October’s $2.47 Class spread proved it: mid-size dairies must choose between commodity and premium now. The middle is gone.

Executive Summary: October 2025’s market data delivered a death sentence to fence-sitters: mid-size dairies (800-1,500 cows) must choose between commodity and premium pricing within 18 months, or risk ceasing to exist. The Class III-IV spread now penalizes operations that haven’t optimized for either protein or butterfat, while global markets are permanently split between simple ingredients (winning) and value-added products (losing). Small farms with fewer than 500 cows survive through premium specialization, while operations with more than 3,000 cows thrive on commodity efficiency. But the middle ground—profitable for three generations—is gone forever. Irish farmers are betting their futures on 2027’s regulatory consolidation. Chinese buyers are only interested in specialty proteins, and industrial customers will pay premiums for consistency over brand. You have 18-24 months to pick your lane: scale up, specialize, or sell out.

Here’s the thing that’s been keeping me up at night—and probably you, too, if you’re running 800 to 1,500 cows. The dairy market’s doing something we haven’t seen before. There’s this growing gap between New Zealand and European dairy prices that should close through normal trading, but it just… won’t. The October GDT auctions show Western European whole milk powder trading at significant premiums compared to New Zealand product for near-term contracts. This structural gap, seen across multiple products, confirms that the market bifurcation is deepening.

But you know what’s really caught my attention?

The gap isn’t just global anymore—it’s right here in our milk checks. October CME data shows a widening spread between Class III and Class IV futures that’s crushing operations heavy on butterfat. With butter prices facing significant pressure while cheese prices hold relatively steady, the Class IV value is reaching levels we haven’t seen in years. This component value crisis is the clearest signal yet that the old rules are broken.

What farmers are finding is that the comfortable middle ground—where most of us have operated successfully for decades—is vanishing faster than morning fog in July. And if you’re still making decisions based on what worked even two years ago, well, we need to talk.

The Value Paradox Nobody Saw Coming

| Operation Type | Butterfat % | Protein % | Class Pref | Revenue Impact ($/cwt) | Annual Impact (1000 cows) |

| BF-Focused (Jersey-Heavy) | 4.8% | 3.6% | Class IV | −$2.47 | −$180k |

| Protein-Focused (Holstein) | 3.6% | 3.2% | Class III | $0.00 | $0 |

| Balanced Components (Holstein) | 4.1% | 3.4% | Mixed | −$1.20 | −$87k |

Looking at September 2025 market reports from the EU Milk Market Observatory, something curious jumps out. European butter—you know, the premium stuff that’s supposed to command top dollar—has been taking a beating. Meanwhile, AMF (anhydrous milk fat), which is essentially melted and clarified butter, appears to be holding up better. Recent Global Dairy Trade data suggests AMF is actually outperforming butter in percentage terms. The simple, non-branded ingredient is holding value better than its consumer-facing counterpart. This is the Value Paradox playing out in real-time, right down to the component level.

Now, why would the simple product outperform the sophisticated one?

I was talking with a Wisconsin dairy producer last week who runs a larger operation in the central part of the state. He’d invested heavily in specialty cheese equipment a few years back, thinking he’d capture those artisan premiums. “Know what’s paying the bills now?” he asked me. “Straight cream to the bakery suppliers. No fancy packaging, no marketing story, just consistent butterfat at 40% minimum.”

Here’s the surprising part—whey powder, the stuff we literally paid to get rid of twenty years ago, now commands respectable prices in the protein market. Yet those beautiful aged cheddars that take skill, time, and capital to produce? They’re facing intense price pressure from all sides.

What’s encouraging, though, is that this shift creates opportunities for those who recognize it early. It’s making me rethink everything we thought we knew about value creation in the dairy industry.

Why Irish Farmers Are Expanding into a Glut

The production numbers coming out of Ireland lately seem counterintuitive. Recent data from their Central Statistics Office shows milk output climbing steadily through the summer months. Belgium’s showing similar patterns according to their agricultural statistics. All this while European butter inventories are already substantial. Industry reports from late summer suggest oversupply conditions in the European market, with stockpiles building to levels not seen since the intervention buying days.

You’d think these folks have lost their minds. But there’s a method to this apparent madness.

