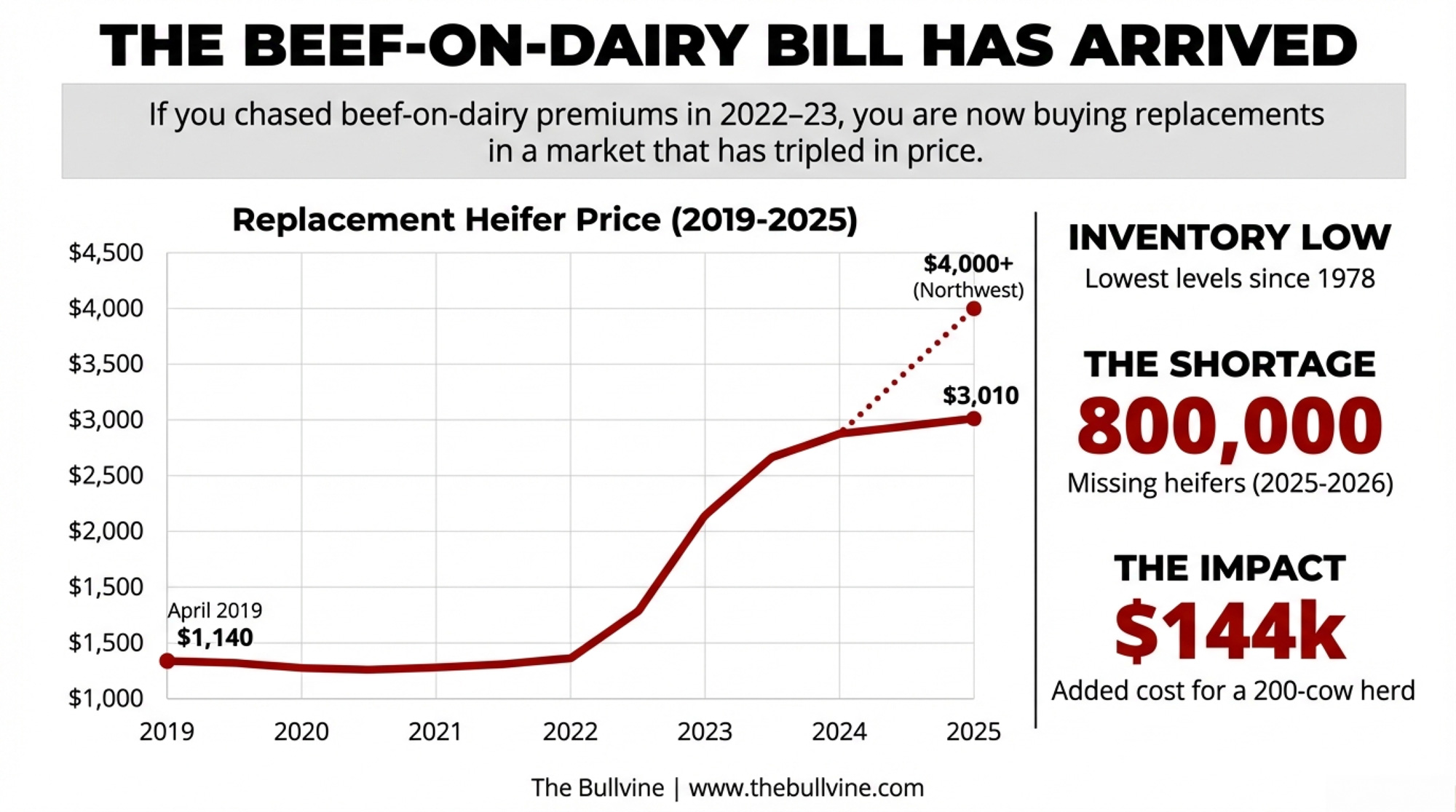

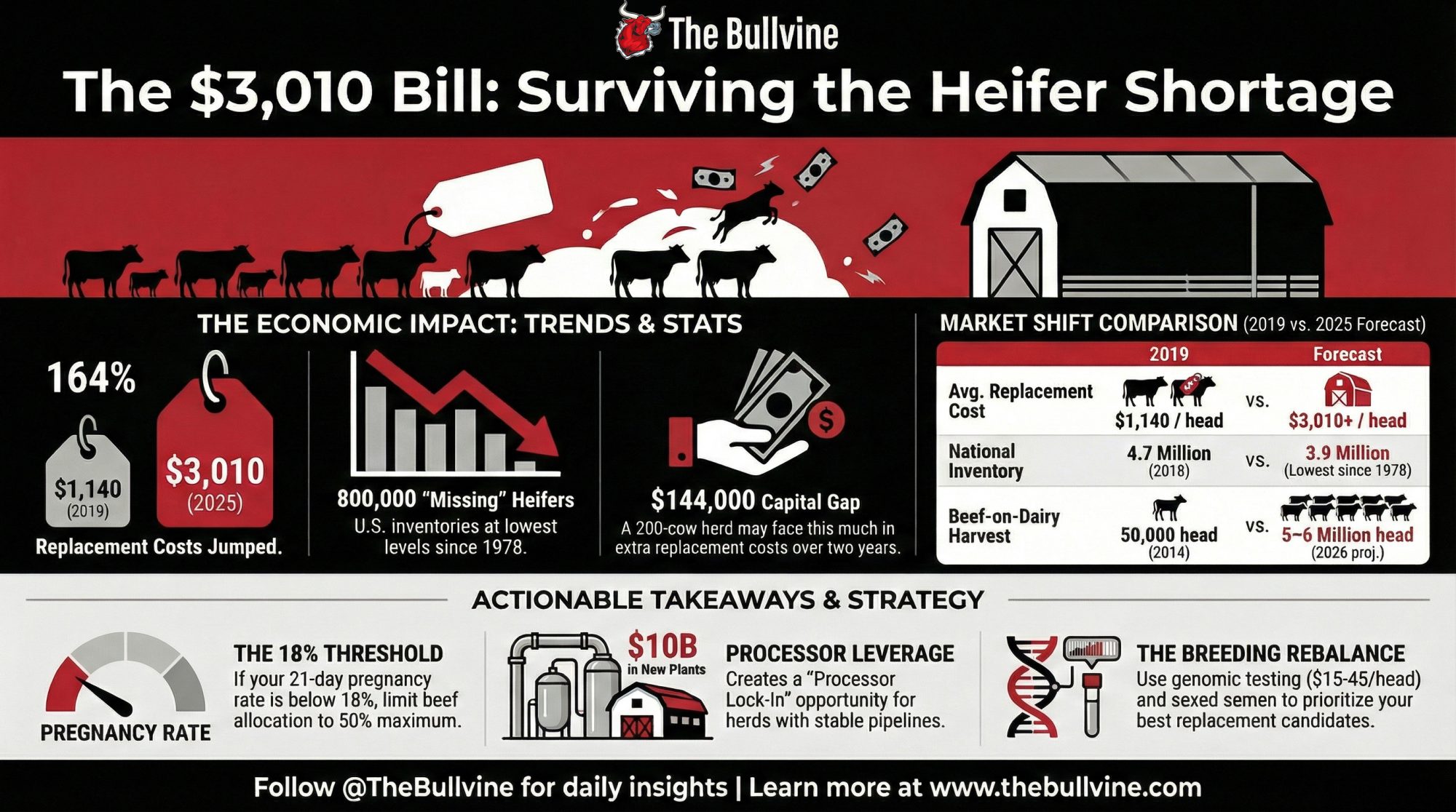

3 out of 4 dairies bred beef-on-dairy. Now 800,000 heifers are missing, and replacements are $3,010 a head. Where does your herd sit in that math?

Executive Summary: If you chased beef‑on‑dairy premiums in 2022–23, you’re now buying replacements in a world where heifer prices jumped from $1,140 in 2019 to $3,010 in mid‑2025 and often top $4,000 in high‑demand regions. At the same time, U.S. replacement inventories have dropped to their lowest level since 1978, leaving roughly 800,000 “missing” heifers across 2025–2026 and making it harder—and more expensive—to keep herds at size. For a 200‑cow herd turning over 35–38% per year, that shift alone can mean an extra $126,000–$144,000 in replacement capital over the next two years if you have to buy those animals instead of calving them in. This piece breaks your options into four concrete paths—breeding rebalance, reduced culling, strategic exit, and processor lock‑in—and spells out where each helps, where it backfires, and the thresholds (like an 18% pregnancy rate or culling below 30%) that should force a rethink. It also links your barn‑level math to the bigger picture: beef‑on‑dairy calves now account for 12–15% of fed beef harvests, and roughly $10 billion in new dairy plants are scheduled to come online by 2027, keeping processor demand for reliable milk flows high even as replacements stay tight. The goal is simple: give you enough numbers and clear decision rules to decide whether your 2026 breeding sheet keeps you in the group processors treat as long‑term partners—or in the group scrambling for $3,000+ heifers with everyone else.

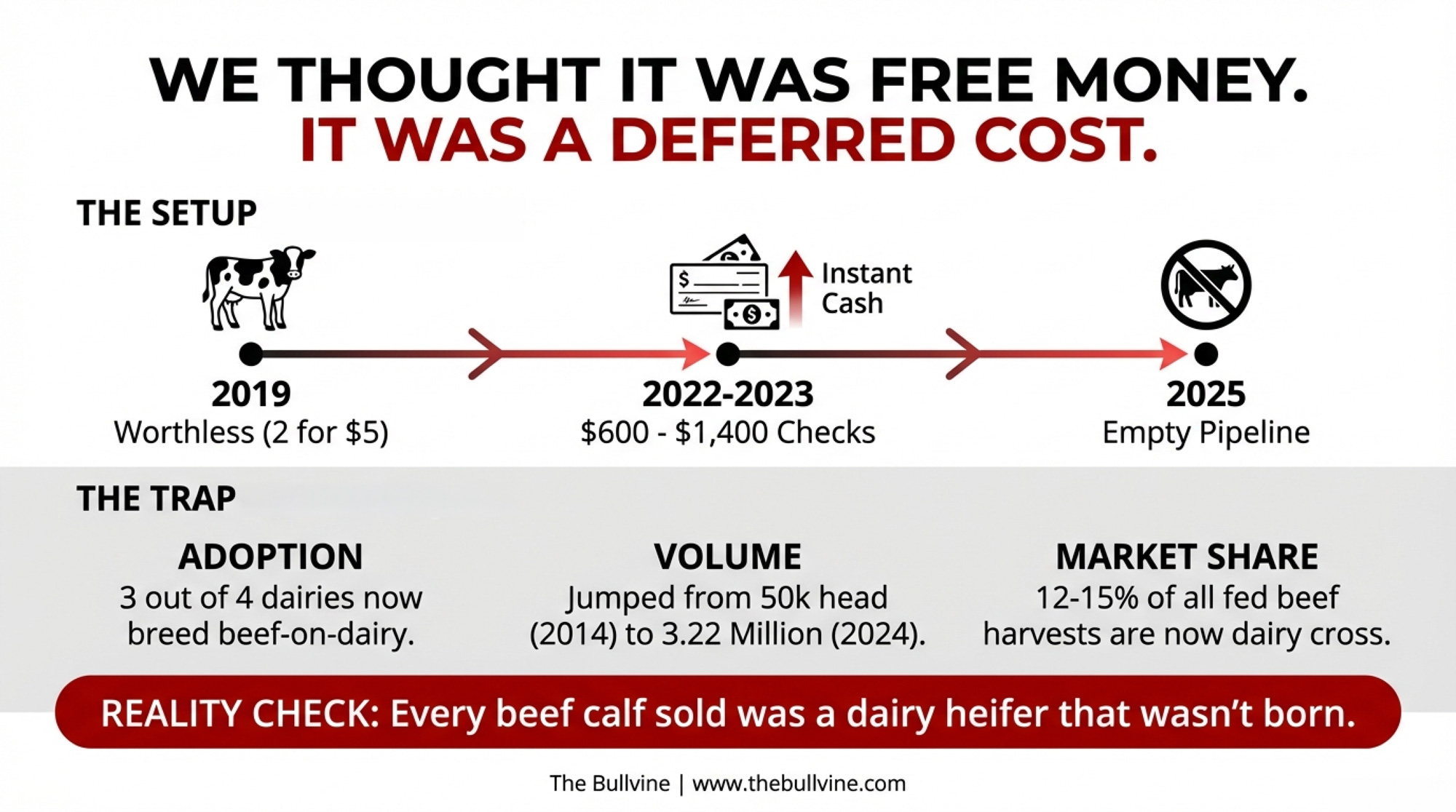

Ken McCarty of McCarty Family Farms still remembers trying to sell Holstein bull calves: “Two for $5″—with no takers. That painful baseline explains why dairy producers didn’t hesitate when beef-on-dairy calves started bringing $600, then $1,000, then $1,400 per head. The math seemed obvious. The check was immediate.

But it wasn’t free money. It was a deferred bill. And that bill has arrived.

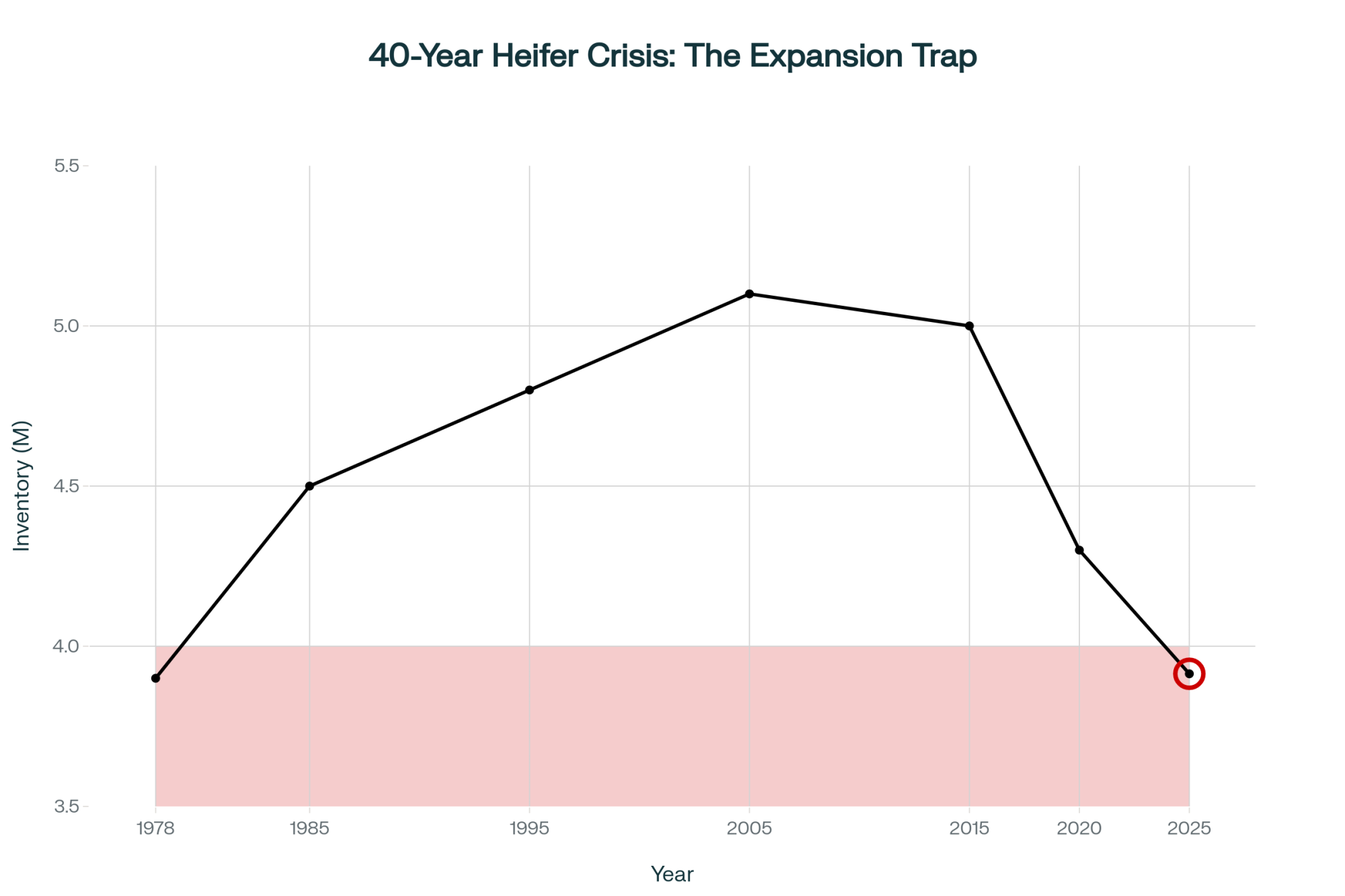

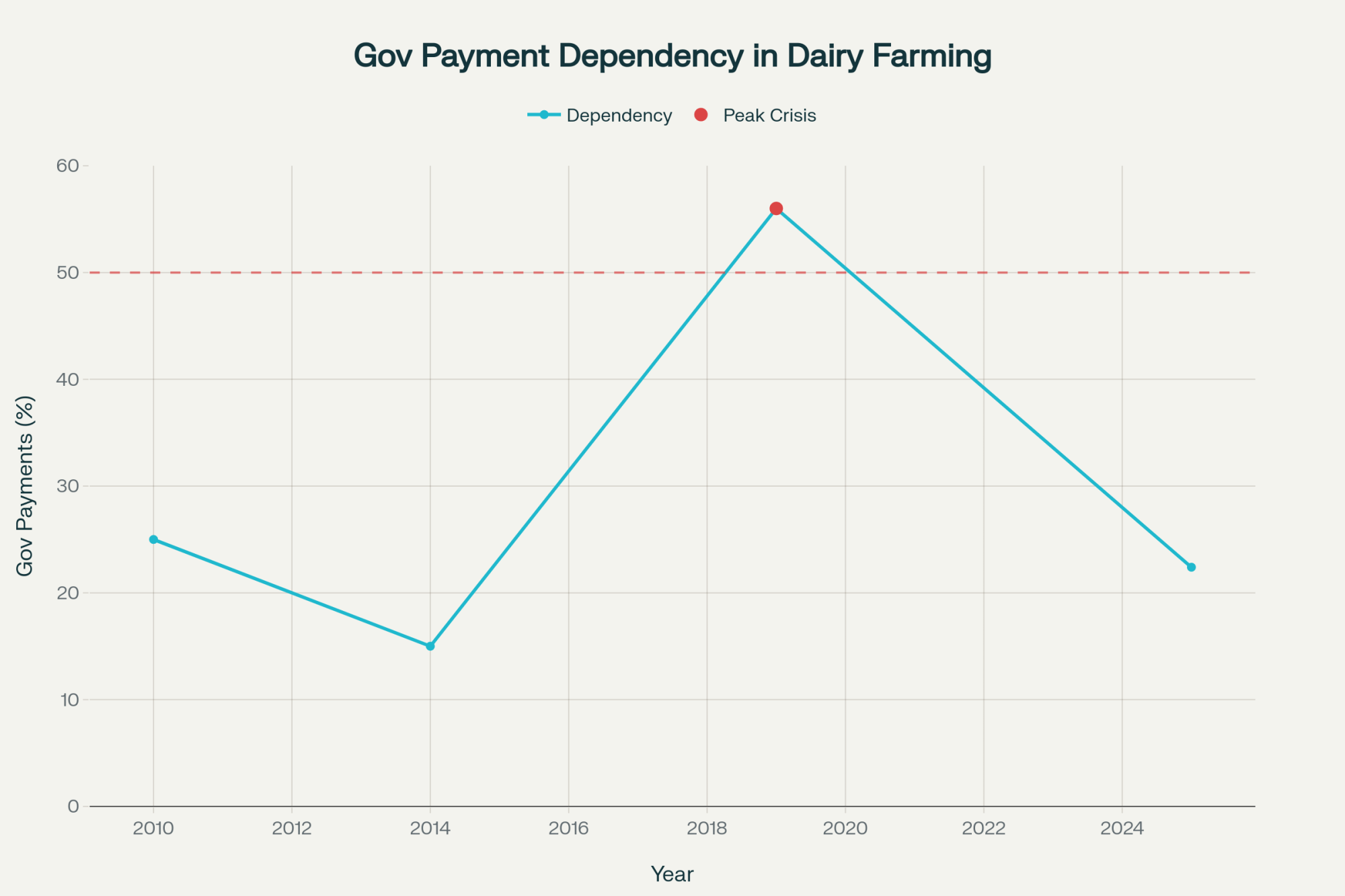

CoBank data shows replacement heifer prices climbed from $1,140 per head in April 2019 to $3,010 by July 2025—with top-quality animals in California and Minnesota auction barns commanding $4,000 or more. USDA’s January 30, 2026, cattle inventory report confirmed the national herd continues to contract. For operations that bred heavily to beef in 2022 and 2023, the pipeline is now empty. For those who maintained balance, a window is opening.

