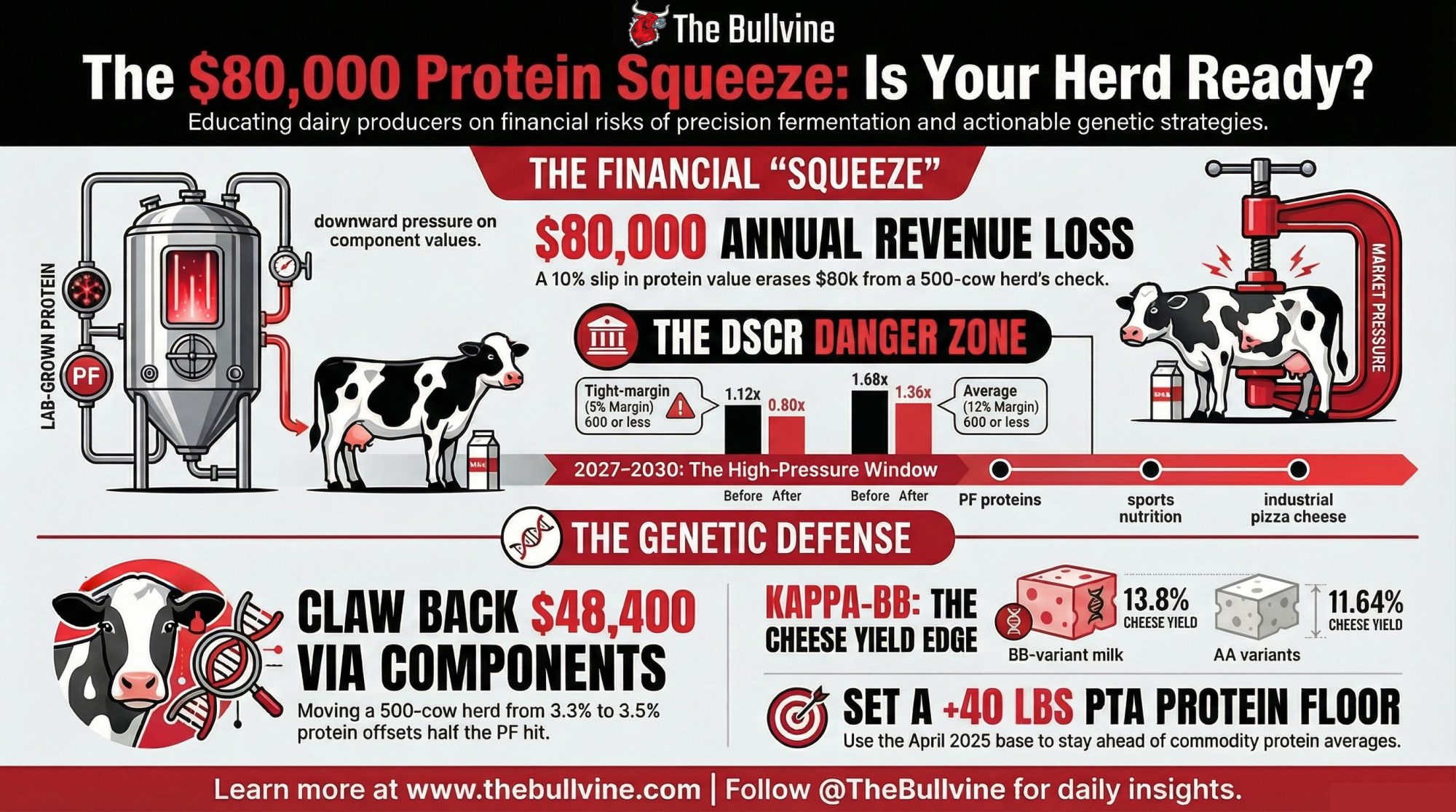

A 10% slip in protein value erases about $80,000 from a 500‑cow herd’s milk check. The real story is what that does to your DSCR when the lender runs the numbers.

Executive Summary: A 10% hit to protein value wipes roughly $80,000 a year off a 500‑cow Holstein herd’s milk check, and for many operations, that’s the difference between a 1.3x and 0.8x DSCR. Leprino’s deal for precision‑fermented casein and Verley’s FDA “no questions” letter for PF whey don’t kill conventional milk, but they give your buyers a second tap for the same proteins you ship. The article walks through barn‑level math on a 500‑cow herd at 25,000 lbs/cow, 3.3% protein, and February 2026’s $1.9373/lb protein price so you can see exactly how a PF‑style squeeze lands on your own cwt. It then shows why organic is a weak PF hedge if your all‑in costs sit in the $35–$49/cwt range against $31/cwt pay, and why your better move is breeding for +40 PTA Protein, kappa‑BB, and A2/A2. You’ll see how those genetics can claw back more than half of the modeled PF hit, and which milk markets (WPI, pizza cheese, fluid, export) are likely to feel PF pressure first. If your DSCR is under about 1.25x or you don’t know where your protein actually ends up, this is one of those pieces you read with your last three milk checks and a pen in hand.

Precision‑fermented dairy proteins just moved from conference slides into your barn math. Leprino’s global non‑animal casein deal and Verley’s FDA “no questions” letter for whey open a second supply lane for the same proteins you’re shipping today — and on a 500‑cow Holstein herd, a realistic precision‑fermentation scenario points to roughly an $80,000 annual squeeze on protein revenue if component values slip about 10%.

That’s not a prediction. It’s a stress test. The question is whether you run it on your own numbers now or wait until your lender or processor does it for you.

What Leprino and Verley Just Told You About Protein

On July 15, 2024, Leprino Foods and Dutch startup Fooditive announced an exclusive global agreement to commercialize non‑animal casein made via precision fermentation. Leprino secured exclusive rights for cheese applications and non‑exclusive rights for other food uses, with president Mike Durkin saying they’d be “incorporating precision fermentation alongside our conventional dairy production” to see how this casein adds to their product portfolio.

That word — “alongside” — matters. Leprino still needs your milk. It’s buying optionality: the ability to source functionally similar casein from a fermenter when the economics, customers, or regulators make that attractive.

On the whey side, French startup Verley became the first company to receive an FDA “no questions” GRAS letter for functionalized whey proteins produced via precision fermentation in October 2025. The letter covers FermWhey Native, a whey protein composed of about 95% beta‑lactoglobulin, and FermWhey MicroStab, designed for thermal and pH stability in high‑protein shots, RTDs, and functional yogurts. CEO Stephane Mac Millan called the ruling “a springboard for growth in the US market and beyond” and made it clear they’re focused on B2B formulations where density, stability, and taste win the sale.

