At roughly $20/cwt milk against $19.14 in full costs and just 15.9¢ of the food dollar, Thunder’s $40–50K months show both what’s possible — and how fast value-added can blow a hole in your cash flow.

Executive Summary: Two Florida dairy farmers built Thunder CoffeeMilk into $40,000–$50,000 a month — starting in a kitchen, driving 15 hours to a Michigan lab, and watching their first shelf-stable batch come out as a solid brick. The reason it matters to you has nothing to do with coffee: you get just 15.9¢ of every food dollar, and the dairy farm share has slid from 52¢ in 1980 to 25¢ today. At an all-milk price around $20/cwt against $19.14 in full costs, a lot of herds are running on fumes, and value-added looks like the way into the other 84¢. But the math is brutal — Thunder ran negative cash flow for two to three years, and if you’re bankrolling a brand off the same balance sheet that feeds your cows, a $1/cwt price dip is another $125,000 to absorb on a 500-cow herd. The piece lays out four real paths past 15.9¢ — branded CPG, on-farm processing, commodity optimization, and carbon/data monetization — and exactly where each one breaks. Read it if you’ve ever wondered whether your operation is built to capture value or just produce it. The 30-day move is the cheapest one: spend half a day auditing your hauling and co-op product mix before you fantasize about cans.

Dave Temple grew up on a dairy farm in Queensland, Australia, where milk-brewed iced coffee is the drink you grab without thinking about it. He moved to Florida, started his own farm, and went looking for that coffee on American shelves. It wasn’t there. So he and fellow multigenerational dairy farmer Ed Henderson decided to build it themselves, starting eight years ago in Ed’s kitchen (Entrepreneur, June 15, 2026).

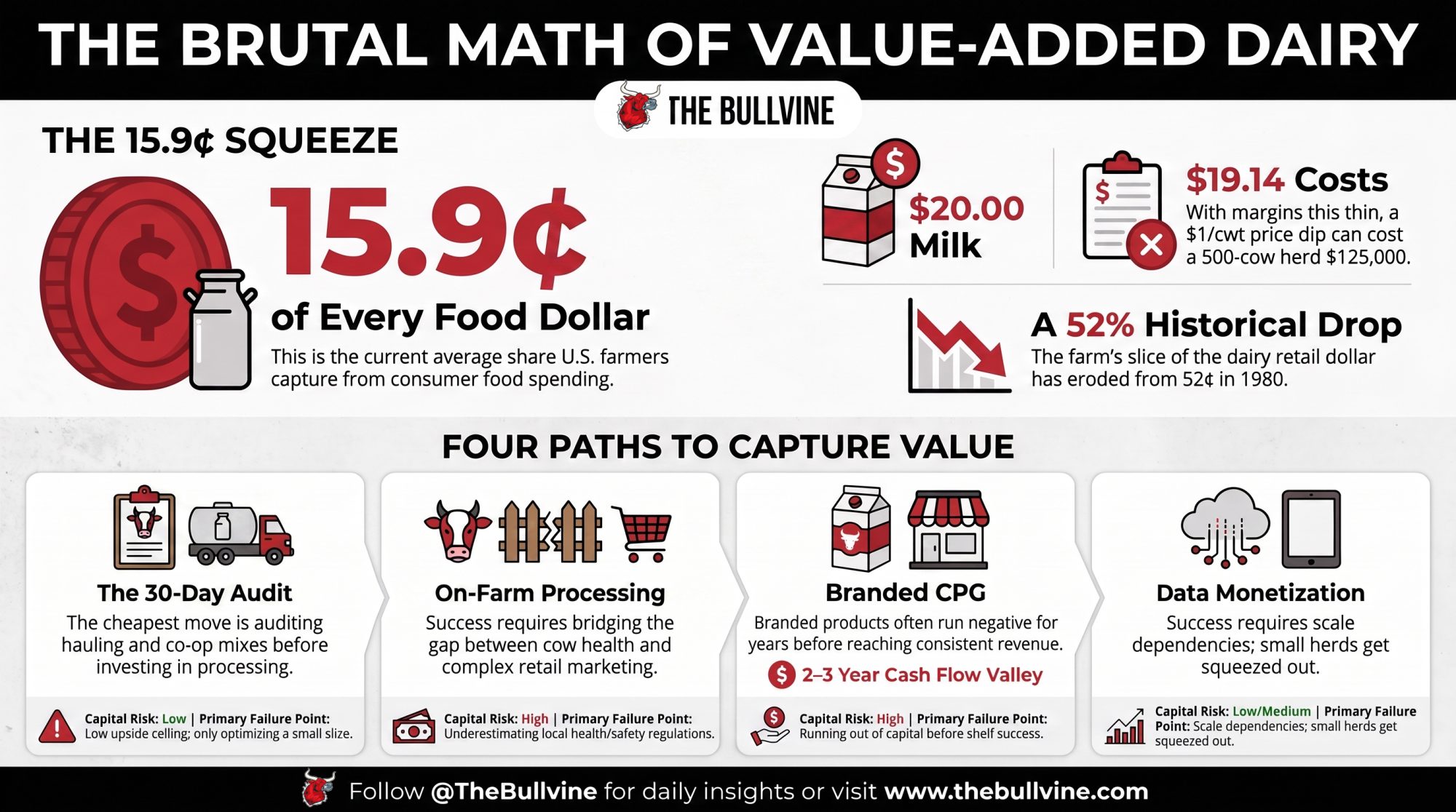

Their brand, Thunder CoffeeMilk, now moves $40,000 to $50,000 a month and rolled out across more than 400 select 7-Eleven stores in Florida when it launched. The numbers sound impressive until you stack them against what USDA says you get from the average food dollar. In 2023, U.S. farmers captured just 15.9 cents of every dollar consumers spent on domestically produced food (USDA ERS Food Dollar Series, 2023 data). That ceiling is the backdrop for what Temple and Henderson built — a value-added product that captures more of the retail dollar than raw milk ever will, one 11-ounce can at a time.

