Stay and pay $190/cow in SGMA fees. Move to Idaho and gamble on processing capacity. Convert to solar and lose those feed acres for 30 years. Pick.

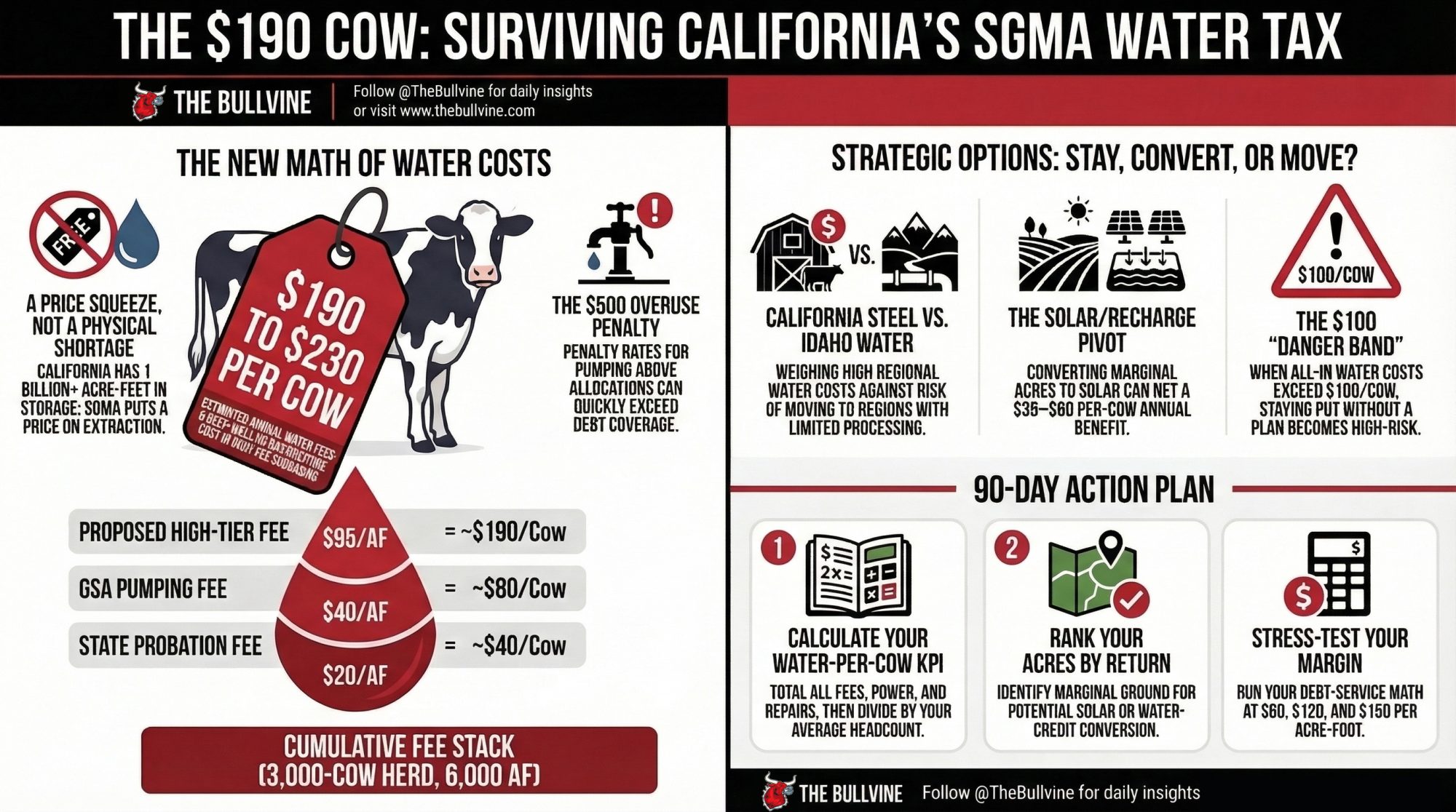

Executive Summary: SGMA has turned groundwater from “free” into a $190–$230 per‑cow, per‑year bill for some Tulare and Kings County dairies once fees and deep‑well costs stack up. Bulletin 118 just confirmed California still has over a billion acre‑feet of groundwater in storage, so the real squeeze is price, not physical shortage. Between Tulare Lake probation fees, Mid‑Kings proposals up to $95/AF, and $500/AF overuse penalties, a 3,000‑cow herd pumping 6,000 AF can see water alone chew through $190/cow before power or feed shifts. Subsidence is forcing faster well turnover, and a single $600K–$700K deep well adds another $40–$47/cow/year when you spread it over 15 years. That level of water cost pushes you toward three paths: stay and absorb SGMA as a formal input cost, convert weaker acres to solar/recharge and buy more feed, or plan a move to cheaper‑water states where processing capacity and contract security are far from guaranteed. The article walks through barn‑math examples, stress‑tests at $80/$120/$150 per AF, and shows where the “$100–$120/cow” danger band starts to threaten debt coverage. If you don’t know your true water $/cow and how it trends under your GSA’s 5‑ to 10‑year plan, you’re already behind the dairies treating SGMA as a capital decision instead of another weather year.

For decades, the Central Valley’s competitive advantage was built on “free” groundwater and sunshine. In 2026, the sunshine’s still free — but water just became the most expensive input on your P&L. If you aren’t accounting for the SGMA “tax,” your genetics aren’t the only thing that’s underwater.

The water under California’s southern San Joaquin Valley dairies didn’t disappear. It just got an invoice, and the numbers are big enough to break the wrong business model.

Aaron Fukuda manages the Kaweah Subbasin Groundwater Sustainability Agency in the heart of Tulare County dairy country. In 2024, SGMA pumping costs in his district jumped from roughly $32 per acre to as high as $140, backed by a $5.8 million annual mitigation program that Kaweah partners signed with Self‑Help Enterprises to keep domestic wells functioning as the water table dropped — all of it funded by pumping fees.

For the 1,500‑ to 5,000‑cow dairies sitting on this ground, that fee trajectory isn’t background noise. It’s a line item marching straight at whatever margin you’ve got left.

