Butterfat’s up 5.3% this year—that’s $20 extra per cow monthly if you’re paying attention.

EXECUTIVE SUMMARY: Here’s what caught my eye in the latest numbers. Milk production jumped 3.3% in June, but the real money maker is butterfat and protein climbing nearly 5%—we’re talking an extra $15-20 per cow each month for operations hitting these targets. Kansas and South Dakota are absolutely crushing it with strategic genomic selection and precision feeding programs. Meanwhile, Argentina’s ramping up 12% while Europe pulls back 5%, which means export opportunities are shifting our way. The farms winning this game aren’t just pumping more milk—they’re getting smarter about components, feed efficiency, and risk management. You should seriously look at your component premiums and feeding program if you haven’t already.

KEY TAKEAWAYS

Push your butterfat above 4.0% through better ration balancing—that 5% bump translates to roughly $1800 extra monthly income per 100 cows. Start by tweaking your forage-to-concentrate ratios.

Lock in 60-70% of your feed costs now while corn’s sitting at $4.05/bushel—this simple hedge can save you $100+ per cow annually when markets get volatile.

Use genomic testing on your replacement heifers—operations doing this right see 10-15% better lifetime production and components. It’s not just about milk volume anymore.

Get Dairy Revenue Protection coverage with premiums as low as 20-30 cents per hundredweight—when margins can swing $2-3, that’s cheap insurance for your milk checks.

I’ve been watching these numbers for a while, and the latest USDA report really got me thinking. This isn’t just about making more milk—it’s about the industry pivoting beneath the surface.

According to USDA-NASS, milk production in the major states reached 18.5 billion pounds in June 2025, a 3.3% increase from the same month a year ago. Kansas led with a 19% jump in April, producing 382 million pounds and swelling its herd by 9.25% to 189,000 cows. Meanwhile, data from the South Dakota Agricultural Office show that the state’s dairy herd has doubled in the last decade, now numbering around 215,000 cows.

What’s behind this surge? Smart investments. Cheese plants, such as Bel Brands and Valley Queen, are expanding, positioning these regions as new dairy powerhouses.

State

Herd Size (2025)

Growth Rate

Key Advantage

Processing Investment

Kansas

189,000 cows

+19% (April)

Lower regulations

Expanding capacity

South Dakota

215,000 cows

+117% (decade)

Land availability

Bel Brands, Valley Queen

Wisconsin

1,270,000 cows

+2.1%

Established infrastructure

Mature market

California

1,720,000 cows

-0.8%

Scale & technology

Market saturation

Components Drive the Real Value

But it’s not just volume—it’s quality too. Butterfat shot up 5.3% and protein climbed near 5%. Producers are pushing butterfat over 4.0% and protein around 3.4%, which matters when you consider Chicago Mercantile Exchange data showing butter at $2.47 per pound and Class III futures near $17.23 per hundredweight.

Feed prices ease somewhat—corn hovers around $4.05 per bushel, December futures near $4.30. Producers locking in 60-70% of feed volume early, a strategy backed by University of Wisconsin Extension research, are managing risk effectively.

Technology and Risk Management Take Center Stage

Risk management is ramping up across the board. Dairy Revenue Protection is becoming standard, offering premium coverage ranging from $0.05 to $0.40 per hundredweight, according to USDA Risk Management Agency data.

Technology advances also play a role. Precision feeding systems, especially on farms with more than 400 cows, deliver returns that often paying back in two years with proper data use. Cornell University research highlights these efficiency gains.

Globally, shifts continue—European production dips by 5%, while Argentina’s grows by 12%, restructuring the competitive landscape.

What Winning Producers Focus On

Here’s what the most successful operations prioritize:

Component optimization—genetics, nutrition, and culling strategies for improved butterfat and protein yields

Strategic feed cost management—hedging decisions and bulk purchasing timing

Thoughtful technology adoption—matching tools like genomic testing and precision feeding to operational scale

Building strong processing partnerships—aligning with facilities’ expanding capacity and market reach

The Bottom Line

The industry is becoming increasingly data-driven and geographically diverse, with quality now taking precedence. Those who adapt quickly and strategically will thrive.

These trends speak to a new era—one where management precision, quality focus, and risk mitigation define success. The bottom line? Volume’s nice, but quality pays the bills in 2025. Time to think like a business, not just a production unit.

Stay alert and nimble. The market’s evolving fast, and the winners will be those who move first.

Analysis based on data from USDA-NASS, Kansas Livestock Association, South Dakota Agricultural Office, Chicago Mercantile Exchange, University of Wisconsin Extension, Cornell University, and USDA Risk Management Agency.

Learn More:

The Ultimate Guide To Increasing Butterfat & Protein – This article provides practical strategies for ration balancing and feed management. It demonstrates how to fine-tune your nutrition program to maximize component premiums, directly supporting this article’s focus on profitability beyond just milk volume.

Dairy Herd Expansion: To Grow or Not To Grow – For producers inspired by the growth in Kansas and South Dakota, this piece explores the critical financial and operational questions behind expansion. It provides a framework for making smart, strategic decisions before investing in new facilities or cows.

Genomic Selection: The Genetic Advantage That Goes Beyond Production – Move beyond the basics of precision feeding and discover how to leverage genomics for long-term value. This article reveals methods for selecting health, fertility, and feed efficiency traits to build a more resilient and profitable herd for the future.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

June milk production jumped 3.4% while feed costs dropped — here’s how smart farms are cashing in on both trends.

EXECUTIVE SUMMARY: June numbers came in hot — 3.4% production jump to 18.5 billion pounds, and here’s the kicker… it’s not about pumping more milk anymore, it’s about making better milk. Operations focusing on components are seeing butterfat hit 4.23% and protein at 3.29%, which translates to an extra $15-20 per cow monthly. That’s $120,000+ annually for a 500-cow operation just from optimizing what’s already in the tank. Feed costs finally dropped too — corn’s forecast at $4.20/bushel, giving smart producers breathing room to upgrade their protein programs.The Canadians and Europeans are already ahead of us on this component game, and frankly… we’re playing catch-up. You need to start thinking genomics and precision feeding now, not next year.

KEY TAKEAWAYS

Component premiums are printing money — Farms averaging 4.5% butterfat and 3.4% protein are banking an extra $0.75-$0.90 per hundredweight. Start genomic testing your replacement heifers today and breed for components, not just volume.

Feed cost relief creates opportunity — With corn at $4.20/bushel, reinvest those savings into bypass proteins and amino acid programs. Operations doing this right are cutting total ration costs 15% while boosting milk quality.

Robot adoption is hitting breakeven faster — Early adopters are seeing 22-month paybacks at current milk prices, plus 23% labor cost reductions. If you’re milking 200+ cows and struggling with labor, run the numbers now.

Regional positioning matters more than ever — Texas and Kansas operations are locking in processing contracts while traditional dairy regions scramble. Secure your milk marketing agreements before capacity fills up.

Technology + genetics = competitive advantage — Farms combining genomic selection with precision feeding are outperforming volume-focused operations by $180,000 annually per 1,000 cows. The gap’s only getting wider in 2025.

We all felt it before the USDA numbers hit. June was… different. Tanks were fuller, checks looked better, and suddenly everyone’s talking about this 3.4% year-over-year production jump like it came out of nowhere. But here’s the thing—this wasn’t some fluke weather event or lucky break. This was years of strategic moves finally paying off, and if you missed it, you’d better understand why your neighbors are starting to pull ahead.

I was at a processor meeting last week, and the room went quiet when someone mentioned their June intake numbers. Dead quiet. Because everybody knew what those numbers meant—some farms are playing a completely different game now.

The Numbers That Actually Tell the Story

Indicator

June 2024

June 2025

Δ % YoY

24-state milk output

17.90 billion lb

18.50 billion lb

+3.4%

U.S. dairy cow herd

9.33 million hd

9.46 million hd

+1.4%

Milk per cow (24 states)

2,045 lb

2,110 lb

+3.2%

2025 Q2 output (U.S.)

58.6 billion lb

60.0 billion lb

+2.4%

The official USDA Milk Production report for June 2025 confirmed what we were feeling: 18.5 billion pounds of milk in the 24 major states, a 3.4% increase from the 17.9 billion pounds in June 2024. Production per cow hit a record 2,045 pounds, up 30 pounds from the same month last year.

