New NAAB data says the heifer gap is 200,000 head smaller than CoBank projected. Good news? Not at $4.46 per cwt of your milk check.

Executive Summary: CoBank’s 800,000-heifer shortage projection got the industry’s attention last August. Updated NAAB semen data, released March 10, says the real gap is closer to 600,000 — but your replacement bill doesn’t care about the difference. At $3,100/head, a 500-cow herd with a 36% cull rate spends $4.46/cwt on replacements alone. That’s 25.5% of gross milk revenue at January’s $17.50 all-milk price, and the spread between scenarios is $108,000 a year. Sexed semen’s pipeline correction is running ahead of CoBank’s model; beef-on-dairy’s 8.1 million units aren’t budging. The national gap is probably shrinking. What it costs you to replace cows this spring isn’t.

CoBank projected an 800,000-head decline in the number of replacement heifers. NAAB’s 2025 year-end semen report, released March 10, suggests the real gap is closer to 500,000–700,000. That sounds like relief — until you run the numbers on your own herd. On a 500-cow operation at today’s replacement prices, the spread between the worst and best scenarios is $0.86/cwt, or $108,000 a year. Against January’s $17.50/cwt all-milk price, that’s the gap between margin and none.

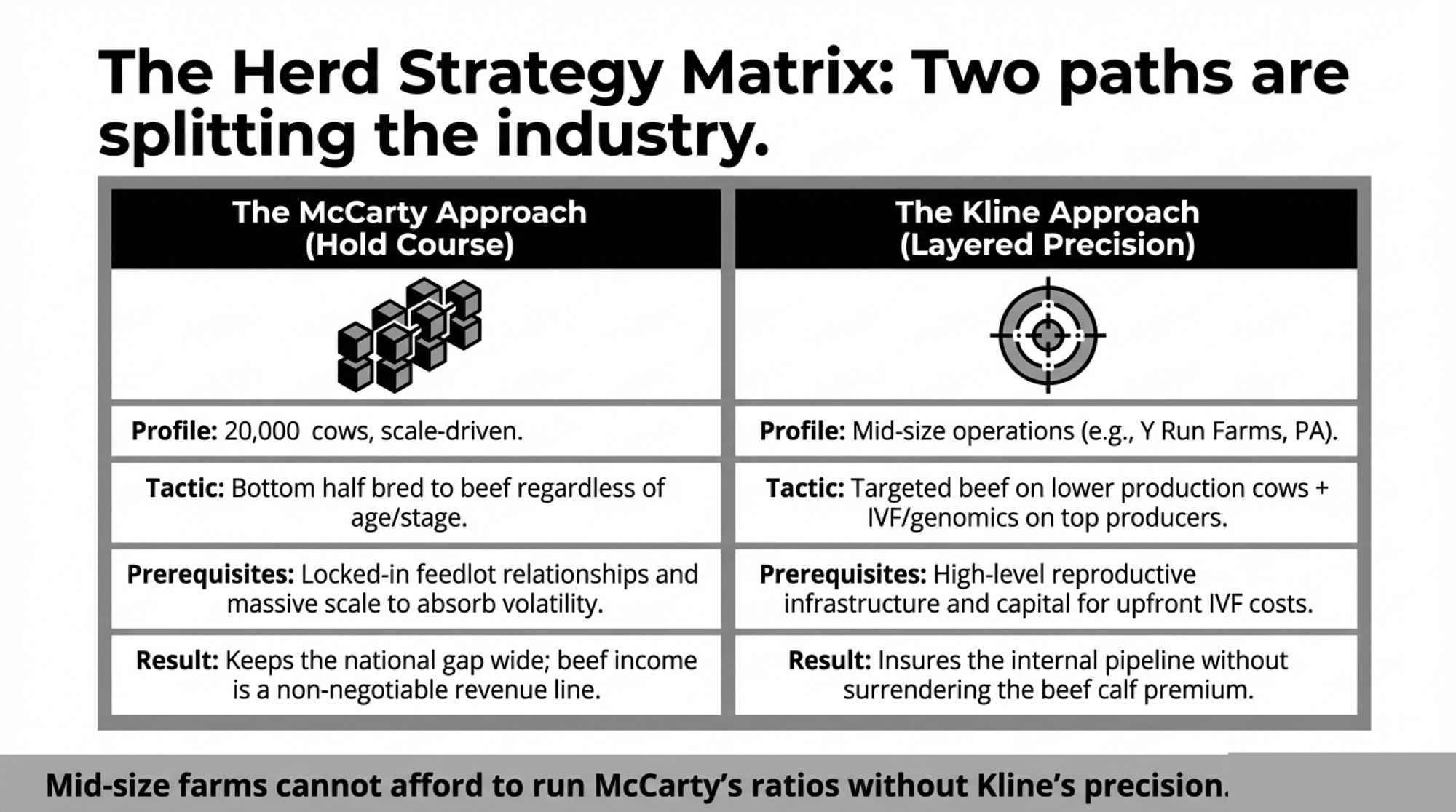

Ken McCarty of McCarty Family Farms in Colby, Kansas — 20,000 cows, Farm Journal’s 2025 Leader in Technology Award winner — isn’t adjusting his breeding plan. His operation genomically tests every female, breeds the top half to dairy and the bottom half to beef “regardless of age or stage,” and markets beef cross calves as day-olds at roughly $1,400 a head. He told Dairy Herd last September that his market analysis of “beef herd trends, heifer retention rates and rancher and cow-calf operator retirement” all point in the same direction: beef-on-dairy values hold “through 2026 and into the first half of 2027.”

But McCarty runs 20,000 cows with locked-in feedlot relationships and a genetics program that ensures his top half keeps producing replacements. Most operations don’t have that math. And the question facing a 400-to-800-cow herd right now isn’t whether CoBank’s 800,000 number is right. It’s whether the actual gap — probably 600,000 to 700,000 — changes what you should do this spring.

