her through the new noise and the spray.

At the fair, they land squarely in the middle of the class. You’d think they’d just won the Supreme.

Fast‑forward a couple of years, and that “quiet kid” shows up as:

A part‑time worker at a dairy down the road.

A student in an ag or ag‑tech program.

The older 4‑H’er is clipping calves and teaching younger kids how to lead a heifer without panicking.

Ask what changed his path, and he’s not going to say “robot model numbers” or “Net Merit.”

He’ll tell you, “Somebody trusted me with something that mattered.”

If you want to talk long‑term herd strategy and genetics, that’s it in one sentence. Your best cow families and proofs don’t mean much if there’s nobody young who wants to be under those cows when they calve, milk, and show.

Robots and genomics might keep your herd competitive.

Kids and the community keep it alive.

What This Means for Your Operation

This isn’t a feel‑good Hallmark story. It’s a survival checklist.

If you’re reading this with a knot in your stomach, you’re exactly who this section is for.

Run Your Robot vs Human vs Hybrid Math in $/cwt

Sit down with your lender and accountant and write it out:

Calculate your real milking labor cost per hour—wages, housing, benefits, turnover, and your own unpaid time. Convert that to $/cwt using your shipped volume.

Get a real AMS quote: equipment, barn modifications, and at least 10 years of service contracts.

Price out a serious hybrid package—activity monitors, sort gates, and a feed pusher. For many 180‑cow herds, that’s a tens‑of‑thousands‑of‑dollars investment, not a million‑dollar note.

Work out your projected $/cwt labor cost for “keep the parlor,” “parlor + tech,” and “full AMS” at five and ten years. If you’re not sure how to do that, ask your lender or extension adviser to walk you through it.

Then ask yourself:

Can I hire and retain three reliable people to cover milking for a total cost of USD $200,000/year or less?

If yes, humans still likely beat robots on pure economics for most sub‑500‑cow herds.

If no, you’re in AMS‑or‑exit territory and need to treat this like the survival decision it is—not a gadget purchase.

If AMS debt would push your total farm debt service well beyond your historic cashflow comfort zone, a clean, profitable exit or a smaller hybrid investment deserves a serious look.

Build a Three‑Farm Emergency Ring

Before the next storm, disease outbreak, or health crisis:

Sit down with two or three nearby dairies.

Agree on who brings the tractor‑driven generator, who understands your panel, and who will show up if you’re suddenly out of commission.

Swap cell numbers, gate codes, and panel details now, not at midnight in a blizzard.

Write it down and post it in the office and on at least one truck.

If you don’t know whose tractor is backing up to your panel, that’s the first hole to patch.

Put Mental Health on the Wall

Take ten minutes and:

Print the Farm Aid hotline (1‑800‑FARM‑AID) and any state/provincial ag mental‑health numbers you can find.

Tape them where people actually look—office fridge, milk house door, robot room.

Tell your family and crew once, “If you ever feel like you can’t keep going, you can talk to us—or you can call these numbers. Both are okay.”

It’ll feel awkward. Do it anyway.

Make Youth Part of Real Decisions, Not Just Photo Ops

If you want someone to care about your herd in 2035, give them work that matters in 2026.

Hand a teenager or young adult a login to your robot or herd‑management software and make them responsible for one metric—SCC alerts, irregular visits, “problem cows.”

Let them sit in on some breeding and culling discussions where AMS performance, genomic proofs, Net Merit/Pro$/LPI, and component performance actually shape the choices.

Put a 4‑H calf or a small project in the hands of one non‑family youth and let them earn your trust.

You’re not just filling labor gaps. You’re building your successor pool.

Tie Genetics Directly to the System You Actually Run

Your sire list should match the barn and milking routine you have now, not the one you had ten years ago.

On AMS herds, prioritize bulls with milking speed, balanced udders, good teat placement, and sound feet and legs alongside components and fertility.

Use genomic tests to push the bottom 15–20% of heifers toward beef‑on‑dairy or terminal matings, protecting your replacement slots for daughters who fit your system.

Treat your top 30% as the cow families that will carry your prefix forward: stack them with sires that fit your milking system, labor realities, and market.

If you’re paid on butterfat and protein, give extra weight to sires whose daughters hold components under higher milking frequency.

If you’re still using bulls that made sense for a twice‑a‑day tie stall in 2008, you’re breeding for nostalgia, not for the farm you’re trying to keep alive.

Key Takeaways

Robots don’t replace neighbors. They raise the stakes on having the right people in your corner when things go sideways.

Under 500 cows, AMS isn’t an automatic yes. If you can still hire and keep good milkers at an honest wage, a hybrid “parlor + tech” setup often delivers most of the benefits at a fraction of the cost.

