AMPI’s Paynesville plant is dark. Its biggest member sells milk to five other processors. You sell to one. Same co-op. Guess who has a backup plan.

Executive Summary: At 10 a.m. Saturday, 18-year AMPI lab tech Heidi Barg walked out of the Paynesville, Minnesota cheese plant — and a $51,000-a-day clock started ticking for 685 farmer-owners who got zero warning. Teamsters Local 471 declared a formal Unfair Labor Practice strike after nearly a year of rejected demands for better wages, health-care flexibility, and a guarantee that jobs survive if AMPI sells the plant. With the facility processing 1.7 million pounds of milk daily and Midwest spot running $3-under, a 30-day shutdown burns through $1.53 million in co-op revenue — on top of margins that were already negative before a single picket sign went up. AMPI’s largest member, Riverview LLP, ships to five processors and is building its own 4-million-lb/day powder plant 90 miles away; most family-scale members ship to one plant and have no backup. Under Minnesota cooperative law, the board may have no legal obligation to warn you — a governance blind spot that seven Ontario farmers cracked open in 2020, when a single public letter forced province-wide reform. Below: the per-herd loss math, the statutory rights most co-op members don’t know they have, and the one action you can take before your next district meeting.

Just before 10 a.m. on Saturday, March 21, Heidi Barg hung up her lab coat at the AMPI cheese plant on West Railroad Street in Paynesville, Minnesota, and walked out to the picket line. She’s spent 18 years in that lab, testing the milk that 685 farm families ship into the cooperative every day. A few minutes later, the rest of her co-workers in Teamsters Local 471 — more than 60 employees in all — followed her out, and AMPI’s highest-capacity cheese plant went dark.