The milk cow herd in the 24 major states was 9.03 million head, representing an increase of 151,000 head from June 2024. This expansion comes even as replacement heifer prices hold at record levels—and that’s telling you something about confidence in the fundamentals.

What’s really fascinating is how this played out regionally. Take the Central Valley—I know operations that are still struggling with H5N1 recovery from last fall. Some herds are still down 8% from pre-outbreak levels, but they are now seeing consistent monthly improvements.

Meanwhile, their neighbors—same feed, same climate, different management approach—posted double-digit jumps over last June. This isn’t just anecdotal. University extension specialists I’ve spoken with confirm this trend, noting that operations recovering from disruption are implementing comprehensive system upgrades, not just replacing what they lost.

What’s interesting is how this trend mirrors what we’re seeing globally. European producers have been dealing with their own production volatility, and New Zealand’s producers are facing similar challenges with weather patterns and input costs. The difference? U.S. producers who adapted early are actually gaining competitive ground internationally.

When you’re seeing fresh cows trade for $2,600-plus and operations are still expanding, what’s the outlook? That tells you where smart money sees profitability heading.

Feed Economics: The Game-Changer Nobody Saw Coming

Here’s where things get really interesting, and honestly, where I think some producers are going to get left behind if they don’t pay attention.

Feed costs. That elephant that’s been stomping around the room for what, three years now? But this spring changed everything. According to the latest USDA World Agricultural Supply and Demand Estimates (WASDE) report, corn is forecast at $4.20 per bushel for the ’25/’26 season. Soybean meal is projected to cost around $310 per short ton, which isn’t cheap, but it’s manageable when your energy costs drop.

Metric

June WASDE (May 12)

Revised June 24 Actual

Variance

Comments

2025 milk, calendar-yr

227.8 billion lb

Tracking 228.3 billion lb annualised

+0.5 billion lb

USDA lifted its forecast 500 million lb in July on herd growth

All-milk price (’25)

$21.95/cwt

Spot forecast $21.60/cwt

-$0.35

Higher supply offsets butter price strength

Class III (’25 avg.)

$18.65/cwt

Futures $18.40

-$0.25

Cheese inventories +4% YoY

Class IV (’25 avg.)

$18.85/cwt

Futures $19.05

+$0.20

Butterfat demand still robust

This created what I’m calling the “feed relief rally.” Suddenly, operations that were white-knuckling through $5+ corn could breathe again. But here’s the catch—and there’s always a catch, right? While corn prices became more favorable, protein costs remained stubborn.

This is the “barbell economy” in action: low-cost energy inputs on one side (like corn) and high-cost, high-value inputs on the other (like specific amino acids and bypass proteins).

Let me break this down with some real numbers. A 1,000-cow operation that was spending $180,000 monthly on feed last year might be looking at $165,000 now—if they strategically reinvested their corn savings into a more efficient protein program. That’s $180,000 annually back in their pocket, which could cover a robot payment, facility upgrades, or just straight profit.

I was speaking with a nutritionist who works with approximately 40 farms across the Upper Midwest. He told me something that really stuck:

“The farms that are crushing it right now aren’t the ones who just dumped more corn in the TMR when prices dropped. They’re the ones who used the corn savings to upgrade their protein program and push butterfat numbers.”

Dairy nutrition experts emphasize that corn cost savings should be reinvested in protein program optimization—something the industry has been preaching for years but now finally has the margin room to implement. The farms that figured this out early are the ones posting those eye-popping June numbers.

The Technology Revolution (Finally Paying Off)

What’s particularly noteworthy is how technology adoption is finally showing real ROI. Robotic milking systems are gaining significant traction across operations of all sizes, but the farms that use them strategically are seeing returns that make the rest of us take notice.

This development is fascinating because it’s not just about the U.S. anymore. Canadian producers have been ahead of us in adoption rates—about 8.7% of their cows are milked by robots, compared to our numbers—and they’re sharing data that’s helping to accelerate learning curves here.

Let me tell you about a Michigan producer I’ve been following—runs multiple robots on about 240 fresh cows, added another unit in March. His labor situation went from crisis to competitive advantage almost overnight.

Not because robots eliminate labor (they don’t), but because they let you deploy people where they actually add value instead of just standing in a parlor twice a day.

The investment’s substantial—we’re talking significant capital depending on the brand, features, and necessary facility retrofits—but this producer’s projecting a sub-24-month payback, based on current milk prices and redeploying labor units. Here’s his math: at $23.50/cwt milk and saving 1.5 FTE positions at $45,000 each, plus production gains of about 8 pounds per cow daily… the numbers work.

He said something that really hit me:

“I’m not just buying equipment, I’m buying the ability to scale without scaling my biggest headache.”

But here’s what nobody talks about enough… the learning curve is steep. Really steep. I am aware of another operation that installed robots last year and spent six months dealing with cow traffic issues because they hadn’t properly redesigned their facility. They’re finally hitting their stride now, but those first six months were brutal.

Robotic milking specialists indicate that facility design accounts for the majority of system success. You can’t just drop advanced technology into an existing setup and expect miracles.

Butterfat Numbers Don’t Lie (And Neither Do Paychecks)

This is where genetics finally started paying real dividends. We’ve been hearing about genomic selection for years, but 2025 is when you can actually see it in the tank and on your milk check.

According to a Q2 2025 analysis from CoBank’s Knowledge Exchange, national butterfat levels hit 4.23% in 2024, and early 2025 data suggests we’re not backing off that trend. Protein is averaging 3.29% across the Federal Milk Marketing Order system, which means your component checks are carrying more weight than ever.

The farms that figured this out early? They’re not just making more milk; they’re making more valuable milk. And in a multiple-component pricing world, that’s everything.

What strikes me about this shift is how it’s creating entirely different business models. Traditional volume-focused operations are finding themselves competing against component-optimized farms that might produce less total milk but generate higher revenue per hundredweight.

I know operations—particularly in Pennsylvania and the Northeast—that have been laser-focused on components for three years. They’re averaging well above 4.5% butterfat and pushing 3.4% protein. Their June component premiums alone were worth an extra $0.75-$0.90 per hundredweight over regional averages. With decent production per cow, that’s serious money—sometimes $15-20 per cow per month straight to the bottom line.

Pennsylvania dairy producers focusing on components report significant premium advantages that compound month after month. As one told me recently, “Every genetic decision, every feeding tweak, every management choice gets measured against components first, volume second.”

Here’s the math that’ll get your attention: a 500-cow operation averaging 70 pounds per cow daily with a $0.80/cwt component premium is looking at an extra $10,080 monthly. That’s $120,960 annually just from optimizing what’s already in the tank.

Regional Reality Check: Winners and Losers Emerge

Region

Stand-out States

YoY Δ %

Contributing Factors

Southwest

Texas

+9%

45,000-cow expansion, new panhandle cheese capacity

High Plains

Kansas

+16%

16,000-cow build-out; three large green-field barns filled

21,000 more cows, genetic gains in fat % and protein %

Northwest Coast

Washington

-3%

Lingering HPAI culls, heat-stress spike mid-month

Here’s what’s happening in the real world, away from the national averages, and this is where it gets uncomfortable for some folks.

The expansion states—Texas, parts of Kansas, South Dakota—they’re building fresh capacity and filling it with good genetics and modern management. Meanwhile, some traditional dairy regions are watching this shift and wondering if they missed the boat.

Take Texas… they’ve been aggressive about new greenfield operations near those big cheese plants in the Panhandle. I heard from contractors working on multiple 4,000-cow facilities that’ll be online before Christmas. That’s not just growth; that’s strategic positioning, with $10 billion in new processing assets coming online throughout the U.S. through 2027.