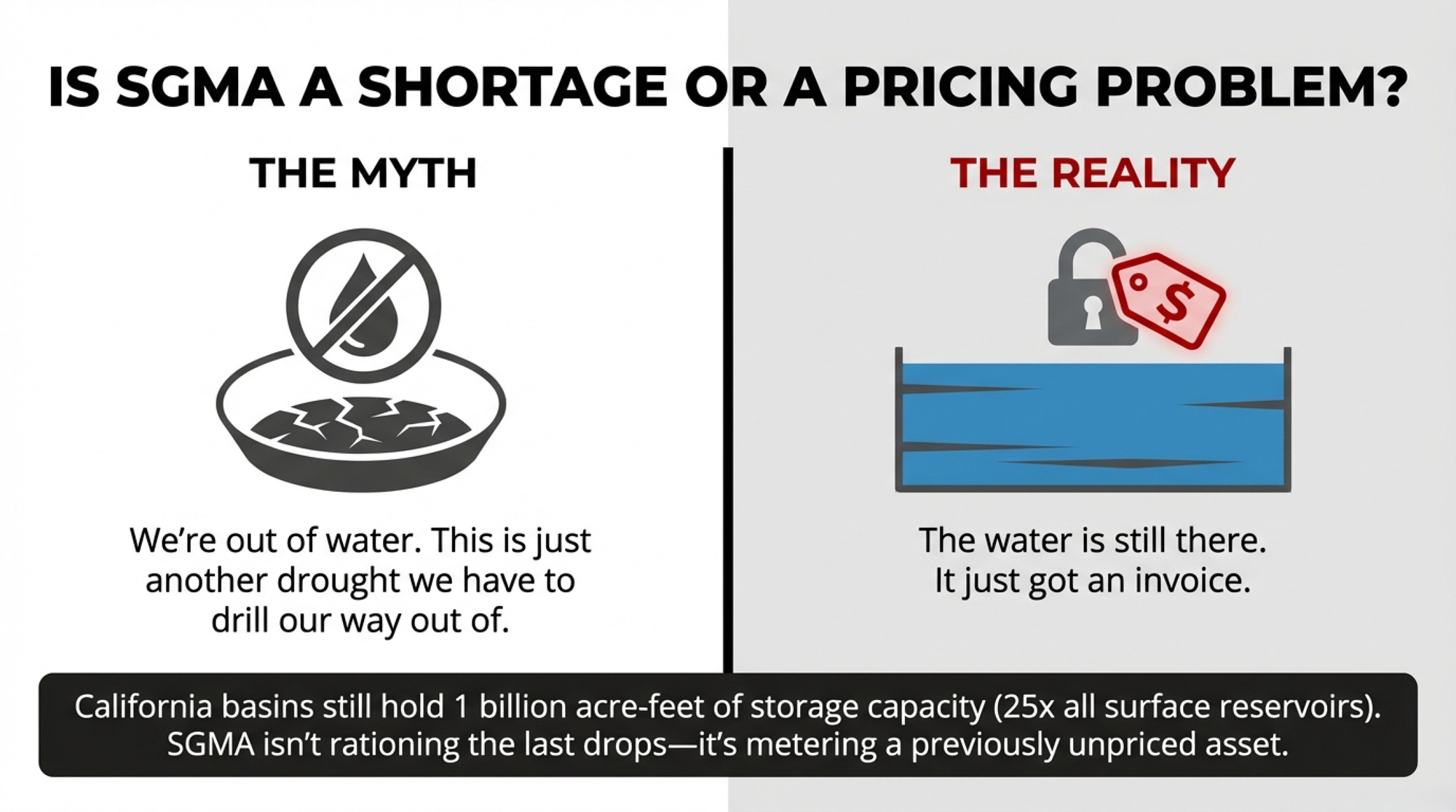

Here’s the part a lot of people still miss: the aquifer isn’t empty. Released just eleven days ago, on March 12, 2026,California’s Department of Water Resources published California’s Groundwater: Bulletin 118 – Update 2025, calling it the state’s most comprehensive groundwater assessment to date. That report estimates that California’s groundwater basins hold more than 1 billion acre‑feet of storage capacity — roughly 25 times the combined capacity of all surface reservoirs — and that groundwater supplies about 40% of statewide water in average years and 60% in drought years. SGMA isn’t about rationing the last drops. It’s about putting a hard price tag on a resource that used to feel free.

Is SGMA a Water Shortage — or a Water Cost Problem for California Dairies?

A lot of Western producers still treat SGMA like another drought: a physical shortage you solve by drilling deeper, chasing a new well, or squeezing more out of the same acres. That worked when groundwater was effectively unpriced.

SGMA changes the game. It turns groundwater from an open‑ended common pool into a metered, allocated, and increasingly expensive input. The 2040 sustainability deadline is set by law, and Bulletin 118 Update 2025 was released this month to update the map showing where each basin actually stands. GSA implementation budgets are now landing on pumpers. What you’ll pay depends heavily on which subbasin you sit in and how overdrafted your neighborhood has been for the last 50 years.

Fukuda’s Kaweah Subbasin is one early warning sign. Just west, the State Water Resources Control Board put the Tulare Lake Subbasin on probation in April 2024, triggering a $20‑per‑acre‑foot state fee on extractions plus a $300‑per‑well annual registration fee and 25% late charges. In Southwest Kings GSA, directors voted in early 2026 to set allocations at just 0.66 acre‑feet per acre and impose fines of $500 per acre‑foot for pumping above that allotment, with penalties kicking in on October 1. Over in the Mid‑Kings River GSA, a 2024 proposal summarized in local farm‑bureau reporting would charge shallow A and B aquifer pumpers up to $95 per acre‑foot, with overuse penalties as high as $500 per acre‑foot.