What’s Actually Squeezing the Farm Share

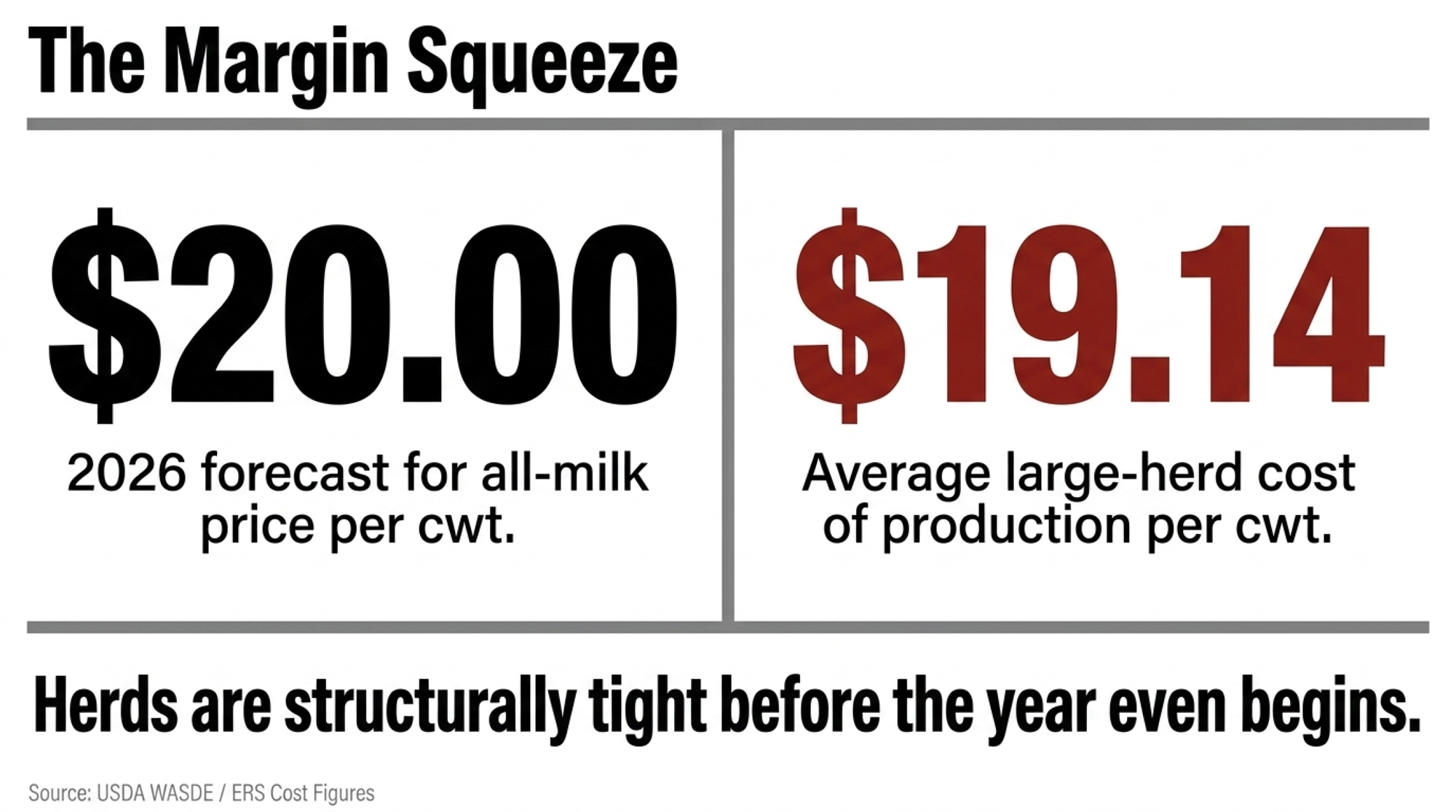

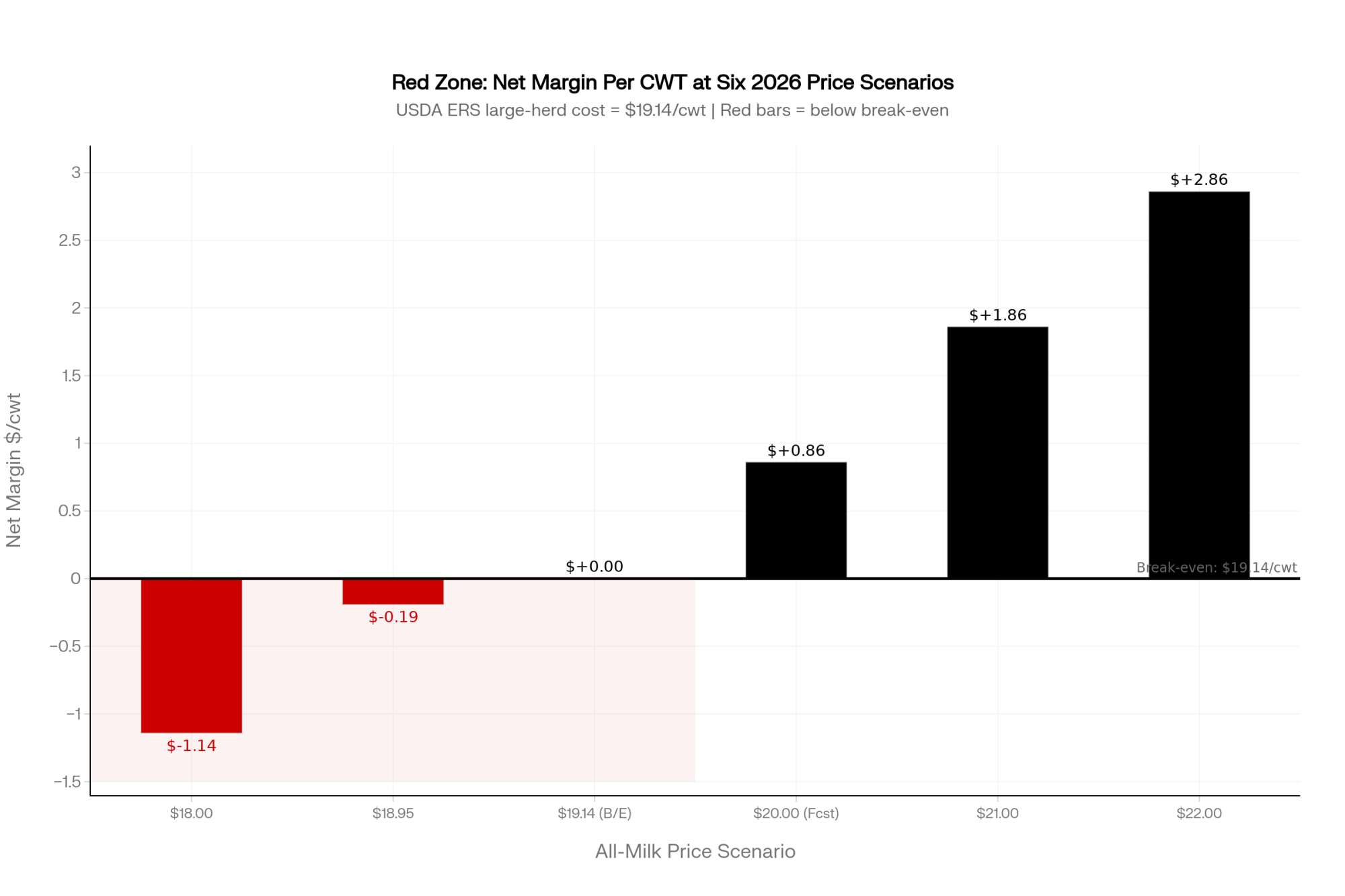

The old playbook was simple. Milk more cows, milk them cheaper, ship to the co-op, and pray the mailbox price covered your cost of production. In 2026, that math is harder to make work. USDA’s latest WASDE outlook has 2026 all-milk hovering around the $20/cwt mark, with 2027 pegged lower. ERS cost figures put average large-herd cost near $19.14/cwt, and the smallest herds run far higher — which is why plenty of dairies start the year structurally tight even when the price looks decent (The Bullvine, “$18.95 Milk, $19.14 Costs,” Feb 10, 2026).