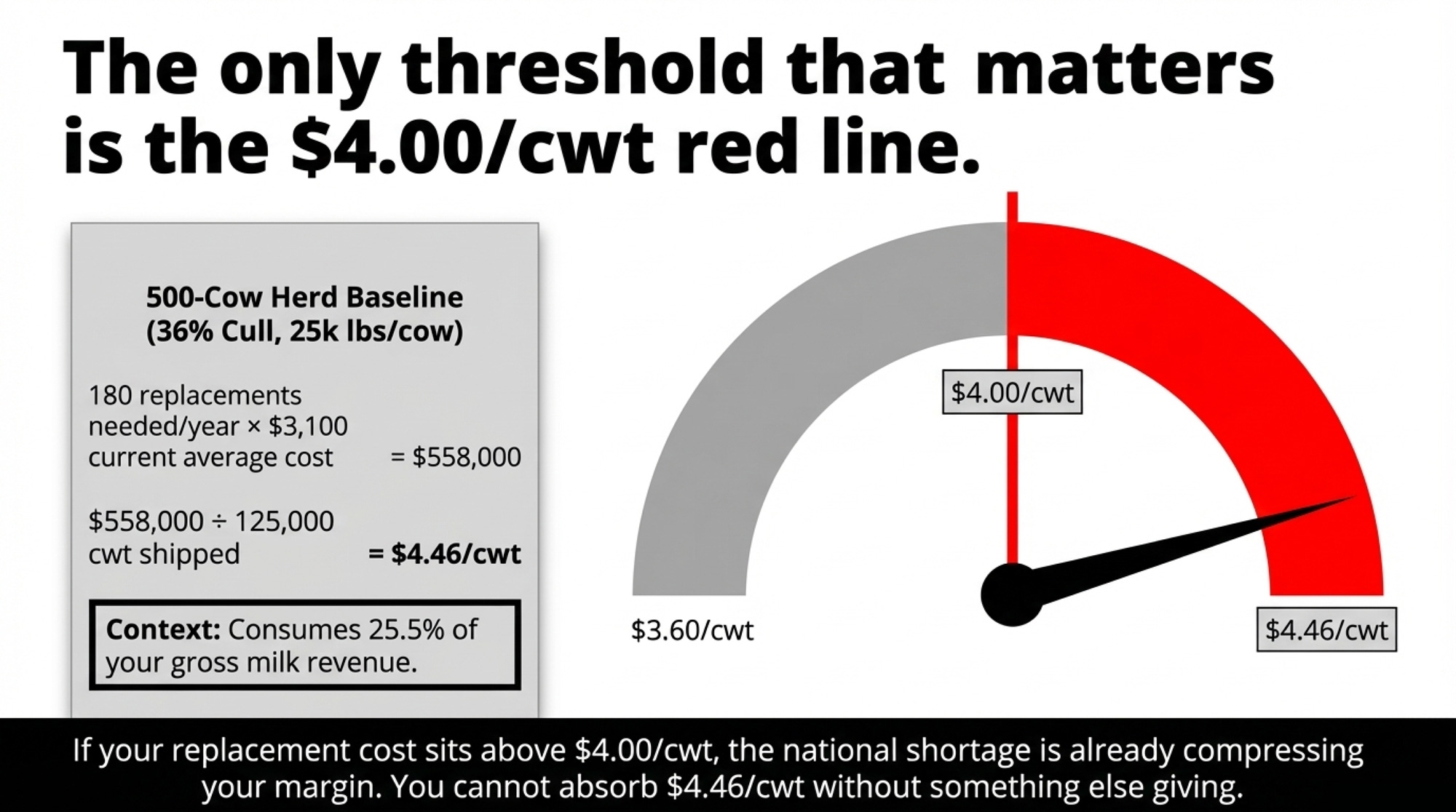

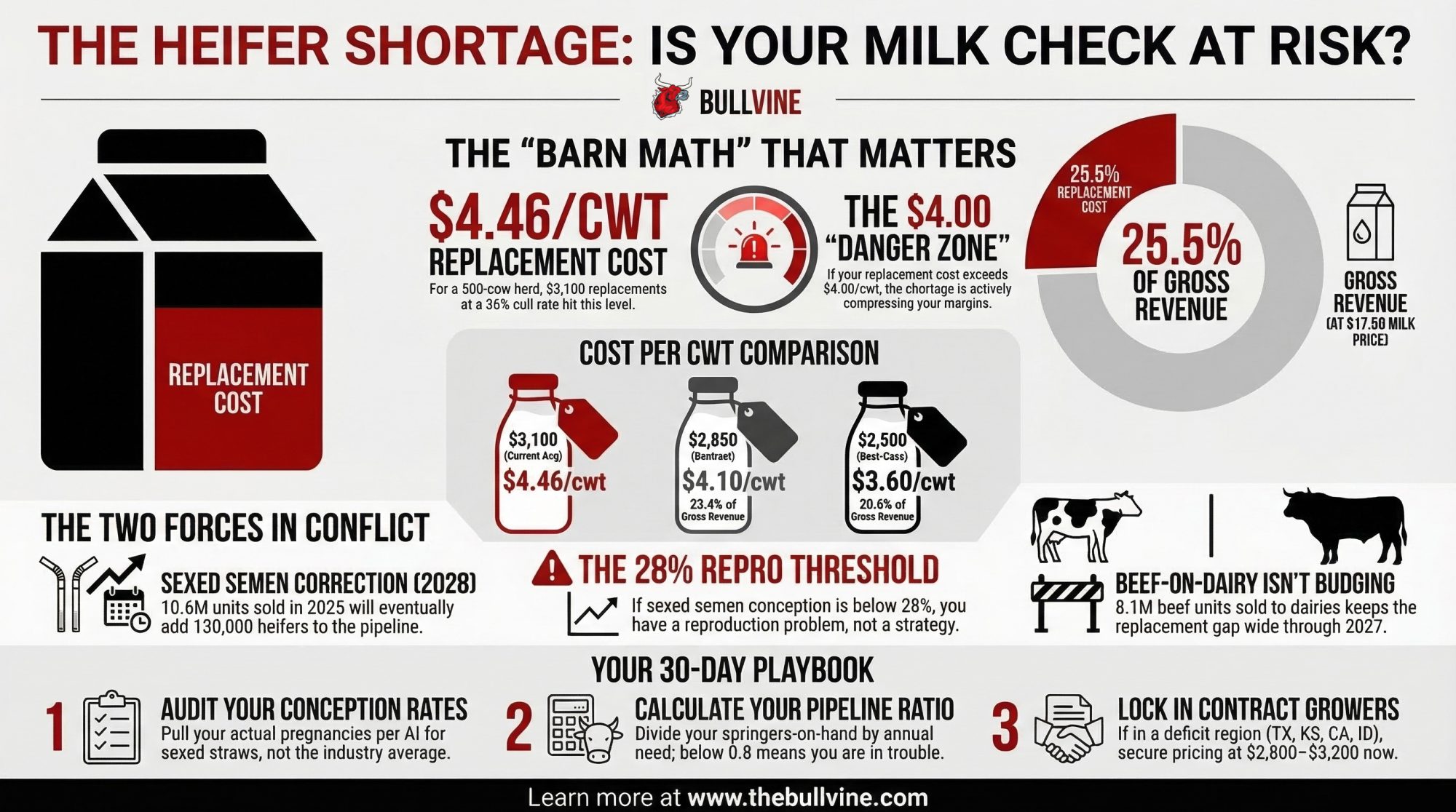

What Does a $3,100 Springer Cost You Per Hundredweight?