The Scale Nobody Predicted

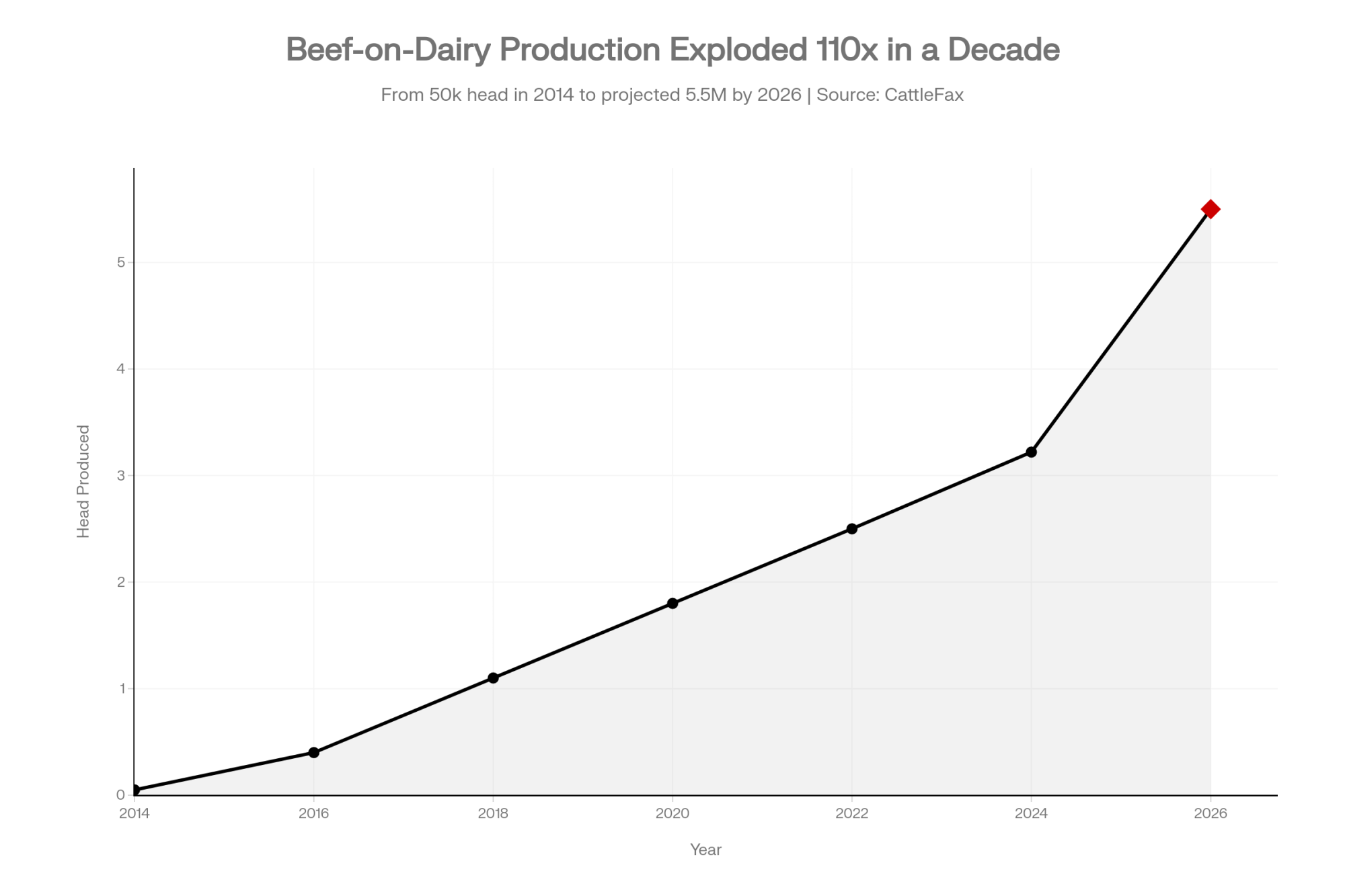

The adoption curve was staggering. Beef semen sales into dairy herds grew from 1.2 million units in 2010 to 9.4 million units by 2023—roughly 84% of which went into dairy cows, according to a 2024 Purina survey. That same survey found almost three-fourths of U.S. dairy farmers are now actively crossbreeding using beef genetics, with another 16% considering it.

CattleFax puts the production numbers in starker terms: beef-on-dairy calf production jumped from 50,000 head in 2014 to 3.22 million in 2024, with projections reaching 5–6 million head by 2026. These crossbred cattle now account for 12–15% of fed beef harvests.

Every one of those calves was a dairy heifer that wasn’t born.

The Pipeline Math That’s Already Locked In

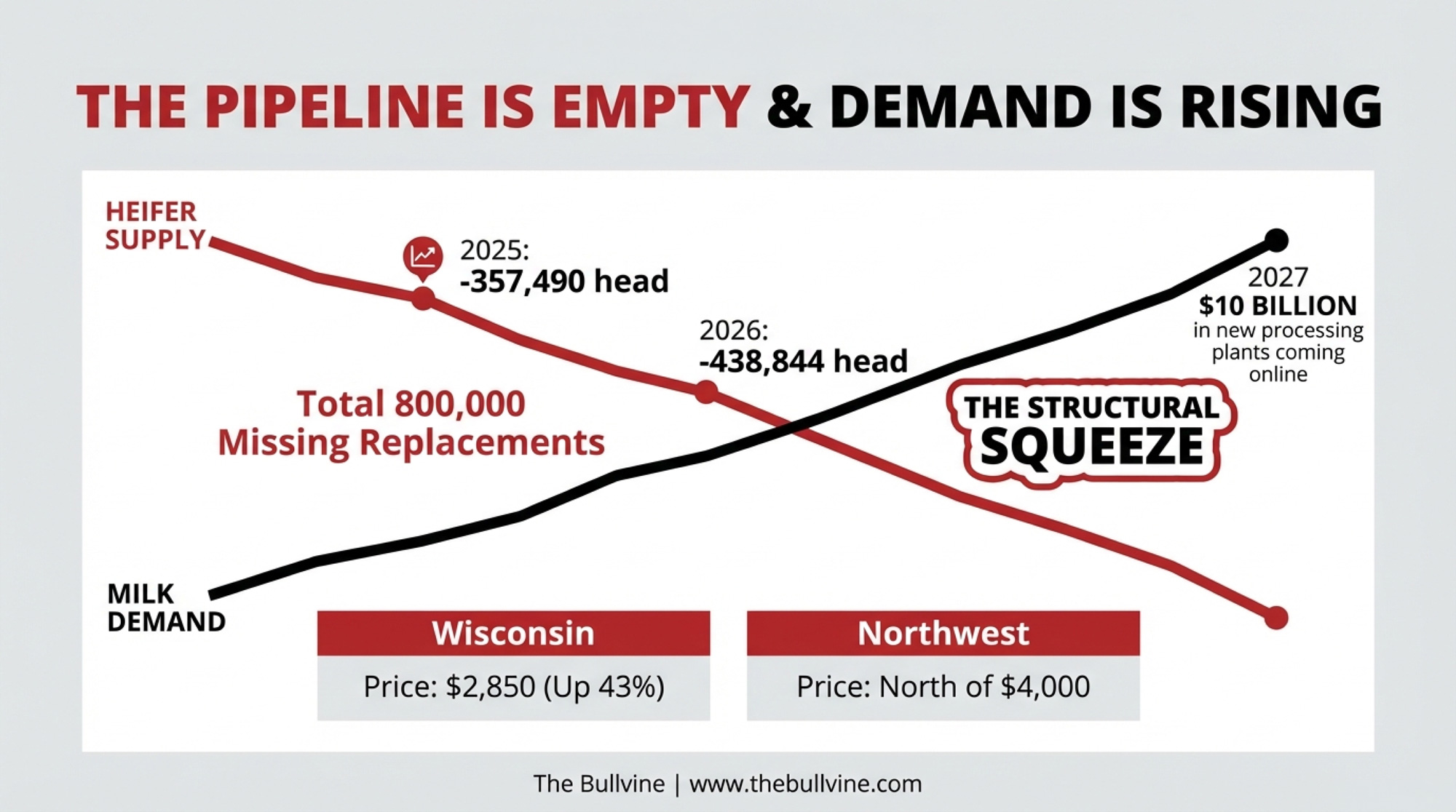

Sarina Sharp at the Daily Dairy Report flagged in early 2024 that dairy heifer inventories had declined for six consecutive years. USDA’s January 2025 snapshot put milk replacement heifers at 3.914 million head—the lowest since 1978, a full 18% below 2018 levels.

CoBank economist Corey Geiger quantified the gap in an August 2025 report: 357,490 fewer dairy heifers available in 2025, then 438,844 fewer in 2026. Add those up. That’s roughly 800,000 missing replacements across a two-year window. And as Geiger commented: “We don’t see a rebound until 2027, and that will be up 285-thousand, but you’ve got to remember, that’s going to be after 800-thousand fewer heifers”.

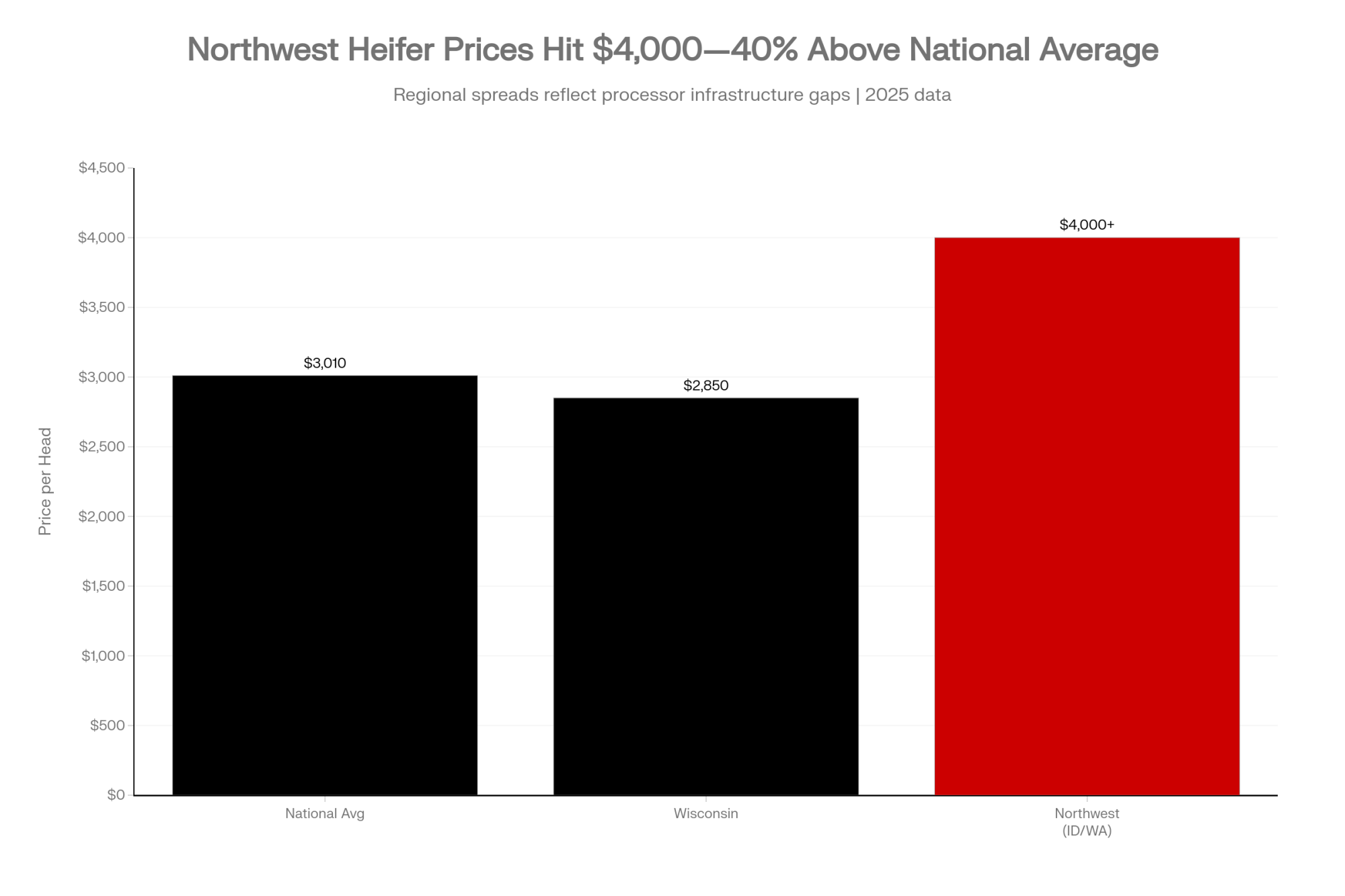

Regional variation tells its own story. Wisconsin replacement values jumped 43% year-over-year between October 2023 ($1,990) and October 2024 ($2,850), according to USDA data. Yet Wisconsin actually gained 10,000 heifers while Texas lost 10,000 head. “Watch” on the Northwest (Idaho/Washington), where prices have reportedly hit that $4,000+ “north of the border” threshold. That divergence comes down to processor relationships and infrastructure, not just breeding decisions.

The Beef-on-Dairy Miscalculation

Here’s what producers believed: beef-on-dairy premiums were an additive income. Extra revenue layered on top of normal operations without meaningful trade-offs.

Here’s what actually happened.

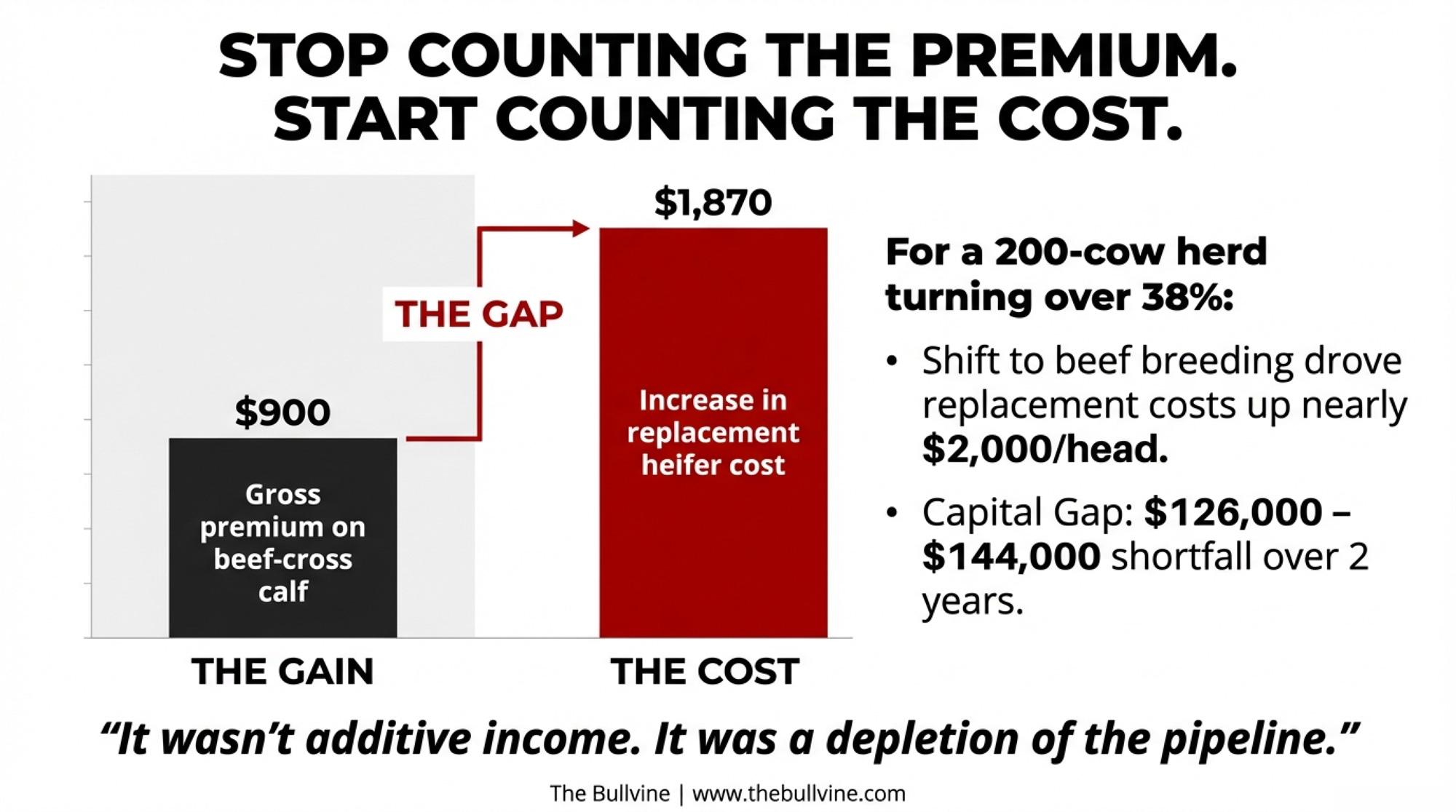

When beef-on-dairy calves climbed toward the $1,400 average that Purina’s Laurence Williams cited by 2024-2025, producers weren’t making a one-time decision. They were depleting a pipeline that takes three-plus years to rebuild. Every beef breeding looked like a $900 gain. What nobody penciled in was the replacement heifer that wouldn’t exist three years later—an animal that now costs $1,870 more than it did in 2019.

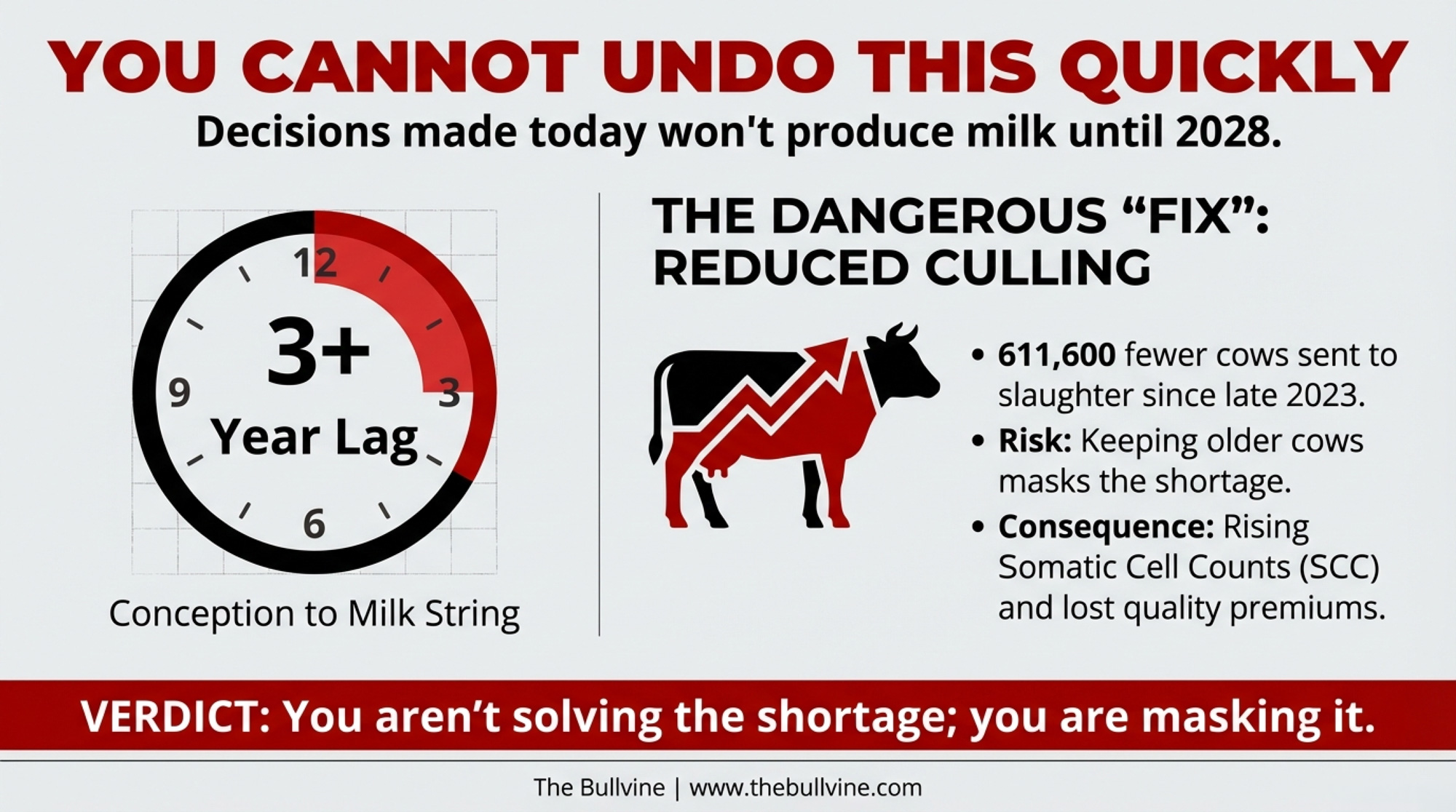

CoBank’s analysis is blunt: from conception to a cow in the milk string is a “three-plus year proposition”. You can’t undo aggressive beef breeding quickly.

