Forget emissions-dairy’s new cash cow is methane. Early adopters are cashing in while others lag. Your move.

While most dairy producers still treat environmental compliance like another cost burden alongside SCC penalties and FARM program requirements, a savvy group of innovative farmers is quietly banking profits that make component premiums look like pennies on the parlor floor. The inconvenient truth? Your operation is either positioned to profit from methane reduction, or you’re leaving serious money on the table.

Dairy farmers have mastered transforming forage and grain into milk solids for generations. An elite group is now learning something potentially more valuable: turning methane into money. As global pressure mounts to address agriculture’s carbon footprint, the question isn’t whether you’ll need to reduce emissions- it’s whether you’ll turn that challenge into a revenue stream or watch others in while you play catch-up.

But let’s cut through the manure, shall we? Is the “carbon goldmine” real, or just another consultant’s fantasy like those $30 cwt milk price projections we’ve all stared at? As some claim, can average producers generate $800-1,200 per cow annually from environmental programs? How can your operation profit from this emerging opportunity before the window closes faster than a milk house door in January?

The Carbon Market Reality Check: Opportunity vs. Hype

Let’s start with some straight talk: The widely circulated claim that dairy farms can generate $800-$1,200 per cow annually through carbon credits represents an optimistic best-case scenario rather than a typical outcome. It’s like saying every heifer will conceive on first service and every cow will peak at 150 pounds-theoretically possible, but not what you’d bank the mortgage on.

The reality is more nuanced. Recent analyses of anaerobic digester (AD) projects producing renewable natural gas (RNG) place typical annual revenue closer to $400-$450 per cow when combining California’s Low Carbon Fuel Standard (LCFS) and federal Renewable Fuel Standard (RFS) credits. Still, it is substantial- about $1.25-$1.50 per hundredweight equivalent- but hardly the goldmine some consultants promise.

This doesn’t mean the opportunity isn’t real- it is. But why are so many dairy producers sitting on their hands while early adopters are already cashing in? Is it fear of the unknown? Skepticism of “green” initiatives? Or is it simply the industry’s notorious resistance to change that keeps us a step behind?

