Your October milk check just got $91 million lighter thanks to Washington’s latest “reform.” Here’s what smart farmers are doing about it.

Quick Market Snapshot (2-minute read)

Today’s Reality Check: Post-Labor Day weakness pressured dairy markets. Butter fell a sharp 3.25¢ to $2.0125, and cheese blocks dropped 1¢ to $1.7650.

Your Milk Check: Cooperatives report varied impacts—Wisconsin producers are seeing 15-25¢/cwt declines, while others with better hedging face smaller hits.

Key Levels: Watch butter at $2.00 and cheese blocks at $1.75—breaks below these on heavy volume signal more pain ahead.

Action Items: Consider Class III puts around $17.90; lock 25-50% winter feed; focus rations on protein over butterfat.

EXECUTIVE SUMMARY: Look, I’ve been tracking dairy markets for years, and what happened after Labor Day isn’t your typical seasonal dip. The FMMO “reforms” just shifted $91 million annually from your milk check straight into processor pockets—and December’s component changes will hit even harder. Here’s the kicker, though… while everyone’s focused on butter dropping 3.25¢ and cheese falling a penny, feed costs are sitting at the most favorable levels we’ve seen in months. Your milk-to-feed ratio’s still healthy at 3.8, but that window won’t stay open forever. Smart operators in Texas are riding 10.6% production gains thanks to new processing capacity and mild weather, while California struggles with H5N1 costs. The global picture? We’re selling butter 37% cheaper than Europe, but somehow still can’t move product. Time to get defensive with your pricing strategy and lock in those feed costs before this window closes.

KEY TAKEAWAYS

- Lock Your Feed Now: December corn at $4.23/bushel won’t last—Texas producers who secured 60% of winter needs at $4.15 are already seeing the payoff as milk prices soften

- Get Defensive on Pricing: Class III put options at $17.50-$17.00 are lighting up for good reason—October milk checks are tracking 15-25¢/cwt lower depending on your cooperative’s risk management

- Focus on Protein Over Fat: With FMMO component changes hitting December 1st (protein factor jumping to 3.3%), shift your ration strategy now—butterfat premiums are getting crushed while protein holds steady

- Watch Those Technical Levels: Butter support at $2.00 and cheese blocks at $1.75—if these break on heavy volume (5+ loads butter, 8+ loads blocks), we’re looking at July lows and even tighter margins

- Regional Reality Check: California producers need milk-to-feed ratios above 4.2 just to match Midwest profitability due to hay costs running $45-65/ton higher—adjust your expectations accordingly

When Labor Day’s Over, Reality Hits Hard

You know that sinking feeling when you walk into the parlor on Monday morning and your milk hauler is shaking his head? That’s exactly what happened to dairy markets today.

Butter fell a sharp 3.25¢ to $2,0125, and cheese blocks dropped a full cent to $1.7650—and here’s what’s going to sting your wallet.

Regional Milk Check Reality Check

Don’t believe anyone giving you generic projections. The impact on your October milk check depends entirely on where you’re milking and who you’re shipping to:

- Wisconsin cooperatives: Reporting 15-25¢/cwt declines depending on marketing strategies

- California operations: Seeing varied impacts based on risk management programs

- Texas producers: Geographic premiums providing some buffer against spot weakness

- Northeast fluid markets: Class I differentials offering partial protection

“We’re seeing milk that used to command a 50¢ premium now at 25¢ over Class,” a Fond du Lac County producer told me yesterday. “When the plants are full and you’ve got extra milk looking for a home, that local basis gets pressured fast.”

Supply Pressures Hitting the Market

Processors came back from the break with cream tanks topped off and zero urgency to chase milk. Here’s why:

The USDA’s Supply-Side Shift: August 12th WASDE report bumped 2025 milk production to 228.3 billion pounds—up 500 million from July’s estimate. That’s 3.4% year-over-year growth, hitting an already saturated market.

Where The Milk’s Coming From

- Texas leads the charge: 4% annual growth, with some counties posting spring gains as high as 10.6% thanks to mild winter weather and new processing capacity.

- California struggles: Production is down 1.2% amid battles with H5N1 and heat stress, with new biosecurity costs adding $0.15-0.25/cwt for some operations.

- Wisconsin and Minnesota are up 2.8%, but regional plant capacity maxed out, pressuring local premiums.

A Deep Dive into the CME Cash Session

The CME cash session told a crystal-clear story if you know the signs:

Butter Market Breakdown

- 7 offers vs. 3 bids = Sellers desperate to move product

- All damage from 1 trade = Either forced liquidation or buyers vanished

- Critical level: $2.00 support—5+ loads trading below triggers $1.95 test

Cheese Block Pressure Mounts

- 13 loads traded down = Real commercial selling, not spec money

- Volume with decline = Sustained weakness likely

- Key support: $1.75—break on 8+ loads targets July lows at $1.70

The Protein Bright Spot

Dry whey showed three bids, zero offers for the third straight session—protein demand holding steady while fat markets crater. While the revenue side of the ledger faces pressure, the expense side offers a critical silver lining for managing margins.