Money is lining up behind them. In the last year, Verley has raised around $38 million; Vivici about $38.4 million; Those Vegan Cowboys about $14.5 million through crowdfunding; and All G Foods around $6.6 million plus a joint venture with Savencia’s Armor Protéines. Fonterra has backed a 4‑million‑litre fermentation plant in the UAE alongside Vivici, The EVERY Company, and the Abu Dhabi Investment Office. Bel Group and Standing Ovation reported in October 2025 that they’d produced all three major caseins from cheese whey at an industrial scale using precision fermentation, with functionality described as comparable to bovine casein.

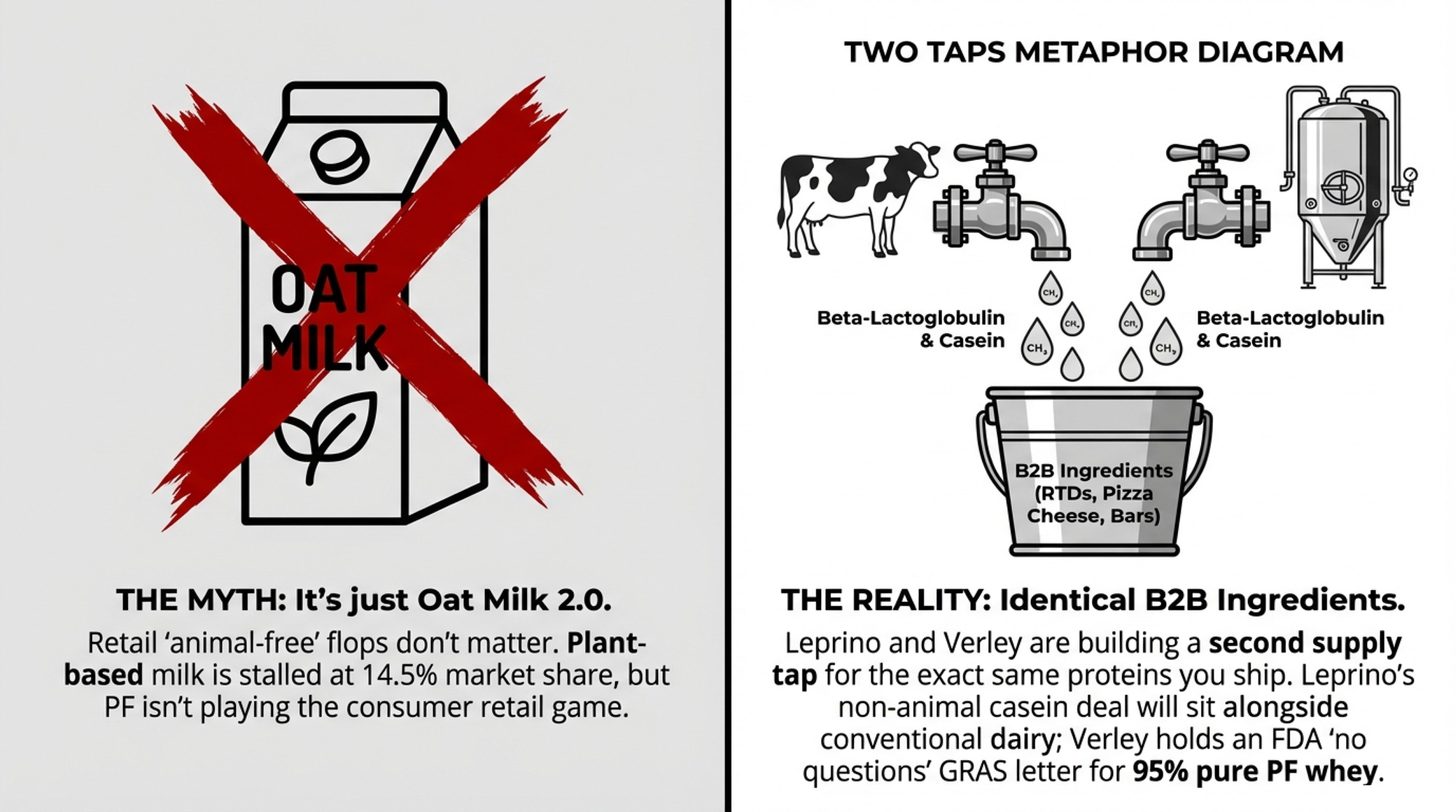

These aren’t oat‑milk startups shouting from the sidelines. They’re some of the same players already connected to your milk check, quietly building a second tap for the proteins that used to come only from cows.

Why Precision Fermentation Isn’t Just “Oat Milk 2.0”

It’s tempting to point to the plant‑based stall and call it a day. Plant‑based beverages hold about 14.5% of the U.S. fluid category after two decades, and 2024 retail sales slipped roughly 4–5%. A 2025 review said Nestlé’s Cowabunga “never hit the mainstream” and noted Straus Family Creamery had cooled on further “animal‑free” dairy launches.

Precision fermentation is playing a different game. It doesn’t try to fake dairy with oats or peas. It uses microbes to make dairy proteins — same amino‑acid sequence — in stainless steel. Verley’s FermWhey Native is 95% beta‑lactoglobulin with a clean amino‑acid profile, and FermWhey MicroStab is engineered for stability in low‑pH, high‑heat systems where conventional whey can struggle.

Bel and Standing Ovation ferment cheese whey into recombinant caseins that match bovine caseins in amino‑acid sequence and functionality. Scientists will remind you that identical sequences don’t guarantee identical post‑translational modifications, so there may be subtle differences in complex matrices and in nutrition. And right now, precision‑fermented products are individual ingredients (BLG, specific caseins, lactoferrin), not full milk with immunoglobulins and minor fractions.

For a glass of 2% at the kitchen table, that matters. For a protein bar, GLP‑1 nutrition drink, or pizza‑cheese shred that cares mainly about density, solubility, melt, or stretch? A tank full of BLG or casein that behaves like the real thing is close enough that your milk starts competing on price, logistics, and contract terms — not chemical uniqueness.

Retail “Animal‑Free” Flops Won’t Save Your Protein Check

A lot of conference chatter stops at “animal‑free dairy failed in retail, so it’s over.” The ingredient side tells a different story.

Several branded “animal‑free” launches struggled to gain traction in mainstream grocery channels, and some pulled back on consumer packs. That’s good for your fluid shelf space. But FoodNavigator‑USA’s 2025 story on Verley is blunt: their target is B2B — protein shots, RTDs, high‑protein yogurts, and medical‑nutrition formats.

Those decisions never hit the dairy case. A protein‑bar co‑packer or contract bottler cares about three things:

- Does the protein behave in this formula?

- Can we get it on time?