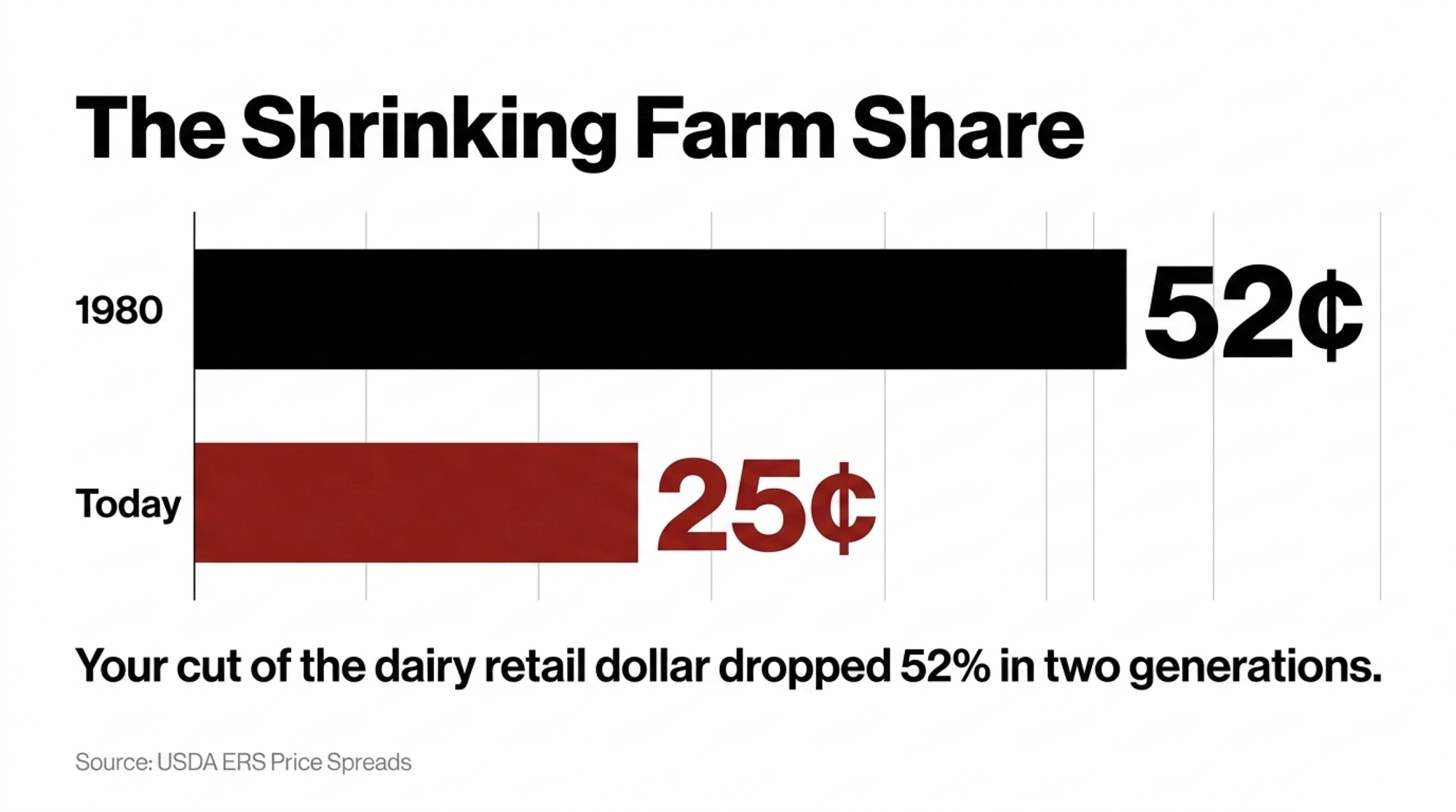

The farm’s slice of the dairy retail dollar has been eroding for two generations. It sat near 52 cents in 1980. USDA’s most recent price-spread data puts it around 25 cents today — the full decline from 52¢ to 25¢ is roughly a 52% drop over that span (The Bullvine, Dec 30, 2025, citing USDA ERS Price Spreads). Same cows. Same barn. A much thinner cut of the same gallon.

