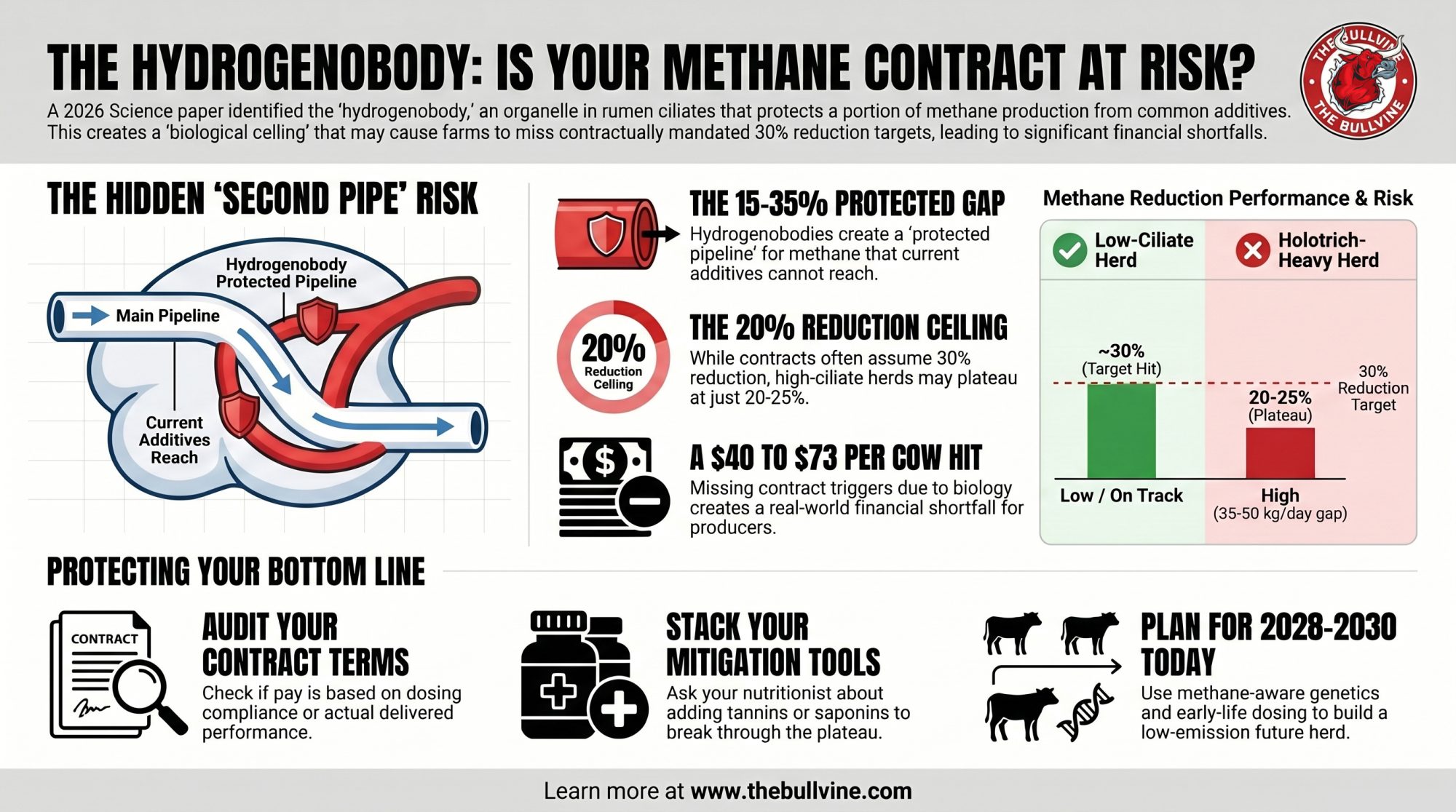

Same ration. Same additive. Same paperwork. A Science paper in April just explained the 35-50 kg/day gap — and it’s the slice of methane your 2027 Bovaer contract assumed didn’t exist.

