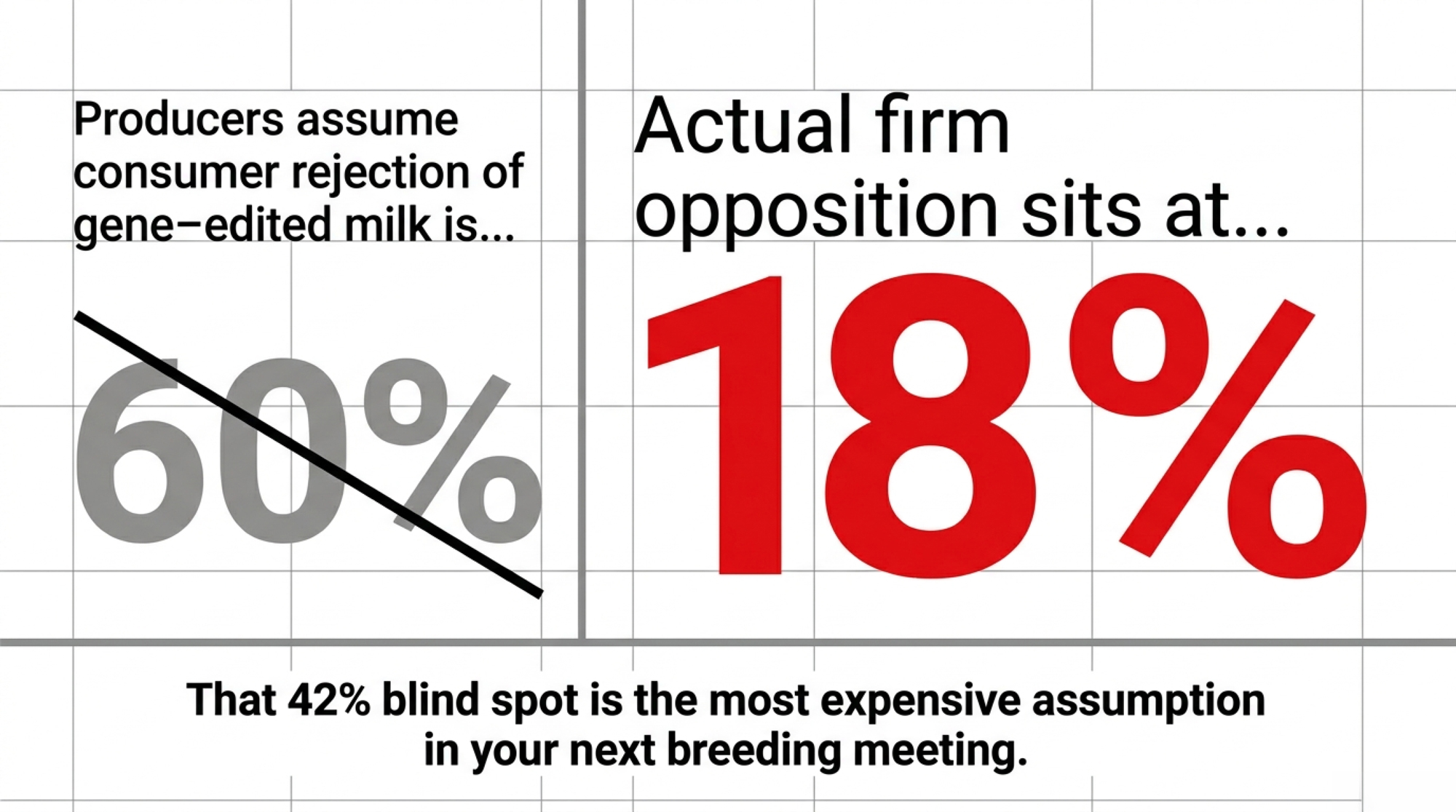

Farmers guess 60% of shoppers reject gene-edited milk. It’s 18%. And a $35–$45 genomic panel on this year’s heifers may decide whether you ever qualify to ship it.