Ireland’s nitrate derogation—the rule that allows them to run higher stocking rates than standard EU regulations permit—expires at the end of this year. When that happens, industry observers from Teagasc estimate that significant production capacity could disappear. Some projections suggest up to 20% of current output might be affected. Belgium faces similar pressures from the EU’s Farm to Fork strategy, though their timeline stretches out a bit further.

So these farmers are expanding now? They’re not playing for today’s prices. They’re positioning for 2027 and beyond, when half their neighbors might be out of business.

A dairy farmer I met at a conference last spring—runs a mid-size operation in County Cork—put it this way: “We’re not thinking about next year’s milk check. We’re thinking about who’s still standing in five years and what market share they’ll control.”

It’s a high-stakes bet on regulatory-driven consolidation. Risky? Absolutely. But, when you understand the regulatory chess game being played, it starts to make strategic sense.

The Chinese Market That Defies Logic

This is where things get genuinely puzzling, especially if you’re used to thinking about dairy as a straightforward commodity.

Recent reports from China’s agricultural authorities indicate that domestic farmgate prices remain under pressure, generally declining year over year, depending on the province. They have adequate production capacity, according to their own data. Traditional economics suggests that imports should be declining.

Instead? Recent customs data suggests import volumes are holding steady or even growing for certain categories. The unexpected piece is the shift in what they’re buying. While whole milk powder imports have moderated, specialty ingredients, such as whey products, appear to be growing. This shift from buying bulk commodities to high-value protein ingredients reinforces the idea that their purchasing is becoming highly selective, focused on functional and premium status, not basic commodity volume.

What’s happening here—and this pattern is also showing up in India, Vietnam, and Indonesia, according to recent observations from the USDA Foreign Agricultural Service—is that consumers in these markets don’t view domestic and imported dairy as the same thing. It’s no longer about measurable quality differences. We’re talking about perception, trust, and increasingly, social status.

An industry contact who works with Asian markets explained it to me this way: “Customers there aren’t comparing prices between domestic and imported milk. To them, it’s like comparing a Corolla to a Lexus. Both get you where you’re going, but they serve completely different needs.”

We’re starting to see this same split here in mature markets. Look at what organic commands—often substantial premiums according to USDA Agricultural Marketing Service data, despite conventional milk meeting all the same safety and nutritional standards. Or A2 milk, grass-fed brands, local farm labels. The bifurcation’s happening everywhere.

Industrial Buyers Play a Different Game

What catches my attention in all this market analysis is how differently industrial buyers behave compared to grocery chains.

When Kroger or Walmart needs butter, they typically put it out to bid quarterly and accept the lowest price that meets the specifications. Simple transaction, price drives everything.

But when a commercial bakery needs AMF for their croissant line? Completely different conversation. Their ovens are calibrated for specific melt points. Their recipes assume consistent moisture content—we’re talking plus or minus half a percent. Switching suppliers means reformulation, line testing, and potential product recalls if something’s off.

Industry procurement specialists I’ve talked with say they’ll routinely pay meaningful premiums just for supply security. One mentioned that every supplier switch costs them tens of thousands of dollars in testing and adjustments, sometimes more if the equipment needs recalibration. So yeah, they’ll pay extra for consistency.

This creates real opportunities for producers who can reliably meet industrial specifications. It’s not glamorous work—nobody’s writing magazine articles about your commodity ingredient sales. But, these contracts often offer better margins and more stability than chasing consumer trends.

Hard Lessons from the Big Cooperatives

Want to understand why those regional price advantages everyone talks about aren’t as permanent as they seem? Take a look at what has been happening with major cooperatives over the past eighteen months.

Even the big players—organizations with decades of export experience, established supply chains, unified farmer bases—have been announcing restructuring plans. Cost cutting initiatives. Plant consolidations. Some are even outsourcing core functions they’ve handled internally for generations.

What happened? Simple—they built cost structures around market conditions they assumed were permanent. Those nice premiums they were capturing a couple of years ago? Turned out to be temporary benefits resulting from supply chain disruptions and unusual demand patterns. When global shipping rates normalized and consumption patterns shifted back, the premiums vanished almost overnight.

A board member from a regional cooperative shared this perspective with me recently: “We all got a little too comfortable with those margins. Built our strategic plans around them. What we’re learning—again—is that very few advantages in commodity markets last more than a cycle or two.”

