Clark Farms operated a creamery for 6 years, serving dozens of accounts. They just shut it down—and kept milking. Here’s the math.

Executive Summary: Clark Farms, a fifth‑generation dairy in Delhi, NY, ran an on‑farm creamery for six years with dozens of local accounts, then shut the plant down in January 2026 while keeping the cows milking. Their numbers show what you’re really trading with on‑farm creamery economics: you’re not going from $1.85 milk to $5.50 milk, you’re buying roughly $1.15–$2.15 per gallon in extra margin at the cost of 70–90 more hours a week in processing and delivery on top of a full dairy workload. Backed by USDA, Rabobank, Cornell Dyson, and PASA data, the article walks through how consolidation, cost gaps, and thin processing margins make “just add a creamery” a much riskier survival plan than it looks on paper. It puts Clark’s pause alongside operations like MOO‑ville, Ronnybrook, and Hudson Valley Fresh that do make processing pay by staffing it as a true second business or sharing plants and brands across multiple herds, instead of piling everything onto one family. You also see how legacy, family bandwidth, and herd genetics change the risk math: a project that steals time from components, repro, and succession can quietly cost you more than it earns. The piece finishes with a clear playbook for your own decision—map out real weekly hours, set hard limits on account numbers and delivery time, build an off‑ramp before you pour concrete, and answer one non‑negotiable question: who’s actually milking while you’re bottling the milk?

A fifth‑generation New York dairy built a creamery with dozens of accounts, then hit pause in 2026—showing exactly how far the real numbers of on‑farm creamery economics can pull away from the brochure version.

If you’ve ever thought, “We should bottle our own milk,” this one’s for you. Clark Farms in Delhi, New York, did almost everything by the book—stainless, brand, accounts, community—and still chose to shut the creamery down while keeping the cows milking. That decision says a lot about survival, hours, and the actual premium left after processing and delivery.

The 2024–2026 Reality: Why On‑Farm Processing Looks Like a Lifeline

Let’s start with your world, not the grant brochure.

