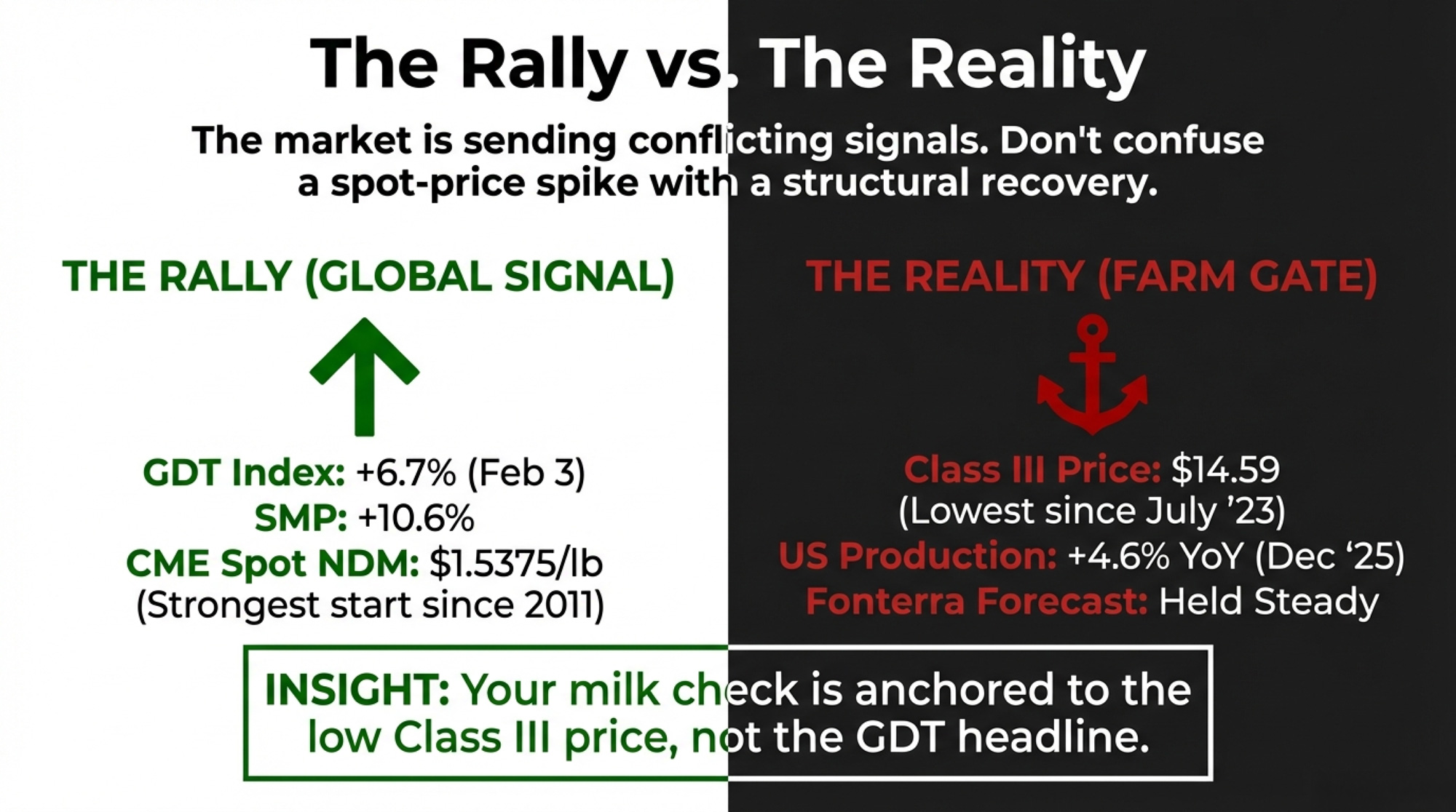

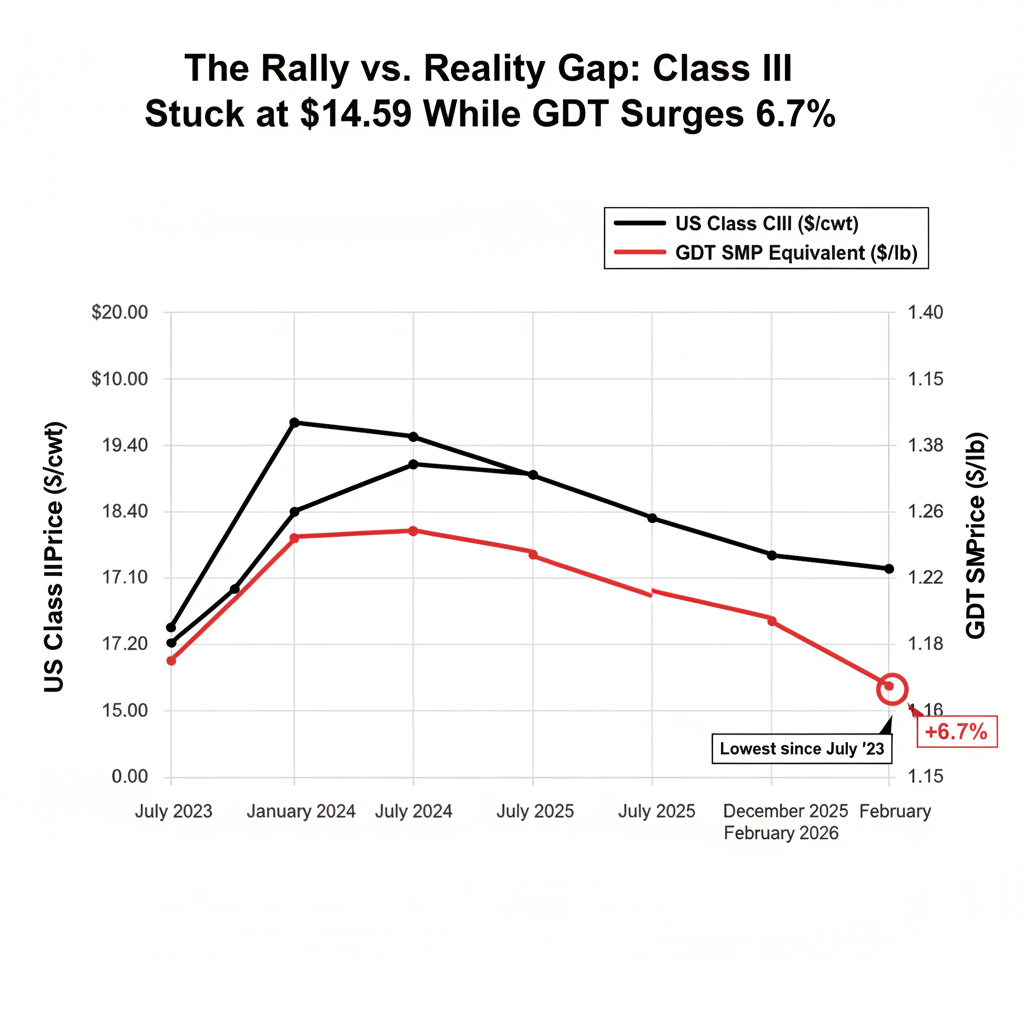

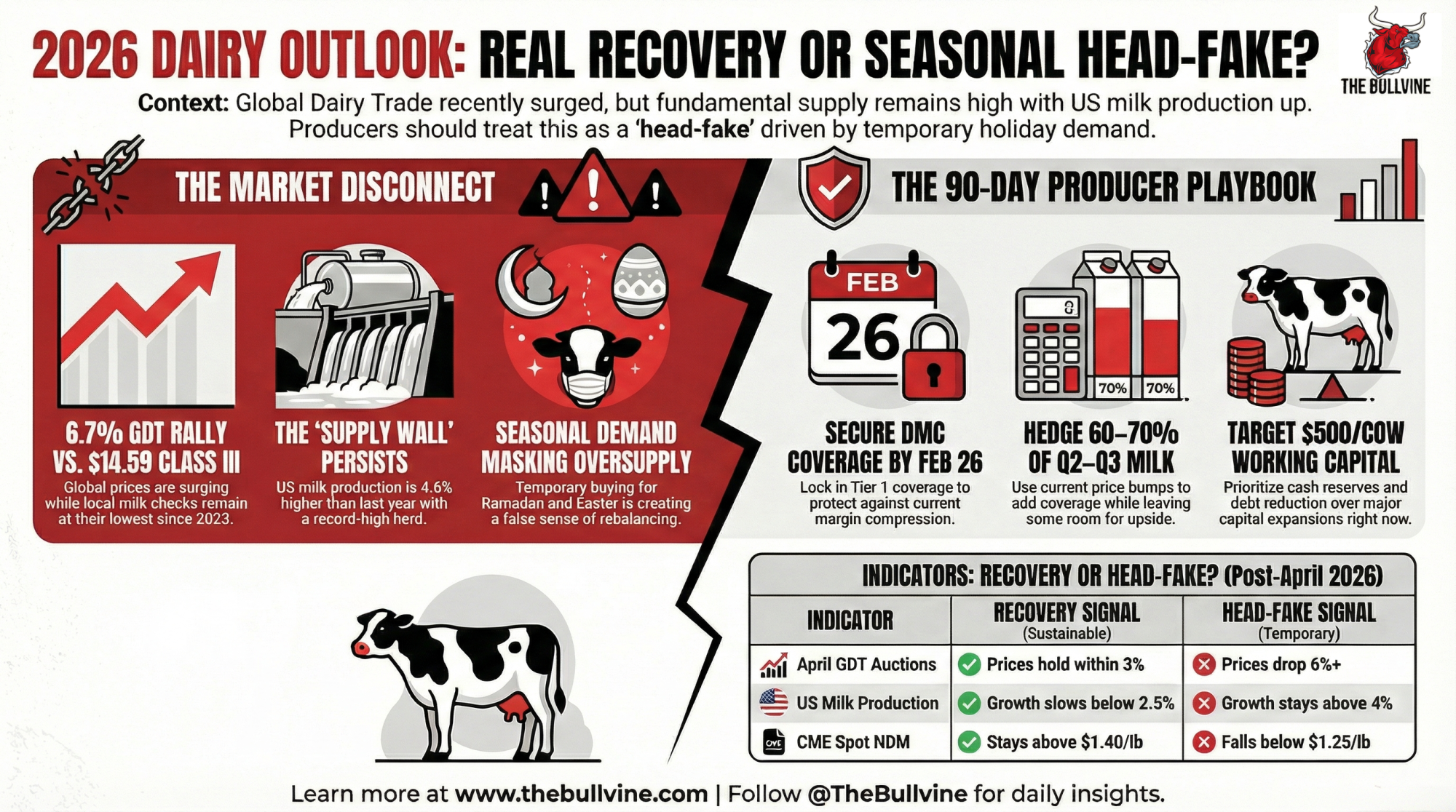

GDT up 6.7%, Class III stuck at $14.59. Is this rally real—or a head-fake you’ll regret chasing before April?

Executive Summary: The early 2026 GDT rally looks impressive—up 6.7% on February 3 with SMP surging 10.6%—but your milk check is still anchored to $14.59 Class III, the lowest since July 2023. At the same time, US milk production is running about 4.6% above a year ago, and New Zealand and EU collections are also climbing, so the supply wall hasn’t gone away. The buying burst from China, the Middle East, and Algeria is largely seasonal, tied to Ramadan and Easter, which means it can mask the underlying imbalance for a few auctions without actually fixing it. Powders look closest to a genuine reset after dropping to value territory late in 2025, while butterfat’s 8.8% bounce is a small blip against a 35–40% price break and a decade of genetically driven fat growth that’s still flooding the system. In this environment, your safest 90‑day play is to treat the rally as a potential head-fake: secure DMC coverage before the February 26 deadline, push Q2–Q3 Class III hedge coverage toward roughly 60–70% if you’re light, and build working capital toward about $500/cow before committing to major capital projects. Any expansion math should be run at $17 Class III, not today’s bounce, and held until the April 7 and 21 GDT auctions show whether prices can hold once holiday demand fades. Those two April sales, along with US milk growth, CME NDM holding above $1.40, and whether Fonterra nudges its forecast higher, are the signals that’ll tell you if this rally has real legs or was just a very expensive head-fake.

Three consecutive Global Dairy Trade gains to open 2026 have producers asking the same question: Is this the recovery we’ve been waiting for, or a seasonal head-fake that punishes anyone who bets on its continuation?

For operations staring at January milk checks based on $14.59 Class III—the lowest since July 2023—the answer shapes every decision over the next 90 days. The February 3 GDT auction delivered a 6.7% index jump, with skim milk powder surging 10.6% to $1.39/lb on an NDM-equivalent basis. CME spot NDM hit $1.5375/lb the same day, its strongest start since 2011, and up 31% year-to-date.

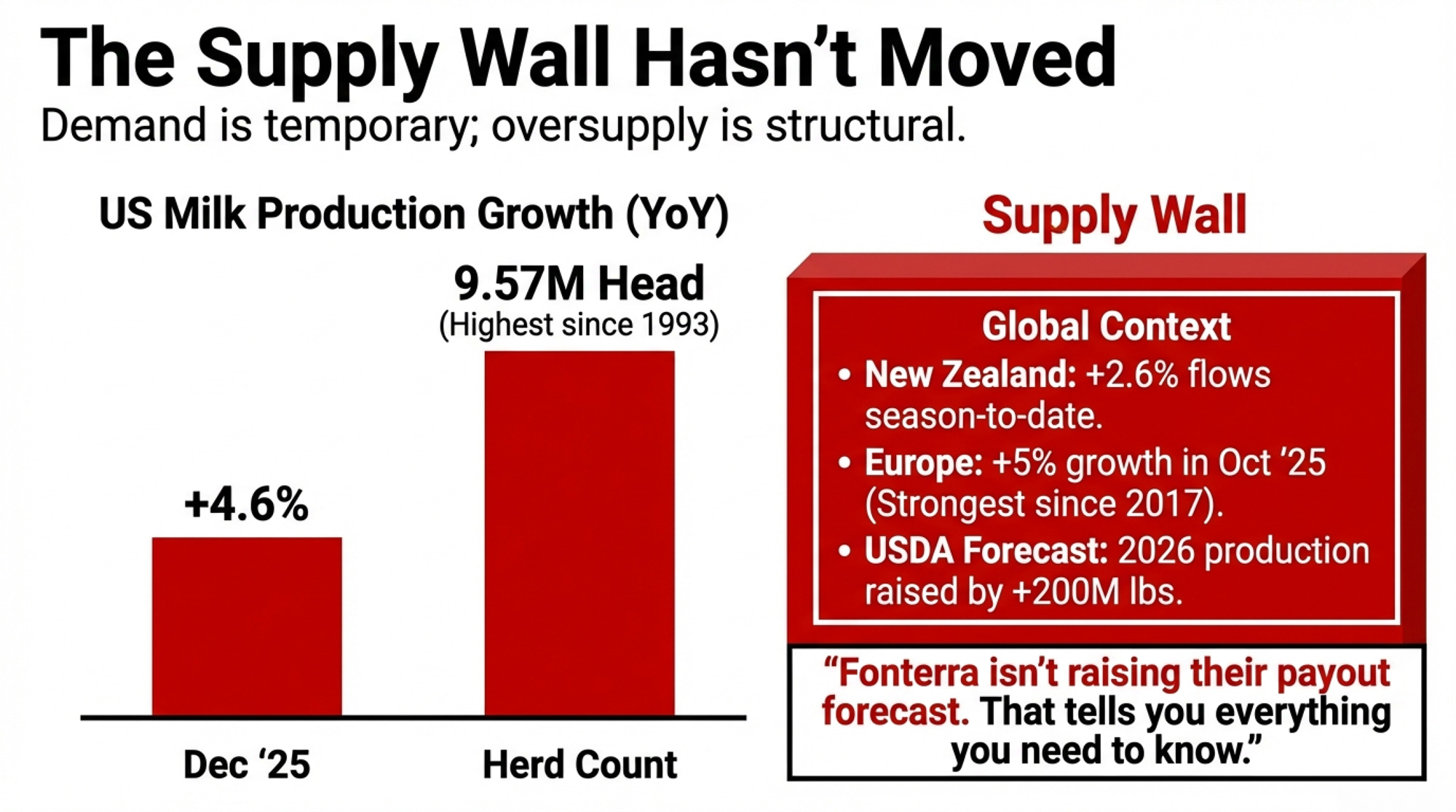

Here’s the tension: US milk production grew 4.6% year-over-year in December, according to USDA; the dairy herd sits at 9.57 million head (the highest since 1993); and Fonterra held its farmgate forecast at NZ$8.50-$9.50/kgMS despite the rally. The supply side isn’t confirming what demand is signaling.

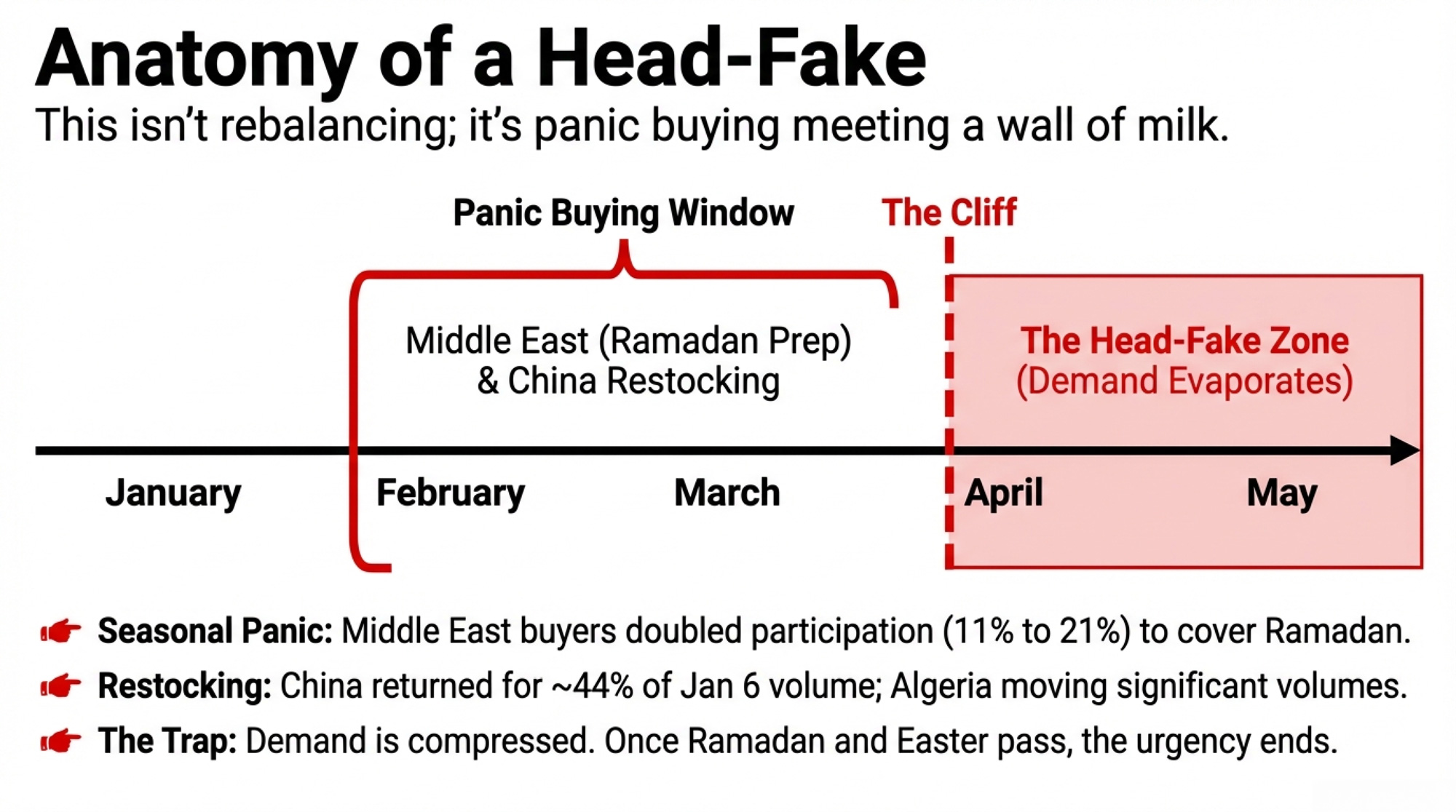

The Head-Fake Setup: Who’s Buying and Why

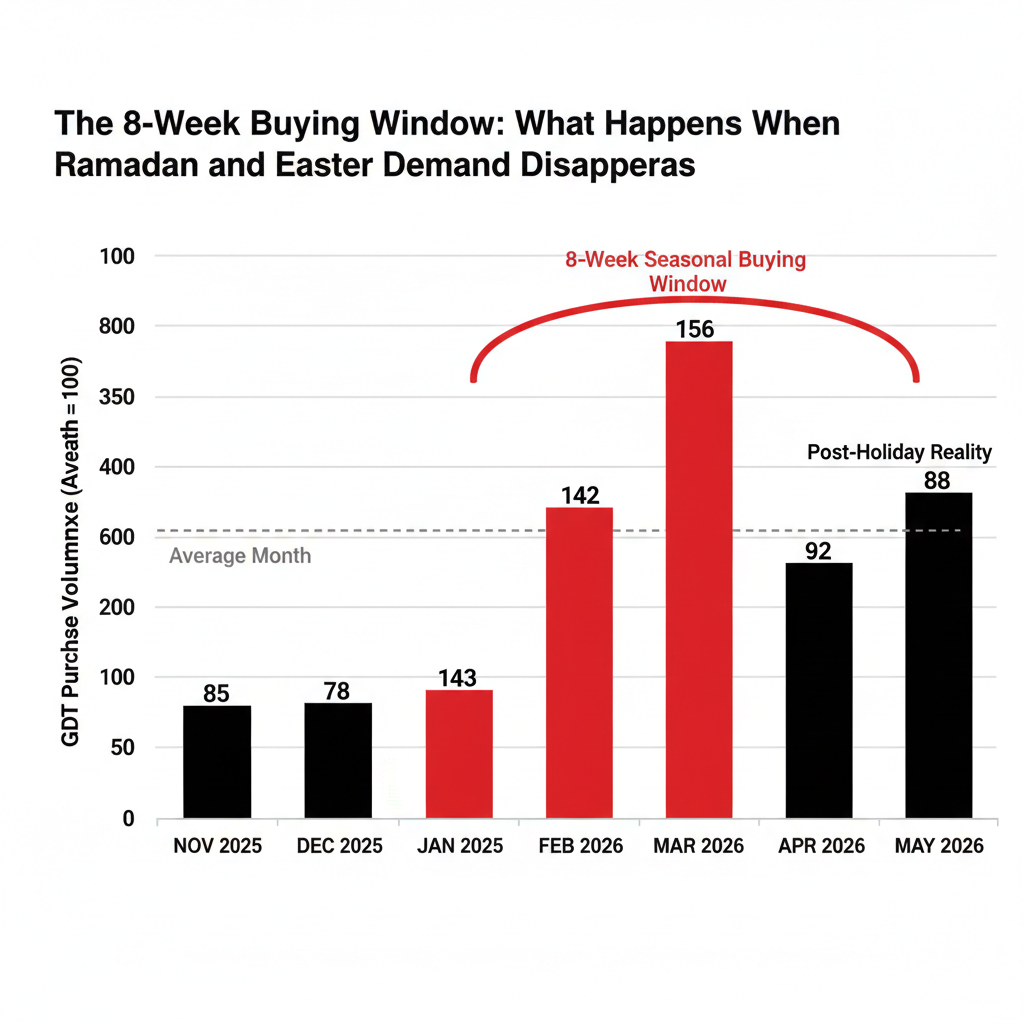

The demand shift between December and February was dramatic. Three buyer groups drove the surge:

Middle East: Reportedly doubled GDT participation from approximately 11% to 21%, according to analyst estimates—their highest share in two years—driven by Ramadan preparation beginning late February.