Your labor market decides more than your dealer does. If you genuinely can’t staff your barn, robots may be the lesser risk—but only with a strong community and management bench behind them.

Genetics has to match your system. Milking speed, udder design, health, and hoof traits become expensive blind spots in a robot barn if you ignore them.

Mental health isn’t soft. It’s a leading indicator of whether your family and business will still be here when the next price cycle turns.

Youth and 4‑H aren’t side projects. They’re your succession plan, your future labor, and the bridge that keeps your best cow families relevant in 20 years.

The Bottom Line

In a world where Wisconsin has dropped from over 16,000 herds to just above 5,300, and immigrant labor holds up half of the hired workforce that keeps the milk flowing, the real question on your farm isn’t “robots or parlor.”

It’s a lot simpler, and a lot harder:

If things go sideways tonight, who is actually turning up your lane?

If you don’t have a clear answer, that’s your real project this year.

Robots might help you milk.

Your people are the reason you’ll still be here to push “start” tomorrow.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The $1750 Calf: Is Your 2026 Breeding Plan Leaving $800 a Head on the Table? – This breaks down how to weaponize genomic data to capture massive beef-on-dairy premiums. It delivers a surgical breeding method that turns surplus pregnancies into a second, high-margin revenue stream that significantly outpaces commodity milk income.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Breeding 14,000 kg Holsteins but milking them in a 9,000 kg barn? Your genetics can’t outrun bad concrete.