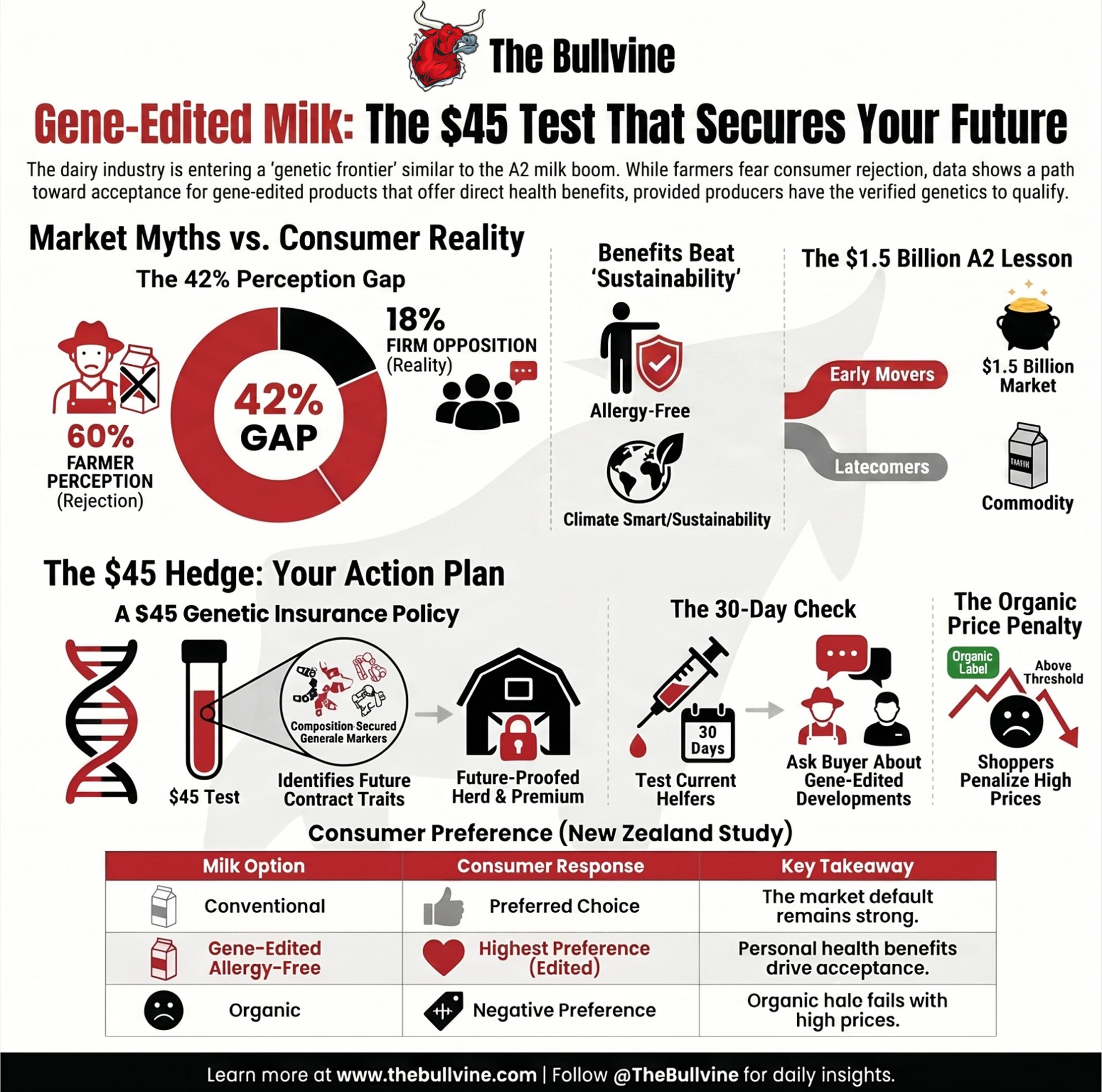

Executive Summary: A University of Otago study put gene-edited milk in front of 1,096 shoppers, and the headline number flips a common assumption: firm opposition runs near 18%, not the 60% farmers tend to guess. The allergy-free version pulled hardest of any edited milk, while organic drew negative preference once the price climbed — a warning for anyone whose premium is the whole business case. On a 200-cow herd at 75 lbs/day, the spread between a $50/cwt grass-fed organic price and an $18.70/cwt mailbox price is roughly $1.64 million a year in gross revenue riding on how durable that premium stays. At the same time, Zoetis is buying Neogen’s GeneSeek labs for $160 million, pulling the testing pipes, the DWP$ index, and the processor relationships under one roof — the exact plumbing a gene-edited supply chain would run through. The A2 playbook still holds: early movers caught the margin, latecomers caught a commodity. Your cheapest hedge is a $35–$45 composition-focused genomic panel on this year’s heifers, so you actually know your casein and beta-lactoglobulin profile before a processor sets a spec. Read the full piece if you’ve got a breeding or contract call this season — it lays out four honest roads and a 30-day checklist.

Editor’s Note: The dairy operators in the opening are a composite scenario modeled on the documented experiences of producers who weighed early A2 adoption against staying conventional. It is not a single named individual. All companies, studies, prices, and dates below are real and sourced.

