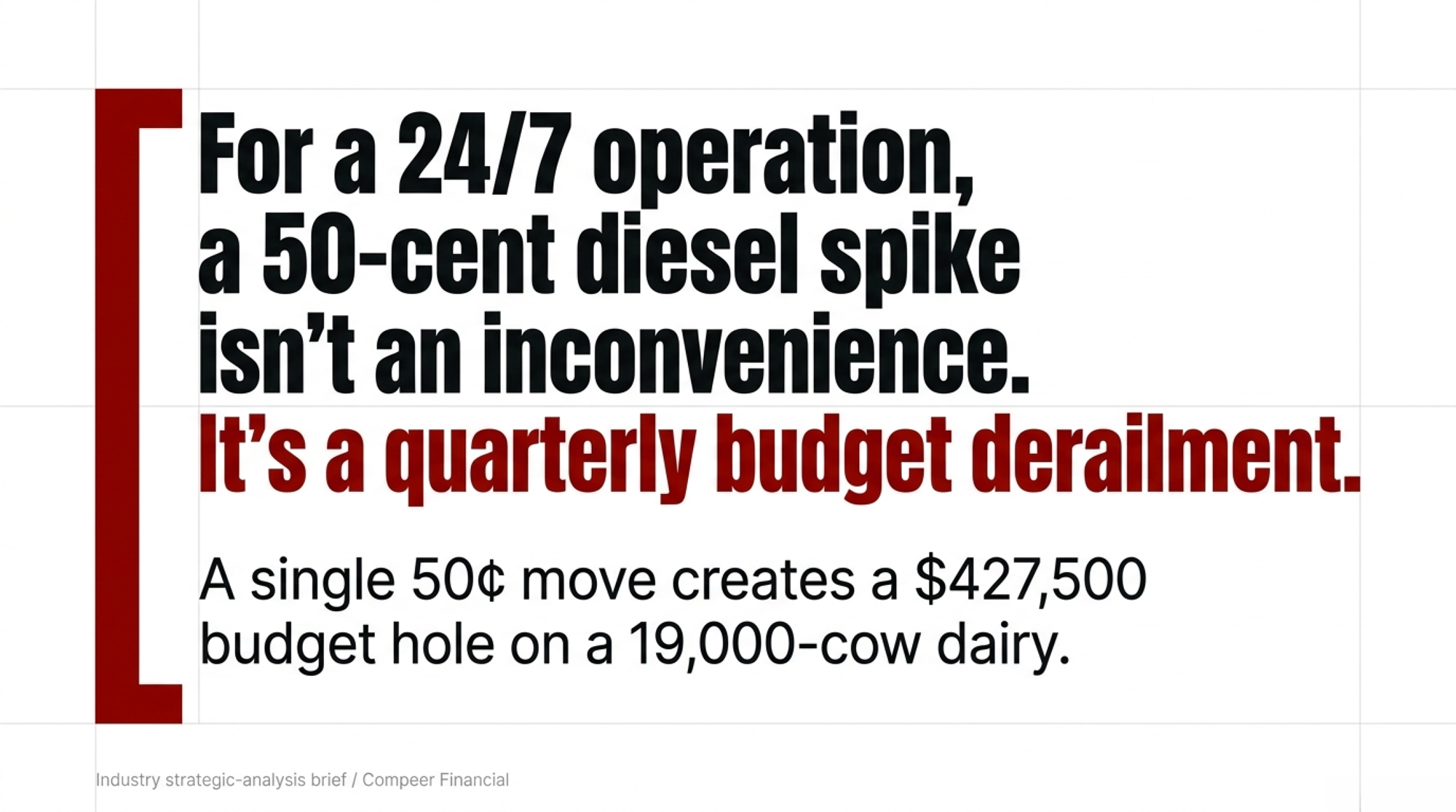

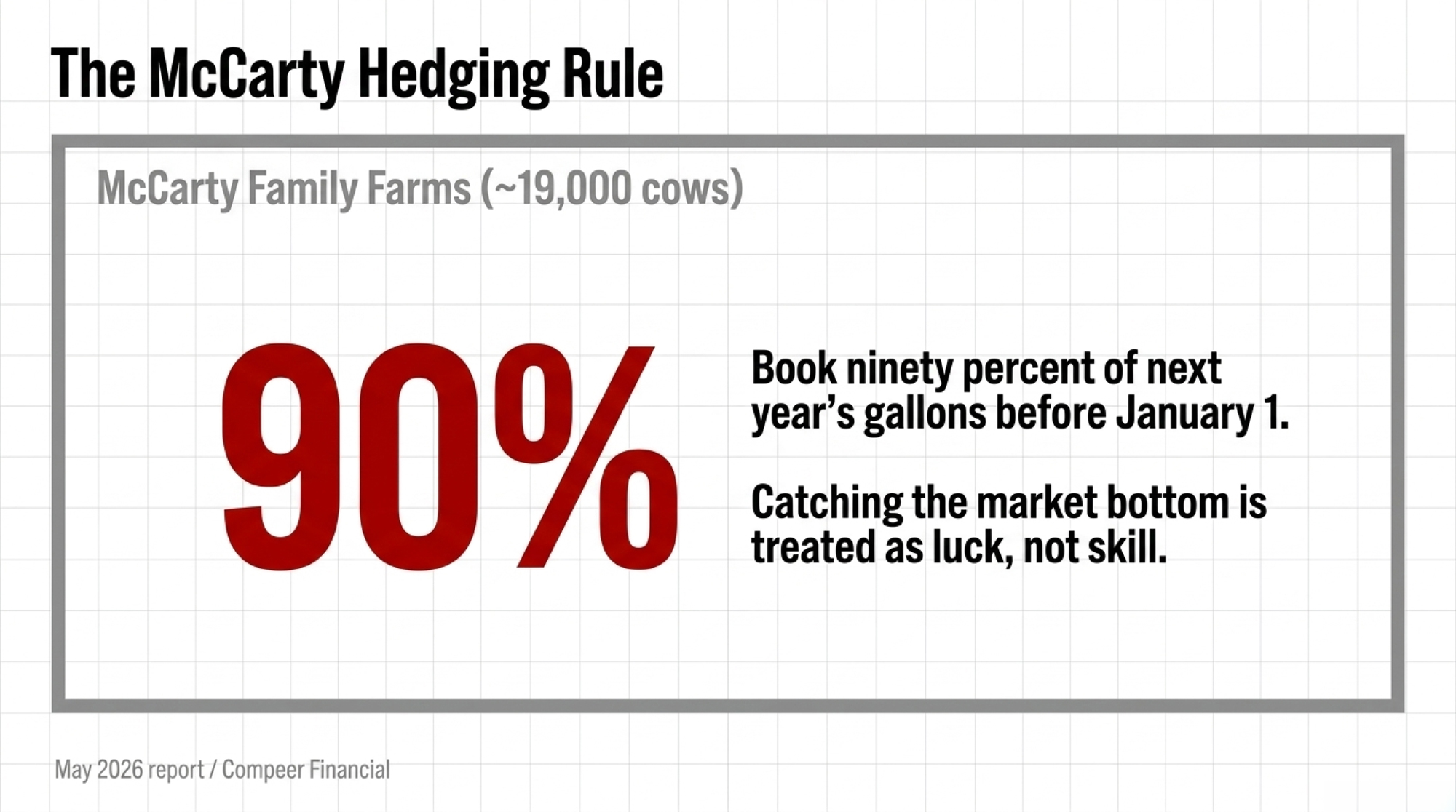

A 50¢ diesel move costs a 19,000-cow dairy roughly $427,500 a year. The McCartys book ~90% of next year’s gallons before Jan 1 — and treat beating the bottom as luck, not skill.