Metric

Jan–Jun 2024

Jan–Jun 2025

Δ %

Driver

U.S. cheese exports

497 million lb

540 million lb

+8.7%

EU supply constraints

Skim-powder exports

772 million lb

735 million lb

-4.8%

China demand lull

Butter-fat exports

52 million lb

74 million lb

+42.3%

MENA bakery demand

This pattern of strategic positioning around processing hubs isn’t unique to the U.S.; it reflects consolidation trends we’re seeing internationally. Australia has been consolidating its operations for years, and European producers are facing similar pressure to scale or specialize. The difference is that our expansion states still have access to land and water that much of the world lacks.

California’s recovery from H5N1 has been slower than anyone had hoped, but the operations that came back strong implemented biosecurity measures that should’ve been standard practice years ago. It’s expensive—around $12,000 per 1,000-cow facility from what I’m hearing—but the alternative is watching your herd get wiped out.

Here’s the thing, though… some of the traditional dairy regions are fighting back smarter than expected. I know operations in New York and Wisconsin that are leveraging their location advantages—being closer to population centers, having better infrastructure, and established relationships—to compete on service and quality, rather than just scale.

Agricultural economists observe that location advantages, combined with management expertise, create a competitive positioning that’s hard to replicate through size alone.

The Management Revolution Behind Those Numbers

What strikes me most about June’s numbers isn’t the production increase—it’s the management sophistication that made it possible. Precision feeding, genetic optimization, and facility design… these are no longer buzzwords. They’re the difference between farms that thrive and farms that just survive.

The operations killing it right now have figured out that success isn’t about any single technology or practice. It’s about systems thinking.

Feed management that optimizes for components, not just pounds. Genetics programs that target profitable traits. Facility design that works in harmony with cow behavior, rather than against it.

I was on a farm in Ohio last month—approximately 450 cows, but every system was perfectly dialed in. The owner walked me through their feeding program, and I swear, he knew the exact cost per pound of every ingredient and how it impacted milk composition. His feed efficiency was running 1.38 pounds of milk per pound of dry matter—that’s exceptional territory.

That level of precision… it’s evident in the numbers. And honestly? A lot of farms are still fighting the last war—optimizing for milk volume when the money’s in milk value.

This trend suggests we’re moving into an era where data literacy becomes as important as animal husbandry skills. The operations that can merge traditional stockmanship with modern analytics are building sustainable competitive advantages.

Risk Factors Nobody Wants to Discuss

Here’s where we need to get real for a minute, because this success story has some warning signs attached.

Weather dependency is huge. June’s favorable conditions helped, but we’re heading into August heat with climate patterns that, to be honest, are unpredictable. The operations that have invested in cooling systems and heat stress management are likely to have a significant advantage if another scorching year like 2023 is on the horizon.

Current global weather patterns are exhibiting concerning similarities to 2012—the last time we experienced a particularly devastating drought. European producers are already facing water restrictions in some regions, which is creating ripple effects in global feed markets.

Processing capacity constraints are building. Those big cheese plants everyone’s building to supply? They’re already running at 85-90% capacity. When they hit their limits, spot milk pricing will become volatile—and not in a way that favors producers without solid contracts.

Labor quality and availability continue to deteriorate in most regions. Technology can help, but it can’t fix everything. The farms that are succeeding aren’t just investing in automation, they’re investing in training their people to work with advanced systems.

Water availability is the sleeper issue. For producers in the West and Southwest, securing long-term water rights is becoming as critical as securing a feed contract. The new facilities in Texas are being built with water strategy as a primary concern, a risk factor that can no longer be ignored.

There’s also a global factor we don’t discuss enough—currency fluctuations affecting export competitiveness. When the dollar strengthens, our exports get more expensive, and that matters more now that we’re producing component-rich milk that commands premium prices internationally.

Forward-Looking: What This Means for Your Operation

Looking ahead, the fundamentals that drove June’s success remain in place, but the competitive landscape is shifting rapidly. Feed costs appear manageable through harvest, and processor demand remains solid. The farms that invested in the right infrastructure are well-positioned to continue capitalizing.

However, here’s the uncomfortable truth: a storm cloud is building that nobody wants to discuss. What happens when everyone catches up? The competitive advantage of being early to automation, early to component optimization, early to precision management—that advantage erodes as more farms make these moves.

The question isn’t whether your operation should modernize. The question is whether you can afford to wait while your neighbors build advantages that’ll be hard to overcome.

I was talking to a banker who specializes in dairy financing, and he put it perfectly:

“The farms that are borrowing money for technology and genetics right now are going to be the ones buying their neighbors’ cows in three years.”

June’s numbers weren’t just about good weather and cheaper corn. They were about an industry finally reaching its stride after years of changes. The farms that understood this early are reaping the rewards. The ones still figuring it out? They better move fast, because this train’s picking up speed.

What’s happening globally reinforces this urgency. Producers in other major dairy regions are making similar transitions, and the competitive landscape is becoming increasingly sophisticated. The margin for error is shrinking, and the rewards for getting it right are growing.

The result is undeniable: we’re creating two different dairy industries. One that’s profitable, efficient, and sustainable. And one that’s just trying to hang on.

The question is, which one are you building?

What’s your best ROI technology investment of 2025? Share your experience in the comments below—your insights could help a fellow producer make the right call.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

The Butterfat Revolution: 5 Strategies to Maximize Your Component Premiums – This article provides the tactical “how-to” behind the main story’s component theme, offering five actionable feeding and management strategies you can implement immediately to boost butterfat production and capture higher premiums on every shipment.

Beyond the Robot: How AI is Creating the ‘Smart’ Dairy Barn – If robotics is today’s revolution, AI is tomorrow’s. This piece explores the next frontier of dairy tech, demonstrating how artificial intelligence is being used to integrate data, predict health events, and find efficiencies you never knew existed.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

5% component-adjusted growth while markets tanked? Something’s broken in how we’re thinking about milk production.

EXECUTIVE SUMMARY: You know that feeling when good news hits like bad news? That’s exactly what happened with June’s milk production report. We hit 19.23 billion pounds nationally—up 3.3% year-over-year—but markets sold off hard anyway. The real story isn’t the volume; it’s that component-adjusted production surged 5% while geographic production is completely reshuffling. Kansas jumped 19.1% thanks to new processing capacity while Wisconsin barely moved at 0.3%. Meanwhile, butterfat climbed to 4.18% and protein hit 3.25%—those improvements alone are worth serious money per hundredweight. European competitors are struggling with environmental constraints, creating export opportunities, but domestic demand challenges aren’t going away. Here’s the thing: if you’re still thinking volume-first instead of components-plus-location strategy, you’re already behind where this industry’s heading.

KEY TAKEAWAYS

Component premiums are the new profit center – With butterfat up 2% and protein up 1.5% year-over-year, focus on genetics and nutrition programs that boost components rather than just volume. That 5% component-adjusted growth versus 3.3% base growth represents real dollars on every milk check.

Geography is destiny in 2025 – Plains states with new processing capacity are seeing explosive growth (Kansas +19.1%, Texas +9.5%) while traditional regions stagnate. If you’re planning expansion, secure processing agreements first—capacity constraints are creating 18-24 month margin pressure cycles.

Feed cost advantages won’t last forever – Current milk-to-feed ratios around 1.8 are workable, but smart producers are locking grain prices now. Weather, trade issues, or energy costs could flip the equation overnight, so build flexibility into your feed program.

Export opportunities exist but don’t count on them – U.S. cheese exports are strong while Europe struggles with environmental limits, but building your whole strategy around international demand is risky. Domestic foodservice demand remains weak, so diversify revenue streams through beef-on-dairy programs.

Strategic thinking beats volume obsession – Cornell analysis suggests 75-85% probability of continued margin pressure through early 2026. Winners will be operations that read market signals, optimize for components over volume, and adapt quickly when conditions change.