| Subbasin / GSA | Status (2026) | Base Fee | Overuse Penalty | Allocation (AF/Acre) | Risk Level |

|---|---|---|---|---|---|

| Kaweah (Fukuda GSA) | Active / Monitoring | $32–$140/AFpumping fee | Not yet published | Not yet set | 🔴 High — rapid escalation |

| Tulare Lake | Probation (Apr 2024) | $20/AF state fee + $300/well/yr | $20/AF + 25% late charge | Under probation review | 🔴 Critical |

| Southwest Kings | Active enforcement | Allocation-based | $500/AF overuse | 0.66 AF/Acre | 🔴 High — tightest allocation |

| Mid-Kings River | Proposal stage (2024) | Up to $95/AF (A/B zone) | $500/AF overuse | TBD | 🔴 High — highest base fee |

| Pixley / Lower Tule | Active / Subsidence risk | Moderate pumping fees | Moderate | TBD | 🟡 Moderate — subsidence concern |

| East Kaweah / Foothill zones | Lower overdraft history | Low–moderate | Low | Higher (less overdrafted) | 🟢 Lower relative risk |

Ag media coverage and Self‑Help’s Kaweah case study both describe farms already scrambling to find balance under SGMA — changing crop mixes, investing in recharge, and absorbing higher water costs to keep domestic and ag wells functioning. If you’re running a large dairy in Tulare or Kings, the question isn’t whether your water cost is going up. It’s how fast — and whether your per‑cow margin can take the punch.

What Does $190 Per Cow in SGMA Water Costs Actually Mean for Your Dairy?

Let’s put real numbers to it. Swap in your own volumes and herd size, but the shape of the math won’t change much.

Take a 3,000‑cow drylot dairy in Tulare County:

- Barn/parlor/cooling water: roughly 300–400 acre‑feet per year (based on regional water‑use benchmarks for large dairies).

- Feed acres: say 1,200–1,800 acres of alfalfa and silage corn under irrigation.

- Applied water rate: around 4 acre‑feet per acre — a common figure for Central Valley forage under surface and groundwater irrigation, per PPIC’s San Joaquin Valley work.

That’s 4,800–7,200 AF just for crops. Add barn water, and you’re looking at 5,000–7,500 AF per year. Use 6,000 AF as a working example.

Now layer on the fee stack.

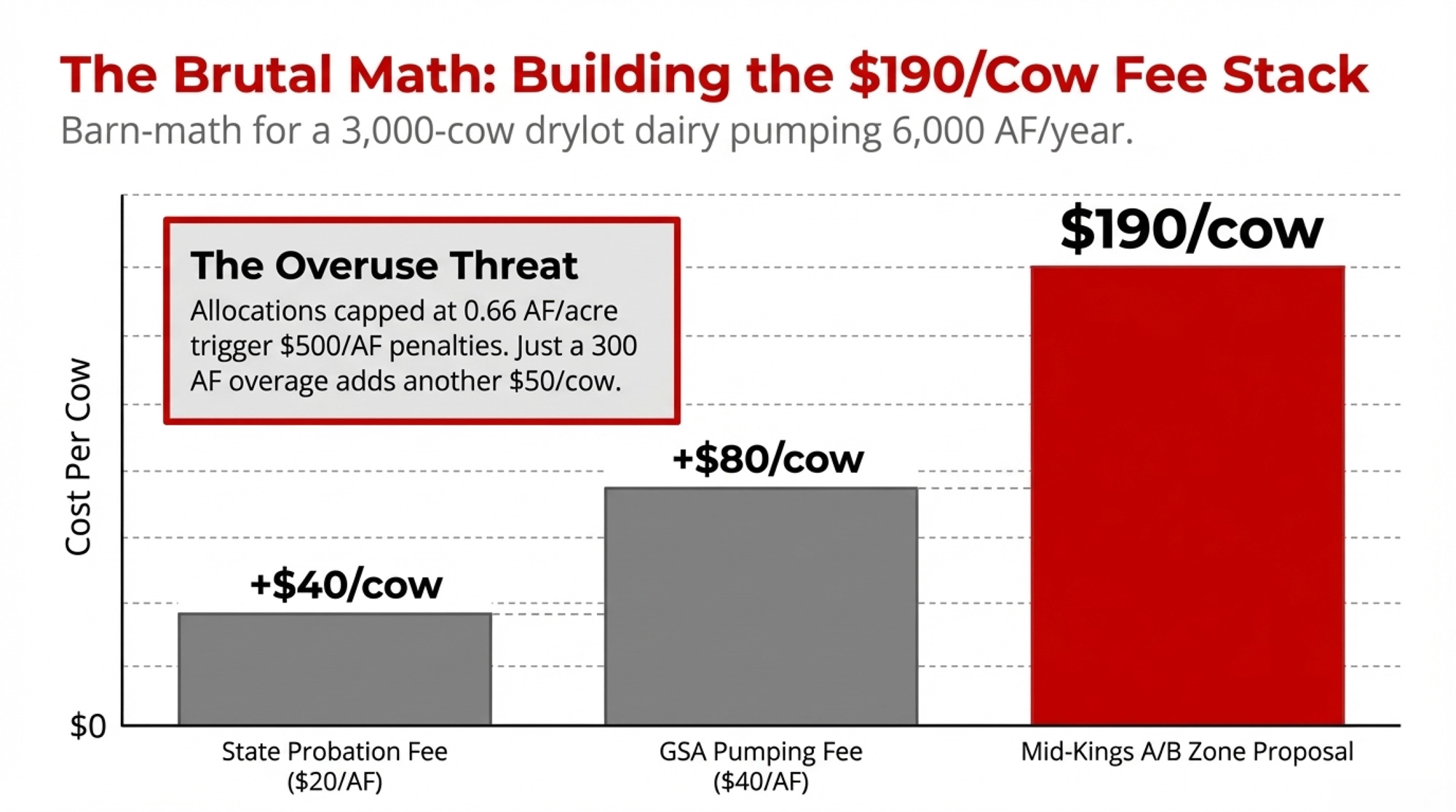

The Fee Stack on 6,000 Acre‑Feet (3,000 Cows)

| Fee scenario | Rate | Annual cost on 6,000 AF | Per‑cow cost (3,000 cows) |

| State probation fee (Tulare Lake, 2024) | $20/AF | $120,000 | ~$40 |

| GSA pumping fee (large‑pumper tier — illustrative) | $40/AF | $240,000 | ~$80 |

| Mid‑Kings A/B zone fee (proposal, 2024) | up to $95/AF | $570,000 | ~$190 |

| Southwest Kings / Mid‑Kings overuse penalty | $500/AF | Depends on overage | — |

The $190‑per‑cow figure isn’t a scare tactic. It’s what Mid‑Kings’ own “up to $95/AF” fee pencils out to when you apply it to 6,000 AF of pumping and divide across 3,000 cows. The $20/AF Tulare Lake probation fee is just the base layer. At $500/AF in overuse penalties, even a 300 AF overage adds $150,000 to your water bill — another $50 per cow on 3,000 head.