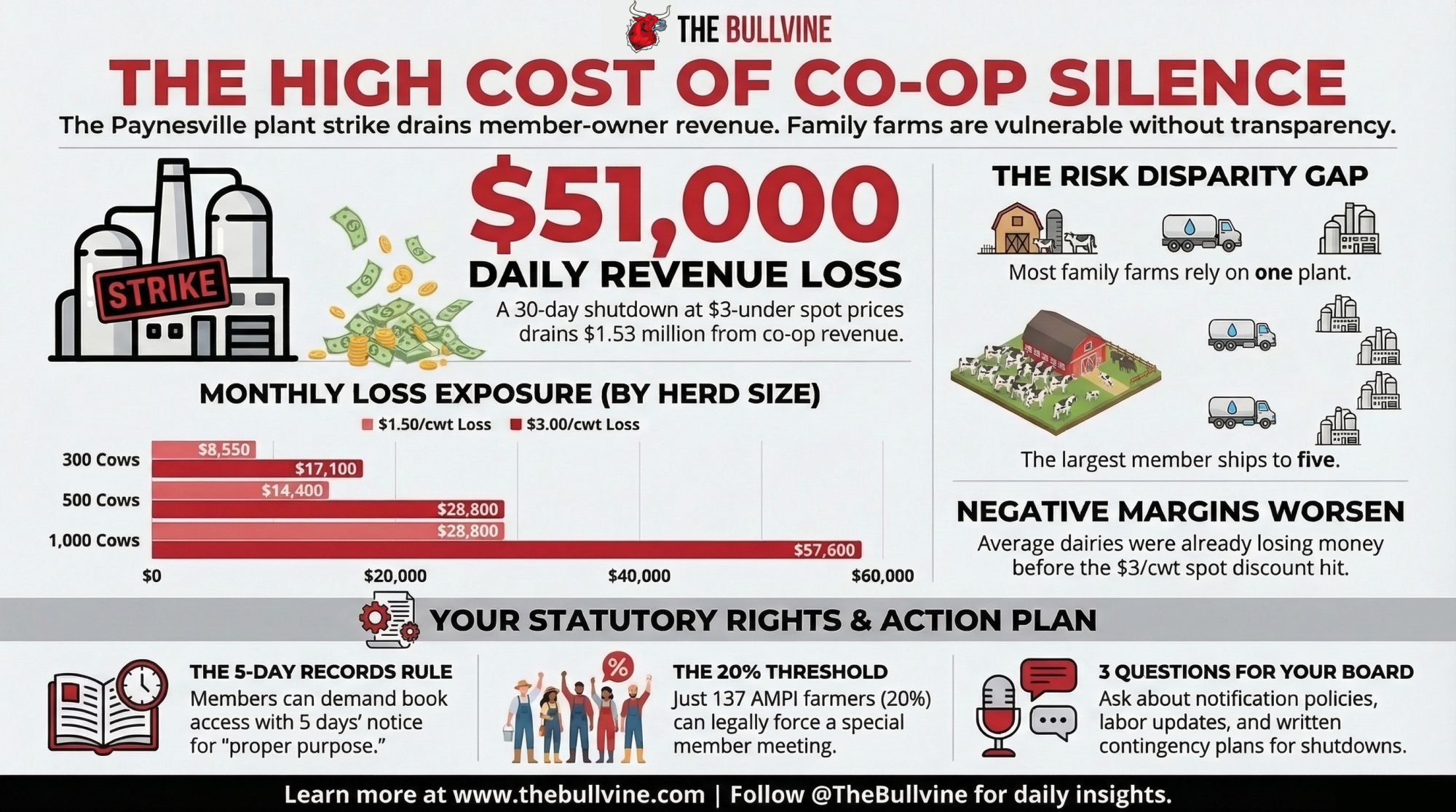

While the lab coats hit the pavement, the clock started ticking — $51,000 a day in lost milk value at the March 19 spot floor, and up to $1.53 million if $3-under conditions persist for a month. That’s a hole your milk check is expected to fill.

“When I started at AMPI 18 years ago, this was a place where people built successful careers in a small town to support their families,” Barg said. “Too many now see it as just a job, and that has been tough for me to watch”.

Eighteen years of institutional knowledge about milk quality, cheese yields, and production standards — gone from the plant floor in a single morning. And there’s no sign that any of AMPI’s 685 farmer-owners received a real warning that their plant was one step from going dark.

How Did a 12-Month Standoff Turn Into a Surprise Shutdown?

This didn’t start with a one-day blow-up. It started in April 2025, when Paynesville workers — who’d spent 50 years under an independent union — voted 71 to 1 to affiliate with Teamsters Local 471. They believed the Teamsters would give them “the leverage, resources, and collective power necessary to bargain the best contract possible”.

Since then, it’s been a long, slow grind. Workers came to the table asking for a meaningful wage increase after more than a year without a raise, more flexibility in health care coverage, and a guarantee that, if AMPI sells the plant, their jobs and union contract will go with it. AMPI said no on all three.

“AMPI has had more than enough time to do right by these workers, but instead they’ve dragged their feet,” said Lyndon Johnson, Secretary-Treasurer of Local 471. “Our members are united in demanding the wages, health care, and job protections they deserve. We’re prepared to stay out as long as it takes”.

Local 471 has called this a formal Unfair Labor Practice strike — meaning they believe they can prove AMPI hasn’t been bargaining in good faith. That’s a legal accusation that builds over months of bargaining records, not one bad meeting. And the dairy labor crisis driving these negotiations isn’t unique to Paynesville.

Three Facilities, One Pattern

| Facility | Product | What Happened | Workers Affected | Timeline | Member Impact |

|---|---|---|---|---|---|

| Paynesville, MN | Cheese | ULP strike — plant went dark | 60+ Teamsters Local 471 | March 21, 2026 | 685 farmer-owners lose outlet for 1.7M+ lb/day |

| Blair, WI | Cheddar → Cottage Cheese | Conversion retool — temporary layoffs | 86 employees | Layoffs start March 31, 2026; reopen early 2027 | Milk rerouted during 9–12 month gap |

| New Ulm, MN | Butter | Sold to Grassland Dairy Products | 185 employees transferred | Late 2025 | AMPI exits butter; “focuses on core business = cheese” |

Paynesville isn’t AMPI’s only moving piece. In Blair, Wisconsin, AMPI is converting its cheddar plant into a cottage cheese facility — temporarily laying off 86 workers starting March 31, with a reopening planned for early 2027. In New Ulm, Minnesota, AMPI sold its butter plant to Grassland Dairy Products in late 2025. AMPI Marketing VP Sarah Schmidt confirmed that 185 employees had transferred, saying the sale would allow AMPI “focus on its core business, which is cheese.”

If you’re a Paynesville worker watching AMPI shut one plant and retool another, you’re going to ask for a guarantee that your facility won’t be sold next. Workers asked for exactly that. Management refused.

AMPI did not respond to a request for comment regarding the strike.

What Does It Actually Cost When Your Co-op Plant Goes Dark?

When a plant shuts down, your cows don’t. Milk has to move. And in late March 2026, it’s moving into one of the ugliest spot markets in recent memory.

USDA’s Agricultural Marketing Service reported Midwest Class III spot milk trading at $ 3 under to flat the week of March 19. One week earlier, the Central region spot was $ 5 under to flat, and cheesemakers were “unable to take on additional volumes of milk, as they are already running full schedules.” A March 17 snowstorm across the Upper Midwest made hauling even messier.