- Does it beat our current cost per functional unit?

If the answers are “yes” and the label can still say “whey protein from fermentation,” they’re not losing sleep over which factory made the BLG.

At the same time, demand for high‑protein foods keeps climbing. A February 2026 investment feature cites data showing U.S. foods making “high‑protein” claims growing at more than 7% annually — faster than the overall food market. Co‑ops and processors are pouring money into ultrafiltered milk and whey capacity to keep up; Michigan Milk Producers Association’s $122.6 million expansion at Ovid is a good example. Even with that, some processors report that whey demand and certain protein specs are outpacing what their existing milk sheds can supply at current margins.

That’s the exact gap precision‑fermented proteins are built to fill. Not to replace dairy everywhere. To slide into high‑growth, high‑spec segments where:

- Your region can’t expand milk and processing fast enough, or

- Ingredient buyers want a second tap so they’re not locked into one supplier for functionality or price.

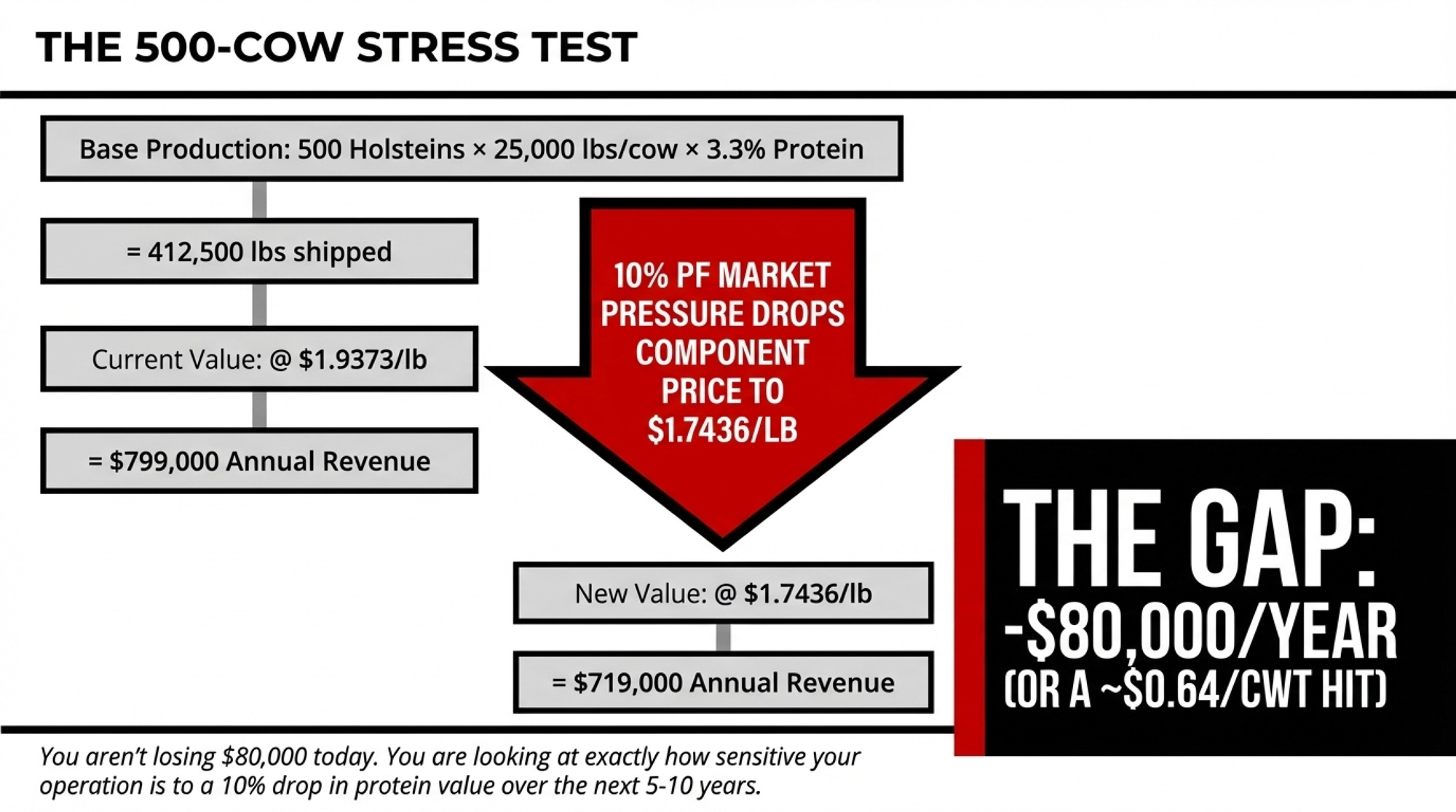

What Does a 10% Precision‑Fermentation Hit Mean for a 500‑Cow Herd?

Let’s get this off the panel slides and onto a yellow pad. You can swap in your numbers later.

Take a realistic Holstein herd:

- 500 cows

- 25,000 lbs shipped per cow per year

- Total milk shipped: 500 × 25,000 = 12,500,000 lbs

- Protein test at 3.3% ⇒ 12,500,000 × 0.033 = 412,500 lbs of protein

- February 2026 U.S. Class III protein component price: $1.9373/lb

At that price, your protein line looks like this:

412,500 lbs × $1.9373/lb ≈ = $799,000 in annual protein value. pa

Now run a scenario — not a forecast. Assume precision‑fermented proteins capture around 10% of B2B whey and casein demand in certain high‑protein categories, and that puts about 10% downward pressure on the protein component value you see in Class III.

- Current price: $1.9373/lb

- “10% pressure” price: $1.9373 × 0.90 ≈ $1.7436/lb

- New protein revenue: 412,500 lbs × $1.7436 ≈ $719,000

Gap: about $80,000 per year, or roughly $0.64/cwt on this herd.