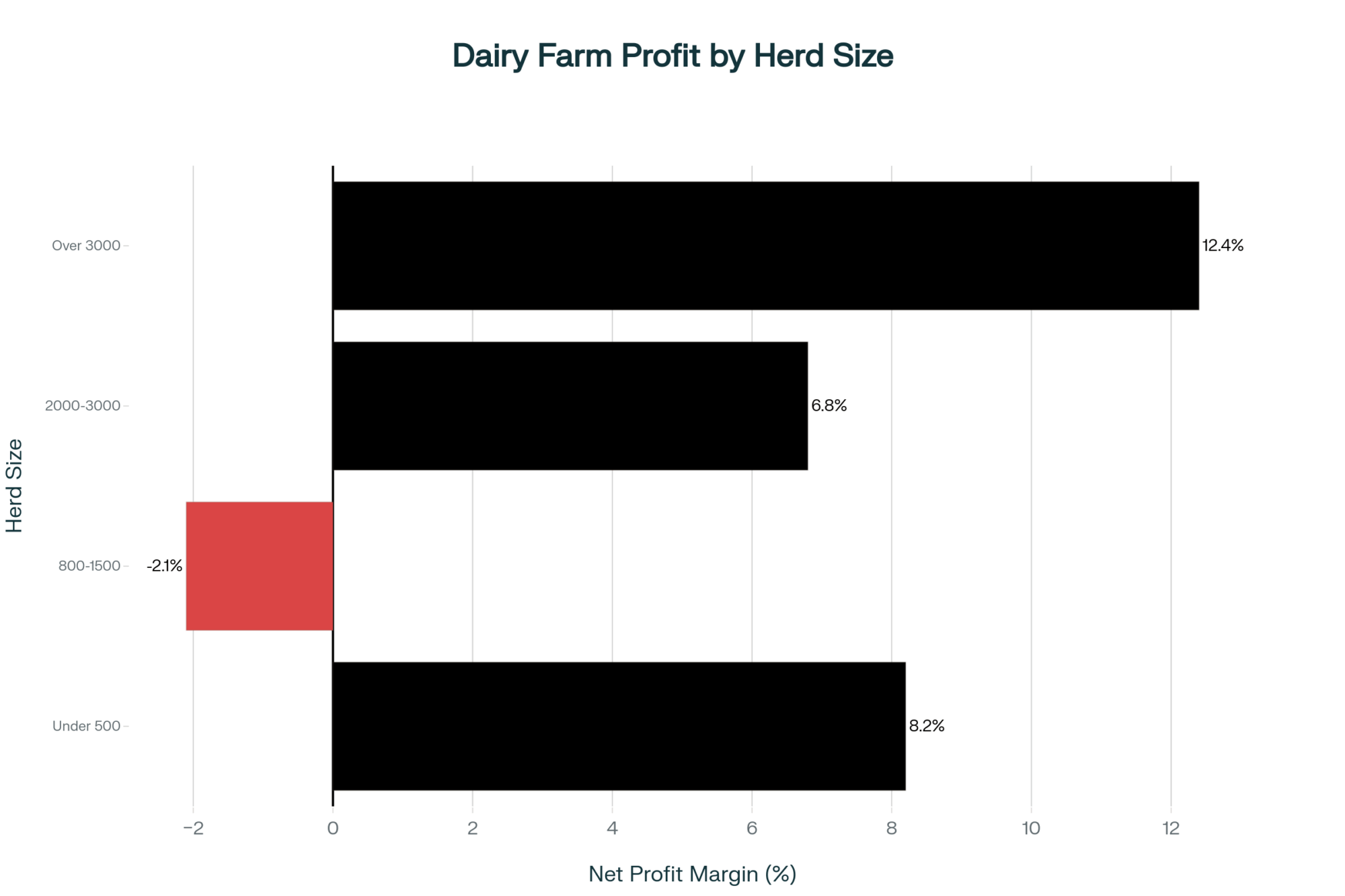

The Reality Check for Different Size Operations

Let me share what recent economic analyses from various land grant universities are telling us about profitability by herd size. The patterns are striking and, frankly, a bit concerning for those of us in the middle.

Smaller operations—let’s say under 500 cows—often achieve higher mailbox prices than the big guys. We’re talking sometimes a dollar fifty to two dollars more per hundredweight through direct marketing, on-farm processing, specialty programs. Sounds great, right?

But here’s the catch—their cost of production typically runs several dollars higher per hundredweight, too, according to extension studies. So that premium price? It’s often not enough to offset the higher costs. Many of these smaller operations are working incredibly hard just to break even.

