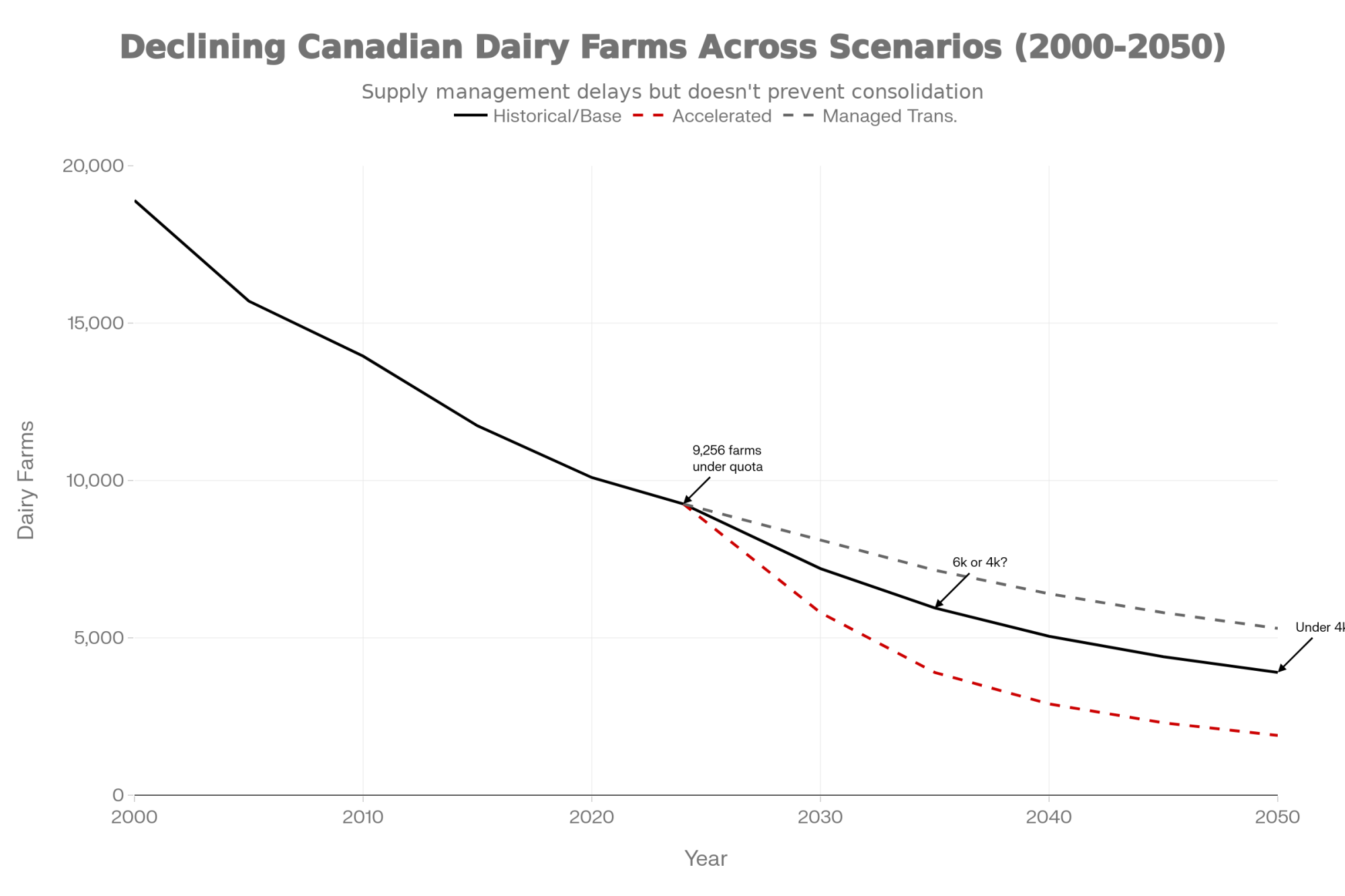

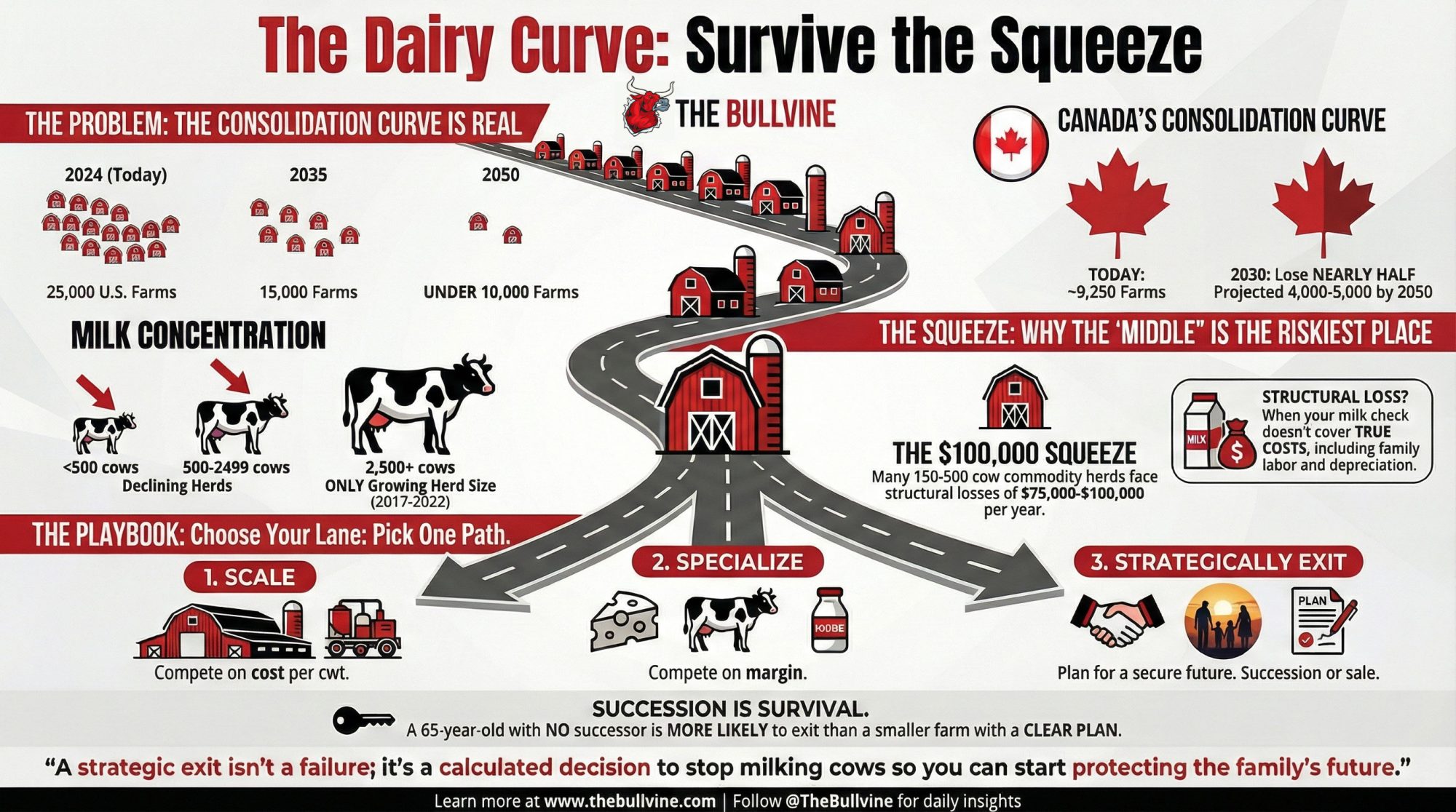

15,000 dairies by 2035. Under 10,000 by 2050. The Bullvine Dairy Curve shows exactly who survives that curve—and who gets priced out.

By 2035, roughly 15,000–16,000 U.S. dairies will be doing the work that nearly 30,000 did a generation ago—and the line between 5,000 and 15,000 herds by 2050 is being drawn right now in cost structure, technology, and succession decisions. What’s interesting is that you don’t have to buy into worst‑case doom to see it; you just have to follow the numbers we already have.

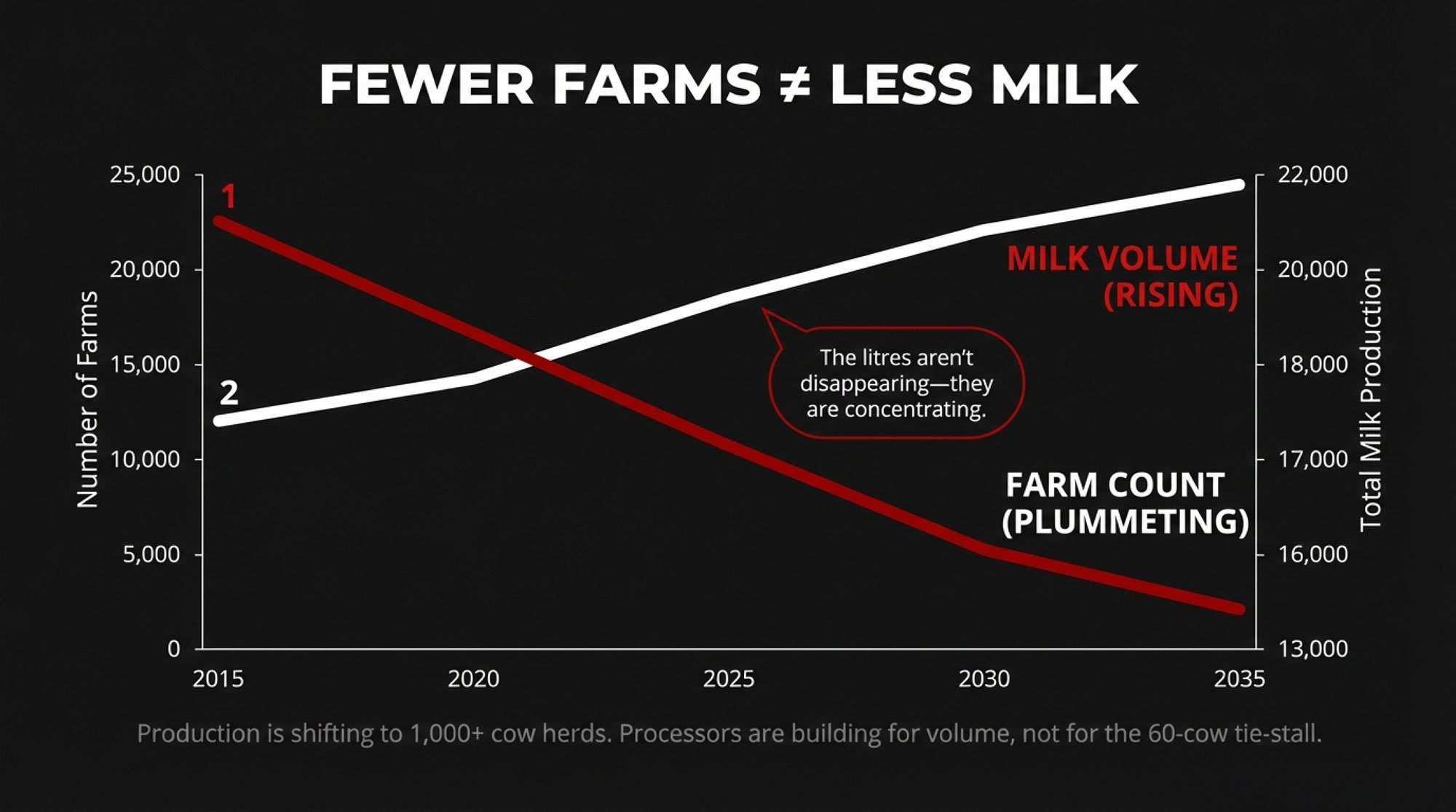

Almost 40% of U.S. dairies disappeared between the 2017 and 2022 Census of Agriculture, even as total milk output increased, and Canadian Agriculture and Agri‑Food Canada (AAFC) data show a similar “fewer farms, more milk” trend under supply management. Using those official data as the foundation, the Bullvine Dairy Curve points to three structural paths:

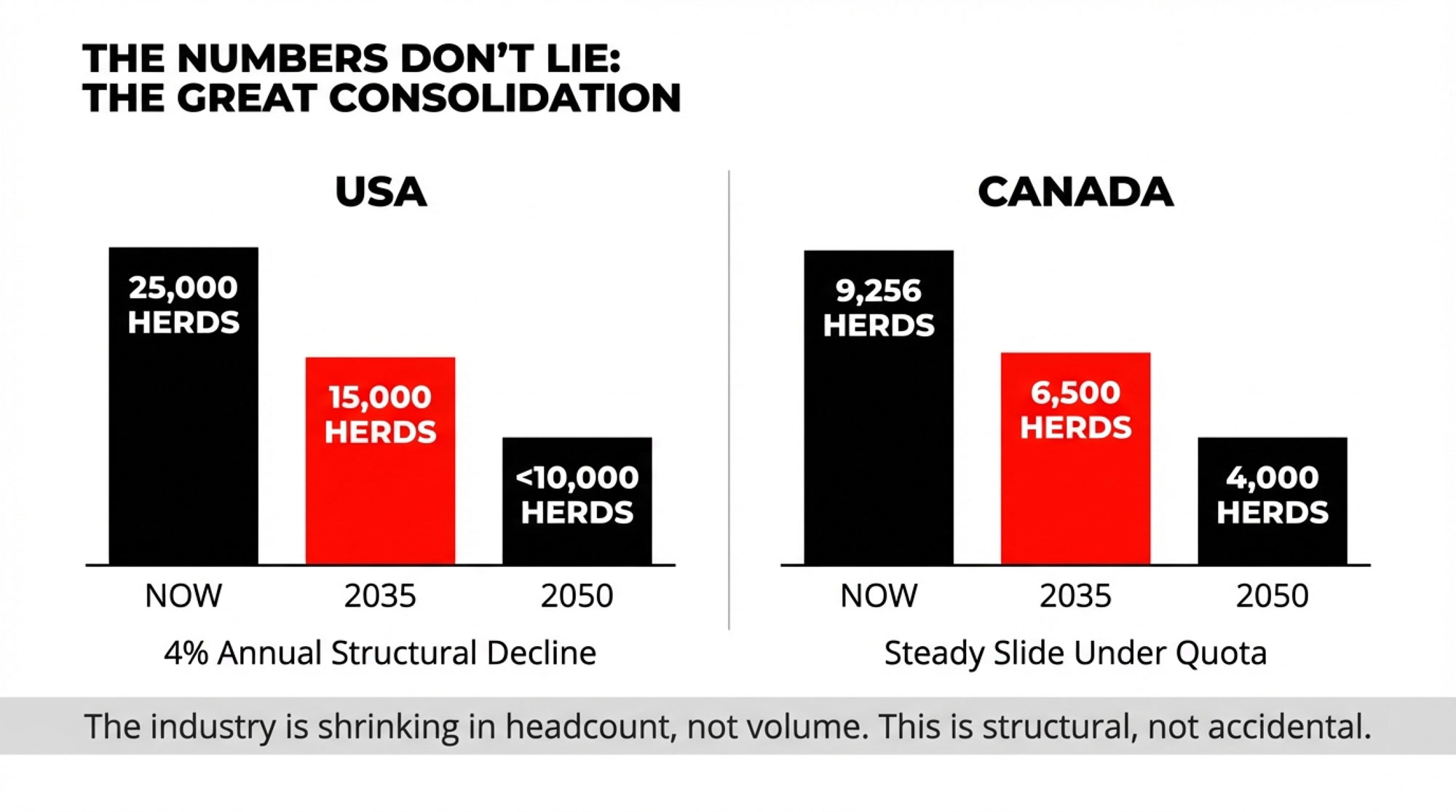

A business‑as‑usual path where U.S. herd numbers decline around 4% per year and land in the 15,000–16,000 range by 2035 and well under 10,000—typically 8,000–9,000—by 2050; Canada tracks toward 6,500–7,000 by 2035 and 4,000–5,000 by 2050 under quota.

A faster consolidation path where tighter labour, higher compliance costs, and alternative products push U.S. farms closer to 5,000 herds and Canadian herds into the 3,500–4,000 range by 2050.

A managed transition path where better use of margin tools, disciplined capital decisions, and deliberate succession planning slow effective exit rates, keeping the U.S. closer to 15,000 herds and Canada around 6,500 by mid‑century.