Teamsters say the plant was running about 1.7 million pounds of milk per day — roughly 17,000 cwt. AMPI’s own 2025 summer tour materials claim Paynesville can process up to 4 million pounds daily — though the plant’s last publicly documented capacity upgrade, reported by Farm Progress in January 2023, put the figure at 3 million pounds. However you measure it, a lot of milk just got orphaned.

At the co-op level: 17,000 cwt/day × $3.00 spot discount = $51,000 per day in lost value. Thirty days at $3-under is $1.53 million in cooperative revenue that isn’t coming back.

| Herd Size | Daily Milk (cwt) | Monthly Loss ($1.50/cwt) | Monthly Loss ($3.00/cwt) |

| 300 Cows | 190 | $8,550 | $17,100 |

| 500 Cows | 320 | $14,400 | $28,800 |

| 1,000 Cows | 640 | $28,800 | $57,600 |

Note: Spot discount losses only. Additional hauling costs (estimated at 20¢/cwt for diversions over 200 miles) would add roughly $1,100–$3,800/month, depending on herd size.

Why the Timing Couldn’t Be Worse

Those dollars land on a base market that’s already bleeding. February’s WASDE put the 2026 all-milk price at $18.95/cwt. ERS estimates the average total cost of production at $19.14/cwt — meaning the average dairy started 2026 losing money before the first truck left the yard. January’s actual Class III came in at $14.59/cwt, the lowest since July 2023. FarmDoc Daily’s December 2025 analysis projected that “economic costs are projected to be above total returns in 2026.”

You’re already underwater. Stack a $3-under spot discount on top of that, and this stops being an academic conversation.

The Member Who Doesn’t Have to Worry — And Why That Should Worry You

Now ask a harder question: who in this cooperative can actually ride out a plant shutdown?

| Metric | Small/Mid Family Dairy | Riverview LLP |

|---|---|---|

| Approximate herd size | 280–1,000 cows | 135,000+ cows (16 MN feedlots) |

| Milk processors used | 1 | 5 |

| Own processing capacity | None | 4M lb/day powder plant under construction (Morris, MN; startup Nov 2027) |

| Strike/shutdown backup plan | None — diverts to spot market at $3-under | Routes volume to 4 other buyers same day |

| Est. 30-day loss if Paynesville dark | $17,100–$57,600 (spot discount only) | Near zero — volume absorbed elsewhere |

| Hauling cost exposure | +$1,100–$3,800/month at $0.20/cwt | Negligible — contracts with multiple plants |

| Co-op governance influence | Attends district meeting | AMPI featured Riverview on summer tour brochure |

| Long-term co-op dependency | High — one plant, one check | Declining — exit ramp under construction |

Riverview LLP, based in Morris, Minnesota, is the state’s largest milk producer — and it’s not close. According to state feedlot records cited by the Star Tribune on March 16, 2026, Riverview now owns 16 permitted dairy feedlots in Minnesota, housing more than 135,000 cows. The company is also permitted for two North Dakota mega-dairies currently under international environmental review after Manitoba flagged potential nutrient impacts on the Red River watershed.

Riverview is an AMPI member. In 2025, AMPI’s own “Future Focused” summer tour bused visitors to the Paynesville cheese plant, then to Louriston Dairy, a 9,500-cow Riverview operation near Murdock. The co-op literally put Riverview on the brochure.

But Riverview doesn’t need AMPI. As of a late-2024 Red River Farm Network tour, Riverview was selling milk to five different cheese processors. If Paynesville goes dark for a month, Riverview shifts volume to four other buyers before your truck has figured out where to go. And in July 2025, Riverview broke ground on the Stevens Milk Plant — a 148,000-square-foot powder facility in Morris that will process 4 million pounds of milk per day. Startup: November 2027. That’s at or above what AMPI says Paynesville can handle.

Nobody’s saying Riverview shouldn’t build its own plant — they’re managing their own risk, same as you should be managing yours. The question is what it means for the members who can’t. You’re subsidizing the overhead on a plant that Riverview is building an exit ramp from. We broke down the full math on what Riverview’s expansion means for Upper Midwest pricing last week — and this strike makes that analysis hit different.

Two realities under the same “farmer-owned” banner:

- A 280-cow Stearns County family dairy with one truck, one plant, one milk check.

- A 135,000-cow-plus member with milk going to five processors and its own powder plant under construction.

Same co-op. Wildly different risk universe. And the consolidation dynamics reshaping cooperative processing aren’t slowing down.