And the 2024 NAAB semen sales data reveals how producers tried to have it both ways. Gender-sorted dairy semen surged 17.9%—an additional 1.5 million units. But beef semen held steady at 7.9 million units. No retreat.

How This Lands on Real Operations

When Mike North of Ever.Ag started seeing two-to-three-day-old beef-cross calves bringing $1,000, his framing captured the logic perfectly: “Why feed an animal for 18 months when the money’s sitting there at day three?”

But North also flagged the inflection point when the math flipped: “Some animals moving in the northwest last week were north of $4,000 an animal. That’s a pretty tall price, and so now, guess what? We’re seeing people starting to switch some of their breeding back to that replacement animal”.

One Minnesota producer’s current allocation illustrates the hedging strategy most operations have adopted: 10% of cows bred to sexed semen, while the rest go to beef; for heifers, 50% bred to sexed semen, while the other half go to beef. That’s not a correction—it’s a bet that partial measures will thread the needle.

Meanwhile, culling rates have collapsed. Dairy farmers have sent 611,600 fewer cows to slaughter since Labor Day 2023, according to CoBank’s analysis of USDA data. That keeps milk flowing but ages the herd.

Running the Numbers: Gross Premium vs. Net Replacement Cost

Here’s the full picture for a typical 200-cow Holstein operation in the Upper Midwest:

The spread:

Beef-cross premium over Holstein bull: ~$750-$1,200/head (2024-2025 market)

Incremental heifer cost increase (2019 vs 2025): ~$1,870/head at national averages

The math: If your replacement ratio means 1.5-2 beef breedings per “lost” heifer, and premiums average $900, you’ve captured $1,350-$1,800 in gross premium. But across the industry, the collective shift toward beef breeding drove replacement heifer costs up $1,870 per head. For a 200-cow operation needing 70-80 replacements annually (35-38% turnover), that gap represents $126,000-$144,000 in additional replacement capital over 24 months—if you can find animals to buy at all.

Metric

Value

Notes

Herd Size

200 cows

Typical Upper Midwest operation

Annual Replacement Rate

35-38%

70-76 replacements needed yearly

Beef-Cross Premium (2024-25)

$750-$1,200/head

Average $900 across regions

Gross Premium Captured

$1,575/replacement

Assumes 1.75 breedings per heifer @ $900

Heifer Cost Increase (2019-2025)

+$1,870/head

From $1,140 to $3,010 national average

Net Gap per Replacement

-$295/head

Premium didn’t cover cost inflation

Total Additional Capital (24 months)

$126,000-$144,000

For 140-152 replacements over 2 years

Critical Time Horizon

2026-2027

When depleted 2022-23 pipeline hits

And here’s the kicker: The $10 billion in new dairy plants are set to come online through 2027, meaning processor demand for milk will keep climbing even as replacement supply stays pinched.

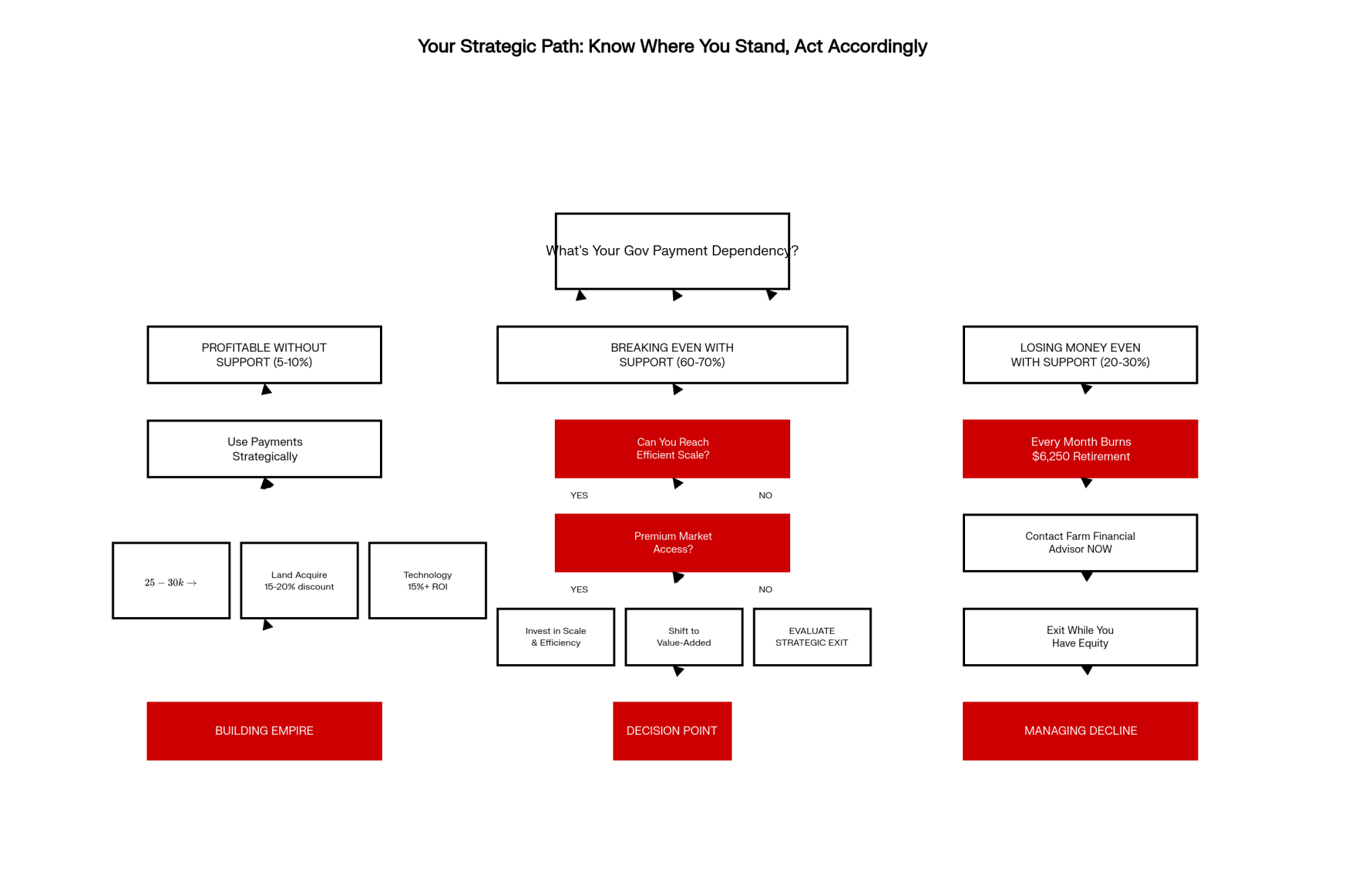

Four Paths Forward—And Where Each Can Backfire

Chris Wolf’s Michigan State analysis of 14,824 farm records found that performance variation among small farms is 38% farm-related compared to only 15% for large farms. Your response to this crisis matters more at 200 cows than at 2,000.

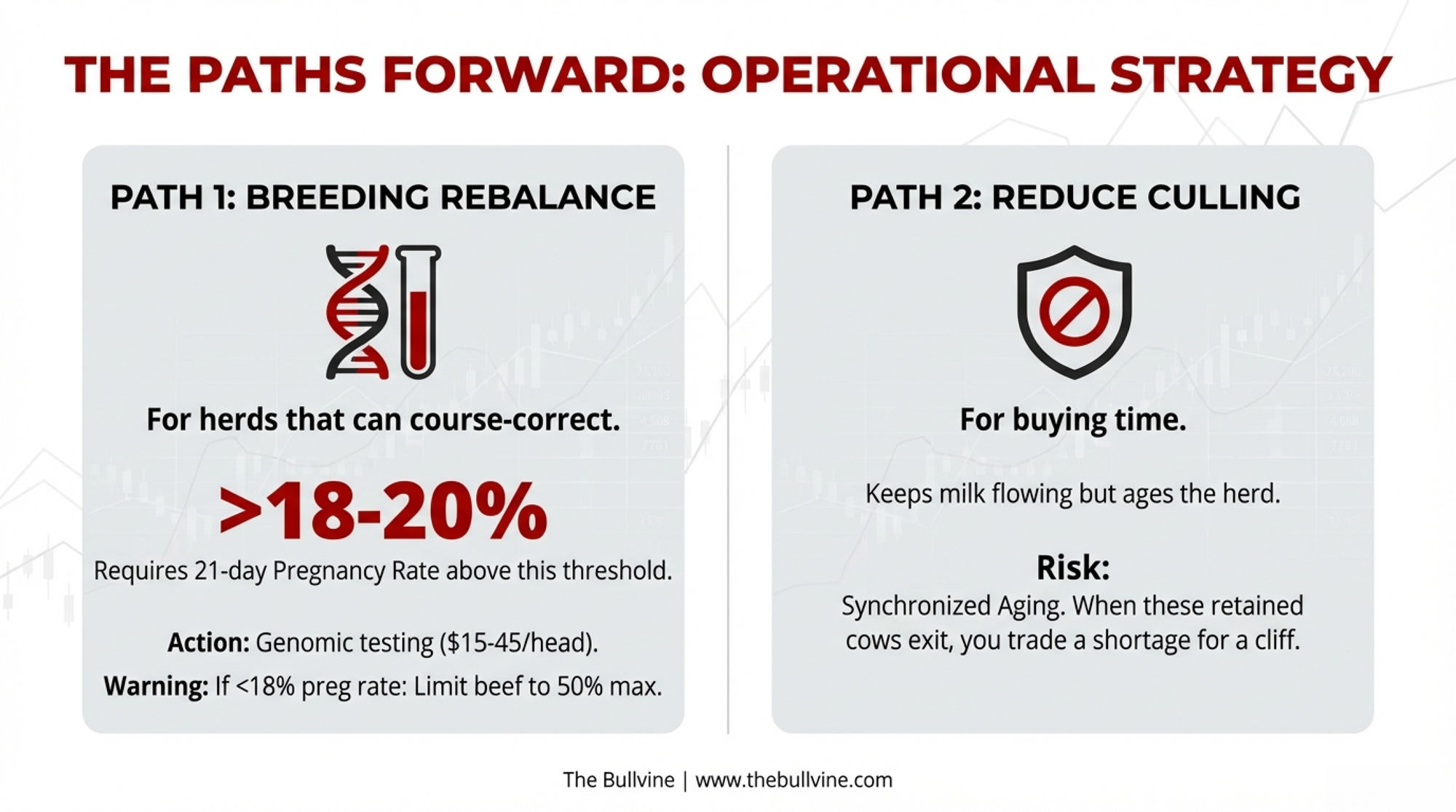

Path 1: Breeding Rebalance

Path 2: Reduce Culling

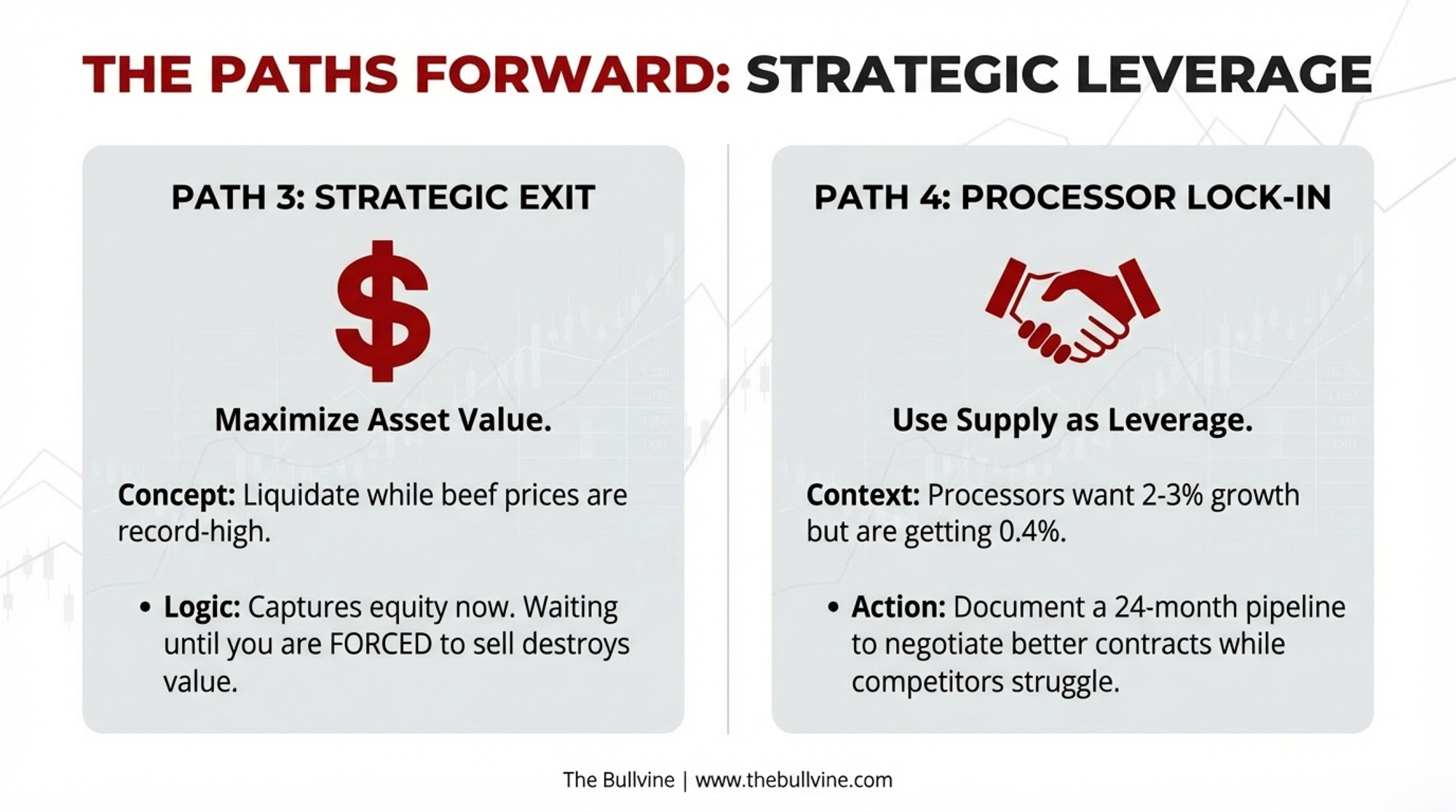

Path 3: Strategic Exit

Path 4: Processor Lock-In

Best for

Herds that can still course-correct the pipeline

Healthy older cows; buys time

Monthly losses; owners near retirement

Stable herds that can prove supply

Requires

Genomic testing ($15-45/head); sexed dairy on top 35-40%

Transition management; accept lower avg production

Honest market assessment before values erode

Documented 24-month replacement pipeline

⚠️ Backfire risk

Below 18% pregnancy rate, can’t maintain pipeline AND premiums

Failing to deliver on the supply commitment damages the relationship

Key threshold

21-day pregnancy rate ≥20% for optimal beef allocation

Monitor herd age distribution and SCC quarterly

Compare current liquidation value vs. projected 2027 value

Can you document pipeline sustainability?

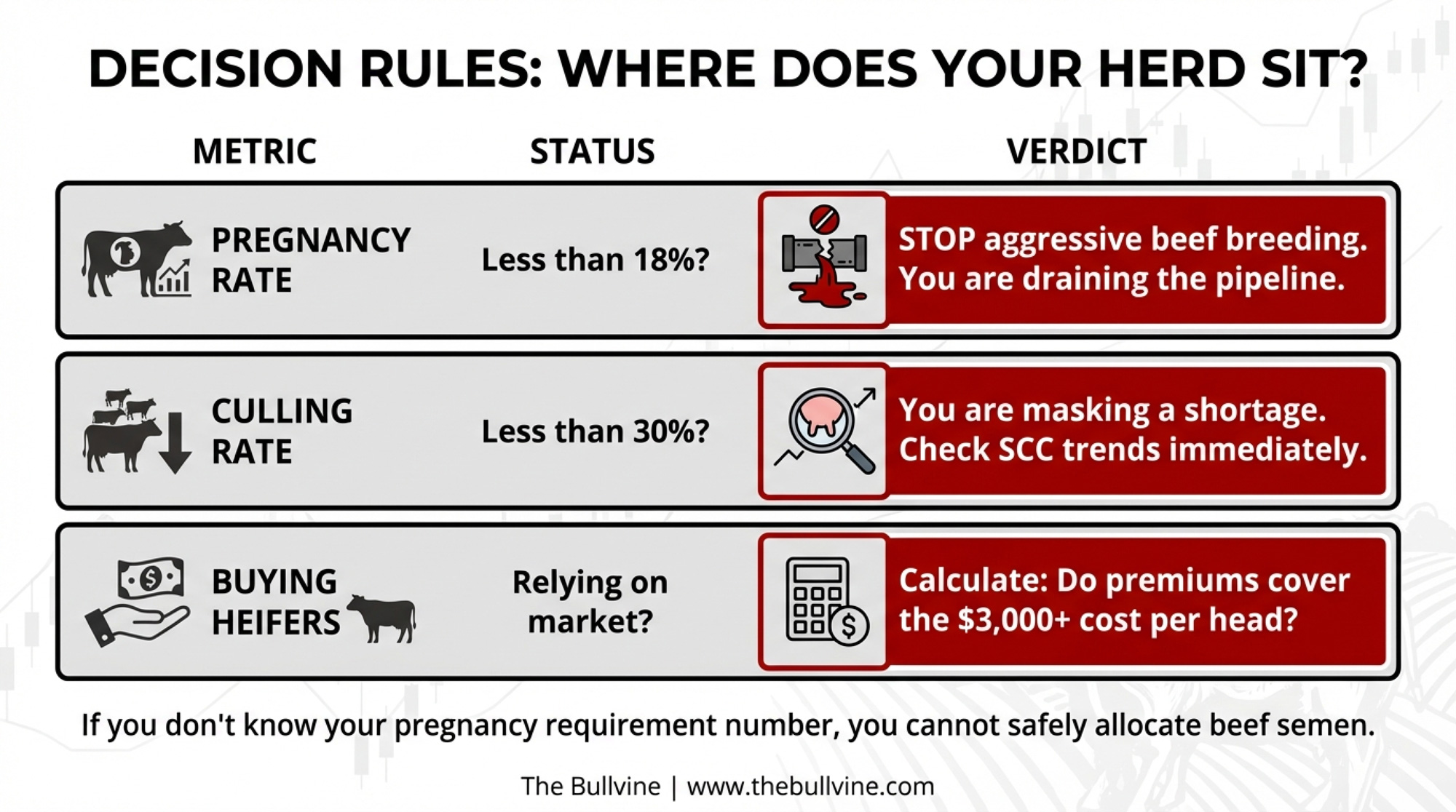

Path 1 is where the Journal of Dairy Science analysis matters most: beef semen becomes economically optimal when crossbred calf price hits at least 2x dairy calf price, AND herd achieves ~20% 21-day pregnancy rate. ⚠️ Below 18%, limit beef allocation to 50% maximum. Only about 10% of Florida producers use genomic testing, per University of Florida estimates—adoption rates vary significantly by region.