You know that pit-in-your-stomach feeling when production reports should make you smile, but instead your phone starts buzzing with panicked calls from concerned producers? That’s exactly where we landed when June’s milk numbers dropped. The raw data—19.23 billion pounds nationally, up a whopping 3.3% from last year—should’ve had us popping champagne. Instead, markets sold off sharply, and honestly, that disconnect is telling us everything we need to know about where this industry’s headed.

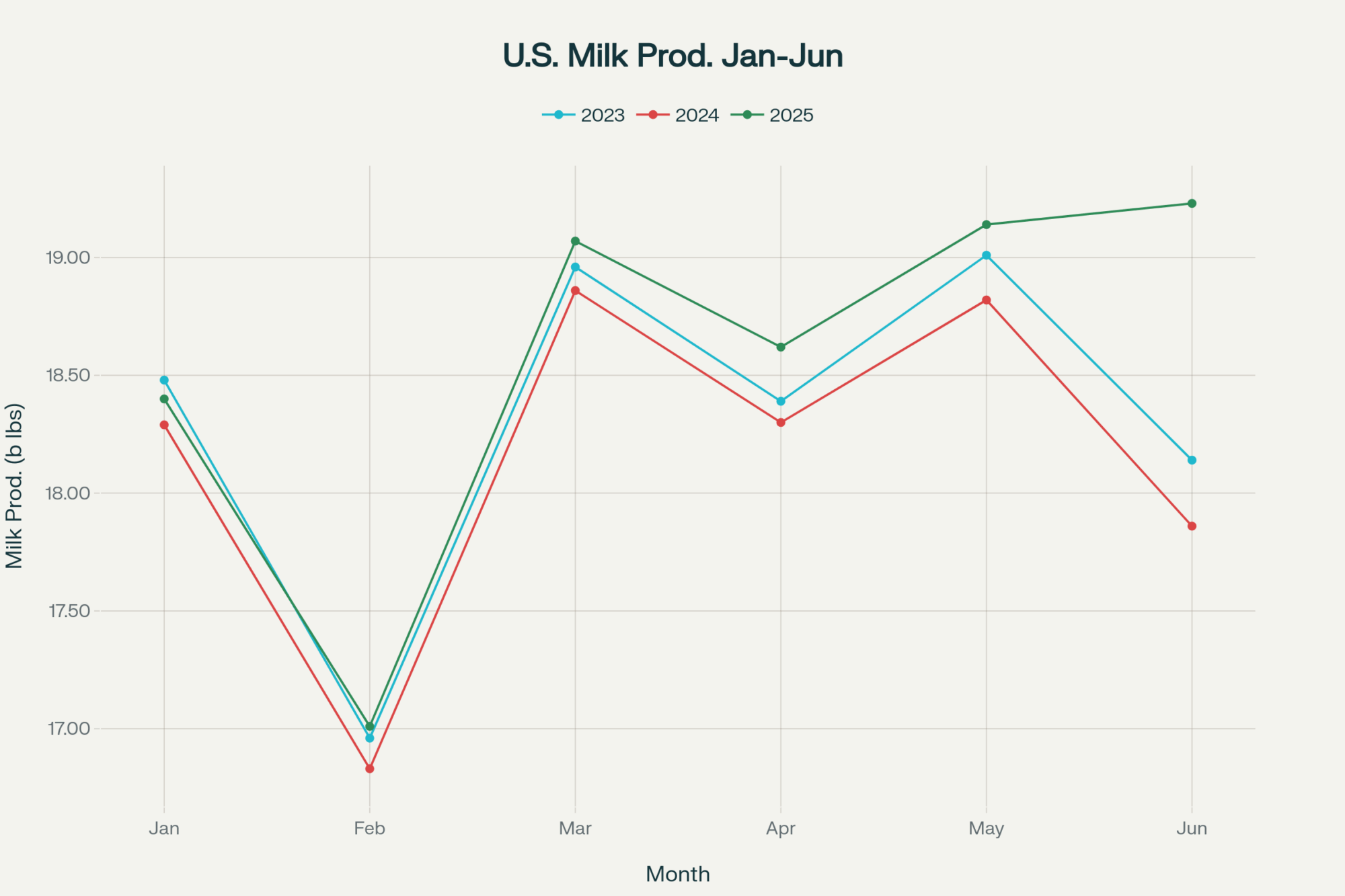

Monthly U.S. Milk Production Trend for January–June, 2023–2025

When Crushing Expectations Becomes the Market’s Nightmare

What strikes me about June’s numbers is how they caught absolutely everyone off guard. According to the latest StoneX analysis¹, the report was “bearish compared to expectations”—and that’s coming from analysts who eat, sleep, and breathe these numbers.

We didn’t just meet projections… we obliterated them. Most folks were penciling in maybe 2% growth, but here we are staring at production that jumped 3.3% year-over-year. What really gets my attention, though, is how the component story amplifies everything. Our butterfat content increased to 4.18% (up from 4.10% last year), while protein levels rose to 3.25%(up from 3.20%). When you factor in those improvements—and this is crucial for understanding the real market impact—we’re looking at component-adjusted production that surged 5% year-over-year.

Five percent! The last time we saw growth like that? May 2021, right when everything was still bouncing back from pandemic disruptions.

What really caught my attention was the 2,031 pounds per head in June, up 1.7% from the previous year. Now, before anyone gets too carried away, remember that we’re comparing this to a brutal June 2024 when H5N1 absolutely hammered production numbers across key regions. The StoneX folks note we were “lapping over a 1.7% drop last year due to bird flu,” so there’s definitely some recovery built into that figure.

However, here’s the thing that should make everyone pause—we’ve added 114,000 head since December (that’s equivalent to adding several good-sized dairies every month), and we’re still seeing these kinds of individual animal improvements. Mark Stephenson from Wisconsin’s dairy markets program has been tracking these patterns for decades, and as he pointed out in his recent university brief, “when you see both scale and efficiency gains happening together, producers are clearly responding to sustained positive signals… but markets don’t always interpret additional supply as welcome news.”

The Geographic Revolution That’s Rewriting Our Industry Map

What’s happening regionally is what really gets my blood pumping about this data. Producers are “culling fewer dairy cows” because margins have been workable, but that’s just scratching the surface.

Year-over-Year Milk Production Change by State, June 2024-2025

Look at these Plains states numbers and tell me we’re not watching a fundamental restructuring:

Texas: jumped 9.5% to 1.503 billion pounds

Kansas: posted a jaw-dropping 19.1% increase to 400 million pounds

South Dakota: surged 11.5% to 255 million pounds

Meanwhile, traditional regions are struggling:

Washington: dropped 9.3% to 475 million pounds

California: managed only 2.7% growth despite adding cows

Wisconsin: barely budged at 0.3%

Milk Production Composition by Top States in 2025

That Kansas number isn’t some statistical fluke. That’s the new Hilmar cheese facility in Dodge City pulling milk like a powerful magnet. I was talking to a producer near there recently—he’s been shipping to that region for about eighteen months now—and he said the local milk market dynamics have completely changed. Premium pickups, shorter hauls, predictable demand… it’s exactly what every operation wants.

Here’s the thing, though, and this is where it gets uncomfortable for those of us in traditional dairy country. Industry investment exceeding $10 billion is flowing toward areas where operations can actually pencil out profitably. Smart money follows processing capacity, and that capacity is definitely heading south and west.

Brian Gould from UW-Madison doesn’t mince words about this trend; he pointed out that “we’re witnessing the most significant geographic restructuring of U.S. dairy production since the 1970s, but this time it’s being driven by regulatory environment and processing economics, not just feed costs.” That’s a sobering assessment from someone who’s tracked these patterns longer than most of us have been in the business.

The Market Reality Nobody Wants to Face

Now, here’s where the story gets really uncomfortable —and why those market reactions weren’t just traders having a rough day. Despite these impressive production numbers, we face some fundamental demand challenges that are unlikely to be resolved anytime soon.

Restaurant traffic still hasn’t bounced back to where we need it. When you consider that over half of America’s food dollars get spent outside the home, weak foodservice demand creates problems that more milk simply can’t solve. Major restaurant chains have been reporting declining traffic in recent quarters, and that ripple effect is felt in cheese demand faster than most people realize.