Path

U.S. Herds 2035

U.S. Herds 2050

Canada Herds 2035

Canada Herds 2050

Key Drivers

Business-as-usual

15,000–16,000

8,000–9,000

6,500–7,000

4,000–5,000

~4% U.S. decline, 2–3% Canada under quota

Faster consolidation

~12,000

~5,000

~5,500

3,500–4,000

Labour, compliance, alt products, weak margins

Managed transition

~15,000

~15,000

~6,500

~6,500

Margin tools, disciplined capex, succession

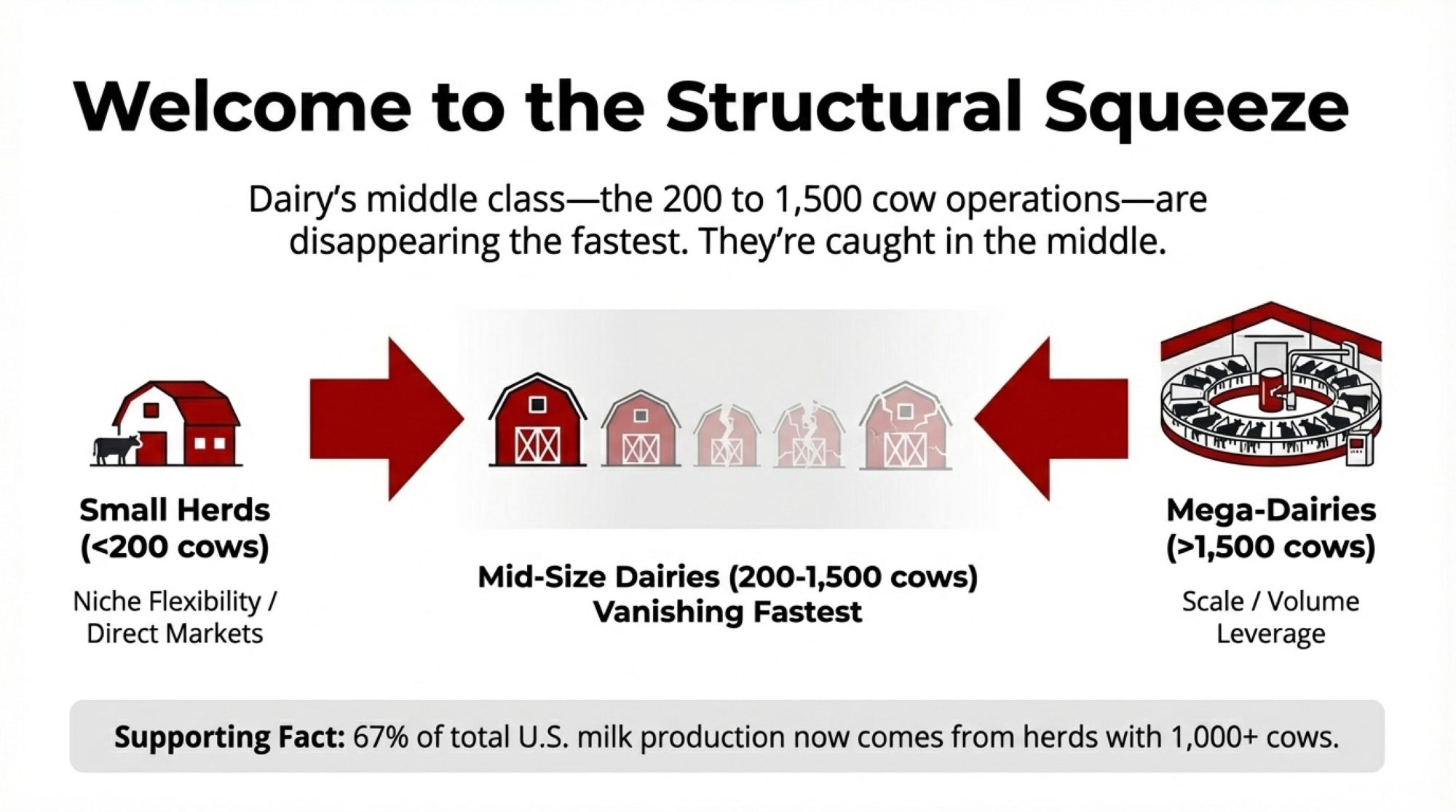

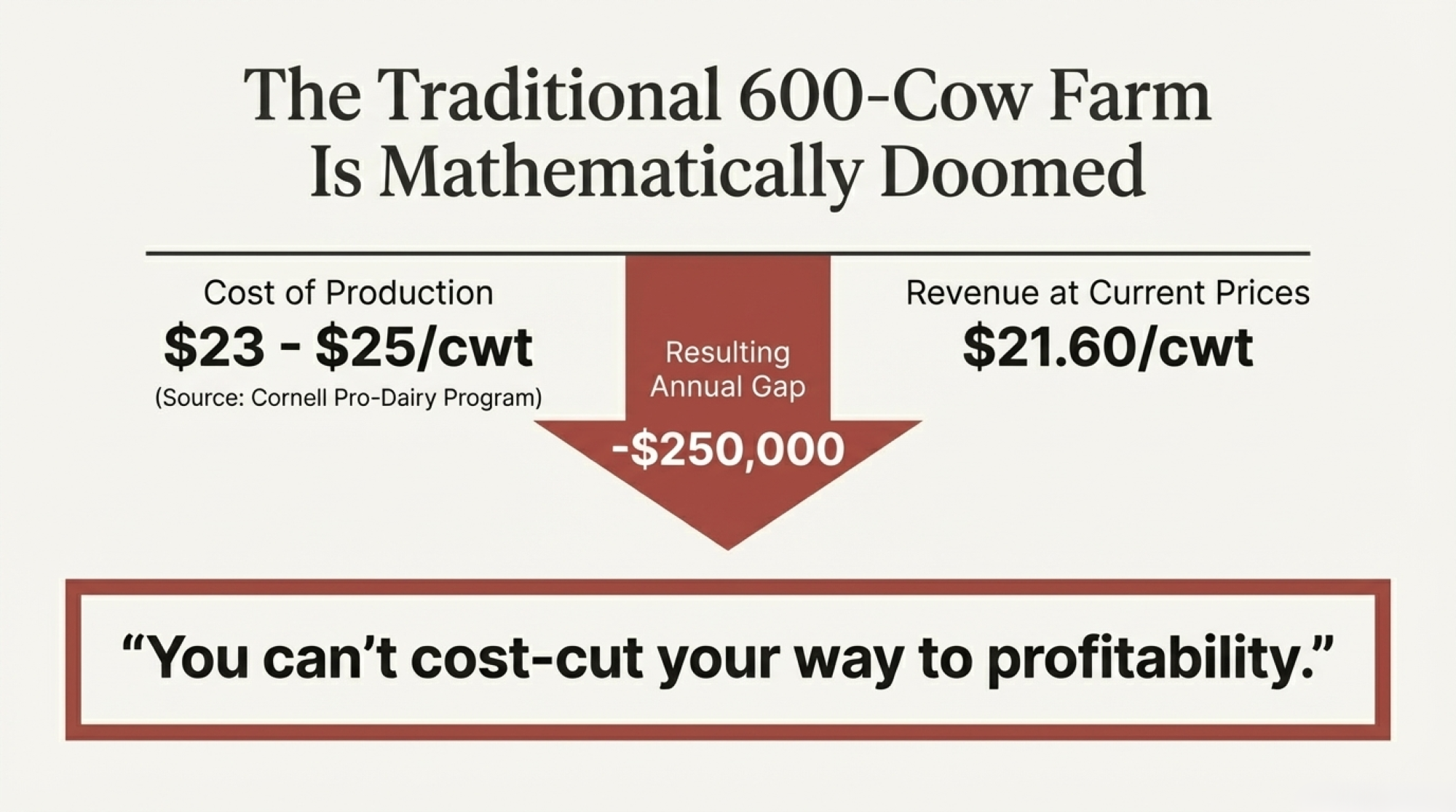

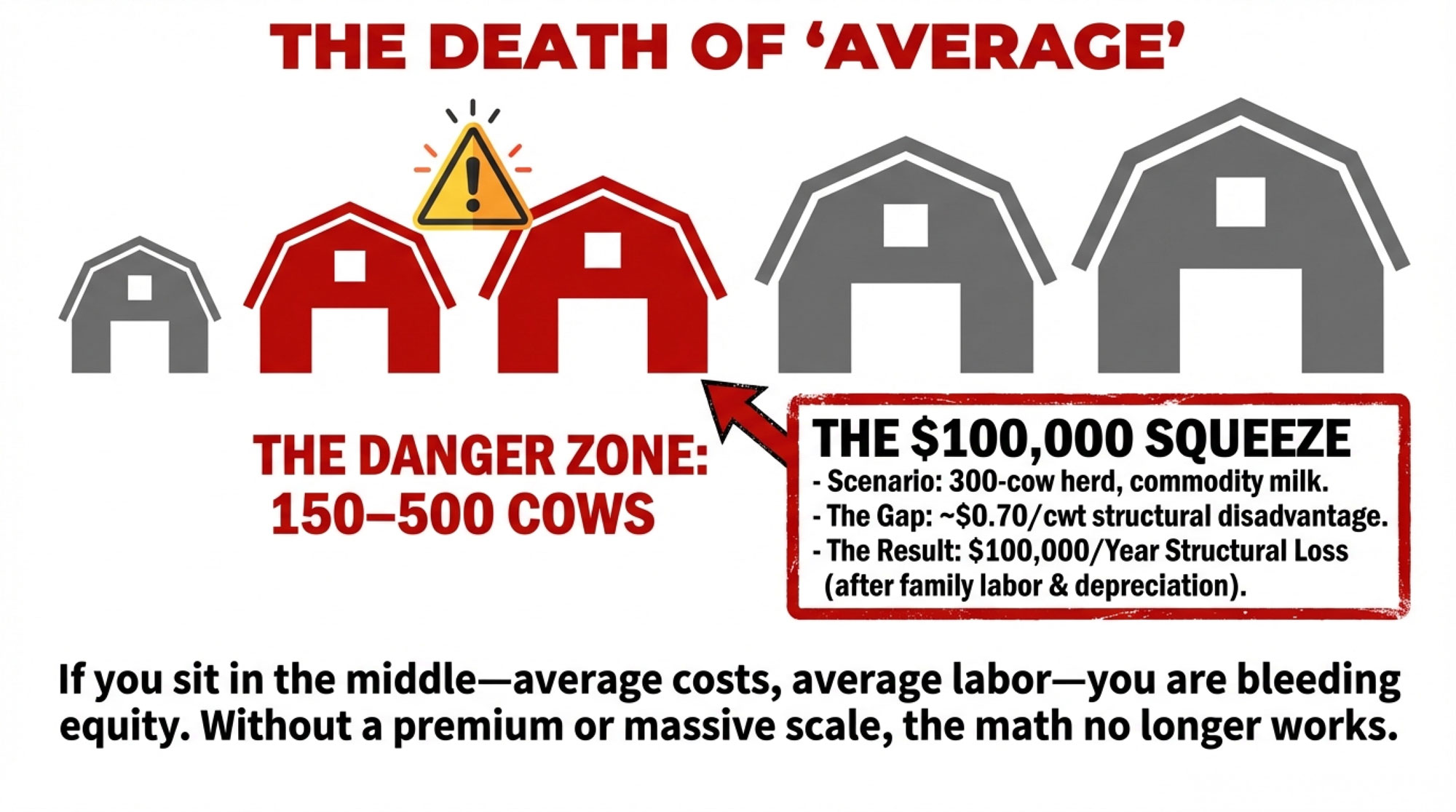

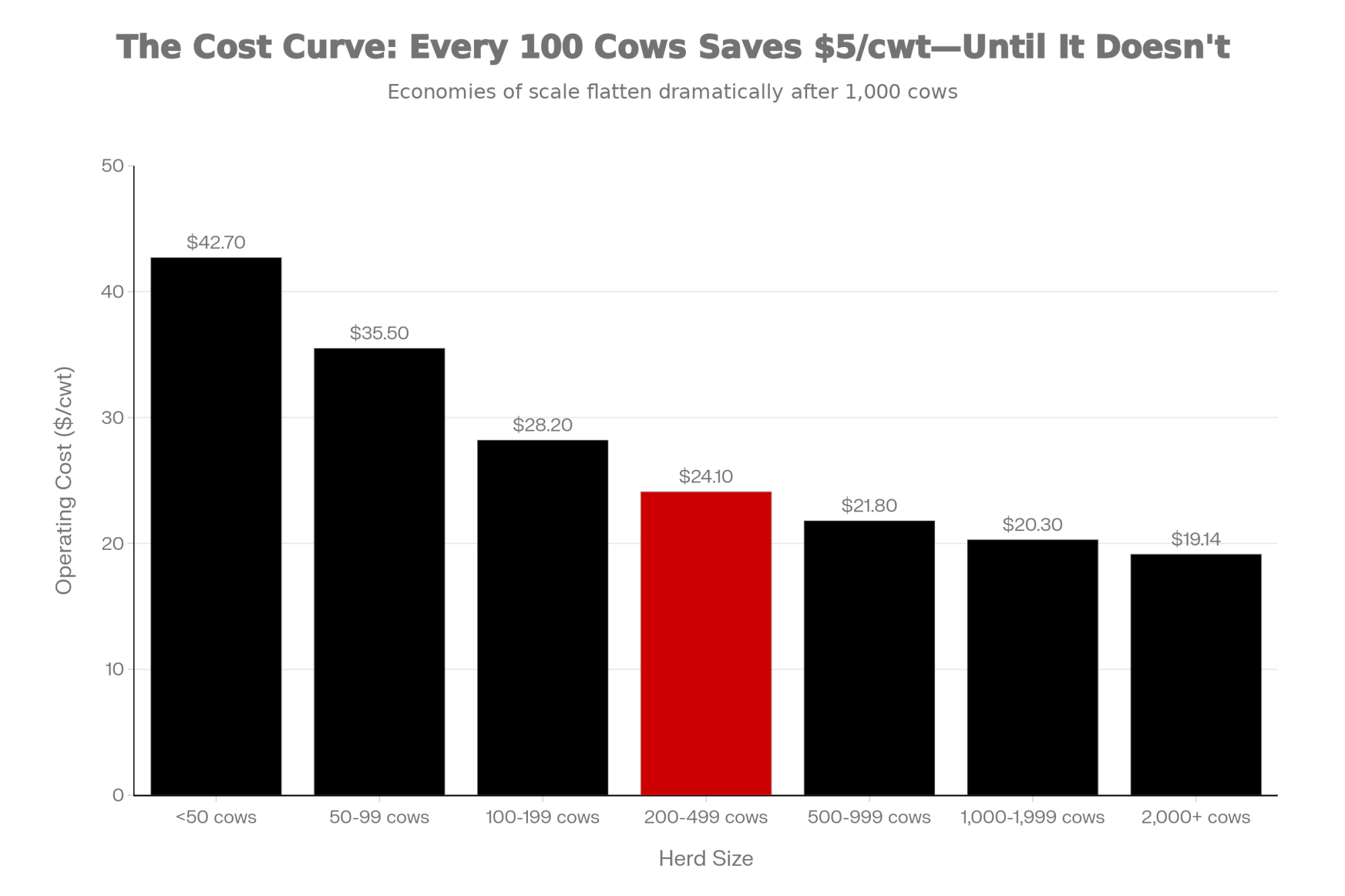

In all three paths, the litres don’t disappear—they concentrate. The largest freestall and dry‑lot systems steadily capture a larger share of the milk pool as economies of scale and processor preferences reward low‑cost, high‑volume suppliers. In that world, 150–500 cow herds that sit “average” on cost and are fully exposed to commodity pricing are often bleeding $75,000–$100,000 per year in structural losses once full labour and capital costs are factored in. That forces a three‑way choice: scale toward 1,000+ cows, pivot into premium/value‑add markets, or cash out while equity is still intact.

The rest of this article lays out the Bullvine Curve in plain language: what the official numbers say, how Bullvine’s forecasts connect the dots out to 2035 and 2050, and a barn‑level playbook to decide whether your operation is building to survive that structure—or quietly betting against it.

Where we’re actually standing today

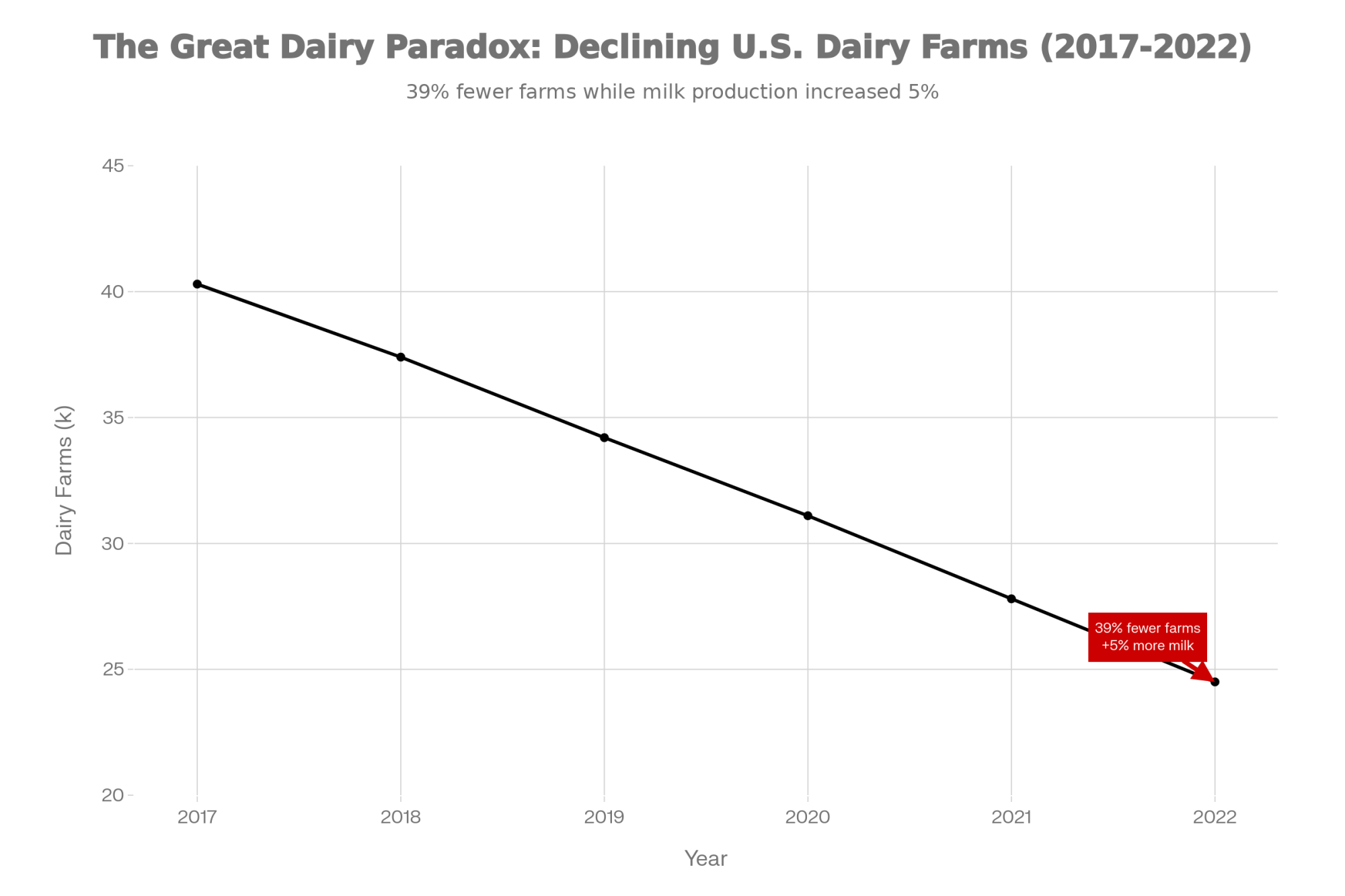

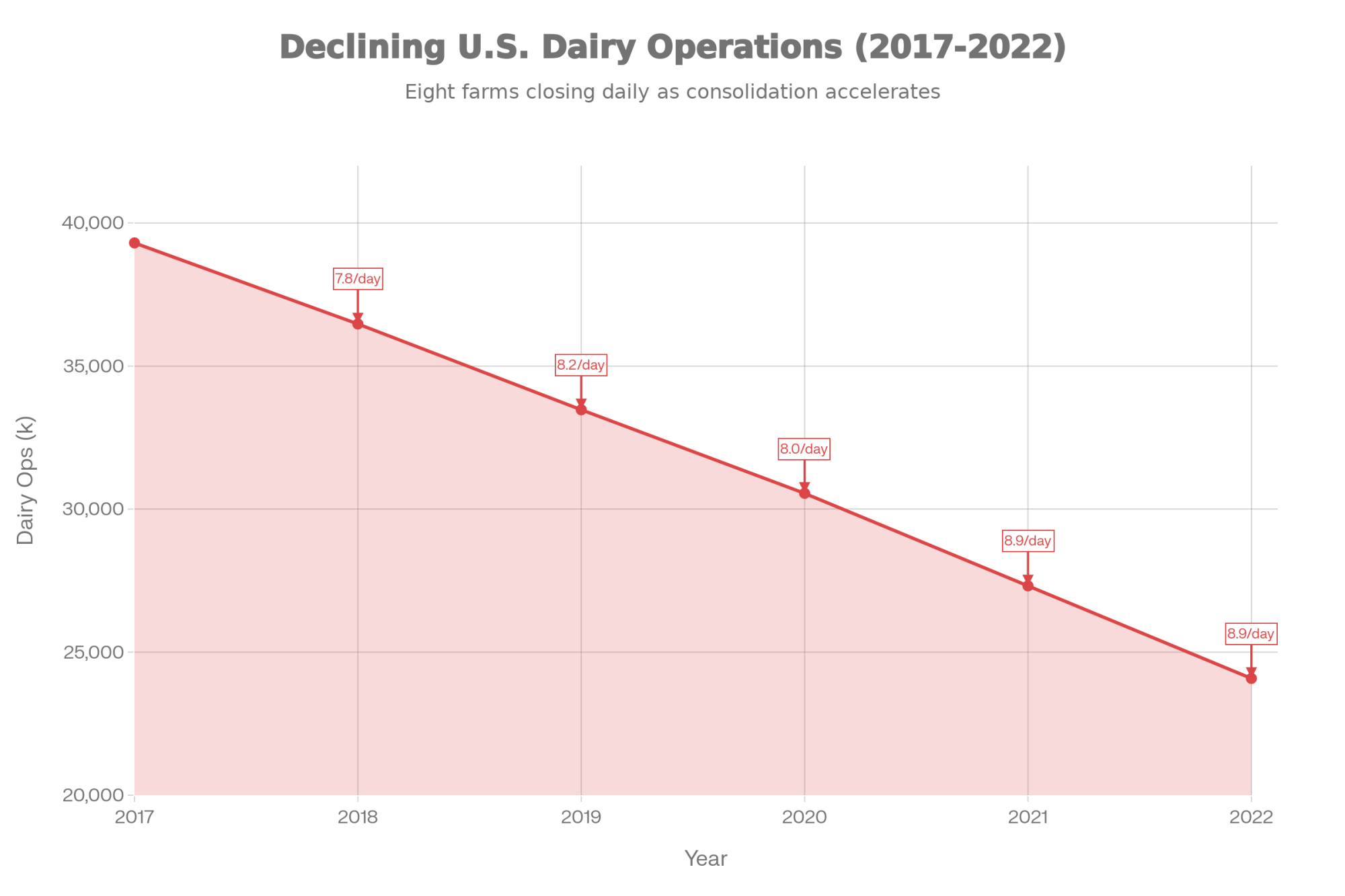

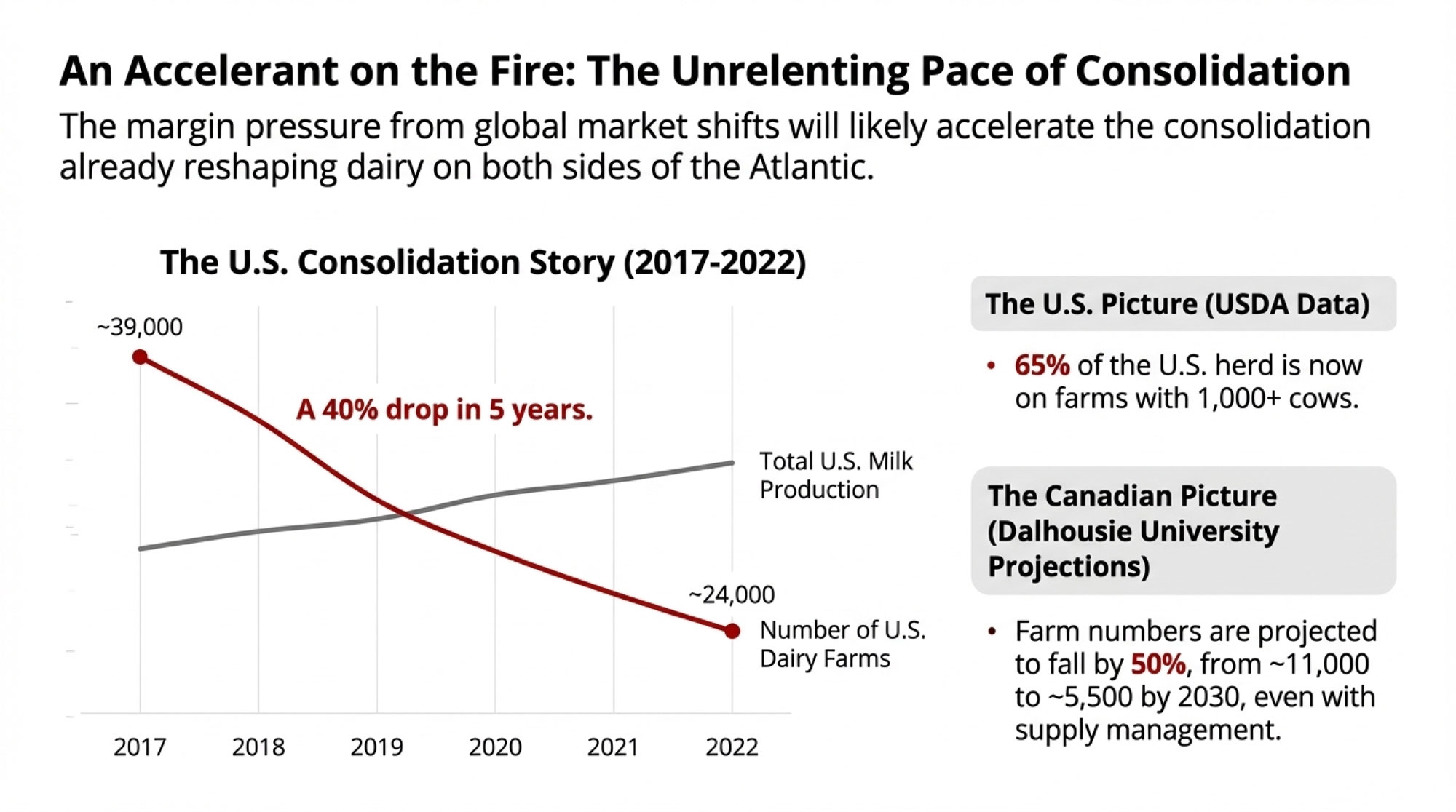

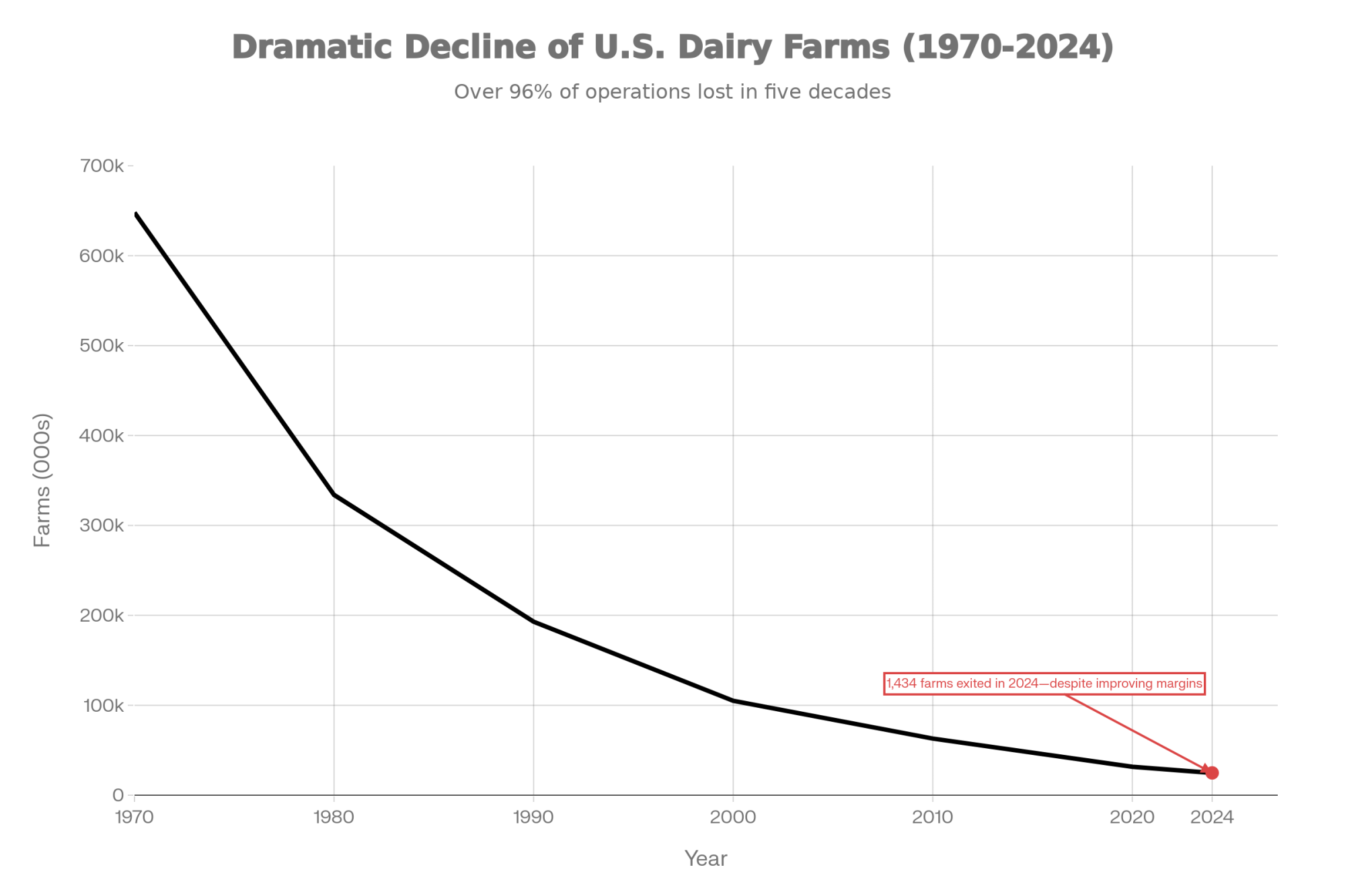

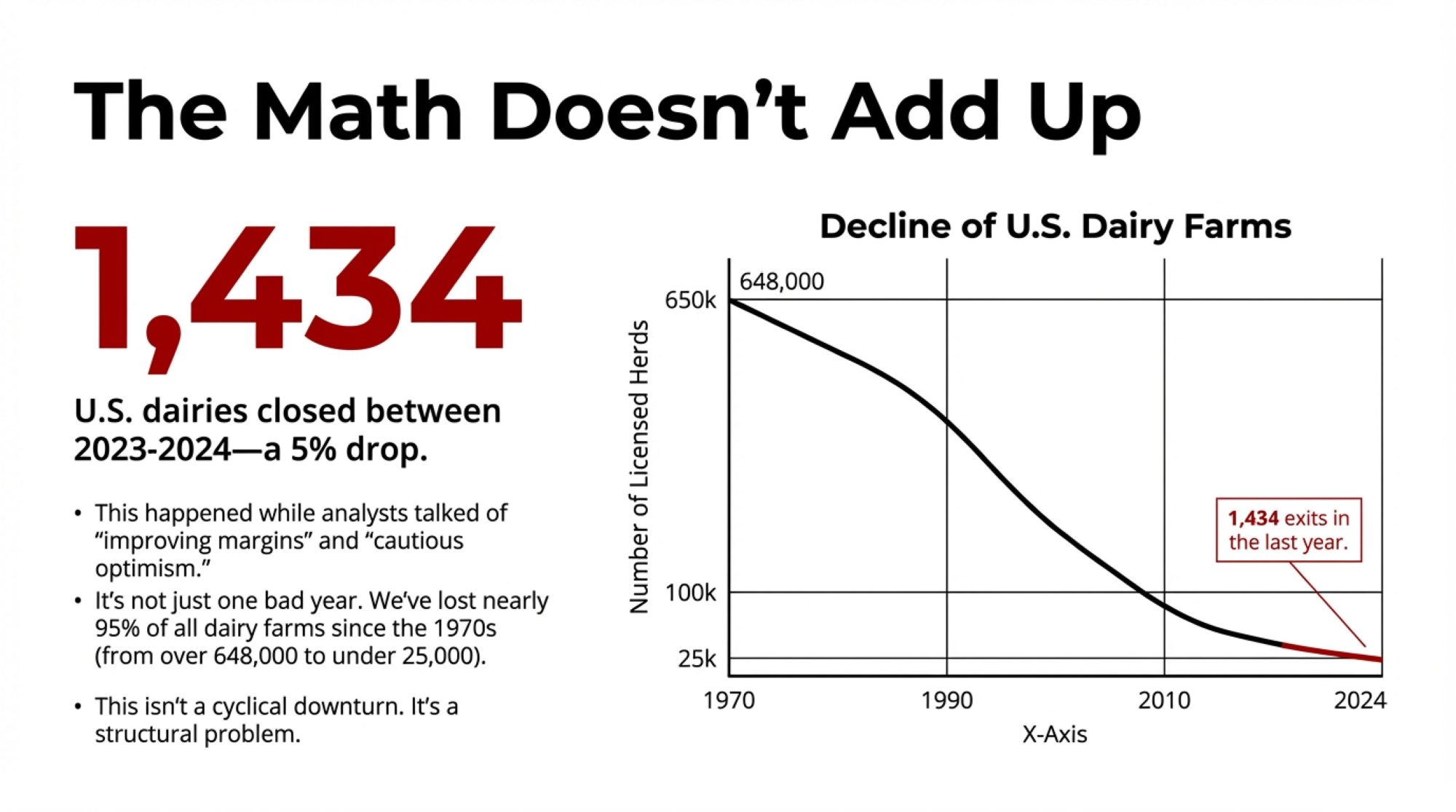

You don’t need a chart to know things have changed; you see it in auction bills and quiet parlours. The 2017 Census of Agriculture recorded 39,303 U.S. farms that sold milk from cows; by 2022, that number had dropped to 24,094, a decline of almost 40% in just five years, even as total U.S. milk production nudged about 5% higher on roughly the same total number of cows. USDA’s Economic Research Service found the longer‑run trend is the same: between 2002 and 2019, licensed U.S. dairy herds fell by more than half while national output increased, with the rate of decline accelerating in 2018–2019 and production shifting toward larger herds with higher yields per cow.