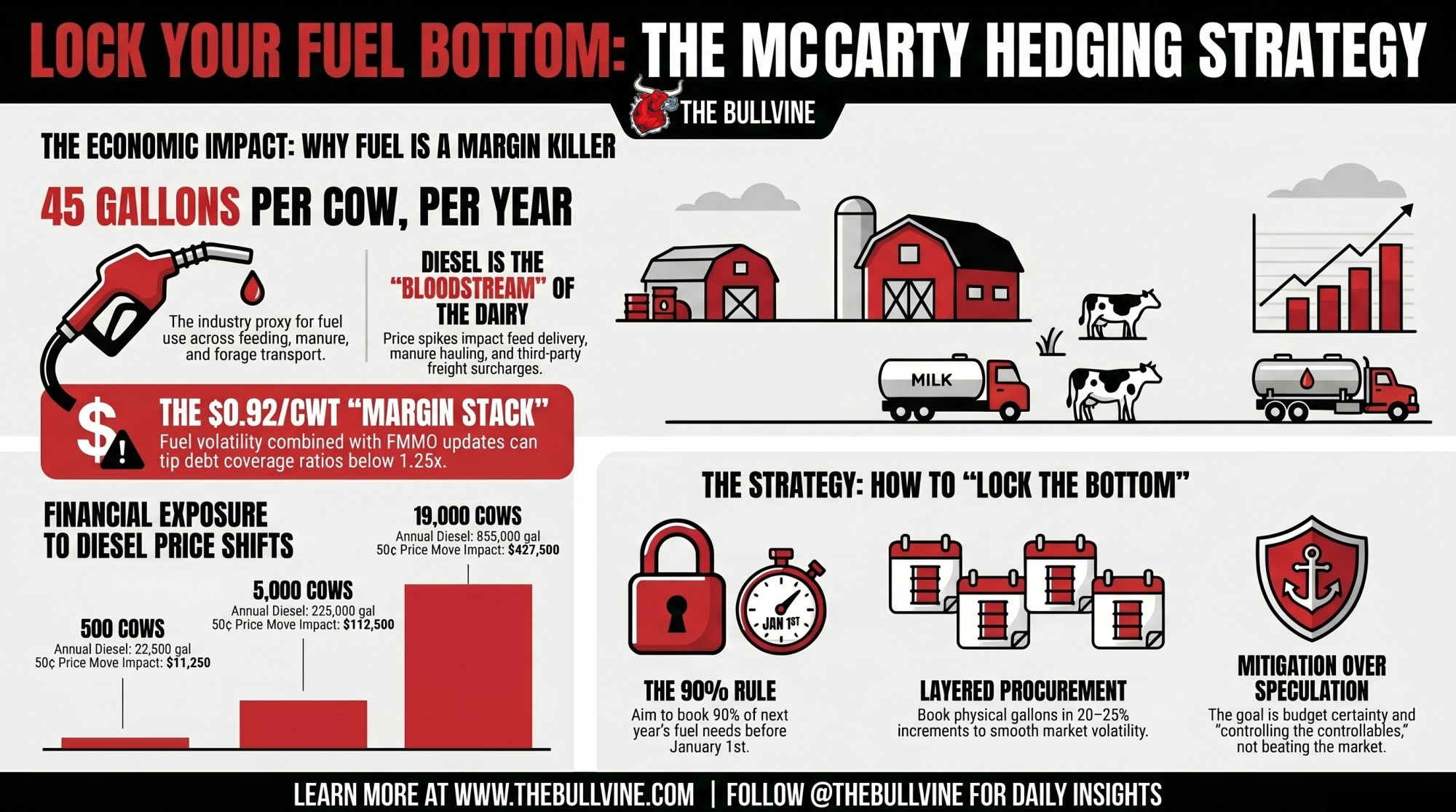

According to a May 8, 2026 report and an industry strategic-analysis brief, McCarty Family Farms aims to enter each fiscal year with roughly 90% of its diesel needs already booked for the next 12 to 18 months, working with Compeer Financial economist Dr. Megan Roberts on a layered procurement plan. Applied to a 45 gal/cow proxy at McCarty’s roughly 19,000-cow scale, a single 50-cent move on diesel would represent about $427,500 in annual exposure. That’s the kind of budget hole the McCarty hedging system is designed to prevent.

The system was built by four brothers — Mike, Clay, Dave, and Ken — who took a 15-cow Pennsylvania herd, moved it to western Kansas in 1999, and grew it into a roughly 19,000-cow operation across Kansas, Nebraska, and Ohio, with a workforce that has grown beyond the 130-plus head count cited in earlier coverage, and a long-term Danone milk contract. Right now, with U.S. retail on-highway diesel sitting at $5.64/gal as of May 12, 2026 per EIA’s weekly update — roughly a 61% jump from a year earlier — that discipline is the difference between funding the next generation and funding the pump.

📌 Editor’s Perspective: Where This Fits in the Bullvine Universe

This piece is the energy-risk leg of a margin story we’ve been mapping all month. Bullvine’s May 2026 Corridor Trap analysis pegged the annual drag at roughly $221,760 on a 600-cow Upper Midwest herd as basis slid from –$0.35 to –$0.85/cwt. The Corridor Trap is what happens to your milk check on the revenue side. The McCarty diesel rule is what locks down the cost side. Same farm. Same lender meeting. Different lever.

What’s Changing — and Why It Hits 24/7 Operations Hardest

Diesel isn’t a line item on a modern dairy. It’s the bloodstream. Feed delivery, manure hauling, milk hauling, cropping, generators, and third-party freight surcharges all move with the price of crude. Brownfield Ag News reported in early May 2026 that one dairy producer’s milk check was running close to .00/cwt while feed and fuel were eating the margin alive — part of a broader 2026 ag-economist warning from David Widmar’s April 28, 2026 Managing for Profitcolumn that energy-market volatility is now a primary 2026 cost-side risk.

For a 24/7 operation, a 50-cent move isn’t an inconvenience. It’s a quarterly-budget derailment. And it’s landing on top of the FMMO Make-Allowance 2025 update — effective June 1, 2025, per the USDA AMS final rule — which trimmed an estimated $0.85–$0.93/cwt off Class III–IV values, with Class III near $0.92/cwt. Stack those two numbers and you can see why lenders are starting to ask for a written energy-risk plan before they renew a line of credit.

The farms feeling it first are the ones running the most equipment hours per cow — large freestall operations with custom hauling contracts, long milk routes to a tightening number of plants, and irrigation. If that’s you, the math below isn’t theoretical.