The Processing Bottleneck That’s Coming for All of Us

What really concerns me—and I’m hearing this from plant managers across multiple regions—is that some facilities are already approaching capacity limits, while others are having to implement milk dumping protocols when volumes exceed what they can handle. We’re seeing this with current production levels, not the higher volumes everyone’s projecting for the rest of .

Recent analysis from Cornell’s Program on Dairy Markets and Policy suggests this kind of regional capacity mismatch typically pressures milk prices for 18 to 24 months until infrastructure catches up or production adjusts. When analysis from sources like Cornell suggests a 75-85% probability of continued margin pressure through early 2026 based on current supply trajectories, that timeline isn’t exactly encouraging news if you’re planning expansions.

Feed Costs Keep Things Manageable… For Now

The one bright spot that’s keeping margins workable? Feed costs haven’t gone completely sideways on us. We’re seeing corn futures trading in the low-four-dollar range, and while protein feeds aren’t cheap, they’re not breaking operations either. That’s maintaining milk-to-feed ratios around 1.8, which most producers can work with.

I was just talking to a guy running 850 cows in central Wisconsin who locked corn back in May when planting conditions looked sketchy. Smart move. He’s feeling pretty good about that decision while watching grain markets bounce around this summer.

But here’s what worries me… feed cost advantages can disappear faster than a fresh cow’s peak production drops off. Weather patterns, trade disruptions, energy costs—any of these could flip the equation pretty quickly.

What This Actually Means for Your Bottom Line

Looking ahead—and this is where three decades in this business starts showing—I don’t think this greater than 3% growth rate continues much longer. The StoneX analysis confirms what most agricultural economists are projecting: we’ll moderate toward 2% growth as we face tougher year-ago comparisons and seasonal heat stress hits those expanding Plains herds.

If you’re operating in traditional dairy regions, Focus on efficiency gains over cow numbers. This geographic shift is real, and trying to counter it by simply adding more animals might not be the most effective approach. The data shows Wisconsin barely growing while Kansas explodes—that should tell you something about where competitive advantages lie.

If you’re in one of those growth regions, Be strategic about it. Just because you can expand doesn’t mean you should do so without first locking in processing agreements. When forward-looking models show a 60-70% probability of regional capacity mismatches continuing through 2026, securing those relationships becomes critical.

Regardless of where you are, Start taking component premiums seriously if you haven’t already. Those butterfat and protein numbers aren’t just statistics on your milk check—they’re becoming the difference between profit and loss. When component-adjusted production is growing at 5% while base volume grows at 3.3%, that spread represents significant financial gains.

What’s interesting about the export picture is that U.S. cheese exports have been hitting strong levels recently while European production struggles with environmental constraints. When your competitors can’t produce, opportunities definitely emerge. But counting on exports to bail us out of domestic oversupply? That’s a risky way to build a business model.

It’s essential to remember that export markets can shift more rapidly than domestic production can adjust. Building a business model that depends entirely on international demand is like farming without crop insurance—it might work until it doesn’t.

The Bottom Line: Strategic Thinking Beats Volume Every Time

If you’re making production decisions for the next 18 months, here’s what I’m telling producers: forget about filling every stall or pushing every cow to maximum output. The operations I see thriving aren’t just focused on making more milk—they’re making smarter milk.

Key strategic moves that separate successful operations:

Prioritize components over volume (those 2% butterfat and 1.5% protein gains matter more than total pounds)

Secure solid processing relationships before expanding (capacity constraints are real)

Diversify revenue streams (beef-on-dairy programs have become essential, not optional)

Build financial flexibility to weather market volatility (18-24 month margin pressure cycles are becoming the norm)

What I’ve learned over the years is that producers who understand market signals, position themselves strategically, and build operations that can adapt when conditions change—and they always do—those are the ones that remain standing when the dust settles.

This June report confirms that we have the technical ability to produce milk like never before. The real question facing our industry is whether we’ve got the wisdom to produce it profitably in a market that’s sending us some pretty clear signals about supply, demand, and where we’re headed.

Honestly? I think that’s the conversation we should be having, rather than just celebrating production records. Because right now, with component-adjusted production up 5% and markets selling off anyway, the story being told is one we might not want to hear… but we’d better start listening.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Unlocking Component Gold: Are You Feeding for Fat and Protein, or Just Volume? – This tactical guide moves beyond why you need higher components to how you achieve them. It offers practical feeding and management strategies for immediately boosting butterfat and protein, directly impacting your milk check and profitability.

The Dairy Industry’s New Math: Are You Ready For The Change? – With the main article forecasting margin pressure and geographic shifts, this piece provides the strategic financial playbook you need. It details the key performance indicators (KPIs) that top herds use to build resilience and weather market volatility.

Beef on Dairy: A Trend That’s Here to Stay – The main article flags beef-on-dairy as essential. This piece breaks down the economics of this strategy, revealing how to leverage terminal genetics and market knowledge to transform your calf program from a cost center into a significant revenue stream.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

That July report just flipped the script—but here’s what most producers are missing about what comes next.

You know that feeling when you’re scrolling through your phone over morning coffee and suddenly stop mid-sip? That’s exactly what happened when the USDA’s July 2025 WASDE report hit my desk last week. After months of producers bracing for financial pain, milk prices got a significant boost that should have every dairy operation rethinking their entire strategy.

Here’s the thing, though—and I’ve been mulling this over since the numbers dropped—while everyone’s celebrating the all-milk price forecast jumping to $22.00 per hundredweight for 2025 (up from those dire earlier projections), most folks are missing the real story. Sure, 2026 forecasts at $21.65 per hundredweight look decent too, but what strikes me about this latest data is how perfectly it demonstrates the kind of market whiplash that’s become our new normal.

Just think about it… months ago, producers across Wisconsin and Iowa were making contingency plans for $19-20 milk. Now we’re looking at $22+ projections. For your typical 500-cow operation, that’s not just numbers on a spreadsheet—that’s the difference between scraping by and actually having room to breathe.

But here’s what’s got me both excited and concerned: the USDA raised milk production forecasts for both 2025 and 2026 based on higher cow inventories and increased milk per cow. According to recent analysis from the University of Wisconsin’s dairy markets program, this kind of supply response to improved pricing often sets us up for the next volatility cycle. The industry learns to respond to good news… sometimes a little too well.

What’s particularly fascinating—and this might surprise you—is that these price improvements actually reinforce why building what I call “financial fortresses” has become more critical than ever. The operations that will thrive aren’t just those riding the good news cycles; they’re the ones using this window to build systems that can handle whatever volatility comes next.

Because let’s be honest—if markets can swing from pessimistic to optimistic this fast, they can swing back just as quickly.

What’s Really Driving These Numbers

The thing about the July WASDE report is that it tells a story that’s both encouraging and complex, and frankly, most of the trade press is missing some crucial details that could impact your decision-making over the next 18 months.

The Milk Price Reality Check

The latest WASDE data shows some genuinely positive developments. That $22.00 per hundredweight forecast for 2025 represents a meaningful improvement, but here’s what’s particularly interesting—and this is where my conversations with dairy economists get really valuable—the breakdown across different classes tells us where the real strength is coming from.

Dr. Mark Stephenson from Wisconsin’s Program on Dairy Markets and Policy recently pointed out in his monthly outlook that the Class IV price increase is being driven by higher butter and nonfat dry milk prices, while Class III actually got lowered due to cheese price adjustments. For 2026, butter, NDM, and whey prices are all projected higher, suggesting strength in component markets that smart producers can leverage.

What’s really exciting—and I’ll admit, I get a bit nerdy about export data—is that commercial dairy exports are being raised for both 2025 and 2026 on both fat and skim-solids basis. According to the USDA’s Foreign Agricultural Service, this indicates stronger international demand that’s supporting domestic pricing. This export strength provides some foundation for optimism that goes beyond just domestic supply-demand dynamics.