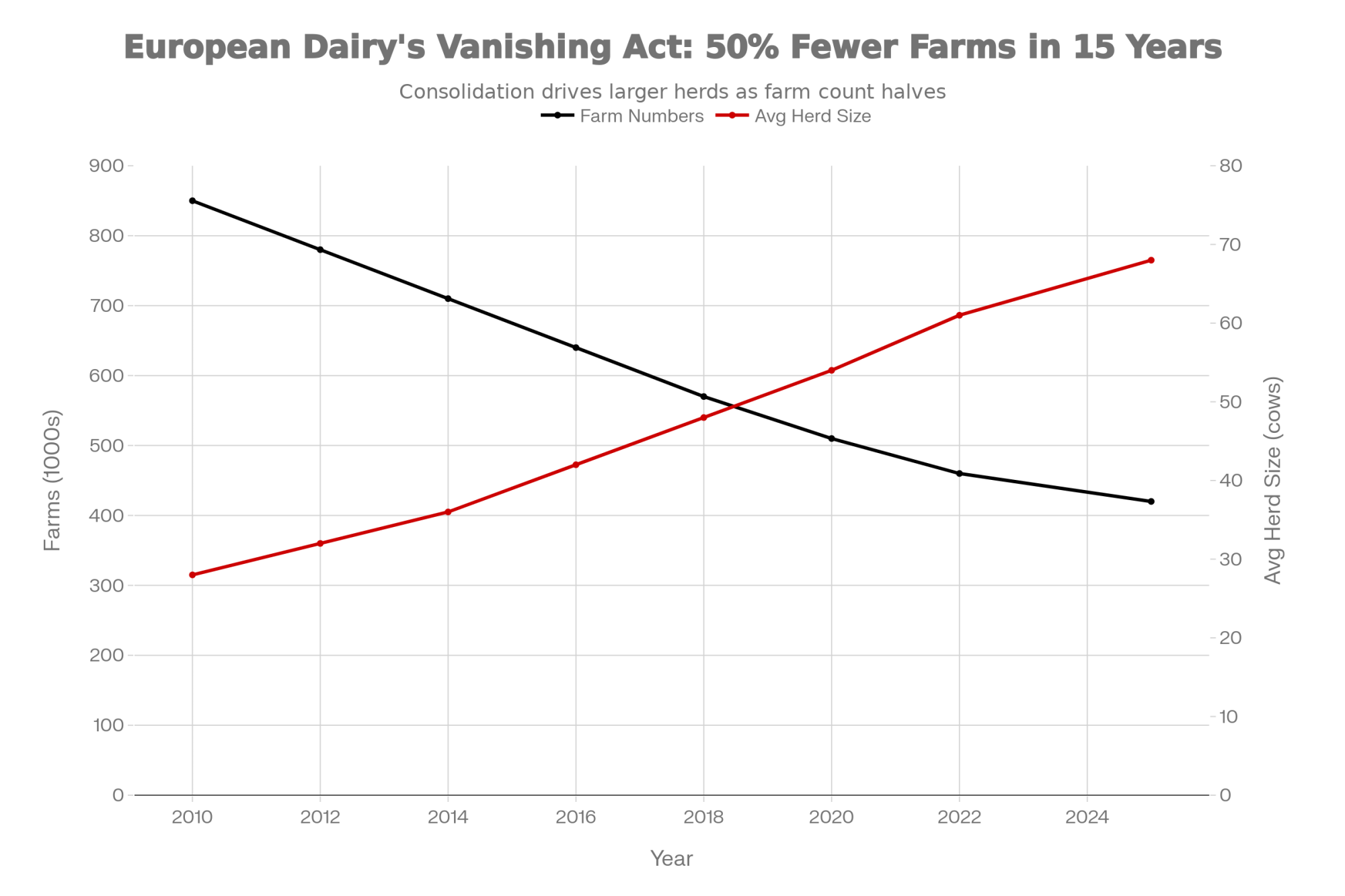

In Canada, AAFC’s Dairy Sector Profile shows farm numbers falling from 12,007 in 2014 to 9,256 in 2024—an average decline of about 2.6% per year—while milk production rose from roughly 78.3 to 96.6 million hectolitresand average farm milk prices increased from just over $82 per hectolitre to more than $97. So on both sides of the border, the story is the same: fewer herds, more milk, with the U.S. consolidating faster and Canada sliding more slowly under quota.

That’s the data the Bullvine Dairy Curve starts from: official census and ERS/AAFC work, but extended into structural scenarios that ask a more practical question—which herds are still milking in 2035 and 2050, and what do they look like?

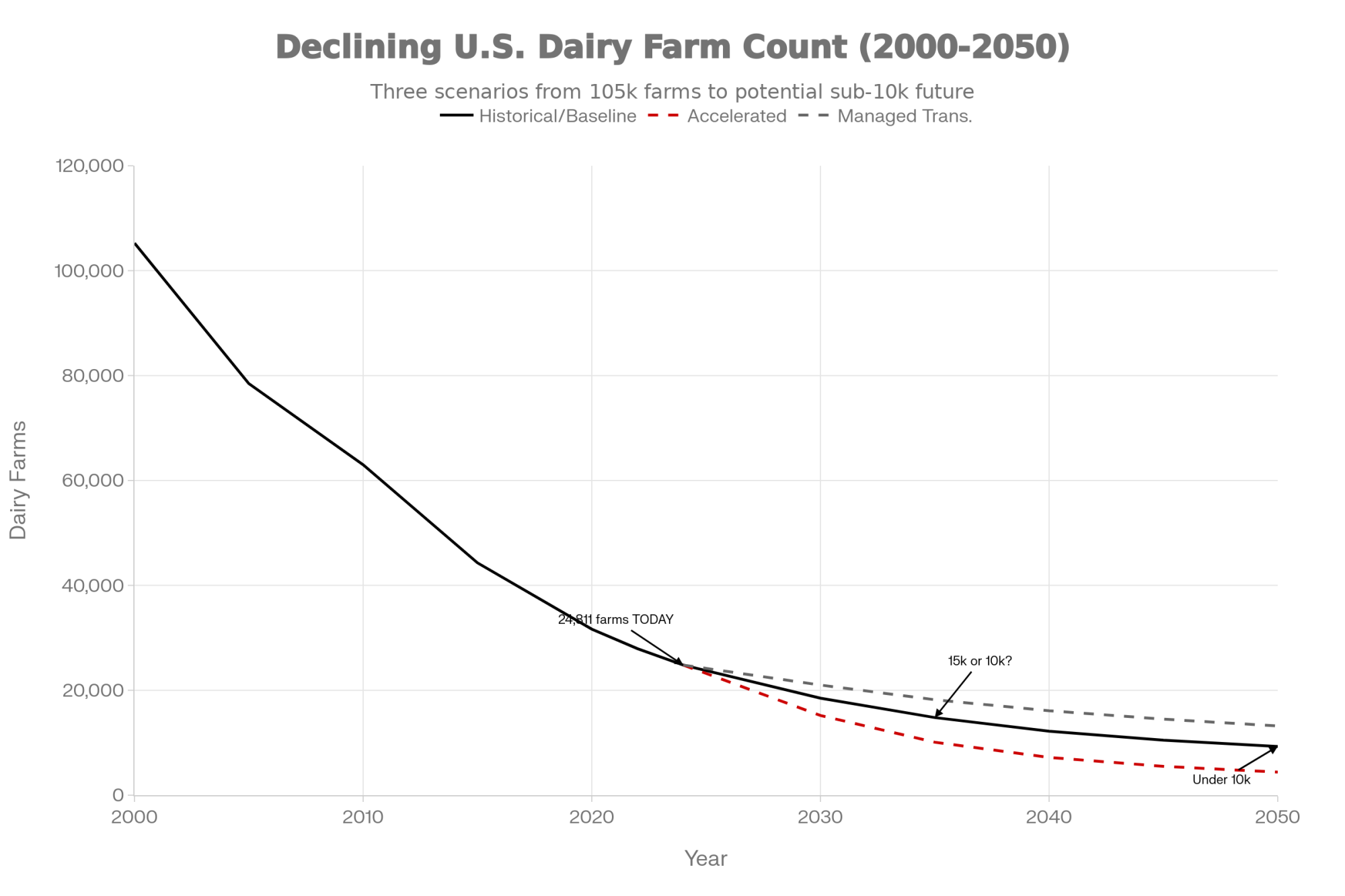

The Bullvine Dairy Curve: 15,000 by 2035, <10,000 by 2050

ERS’s Consolidation in U.S. Dairy Farming gives the cleanest long‑term U.S. baseline: herd numbers down about 55% from 2002–2019, roughly a 4% annual decline, while national production increased and midpoint herd size kept rising. When you extend that 4% curve from today’s roughly 25,000 U.S. herds and overlay it with the 2017–2022 cliff—where the only U.S. size class that actually grew was herds with 2,500+ cows—you land in the same band Bullvine’s early consolidation work described.

U.S. baseline band: about 15,000–16,000 licensed herds by 2035, with 8,000–9,000 by 2050 if that structural rate holds.

Canadian baseline band: a slower but steady slide toward 6,500–7,000 farms by 2035 and 4,000–5,000 by 2050, consistent with 2–3% annual attrition under supply management.

Since those first Bullvine forecasts, the signals have only sharpened. Follow‑up Bullvine work has documented that U.S. closures have effectively been running closer to 4–8 farms per day, and that about half of U.S. farms vanished between 2013 and 2025, with another 50% reduction projected by 2035 if current pressures persist—implying the industry could land in the lower half of that 15,000–16,000 band. In Canada, commentary that the country is “on track to lose nearly half of its remaining dairy farms by 2030,” with production concentrating in Quebec and Ontario, aligns with the 6,500/4,000–5,000 Bullvine bands.

Path

U.S. Herds 2035

U.S. Herds 2050

Canada Herds 2035

Canada Herds 2050

Key Drivers

Business-as-usual

15,000-16,000

8,000-9,000

6,500-7,000

4,000-5,000

~4% U.S. decline, 2-3% Canada under quota

Accelerated consolidation

~12,000

~5,000

~5,500

3,500-4,000

Labor, compliance, alt products, weak margins

Managed transition

~15,000

~15,000

~6,500

~6,500

Margin tools, disciplined capex, succession

The exact number isn’t the point. The curve is. The Bullvine Dairy Curve says: plan for an industry with far fewer farms, more concentrated milk, and a structure where being “average” in the middle is the riskiest place to stand.

How the curve hits different herd sizes and regions

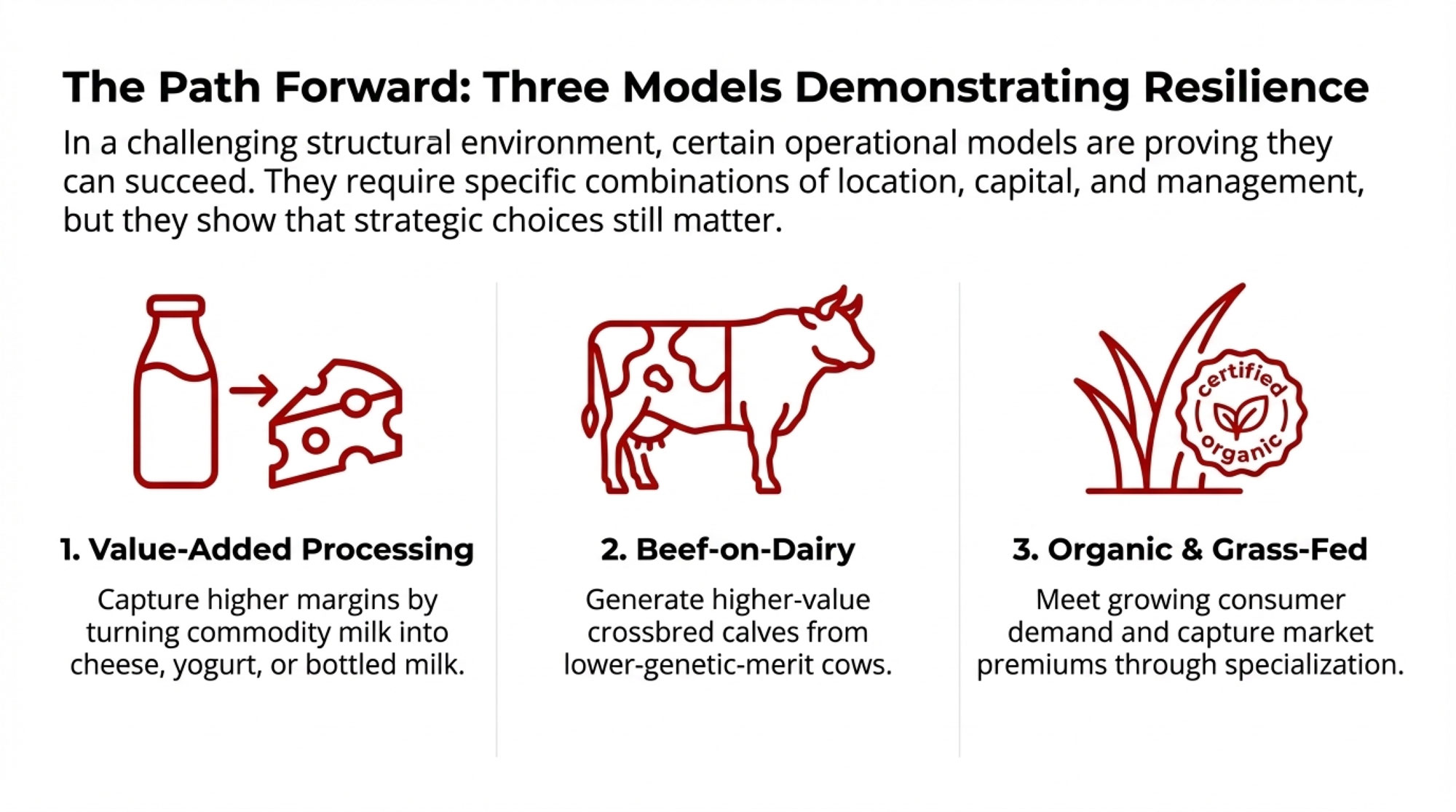

Under ~150 cows: small, but only if it’s specialized

Cost‑of‑production work and intensification studies consistently show that small conventional herds carry higher costs per cwt unless they combine very low debt, strong home‑grown forage, and heavy reliance on family labour. The small herds that are thriving as the curve plays out almost all made a deliberate move away from being “average” commodity suppliers—into organic, grass‑based, A2, on‑farm processing, or other premium systems where margin comes from price, not just volume.

This development suggests that “staying small” only works when you’re deliberately un‑average—either in cost or in the milk cheque you’re targeting. A 60‑cow tie‑stall under quota with direct‑marketed fluid milk or value‑added cheese lives on a different part of the curve than a 60‑cow conventional herd shipping into a generic pool.

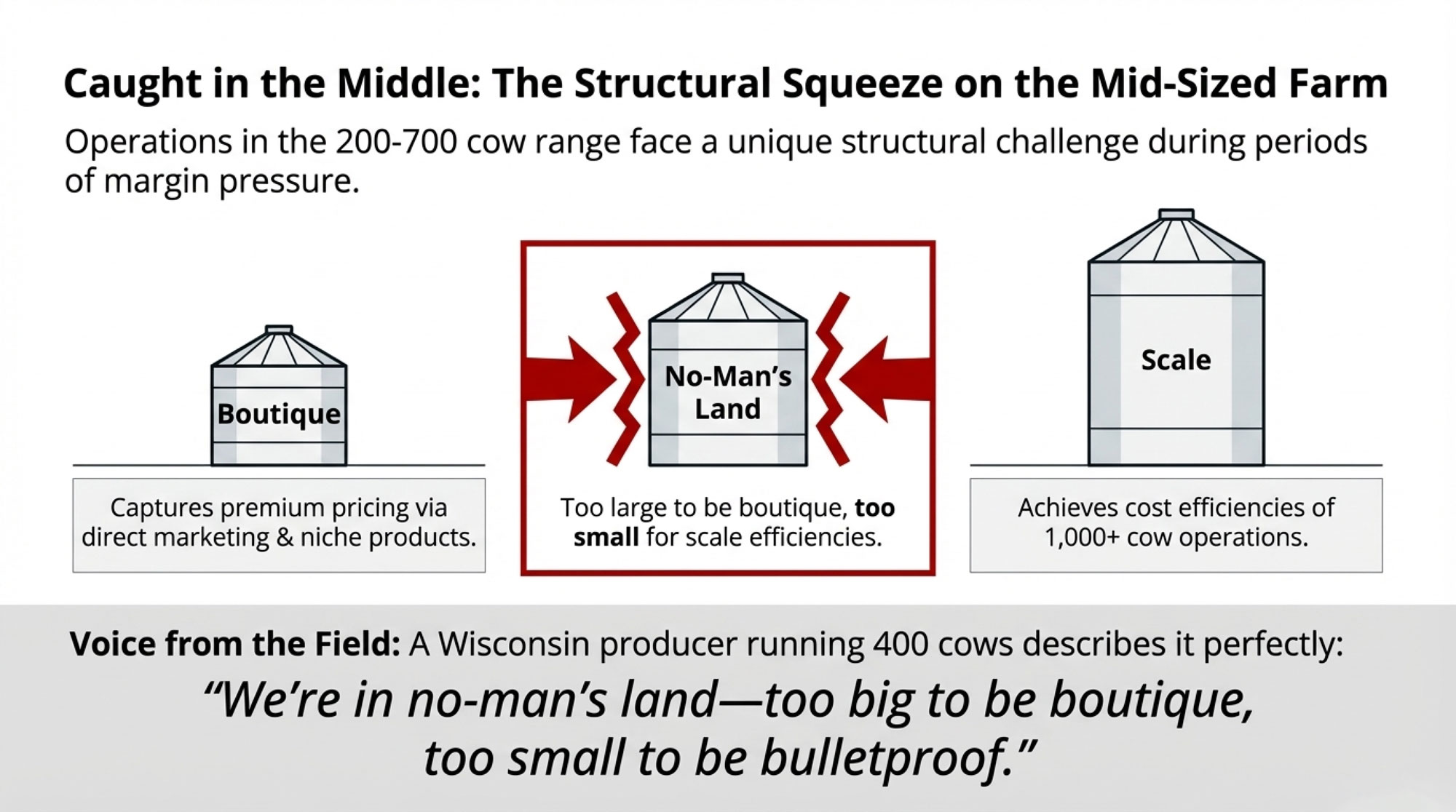

150–500 cows: the middle that the math squeezes first

Bullvine’s early projections already highlighted structural pressure on 250–400 cow freestalls: too big to be niche without a clear premium plan, too small to spread fixed costs like a 1,500‑cow system. Updated census and case work show that:

Over 15,200 U.S. dairy farms vanished between 2017 and 2022, with a big share in the 100–499 and 500–999brackets.

Many 250–400 cow herds running “average” cost structures and fully exposed to commodity pricing are carrying $75,000–$100,000 in structural losses per year once full labour and capital costs are accounted for.

Herd Size

Cows

Annual Milk (cwt)

Structural Gap ($/cwt)

Annual Loss (approx.)

Small mid

200

96,000

$0.80

$76,800

Core mid

300

144,000

$0.70

$100,800

Large mid

400

192,000

$0.60

$115,200

One Upper Midwest producer told us their 320-cow herd looked profitable on their milk cheque—until they ran a full-cost analysis with realistic family labour and depreciation. The gap? About $0.72 per cwt, which worked out to roughly $95,000 a year, they’d been quietly losing without realizing it. That’s not a bad year; that’s structure.

That’s why the Bullvine Curve is so blunt about this band: in a 15,000‑farm, <10,000‑farm future, the conventional middle either deliberately scales, specializes, or exits; drifting is the expensive option.

Honestly, what jumps out is how many 300‑cow herds are still trying to play yesterday’s game—commodity milk, average cost, no clearly defined premium hook—in a structure that’s already priced that strategy out for a lot of regions.

1,000+ cows: where the early assumptions became reality

From the beginning, the structural projections assumed economies of scale and lower total cost per cwt would keep pulling volume into larger herds, with a significant share of U.S. milk concentrated in herds of 2,000–2,500 cows by 2050. ERS follow‑up work and Bullvine’s Great Consolidation analysis confirm that:

Net returns for 1,000+ cow herds have outpaced smaller herds in most years studied.

Only the 2,500+ cow herd class actually grew in number between 2017 and 2022, and those herds now account for a very large share of U.S. milk sold.

Farm Size

Annual Exit Rate

10-Year Survival

Risk Level

10-49 cows

12%

28%

CRITICAL

50-99 cows

8%

43%

HIGH

100-199 cows

7%

48%

HIGH

200-499 cows

5%

60%

MODERATE

500-999 cows

3%

74%

LOW

1,000+ cows

2%

82%

STABLE

In Canada, the curve is flatter, but the logic is similar: fewer farms, more quota concentrated in larger herds, and a national structure where roughly 90% of farms are now clustered in a few provinces, especially Quebec and Ontario.

What’s interesting here is that the “big herds win on cost” assumption from 10–15 years ago has largely become a day‑to‑day reality—but with it comes a different risk profile tied to environmental regulation, export dependence, water, and labour, especially in dry‑lot systems.

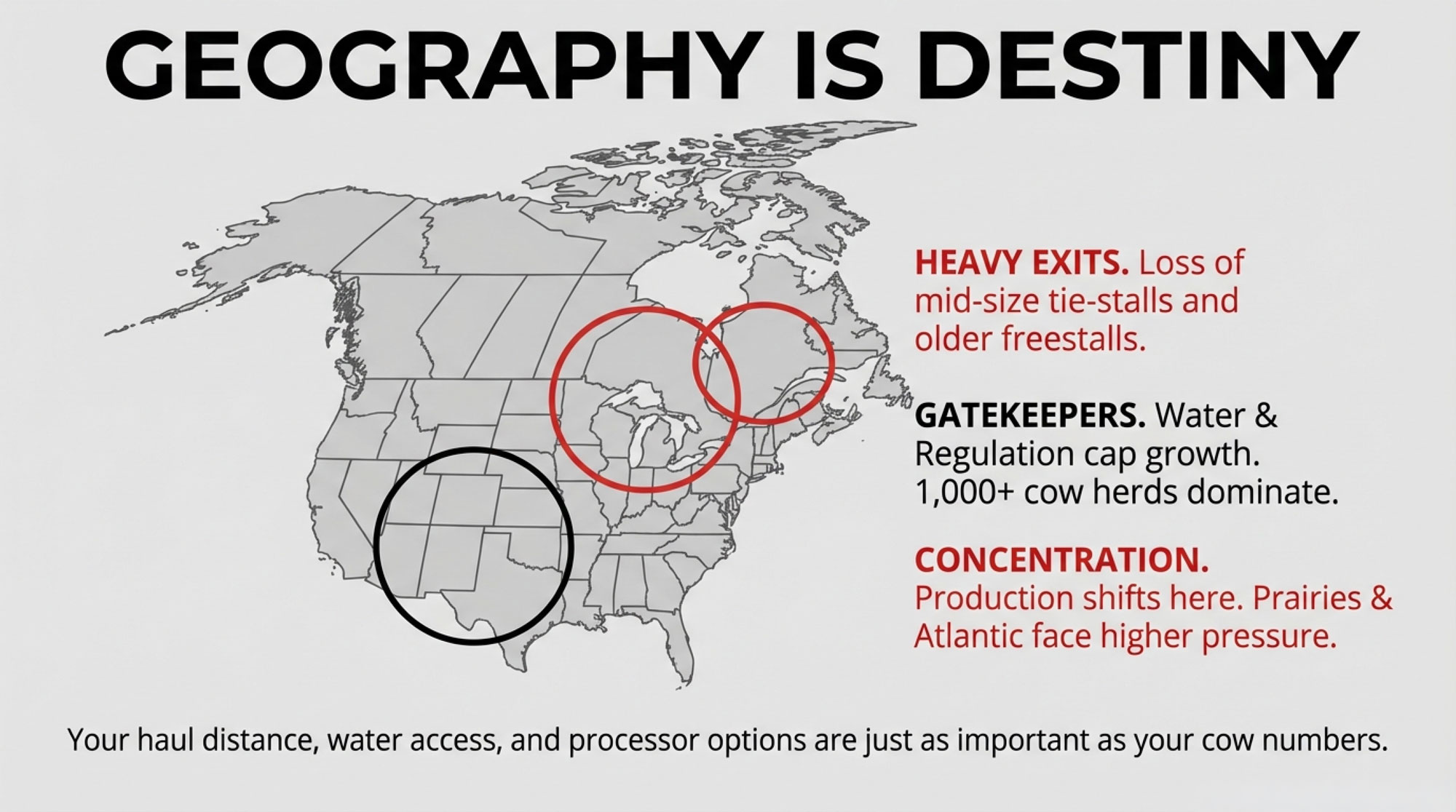

Regional reality: the curve isn’t smooth everywhere

The Bullvine Curve was never “every region looks the same.” The shape is similar; the slopes and pain points aren’t.

In the Upper Midwest and Northeast, exits are concentrated among smaller and mid‑size tie‑stalls and older freestalls, with modest growth in 1,000–2,000 cow herds and strong but concentrated production in states like Wisconsin and New York.

In the Southwest and High Plains, a relatively small number of very large freestall and dry‑lot systems supply big cheese and powder plants, with water, heat, and environmental rules acting as both risk and gatekeeper.