Before the variables, the barn math. This is the number that should drive your next move.

Assumptions for a 500-cow herd (adjust to your own):

- Annual cull rate: 36% → 180 replacements per year

- Milk shipped: 25,000 lbs/cow/year → 125,000 cwt total

- January 2026 all-milk price: $17.50/cwt (USDA)

At the USDA’s October 2025 national average of $3,100/head:

- 180 × $3,100 = $558,000 annual replacement cost

- $558,000 ÷ 125,000 cwt = $4.46/cwt

- That’s 25.5% of your gross milk revenue going to replacement procurement alone

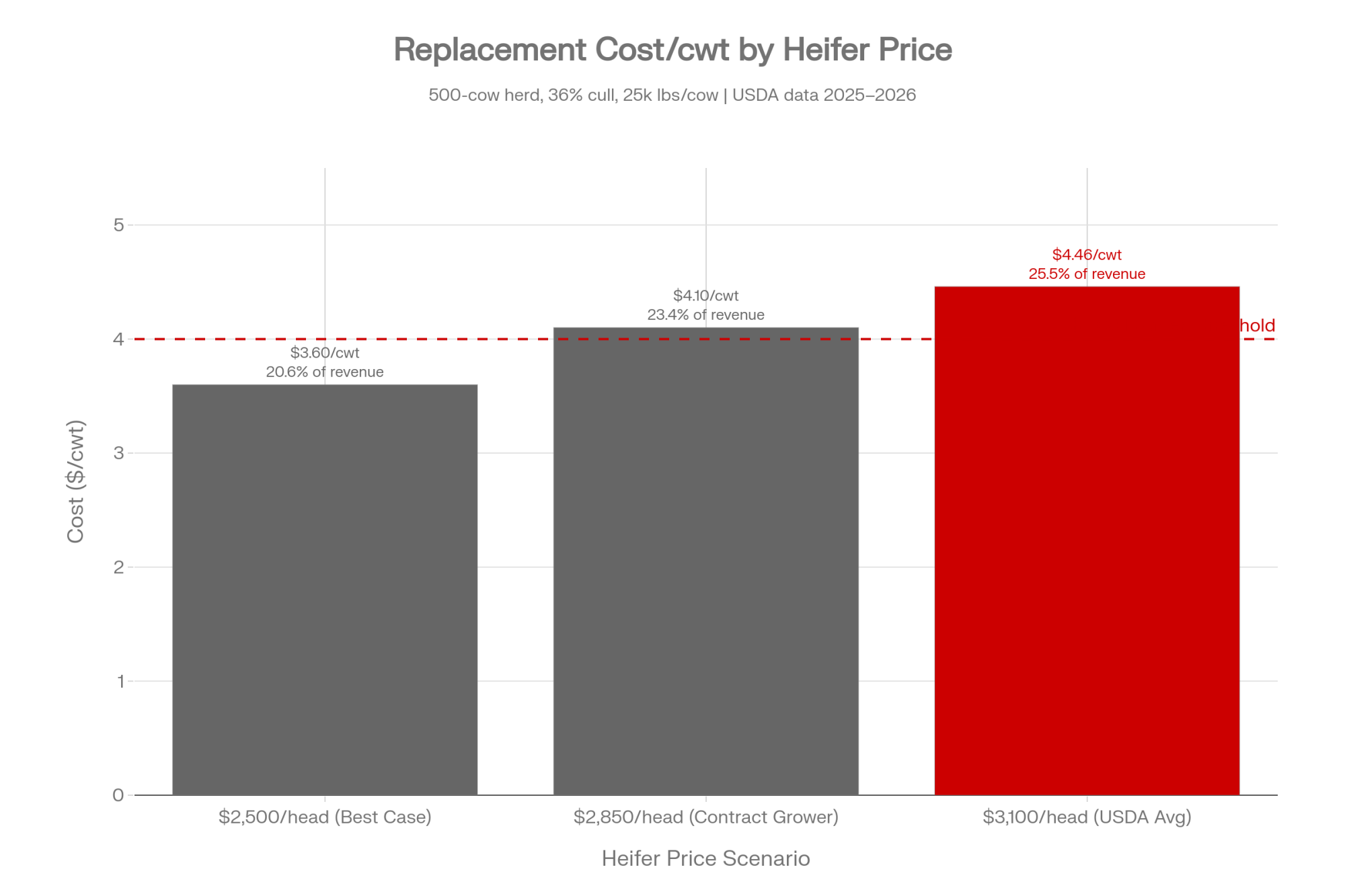

At $2,850/head via contract grower (reported pricing, late 2025):

- 180 × $2,850 = $513,000

- $4.10/cwt — still 23.4% of the check

At $2,500/head (best-case, surplus regions, late 2027):

- 180 × $2,500 = $450,000

- $3.60/cwt — 20.6% of revenue

The threshold that matters: $4.00/cwt. If your replacement cost sits above that line, the heifer shortage is already compressing your margin — regardless of whether the national gap is 500,000 or 800,000 head. For context, USDA-ERS pegs full-cost production for even the most efficient 2,000+ cow herds at $19.14/cwt. The 2026 all-milk forecast is $18.95. Nobody has room to absorb $4.46/cwt in replacement costs without something else giving.

The Two Forces You’re Watching

Two macro variables determine whether the final gap lands at 600,000 or 800,000. You don’t control either one. But you need to track both.