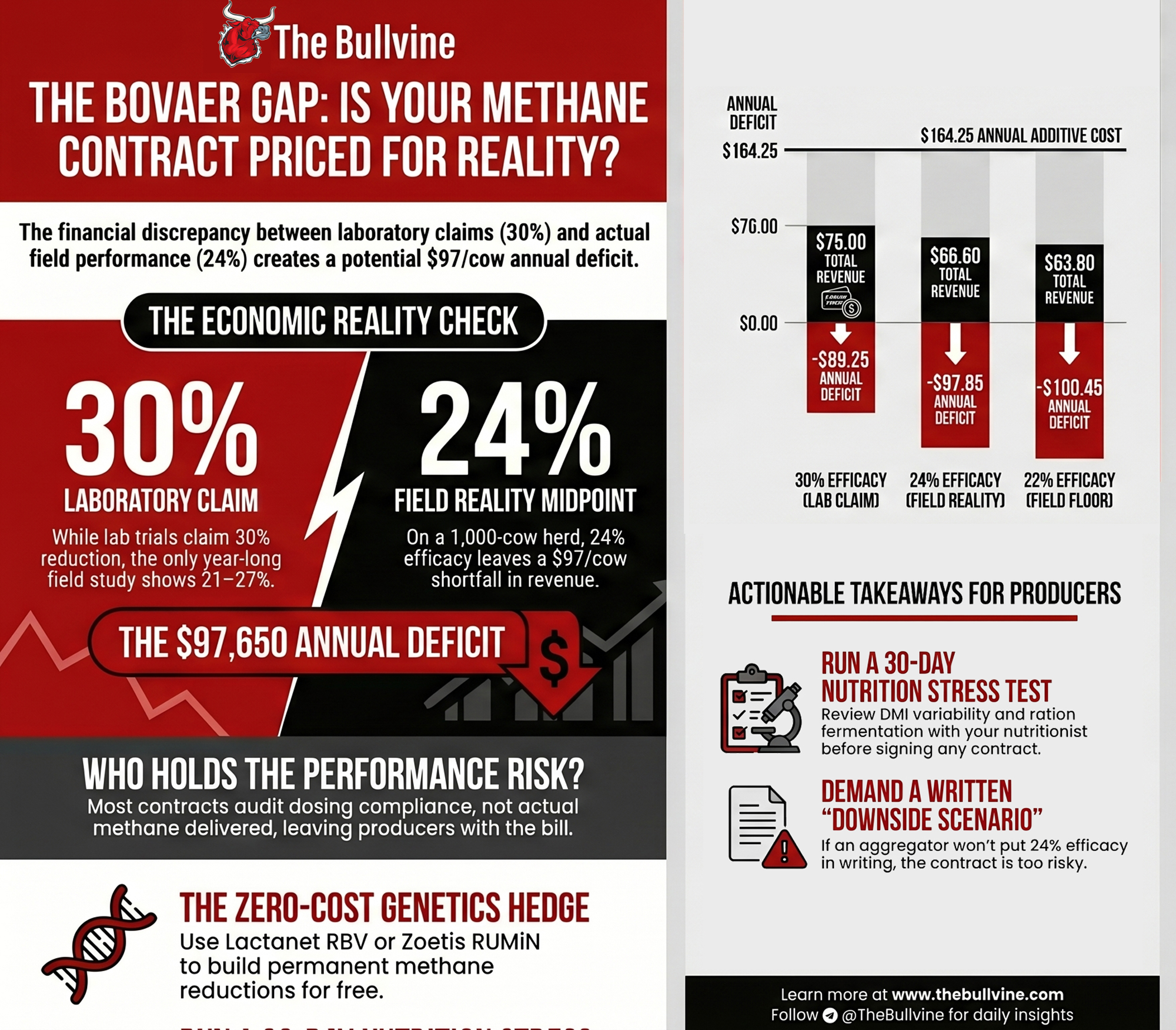

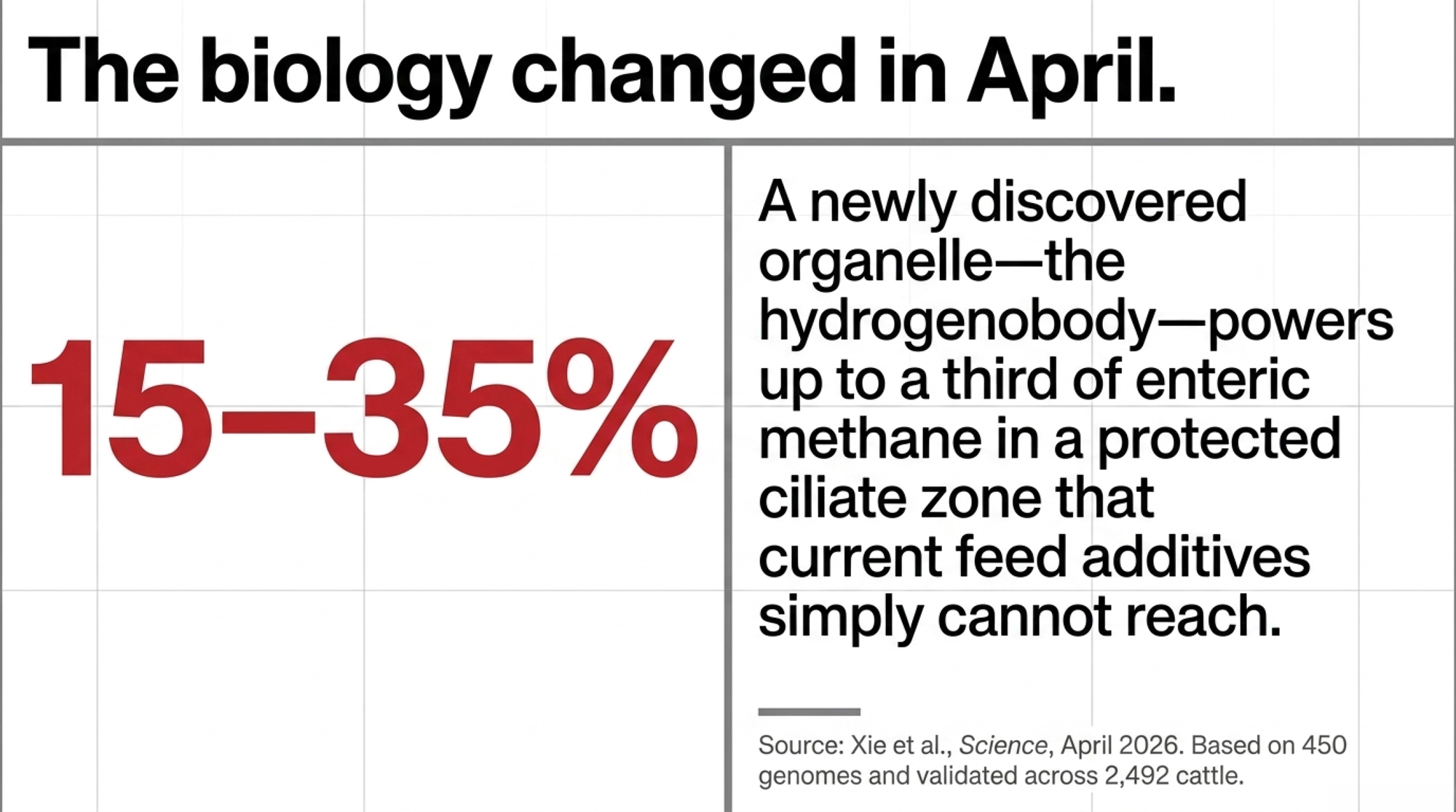

Executive Summary: A Science paper in April identified a new organelle inside rumen ciliates — the hydrogenobody — that powers an estimated 15-35% of enteric methane through a pathway 3-NOP can’t fully reach, which means every flat-30% Bovaer-linked 2027 contract on the continent is carrying biological risk nobody priced in. Two 500-cow herds on the same TMR and the same additive can now sit 35-50 kg of methane per day apart, purely on ciliate community: a low-ciliate herd can honestly land near a 30% reduction, while a holotrich-heavy herd ceilings around 20-25% and burns the difference straight through the contract’s minimum trigger. The hit lands somewhere between and a cow on most deals, depending on dose, premium tier, and carbon price — real money on a 500-cow shipper. Single-additive tools like Bovaer aren’t broken; they’re working on one of two hydrogen pipelines, which is why asparagopsis, nitrates, and most next-gen inhibitors hit the same plateau. The 30-day move is pulling your contract and reading three lines: who owns the shortfall, whether payment triggers on dosing or delivered performance, and whether there’s a re-opener clause for new science. The 90-day move is deciding whether early-life 3-NOP dosing through 14 weeks plus methane-aware Lactanet/CDCB sire selection are on the table for replacements — that’s where the structural reductions for your 2028-2030 contracts actually live.

A Science paper in April identified a cell structure inside rumen ciliates that powers an estimated 15-35% of enteric methane through a pathway current feed additives can’t fully reach — and every flat-30% Bovaer deal on the continent now carries biological risk that wasn’t priced in.

Picture a 500-cow Holstein dairy in southern Ontario — the kind of mid-size family operation you find every twenty minutes off Highway 401. Late last year, the owner signed a 2027 Bovaer-linked carbon and premium deal. The front-page math looked clean: feed 3-NOP, hit a modeled 30% reduction in enteric methane, collect a per-cwt sustainability premium, and a per-head carbon credit through Elanco’s Athian marketplace. Six months in, the cows are eating it, the milk is shipping, and the owner is starting to wonder whether the rumen ever read the contract.

In April, a paper in Science dropped a new piece of biology into the middle of every methane deal on the continent. Fei Xie and colleagues identified a previously unknown organelle inside rumen ciliates — the hydrogenobody — that helps power an estimated 15-35% of total enteric methane through a pathway current feed additives can’t fully reach (Xie et al., Science, April 2026). If you’ve already signed, or you’re about to, that single discovery rewrites the risk math on your contract.