In Canada, AAFC data and quota policy mean the curve is slower and more managed, but the direction is the same: fewer farms, more litres per herd, and more of that production anchored in Quebec and Ontario, with smaller operations in the Atlantic and Prairies under more pressure.

I’ve noticed that when producers really “get” the curve, it’s often after they plot themselves against regional realities: haul distance, processor options, land prices, and labour pool, not just cow numbers.

From forecast to milk‑house: the Bullvine playbook

Forecasts only matter if they change decisions. The Bullvine Dairy Curve is built to drive a handful of blunt, barn‑level questions rather than just scare charts.

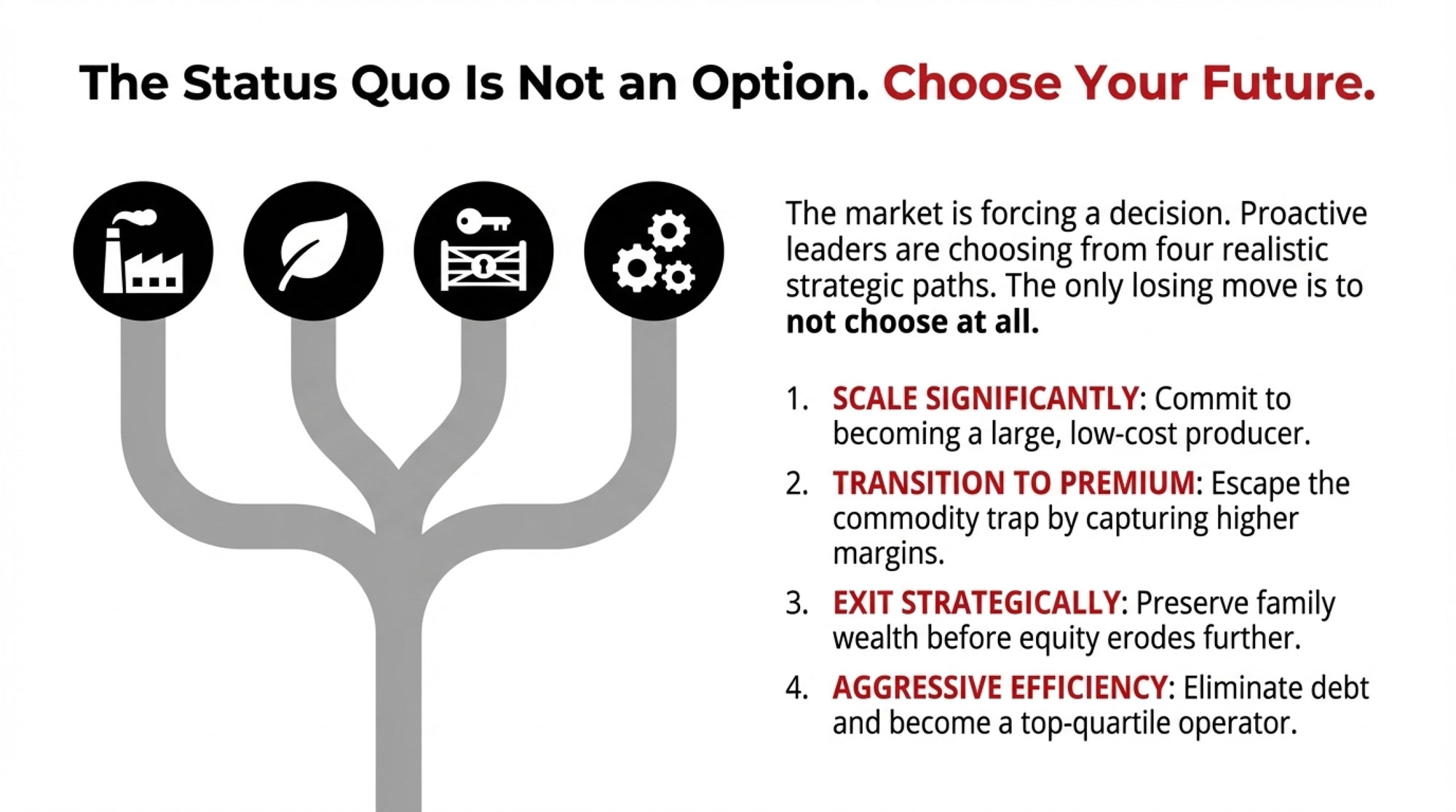

1. Which lane are you actually in?

In a 15,000‑farm, <10,000‑farm world, most herds that stay in the game long‑term are choosing one of three lanes:

Scale: Build toward 1,000+ cows with a cost structure that genuinely competes per cwt, understanding the capital, labour, and concentration risk.

Specialize: Stay smaller or mid‑size but sell into markets that pay on margin—organic, grass‑based, A2, on‑farm processing, or tightly integrated supply contracts.

Strategic exit: Use the forecast window to sell or transition on your terms while equity is intact, especially where succession isn’t clear.

Not choosing is still a choice; it just lets the curve choose for you. What farmers are finding is that being vague—“we’ll see how it goes”—is often the costliest option.

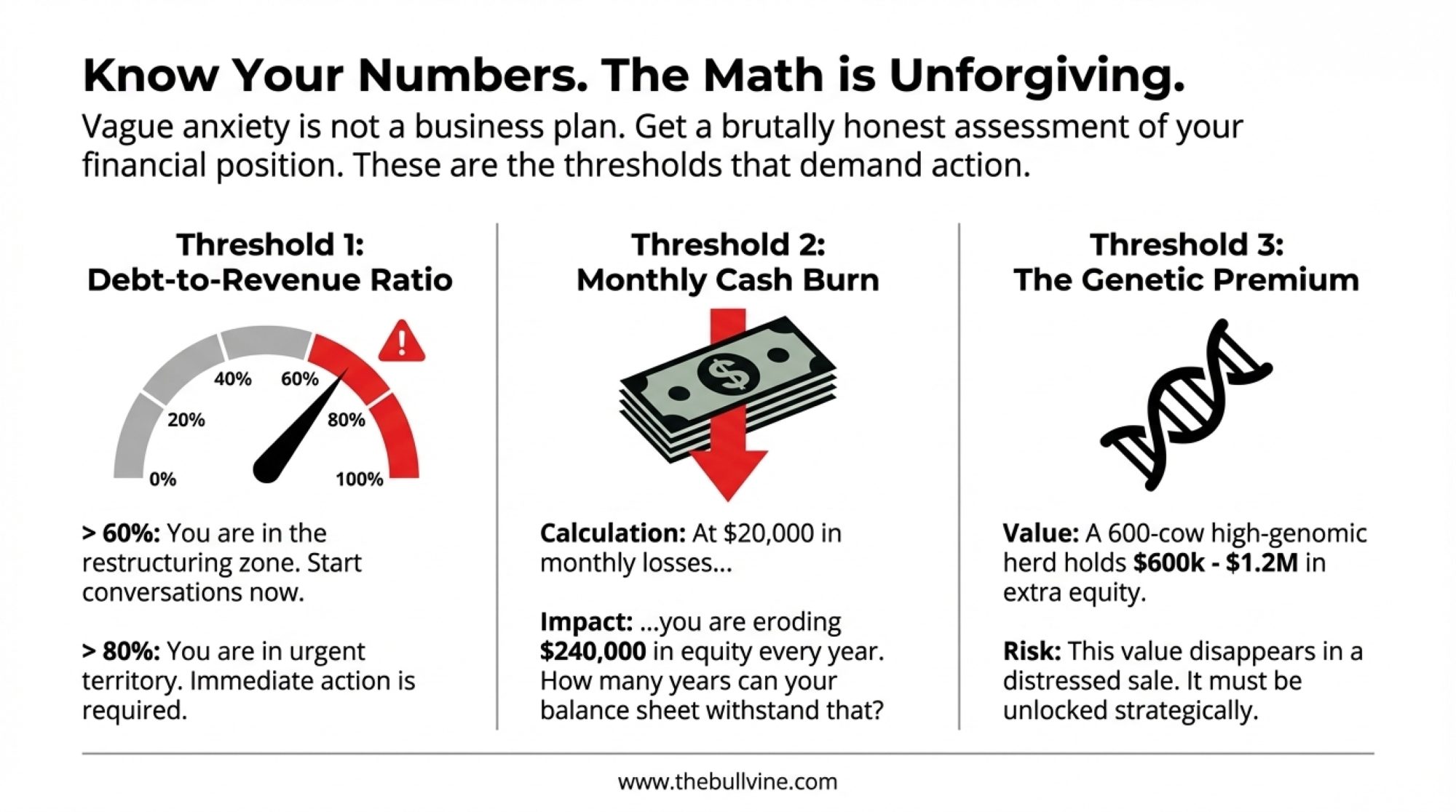

2. What is your true cost per cwt and “danger zone”?

ERS cost‑of‑production data and extension tools show that, on average, larger herds have lower total economic costs per hundredweight, but there’s a wide spread inside every size class. The farms that navigate the curve best usually:

Know their full cost per cwt with realistic values for family labour and capital.

Have a clear milk‑feed ratio “danger zone” where they tighten capital, sharpen feed, and check in with lenders more often.

In a 200‑cow herd shipping 8,000 cwt a month, a 50‑cent swing in margin is roughly $4,000 a month or $48,000 a year—almost exactly the gap between treading water and investing in the next needed project. That’s the kind of math that quietly decides whether you can upgrade a parlour or add stalls to lift butterfat performance and fresh cow comfort.

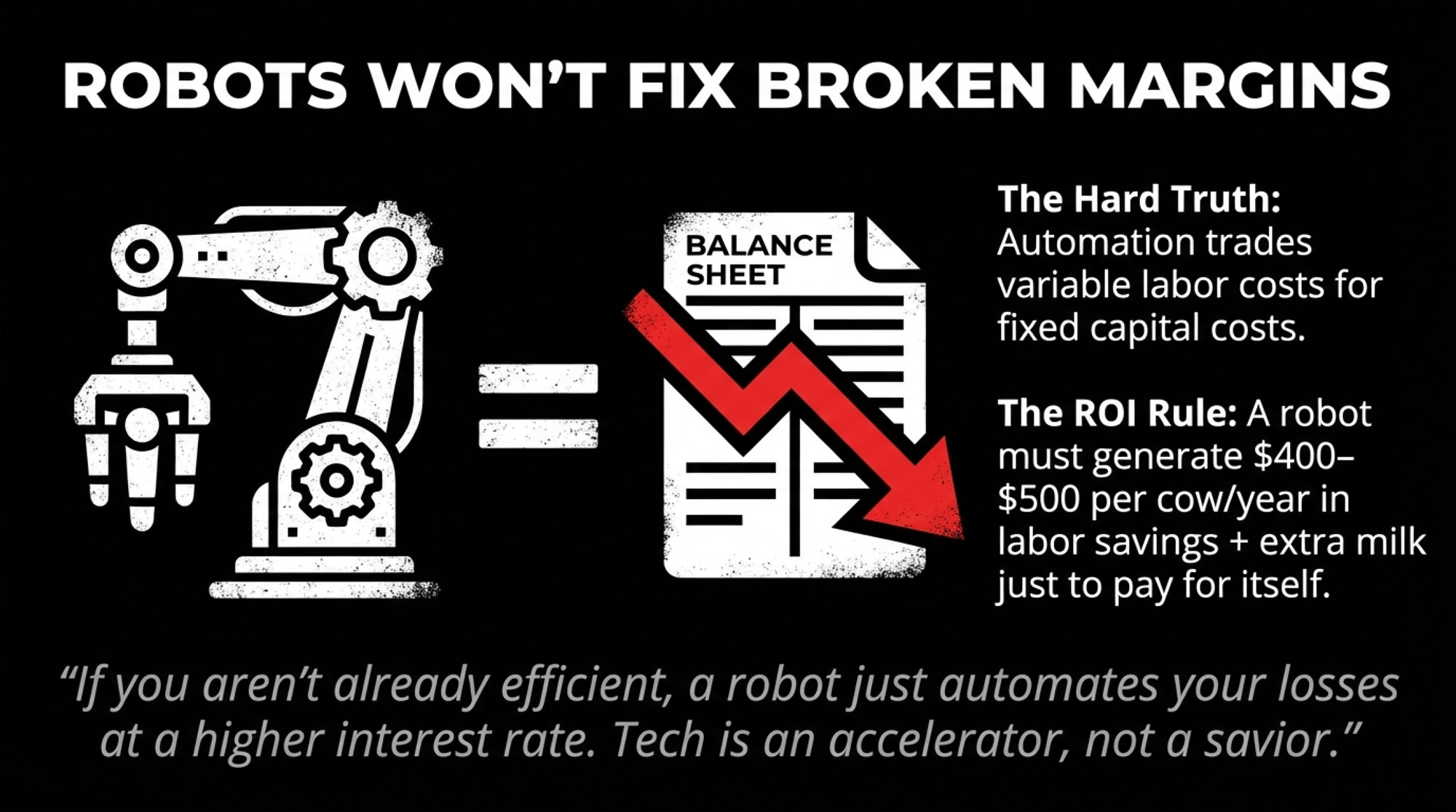

3. Is your next dollar going into scale, comfort, or robots—and why?

The curve doesn’t say “robots good, parlours bad,” it says “robots amplify whatever is already in your numbers.” While Automated Milking Systems (AMS) solve the immediate headache of labor availability, they fundamentally shift your balance sheet. You are trading variable labor costs for high fixed capital costs. In a “commodity milk” lane, this move pushes you further into the “efficiency required” lane: because your fixed costs per hundredweight are now higher, your margin for error on milk production and components disappears.

On smaller herds under ~100–120 cows, AMS often struggles to pencil out unless there’s a premium market, off‑farm income, or a clear growth plan.

In the 150–250 cow band, robots can work where labour is genuinely tight, and management is strong, but they typically need $400–500 per cow per year in a mix of labour savings and extra milk to carry their weight over a typical financing term.

Larger freestall/dry‑lot systems treat robots, high‑throughput parlours, sort gates, and sensors as part of broader cow‑flow and labour strategy, not silver bullets.

The Robot Reality Check: If your herd isn’t already hitting top-tier production and health metrics, a robot won’t fix the margin—it will just automate the loss at a higher interest rate.

The Bullvine playbook is simple: if you can’t show on paper where the extra dollars per cow per year come from, ask whether stalls, feed storage, or transition pens would move your position on the curve more. In other words, don’t let fatigue drive a million‑dollar robot decision if fresh cow management and housing are still your biggest bottlenecks.

4. Who actually wants to be milking here in 2035?

Succession is the quiet driver you don’t see on the milk cheque, but it shows up in the forecast. National surveys by lenders and advisory firms consistently find that only a minority of producers have formal written succession plans, even when an adult child is active. Research on exits also shows that age and the presence of an identified successor are strong predictors of whether a farm continues to operate 10–15 years later, even after controlling for herd size and profitability.

In practice, that means a financially solid 65‑year‑old with no successor is more likely to be on the “exiting half” of the Bullvine Curve than a somewhat smaller or slightly less efficient herd where a 35‑year‑old is already leading breeding, facilities, and lender meetings. Putting a basic timeline and ownership plan on paper is one of the simplest ways to move your operation onto the “still milking by choice” side of the 2035/2050 lines.

I’ve seen more than one herd where the real turning point wasn’t a bad milk price year—it was the moment the family admitted no one under 40 actually wanted night checks and bank meetings for the next 20 years.

The “Strategic Exit”: Harvesting Equity, Not Admitting Defeat

One of the hardest parts of the Bullvine Dairy Curve is the “Exit” conversation. We need to change the vocabulary around leaving the industry. In every other sector of the global economy, “exiting” at the top of a market or when equity is strongest is called a successful business cycle.

If the curve shows that your regional processor access is shrinking or your cost structure is hitting a structural ceiling, executing a Strategic Exit is an act of leadership. It allows you to:

Protect Generational Wealth: Cash out while land and quota values are high, rather than “burning the house for warmth” by eroding equity during years of structural losses.

Define Your Legacy: Transitioning the land to its next best use—whether that’s cash crops, beef, or development—on your timeline, not the bank’s.

A strategic exit isn’t a failure; it’s a calculated decision to stop milking cows so you can start protecting the family’s future.

5. Does your regional strategy match the curve you’re actually in?

Processor access, hauling distance, water rules, land markets, and labour conditions shape how the curve feels locally. A 200‑cow freestall near several plants in southern Ontario lives in a different structural world than a 200‑cow herd in northern Vermont or a 3,000‑cow dry lot in west Texas.

The Bullvine Curve is a map, not a script; the job is to locate your farm on that map honestly—by size, cost, region, and succession—and then build a plan that fits the structure you’re heading into, not the one you remember.

The Bullvine Bottom Line: forecasts as a tool, not a headline

The consolidation trend itself isn’t up for debate anymore; the 2022 Census of Agriculture, USDA ERS work, and AAFC’s Dairy Sector Profile all tell the same story of fewer herds, more milk, and more of that milk coming from larger operations. What the Bullvine Dairy Curve adds is a clear, named set of paths—15,000–16,000 vs <10,000 U.S. herds, 6,500–7,000 vs 4,000–5,000 Canadian herds—and a practical way to turn those numbers into decisions about cost structure, technology, and succession while there’s still time to move.

The data strongly suggest there will be fewer dairy farms in 2050 than there are today; they do not say which farms those will be. That part is still being written—day by day, barn by barn—and the whole point of the Bullvine forecast is to help you write your own line on the curve instead of letting the averages write it for you.

KEY TAKEAWAYS

15,000 U.S. farms by 2035. Under 10,000 by 2050. Where do you land? The Bullvine Dairy Curve extends the 4% annual decline documented by the USDA from 2002 to 2019. Canada tracks toward 6,500–7,000 farms by 2035 and 4,000–5,000 by 2050. These aren’t worst-case guesses—they’re the middle of the road.

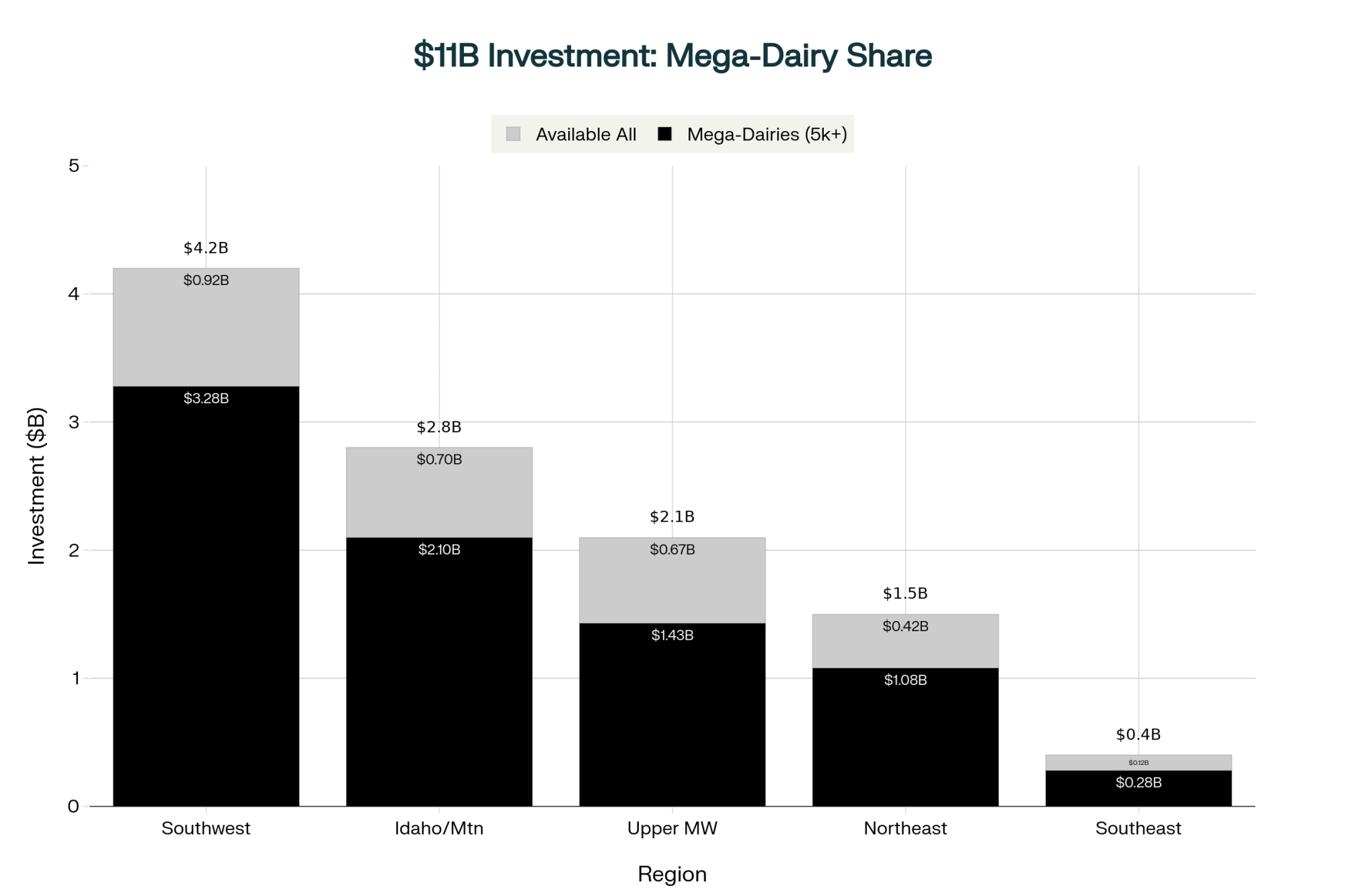

Milk isn’t disappearing—it’s moving into bigger barns. The 2,500+ cow herd class is the only one that grew between 2017 and 2022. Processors are building $11B in new capacity around these mega-suppliers, not 300-cow herds.

The $100k squeeze hits mid-size hardest. Many 150–500 cow commodity herds running “average” costs incur $75,000–$100,000 in structural losses per year. Stay average, and you’re betting against the curve.

Three paths remain—pick one. Scale toward 1,000+ cows with genuinely competitive cost per cwt, specialize into premium markets that pay on margin, or execute a strategic exit while equity is intact. Not choosing lets the curve choose for you.

Succession decides who’s still milking in 2035. A 65-year-old with no successor is more likely to exit than a smaller herd where a 35-year-old already leads. Put the timeline on paper now—”someday” isn’t a plan.

Executive Summary:

By 2035, the Bullvine Dairy Curve has U.S. dairy farms shrinking from roughly 25,000 herds today to 15,000–16,000, and to well under 10,000 by 2050. That’s what happens if the long‑run 4% annual decline identified by USDA’s Economic Research Service continues. In Canada, AAFC’s Dairy Sector Profile and Bullvine’s modelling show a slower but similar slide from 12,007 farms in 2014 to 9,256 in 2024, heading toward roughly 6,500–7,000 farms by 2035 and 4,000–5,000 by 2050—even as national milk output climbed about 23%, from 78.3 to 96.6 million hectolitres. Across all three paths—business‑as‑usual, a faster shakeout, or a more managed transition—the litres don’t disappear; they concentrate into larger freestall and dry‑lot systems as processors, and lenders channel more volume to 1,000‑plus‑cow herds with lower cost per cwt. That structural shift leaves many 150–500 cow commodity herds that sit “average” on cost and fully exposed to commodity pricing, facing $75,000–$100,000 a year in structural losses, unless they either scale, specialize into premium/value‑add markets, or plan a strategic exit while equity is still strong. This article turns the Bullvine Dairy Curve into a five‑question barn‑level playbook—covering lane choice, true cost per cwt, tech and barn investments, succession, and regional realities—so you can decide whether your operation will be one of the 15,000 still milking by choice in 2035 and beyond, or one of the herds the curve quietly averages out.

About the Bullvine Dairy Curve Model

The Bullvine Dairy Curve is an analytical framework—not an official government forecast—built by extending documented historical trends into scenario-based projections. The U.S. baseline draws on USDA’s 2017 and 2022 Census of Agriculture (39,303 farms → 24,094 farms) and USDA Economic Research Service report ERR-274, Consolidation in U.S. Dairy Farming, which documented a roughly 4% annual decline in licensed herds from 2002–2019 alongside rising national production and increasing concentration in larger operations. The Canadian baseline uses Agriculture and Agri-Food Canada’s Dairy Sector Profile, which tracks farm numbers from 12,007 in 2014 to 9,256 in 2024 (approximately 2.6% annual decline) under supply management. Rather than a single-point prediction, the Bullvine Dairy Curve presents three scenario paths: a business-as-usual path that extends historical decline rates, a faster consolidation path that accounts for accelerating pressures (labor constraints, compliance costs, alternative proteins, and margin compression), and a managed transition path where disciplined use of margin tools, capital decisions, and succession planning slow effective exit rates. All projections assume continued structural concentration—consistent with Census data showing the 2,500+ cow herd class as the only size category that grew between 2017 and 2022—and are intended as planning tools for producers, lenders, and advisors rather than definitive forecasts.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Profit and Planning: 5 Key Trends Shaping Dairy Farms in 2025 – Arms you with critical benchmarks—like the 1.4 feed efficiency ratio—to stop cash flow leaks today. You’ll gain a tactical roadmap for cleaning balance sheets and securing contracts before the next market recalibration shifts the goalposts.

Cheap Milk Is Breaking the Farm: What’s Really Hollowing Out Dairy’s Middle Class – Reveals the structural vise squeezing mid-size dairies and explains why traditional efficiency isn’t enough to survive. You’ll gain a clear-eyed analysis of the business models available for those caught between niche premiums and massive scale.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

39% fewer farms. Record milk. If your strategy is ‘wait for the next good cycle,’ this article is your reality check.

