UK dairy: 5% production surge meets £0.35/L crash while 17% of farms face 60%+ debt ratios

EXECUTIVE SUMMARY: UK dairy farmers find themselves caught in an unprecedented paradox—production’s up 5% while farmgate prices plummet toward £0.35 per liter, creating what could be the industry’s most challenging period since Brexit. AHDB’s October data reveals the cruel mathematics at work: that 1.78 milk-to-feed ratio historically signals expansion, yet farmers following this indicator are walking into a structural crisis, not a cyclical downturn. With 17% of UK dairy operations already carrying debt-to-asset ratios above 60% according to DEFRA’s July survey, and working capital averaging just £800-1,200 per cow versus the £1,500 recommended minimum, the next three months will determine who survives this consolidation. What’s different this time is the convergence of permanent factors: Brexit has eliminated our EU export safety valve (down 21% since 2018), processing capacity’s shrinking as plants close, and global oversupply’s hitting simultaneously, with the US up 4.2% and Argentina up 7.7%. The farms that will survive will be those that take action now: locking in feed costs at current levels before winter volatility, applying for retail contracts offering 4-5p premiums over manufacturing milk, and having honest conversations with lenders before January reviews. This isn’t about weathering another cycle—it’s about recognizing a fundamental market restructuring that’ll likely see UK dairy consolidate from 8,500 to around 5,500 farms by 2030, with survivors emerging stronger but the middle ground disappearing entirely.