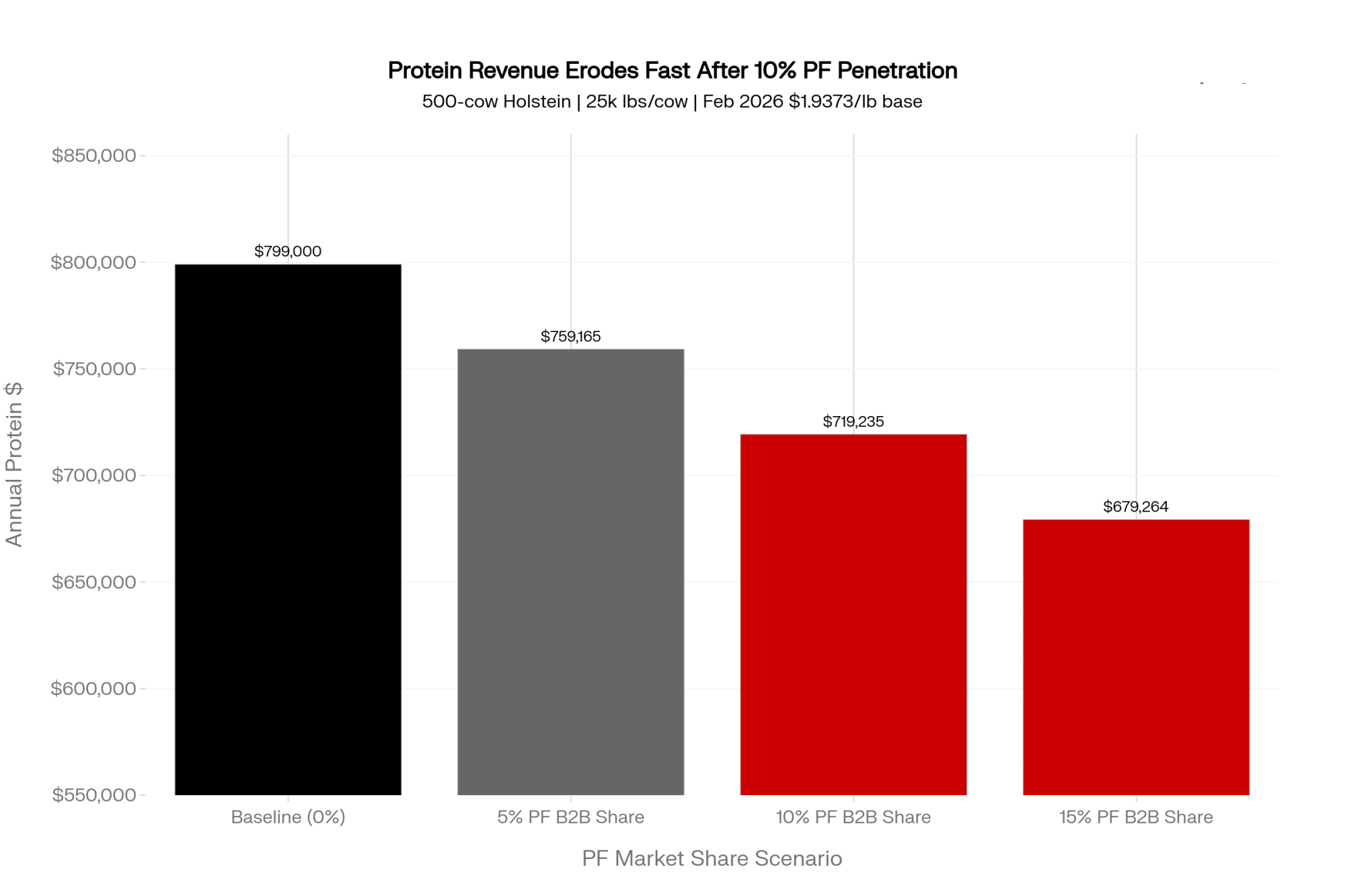

Here’s the same math at a glance across scenarios (rounded for readability):

| PF B2B share (scenario) | Protein price (rough) | Annual protein hit (500 cows) | Approx. per‑cwt impact |

| 5% | $1.94 → ~$1.84/lb | ~$40,000 | ~$0.32/cwt |

| 10% | $1.94 → ~$1.74/lb | ~$80,000 | ~$0.64/cwt |

| 15% | $1.94 → ~$1.65/lb | ~$120,000 | ~$0.96/cwt |

Two guardrails so you keep this in perspective:

- FMMO protein values come from surveyed cheddar and dry whey prices, not Verley’s or Fooditive’s internal contracts. Any PF effect gets filtered through cheese plants, exporters, and traders first, which makes the timing and magnitude of your milk check messy and delayed.

- Industry reviews still put precision‑fermented protein costs several times higher per kg than those of conventional whey or casein. PF doesn’t beat dairy on cost today. But every new fermenter project is backed by investors who bet that the gap will close over time.

So you’re not “losing $80,000 already.” You are seeing how sensitive your operation is to a 10% drop in your protein price over the next 5–10 years.