Executive Summary: Dairy isn’t just in a rough patch—it’s in a structural reset where exits don’t automatically tighten supply anymore. USDA’s 2022 Census shows a 39% drop in farms selling milk between 2017 and 2022, yet total production still climbed to about 226 billion pounds from roughly 9.4 million cows, backing Rabobank’s finding that nearly 70% of U.S. milk now comes from herds with 1,000+ cows. At the same time, CoBank reports that replacement heifer inventories are at a 20‑year low and could shrink by another 800,000 head even as processors pour about $10 billion into new plants that will need more reliable, high‑volume milk supplies. High cull values, record heifer prices, and strong beef‑on‑dairy calf markets are reshaping net replacement costs and culling strategy, while regional realities—from Darigold’s $4/cwt Pasco deduction in the Pacific Northwest to stronger Class I returns in the Southeast and thin‑margin “deadly middle” herds in the Upper Midwest—are making geography as important as genetics. This feature gives producers an 18‑month playbook: clean out chronic problem cows while beef is still strong, treat a 0.1 gain in feed efficiency as a $35–55/cow/year opportunity, and sit down with processors and lenders before they end up making the big decisions for the farm. The aim isn’t to preach a single “right” model, but to put the math, regional context, and survival questions on the table so every herd—from 200‑cow grazing outfits to 4,000‑cow dry‑lot systems—can decide whether to grow, pivot, or exit on its own terms.

Most of us have ridden out more than one down cycle. You know the pattern: prices drop, some herds sell out, milk supply tightens, and eventually things come back around.

Back in the 2000s, Cooperatives Working Together (CWT) ran 10 herd retirement rounds between 2003 and 2010 that removed 506,921 cows and an estimated 9.672 billion pounds of milk, according to CWT program reports and University of Missouri economic analysis cited in both Progressive Dairy coverage and academic case studies on U.S. dairy market power. Those removals were designed to pull milk off the market and did help support farmer milk prices during the 2009 crash, based on those evaluations. The playbook then was pretty straightforward: enough cows and herds left the industry, and the market eventually corrected.

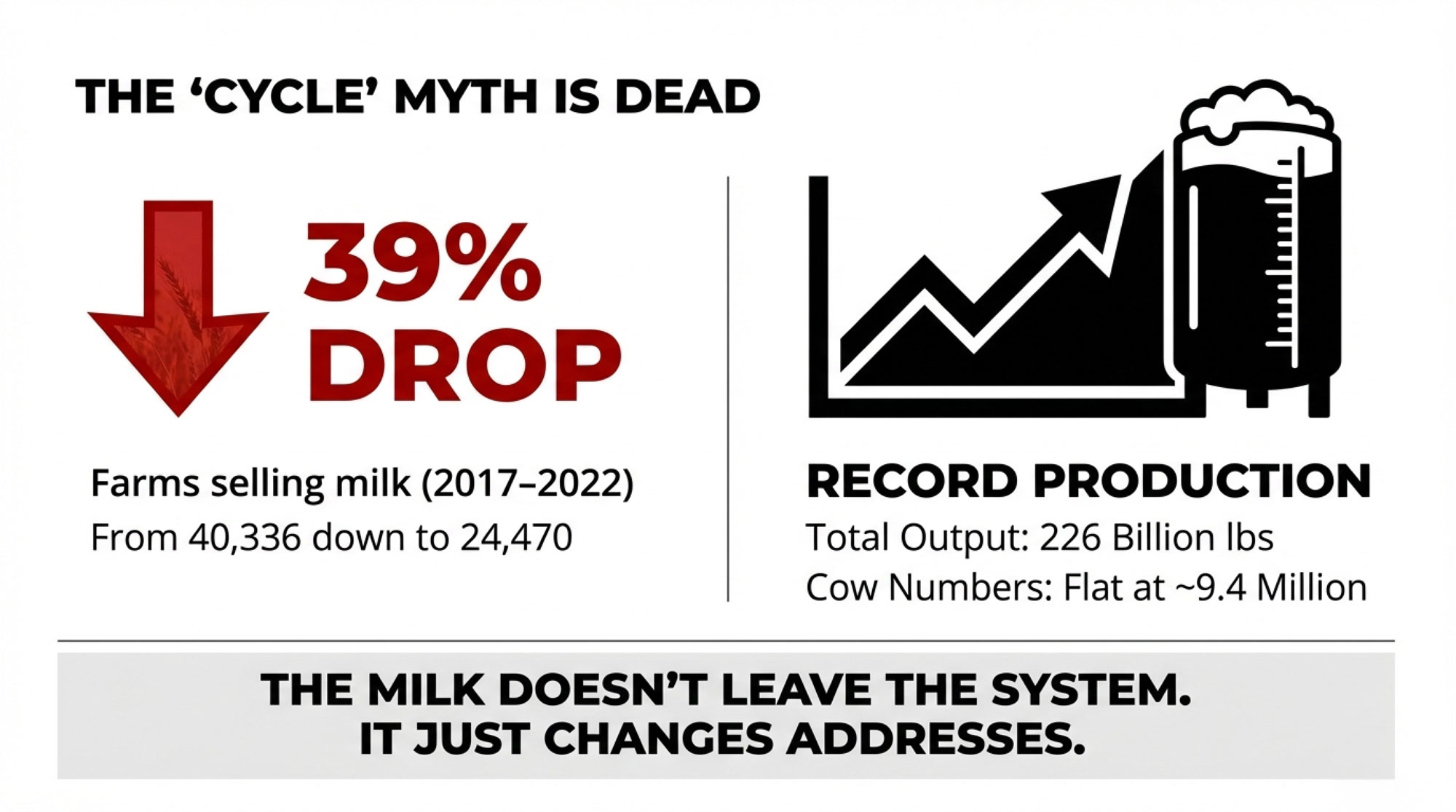

What’s interesting now is that we’re seeing plenty of exits again—but the milk isn’t disappearing the way it used to. USDA’s 2022 Census of Agriculture and milk-production summaries show that while farms with sales of milk from cows dropped from 40,336 in 2017 to 24,470 in 2022—a decline of about 39%—national milk output still climbed to around 226 billion pounds in 2022 with about 9.4 million milk cows, essentially steady cow numbers compared to prior years. Industry outlets covering the same census data have underscored that almost 4 in 10 dairy farms disappeared over those 5 years, yet total U.S. milk sales rose about 5%.

The Great Dairy Paradox: Between 2017 and 2022, U.S. dairy farms dropped 39% while national milk production increased 5% – proving the old “herd retirement tightens supply” playbook is broken

So the quiet question a lot of folks are asking—over coffee at winter meetings or in the parlor office—is: if this isn’t just another cycle, what exactly are we dealing with?

And honestly, if you’re still betting the next round of sellouts will rescue your milk price, you’re betting against the numbers.

Let’s walk through what the data says, how it’s playing out in different regions, and the kinds of decisions that seem to matter most over the next 18 months.

Looking at This Trend: Old Playbook vs. New Reality

Looking at this trend over time, it’s pretty clear that the industry’s default settings have changed. The tools that worked from roughly 2000 through the mid‑2010s just don’t behave the same way anymore.

The Structural Reset

Metric

Old Playbook (2000–2015)

New Playbook (2026+)

Supply control

Herd retirements and voluntary supply cuts through programs like CWT

On-farm culling targeted at performance, health, and butterfat; exits absorbed by larger herds

Growth strategy

Adding more stalls and more cows

Maximizing energy-corrected milk per cow and per pound of dry matter; feed efficiency as the primary lever

Primary income

Almost entirely from the milk check

Milk check plus stronger beef value from beef-on-dairy calves and high cull prices; some herds adding niche or premium markets

Heifer strategy

Raising nearly every dairy heifer born into the herd

Sexed dairy semen on top cows, beef semen on lower-end cows; raising or buying fewer, higher-value replacements

The old mindset assumed that enough CWT rounds or herd sales would tighten supply and lift prices. The data suggest something different: larger herds with lower costs per hundredweight are ready to step in when neighbors exit, blunting the supply‑tightening effect of those departures. University of Illinois economists looking at the 2022 Census noted that herds with 2,500 cows or more actually increased their share of the national milk supply even as total farm numbers dropped, confirming what many of us have seen anecdotally.

That’s a big shift in how risk and opportunity line up.

What the Census Is Really Telling You

The 2022 snapshot gets pretty eye‑opening when you dig into it. USDA’s dairy census highlights show that farms with sales of milk from cows fell from 40,336 in 2017 to 24,470 in 2022, a 39% drop in just five years. Over that same period, NASS milk‑production data show total U.S. milk production at roughly 226 billion pounds in 2022, with an average of 9.4 million cows—almost the same number of cows producing more milk.

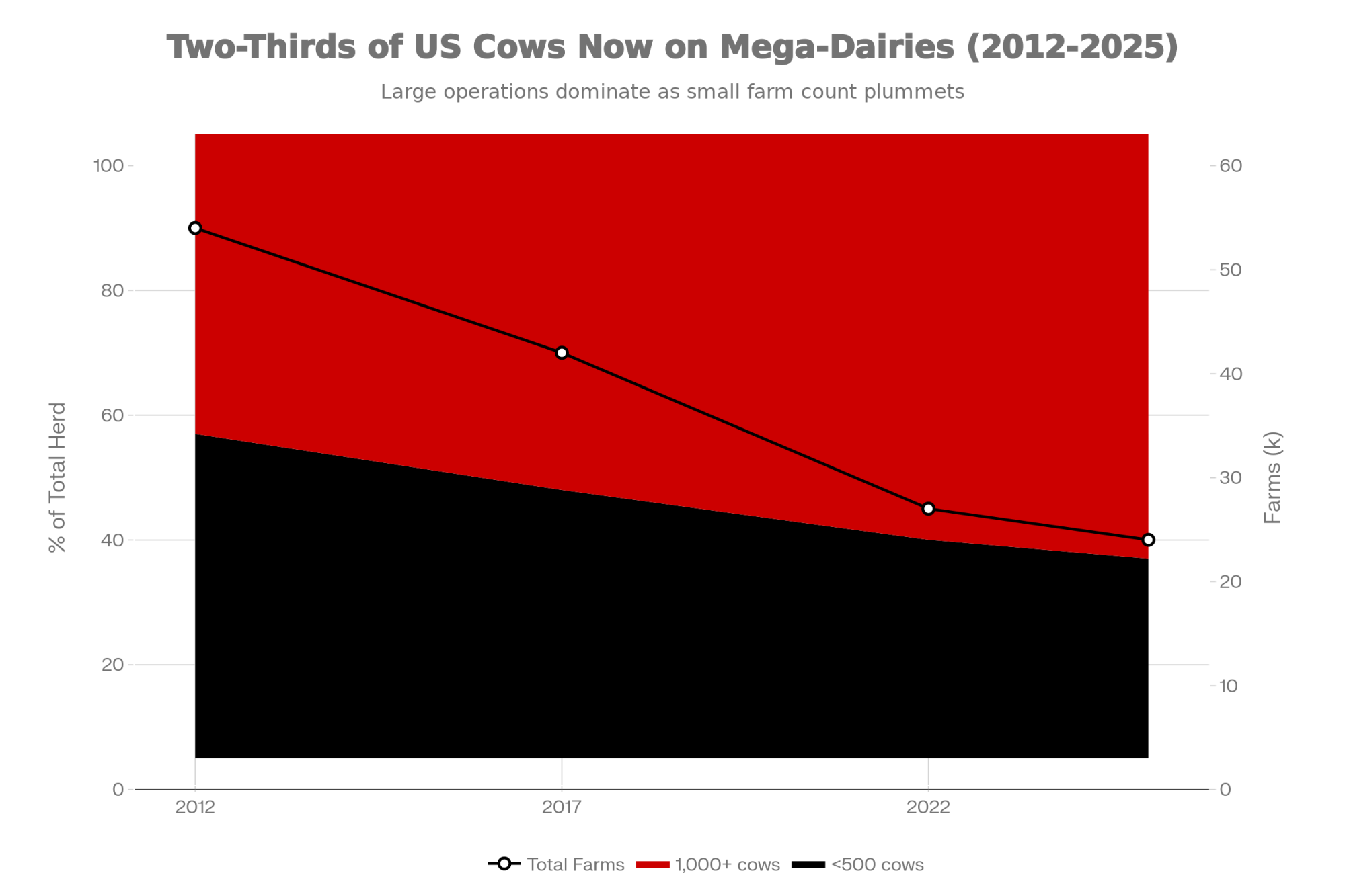

Rabobank’s consolidation analysis provides more detail. Senior dairy analyst Lucas Fuess points out that about 67–68% of U.S. milk is now produced on farms with 1,000 or more cows, even though those herds account for only a small single‑digit share of total operations. Summary of the same work notes that farms with more than 1,000 head produced 67% of U.S. milk in 2022, up from 60% in 2017.

So what many of us have seen on the ground—the milk concentrating on fewer, larger farms—is exactly what the national numbers are telling us.

You probably know this pattern already if you’ve watched what happens when a neighbor exits. Many larger operations in Wisconsin, the West, and the Plains report absorbing cows from exiting neighbors—keeping the best animals, tightening up their fresh cow management and transition period, and culling more sharply for poor butterfat performance, health, and reproduction. The net result is that the milk doesn’t really leave the system. As one producer put it at a recent regional meeting, when a herd sells out, “the milk just changes addresses.”

That’s why one of the old assumptions—“enough farms sell out, and prices will snap back”—just isn’t as reliable as it used to be. The supply side has become much more resistant to exits because large herds, often with strong genetics and efficient systems, are ready and able to absorb the volume.

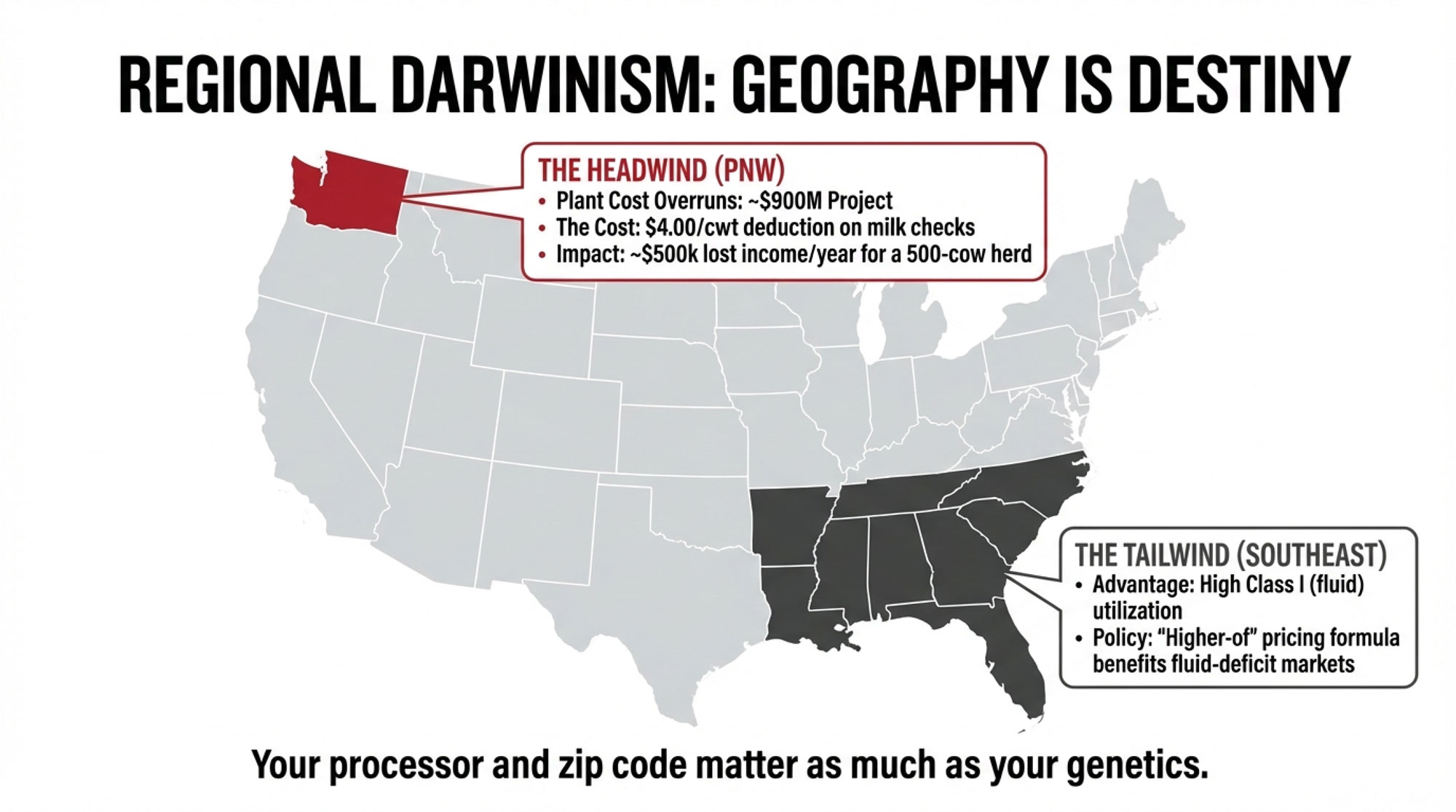

Regional Darwinism: Why Geography Is Now Destiny

What farmers are finding is that national averages hide a lot. Your region—and quite often your processor mix—now matters almost as much as your butterfat and protein levels when it comes to long‑term viability.

Region

Structural Tailwinds

Structural Headwinds

Class I Utilization

2025 Outlook

Pacific Northwest

Export-oriented processing capacity (Pasco plant)

$4/cwt co-op deduction, low Class I (~20%), environmental scrutiny

~20–22%

High risk: Co-op capital costs hitting checks directly

Southeast

High Class I demand, restored “higher-of” pricing, dense population

Limited land for expansion, summer heat stress

~28–32%

Favorable: Policy and demographics working together

Upper Midwest

Strong processing base, established supply chains, agronomic fit

Massive scale, sophisticated genetics, year-round production

High land/labor costs, strict environmental regs, water constraints

~21–24%

Stable consolidation: Fewer, larger, more efficient herds

Pacific Northwest: When Headwinds Stack Up

In the Pacific Northwest, especially Washington and Oregon, producers are facing several headwinds at once.

The one everyone’s talking about is Darigold’s new plant at Pasco, Washington. Darigold announced and broke ground on a $600‑million production facility at the Port of Pasco in 2022, designed to handle milk for butter and powder and serve export markets, according to cooperative announcements and Bullvine coverage. By May 2025, Capital Press was reporting that the plant was about $300 million over budget, based on people familiar with the project, pushing total costs toward $900 million. Follow‑up coverage has described the Pasco facility as the largest dairy plant in the Northwest, coming online at a much higher price tag than originally forecast.

To help cover those overruns and broader financial strain, Darigold’s board approved a $4‑per‑hundredweight deduction on member milk checks for at least several months, with $2.50 of that earmarked explicitly for Pasco construction costs, according to a mid‑April member letter. The $4/cwt reduction hit member pay prices in mid‑2025. For a 500‑cow herd shipping 125,000 cwt a year, that’s roughly $500,000 less milk income across 12 months—before you even talk about feed, labor, or interest.

Darigold’s Pasco plant ballooned from $600M to $900M, triggering a $4/cwt member deduction that costs a typical 500-cow operation roughly $500,000 annually

Several Washington producers shipping to Darigold have told reporters at Dairy Herd Management and local papers that the $4/cwt reduction, stacked on top of regular cooperative deductions, made it very hard to cash flow their operations. Those are the kinds of numbers that separate “tight” from “unworkable.”

Then there’s the federal order piece. USDA federal order data shows Class I (fluid) utilization in the Pacific Northwest order hovering around 20–22% in recent years, while “All Markets Combined” Class I utilization nationally is typically in the mid‑ to upper‑20% range. That gap matters because it means more milk in that region gets priced into lower‑valued Class III and IV pools rather than the Class I fluid market.

Regulation adds another layer. In Washington’s Yakima Valley, nitrate contamination concerns have led to consent decrees and added oversight of several large dairies, with some operations closing or restructuring under pressure from regulators and environmental groups, as described by Capital Press and Washington State Dairy Federation representatives. So producers there are trying to operate under below‑average Class I utilization, substantial environmental scrutiny, and a major co‑op project that’s gone significantly over budget.

The Pasco Lesson: When Co‑op Projects Become Producer Risk

The Darigold Pasco story has become a cautionary lesson about how cooperative‑led capital projects can shift risk back onto member farms.

Initial plan: A $600‑million, world‑class plant to process up to 8 million pounds of milk per day and export butter and powder to more than 30 countries.

Updated reality: Cost overruns pushing total investment toward $900 million, plus a $4/cwt deduction on member milk checks, with $2.50 directly tied to the plant and the remainder covering other financial shortfalls.

What this development suggests isn’t that co‑ops shouldn’t invest. It’s that:

The scale and risk of major projects need to be clearly communicated to members at the farm level.

There should be a realistic plan for what happens if budgets slip or markets change.

Producers need to know how much of their milk check might be diverted to debt service if things don’t go according to plan.

In plain terms, Pasco is a reminder of what co‑op membership really means: you’re not just selling milk—you’re partnering in capital decisions. That kind of surprise bill would hurt any operation, no matter how well run.

Southeast: Structural Tailwinds and Careful Optimism

Now slide across the map to the Southeast—Florida, Georgia, the Carolinas, parts of the lower Appalachians—and the structural picture looks very different.

USDA federal order summaries consistently show higher Class I utilization in Southeast‑oriented orders because of dense population and strong fluid‑milk demand. That built‑in demand has always mattered, but recent policy changes have made it even more important.

USDA’s federal order modernization decision restored the “higher‑of” Class I skim pricing formula and updated Class I differentials. Analysis found that these changes tend to increase Class I values more in fluid‑deficit markets in the East and Southeast than in regions dominated by manufacturing. Progressive Dairy and Dairy Herd coverage of the 2024–2025 seasons described many Southeastern producers as having one of their better financial years in a while, with improved Class I pricing, decent overall milk prices, and somewhat softer feed costs lining up in their favor.

So if you take two 500‑cow herds—similar genetics, comparable butterfat performance, similar feed efficiency—and put one in a strong Southeast Class I market and the other in a Western market with lower Class I utilization, it’s common for the Southeast herd to see significantly higher gross revenue at the same production level. That’s geography and policy working together, not just management.

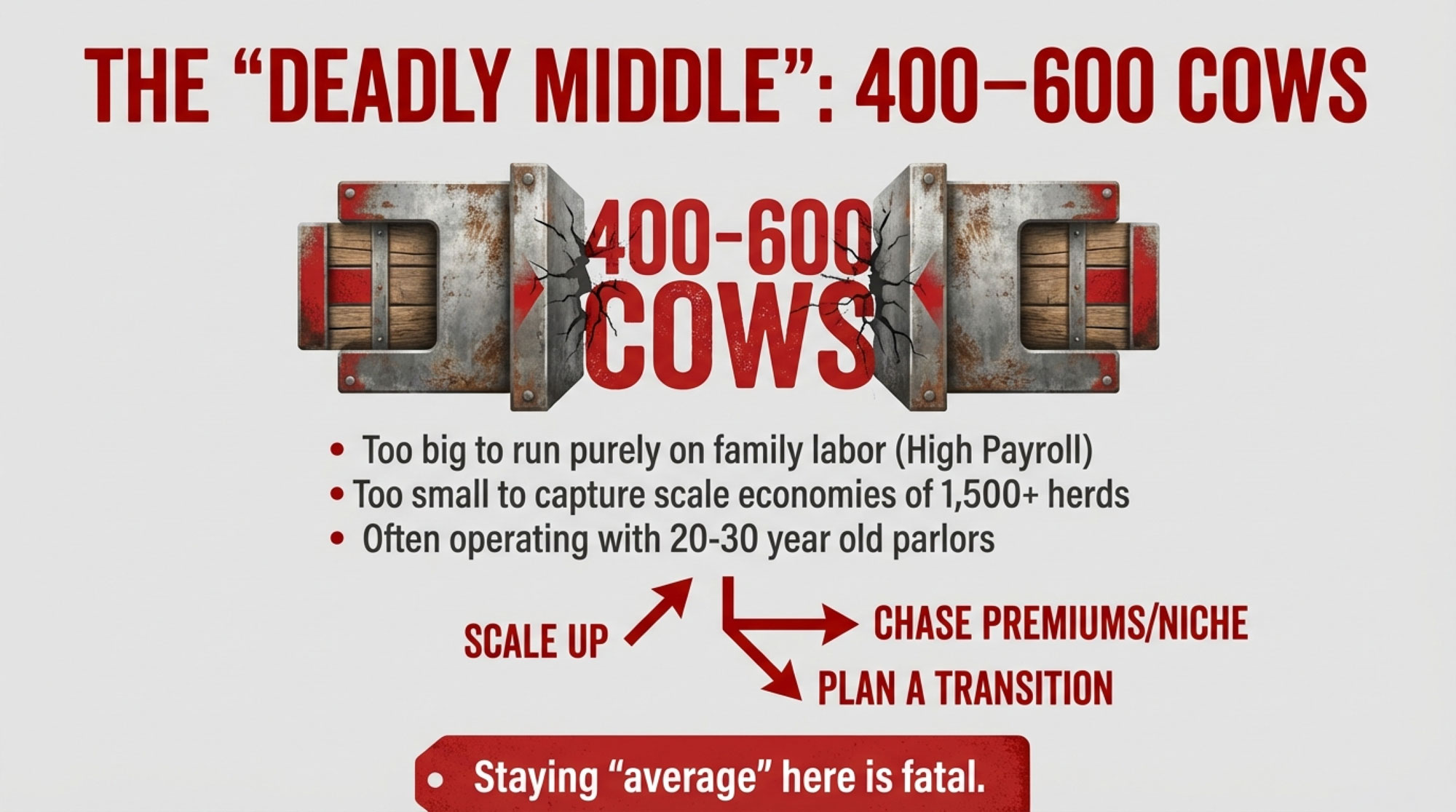

Upper Midwest: The “Deadly Middle” in America’s Dairy Heartland

In Wisconsin and Minnesota, the story is familiar but still evolving. This region still feels like the heart of U.S. dairying, but a certain band of herds is under real structural pressure.