China: Returned as active purchasers after months of cautious observation, accounting for an estimated 44% of volume sold at the January 6 auction based on analyst tracking.

Algeria: The ONIL tender in January moved significant volumes of WMP and SMP, re-establishing global price benchmarks after weeks of volatility.

Katie Burgess of Ever.ag captured the core dynamic: global milk powder prices remain “very highly correlated,” so what happens at GDT in New Zealand directly influences US pricing. That correlation is holding. CME spot NDM now trades at roughly a 10% premium to GDT SMP equivalent, suggesting both domestic and export demand are active simultaneously. USDA’s weekly Dairy Market News confirms “tight spot inventories” and “strong international interest.”

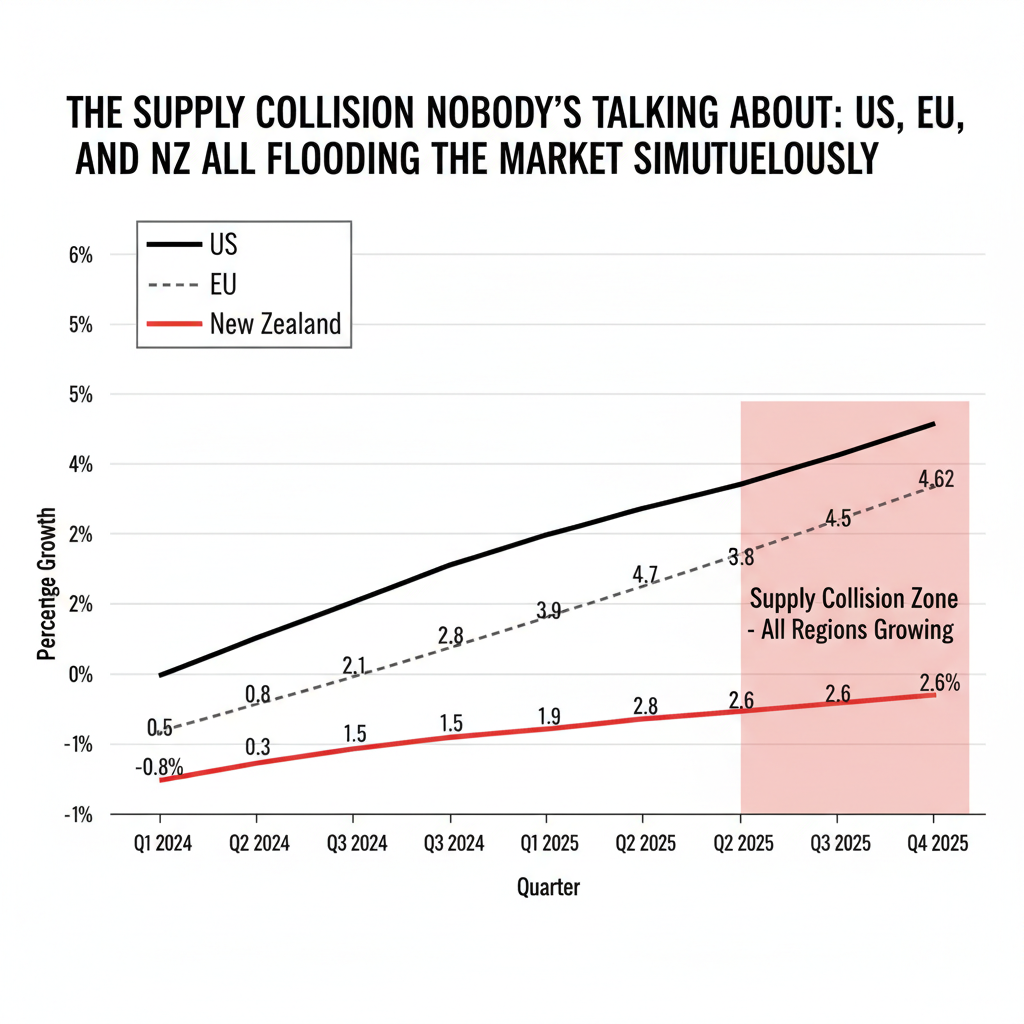

But Fonterra’s decision to hold—not raise—its price forecast tells you what the largest dairy exporter sees in its collection data. New Zealand season-to-date milk flows are running 2.6% above last year, and their full-season forecast was raised to 1,545 million kgMS in November. The supply wall that drove nine consecutive GDT declines through late 2025 hasn’t disappeared. It’s temporarily obscured by compressed seasonal demand.

Why This Head-Fake Looks Different: The Supply Collision

The conventional read on this rally goes something like: “Prices found a floor, buyers returned, the market is rebalancing.”

That assumes supply and demand are moving toward equilibrium. The data says otherwise.

US milk production grew 4.5-4.6% year-over-year in both November and December 2025, per USDA. The January WASDE raised the 2026 production forecast by 200 million pounds to 234.3 billion—up 3.2 billion pounds from 2025. EU milk output posted its strongest growth since 2017 in October 2025, running 5% above year-ago levels according to Eurostat. Rabobank analyst Michael Harvey noted that what made the late-2025 decline unusual wasn’t weak demand—GDT bidder participation stayed above 150—but a “supply collision” where multiple exporting regions flooded the market simultaneously.

What’s happening now isn’t rebalancing. It’s seasonal demand compression meeting a temporary shift in buyer psychology. Purchasers who depleted inventories waiting for the bottom are scrambling to cover positions before Ramadan and Easter. When that seasonal window closes in April, supply fundamentals reassert themselves.

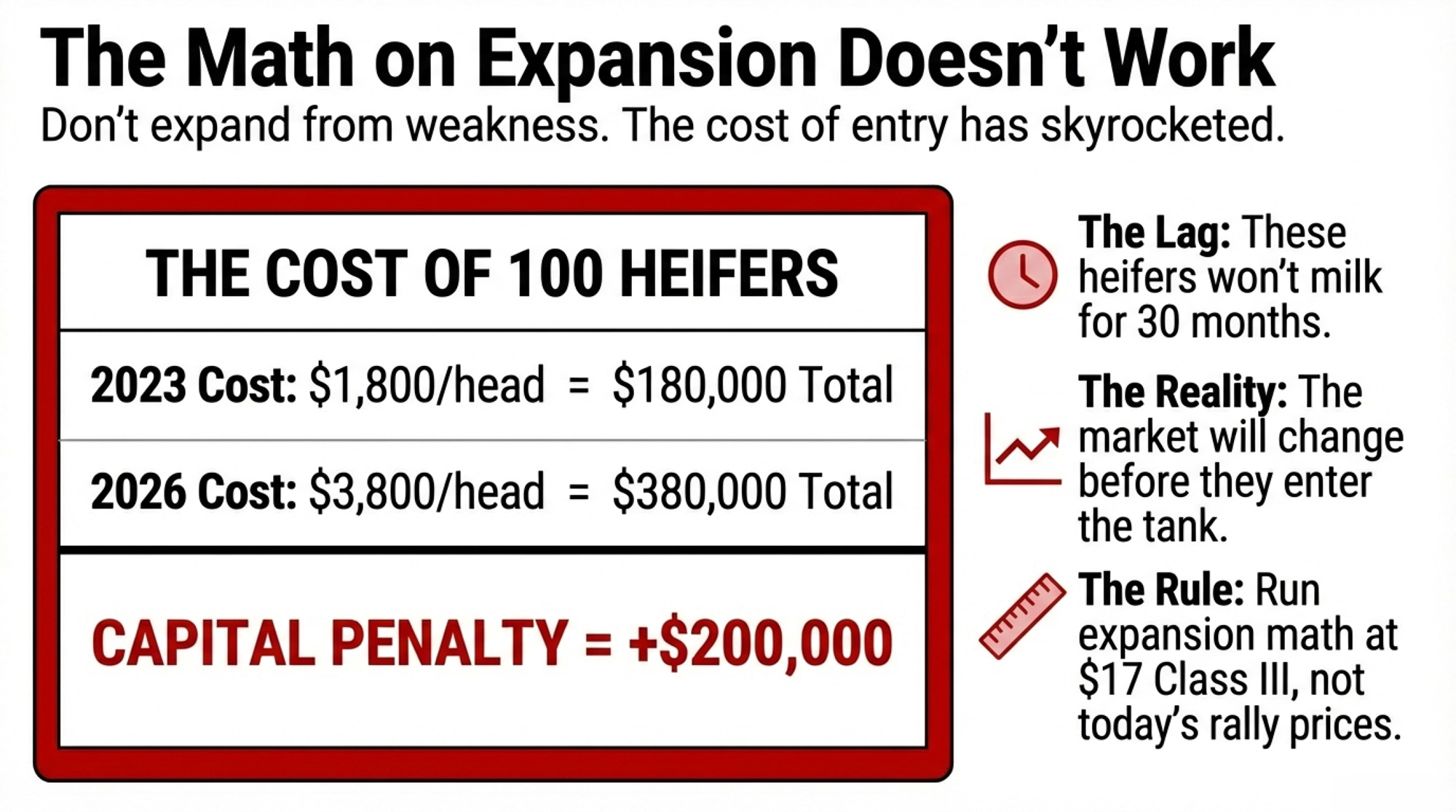

Head-Fake Math: Margins, Heifers, and Timing Traps

The immediate margin picture remains tough despite the GDT rally. USDA’s December 2025 All-Milk Price came in at $19/cwt, down 70¢ from November. January erodes by another $1/cwt-plus because Class III ($14.59) and Class IV ($13.55) prices are the lowest since July 2023 and February 2021, respectively. For operations in the Upper Midwest and similar regions—where many herds break even in the mid-$16/cwt range based on regional benchmarking data—Q1 2026 milk checks are already underwater.

The futures market sees improvement ahead, with Class III contracts trading in the $17-18/cwt range for Q2-Q3 2026 on CME. But here’s where the timing trap for expansion kicks in.

Replacement heifers currently run $3,000-$4,000/head according to USDA livestock data, versus $1,800 in 2023. A 100-heifer expansion now costs $120,000-$220,000 more in heifer costs alone than it would have two years ago—and those heifers won’t hit the milking string for 27-30 months. Market conditions will shift multiple times before the genetics purchased today reach the bulk tank. Producers running that heifer math are finding the rally looks different than it feels.

A December 2025 Bullvine analysis examined the expansion timing gap: operations expanding at 80% barn capacity with intact working capital face dramatically better outcomes than those expanding at 95% capacity with depleted reserves. This rally creates exactly the psychological conditions that lead producers to expand from weakness rather than strength.

Cost Category

2023 Cost (100-Head)

2026 Cost (100-Head)

Cost Increase

Replacement Heifers

$180,000 ($1,800/hd)

$350,000 ($3,500/hd)

+$170,000

Feed Costs (27-mo to freshening)

$81,000 ($810/hd)

$95,000 ($950/hd)

+$14,000

Facility/Equipment Allocation

$125,000

$160,000

+$35,000

Interest Carry (2-yr avg on capex)

$18,000 (5.5% rate)

$28,000 (7.2% rate)

+$10,000

TOTAL EXPANSION COST

$404,000

$633,000

+$229,000 (+57%)

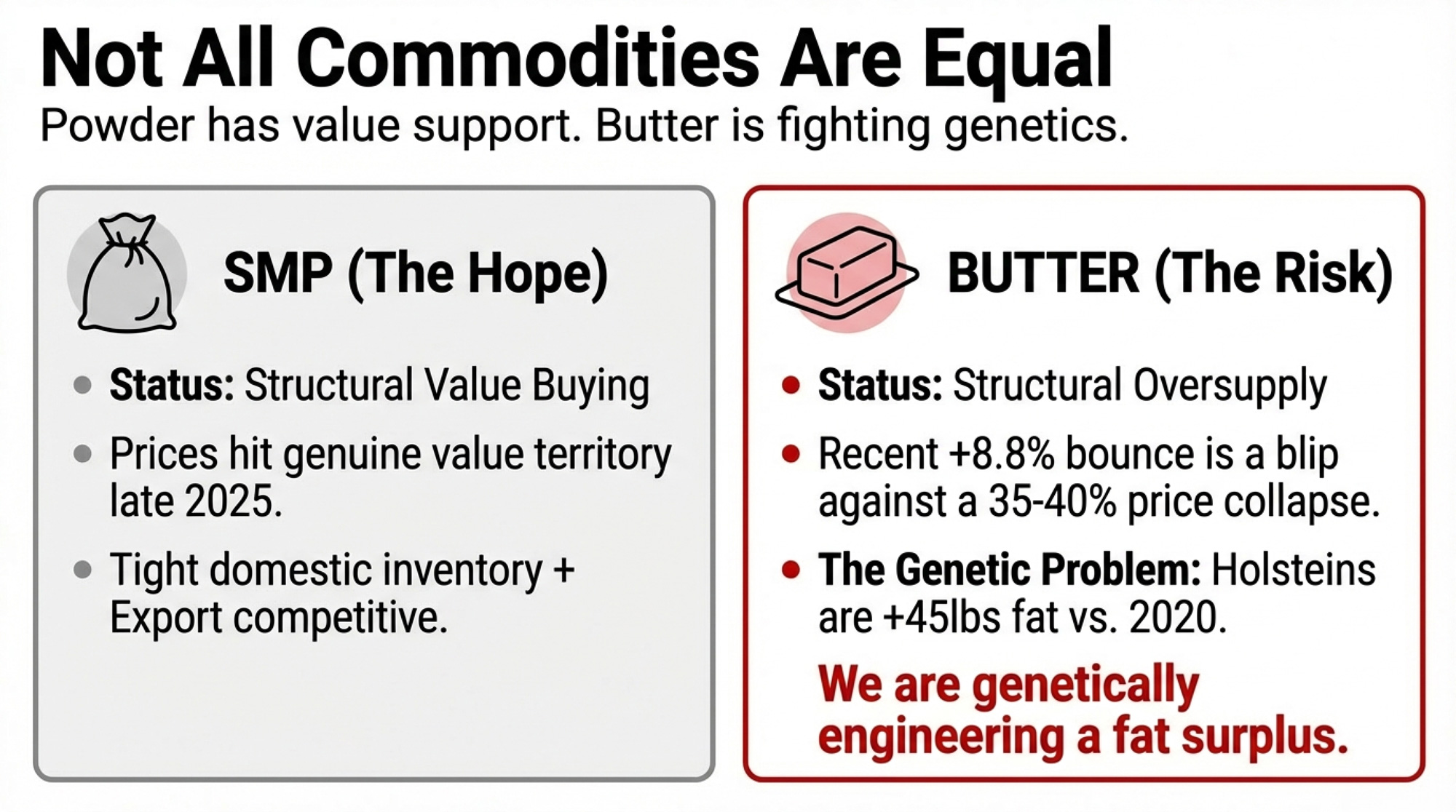

The Butterfat Head-Fake: Why Components Tell a Different Story

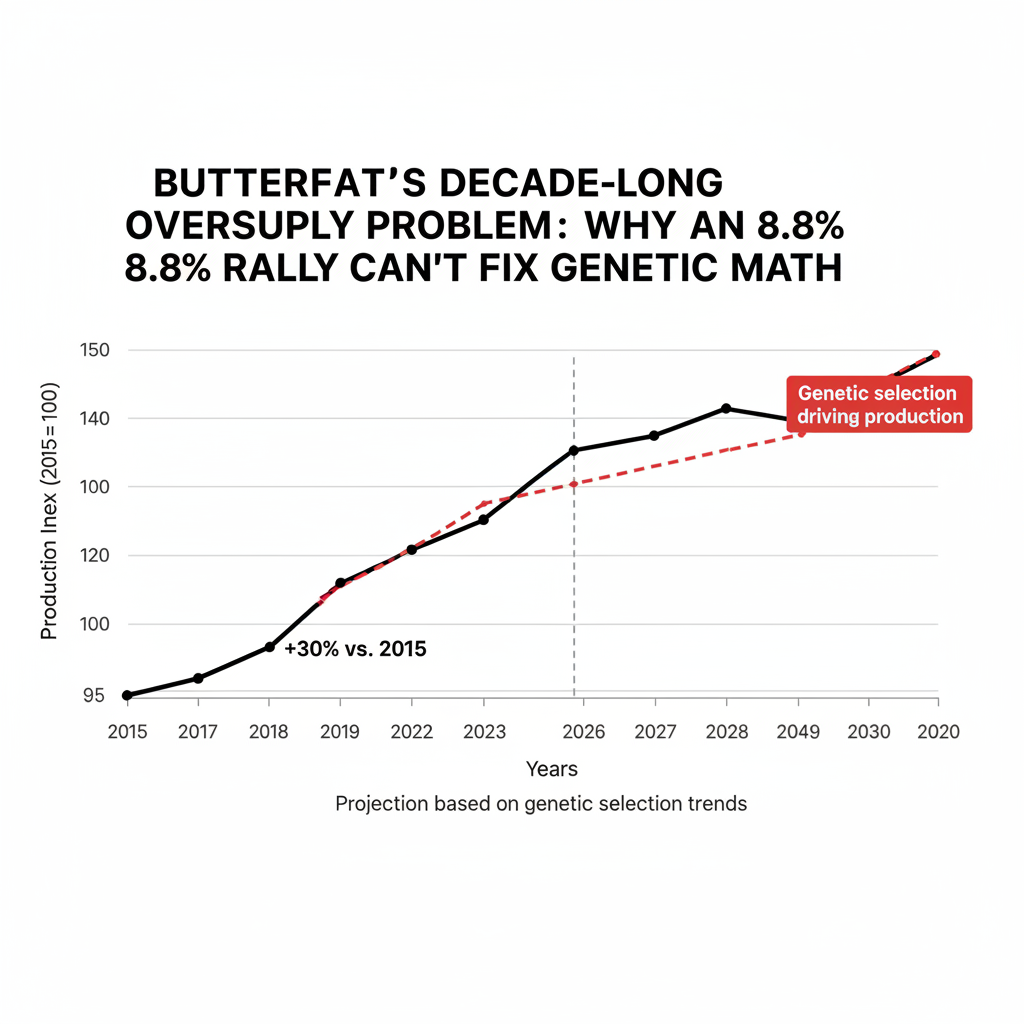

Product category behavior reveals which segments are genuinely rebalancing versus catching temporary bids. At the February 3 GDT auction, SMP led at +10.6% while butter rose 8.8% to $5,773/MT. That might look like broad-based strength. Context says otherwise: butter dropped roughly 35-40% from its May 2025 peak to December’s lows on GDT. The 8.8% bounce doesn’t erase that collapse.

The structural problem for butterfat is genetic. US butterfat production grew approximately 30% from 2011 to 2024, outpacing overall milk production growth. Corey Geiger of CoBank put it directly: “This isn’t a demand issue. It’s clearly a ‘We’re supplying way too much.'” Holsteins averaged a 45-lb butterfat rollback in the April 2025 CDCB evaluation—significantly higher than 2020 levels. The cows producing today’s oversupply are already in herds, and some geneticists project genetic selection could push average butterfat content toward 5% within the decade.

SMP tells a different story. Prices genuinely reached value territory at late-2025 lows ($1.18/lb equivalent on GDT), triggering buying that appears more structural than seasonal. Both CME and GDT powder markets are moving in sync, domestic inventories remain tight, and the US has regained export competitiveness after losing Asia market share to New Zealand in 2023-2024.

For hedging decisions, this divergence matters. Butter exposure carries a higher reversal risk post-Easter; powder positions have better structural support—though still vulnerable to the production surge.