What’s Changing and Why

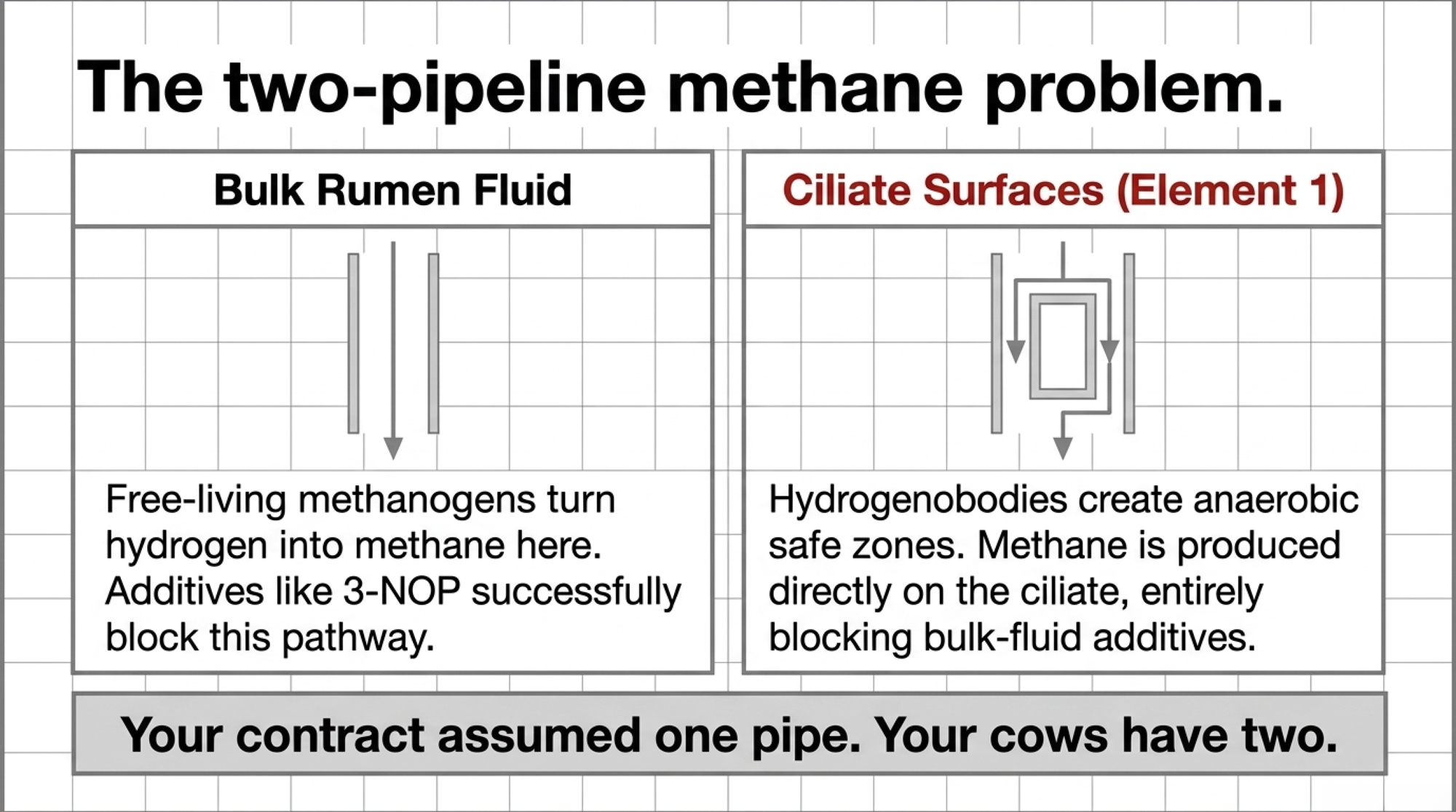

For two decades, the industry has treated enteric methane as basically one pipe. Fermentation makes hydrogen, free-living methanogens in rumen fluid turn that hydrogen into methane, an inhibitor like 3-NOP knocks them back, and you book a reduction. That single-pipe assumption is baked into the 20-30% headline quoted for Bovaer in dairy cows and into the carbon methodologies that pay on it.

The April 2026 study — built on 450 rumen ciliate genomes and validated against 2,492 cattle across five countries — showed there’s a second pipe. Rumen ciliates, the protozoa that make up roughly half of rumen microbial biomass, carry a single-membrane organelle at the base of their cilia. That organelle produces hydrogen and strips oxygen at the same time, creating tiny anaerobic safe zones where attached methanogens churn out methane right on the ciliate surface.

Most current feed additives weren’t designed for that micro-zone. They work where hydrogen is floating in bulk rumen fluid, not where it’s being handed cell-to-cell. Translated to a feed bunk: a chunk of your methane lives in a part of the rumen your contract assumed your additive could reach. The new paper puts that estimated share at 15-35% of total enteric methane, and higher in herds loaded with holotrich ciliates like Dasytricha.

How This Plays Out on Real Farms

Two 500-cow Holstein dairies on the same TMR, shipping to the same processor, can now end up on very different sides of the same contract. The Xie study found high-methane sheep on the same diet carried nearly 100 times more Dasytricha than low-methane sheep, and each of those cells packed about 28 times the hydrogenobody density of a common low-emission ciliate genus. On a dairy, that means a holotrich-hot herd is running more of its methane through the protected pipeline. Same additive program, lower ceiling.

These reduction ceilings aren’t measured outcomes from a single trial. They’re inferences from layering the hydrogenobody paper’s two-pipeline framing on top of published 3-NOP efficacy ranges. The directional logic is solid. The precise plateau on your farm will depend on your herd’s ciliate profile — and the only way to know which barn you’re standing in is a rumen fluid sample run for ciliate community composition, still primarily a research-lab service today, but one your nutritionist or extension specialist can route through a university partner if you want a real answer rather than an industry assumption.