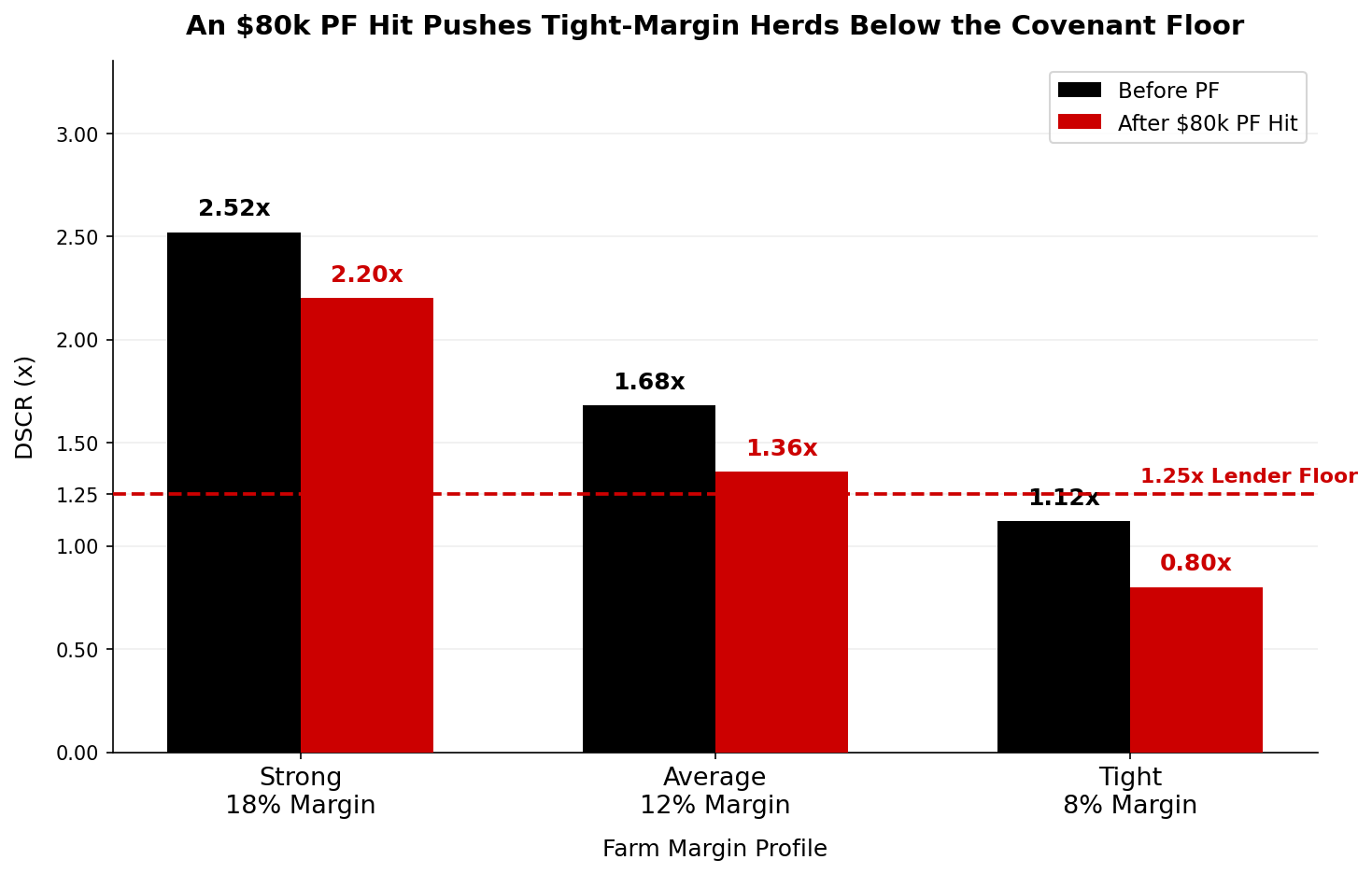

Where a $0.64/cwt Squeeze Hits First: Debt Service

For most herds, the first place a PF‑style squeeze really bites isn’t the milk check. It’s your DSCR and how your lender talks to you.

Farm Credit Canada defines a debt service coverage ratio (DSCR) below 1.0 as an inability to rely on net cash income to service debt; most commercial ag lenders in North America require at least 1.25x.[fcc-fac:1] That means $1.25 of cash for every $1 of principal and interest due.

Stick with our 500‑cow scenario and assume:

- Gross revenue ≈ $3.5 million

- Annual principal + interest = $250,000

Take three margin profiles before any PF pressure:

- Strong: 18% net margin before debt service

- Average: 12%

- Tight: 8%

Here’s how the $80,000 PF‑style hit lands on each:

| Profile | Net before debt (on $3.5M) | DSCR before PF | DSCR after ~$80k hit | What that means |

| Strong 18% | $630,000 | 2.52x | 2.20x | It’s a drag, not a crisis |

| Average 12% | $420,000 | 1.68x | 1.36x | More than half your cushion disappears |

| Tight 8% | $280,000 | 1.12x | 0.80x | Already under 1.25x — and you lose recovery room |

That bottom row is the one to stare at. A tight‑margin 500‑cow herd at 1.12x DSCR is already below a typical 1.25x covenant before any PF effect.[fcc-fac:1] Precision fermentation doesn’t “cause” that covenant problem. It just erases the little headroom you had to climb back above it.

For the average 12% herd, the same $80,000 squeeze takes DSCR from 1.68x to 1.36x. Nobody hits the panic button at 1.36x, but your banker’s questions change. Capex is scrutinized harder. Genetics spending gets framed in terms of payback. “What happens if components soften?” stops being hypothetical small talk.

If your DSCR sits well over 2.0x, PF is mostly a planning exercise. If you’re hovering between 1.0x and 1.4x already, you’re exactly the herd this scenario is about — whether PF shows up in your local market in three years or seven.

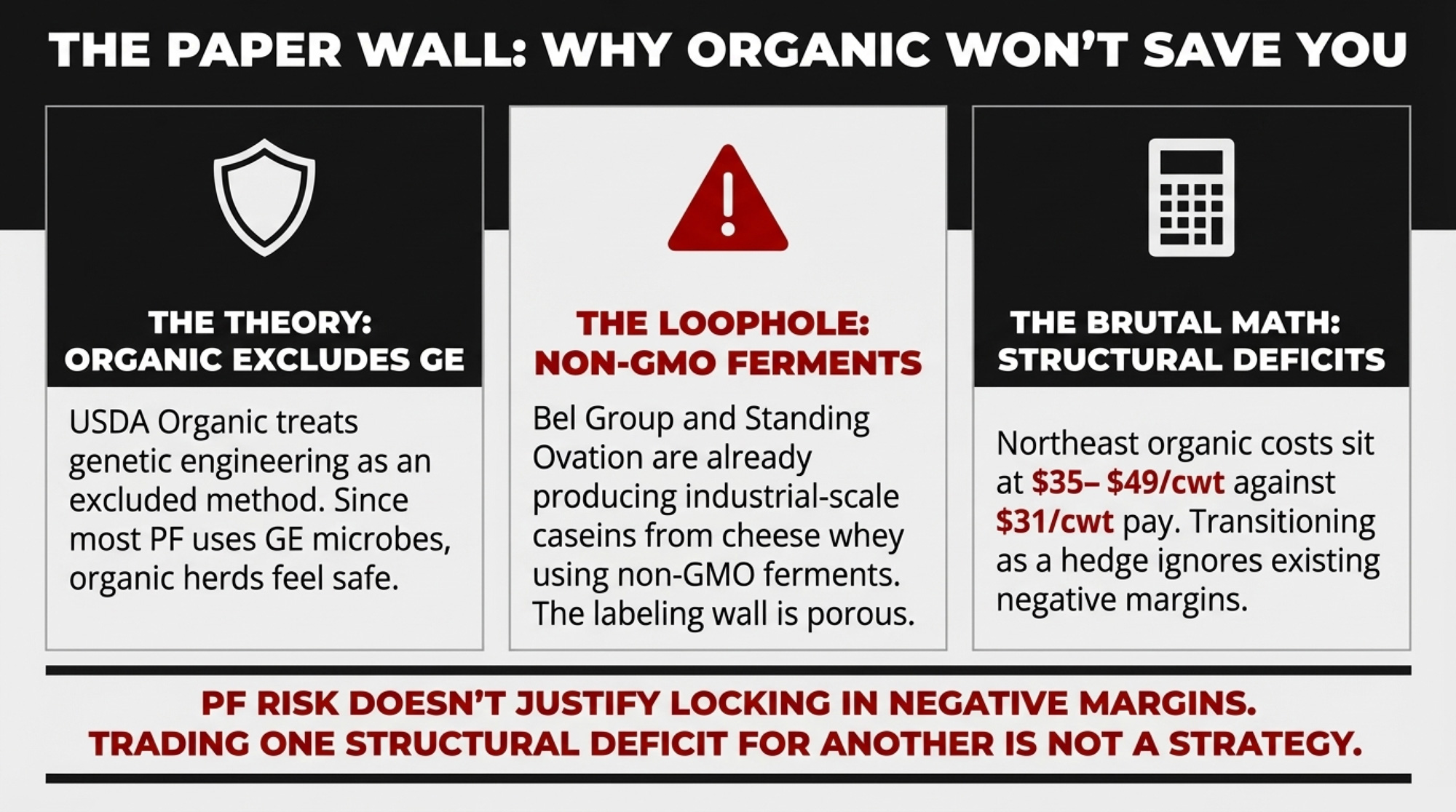

Organic’s Wall Is Real on Paper — and Tough on Math

One common comfort line is: “Precision‑fermented ingredients can’t be organic, so organic herds are safe.” There’s some truth there, but the story is more complicated — and the math is ugly for many herds.