But here’s where it gets interesting… and a little concerning. Recent research from Cornell’s dairy program suggests that rapid price improvements often coincide with production expansions that can create oversupply situations down the road. We’re seeing exactly that pattern in the current forecasts.

Feed Costs: The Other Half of the Equation

While everyone’s celebrating milk prices, the feed cost story is equally important—and honestly, it might be even better news for your bottom line. The July report shows corn production forecast at 15.705 billion bushels for 2025/26, down 115 million bushels from June projections due to lower planted and harvested area.

Now, you might think lower corn production means higher feed costs, but here’s the interesting part: the season-average farm price for corn is staying put at $4.20 per bushel. Feed and residual use was actually cut by 50 million bushels based on lower supplies, which suggests we’re looking at relatively stable input costs for the immediate future.

What’s got me particularly optimistic is how soybean meal prices were lowered $20 to $290 per short ton. For dairy operations—especially those in the Midwest, where transportation costs are lower—this combination of stable corn and cheaper soybean meal could improve feed cost margins by $0.30-0.50 per hundredweight when combined with the higher milk price forecasts.

I was talking with a nutritionist friend in Ohio last week (this is becoming more common in our industry), and she mentioned that operations implementing precision feeding systems are seeing even better results when input costs stabilize like this. The technology works best when you’re not constantly adjusting for wild price swings.

Market Volatility: The New Constant

Here’s what really gets me thinking… the rapid shift from pessimistic to optimistic forecasts demonstrates exactly why resilient planning systems have become essential. Markets that can swing from concern to optimism within a few months—well, they’re going to swing back eventually.

Current milk production forecasts are being raised based on higher cow inventories and increased milk productivity per cow. Industry experts I’ve spoken with suggest that this reflects improved margins, encouraging expansion, but it also means we could be setting ourselves up for oversupply situations if demand doesn’t keep pace.

According to recent work from UC Davis’s dairy economics group, this pattern of supply response to price improvements has historically led to market corrections within 18-24 months. Not trying to be a pessimist here, but the data suggests we should use this favorable window strategically.

Building Financial Resilience: What Smart Producers Are Doing Now

The improved price outlook creates opportunities, but the producers I know who’ve survived multiple market cycles aren’t just celebrating—they’re using this period to strengthen their operations for whatever comes next.

USDA Dairy Margin Coverage program performance showing the dramatic swing from record highs in late 2024 to projected compression in 2025

Government Programs: Strategic Leverage

The Dairy Margin Coverage program becomes even more valuable as a strategic tool when markets are improving. Brian Gould from Wisconsin’s dairy markets program recently noted that with current price forecasts showing stronger margins, this is actually the optimal time to evaluate whether your coverage levels are positioned for the new market reality.

Here’s what’s interesting about the Dairy Revenue Protection program—it offers quarterly revenue protection that becomes particularly valuable when you’re operating with higher baseline revenues. I’ve been talking with producers who are using this combination to provide both margin protection and revenue stability, which honestly has become essential regardless of whether markets are moving up or down.

What many producers don’t realize—and this came up in a conversation with a risk management consultant in Minnesota—is that strong market periods are actually the best time to implement protective strategies. When cash flows are better, operations have more flexibility to invest in systems that will protect them when markets inevitably turn challenging again.

Advanced Risk Management: Capitalizing on Opportunity

The improved price outlook creates opportunities for more sophisticated hedging strategies. With milk prices at $22.00 per hundredweight for 2025, operations can consider forward contracting strategies that lock in profitable margins while maintaining exposure to potential upside.

Options trading becomes particularly attractive in improving markets because it allows producers to maintain upside potential while protecting against downside risk. Recent analysis from the Chicago Mercantile Exchange shows that current price environments provide opportunities to implement protective strategies at relatively attractive premium costs.

What’s working in practice—and I’ve seen this across operations in different regions—is using the improved market outlook to implement blended strategies. Smart producers are contracting maybe 40% of production to guarantee profitable margins while leaving exposure to capture additional gains if markets continue strengthening.

Operational Excellence: The Foundation

You can’t hedge your way to long-term success without operational excellence, and improving markets provide the cash flow flexibility to invest in productivity improvements that create enduring value.

Feed Efficiency in the Current Environment

With corn prices stable at $4.20 per bushel and soybean meal costs declining to $290 per short ton, precision feeding systems can deliver enhanced returns. Research from Penn State’s dairy nutrition program shows that operations implementing advanced feed management systems can potentially save $0.75-1.25 per hundredweight in production costs while optimizing milk components.

I visited a 1,200-cow operation near Lancaster last month that’s been running precision feeding for about 18 months. “The ROI is real,” the manager told me, “but the consistency is what really matters. We’re hitting our butterfat targets every month now, not just when everything goes right.”

The combination of stable feed costs and improved milk prices creates favorable conditions for these investments. Operations that implement precision ration formulation during this period can build sustainable advantages that serve them well, regardless of future market conditions.

Component Optimization Strategy

Current market conditions show particular strength in butter and NDM prices, making component optimization especially valuable. Each 0.1% increase in butterfat content can add $0.15-0.20 per hundredweight to milk checks, and the current price environment may provide even better returns.

Here’s what’s working: I know a 350-cow operation in Vermont that worked systematically with their nutritionist to optimize components while maintaining overall production efficiency. They adjusted their TMR formulation, modified their breeding program to emphasize component traits, and invested in better feed storage. The result? Their average butterfat increased from 3.65% to 3.82% over 18 months, adding approximately $0.34 per hundredweight to their milk check.

Operations that focus on component optimization during favorable market periods often maintain those advantages even when overall market conditions become more challenging.

Climate Adaptation: Building for the Long Haul

Comparison of annual return on investment per cow for different climate adaptation and efficiency strategies

Improved market conditions provide the financial flexibility to invest in climate resilience, positioning operations for sustained success regardless of weather challenges. And frankly, with the summers we’ve been having…

Heat Stress Management: The Numbers Don’t Lie

Current price forecasts make cooling system investments even more attractive from an ROI perspective. With milk prices at $22.00 per hundredweight, the revenue maintained through effective heat stress management becomes more valuable.

Research from the University of Florida shows that properly designed cooling systems typically pay for themselves within 18-24 months through maintained milk production, but higher milk prices accelerate these payback periods. I know operations investing in these systems during favorable market periods that are seeing payback in 12-18 months while creating enduring operational advantages.

A 500-cow operation in Texas that I worked with last year invested $125,000 in a comprehensive cooling system. The manager told me, “We wish we’d done this five years ago. Summer milk production increased by 8%, breeding efficiency improved by 15%, and our vet costs dropped by 20%. The investment paid for itself in less than two years.”

Genetic Selection: The Long Game

The integration of heat tolerance into breeding programs becomes more attractive when cash flows support long-term investments. Holstein Association USA’s genomic evaluations for heat tolerance allow producers to select for climate resilience without sacrificing production traits.

What’s particularly interesting—and this comes from recent research at the University of Georgia—is how heat tolerance traits are being incorporated without sacrificing production or component quality. The SLICK gene, which creates a short, sleek hair coat that enhances heat dissipation, is being used in crossbreeding programs across the South with impressive results.

Current market conditions provide the financial stability to implement breeding programs focused on long-term sustainability rather than just immediate production gains. These investments pay dividends over multiple market cycles.

Technology Integration: Investing for the Future

Favorable market conditions create opportunities to implement technology solutions that provide persistent operational benefits. But here’s the thing—not all technology investments are created equal.

Precision Agriculture: What’s Actually Working

The current price environment makes precision agriculture investments more attractive from a cash flow perspective. Wearable sensors, automated monitoring systems, and precision feeding technologies require initial investments but deliver ongoing advantages.

According to recent surveys from Progressive Dairy, operations implementing precision agriculture during favorable market periods can develop systems that enhance efficiency and reduce costs, regardless of future market conditions. The key is selecting technologies that address specific operational challenges, rather than pursuing technology for its own sake.