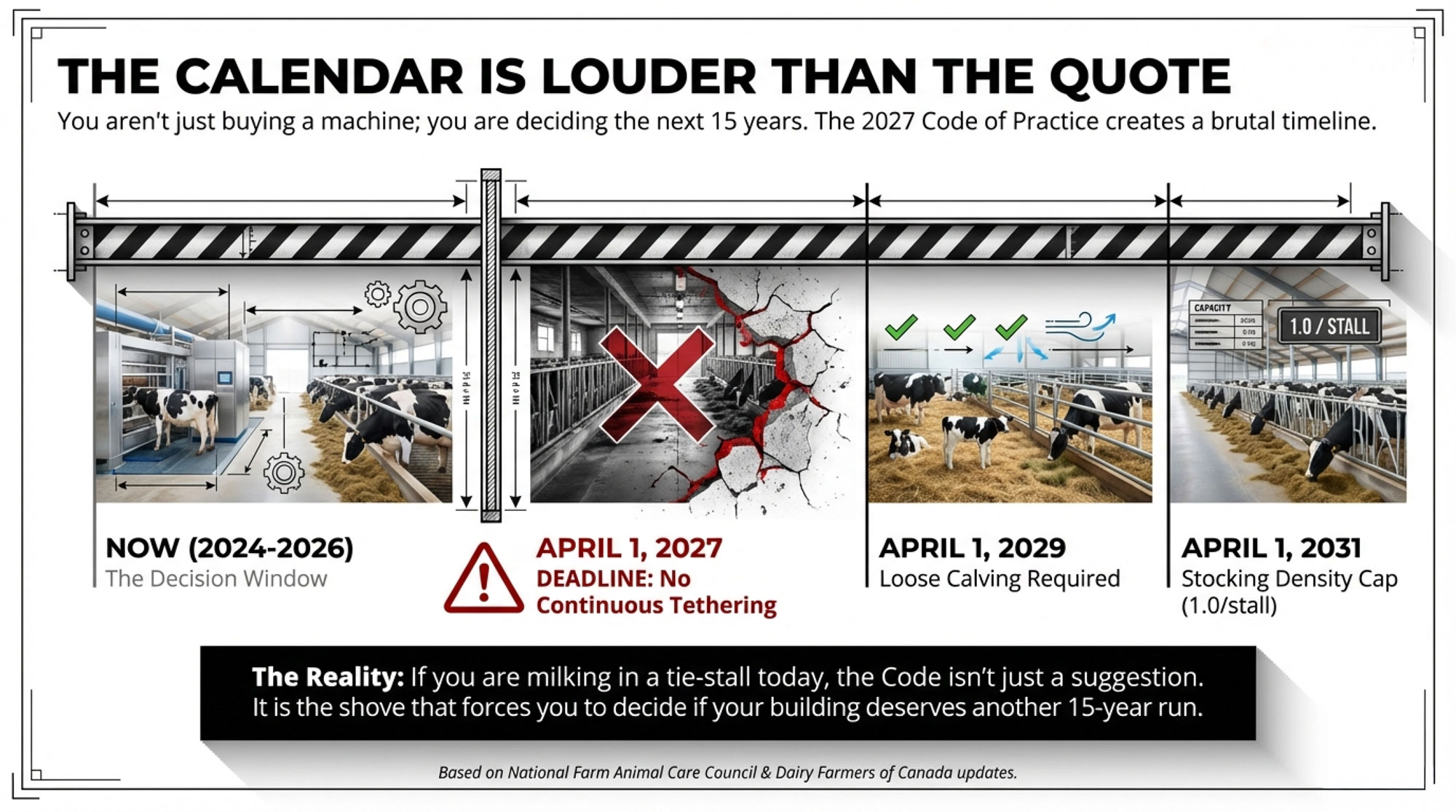

Executive Summary: Canadian tie‑stall herds are heading into the 2027 Dairy Code with a brutal choice: spend roughly $480K on a retrofit or about $1.48M on a new robot barn for 60 cows. The article shows why the cheapest quote often isn’t the best bet once you price in cow‑flow, ventilation, fetch time, and mid‑life “correction” projects that can add $75,000–$100,000 back onto a tight retrofit. Using current Canadian Holstein averages — 11,364 kg in 305 days at 4.15% fat and 3.36% protein — it walks through how even a 5% drop in performance and an extra 275 hours of fetching per robot per year can erase a $200K saving over 15 years. Producers get three clear paths: minimal Code‑compliant upgrades to buy time, a serious long‑term retrofit for barns with good bones, or a full new robot barn for growth‑minded, multi‑generation herds. Along the way, it ties barn design back to labour, succession, and the ability to actually express the 14–15,000 kg Holstein genetics many Canadian breeders are already paying for. The core takeaway is simple: start your AMS decision with the building and your 15‑year horizon, or risk locking your robots—and your genetics—into bad concrete.

Here’s the picture. It’s a cold January morning in an older 60‑cow tie‑stall. The pipeline’s humming, the concrete’s polished from years of hooves and boots, and you’ve got a robotic milking quote on the table that says you can “go automated” for about $17,000 less per cow if you retrofit instead of building new. On paper, that looks like the easy choice.

But the calendar is louder than the quote. As of April 1, 2027, Canada’s updated Dairy Code of Practice says cows in existing barns can’t be tethered continuously through their production cycle anymore. Not long after that, new rules land for loose calving and stocking density, all while you’re staring at a seven‑figure gap between the cheapest retrofit and a purpose‑built robot barn — plus your own body, your family’s future, and your quota investment. If you’re milking in a Canadian tie‑stall in 2024–2026 and thinking about robots, you’re not just buying a machine. You’re deciding what kind of barn — and what kind of life — you want for the next 15 to 20 years.

The New Code, Real Money, and Real Cows

Recent Canadian analysis of automated milking system (AMS) costs after tie‑stalls pegs a green‑site robotic facility at about $24,718 per cow once you factor in everything. That breaks down to roughly $6,800 per cow for the milking equipment and $10,700 per cow for the barn and core infrastructure, plus handling, feed storage, and manure systems. For a 60‑cow herd, you’re looking at roughly $1.48 million tied up in that project.

In a retrofit, the robot cost doesn’t change much. A single box typically runs in the $150,000–$220,000 range and realistically serves about 55–60 cows, with a working life of 7-15 years, depending on usage and maintenance. The savings show up when you reuse concrete and steel that are already in the ground. In some Canadian retrofit case studies, the total invested cost is closer to $8,000–$14,000 per cow once you upgrade floors, ventilation, and electrical systems, while keeping the shell. On a 60‑cow herd, that’s roughly $480,000–$840,000.

Now add the Code pressure. The 2023 Dairy Code of Practice update — released by the National Farm Animal Care Council and rolled into Dairy Farmers of Canada’s timelines — lays out three big structural dates:

By April 1, 2027, cows in existing barns must not be tethered continuously throughout their production cycle.

By April 1, 2029, all calving must take place in loose housing that allows cows to turn around — pens, yards, or pasture — not in a tie‑stall.

By April 1, 2031, stocking density in freestall systems must not normally exceed 1.0 cow per stall, stepping down from earlier allowances of 1.2 then 1.1 cows per stall.

At the same time, reporting around the Code notes that nearly two‑thirds of Canadian dairy farms still use tie‑stall housing. Some of those barns already provide turnout or loose housing that help meet the new “freedom of movement” requirement, but there’s no national count of how many. If your barn is tired, your body’s tired, and you’re looking at robots anyway, the Code isn’t just a welfare document — it’s the shove that forces you to decide whether that building really deserves another 15‑year run.

You’re not just weighing a robot quote. You’re deciding whether to bolt a complicated, very expensive piece of automation onto something that might already be past its best‑before date — and how much that’s going to cost you in labour, milk, and sanity down the road.