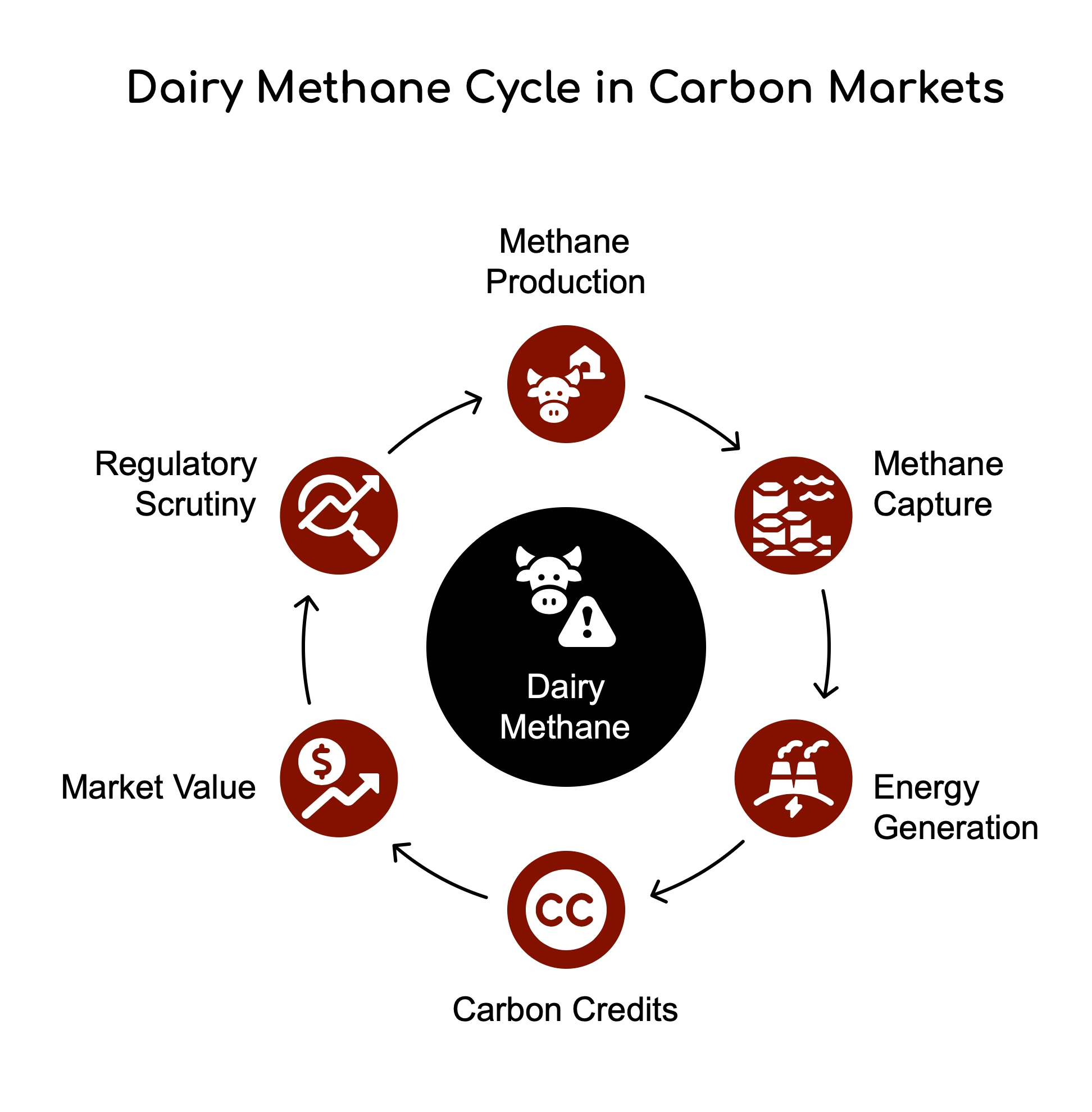

Why Dairy Methane is Carbon Market Gold

What makes dairy operations uniquely positioned in carbon markets? It comes down to methane’s potency and the accounting methods used in carbon crediting.

Methane has been approximately 28 times more potent than carbon dioxide as a greenhouse gas for over 100 years. This means reducing one ton of methane is equivalent to reducing 28 tons of CO2-instantly multiplying the potential credit value. It’s like the difference between shipping whole milk versus protein concentrate- the same truck, exponentially more value.

For dairy operations, methane comes from two primary sources:

- Enteric fermentation – The natural digestive process in a cow’s rumen that produces methane, released primarily through eructation (belching). Your best 35,000-pound Holsteins can produce over 500 liters of methane daily, while your Jerseys might produce somewhat less per head but with higher intensity per pound of milk solids.

- Manure management – Methane is released when manure decomposes anaerobically in lagoons or pits. That 5,000-cow free-stall operation with a 3.5-acre lagoon can generate enough methane to power 1,000 homes.

Under California’s LCFS, dairy RNG receives exceptionally favorable treatment through a methodology that assigns negative carbon intensity scores by crediting “avoided methane emissions.” This accounting approach creates extraordinary value for dairy RNG projects that can access this market.

Let’s be blunt: The dairy industry has been handed a gift in this accounting methodology, and we’d be fools not to capitalize on it. How long do you think regulators will maintain this generous approach if we don’t demonstrate meaningful adoption?