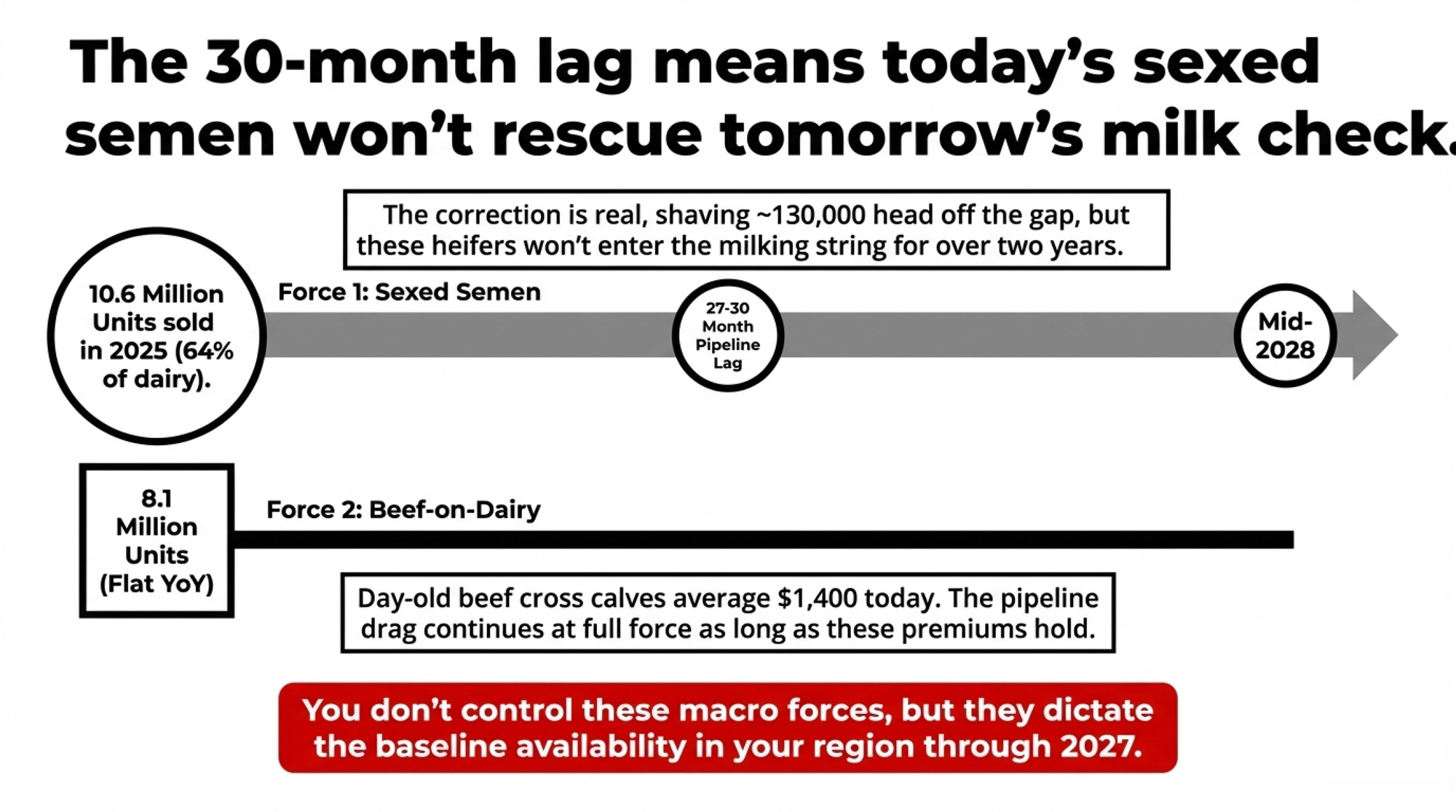

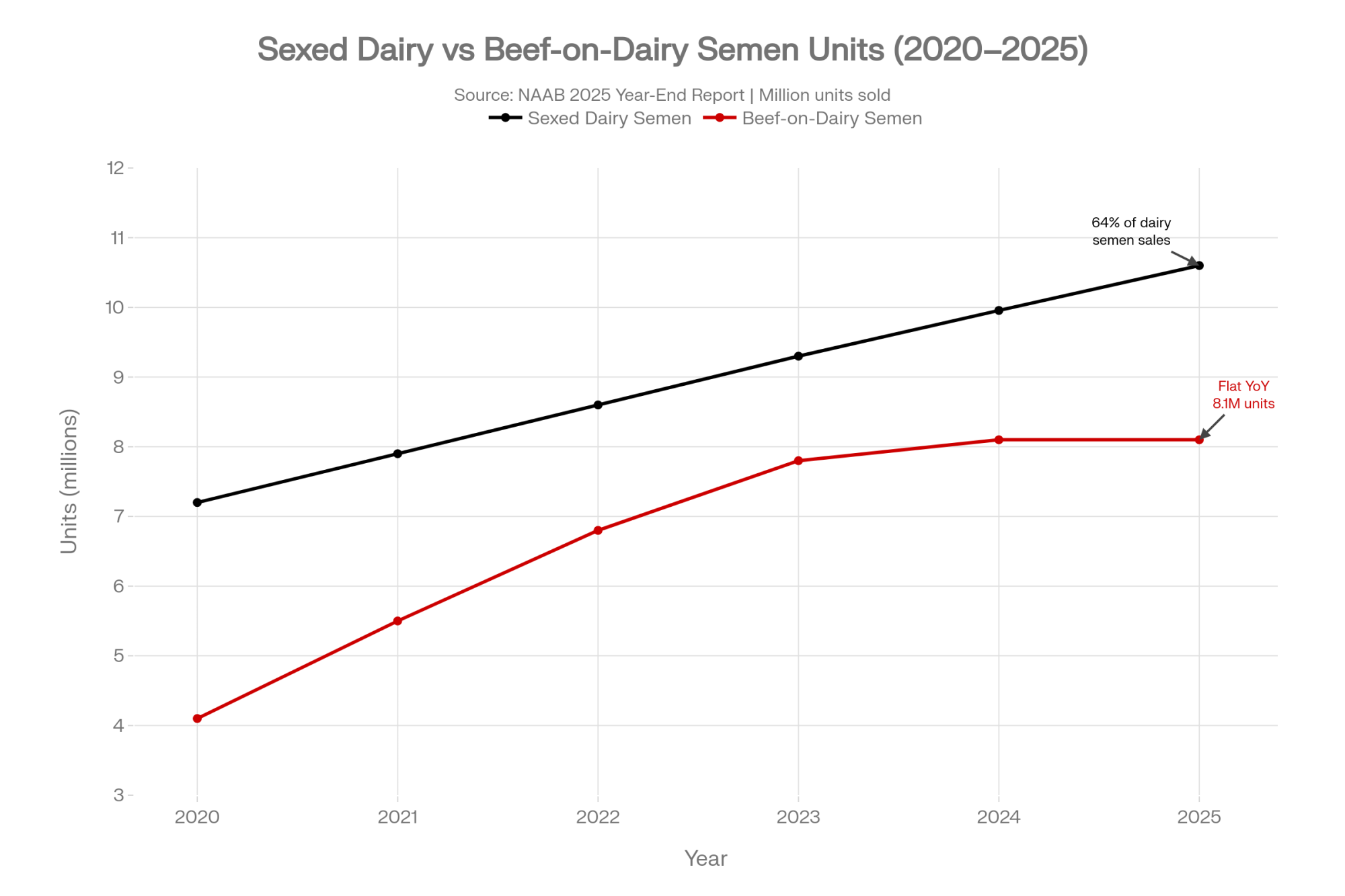

Sexed semen is running ahead of CoBank’s model. NAAB’s year-end data shows sexed dairy semen hit 10.6 million units in 2025 — up 644,000 from 2024 — now 64% of all domestic dairy semen sales (dairy semen only, excluding beef-to-dairy). CoBank’s model captured the 2024 spike but didn’t fully price in a second sustained wave. At industry-average conception rates (29–35% in cows, 46–59% in heifers), each additional million units of sexed semen adds roughly 85,000–120,000 heifers to the pipeline after rearing attrition. That 2025 semen produces heifers entering milking strings in 2028 — the correction is real, but the lag is 27–30 months.

Impact on the gap: shaves an estimated 100,000–130,000 head off CoBank’s projection.

Beef-on-dairy isn’t budging. The 2025 NAAB number: 8.1 million beef semen units sold to dairy. Flat year-over-year. DFA estimates 70% of dairy farmers are now engaged in beef-on-dairy, adding $2.50–$3.00/cwt to their bottom line. According to Laurence Williams at Purina, day-old beef-on-dairy calf prices averaged about $650 three years ago compared to roughly $1,400 today. The U.S. cattle inventory sits at a 75-year low of 86.2 million head (USDA, January 2026). McCarty’s read — that beef values hold through early 2027 — looks well-supported by fundamentals.

| Year | Sexed Dairy Semen (M units) | Beef-on-Dairy (M units) |

|---|---|---|

| 2020 | 7.2 | 4.1 |

| 2021 | 7.9 | 5.5 |

| 2022 | 8.6 | 6.8 |

| 2023 | 9.3 | 7.8 |

| 2024 | 9.956 | 8.1 |

| 2025 | 10.6 | 8.1 |

Phil Plourd, president of Ever.Ag Insights offered the most honest framing: “It’s certainly possible that beef and cattle prices will retreat at some point over the next couple of years,” but “even a major retreat would still leave dairy producers with much more beef income than they enjoyed seven or 10 years ago.”

Translation: don’t plan on beef-on-dairy fading fast. If it holds at 8.1M units through 2026, the pipeline drag continues at the pace CoBank modeled. The gap stays wide — 700,000 to 800,000 range.

The Two Levers You’re Actually Pulling

Here’s where it gets personal. Two variables sit inside your operation, and they swing the gap by 90,000–140,000 head nationally — and by thousands of dollars on your own P&L.