Four Paths If This Is a Head-Fake

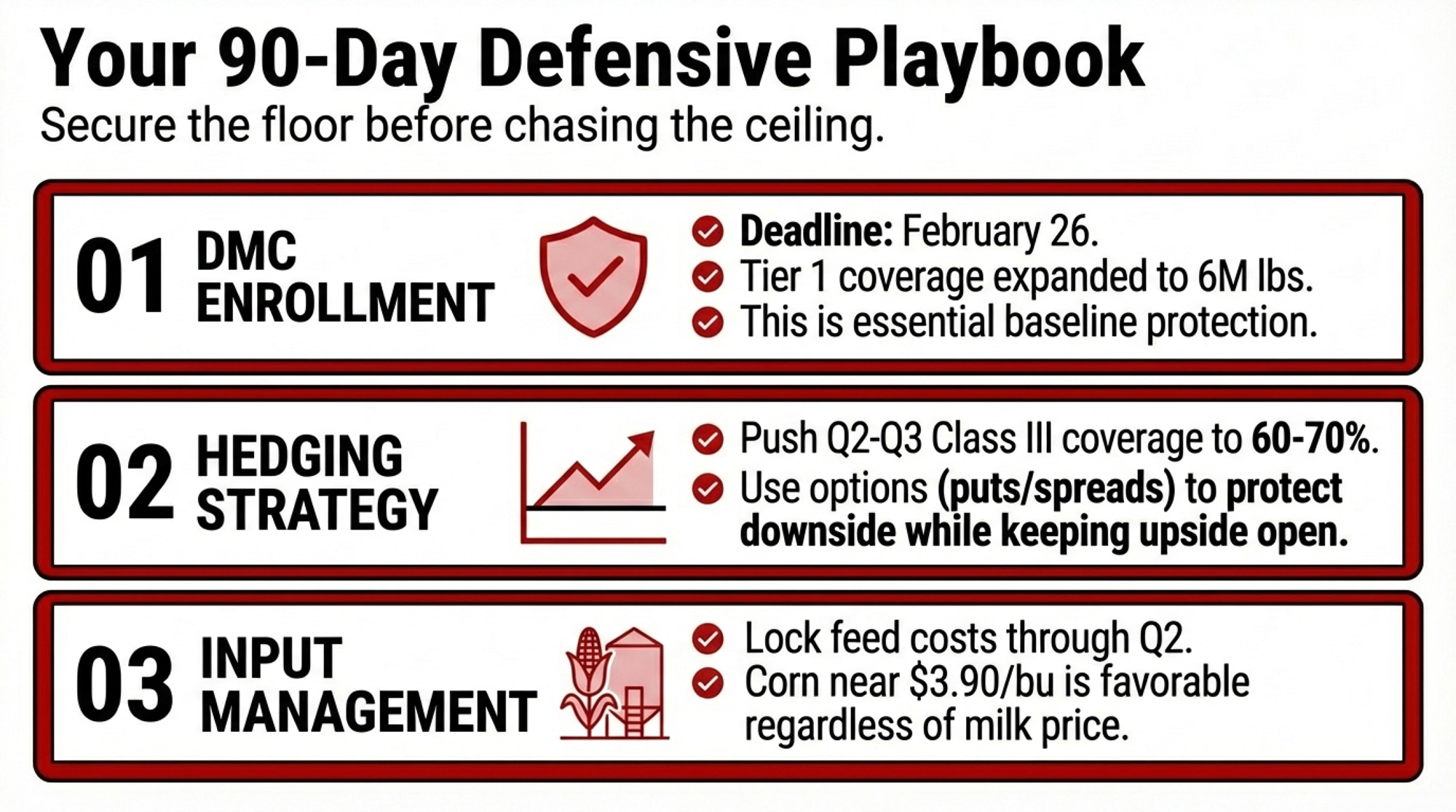

DMC Enrollment (Deadline: February 26, 2026)

USDA’s Tier 1 coverage was expanded to 6 million pounds for 2026, and analysts expect payments early this year amid current margin compression. The multi-year commitment option (2026-2031) locks in a 25% premium discount per FSA program terms.

Trade-off: You’re paying premiums through 2031 even if margins recover strongly. But current signals don’t support betting on a rapid recovery. Use the University of Tennessee DMC calculator to optimize coverage level for your production history.

Hedging Coverage

Risk management advisors often suggest 60-70% coverage at elevated premium levels for Class III, keeping 25-30% open for potential upside. Options (puts/put spreads) preserve participation if the rally extends, versus futures that lock you out of gains. Lock feed costs through Q2—corn near $3.90/bu on CME represents favorable input pricing regardless of milk price direction.

Trade-off: Over-hedging costs you if this rally proves structural; under-hedging hurts if April auctions give back Q1 gains.

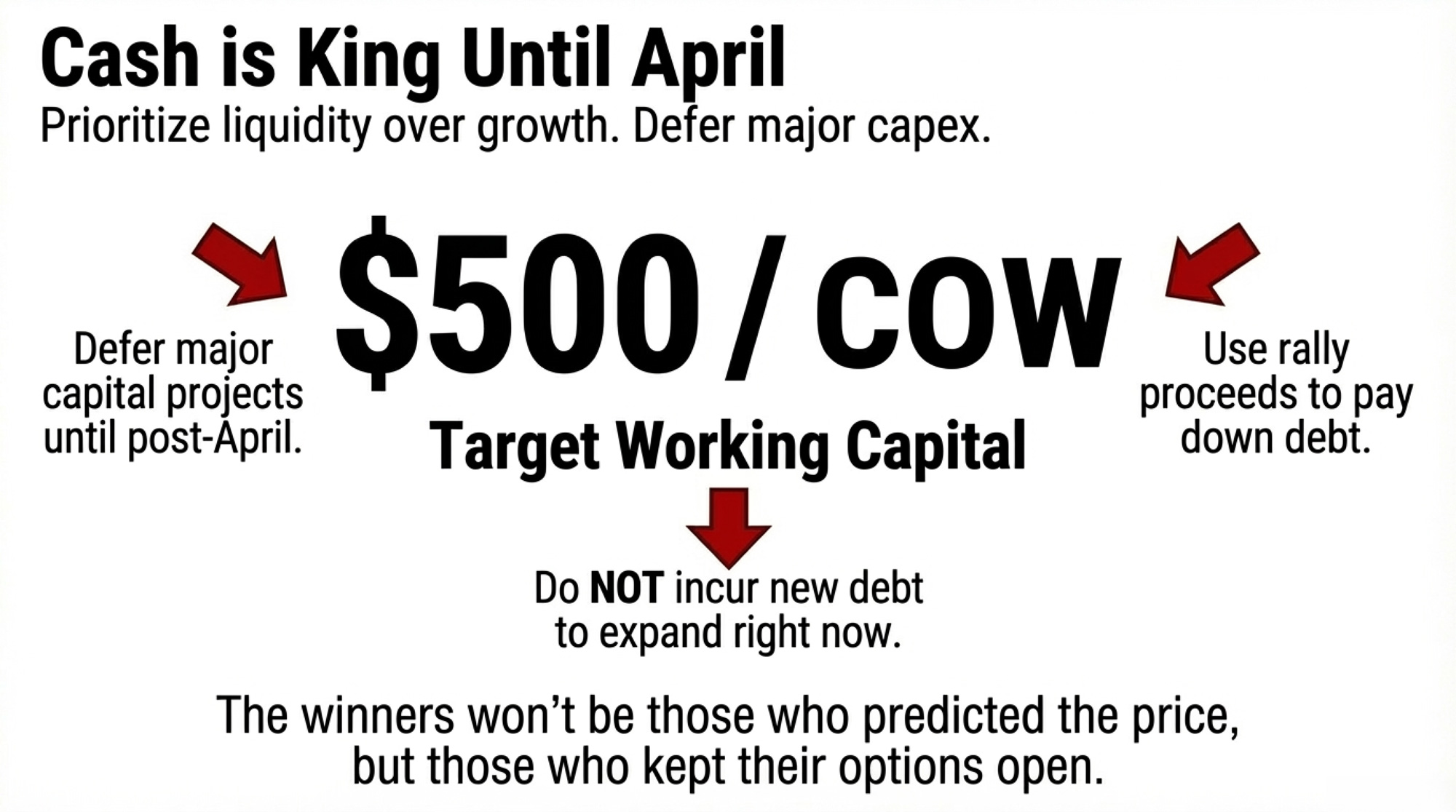

Capital Allocation

Lender reports indicate many producers are prioritizing paying down loans and building working capital over expansion. That’s the right read for this environment. Many advisors suggest targeting working capital at $500-550/cow before committing to expansion. Defer major capital projects until post-April GDT results confirm whether the rally has structural support.

Expansion Timing

Wait for post-holiday GDT auctions (April 7 and April 21) before committing. Test project economics at $17/cwt Class III, not current rally prices. Don’t expand from a position where depleted reserves require the rally to continue.

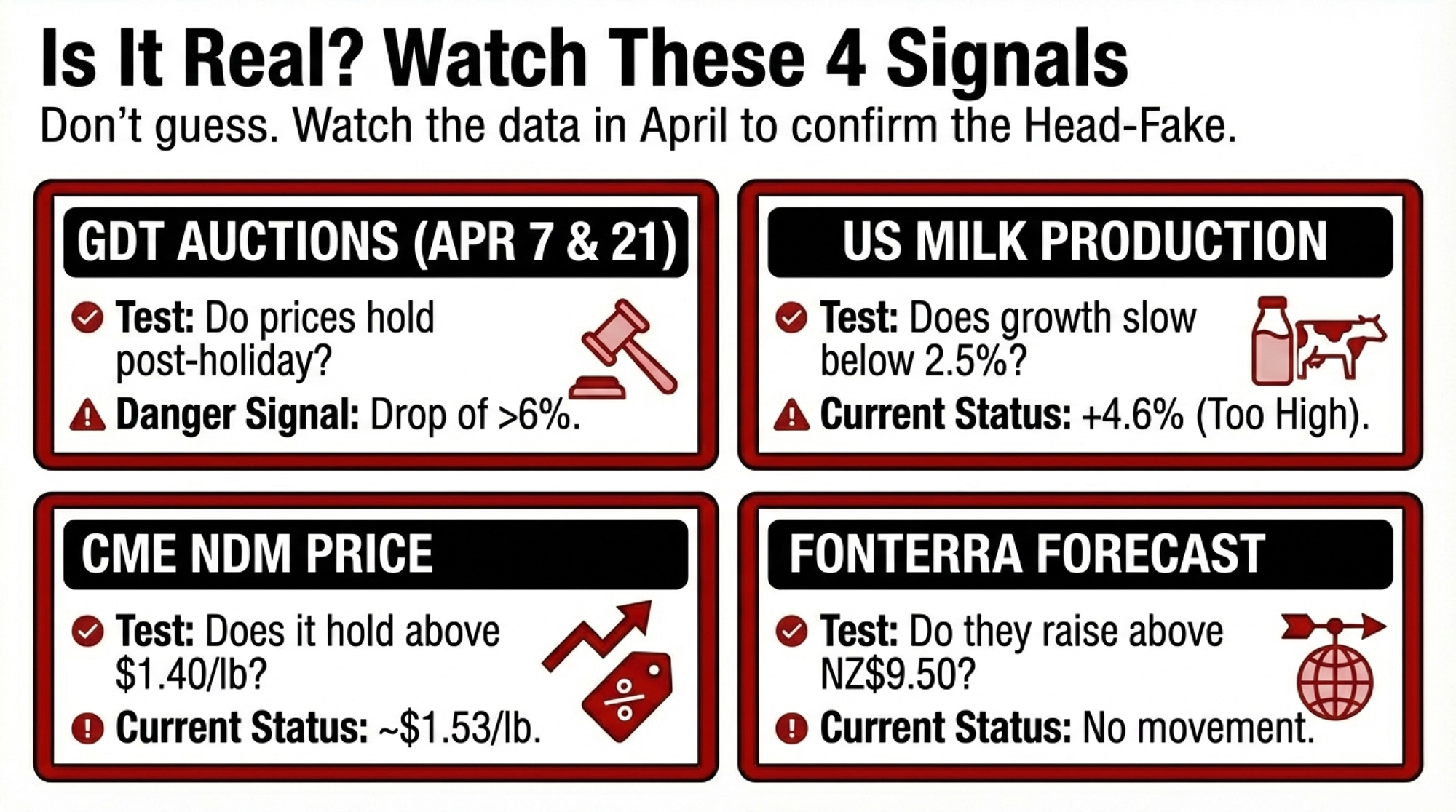

Four Indicators: Head-Fake or Real Recovery?

Indicator

“Recovery Has Legs”

“Head-Fake Confirmed”

GDT Post-Holiday (Apr 7, 21)

Prices hold within 3% of March highs

Drop 6%+ from March levels

US Milk Production

Growth moderates to <2.5% YoY by the March report

Continues at 4%+ YoY

CME Spot NDM

Holds above $1.40/lb through April

Falls below $1.25/lb

Fonterra Forecast

Raises above NZ$9.50

Holds or cuts below $8.50

The April 7 and April 21 auctions are the critical test per GDT’s published calendar. That’s when Ramadan and Easter demand releases. If prices hold, it’s fundamentals. If they crash, the head-fake is confirmed.

What This Means for Your Operation

Enroll in DMC by February 26. The expanded Tier 1 coverage and current margin compression make this a defensive baseline regardless of rally outlook.

If you’re hedged below 50% for Q2-Q3, the current rally provides an opportunity to add coverage. Target 60-70% total to balance protection with upside participation.

If you’re considering expansion, run your economics at $17/cwt Class III—not current futures—and don’t commit until April GDT results confirm or deny structural support.

The critical threshold: working capital around $500/cow before any major capital deployment. Below this, use the rally to strengthen reserves rather than expand commitments.

If you’ve been assuming the supply surge would self-correct through lower prices driving exits, check whether your region is actually seeing herd contraction. National USDA data shows the opposite.

Red flag: Any expansion plan that requires Class III to stay above $18/cwt carries an elevated risk given the current production trajectory.

Key Takeaways

The rally is real, but likely a seasonal head fake. Three consecutive GDT gains driven by Ramadan/Easter buying and inventory restocking—not structural rebalancing of a 4.6% US production surge.

April auctions are your decision point. The post-holiday GDT events (April 7 and 21) will reveal whether demand can absorb the supply wall. Don’t make irreversible commitments before then.

Butterfat and powder are telling different stories. SMP shows signs of genuine value buying; butter’s 8.8% bounce doesn’t offset a 35-40% collapse driven by structural genetic oversupply.

Use the rally to strengthen the position, not bet on continuation. Build working capital, add hedging coverage, pay down debt. The producers who maintain optionality will outperform those who commit prematurely.

The Bottom Line

The producers who navigate the next 90 days successfully won’t be the ones who correctly called the market’s direction. They’ll be the ones who kept their options open while others locked themselves into bets they couldn’t afford to lose.

Every cycle looks obvious in hindsight. Where does your operation sit on the spectrum between building reserves and betting on continuation?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Squeezed Out? A 12-Month Decision Guide for 300-1,000 Cow Dairies – Gain a concrete roadmap for navigating high replacement costs and component shifts. This guide breaks down robotic milking ROI and identifies specific management cuts that protect your cash flow when margins tighten.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

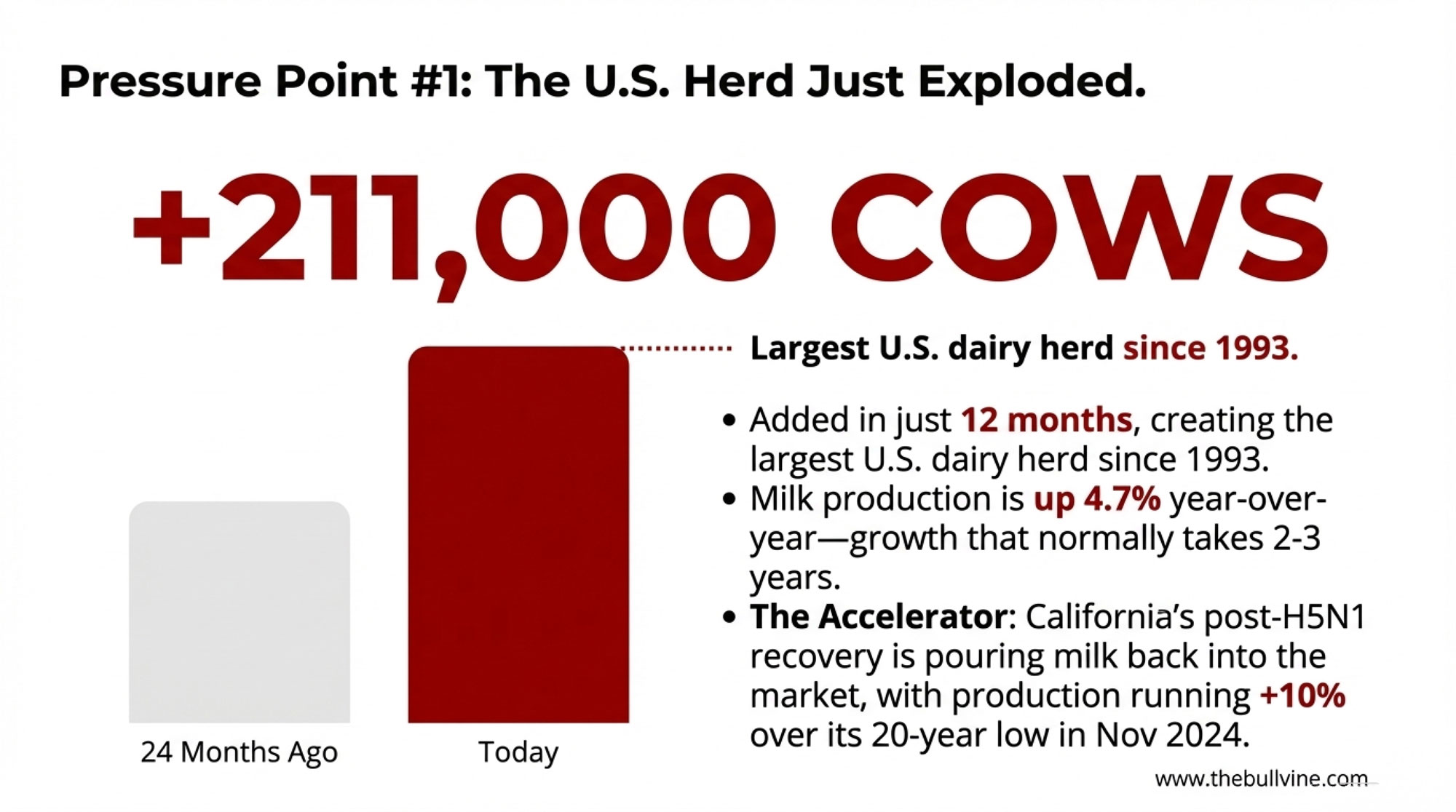

You’re bleeding $80/cow every month, and the industry just added 211,000 more cows to make it worse. 5 moves to make before spring.

Executive Summary: Every month you wait, you’re losing $80 per cow. Class III has crashed from $20 to $15.86 since spring—and the industry just added 211,000 cows to make sure it stays there. California’s rapid H5N1 recovery, surging EU production, and strong New Zealand output have created a global oversupply that isn’t easing anytime soon. Need replacements? Quality springers now cost $4,000-plus amid the tightest heifer pipeline in 20 years. Add $4.40 corn to the equation, and margins are getting crushed from every angle. Here’s what’s actually driving the squeeze—and five specific moves to protect your operation before spring.

The U.S. dairy industry just added 211,000 cows in 12 months—the largest herd since 1993, according to USDA NASS—at the exact moment Class III prices dropped from $20 to $15.86 per hundredweight. Meanwhile, anyone trying to expand is staring at $4,000 springers and the tightest heifer supply in two decades. That collision of forces is going to define 2026 economics for operations of every size, whether you’re milking 80 cows in Vermont or 8,000 in the Central Valley.

Let me walk through what the numbers actually show and what the producers who are navigating this successfully are doing differently.

The Production Surge Nobody Can Ignore

USDA NASS confirmed that November 2025 milk production in the 24 major states hit 18.1 billion pounds—a 4.7% jump from the prior year. Nationwide, we’re looking at 18.8 billion pounds, up 4.5% year-over-year. For context, that’s the kind of production growth that typically takes two to three years to accumulate. We got it in twelve months.

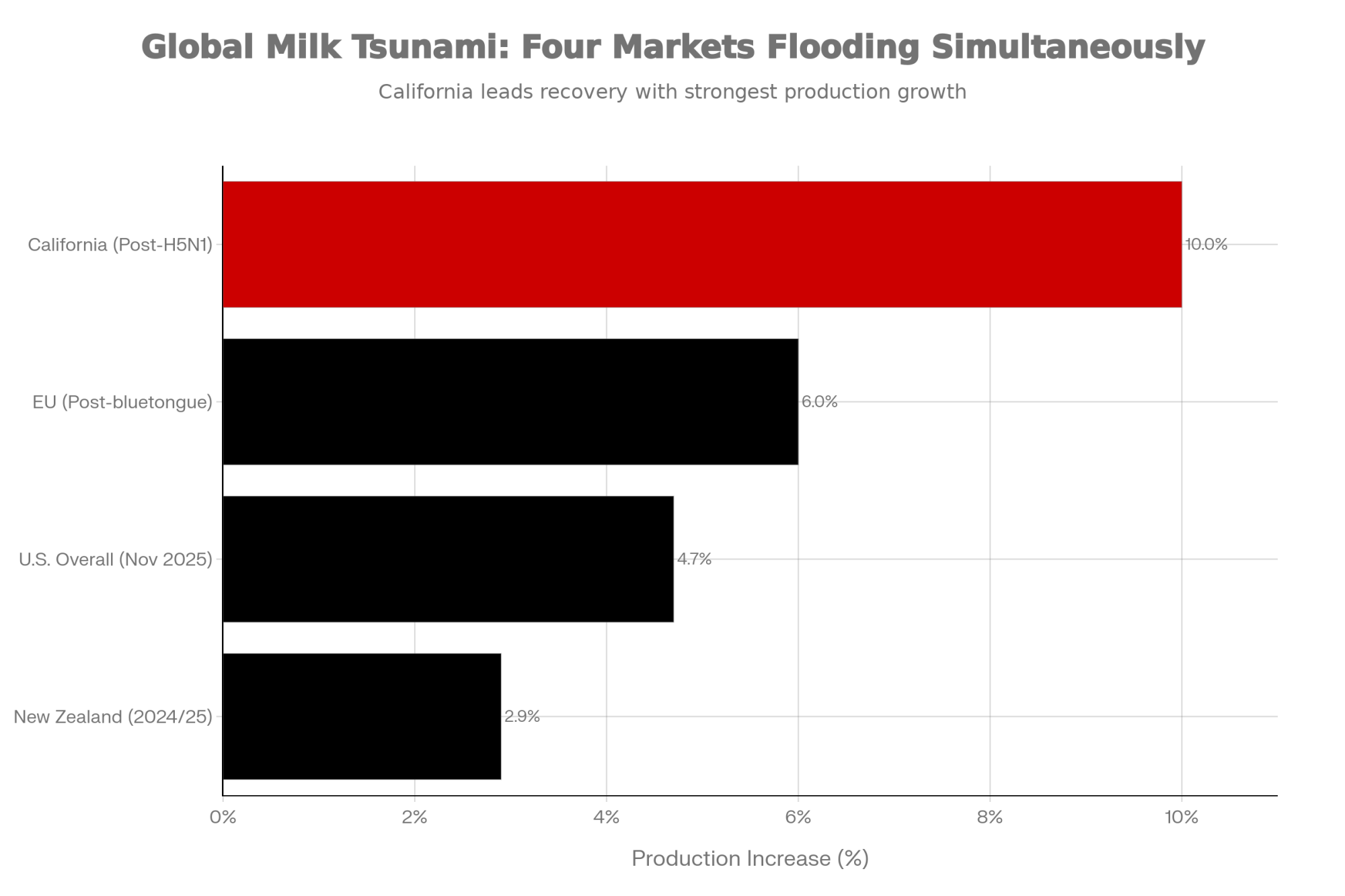

And California’s recovery has accelerated the math. After H5N1 hammered the state through late 2024 and into 2025—federal livestock program records indicate roughly 75% of commercial herds experienced infections at some point—production is now running more than 10% above year-ago levels. November 2024 represented a 20-year production low for California. The turnaround has happened faster than most analysts expected, and all that milk is flowing back into national markets.