Feed Costs: Your Margin Lifeline

Here’s the silver lining keeping margins alive:

- December corn: $4.23/bushel

- Soybean meal: $283.30/ton

- Milk-to-feed ratio: 3.8

But regional variations are significant:

Midwest Advantage

“We locked 60% of our winter corn at $4.15 back in July,” an Iowa producer shared. “That forward thinking’s paying off now with milk prices softening.”

Western Challenges

California dairies face hay costs $45-65/ton higher than Midwest operations, plus water expenses adding $1.20/cwt. UC Davis Extension data show that Western producers need ratios of 4.2 or higher to match Midwest profitability.

Key On-Farm Strategies

Protein Optimization: Beyond The Buzzword

With FMMO protein factor changes hitting December 1st, smart producers are already adjusting:

What Wisconsin Nutritionists Recommend

- Balance third-cutting alfalfa quality with commodity proteins

- Target rumen-degradable vs. undegradable protein ratios

- Hit 16.8% crude protein without over-supplementing

“We’re shifting from chasing butterfat premiums to optimizing protein yield,” explains a Lancaster County producer running 800 head. “With the December component changes, protein’s where the money is.”

FMMO Now: What Farmers Need To Know

June 1st’s Federal Milk Marketing Order reforms created the biggest structural change in a decade:

What Changed

- Class I skim pricing returned to “higher-of” Class III or IV

- Make allowances updated: cheese to $0.2519/lb, butter $0.2272/lb

- Net effect: $91 million annually transferred from producer checks to processor margins

Who Gets Hit Hardest

Order 5 regions with manufacturing-heavy operations feel the biggest squeeze. December’s component factor changes (protein to 3.3%, nonfat solids to 9.3%) will create another pricing shift (USDA AMS, Bullvine analysis).