And none of that touches pump energy, well repairs, or the feed‑side hit when allocations force you to fallow acres and buy replacement tons in a tight market. If allocations drop 20% and you idle 80–100 feed acres, you’re clawing back that tonnage on the open market in the same years every other SGMA‑hit dairy is chasing forage.

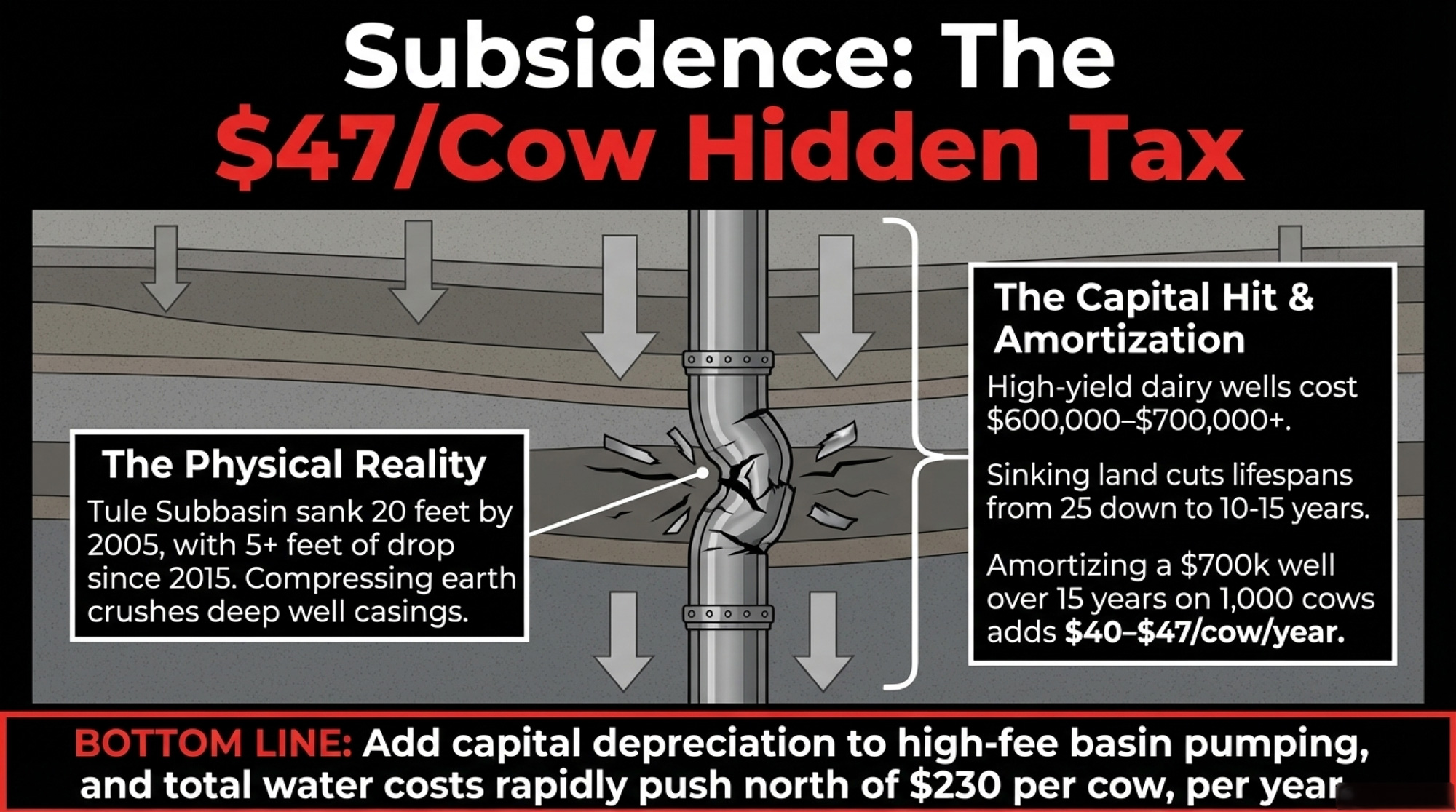

What Subsidence Really Costs Your Wells

While fees work from the top down, subsidence is chewing at you from below.

Lower Tule River Irrigation District’s “Subsidence 101” lays it out: parts of the Tule Subbasin have seen up to about 20 feet of cumulative subsidence between 1949 and 2005, with more recent InSAR and GPS data showing as much as 5 additional feet of land‑surface decline since 2015 in sections of Tule and neighboring Pixley. USGS and DWR maps confirm ongoing inches‑per‑year sinking in slices of Tulare and Kern counties, even after wet winters.

Subsidence doesn’t just bend canals. It shortens the life of your wells.

Residential well‑cost tools put basic domestic wells in Tulare County in the $3,750–$15,300 range. But commercial dairy wells are bigger, deeper, and far more complex. California farm and land‑use guidance shows that large, deep, high‑capacity ag wells can run into the hundreds of thousands of dollars, with high‑yield projects pushing toward the $600,000–$700,000+ range once drilling, casing, screens, and development are included.

Hidden cost check:

A single $600,000–$700,000 deep production well, amortized over 15 years on a 1,000‑cow herd, adds roughly $40–$47 per cow per year to your true water price — before you pay a cent in SGMA fees or power.

If subsidence damage forces you to turn wells over every 10–12 years instead of 20–25, those per‑cow numbers climb even higher.