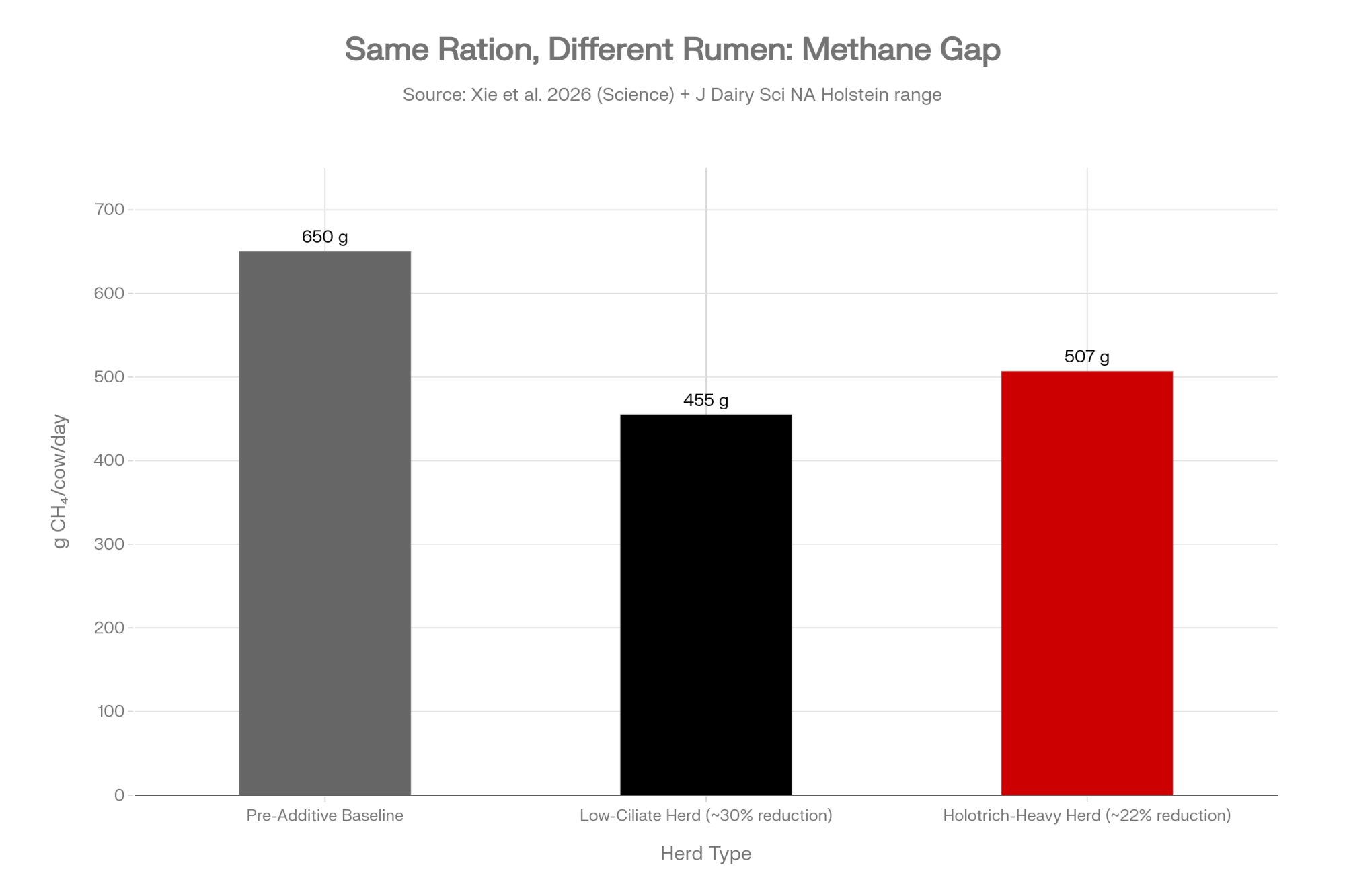

Here’s the barn math at the methane level. Set the dollars aside for a moment. Take a higher-producing Holstein at roughly 600-700 g of enteric methane per cow per day — a range consistent with peer-reviewed Journal of Dairy Science enteric-methane work on NA lactating cows fed typical TMRs. A lower-ciliate herd may have about 20% of its methane locked in hydrogenobody zones, so a well-run 3-NOP program can honestly land near the 30% headline reduction — putting it around 430 g/cow/day post-additive. A holotrich-heavy herd, with 30-35% of methane in that protected zone, can do everything right and still plateau around 20-25%, landing closer to 530 g/cow/day. Same ration, same additive, same paperwork — different rumen.

Two 500-Cow Herds, Same Ration, Different Rumens

| Rumen Ciliate Profile | Methane in Protected Zone | Realistic 3-NOP Reduction | Post-Additive Methane per Cow/Day | Total Herd Methane per Day (500 cows) | Contract Shortfall Risk |

| Low-ciliate herd | ~20% | ~30% (target hit) | ~430 g | ~215 kg | Low / on track |

| Holotrich-heavy herd | 30-35% | 20-25% (plateau) | ~530 g | ~265 kg | High — 35-50 kg/day gap |

Inputs: ~600-700 g/cow/day pre-additive baseline (peer-reviewed NA lactating Holstein range, J Dairy Sci); reduction percentages reflect inferred biological ceiling under the two-pipeline framing of Xie et al. 2026, not measured trial outcomes. Per-cow and per-herd numbers scale linearly to your own herd size and baseline.

That kilogram gap is what your contract’s dollar math sits on top of. Whether it costs you something closer to $40 a cow or something closer to $73 a cow depends on dose, premium tier, and carbon price — and the full cow-by-cow teardown runs in next week’s Methane Contract Files.

The Mechanics Behind the Outcomes

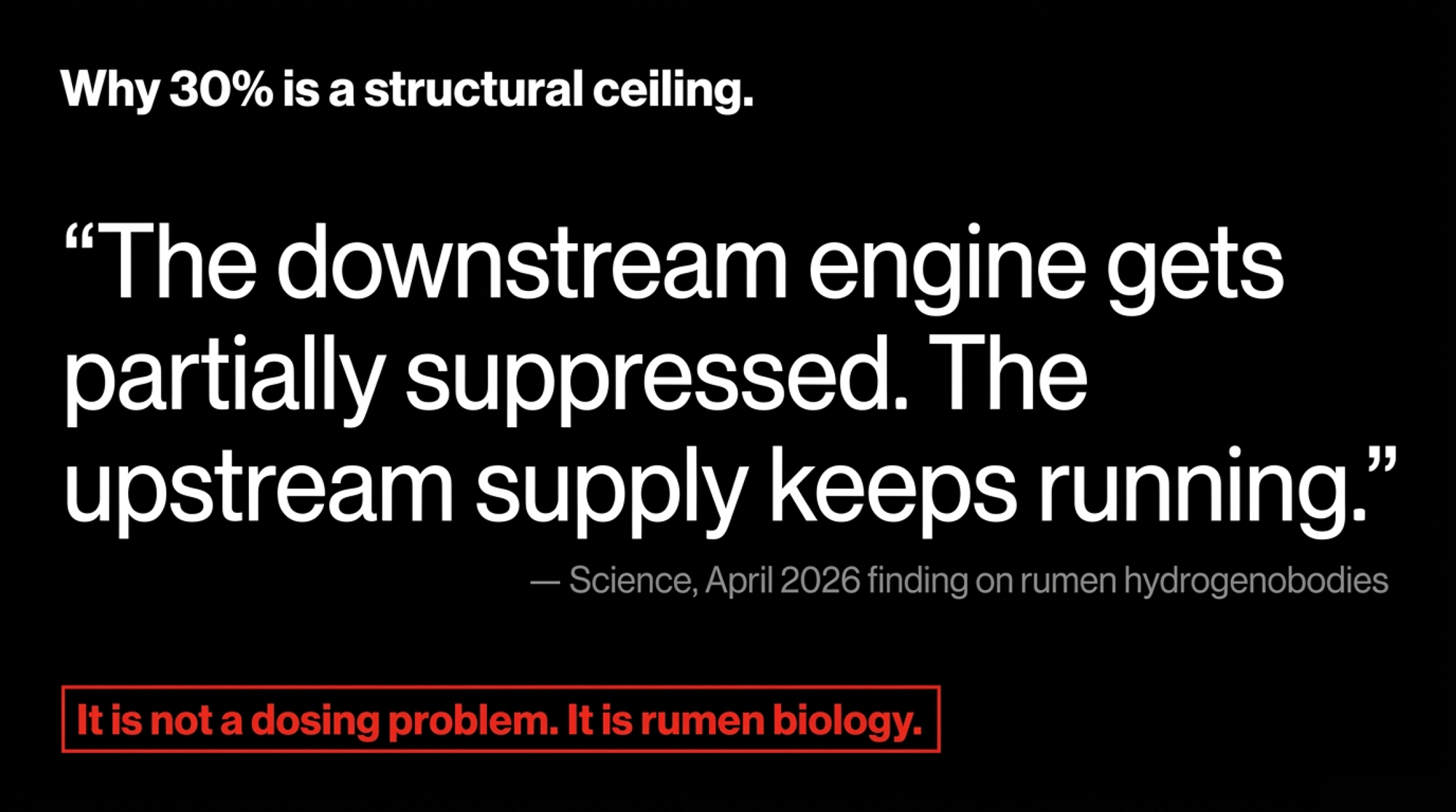

Picture two hydrogen economies in the same rumen. The first is the open one. Hydrogen released into rumen fluid, picked up by free-living methanogens, is turned into methane. 3-NOP, the active ingredient in Bovaer, inhibits methyl-coenzyme M reductase in those methanogens, and that’s where most of its 20-30% reduction comes from.