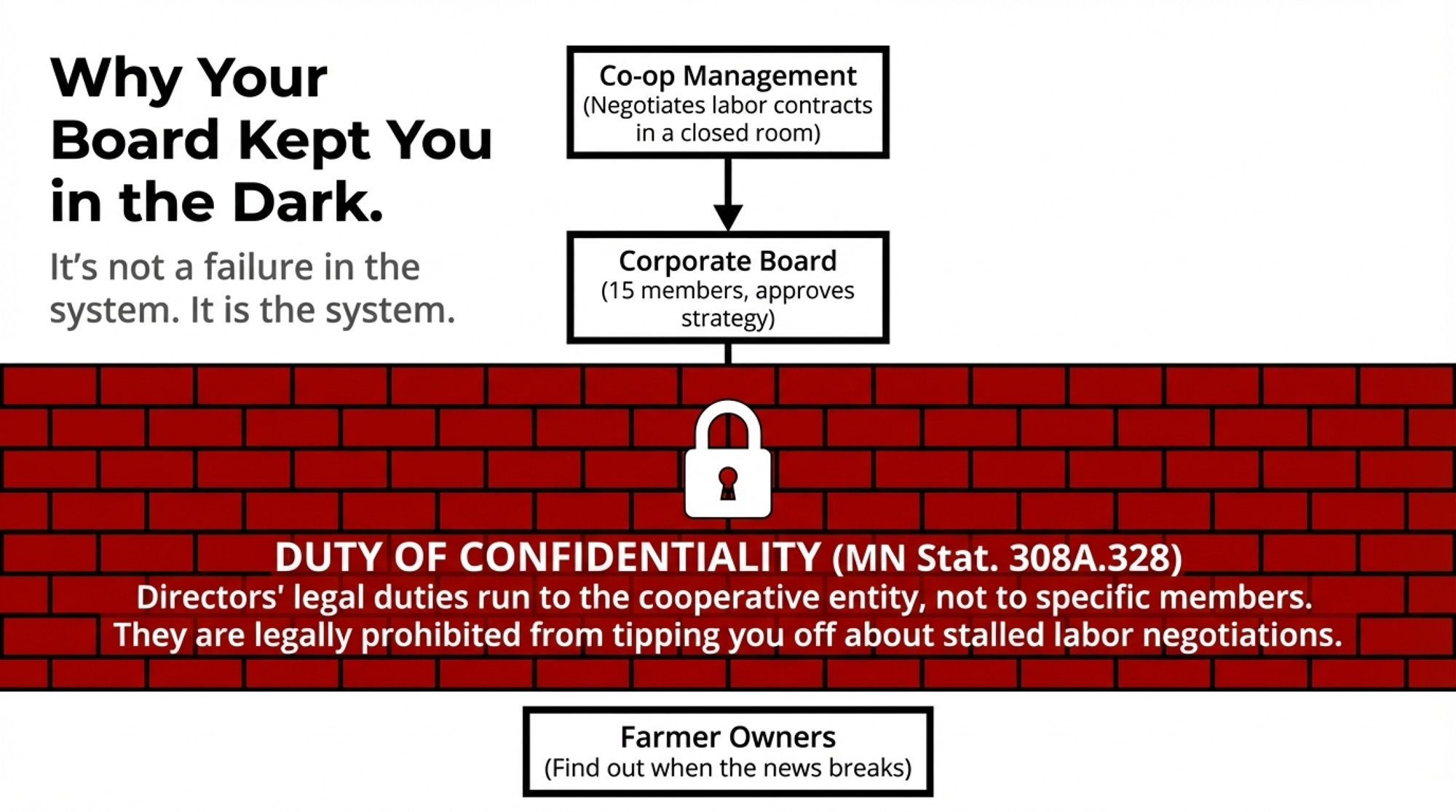

Why Your Co-op Board May Be Legally Required to Keep You in the Dark

AMPI runs a three-tier governance system. You go to district meetings. District reps go to division meetings. Division reps elect a 15-member corporate board on three-year terms. The board oversees management. Management negotiates labor contracts.

There’s no standing labor relations committee you elect. No bylaw trigger that says “if a negotiation drags past 180 days, members get notified.” Nothing.

Minnesota Statute 308A.328 says directors must act “in good faith, in a manner the director reasonably believes to be in the best interests of the cooperative.” Those duties run to the cooperative as a legal entity — not to specific members. Directors can rely on management reports they “reasonably believe to be reliable and competent.” On top of that, directors carry a duty of confidentiality on labor and legal strategy that may actually prohibit them from tipping you off at a district meeting.