Stack it on top of the fee math. In a high‑fee basin like Mid‑Kings or Southwest Kings, a dairy could be looking at roughly $190/cow in SGMA‑related pumping fees plus $40–$47/cow in deep‑well amortization. You’re quickly north of $230 per cow per year to keep water coming out of the pipe.

USDA ERS “Milk Cost of Production” data and recent economic reviews point to Western dairies juggling some of the highest feed, labor, and overhead burdens in the US, with relatively thin net margins once full costs are booked. When water alone is eating $200‑plus per head, it’s no longer a small line item — it’s the kind of cost that forces you to re‑run whether your current structure still competes in your region.

The Competitive Cliff: When California Efficiency Meets Idaho’s Water Bill

Some Tulare County dairies have already started shifting acreage out of feed production — moving ground into recharge basins, solar installations, and methane digester projects that Central Valley media profiled in recent years. Public reporting doesn’t track every acre, but in the examples The Bullvine has reviewed, conversions in the 15–20% range tend to start with the weakest water‑return parcels. On the surface, it looks like farming less. On the spreadsheet, it reads as capital reallocated to assets that can survive a $100‑plus/AF world.

These operations are also moving away from the question most people still default to: “Do we have enough water to keep farming here?”

In most of these basins, the answer is still “yes, at some price” — at least for the next decade or two, according to DWR and PPIC modeling. Comforting enough to push the hard decision off another year. The sharper question is this: At what water price does your cost structure stop competing — not just with the neighbor who already right‑sized, but with Idaho and Texas operators who don’t carry SGMA overhead at all?

Recent coverage from the Idaho Farm Bureau, drawing on USDA milk production data, shows Idaho and Texas trading places for the No. 3 milk‑producing state in recent years, with Idaho’s output growing by just over 3% year‑over‑year and edging back ahead of Texas into third place. Idaho’s lower land and water costs have helped attract cows and processing investment, including sizeable powder and protein capacity expansions by regional players.

But here’s the steel‑in‑the‑ground reality: processing doesn’t move as fast as cows. New or expanded dairy plants — from Idaho powder and whey facilities to large protein and yogurt projects across the US — typically take several years of capital planning, permitting, and construction before they can absorb additional milk. A dairy can, on paper, relocate in two to three years; a major new processing plant often takes closer to a decade from concept to full operation once you factor in siting, environmental review, construction, and commissioning.

On the California side, that cuts both ways. SGMA makes your water bill painful, but steel is already in the ground: cheese, powder, and high‑value fluid plants with established brands and export channels. If you’re sitting on a guaranteed, high‑value fluid or cheese contract that doesn’t exist yet in the basin you’re eyeing — or that would be much harder to secure there — paying $190/cow in SGMA‑driven water costs might still pencil out better than chasing cheap water into a shed where the co‑op can’t easily take all your milk.

| Factor | Central Valley (Tulare/Kings) | Magic Valley (Idaho) |

| Water Cost | $190–$230/cow (High Fee) | Minimal (Power + Surface Fees) |

| Regulatory Stack | High (SGMA + Air + Methane) | Moderate |

| Processing | Over-saturated but High Capacity | Tight (Limited by Steel in Ground) |

| Labor | High Cost / High Availability | Lower Cost / Lower Availability |

So the competitive cliff isn’t just “California vs Idaho water price.” It’s:

- Your all‑in water and infrastructure cost per cow,

- Plus your basis for local processing and the security of your offtake contracts,

- Minus the real cost and risk of betting your next decade on a market where processing capacity and co‑op intake rules are still being built.

| Decision Factor | Stay & Absorb | Partial Conversion | Relocate (Idaho/Texas) |

|---|---|---|---|

| Water Cost/Cow/Yr | $190–$230 (and rising) | $130–$170 (reduced acres) | Minimal (~$15–$30 power only) |

| Capital Required | Deep well: $600K–$700K | Solar dev: $0 upfront (lease) | New barn build: $2,000–$3,000/cow |

| Processing Security | ✅ High — steel in ground | ✅ High — no location change | ⚠️ RED FLAG: Intake not guaranteed |

| Feed Cost Exposure | Moderate | ⚠️ Rises when acres fallowed | Low (local forage typically cheaper) |

| SGMA Timeline Risk | High — fee curve uncontrolled | Moderate — reduces pumping exposure | Eliminated |

| 30-Year Lock-in Risk | None | ⚠️ Solar lease = 20–30 yrs | Moderate (new infrastructure) |

| Herd Value on Exit | Declines if delayed | Stable | Strong if timed well |

| Best Fit For | High-value contract holders | Mid-size operators with marginal acres | Large operators with co-op flexibility |