The second economy is the ciliate one. The hydrogenobody, sitting at the base of the hair-like cilia, generates hydrogen and scrubs oxygen out of its immediate neighborhood. Methanogens latch onto the ciliate surface and tap that hydrogen directly. They never really mix it into the open rumen fluid. An inhibitor floating in bulk fluid has a hard time reaching reactions in those nanometre-scale pockets.

That’s why the reduction curve from a single additive bends. You get a steep early drop as the bulk-fluid pathway is suppressed. Then the line flattens as more of the remaining methane sits in the ciliate-protected pipeline. Genetics, early-life colonization, and feed history all shape how big that protected slice is — host genes like SPINK5, which influence rumen wall structure and local oxygen gradients, help decide which ciliates can colonize and thrive. In other words, your herd’s methane ceiling is partly baked in long before any product hits the feed bunk.

Why This Goes Beyond Bovaer

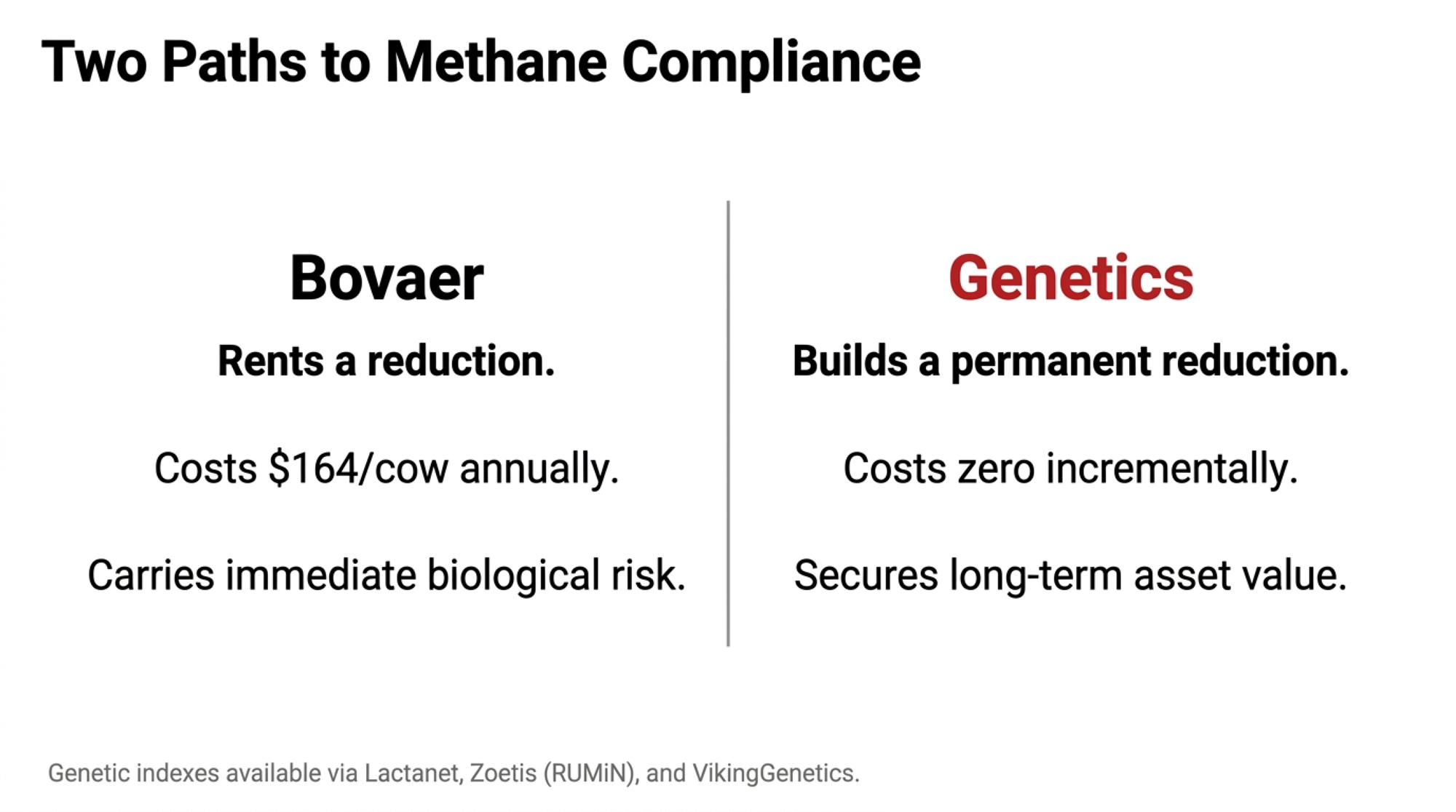

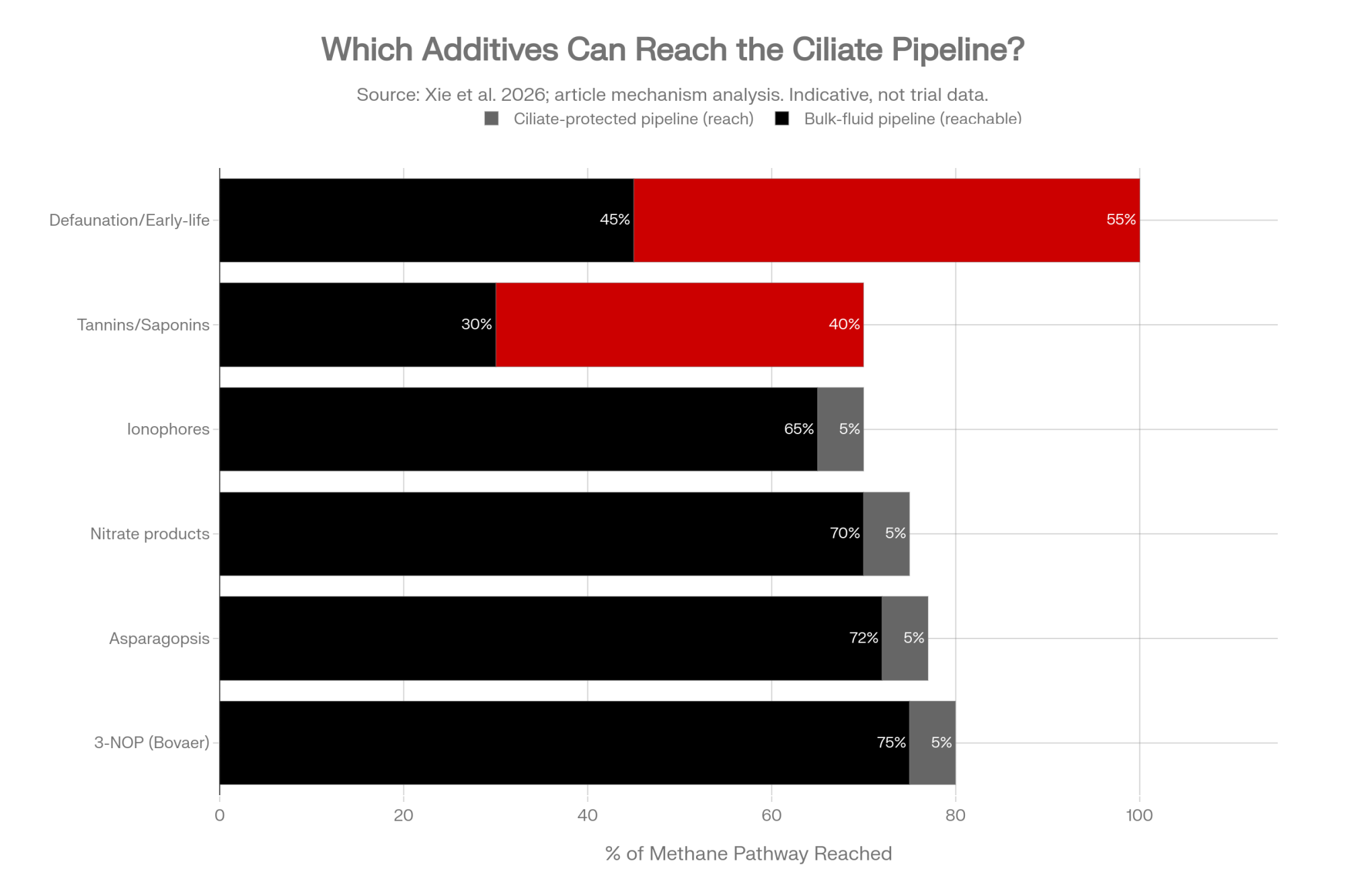

This isn’t just a 3-NOP problem. Any additive that works primarily on free-living methanogens in bulk rumen fluid runs into the same wall. Asparagopsis seaweed, nitrate-based products, certain ionophores, and most next-gen inhibitors in commercial trials all share that mechanism family. The two-pipeline framing applies to every one of them.

Ciliate-targeting tools — tannins, saponins, defaunation strategies, and the early-life microbiome interventions now in research — work on the other pipe. That’s why the Science paper matters beyond a single product launch. It reframes the entire commercial methane stack as a hydrogen-supply problem with two valves, not one inhibitor problem with a 30% ceiling. Your 2027 contract may be priced on Bovaer, but the next contract cycle will be written on a stack.

Options and Trade-Offs for Farmers

There’s no single move that fixes this. There are four practical paths, and most operations will end up combining pieces of them.

| Path | Best For | 30-Day Action | 2027 Contract Risk | 2030 Impact |

|---|---|---|---|---|

| 1. Single-tool, stress-test contract | Already signed, dosing dialled in | Pull contract; find performance trigger language | HIGH if payment on delivered reductions — holotrich herd may plateau at 20–25% | Low — no structural change |

| 2. Stack 3-NOP + tannins/saponins | Nutritionist sees holotrich-dominant profiles | Add tannin/saponin layer; monitor DMI + NDF digestibility | MODERATE — may close gap to high 20s, not close it fully | Moderate — partial ceiling lift |

| 3. Genetics + early-life dosing | Raising your own replacements | Dose calves 0–14 wks; audit sire lineup for methane indices | Low for 2027 — no near-term impact | HIGH VALUE — structural reduction baked into 2030 herd |

| 4. Renegotiate now | Signed before April 2026 Science paper | Document compliance data; bring Xie et al. to rep | CRITICAL — waiting means underwriting the biological shortfall alone | High — sets correct baseline for next contract cycle |

Sources: Article (Hydrogenobody/Xie et al. 2026); Meale et al. 2021, Scientific Reports (early-life 3-NOP); article’s four-path framework.