USDA and state data show licensed dairy herds in Wisconsin falling from more than 10,000 in the early 2010s to under 7,000 by 2022, even as total state milk production stays near or at record highs. Farmdoc’s national work highlights the same pattern: sharp drops in herd numbers, modest changes in total cow numbers, and higher milk production overall.

Zisk Analytics’ profitability maps, featured regularly in Dairy Herd and other farm media, often show the Southeast and parts of the Southwest near the top for projected profit per cow, with many Upper Midwest herds—especially smaller and mid‑size ones—clustered in thinner‑margin categories. Plenty of Midwest producers say they’re still “making it work,” but they also admit there isn’t much cushion left if something goes sideways.

The 400–600 Cow Squeeze: Dairy’s “Deadly Middle”

This is the segment that’s really stuck in the middle.

Typical profile of the 400–600 cow “no‑man’s land” herd:

400–600 Holsteins, often in 20‑ to 30‑year‑old parlors or older freestalls

Solid, but not elite, feed efficiency and components

Bulk milk is sold into commodity pools, with limited premiums

Mix of family and hired labor, with real payroll costs

Some debt, but not extreme

Too big to run purely on family labor. Too small to fully capture the per‑cow cost advantages that 1,500‑ or 3,000‑cow herds can achieve. Not differentiated enough to earn strong value‑added premiums consistently. That picture lines up with Rabobank’s census‑based finding that farms with 100–499 cows have lost share of U.S. milk output while 1,000‑plus cow units gained share.

In many Wisconsin operations and across the Upper Midwest, what I’ve noticed is that these herds often feel boxed in. They can’t easily cut costs without hurting cow comfort or fresh cow management. They can’t easily scale without major capital. And they’re not always well‑positioned for organic, grass‑based, or on‑farm processing.

If you’re in that 400–600 cow band, the uncomfortable reality is that staying “average” has become a very risky strategy. Hoping your way out of structural math isn’t a plan—it’s a gamble. That doesn’t mean you’re out of options. It does mean this group needs especially clear decisions: whether to pursue scale, chase premiums, partner with neighbors, or plan a well‑timed transition. Just waiting for the next “good cycle” is a much bigger bet than it used to be.

California: Big, Efficient, and Still Under Pressure

We can’t talk about U.S. dairy without mentioning California. The state still has more dairy cows than any other and remains a powerhouse for cheese, butter, and milk powder.

Reports from the California Department of Food and Agriculture and USDA’s milk production summaries show that California’s dairy cow numbers have leveled off or edged down slightly in recent years, while per‑cow production remains among the highest in the country. Many of those cows are in large freestall and drylot systems with strong genetics, sophisticated feeding programs, and very deliberate fresh-cow management.

At the same time, California herds are navigating:

Groundwater and surface‑water regulations that shape where and how dairies can operate

Air quality and manure‑management rules that add cost and complexity

High land and labor costs relative to many other regions

A competitive but sometimes volatile processing environment

Analysts generally expect California to remain a major milk state, but to continue consolidating toward fewer, larger herds—similar to broader trends in the West. Some operations will double down on scale and efficiency, while others are leaning into value‑added products or multi‑state footprints to spread risk.

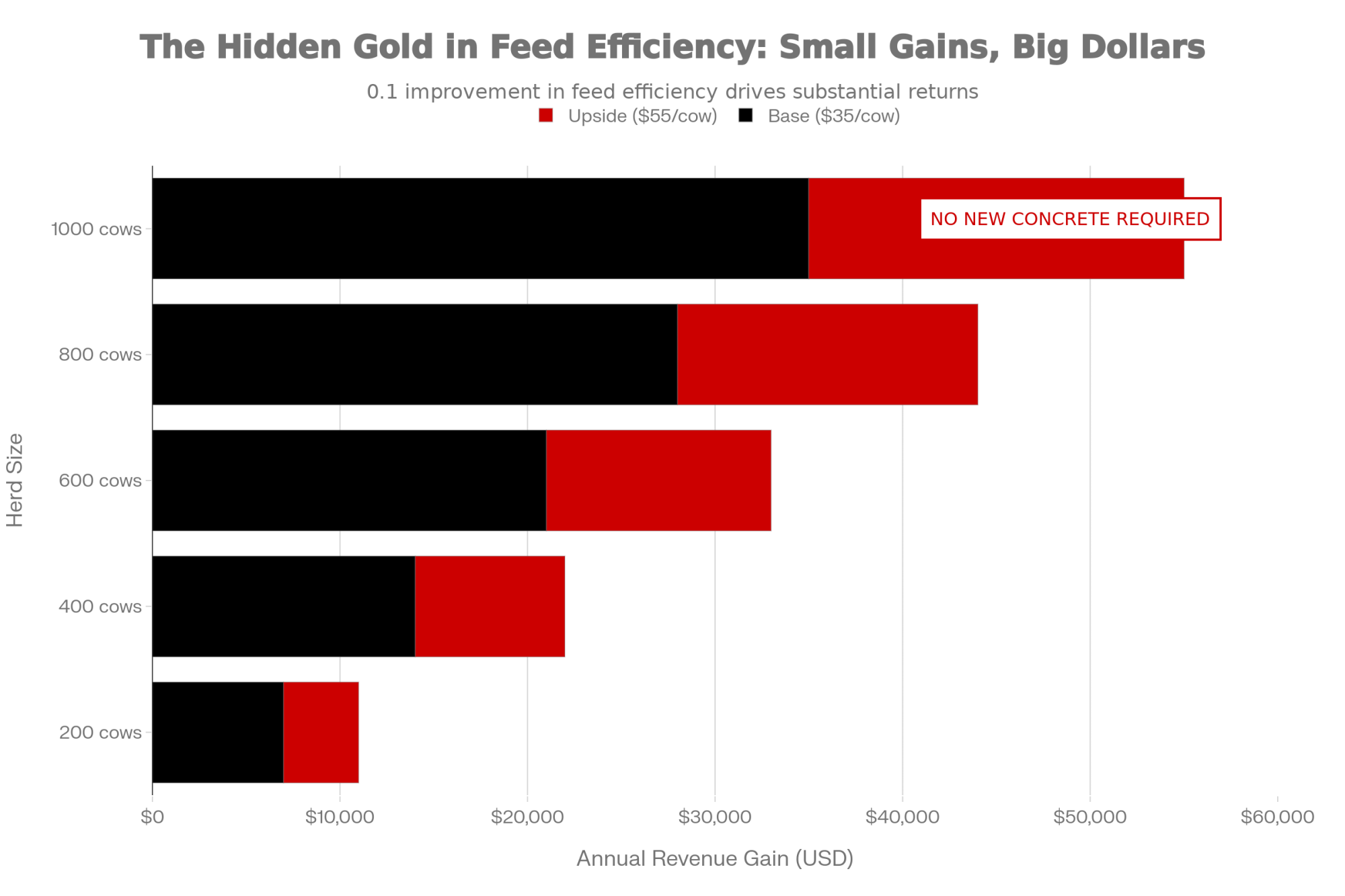

What Farmers Are Finding About Feed Efficiency

What farmers are finding, as they dig into their numbers with nutritionists and Extension, is that feed efficiency may be one of the most powerful levers they still fully control.

A national dairy Extension article on feed efficiency describes energy‑corrected milk per pound of dry matter as one of the strongest and most overlooked tools on many dairies. As a guideline, that article notes that for each improvement of 0.1 unit in feed efficiency—say, from 1.4 to 1.5—the increase in income can range from 15 to 22 cents per cow per day, assuming typical milk and feed prices. University economists and consultants have shown similar numbers, with Mike Hutjens demonstrating that feed efficiency improvements can quickly add tens of cents per cow per day to margins when feed costs are 15 cents per pound of dry matter.

To stay conservative, many advisors suggest budgeting 10–15 cents per cow per day for a 0.1 improvement. Over a full year, that’s about $35–55 per cow. On a 500‑cow herd, that’s roughly $18,000–27,500 a year from one modest bump in efficiency.

Feed efficiency improvements offer $35-55 per cow annually with no capital investment – on a 600-cow herd, that’s up to $33,000 from better forage allocation and transition management

Herd Size

Low Estimate ($35/cow)

High Estimate ($55/cow)

Total Range

200 cows

$7,000

$11,000

$7K–$11K

400 cows

$14,000

$22,000

$14K–$22K

600 cows

$21,000

$33,000

$21K–$33K

800 cows

$28,000

$44,000

$28K–$44K

1,000 cows

$35,000

$55,000

$35K–$55K

Peer‑reviewed work and Extension surveys on transition health and disease keep reinforcing that connection. A 2021 study of dairy herds in the journal Pathogens and subsequent reviews in Animals and other journals documented that mastitis and other health events increase treatment costs, reduce milk yield, and increase culling risk. Reviews of cow longevity and economic performance show that herds with fewer transition‑period problems and better reproductive performance can improve both animal welfare and profitability by extending productive lifespans.

On real farms, the herds that are squeezing more milk out of each pound of dry matter tend to share a few habits:

Forage testing and smart allocation. Forage analyses—NDF digestibility, starch, protein—are actually used, not just filed. The highest‑quality forages go to fresh and high‑producing cows, with lower‑quality lots assigned to late‑lactation cows and heifers. Extension specialists and industry nutritionists consistently show how differences in forage quality drive both butterfat performance and overall feed efficiency.

Transition period as a non‑negotiable. Comfortable close‑up and fresh pens, consistent DCAD and energy strategies, and careful monitoring of fresh cow intakes and health are built into daily routines. Field work and research keep showing that fewer fresh‑cow disorders mean higher peaks, better reproduction, and more efficient use of feed over a cow’s life.

Bunk management discipline. Feeding times are consistent, loading errors are minimized, refusals are checked, and feed is pushed up often enough that cows can access it throughout the day. Economists and nutritionists have pointed out how inconsistency—especially in timing and mix accuracy—can quietly erode both feed efficiency and component yields.

What’s encouraging is that most of these improvements don’t require new concrete. They require better measurement, clear targets, and consistent habits. In a year where margins are tight and interest isn’t cheap, that’s where a lot of the hidden money is.

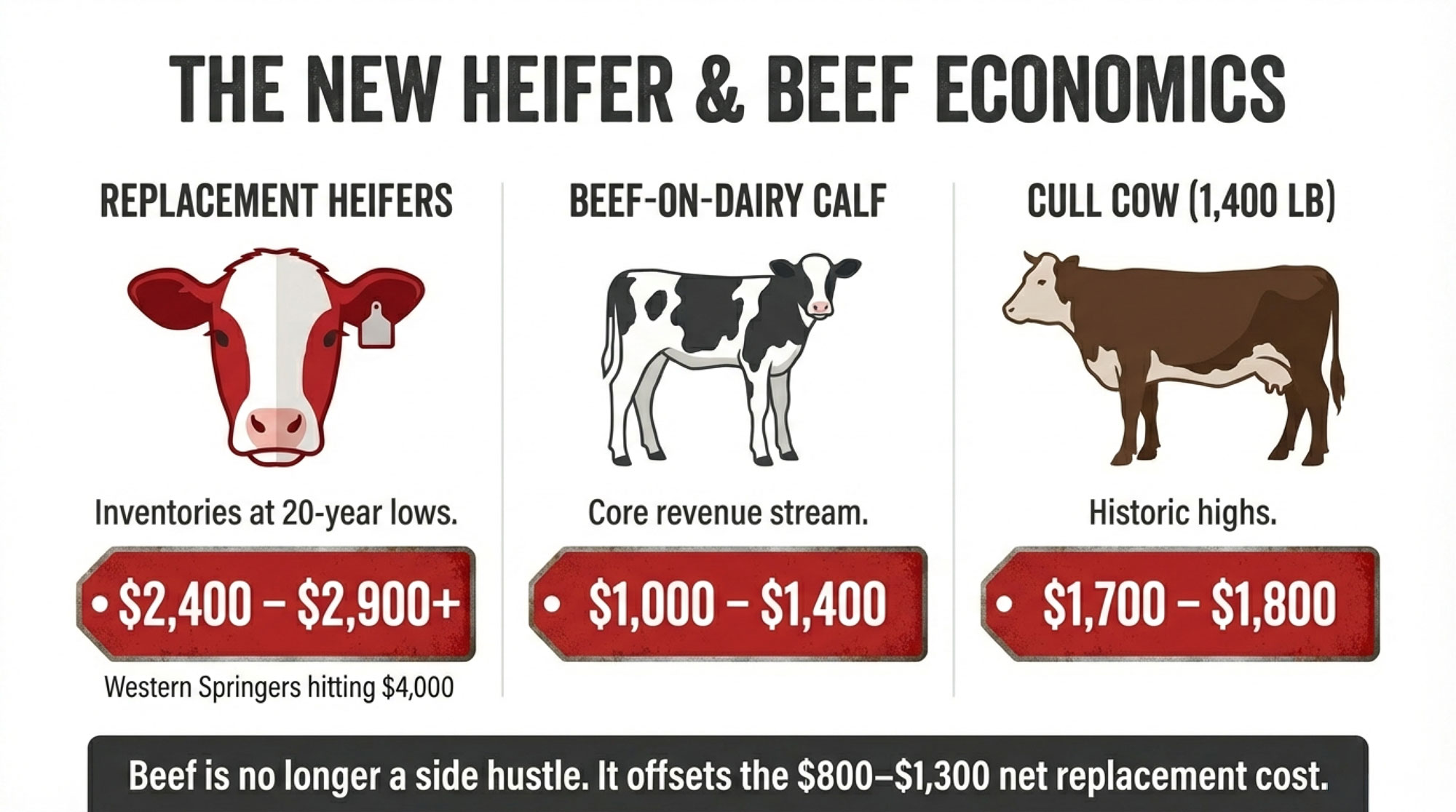

Replacement Heifers, Beef‑on‑Dairy, and the New Culling Math

Category

Typical 2025 Range (USD)

Annual Impact (500-cow herd, 35% cull rate)

Replacement heifer (national avg)

$2,400 – $2,900

+$420,000 – $507,500 (175 replacements)

Western springer (top end)

$3,500 – $4,000

+$612,500 – $700,000 (if sourcing West)

Beef-on-dairy calf(weaned/feeder)

$1,000 – $1,400

+$50,000 – $70,000 (50 calves)

Day-old beef-cross calf

$600 – $750

+$30,000 – $37,500 (50 calves)

Cull cow (sound, 1,400 lb)

$1,700 – $1,800

+$297,500 – $315,000 (175 culls)

Net replacement cost (heifer – cull)

$800 – $1,300 per head

+$140,000 – $227,500 annual

Cost per CWT across tank

$0.50 – $0.75/cwt

Spread across 125,000 cwt shipped

Cull price risk (20% decline)

–$340 – $360 per cull

–$59,500 – $63,000 if you wait

To understand why culling decisions feel so different now, you’ve got to look at heifers and calves.

A 2025 report from CoBank’s Knowledge Exchange, highlighted that U.S. dairy replacement heifer inventories have fallen to a roughly 20‑year low. CoBank’s modeling suggests heifer inventories could shrink by another 800,000 headover the next two years before beginning to rebound around 2027, based on predictions of breeding practice changes and herd demographics. That’s coming from sexed dairy semen being used more strategically on the top end of the herd, beef semen on the rest, and more disciplined replacement strategies.

USDA’s Agricultural Prices reports show average replacement dairy heifer values moving into the mid‑$2,000s nationally, with some states seeing averages in the high‑$2,000s. In Wisconsin, the average replacement heifer prices jumped from about $1,990 to roughly $2,850 year over year—about a 69% increase—as the beef‑on‑dairy trend curtailed dairy heifer supply. Reports also show Western Holstein springers bringing $4,000 or more at the top end.

On the beef side, allied beef‑on‑dairy programs have documented how crossbred calves that might have brought $600–700 a few years ago are now often selling for $1,000–1,400 in many markets, depending on weight and timing, and how reports of day‑old beef‑cross calves at $600–750 in some Midwest and Plains auctions have become more common. Straight Holstein bull calves, as most of you unfortunately know from the checks, still trade at much lower levels.

In CoBank’s 2025 outlook, Corey Geiger, lead dairy economist at CoBank, emphasized that beef is contributing a larger share of total dairy revenue every year and that beef‑on‑dairy breeding has moved a significant portion of calves out of replacement pipelines and into beef streams.

Heifer & Beef‑on‑Dairy Economics at a Glance

Category

Typical 2025 Range

Replacement heifer (national avg)

$2,400–$2,900+

Western springer (top end)

$3,500–$4,000+

Beef‑on‑dairy calf (weaned/feeder)

$1,000–$1,400

Day‑old beef‑cross calf

$600–$750

Cull cow (sound, 1,400 lb)

$1,700–$1,800

Net replacement cost

$800–$1,300/head

Spread across the tank, that net replacement cost can quickly add 50–75 cents per cwt to your true cost of production, depending on cull rate and herd size. When you add in the fact that the transition period is still the highest‑risk phase of a cow’s life for disease, culling, and reproductive failure—something documented repeatedly in herd‑health research and field data—you can see why many herds are taking a closer look at which cows they ship and which they keep.

What I’ve noticed, talking with producers from the Upper Midwest to California’s Central Valley, is that many herds are shifting in three ways:

Using culling to clean up truly chronic problems first: repeated mastitis or high SCC, cows that don’t breed back after multiple services, recurring lameness, and persistently low fat‑protein corrected milk.

Being more thoughtful about longevity: hanging on to efficient, healthy fourth‑ or fifth‑lactation cows if they’re still producing well and breeding back, instead of automatically moving them just because of age. Recent work on cow longevity and economic performance from European and North American studies supports the idea that well‑managed, longer‑lived cows can improve both welfare and profit.

Raising or buying fewer replacement heifers overall, but putting more emphasis on genetics, calf and heifer management, and a smooth transition into the milking herd for those they do keep.

Three Decisions That Matter in the Next 90 Days

Given all this—consolidation, regional differences, heifer inventories, processor investment—three near‑term decision areas keep coming up in conversations with producers, nutritionists, and lenders.

1. Culling While Beef Prices Are Still Favorable

Right now, cull cow values are historically strong in many regions. USDA market reports and industry summaries show sound cull cows bringing high prices relative to long‑term averages, supported by a tight national beef supply after heavy beef‑cow liquidation. Beef‑market outlooks in USDA’s Livestock, Dairy, and Poultry Outlook and land‑grant analyses note that as the U.S. beef cow herd slowly rebuilds from very low levels, cull prices could soften over the next couple of years, especially if slaughter numbers ease.

For a 1,400‑pound cow, that’s easily a $250–300 swing per head between today’s strong prices and a softer market. For a 500‑cow herd with a 35% cull rate, that’s $40,000–50,000 across the year. So if you’ve got cows that are clearly on your “watch list”—chronic mastitis, repeated reproductive failures, recurring lameness that never fully resolves, consistently poor butterfat performance—the timing matters.

A simple cull checklist that many herds are using with their vets and consultants looks like this:

Chronic mastitis or consistently high SCC despite treatment

More than two or three unsuccessful breedings this lactation

Recurring hoof problems affecting production or mobility

Persistently low fat‑protein corrected milk compared with pen mates

At a recent Extension meeting in the Upper Midwest, a herd manager described sitting down with their vet and nutritionist, flagging about 60 cows that met those criteria, and prioritizing shipping them over several weeks while beef prices stayed strong. The cull income went straight to reducing their operating line and funding upgrades in their fresh‑cow area. Examples like that are showing up more often in Extension case studies and farm financial workshops.

If cull prices are 20% lower next year, are there cows you’ll wish you’d moved sooner? That’s the kind of question this window forces you to ask.

2. Treating Feed Efficiency as a Standing Agenda Item

We’ve already walked through the economics: a 0.1 bump in feed efficiency can reasonably be worth $35–55 per cow per year, or $18,000–27,500 on a 500‑cow herd, using conservative values drawn from Extension and economic analysis.

What farmers are finding is that the herds capturing that value aren’t necessarily spending more—they’re just managing more intentionally. A practical way to bake feed efficiency into your routine is to treat it as a standing agenda item at your regular herd meetings.

Here’s a simple framework to work from:

This month: forage and ration review

Are all current forages tested for NDF digestibility, starch, and protein?

Are the highest‑quality forages being targeted to fresh and high‑producing groups?

Are ration changes reflected in updated dry‑matter intake targets for each group?

This quarter: transition and fresh cow focus

Are close‑up and fresh pens overcrowded or short on bunk space?

Are fresh cows being checked daily for intakes, temperature, and behavior during the first 10–14 days in milk?

Are DA, ketosis, metritis, and early culling rates tracked and reviewed with your vet and nutritionist?

Every week: bunk management habits

Are feeding times consistent from day to day?

Are refusals checked and recorded, not just guessed at?

Are feed push‑ups happening often enough to keep feed in reach between feedings?

From Wisconsin freestalls to Texas dry lot systems to Northeastern tie‑stalls, I’ve noticed the same pattern: the herds that treat feed efficiency as a core KPI—not just a once‑a‑year number—tend to be the ones that stay more resilient when margins tighten.

3. Getting Ahead of Liquidity and Risk Management

Class III futures and industry outlooks remain volatile for 2026, with projections shifting as feed costs, export demand, and herd size estimates change. USDA’s 2025 dairy outlooks highlight a wide range of possible milk‑price outcomes depending on those factors, rather than a single clear price path. For herds with low cost of production and strong efficiency, most reasonable price scenarios can still work. For those needing $18–19 just to break even—including full debt service and family living—it’s worth paying very close attention.

Farm financial advisors—from land‑grant universities to private consultants—keep coming back to a few core moves:

Use today’s strong beef and calf checks to build working capital. Paying down the operating line or building cash reserves when beef and beef‑cross calf prices are high gives you more room to maneuver if milk prices under‑perform. With interest costs where they are, every dollar you take off your line is worth more than it used to be.

Sit down with your lender early, not late. Bringing updated cost‑of‑production numbers, your culling and heifer plan, and your feed‑efficiency priorities to the table changes the tone: you’re managing risk, not just reacting to it. University Extension finance specialists make the same point in their 2024–2025 dairy profitability guides.

Match your risk tools to your comfort level. That might mean Dairy Margin Coverage for smaller herds, Dairy Revenue Protection or LGM for others, and selective use of forward contracting on milk or feed. The goal isn’t to hit the top of the market every time; it’s to keep the worst‑case scenarios off the table.

As one Wisconsin‑based advisor told a group at a recent meeting, you don’t want your first serious talk with the bank to be when you’re already in trouble. You want it to be when you still have options.

Why Processors Are Still Building While Farms Are Closing

A question that comes up a lot right now is: if producers are under this much pressure, why are processors pouring billions into new plants?

CoBank’s Knowledge Exchange team tackled that in a 2025 report. They estimate that the U.S. is undergoing a historic $10‑billion investment in new dairy‑processing capacity, expected to come online through 2027, much of it in large cheese, powder, and extended‑shelf‑life beverage plants in Texas, the Southwest, the Midwest, and the Northeast. Darigold’s Pasco facility is one example of these large investments in the Northwest.

Rabobank’s consolidation reports reinforce the big picture: processors see long‑term domestic and export demand for dairy proteins and fats, but expect that demand to be met by fewer, larger, more efficient herds with lower per‑unit costs. Modern plants designed to process 5–8 million pounds of milk per day require high utilization and a consistent supply to remain profitable.

Those plants aren’t being built for a world with more small herds. They’re being built assuming fewer, bigger suppliers who can hit volume and quality specs every day.

When you talk with processor representatives at meetings and plant tours, what often comes through is that they’re laser‑focused on reliability. They want suppliers who can hit volume, component, and food‑safety targets day in and day out. It’s simply easier to do that with a smaller group of large herds than with hundreds of small ones.

That doesn’t mean smaller and mid‑size farms are written out of the story. But it does mean they’re more likely to thrive if:

They’re among the most efficient herds in their region.

They supply processors that value specific quality traits—such as components, traceability, animal care, or local branding.

They focus on premium or niche markets where volume isn’t the only metric that matters.

So Where Does This Go—and What Can You Do?

USDA’s long‑term baseline projections, combined with outlooks from CoBank and Rabobank, point in a broadly similar direction:

Fewer dairy farms overall, but national cow numbers are hovering around 9–9.5 million in the medium term.

A growing share of milk is coming from herds with 1,000 or more cows, continuing the trend already highlighted by the 2022 Census and consolidation analyses.

Continued growth in regions like Texas, New Mexico, Idaho, South Dakota, and parts of the Southeast, with slower growth or contraction in higher‑cost or heavily regulated areas such as parts of the PNW and California.

Ongoing processor consolidation and large‑scale plant investments, including dry lot and freestall‑based supply clusters in the Plains and Southwest.

Nobody can promise exactly what the five‑year average milk price will be. But the structural forces—consolidation, plant expansion, heifer shortages, beef‑on‑dairy, Class I reform—are not hypothetical. They’re visible in USDA data, industry reports, and the checks you’re cashing.

Different operations will respond differently. A 4,000‑cow dry lot in west Texas, a 1,600‑cow freestall in California’s Central Valley, a 600‑cow parlor dairy in Wisconsin, and a 200‑cow grazing herd in Vermont all have different strengths, constraints, and family goals.

What’s encouraging is that some of the most important questions are the same for all of them:

Where’s our real edge—cost of production, components, quality, location, niche market, or some combination?