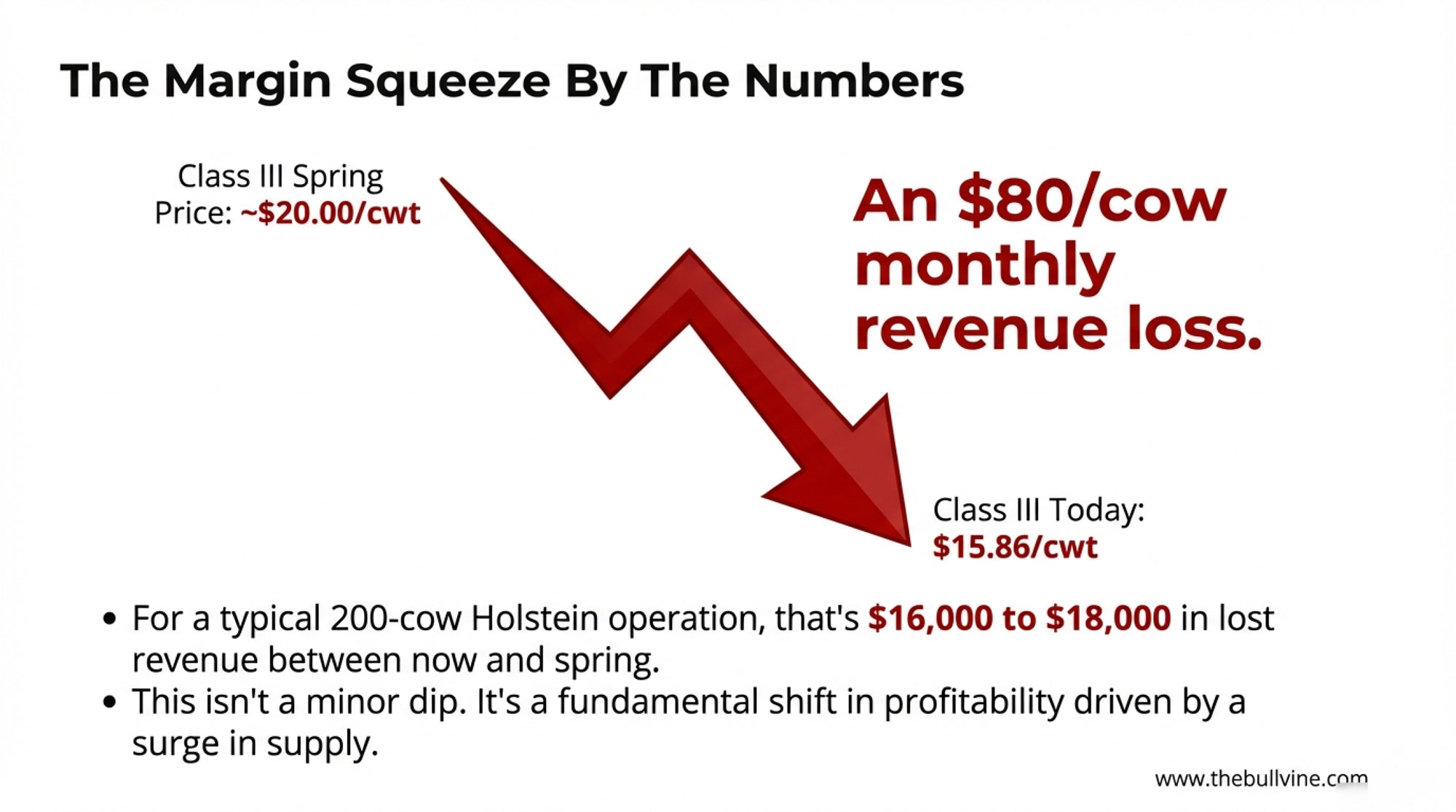

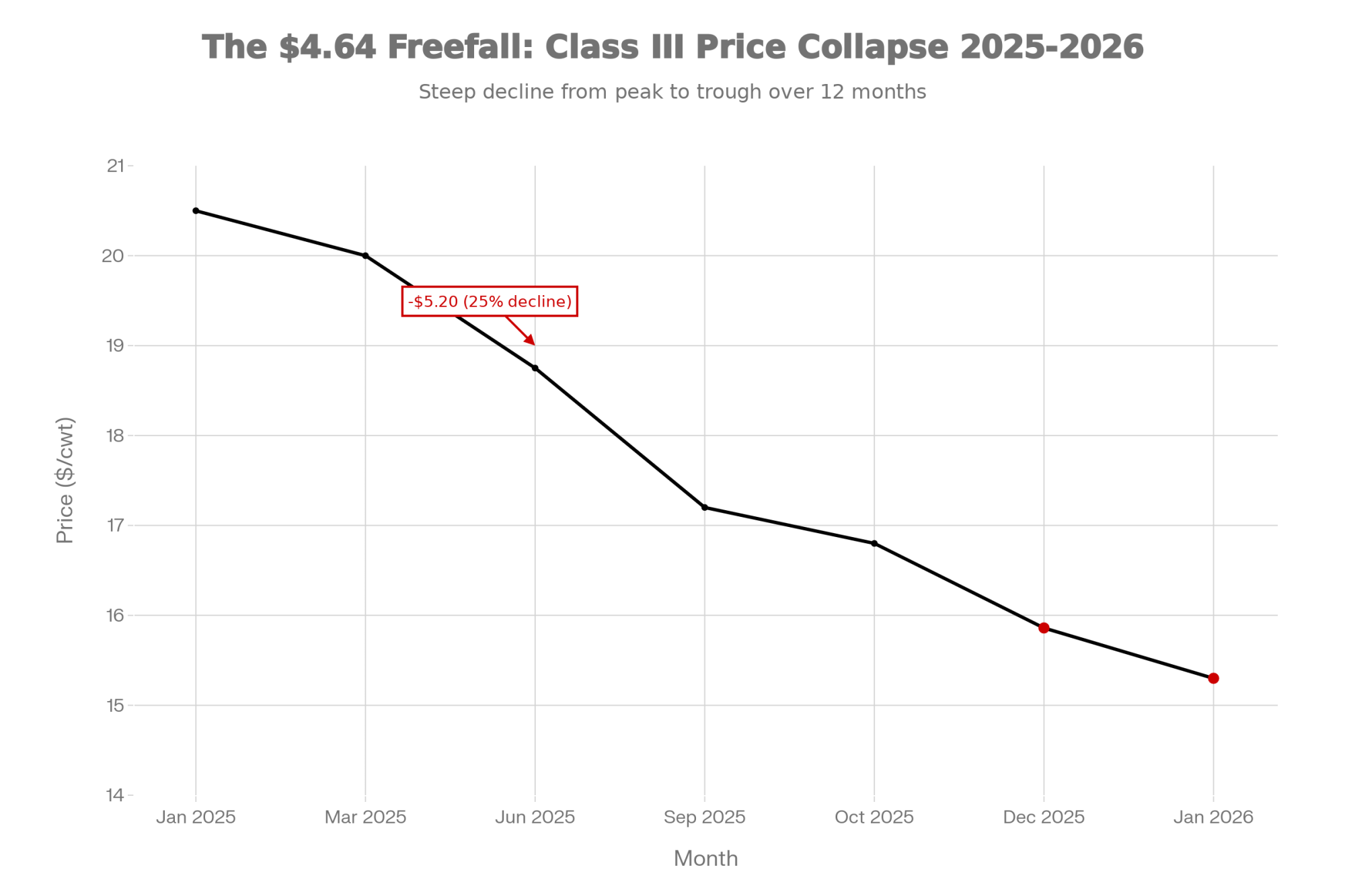

Class III milk prices have collapsed from $20.50 to $15.30 per hundredweight in just 12 months—a 25% decline that’s costing dairy producers $80-90 per cow monthly across all operation sizes

Here’s what this means for your check: at $15.86 Class III versus $18.50 three months ago, that’s roughly $80-90 per cow per month in lost revenue for a typical Holstein operation. On a 200-cow herd, you’re looking at $16,000-18,000 less coming in between now and spring—assuming prices don’t drop further.

Herd Size

Monthly Loss ($80/cow)

Spring Loss (3 months)

Annual Impact

50 cows

$4,000

$12,000

$48,000

100 cows

$8,000

$24,000

$96,000

200 cows

$16,000

$48,000

$192,000

500 cows

$40,000

$120,000

$480,000

1,000 cows

$80,000

$240,000

$960,000

2,500 cows

$200,000

$600,000

$2,400,000

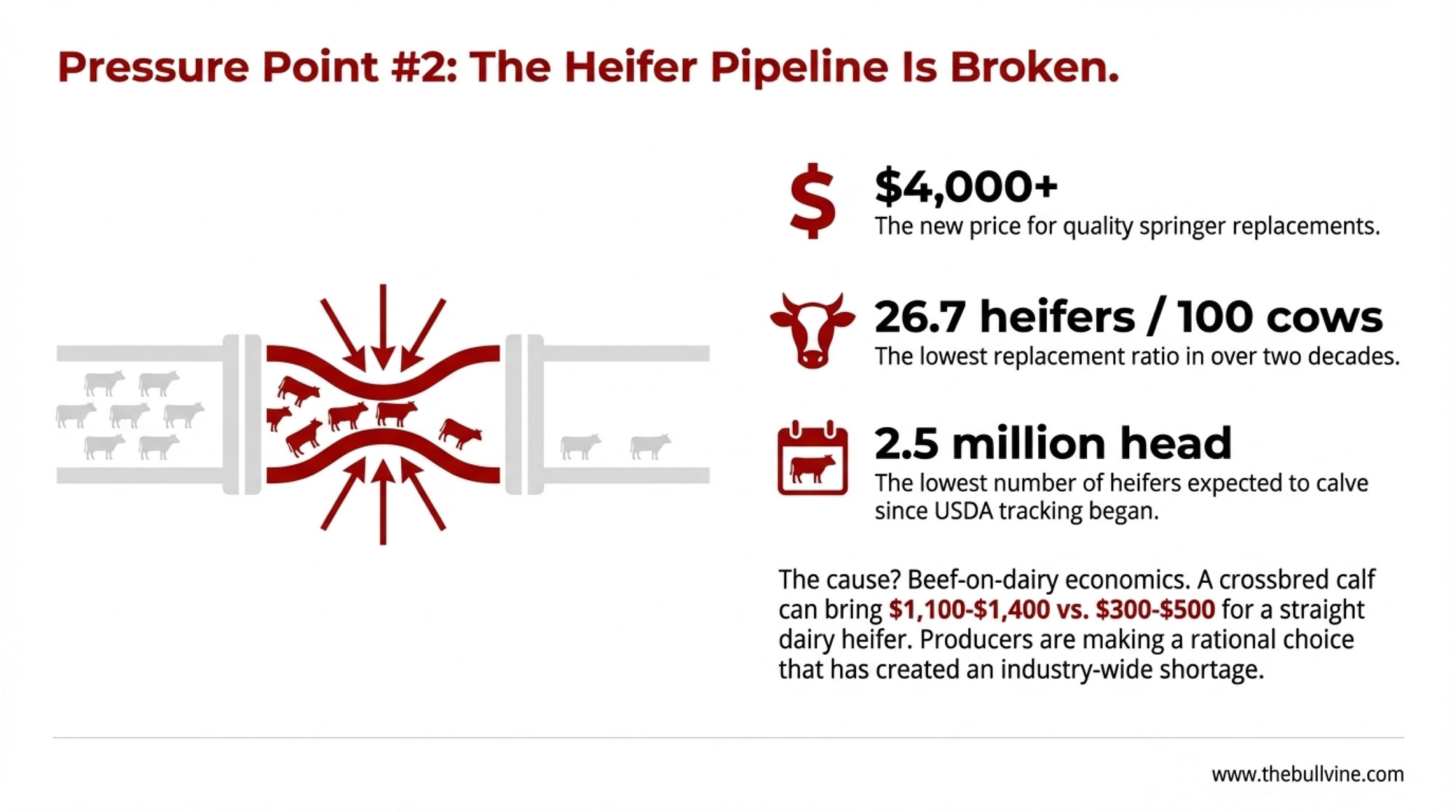

The Heifer Bottleneck Is Real

This is the constraint that will shape expansion decisions over the next three years, so let’s dig into it.

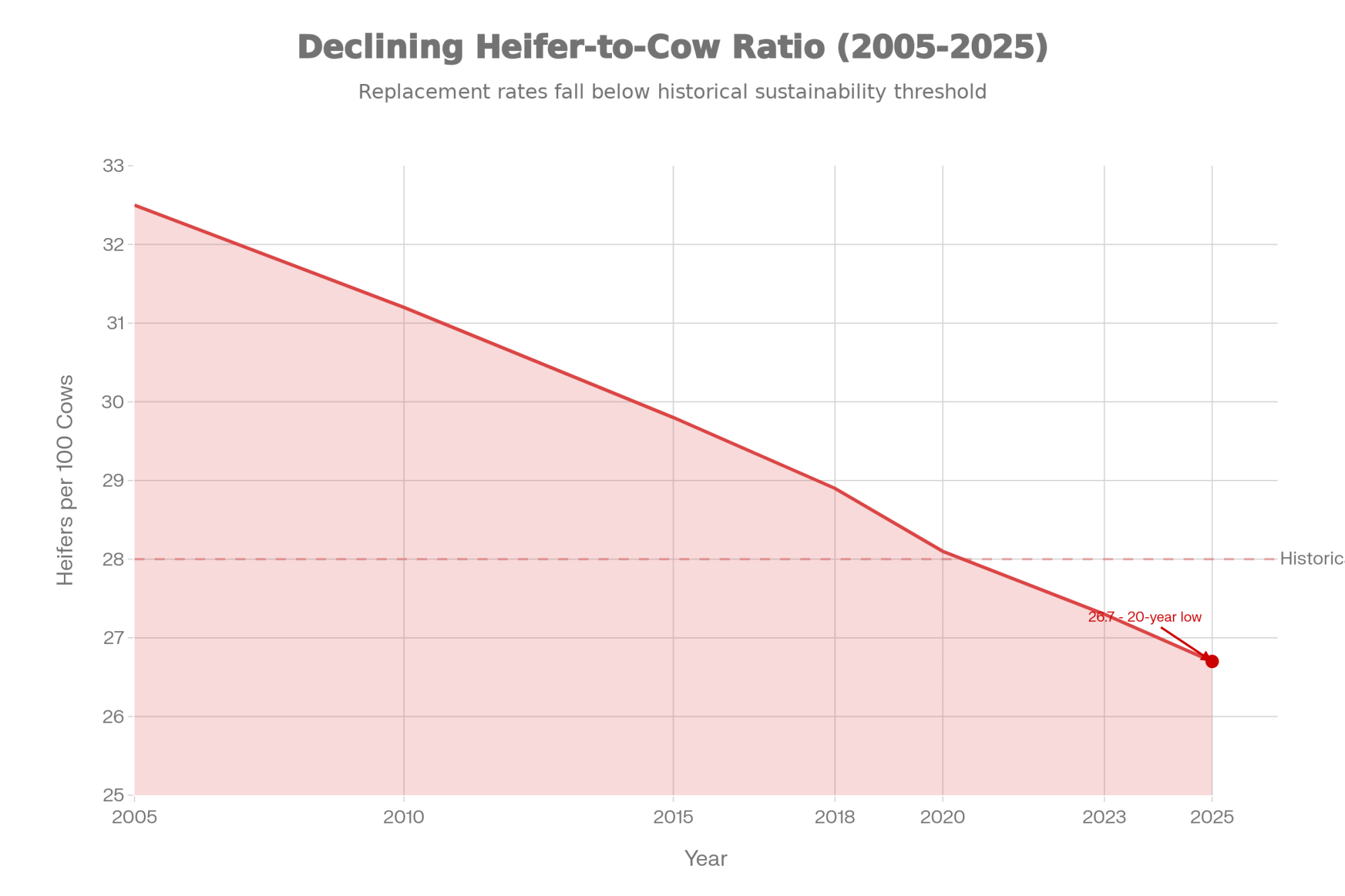

USDA data shows approximately 26.7 heifers expected to calve per 100 milk cows—the lowest ratio in at least two decades. Total dairy heifers expected to calve in 2025? Just under 2.5 million head, the lowest since USDA began tracking this metric.

The heifer-to-cow ratio has declined to a 20-year low of 26.7 per 100 cows, creating a replacement crisis that explains why quality springers now cost $4,000+ and why expansion-minded producers need to source animals immediately

The economics driving this aren’t mysterious. Ag Proud market reports show beef-cross calves bringing $1,100-1,400 at many auctions, sometimes higher for well-bred Angus or Limousin crosses. Straight dairy heifers? Often $300-500 unless they come from high-genomic programs with strong marketing. When beef-on-dairy creates that much value differential, producers make rational decisions about their breeding programs.

I was talking with a Wisconsin producer last month who’s running about 70% beef semen across his herd. His logic is straightforward: the premium on those crossbred calves more than offsets the cost of purchasing replacements when he needs them. For his operation and cash flow, that math works.

Metric

Beef-Cross Calf

Raise Own Dairy Heifer

Buy Springer

Calf Sale Value

$1,250

$400

N/A

Heifer Raising Cost (to calving)

$0 (sold)

$2,200

$0

Purchase Price (springer)

N/A

N/A

$4,000

Net Economics per Head

+$1,250

-$1,800

-$4,000

Value Differential

Baseline

-$3,050 vs beef

-$5,250 vs beef

A Northeast producer I know takes the opposite approach—she’s kept her replacement program intact because she doesn’t want to be buying springers at $4,000 when she needs them. Her calculation: the heifer she raises for $2,200 all-in is worth $1,800 more than the one she’d have to buy.

Both strategies can pencil out. The question is which matches your operation’s cash flow, facilities, and expansion timeline.

The practical implication: quality springer replacements now command $3,500-4,000 or more in many markets. If you’re planning any expansion over the next 18-24 months, heifer sourcing needs to be part of your planning conversation this month. The animals aren’t available in the numbers we’ve historically seen.

Global Oversupply Compounds the Problem

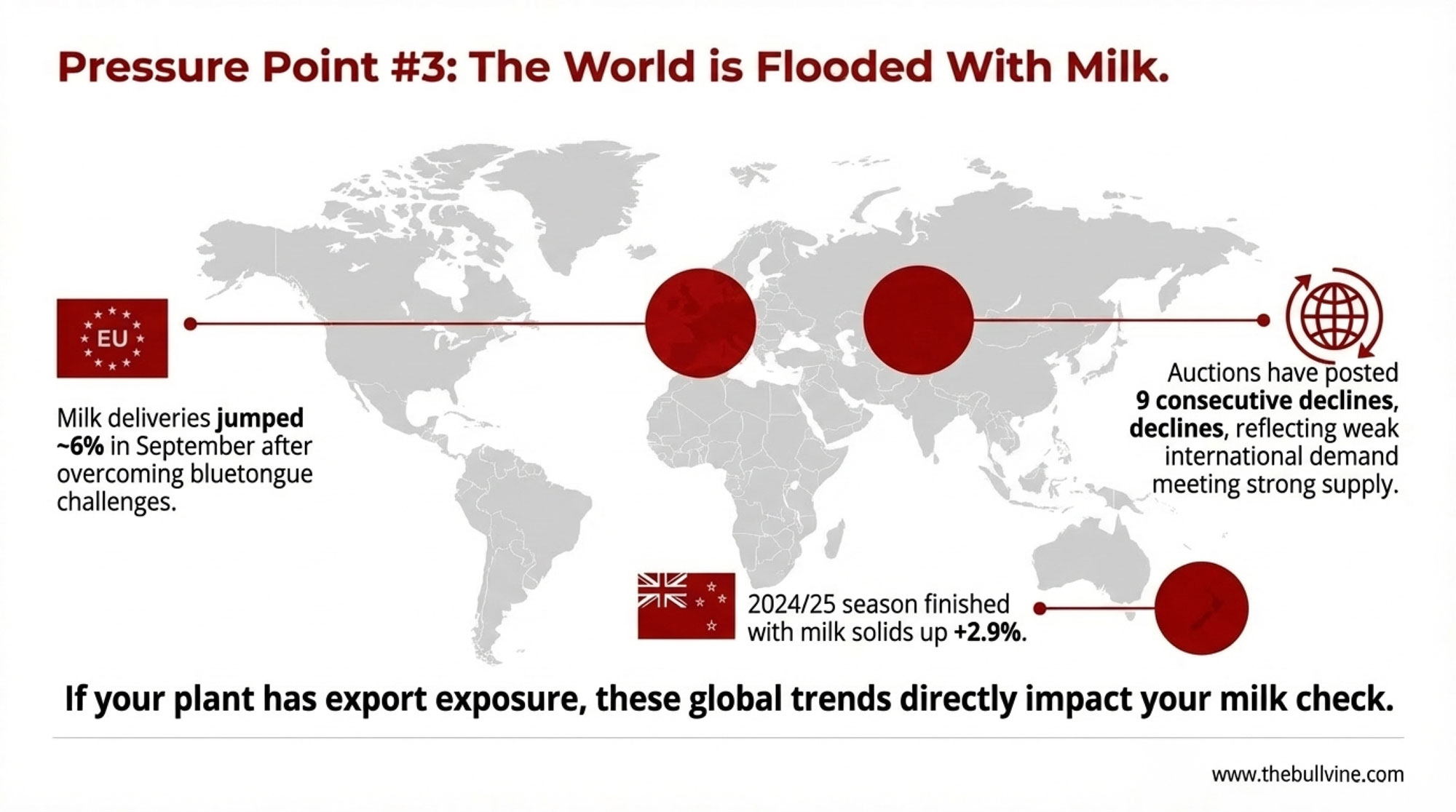

Four major dairy-producing regions are simultaneously flooding global markets with increased production—California up 10%, EU up 6%, U.S. overall up 4.7%, and New Zealand up 2.9%—creating synchronized oversupply that’s crushing milk prices worldwide

It’s not just U.S. production running hot. The latest AHDB market review shows EU milk deliveries jumped around 6% in September after the bloc worked through its bluetongue challenges. DairyNZ and LIC statistics show that New Zealand’s 2024/25 season finished with total milk solids production up 2.9% to 1.94 billion kilograms.