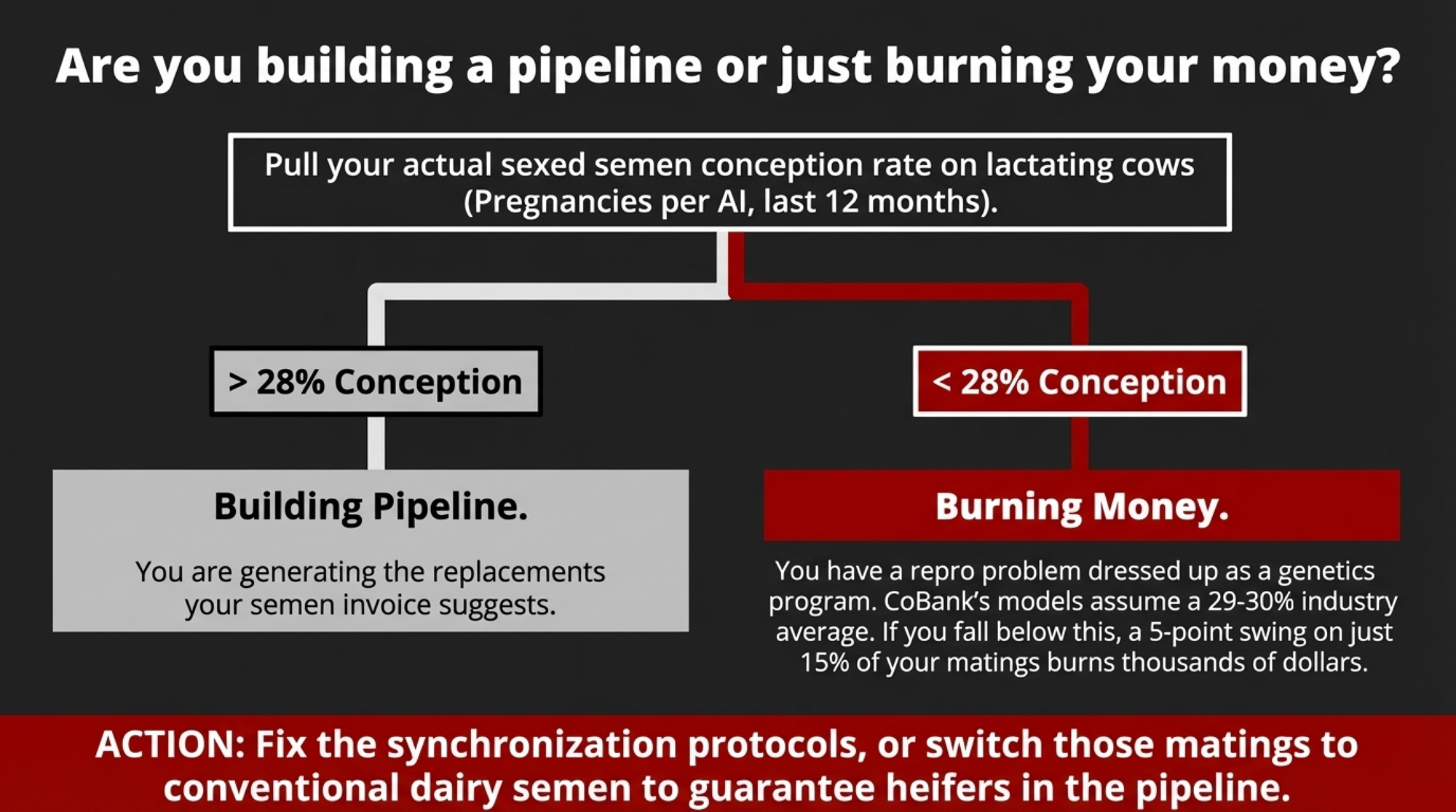

Your sexed semen conception rate is either building your pipeline or burning your money. CoBank applied an industry-average rate of 29–30% to lactating cows. Reality ranges from 18% to 40%, depending on synchronization protocols, technician quality, and body condition management. Across 9.57 million cows, a 5-point swing on 15% of matings (the share using sexed semen in cows) translates to 40,000–60,000 heifers nationally. On your herd, the question is blunter: if your conception rate on sexed semen in cows is below 28%, you’re producing fewer replacements than your semen invoice suggests. You’ve got a repro problem dressed up as a genetics program.

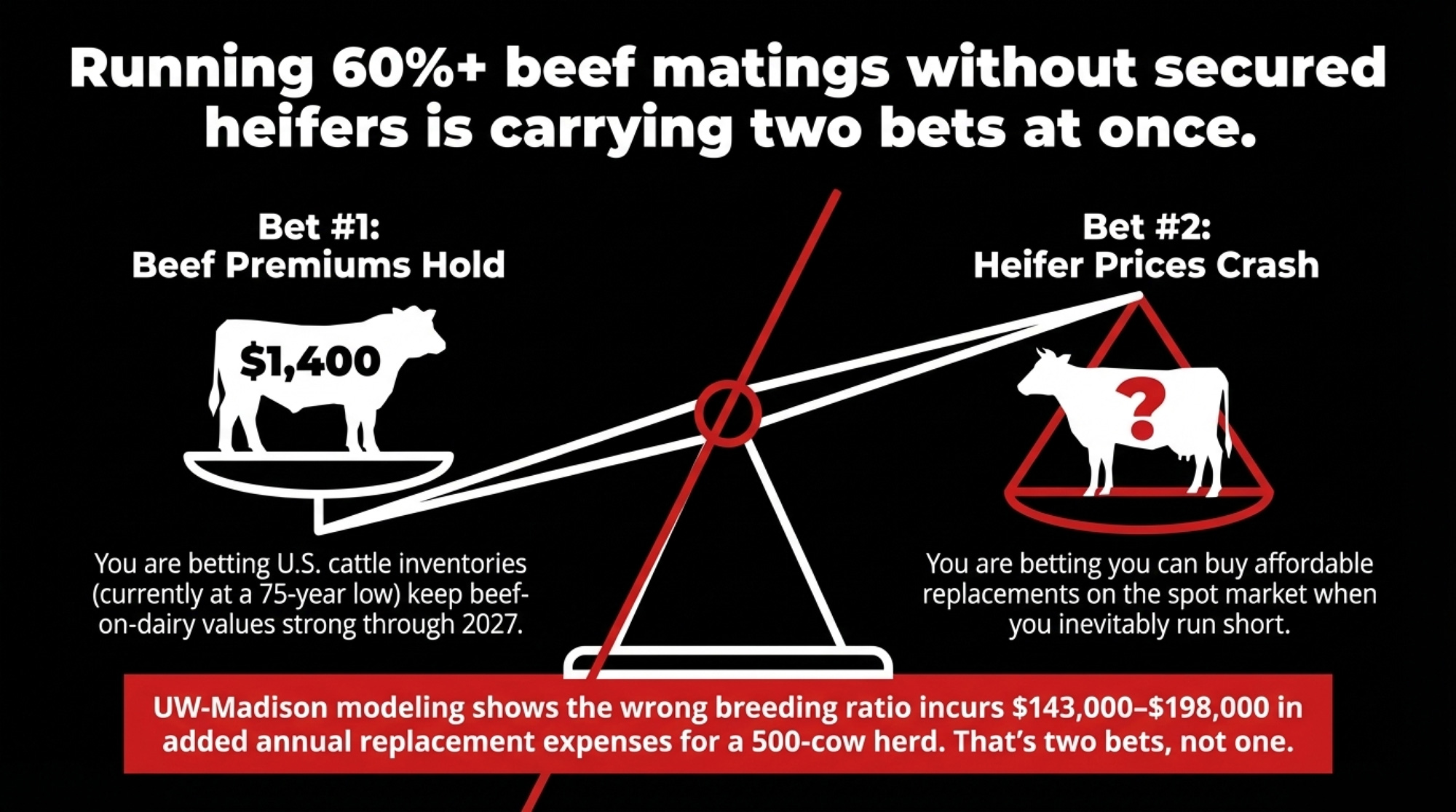

Your breeding ratio decision is a bet — make sure you know both sides. UW–Madison’s beef-on-dairy economics model, published early this year, found that the wrong breeding plan incurs $86,000–$119,000 in replacement costs per 300-cow pen at today’s heifer prices of $3,000–$4,100+. Scale that proportionally to 500 cows, and you’re looking at roughly $143,000–$198,000 in added annual replacement expense. (That’s rough math, not a spreadsheet — the point is order of magnitude.)

Two approaches are splitting the industry right now:

McCarty’s group holds course. Large Western herds and processing-aligned mega-dairies with locked-in beef calf contracts and feedlot relationships. Beef-on-dairy income is a non-negotiable revenue line. They won’t adjust ratios until calf prices move against them. This group keeps the national gap wide.