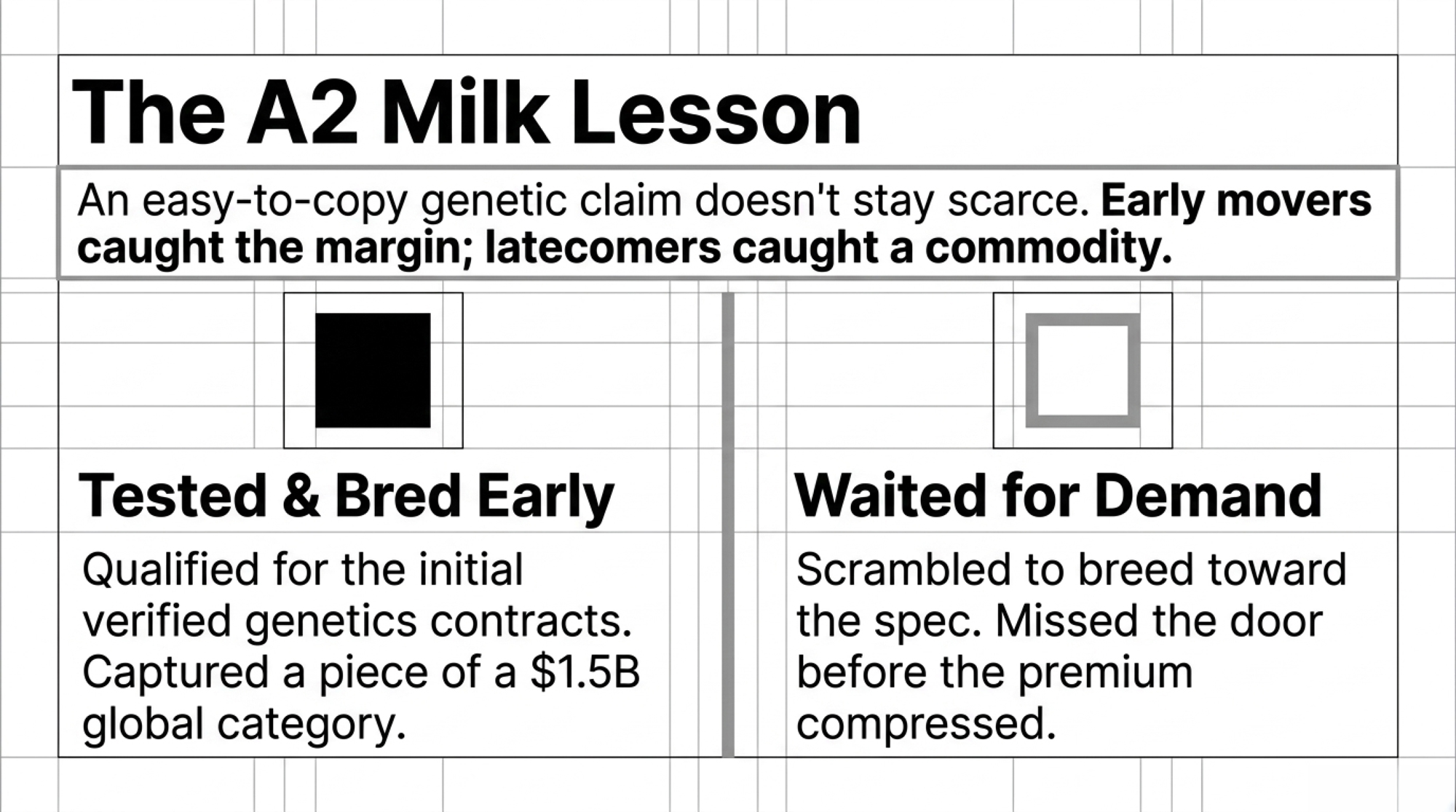

Back in 2012, plenty of sharp dairy operators looked at A2 milk and shrugged. The science was contested. The “easier on your stomach” claim sounded like health-food shelf talk, and serious producers had real work to do. By 2024, A2 had grown into a global category valued at roughly $1.5 billion, by one industry estimate, with some trackers putting it higher. The a2 Milk Company built that on controlled supply and verified genetics, rewarding producers who’d made the transition early, since qualifying milk required herds with the right A2 genetics.

Nobody mailed the latecomers a notice explaining what they’d missed. They eventually noticed that certain buyers were paying certain suppliers more, and the door to qualify had already swung shut. That same setup is forming again around gene-edited milk — and this time there’s fresh, hard data telling you which way it breaks. Researchers in New Zealand just put gene-edited milk in front of nearly 1,100 consumers, and the results land squarely on a breeding decision you’re making this season.

How a Skeptical Crop Became a Billion-Dollar Carton

The A2 story is worth a beat, because it’s the closest map we have to what’s coming. The a2 Milk Company started as a contrarian bet that a single protein variant — A2 beta-casein instead of A1 — would matter to shoppers. For years, it was a curiosity in the dairy case. Then it wasn’t.

By 2024, the category cleared roughly $1.5 billion globally, and the supply model that got it there mattered as much as the marketing. Qualifying milk required herds with verified genetics. The farms that tested and bred early were the ones holding the contracts when demand arrived.

But here’s the catch the A2 run also taught — and it’s the part worth carrying forward: an easy-to-copy genetic claim doesn’t stay scarce. As The Bullvine has noted, once the major studs started selecting for A2, “the ‘A2 advantage’ was never a sustainable moat” — any farm could test and qualify, and as more piled in, the premium compressed. So the lesson cuts both ways. Early movers caught the margin; latecomers caught a commodity. That’s the pattern to keep in your head as you read the rest of this — not because gene-edited milk is guaranteed to follow it, but because the plumbing being built right now looks awfully familiar.