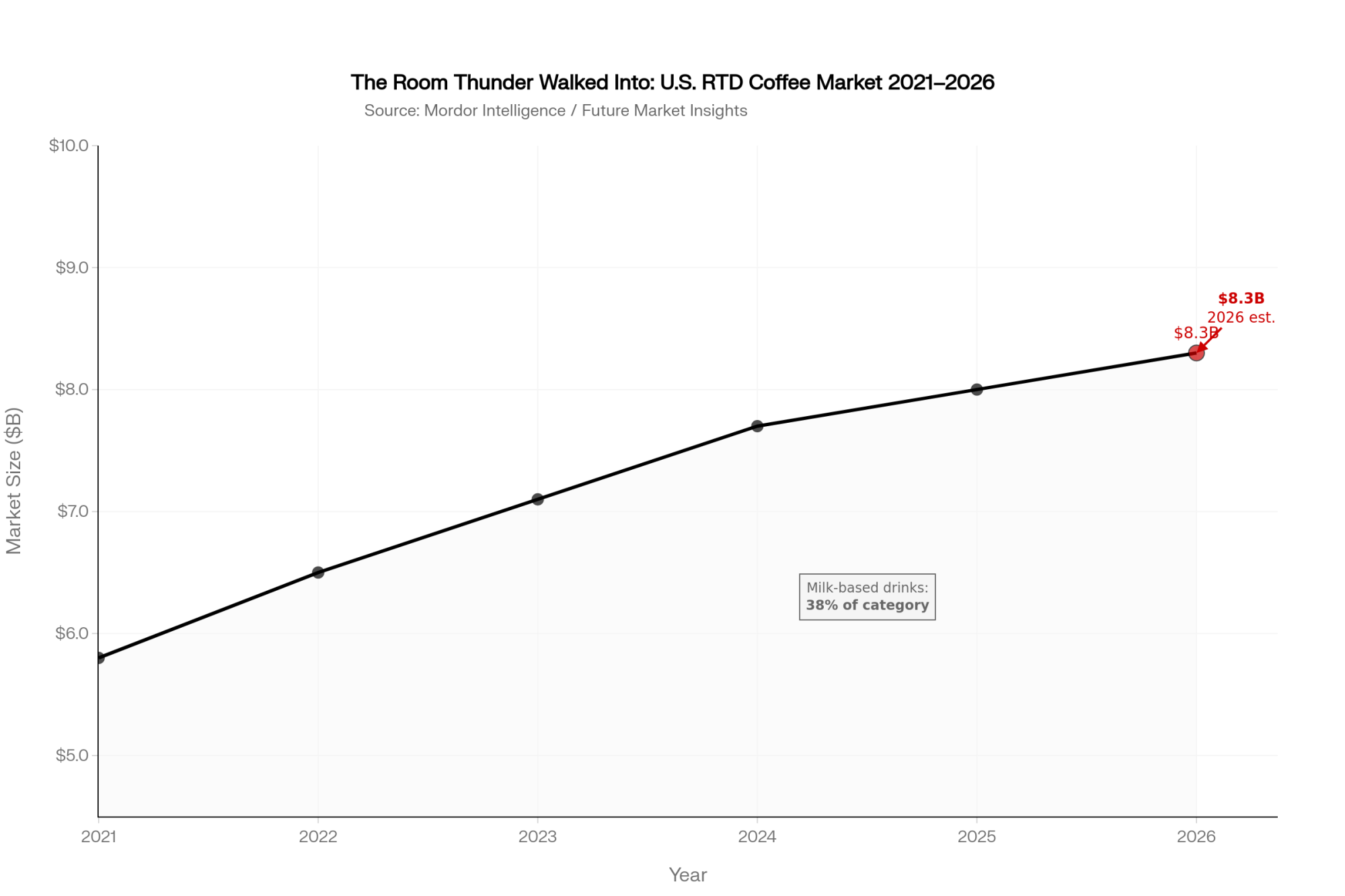

That’s the pressure pushing more farmers to look past the tank. Bullvine’s own analysis puts value-added dairy growth near 12% a year while commodity fluid milk stays roughly flat (Nov 24, 2025). And ready-to-drink coffee is one of the hottest rooms in that house — Mordor Intelligence pegs the U.S. RTD coffee market at about $8.3 billion in 2026, and Future Market Insights has milk-based drinks leading the category at 38% (May 2026). Temple and Henderson didn’t chase a fad. They walked into a growing category and noticed most canned coffee is brewed in water, with milk added as an afterthought. Their whole thesis was to flip that — brew the coffee in real milk from the start.

The Solid Block: What It Costs to Cross the Fence

Picture it: two dairy farmers, fifteen hours from home, standing in a food-processing lab at Michigan State University’s Food Processing Innovation Center, watching their first shelf-stable run come out of the machine. Except it didn’t pour. It thudded. The whole batch had seized into a solid block — not a drink, a brick (Entrepreneur, June 15, 2026). That brick is the whole story of value-added dairy in one image.

They spent two days on-site reworking the recipe before they could move forward. And here’s the honest part they’ll tell you themselves: neither had a background in sales, marketing, or distribution. Just decades of farming and a willingness to keep asking questions until they found the right people.

That solid block is worth more than a laugh. It’s the tuition receipt for crossing from commodity supplier to manufacturer. Inside the fence, these two can diagnose a sick cow or a broken ration in seconds. Step outside it into protein chemistry and shelf-life validation, and none of that instinct transfers. You’re back at square one. The failure wasn’t a fluke — it’s what the leap actually feels like. A 2024 Tarleton State University review names limited business and technical expertise, plus thin access to processing infrastructure, as core barriers stopping small U.S. dairy farms from making exactly this kind of move (Tarleton State University, Dec 22, 2024).