USDA Organic rules treat genetic engineering as an excluded method.[ams.usda.gov:2] Most PF companies — Verley, Perfect Day, Vivici, others — use genetically engineered microbes, so their proteins can’t appear in certified‑organic products under current rules.[ams.usda.gov:2] That’s a real labeling wall.

Bel and Standing Ovation are testing the edges. Their October 2025 announcement described producing caseins from cheese whey using non‑GMO ferments at an industrial scale. If regulators treat that as a process change to an existing dairy by‑product rather than an excluded method, it may face a different organic classification path than GE‑microbe routes. That’s still an open question — not settled law.

Meanwhile, many organic herds are already struggling to make the math work. In 2022, NODPA executive director Ed Maltby told DairyReporter: “At this time, there is no economic reason for dairies to transition to organic production.” Their 2023 Northeast organic survey showed production costs in the $35–49/cwt range, while pay prices were around $31/cwt, with about two‑thirds of grass‑fed producers facing costs above their milk price.

So yes, the organic seal blocks most GE‑based PF proteins today. But:

- A non‑GMO PF casein route is already at industrial scale in at least one project.

- Many organic herds are already losing money at today’s pay prices.

If your cost of production is near or above your organic pay price, transitioning as a “PF hedge” is trading one structural problem for another. The only sound reason to go organic is the old one: because your cost structure and signed contracts give you a reliable margin, not because you hope a label will shield you from PF in 2033.

The Genetics Turn: Making Your Protein Less Generic

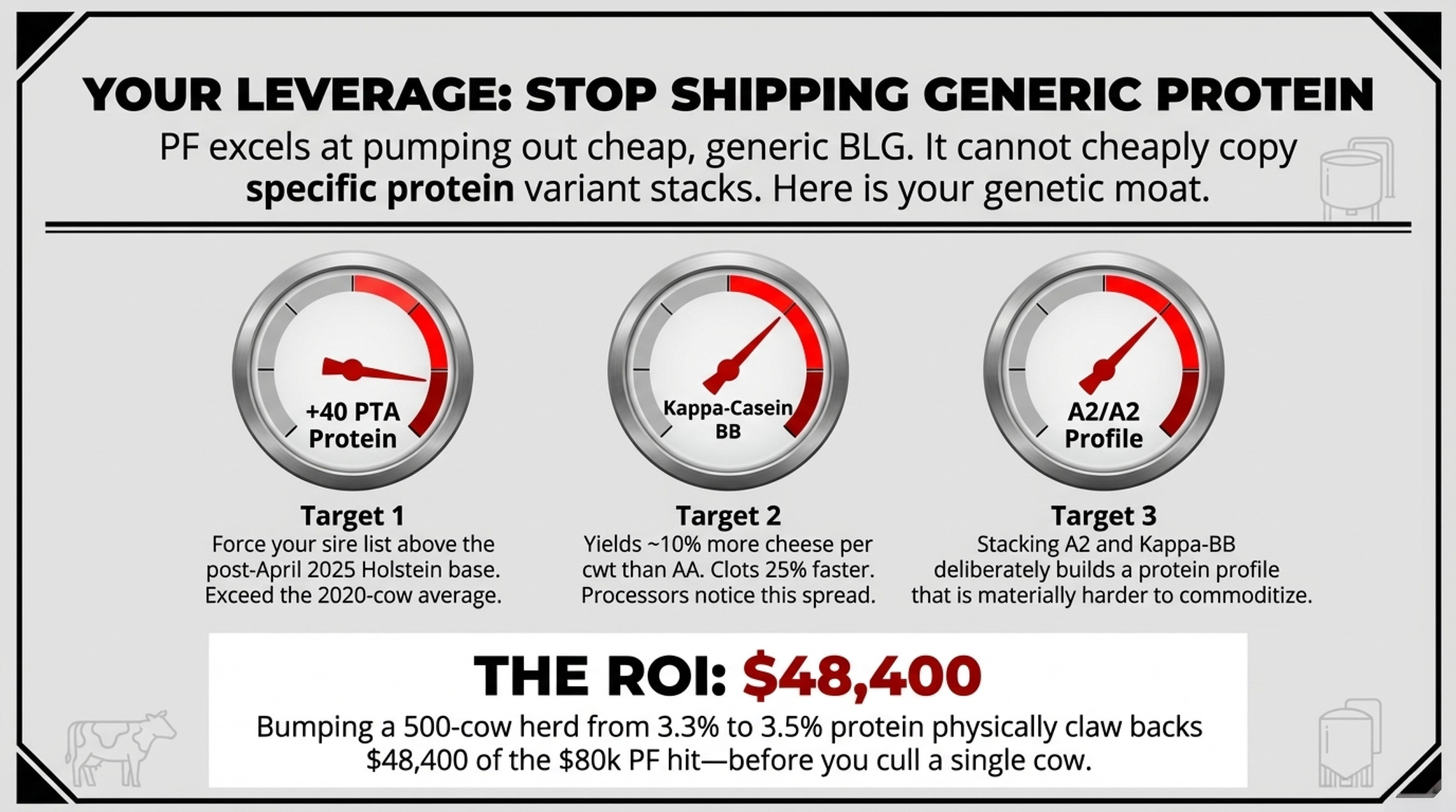

Here’s the part of the PF story where you actually have leverage. Precision fermentation is great at pumping out standard proteins: typical BLG, typical casein. It’s not built to cheaply copy whatever stack of protein variants you decide to breed for.