Same Robot, Two Very Different Barns

What producers keep finding is pretty simple: the robot almost never lets you down. The barn design does.

Think about one of the better retrofits you’ve toured.

You walk into the old tie‑stall, and the first thing you notice is space. The family bit the bullet, dropped from 90 milking cows to around 60, and made the building fit one robot instead of trying to squeeze two into a footprint that couldn’t handle it. They tore out a row of stalls to carve out 15 to 20 feet of open approach in front of the robot, gave cows a clean exit lane that leads straight past fresh water, and built a small but functional separation pen for fresh, lame, and “special” cows.

Ceiling height is 10–12 feet instead of a tight 8. The foundation and posts checked out structurally, and there’s enough sidewall height to hang curtains and install big fans without blowing air into the beams instead of the cows. They didn’t try to force guided cow traffic into a shoebox. They went with free‑flow, grooved and leveled the floors so cows weren’t skating, and gave cows reasons to walk past the robot on their own — feed, water, and an easy path.

Startup was still messy — every AMS startup is. But once cows and people settled, fetch time landed in the “normal” range you see out of AMS field data: roughly 45–60 minutes per robot per day, depending on stage of lactation and season. Fetching is still work, but it feels like the system is on your side.

Now picture another barn you’ve walked into, where the quote looked great and the robot “fit” on paper.

The box is shoved into an end wall because that’s where it was easiest to cut concrete. There’s one narrow alley, maybe 8 feet wide, leading to it with a sharp corner around a post. Dominant cows love to stand there, blocking timid heifers and fresh cows. There’s no real waiting area and no proper separation pen because no one wanted to give up stalls. It technically fits. Practically? It’s a choke point.

Research on automatic milking systems has documented fetch time per robot anywhere from 5 minutes to 120 minutes per day, heavily influenced by barn layout, stocking density, and cow traffic design. In herds with bottlenecks like that second barn, the fetch list never really shrinks. In at least one AMS cow‑traffic study, increasing stocking density by just over ten percentage points made cows roughly one‑and‑a‑half times more likely to end up on the fetch list. That’s the difference between a quick pass through the barn and another hour and a half of “come on girl, let’s go.”

Ventilation amplifies it. When robots and robot rooms are tucked into sidewalls without thinking about inlets and outlets, they can block the main curtain area. Work using Canadian Holstein data and climate records has shown that heat stress hits production and components well before cows are visibly panting, especially in barns with weak air movement. In a retrofit where the robot approach is the hottest, stalest air in the barn, you’re literally asking cows to walk into a sauna to get milked. They’re not going to volunteer.

Component

Good Ventilation (Well-Designed)

Weak Ventilation (Compromised Retrofit)

Difference

Butterfat %

4.15%

4.00%

−0.15%

Protein %

3.36%

3.26%

−0.10%

Same robot. Two very different barns. And completely different lives for the cows and people inside them.

Metric

Good Layout

Compromised Layout

Difference

Daily fetch time per robot

45 min

90 min

+45 min

Annual fetch hours per robot

274 hrs

549 hrs

+275 hrs

Labour cost per hour (loaded)

$30

$30

—

Annual fetch labour cost

$8,220

$16,470

+$8,250

15-year cumulative labour cost

$123,300

$247,050

+$123,750

The Barn‑Design Math You Don’t See on the Quote

Here’s where the “cheapest option” can quietly turn into the most expensive barn you own.

For a 60‑cow herd, using the Canadian cost work above as a guide, the three basic options look like this:

Full new robotic build: About $24,718 per cow in total → roughly $1.48 million. Clean‑sheet layout, designed cow flow, new manure and ventilation systems.

Strategic retrofit with proper upgrades: Around $14,000 per cow → roughly $840,000. Serious spend on floors, air, robot area, and separation, but within the old shell.

Minimal retrofit (robot dropped into existing layout): As low as $8,000 per cow → roughly $480,000. Robot, basic wiring and plumbing, but little to no change to alleys or ventilation.

If you stop there, minimal retrofit wins every time. That’s why so many kitchen‑table conversations end at the quote.

But AMS economics don’t end at installation. They run for over 10–15 years.

AMS comparisons from several North American and European extension projects have reported labour savings of roughly 10–29%, depending on herd and system, when cow flow and stocking match the robot’s capacity. That’s the upside.

On the downside, the gap between a barn fetching 45–60 minutes per robot per day and one fetching 90–120 minutes per robot per day is enormous. If your retrofit ends up on the wrong side of that line, you’ve effectively given yourself a permanent labour tax:

Roughly 275 extra hours per robot per year of fetch time when you jump from 45 to 90 minutes a day.