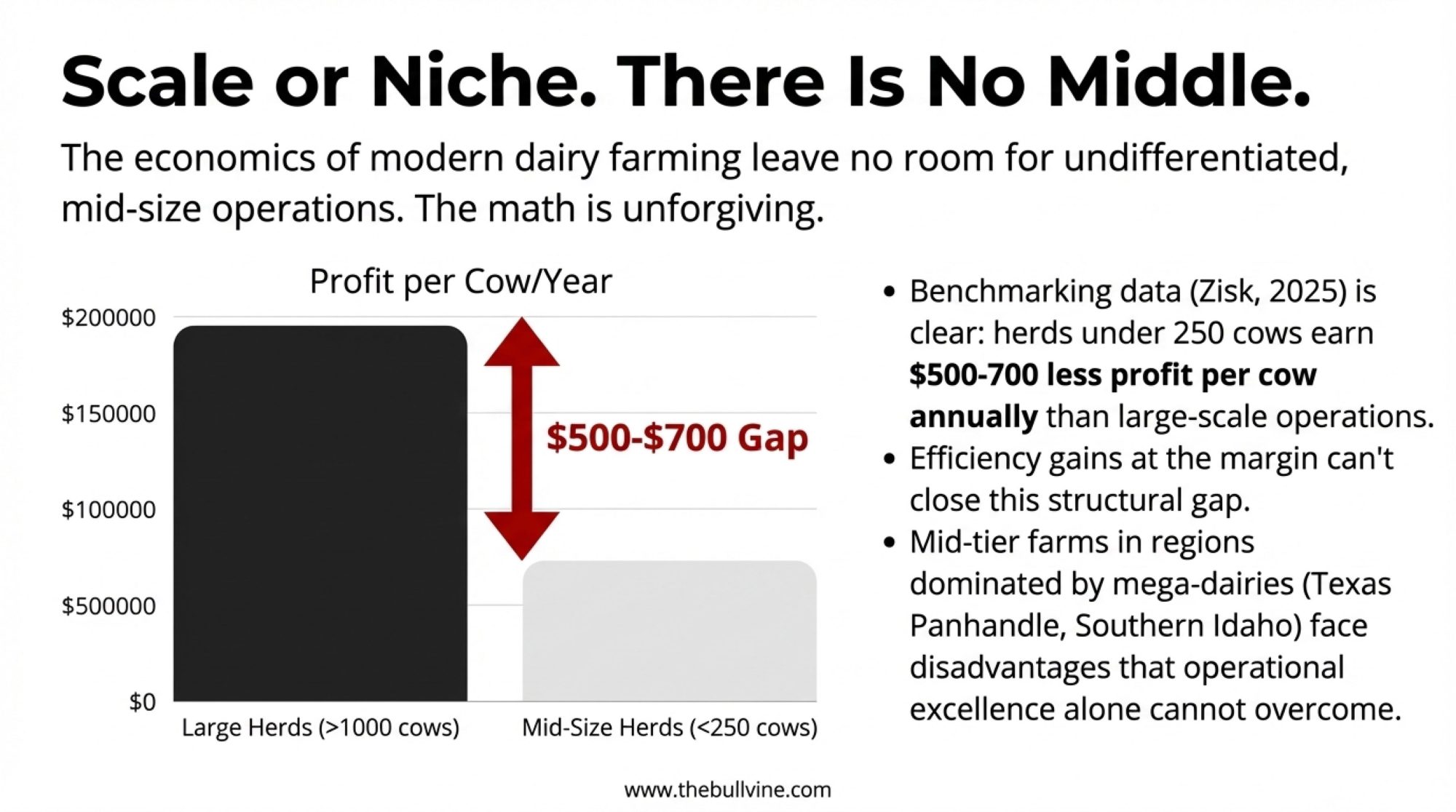

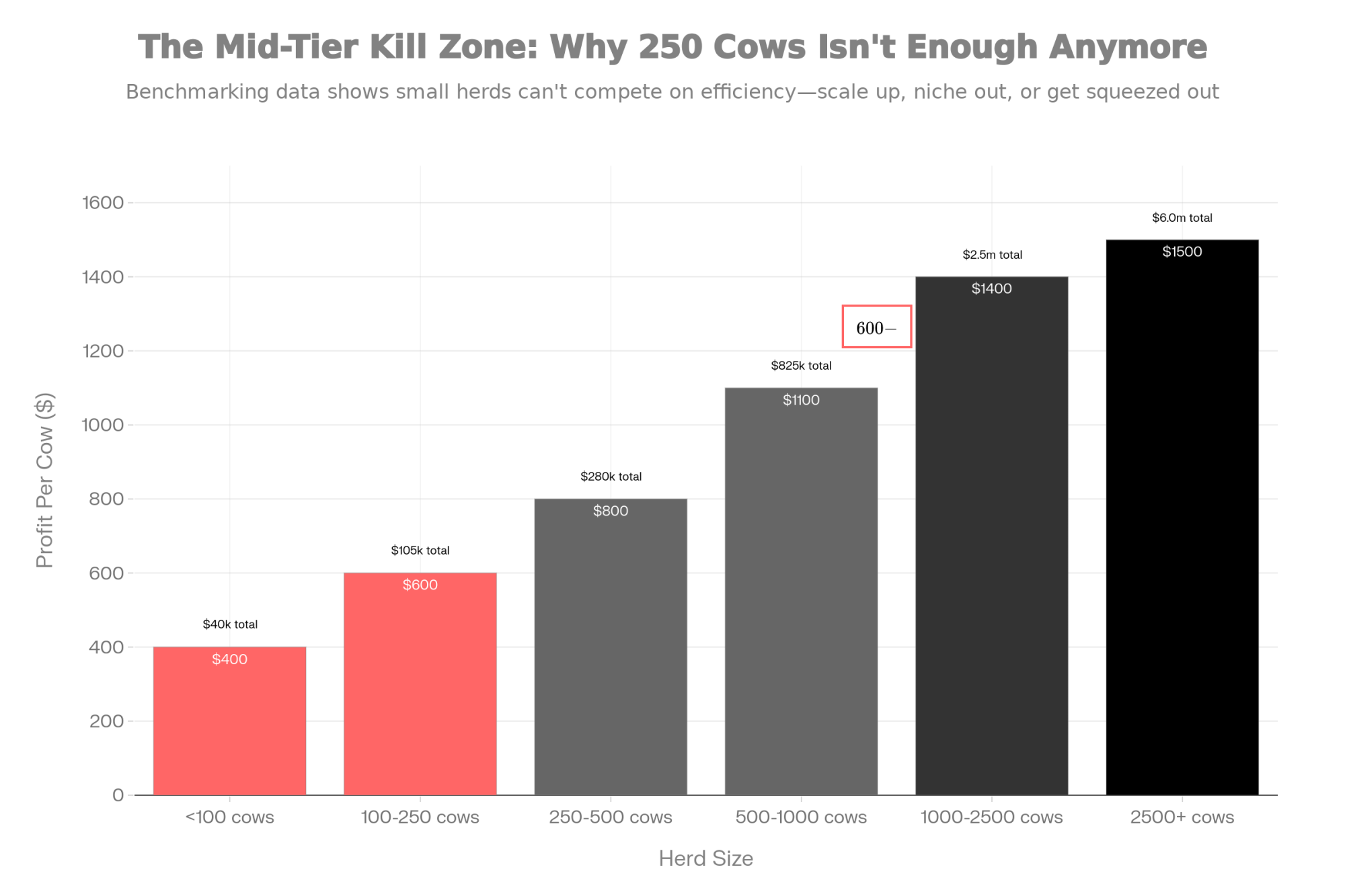

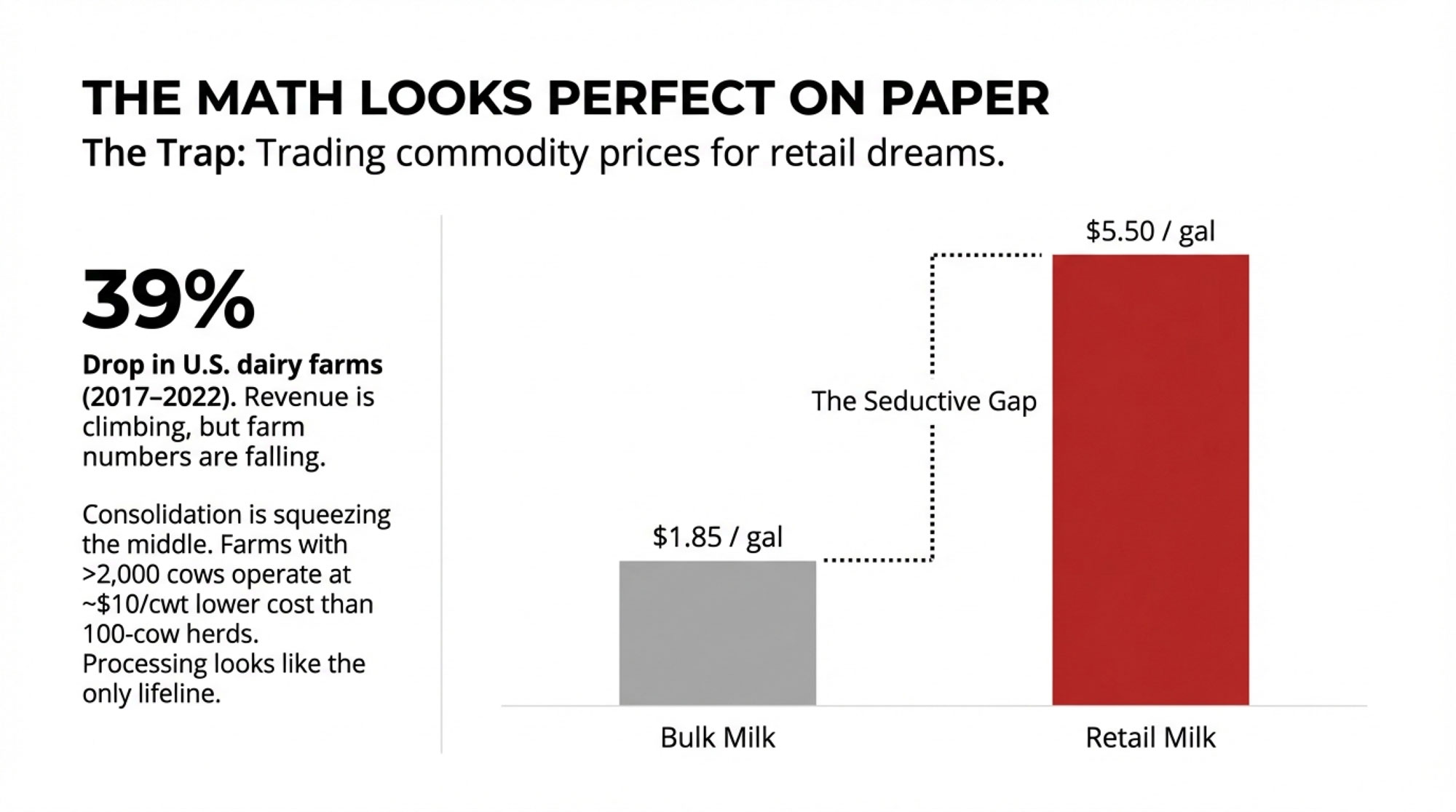

USDA’s 2022 Census of Agriculture dairy highlights show that the number of U.S. farms with milk sales from cowsfell from 40,336 in 2017 to 24,470 in 2022—a 39% drop in five years. Over that same period, the value of milk sales climbed 44%, from $36.7 billion to $52.8 billion, while the national herd sat around 9.3 million cows. Fewer farms. Similar cow numbers. More milk money is stacked on a smaller group of operations.

Rabobank analysis calculated that in 2022, farms with more than 1,000 cows produced about 67% of U.S. milk, up from 60% in 2017. Brownfield Ag News, quoting Rabobank’s Lucas Fuess, reported that farms milking more than 2,000 cows carried total costs around $23.06/cwt in 2022, roughly $10/cwt lower than typical costs on 100–199‑cow farms. In a market where Class III, Class IV, or all‑milk prices bounce in the high teens to low‑$20s, that cost gap is the line between breathing room and quietly wondering how much longer you can hang on.

In Delaware County, New York—Clark’s backyard—county plans and extension work describe a long slide in dairy farm numbers since the 1990s, leaving only a fraction of the former herds still milking. You don’t need a chart if you live there. You see it in empty barns and fewer bulk tanks meeting you on the road.

Against that backdrop, on‑farm processing looks like a lifeline. In recent months, New York’s all‑milk price has often sat in the high‑teens to low‑$20s per hundredweight; USDA pegged the New York all‑milk price at $21.40/cwt in November 2024, roughly $1.85 per gallon before hauling and pooling. Farmstead creamery case studies and Cornell‑linked reports show small processors selling branded fluid milk in the mid‑single‑digit dollars per gallon, several dollars above that effective blend value.

On paper, you’re trading $1.80 milk for $5‑plus milk. When the feed bill is chewing up your cheque, that’s a tempting trade.

Clark Farms took that road. Their experience shows you where the math—and the calendar—start to bite back.

Clark Farms: A Real‑World Test of the Dream