Management runs it. The board approves it in a closed room. You find out when the news breaks. That’s not a failure in the system. That’s the system.

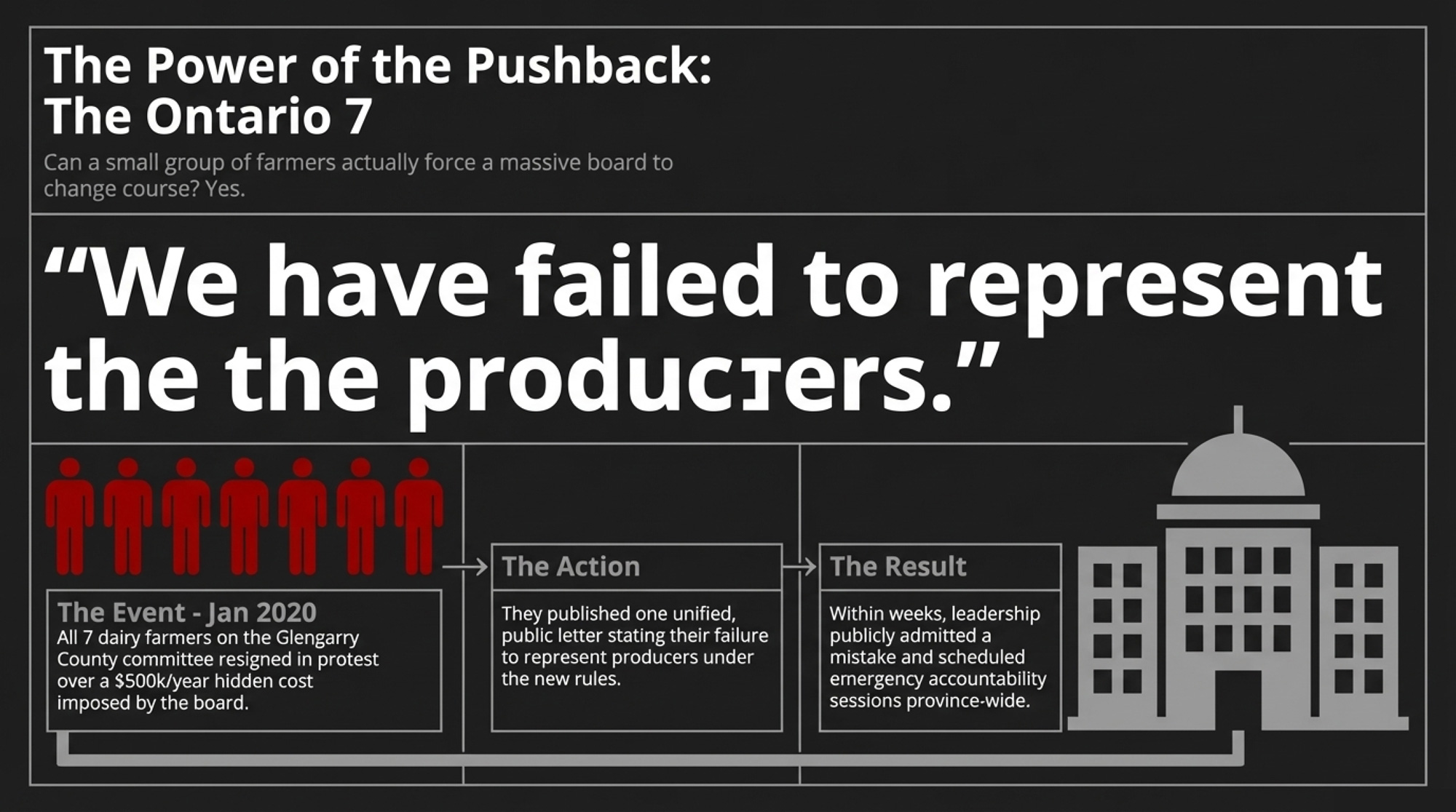

What Happened When Seven Ontario Farmers Said “Enough”?

In January 2020, all seven dairy farmers on the Glengarry County milk producer committee in eastern Ontario resigned at once. Their target: Dairy Farmers of Ontario, which had unilaterally switched to third-party verification for its proAction quality program without consulting any of the province’s 48 local committees.

Their letter didn’t mince words: “We have failed as a committee to represent the producers that have elected us.” They estimated the switch would cost Ontario producers at least $500,000 a year on top of what they called “millions and millions” already spent, with absolutely zero to show for it.