The Partial Conversion Play — and Where It Breaks

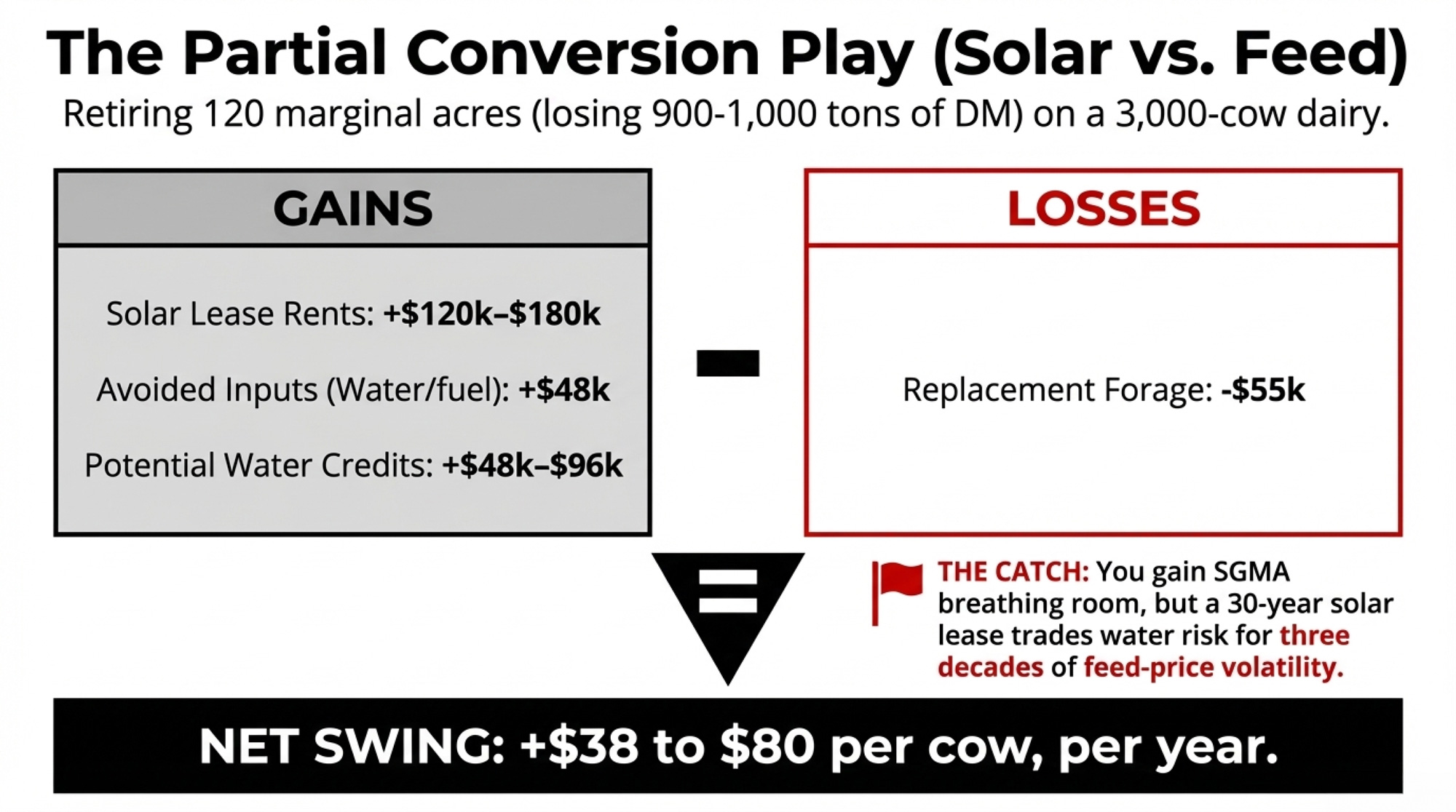

Packing up the whole herd and heading to Idaho or Texas isn’t in the cards for everyone. For many outfits, the first real move is a partial conversion of the weakest ground.

Many large California dairies are already net feed buyers. A 3,000‑cow herd farming 600 acres might grow roughly 4,650–4,950 tons of dry matter at 7.75–8.25 tons DM per acre — often only 13–15% of total herd needs once you factor in purchased hay, silage, and byproducts. Cut 120 acres — the lowest‑yield, highest‑water parcels —, and you might lose 900–1,000 tons of home‑grown DM. That’s around 2.5–3% of total herd requirements.

If replacement forage runs about $55/ton DM (a conservative figure in recent California forage markets), that’s roughly $55,000 per year in new purchased‑feed cost.