Clark didn’t just bolt a filler onto a corner of the milkhouse. They built a serious on‑farm creamery.

The farm sits on about 630 acres outside Delhi, New York, anchored by a barn Peter Clark built in 1907. A 2022 feature in Scribner Hollow describes it as a fifth‑generation dairy, already milking cows on that hill for about 114 years.

Kyle Clark picked up the processing bug while studying dairy business management at SUNY Morrisville. Scribner Hollow reports that he spent roughly four years digging into New York regulations, working through inspections, and hunting down used dairy‑grade stainless pasteurizers, tanks, and bottlers from all over the country before the creamery opened in 2020. That’s not a spur‑of‑the‑moment pivot. That’s a long, careful build.

By early 2022, the creamery was processing **about 25% of the farm’s milk—roughly 3,000 gallons a week—**with the remaining 75% still leaving on a tanker. That milk became bottled whole milk, flavored milks like chocolate and coffee, plus cream and butter under the Clark Farms Creamery label.

They didn’t just sell from the farm store:

- Their products moved through small groceries, cafés, and farm stands across the Catskills—Delhi, Andes, Phoenicia, Woodstock, and more.

- Cafés like Prospect and Fellow poured Clark milk into lattes and gelato and told that story to their own customers.

- Locals knew the Clark name when they opened a fridge door in town.

Demand wasn’t the snag. The cows were milking. The creamery was moving product.

On January 28, 2026, Clark Farms posted on Facebook that “after careful consideration,” they would be closing their creamery operations, while continuing to run the dairy farm. They wrote that “it has been a great joy to be able to produce dairy products for the community over the last six years,” thanked customers for their support, and admitted that keeping both the farm and the creamery to their standards had become too much. WBNG‑TV shared the news as “Clark Farms in Delaware County is closing its creamery doors after years of service,” and the comments quickly filled with people grabbing the last pints and thanking the family.