- Path 1 — Stay single-tool, but stress-test the contract. When it makes sense: you’ve already signed, and dosing is dialed in. What it requires: a 30-day contract teardown. Risks/limits: if the deal pays on delivered reductions with a hard floor rather than dosing compliance, you’re carrying biological risk that wasn’t priced. Pull the contract this month, find the language on performance triggers, minimum reductions, and clawbacks, and map them against a realistic 20-25% biological ceiling for a ciliate-heavy herd.

- Path 2 — Stack a second mechanism on top of 3-NOP. When it makes sense: your nutritionist sees holotrich-dominant rumen profiles. What it requires: a moderate, well-managed tannin or saponin program. Risks/limits:gains are conditional on dose, ration, and whether you can hold DMI and fiber digestibility steady. Used carefully, this may move a holotrich-heavy herd from a 22-25% wall toward the high 20s. This is a nutritionist conversation, not a “throw it in the TMR” decision.

- Path 3 — Invest in the next herd, not just this one. When it makes sense: you raise your own replacements. What it requires: early-life 3-NOP dosing plus methane-aware sire selection. Risks/limits: won’t move 2027 numbers — it changes what your 2030 contract can honestly promise. Calves dosed with 3-NOP from birth through about 14 weeks held lower methane out to at least 60 weeks of age in published trials (Meale et al., 2021, Scientific Reports), with shifts in the underlying microbial community.

- Path 4 — Renegotiate now, while the science is fresh. When it makes sense: you signed before the Sciencepaper hit. What it requires: documented compliance, real reduction data, and the hydrogenobody science walked into the room. Risks/limits: relationship cost — your rep or broker may push back hard. The alternative is eating the gap quietly for the next four years.

How Much Does Waiting 30 Days Actually Cost?

On a 500-cow herd already running a single-additive program, the cost of waiting hides in two places: contract risk and lost renegotiation timing.

Run it on your own deal. Every month you wait to tighten the contract, layer in a second mechanism, or formally flag the biological risk to your rep is another month you’re underwriting a reduction your rumen may not deliver — without anyone else on the contract sharing that exposure. The faster you put the hydrogenobody science in front of the people who wrote the deal, the cleaner the conversation about who eats the shortfall.

Is Your Herd’s Genetic Strategy Already Behind?

Methane and feed-efficiency traits are now available in mainstream NA sire indices through Lactanet and CDCB, but uptake data and A.I. sales mix suggest most herds still rank sires primarily on production, components, type, and health. If your processor or carbon partner is steering toward stricter methane targets through 2030, that gap shows up later as a herd whose rumen architecture quietly fights your mitigation stack.

The practical move this month is small but real. Ask your genetics rep where your active sire lineup sits on whatever methane or feed-efficiency indices they offer, and whether they can flag bulls already in your list that lean lower-emission without giving up milk or fertility. You don’t have to rebuild your mating plan tomorrow. But you want to know whether the daughters entering your parlor in three years will make your two-pipeline strategy easier or harder.