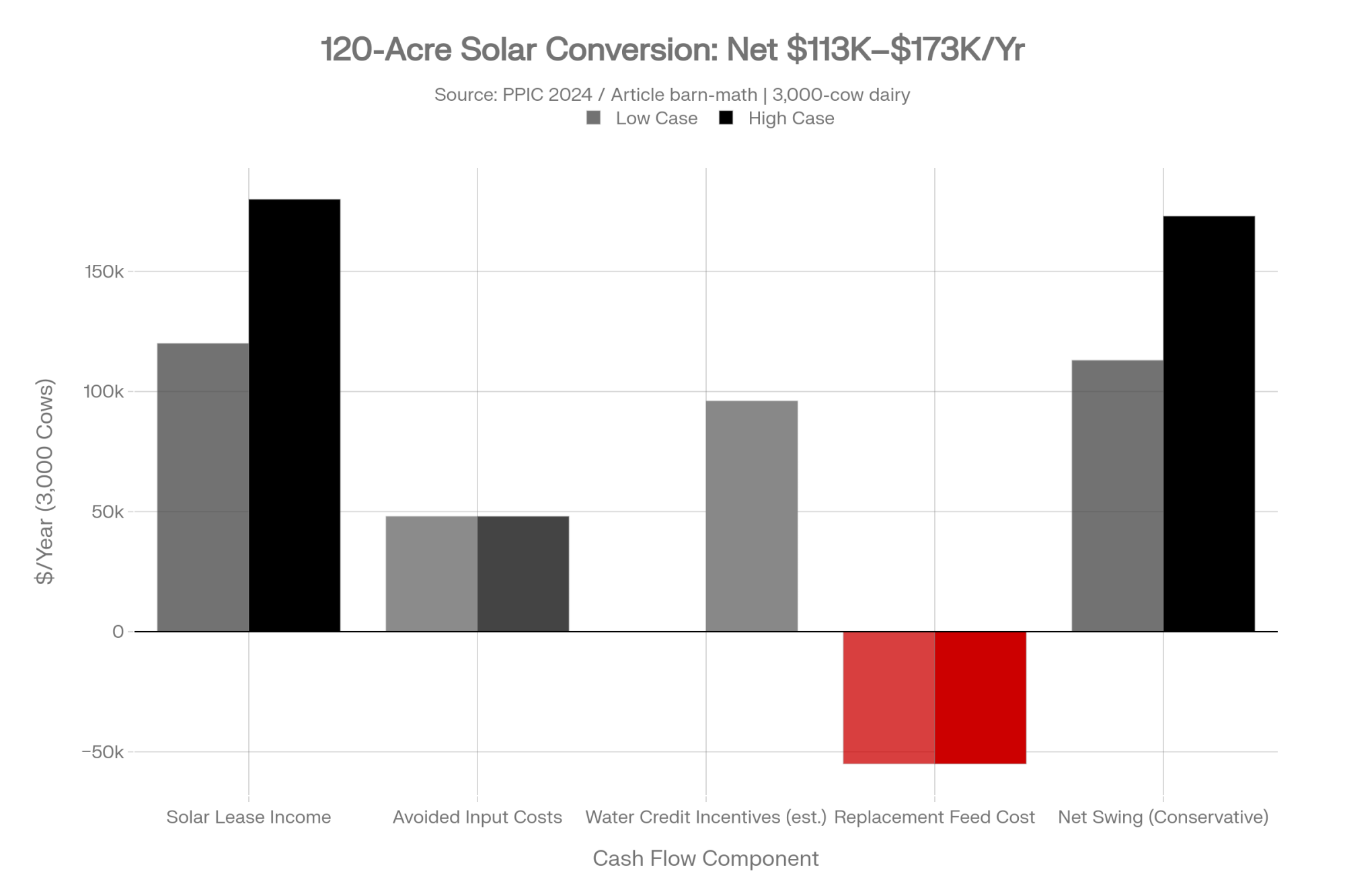

Now flip the ledger using PPIC’s January 2024 “Solar Energy and Groundwater in the San Joaquin Valley” analysis:

- Solar lease income: PPIC reports that stakeholders cite annual rents of roughly $1,000–$1,500 per acre for suitable valley sites, totaling $120,000–$180,000 per year on 120 acres.

- Avoided input costs: water, fertilizer, fuel, seed, labor — conservatively $400/acre, or $48,000 saved.

- Potential water credits: Some pilot following/recharge programs have tested incentive levels in the $100–$200 per acre‑foot range in parts of the valley. If your GSA offers similar terms and you save 480 AF (120 acres × 4 AF), that’s $48,000–$96,000 in incentive income. Not guaranteed — but worth checking with your basin.

Conservative version (solar + input savings, no water credits):

- Income: $120,000–$180,000 in lease + $48,000 avoided inputs = $168,000–$228,000.

- Extra feed cost: about $55,000.

- Net swing: roughly $113,000–$173,000, or about $38–$58 per cow per year on 3,000 cows.

If real water‑credit programs in your basin pay toward the higher end, your net could push closer to $60–$80 per cow. In some setups, that nearly offsets the SGMA fee curve on the water you still pump.

But this isn’t free money:

- A 20‑ to 30‑year solar lease means those acres are effectively gone from your forage toolbox for a generation.

- You gain SGMA breathing room but give up the option to swing those acres back into feed if policy or markets change.

- The years when your water allocation is tightest are the same years when replacement feed is most expensive — hay, silage, and byproducts all tighten together.

If you’re not lining up forward contracts or at least defined sourcing plans for that 900–1,000 tons of DM, you’re trading water risk for feed‑price volatility. Sometimes that’s still the right trade. But it’s not a simple one.

Your SGMA Water Cost Playbook: What to Do Before Summer 2026

In the Next 30 Days

- Call your GSA and get your numbers. Ask for your current extraction account balance and projected allocation schedule through at least 2030. That turns SGMA from a policy headline into a cost curve with your name on it.

- Send that schedule to your lender and accountant. Attach a single line: “I want to understand how this changes our cost structure and collateral position over the next five years.” You want your lender to consider water a capital constraint before the next renewal, not after.

- Run your water‑per‑cow check. Add up the last 12 months of water‑related spending — GSA fees, state probation fees, pump power, well service, SGMA penalties, replacement feed on fallowed ground. Divide by the average head count. That’s your current water cost per cow/year.

If your lender can’t yet explain how they’re pricing SGMA risk into your loan, that’s not a reason to relax. It’s your reminder to start the conversation.

In the Next 90 Days

- Break water out as its own budget line. Pull it out from “repairs” and “utilities.” Track: (1) GSA fees, (2) state SGMA probation fees, (3) power for pumping, (4) well service and repairs, (5) replacement feed tied to the fallowing. Until it has its own line, you can’t manage it.

- Rank your acres by return per acre‑foot. Simple buckets — strong, middle, marginal — based on yield and gross margin per AF. Your marginal bucket becomes your candidate pool for solar, recharge, or sale.

- Get real solar lease indications, not coffee‑shop numbers. Ask developers about term length, annual rate, escalator, who pays for decommissioning, and how interconnection timelines look in your area. Proximity to transmission and substation capacity can kill an otherwise good lease.

Policy on the Williamson Act, solar on farmland, and SGMA compliance is still moving forward. If rules shift to make it easier to convert non‑viable irrigated acres, early movers often have more leverage to shape lease terms than the fifth guy to call.