The Global Dairy Trade auctions have posted nine consecutive declines now, reflecting strong global supply meeting softer demand from key importing regions. If you’re shipping to a plant with export exposure—and that includes many operations in Wisconsin, Idaho, and the Southwest—those GDT results eventually flow back into your mailbox price.

For Canadian producers watching from across the border, the U.S. production surge creates its own dynamics. American oversupply tends to intensify pressure on USMCA access negotiations and affects cross-border pricing signals, even within the quota system.

California’s role amplifies these dynamics domestically. The state produces roughly 18% of U.S. milk, but here’s what really matters for price discovery: California Dairies Inc. alone churns over 480 million pounds of butter annually (about 23% of U.S. production), and the state manufactures the largest share of nonfat dry milk powder in the country. When California production swings, commodity pricing moves for everyone.

The Butter Paradox

Here’s something that looks like good news until you understand what’s actually happening.

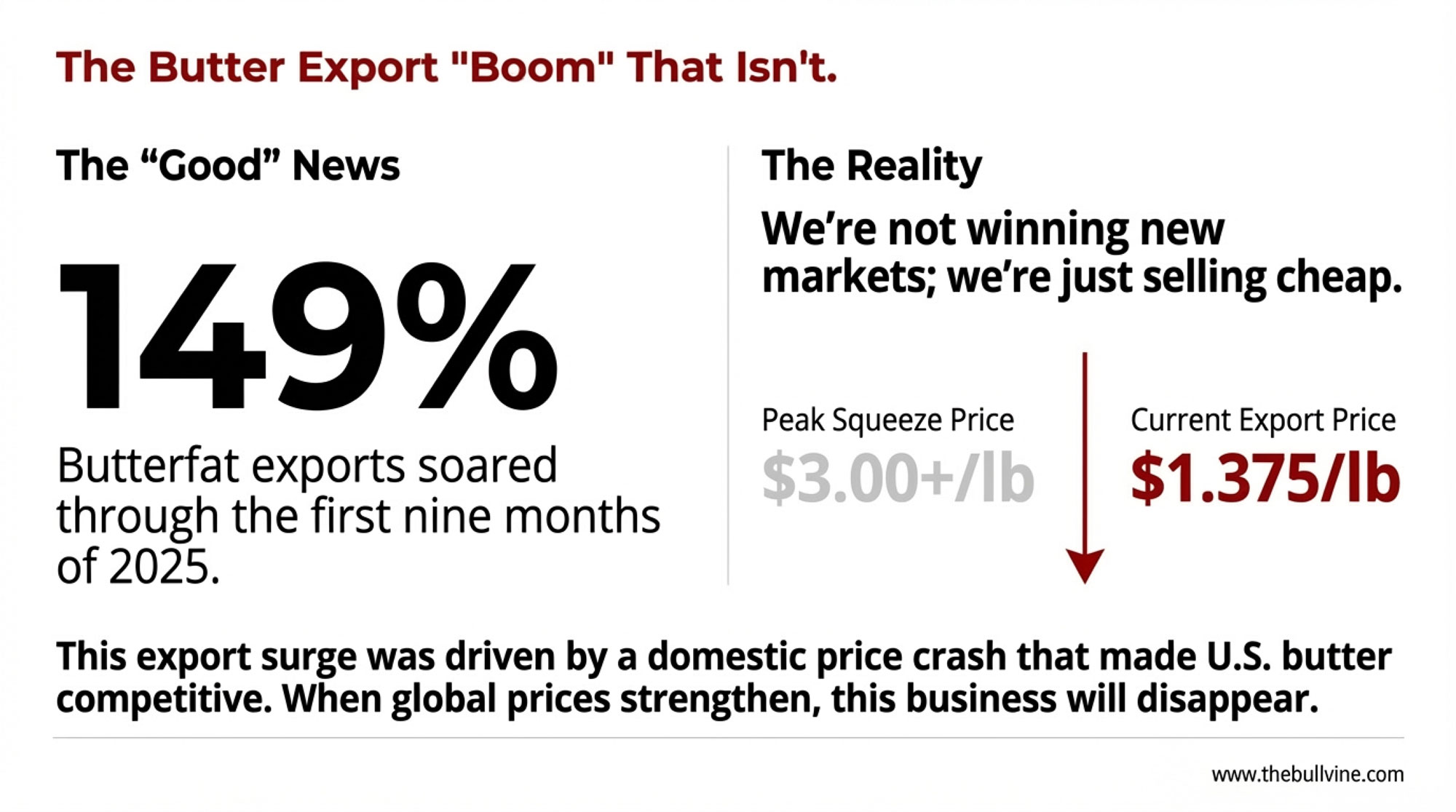

USDEC data shows butter exports surged in 2025. January alone was up 41% year-over-year, and through the first nine months, total butterfat exports soared 149%.

Sounds great, right? Here’s the catch: U.S. prices had dropped enough to compete in markets we typically can’t reach. Brownfield Ag News reports CME spot butter trading around $1.375 to $1.40 per pound as we moved into January—a long way from the $3.00-plus prices we saw during the supply squeeze.

We were essentially selling butter globally because domestic prices made us competitive, not because we’d developed new market access. That’s fundamentally different from export growth driven by structural demand improvement. When global prices strengthen, that business disappears.

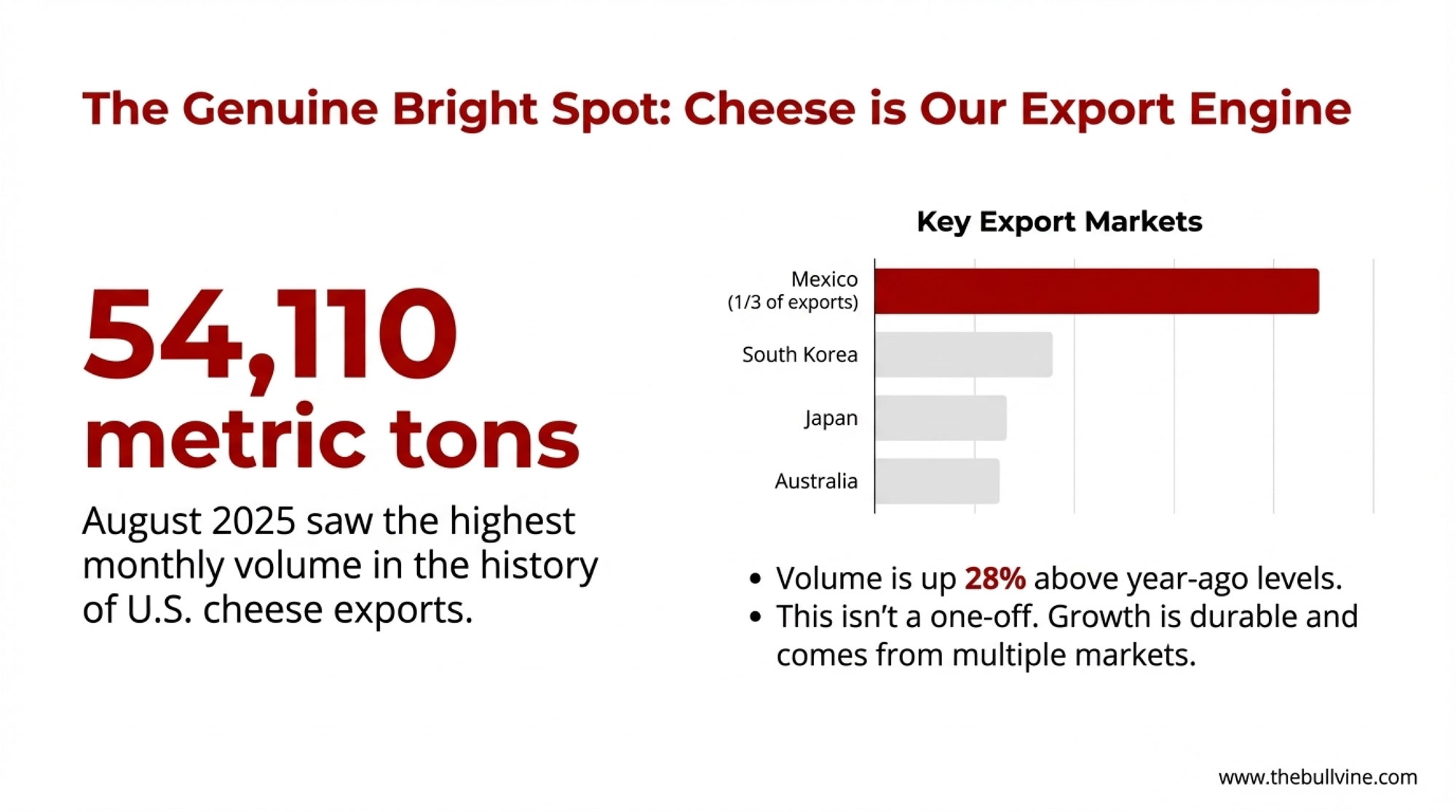

Cheese Exports: The Genuine Bright Spot

If you’re looking for actual strength in the dairy complex, cheese exports tell a legitimately positive story.

USDEC confirmed that August 2025 reached 54,110 metric tons—the highest monthly volume in the history of U.S. cheese exports. That’s 28% above year-ago levels, and the growth has come from multiple markets rather than depending on any single buyer.

Mexico remains our foundation, accounting for roughly a third of total U.S. cheese exports, according to USDEC trade data. But South Korea, Japan, and Australia all posted strong growth in the first half of 2025. The fundamentals here—growing global demand, improved U.S. product quality, established market relationships—look durable.

One constraint worth watching: USTR data shows USMCA quota utilization is still around 42%, suggesting meaningful upside if Canadian market access improves. That’s a trade policy question beyond any individual producer’s control, but it represents real unrealized potential.

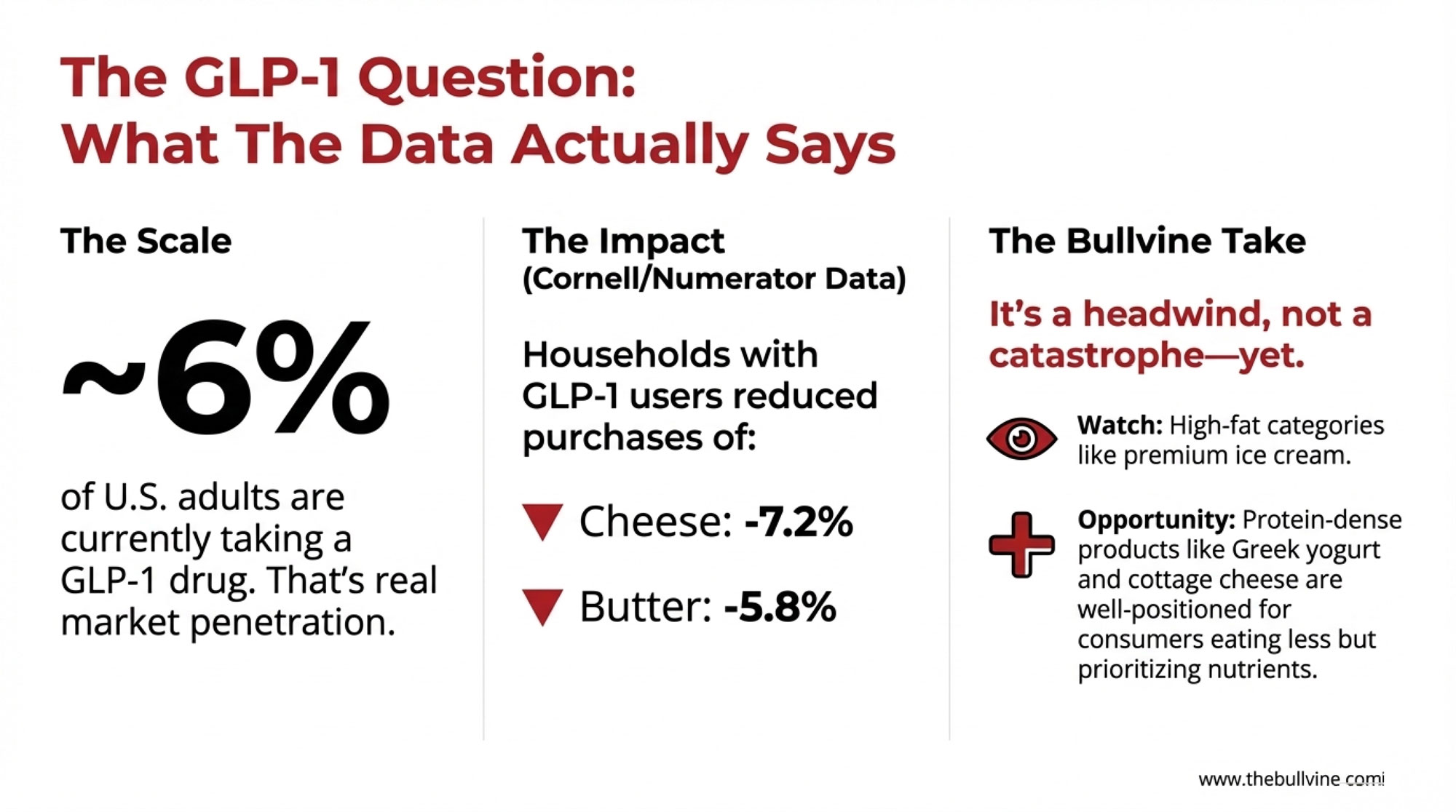

The GLP-1 Demand Question

GLP-1 drugs have some dairy economists predicting significant demand shifts. The actual data tells a more nuanced story, concerning in specific categories but not the catastrophe some suggest.

Kaiser Family Foundation polling indicates about 12% of American adults have used a GLP-1 medication at some point, with roughly 6% currently taking one. That’s real market penetration.

Cornell University and Numerator recently published detailed grocery purchasing data on this population. Households with GLP-1 users reduced cheese purchases by 7.2% and butter by 5.8%. They cut sweet bakery items and cookies by 6-11% across categories.

Here’s how I’d frame this practically: it matters, but it’s not an existential threat—yet. The protein density of dairy actually positions products like Greek yogurt and cottage cheese favorably for consumers who are eating less but prioritizing nutrient-dense foods.

Where I’d watch more carefully is high-fat categories. If GLP-1 adoption reaches the 15-24% levels Morgan Stanley projects for the early 2030s, premium ice cream and butter-heavy applications could face meaningful headwinds. Worth factoring into long-term product mix thinking, but not a reason to panic about 2026.

Current Price Reality

Let’s be direct about where we are.

According to USDA’s official Class and Component Price announcements, December Class III came in at $15.86/cwt—January futures point to the low-to-mid $15 range. That’s the math when production expands as quickly as it has.

The Class III to Class IV spread has been particularly notable. December showed Class III at $15.86 versus Class IV at $13.64—a $2.22 gap favoring cheese markets over butter and powder. If you’re a Class IV shipper, you’ve felt that spread directly in your check. Geography and market assignment matter more than usual right now.

On the feed side, corn has been trading around $4.40 per bushel according to Trading Economics futures data. USDA projects an average farm price around $4.00 for the 2025/26 marketing year, which would provide some relief—but that’s not guaranteed.

What to Do Before Q2

Based on the data and the producer conversations I’ve been having, here are five moves worth considering before spring:

Run your break-even calculation this week. Know exactly what Class III price puts you underwater. If you haven’t updated this math since prices were $20, you’re operating blind. Have contingency triggers ready—what do you cut first at $15? At $14?

Audit your heifer pipeline now. Calculate your replacement availability for the 2027-2028 calving. If you’re below 28 heifers per 100 cows, start sourcing conversations immediately. Set a price ceiling before you need animals urgently—desperation buying at $4,500 in twelve months is a lot more expensive than planned purchasing at $3,800 today.

Evaluate your beef-on-dairy math quarterly. The premium calculation shifts with calf prices and heifer availability. A 70% beef semen strategy that worked at $1,400 crossbred calves might need adjustment if those prices soften. Don’t set-and-forget your breeding program.

Review feed cost protection. With corn at $4.40 and possible relief toward $4.00, evaluate whether forward contracts make sense for Q1-Q2 before spring planting volatility. Locking in $4.25 corn looks smart if prices spike; it looks expensive if they fall to $3.80. Know your risk tolerance.

Examine your processor relationship. If you’re Class IV-dependent and watching checks come in $2.20 below Class III equivalents, it’s worth exploring whether component shipping options or processor alternatives exist in your region. Not every operation has flexibility here, but some do and aren’t using it.

The Bottom Line

The operations that navigate the next 12-18 months successfully won’t be the ones waiting for prices to recover on their own. They’ll be the ones who used this window to lock in replacement animals before the shortage intensifies, controlled feed costs where possible, and knew their break-even to the penny.

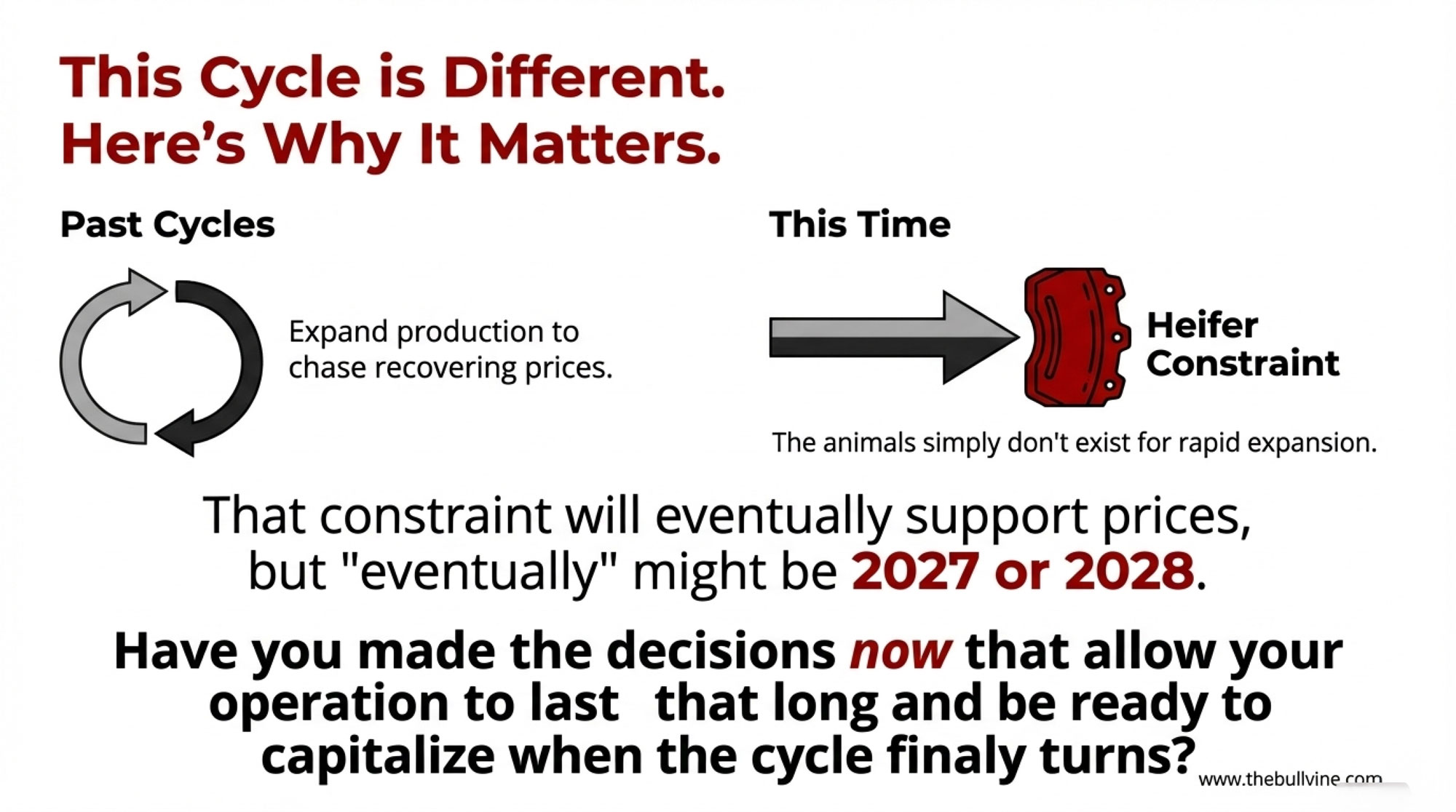

Dairy has always been cyclical. Strong production, recovering global supply, and moderating prices—we’ve been through this pattern before. What’s different this time is the heifer constraint underneath it all. The industry can’t simply expand out of tight margins when replacement animals don’t exist.

That constraint will eventually support prices. But “eventually” might be 2027 or 2028. The question is whether your operation’s financial position lets you wait that long—and whether you’re taking the steps now that position you to expand when the cycle turns.

The fundamentals of dairy demand remain constructive. Protein consumption is growing. Convenience continues driving category growth. Despite years of plant-based competition, real dairy holds its market share.

Those realities matter. But so does the math of $15.86 Class III with $4.40 corn and $4,000 springers. The producers who acknowledge both—the long-term demand strength and the short-term margin pressure—are the ones making decisions right now that they won’t regret in 2027.

Key Takeaways

You’re bleeding $80/cow monthly — Class III crashed to $15.86; that’s $16,000 vanishing from a 200-cow herd before spring

211,000 cows added in 12 months — Largest U.S. herd since 1993; prices won’t recover until supply corrects

Springers hit $4,000+ — Tightest heifer pipeline in 20 years; replacement economics have flipped

Global milk keeps flooding in — California +10%, EU +6%, New Zealand +3%; no relief coming in 2026

5 moves to make now — Know your break-even, source heifers before desperation, reassess beef-on-dairy, lock feed, review your processor

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – Master the precise breeding ratiostop-tier herds use to thrive and secure an immediate cash flow advantage. This breakdown arms you with the math to capture $700 premiums per calf without sacrificing your future replacement pipeline.