Are we measuring feed efficiency, fresh cow performance, and butterfat and protein yields clearly enough to guide decisions?

Does our region and processor mix support the kind of operation we want to be five to ten years from now?

If not, what realistic paths do we have—scaling up, shifting markets, partnering with neighbors, or planning a dignified exit or transition?

The Bottom Line: Three Moves for the Next 18 Months

If you boil this down, here’s the hard truth: hoping the next “good cycle” will fix structural math is a much riskier bet than it used to be. In the next 18 months, most herds will be better off if they:

Ship chronic problem cows while beef is still strong and replacement math still pencils, rather than waiting for cull prices to soften.

Put a real dollar figure on a 0.1 feed‑efficiency gain for their own herd and pick one or two habits to move that number, using Extension benchmarks and their own records.

Look their processor and region in the eye—on paper—and decide whether they’re doubling down, diversifying, or slowly pivoting, given the $10‑billion processing build‑out and the consolidation patterns already underway.

The “18‑month window” isn’t a countdown clock to disaster. It’s a realistic horizon in which most herds still have meaningful choices—about culling, feed efficiency, liquidity, and long‑term direction. Those choices are a lot easier to make while you still have room to maneuver than when your bank, your cooperative, or your cash flow is making them for you.

What I’ve noticed, talking with producers from British Columbia to Florida and from California to New York, is that the farms that come through tough stretches in good shape usually aren’t the ones with the fanciest barns. They’re the ones that combine solid cow sense with uncomfortable honesty about their numbers, their region, and their options—and then act before circumstances force their hand.

There’s still time to be one of those herds. The real opportunity in this next 18‑month stretch is to quietly, deliberately tilt the odds in your favor for whatever dairy looks like in 2030 and beyond.

Key Takeaways

Farm exits no longer fix milk prices. USDA’s 2022 Census shows 39% fewer dairy farms since 2017, yet total U.S. milk still climbed to 226 billion pounds—large herds absorb the volume, and the old “sellouts tighten supply” assumption no longer holds.

Heifer inventories are at a 20-year low—and still falling. CoBank projects another 800,000-head decline before a 2027 rebound, pushing replacements into the mid-$2,000s nationally and past $4,000 for top Western springers.

Geography now rivals genetics for survival. Darigold’s $4/cwt Pasco deduction, below-average Class I utilization in Western orders, and stronger fluid returns in the Southeast are making your region and processor mix as important as your herd’s butterfat.

Feed efficiency is hidden cash you already control. A 0.1 improvement can add $35–55 per cow per year—up to $27,500 on a 500-cow herd—without new buildings or equipment.

The next 18 months are a decision window, not a waiting room. Cull chronic cows while beef checks are strong, put a real dollar target on efficiency gains, and sit down with your lender while you still have options—not after your cash flow decides for you.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Feed Smart: Cutting Costs Without Compromising Cows in 2025 – Grab the blueprint to shave $470 per cow off your annual feed bill. This guide delivers precise procurement tactics for 2025’s volatile markets, arming you with the forage analysis and ration discipline needed to thrive.

Decide or Decline: 2025 and the Future of Mid-Size Dairies – Face the hard truth about surviving the ‘deadly middle’ of dairy’s structural shift. This analysis breaks down five-year positioning for 500-head herds, unpacking the exact moves needed to protect your equity before regional processor leverage shifts entirely.

Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – Stop leaking profit by treating beef-on-dairy like a side hustle. This deep dive exposes the genomic multipliers and reproductive benchmarks that separate elite operators from the 72% of herds currently playing the game wrong.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

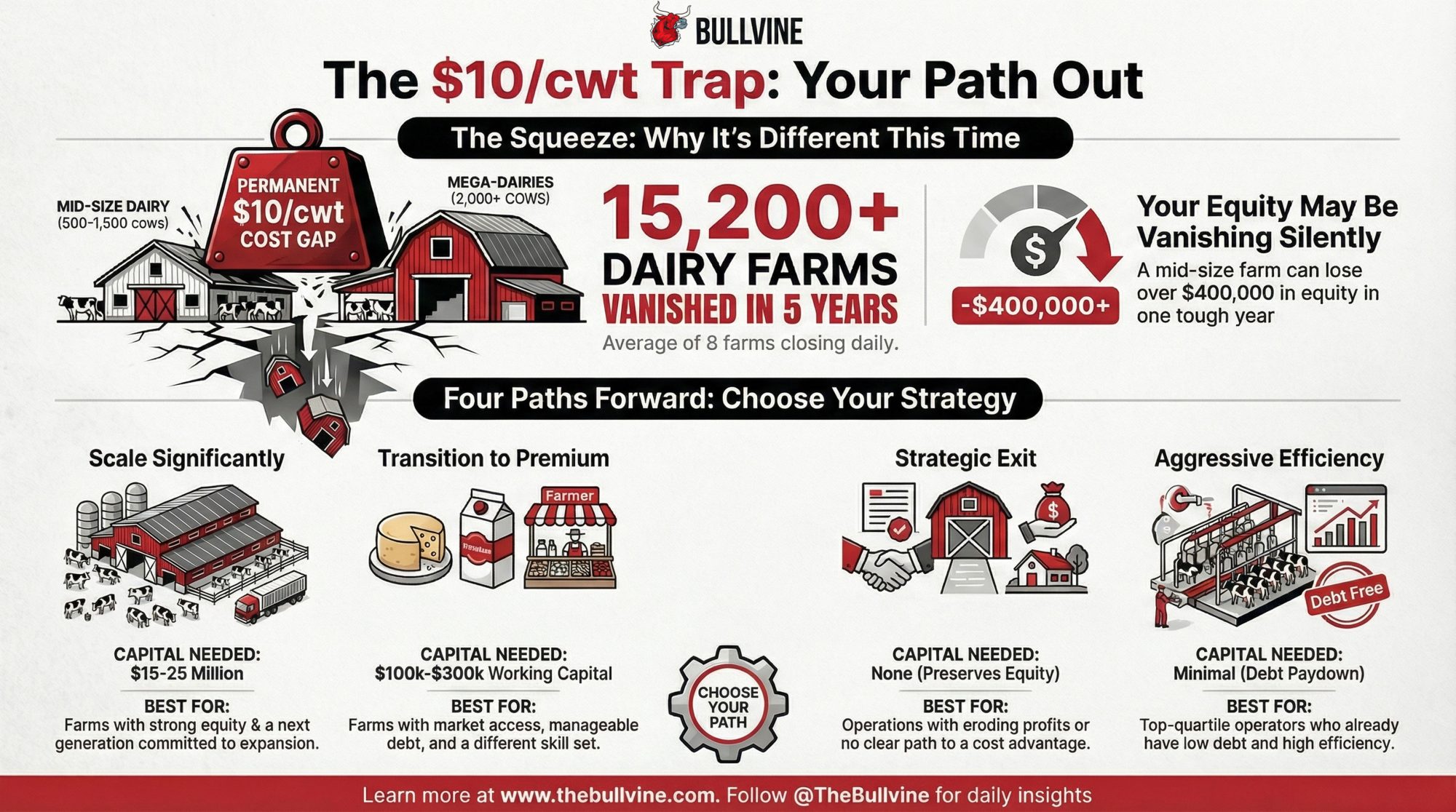

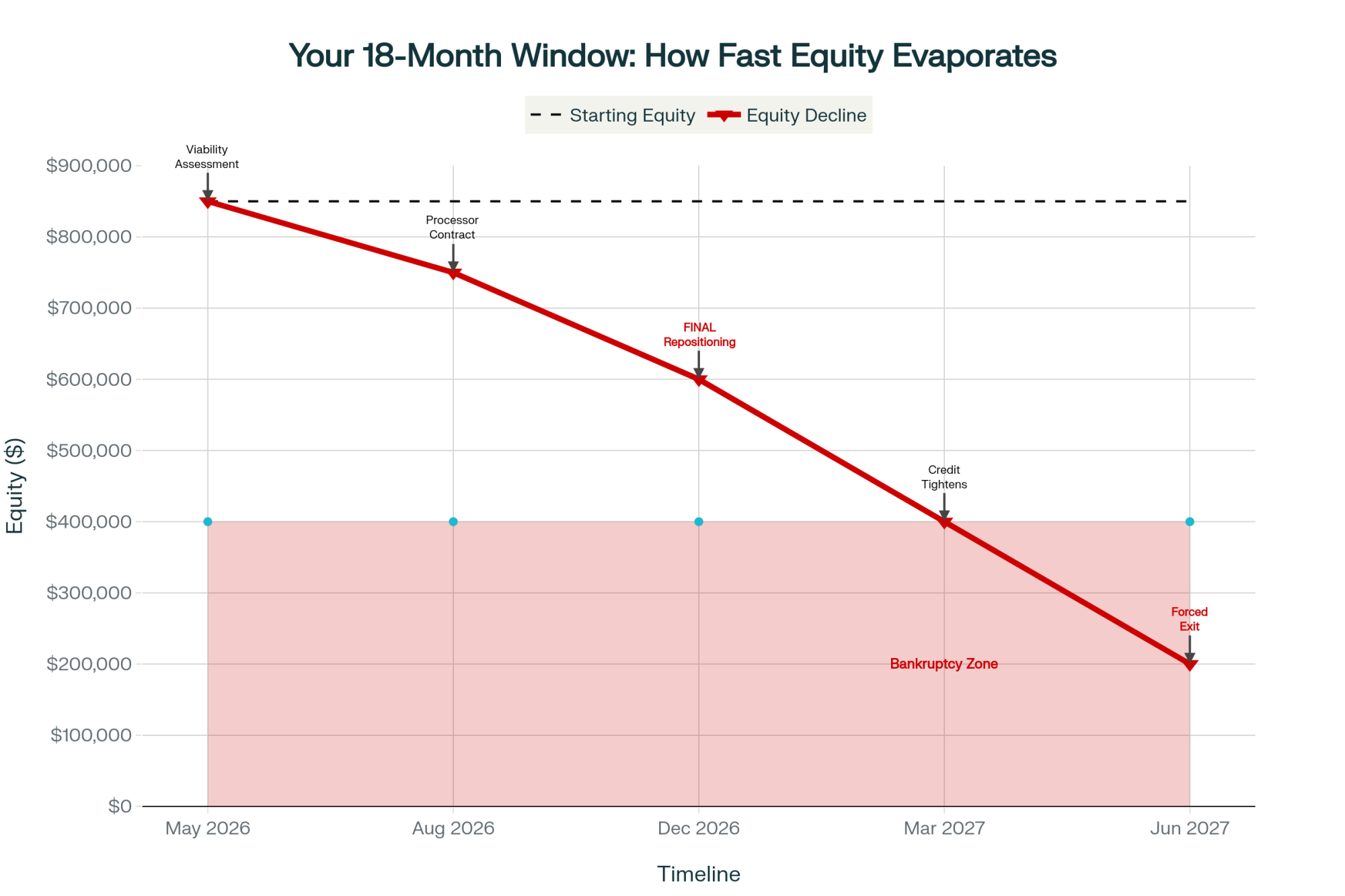

Eight dairy farms close every single day in America. Understanding what’s driving this consolidation—and your options for navigating it—has never been more important.

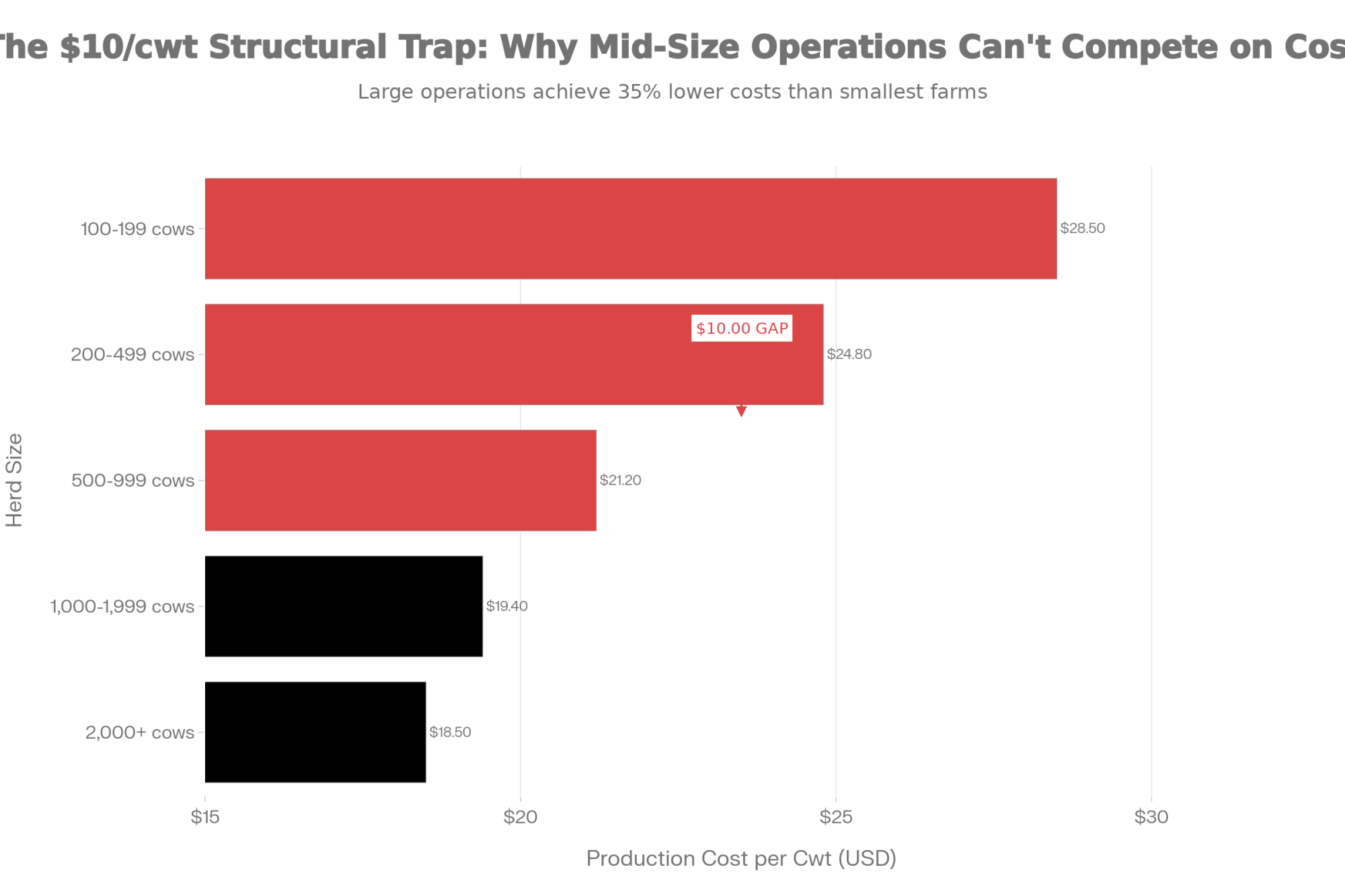

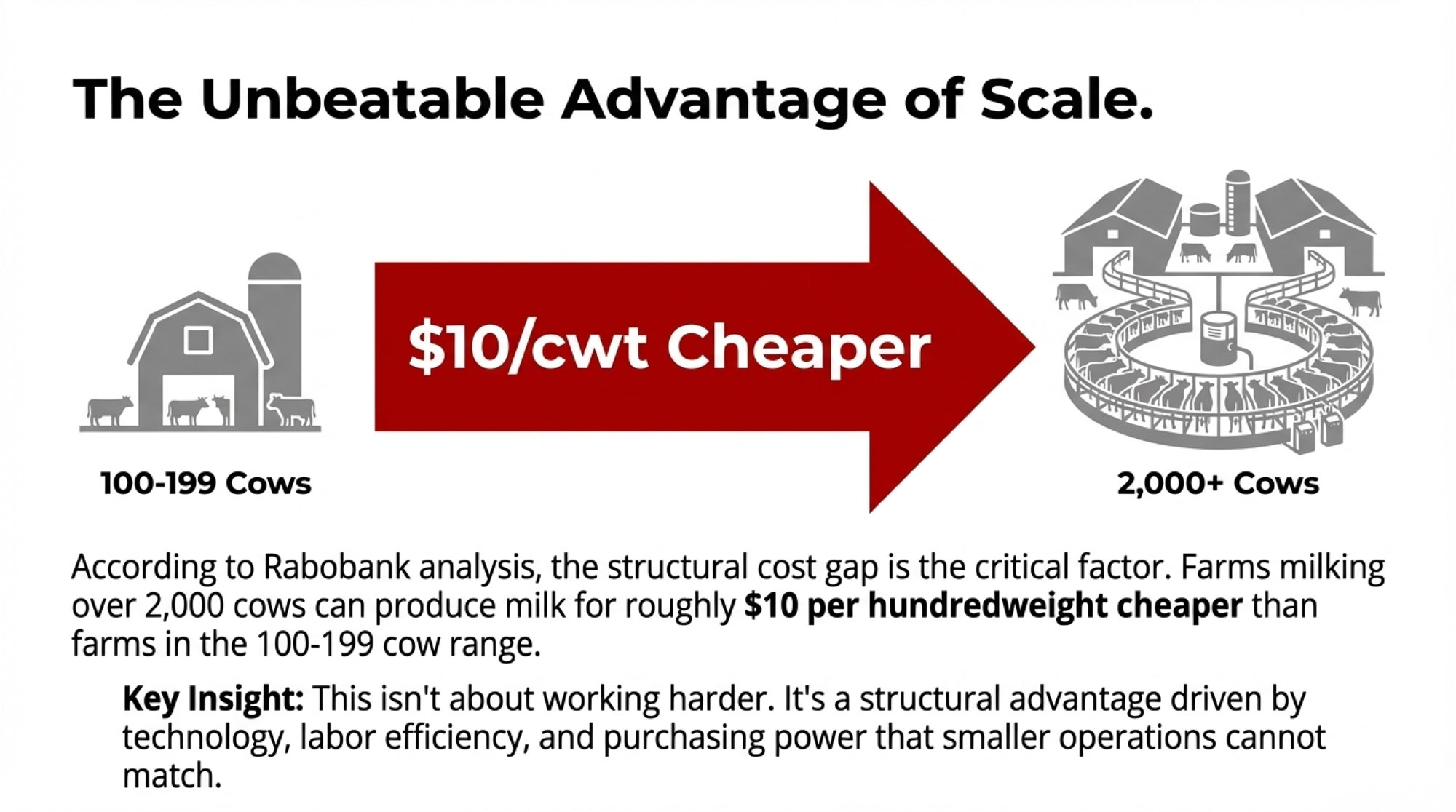

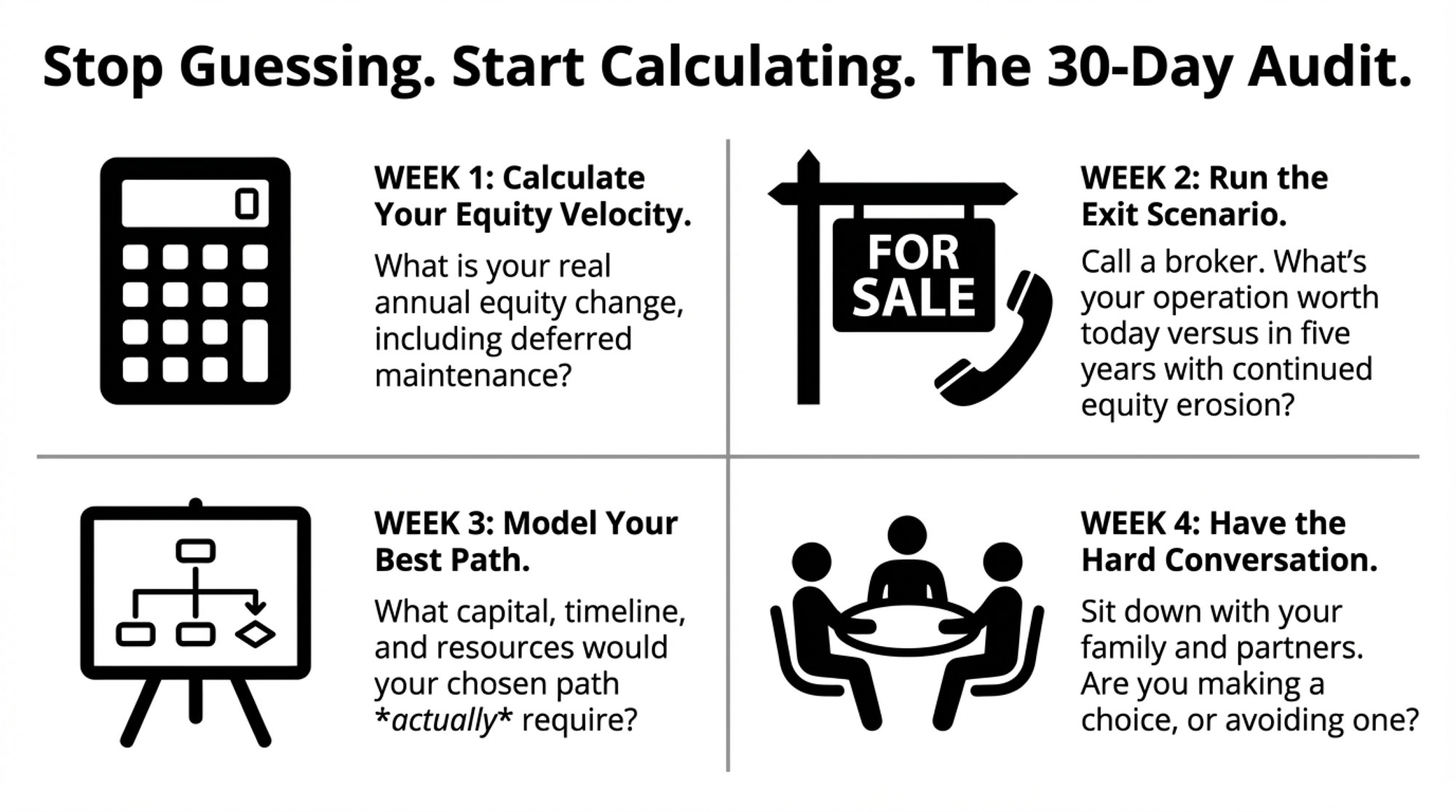

Executive Summary: Eight dairy farms close every single day in America—and mid-size operations (500-1,500 cows) are taking the hardest hit. USDA Census data shows over 15,200 farms vanished between 2017 and 2022, driven by a $10/cwt cost gap that gives 2,000+ cow operations a decisive structural advantage. This isn’t a price cycle to wait out; it’s a permanent industry transformation, and silence is a losing strategy. This analysis breaks down four realistic paths forward—scale significantly, transition to premium, exit strategically, or pursue aggressive efficiency—with specific capital requirements, timelines, and success factors for each. The essential first move: calculate your “equity velocity” to determine if you’re silently bleeding $400,000+ annually while your balance sheet looks stable. Take the 30-Day Financial Audit Challenge and choose your path before the market chooses it for you.

That number stopped me cold when I first calculated it. Eight farms. Every day. For five years straight.

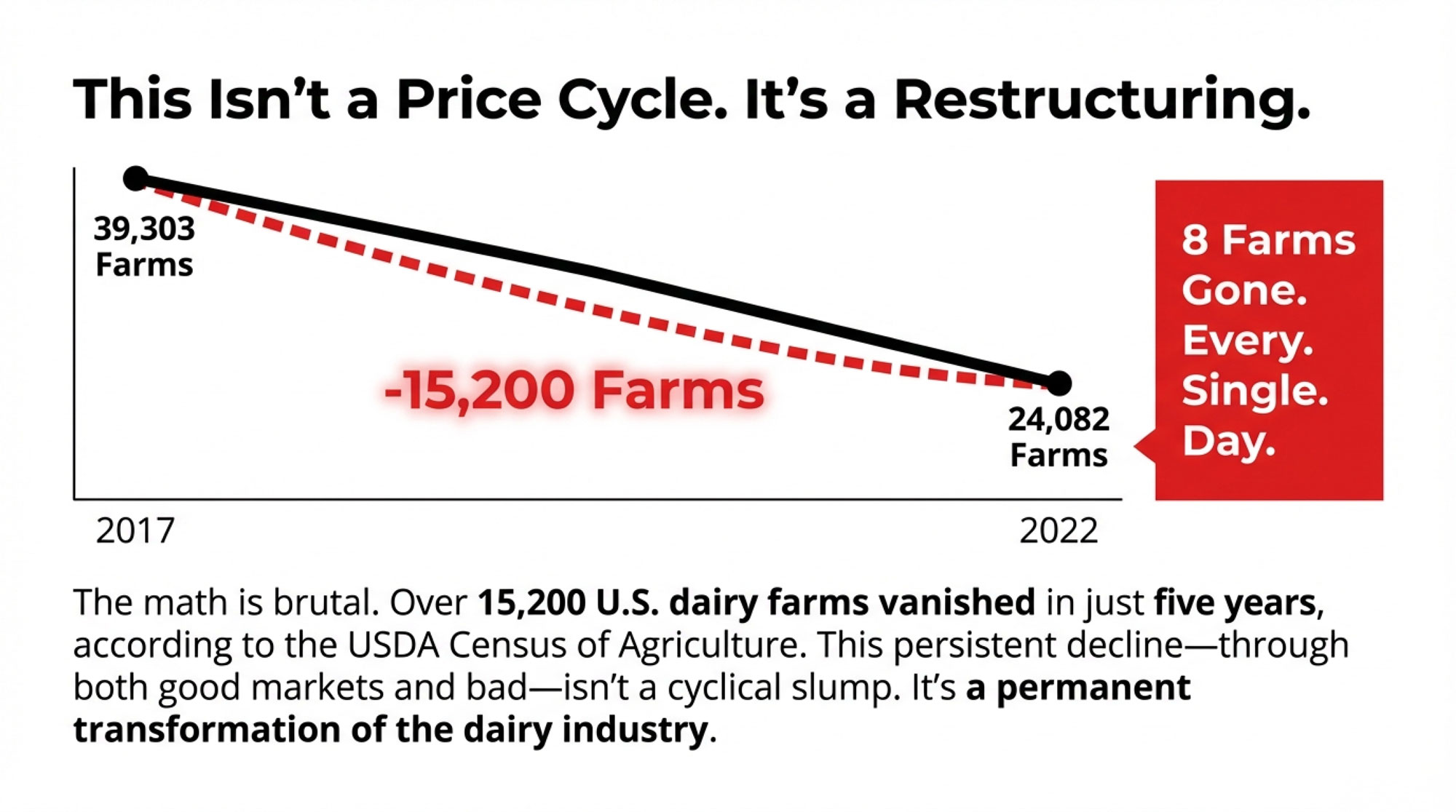

USDA’s 2022 Census of Agriculture documents the math clearly: U.S. dairy operations dropped from 39,303 in 2017 to 24,082 in 2022—more than 15,200 farms gone in half a decade. The closures slow down during high-price periods, but they never actually stop. And that persistence through both good markets and bad tells us something important: we’re not watching a normal price cycle play out. This is a structural change.