What the New Zealand Study Actually Found

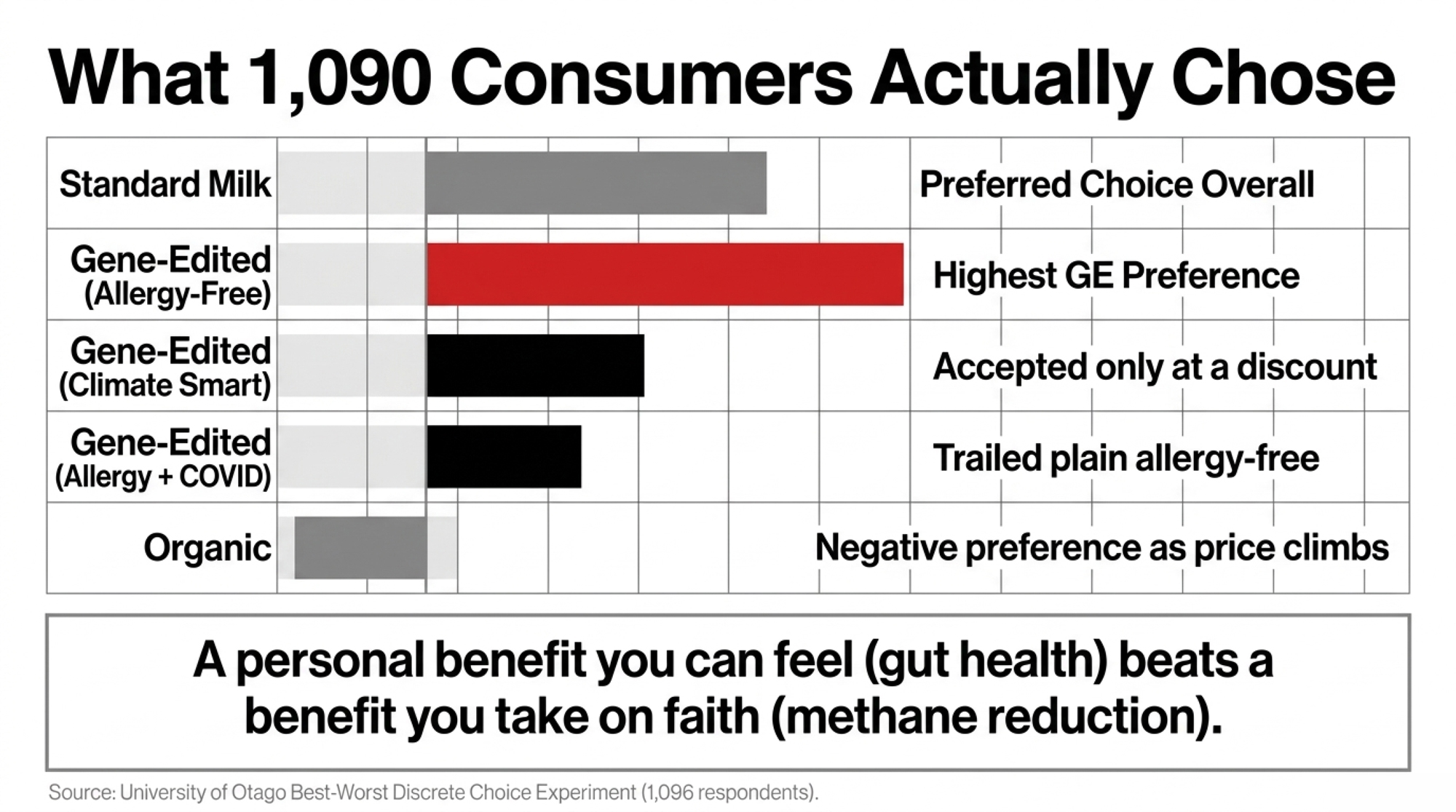

This wasn’t an opinion poll asking whether people “support” gene editing in the abstract. The study — a University of Otago Best–Worst Discrete Choice Experiment with 1,096 respondents — simulated a shopping trip in which people chose among standard milk, organic milk, and three gene-edited “Climate Smart” versions at varying prices.

Here’s how the five options sorted out:

| Milk option | How shoppers responded | What it tells you |

| Conventional (standard) | Preferred choice overall | The default is still the default |

| Gene-edited, allergy-free | Highest preference of the three edited versions | A personal benefit you can feel moves people |

| Gene-edited, standard “Climate Smart” | Accepted only at a price advantage | Sustainability alone won’t carry a premium |

| Gene-edited, allergy-free + COVID protection | Trailed the plain allergy-free version | Stacking a second novel claim didn’t help |

| Organic | Negative preference at every price point, steepest at average and above-average prices | The halo isn’t bulletproof once price climbs |

Standard milk won the overall vote. No shock there. But two findings crack the story open. Consumers treated Climate Smart milk as a real option only when it offered a price advantage, and among the three edited versions, the allergy-free one drew the highest preference. The authors didn’t hedge on what drives that. Writing in The Conversation, they concluded there’s “a potential pathway towards greater consumer acceptance, particularly when innovations provide direct and significant benefits instead of vague promises of future sustainability”. In plain terms, “this milk won’t wreck your gut” beats “this milk lowers methane” because one benefit you can feel, and the other you take on faith.

That organic line in the table should make any organic producer sit up. Shoppers in this experiment didn’t reward the label — they penalized it once the price climbed. That’s one survey in one market, not gospel. But it cuts hard against the assumption that the organic halo is bulletproof.

There’s real science under that allergy-free claim. CRISPR knockout of the beta-lactoglobulin gene — a protein implicated in many milk allergies — can produce milk far less likely to trigger a reaction. Keep one thing straight when you size that market, though: milk allergy and lactose intolerance aren’t the same condition, and this edit targets the protein that drives the allergic response, not the lactose that troubles a much larger group. Cow’s milk protein allergy is the most common food allergy in infants, but affects a relatively small share of the general population — developed-country prevalence studies range from roughly 0.5% to 3.8%. So the addressable market is real, but it’s a defined clinical group, not “everyone who feels bloated.”

| Factor | Cow’s Milk Protein Allergy (CMPA) | Lactose Intolerance |

|---|---|---|

| Mechanism | Immune response to proteins (casein, beta-lactoglobulin) | Enzyme deficiency (lactase); can’t digest lactose sugar |

| Population affected | 0.5%–3.8% (developed countries); most common in infants | ~65–70% of adults globally have some degree of reduction |

| GE intervention target | ✅ Yes — BLG knockout addresses protein trigger | ❌ No — protein edit doesn’t affect lactose content |

| Addressable market size | Defined clinical group; real but smaller | Much larger; already served by lactose-free products |

| Premium pricing logic | Justifiable for a clinical need; niche but defensible | Crowded market; commodity pricing pressure |

| Shopper confusion risk | High — “allergy-free” easily misread as lactose-friendly | Messaging must be precise or it creates backlash |

One gap is worth sitting with. Dairy farmers tend to estimate that around 60% of consumers reject gene-edited products. The research puts firm opposition closer to 18%. That spread — between what producers assume and what shoppers actually feel — might be the most expensive blind spot in your next breeding meeting.