I’ve been tracking adoption rates across different regions, and what’s fascinating is how the Midwest and Northeast are seeing faster uptake due to labor constraints, while Western operations are focusing more on resource efficiency technologies. Current milk price forecasts provide the financial flexibility to invest in integrated systems that combine multiple technologies for maximum operational benefit.

Data Analytics: Making Sense of Information

Improved cash flows enable investments in data analytics platforms that track production trends and identify opportunities for efficiency. The most successful systems integrate seamlessly with existing management practices, providing valuable insights that support informed decision-making.

An 800-cow operation in Michigan that I know implemented a comprehensive herd management system integrating feed management, reproduction, and financial tracking. “The system helped us identify patterns we never would have seen otherwise,” the manager explained. “We discovered that our reproduction efficiency was directly correlated with feed delivery timing—something we’d never connected before.”

Regional Strategies: Adapting to Local Realities

The improved national price outlook affects different regions differently, and understanding these regional variations is crucial for effective strategy development. Because let’s face it—dairy farming in Wisconsin is different from dairy farming in California.

Midwest Opportunities

Midwest operations benefit from both improved milk prices and relatively stable feed costs. The combination of $22.00 per hundredweight milk prices and $4.20 per bushel corn creates favorable margins for efficiency improvements and technology investments.

Regional feed cost advantages in the Midwest become more pronounced when national milk prices improve. I recently spoke with an operator in Iowa who is leveraging these advantages to invest in productivity improvements that capitalize on their natural cost benefits. Corn costs typically run $0.25-0.50 per bushel below national averages, while soybean meal costs are often $15-25 per ton lower.

The weather volatility is real, though. Spring flooding and summer droughts are becoming more frequent, making feed storage and climate adaptation investments increasingly important. Operations that have invested in climate-controlled storage and comprehensive drainage systems are maintaining more consistent performance.

Western Adaptation

Western operations face unique challenges, including water costs and extreme climate conditions, but improved milk prices provide better margins to invest in solutions. The higher price environment makes water-efficient technologies and advanced cooling systems more economically attractive.

Scale advantages in Western operations become more pronounced during favorable market periods. Operations with 1,000+ cows can justify technology investments that smaller operations can’t, including robotic milking systems, precision feeding, and comprehensive environmental monitoring.

Water costs and availability create unique constraints, though. In California, water costs can add $0.15-$ 0.25 per hundredweight to production costs, making water-efficient technologies and management practices essential.

Northeast Premium Markets

Northeast operations benefit from both improved national pricing and continued opportunities for premium pricing through direct marketing channels. The combination creates opportunities for value-added processing and direct sales that capture additional margins beyond commodity pricing.

Direct marketing opportunities are particularly strong in the Northeast. Operations with access to metropolitan markets can often capture premiums of $3 to $ 5 per hundredweight through direct sales to processors serving premium retail channels.

The key is balancing these opportunities with risk management. Higher costs mean less margin for error, making programs like DMC and DRP particularly valuable for smaller operations that can’t absorb major market swings.

Implementation: Making It Work in Practice

Improved market conditions create opportunities, but successful implementation requires systematic approaches that build on favorable conditions rather than simply hoping they continue. Here’s what I’m seeing work across different types of operations…

Quick Wins in a Stronger Market

DMC and DRP Optimization: This is something you can tackle this month. Review and optimize coverage levels based on current price forecasts and margin projections. Higher baseline prices may justify different coverage strategies than were appropriate during lower price periods.

The key is analyzing your actual feed costs and production levels to determine optimal coverage. Operations with lower feed costs (typically Midwest) often benefit from higher coverage levels, while operations with higher feed costs might optimize at lower coverage levels with supplemental private insurance.

Component Premium Analysis: Evaluate component premiums across multiple buyers to capture the full benefit of current market strength in butter and NDM pricing. Market improvements often create premium opportunities that weren’t available during weaker periods.

I know this sounds basic, but premium differences of $0.30-0.50 per hundredweight for the same milk in the same region are more common than you might think. It’s worth a few phone calls to make sure you’re getting paid fairly for what you’re producing.

Feed Efficiency Quick Wins: With stable corn prices and lower soybean meal costs, implement feeding improvements that deliver immediate returns while establishing long-term efficiency gains. Working with your nutritionist to evaluate current feeding practices often identifies immediate opportunities.

Simple changes like improving TMR mixing consistency, adjusting feeding schedules, or optimizing bunk management can deliver returns of $0.25-0.50 per hundredweight within 30-60 days.

Medium-Term Strategic Investments

Technology Integration: Use improved cash flows to implement precision agriculture and automation systems that provide enduring operational benefits. Current market conditions make these investments more attractive from both cash flow and ROI perspectives.

The most successful implementations I’ve seen start with specific problems—such as improving reproduction efficiency, reducing feed waste, or optimizing component levels—and then select technologies that address those problems. Operations that try to implement everything at once typically struggle with integration and training challenges.

Current implementation costs vary significantly by technology and operation size. Precision feeding systems typically run $15-25 per cow for smaller operations (under 500 cows) and $8-12 per cow for larger operations. Wearable monitoring systems cost $40-60 per cow initially, with ongoing costs of $8-12 per cow annually.

Infrastructure Development: Invest in climate adaptation systems, feed storage improvements, and facility upgrades that address multiple operational challenges while market conditions support capital investments.

The key is prioritizing investments that address multiple challenges simultaneously. A climate-controlled feed storage facility addresses feed quality, waste reduction, and weather resilience. Comprehensive cooling systems enhance animal comfort, improve milk quality, and increase reproduction efficiency.

Market Diversification: Explore direct marketing opportunities and value-added processing options that can provide revenue stability and premium pricing beyond commodity markets.

The key is to start small and build based on market response and operational capacity. Many successful diversification efforts begin with 10-15% of production and expand based on demonstrated success.

Long-Term Competitive Positioning

Genetic Improvement Programs: Implement breeding strategies focused on climate tolerance, feed efficiency, and component quality that deliver advantages across multiple market cycles.

The most successful programs integrate heat tolerance with production traits and component quality. Current genetic evaluation tools make it possible to select for multiple traits simultaneously without sacrificing overall performance.

Research from various land-grant universities suggests that operations selecting for heat tolerance genetics are seeing 10-15% better summer performance compared to conventional genetics, with some programs reporting even better results during extreme heat events.

Operational Scaling: Evaluate expansion opportunities or efficiency improvements that leverage improved market conditions while establishing long-term competitive positioning.

Whether expanding or optimizing existing facilities, scaling decisions require a comprehensive analysis of market conditions, financing, and management capacity. The most successful expansions I’ve seen are those that maintain focus on operational excellence while growing.

Where the Industry Goes from Here

The improved milk price forecasts in the July WASDE report provide welcome relief for dairy producers, but they also reinforce the importance of building operations that can thrive regardless of market conditions. And honestly, that’s what separates the survivors from the thrivers in this business.

Success Patterns in Volatile Markets

The most successful operations treat improved market conditions as opportunities to invest in systems that provide advantages during both good times and challenging periods. They’re not just celebrating better prices—they’re using the improved cash flows to create sustainable operational benefits.

What’s particularly interesting is how these operations approach market improvement. They recognize that favorable conditions are temporary and use them strategically to strengthen their foundations for whatever comes next. According to research from several dairy economics programs, operations that invest during favorable periods consistently outperform those that simply ride the cycles.

I’ve been tracking patterns across different regions and operation sizes, and the farms that consistently perform well share several characteristics: they treat risk management as a core business function, invest in people and systems that can adapt to changing conditions, maintain focus on operational excellence while implementing new strategies, and build relationships with service providers who understand their specific challenges.

Building Sustainable Advantages

The dairy operations that will thrive over the long term are those that use favorable market periods to invest in operational excellence, technology adoption, and protective systems that provide advantages regardless of market conditions.

Current price improvements create opportunities, but smart producers are using this period to build resilient operations that can handle whatever volatility the future brings. Because if there’s one thing we know for certain about dairy markets, it’s that they’ll keep changing.

Your Strategic Decision Point

The question isn’t whether to celebrate the improved milk price forecasts—it’s whether you’ll use this opportunity to create enduring operational advantages or simply hope that favorable conditions continue. And frankly, hope isn’t much of a business strategy.