How This Plays Out on Real Farms — The Energy Risk Management Math

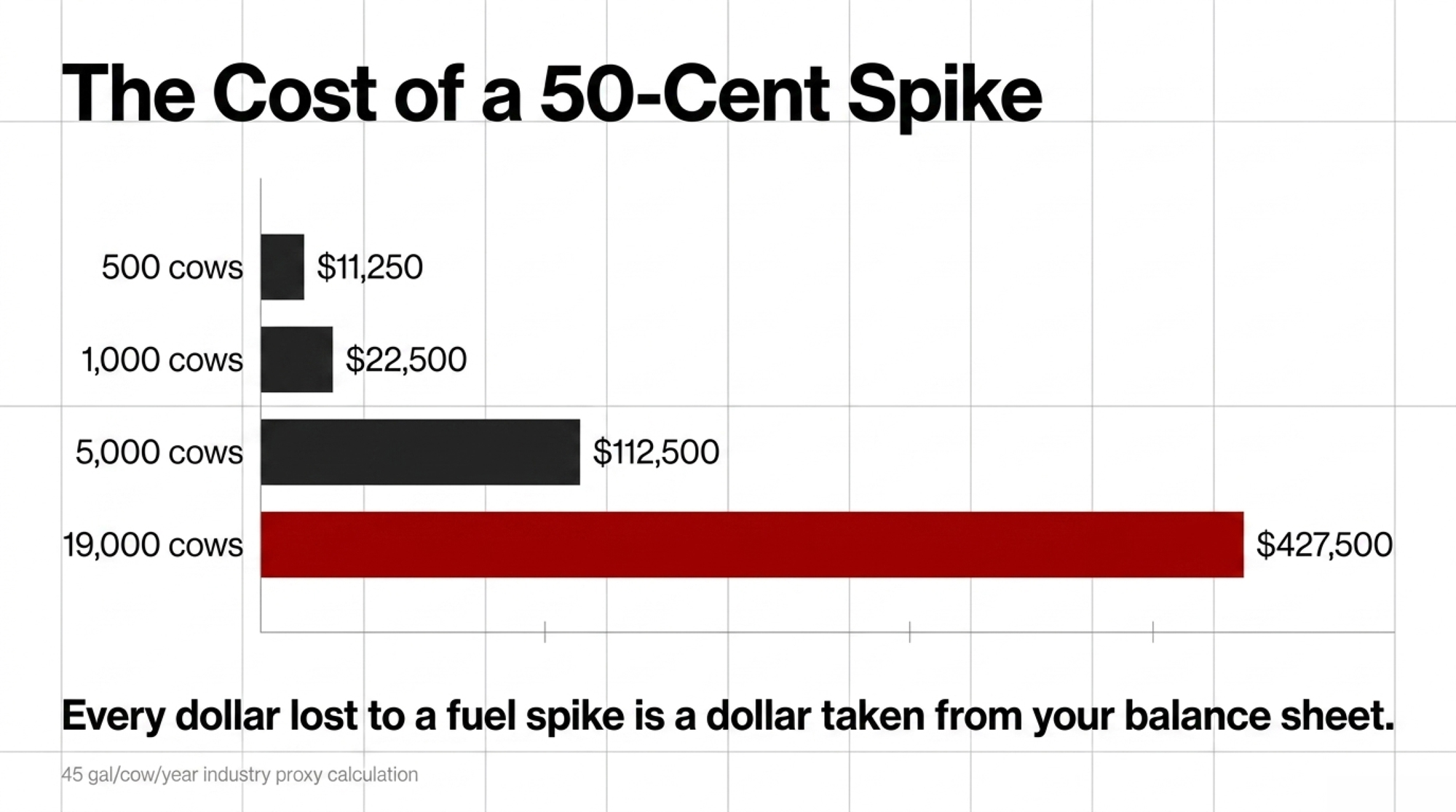

Here’s the back-of-the-envelope every dairy CFO should run today. Using an industry proxy of roughly 45 gallons of diesel per cow per year — covering feeding, manure, and basic forage transport — a 500-cow herd burns about 22,500 gallons annually. A 50-cent spike costs that herd $11,250. A dollar move costs $22,500. At 5,000 cows, the same 50-cent move costs $112,500. At McCarty’s roughly 19,000-cow scale, illustrative math points to about $427,500 in exposure on that one move.

| Herd Size | Annual Diesel (gal) | 25¢ move | 50¢ move | $1.00 move |

| 500 cows | 22,500 | $5,625 | $11,250 | $22,500 |

| 1,000 cows | 45,000 | $11,250 | $22,500 | $45,000 |

| 5,000 cows | 225,000 | $56,250 | $112,500 | $225,000 |

| McCarty (~19k) | 855,000 | $213,750 | $427,500 | $855,000 |

| 40,000 cows | 1,800,000 | $450,000 | $900,000 | $1,800,000 |

Source: 45 gal/cow/year industry proxy. Your actual intensity moves with cropping system, hauling distance, manure logistics, and how much fuel sits on a custom operator’s invoice rather than yours. Farms growing most of their own forage will run hotter than this proxy.