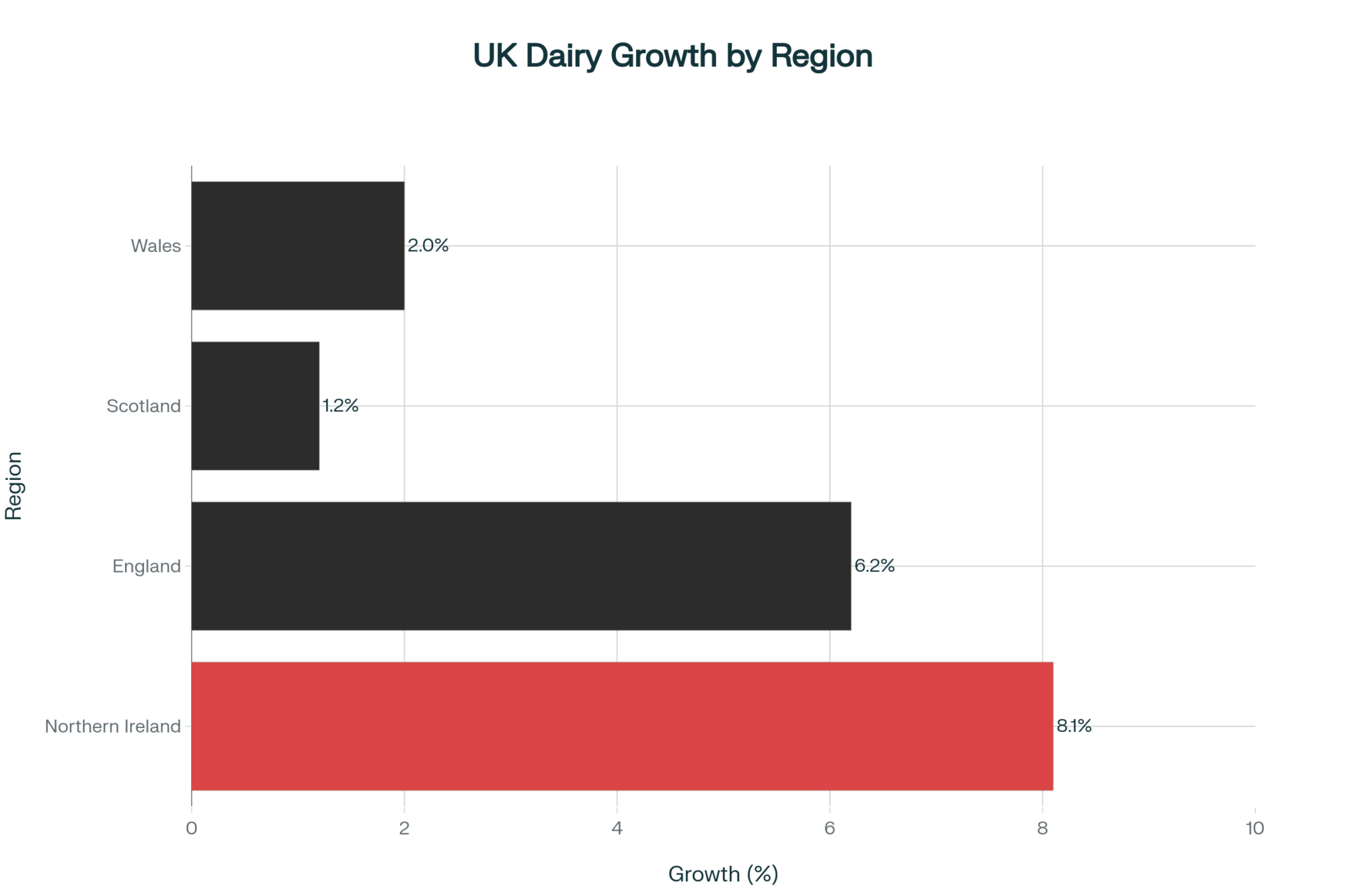

So here’s what caught my attention this week. I’m reading through AHDB’s October quarterly review, and UK milk production increased by 5% last quarter, while farmgate prices dropped by nearly 10% to £0.38 per liter. Northern Ireland’s pushing production up 8.1%, England’s at 6.2%… and yet we’re all watching prices slide toward what could be £0.35 by February.

You know what’s really interesting, though? This actually makes sense when you look at that milk-to-feed ratio AHDB calculates every month. At 1.78, it’s telling producers to expand—that’s what the numbers say. Feed’s relatively cheap compared to milk, historically speaking. But I’ve been doing this long enough to know that sometimes the numbers don’t tell the whole story.

Why Good Farmers Are Making Tough Calls

I was talking with a Shropshire producer last week—let’s call him Tom—who runs about 280 cows near Market Drayton, and he summed up what a lot of you are probably feeling. “Look,” he said, “I’ve already put £150,000 into expanding the parlor. Started construction in March when things looked different. The heifers are bred, the concrete’s poured. What do you want me to do, just walk away?”

And honestly? He’s got a point. Most expansion decisions were made back in the spring when the outlook was completely different.

Here’s something interesting from the Journal of Dairy Science that came out in March—they found that farmers feel losses about twice as strongly as gains. Makes sense, right? When you’ve already invested that much, stopping feels worse than pushing through, even when the numbers get tight.

The math producers are doing… I get it. Your barn mortgage is £8,000 a month, whether you milk 200 cows or 250. The mixer wagon, the parlor equipment—those costs don’t change. So you think, well, if I can spread those fixed costs over more milk…

The thing is, when everyone thinks that way, we create our own problems.

What Brexit Really Changed (And Nobody Wants to Talk About)

You know what’s different this time around? We can no longer simply ship excess milk to Europe. Government trade stats from September show our dairy exports to the EU are down 21% since 2018. Meanwhile—and this is what really gets me—HMRC data shows New Zealand imports to the UK jumped 81% just in the first half of this year.

Remember 2015-2016? When prices tanked, we could at least move milk to Irish processors or French cheese makers. Not a great amount of money, but it kept things moving. That safety valve? It’s gone.

I’ve been reading through the House of Commons trade committee report from last year, and the reality is stark. Between sanitary certificates, health requirements, and three-day border delays, fresh dairy exports just don’t pencil out anymore. The Trade Policy Observatory figures these non-tariff barriers add 5-10% to costs. That’s not something that fixes itself when prices recover—it’s the new normal.

The Numbers That Keep Me Up at Night

I’ve been reviewing the Farm Business Survey data—DEFRA has published their July numbers—and there are some clear warning signs. Approximately 17% of dairy farms already have debt-to-asset ratios exceeding 60%. That’s… that’s concerning.