Who’s Actually Exposed Here — and Who Isn’t

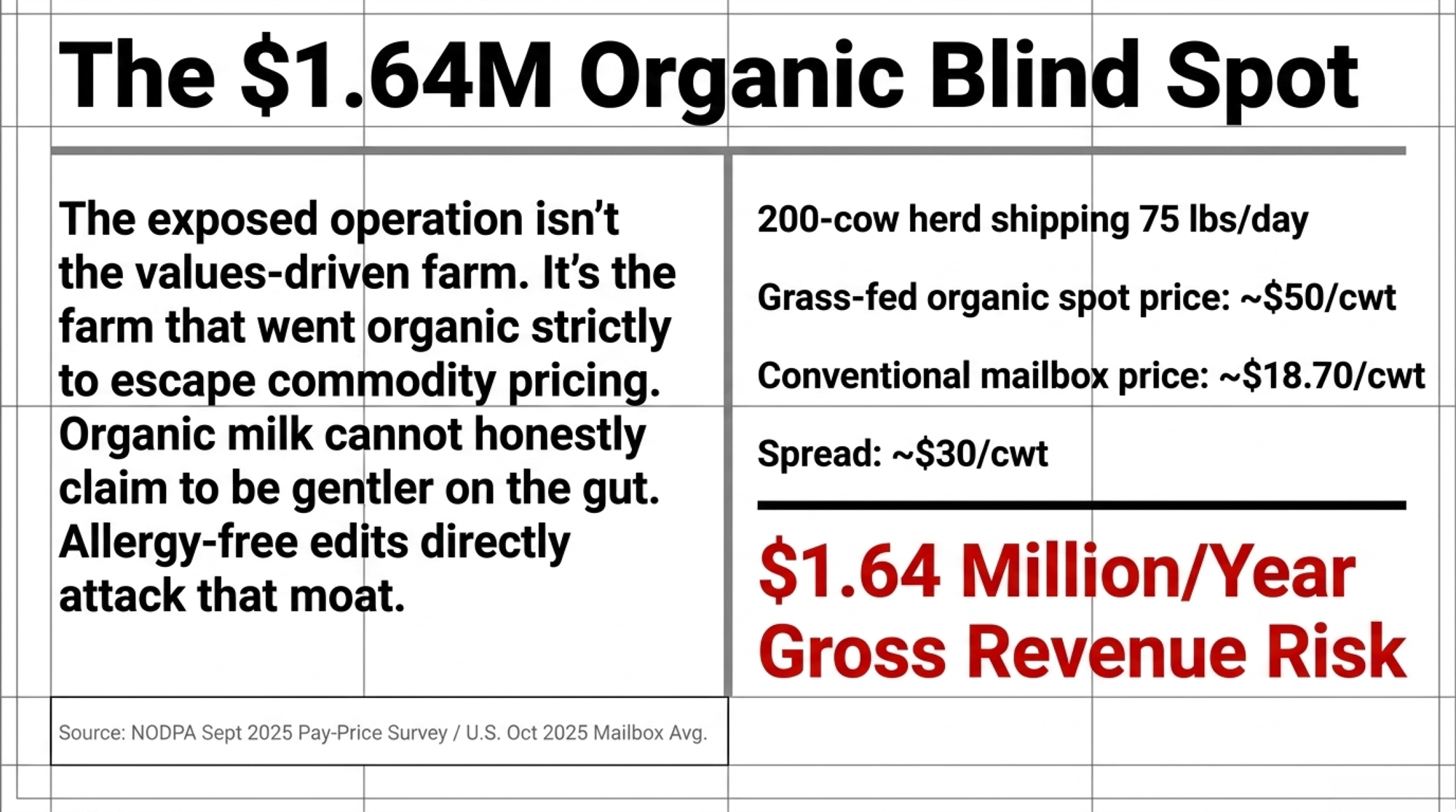

The farms most at risk from this shift aren’t the obvious ones. The values-driven organic producer — the one whose customers buy organic because it’s part of who they are — is largely insulated. That buyer isn’t switching for a molecular benefit claim, no matter how slick the marketing.

The exposed operation is the one that went organic mainly to escape commodity pricing. That farmer chased a premium, and the premium is real. As of NODPA’s September 2025 pay-price survey, grass-fed organic premiums ran from about $36/cwt to $52/cwt depending on the buyer, with spot organic milk in the short Northeast market topping $50/cwt. That premium is the whole business case. And it rests on a consumer perception that gene-edited allergy-free milk can quietly chip away at — because organic has never been able to honestly tell a lactose-sensitive shopper it’s gentler on their gut.

Run rough barn math on the size of that bet. Take a 200-cow herd shipping 75 lbs/day — that’s about 54,750 cwt a year. The gap between a strong grass-fed organic price near $50/cwt and an October 2025 U.S. average mailbox price of $18.70/cwt runs north of $30/cwt. At a $30/cwt spread, that’s roughly $1.64 million a year in gross milk revenue riding on how durable the organic premium stays. That’s not a number to panic over. It’s a number to stress-test before your next contract renewal.

How Much Does Sitting Still Actually Cost You?