Glenn Kline’s group hedges differently. Kline runs Y Run Farms LLC in Pennsylvania and told a CDCB panel last fall that his team uses a layered approach: “We’ve been using beef on dairy to keep our lower production cows using beef, and we use IVF to try to make better heifers of the good ones.” That’s a third path — keeping beef-on-dairy revenue flowing while using IVF and genomic testing to intensify replacement production from the top genetics. It costs more per heifer to produce, but it insures the pipeline without giving up calf income. Operations recalibrating their ratios — from 65% beef back toward 50–55% — or investing in IVF to protect their replacement pipeline are tightening the national gap toward the 500,000–600,000 range.

| Metric | McCarty Model (Large Western) | Kline IVF-Layered | Mid-Herd Pivot (50–55% Beef) |

|---|---|---|---|

| Beef-on-dairy ratio | 50% (bottom genomic half) | 40–50% selective | 50–55% (down from 65%+) |

| Sexed semen use | Top 50% genomic females | Top IVF donors + genomic selection | Broadly applied to top cows |

| IVF/embryo use | No (genomic only) | Yes — pipeline insurance | No (cost barrier) |

| Day-old calf revenue | ~$1,400/head | $1,200–$1,400/head | $900–$1,200/head |

| Heifer pipeline ratio | Secured via feedlot contracts | Self-sufficient + potential surplus | Below 1.0 — at risk by 2027 |

| Springer procurement | Internal supply | Internal supply | Spot market dependent |

| Risk if beef price drops below $1,100 | Low (scale absorbs) | Low (IVF covers gap) | HIGH — dual bet exposed |

| Annual replacement cost/cow | Lowest (scale efficiency) | Highest (IVF premium) | Middle |

| Best suited for | 5,000+ cow ops with feedlot ties | 200–800 cow ops, strong repro mgmt | Operations actively recalibrating now |

Every month you continue running 60%+ beef matings without a secured heifer supply source, you’re making two bets at once: that the beef premium holds and that heifers stay available at a price you can afford. That’s two bets, not one.

Which Scenario Are You In? Here’s How to Tell

The range — 500,000 to 800,000 — maps to three distinct price trajectories. Where you land depends on the region and timing.

| Scenario | Heifer inventory, end of 2026 | What happens to springer prices |

| CoBank base (~800k gap) | ~3.1–3.3M head | Above $3,000 nationally; $4,000+ in deficit regions (TX, KS, CA, ID) into 2028 |

| Mid-range (~600–700k) | ~3.3–3.5M head | Modest softening H2 2027 in surplus regions; deficit regions still tight |

| Best case (~500k) | ~3.5M head | Easing visible mid-2027 in Midwest/Northeast; PA and WI markets loosen |

State-level data sharpens the picture. In the most recent USDA quarterly survey with state breakdowns (January 2025), Vermont ran highest at $2,930/head, Wisconsin at $2,860/head, and Kansas lowest nationally at $2,350/head — even as new dairy processing capacity comes online in southwest Kansas, Idaho, and Michigan. By October 2025, the national average hit a record $3,110. At auction in early 2026, bred heifers are clearing $3,500–$5,000+, depending on stage and genetics.

| Region | Jan 2025 | Oct 2025 |

|---|---|---|

| Kansas | $2,350 | $2,700 |

| Wisconsin | $2,860 | $3,100 |

| Vermont | $2,930 | $3,200 |

| National Avg | $2,850 | $3,110 |

Watch two signals:

- NAAB Q1 2026 semen data (expected mid-year): If sexed dairy semen holds above 10.5M annualized and beef-on-dairy drops below 7.5M, you’re in the softer 500k–600k range. If both hold flat, plan for the full 700k–800k gap.

- Day-old beef-on-dairy calf prices at auction: When these fall below $1,100 consistently — not a one-week dip, a trend — the economic case for beef-on-dairy weakens and breeding ratios shift. We’re not there. January 2026 reports still show strong premiums.

Your Playbook: 30, 90, and 365 Days

In the next 30 days:

- Pull your actual sexed semen conception rate — cows and heifers, separately — for the last 12 months. Not the semen rep’s number. Your pregnancies per AI on sexed straws. Below 28% in cows? Fix the repro management or switch those matings to conventional dairy semen. At least you’ll get heifers in the pipeline.

- Calculate your replacement cost per cwt using the formula above. Plug in your cull rate, your milk shipped, and your actual replacement price. If you’re above $4.00/cwt, you need to act on one of three levers: cut your cull rate, lock in contract grower pricing, or build internal heifer capacity. There’s no fourth option.