The 90-Day Dairy Pivot: Converting Beef Windfalls into Next Year’s Survival – Convert fleeting beef premiums into long-term resilience before the 2026 market shift hits your balance sheet. This analysis delivers the component-focused economic strategy and processor relationship audit required for survival in a $17 milk environment.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Dec 15: Germany’s butter -9.3%. Chicago cheese at 18-month low. NZ powder is falling. Every dairy market crashed the same week—despite record exports. What broke, and what’s next for your operation

Executive Summary: Record dairy exports should lift prices—instead, every global market crashed simultaneously the week ending December 15, 2025, revealing that fundamental pricing mechanisms have broken. U.S. cheese shipments hit all-time highs while CME prices fell to 18-month lows; European butter dropped 5.8%; powder weakened globally. The paradox persists because cheap feed costs ($4.40 corn) enable production growth despite distressed milk prices—the normal supply response isn’t working. Worse, processors worldwide are simultaneously shifting from butter into cheese, creating concentrated inventory that will mature in Q2 2026 precisely when the spring flush arrives—a collision that could severely pressure spot milk prices. This signals a structural reset, not a cyclical downturn: operations must rebuild for sustained viability at $15-16 milk through cost efficiency, component optimization, balance sheet strength, and strategic feed hedging. The industry emerging from this transition will operate under fundamentally different economics than those of the past decade.

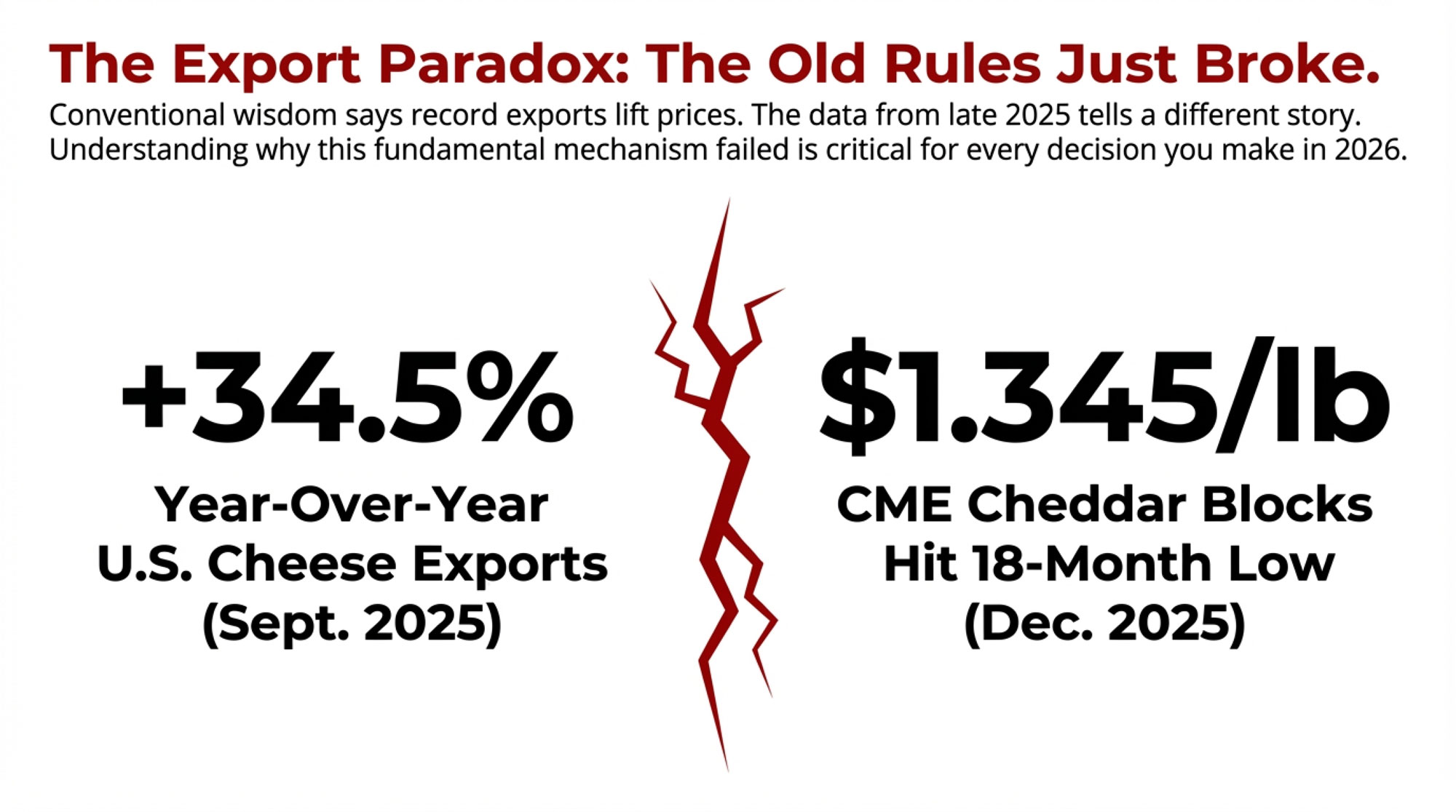

You probably felt it in your milk check before you saw it in the data. But here’s what actually happened the week ending December 15, 2025: butter futures crashed 3.6% in Leipzig to €4,314. EU physical butter dropped 5.8% to €4,313. Whole Milk Powder on the Global Dairy Trade fell to $3,230 per metric tonne. And CME Cheddar blocks hit $1.345 per pound—the lowest since July 2023. When every major commodity tanks simultaneously across every major exchange, we’re not looking at another rough patch. We’re watching the global dairy industry reset itself in real time.

Market/Product

Price (Week of Dec 15)

Weekly Change

Significance

German Butter

€4,150/tonne

-€425 (-9.3%)

Steepest weekly crash

EU Physical Butter (avg)

€4,313/tonne

-€251 (-5.8%)

18-month low

CME Cheddar Blocks

$1.345/lb

-4.1%

Lowest since July 2023

Global Dairy Trade WMP

$3,230/tonne

-3.8%

Sustained weakness

Dutch Butter

€4,070/tonne

-€250 (-5.8%)

Export benchmark falls

EEX Butter Futures (Leipzig)

€4,314/tonne

-3.6%

Futures signal no recovery

EU Young Gouda

€2,961/tonne

-34.3% YoY

Near five-year lows

EU Mild Cheddar

€3,248/tonne

Just €4 above 5-yr low

Testing historical floor

Here’s the part that should really get your attention: U.S. cheese exports hit 116.5 million pounds in September—up 34.5% from the previous year and representing the highest daily average on record, according to the U.S. Dairy Export Council. Record exports should be lifting prices, not coinciding with an 18-month low. That mechanism just broke, and understanding why matters for every decision you’re making about 2026.

Month

U.S. Cheese Exports (Million lbs) – Left Axis

CME Cheddar Blocks ($/lb) – Right Axis

Mar 2025

95.2

$1.62

Apr 2025

98.7

$1.58

May 2025

102.3

$1.54

Jun 2025

107.8

$1.49

Jul 2025

110.5

$1.46

Aug 2025

113.2

$1.41

Sep 2025

116.5

$1.38

Dec 2025

118.8 (est)

$1.345

A Brief Look Back: Context for What We’re Seeing

Before diving into current dynamics, it’s worth understanding that synchronized global dairy price collapses of this magnitude are relatively rare. The last time we saw coordinated weakness across multiple regions and products simultaneously was during the 2014-2016 period, when a combination of Russian import bans, a slowdown in Chinese demand, and the removal of European quotas created a global surplus that took nearly two years to work through. That episode saw U.S. Class III milk drop from over $24/cwt in 2014 to under $14 in 2016.

What eventually resolved that situation was a combination of weather-driven production disruptions (the 2016 New Zealand drought), gradual demand recovery in Asia, and ultimately, many smaller farms exiting the industry entirely. The recovery wasn’t quick, and the industry that emerged on the other side looked structurally different—more consolidated, more efficient, and arguably more vulnerable to the kind of dynamics we’re seeing today.

When the Safety Valves Stop Working

For as long as most of us have been in this industry, global dairy markets have operated with a kind of built-in equilibrium. When prices drop in one region, traders buy there and sell elsewhere, which lifts the cheap market and cools the expensive one. If a U.S. product is discounted, exports surge until domestic prices align with international benchmarks. It’s the arbitrage mechanism that keeps regional markets from getting too far out of whack.

What’s striking about mid-December is how that mechanism appears to have stopped functioning.

Looking at the data from European exchanges, German physical butter crashed by €425 in a single week—that’s a 9.3% drop—settling at €4,150. The weekly EU dairy quotations showed Dutch butter at €4,070, down €250. Yet French butter actually firmed €200 to €4,720. So you’ve got a €650 per tonne spread between French and Dutch butter, which shouldn’t persist in an integrated market.

At the same time, the Singapore Exchange was seeing pressure across its dairy complex despite solid trading volumes of 18,915 tonnes for the week. And back in the States, CME Cheddar blocks are sitting at $1.345 per pound—the lowest we’ve seen since summer 2023.

When these markets all move down together like this, it tells you the buyers are either already full or they’re waiting for even lower prices. That’s a fundamentally different dynamic than we’re used to seeing. What we’re watching is the global dairy complex running out of capacity to absorb current production levels at anything close to recent historical prices.

Why Production Keeps Growing Despite Terrible Prices

In a typical cycle, you’d expect falling prices to trigger pretty predictable responses. Farmers cull marginal cows, dial back feed inputs where it makes sense, and overall production gradually contracts. That supply reduction creates scarcity, and prices eventually recover. It’s the classic pattern the industry has relied on for generations.

That’s not what’s happening, and here’s why it matters.

The USDA’s December World Agricultural Supply and Demand Estimates held 2025 U.S. milk production steady at 115.70 million tonnes—still up 2.4% from 2024. They lowered the 2026 projection slightly, from 117.15 to 117.05 million tonnes, citing reduced dairy cow inventory offsetting per-cow production gains. But even with that downward revision, we’re still looking at 1.2% growth in 2026.

Think about that for a minute. Even with prices at distressed levels across multiple product categories, American milk production is forecast to keep expanding.

And if you want to understand why, take a look at what’s happening in feed markets. The December USDA grain outlook shows March 2026 corn futures trading around $4.405 per bushel, with projected ending stocks of 2.03 billion bushels. That’s the highest level in seven years and 32% greater than last season. The agency actually raised its corn export forecast to 3.2 billion bushels—that’s up 12% from last year’s record—yet domestic supplies remain massive. Soybean meal closed the week at $302 per ton, down $5.40.

What this creates is production that stays high because historically cheap feed costs insulate producers from the full pain of low milk checks. When you run the income-over-feed-cost calculations—and I know most of you do this weekly if not daily—many operations can still pencil out positive margins even with Class III in the mid-$15s. That math keeps marginal cows in the herd even when finished product prices are screaming oversupply.

I was looking at numbers from a 500-cow Wisconsin operation recently that illustrates this perfectly. With corn at $4.40, their feed costs are down 18% from last year. That keeps their IOFC positive at $16.50 milk, even though that’s $3 below what they budgeted for 2025. So the economic signal telling them to cut back gets overwhelmed by the reality that they’re still cash-flow positive on a monthly basis.

Period

Feed Cost

Other Costs

Milk Price

IOFC Margin

Q4 2023

$10.20

$7.50

$19.80

$9.60

Q1 2024

$9.80

$7.60

$18.50

$8.70

Q2 2024

$9.20

$7.70

$17.90

$8.70

Q3 2024

$8.90

$7.80

$17.20

$8.30

Q4 2024

$8.40

$7.90

$16.80

$8.40

Q1 2025

$7.80

$8.00

$16.20

$8.40

Q4 2025

$7.20

$8.10

$15.90

$8.70

Here’s something else worth noting: the USDA report mentions explicitly that winter weather isn’t the constraint it used to be, particularly in the Midwest. Modern housing systems mean operations in Wisconsin, Michigan, and Minnesota can maintain high production levels regardless of what’s happening outside. Better ventilation, more sophisticated environmental controls—which is great for consistency and animal welfare, but it also makes production less responsive to price signals.

The Export Picture Gets Complicated

Here’s where things get really interesting, and why the volume numbers deserve a closer look.

September numbers from the U.S. Dairy Export Council showed cheese exports up 34.5% year-over-year to 116.5 million pounds—the highest daily average shipments on record. Butter exports were 2.7 times larger than the previous year. Whey powder exports hit their highest level since March 2023, up 8.3%.

You’d think those export numbers would support domestic prices. When foreign buyers aggressively purchase U.S. products, that should create competition for available inventory. But that’s not what we’re seeing. Strong export volumes are coinciding with some of the weakest domestic prices in years.

What this tells you is that the industry is exporting what it has to produce to keep processing plants running at capacity. These modern cheese plants have massive fixed costs and debt service obligations. You can’t afford to run at 70% capacity—your cost per unit skyrockets. So you run full-throttle and discount product to move volume into export channels.

And here’s where the story gets more nuanced. While cheese exports are at record levels, nonfat dry milk exports collapsed 18.5% year over year in September, hitting an eight-month low. Even sales to Mexico—and Mexico has been one of our most reliable powder markets—dropped 17.3%. When you can’t move powder to Mexico, that tells you demand is genuinely soft across categories.

The cheese export story breaks down in interesting ways by region. Mexico remains the dominant market, which makes sense given proximity and trade relationships. But what’s notable is that Australia has become the third-largest destination for U.S. cheese. USDEC data shows Australia has already imported more U.S. cheese in 2025 than in any previous year on record, and we’ve still got three months of shipments to count.

This matters because it represents a shift in the Australian dairy sector. Chronic drought conditions and herd contraction have pushed Australia from being a dairy-surplus nation to one that’s increasingly dependent on imports. U.S. cheese is essentially backfilling the gap left by shrinking Australian milk production.

The challenge with this dynamic is sustainability. Mexico is buying finished U.S. cheese because, at current prices, it’s cheaper than importing powder and manufacturing cheese themselves. Australia is buying because they don’t have enough domestic milk. Neither situation represents organic demand growth driven by expanding consumption—they’re opportunistic purchases driven by price dislocations and supply shortfalls elsewhere.

When those conditions change—and at some point they will—it raises legitimate questions about where all that U.S. cheese production capacity is directed.

Europe’s Markets Fragment Under Pressure

The European physical spot markets during the week of December 10 showed how extreme stress can break down normally efficient trading systems, and it’s worth understanding these dynamics because they affect global price relationships.

The weekly EU dairy quotations showed the aggregate butter index down 5.8% to €4,313. But that overall number hides some significant regional variations. German butter crashed €425 per tonne in a single week—that 9.3% decline—settling at €4,150. Dutch butter, which tends to serve as a key pricing benchmark for export markets, fell €250 to €4,070. Yet French butter actually firmed €200 to €4,720.

So you’ve got a €650 per tonne spread between French and Dutch butter. That’s roughly a 16% price difference for essentially the same commodity in neighboring countries with no trade barriers. Under normal circumstances, traders would move product to capture that arbitrage opportunity, and the spread would compress.

The persistence of this spread likely reflects panic selling in the German and Dutch markets—processors liquidating inventory to generate cash flow—while France’s unique regulatory structure (particularly the Loi EGalim laws that protect farmer margins) and strong domestic preference for high-quality branded butter with protected designations create price support that can’t be easily arbitraged away.

Meanwhile, the European cheese complex is testing historical support levels. The EEX European Weekly Cheese Index shows Mild Cheddar trading at €3,248—just €4 above its five-year low. Cheddar Curd sits at €3,221, €27 above its five-year floor. Young Gouda has fallen to €2,961, down 34.3% year-over-year.

When you’ve got multiple cheese varieties simultaneously trading within pennies of multi-year lows during what should be a seasonally firm period—pre-holiday demand, typically lower winter milk production—it signals fundamental oversupply rather than temporary weakness. The market is grinding against production costs, and may already be below them for higher-cost operators.

The Strategic Pivot Creating Future Pressure

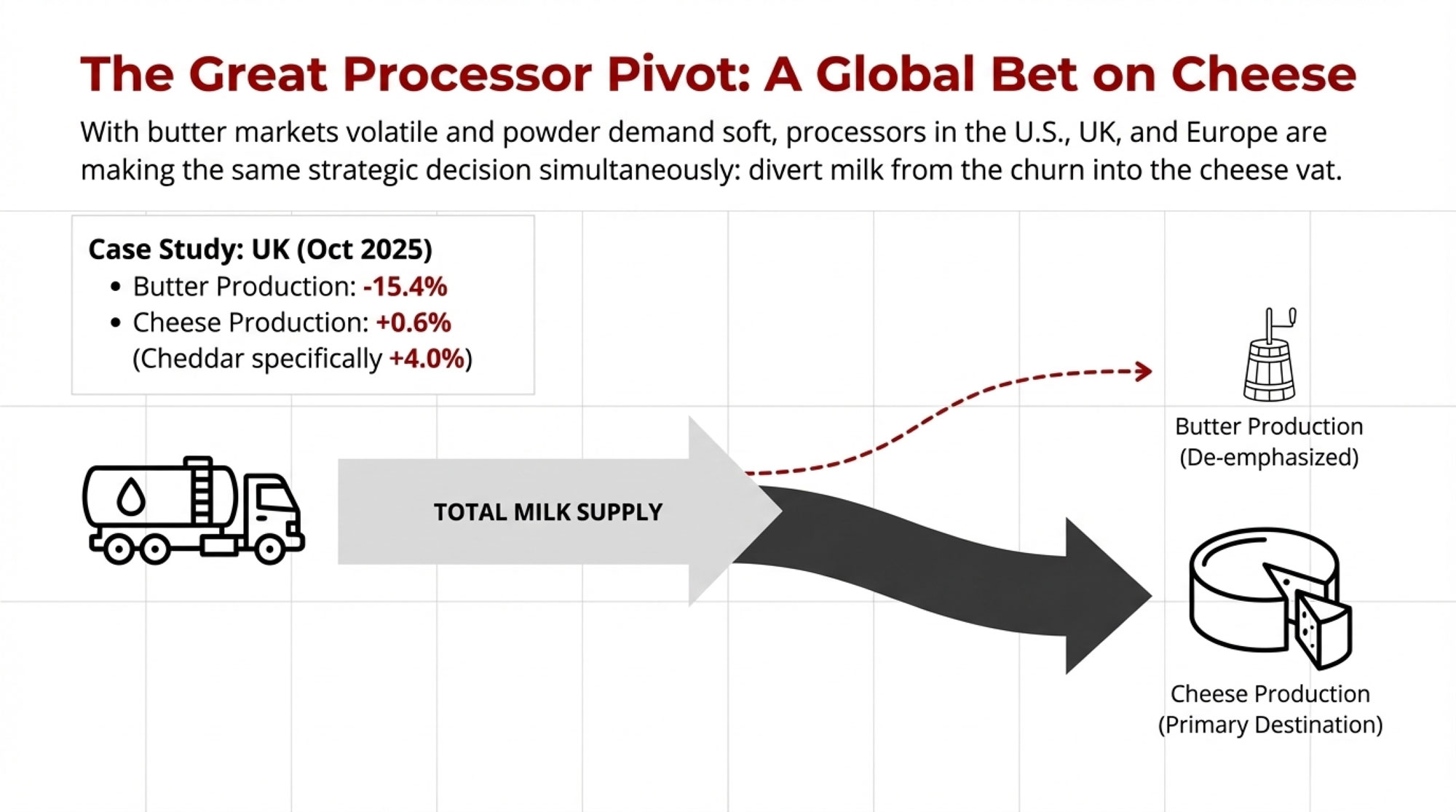

One pattern emerging from the data that has real implications for 2026 is a simultaneous shift by processors across multiple countries away from butter production and toward cheese.

UK production statistics from DEFRA for October 2025 tell the story: butter production down 15.4% year-over-year while cheese production increased 0.6%, with Cheddar specifically up 4.0%. You’re seeing similar dynamics in U.S. processing facilities—milk diverted from volatile butter markets into cheese vats.

The logic makes sense on paper. Butter is highly price-sensitive and difficult to store long-term without incurring significant cold-storage costs. Cheese, particularly aged varieties like Cheddar, can sit in inventory for 6 to 12 months as it matures. From a processor’s perspective, cheese acts as a kind of financial buffer—you can convert today’s surplus milk into a solid commodity and hope that by the time it’s ready for market, prices will have improved.

The complication is that when processors in the U.S., UK, and EU all make the same decision simultaneously, they shift oversupply in time and concentrate it into a single product category.