Key Takeaways

- If your contract assumes a flat 30% reduction with a single additive, treat that as a working hypothesis, not a guarantee — the hydrogenobody work suggests an estimated 15-35% of enteric methane sits in a ciliate-protected pipeline that current tools can’t fully reach.

- Pull your current contract this month and check three lines: who owns the shortfall if reductions come in low, whether payment triggers on dosing or on delivered performance, and whether there’s a re-opener clause for new science.

- If you’re running 3-NOP solo on a holotrich-heavy herd, model a 20% reduction scenario against your contract’s minimum trigger before you sign anything new — that’s the realistic biological floor, not the 30% headline.

- If your nutritionist sees holotrich-dominant rumen profiles, ask about a tannin or saponin layer — but only with NDF digestibility, DMI, and component impacts on the same spreadsheet.

- If you raise replacements, decide within 90 days whether early-life 3-NOP dosing through about 14 weeks and methane-aware sire selection are on the table — that’s where the structural reductions live for 2028-2030 herds.

📋 4 Questions to Ask Before Signing Your Next Methane Deal

- Where does your model account for the protected ciliate pipeline?

- Is my payout based on strict dosing compliance, or on delivered methane performance metrics?

- How does this contract handle baseline shortfalls in high-ciliate (holotrich-dominant) herds?

- Do you credit stacked mitigation mechanisms (for example, 3-NOP + tannins) separately?

What This Looks Like at Your Bunk

The question isn’t whether your contract still works on the slide deck. It’s whether your specific rumen, on your specific ration, with your specific replacements, can deliver the number your processor and broker are quietly counting on. Where does your breakeven sit if you only hit 22% instead of 30% — and how much of that gap is your operation willing to wear before someone else has to come back to the table?

Run Your Numbers

Component Value Tracker — Before you sign a flat-30% Bovaer-linked premium, run your fat, protein, and other solids through the Component Value Tracker to see what each per-cwt sustainability premium is actually worth on your milk check — and how much margin a 22% rumen plateau eats into before the contract bonus catches up.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