Options Market Signals Caution

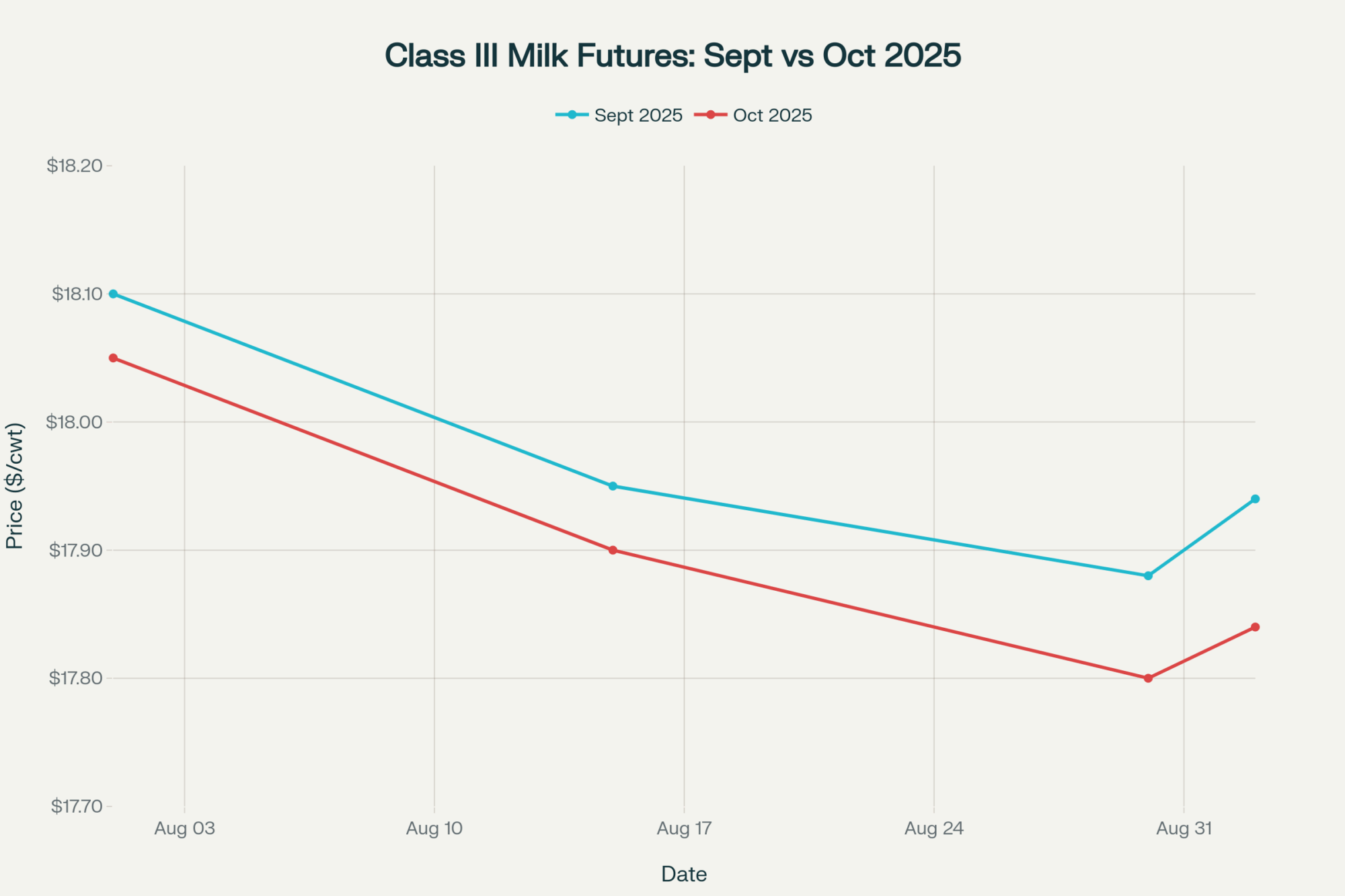

On the futures board, September Class III settled at $17.94 and October near $17.84 — a backward curve, meaning the market expects prices to rebound over the coming months. But, with today’s cash price moves, that hope might be premature (CME Group).

Class III put options at $17.50 and $17.00 strikes are lighting up—volume spikes showing producers getting defensive fast. Implied volatility jumped 15% last week, making hedging more expensive but potentially more valuable (CME data).

Smart Hedging Moves

- Put options around $17.90-$18.00 to establish minimum milk prices

- Call spreads on feed protect against crop weather surprises

- Timing matters: Wait for volatility dips to reduce option costs

The Big Picture: Global Markets and Tomorrow’s Level

Global Export Disconnect

Here’s the head-scratcher: U.S. butter at $2.01/lb trades 37% below EU prices ($3.18/lb) and 36% under New Zealand ($3.14/lb).

That massive discount should drive explosive exports, but Global Dairy Trade’s September 1st auction saw its overall price index drop 4.3% to an average of $1,209/MT—international weakness removing any upward price pressure from world markets.

Tomorrow’s Critical Levels

What I’m Watching At 10:00 AM

- Butter: Support test at $2.00—more than three loads below triggers $1.95 target

- Cheese blocks: $1.75 line in sand—heavy volume break signals July lows retest

- Dry whey: Bid strength continuation could support protein complex recovery

Volume Thresholds That Matter

- Butter: >5 loads confirms directional moves

- Blocks: >8 loads breaks technical levels

- Any NDM volume signals export developments

Your Regional Action Plan

Upper Midwest Producers

- Immediate: Review cooperative marketing agreements for basis risk

- Feed strategy: Lock winter corn before harvest pressure lifts futures

- Component focus: Optimize protein rations for December changes

Western Operations

- Cost management: Evaluate water-saving technologies, rotational grazing

- Hedging priority: Protect against feed cost spikes with call options

- Margin reality: Adjust profitability expectations 15-20% below national averages

Texas Expansion Areas

- Capacity planning: Monitor regional plant utilization rates

- Growth management: Balance herd expansion with local milk demand

- Weather hedge: Prepare for potential winter weather disruptions

The Bottom Line

This isn’t just market noise—it’s structural change happening in real time. The supply situation is strong, demand is cautious, and FMMO reforms are reshuffling who gets what from every hundredweight.

What Winners Are Doing Now

✓ Locking feed costs at current favorable levels

✓ Getting defensive with put options on Class III

✓ Focusing on protein over butterfat in ration management

✓ Managing cash flow for smaller October checks

✓ Planning component strategies for December FMMO changes

The margin squeeze is real, but it’s not panic time. Producers with solid risk management, flexible feeding programs, and tight cash flow control will weather this downturn better than those hoping for a quick recovery that might not come.

Feed costs are still your friend. Protein optimization is becoming crucial. And regional differences matter more than ever in determining who stays profitable through this challenging period.

Smart money is getting defensive now—not waiting to see how much worse it gets.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Navigating the Volatile Dairy Market: Essential Risk Management Strategies for Farmers – This article provides a practical framework for implementing the hedging strategies mentioned in our report. It breaks down how to effectively use futures and options to protect your operation from the exact price volatility seen today, reducing risk on future milk checks.

- The Future of Dairy: Innovations in Processing and Product Development – To understand where the market is heading long-term, this piece unpacks the strategic trends in dairy processing and consumer demand. It offers insights into how new products and technologies will create future revenue streams beyond today’s commodity market pressures.

- The Genetic Revolution: How Marker-Assisted Selection is Reshaping Dairy Herds – This report reveals how to boost profitability from within the herd using advanced genetics. It details innovative selection methods for improving feed efficiency and component yields, offering a powerful, long-term strategy to counter the margin squeeze discussed in today’s market analysis.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.