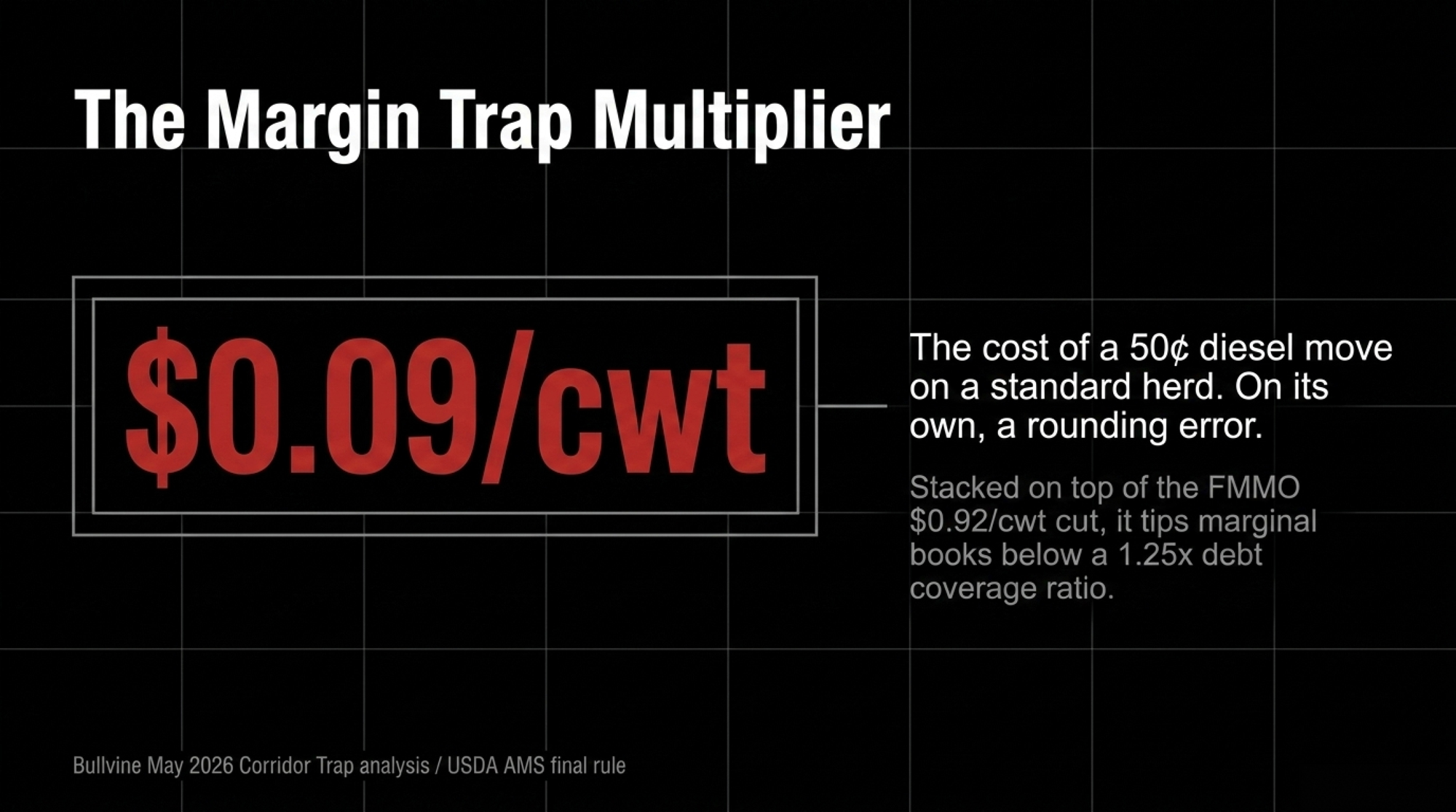

🎯 The Magic Number: $0.09/cwt

That’s the cost of a 50-cent diesel move on a 200-cow herd shipping 24,000 lbs/cow (9,000 gallons × $0.50 = $4,500; ÷ 48,000 cwt of milk ≈ $0.09/cwt). On its own, a rounding error. Stacked on the FMMO Make-Allowance 2025 drag of roughly $0.92/cwt and a basis slide, it can be the number that breaks the bank — and on a marginal book, the variable that tips a Debt Service Coverage Ratio below 1.25x.

The Mechanics: Three Pillars of the McCarty System

The McCarty system rests on three pillars: proactive layering, historical benchmarking, and mitigation over speculation. They don’t try to call the bottom — the McCartys are described as treating that as luck, not skill. As forward months become available, the team books physical gallons in increments — 20–25% at a time — smoothing what the Compeer team has publicly framed as the “fat tails” of the energy market.