At roughly $25–$35 per hour for fully loaded labour on many dairy farms today, that’s about $6,875–$9,625 per robot per year just to drag cows to the box.

Production is the other quiet killer. Recent Canadian Dairy Information Centre data show Holsteins averaging 11,364 kg in 305 days, 4.15% fat, and 3.36% protein in 2024. If a compromised layout and heat load cost you even 5% of that potential, you’re giving up around 570 kg of milk per cow per year, plus components. On 60 cows, that’s over 34,000 kg of milk a year gone.

Stretch that over a 15‑year robot life, and the real cost of that “cheap” retrofit starts to show itself. A project that saves a couple hundred thousand dollars on day one can easily give that back — and more over 15 years — through extra labour, lost milk, and the kind of “year eight correction” AMS designers warn about.

That correction cheque usually shows up when the compromises you thought you could live with stop being tolerable: tearing out and re‑pouring the main alley, moving a robot that was jammed into the wrong corner, cutting new curtain openings, or finally building the separation pens you knew you needed from day one. In some retrofits, those correction projects can easily reach$75,000–$100,000.

So you’re not really choosing between a $480,000 retrofit and a $1.48 million new barn. You’re choosing between:

A cheaper‑to‑build, potentially more expensive‑to‑operate barn that could lock you into chronic labour and production penalties.

A more expensive‑to‑build facility that, if designed right, is cheaper and saner to live with for the next 15–20 years.

Year

Minimal Retrofit

Strategic Retrofit

New Robot Barn

0

$480,000

$840,000

$1,480,000

5

$590,000

$920,000

$1,520,000

10

$730,000

$1,020,000

$1,570,000

15

$900,000

$1,140,000

$1,630,000

New construction isn’t automatically “right.” For some herds, the capital hit and land base requirements make it a non‑starter. But if you’re only looking at the quote and not the 15‑year picture, you’re flying blind.

Quick Comparison: Retrofit vs New Robot Barn

A lot of this comes down to how much risk you’re willing to carry — and for how long.

Path

Typical Investment (60 cows)

Labour Relief

Best For

Biggest Risk

Minimal Compliance(No Robot)

$50K–$150K(loose pens, ventilation, turnout)

None

<10 yrs to retirement, no successor, tight capital, already offer turnout

Cutting corners on air/flow turns it into a bridge you never leave

Bridge Retrofit(Robot Now, New Barn Later)

$480K–$600K(clean one-robot setup)

Moderate(temporary)

Next generation committed, need relief now, capital for Phase 2 coming

Bridge quietly becomes destination—Phase 2 never happens

Purpose-Built Robot Barn

$1.48M (clean-sheet design)

High (best layout)

Growth-minded, multi-generation, want 15–20 yrs of good cow-flow

Highest upfront cost—requires strong balance sheet and land base

Three Realistic Paths Between Now and 2027

If your tie‑stall barn still has decent bones, you’re not stuck between “retrofit now” and “build new now.” In practice, most serious Canadian producers are landing in one of three lanes.

Path A: Minimal Compliance, Maximum Optionality

This lane says, “I’ll get Code‑compliant by 2027, but I’m not ready to bet six or seven figures on robots yet.”

It fits when you already give cows turnout or pasture, or have loose pens for dry and close‑up cows, so you’re not continuous tethering today. It also fits when there’s no clear successor, or you’re within 10–12 years of stepping back. And it fits when debt capacity is tight, and a $500,000–$1 million project would stretch things uncomfortably.

On this path, you focus on making freedom‑of‑movement time real and defensible, upgrading or adding loose maternity pens well before the April 2029 deadline, and fixing obvious stall, bedding, and ventilation issues within your tie‑stall footprint to protect comfort and longevity. You watch AMS tech and neighbour experience, so when you do make a move, it’s on your terms—not because you panicked.

The trade‑off is straightforward: you guard flexibility and your balance sheet, but you don’t ease the daily labour grind much. If your body’s already telling you you’re done with twice‑a‑day pipeline milking, this path buys time — not relief.

Path B: Strategic Retrofit as Your Long‑Term Barn

Path B is for when you look at your barn and honestly say, “She’s got another 15 years in her — if we don’t cut corners.”

It fits when a structural engineer has reviewed the foundation, posts, and roof and given you the green light for robot pads and ventilation upgrades. You can carve out 15–20 feet of clear approach in front of the robot, plus a clean exit lane and at least one functional separation pen. Ceiling height is closer to 10–12 feet than 8, or you’re committed to opening up low loft space to gain headroom. Once you’ve made room for cow flow and separation, your stall count still matches realistic robot capacity — about 60 cows per box, not 80 or 90 forced through. And you don’t see yourself doubling cow numbers in the next decade.