On the flip side, operations over 3,000 cows generally receive lower prices—maybe fifty cents to a dollar below the smaller farms. But their cost structure? They’re often producing for significantly less per hundredweight than mid-size operations. Volume multiplied by even small margins adds up.

The really tough spot? That 800 to 1,500 cow range. Not big enough to capture serious economies of scale. Not small enough to be nimble with specialty markets. These operations are either expanding aggressively right now or transitioning to some form of differentiated production. Standing still is no longer viable.

Here’s what I’ve noticed about how different regions are handling this—and it’s telling. In California’s Central Valley, where water rights and environmental regulations create unique pressures, several mid-size operations have formed marketing cooperatives to achieve scale without individual expansion. Northeast producers, located near major population centers, are exploring the benefits of shared processing facilities and distribution networks. Down in Texas and New Mexico, where expansion’s still possible, they’re going big—really big—with new facilities starting at a minimum of 5,000 head. And in the Southeast? They’re dealing with heat stress and hurricane risks that add another layer to these strategic decisions. Each region’s finding its own path through this transition.

Choosing Your Lane (Because You Have To)

After watching hundreds of operations navigate these changes, it’s becoming increasingly clear: you must pick a strategy and commit to it fully. The days of hedging your bets, of being pretty good at everything? Those days are over.

If you’re going the commodity route, several factors become absolutely critical. First, you need scale—probably a minimum of 2,000 cows in the Midwest, based on recent farm management analyses, and more like 3,500 in the West, where you’re competing with those massive operations. Second, you need industrial customers who value consistency over brand. Third, you must accept that you’re selling ingredients, not food, and optimize your approach accordingly.

If you’re choosing the differentiated path, different rules apply. You need a story that resonates—organic certification, grass-fed verification, local processing, something authentic that consumers will pay for. You need direct relationships or processors who value what makes you different. You have to accept higher costs, likely several dollars more per hundredweight, based on various enterprise budgets, in exchange for capturing those premiums.

Are the operations struggling the most? Those trying to do both. I am aware of a Pennsylvania dairy that has installed robots to reduce labor costs, yet it still sells commodity milk. Their debt service alone is crushing them. Another farm in Vermont has built a beautiful processing facility, but cannot achieve enough consistent volume to run it efficiently.

And here’s something worth considering—how does your chosen path affect succession planning? If you’re hoping the next generation takes over, which strategy gives them the best shot at success? The commodity route requires constant reinvestment and scale. The premium path needs marketing savvy and customer relationships. Neither’s wrong, but they require different skills and interests from whoever’s taking the reins.

Practical Decisions for Today’s Reality

So what does this mean for your operation over the next few years?

For smaller dairies with fewer than 500 cows, specialization appears to be the key. Pick something you can be genuinely excellent at. Perhaps it’s organic production, perhaps it’s A2 genetics, or perhaps it’s on-farm bottling with local distribution. But competing head-to-head with large commodity operations? The math rarely works.

For larger operations over 2,000 cows, it’s about operational excellence and simplification. Strip out complexity, focus on one or two products at most, and secure those industrial contracts. The 3,000-cow dairy selling everything to a single cheese plant at predetermined prices might not be exciting, but they’re sleeping well at night.

And if you’re in that challenging middle zone—800 to 1,500 cows? You’re facing the toughest decisions. Based on what extension economists are seeing, you’ve probably got 18-24 months to make a strategic choice. Scale up significantly, find a genuine differentiation strategy, or… well, we all know what the third option looks like.

Here’s what’s worth tracking closely in your own operation:

- What’s your actual premium above base price? Many folks are surprised by how small it really is

- What percentage of your milk is under contract versus sold on the spot market? Aim for at least 70% contracted

- Where do your costs rank compared to others in your region? You need to be in the better half

- Could your operation survive a 15% price drop for six months? If not, you’re probably over-leveraged for this environment

- Are you optimized for protein or fat? Recent market shifts show component strategy is no longer optional—it’s essential for survival

Examining government programs reveals some resources worth exploring. USDA’s Value-Added Producer Grants can help with the transition to specialty markets. Environmental Quality Incentives Program funding may offset some of the costs of organic transition. State-level programs vary widely—Minnesota, Wisconsin, and Vermont all offer different types of support for dairy operations making strategic transitions.