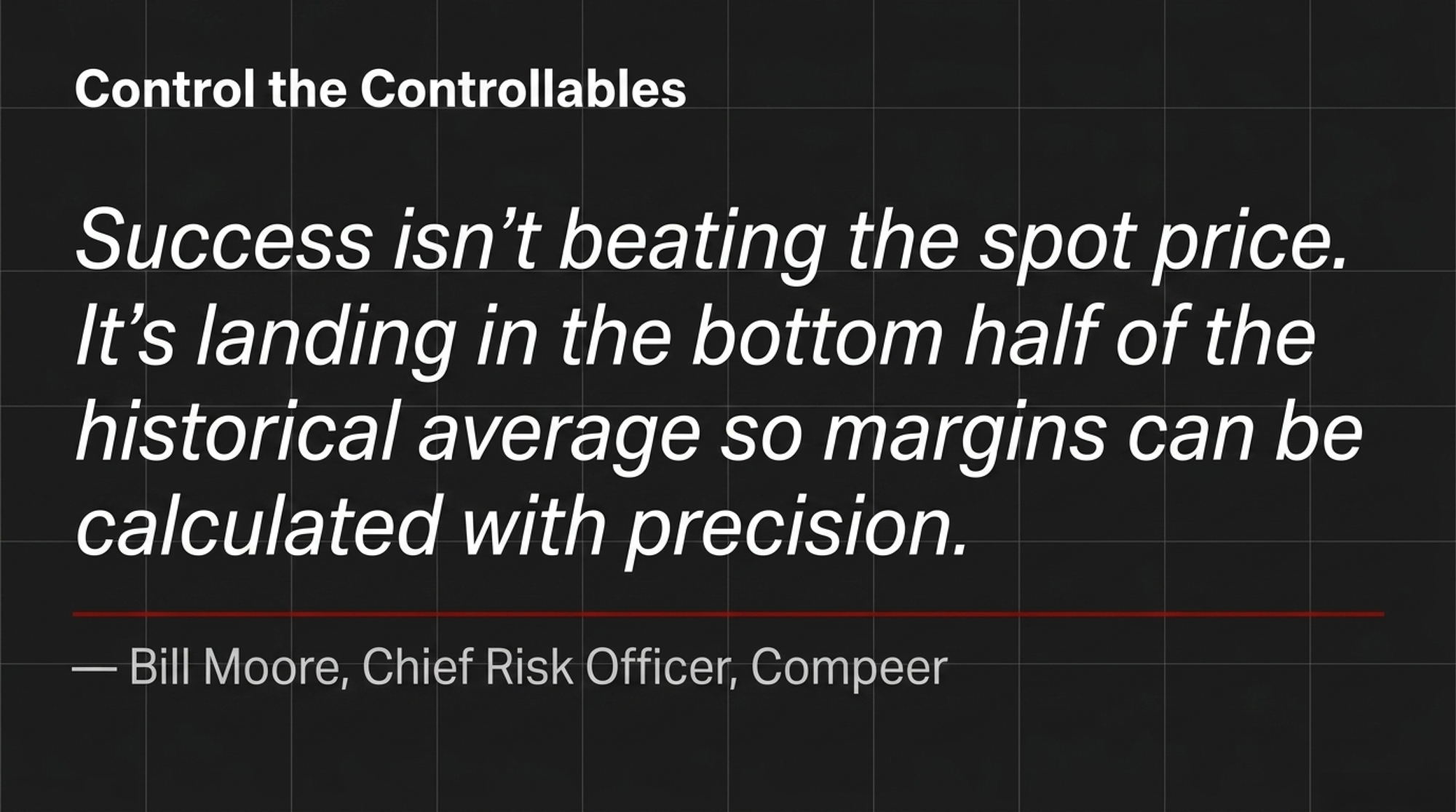

Success isn’t beating the spot price. It’s landing in the bottom third or bottom half of the 5- to 10-year historical average — or simply staying consistent year over year — so milk margins can be calculated with precision before the cows ever produce them. Compeer’s Chief Risk Officer Bill Moore calls it “controlling the controllables.” Translation: lock down breakeven, watch the consensus, and stress-test what happens if ad-hoc government payments fall or Class III drops below $15/cwt.

The 18-month plan is a family-business mechanism for the McCarty brothers — Mike, Clay, Dave, and Ken — built on the same data discipline behind their genetics program, their 2012 Rexford milk condensing plant, and the long-term Danone partnership that anchors their revenue side. None of this is about the next quarter. It’s a question every multi-generational operation faces: whether the next generation inherits a balance sheet they can run, or one they have to dig out from under.