Here’s where it gets uncomfortable: you may have to drop from 90 cows to 60. That means less quota in the main string and, on paper, less milk shipped. But if those 60 cows are closer to their genetic potential in a barn that flows, with a robot that isn’t choking on overstocking, your dollars per cow and dollars per labour hour can look a lot better than fighting 90 in a compromised setup. Run the margins both ways before you decide.

If you choose this lane, you have to mean it. Floors, air, cow‑flow, and separation are the engine room of your AMS system. If that’s where you decide to save money, you’re setting your future self up to write that correction cheque and wonder why you didn’t do it right the first time.

Here’s a rough rule of thumb barn planners talk about: if your strategic retrofit budget is climbing past about half of what a new barn would cost and you’re still compromising on cow flow and air, that’s your cue to run full‑build numbers side by side seriously.

Path C: Retrofit as a Bridge to the Next Barn

This lane is for families where the next generation is coming home, but the timing and capital for a full new build aren’t there yet.

It works when the current operator needs physical relief now — backs, knees, and shoulders are sore from tie‑stall milking. The next generation is committed to staying in dairy and sees future growth in cow numbers or robots. The existing tie‑stall can be turned into a solid one‑robot, 60‑cow barn with honest upgrades, but everyone agrees it’s not the 2040 barn.

Here, you retrofit cleanly for one robot and about 60 cows with good cow flow and air, knowing this is Phase 1. You use this barn as your AMS training ground — learning how your cows behave in free‑flow, how to manage data, feed tables, and alarms. You start planning the new build right away: land base, manure storage, feed layout, number of robots, and cow capacity. And you put a real-time frame on Phase 2 (even if it’s a range like 2030–2033) and build your capital plan around it.

The risk? The bridge quietly becomes the destination. A few years in, payments feel normal, the worst of the old problems are gone, and the push for a purpose‑built barn fades. That’s how you end up a decade later, still in a building you meant to use “for a while,” staring again at the same cow‑flow and expansion walls.

What This Means for Your Operation

Start with the building, not the robot. Before you call a single dealer, get a structural engineer and a barn/AMS designer to walk your place. If your foundation is suspect, ceiling height is under 9 feet across most of the barn, or you can’t find 15–20 feet of clear approach space for a robot, you’re not choosing between two good options. You’re choosing between a new barn and an AMS retrofit that may never work right.

Run 15‑year numbers, not 15‑month paybacks. Sit down with your lender or advisor and build three cash‑flow models—minimal compliance, strategic retrofit, and new build—out 15 years. Use realistic labour assumptions (including fetch time at $25–$35/hour) and plug in current Canadian Holstein production as a baseline, then model what happens if you’re 5% under that due to layout and air. The spreadsheet might tell a very different story than the quote.

Be brutally honest about herd size and quota. If a workable robot layout means dropping from 90 cows to 60, are you actually going to do it? Or are you planning to sneak cows back in until the barn is overstocked again? Be honest about how many cows your footprint can truly handle and how that lines up with robot capacity.

Use fetch time as a barn‑health metric. If you’re regularly spending more than about 90 minutes per robot per day fetching cows once the system is “broken in,” treat that as a warning sign. It’s not just a bad day — it’s your layout, stocking density, or air telling you something.

Separate “Code‑compliant” from “livable.” You may be able to meet the 2027 tethering rule with turnout, exercise yards, or loose housing for some groups without robots. That might be the right move if capital’s tight and you can still physically handle the pipeline. But if your body is already done, that’s just postponing the real decision.

Match your path to your horizon. If you’re a decade from retirement and no one’s stepping in behind you, a smart retrofit or even minimal compliance might be perfect. If your kids are already talking about 120 cows and two robots, your plan should focus on where you want to be in 2035, not just how to squeeze one more trick out of a 1970s barn.

Check if your barn matches your genetics. If your breeding decisions and proofs say 14–15,000 kg Holsteins and strong component genetics, ask yourself honestly whether your barn is built for that — or whether the concrete and air in front of your robot are still a 9,000‑kg design. Genetics can’t outrun a barn that holds them back.

Scenario

Realized Milk (kg/year)

Lost to Layout/Heat (kg/year)

Genetic Potential (kg/year)

Good Layout (New Barn)

11,364

0

11,364

Moderate Retrofit

10,796

568

11,364

Compromised Layout

10,296

1,068

11,364

Talk it through before you call the dealer. Sit down with your family and your lender, map each of these paths on paper, and make sure everyone’s aligned on which lane you’re actually in — before anyone falls in love with a shiny robot quote.

Watch your cows for a week before you draw lines on paper. Set the notebook and the quote aside and just watch. Where do cows hesitate? Where do they bunch up? Who owns which alleys? Any robot layout that fights their natural movement will cost you in fetch time, milk, and patience for as long as that concrete is there.