So the hard question isn’t “Why didn’t people support them?” It’s “What did the money and the hours really look like when they chose to stop?”

The Big Math: What You’re Actually Trading

Here’s where on‑farm creamery economics stops being a dream and turns into a decision.

The Revenue Side

Picture a herd in the Clark range: roughly 200 Holsteins in milk, in a system where cows can produce around 80 pounds per day. Once you factor in dry cows, heifers, and the fact that no week ever runs perfectly, you’re in the ballpark of 9,000–10,000 gallons of milk per week for a solid 200‑cow Holstein herd in New York.

If every gallon went into the pool at an effective $1.85/gallon (using that $21.40/cwt November 2024 New York all‑milk price as a real example), you’re looking at roughly $16,650–$18,500 per week in milk cheques at that volume, before hauling and other deductions.

Now drop in the 25% processing share Scribner Hollow documented. In 2022, Clark was bottling about 3,000 gallons a week and shipping the rest as bulk. Say you can wholesale those 3,000 gallons at $5.50/gallon, right in the middle of what small on‑farm fluid and flavored milks often fetch locally.

On a typical week, the rough revenue picture looks like:

- Bulk milk: 6,000–7,000 gallons × $1.85 ≈ $11,100–$12,950.

- Creamery: 3,000 gallons × $5.50 = $16,500.

Total: about $27,600–$29,450/week, versus $16,650–$18,500/week if every gallon went bulk at $1.85. On gross, that 25% slice looks like $9,000–$12,800 in additional cash flowing through the business.

That’s the number you hear in most creamery seminars. Now we get honest about what’s left after costs.

The Cost Side

Cornell’s Dyson School looked at 27 value‑added dairy businesses in New York, Vermont, and Wisconsin and didn’t sugar‑coat it: value‑added processing “is not a panacea.” In that study, mean net income from processing was modest at best and often negative, and average returns per cwt of processed cow milk were about $90/cwt lower than full economic costs once you charged a fair wage for family labor and a return on investment. The top performers did well, but the average small plant wasn’t swimming in cash.

Farmstead creamery case studies from PASA and Penn State show direct processing costs (excluding milk) for small fluid plants often run about $1.00–$1.50 per gallon, once you add electricity, hot water, CIP chemicals, packaging, labels, maintenance, and required testing. That’s just to get a gallon into a bottle safely.

Distribution costs pile on. Those same case studies document delivery expenses—fuel, truck payments, insurance, repairs, and driver labor—adding another $0.50–$1.00 per gallon in many rural, small‑drop routes.

Now the comparison on a processed gallon looks more like this:

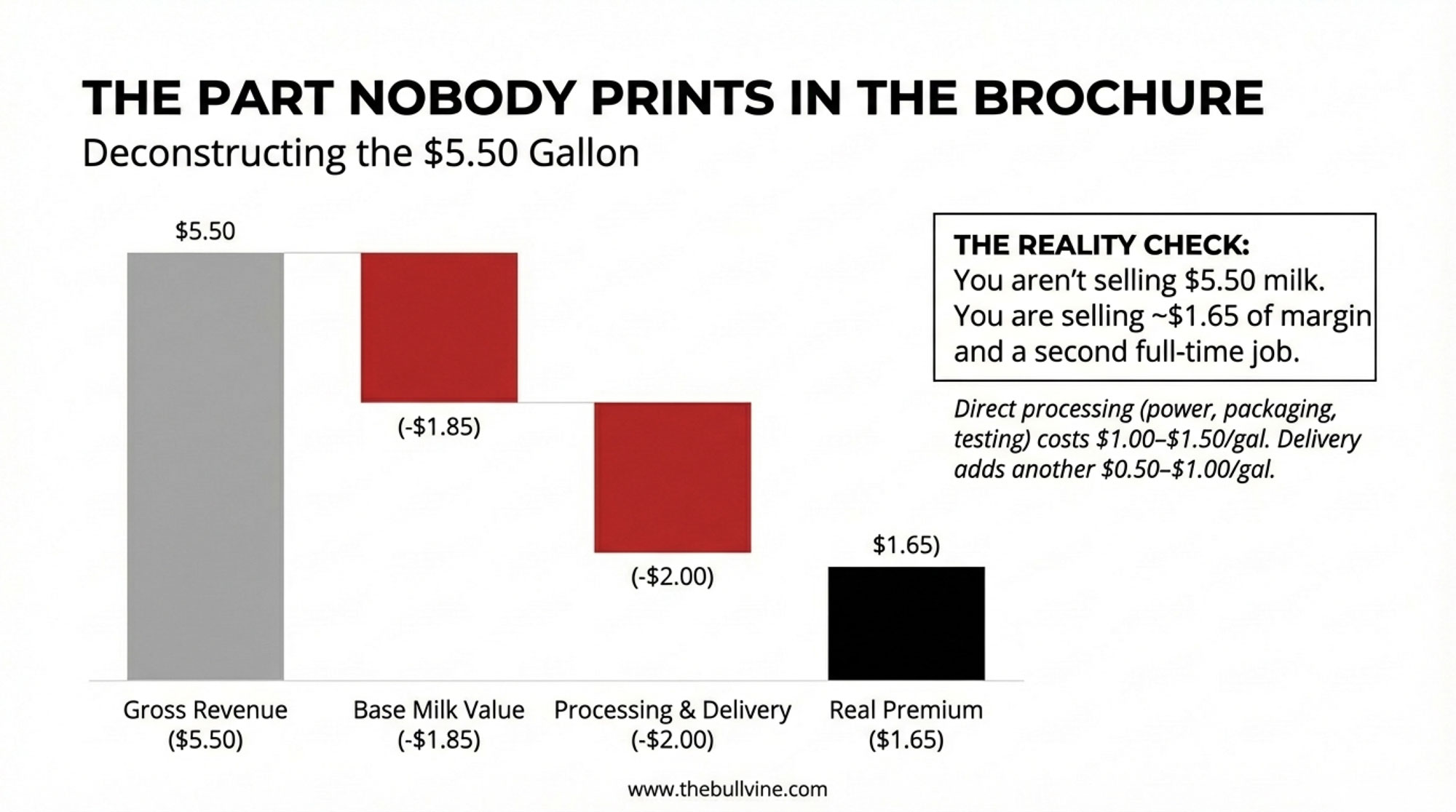

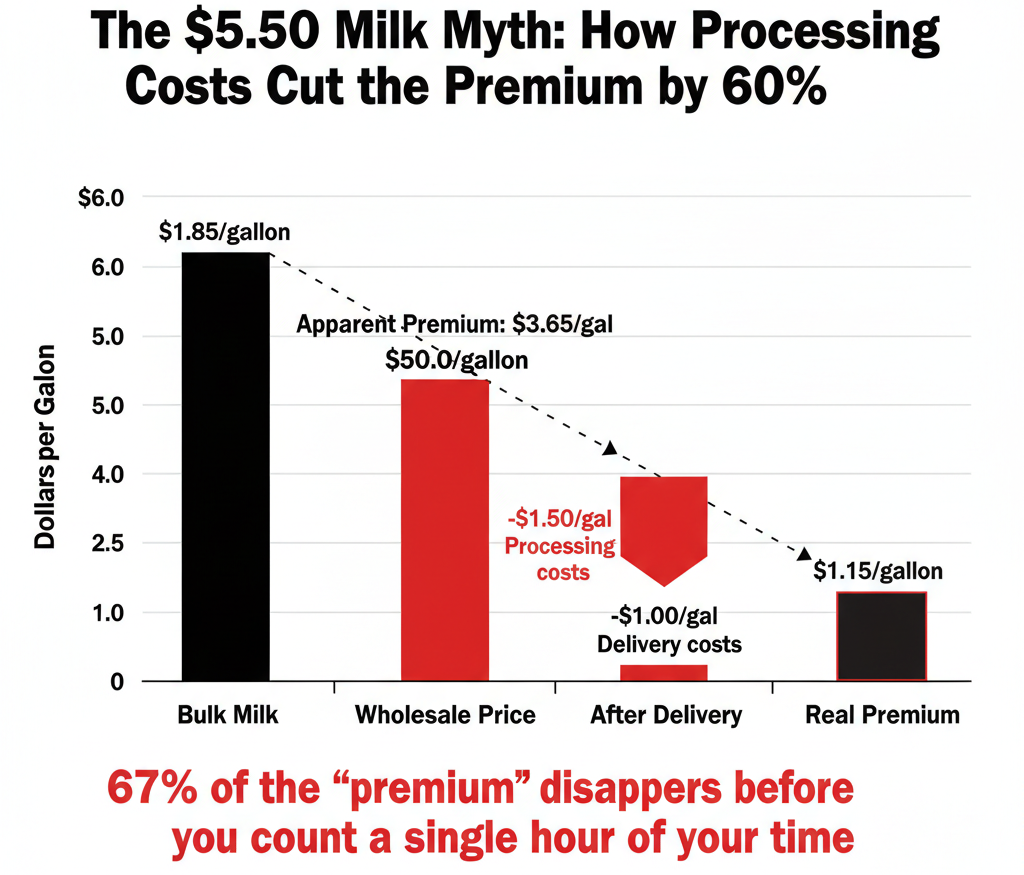

- Extra revenue over blend: $5.50 – $1.85 ≈ $3.65.

- Less processing + delivery: roughly $1.50–$2.50 per gallon combined.

That leaves a real premium of about $1.15–$2.15 per gallon before you pay yourself or cover downtime. On 3,000 gallons, you’re talking roughly $3,450–$6,450 per week more than sending that milk down the driveway.

Still serious money. But the “$5.50 instead of $1.85” story has already shrunk by more than half once stainless, cardboard, and diesel get their cut.

The Part Nobody Prints in the Brochure

For the days you’re reading this in the tractor cab, here’s the premium at a glance:

| The Metric | The “Brochure” Dream | The Clark‑Style Reality (Illustrative) |

| Gross revenue | $5.50/gal (wholesale price) | $5.50/gal |

| Base milk value | (Often ignored) | ($1.85/gal) |

| Processing & delivery | “Minimal” | ($1.50 – $2.50/gal) |

| Real premium | $3.65/gal | $1.15 – $2.15/gal |

| The “price” you pay | “Being your own boss.” | 70–90 extra hours/week |

You’re not really selling $5.50 milk. You’re selling about $1.50 of margin and a second full‑time job.