Kappa‑casein is the obvious starting point. Work under Wales’s Farming Connect program found kappa‑casein BB milk producing about 13.8% cheese yield versus 11.64% for AA — roughly a 2.2‑percentage‑point edge. Bullvine modeling on that and similar studies puts BB milk at around 10% more cheese per cwt, with BB milk clotting about 25% faster and producing cheese nearly twice as firm as AA‑heavy tanks.

| Genetic Trait | Baseline Herd Average | Target (PF Defense) | Processor Value | PF Resistance Logic |

|---|---|---|---|---|

| PTA Protein (lbs) | +10 to +20 lbs | +40 lbs minimum | More lbs shipped/cwt | More volume per cow, harder to cut |

| Kappa-Casein | ~60% AA, ~35% AB | BB or AB target | ~10% more cheese/cwt | BB milk clots 25% faster; 13.8% vs 11.64% cheese yield |

| A2/A2 Status | ~30–40% of Holsteins | A2/A2 priority | Premium fluid & export | Differentiated label; not replaceable by generic BLG |

| Protein % (herd avg) | 3.3% | 3.5%+ target | Higher component pay | 25,000 extra lbs protein/yr = ~$48,400 offset |

| Inbreeding (F%) | 8–10% | <8% with genomic tools | Health, fertility, yield | High inbreeding cancels genetic protein gains |

Processors — especially ones who also make cheese — notice that kind of spread. As PF pushes down the cost of generic protein, the premium on variant‑specific milk (A2/A2, kappa‑BB, higher protein % per pound of milk) becomes one of the few solid ways to say: “You can’t just swap me out one‑for‑one with a tank of BLG.”

Genetically, we’ve been blunt: treat +40 lbs PTA Protein on the post‑April‑2025 Holstein base as your minimum sire threshold in a PF world. It’s not magic. It’s simply forcing your sire list above the new average on protein transmission.

The April 2025 CDCB base change moved the Holstein reference from 2015‑born cows to 2020‑born cows. Bullvine’s analysis of the final base‑change values showed realized genetic progress over that window of about 29 lbs of protein, 44 lbs of fat, and 752 lbs of milk. Once inbreeding adjustments were applied, the average PTA fat rollback landed closer to 39 lbs than the headline 44 lbs.

So a +40 PTA Protein bull on the new base isn’t just a little better than zero. He’s materially ahead of the 2020‑cow average. You’re stacking advantage on top of a breed that already moved.

Now run that through barn math on our 500‑cow herd. If you move from 3.3% to 3.5% protein over time at 25,000 lbs shipped per cow:

- Old protein shipped: 12.5 million lbs × 3.3% = 412,500 lbs

- New protein shipped: 12.5 million lbs × 3.5% = 437,500 lbs

- Gain: 25,000 lbs of protein per year

At $1.9373/lb, that extra 25,000 lbs is worth about $48,400 annually. You’ve just clawed back more than half of the $80,000 PF‑scenario squeeze through genetics alone, before you change a contract or cull a single cow.

Combine a +40 PTAP filter with kappa‑casein genotyping and A2/A2 selection, and you’re deliberately building a protein profile that’s harder to commoditize. Most commercial herds still haven’t screened kappa at scale. The ones that start now will be the ones who can sit across from a processor and talk about cheese yield and functionality, not just volume.

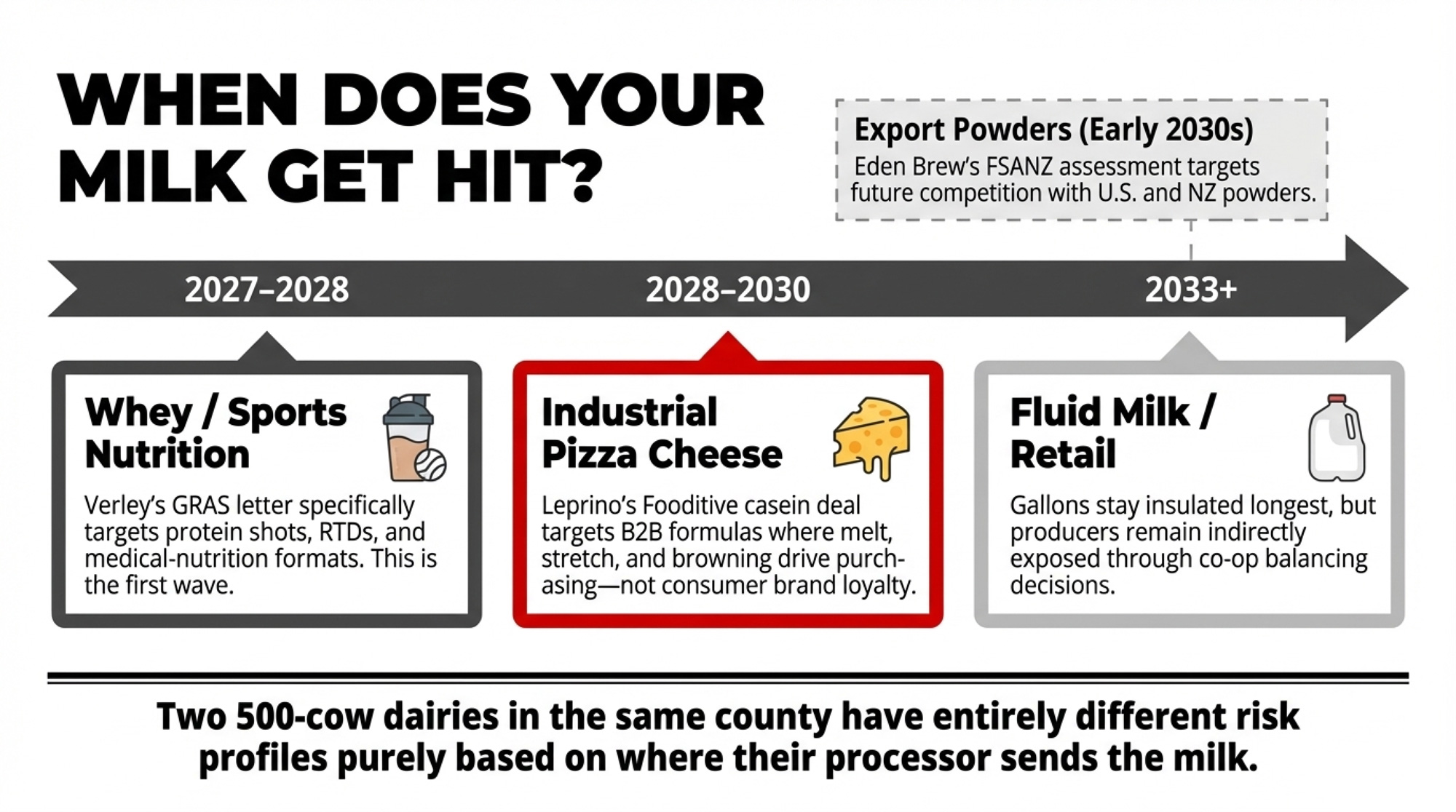

Your Milk’s Destination Sets Your Precision‑Fermentation Timeline

Two 500‑cow dairies in the same county can have very different PF exposure without changing a thing in the barn — purely because their processors send milk to different end markets.