Here’s how I think about it:

- Below 40% debt-to-asset: You can probably ride this out for 12-18 months

- 40-60% debt-to-asset: Vulnerable but manageable with strategic adjustments

- Above 60% debt-to-asset: At £0.35 milk, you’ve got maybe six months before the bank starts asking hard questions

Working capital’s the other piece that worries me. The Farm Finance Institute’s been saying for years you need about £1,500 per cow as a buffer. But Kite Consulting’s recent surveys? Most UK farms are running at a cost of £800 to £1,200 per cow. And if you drop below £500 per cow… well, one major breakdown, one disease outbreak, and you can’t make payroll.

Michael Thompson over at Promar—he’s worked with over 200 dairy clients through the years—he put it to me straight: “Banks don’t care about your profit projections. They care about whether you can make next month’s payment.”

Why I Think £0.35 Is Coming by February

Now, I’m not one to make predictions, but the math here is fairly straightforward. AHDB has been tracking this for 15 years, and their Milk Market Value model indicates a three-month lag between commodity prices and what we receive at the farm gate. Typically accounts for about half of the commodity price movement.

Look at where commodities are right now. The EU Milk Market Observatory’s October data has butter at €605 per 100kg—that’s down 22% from last year. Skim milk powder’s off 12%. And those Global Dairy Trade auctions? Down nearly 6% across September and October.

When that works through our processing contracts… According to Dr. Robert Chen from AHDB’s market intelligence team on Tuesday, and he estimates the probability of reaching £0.35-0.36 by February at approximately 85%. The only thing that changes this is if we experience a major supply shock or China suddenly starts buying again. Neither looks likely right now.

What Different Regions Are Teaching Us

What’s fascinating is watching how different parts of the UK are handling this. Scotland’s production is only growing production by 1.2% according to Dairy UK’s latest numbers. Why the restraint?

Well, they learned the hard way. When Müller closed those plants in East Kilbride and Aberdeen back in 2018, 43 farms in northeast Scotland suddenly had nowhere to send their milk. They ended up paying 1.75p per liter just to truck milk to Bellshill—that’s over 100 miles. When you’re getting £0.35 at the gate and paying nearly 2p for transport… you’re basically paying to produce milk.

Northern Ireland? Totally different story. They’re expanding by 8.1%, but here’s the context: Dale Farm invested £70 million in its Dunmanbridge facility last June. They’ve secured an £8 billion deal to supply Lidl stores across 22 countries. When your processor’s investing that kind of money and has those contracts locked in, expansion makes more sense.

I was just in Devon last month, and producers there are taking a completely different approach. A small operation I visited—about 85 cows—they’ve gone fully grass-based, selling directly to local shops at £0.65 per liter. Different game entirely.

Your Next 90 Days: The Decisions That Matter

1. Lock Your Feed Costs (This Week, Seriously)

The Chicago Board of Trade had corn at $4.20 a bushel and beans at $10.17 as of October 15th. That’s not terrible, historically. But you know how fast that can change. Progressive Dairy’s data shows January-February usually brings volatility when South American weather becomes a factor.

Emma Davies at ForFarmers—she handles purchasing for over 150 dairy clients—she made a great point to me last week: “Forward contracting through March doesn’t cost anything upfront if your credit’s good. Why wouldn’t you lock that in?”

Think about it. If corn jumps to $6—which happened in the 2012 drought—you’re looking at an extra £0.04 per liter in feed costs. For a 200-cow farm, that’s £64,000 a year. That’s not margin optimization anymore, that’s survival money.

2. Those Retail Contracts (Application Windows Are Now)

Here’s what really struck me in the October price announcements. Arla and First Milk cut manufacturing contracts by 1.00 to 1.66p per liter. But the retail-aligned contracts? The Tesco Sustainable Dairy Group and Sainsbury’s groups actually increased by 0.88 to 2.85p.