Key Takeaways

The robot is the cheap part. The expensive part is where you bolt it. If the cow flow and air are wrong, that box will spend 15 years amplifying every design mistake.

A $17,000‑per‑cow cost gap between a retrofit and a new build can disappear over 15 years if you’re burning an extra 30–60 minutes a day on fetching at $25–$35/hour and running 5% under your herd’s production potential.

Strategic retrofits work when the barn has genuinely good bones, your realistic future herd size lines up with about 60 cows per robot, and you’re willing to give up stalls and invest in floors, ventilation, and separation.

Minimal‑change “compliance only” strategies can buy you time on the Code and protect your borrowing capacity, but they don’t fix labour, ergonomics, or succession pressures.

Bridge‑style retrofits only make sense if everyone’s honest that Phase 2 — a true, purpose‑built robot barn — is coming, with a rough date and a financial plan. If that’s never going to happen, treat the retrofit as permanent and design it that way.

A well‑designed robot barn isn’t just about labour; it’s how you actually realize the ROI on your high‑LPI and genomic investment. You can’t breed for 14,000–15,000 kg and build for 9,000 kg and expect those proofs to show up on the milk sheet.

Cost Category

Minimal Retrofit

Strategic Retrofit

New Robot Barn

Initial Investment (60 cows)

$480,000

$840,000

$1,480,000

Robot & equipment

$200,000

$200,000

$200,000

Barn/infrastructure

$280,000

$640,000

$1,280,000

Hidden Operating Costs (Annual)

Extra fetch labour (vs. good layout)

+$8,250/yr

+$2,000/yr

$0

Lost production (5% vs. genetic potential)

+$8,500/yr

+$3,000/yr

$0

Mid-Life Correction Project (Year 8)

+$85,000

+$25,000

$0

15-Year Total (All-In)

~$900,000

~$1,140,000

~$1,630,000

Real 15-Yr Cost Gap vs. New Barn

−$730,000 (not −$1M)

−$490,000

Baseline

The Bottom Line

At the end of the day, you’re not just picking a milking system — you’re designing how every single day is going to feel in that barn in 2030 and 2035. The Code, the cost of concrete and steel, and the genetics you’ve already paid for are all going to meet in that alley. Before you chase the cheapest ticket into robotic milking, ask yourself one blunt question: when you’re walking that alley with a fetch list in year eight, will this still feel like a smart move — or just the move that cost the least on paper?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Dairy Tech ROI: The Questions That Separate $50K Wins from $200K Mistakes – Gain a hard-nosed checklist for Monday morning that stops you from buying trade-show hype. This breakdown exposes the $27/hour labor threshold and armors your operation against the infrastructure failures that sink 62% of automation projects.

More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Secure your farm’s 2026 viability by running the five mission-critical numbers lenders are watching. It delivers a risk-management playbook that shifts you from simply watching Class III prices to proactively protecting your regional processor contract.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

If you’re milking 300–600 cows, the real choice isn’t H‑2A or robots—it’s which math keeps you in business 10 years from now.

Executive Summary: If you’re running 300–600 cows, the biggest decision in front of you isn’t just H‑2A or robots—it’s what the labor math says about your next ten years. This piece digs into new USDA‑ERS, Rabobank, and university data to show why H‑2A rarely ends up “cheap,” how global cost gaps are shifting the ground under your feet, where robotic milking and targeted automation genuinely save labor, and how compliance risk fits into the picture. Along the way, it looks at real-world systems—from California dry lots to Wisconsin freestalls and Ontario mixed herds—to ground the numbers in the kind of operations you actually recognize. The article then lays out three honest paths for mid-size dairies: selective automation around bottlenecks, fully legal higher‑cost labor in exchange for stability, or a planned transition out of milking while you still control the terms. It finishes with a practical 30‑day checklist—know your true labor cost per cow and your multi‑year DSCR—so you can stop guessing and see which path really fits your farm.

If you sit down with a table of dairy folks this winter—whether it’s in Wisconsin, California’s Central Valley, or around eastern Ontario—you’ll hear the same three things come up over coffee: labor, margins, and what the next ten years really look like for that 300‑ to 600‑cow family operation. You know the look on people’s faces when the talk turns to “who’s going to milk these cows in five years?”—it’s the same in a lot of kitchen tables and vet trucks right now.