Based on current announcements, regulatory filings, and public timelines, the PF pressure bands look roughly like this:

- Whey protein isolate/sports nutrition (2027–2028). Verley’s GRAS letter explicitly positions FermWhey Native and MicroStab for protein shots, RTDs, high‑protein yogurts, and medical‑nutrition formats. If your processor sells into those categories, that’s where PF appears first as an alternative ingredient in specs.

- Industrial mozzarella and pizza cheese (2028–2030). Leprino’s Fooditive partnership is all about casein functionality, especially for pizza cheese, where melt, stretch, and browning drive purchases. As fermenter capacity scales, it becomes easier to blend PF casein into frozen pizza and QSR formulas.

- Fluid milk / regional retail (2033+). Fluid gallons stay insulated longer. Consumers still care about “real milk,” distribution remains local, and PF today is an ingredient business, not a branded gallon business. If most of your check comes from Class I, your PF clock is slower — but you’re still exposed indirectly through cream, concentrates, and your co‑op’s balancing decisions.

- Export powders to Asia/Oceania (regulation‑dependent). Eden Brew’s PF dairy protein application was accepted for FSANZ assessment in December 2025, with public consultation expected in 2026 and a review period of around a year. If FSANZ and other regulators approve these proteins, PF caseins and whey start competing more directly with U.S. and NZ powders in some export channels in the early 2030s.

None of that is guaranteed. Plants slip. Regulators delay. Customers change course. But your processor already has a working view of which segments would feel PF competition first and where they’d like more bargaining power. You only see that view if you ask.

What This Means for Your Operation

This stops being an interesting article and becomes useful when you plug in your own numbers and contracts. Here’s where to start.

- Stress‑test your DSCR this month. Grab your most recent full‑year financials. Calculate DSCR as net operating income ÷ total annual principal + interest. Then subtract a PF‑style hit from protein revenue — use roughly $0.64/cwt on your actual hundredweights shipped as a 10% scenario — and recalc.[fcc-fac:1] If you’re under about 1.25x now, you’re already in the vulnerability band this piece describes.

- Ask your processor where your milk really goes before April 30. Don’t stop at “cheese” or “fluid.” Ask for approximate percentages of fluid, commodity cheese, whey protein, and powders. Ask which customers are asking about “whey from fermentation” or “alternative casein,” and what PF developments they’re watching. If your field rep can’t answer, that tells you something about your information gap — and maybe about how seriously your buyer is planning.

- Audit your protein genetics. Pull your last 2–3 years of sire lists and herd‑level genetic reports. How many bulls have you used, clear +40 lbs PTA Protein, on the post‑April‑2025 Holstein base? How many cows and heifers are A2/A2 or kappa‑BB? If you don’t know, you can’t credibly argue that your protein is worth more than a commodity.

- Genotype before your next semen order. Before you book 2026 semen, genotype a meaningful slice — ideally your whole young‑stock and cow herd — for kappa‑casein and A2 status. Use that data to: prioritize A2/A2 and kappa‑BB matings for replacements; push beef‑on‑dairy hardest on cows with weak protein variants or low PTAP; and avoid wasting sexed semen on cows that’ll never give you the protein profile your processor wants.

- Do a hard organic math check, not a hope check. If you’ve been eyeing organic as a PF wall, sit down with your accountant and nutritionist. Map your all‑in cost of production — including unpaid labor and realistic depreciation — against actual organic pay prices you can sign in your region. If your breakeven is already near or above those pay prices, the rational move is to walk away. PF risk doesn’t justify locking in negative margins.

- If exit is on your mind, let PF shape timing, not your story. If you’re over 55, have no committed successor, and your DSCR has been sliding, precision fermentation isn’t “forcing” you out. It’s one more reason to time a strategic exit while buyers still see your herd as protein production capacity, not distressed culls. The gap between a planned sale and a forced liquidation can easily reach six figures on a 500‑cow herd.

- Block off one focused hour in the next 30 days. Grab this article, your last three milk checks, your year‑end financials, and your genetic reports. Work through the 500‑cow scenario with your actual cwt, tests, and debt service. If what you see on your own pad makes you uncomfortable, that’s your cue to change something while it’s still your choice.

Key Takeaways

- If your DSCR sits below roughly 1.25x at today’s margins, you’re already in the danger band this precision‑fermentation scenario exposes — whether fermenters show up in your market in 2028 or 2034.[fcc-fac:1]

- Precision fermentation is a 5–10‑year ingredient‑side pressure first, not a retail collapse next quarter. It shows up earliest in sports‑nutrition WPI, RTDs, and pizza‑cheese contracts, not in the gallon of fluid your neighbors buy.

- Your most practical defense isn’t arguing about PF in the press. It’s breeding for higher PTA Protein, kappa‑BB, and A2/A2, so your milk’s protein profile is harder to swap out for generic BLG coming from a tank.

- The organic seal blocks most GE‑based PF proteins on paper, but Bel’s non‑GMO casein route and the brutal organic cost structure mean “going organic to block PF” is a weak economic play unless your cost‑of‑production math already works with signed contracts.

The Bottom Line

Processors like Leprino, Bel, Fonterra, and their partners aren’t abandoning your milk. They’re adding precision‑fermented casein and whey alongside it to increase their sourcing options and leverage. Your job is to understand how that optionality affects your component price, your contracts, and your genetics plan — and to move on your own terms before a price sheet or covenant redraws the line for you.

When you look at your own herd, the real question isn’t whether PF is good or bad “for dairy.” It’s sharper: if protein gets cheaper in the markets your milk serves, are you set up as a commodity supplier fighting over pennies — or as a differentiated protein source your processor really doesn’t want to replace with what’s growing in a fermenter across town?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Protect your equity from 2026’s brutal $250,000 margin gap with the specific breakeven math and stress tests found in this survival playbook. It delivers immediate management tactics to take control before market shifts decide for you.

- The December Genetic Reckoning: Former Champions Fall, New Kings Rise – and Your 2026 Strategy Just Changed – Insulate your milk check against volatility by identifying the “component kings” of the massive 2025 genetic reset. This strategy reveals why diversifying your sire portfolio is now a non-negotiable risk management tool for long-term resilience.

- Your Cheese Plant’s New Bacteria Can Run 56% Faster – Why This Technology Decides Which Processors (and Farms) Survive 2030 – Capture a competitive advantage by understanding how gene-edited bacterial cultures are slashing processing times by 56%. This disruptive look at “programmable fermentation” exposes the future of supply chain survival through the 2030 automation era.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.