How This Plays Out on a Real Balance Sheet

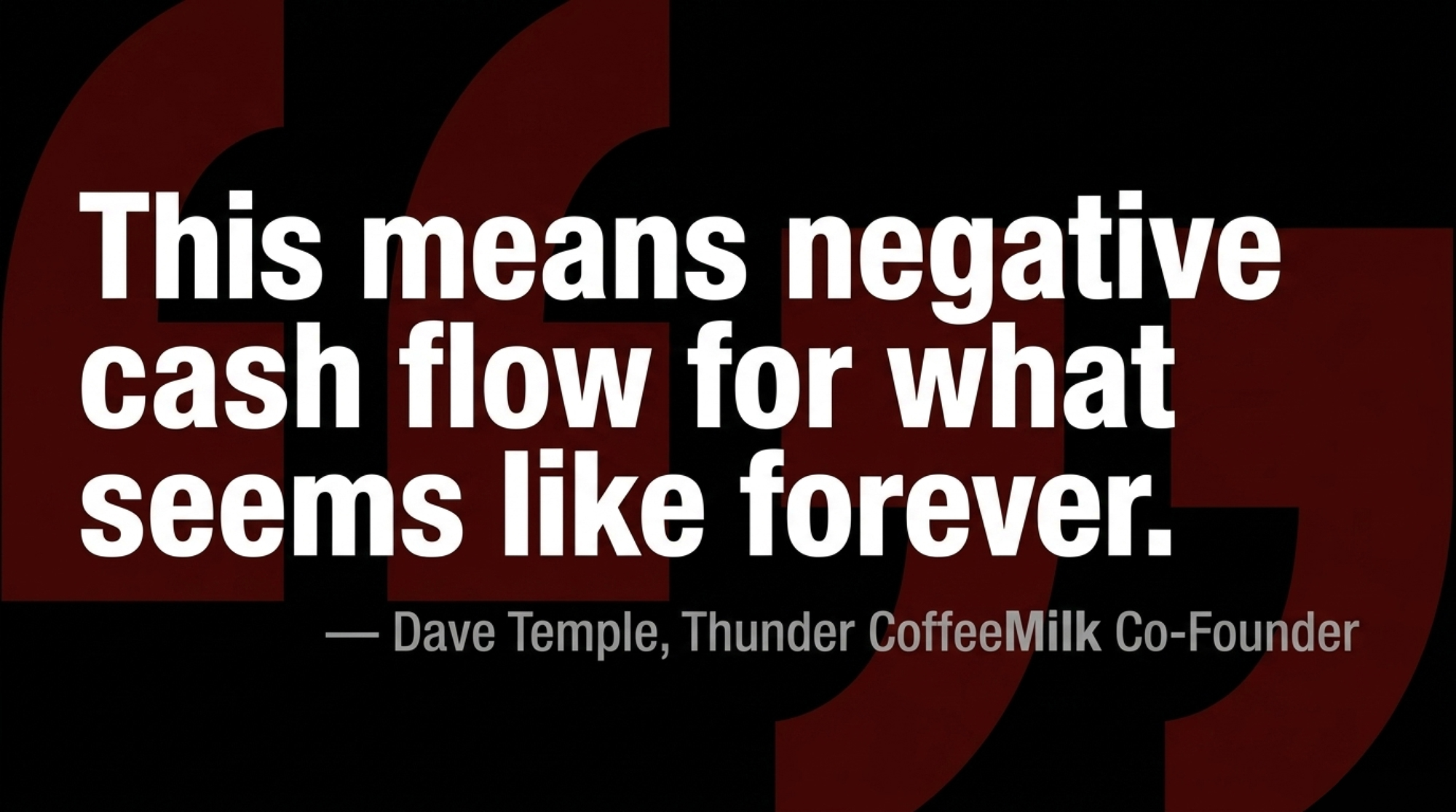

The line from Dave that should stop any producer cold is about retail, not chemistry. “For us to get our toe in the door, it has cost a large amount of money to effectively buy space to get our product in stores,” he told Entrepreneur. “This means negative cash flow for what seems like forever.” That’s not a Silicon Valley runway story with venture money padding the fall. That’s an operating line feeding cows and buying shelf space at the same time.

Put real numbers on the milk side first, because that’s the floor this whole bet stands on. Take a 500-cow herd averaging around 25,000 lb per cow — call it 125,000 cwt a year. A $1.00/cwt swing in your mailbox price — well within the range USDA has moved its 2026 forecast this year alone (from $18.95 in February toward the low $20s by mid-year) — is $125,000 in cash flow, up or down, across twelve months. Run lighter cows at 22,000 lb, and you’re closer to $110,000, but the point holds either way. That’s the sensitivity before you add a thing — then you stack a second business on top, one you’re deliberately running at a loss to hold a cooler slot.

| Herd Size | Avg Production (lbs/cow) | Annual CWT Produced | Impact of $1/cwt Swing | Impact of $2/cwt Swing | Margin Note |

|---|---|---|---|---|---|

| 100 cows | 25,000 lbs | 25,000 cwt | $25,000 | $50,000 | Modest swing — still can’t absorb brand losses |

| 250 cows | 25,000 lbs | 62,500 cwt | $62,500 | $125,000 | One bad year = value-added runway gone |

| 500 cows | 25,000 lbs | 125,000 cwt | 🔴 $125,000 | $250,000 | Article benchmark — two ventures, one balance sheet |

| 750 cows | 25,000 lbs | 187,500 cwt | $187,500 | $375,000 | Enough scale to potentially isolate ventures |

| 1,000 cows | 25,000 lbs | 250,000 cwt | $250,000 | $500,000 | Scale helps but concentrated risk remains high |

| 1,500 cows | 22,000 lbs | 330,000 cwt | $330,000 | $660,000 | 🔴 Large exposure — separate entity structure essential |

Here’s the retail side in plain barn terms. For example, say you sell a can wholesale for around a dollar and it costs you 70 cents to make and ship — that’s 30 cents of gross margin per can. Slotting fees, demos, and marketing to hold shelf space in a category run by recognized brands can eat into five figures per chain, per year. At 30 cents per can, you’re moving tens of thousands of units just to cover the cost of being on the shelf — before you clear a dime. That’s the arithmetic hiding inside “negative cash flow for what seems like forever,” and it’s why it took Thunder two to three years to reach consistent monthly revenue. (Those per-can figures are illustrative; Thunder hasn’t published its unit economics.)

Why Is the Farm’s Slice So Thin to Begin With?

Most of the value in food gets built after the product leaves the farm gate. USDA’s Food Dollar data assigns more than 88 cents of every consumer food dollar to the “marketing bill” — processing, packaging, transportation, retail, and food service. A farmer selling raw milk into that system is, by design, holding the smallest slice on the table. In 2024, the all-food farm share slipped to 11.8 cents, with only about 5.8 cents representing true farm-level value added (American Farm Bureau, citing USDA ERS, 2024).

Ed Henderson framed the real barrier better than any economist could. Marketing, he said, is “a feeling. I’m not a feeling kind of guy.” That’s the whole problem in one sentence. Deep expertise inside the fence can turn into a blind spot outside it — you don’t know what you can’t see.

But that same trap cut in their favor once. Not knowing the “proper” RTD formulation rulebook, they built the simplest version that survived the science: cold brew, real milk, a short ingredient list, no artificial sweeteners. Their one stated regret is not bringing a food scientist in earlier. Yet that clean label — the thing shoppers now reward — may exist precisely because two farmers didn’t over-engineer a product they were still learning to make.

Which Path Actually Fits Your Balance Sheet?