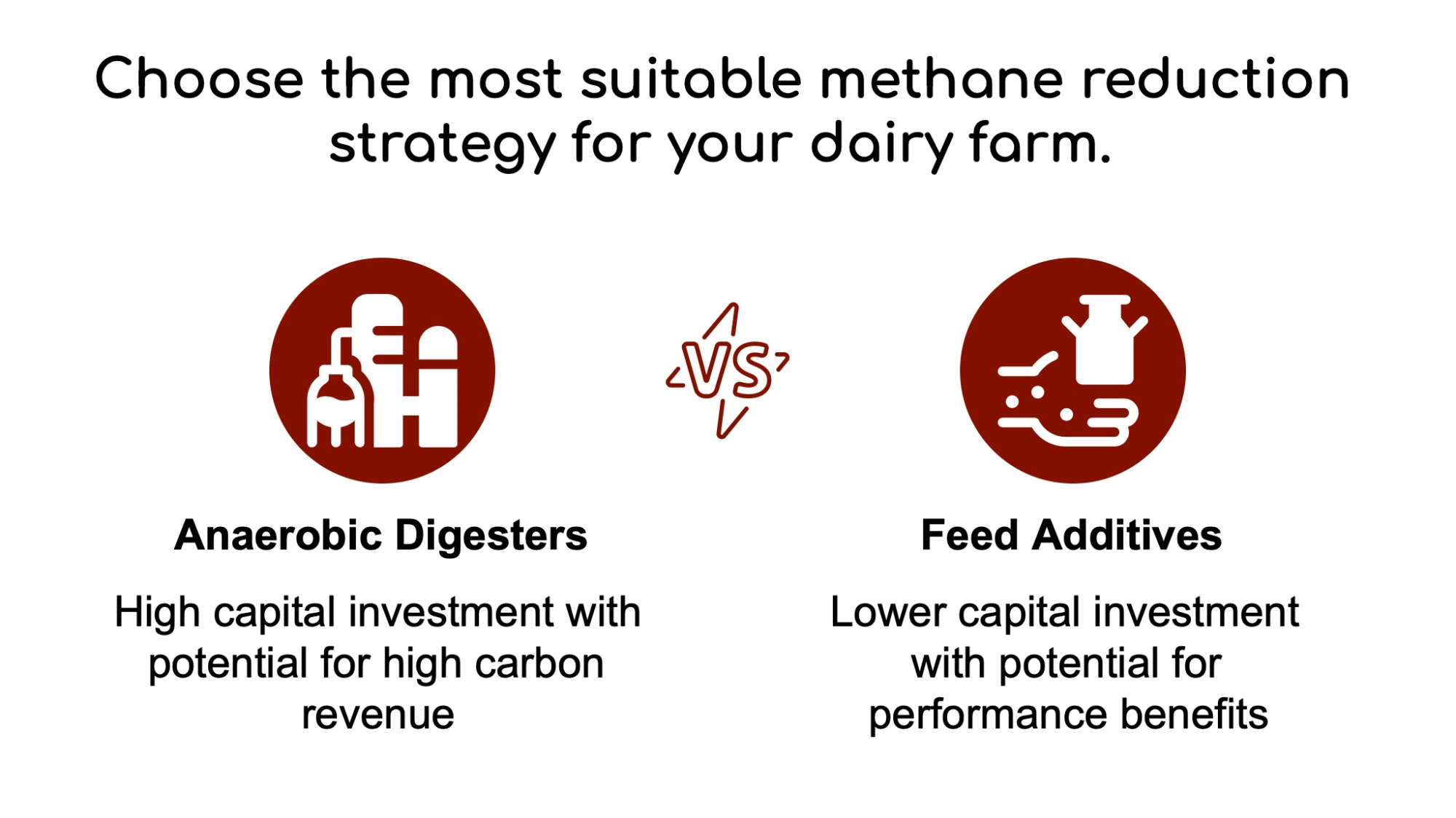

The Methane Reduction Toolkit: What’s Working Now

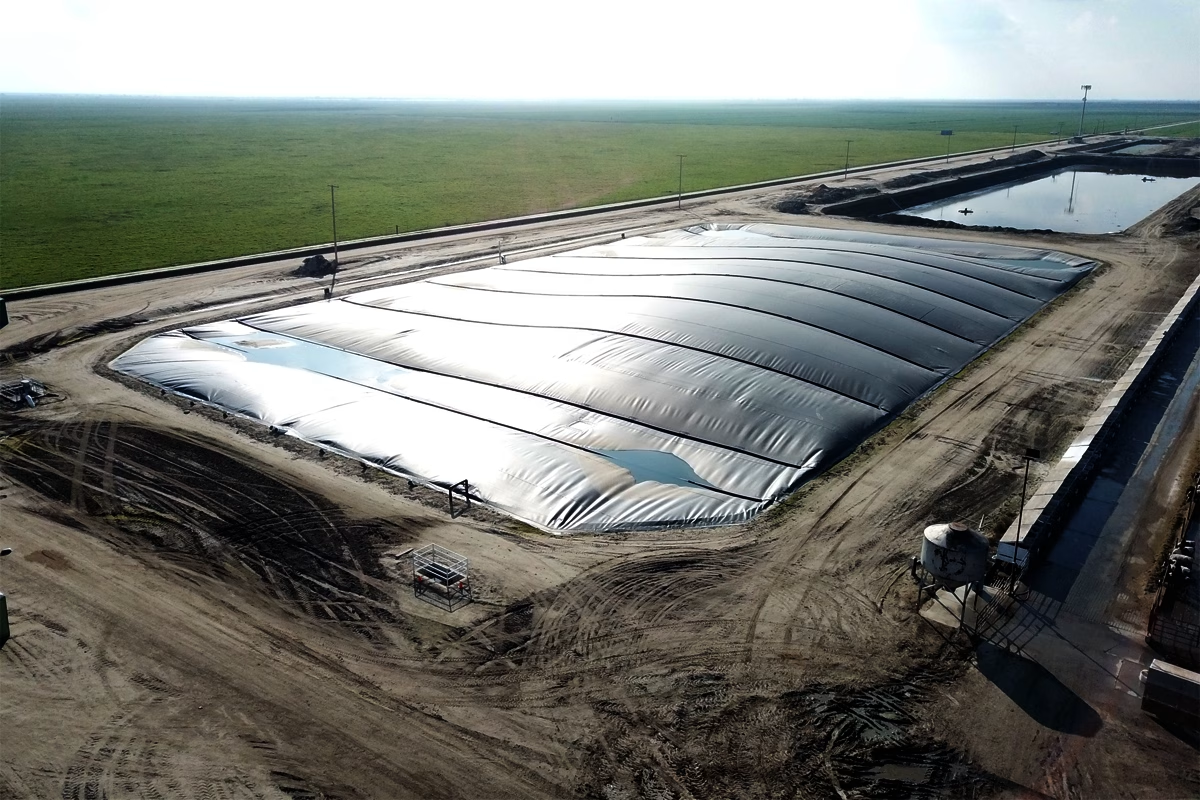

Anaerobic Digesters: The High-Value Pathway

Anaerobic digestion remains the gold standard for generating maximum carbon revenue, particularly when manufacturing RNG for transportation fuel markets.

The economics are heavily scale-dependent operations (typically over 2,000 cows) benefit from economies of scale that make the substantial capital investment (often $3-10 million) more feasible. For medium-sized farms, viability usually depends on grant funding, co-digestion of food waste, or participation in cooperative “hub-and-spoke” models.

Beyond carbon credits, digesters generate valuable co-products: renewable energy, separated solids used as bedding (saving $80-100 per cow annually on sand or sawdust), and nutrient-rich digestate that can reduce commercial fertilizer costs for your corn silage ground.

The practical challenges are significant. Sand bedding- the gold standard for cow comfort and mastitis prevention- can wreak havoc on digester systems, requiring sophisticated separation equipment. Farms with flush systems must carefully consider dilution rates, as too-watery manure (under 3% DM) reduces biogas potential, while thicker scrape manure (8-12% DM) may require different digester designs.

The dairy industry’s current approach to AD adoption is fundamentally flawed. We’ve created a system where only the most significant operations can realistically access the highest-value pathways. Why aren’t we seeing more cooperative models where multiple mid-sized farms combine resources to build shared facilities? The answer lies in our stubbornly independent mindset- the same one that’s held back progress in other areas like genetic improvement, equipment sharing, and marketing innovation.

Feed Additives: The Accessible Option

For farms unable to justify the massive capital investment of digesters, feed additives targeting enteric methane represent a more accessible entry point to carbon markets.

Two leading options are making headway in North American dairy:

3-Nitrooxypropanol (3-NOP/Bovaer®): Developed by DSM-Firmenich and marketed in the U.S. by Elanco, this compound inhibits the enzyme that catalyzes methane production in the rumen. Studies consistently show 25-30% enteric methane reductions in dairy cattle.