The July WASDE report shows all-milk prices at $22.00 per hundredweight for 2025, providing improved margins that create strategic opportunities. But markets that can swing from pessimistic to optimistic forecasts within months will inevitably swing back, and the operations that prepare for that reality will be the ones that thrive long-term.

Here’s what I keep coming back to in conversations with producers across the country: the tools, strategies, and support systems exist today to build resilient, profitable operations that can prosper in any market environment. The question is whether you’ll implement these strategies while market conditions provide the cash flow flexibility to do so effectively.

Current market improvements provide a window of opportunity to build operational resilience, but that window won’t stay open indefinitely. The operations that recognize this reality and act strategically now will be positioned to thrive regardless of what market conditions emerge next.

Are you building operational resilience with the improved resources these market conditions provide, or are you simply hoping that good times continue? The choice is yours, but the opportunity to create sustainable advantages may not present itself again soon.

Because at the end of the day, the producers who build financial fortresses during good times are the ones who sleep well during bad times. And in this business, that peace of mind is worth more than any short-term price improvement.

Strategic Action Guide for Current Market Conditions

Immediate Opportunities (Next 30 Days): Start by optimizing your DMC and DRP coverage based on that $22.00 per hundredweight baseline pricing. Take a hard look at component premium capture with current butter and NDM strength—you might be surprised what you find. Implement feed efficiency improvements while corn costs are stable, and honestly assess technology investment opportunities now that cash flow has improved.

Strategic Investments (Next 3-6 Months): This is the time to develop those integrated protection systems we’ve been talking about. Build climate adaptation infrastructure that’ll serve you for decades. Integrate precision agriculture technology that addresses your specific challenges, not just the latest gadgets. Evaluate market diversification opportunities that make sense for your operation and region.

Long-Term Competitive Positioning (6-24 Months): Establish genetic selection programs for climate resilience and efficiency—this is a marathon, not a sprint. Complete operational scaling or efficiency optimization projects while financing is favorable. Implement advanced automation and data analytics that’ll give you an edge for years to come. Develop sustainable operational advantages that’ll serve you through multiple market cycles.

Key Performance Metrics: Monitor margin stability across market cycles, track operational efficiency improvements, measure component optimization progress, and evaluate technology ROI achievement. But remember—the best metrics are the ones that help you make better decisions, not just track what happened.

KEY TAKEAWAYS

Lock in profitable margins while you can: With DMC and DRP programs, you can optimize coverage levels based on $22/cwt baseline pricing—higher baseline prices justify different strategies than what worked during $19-20 milk, potentially saving thousands in premium costs while improving protection

Feed efficiency pays double right now: Precision ration formulation delivers $0.75-1.25/cwt savings when corn’s stable at $4.20/bushel and soybean meal dropped $20 to $290/ton—implement these systems during favorable cash flow periods for 18-24 month paybacks that compound over time

Component optimization hits different in this market: Butter and NDM strength means each 0.1% butterfat increase adds $0.15-0.20/cwt to milk checks—work with your nutritionist now to capture these premiums while markets support the investment in better genetics and feeding programs

Climate adaptation ROI accelerates with higher milk prices: Cooling systems that normally pay for themselves in 18-24 months are hitting 12-18 month paybacks when milk revenue per cow increases—invest in heat stress management while cash flows support the capital expenditure

Regional advantages compound during price improvements: Midwest operations with $0.25-0.50/bushel corn advantages and Northeast farms capturing $3-5/cwt direct marketing premiums should leverage these natural benefits to implement technology and infrastructure that smaller margins couldn’t justify

EXECUTIVE SUMMARY

Look, I get it—seeing $22.00 per hundredweight for 2025 milk prices feels pretty good after the doom and gloom we’ve been hearing. But here’s the thing most producers are missing: the smart money isn’t celebrating these WASDE numbers, they’re using this window to build operations that can handle whatever volatility comes next. We’re talking about precision feeding systems that can save you $0.75-1.25 per hundredweight while corn sits stable at $4.20 per bushel, and component optimization strategies that add $0.15-0.20 per hundredweight for every 0.1% butterfat increase. The global dairy markets are showing us that what goes up comes down fast—just look at how we swung from pessimistic to optimistic forecasts in months. European producers learned this lesson the hard way after milk quotas ended, and the ones who survived built fortress operations during good times, not bad ones. You’ve got maybe 18 months of favorable conditions to implement the risk management systems, climate adaptation, and operational improvements that’ll keep you profitable when markets inevitably swing back—don’t waste it hoping good times continue.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Processors’ allocation blindness costs dairy farmers 40% butter premiums while missing exploding APAC demand—110-year inventory records prove it

EXECUTIVE SUMMARY: Dairy processors have systematically failed at basic milk allocation decisions, costing producers 40% potential butter premiums while chasing low-margin cheese volumes. New USDA data exposes butter inventories at their lowest April level since 1915—just 337,352 thousand pounds—while cheese stocks remain relatively comfortable at 1.4 billion pounds, down only 2% year-over-year. This isn’t market volatility; it’s strategic incompetence that’s left money on the table while global butter demand explodes across Asian markets. With U.S. milk production declining 1.1% and the dairy herd contracting 0.8%, every allocation decision now carries amplified consequences that processors continue to botch. European competitors are already capturing premium Far East markets with specialized butter formats while American processors remain stuck in 1990s thinking. The math is brutal: butter’s record scarcity has created premium pricing opportunities that could reshape dairy profitability overnight, but only for producers smart enough to exploit processor failures. Stop following the herd toward mediocrity—these allocation disasters represent the biggest profit opportunity in modern dairy history.

KEY TAKEAWAYS

Capture 40% butter premiums immediately: With inventories at 110-year lows and processors still prioritizing cheese volume over butter value, producers can renegotiate milk pricing contracts to exploit this artificial scarcity and secure premium differentials that could boost annual revenue by $15,000-25,000 per 100-cow operation.

Exploit global market misalignment: While U.S. processors fumble domestic allocation, exploding Asian demand for premium butter formats (sheets, dishes, sticks) offers direct-market opportunities worth 25-30% price premiums over traditional commodity pricing—European exporters are already capitalizing on Singapore, Malaysia, and China markets.

Leverage production flexibility advantage: With milk production declining 1.1% year-over-year, producers with the ability to adjust component profiles toward butter-optimized milk (higher butterfat percentages through strategic breeding and nutrition) can command premium pricing from desperate processors seeking to rebuild depleted inventories.

Position for inevitable market correction: Historic butter shortages alongside stable cheese supplies prove systematic processor misallocation—smart producers building butter-focused relationships now will benefit when the industry inevitably corrects these strategic failures, potentially capturing 15-20% sustained margin improvements.

Implement risk management strategies: Record-low buffer stocks mean any production hiccup triggers disproportionate price movements—producers should secure import sourcing relationships and develop contingency pricing mechanisms to protect against volatile input costs while maximizing upside capture during supply disruptions.

April 2025 inventory data reveals butter stocks at a 110-year low while cheese remains stable, exposing fundamental processing misallocation that smart producers can exploit for maximum profitability

Every dairy producer must face the uncomfortable truth: U.S. butter inventories just crashed to their lowest April level since 1915, while cheese stocks remain relatively comfortable. This isn’t market volatility—it’s a systematic failure by dairy processors who’ve played the wrong game for years.

The numbers paint a devastating picture. Butter stocks plummeted to just 337,352 thousand pounds as of April 30, 2025—a crushing 7% drop from last year’s 362,089 thousand pounds. Meanwhile, cheese inventories managed only a modest 2% decline to 1.4 billion pounds.

This divergence exposes what should terrify every producer: processors have been systematically undervaluing butter production while chasing volume over value in cheese.

The Reality Check: An Industry in Denial

Let’s cut through the processing sector’s collective delusion. When butter hits record lows while cheese stays stable, it reveals a strategic blind spot that’s costing producers millions in lost premiums.