Seven farmers. One public letter. Within weeks, DFO board member Bart Rijke told the farm press, “Maybe we made a mistake.” Leadership reached out to committee chair Melanie Trottier. DFO scheduled emergency sessions with all 48 committees. Trottier and six neighbors changed the conversation province-wide. You don’t have to resign from anything. But Glengarry proves that coordinated, specific pushback from a small number of members can move organizations that usually feel untouchable. And when cooperative accountability actually works, it changes what’s possible for the whole community.

Does Your Co-op Have the Same Blind Spot?

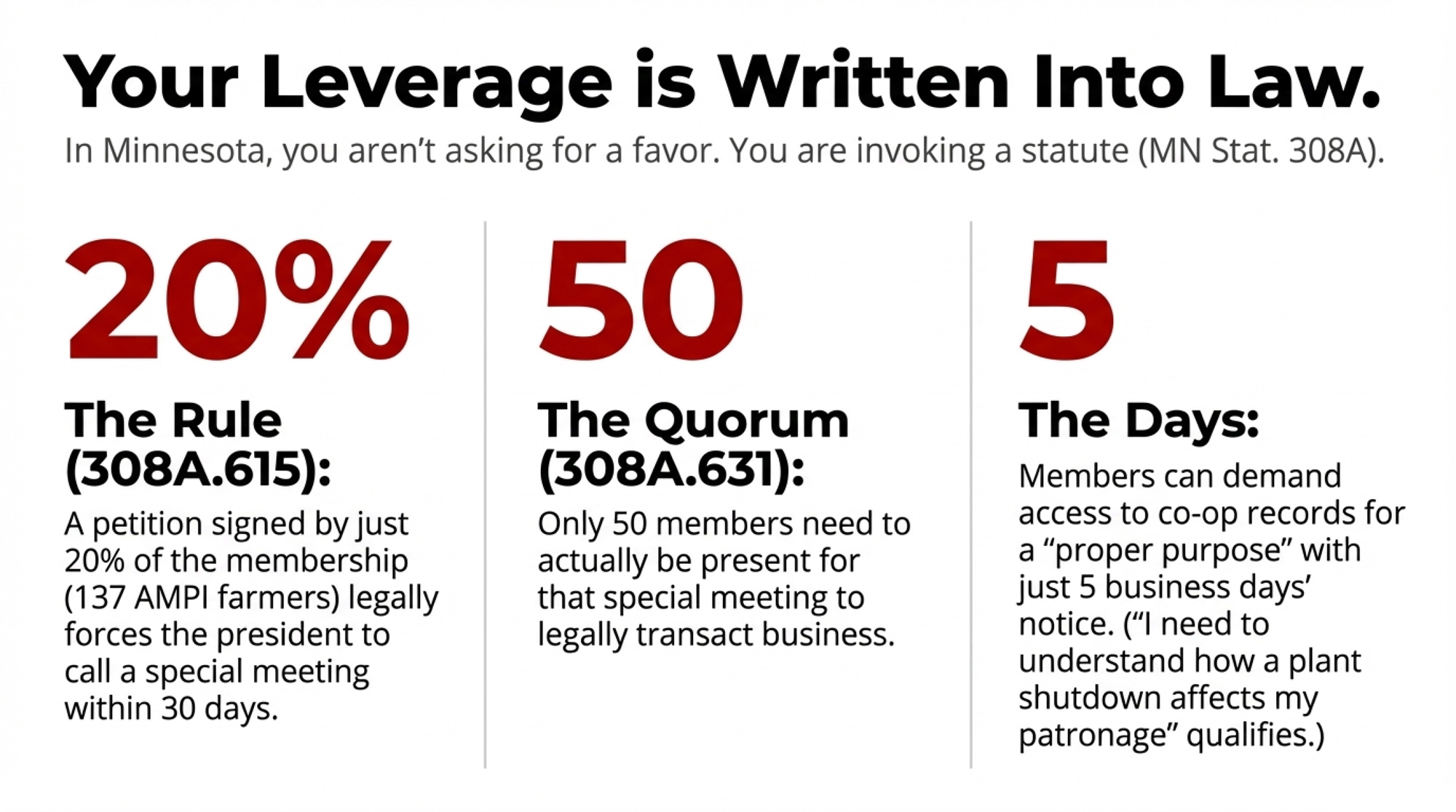

In Minnesota, your leverage is written into law. Most members just haven’t read the statute.