We’re talking about a 4-5p per liter gap opening up. On 1.6 million liters a year, that’s a £64,000 to £80,000 difference. That’s transformative for cash flow.

However, and this is crucial, these applications typically run from October through November for Q1 contracts. Miss this window? You’re waiting another whole year. And next year, everyone will be trying to get in.

3. Hard Choices About Herd Size

If your working capital’s dropping toward £500 per cow, or you’re burning through more than £15,000 a month in cash… strategic culling might be necessary. I know how that sounds when you’ve been building the herd, but sometimes taking a step back is the smart move.

AHDB’s latest deadweight prices show culls at £3.20 to £3.80 per kg—so £800 to £1,000 per head depending on condition. However, history tells us from 2016 that when everybody starts selling, prices can drop by 30-40%. You could be looking at £550-650 by February if panic sets in.

Three Things That Could Make Everything Worse

- The Heifer Shortage Nobody’s Watching

British Cattle Movement Service data shows UK cow numbers actually dropped 0.6% year-over-year. However, what concerns me is that the replacement pipeline’s drying up.

AHDB Breeding+ stats show beef-on-dairy programs are up 40% this year. Makes sense for cash flow, right? But Genus ABS tells me sexed semen’s now 60-70% of all breedings. Add in farms selling pregnant heifers for quick cash, and we’re setting up a replacement shortage for the 2027-2028 period.

Current market reports have bred heifers at £1,400-1,600. Based on what happened after 2016, when will the shortage hit? Those could easily reach £2,200-£ 2,800. Farmers selling heifers now won’t be able to buy them back when things recover.

- Banks Are Quietly Changing the Rules

I can’t name names, but I’ve talked to lending officers at three major UK banks, and they’re all tightening up. Operating lines that used to get annual reviews? Now it’s quarterly. Farms with weakening ratios are seeing credit limits cut 10-20%. They’re asking for more collateral across the board.

The killer is the timing. Banks do their big reviews in January-February—exactly when milk prices will be at their worst, and your numbers look terrible. A farm expecting to roll over £200,000 in operating credit might get offered £140,000 at higher rates. That £60,000 difference in working capital, right when you need it most? That could be the ballgame.

- Processing Capacity Keeps Shrinking

Kite Consulting’s September analysis is sobering. We have too much processing capacity for a market where liquid consumption’s dropping by about 1.5% annually, according to Dairy UK. When processors can’t make money at £0.35 per liter of milk, plants close.

Remember what happened to those Scottish farms after Müller’s closures. And that Skelmersdale plant breakdown last April that caused 12 days of dumping? Word is that they’re “evaluating the facility’s future”—that’s code for “might close.”

If you don’t have a backup plan for what happens to your milk if your processor shuts down or cuts contracts, you need one. Now.

Looking Past the Crisis: UK Dairy in 2030

We will get through this—we always do—but UK dairy will look different on the other side. Based on historical consolidation patterns and current trends, I anticipate that we will have approximately 5,500 farms by 2030, down from around 8,500 today. Three main types of operations will likely dominate:

The big effort from efficient farms—350 to 600 cows—with retail contracts and costs below £0.35 per individual —folks entered this crisis with a strong balance sheet, likely to acquire assets from distressed neighbors. You’ll see them clustered near the big processing hubs in the Midlands, and Yorkshire, and Northern Ireland.

The premium producers—smaller operations, typically with 60 to 120 cows—sell organic, grass-fed, or direct-to-consumer products at £0.50 to £0.70 per liter. They’re avoiding the commodity game entirely. Scotland and Wales tourism areas will probably have clusters of these.

The diversified operations—200 to 350 cows—mixing milk production with beef-on-dairy, maybe some renewable energy, and custom heifer raising. Multiple income streams mean that when one market tanks, you’re not sunk.

What probably won’t make it? A traditional 150- to 250-cow farm operating on commodity contracts with debt exceeding 50%. That middle ground… it’s just tough to see how it works anymore.