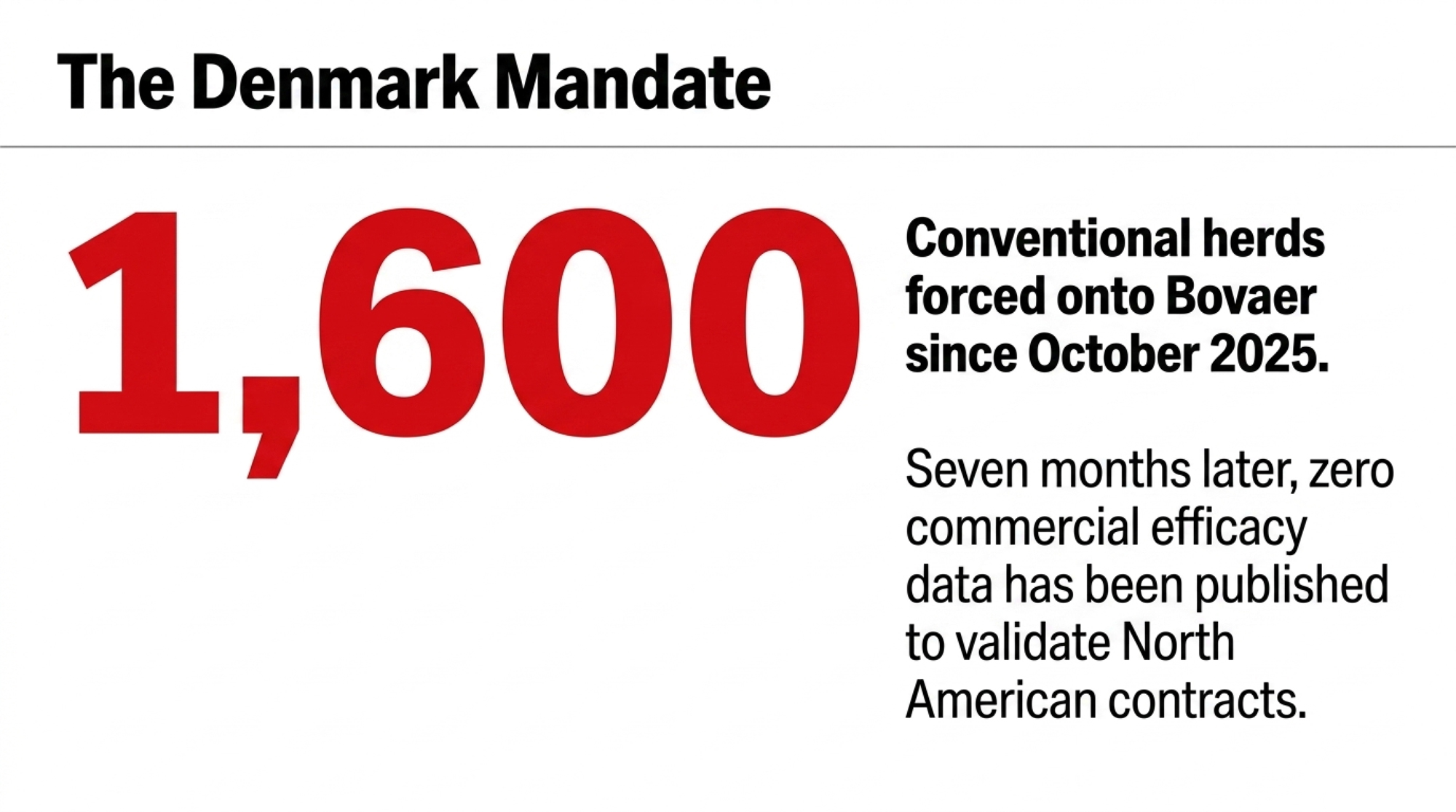

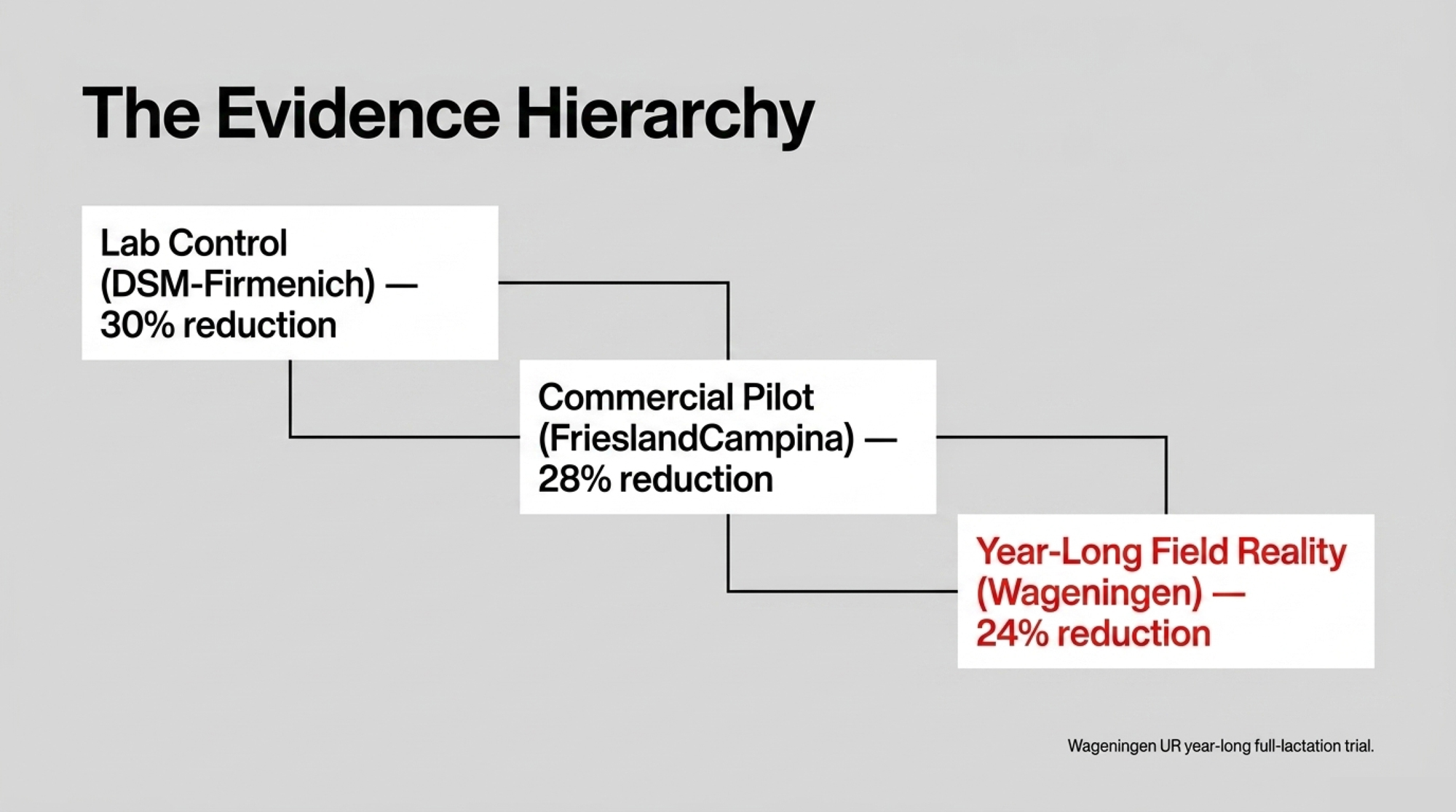

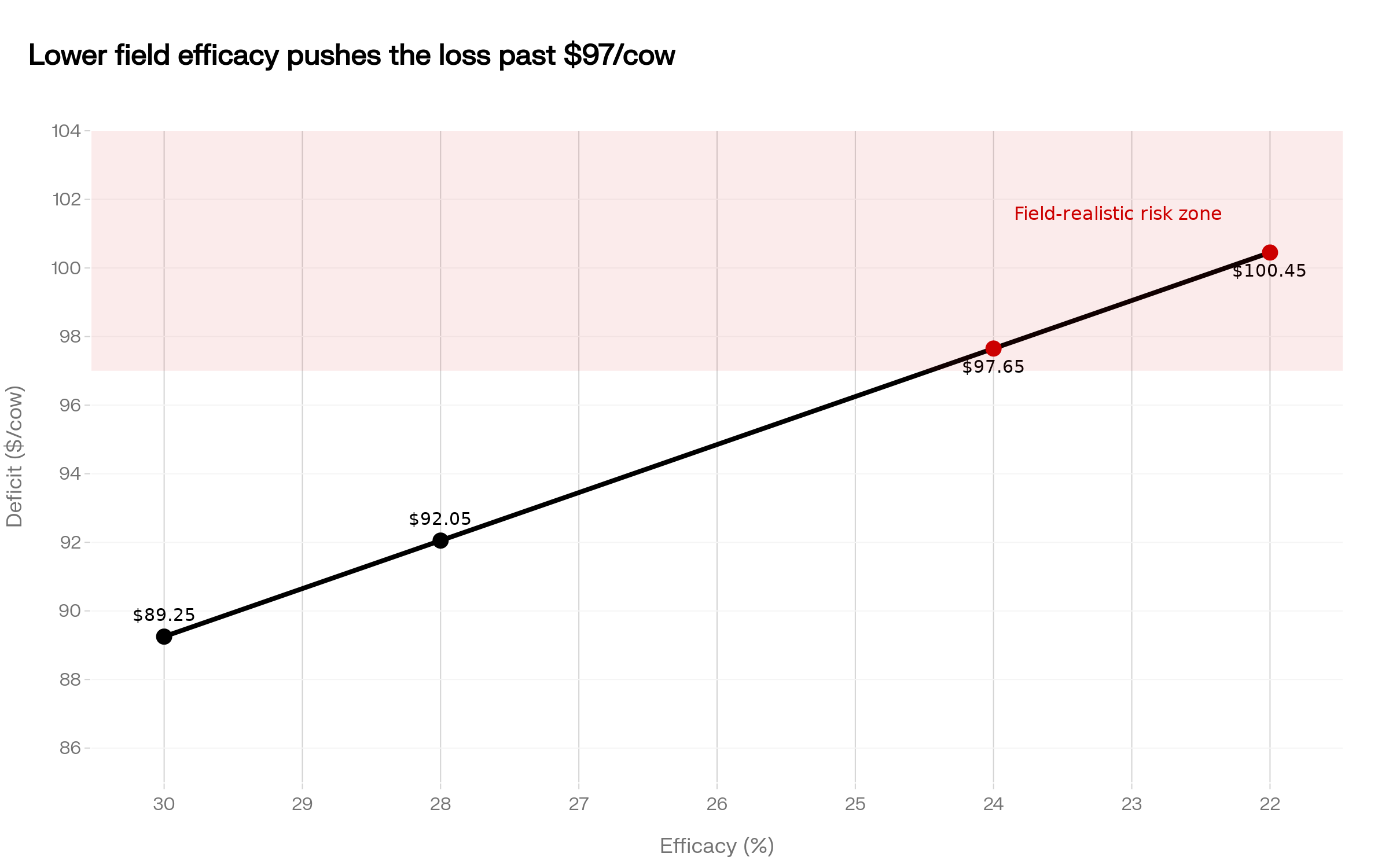

- Your 2027 Bovaer Contract Prices 30%. Denmark’s Real Number Doesn’t Exist Yet. — Exposes the 24% field-reality benchmark from full-lactation European data to protect you from underwriting an unpriced $97 per cow annual deficit if your contract forces performance triggers rather than simple dosing compliance.

- Carbon Credits: $150000 for Large Dairies, $3000 for Family Farms – Here’s Why — Follows the money on the structural barriers of carbon programs, revealing why scale limits small farms to a $3,000 payout while 2,000-cow dairies pocket $150,000 annually against an identical $40 to $56 per-cow profit potential.

- Unlock Hidden Dairy Profits Through Lifetime Efficiency: How Modern Genetics and Strategic Nutrition Can Cut Feed Costs by $251 Per Cow — Arms you with a genomic blueprint to bypass short-term additive dependencies, delivering $251 in annual feed savings per cow and a 422 kg reduction in lifetime greenhouse gases through targeted residual feed intake selection.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.