The economics are complex. The additive costs approximately $0.15-0.30 per cow daily, and economic analyses suggest performance benefits alone may not offset this cost. Carbon credit revenue becomes essential for adoption, with breakeven estimates ranging from $0.10 to $0.45 per cow daily, depending on carbon price and performance assumptions.

Think of it like rBST back in the day: additive with a proven effect but requiring careful economic calculation. Just as you’d calculate the return on each $40 dose of a reproductive hormone, you need to calculate the return on methane reduction additives with the same precision.

Agolin® Ruminant: This blend of essential oils certified by The Carbon Trust shows more modest methane reductions (around 10-11%) but may offer better economics through improved feed efficiency and milk production. Some analysts suggest benefit-to-cost ratios exceeding 12:1 from performance improvements alone, with carbon credits providing additional upside.

Implementation can be straightforward for operations already using computerized feed management systems like Feed Watch, EZ Feed, or TMR Tracker, as these platforms can document additive inclusion rates and dry matter intake-critical data points for verification.

Here’s a hard truth: Most nutritionists aren’t discussing methane reduction options with their clients because they’re stuck in the mindset that their only job is maximizing milk output. Is your feed advisor bringing these opportunities to your attention, or are they still pushing the same old ration software outputs they’ve used for decades? It’s time to demand more from your nutrition team.

Show Me the Money: How Credits Work

The path from methane reduction to bankable revenue involves several critical steps many producers underestimate. It’s not unlike qualifying for your cooperative’s highest quality premiums- the potential payoff is there, but only if you’re willing to do the work.

Step 1: Project Identification & Feasibility Assessment

Before diving in, you must clearly define your methane reduction strategy and conduct a thorough feasibility assessment. This involves evaluating technical suitability for your specific farm, estimating potential methane reduction, projecting costs, and exploring revenue streams.

Just as you wouldn’t build a new parlor without calculating potential throughput and return on investment, you shouldn’t jump into carbon markets without understanding the numbers. If your BouMatic dealer or DeLaval rep proposed a new system based on best-case scenarios with no downside analysis, you’d show them the door. Apply the same skepticism to carbon project developers.

Step 2: Select Carbon Standard & Methodology

Next, you’ll need to choose a recognized carbon crediting program such as Verra, Climate Action Reserve (CAR), or American Carbon Registry (ACR) and select the specific methodology for your chosen activity.

This is like choosing between organic certification, conventional production, or specialized programs like A2 milk or grass-fed-each, which have specific requirements that dictate your management practices and verification needs.

Step 3: Establish Baseline & Demonstrate Additionality

This is where many projects stumble. You must determine your “business-as-usual” emissions scenario and prove that your reductions wouldn’t happen without carbon market incentives.

It’s somewhat like proving to your lender that you need that operating line to make it through to milk checks-if you’ve got a million in the bank, you won’t qualify for emergency financing.

Step 4: Implement Rigorous Measurement, Reporting & Verification (MRV)

Carbon markets demand meticulous documentation. For digesters, this means continuously measuring biogas flow rates, periodically testing methane concentration, and maintaining precise records of animal populations and manure inputs.

You’ll need to track inclusion rates, measure feed intake, and maintain detailed herd records for feed additives.

If you’ve ever been through a whole-herd DHIA verification for genetic evaluations or maintained records for a Certified Organic audit, you understand the level of detail required. The good news is that farms with existing management software like DairyComp 305, PCDart, or Dairy Management Systems already have many data structures needed for verification.

But many dairy farms still operate with record-keeping systems one step above a pencil and notepad. How can you possibly compete in carbon markets when you can’t even tell me your somatic cell count by string or your pregnancy rate by lactation group? The farms that will capitalize on carbon opportunities are the same ones already using data to drive decisions.

Step 5: Monetize Your Reductions

After verification confirms your emission reductions, you’ll receive carbon credits that can be sold through brokers, direct contracts, or partnerships with project developers.

As milk can be sold as fluid, cheese, powder, or components, carbon credits can be marketed with different value propositions and pricing structures.