The Conversation We Need to Have

Look, I know this is heavy. For most of us, this isn’t just business—it’s family, it’s identity, it’s everything we’ve worked for. The stress is real. It affects everything from how you sleep to how you make decisions.

Dr. Lisa Roberts at Edinburgh has done great work on farm mental health, and she’s right—reaching out for help, whether that’s financial advisors, family, or counseling, is not a sign of weakness. That’s being smart. The best farmers I know are those who recognize when they need an outside perspective.

And for some operations… this is hard to say, but if the numbers truly don’t work, exiting on your terms now might be better than bleeding equity for 18 months, hoping for a miracle. That’s not failure. That’s protecting what you’ve built.

Why This Time Really Is Different

I’ve been through 2009, 2015-2016, COVID, and a bunch of smaller crashes. This one feels different because it IS different.

Brexit changed our export markets permanently—that 21% drop isn’t coming back. Processors are consolidating, not expanding. And the whole world’s producing more—USDA data shows the US up 4.2%, Argentina up 7.7%—while China’s barely importing based on their customs data.

This isn’t just a cycle that’ll fix itself. It’s a structural shift. The ones that make it will be more profitable, but there’ll be fewer of them.

The Clock’s Ticking

Every crisis creates winners and losers. The difference usually isn’t resources—it’s timing. The decisions you make in the next 90 days matter more than what you hope happens in the next 90 weeks.

Lock in feed costs. Apply for retail contracts if you can. Have honest conversations with your bank now, not in February. Look at your working capital realistically. And if the numbers say you need to make changes, make them while you still have options.

That 1.78 milk-to-feed ratio everyone’s watching? It’s yesterday’s indicator for tomorrow’s market. The game’s changed. Question is whether you change with it.

Make the calls. Have the conversations. Run the real numbers, not the hopeful ones.

February’s coming whether we’re ready or not. What you do between now and then… that’s what determines whether you’re still milking in 2027.

KEY TAKEAWAYS

- Lock feed costs this week to save £64,000 annually—with Chicago Board corn at $4.20/bushel (October 15), forward contracting through March protects against potential jumps to $6 that would add £0.04/liter to costs on a typical 200-cow operation

- Retail contract applications close in November for Q1 2026—the 4-5p/liter premium between manufacturing and liquid contracts (Tesco Sustainable Dairy Group, Sainsbury’s programs) represents £64,000-80,000 annual difference on 1.6 million liters, but miss this window and you’re waiting another full year

- Strategic culling becomes necessary below £500/cow working capital—with AHDB showing cull prices at £800-1,000/head currently, versus likely £550-650 by February, when panic selling starts, farms burning over £15,000 monthly need to act while values hold

- Regional strategies vary based on processor infrastructure—Northern Ireland’s 8.1% expansion makes sense with Dale Farm’s £70 million investment and Lidl contracts, while Scotland’s 1.2% restraint reflects lessons from Müller closures that left farmers paying 1.75p/liter transport

- Bank credit reviews in January-February will catch unprepared farms—lending officers at major UK banks confirm they’re cutting operating lines 10-20% for weakening operations, meaning that a £200,000 credit renewal might only get £140,000 right when milk prices hit their floor

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- UK Dairy’s Lupin Bet: Are the Profits Real in 2025? – This tactical guide reveals how to achieve immediate, quantifiable cost savings by replacing 50% of soya protein with lupin. Learn the key milling and contract strategies to save over £750 monthly on a 250-cow herd, directly boosting your working capital during the price crash.

- The Real Reason 190 UK Dairy Farms Disappeared – And What They’re Not Telling You – Gain critical strategic insight into the structural forces driving farm exits. This analysis uncovers the harsh reality of processor redlining, geographic transport penalties, and market power dynamics, providing a vital risk assessment tool for your long-term survival strategy.

- The Great UK Dairy Cull: What’s Really Driving the Farm Exodus – Learn how scale and technology are now essential survival metrics. This article details the automation reckoning, providing crucial ROI metrics for robotic milking and achieving feed conversion ratios below 0.9 kg/litre to survive the coming industry consolidation.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.