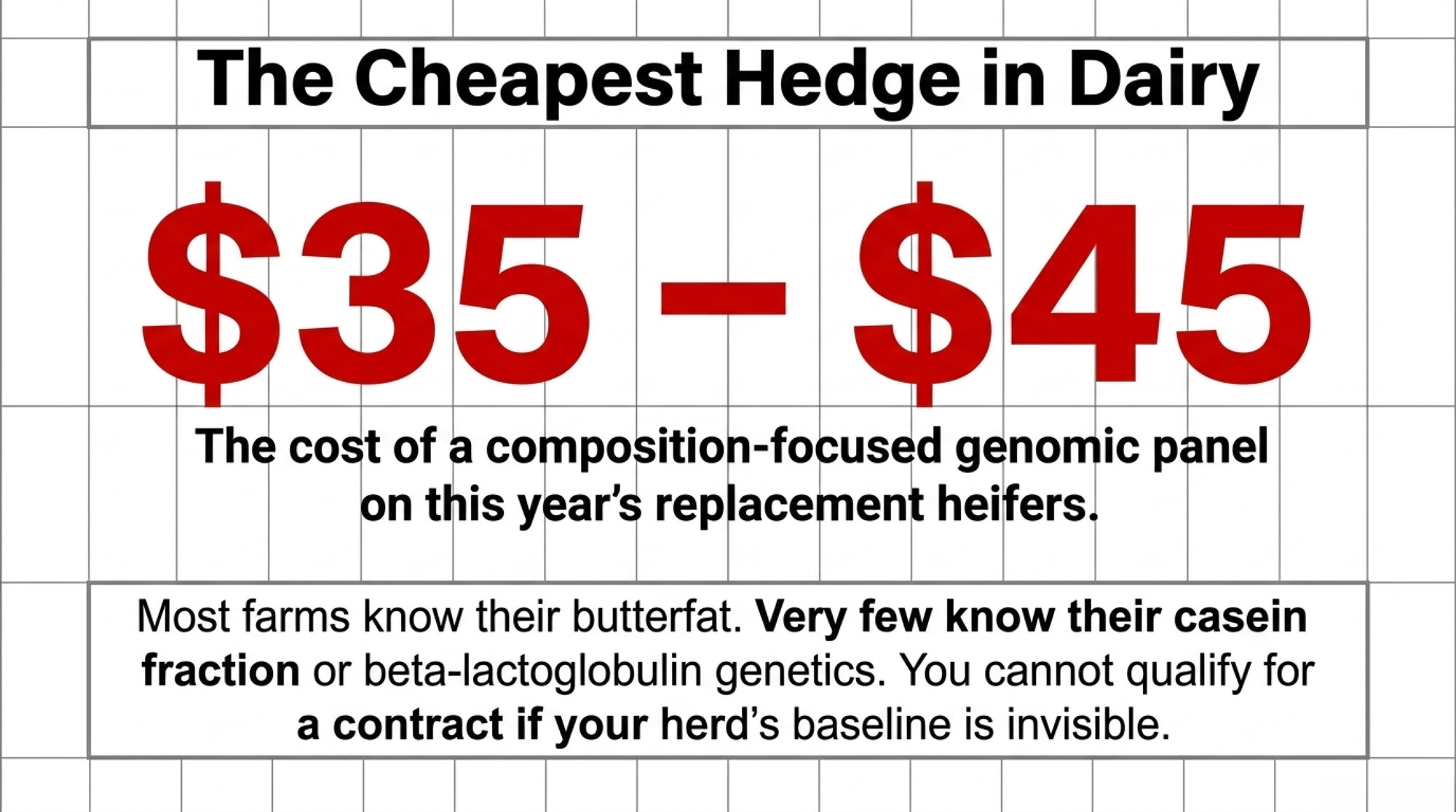

Almost nothing to start moving — and that’s the point. The first real action here runs about $35 to $45 per head: a genomic panel on this year’s replacement heifers that covers milk-composition traits, not just standard production indices. Most farmers can rattle off their herd’s butterfat and protein percentages. Far fewer can name their casein fraction profile or their beta-lactoglobulin genetics — the exact traits a differentiated supply chain would screen for.

Compare that few-dollars-per-head test to the cost of being invisible when a processor shows up with a verified genetic spec and a qualification threshold, the way A2 contracts did. Those deals don’t ask whether you’d like to join. They sign with the farms that already qualify. The operation scrambling to test and breed toward the spec after the contract’s announced is already a breeding cycle — call it 18 months — behind the farms that saw it coming.

The Overlooked Layer: Where the Supply Chain Actually Gets Built

The piece almost nobody’s talking about out loud is where this supply chain is getting built — down at the genomics layer, where most farmers never look.