| Tool | Statute | Threshold | Timeline | What It Forces |

|---|---|---|---|---|

| Records Inspection | MN 308A (records access) | Any single member, written request | 5 business days after certified notice | Board must disclose financials relevant to your “proper purpose” — e.g., patronage impact of plant downtime |

| Special Member Meeting | MN 308A.615 | 20% of membership = 137 AMPI farmers | Board must call meeting within 30 days | Forces full membership discussion of any governance issue, including labor crisis transparency |

| Quorum to Transact Business | MN 308A.631 | 50 members present | At any duly called meeting | Meeting can vote on resolutions, bylaw amendments, or formal demands — 50 farmers is enough |

| Bylaw Amendment | Standard co-op governance | Majority vote at qualified meeting | Variable — next district or special meeting | Can add mandatory notification trigger (e.g., “board alerts members if labor talks exceed 180 days unresolved”) |

The 20% Rule: Under 308A.615, a petition signed by 20% of the membership — that’s 137 AMPI farmers — forces the president to call a special meeting within 30 days.

The Quorum Factor: Under 308A.631, only 50 members need to be present for the meeting to transact business.

The 5-Day Rule: Members may demand access to the cooperative’s books and records for a “proper purpose” with 5 business days’ written notice. “I need to understand how a plant shutdown is affecting my patronage allocation” is about as proper as it gets.

You’re not asking for a favor. You’re invoking a statute.

What’s Your Actual Monthly Exposure If Your Plant Goes Down?

Plug your own herd into the formula:

Your daily cwt × spot discount ($/cwt) × days offline + extra hauling cost = your monthly strike exposure.

At 500 cows shipping 320 cwt/day with spot $2-under and 20¢ in extra hauling: (320 × $2.00) + (320 × $0.20) = $704/day. Over 30 days: $21,120. That’s why the question for AMPI members isn’t just “Are workers being treated fairly?” It’s “How much is this costing my farm, and did anyone tell me we were getting close to this?”

Even if you’re nowhere near Paynesville, at your next meeting, ask three questions:

- Does our cooperative have any policy requiring member notification when a contract negotiation drags past a set point?

- When was the last time the board gave members a plain-English update on labor relations at each plant?

- What’s our written contingency plan — and member cost estimate — if any plant goes offline for 30, 60, or 90 days?

If nobody has answers, you’ve found the blind spot.