Thunder isn’t a template you can photocopy. It’s proof the staircase exists. There are four real paths producers are using to reach past 15.9 cents — and each one breaks in a different, predictable place. Find yours before you commit a dollar.

| Strategy Path | Capital Risk | Time to Positive Cash Flow | Primary Skill Gap | Primary Failure Point | Best Fit Herd Size |

|---|---|---|---|---|---|

| Branded CPG(Thunder path) | 🔴 High — multi-year negative cash flow | 2–3 years | Marketing, slotting, CPG brokers | Running out of capital before shelf velocity covers fees | Any — if balance sheet is isolated from farm |

| On-Farm Processing(cheese/bottled) | 🔴 High — infrastructure upfront | 3–5 years | Regulatory compliance, local sales | Underestimating health/safety compliance cost | 100–500 cows with local market access |

| Commodity Optimization(hauling/co-op audit) | ✅ Low — no new entity | 30–90 days | Internal ops, premium program knowledge | Low ceiling; optimizing a small slice | All herd sizes — start here |

| Carbon/Data Monetization | 🟡 Low–Medium — verification cost | 1–2 years | Disciplined record-keeping | 🔴 Scale dependency: 500-cow farm ≈ $3,000/yr vs 3,000-cow ≈ $150,000/yr | 1,000+ cows to make verification overhead worthwhile |

¹ Entrepreneur, June 15, 2026 · ² Nuffield Scholar report, 2016 · ³ The Bullvine, “You Only Get 15.9¢ of the Food Dollar” · ⁴ The Bullvine, “Data That Pays”

The branded-product path — Thunder’s — makes sense when you’ve got capital tolerance, a genuine market gap, and someone willing to learn the outside-the-fence game. And retail is no safe harbor: 7-Eleven’s parent, Seven & i, disclosed in its Q4 earnings documents that it expects to close or convert roughly 645 North American stores in fiscal 2026, per cstoredive (April 12, 2026) — even the shelf you fought to reach can move under you.

On-farm processing is the more traveled road, the one most research treats as the default value-added move (Nuffield Scholar report, 2016, Ireland/EU). The limit shows up early: regulatory complexity and capital cost stop most farms before they start. Only a small fraction of Irish farms are formally diversified, per Nuffield’s data — a useful signal for how steep the on-ramp is.

Then there’s the move you can actually start this month, no new company required. Capture more inside the commodity system — audit your hauling routes, question your co-op’s product mix, and press on component and premium programs, the cents-per-cwt kind of work that doesn’t require you to build a thing (The Bullvine, Jan 21, 2026). The ceiling is lower, but the risk is low and the payback is fast.