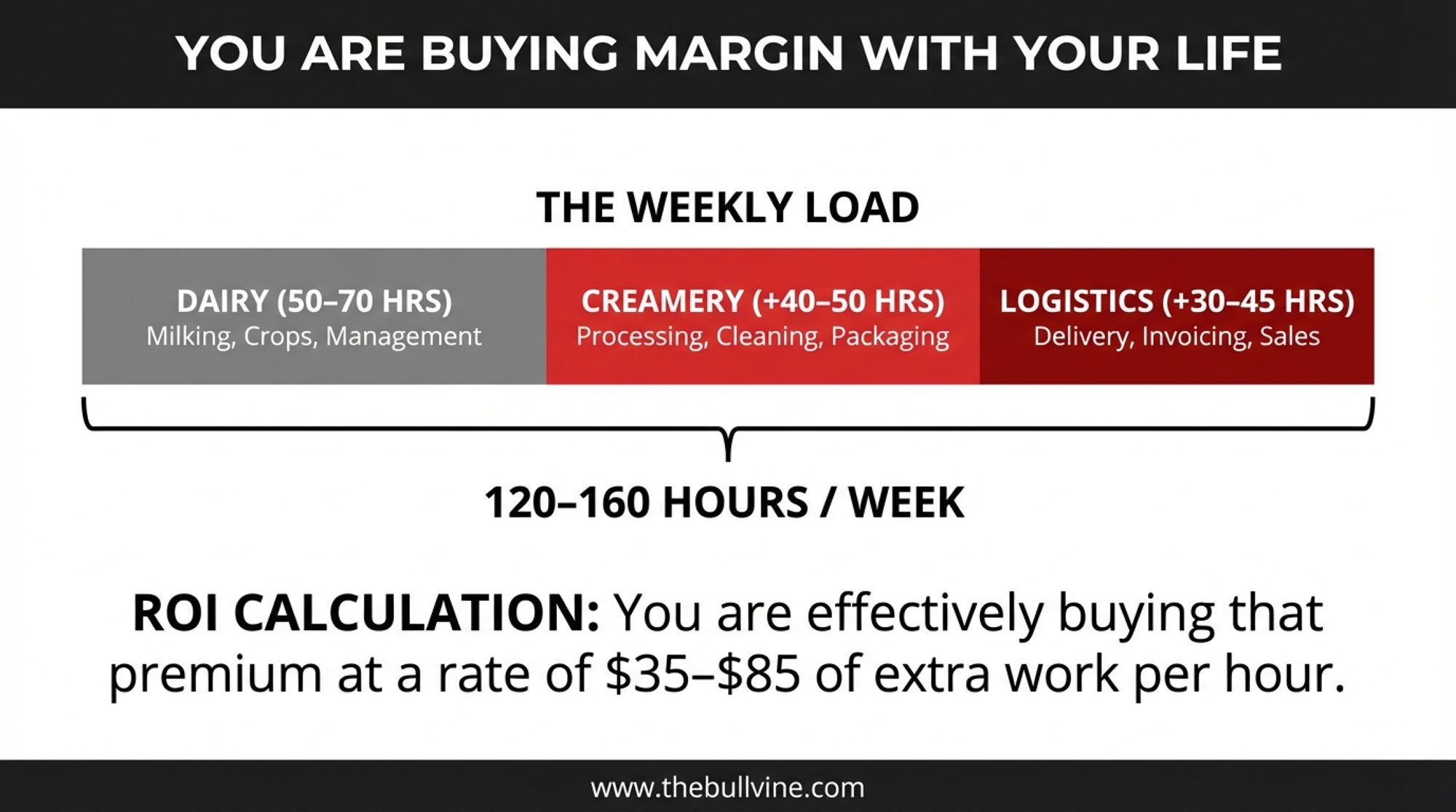

The Time Math: Buying Margin with Hours

Here’s where on‑farm creamery economics stops being just dollars and starts being bodies and weeks.

PASA/Penn State’s farmstead creamery report logs weekly labor for small plants that easily hits 40–60 hours of processing and packaging once volumes reach a few thousand gallons. Add full cleaning and sanitation—CIP cycles, scrubbing floors and drains—and you’re realistically looking at about 40–50 hours inside the plant on a 3,000‑gallon week.

Distribution and admin sit on top of that. For farms serving a couple of dozen accounts, those case studies show another 30–45 hours per week spent on ordering, route planning, loading, driving, stocking shelves, talking with store managers, invoicing, and chasing cheques.

Now remember what the dairy alone demands. Cornell’s long‑running dairy farm business work shows that a 200‑cow Holstein herd with crops, youngstock, maintenance, and paperwork can easily soak up 50–70 hours a week from your core people. You probably don’t need Cornell to tell you that—you feel it in your knees.

Put it together:

- Dairy: 50–70 hours.

- Creamery: 40–50 hours.

- Distribution/admin: 30–45 hours.

You’ve put in yourself well over 100 hours of work every week just to keep both sides upright. On a lot of family places, it feels like a 130‑ or 140‑hour week spread across three or four people, even if nobody ever writes it down.

| Work Category | Weekly Hours (Conservative) | Weekly Hours (Realistic) | Notes |

|---|---|---|---|

| Dairy Operations | 50 | 70 | Milking 2×, feeding, bedding, calves, breeding, maintenance, crop work |

| Creamery Processing | 40 | 50 | Pasteurizing, bottling, labeling, batch records, quality testing |

| Plant Cleaning & Sanitation | Included above | Included above | CIP cycles, floors, drains—often 8–10 hrs/week on its own |

| Distribution & Delivery | 20 | 35 | Route planning, loading, driving, unloading, stocking shelves |

| Admin & Sales | 10 | 15 | Invoicing, ordering, customer calls, chasing payments |

| Emergency/Downtime | 5 | 10 | Equipment breakdowns, inspector visits, surprise runs |

| TOTAL WEEKLY HOURS | 125 | 180 | Spread across 2–4 family members—still unsustainable |

| $ Premium per Extra Hour | $27–$49/hr | $36–$90/hr | Based on $3,000–$6,000/week margin ÷ 70–90 processing hours |

Now take that extra $3,000–$6,000/week and divide it by the 70–90 extra hours wrapped up in processing and delivery. You’re effectively buying that premium at roughly $35–$85 of extra work per hour. On a spreadsheet that can be edited with a pencil. In a family that already feels stretched, it’s a different conversation.

At some point, many family‑run creameries, Clark’s included, look at that trade‑off and decide it no longer fits their standards for product quality, family time, or herd care.

When On‑Farm Processing Really Works

This isn’t “never build a creamery.” It’s “be honest about what kind of creamery actually works.”