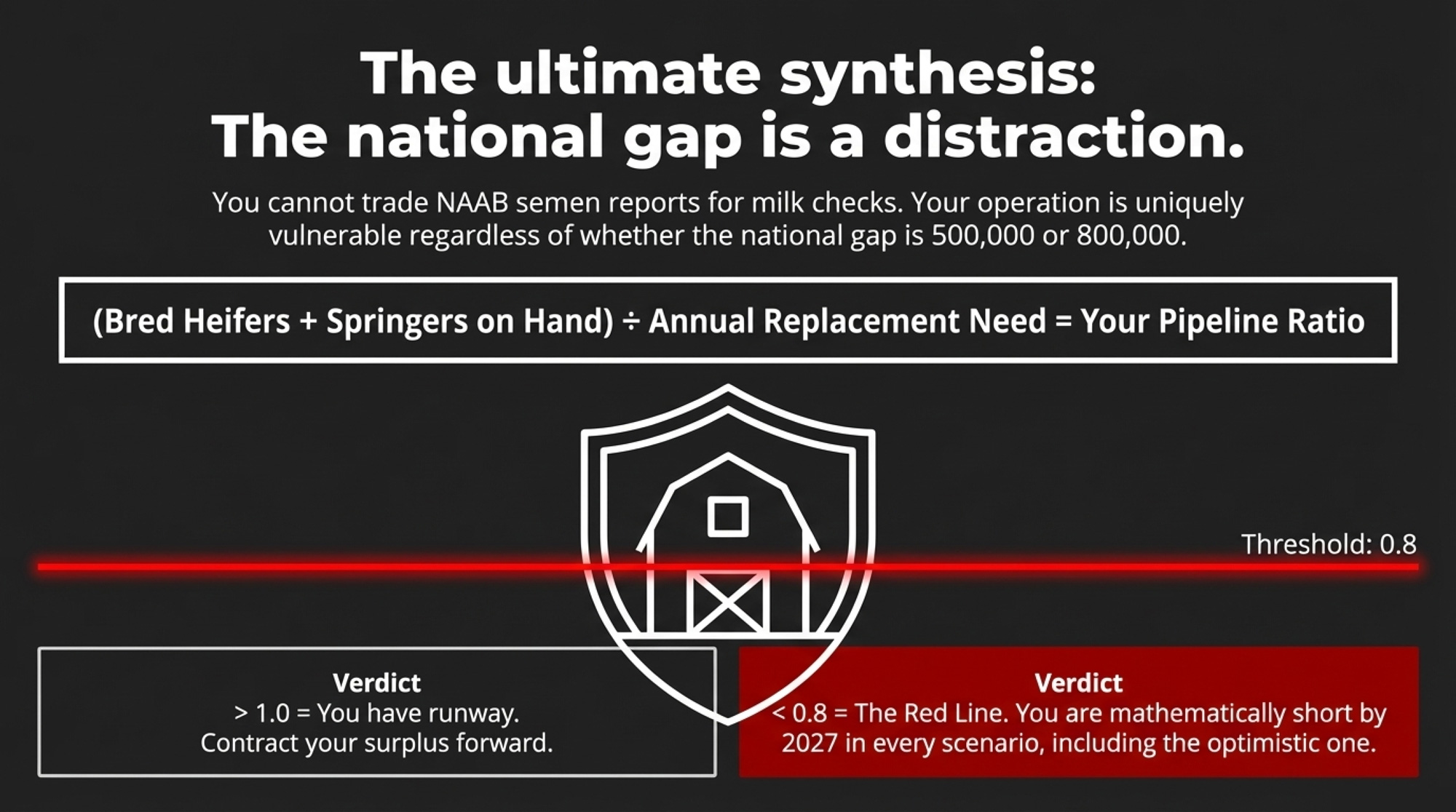

- Count your bred heifers and springers on hand. Divide by your annual replacement need. Below 1.0? You’re already short. Below 0.8? You’re in trouble by 2027 regardless of the scenario.

| Pipeline Ratio | Status | What It Means | Action Required |

|---|---|---|---|

| Above 1.2 | ✅ Surplus | More replacements than you need | Contract bred heifer surplus forward at $3,100+ while pricing holds |

| 1.0–1.2 | ⚠️ On Track | Adequate 2026–2027 coverage | Monitor NAAB Q1 data; lock in contract growers if you’re in a deficit region |

| 0.8–1.0 | 🔴 At Risk | Short in the CoBank 800k scenario | Pull sexed semen conception rates now; evaluate contract grower pricing |

| Below 0.8 | 🚨 Critical | Short in EVERY scenario | Secure supply immediately — you’re buying on a seller’s market regardless of the national gap |

By 90 days (June 2026):

- When NAAB releases Q1 2026 data, check sexed dairy semen against the 10.5M annualized threshold and beef-on-dairy against 7.5M. Those two numbers tell you which scenario is materializing. Price your heifer contracts accordingly.

- If you’re in a deficit region (TX, KS, CA, ID), lock in contract grower arrangements now. DFA’s Dennis Gillins noted processing capacity is growing in “Idaho, southwest Kansas, Michigan, and New York” — exactly the areas where replacement demand will be fiercest. Don’t plan around the optimistic scenario.

- If you’re in a surplus region (PA, WI, parts of the Midwest), contract your bred heifer surplus forward at today’s pricing. Wisconsin’s heifer inventory for milk cow replacement was already down 2% year-over-year as of January 2026 (DATCP/NASS).

By 365 days (March 2027):

- Reassess your replacement cost per cwt against your milk price. If the gap has narrowed below $3.50/cwt, the pipeline correction is landing. If it hasn’t, lock in 2028 supply before the rest of the market figures it out.

- Review your beef-on-dairy ratio against the updated calf price environment. If day-old calves have dropped below $1,100, the math has shifted — recalculate and adjust.

Key Takeaways

- Calculate your replacement cost per cwt. At $3,100/head and a 36% cull rate, a 500-cow herd hits $4.46/cwt. Above $4.00, the shortage is already in your margin — the national gap number won’t change that.

- Pull your sexed semen conception rate — cows and heifers, separately. Below 28% in cows, you’re producing fewer replacements than your semen invoice suggests. That’s a repro problem, not a genetics strategy.

- If you’re running 60%+ beef matings without a secured heifer source, you’re carrying two bets at once. Beef-on-dairy held flat at 8.1M units — that bet looks solid. Affordable heifers when you need them? That one doesn’t.

- Check your pipeline ratio — bred heifers and springers on hand divided by annual replacement need. Below 0.8, you’re short by 2027 in every scenario, including the optimistic one.

- Deficit region? Lock in contract growers now at $2,800–$3,200/head. Surplus region with a ratio above 1.0? You have runway — but contract your bred heifer surplus forward while $3,100+ pricing holds.

The Bottom Line

Two paths. Neither is risk-free.

Lock in supply certainty now via contract growers at $2,800–$3,200/head delivered. You pay a $200–$400/head premium over your best-case spot price. But you eliminate the risk of paying $3,500+ if the 800k scenario materializes. Insurance isn’t free — but neither is scrambling for heifers when every other operation in your region is doing the same thing.

Hold and bet on softening by late 2027. You save the contract premium if the pipeline correction delivers cheaper heifers in surplus regions. But if beef-on-dairy holds at 8.1M units and the gap stays wide, you’re buying on the spot market at whatever price deficit-region demand sets. McCarty’s group can absorb that volatility. Kline’s approach — IVF on top of genetics plus targeted beef matings — offers a middle path, but it requires the herd genetics and reproductive infrastructure to execute. Can your operation run it?

The honest answer depends on your pipeline ratio, your region, and your balance sheet. Run the numbers. Then decide.

What’s your replacement cost per cwt right now — and when’s the last time you actually calculated it?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- $3,010 Per Heifer. 800,000 Short. Your Beef-on-Dairy Bill Is Due. – Gain a concrete roadmap to survive the replacement crunch by auditing your breeding balance and processor contracts. This breakdown delivers four specific paths—from strategic culling to internal rebalancing—to protect your operation’s capital before the 800,000-heifer hole deepens.

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – Position your herd for the long-term structural reset by identifying why traditional culling math no longer works. This analysis exposes how new processing capacity and beef-on-dairy premiums are permanently altering the industry landscape, arming you with a 2026 survival playbook.

- Your Top Heifers All Trace to Three Cow Families. That’s a $93,300-A-Year Trap. – Reclaim your genetic diversity and avoid the costly trap of over-concentrated maternal lines. This innovation-focused guide reveals how adding cow family filters to your genomic sorting can stop a $93,000 annual capital drain and insulate your herd against inbreeding-driven frailty.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.