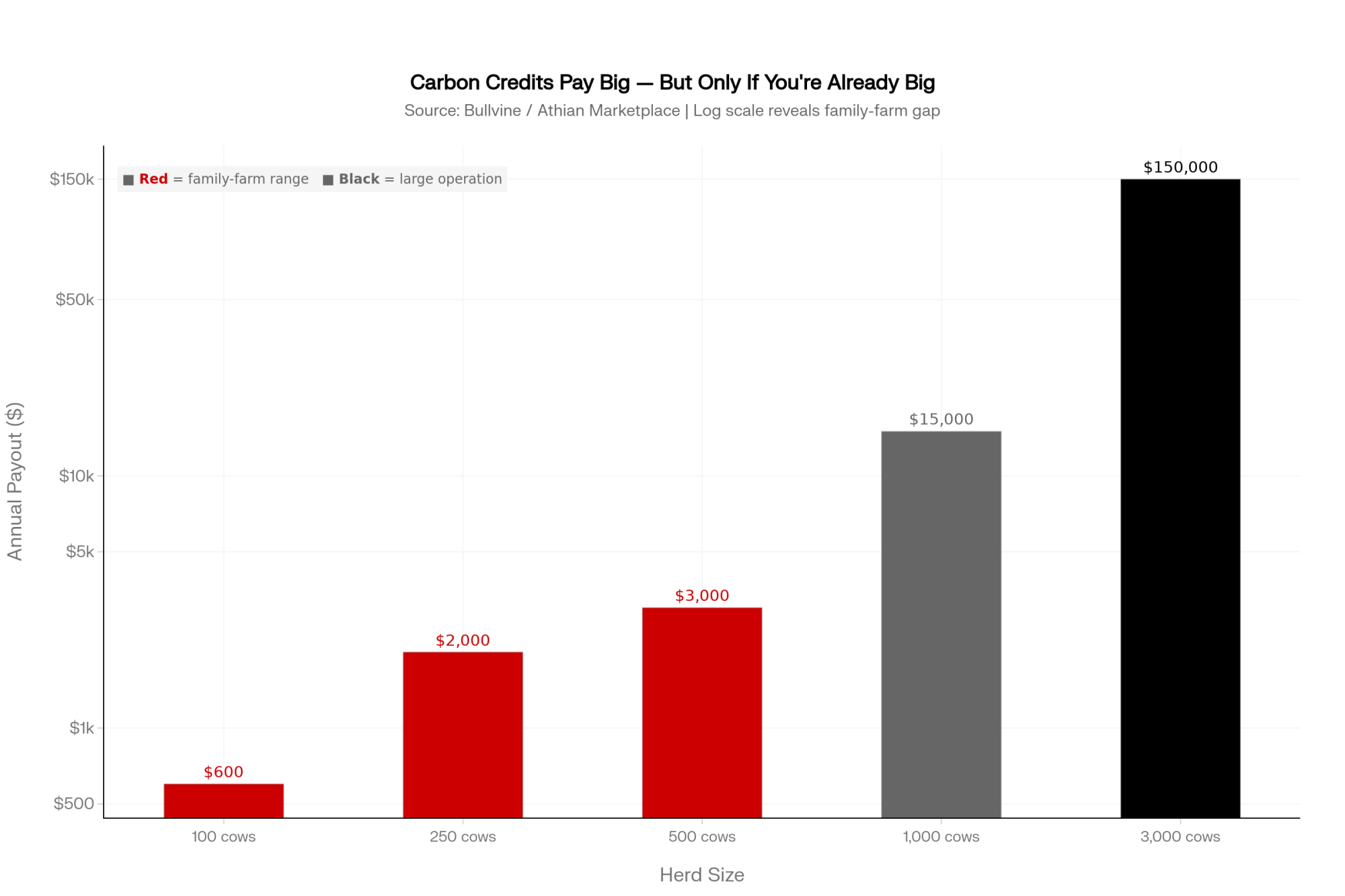

The fourth path is younger and worth watching: monetizing data and verified sustainability. Bullvine’s reporting found the Athian Marketplace has paid between $15 and $35 per metric ton of CO₂ equivalent for certified U.S. livestock emission reductions (The Bullvine, “Data That Pays,” Oct 22, 2025). It requires verification infrastructure and disciplined record-keeping. The catch is scale — payouts skew hard toward large operations, with 3,000-cow dairies capturing around $150,000 a year while family farms see closer to $3,000 (The Bullvine, Nov 23, 2025).

How Much Does “Buying Your Way In” Really Cost?

More than the slotting fees, honestly. The real cost is concentrated risk. When one family balance sheet backs both the farm and the new venture, a milk-price dip or a feed-cost spike hits both businesses on the same day. Bullvine’s robotic-milking case study describes the same shape of pain — Iowa State’s Larry Tranel found a typical two-robot install can run roughly $8,776 a year in the red for seven years before the payoff arrives (The Bullvine, “Robotic Milking Labor Math,” Apr 10, 2026). If your 500-cow herd hits a $1/cwt price drop in the middle of that valley, that’s another $125,000 you have to absorb. Thunder lived a beverage version of the same thing: two to three years before steady revenue, shelf space bought on borrowed patience. Before you chase any value-added play, the real question isn’t “can I make the product.” It’s “can my balance sheet survive the years before it pays.”

Is Your Operation Built to Capture Value, or to Produce It?

This is the shift worth sitting with, and it has nothing to do with coffee. Most dairies are built — financially and mentally — as commodity producers: fill the tank, ship the milk, take whatever price the system hands back. Temple and Henderson took the other route — a producer-owned brand that signs its own co-packer contracts and holds a piece of the story beyond the farm gate. You don’t need to launch canned coffee to make that shift. But it does mean asking, honestly, whether your operation is set up only to produce milk — or to capture some of what your milk becomes. Australian value-adding scholar Fiona Aveyard put it plainly in her 2023 Nuffield report: farmers “often have more control over their product than they realise” (Nuffield Australia, “Beyond the Farm Gate,” Aug 13, 2025).

Key Takeaways

- If your net runs below full economic cost — check your real number against the ERS large-herd benchmark near $19.14/cwt against an all-milk forecast around $20/cwt — you’re in the same squeeze pushing farmers toward value-added plays. Nail down your breakeven before you consider one.