The Implementation Roadmap: Different Paths for Different Farms

The optimal carbon strategy varies dramatically based on farm size and circumstances. Here’s how to approach it based on your operation:

For Large Operations (>1,000 cows)

You’re best positioned to consider capital-intensive technologies like anaerobic digesters, particularly those producing RNG for compliance markets. Your scale allows you to achieve the necessary economies to make AD financially viable, especially when leveraging LCFS/RIN credits.

A Western dairy friend with 5,500 Holsteins recently shared that his digester is now generating more annual profit than his milk production, $1.4 million in carbon credit revenue after expenses, while his milk margin hovers around $1.2 million in a good year. It’s become the tail wagging the cow, so to speak.

For Medium Farms (300-1,000 cows)

The economics of standalone AD systems are more challenging at your scale. Viability might be achieved through:

- Significant grant funding

- Co-digestion of off-farm organic waste (generating tipping fees)

- Participation in cooperative “hub-and-spoke” models

Feed additives represent a more financially accessible option for direct methane reduction. Also, the focus should be on improving overall farm efficiency and implementing sustainable cropping practices.

Think of it like buying your combine versus using custom harvesters for your corn silage. The per-ton cost might be higher, but without the capital expenditure and maintenance headaches, it often makes more financial sense at your scale.

For Small Farms (<300 cows)

Individual AD projects are typically uneconomical at your scale unless exceptional subsidies or co-digestion opportunities exist.

Focus instead on:

- Evaluating feed additives (if cost-benefit analysis is favorable with incentives)

- Optimizing manure handling and storage to minimize emissions

- Maximizing production efficiency

- Adopting sustainable cropping and grazing management

Accessing carbon markets requires partnering with an aggregator who can bundle credits from multiple small farms to achieve marketable volumes.

Small farms are getting a raw deal in the carbon economy, but it’s partly our fault. While farmers excel at complaining about processors, cooperatives, and government, we’ve been painfully slow to form the collaborative structures needed to compete in these new markets. When will we learn that sometimes, the only way to maintain independence is through strategic collaboration?

The Early Mover Advantage: Why Timing Matters

The carbon opportunity isn’t static-it’s evolving rapidly, and early adopters stand to gain significant advantages:

- Securing favorable contracts: Early participants can negotiate better terms with developers or credit buyers before the market becomes more crowded.

- Operational experience: Gaining valuable experience in implementing reduction technologies and navigating MRV requirements leads to efficiency gains over time.

- Brand differentiation: Demonstrating proactive environmental leadership enhances your position with processors, consumers, and the community.

- Regulatory positioning: Establishing projects early positions your farm favorably should future regulations mandate emissions reductions.

However, early adoption also carries risks. Carbon markets are subject to significant price volatility, and policies underpinning compliance programs like LCFS and RFS can change, potentially altering eligibility rules or credit values.

It’s not unlike transitioning to robotic milking. Pioneers faced higher costs and steeper learning curves, but many now enjoy labor savings and operational advantages that latecomers are scrambling to match.

Ask yourself this: Are you typically an early adopter, or do you wait until technologies are proven before implementing them? And more importantly, how has that approach worked for your bottom line over the past decade? The dairy industry’s most profitable operators are rarely the first to adopt every innovation, but they’re never the last.

Avoiding the Pitfalls: Common Mistakes That Kill Carbon Projects

Many promising carbon projects falter due to avoidable mistakes:

1. Insufficient Due Diligence

Rushing into projects without a comprehensive understanding of the technology’s suitability, realistic costs and revenues, market risks, and contractual obligations.

Solution: Conduct thorough, independent feasibility studies and seek expert review.

It’s like buying a herd of cattle without seeing them or their DHIA records- the results rarely match the sales pitch.

2. Poor Partner Selection

Engaging with inexperienced or disreputable project developers, brokers, or verifiers.

Solution: Check credentials, demand references for similar completed projects, and verify adherence to industry codes of conduct.

As you carefully select your A.I. company, feed supplier, or equipment dealer, vet your carbon partners thoroughly. The wrong supplier can cost you far more than a few points of conception rate or a slight component drop.

3. Inadequate Record Keeping

Failing to establish robust systems for collecting, managing, and reporting monitoring data accurately and consistently.