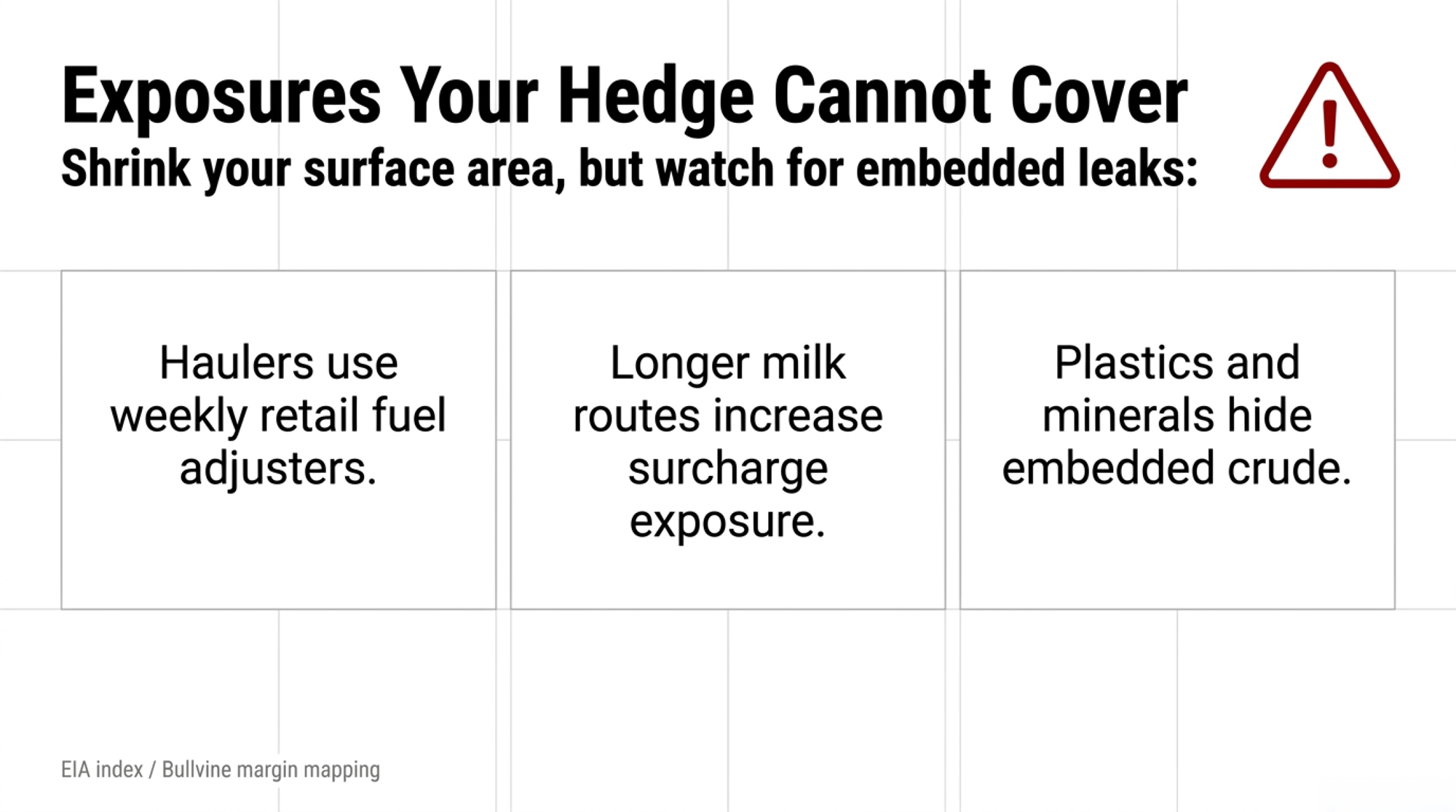

The Hidden Exposures a Hedge Doesn’t Cover

Worth saying out loud: a 90% fuel hedge is not a shield. Three exposures still run through the system the contracts can’t reach.

- Hauling adjusters. Milk haulers and commodity deliverers run fuel surcharges that re-price weekly off the EIA index. Your tank is locked. Their truck isn’t.

- The processing paradox. As regional plant capacity tightens, dairies get pushed to longer milk routes to find an accepting plant. Longer routes mean more surcharge surface area.

- Embedded energy. Mineral premixes, plastic resin, distillers grains, equipment parts — all carry crude-oil cost inside the invoice. Lock the diesel; the inflation still leaks in.

That’s why the 90% target matters. Shrinking the surface area of the things you can’t control is the entire point.

How Much Does Skipping the Hedge Actually Cost You?

Run your own number. If you milk 500 cows and diesel moves $1.00 — and weekly EIA retail diesel did exactly that, climbing roughly $2.14/gal year-over-year through May 2026 — that’s $22,500 you didn’t budget for. On 1,000 cows, $45,000. That’s well above the USDA NASS national livestock-worker average of $17.51/hr for the October 2024 reference week, per the November 20, 2024 Farm Labor release — i.e., real wage money, regardless of region. It’s also more than seven times the bid on a single replacement heifer at the USDA AMS national average of $3,010/head, with USDA NASS’s January 30, 2026 Cattle Inventory printing 3.90 million dairy replacement heifers — the lowest since 1978, per Farm Progress’s February 16, 2026 reporting on the same release.

Every dollar you don’t lose to a fuel spike is a dollar that stays in the business — for cows, for people, for technology, for principal paydown.

Is Your Lender Already Asking About This? — The Energy Risk Management Conversation

In Bullvine’s May 2026 Corridor Trap analysis, a corridor-aware stress test pegs the annual drag at roughly $221,760 on a 600-cow Upper Midwest herd as basis slid from –$0.35 to –$0.85/cwt — and lenders increasingly want to see that same kind of stress test applied to your fuel budget. A documented energy-risk plan — even a one-pager showing how you forward-book diesel — improves your risk profile. In a corridor-aware stress test, an unhedged fuel budget can be the variable that tips a marginal Debt Service Coverage Ratio from acceptable to constrained.

If your bank hasn’t asked yet, your next renewal conversation is the right moment to bring the document yourself.

Options and Trade-Offs for Farmers — Including Dairy Margin Coverage Stacking

You don’t need a 19,000-cow footprint or a quant analyst on retainer to copy the discipline. You do need to pick a lane.

| Strategy | Primary Benefit | The Price You Pay | Best-Fit Dairy | Watch This Metric |

| Lock fixed diesel price | Budget certainty before the fiscal year starts | Lose upside if spot diesel falls | Any dairy with predictable annual fuel use | Coverage above 90% can leave no room for usage surprises |

| Layer 20% to 25% increments | Smooths volatility across the buying cycle | More supplier calls and internal tracking | 500 to 5,000 cow dairies building discipline | Gallons booked vs. actual 12-month use |

| Prepay forward gallons | Gives lender visible cost control | Ties up working capital | Larger dairies with strong liquidity | Cash tied up before milk revenue arrives |

| Pair fuel with DRP or LGM-Dairy | Stabilizes more of the milk, feed, and fuel margin | Premium cost plus more paperwork | Margin-managed dairies with lender scrutiny | Net margin after premium, not gross protection |

| Keep spot-market exposure | Maximum upside if diesel falls | No protection when the market jumps | Only farms with low fuel intensity or strong cash reserves | 50¢ move exposure before Jan. 1 |