What’s interesting here is that two big storylines keep colliding almost immediately. One is the rapid growth of the H‑2A visa program, which economists at USDA’s Economic Research Service and Congressional analysts say has become a central labor pipeline for a big chunk of U.S. agriculture. The other is the steady march of automation—from collars and sort gates to full robotic milking—backed by university and peer‑reviewed research showing real changes in how labor is used on both small and large herds. Put those alongside the structural lift in global production costs that Rabobank’s dairy team has been documenting, and the real question for most dairies becomes, “Given our cost structure, our people, and what we want this farm to look like in ten years, do we lean into selective automation, formalize labor at a higher cost, or plan a controlled transition while we still have options?”

If you’re in that 300–600 cow bracket, this is the labor math that’s going to have a lot to say about whether you’re still milking in ten years.

How H‑2A got so big, so fast

Looking at this trend from thirty thousand feet, USDA economist Marcelo Castillo and his team did a deep dive on H‑2A for the journal Choices. They found that the U.S. Department of Labor certified employers to fill just under 372,000 seasonal farm jobs with H‑2A workers in fiscal year 2022—more than seven times the number in 2005 and roughly double what it was in 2016. That’s a huge structural shift in less than two decades.

And it’s not just that the program has grown; it’s who’s using it. Castillo’s work shows that around 12,200 employers were certified in 2022, but the top 5 percent—roughly 620 operations, each approved for 100 or more H‑2A workers—accounted for about two‑thirds of all certified jobs. Farm labor contractors alone supplied a large share of those positions. So, as many of us have seen, H‑2A has turned into a core labor tool for labor‑intensive crops, not a side program used by a handful of farms.

Dairy, by comparison, has mostly been watching from the sidelines. A big reason is baked into the design. H‑2A was built for “temporary or seasonal” work. Congressional Research Service reports spell that out clearly: by statute, year‑round industries like dairies, greenhouses, and many livestock operations don’t fit neatly into the current rules. Folks at American Farm Bureau Federation have said the same thing in interviews, pointing out that dairy, livestock, and greenhouse employers often can’t legally use H‑2A for the year‑round jobs they need filled.

Looking at this trend politically, pressure to change it is building. Dairy and meat industry leaders have pushed hard for access to year‑round H‑2A labor, and several recent immigration and farm labor proposals in Congress—including versions of the Farm Workforce Modernization Act and related efforts—have included provisions for limited year‑round H‑2A visas that would explicitly cover dairies and other non‑seasonal operations. Policy coverage into 2025 and early 2026 notes that these proposals would, if enacted, create capped pools of year‑round H‑2A positions and formally recognize dairy’s year‑round labor needs, but as of early 2026, they remain proposals rather than settled law. So the mix of hope and frustration producers feel—“Every politician says they understand dairy’s problem, but we still don’t have a year‑round fix”—is grounded in the current policy reality.

If you hop north into Ontario, the mechanics are different, but the flavor is similar. Canadian producers rely on the Temporary Foreign Worker Program and the Seasonal Agricultural Worker Program, and federal guidance makes it clear that those programs also come with strict requirements around approved housing, travel arrangements, and documentation. The tool names change across the border; the core challenge doesn’t. You can get legal, reliable labor, but it takes real money and real management.

H‑2A labor costs: it’s a lot more than an hourly wage

On the surface, H‑2A starts with one number: the Adverse Effect Wage Rate, or AEWR. That’s the minimum hourly wage you’re required to pay H‑2A workers in your state. USDA and CRS explain that AEWR is based on USDA’s Farm Labor Survey and, in many states, has moved into the mid‑ to high‑teens per hour, with some regions above that. American Farm Bureau government affairs staff have pointed out that, nationally, AEWR has jumped by roughly 20 percent over about five years, while revenue for many labor‑intensive crops hasn’t kept pace.

Cost Category

Amount (USD)

% of Total

AEWR Wages (6 months @ $18.50/hr, ~1,080 hours)

$19,980

67.7%

Housing (on-farm or rental, utilities, maintenance)

$4,200

14.2%

Transportation (airfare, ground travel, visa)

$3,800

12.9%

Recruitment & Admin (legal, HR, processing fees)

$1,520

5.2%

Total Employer Cost

$29,500

100%

But what I’ve found is that the hourly wage is only the tip of the iceberg.

Castillo’s ERS analysis emphasizes three big non‑wage buckets that matter just as much as the posted rate.

Housing. Employers have to provide housing that meets specific federal and state standards at no cost to the worker. In practice, that often means building or renovating bunkhouses on‑farm or renting apartments in town, then paying for utilities, maintenance, and inspections. USDA’s own H‑2A assistance initiatives and Farmers.gov resources highlight housing as one of the biggest cost and compliance barriers.

Transportation. H‑2A employers must pay for workers’ travel from their home country to the job site and back, and they’re responsible for daily transportation between housing and the farm. Congressional researchers list transportation costs as a major recurring expense across H‑2A employers.