USDA Census data reveals 15,221 dairy farms vanished between 2017-2022—an average of 8.2 operations closing every single day for five years straight, with no slowdown during high-price periods

What’s driving it? Part of the answer showed up in some Canadian grocery pricing data I was reviewing recently. During the period when farm input costs were climbing sharply, food retailer margins expanded rather than compressed. Much of the additional money consumers were paying didn’t flow back to producers. It accumulated in other parts of the supply chain.

Now, I want to be fair here—retailers face their own cost pressures and competitive dynamics. But the pattern illustrates something Dr. Michael Boehlje has written about extensively. He’s a Distinguished Professor Emeritus in Agricultural Economics at Purdue who’s studied farm and agribusiness management for decades, and his analysis suggests that commodity supply chains tend to extract value from the farm level when one segment has more pricing power than another. That’s not an accusation. It’s just how these systems often work.

The question for dairy producers isn’t whether this structural shift is happening—the data makes that clear. The question is what to do about it.

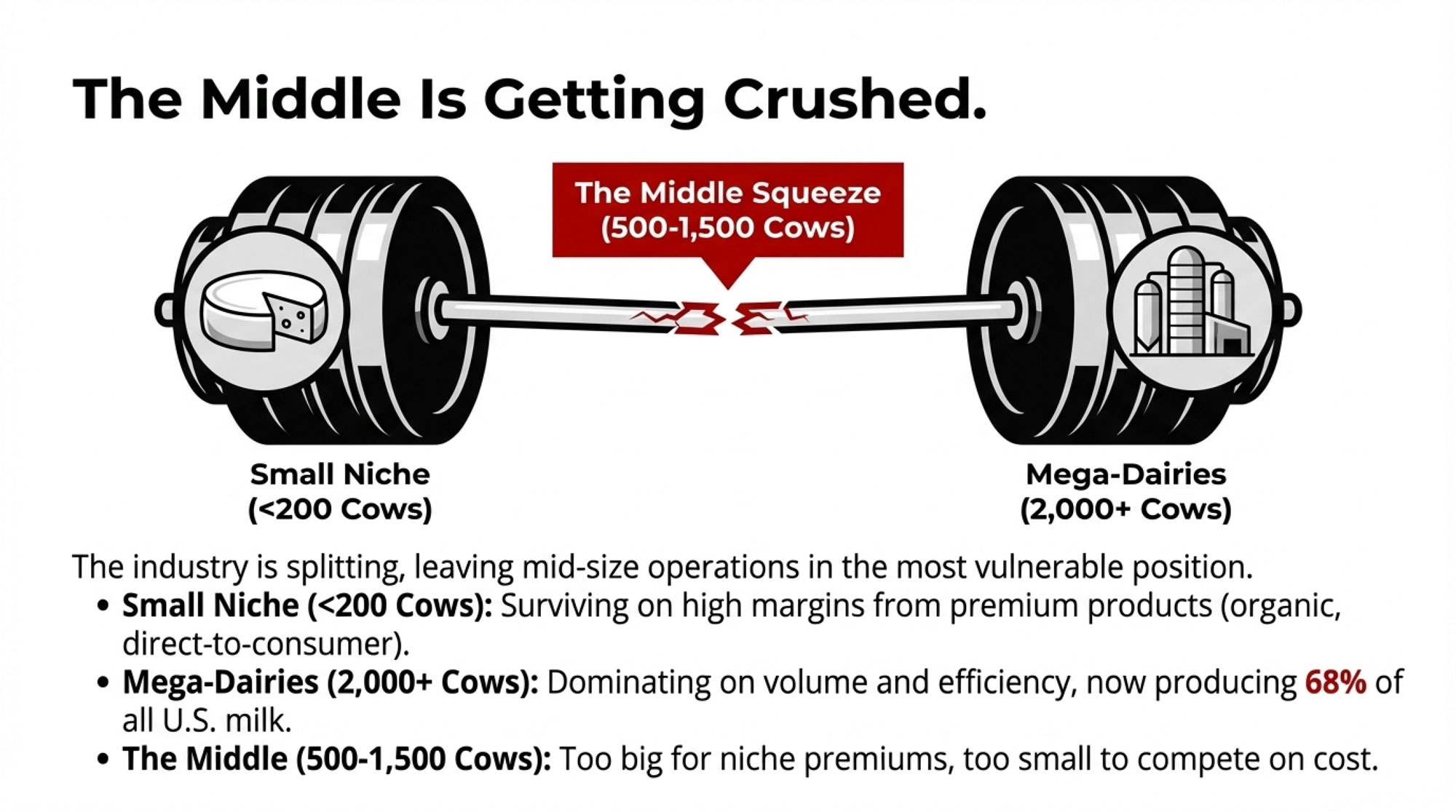

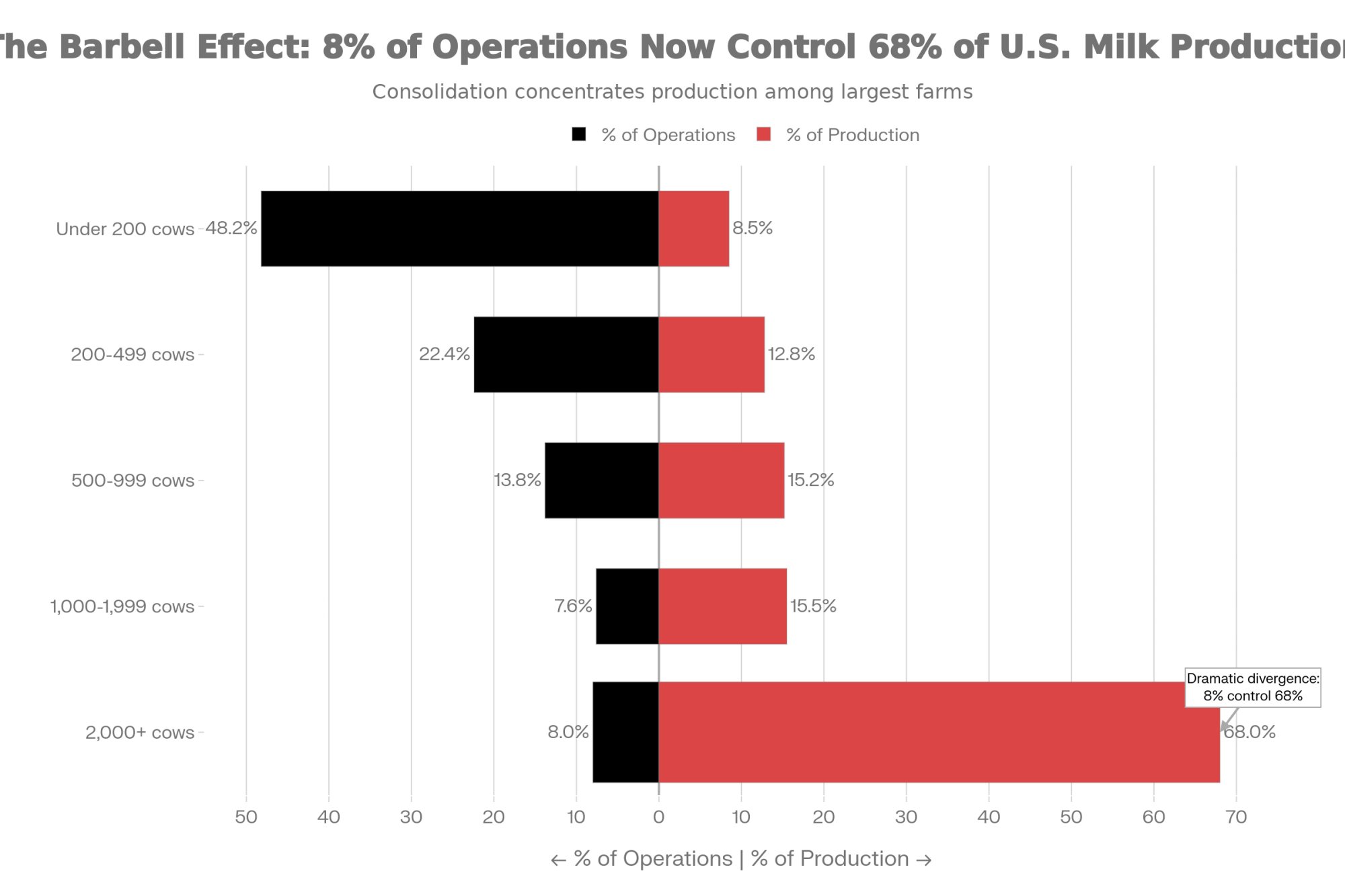

The Barbell Effect: Where the Industry Is Headed

What we’re witnessing isn’t random attrition. It’s a fundamental reshaping of the industry into what economists call a “barbell” structure—growth at both extremes while the middle gets squeezed out.

On one end: Small operations under 200 cows that have carved out premium niches—organic, grass-fed, farmstead cheese, direct-to-consumer sales. They survive on margins, not volume.

On the other end: Large operations running 2,000+ cows with aggressive automation, professional management teams, and cost structures that commodity markets actually support. Rabobank data shows these large operations now account for roughly 68% of U.S. milk production.

In the middle: Operations running 500-1,500 cows that are too big to capture premium pricing but too small to achieve the cost efficiencies of mega-dairies. This is where the structural pressure is most intense—and where farm losses are concentrated.

Operation Size

% of Operations

% of Milk Production

Under 200 cows

48.2%

8.5%

200-499 cows

22.4%

12.8%

500-999 cows

13.8%

15.2%

1,000-1,999 cows

7.6%

15.5%

2,000+ cows

8.0%

68.0%

The Consolidation Numbers Tell a Consistent Story

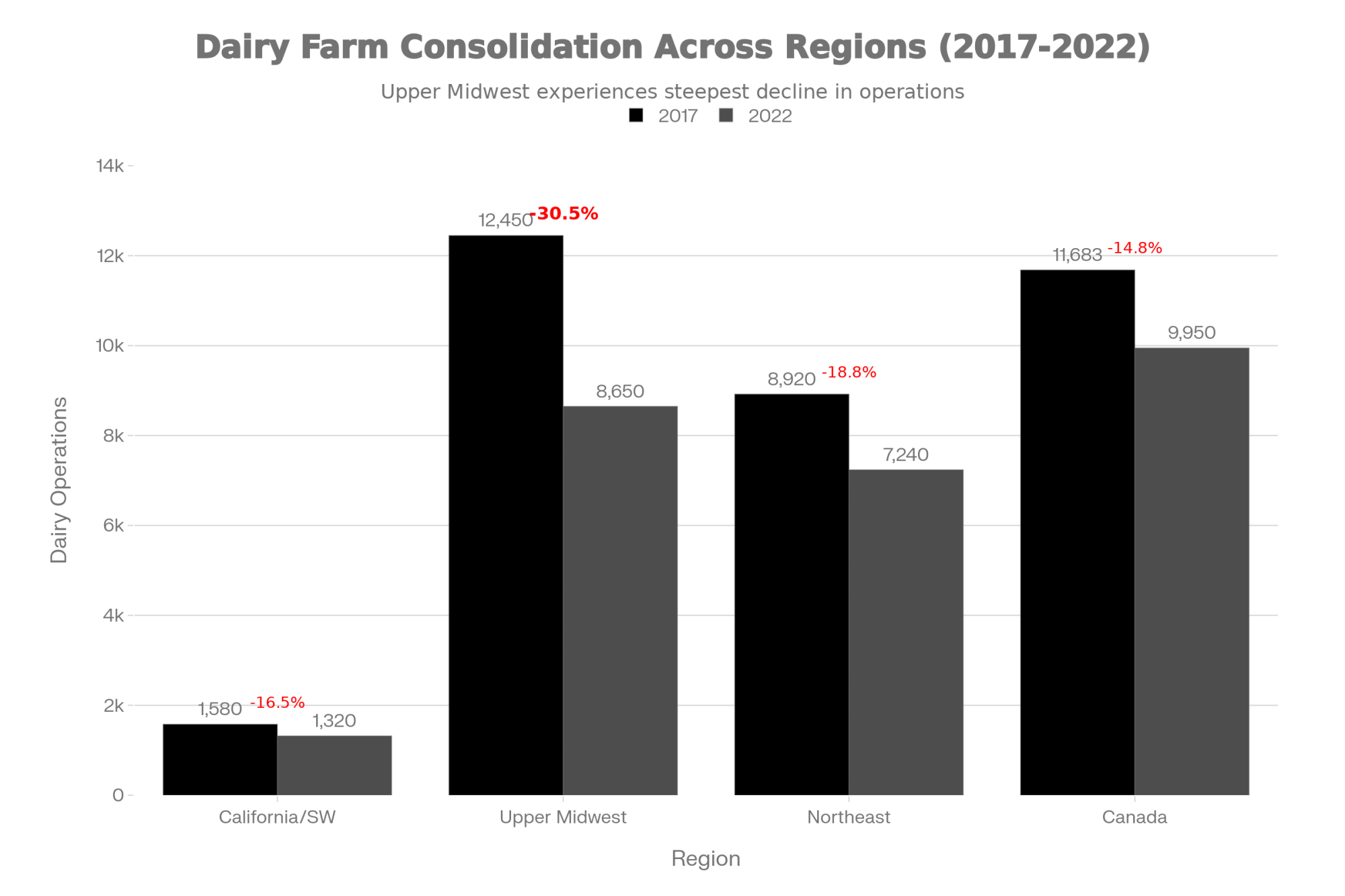

The trajectory has been remarkably steady across regions and time periods, which is what makes it feel structural rather than cyclical.

The Upper Midwest lost 3,800 dairy operations in five years—a 30.5% collapse that’s double California’s rate, where consolidation has largely stabilized after shifting to mega-dairies decades ago

Wisconsin DATCP licensing data shows the state lost 818 dairy farms in 2019, another 455 in 2023, and roughly 400 more in 2024. Add up the losses since 2019, and you’re past 1,500 operations—gone from a state that still thinks of itself as America’s Dairyland. Minnesota shows similar patterns. So does New York.

What surprised me when I dug into the regional data is how differently this plays out depending on where you’re farming.

Rabobank data shows 2,000+ cow operations produce milk at $18.50/cwt while 500-cow dairies struggle at $21.20/cwt—a $2.70 permanent structural disadvantage that bleeds $270,000 annually on 10 million pounds of production

In California’s Central Valley and the Southwest—Texas, New Mexico, Arizona—consolidation has largely run its course. These regions now operate predominantly with very large dairies, many running drylot systems suited to arid climates, that have achieved cost structures that smaller operations struggle to match. Lucas Fuess, a senior dairy analyst at Rabobank, has noted that farms milking more than 2,000 cows can produce milk about $10 per hundredweight cheaper than farms running 100-199 cows. That’s not a small advantage. Over a year of production, that gap becomes the difference between building equity and burning through it.

The Upper Midwest presents a more complicated picture. You still find significant numbers of 200-800 cow operations in Wisconsin and Minnesota, but the economics are getting harder. The survivors tend to fall into two camps: those scaling toward 1,500+ cows to capture efficiency gains, and those capturing specialty premiums through organic certification, grass-fed programs, or artisan cheese partnerships. The middle ground between those strategies has gotten thin.

The Northeast faces high land costs and increasingly complex environmental regulations—such as nutrient management plans, CAFO permitting requirements, and setback rules that vary from county to county. But proximity to premium urban markets creates opportunities that don’t exist in rural South Dakota. I’ve talked with Vermont and New York producers who’ve built genuinely sustainable businesses through direct sales and value-added products. It requires different skills than commodity production, but the path exists.

Canadian producers operate under supply management, which provides price stability that U.S. farmers can only dream about. But even that hasn’t stopped consolidation entirely. A peer-reviewed study in the Canadian Veterinary Journal documented that Canadian dairy farms decreased by nearly 62% between 1991 and 2011—from over 39,000 operations down to fewer than 15,000. Current government data shows the decline continuing, with farm numbers dropping from about 12,000 in 2014 to roughly 9,250 in 2024.

Several industry analysts—including teams at Rabo AgriFinance and various land-grant universities—have projected that if current attrition rates continue, total U.S. dairy operations could fall into the 8,000 to 12,000 range by the mid-2030s. That’s not a formal USDA forecast, just an extrapolation. But the math isn’t complicated.

Technology and Labor: The Accelerating Factors

Two forces are speeding up the consolidation timeline in ways worth understanding.

Precision dairy technology—robotic milking systems, automated feeding, sensor-based health monitoring—requires significant capital investment but dramatically reduces labor needs per cow. A 2,000-cow operation with modern automation might run with 12-15 employees. Try running 500 cows with proportionally fewer workers, and you’ll find the per-cow labor costs much harder to manage. The technology favors scale in ways that weren’t true twenty years ago.

And then there’s the labor market itself. Finding reliable dairy workers has become genuinely difficult across most regions. The work is demanding, the hours are long, and competition from other industries has intensified. Larger operations can offer better wages, benefits, and more predictable schedules. Smaller operations often rely heavily on family labor—which works until the next generation makes different choices. Larger farms don’t just have more employees; they have HR systems. A 500-cow dairy often lacks the scale to hire an HR manager but is too big for the owner to handle all personnel issues personally. This adds to the “middle squeeze.

That generational piece matters more than we sometimes acknowledge. USDA data consistently shows the average age of farm operators climbing—it’s now 58.1 years for primary operators nationally, according to the 2022 Census. The same Census found that producers aged 65 and older now outnumber those under 35 by more than 4 to 1. And when the current generation steps back, many of those farms won’t continue as dairies, regardless of market conditions.

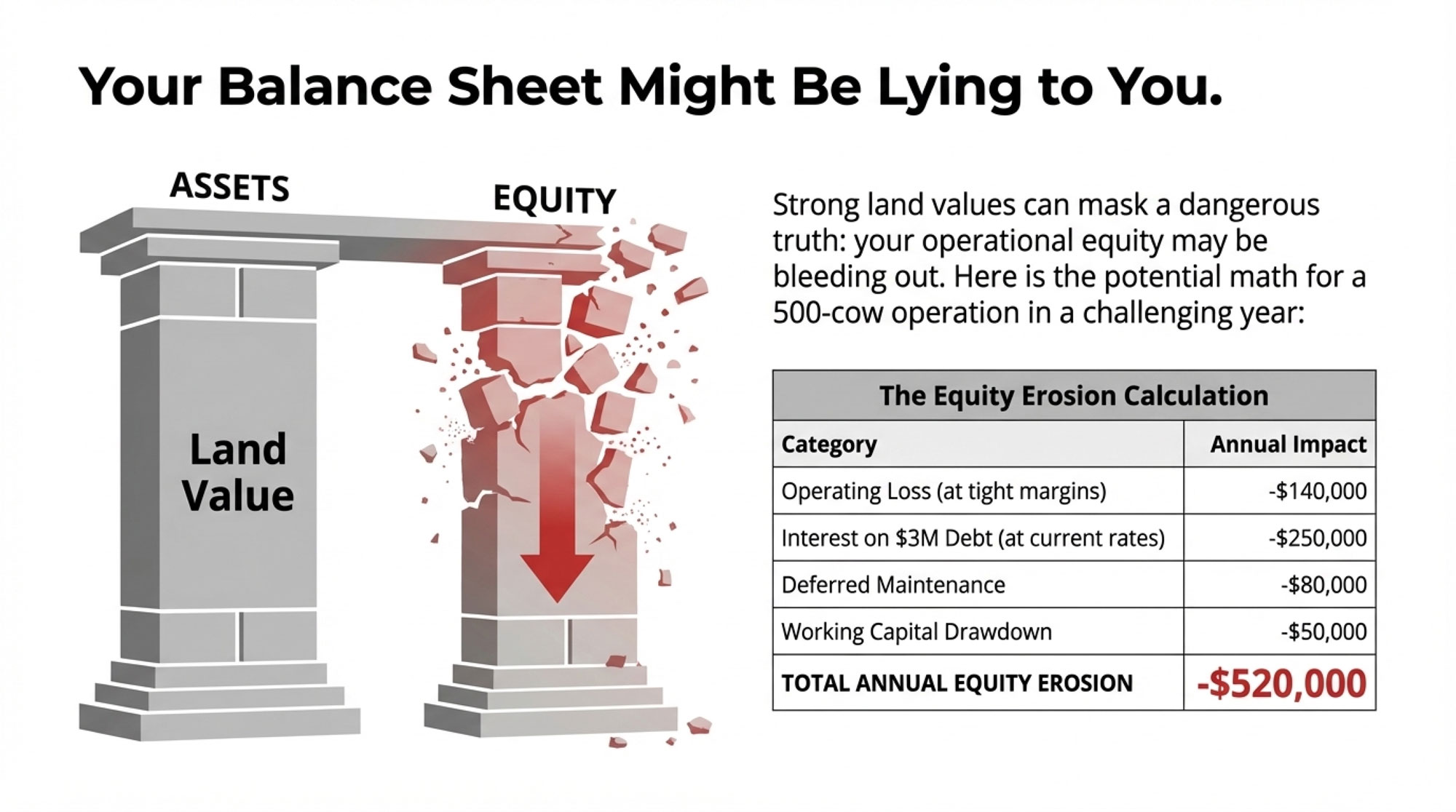

The Equity Question: What’s Really Happening to Your Balance Sheet

This is the piece I think deserves more attention, because it changes how you think about timing.

Many operations show strong balance sheets on paper. Land values appreciated significantly from 2010-2022. Multi-generational farms often carry substantial equity. But when you calculate what I’ve started calling “equity velocity”—the rate at which that equity is actually changing when you account for everything—the picture sometimes shifts dramatically.

Here’s a concrete example. Say you’re running a 500-cow operation with $5 million in starting equity. Not unusual for an established family dairy in Wisconsin or Minnesota.

THE EQUITY EROSION CALCULATION

In a challenging year, here’s what the math might actually look like:

Category

Annual Impact

Notes

Operating loss at negative margins

-$140,000

Assumes $1.50-2.00/cwt below breakeven

Interest on $3M debt at current rates

-$200,000 to -$250,000

6.5-8.5% rates vs. 3-4% in 2019-2021

Deferred maintenance

-$60,000 to -$80,000

Mixer wagon, parlor equipment, facility repairs pushed to “next year”

Working capital drawdown

-$30,000 to -$50,000

Feed inventory, supplies, cash reserves declining

TOTAL ANNUAL EQUITY EROSION

-$430,000 to -$520,000

Before major breakdowns, herd health crises, or feed quality issues

That’s potentially half a million dollars gone in a single difficult year. Before any major breakdowns. Before any herd health crises during the transition period with your fresh cows. Before a mycotoxin problem shows up in your feed.

Strong milk price years can reverse the trend. Some operations manage costs far better than others. But if you haven’t run this calculation for your own operation recently, you’re flying blind.

Mark Stephenson at UW-Madison—he’s the Director of Dairy Policy Analysis and received the Distinguished Service to Wisconsin Agriculture award in 2024—has made an observation that stuck with me. Farmers often think of equity as their safety net, he’s noted, but the erosion can happen gradually enough that it’s not obvious until a lender review reveals how much the picture has changed.

What One Producer Learned

I recently talked with a Wisconsin dairy farmer who exited in 2023 after 28 years running a 650-cow operation. He asked that I not use his name—these decisions still carry emotional weight in our communities—but his perspective is worth hearing.

“I had $4.2 million in equity on paper,” he told me. “But when I really calculated the trajectory—the interest costs, the maintenance I kept deferring, my wife’s off-farm income basically subsidizing everything—I could see where things were headed if conditions didn’t improve substantially.”

He sold in early 2023, netting $3.8 million after paying off all debt, and now consults with other operations facing similar decisions.

“The hardest part was telling my dad, who’s 84 and started the place in 1968. But he said something I think about a lot: ‘I built this to take care of the family, not the other way around.'”

That’s not the only path forward, obviously. But it’s one that more operations are considering seriously.

A Different Story: Making the Middle Work

Not every mid-size operation is struggling, though. I spoke with a 400-cow dairy in central Wisconsin—they asked me not to identify them specifically—that’s been consistently profitable through the recent volatility.

Their formula:

Aggressive cost tracking (feed costs monitored weekly, not monthly)

Premium processor relationship (specialty cheese buyer paying for high-component milk)

Zero debt (paid off expansion fifteen years ago)

Professional management (next-gen operator returned with agribusiness career experience)

“We’re not getting rich,” the father told me, “but we’re not burning equity either. The key was getting our debt to zero before the interest rate spike. That changed everything.”