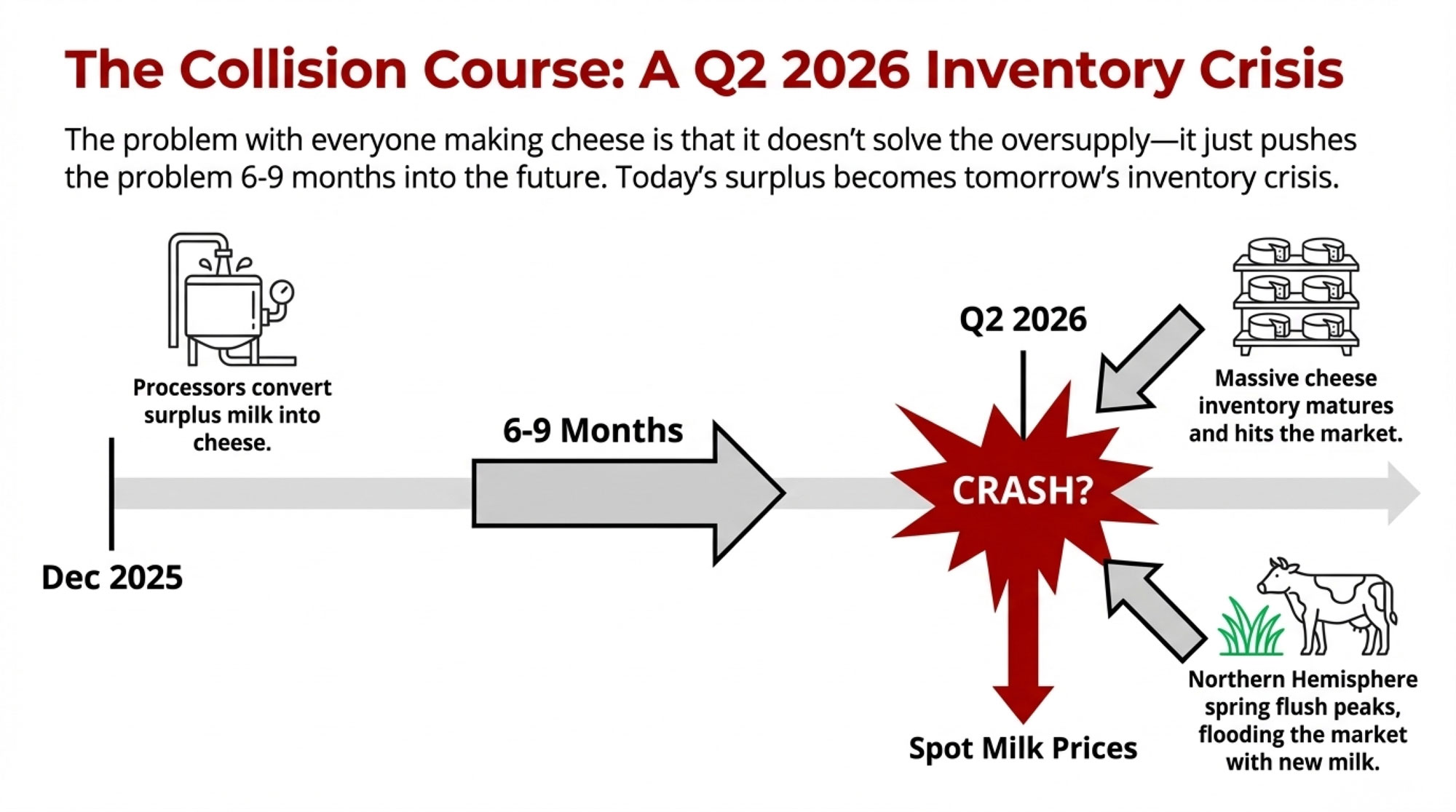

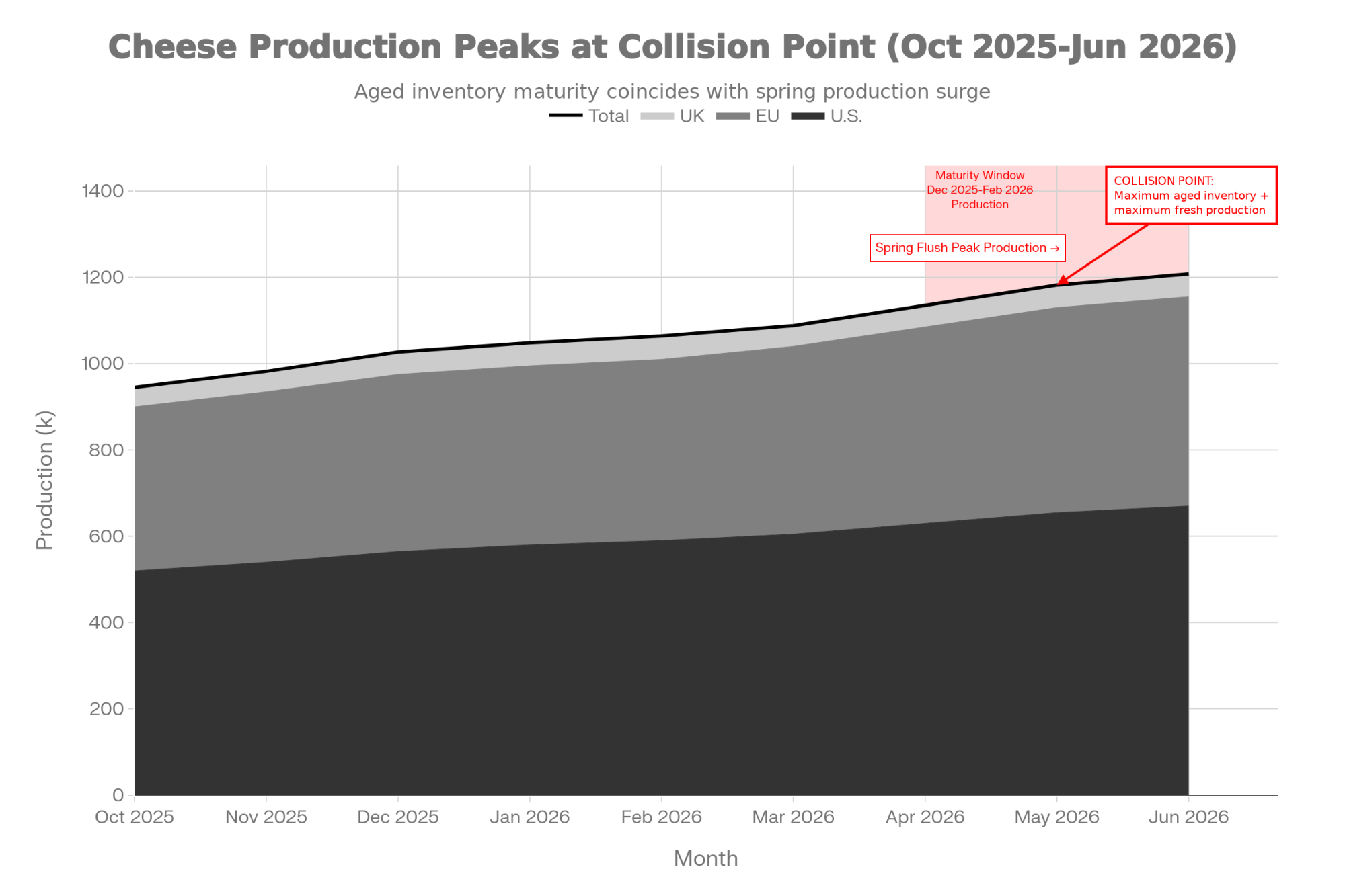

All that cheese being produced right now in December 2025 will mature and need to move to market in mid-2026—right around the time the Northern Hemisphere spring flush begins, bringing another seasonal surge in milk production. If export warehouses in key markets like Mexico and Australia are already well-stocked from late 2025’s record shipments, buyer demand could slow just as supply peaks.

Month

U.S. Cheese Production

EU Cheese Production

UK Cheese Production

Total Industry Production

Oct 2025

520

380

45

945

Nov 2025

540

395

47

982

Dec 2025

565

410

52

1,027

Jan 2026

580

415

53

1,048

Feb 2026

590

420

54

1,064

Mar 2026

605

435

48

1,088

Apr 2026

630

455

50

1,135

May 2026

655

475

52

1,182

Jun 2026

670

485

53

1,208

This creates what you might call borrowed demand—the cheese you’re making today to avoid the butter price collapse will need to clear the market in six months. If prices haven’t recovered by then, given the volume being produced across multiple regions, you’ve delayed the problem and possibly intensified it by concentrating everyone’s surplus into the same product at the same maturity window.

What Futures Markets Are Signaling

Despite the physical market’s weakness, there’s a notable divergence in how futures markets are pricing the outlook for different milk classes, and it’s worth understanding what that spread reveals about traders’ expectations.

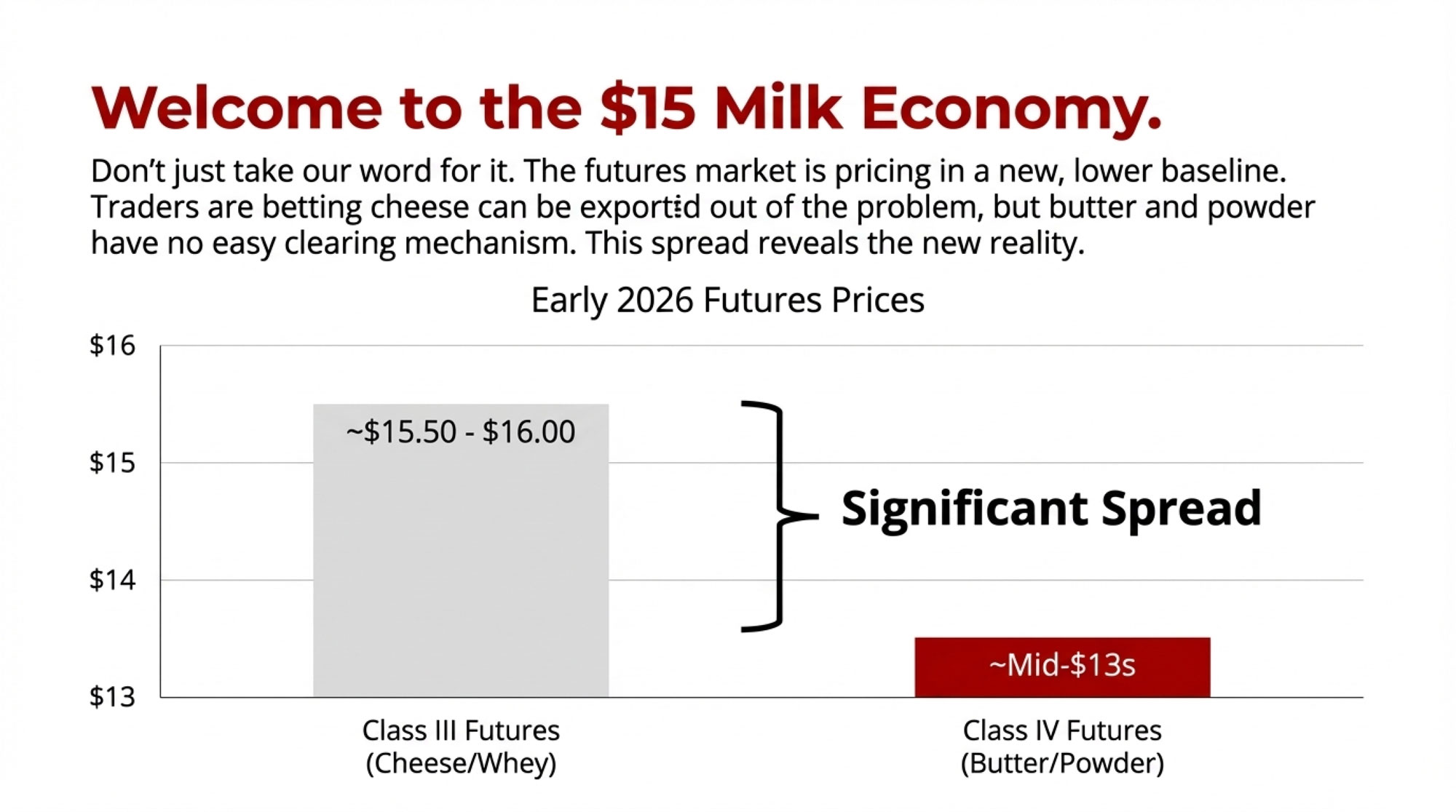

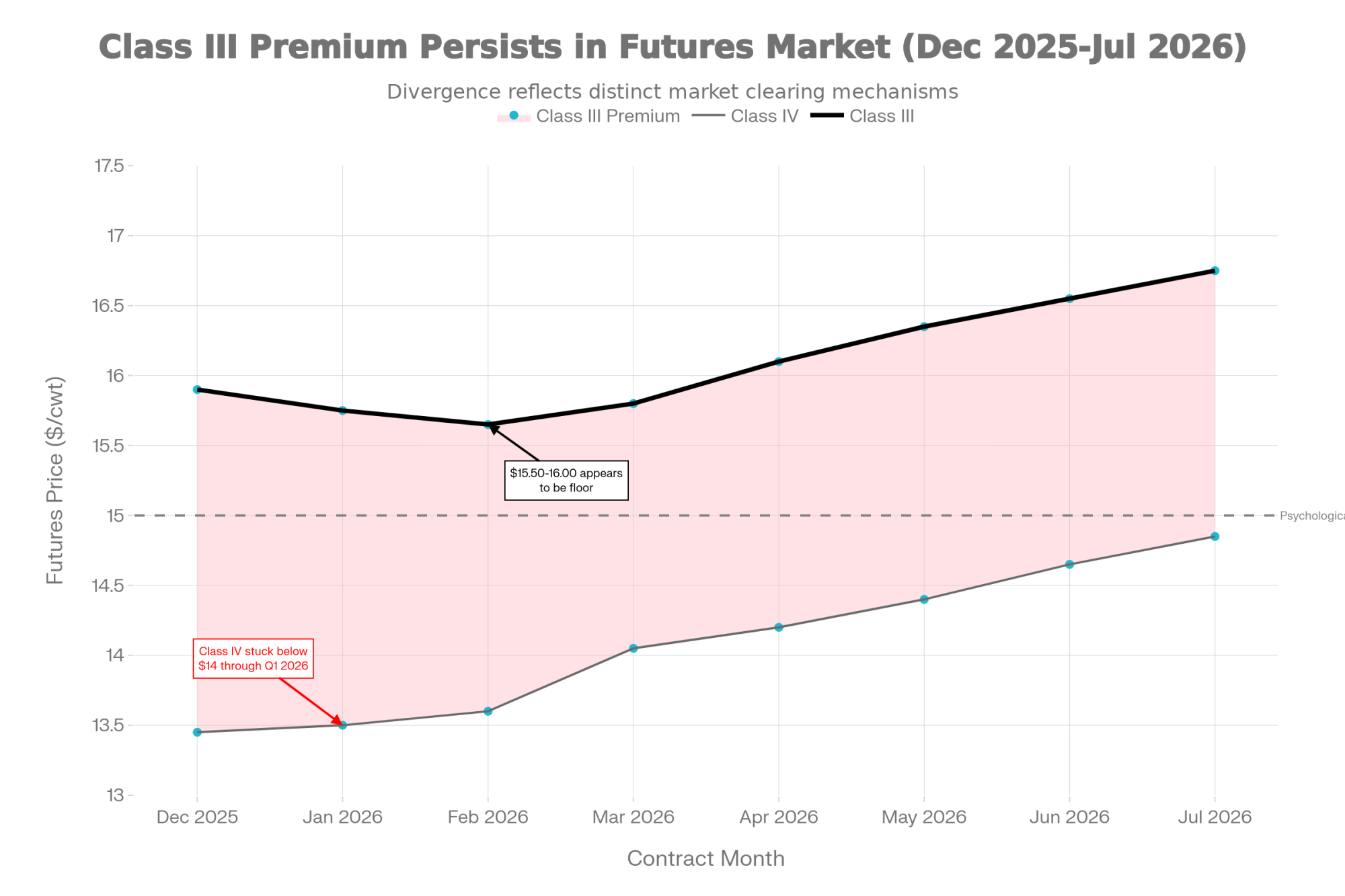

CME Class III futures for December 2025 fell 12 cents during the week to settle at $15.90 per hundredweight. But deferred 2026 contracts showed some resilience. The market seems to be betting that somewhere around the $15.50-16.00 range represents something close to a floor—that at these levels, demand will kick in enough and production will slow enough to stabilize things.

Class IV futures—driven by butter and nonfat dry milk prices—remain stuck in the mid-$13s through early 2026. The futures curve doesn’t show Class IV climbing above $14 until March at the earliest.

This spread reveals how traders are thinking about clearing mechanisms for different product categories. They’re betting that cheese can be cleared through aggressive export pricing, despite concerns about inventory. The record U.S. shipment volumes support that view. But they see no similar clearing mechanism for butter and powder, where domestic consumption is relatively fixed, and export competition from New Zealand and Europe remains intense.

Month

Class III Futures

Class IV Futures

Dec 2025

$15.90

$13.45

Jan 2026

$15.75

$13.50

Feb 2026

$15.65

$13.60

Mar 2026

$15.80

$14.05

Apr 2026

$16.10

$14.20

May 2026

$16.35

$14.40

Jun 2026

$16.55

$14.65

Jul 2026

$16.75

$14.85

Another factor supporting Class III that is often overlooked is the relative strength in the dry whey market. While butter and cheese prices are under serious pressure, whey is showing some resilience. The EU weekly quotation showed whey firming €15 to €989 per tonne, now up 12.6% year-over-year—making it the only major dairy commodity showing positive year-over-year performance in European markets. U.S. whey powder exports jumped 8.3% in September, with strong sales to China and Vietnam.

Because the Class III formula includes both cheese and whey components—specifically cheese price times 9.6 plus whey price times 5.9—the strength in whey provides a mathematical floor that Class IV doesn’t have. Even if cheese prices stay depressed, firm whey values help support the overall Class III calculation.

The question is whether futures traders are correctly assessing the inventory risk. If those strong cheese export numbers reflect stockpiling by buyers taking advantage of low prices rather than genuine ongoing consumption demand, then the apparent clearing mechanism could weaken in Q2 2026, just when the spring flush and all that aged cheese hit the market simultaneously.

The Feed Cost Variable Worth Watching

While most market signals point toward continued pressure through early 2026, there’s one variable that could shift the equation, and it’s worth keeping on your radar: what happens in grain markets.

The current dairy situation is enabled by historically low corn and soybean meal prices. As long as those input costs stay depressed, the income-over-feed-cost margins for many operations remain positive enough to justify maintaining production even with low milk prices.

But grain markets can turn quickly. The USDA is forecasting massive corn ending stocks, but those projections assume reasonably normal weather conditions. If drought develops in Brazil or Argentina during their growing season—December through March—grain prices could spike. The soybean complex, in particular, is trading with skepticism about Chinese demand. U.S. commitments to export soybeans through early November were running 40% lower than the prior year.

If China steps back into the market aggressively, or if South American weather turns problematic, soybean meal could rally from current levels near $300 per ton to $350 or higher fairly quickly. That kind of move would change the feed cost equation that’s currently supporting milk production despite low prices.

A grain rally might trigger a supply response driven by economics rather than operational necessity. If feed costs spike while milk prices stay low, you’d see the cull rate accelerate. That would tighten milk supplies before the spring flush, which might prevent some of the more challenging scenarios being discussed for Q2.

The complication, of course, is that this kind of adjustment through higher input costs isn’t exactly a rescue—it would address the oversupply by further pressuring margins. But it might be one of the few mechanisms left that can trigger a meaningful supply response.

Looking Ahead to Spring 2026

As we look toward the next few months, there are several scenarios worth considering, and I think it’s important to think through both the optimistic case and the more challenging possibilities.

The optimistic case would be that export demand continues absorbing U.S. cheese at roughly current volumes, European production contracts modestly as various forecasts suggest, New Zealand’s season ends normally, and the market finds a new equilibrium at these lower price levels without major disruption. Farmers who can operate profitably at Class III in the $15-16 range continue; those who can’t gradually exit through normal business cycles. It’s a slow grind, but it avoids a crisis.

The challenge with that scenario is that it assumes multiple things align favorably simultaneously, and it doesn’t fully account for the inventory dynamics building in the cheese complex.

A more complete assessment acknowledges that we’re heading into Q2 2026 with several risk factors converging. The spring flush will bring seasonal increases in production—that’s biology; you can’t avoid it. Cheese produced in late 2025 and early 2026 will be maturing and needing to move to market. And if export warehouses in key markets are already well-stocked from late 2025’s record shipments, buyer demand could slow as supply peaks.

In that scenario, cold storage space becomes a limiting factor. Processors would face pressure to either move product into lower-value channels—such as converting aged cheese into processed cheese ingredients—or implement supply management measures. Spot milk prices could come under significant pressure in some regions.

Whether these dynamics develop into a more serious situation depends on variables we can’t yet fully predict—export demand patterns, weather affecting production, and policy responses. But the risk is substantial enough that operations should plan for various scenarios rather than assume conditions will improve on their own.

What This Means for Your Operation

So, where does all this leave us? I think there are some practical considerations worth thinking through, and they vary depending on your role in the industry.

For Producers:

The evidence suggests we’ve moved beyond a typical cyclical downturn. Relying on historical price recovery patterns to guide current decision-making carries real risk.

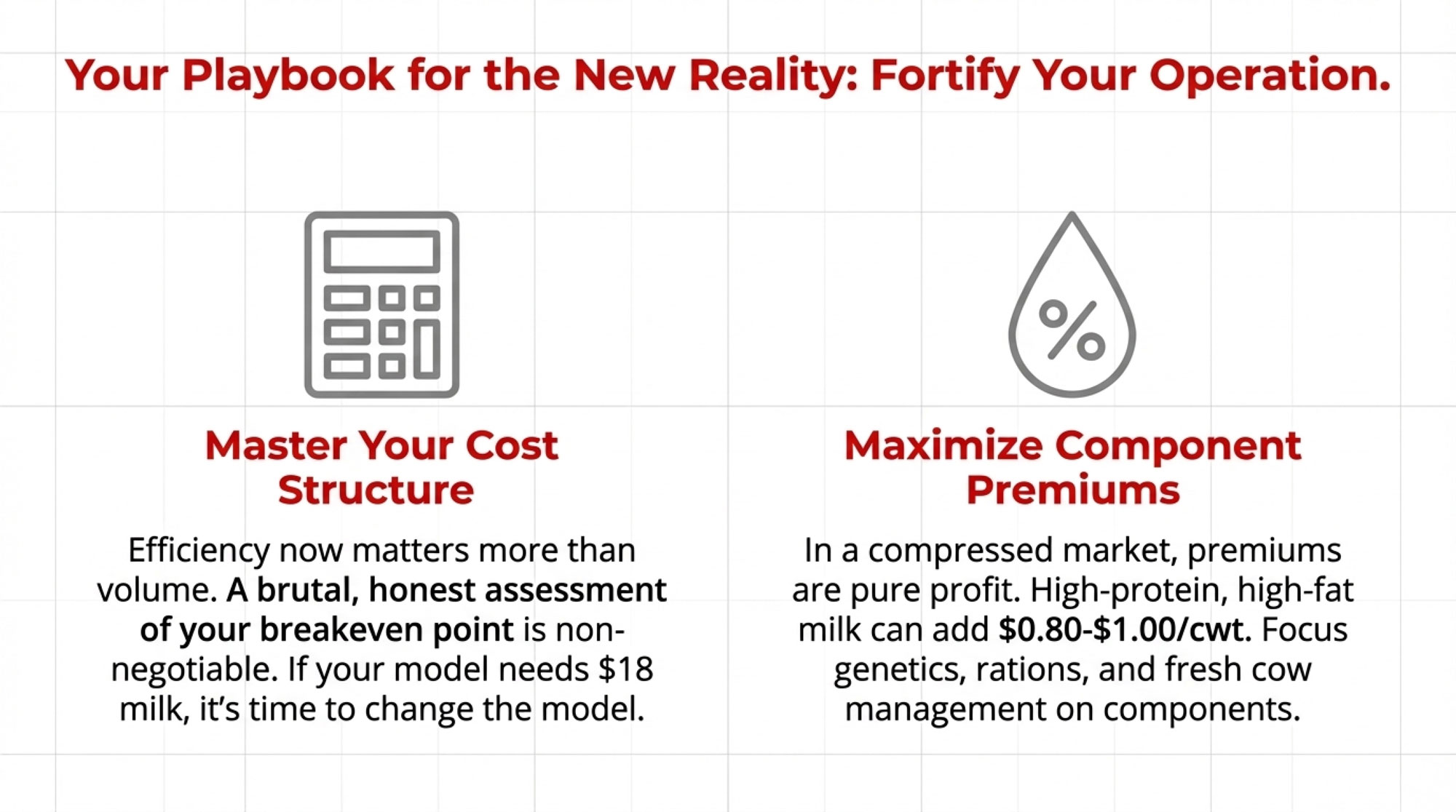

The most important focus right now is cost structure. In a market where establishing a lower baseline price, efficiency matters more than production volume. A realistic assessment of your operation’s true breakeven point is critical. If your business model requires $18-19 milk to be profitable, fundamental changes may be necessary because the market is signaling that $15-16 could be the range for extended periods.