Path 2 carries a hidden cost. Retaining older cows often means rising somatic cell counts, which can erode quality premiums from your processor—compounding financial strain at exactly the wrong time. Worse, when a wave of retained cows exits simultaneously, you’ve traded a gradual shortage for a cliff.

Path 3 isn’t a failure. With beef cattle prices at record highs, liquidating today captures significantly more equity than waiting until the shortage resolves. ⚠️ Waiting preserves optionality but erodes equity if exit becomes forced rather than chosen.

Path 4 is the angle most producers haven’t considered. Strong signals suggest processors expecting 2-3% milk supply growth and getting 0.4% are becoming choosy about who they keep. If you can document pipeline sustainability, you may find yourself first in line for favorable contract terms as competitors struggle to guarantee supply.

Signals to Watch

Heifer inventory trajectory. CoBank projects inventories won’t normalize until 2027 at the earliest. Watch USDA semi-annual reports for evidence that national heifer numbers have stopped declining.

Regional price spreads. The gap between Wisconsin’s $2,850 and Northwest prices “north of $4,000” reflects infrastructure differences, not just supply. Where does your region sit?

Your own replacement math. How many dairy heifer pregnancies must you generate annually to maintain herd size at the target age structure? If you don’t know that number, you can’t evaluate your breeding allocation.

What This Means for Your Operation

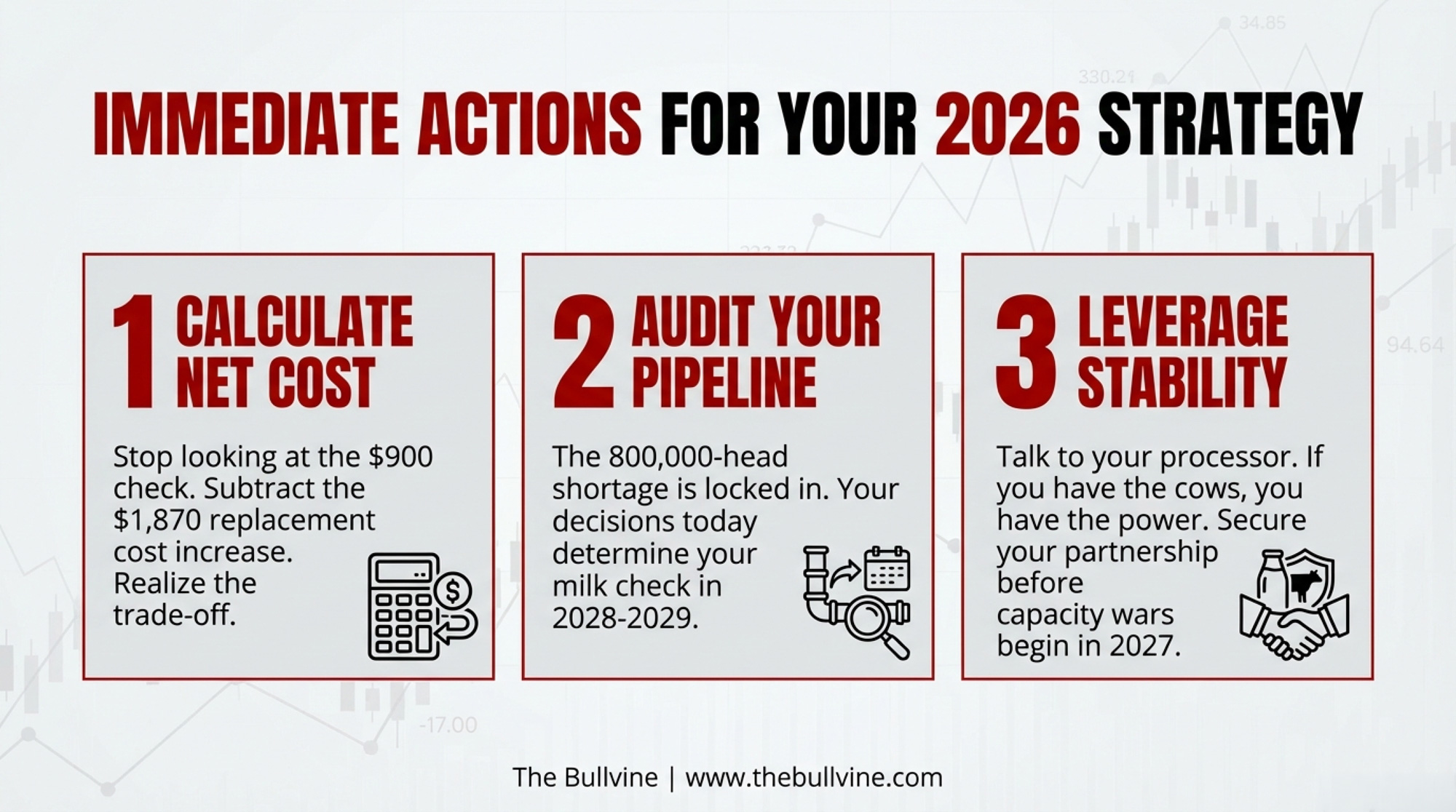

Calculate the real cost, not the gross premium. The $900 beef-cross check was real income—but if replacement costs have jumped $1,500+ per head since 2022, determine whether premiums actually offset that increase or simply deferred it

Run your replacement pipeline projection: at current breeding allocation and reproductive performance, will you have the heifers you need in 2028?

If “hard to breed” or “lower producing” remain your primary beef allocation criteria, the room for instinct-based allocation has narrowed sharply

Check your culling rate—if you’ve dropped below 30%, you’re likely masking a shortage rather than solving it—and check your SCC trends while you’re at it

Ask your processor what they value. If you can demonstrate a documented 24-month replacement pipeline, you may be in a stronger negotiating position than you realize

Opportunity signal: Balanced breeding programs with adequate heifer inventory could mean more favorable processor contracts as competitors struggle to guarantee supply

Key Takeaways

The 800,000-head shortage is locked in through 2026. Breeding decisions made today won’t produce milking cows until 2028-2029. The next 18 months are about managing what’s already baked in.

Don’t confuse gross premium with replacement reality. Across the industry, the collective shift drove replacement costs up $1,870 per head. For operations now buying replacements, the premium captured doesn’t come close to covering the increase in costs.

The 18% pregnancy rate threshold matters. Below that level, aggressive beef allocation creates unavoidable replacement shortfalls regardless of premium levels.

$10 billion in new dairy plants through 2027 means processor demand for milk keeps climbing while replacement supply stays pinched. Processors are likely choosing partners rather than just buying milk.

The Bottom Line

The operations that survive this won’t be those who avoided beef-on-dairy—many of the largest, most sophisticated dairies bred heavily to beef. They’ll be the ones who tracked replacement pipeline math while capturing premiums, rather than assuming the check today wouldn’t create a bill tomorrow.

Where does your operation sit on that spectrum—and what does your 2026 breeding sheet say about the answer?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

High-Value Crosses: The Next Phase of the Beef-on-Dairy Revolution – Breaks down advanced terminal crossbreeding strategies that maximize carcass value without sacrificing your herd’s future. It delivers the blueprints for “Elite Beef” programs that command significantly higher premiums than standard auction barn crosses.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Four breeders made four impossible bets. Every Holstein alive today is the payoff. Here’s what they knew that we forgot.

In 1926, a 69-year-old insurance executive did something that made the entire Holstein world think he’d lost his mind.

T.B. Macaulay—president of Sun Life Assurance, a man who’d spent his career calculating risk down to the decimal point—wrote a check for $15,000 for a single bull. According to the Bank of Canada’s inflation calculations, that’s roughly $260,000 in today’s dollars. For one animal. In a post-WWI economy where farmers were still digging out from the crash.

The old-timers called it insanity. The industry press questioned his judgment.

And here’s the thing—virtually every registered Holstein walking the planet today carries that bull’s blood. That’s not hyperbole. Holstein Canada pedigree records confirm that Johanna Rag Apple Pabst appears in the ancestry of essentially every animal in the modern registered population.

Which got me thinking: where did all this actually come from? We spend so much time staring at genomic indexes and GTPI rankings—debating inbreeding levels and trait selection—that we forget every number on that screen traces back to flesh-and-blood decisions. Made by breeders who couldn’t run a computer simulation to save their lives. They had paper records, sharp eyes, and guts.

So let’s talk about the ones who shaped everything. Four distinct philosophies, five legendary figures—because sometimes the right partnership counts double.

The Actuary Who Outbred Everyone: T.B. Macaulay

T.B. Macaulay: The insurance actuary who treated genetic improvement like a math problem—and solved it with a $15,000 check.

Here’s what made Macaulay different from every other breeder of his era: he didn’t grow up in cattle. No family farm, no inherited wisdom about which bloodlines “nick” well together. According to Sun Life corporate histories, he built one of Canada’s largest insurance companies through rigorous statistical analysis. He came from actuarial science—probability tables and risk calculation.

That turned out to be his superpower.

Picture Mount Victoria Farm in the 1920s. The buildings were functional, the land unremarkable—historical accounts describe it as a sandy plot in Quebec that nobody expected much from. The magic was all in the records. While neighboring operations made breeding decisions based on “well, his grandsire threw nice calves,” Macaulay’s office walls were covered in charts. Milk weights. Butterfat percentages. Daughter comparisons across lactations. They say he’d review those records the way other men read the morning paper—coffee in hand, pencil making notes in the margins.

He was doing progeny testing—evaluating bulls by their daughters’ actual performance rather than the bull’s own appearance—decades before the Holstein Association formalized the practice in the 1930s.

The man treated genetic improvement like a math problem. And he was solving for a specific value: 4% butterfat.

This might seem obvious today. With GLP-1 weight-loss drugs now shifting consumer demand toward protein—something the University of Wisconsin dairy economists have been tracking closely—and component pricing dominating most milk checks, we’re all thinking about what’s in the milk, not just how much of it there is. But in Macaulay’s time? Everyone chased volume. More milk, more milk, more milk. He looked at the numbers and saw where the industry was heading before the industry knew it.

His methods? Aggressive. Linebreeding. Calculated inbreeding. The kind of tight matings that would make some modern breeders nervous—though honestly, with average inbreeding coefficients now exceeding 9% according to CDCB data, maybe we should be having that conversation more openly. But Macaulay understood something crucial: if you want to fix a trait, you concentrate on genetics. You can’t be timid.

Which brings us back to that $15,000 bull—Johanna Rag Apple Pabst, “Old Joe.”

The critics had a field day. Fifteen thousand dollars! In 1926! But Macaulay had done his homework. He’d traced the butterfat genetics through the pedigree, analyzed Joe’s dam and grandam records, and calculated the probability that this bull would sire daughters that hit his 4% target.

He was right. Holstein Canada production records from the era show Old Joe’s daughters consistently met that benchmark. And his genetic influence spread so far that—I’m not exaggerating—it’s essentially impossible to find a registered Holstein today that doesn’t trace back to him.

Think about that next time you’re scrolling through bull proofs.

The Empire Builder: Stephen Roman. From uranium mines to the Royal Winter Fair, he proved that deep pockets are useless without a marketing strategy—and that the show ring is where brands are built.

Two men. Opposite approaches. Roman bought everything. Ormiston bought one cow for $750. Both changed the breed forever—just in completely different ways.

Stephen Roman’s story is pure immigrant ambition. According to Canadian business histories, he arrived from Slovakia with basically nothing, worked the assembly line at General Motors, and somehow—through uranium mining at Denison Mines—became a billionaire by the 1960s. When he turned to Holsteins, he didn’t want to breed good cattle. He wanted to build an empire.

Romandale Farms became exactly that. But Roman was smart enough to know his limitations. He had the capital to buy the best cattle in North America. But he needed someone who could see cattle the way the great ones did. So he hired Dave Houck as herd superintendent—a man people in Ontario breeding circles described as having an almost spiritual connection to Holsteins. An old-timer once told me that watching Houck evaluate a heifer was like watching a sculptor see the statue inside the marble.

Money plus cow sense. That combination is almost unbeatable.

Roman’s real genius was understanding that the show ring wasn’t about ribbons. It was marketing. Every Supreme Champion, every Royal Winter Fair banner—that was brand building. “Through the show ring,” he said, according to accounts from breeders who worked with him, “lay the path to the Holstein mountain-top.”

And his sale tactics? Still copied today. He’d sell elite females in pairs on “choice”—the highest bidder picked one, Romandale kept the other. Record prices and retained genetics. The man understood both sides of the sale ring.

The crown jewel was Romandale Reflection Marquis. “The white male monster,” people called him—not affection, exactly. More like grudging respect mixed with a little fear. In 1964, Marquis topped the Romandale sale at $37,000 to Curtiss Breeding Service—a price documented in Holstein sale records from that era. I heard someone describe watching him enter that sale ring—said you could feel the air change in the building. Everyone knew they were seeing something.

What does Roman teach us now? Look around at successful embryo programs, operations with strong social media presence, and breeders who understand that perception drives demand. Great genetics need great marketing. That hasn’t changed.

Roy Ormiston in the Roybrook office. While the industry chased trends, Ormiston sat here and built a global dynasty from that single $750 foundation.

They called him “The Holstein Man’s Holstein Man,” and if you spent time around Ontario dairy circles mid-century, you understood why. According to Holstein Canada records, Ormiston had served as a fieldman for the association—walked through hundreds of herds, handled thousands of cattle, developed the kind of eye that can’t be taught. Only earned.

His philosophy was almost Zen-like.

“I like to compare a dairy cow to a building,” he explained in interviews preserved by breed historians. “If you don’t have a very good foundation, then it isn’t going to stand up too long.”

One foundation. One cow. Build everything from her.

In 1956, he found her.

Balsam Brae Pluto Sovereign wasn’t flashy. Wasn’t the cow everyone talked about. At $750, according to sale records, she was priced like an afterthought. But Ormiston saw something others missed—some combination of structure, constitution, and… something else. Call it transmitting ability. Call it prepotency. Whatever it was, The White Cow had it.

Here’s the moment that changed everything. Ormiston bred her to different bulls over several calvings, watching daughters develop. And something became clear.

“It was then I realized,” he said, “that no matter what she was bred to, The White Cow would always produce a good daughter. That’s when I knew I could line breed on her.”

If she threw excellence regardless of the sire, he could concentrate her genetics without fear. That insight was the Roybrook program. He didn’t chase outside genetics. He built on what he had.

The result? Telstar, Starlite, and Tempo—three bulls whose influence is documented in Holstein pedigree databases worldwide. Telstar’s impact in Japan was so profound that Japanese breeders erected a life-size bronze statue in his honor. A statue. For a Canadian bull. It still stands today as a testament to how far one cow family’s influence can reach.

What does Ormiston teach us in the genomic age? Something counterintuitive, maybe. We’ve got more sire diversity than ever. Can sort embryos by sex, screen for dozens of recessives, and select for indexes that didn’t exist five years ago. But Ormiston’s lesson wasn’t about tools. It was conviction. Find the cow family that works. Have patience to build on it. Stick with what works, and it keeps working.

Some of the most successful programs I see today do exactly that. Not chasing every new sire topping the rankings. Developing maternal lines, generation after generation.

The Partnership That Multiplied Everything: Hanover Hill Holsteins

The perfect balance: Ken Trevena (left) brought the unmatched “cow sense” for the 1:00 AM checks, while Peter Heffering (right) masterminded the global strategy. Together, they didn’t just add skills—they multiplied them.

Our final visionaries proved something the others couldn’t—that the right partnership doesn’t just add skills. It multiplies them.

In the spring of 1973, Peter Heffering and Ken Trevena moved from New York to a 300-acre farm in Port Perry, Ontario. They’d already built reputations south of the border. But Hanover Hill—the operation they created together—would reshape the entire industry.

“We didn’t set out to create a dynasty,” Heffering once said. “Our aim was simple: breed the best Holsteins in the world.”

What made them different was how they divided the work. Trevena was in the barn at 1:00 AM for the first milking, evaluating movement and watching how the heifers carried themselves. By the time Heffering arrived with the day’s marketing strategy, Trevena already knew which animals were ready for their next photo shoot. They’d meet over coffee, decisions would get made, and neither man held the other back. I’ve seen plenty of partnerships collapse over the years. This one just… worked.

But here’s what really set them apart: they rejected the numbers game.

By the early 1970s, American geneticists were pushing hard toward index-based evaluation—production numbers above all else. Heffering called it out publicly. He argued the indexes ignored what actually keeps a herd profitable: cow families, type, and longevity. Sound familiar? The tension between index-chasing and holistic evaluation hasn’t gone away—it’s just moved to genomic proofs. Same argument, different decade.

Their timing was impeccable. And their marketing? Relentless. They showed cattle everywhere, racking up 140 All-American and 87 All-Canadian nominations. From 1983 to 1988, they were Premier Breeders at both the Royal Winter Fair and World Dairy Expo. Their 1972 dispersal—before the Canada move—saw 286 head cross the auction block, averaging over $4,000 each. Numbers unheard of at the time.

But the crowning achievement came in 1985. Picture the scene: twenty-five hundred people packed around the sale ring. When bidding on Brookview Tony Charity crossed a million dollars, the crowd went silent. Then Stephen Roman’s hand went up one more time. $1,450,000. Two Holstein legends—Roman the empire builder, Hanover Hill the partnership that rewrote the rules—converging in a single moment.

The real legacy, though? Starbuck.

Hanoverhill Starbuck might be the most influential Holstein sire in modern history. A son of Round Oak Rag Apple Elevation out of Anacres Astronaut Ivanhoe, he combined the production Heffering and Trevena demanded with the type and cow family depth they’d staked their reputation on. His daughters milked. They lasted. They bred on. They produced nine Class Extra sires in total—a concentration of top-tier bloodlines that no other single operation has matched.

For the complete Hanover Hill story, including their legendary cow families and the full list of influential bulls, see our detailed profile.

What These Legends Teach Us Now

So here we are, late 2025. Genomics have transformed selection. Sexed semen is standard. We’ve got precision feeding, robotic milking, and indexes our grandparents couldn’t have imagined. The debates continue—just swap “progeny testing” for “genomics” and “linebreeding” for “inbreeding depression,” and we’re having the same arguments these breeders had decades ago.

The tools are different. The philosophies haven’t changed.

Macaulay teaches us that data—rigorously collected, honestly analyzed—beats intuition. More true than ever. If you’re not using herd management software to drive breeding decisions, you’re leaving money on the table.

Roman teaches us that great genetics need great marketing. In an age of Instagram breeders and embryo auctions livestreamed to three continents, that lesson hits harder than ever.

Ormiston teaches patience and conviction. Find your cow family. Build on it. Don’t get distracted by every shiny new thing topping the proof run.

And Heffering and Trevena? They teach us that the right partnership multiplies everything—and that rejecting index-only thinking in favor of holistic breeding isn’t stubbornness. It’s a strategy. Something worth considering as operations navigate succession and the next generation steps up to take the reins.

Four philosophies. Five legends. All still valid.

Next time you see a sire topping the rankings, ask yourself: which of these philosophies got him there? And which one guides your operation? Or—maybe this is the real answer—which combination are you building?

Because the producers I see succeeding right now pull from all of them. Data-driven decisions. Marketing awareness. Commitment to maternal lines. Strategic partnerships. Willingness to reject conventional wisdom when it doesn’t serve the cow.

The legends left us the playbook. We just have to read it.

Which breeding philosophy resonates most with your operation? Drop a comment below or find us on social media—these conversations are how we all get better.

Key Takeaways:

Data beats intuition: Macaulay paid $15,000 for one bull when everyone called him crazy. His daughters hit 4% butterfat. His genetics run through every Holstein alive. Trust the numbers.