- Before launching any branded product, model a two-to-three-year negative cash-flow window and stress-test whether your balance sheet absorbs it while milk prices swing.

- Too big a leap? This month, set aside half a day to audit hauling costs and your co-op’s product mix for the cents-per-cwt you’re leaving on the table.

- Name your outside-the-fence skills gap out loud. If you can’t spot what’s broken in marketing the way you can in the parlor, budget for the expertise you don’t have.

- Don’t over-engineer the product. Thunder’s clean, short-ingredient label came from building the simplest version that worked.

- Treat data and sustainability programs as a real but young value stream — and check where a herd your size actually lands, since a 3,000-cow dairy can bank roughly $150,000 while a 500-cow family farm might see around $3,000.

Where does your operation sit on that staircase right now — still shipping into the 15.9 cents, or reaching for a piece of the other 84? You don’t have to answer with a product launch. You do have to answer with your own numbers, because at an all-milk forecast around $20/cwt against $19.14 costs, ERS math says a lot of herds are running on a razor-thin full-cost margin.

Run Your Numbers

Dairy Profit Projector — Before you chase the other 84¢, find out if your core business even pencils. Drop in your herd size, milk price, and ration to see your breakeven milk price, IOFC, and 12-month margin — then stress-test what a $1/cwt swing does to your bottom line before you bet a second business on it.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- You Only Get 15.9¢ of the Food Dollar: A Dairy Farmer’s Playbook for Hauling, Co‑ops, and Premium Milk — Arms you with a concrete framework to evaluate alternative volume contracts, establishing a non-negotiable 15% to 20% net premium hurdle rate your farm must clear before shifting volume into niche processing channels.

- 25 extra miles is where your milk check starts bleeding — Exposes the hidden location and basis differentials in your contract, proving how a simple 25-mile re-route by your processor triggers a 1% hit to your gross revenue and eats up remaining operating margins.

- 1% Labor or $200,000 Debt: The Robotic Milking Bet That Could Make or Break Your Dairy — Delivers an unvarnished audit of capital diversification, revealing why a typical automation install runs $8,776 in the red annually for seven years and providing the structural survival metrics your balance sheet needs to withstand that valley.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.