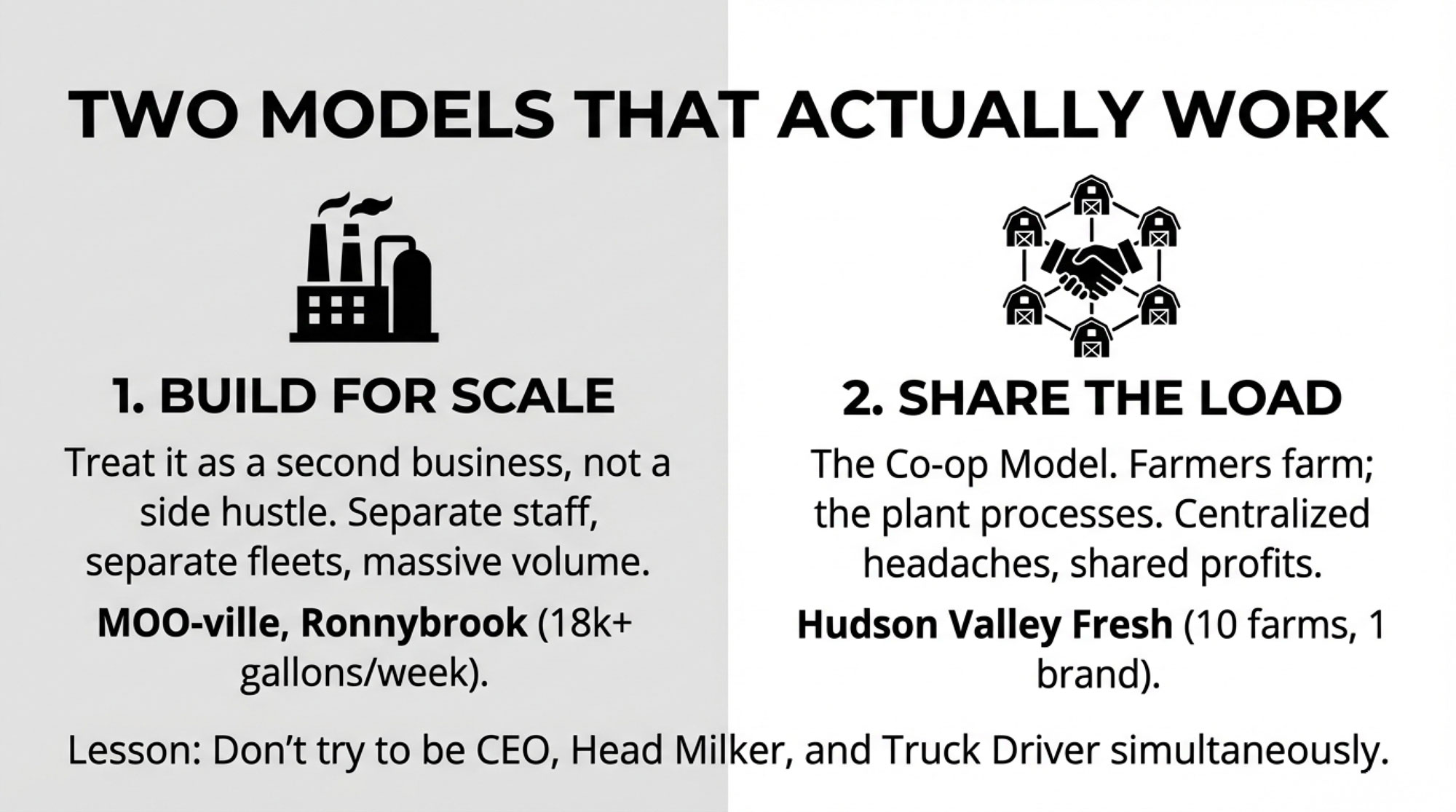

When You Build It for Scale

MOO‑ville Creamery & Westvale‑View Dairy (Nashville, Michigan). Doug and Louisa Westendorp started milking about 50 cows in 1992. When their six kids—including twins and triplets—wanted to stay on the farm, the family opened MOO‑ville Creamery in 2005 rather than chasing a multi‑thousand‑cow expansion. Today, Westvale‑View milks around 240 Holsteins, averaging over 100 pounds per cow per day, and MOO‑ville processes about 18,000 gallons of milk per week—roughly six times Clark’s processed volume. They’ve grown to four retail locations and products in over 140 retail stores and 50 ice cream shops. Their chocolate ice cream won first at the North American Ice Cream Association Conference in 2021, and vanilla followed in 2022. Every kid has a defined lane—herd, crops, ice cream, retail, tours—so nobody’s trying to juggle dairy, plant, and distribution alone.

Ronnybrook Farm Dairy (Pine Plains, New York). Ron and Rick Osofsky started bottling unhomogenized milk in glass bottles at their Hudson Valley farm in the early 1990s. Thirty years on, Ronnybrook employs about 50 staff, crops roughly 760 acres, and sends milk, yogurt, and butter from their herd to 13 New York City Greenmarkets plus supermarkets across the region. In 2023, Scenic Hudson and Columbia Land Conservancy permanently conserved the farm, calling Ronnybrook “a local icon.” They built glass bottles and direct distribution into the business model from day one and staffed accordingly.

In both cases, processing isn’t a side hustle tacked onto the dairy. It’s a second, fully staffed business.

| Operation | Gallons Processed/Week | Processing/Retail Staff (Approx.) | Herd Size | Outcome |

|---|---|---|---|---|

| Clark Farms | 3,000 | 2–3 (family) | ~200 cows | Paused 2026 |

| MOO-ville | 18,000 | 15–20+ | ~240 cows | Thriving, 4 retail locations |

| Ronnybrook | ~20,000+ | ~50 | Large herd + 760 acres | Regional icon, 30+ years |

When You Share the Load

Hudson Valley Fresh (Hudson Valley, NY). Instead of each farm building a plant, 10 family dairies pool their milk into a shared processing facility at Boice Brothers Dairy, a family‑run plant dating back to 1914. Member farms—Jersey, Holstein, Guernsey, Brown Swiss, Ayrshire—must meet tight quality standards: somatic cell counts under 200,000, and raw bacteria counts under 5,000. In return, Hudson Valley Fresh has historically paid a premium, as evidenced by $23/cwt vs. $16/cwt for the commodity, through a base price plus quarterly profit‑sharing. The brand is strong, the creamery is centralized, and no single farm has to own all the stainless and all the route headaches.