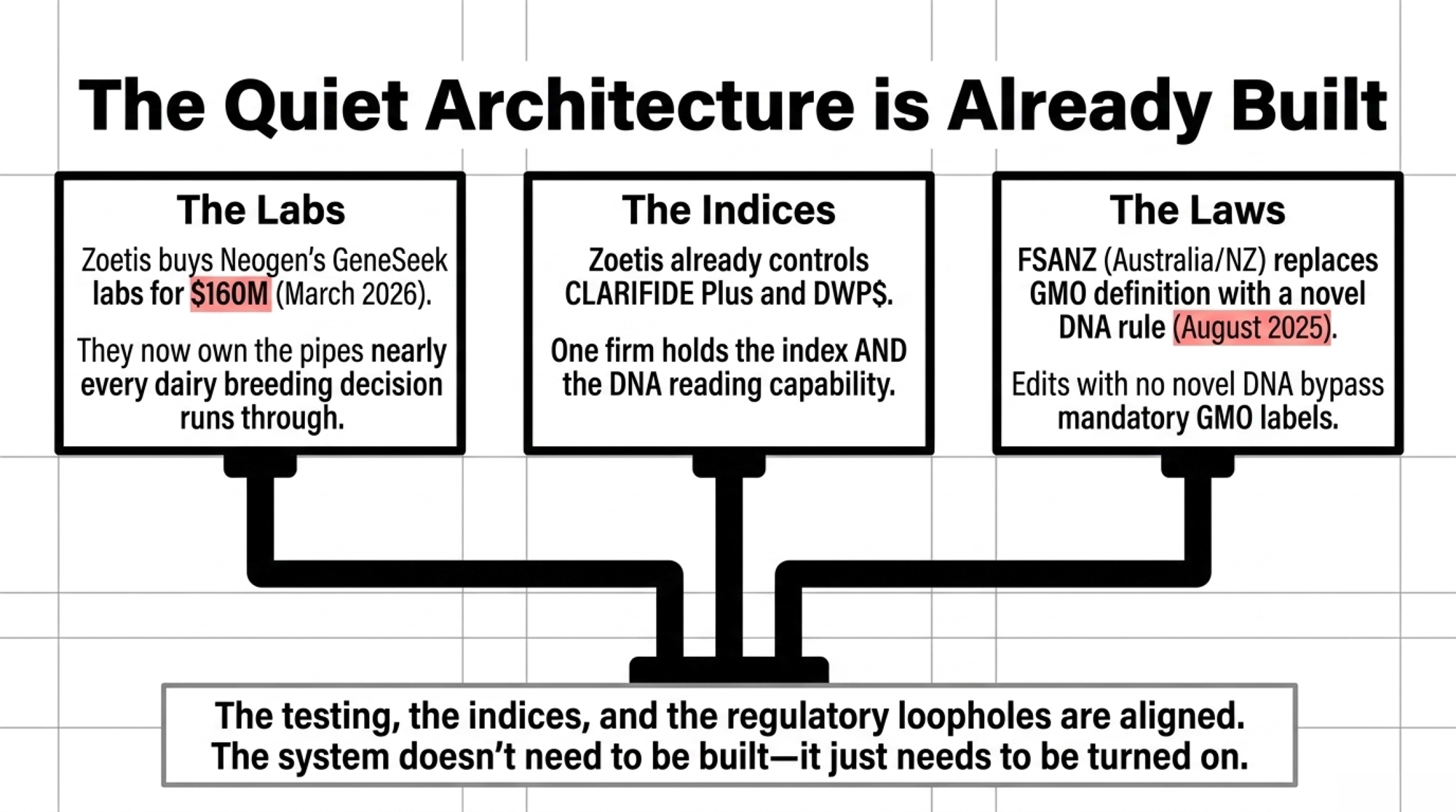

On March 2, 2026, Zoetis announced a definitive agreement to buy Neogen’s animal genomics business, including its GeneSeek laboratories, for $160 million, with the deal expected to close in the second half of 2026. That’s not a company buying a testing service. It’s a company buying the pipes nearly every breeding decision in dairy runs through — five labs across the U.S., Brazil, Australia, China, and the U.K., and, per prior reporting on the deal, roughly $90 million in annual genomics revenue. Zoetis already runs CLARIFIDE Plus and the Dairy Wellness Profit Index (DWP$), which it expanded in April 2026 with new traits. So one firm increasingly holds both the index that shapes how animals get selected and the labs that read the DNA underneath.

Here’s why that matters. A company holding the testing, the index, and the processor relationships wouldn’t need a gene-edited dairy program today to be positioned for one tomorrow — though Zoetis has announced no such plans. Whether any single firm intends to go there or not, that combination of assets is what a future gene-edited supply chain would likely run through. Semex and Recombinetics have been partnering on polled gene editing since 2018 — that work didn’t die when the headlines faded. It went quiet and waited for the rules to catch up.

And the rules are catching up fast. New Zealand’s effective gene-tech ban lifted at the end of 2025. The UK’s Precision Breeding Act is now in force, and the EU moved toward a more permissive framework in 2025. The one most farmers haven’t clocked: in 2025, Food Standards Australia New Zealand replaced its old process-based GM definition with an outcome-based one built around “novel DNA” — the board approved the change in June, and food ministers gave final approval in August 2025. Under that rule, a gene-edited food that introduces no novel DNA isn’t classified as GM — and doesn’t carry a mandatory “genetically modified” label. That’s the regulatory hinge the whole consumer-acceptance question swings on, because a beta-lactoglobulin knockout could reach the shelf without the label baggage that sank first-generation GMOs.

Options and Trade-Offs for Your Operation

| Strategy | Best Fit | Upfront Cost | Breeding Lag Risk | Premium Capture Potential | Key Dependency |

|---|---|---|---|---|---|

| Early Mover | Already genomic testing; chasing component premiums | $35–$45/head panel now | Low — 0 cycles behind | High — catches first-wave contracts | Regulatory timeline; retail uptake speed |

| Fast Follower | Solid balance sheet; risk-averse | $35–$45/head + higher sire cost later | High — 18+ months behind | Moderate — pays margin to early movers | Speed of decision when signal arrives |

| Niche / Direct | Smaller ops with artisan or local markets | Low genomic investment | Minimal — not competing on spec | Variable — relationship-dependent | Channel loyalty; scale ceiling |

| Deliberate Wait | Weighed the options; decided to hold | None today | Grows with each cycle | Low near-term; could re-enter at cost | Honest reassessment at each contract renewal |

There’s no single right answer here. There are a few honest roads, and each costs you something. Find the one that matches how you actually run your operation.

Option 1 — Position early as a potential supplier

Best fit: You already genomic-test and chase component or differentiated premiums. What it requires: Knowing your herd’s protein genetics, not just its butterfat. The risk: You invest in readiness for a market whose commercial timeline is still a few years out, and the regulatory or retail picture could shift under you. The FSANZ “novel DNA” reframing makes this less of a gamble than it looked a year ago — but it’s not a sure thing yet.

Option 2 — Wait deliberately as a fast-follower

Best fit: Your balance sheet can’t carry timing risk, and you’d rather let others prove the category. What it requires:Accepting that you’ll likely pay someone else’s margin to get in later. The risk: Breeding lead times mean “later” can land you 18 months or more behind by the time you decide to move.

Option 3 — Carve out a niche the genomics giants can’t reach

Best fit: Smaller operations with local, direct, or artisanal channels. What it requires: A relationship-based market instead of a commodity one. The risk: You give up scale — but you also shed the exposure to the consolidation game entirely.

Option 4 — Do nothing, but choose it on purpose

Best fit: Anyone who’s genuinely weighed the above and decided to hold. What it requires: An honest look, not an avoided one. The risk: The danger was never the farmer who weighed this and decided to wait. It’s the one who never looked at all.

The one move worth making in the next 30 days costs the least: book that composition-focused genomic panel on this cycle’s heifers at $35–$45 a head, and ask your milk buyer one flat question — “Are you watching gene-edited dairy product development, and who do you call first when it goes commercial?” The answer costs you nothing and tells you whether your relationship with the processor is an asset or a liability in this shift.

Is Your Herd’s Genetic Strategy Already a Cycle Behind?