Genetics without marketing is wasted potential: Roman treated the show ring as advertising, not trophies. Today, that’s Instagram, livestreamed embryo sales, and understanding that perception drives price.

One cow family. Total commitment: Ormiston bought a $750 cow nobody wanted and built a dynasty that earned a bronze statue in Japan. Find your foundation. Stop chasing.

Partnerships multiply—when you divide right: Trevena worked the 1 AM milkings. Heffering ran the strategy. Neither held the other back. Hanover Hill dominated two continents for a decade.

Same four choices. Different tools: Data, marketing, conviction, and collaboration. The philosophies that built the breed are the philosophies that’ll carry your operation forward. Which combination are you building?

Executive Summary:

Every registered Holstein alive today carries genetics shaped by four breeders who ignored what everyone else believed. T.B. Macaulay paid $15,000 for one bull in 1926—critics called it insanity, but his data-driven gamble now flows through your entire herd. Stephen Roman built Romandale into an empire by treating the show ring as marketing, not trophies. Roy Ormiston turned a single $750 cow into bloodlines that earned a bronze statue in Japan. Heffering and Trevena rejected index-only thinking and proved that the right partnership multiplies everything. Four philosophies—data, marketing, conviction, collaboration—all still shaping who succeeds. The only question: which combination are you building?

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

73% of the top 30 NM$ bulls. One breeding program. The December 2025 Holstein evaluations just rewrote the genetic playbook.

Executive Summary: The December 2025 US Holstein genetic evaluations expose a seismic shift: Genosource now owns 22 of the top 30 Net Merit bulls—73% of the industry’s elite profit genetics under one roof. GENOSOURCE RETROSPECT-ET defends the #1 NM$ position at $1296, while BEYOND HI-LEVEL-ET commands GTPI at 3612, a 73-point jump that widens the gap at the top. Newcomer SAN-DAN ON CALL-ET exploded onto the scene at #3 GTPI (3574) with production numbers that demand attention: 1845 Milk, 151 Fat, 70 Protein. Type leadership remains locked between SHG LEGO and REDCARPET STORY ARC-ET at 3.85 PTAT, while Red & White genetics surge forward with SIEMERS RLE PAPAYA-RED-ET topping at 3221 GTPI. The consolidation of profitable genetics into a single program isn’t a trend—it’s the new reality, and breeders who adapt their sire selection now will compound this advantage for generations.

Dairy breeders and industry professionals, welcome to our analysis of the December 2025 US Holstein Genetic Evaluations. This round of evaluations saw numerous high-ranking newcomers and shifts among the established leaders across the major indices, underscoring the continued rapid turnover in elite genomic performance.

GTPI (Genomic Total Performance Index) Highlights

The December 2025 evaluations present a highly competitive Top 100 GTPI list for bulls over 12 months with NAAB codes, with significant consolidation among the leading bull providers.

Top Movers and Shakers

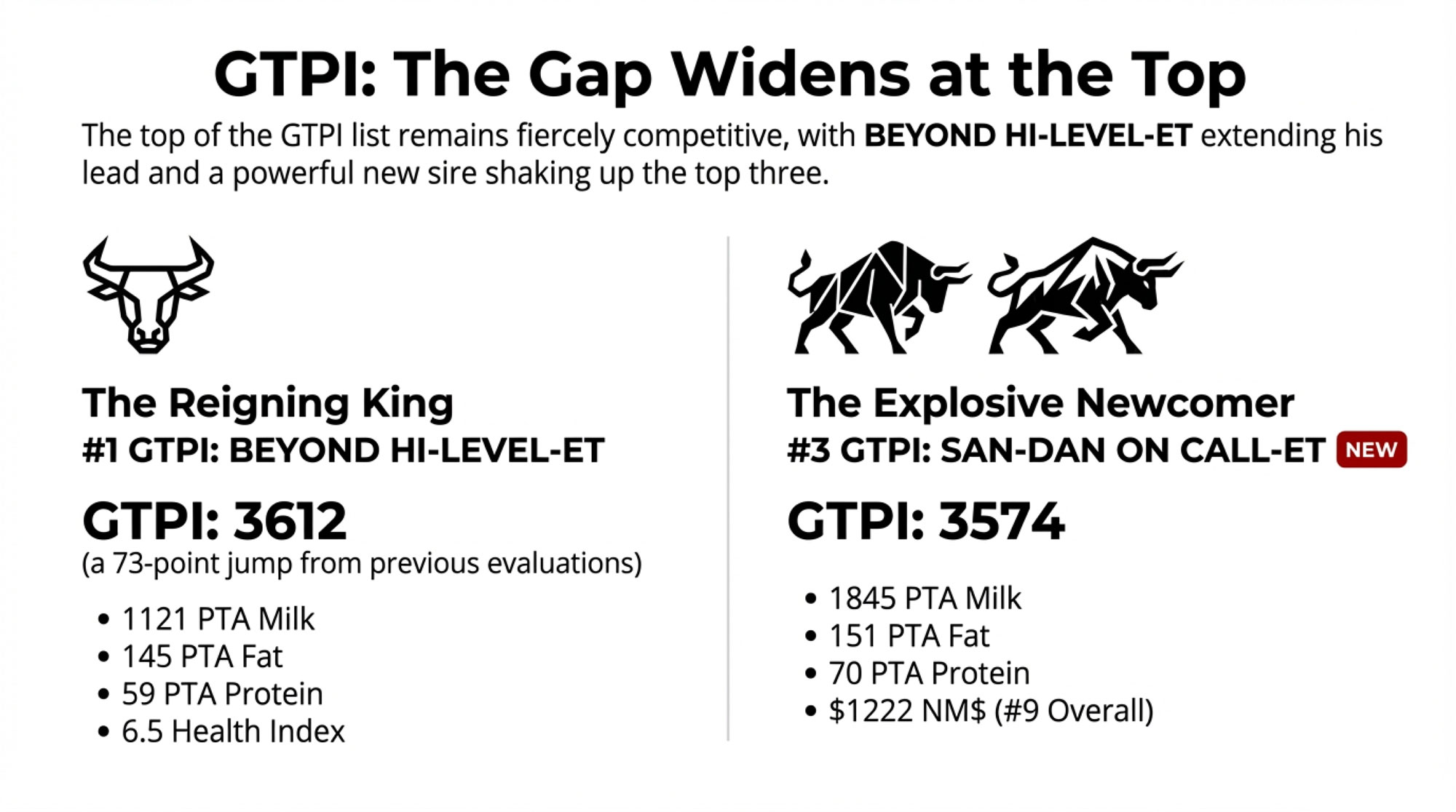

BEYOND HI-LEVEL-ET maintains its position as the #1 GTPI bull overall, posting a GTPI of 3612. The bull demonstrates strong production credentials with 1121 PTA Milk, 145 PTA Fat, and 59 PTA Protein, combined with a solid Health Index of 6.5.

The top of the list saw considerable shifting:

BEYOND SHPSTR GOLLEY-ET made a major move to the #2 position in December, reaching 3605 GTPI. This sire excels with high PTA Fat (147) and strong PTA Type (1.51).

SAN-DAN ON CALL-ET (3574 GTPI) enters the top rankings directly at #3. This sire is exceptional for production, yielding 1845 PTA Milk, 151 PTA Fat, and 70 PTA Protein, while also ranking #9 for Net Merit at $1222.

OCD TROOPER SHEEPSTER-ET (3572 GTPI) now stands at #4 in the general Top 100 GTPI ranking.

PROGENESIS WATCHMAN rounds out the top five at 3568 GTPI.

BEYOND HI-PACE-ET secures #6 with 3566 GTPI, adding depth to the Beyond program’s GTPI dominance.

New Sires in the GTPI Top 100

The December 2025 GTPI ranking features numerous exciting new entrants that cracked the Top 100. Key new sires debuting near the top include:

S-S-I OLD RICHARD-ET ranks high at #7 with 3553 GTPI

S-S-I SIEMERS N MCLAURIN-ET follows closely at #8 with 3549 GTPI, showing impressive PTA Type (1.81) and Udder Composite (1.16)

STGEN MAZOR-ET (3539 GTPI) and GENOSOURCE LANDMAN-ET (3537 GTPI) secured the #11 and #12 spots, respectively

BEYOND HOORAY-ET also debuts strongly at #13 (3537 GTPI)

GENOSOURCE YAGERMEISTER-ET at #16 (3533 GTPI) and OCD SHEEPSTER ROCK-ET at #17 (3528 GTPI)

Net Merit ($NM) Evaluation Overview

The December 2025 Net Merit rankings reveal a seismic shift in genetic leadership that dairy breeders cannot ignore: Genosource bulls now hold an astounding 22 of the top 30 NM$ positions—representing 73% of the elite profitability tier. Even more remarkably, Genosource claims 5 of the top 7 spots, including the #1 position.

This level of concentration is unprecedented in modern Holstein genetics and signals a fundamental change in how profitable genetics are being developed and marketed. The Genosource breeding program has clearly cracked the code on balancing high production with health, fertility, and longevity traits that drive lifetime profitability.

NM$ Leaders

GENOSOURCE RETROSPECT-ET successfully defends its title as the #1 NM$ bull, achieving $1296 NM. This bull also appears at #87 on the GTPI list with a GTPI of 3477, demonstrating balanced genetic merit across multiple selection indices.

The Genosource dominance continues throughout the rankings:

551HO06566 is the #2 NM$ sire at $1274 NM, featuring 2089 PTA Milk and 77 PTA Protein

STGEN STUART-ET ranks #3 NM$ at $1250 NM, providing 1666 PTA Milk, 145 PTA Fat, and 71 PTA Protein

GENOSOURCE MIKAIL-ET holds the #4 NM$ position with $1246 NM

GENOSOURCE ELVIS-ET at #5 with $1245 NM

GENOSOURCE VAMOOSE-ET at #6 with $1231 NM

GENOSOURCE ENDURANCE-ET at #7 with $1227 NM

Production Powerhouses in the NM$ Rankings

Many of the top NM$ bulls exhibit high combined Fat and Protein (CFP) figures, which are vital for milk component revenue. Notable examples include:

GENOSOURCE BENCHMARK-ET (NM $1207, #11) boasts the highest CFP among the top NM sires at 228

SAN-DAN ON CALL-ET, ranking #9 NM$ with $1222, delivers 221 CFP from 1845 PTA Milk

GENOSOURCE YUPPIE-ET (#27 NM$) showcases extreme production at 2662 PTA Milk, ranking high despite challenging functional traits, including Productive Life of -0.3 and Daughter Pregnancy Rate of -3.0

PTAT (Prediction of Transmitting Ability for Type) Focus

The December 2025 PTAT list features sires that transmit superior conformation and functional type.

PTAT Top Performers

The top two sires continue their dominance:

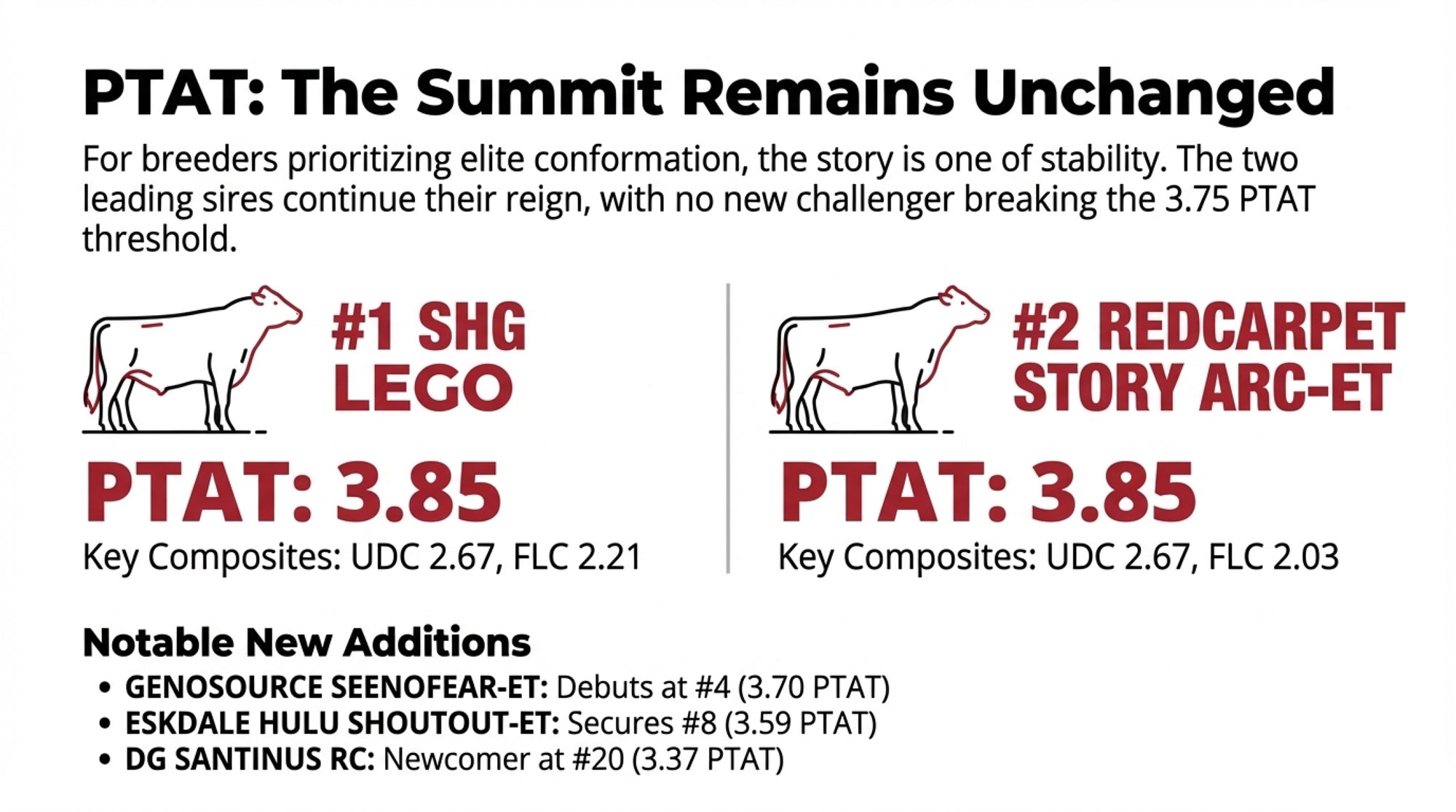

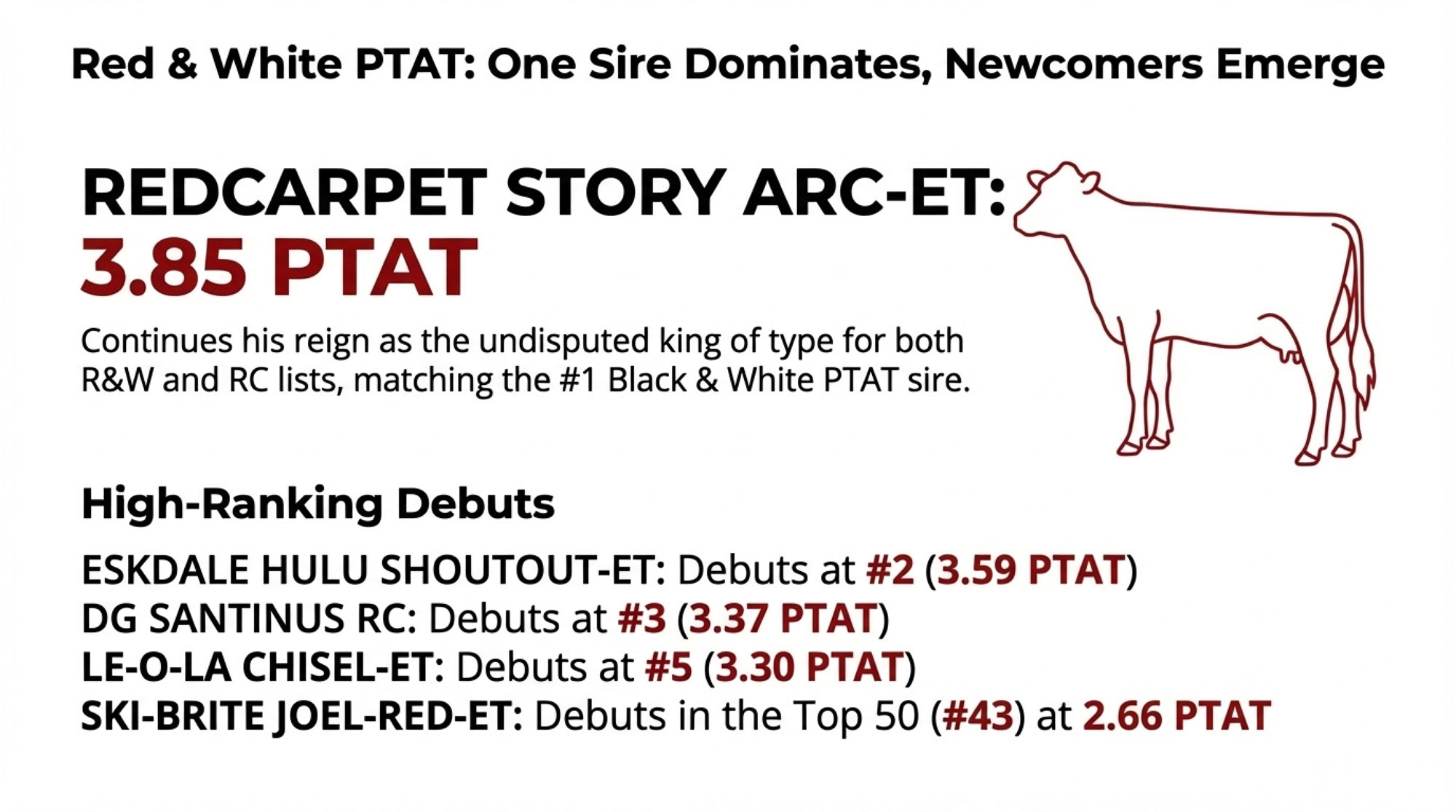

SHG LEGO remains #1 with 3.85 PTAT

REDCARPET STORY ARC-ET holds #2 with 3.85 PTAT

For breeders prioritizing show ring success or building maternal lines with exceptional udder quality, the stability at the top provides confidence—these proven type transmitters aren’t going anywhere. No emerging challenger has broken 3.75 PTAT, meaning the path to elite conformation genetics remains clearly defined.