- Co-op forward booking — the 500-cow blueprint. Work with your local fuel co-op to forward-contract gallons 12 months out. Lock 25% in September for Q1 delivery. Another 25% in December for Q2. And so on. By the time the calendar flips, you’ve layered four price points instead of betting on one. When it works: you’ve got working capital and a lender comfortable with prepaid inventory. Risk: if spot prices fall below your locked rate, you’ll pay more than the neighbor who didn’t hedge. You’re buying budget certainty, not the bottom of the market.

- The “Jan 1, 90%” rule. Set a hard target to have 90% of next year’s diesel booked before the fiscal year starts. When it works: any size farm running an annual budget. Requires: 12 months of clean fuel-use data. Limit: leaves 10% open for genuine consumption surprises — herd expansion, new acreage, beef-on-dairy intensity.

- 30-day on-ramp. This month, pull last year’s fuel invoices, calculate your gallons-per-cow, and call your fuel supplier to ask what forward-contract terms they offer. That’s the entire starting move. No working capital required to make the phone call.

- Integrate fuel with milk and feed risk. Fuel hedging is one piece of a margin toolkit. Compeer’s published framework treats it alongside DRP for component-based revenue protection, LGM-Dairy for bundled feed risk, and Dairy Margin Coverage as a Tier 1 backstop that’s often too small for large herds. None of these tools work alone. Pair them.

The trade-off table — benefit vs. cost, plain English:

| Strategy | Primary Benefit | The “Price” You Pay |

| Locking price | Budget certainty | Loss of “downside” opportunity if spot falls |

| Layering 25% increments | Cost averaging across the cycle | Increased admin and supplier time |

| Prepaying forward gallons | Lender confidence in your risk plan | Working capital tied up |

| Pairing with DRP / LGM-Dairy | Margin certainty across feed + milk | Premium cost on the policy |

Key Takeaways

- If you can’t say what you paid per gallon over the last 12 months, you don’t have a fuel strategy — you have a fuel bill.

- If your fuel exposure on a 50-cent move would change a hire, an expansion, or a debt payment, you have a hedging case. Run the test: gallons/cow × $0.50 × your herd size.

- If you can hit 50% coverage by January 1, you’re ahead of the spot-market crowd. 90% is the McCarty benchmark, not the entry point.

- If you book a layer, book another. One fixed price isn’t a strategy — three or four staggered layers is.

- If you hedge fuel without hedging milk or feed, you’ve stabilized one leg of a three-legged stool. Pair it with DRP, LGM-Dairy, or a forward milk contract.

- If your milk hauling, mineral premix, or replacement heifer bills are climbing faster than diesel, the embedded energy is leaking in. Track those line items separately.

- If your next lender meeting is inside 90 days, bring a one-page energy-risk plan before they ask for it.

The Real Question

The next 50-cent diesel move is coming. The only question is whether your operation has decided in advance who it’s going to hurt — the market, or you. Where does your fuel coverage sit on January 1, and what would you have to change this month to get it closer to 90? The McCarty brothers built a 12–18 month answer to that question. Many multi-generational dairy families face the same calculus when planning for succession — and yours can do the same work at a smaller scale.

Reporting in this article is based on published trade-press coverage (Dairy Herd Management, Brownfield Ag News, Farm Progress, Bullvine archive), public Compeer Financial materials, USDA AMS and NASS data (USDA NASS Farm Labor 11/20/2024; USDA NASS Cattle 01/30/2026), EIA weekly retail diesel data, and an industry strategic-analysis brief. The Bullvine did not independently interview McCarty Family Farms or Compeer Financial for this piece. Diesel-cost figures are illustrative calculations using a 45 gal/cow industry proxy and will vary by farm.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $586‑Per‑Kilo Dairy Quota Trap: Why New Ontario Quota at 6% Bleeds Cash Every Year — Arms you with the cash-flow math to survive high-interest borrowing. Reveals why new Ontario quota at 6% destroys equity, delivering a 30-day strategy to prioritize debt retirement over aggressive, money-losing expansion.

- Unlock the Secrets to Dairy Farm Profitability: Discover Which Regions Will Soar in 2025! — Delivers precise regional profit projections for the 2025 fiscal year. Exposes how herd scale and geographic positioning drive a $1,100 per cow earnings gap, helping you benchmark your current margin against top-performing operations.

- 9.57 Million Cows, 3.9 Million Replacements: Genetics Built This Dairy Herd Paradox – and 2027 Ends It — Navigates the structural reset of a heifer market hitting 48-year lows. Breaks down the $903,000 replacement bill facing 1,000-cow herds, highlighting the genomic sorting tactics needed to capture the $8,000 per cow longevity dividend.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.