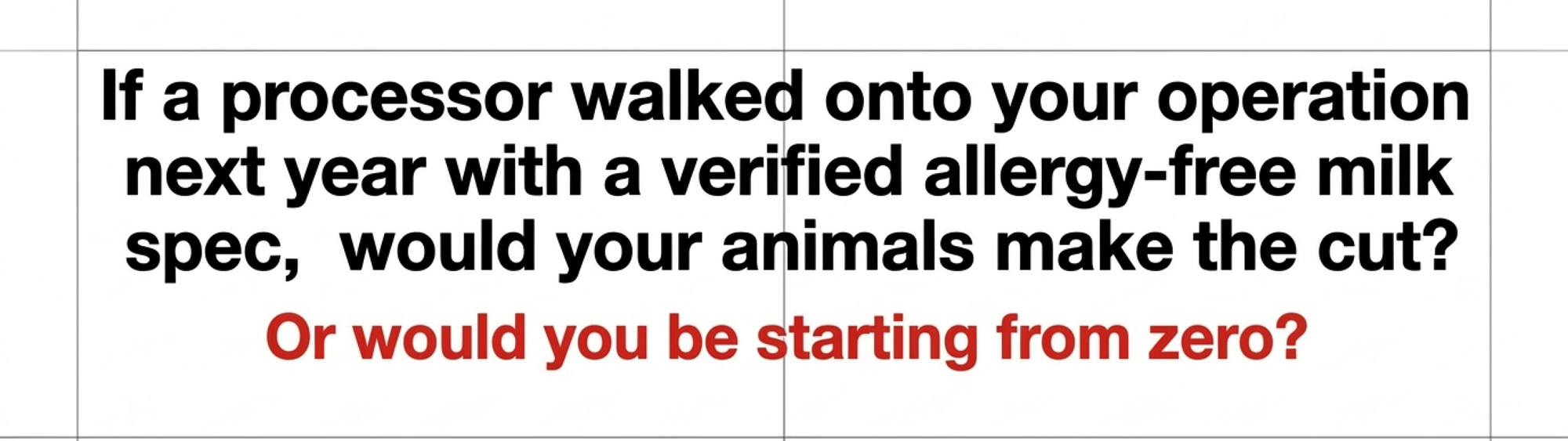

Maybe. The honest answer depends on data that most farms haven’t bothered to pull, because it hasn’t mattered commercially until recently. If you can’t name your herd’s casein and beta-lactoglobulin profile right now, you’re not positioned — you’re hoping.

The breeding moves that build a real position aren’t exotic. Select for milk-protein composition. Prioritize health traits. Keep detailed genomic records, and build an actual relationship with a processor who’s watching this space. None of that requires a single gene-edited animal today. All of it builds the foundation to qualify when clearance lands — and it keeps your options open if you’d rather wait and watch. There’s a quieter cost worth checking, too: read the data-ownership terms in your genomic-testing agreement and your co-op membership before you assume your herd data is yours to direct. That data feeds the proprietary indices — and eventually the product specs — being built right now.

Your Next 30 Days: A Working Checklist

Before this drops off your radar, here’s the sequence — none of it commits you to a gene-edited animal, and all of it keeps your options open:

- This week — pull your numbers. Find out whether you already have casein and beta-lactoglobulin data for your herd, or if you’re starting from scratch.

- Within 30 days — book the panel. Order a composition-focused genomic panel for this cycle’s replacement heifers, at roughly $35–$45 per head.

- Within 30 days — ask your buyer the question. “Are you watching gene-edited dairy product development, and who do you call first when it goes commercial?” The answer tells you where you stand.

- Before your next contract renewal — read the fine print. Pull your genomic testing agreement and co-op data terms to know who actually controls your herd data.

- Then decide on purpose. Pick your road from the four options above — early mover, fast-follower, niche, or deliberate wait — and write down why.

Key Takeaways

- If your organic premium is the whole business case rather than a loyal values-driven base, stress-test it before your next contract renewal — the study shows shoppers penalized organic once the price climbed.

- A $35–$45 genomic panel on this cycle’s heifers is the cheapest hedge there is. Run it now so you know your casein and beta-lactoglobulin profile before a processor ever sets an allergy-free spec.

- Stop budgeting for 60% consumer rejection of gene-edited milk when firm opposition sits closer to 18% — that gap could be the costliest wrong assumption in your breeding plan.

- Remember the A2 timing lesson: the margin went to farms that qualified early, not the ones who waited for the contract to be announced.

So where does your herd actually sit — not philosophically, but genetically? If a processor walked onto your operation next year with a verified allergy-free milk spec and a qualification threshold, would your animals make the cut, or would you be starting the transition from zero?

That’s the question worth carrying into your next breeding meeting. We’re building out the full supplier-positioning model — the real cost-per-cwt of moving early versus following late, broken down by herd size — in an upcoming Bullvine deep dive. That’s where the numbers that fit your balance sheet actually live.

Run Your Numbers

Genomic Testing ROI Calculator — That $35–$45-per-head panel is the article’s whole argument. Run it through the Genomic Testing ROI Calculator to pressure-test whether testing this cycle’s heifers actually pencils on your replacement costs, your value spread, and your beef-on-dairy market — before a processor ever sets a spec.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Stop Breeding by Color: Genomics, Heat Stress and Beef‑on‑Dairy Math That Can Add Over $4/cwt to Holstein Margins — Arms you with immediate risk-management protocols to allocate sexed versus beef semen. Protects your $2,000 heifer-rearing investments by ranking animals on pure genomic merit rather than visual traits or unverified pedigree hunches.

- Why the A2 Boom Bypassed Heritage Breeds – And What’s Actually Working — Exposes the long-term plant logistics and structural volume limits that squeezed late-moving herds out of the niche milk boom. Delivers critical forecasting maps to ensure your multi-year contract strategy survives corporate consolidation.

- Fluid Milk Sales Waver But Organic and Value-Added Products Surge in the Dairy Market — Reveals the concrete data behind a shifting 9% surge in organic demand alongside a steep 44% spike in specialized, value-added alternatives. Contrasts traditional fluid sales trends with high-value retail niches changing processing dynamics.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.