In the Next 12 Months

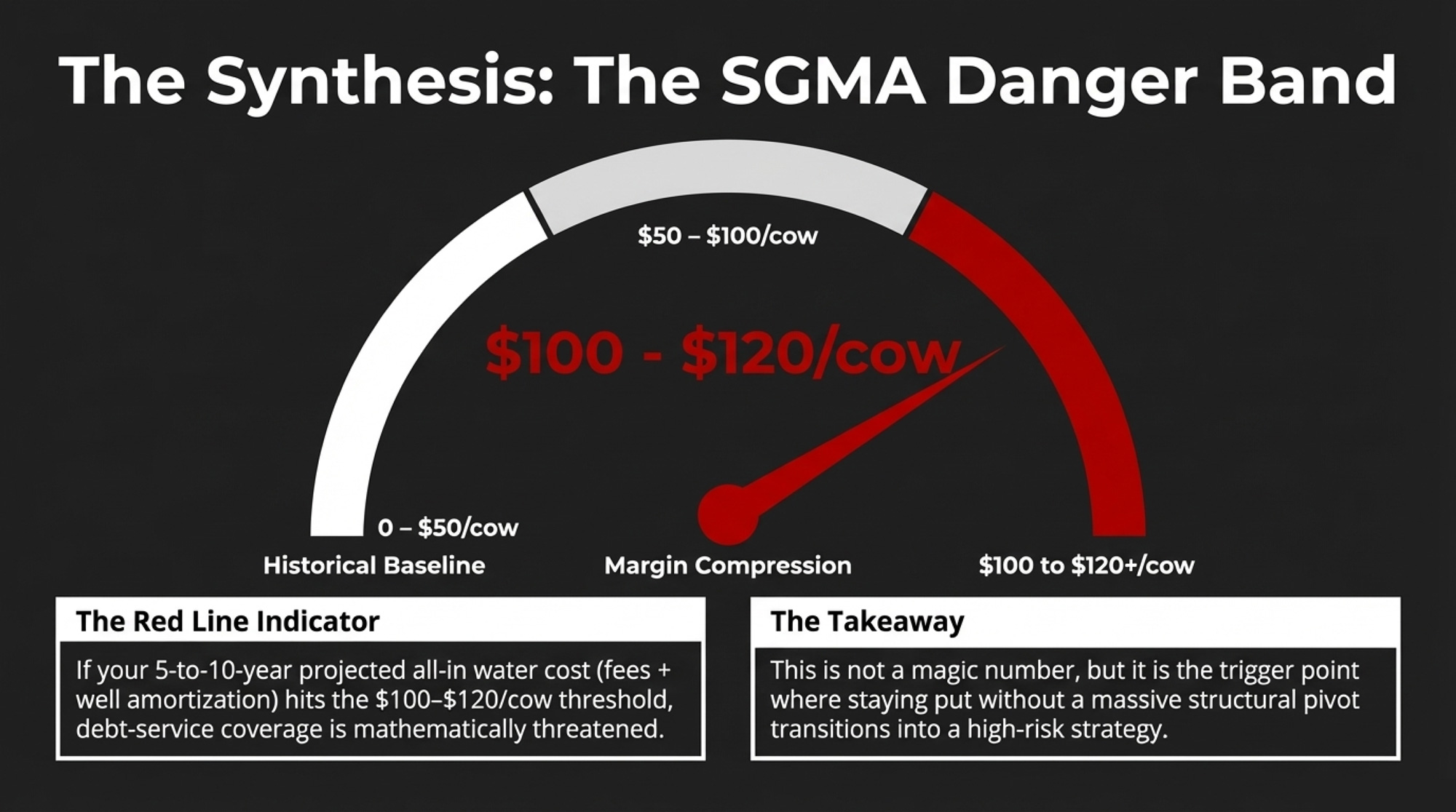

- Stress‑test your herd at three water prices: $80/AF, $120/AF, $150/AF. Use your actual pumping volumes. Translate each scenario into $/cow/year and into your debt‑service coverage ratio. Where does the math start to fail?

- If you’re trending toward $100–$120 per cow per year in all‑in water cost on a 5‑ to 10‑year view, schedule a relocation feasibility meeting. Not a commitment. A meeting — you, your accountant, your lender, and someone who’s actually built barns in a lower‑cost state. Look at capital cost per cow, co‑op access, packer/processor options, cull values, and realistic timing.

- If you’re in the 800–1,500‑cow band on the hardest‑hit basins, run exit math now. Smaller herds have less scale to spread rising SGMA fees and deep‑well costs, and less collateral to support a full relocation. A deliberate, timed exit while herd values are still decent can beat a rushed sale after covenants are already under stress.

What This Means for Your Operation

- Water is no longer a background condition. It’s an input with a unit cost. Until it sits on its own line on your P&L, you’re underestimating it.

- Your water‑per‑cow number is now a key KPI. If you can’t write it down today, your first task isn’t to argue policy — it’s to pull your bills.

- Partial conversion can free up roughly $38–$80 per cow per year in the right setup — but only if you lock in lease income, understand your basin’s incentive programs, and secure replacement feed before you sign a 20‑year solar deal.

- Relocation is a spreadsheet question, not a moral one. If water alone is eating a third to half of your average‑year margin on a forward view, you owe it to your family and your lender to at least compare that picture to a different geography.

- Processing steel matters as much as the price of water. Cheap water without committed plant capacity can strand your milk just as surely as expensive water under a rock‑solid, high‑value contract can keep your dairy viable.

- Your most important SGMA conversation this spring is with your lender. Bring real allocation schedules, a water‑per‑cow number, and a rough plan for your weakest acres — instead of waiting for the next appraisal to dictate the options.

Key Takeaways

- If your all‑in water costs are trending toward $100–$120 per cow per year on a 5‑year projection, you’re in the range where this analysis says staying put without a plan starts to look like a high‑risk strategy. That threshold is the article’s working definition of the danger band — not a magic number, but a line worth testing against your own books.

- SGMA’s real threat isn’t that California runs out of groundwater — it’s that you get priced out of using it. The state still has over a billion acre‑feet of storage capacity, per DWR’s Bulletin 118 Update 2025. The bill is what’s changing.

- Cutting 20% of your weakest feed ground can improve cash flow — but only if lease income, incentives, and replacement feed are nailed down ahead of time. Otherwise, you’re swapping one form of volatility for another.

- Before you chase cheaper water out of state, put your current SGMA bill beside your contract security and local plant capacity. A painful $190‑per‑cow water line can still beat cheap water feeding into an oversupplied shed with shaky intake rules.

The Bottom Line

The Tulare County dairies that shifted 20% of their ground out of feed production weren’t chasing a green label. The moves read as accounting choices — capital redirected into assets that can withstand SGMA pricing and subsidence, rather than assuming water costs will remain where they are today. Pull up your own last 12 months of water spending, divide by your herd size, and put that number beside your feed cost per cwt. If you don’t like the gap between those two lines, that’s your real SGMA deadline — and it’s already running.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – Strips away the noisesurrounding the current oversupply, showing how beef-on-dairy income is hiding dangerous management gaps. You’ll secure your 2026 bottom line with a precise culling strategy that prioritizes genetic value over temporary calf premiums.

- The $100 Springer Gap: Dairy Farm Relocation Is Moving America’s Milk Map to I-29 – Exposes the cold, hard math of the Great Migration. It arms you with a 90-day decision framework to weigh your California processing security against the raw economic pull of the I-29 corridor’s abundant feed and water.

- The Next Frontier: What’s Really Coming for Dairy Cattle Breeding (2025-2030) – Unlocks the profit potential of “Designer Milk.” You’ll gain a biological edge by integrating feed-efficiency genetics and genomic health traits that turn environmental compliance from a cost center into a high-margin, market-beating asset for your herd.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.