Component quality is becoming increasingly important in compressed markets. When commodity prices are under pressure, the premiums for high-protein, high-fat milk become proportionally more valuable. Fresh cow management, ration formulation, and genetic selection decisions that maximize components—all of this can add meaningful value when the base price is low. I’ve seen operations in the Upper Midwest boost their component checks by 80 cents to a dollar per hundredweight through focused attention to butterfat and protein levels, and that differential matters more than ever in this environment.

Focus fresh cow management; optimize rations for fat/protein; select genetics for components

Add $0.80-1.20/cwt to milk check

High Priority

Balance Sheet Resilience

Build working capital reserves; defer non-critical capital projects; restructure high-interest debt

Survive 6-12 months low prices

Critical Action

Feed Cost Management

Forward contract 50-60% of corn/soy needs through summer 2026 at current lows ($4.40 corn)

Lock controllable cost advantage

High Priority

Risk Management Tools

Implement Dairy Revenue Protection or LGM; set minimum price floors for Q2-Q3 2026

Protect against worse-case scenarios

Recommended

Balance sheet resilience will be critical heading into 2026. Operations with stronger working capital and lower debt service obligations will be better positioned to navigate extended low prices. This may not be the optimal time for major expansion projects or capital spending that increases fixed costs. I know that’s difficult advice when you’ve got planned improvements or a son or daughter wanting to come back to the farm, but timing matters.

Feed cost management deserves attention. With corn and soybean meal at multi-year lows, locking in favorable input costs for at least a portion of needs provides one of the few controllable variables in the current environment. Even partial coverage—50-60% of expected needs—can provide meaningful protection if grain markets rally. Some Northeast operations I’m familiar with are forward contracting corn through summer 2026 to remove at least that uncertainty from their planning.

For Processors:

Inventory management has moved from routine practice to strategic necessity. The industry-wide shift toward cheese production requires realistic planning for when and where that inventory will clear. Frank conversations with customers about forward commitments and careful evaluation of speculative inventory positions are warranted, given uncertainty about the timing of price recovery.

Export channel diversification matters more in volatile markets. Heavy reliance on one or two markets—particularly those that may be engaging in stockpiling rather than steady consumption—creates vulnerability if buying patterns shift.

Processing flexibility offers strategic advantages. Assets that can shift between products as market conditions change provide more options than single-purpose facilities in volatile environments. I recognize that’s easier said than done when you’ve got specialized equipment and a trained workforce, but it’s worth considering in future capital planning.

For the Broader Industry:

The synchronized weakness across global markets raises questions about coordination and supply discipline. Without mechanisms to better align supply with realistic demand expectations, these boom-bust cycles may become more frequent and severe. This doesn’t necessarily mean government intervention, but it might involve processors implementing more structured base-excess programs or cooperatives taking stronger action to manage supply.

Export infrastructure and market development will become increasingly critical if the U.S. continues to position itself as a large-scale global supplier. This means sustained investment in logistics, market access, technical assistance to importing countries, and trade relationships that can reliably absorb substantial volumes.

Better market intelligence and information sharing could help prevent simultaneous strategic pivots that amplify imbalances. If processors in different regions had better visibility into global production decisions, they might make different product-mix choices. Industry associations and market data services have a role in providing that transparency.

The Bottom Line

The week of December 15, 2025, may mark a transition point—when global dairy markets shifted from familiar cyclical volatility into something more structural and challenging to navigate.

The traditional mechanisms that historically dampened these cycles are evolving. Smaller farms that used to exit during downturns and help tighten supply represent a declining share of production. Regional markets that operated somewhat independently are increasingly interconnected and moving together. Feed costs, which tend to move inversely with milk prices and provide a natural hedge, are currently low, removing that counterbalance.

What’s emerging is a more consolidated, more efficient production system that responds to price signals differently than in previous decades. Large operations with modern facilities and low per-unit costs can remain profitable at price levels that would have historically triggered widespread exits. That’s economically efficient in many ways, but it also means markets may need to fall further and stay low longer to trigger the supply response needed to rebalance.

For all of us navigating this transition, the fundamental challenge is to build operations and business models that remain viable at these new baseline prices rather than relying on assumptions of a return to historical averages. The traditional wisdom that low prices eventually cure low prices still holds. The cure is working—you can see it in the data. But the adjustment period may be longer than in previous cycles required.

These are sending clear signals about the current supply-demand balance. The question facing every operation is how to adapt business strategies and risk management approaches to this evolving reality while maintaining the flexibility to capitalize on opportunities as they develop.

Market data referenced in this analysis comes from the European Energy Exchange (EEX), Singapore Exchange (SGX), Global Dairy Trade platform, CME Group, USDA World Agricultural Supply and Demand Estimates (WASDE), U.S. Dairy Export Council (USDEC), UK Department for Environment, Food & Rural Affairs (DEFRA), and European Commission weekly dairy quotations for the period ending December 15, 2025.

Key Takeaways:

The Export Paradox: Record U.S. cheese exports (+34.5%) met 18-month price lows as every global dairy market crashed simultaneously the week of December 15—revealing fundamental pricing mechanisms have broken.

Why Supply Won’t Self-Correct: Cheap feed ($4.40 corn, $302 soy meal) keeps income-over-feed-cost positive at $15-16 milk, preventing the production cuts that normally cure oversupply.

Q2 2026 Inventory Collision: Processors globally are shifting from butter to cheese simultaneously. This inventory matures in spring 2026, precisely when the flush hits—creating a potential crisis for spot milk prices.

This Is a Reset, Not a Cycle: Class III holding near $16 while Class IV languishes in mid-$13s signals new baseline economics. Operations must be built for sustained viability at these levels, not temporary survival.

Immediate Producer Priorities: (1) Cost structure over production volume, (2) Maximize component premiums—they matter most in compressed markets, (3) Strengthen balance sheets before spring, (4) Lock feed costs now via forward contracting.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Are you leaving money on the table by ignoring real-time milk data? Let’s fix that.

EXECUTIVE SUMMARY: This year’s markets are forcing us to take the basics seriously. Here’s something that’ll grab your attention: just 10% better feed efficiency can add over $100 per cow annually to your bottom line. That’s real money we’re talking about, Milk yield improvements through genomic testing? You’re not just throwing darts anymore — you’re making calculated moves. Farms around the globe that’ve embraced these tools are actually squeezing out better margins despite rising feed costs. The Journal of Dairy Science and USDA data back this up. With milk prices fluctuating as they are, adapting isn’t optional anymore. To stay profitable, you need to get ahead in genetics and feed efficiency now. Don’t wait — farm profits sure won’t.

KEY TAKEAWAYS

Boost feed efficiency by 10% using precision feeding tech — that translates to $100+ extra per cow in 2025 margins. Get a feed analysis this week to spot where you’re losing money.

Leverage genomic testing to improve milk yield by up to 15% over traditional herds. Contact your breeding consultant tomorrow to discuss a tailored genetic plan.

Monitor your milk-to-feed ratio monthly — target 1.8 or above to protect margins when prices get volatile. Track this through your DHI reports starting now.

Stay ahead of export demand by adjusting production to seasonal swings. Review USDA export data quarterly so you’re not caught off guard.

Apply for those Dairy Business Innovation Alliance grants — up to $100K for efficiency projects that pay back in 1-2 years. Begin your application this month if you haven’t already started. The bottom line? Markets are rewarding the prepared and punishing those who wait. These aren’t just nice-to-have improvements anymore — they’re survival tools for 2025 and beyond.

The thing about today’s cheese market moves? They’ve shaken up what was shaping up to be a pretty steady run for Class III prices this summer. Cheese blocks? They dropped 10¢, slicing through the optimism like a wire through butterfat. Moments like this get your attention fast — especially when you’re counting every cent on the farm.

But butter? Butter’s steady, hanging in there even though the weekly numbers show some softness creeping in. What strikes me is how exports keep bolstering these prices — like a sturdy fence you can lean on when the wind howls. Lock in those profits when you can, especially on cheese, because these swings aren’t waiting around.

Let’s get real with the numbers farmers actually care about — none of that finance jargon that’ll put you to sleep.

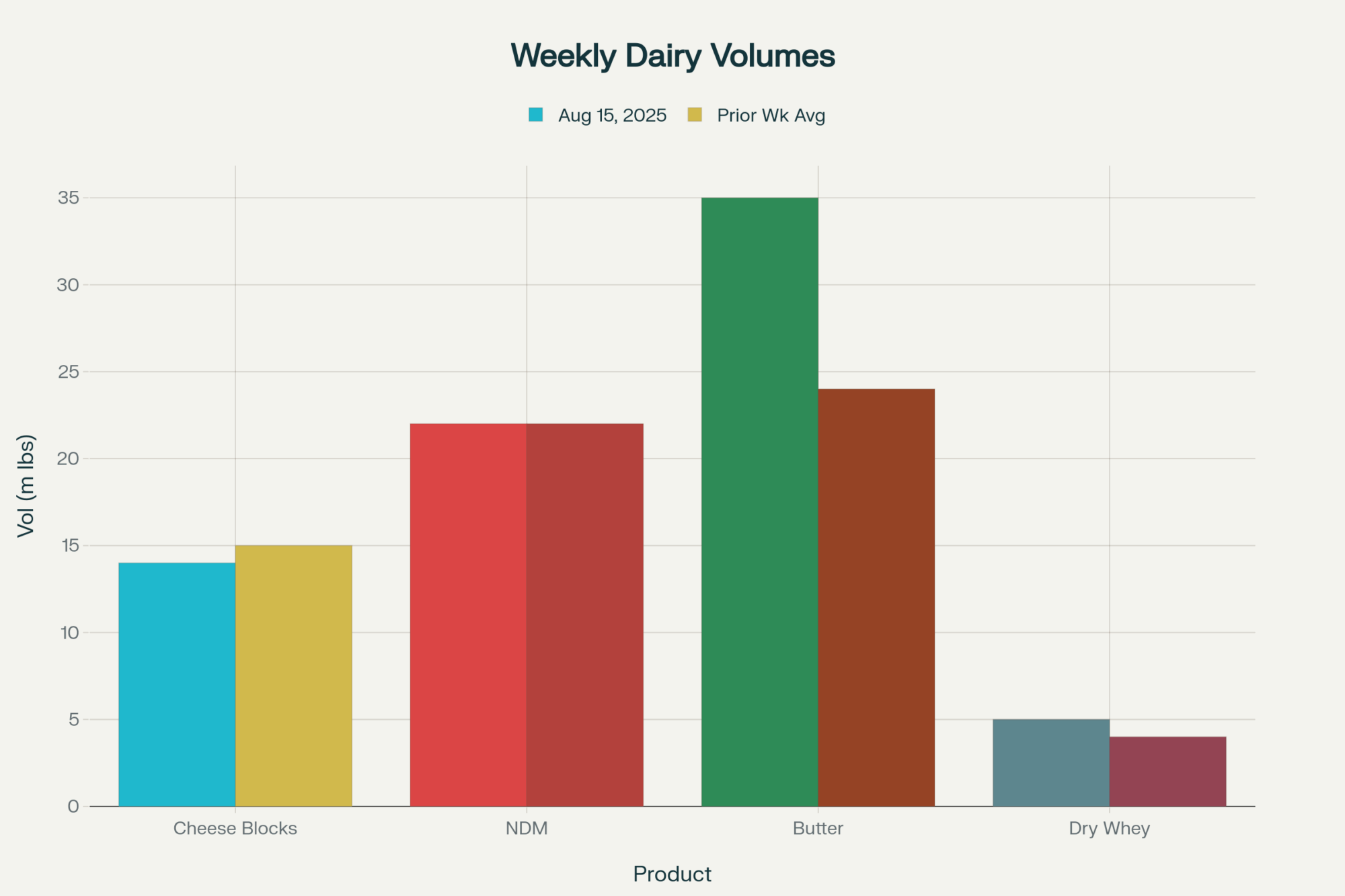

Weekly volume comparison for key CME dairy products, week ending August 15, 2025

Market Snapshot & What It Means to Your Farm

Product

Price

Change

Weekly Trend

Farm Impact

Cheese Blocks

$1.78/lb

-10¢

+2.1%

Today’s drop could reduce your milk checks by about 60¢/cwt, based on the latest Class III formula weightings.

Cheese Barrels

$1.83/lb

-4¢

+2.9%

A softer drop here, but just as much a signal of jitters.

Butter

$2.28/lb

Unchanged

-4.8%

Standing firm for now, though weekly softness rings alarms for Class IV pricing.

NDM Grade A

$1.26/lb

-0.5¢

-1.4%

Steady as the export bookings hold strong.

Dry Whey

$0.60/lb

-1¢

+5.6%

Minor pullback, but the weekly trend says it’s riding high.

Here’s what’s interesting: while cheese blocks saw a gain earlier this week, padding that weekly climb to 2.1%, today’s sharp 10-cent pullback feels like the market taking a breath — a sprint, then a pause, if you will. Real markets don’t operate in a straight line.

That late-day selling? Probably some profit-taking and hedging ahead of reports. Only a handful of loads changed hands, but that’s enough to send a signal.

Butter has been more active this week, a sign that exports are still fueling interest. Cheese? Traders are a little more hesitant.

30-Day Price Trends: Cheese and Butter

This shows the gradual rise with today’s bump downward — a sign the market’s keeping everyone on their toes.

How Are We Doing Globally?

No matter how tight things look here, it’s a global market. Our butter prices are about a dollar cheaper than those in Europe and New Zealand, and NDM prices are comparable. That helps us stay competitive on exports — the lifeblood of our market.

Product

U.S. Price

Europe Price

New Zealand Price

Butter

$2.28/lb

~$3.20/lb

~$3.29/lb

NDM

$1.26/lb

~$1.08/lb

~$1.26/lb

California farms face higher feed and energy costs — an extra 15 to 25 cents per cwt — because water’s expensive and drought has tightened availability. That’s pushing folks to double down on water-saving tech and efficiency tweaks.

This August’s heatwave is another story — the Southwest’s dealing with stressed cows and chipped feed quality, which is cutting milk production there somewhat. Meanwhile, the Upper Midwest has been fortunate with timely rain, which has improved forage and sustained production.

Exports: Where The Pressure and Opportunity Meet

Exports stay strong. USDA’s Foreign Agricultural Service shows cheese shipments up roughly 25% year-over-year through June. Mexico remains a solid top customer, while Southeast Asia and the Middle East emerge as new markets. But the EU and Australasia aren’t giving up any ground.

China’s ramping up selective butter imports even as their milk production slips — something to watch.

And USDA keeps the 2025 all-milk price pegged near $22 per cwt, with Class III and IV futures about $17.40 and $18.54. Locking prices ahead feels smart.

If you’re considering investments or diversification, consider grants like those offered by the Dairy Business Innovation Alliance. They’re offering up to $100,000 for efficiency and modernization projects.

Dairy-beef crosses and automation technologies — such as feeders and meters — are becoming increasingly vital for managing the fluctuations.

What It Means for You

Markets are swinging — today’s cheese price pullback is proof. If you can, lock in your prices to protect your margins.

Know your local reality: feed costs and weather conditions differ widely by region, so tailor your plan to your specific farm.

Keep an ear on global trade moves and currency shifts. That’s the tune your milk check dances to.

The bottom line? This industry rewards the prepared and punishes the complacent. Today’s moves are just another reminder that having a plan — and sticking to it — beats hoping prices will always go your way.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Cracking the Code: The Unseen Financial Power of A2 Milk in Your Herd – For a tactical edge, this piece reveals how to leverage genetic selection for A2 milk to unlock new revenue streams and increase herd value. It offers a practical guide to capitalizing on a high-demand consumer trend.

The Digital Cow: How Big Data is Revolutionizing Dairy Farming – Looking to the future, this article explores how innovative data analytics and AI are transforming herd management. It demonstrates how to turn farm data into predictive insights for boosting efficiency, health, and your overall bottom line.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

EXECUTIVE SUMMARY: The dairy industry’s obsession with feed cost management is dangerously misguided when Class III futures crater 28 cents while corn sits comfortably below $4.50/bushel. This comprehensive CME market analysis reveals how 25 block cheese trades with zero bids created a $1.27 weekly Class III collapse, pushing income-over-feed costs below $12/cwt despite historically favorable grain prices. The brutal math exposes a 20% margin compression driven entirely by milk price destruction, not input inflation—contradicting decades of conventional wisdom that positions feed cost hedging as the primary risk management tool. Global demand destruction is overriding domestic supply fundamentals, with Mexican buyers becoming “price-selective” on $2.47 billion in annual purchases while U.S. component-adjusted production surges 3.0% year-over-year. FMMO reforms effective June 1st are creating structural pricing advantages for butterfat producers, with Class IV projected to outperform Class III by $0.60/cwt in 2026. Progressive producers implementing Dairy Revenue Protection within 48 hours and optimizing for 4.50%+ butterfat levels will capture $0.75-$1.50/cwt premiums while competitors cling to outdated volume-focused strategies.

KEY TAKEAWAYS

Immediate DRP Implementation Delivers Crisis Protection: With Class III below $17.00/cwt and further weakness projected, establishing Dairy Revenue Protection floors within 48 hours protects against $1.25-$1.75/cwt additional losses through August 2025—far exceeding potential feed cost savings

Butterfat Optimization Captures Structural Premium: Target 4.50%+ butterfat levels to access $0.75-$1.50/cwt premiums as Class IV prices maintain $0.60/cwt advantage over Class III in 2026 projections, reversing traditional protein-focused strategies

Component-Focused Production Trumps Volume Strategy: U.S. milk shows 3.0% component-adjusted growth versus 1.6% volume growth, yet cheese prices collapse—proving market values manufacturing solids over raw gallons, demanding strategic breeding and nutrition shifts

Regional FMMO Advantages Create Geographic Arbitrage: June 1st reforms increased Northeast Class I differentials to $5.10/cwt while manufacturing regions face relative disadvantages—strategic location evaluation now delivers measurable pricing benefits

Trading Pattern Analysis Reveals Market Paralysis: 25 block trades with zero bids versus 6 barrel bids with zero offers signals bifurcated cheese market requiring sophisticated risk management beyond traditional spot price monitoring

Class III milk futures plunged $0.28/cwt as cheese blocks collapsed 5.50¢ and barrels fell 4.25¢, extending a brutal week that’s pushing farm margins below break-even levels. With July Class III now at $16.98/cwt and income-over-feed costs projected to slip below $12/cwt through August, immediate risk management action is critical.

Today’s Price Action & Farm Impact

Product

Closing Price

Daily Change

Weekly Trend

Direct Impact on Farmers

Cheese Blocks

$1.5950/lb

-5.50¢

-10.0¢ (-5.8%)

Severe Class III pressure continues

Cheese Barrels

$1.6150/lb

-4.25¢

-11.2¢ (-6.5%)

Amplifies protein value destruction

Class III (JUL)

$16.98/cwt

-$0.28

-$1.27 (-7.0%)

Milk checks under severe pressure

Class IV (JUL)

$18.83/cwt

-$0.22

-$0.44 (-2.3%)

Butterfat premium maintaining

Butter

$2.5350/lb

+1.00¢

+0.56¢ (+0.2%)

Modest support for Class IV

NDM Grade A

$1.2500/lb

-1.00¢

-1.88¢ (-1.5%)

Export demand softening

Dry Whey

$0.5725/lb

+0.25¢

+1.81¢ (+3.3%)

Protein markets holding better

Market Commentary: Today’s cheese rout extends what’s becoming a devastating June for Class III valuations. Block cheese has now shed over 15¢ in two weeks, with domestic buyers reportedly “gone dark” as they await further price declines. The 25 trades in blocks today show active selling pressure, while the complete absence of bids signals market participants are stepping aside until this correction finds a floor.

Enhanced Trading Activity Analysis

Detailed Market Depth Snapshot (June 24, 2025):

Product

Trades

Bids

Offers

Bid-Ask Environment

Market Sentiment

Cheese Blocks

25

0

2

Sellers Only – No buying interest

Panic selling

Cheese Barrels

5

6

0

Buyers Only – No selling interest

Distressed demand

Butter

0

2

2

Balanced but inactive

Cautious neutrality

NDM Grade A

1

0

1

Minimal activity

Disinterest

Dry Whey

2

3

2

Modest interest both sides

Stable engagement

Critical Market Signal: The stark contrast between blocks (25 trades, 0 bids) and barrels (5 trades, 6 bids, 0 offers) reveals a bifurcated cheese market. Block cheese is experiencing liquidation selling with no buying interest, while barrel cheese shows distressed demand with buyers present but no willing sellers. This unusual pattern suggests different end-user dynamics and potential processing disruptions affecting specific cheese formats.

The Brutal Math: Despite corn trading well below $4.50 and soybean meal under $300/ton, income-over-feed costs are projected to crash below $12/cwt from March through August 2025. This represents a devastating 20% margin compression for most operations, driven entirely by collapsing milk prices rather than input cost inflation.

Production & Supply Insights

Production Surge Continues: U.S. milk production reached 19.9 billion pounds in May 2025, up 1.6% year-over-year, marking the second consecutive month of significant gains. The U.S. dairy herd expanded to 9.45 million head, the highest since August 2021.

Component Quality Rising: Fat content reached 4.31% (up 1.7% year-over-year) while protein climbed to 3.34% (up 1.2% year-over-year). Farmers are producing the highest-quality milk in years, yet the market is punishing them with lower prices – a clear signal that demand destruction is overpowering supply-side quality improvements.

Market Fundamentals Driving Prices

Domestic Demand Crisis: Retail cheese buyers have “gone dark,” holding off purchases while waiting for further declines. Domestic cheese consumption dropped 56 million pounds in Q1 2025, while weak restaurant traffic continues dampening foodservice demand.