Key Shifts and New Additions in the PTAT Top 50

STONE-FRONT EYECANDY APOLLO holds steady at #3 with 3.73 PTAT

GENOSOURCE SEENOFEAR-ET is a new, high-ranking entrant at #4 with 3.70 PTAT

ESKDALE HULU SHOUTOUT-ET (3.59 PTAT) secured the #8 spot

LAND-PRIDE UNBEATABULL-ET debuts at #19 with 3.38 PTAT

DG SANTINUS RC is a high-ranking newcomer at #20 (3.37 PTAT)

LE-O-LA CHISEL-ET secured #27 (3.30 PTAT)

COLDSPRINGS LAURENT 9901-ET debuted at #47 (3.14 PTAT)

Red Carrier and Red & White Genetic Leaders

Red Carrier (RC) GTPI

The Red Carrier list shows strong genetic progress at the elite level:

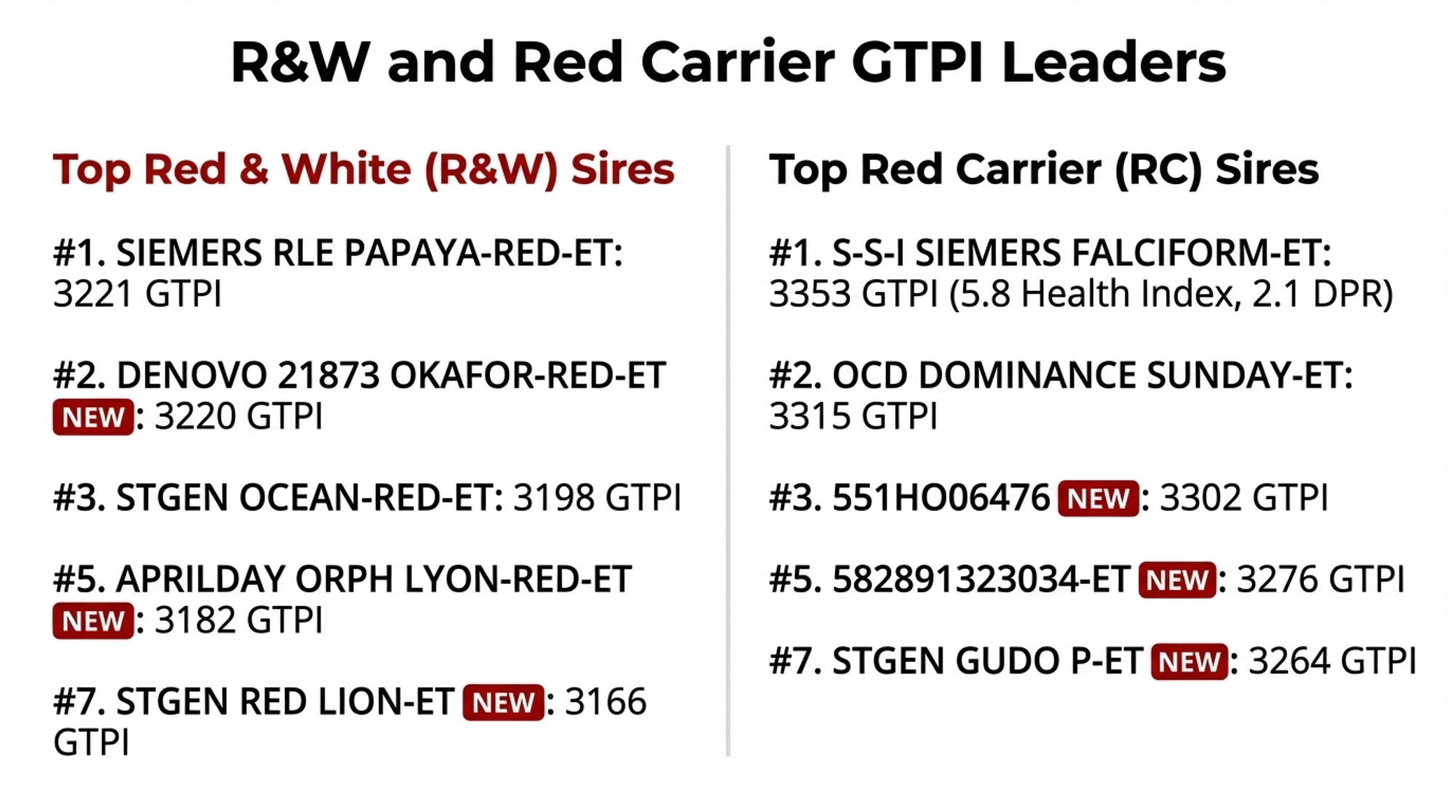

S-S-I SIEMERS FALCIFORM-ET maintains the #1 RC GTPI position at 3353, demonstrating a strong Health Index (5.8) and high Daughter Pregnancy Rate (DPR 2.1)

OCD DOMINANCE SUNDAY-ET holds steady at #2 with 3315 GTPI

The newcomer 551HO06476 enters at #3 (3302 GTPI)

New sires penetrating the Top 50 include 582891323034-ET (#5, 3276 GTPI) and STGEN GUDO P-ET (#7, 3264 GTPI)

Red & White (R&W) GTPI

The R&W GTPI rankings remain dynamic with multiple new entrants:

SIEMERS RLE PAPAYA-RED-ET is the #1 R&W GTPI bull at 3221 GTPI

DENOVO 21873 OKAFOR-RED-ET debuts strongly at #2 (3220 GTPI)

STGEN OCEAN-RED-ET is the #3 R&W GTPI bull at 3198 GTPI

GENOSOURCE MORRIS-RED-ET holds the #9 position at 3164 GTPI

New sires APRILDAY ORPH LYON-RED-ET (#5, 3182 GTPI) and STGEN RED LION-ET (#7, 3166 GTPI) mark strong debuts

The 391-point gap between SIEMERS RLE PAPAYA-RED-ET (3221) and BEYOND HI-LEVEL-ET (3612) represents the closest Red & White genetics have come to elite black & white performance in recent memory—a milestone that validates years of focused colored cattle breeding.

Red Carrier and R&W PTAT

In the Type rankings for colored cattle, REDCARPET STORY ARC-ET remains the dominant sire, leading the combined R&W and Red Carrier PTAT list at 3.85 PTAT. Other notable performers include:

ESKDALE HULU SHOUTOUT-ET makes a powerful entrance at #2 with 3.59 PTAT

DG SANTINUS RC debuts at #3 with 3.37 PTAT

LE-O-LA CHISEL-ET debuts at #5 with 3.30 PTAT

SKI-BRITE JOEL-RED-ET debuts in the Top 50 at #43 (2.66 PTAT)

The Bottom Line

This consolidation of profitable genetics demands a strategic response. Review your current sire lineup against these rankings and ask: Does your genetic strategy align with where profitability is actually being generated? Whether you prioritize NM$, GTPI, type, or colored genetics, the December 2025 evaluations provide clear direction—and clear leaders—in every category.

Key Takeaways

Profit genetics monopolized: Genosource captures 22 of 30 top Net Merit positions—73% of the industry’s most profitable sires now come from one program, led by RETROSPECT-ET at $1296

GTPI leadership extends: BEYOND HI-LEVEL-ET dominates at 3612; newcomer SAN-DAN ON CALL-ET explodes to #3 (3574) with 1845 Milk, 151 Fat, and dual ranking at #9 NM$

Type titans hold firm: SHG LEGO and REDCARPET STORY ARC-ET lock the PTAT summit at 3.85—no emerging challenger breaks 3.75

Red & White within striking distance: SIEMERS RLE PAPAYA-RED-ET reaches 3221 GTPI, closing the gap to just 391 points behind the #1 overall bull

Data source: Council on Dairy Cattle Breeding (CDCB), December 2025 genetic evaluations. All rankings reflect bulls with NAAB codes over 12 months.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

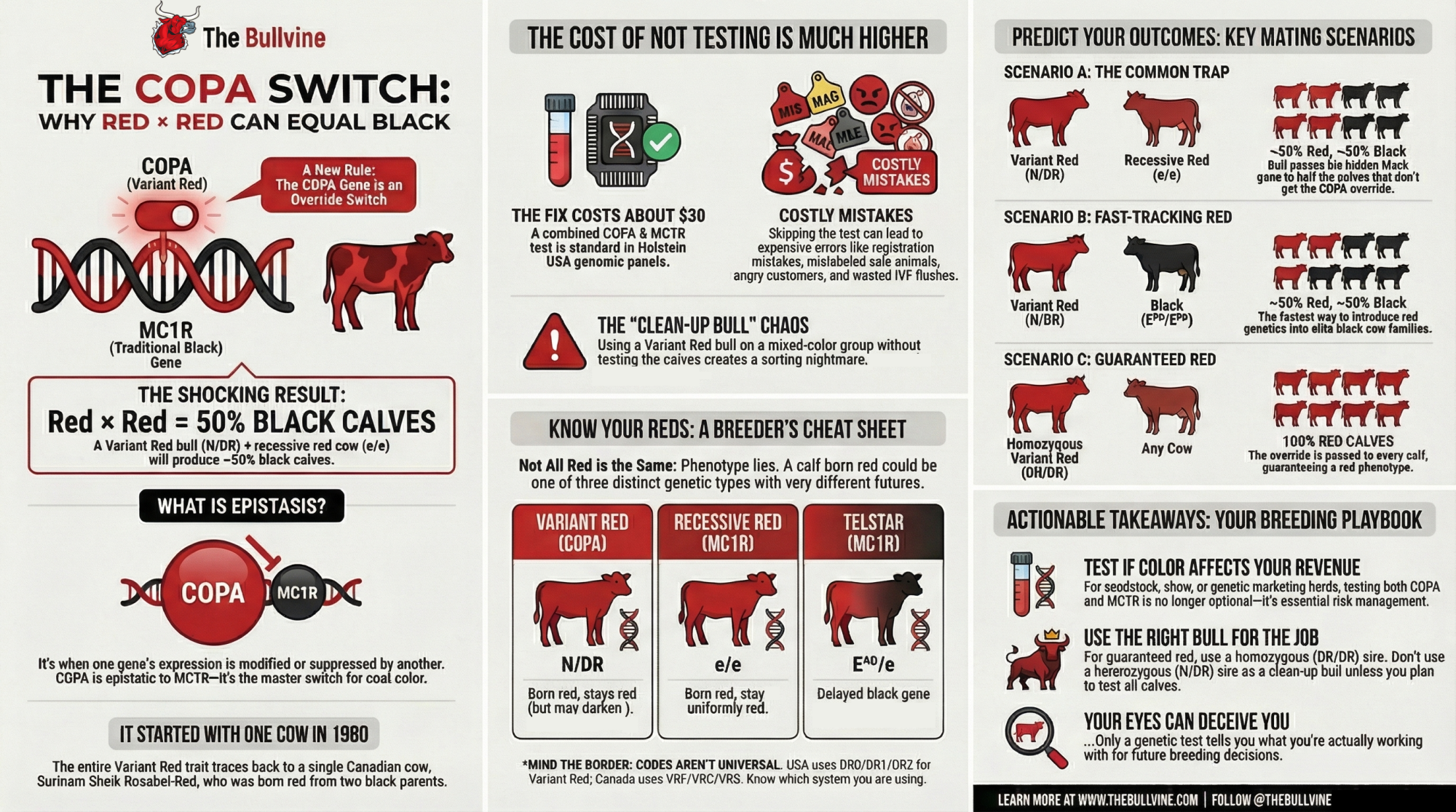

Red × Red should equal Red. But half your calves came out black. The COPA gene is the override switch you didn’t know existed.

For decades, Holstein breeders operated on a simple truth: Black dominates Red. It was a comfortable, binary rule—and one that served us well for generations. But here’s the thing: it was incomplete as well.

The emergence of Variant Red (COPA) hasn’t just added a new color pattern to our toolbox; it’s also changed the way we think about color. It’s exposed a blind spot in how we think about genetic pathways. And if you’re making mating decisions without accounting for this “override” switch, you’re working with incomplete information. That costs money.

The Mechanic: Two Systems, One Outcome

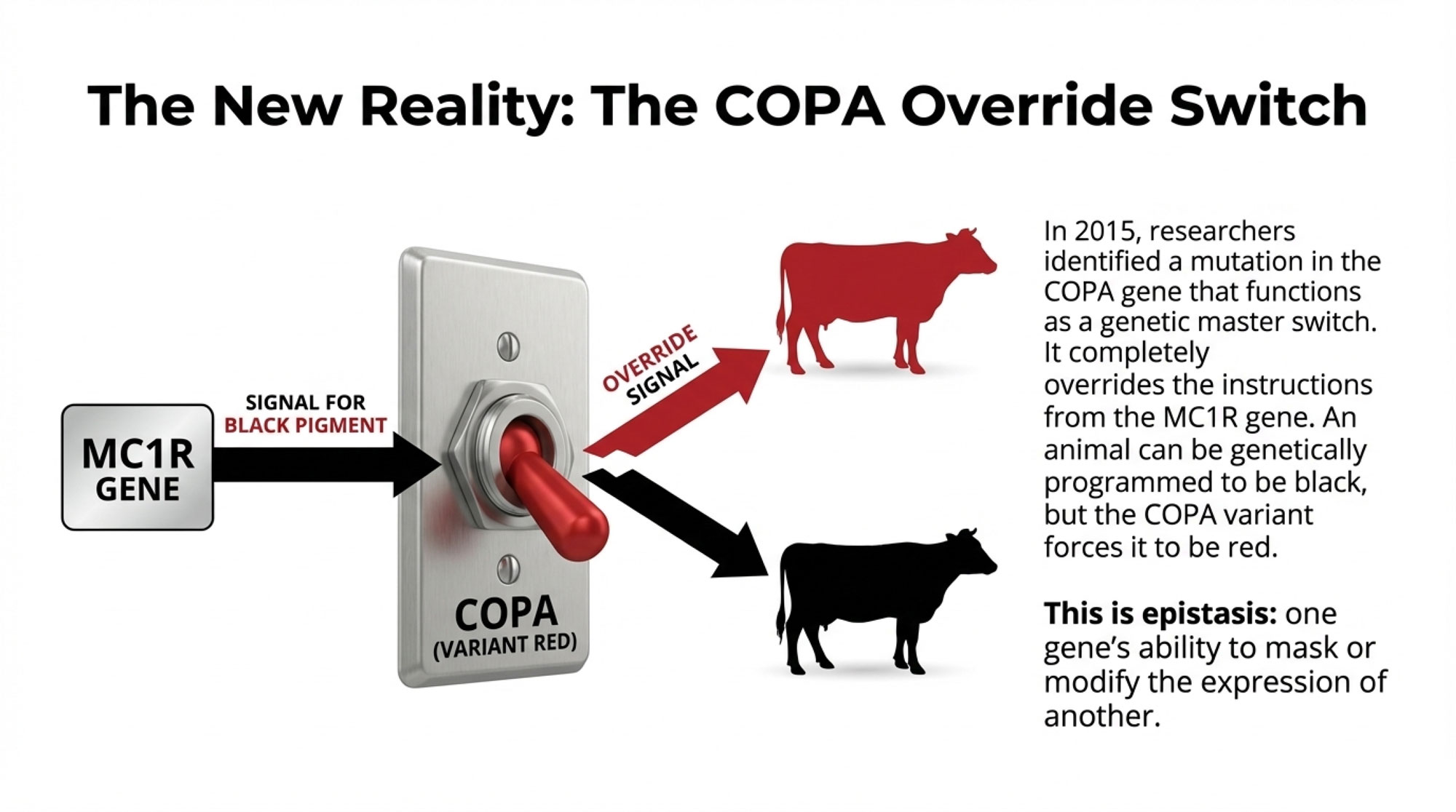

You probably already know the old model. The MC1R gene—what geneticists call the Extension locus—controls coat color through a clear dominance hierarchy: E^D (dominant black) > E^BR (Telstar) > E^+ (wild-type) > e (recessive red). Two copies of e gives you a red calf. Simple enough.

Then in 2015, researcher Ben Dorshorst and an international team published findings in PLOS ONE that changed everything. They identified a second switch: a mutation in the COPA gene that produces what we now call Variant Red. The critical discovery? COPA overrides MC1R entirely. An animal can be genetically programmed to be black at MC1R, but if it carries the COPA variant, it still expresses red. A decade of breeding experience and subsequent genetic research has validated this finding—the mechanism holds up.

This is epistasis in action—one genetic pathway superseding another. Practically, it means that phenotype alone tells you nothing about what’s actually happening under the hood.

The good news? We now have reliable tests for both systems. UC Davis Veterinary Genetics Laboratory offers both COPA and MC1R panels, and Holstein Association USA includes both in their standard genomic testing. Once you know both pieces, you can actually plan your color outcomes instead of guessing.

The Cheat Sheet: Mating Outcomes at a Glance

Let me walk you through the scenarios breeders ask about most. This is the section you’ll probably want to bookmark.

Scenario A: Variant Red Sire (N/DR) × Black Dam (E^D/E^D)

Outcome: ~50% Red / ~50% Black

What’s happening: Red calves inherit the dominant DR allele, which overrides their black MC1R genetics. Black calves inherit the N allele and express normally.

Scenario B: Variant Red Sire (N/DR) × Recessive Red Dam (e/e)

Outcome: ~50% Red / ~50% Black (if sire carries E^D at MC1R)

What’s happening: This scenario assumes your Variant Red bull is carrying the Dominant Black gene (E^D) “underneath” his red coat—which many do, since the COPA mutation originated in black Holsteins. Red calves inherit DR (Variant Red) and express red regardless of MC1R. But calves inheriting N from the sire are now N/N at the COPA locus (no override present). If they also inherit E^D from the sire and e from the dam, they genotype as E^D/e at MC1R—which results in a black phenotype. Important note: If your Variant Red bull happens to be e/e (recessive red) at MC1R, he won’t throw black calves even when passing N—but this is less common.

Scenario C: Homozygous Variant Red Sire (DR/DR) × Any Dam

Outcome: 100% Red

What’s happening: Every calf inherits at least one DR allele. The override is guaranteed. This is your cleanest path to predictable red outcomes.

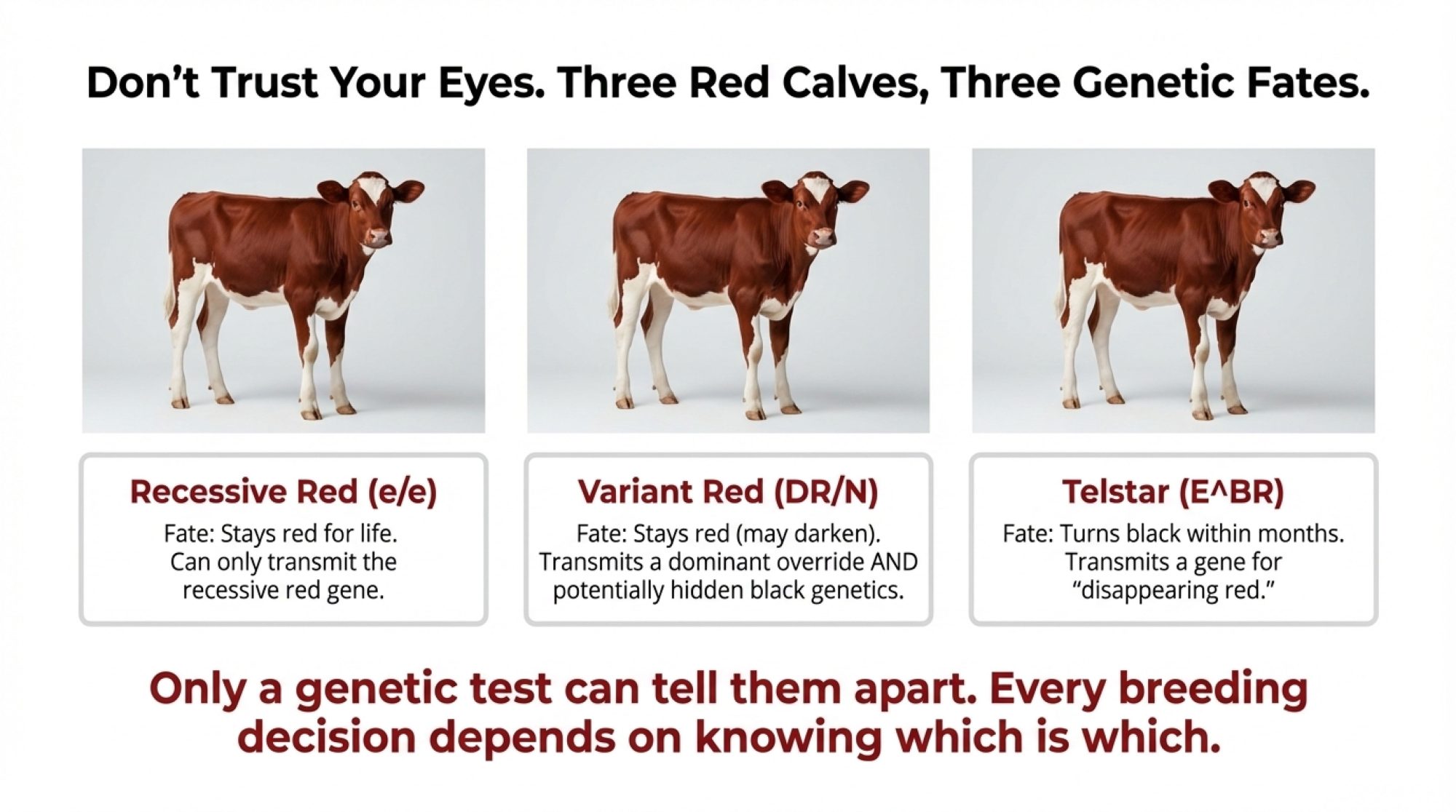

Scenario D: Telstar (E^BR) Animals

Outcome: Born red, turn black within 2-6 months

What’s happening: Completely different mechanism—MC1R timing, not COPA override. Don’t confuse these in your records.