Solution: Implement clear MRV protocols, use calibrated equipment, and maintain meticulous records.

Think of MRV as antibiotic residue prevention: The testing will happen, and if your records aren’t in order, the consequences will be severe.

4. Misunderstanding Complex Rules

Failing to fully grasp the nuances of additionality criteria, permanence obligations, or specific methodology requirements.

Solution: Work with knowledgeable advisors and carefully study the relevant protocols.

Carbon markets make the federal milk marketing order look simple by comparison. When hiring a milk marketing consultant for hedging strategies, bring carbon market expertise before committing.

5. Unrealistic Financial Expectations

Overestimating potential carbon credit prices or co-product values while underestimating capital or operational costs.

Solution: Use conservative assumptions and conduct sensitivity analyses.

We’ve all seen those enticing projections where everything goes perfectly- 100% conception rates, no transition cow issues, $25 milk-and reality never measures up. The same applies here.

The Bottom Line: Is Carbon Farming Right for Your Operation?

The dairy industry faces both challenges and opportunities as it addresses methane emissions. While the often-cited revenue potential of $800-$1,200 per cow per year represents an optimistic scenario rather than a guaranteed outcome, real financial opportunities exist.

Forward-thinking dairy producers who undertake thorough feasibility studies, select appropriate technologies and partners, implement robust MRV systems, and manage risk effectively can potentially transform environmental compliance from a cost center into a profit opportunity.

The most frustrating aspect of the dairy carbon discussion is watching farms drag their feet while consultants and developers with no skin in the game make all the decisions. It’s time for dairy producers to seize control of this narrative and develop carbon reduction strategies that benefit farms first and foremost, not just the middlemen.

As one innovative Wisconsin producer put it: “Carbon isn’t just about compliance anymore-it’s becoming as much a part of our business model as milk production itself. On our 1,200-cow operation, the methane we capture offsets the carbon footprint of our entire milk supply chain, and the processor premium we get for that is worth nearly a dollar per hundredweight. Between that and the bedding savings from separated solids, we’ve turned what used to be a waste management headache into a solid profit center.”

Your Call to Action

It’s time to stop viewing environmental practices as merely a cost of doing business and start recognizing them as potential profit centers. Here’s what you need to do today:

- Assess your farm’s carbon potential by requesting a baseline emissions assessment from a qualified consultant

- Explore multiple technology options, not just what the first salesperson tries to sell you

- Talk to producers who have already implemented these systems rather than relying solely on developer claims

- Demand more from your industry organizations in creating collaborative models that make carbon markets accessible to farms of all sizes

- Start improving your record-keeping systems now, even if you’re not ready to implement a carbon project immediately

The carbon opportunity won’t wait for those who drag their feet. Are you ready to mine the carbon goldmine on your farm, or will you watch from the sidelines as your competitors cash in?

Key Takeaways:

- Methane isn’t just emissions-it’s a revenue stream via carbon credits, with compliance markets (LCFS/RFS) offering the highest payouts.

- Anaerobic digesters dominate profitability but demand heavy upfront costs; feed additives (e.g., 3-NOP, Agolin) provide low-barrier entry.

- The $800-$1,200/cow claim is aspirational-realistic returns hover near $400-$450/cow for RNG projects.

- Early adoption matters: First movers lock in contracts, build expertise, and position as sustainability leaders.

- Success requires feasibility analysis, risk mitigation, and leveraging USDA/EQIP grants or aggregator partnerships.

Executive Summary:

Forward-thinking dairy producers are transforming methane reduction from a regulatory burden into a lucrative revenue stream. By leveraging carbon markets, technologies like anaerobic digesters (generating $400-$450/cow annually via compliance credits) and methane-inhibiting feed additives are turning environmental compliance into profit. While the widely touted $800-$1,200/cow claim reflects peak market optimism, real opportunities exist for farms willing to navigate complex verification processes and volatile credit prices. Success hinges on strategic partnerships, rigorous feasibility studies, and aligning practices with compliance or voluntary markets. Early adopters gain competitive advantages as corporate sustainability demand grows, but scalability and policy risks require careful management.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.