The Transition Nobody Talks About

What often gets overlooked in these strategic discussions is the cost and complexity of transitioning from one model to another.

Going organic? That’s a three-year transition period during which you’re paying organic feed prices but receiving conventional milk prices. Extension studies suggest that transition costs can run into the hundreds of dollars per cow, plus you need secured market access before you start.

Scaling up to commodity efficiency? We’re talking millions in capital investment for meaningful expansion based on recent construction trends, and that’s if you can find the labor. Speaking of labor—good luck finding qualified people right now. Everyone’s struggling with that.

Even switching to industrial supply contracts requires investment. Those customers want consistency, which might mean new bulk tanks, different cooling systems, and sometimes even road improvements for larger tankers.

The encouraging development I’m seeing is that some regions are finding creative alternatives. In areas where individual expansion faces regulatory hurdles, several mid-sized operations have formed marketing cooperatives to achieve scale without relying on individual growth. Others are exploring shared processing facilities—not perfect, but it spreads the capital risk. Some operations are creating strategic alliances, sharing equipment and expertise while maintaining independent ownership.

Looking Forward

Those pricing gaps we’re seeing between regions and products? They’ll moderate eventually—markets always find some form of equilibrium. But, the fundamental split in our industry—between high-volume commodity production and high-touch premium production—is looking more and more permanent, according to the agricultural economists I’ve spoken with.

Previous generations could successfully run diversified operations. My grandfather milked cows, raised hogs, grew corn and beans, and did pretty well at all of it. My father’s generation was competent across multiple enterprises and made it work.

Today? Today, rewards focus and excellence in a chosen strategy. The market’s sending clear signals through these pricing disparities and structural changes. We can either listen and adapt or ignore them at our peril.

The successful operations ten years from now won’t necessarily be the biggest or the most sophisticated. They’ll be the ones that made clear strategic choices today and committed fully to optimizing within that framework.

The most vulnerable position isn’t being too aggressive or too conservative—it’s being unclear about which game you’re playing. Pick your lane, optimize everything for that choice, and don’t look back.

Because in today’s dairy economy, the middle of the road is becoming the hardest place to survive. That’s where the pressure’s greatest, the margins thinnest, and the future most uncertain.

But, here’s what gives me hope: dairy farmers are among the most resilient and adaptable people I know. We’ve weathered worse storms than this. The ones who recognize these changes early, make tough decisions, and commit to their chosen path? They’ll not just survive—they’ll thrive.

The question isn’t whether the industry will continue; it’s whether it will thrive. It’s whether your operation will be part of its future. And that decision? That’s entirely in your hands.

Key Takeaways:

- Pick Your Lane in 18 Months or Perish: Operations with 800-1,500 cows must commit fully—scale to 2,000+ for commodity efficiency, specialize for premium capture, or exit. Half-measures guarantee failure.

- Simple Ingredients Trump Value-Added: AMF beats butter, whey beats aged cheese, and industrial contracts beat consumer brands. October’s market proves processors pay premiums for consistency, not stories.

- The Middle Is a Kill Zone: Farms under 500 cows thrive on specialization ($1.50-2.00/cwt premiums), operations over 3,000 profit on scale. But 800-1,500? Neither advantage = both disadvantages.

- Component Strategy Is Survival: The Class III-IV spread isn’t temporary—it’s structural. Optimize for protein OR fat, not both. Your bulk tank average means nothing if components are wrong.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Why Are Class III Milk Prices So Low? Causes, Consequences, and Solutions – This article provides the deep component analysis necessary for the “optimized for protein or fat” ultimatum. It dissects the outdated USDA Class III formula and reveals why protein prices are plummeting despite high butterfat values, providing strategies to enhance milk solids.

- AI and Precision Tech: What’s Actually Changing the Game for Dairy Farms in 2025? – Essential for choosing the scale-up path, this article details the tangible ROI metrics for technology adoption. Learn how precision feeding delivers 15-25% feed savings and how health monitoring generates up to $500/cow savings, critical for tightening commodity margins.

- The €1 Billion Strategy That’s Splitting Dairy into Premium Players and Price-Takers – This tactical guide provides the blueprint for mid-size survival, detailing how cooperative arrangements can reduce capital exposure by 60-80%. It delivers size-specific ROI timelines for robotics and automation, proving cooperation is a feasible path to scale.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.