The Trap: When Red × Red = Black

This scenario deserves special attention because it’s the one that burns breeders most often.

You have a nice Variant Red bull (N/DR). You breed him to your recessive red cows (e/e). You’re expecting all-red calves—makes sense, right? Red bull, red cow, red calves.

Except that about half those calves come out black. What gives?

Here’s what’s happening genetically: Your N/DR bull passes either N or DR to each calf (50/50 chance). The calves that get DR are red—the override kicks in, and they express Variant Red. But the calves that get N are now N/N at the COPA locus (no override present), assuming your dam is N/N like most Holsteins. If those calves also inherit E^D from the sire and e from the dam, they genotype as E^D/e at MC1R—and since Dominant Black is dominant over recessive red, you get a black calf.

The key detail here: this trap only springs if your Variant Red bull carries E^D at MC1R. Many do—the COPA mutation originated in black Holstein lines, so most Variant Red animals are “hiding” black genetics underneath that red coat. But if your bull happens to be e/e at MC1R (homozygous recessive red), he can’t pass E^D, and you won’t see black calves even when he passes the N allele.

This is exactly why UC Davis VGL’s documentation is explicit: phenotype cannot distinguish between color mechanisms. You need to test both COPA and MC1R to know what you’re actually working with.

Select Sires addresses this directly in their bull catalogs. Their DR1 code indicates heterozygous Variant Red status, and their technical materials—using LUCKY SEVEN-RED as an example—walk through exactly these scenarios. That’s the kind of transparency the whole industry should be moving toward.

The Money: Testing Costs vs. Breeding Errors

Let’s talk economics, because this is where the rubber meets the road.

Testing costs are pretty reasonable. UC Davis VGL lists coat color testing at $30 for the first test and $10 for each additional test on the same animal (pricing as of October 2023—worth verifying current rates at vgl.ucdavis.edu/pricing/cattle before you budget).

The cost of NOT testing? That’s where it gets expensive.

The Telstar Trap: You sell a red heifer as breeding stock. Buyer’s excited, pays a premium for red genetics. Six months later, she’s turned black. Now you’ve got an angry customer and reputation damage that’s hard to quantify but very real.

The Registration Error: You register a Variant Red calf as recessive red because it looks the same as a red calf at birth. Now every mating decision based on that animal’s record is built on false assumptions. Future buyers make breeding plans expecting recessive red transmission—and get results that don’t make sense. These errors compound across generations.

The Donor Disaster: You flush a valuable cow expecting specific color outcomes based on her phenotype. Wrong assumptions about her COPA/MC1R status mean the resulting embryos don’t deliver what you promised buyers. Cost: the flush investment, recipient management, and potentially refunds or re-dos.

The Clean-Up Bull Chaos: You turn a Variant Red bull out with a mixed color group during summer breeding. Come calving season, you can’t tell by looking which calves are carrying what. Now you need to genomically test the whole crop to sort replacements from sale animals—that’s $30-40 per head across your calf crop.

A $30 test looks pretty reasonable compared to any of those scenarios.

Where the Industry Is Heading

Here’s my read on where this is going: mandatory COPA/MC1R testing at registration isn’t a question of “if” for the elite tier—it’s a question of “when.” The economics and technology make it inevitable.

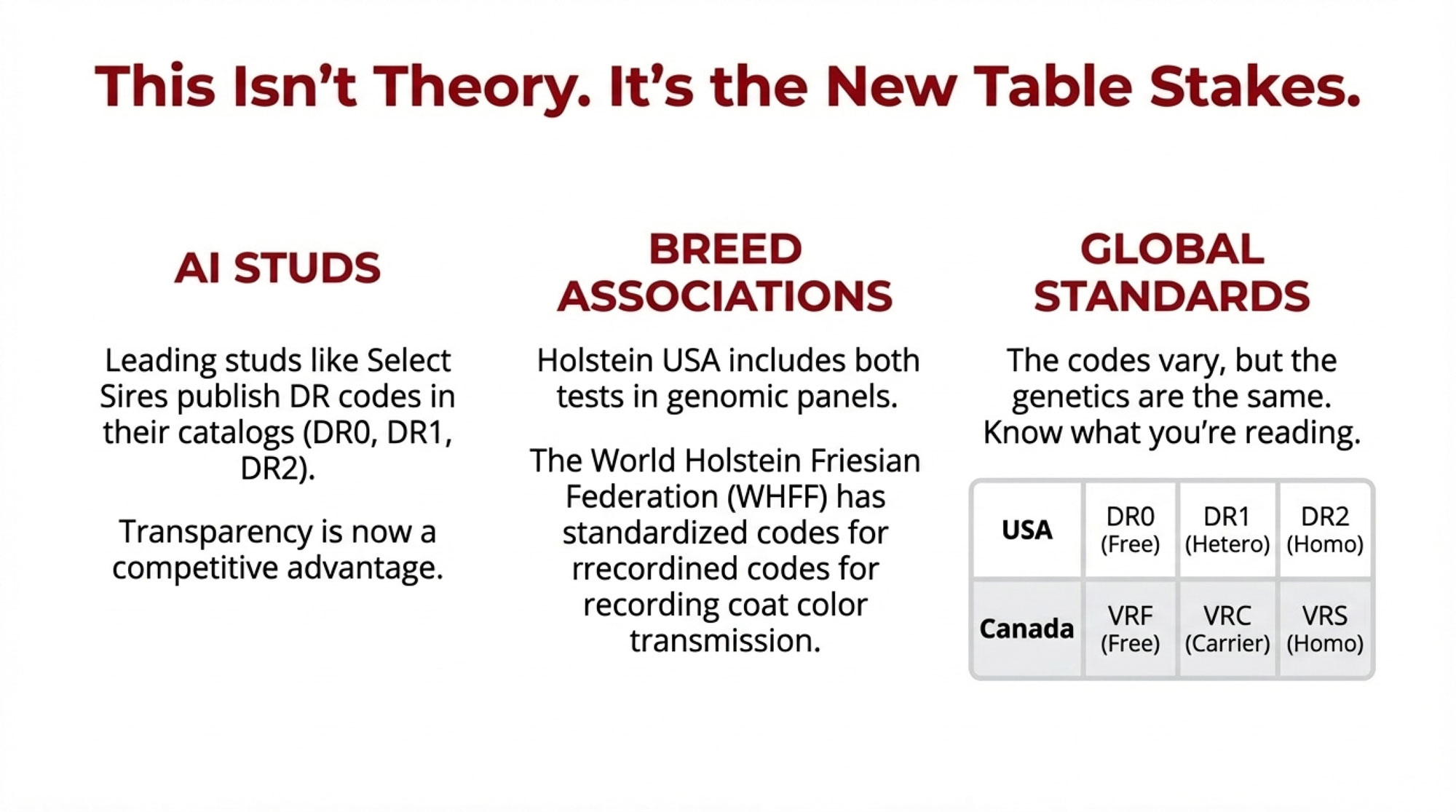

The AI studs are already there. Select Sires publishes DR codes in their catalogs and provides detailed mating guidance. Other major organizations are following suit with color genetics in their genomic offerings. The competitive pressure is real—if one stud provides complete color transparency and another doesn’t, breeders making premium decisions will choose clarity every time.

A note on codes: If you’re working across borders, be aware that the US and Canada use different labeling systems. In the US, Holstein Association USA and CDCB use DR0 (tested free), DR1 (heterozygous carrier), and DR2(homozygous Dominant Red). Holstein Canada uses VRF (free of Variant Red), VRC (carrier of Variant Red), and VRS (homozygous Variant Red). Same genetics, different shorthand—just make sure you’re reading the codes correctly for whichever system you’re working in.

The breed associations have built the infrastructure. WHFF registration guidelines already require member organizations to record coat color transmission and carrier status using standardized codes. Holstein Canada’s genetic trait coding system is in place. Holstein USA includes both recessive red and Dominant Red in their genomic panels. The recording framework exists—it’s just not universally enforced yet.

The holdouts make sense. For a 500-cow commercial dairy, shipping bull calves at a week old and selecting replacements purely on production and health? Color genetics are irrelevant. That’s a perfectly rational business decision, and mandatory testing across all registrations would be unnecessary friction for these operations.

But for seedstock operations, show herds, and anyone marketing genetics where color affects value? Testing both COPA and MC1R isn’t optional anymore. It’s table stakes.

The Verdict: Manage the Complexity You Create

So where does this leave you? Here’s my thinking:

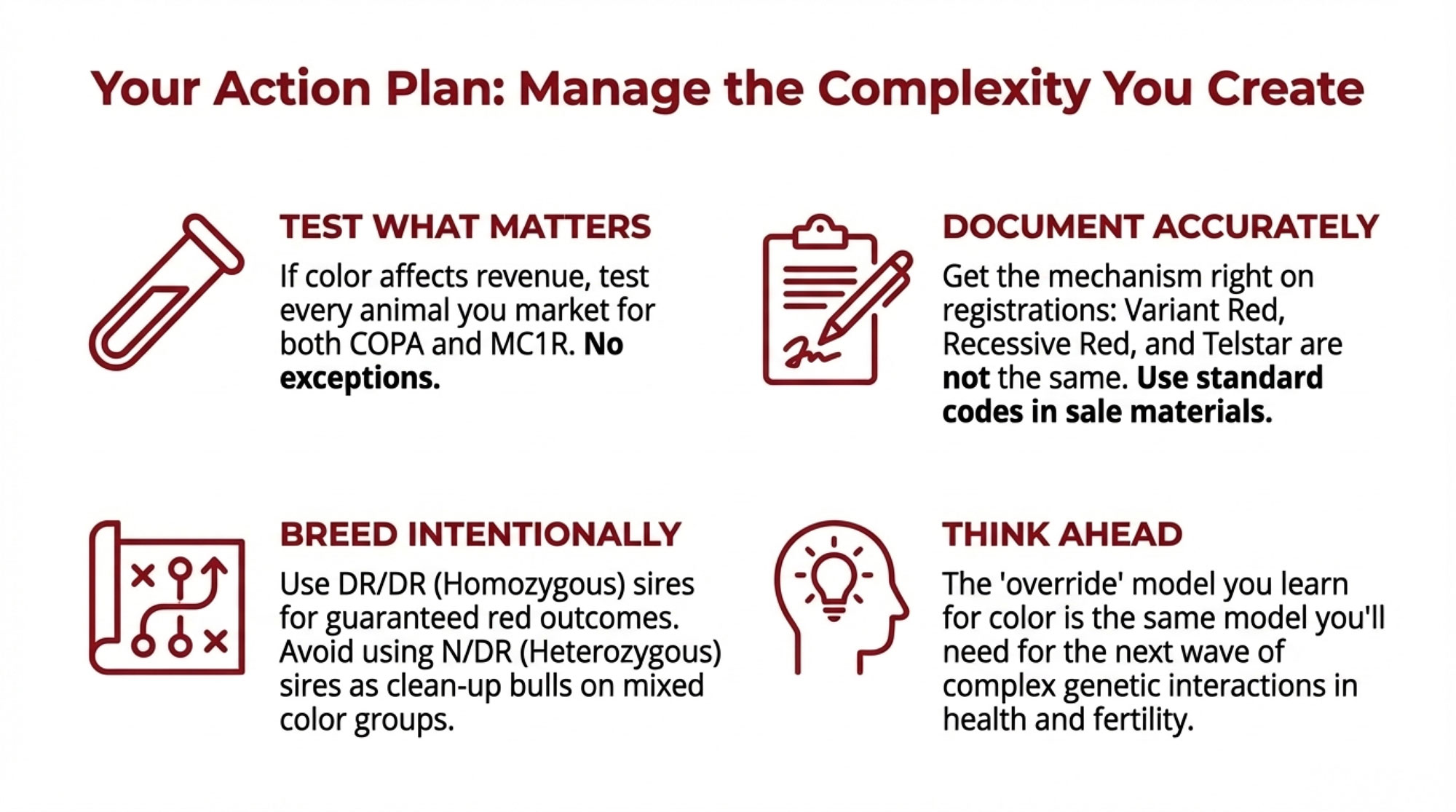

If color affects your revenue, test every animal you plan to market as breeding stock. Document the COPA and MC1R status in your sale materials. Use breed-standard codes so the information travels cleanly when animals change hands.

If you’re breeding for red: Understand that N/DR sires will throw ~50% black calves even on red cows—provided the sire carries E^D at MC1R. If you need guaranteed red outcomes, use DR/DR sires. Plan accordingly.

If you’re managing clean-up bulls: Don’t use Variant Red bulls on mixed-color groups unless you’re prepared to test the resulting calves. The sorting headache isn’t worth it.

If you’re registering animals: Get the mechanism right. Variant Red, recessive red, and Telstar are three different things with different inheritance patterns. Mislabeling creates downstream problems for everyone.

If you think phenotype tells you enough: It doesn’t. A red calf at birth could be Variant Red (stays red, might darken slightly), recessive red (stays red), or Telstar (turns black in months). Only testing tells you which—and that distinction matters for every breeding decision that follows.

“Understand the genetics, test what matters for your operation, communicate clearly with buyers, and manage the complexity you’re creating.”

The COPA discovery didn’t complicate Holstein color genetics—it revealed the complexity that had always been there. We just couldn’t see it before. The breeders who adapt their programs to account for genetic networks, not just single-gene thinking, are the ones who’ll avoid expensive surprises.

And honestly, color is just the beginning. The same epistatic interactions—one pathway overriding another—show up in fertility, health, and efficiency traits. The mental model you build managing Variant Red is the same model you’ll need for the next layer of genetic complexity headed for your breeding program.

Test what matters. Document what you find. Plan accordingly. That approach will serve you well regardless of what genetic curveball comes next.

Key Takeaways

COPA is the override switch. An animal can carry black genetics at MC1R but still express red if COPA is present—traditional color rules don’t apply.

Red × Red can equal Black. Variant Red bulls throw ~50% black calves on red cows if they carry hidden black genetics underneath their red coat.

A $30 test prevents expensive mistakes. UC Davis VGL tests both COPA and MC1R; Holstein USA includes both in standard genomic panels.

Codes vary by country. The US uses DR0/DR1/DR2; Canada uses VRF/VRC/VRS. Same genetics, different shorthand—read them correctly.

Skip the test, accept the gamble. Registration errors, mislabeled sale animals, and buyer disputes cost far more than $30.

Executive Summary:

Red bull × red cow should equal red calf—except when it doesn’t. The COPA gene, discovered in 2015, acts as a genetic ‘override switch’ that supersedes traditional color inheritance. A Variant Red bull can throw 50% black calves even on red cows if he carries hidden black genetics underneath his red coat. That surprise leads to angry buyers, botched registrations, and breeding decisions built on wrong assumptions. The fix is simple: test both COPA and MC1R status. It runs about $30 through UC Davis VGL and comes standard with Holstein USA genomic panels. For seedstock operations and anyone marketing genetics where color affects value, skipping this test is a gamble you don’t need to take.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Plot twist: Dairy farms now produce more beef profit than beef ranches. $1,400/calf vs. their $800. The math is devastating.

EXECUTIVE SUMMARY: Dairy has stumbled into the opportunity of a generation: we’re producing 230 billion pounds of milk while simultaneously filling the void left by beef’s collapse to 1961 lows—effectively owning both markets. Three strategies are generating $600-770K in additional annual revenue for progressive operations: beef-on-dairy genetics transforming worthless bull calves into $1,400 assets; component optimization capturing $84,000 from butterfat premiums; and export positioning, as China and India desperately need our proteins. The proof is compelling—producers investing $70,000 are returning $200,000 in year one, with 60% efficiency. Here’s the urgency: only 28% have moved while premiums are maximum; by 2027, when adoption hits 70%, the window closes. Make no mistake—this isn’t about incremental improvement, it’s about who survives the next decade.

I was reviewing the November USDA reports, and something remarkable jumped out that deserves our attention. The latest WASDE data shows dairy production surging to 230 billion pounds, while beef production drops by 70 million pounds and pork production falls by 80 million pounds. What’s particularly noteworthy is how few producers have fully grasped the implications of this shift.

This development builds on what we’ve been seeing across the industry—not just another typical market cycle, but what appears to be a fundamental restructuring of North American protein production. Several economists I’ve spoken with are describing this as an 18-month window of genuine opportunity, and the more I analyze the data and talk with producers, the clearer the pattern becomes.

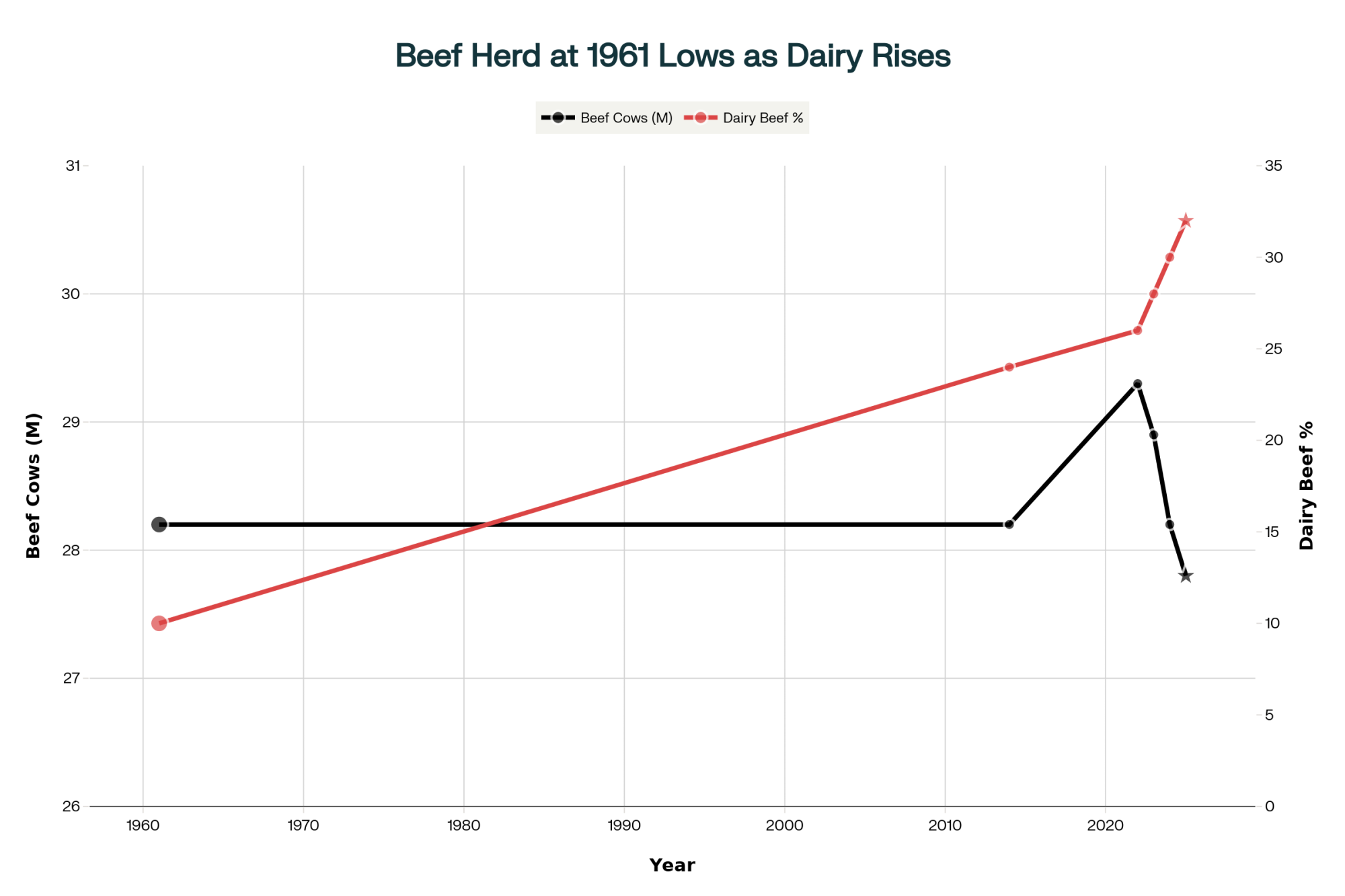

The consumption trends align with this narrative. USDA’s Economic Research Service shows Americans consuming record levels of dairy products, reaching historic highs that would have seemed impossible just five years ago. Globally, the milk protein market continues its substantial growth trajectory, with multiple analyses projecting sustained expansion through 2032. This coincides with the beef cow herd dropping to approximately 28 million head—USDA data confirms this represents the lowest level since the early 1960s.