Options and Trade-Offs for Farmers

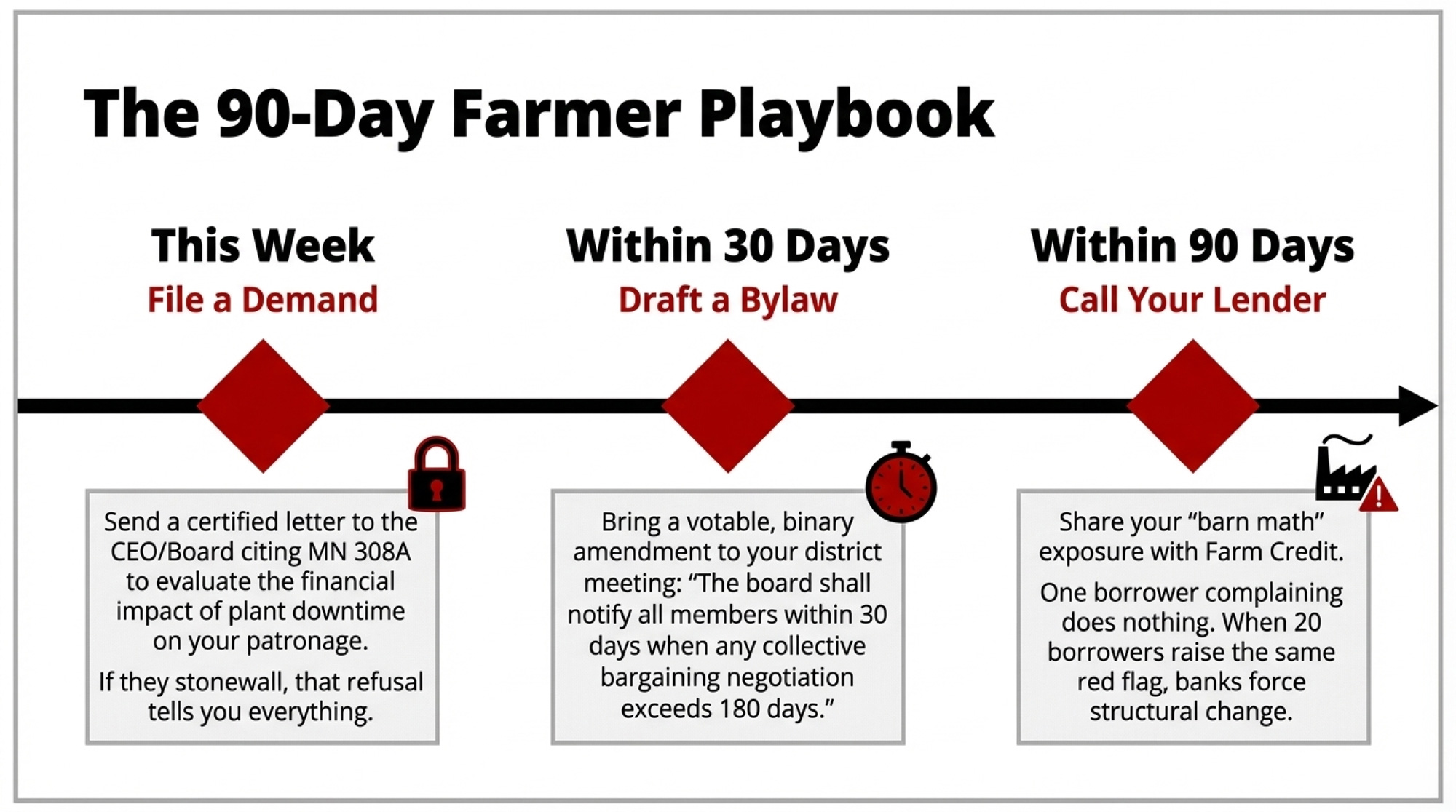

This Week: File a Records Inspection Demand

Write a short letter stating your proper purpose — evaluating the financial impact of plant downtime on your patronage — and cite Minnesota 308A. Send it certified mail to the CEO and board secretary. They have five business days. If they comply, you learn what the board knew and when it knew it. If they stonewall, that refusal tells you everything. Total cost: postage.

Within 30 Days: Draft a Bylaw Amendment

Something binary and votable. Example: “The board shall notify all members within 30 days when any collective bargaining negotiation at a cooperative facility exceeds 180 days without resolution.” Bring it to your district meeting, on the record. Management will argue disclosure hurts negotiating leverage — and they’re not entirely wrong. But the question isn’t whether to live-stream bargaining on Facebook. It’s whether member-owners deserve a heads-up before their plant goes dark.

Within 90 Days: Bring Your Lender Into the Conversation

Share your barn-math exposure with Farm Credit or your bank. Ask how they evaluate processor concentration riskwhen they underwrite your operation. One borrower raising the flag does nothing. 20 borrowers raising it with the same lender start to move things.

Within 12 Months: Decide If the Needle Moved

Did the board start reporting on labor status? Did they respond to your records demand? Remember: 137 members force a meeting. Fifty make it legal.

Key Takeaways

- If your plant could go dark, run your own diversion math this week. Your daily cwt × spot discount × 30 days, plus hauling. For a 300-cow herd at $3-under, spot losses alone hit $17,100 over a month — add hauling, and you’re near $18,200.

- If your co-op has no notification trigger for stalled labor talks, the gap isn’t the strike — it’s the silence.Ask, on the record.

- If you don’t know your statutory rights, learn them before you need them. Minnesota: five days for records, 20% for a special meeting, 50 for a quorum.

- If your largest member is building its own plant, pay attention. When they no longer need the co-op, you’re the one paying for the empty capacity.

The Bottom Line

Heidi Barg walked out of that Paynesville lab Saturday morning after 18 years of testing your milk and your neighbors’ milk. Melanie Trottier and six Ontario farmers proved that names on a letter can force a marketing board to sit down and listen. The tools exist. The statutes are on the books. The barn math is real.

The Paynesville strike isn’t just a labor dispute. It’s a transparency stress test. AMPI just failed. Is your co-op next?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- $18.95 Milk, $19.14 Costs: USDA’s 2026 Milk Price ‘Upgrade’ Still Leaves Your Dairy in the Red – Stops you from guessing and arms you with a 30-day survival playbook. It breaks down the brutal $19.14 production cost reality, revealing why relying on government checks is a high-risk strategy for 2026.

- The $11 Billion Reality Check: Why Dairy Processors Are Banking on Fewer, Bigger Farms – Exposes the $11 billion processor shift that is quietly locking out mid-size dairies. You’ll gain a clear-eyed strategy for positioning your farm before the 2026-2027 shakeout permanently consolidates 40% of the industry.

- Riverview’s 18,855-Cow Bet: The $0.60/cwt Drain That Won’t Show Up on Your Milk Check – Delivers the hidden math behind the world’s largest dairy expansions. It reveals how massive sites like West River manipulate hauling and basis, giving you the foresight to protect your milk check from invisible drains.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.