In recent conversations with producers from various regions—Wisconsin cooperatives, California independents, Texas operations—those experiencing the most success share a common trait: they’re adapting now, even if imperfectly, recognizing that this convergence of factors presents opportunities we haven’t encountered in decades.

Beef-on-dairy calf prices have surged from $225 to $1,439 in under three years—a 540% increase—while Holstein bull calves remain virtually worthless at $50. This $1,389 price gap represents the single largest profit opportunity in modern dairy history

The Beef-on-Dairy Revolution: From Liability to Asset

How Forward-Thinking Farms Discovered the Formula

Here’s what’s happening on farms across the country. Producers are telling me they used to essentially give away Holstein bull calves—some mentioned getting as little as five dollars for two calves just a few years back. Today, according to USDA Agricultural Marketing Service data this fall, those same genetics bred to carefully selected beef sires are commanding $1,200 to $1,400 each.

For perspective, a large dairy operation implementing this strategy could potentially generate $600,000 to $770,000 in additional annual revenue, depending on their size and execution. Same facilities, same management team, fundamentally different economics.

What’s particularly interesting—and this has been confirmed through discussions with extension specialists at both Cornell and Wisconsin—is how beef genetics on dairy has evolved beyond simple calf value. It’s reshaping our entire approach to genetic progress and herd optimization.

The Strategic Framework That Makes It Work

The most successful implementations I’ve observed, from California’s Central Valley to New York’s traditional dairy regions, share common elements that go well beyond basic crossbreeding.

Progressive producers are walking me through their approach: genomic testing of the entire herd at approximately forty dollars per animal, creating a precise roadmap of genetic potential. This allows targeted breeding decisions—sexed semen (at a fifteen to twenty-five dollar premium per breeding) on the top 40 to 50 percent of cows, while the remainder are bred to proven beef sires.

The sire companies report Angus and SimAngus dominating these selections, and for good reason—the calving ease and growth characteristics align well with dairy operations. University of Wisconsin research continues to validate this approach, showing consistent economic advantages.

The beef cow herd has crashed to 27.8 million head—matching 1961 levels—while dairy’s contribution to the beef supply has surged from 10% to 32%. Dairy isn’t supplementing beef production anymore; it’s becoming the backbone of the entire protein system

Current industry data indicates dairy contributes approximately 28 percent of the total U.S. calf crop, compared to roughly 24 percent in the mid-1990s. Given beef cow rebuilding timelines—typically five to six years minimum based on historical cattle cycles—this percentage could realistically reach 32 to 35 percent by 2027.

The math is brutal: as adoption rates surge from 28% today to 70% by 2027, beef-cross calf premiums will collapse from $1,400 to $800. Early movers capture maximum value; late adopters fight for scraps. The 18-month window isn’t marketing hype—it’s market mechanics

Component Optimization: The Hidden Value in Every Tank

Why Volume-Based Production Is Becoming Obsolete

Producers in California have been showing me compelling comparisons of their milk checks from 2023 versus the current year. The transformation in how milk is valued has been striking.

When Federal Order changes took effect this summer, the entire pricing dynamic shifted. California pricing announcements show butterfat reaching $2.62 per pound, making component optimization increasingly critical. The economics are straightforward yet powerful—every 0.1 percent increase in butterfat adds approximately thirty-five cents per hundredweight in additional revenue.

Component premiums reward precision nutrition: a 0.2% butterfat improvement from 4.1% to 4.3% delivers $61,320 in additional annual revenue for a mid-sized operation, with zero additional cows or facilities. It’s not glamorous, but it’s pure margin expansion

For a typical herd producing 24,000 pounds daily, improving from 4.1 to 4.3 percent butterfat could translate to roughly $84,000 in additional annual revenue under optimal conditions.

These aren’t just theoretical projections—producers are seeing real improvements in their milk checks.

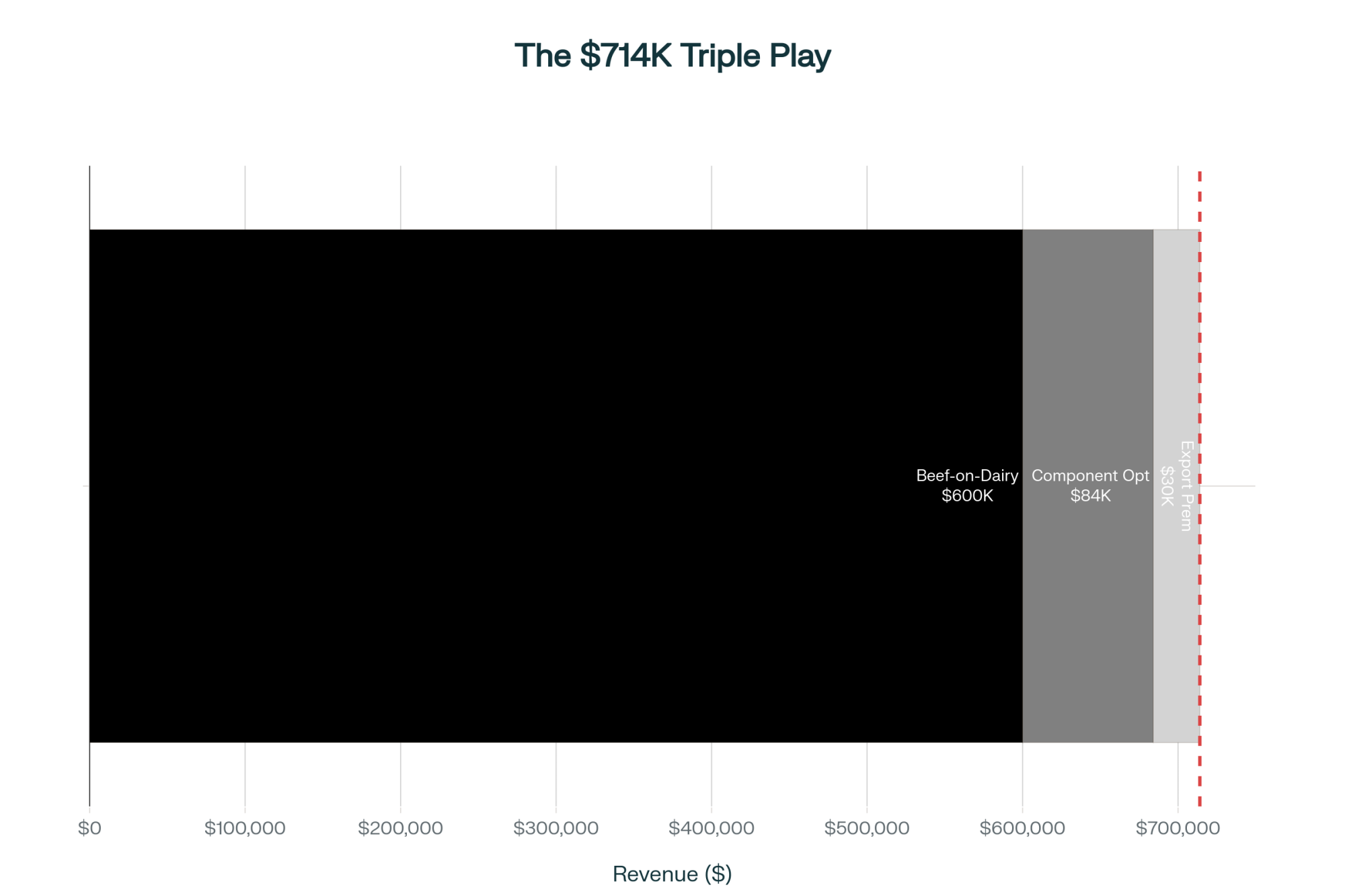

Progressive dairy operations are stacking three distinct revenue streams—beef-on-dairy genetics ($600K), butterfat optimization ($84K), and export premiums ($30K)—to generate over $714,000 in additional annual revenue without adding a single cow to the milking herd

The Genetic Revolution Driving Component Gains

The April genetic base change data from the Council on Dairy Cattle Breeding revealed something significant—a 45-pound rollback in butterfat Estimated Breeding Values, representing substantial industry-wide genetic progress.

During a recent genetics conference, specialists characterized this as unprecedented selection intensity for components. The practical impact? Producers selecting bulls with plus-50 pounds butterfat and plus-40 pounds protein are creating meaningful competitive advantages over operations using industry-average sires.

Nutritionists working with herds across Wisconsin are sharing their evolving approach: precise rumen pH management, maintaining a pH of 6.0 to 6.2 for optimal fat synthesis, and transitioning from generic bypass fats to targeted palmitic acid supplements at 200 to 250 grams per cow daily. University research from this past spring demonstrates that this can increase butterfat by 0.2 percent within 30 days—seemingly modest yet economically significant across an entire herd.

While the U.S. Trade Representative confirms 135 percent tariffs on many dairy products to China, the underlying trade dynamics tell a more nuanced story. USDA Foreign Agricultural Service data from this fall reveals interesting patterns in China’s import behavior.

According to trade data, imports of sweet whey powder have been growing significantly year over year, even as imports of commodity milk powder have declined. The driver appears to be specialized demand for swine feed ingredients and infant formula components rather than bulk commodities.

Producers shipping to export-oriented processors are reporting premiums of approximately forty cents per hundredweight for high-protein milk that yields better in whey extraction. For a mid-sized operation, that could translate to meaningful additional annual revenue—we’re talking potentially $25,000 to $30,000 for a 600-cow herd.

India’s Protein Crisis Opens New Channels

The opportunity in India may be even more significant, based on USDA attaché reports from New Delhi. Given that 70 to 80 percent of Indians do not meet daily protein requirements, according to the Medical Research Council, the government has launched a revised National Program for Dairy Development with substantial funding for fortification initiatives.

The tariff structure clearly reveals the opportunity. India applies approximately 30 to 60 percent tariffs on fluid milk and cheese imports, yet only around 8 percent on whey protein and 5 percent on lactose—reflecting limited domestic production capacity for these specialized ingredients.

European Market Dynamics

What’s also developing—and this hasn’t received much attention—is the European Union’s shifting protein strategy. With increasing pressure on their livestock sector from environmental regulations, industry reports suggest EU imports of specialized dairy proteins have been growing substantially since 2023. U.S. producers meeting specific sustainability metrics are finding opportunities for premium access to these markets.

The Operations at Risk: Recognizing Warning Signs

Who Faces the Greatest Challenges

We need to acknowledge candidly that not all operations are positioned to capture these opportunities. USDA’s Agricultural Resource Management Survey data from recent years indicates that operations with fewer than 200 cows face average production costs of around $20.93 per hundredweight, compared to $16.50 for operations with more than 1,000 cows.

Producers who’ve recently exited the industry have shared their experiences. When cooperatives announce infrastructure deductions—like the documented four-dollar-per-hundredweight case with Darigold in May—smaller operations can face thousands of dollars in additional monthly costs. For a 150-cow operation, that could mean over $7,000 in additional monthly expenses, creating immediate cash-flow challenges.

Studies suggest the majority of recent dairy exits have involved smaller operations with single-processor relationships and limited value-added strategies. While difficult to discuss, understanding these dynamics is essential for informed decision-making.

Regional Variations Matter

The strategies that succeed in Wisconsin may face challenges in Georgia—regional context matters tremendously. University of Florida dairy specialists have documented that Southeast operations often face production costs per hundredweight that are 2 to 3 dollars higher due to heat-stress management and feed procurement requirements.

Conversely, Texas Panhandle operations benefit from proximity advantages. Producers there report capturing an additional hundred to hundred-fifty dollars per calf on dairy-beef crosses compared to operations shipping longer distances, simply because of their location near multiple beef feedlots.

Technology Adoption Patterns

What’s interesting is how technology adoption varies by operation size. Research suggests operations between 500-1,000 cows often show strong adoption rates for genomic testing and precision feeding—they seem to hit a sweet spot of having adequate resources while maintaining operational flexibility.

Practical Implementation: Learning from Those Who’ve Done It

The Measured Approach That Works

Producers who’ve successfully transitioned share common timelines and approaches. They typically start with genomic testing—investing approximately $40-50 per animal for a comprehensive herd evaluation. This provides the genetic roadmap.

Within a few months, they’re implementing sexed semen on superior genetics. Then comes beef sire selection tailored to their facilities—calving ease often proves critical, especially in older barn configurations. By the following fall, they’re seeing the first beef-cross calves arriving.

“Year one, we captured perhaps 60 to 70 percent of the potential while learning the system. Even at that efficiency level, we generated substantial additional revenue on essentially unchanged feed costs.” — Minnesota dairy producer

Investment Reality Check

Based on producer experiences and consulting firm analyses, here’s the realistic investment framework:

Genomic testing: $40-50 per animal (one-time investment)

Sexed semen: $15-25 premium per breeding above conventional

Nutritionist consultation: $2,000-5,000 monthly, depending on service level

Component feed adjustments: Approximately $0.50 per cow daily

Data management software: $200-500 monthly for quality tracking systems

For a representative mid-sized operation, year-one implementation might total $60,000 to $80,000. However, combining beef-calf premiums with component improvements could potentially generate substantial additional revenue. While results vary, the fundamentals of economics generally favor well-managed operations.

Sustainability Considerations

What’s encouraging for long-term viability is how these strategies align with sustainability goals. The genetic improvements that reduce days to market for beef-cross calves can translate into lower lifetime emissions per pound of protein produced. Several processors are beginning to consider these metrics—something worth monitoring as carbon markets develop.

Looking Ahead: The Questions That Matter

Is This Sustainable or Another Bubble?

In discussions with agricultural economists and market analysts, the consensus suggests solid fundamentals underpin current conditions. Beef cow herd rebuilding faces structural constraints, with projections indicating a return to pre-drought inventory levels at the earliest in 2030. Global protein demand maintains 2 to 3 percent annual growth,according to FAO data—this reflects structural rather than cyclical factors.

However, appropriate caution is warranted. As beef-on-dairy adoption increases—already substantial in certain regions—some premium compression is likely. Markets are already seeing variation, with premiums ranging from $1,000 to $1,400 depending on genetics, location, and buyer relationships.

The indicator I’m monitoring most closely? USDA’s quarterly Cattle on Feed reports tracking dairy replacement heifer inventories, currently at approximately 1.88 million head—the lowest since the late 1970s, according to NASS data. Continued decline through 2026 would suggest structural transformation; recovery above 2.1 million might indicate temporary market dynamics.

What About Farmers Who Can’t or Won’t Change?

I’ve spoken with veteran producers approaching retirement who’ve made the conscious choice to maintain current practices rather than implementing new strategies. With paid-off operations and no succession plans, this approach has validity.

Industry observers suggest a significant portion of current operations may exit within the next decade, regardless of market conditions—due to demographic realities rather than economic failure. For these producers, operational stability may appropriately outweigh optimization opportunities.

Key Takeaways for Your Operation

After extensive data analysis, producer conversations, and expert consultation, several key insights emerge.

The opportunity window exists, but it continues to narrow. Early adopters captured the highest premiums with limited competition. Current implementers are seeing good returns, though not quite at early-adopter levels. By 2027, returns may normalize further, though they will remain profitable for efficient operations.

Geography influences profitability more than scale—surprising but documented. A strategically located, smaller dairy near beef infrastructure can perform well compared to larger operations that face logistical challenges. Understanding your regional advantages and constraints proves essential.

Processor relationships have evolved from customer-vendor to strategic partnerships. If your processor cannot articulate clear export strategies or component valuation methods, opportunities may remain unexploited. Business alignment now matters as much as traditional loyalty considerations.

Experience teaches that perfection often impedes progress. Producers achieving partial efficiency in year one while generating meaningful profits demonstrate that imperfect action often surpasses perfect planning.

Your Next Steps

Looking at actionable items for interested producers:

Request genomic testing information from your breed association or genetics provider—understanding costs and logistics is the first step

Schedule a conversation with your nutritionist about component optimization potential in your current ration

Contact your processor to understand their component pricing structure and export market positioning

Reach out to beef breed associations for information on dairy-appropriate sires and local calf buyer networks

Connect with producers who’ve already made transitions—their practical experience proves invaluable

As we consider the industry landscape this November, dairy isn’t declining—it’s transforming. Producers who recognize the shift from commodity milk production to strategic protein business models position themselves for success. Those awaiting return to historical norms may discover that “normal” has fundamentally changed.

The data supports action. Strategies have proven effective. Progressive neighbors are already implementing changes. The question has evolved from whether to adapt to how rapidly you can position your operation for emerging opportunities.

KEY TAKEAWAYS

The $1,400 Reality Check: Your Holstein bull calves are worth $1,400 to smart producers, $50 to you—the difference is three breeding decisions and genetics testing

Triple Revenue Stream, Same Cows: Beef-on-dairy ($600K) + butterfat optimization ($84K) + export premiums ($30K) = $700K+ additional annual revenue without adding a single cow

The 18-Month Countdown: Today, only 28% have adapted; when it hits 70% by 2027, premiums crash from $1,400 to $800—early movers win, others consolidate

Proven ROI Formula: Invest $70K (genetics + nutrition + consulting) → Return $200K year one, even at 60% efficiency—this isn’t theory, it’s what producers are doing now

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The $1,350 Replacement Advantage – Analyzes the critical heifer shortage driving replacement costs to over $3,000, providing specific breeding strategies to balance beef premiums against the rising cost of maintaining herd size in a shrinking inventory market.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Milk at $18. Butter at $1.50. But heifers at $3,200 tell the real story. The recovery’s already starting—if you know where to look.

EXECUTIVE SUMMARY: A Wisconsin dairy producer’s confession reveals the new reality: “I watch New Zealand milk production closer than my own bulk tank.” While traditional metrics show disaster—butter at $1.50, milk under $18, three forward signals are flashing a recovery 3-4 months out. Weekly dairy slaughter remains at historic lows (230k vs. 260k trigger) because $900-$1,600 crossbred calves are keeping farms afloat, breaking the normal correction cycle. Smart operators monitoring Global Dairy Trade auctions and $230/cwt cattle futures have already locked in $4.38 corn, gaining $1.20/cwt margin advantage over those waiting for Class III improvements. With heifer inventories at 40-year lows (3.914 million head), operations that went heavy on beef-on-dairy face a cruel irony: they survived the crash but can’t expand in recovery. The next 18 months won’t reward efficient production—they’ll reward those watching the right signals.

Last week, a Wisconsin producer told me something that stopped me in my tracks: “I’m watching New Zealand milk production closer than my own bulk tank readings.”

That conversation captures perfectly how dairy economics have shifted. And looking at Monday’s CME spot prices—butter hitting $1.50 a pound, lowest we’ve seen since early 2021—alongside December cattle futures losing nearly twenty bucks per hundredweight over the past couple weeks, you can see why traditional metrics aren’t telling the whole story anymore.

Here’s what’s interesting, folks… while everyone’s fixated on Class III and IV prices that essentially report yesterday’s news, there are actually three specific signals providing genuine forward-looking intelligence. I’ve been tracking these with producers across the country for the past year, and what I’ve found is that the patterns could determine which operations thrive during this transition period.

AT A GLANCE: Your Three Critical Market Signals

Three Forward Signals Dashboard provides dairy producers with actionable intelligence 90-120 days before traditional Class III prices signal recovery—those monitoring these indicators have already locked in $4.38 corn and gained $1.20/cwt margins over competitors waiting for conventional signals. This is Andrew’s edge: forward-looking data that beats reactive strategies.

📊 Signal #1: Weekly dairy cow slaughter exceeding prior year by 8-10% for three consecutive weeks 📈 Signal #2: GDT auctions showing 6-8% cumulative gains over four consecutive sales 📉 Signal #3: December cattle futures 30-day moving average crossing above 200-day at $230+/cwt

The Perfect Storm We’re Navigating Together