The pattern is pretty clear:

- Some farms make processing work by building enough scale and staffing to treat it as a true second business.

- Others make it work by sharing the plant and brand so their own time stays focused on cows and crops.

Clark’s situation—running a full dairy and a full processing/distribution business with essentially the same core people—is where a lot of smaller creameries stall out.

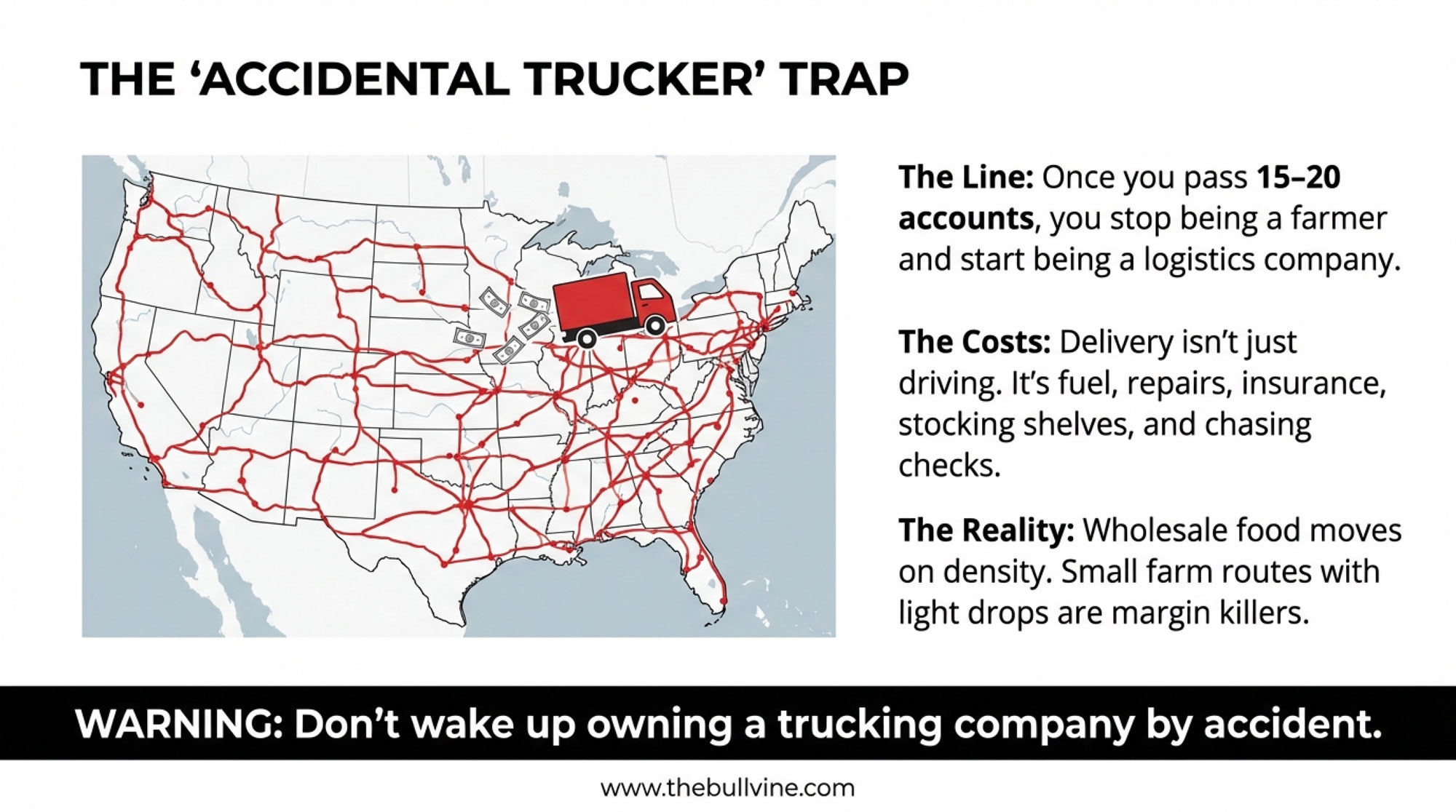

The Accidental Trucker: When Your Farm Becomes a Logistics Company

When you first picture an on‑farm creamery, you see stainless steel and glass bottles. When it actually starts to succeed, you see routes.

Wholesale food moves on trucks, not spreadsheets. Dairy plant and creamery closure coverage—like Hastings Creamery in Minnesota or Prairie Farms plant changes—regularly points to transportation, labor, and maintenance costs chewing up thin margins. Grocery distributors live on low‑teens gross margins and 1–3% net margins once trucks, fuel, drivers, insurance, and warehouses are paid. They make it work with dense routes and big drops at each stop.

A single‑farm creamery starts with none of that. You’re hauling your own product, on your own dime, to customers who might order heavy one week and light the next.

Somewhere between “a few good accounts” and “we deliver to everyone,” there’s a line. On one side, you’re still basically a farm that brings your own milk. Cross it, and you’ve become a logistics company that happens to own cows.

PASA’s case studies suggest that once you slide into the 15–20 account range, route planning, cooler space, and delivery windows start dictating your week more than milking times. With products in multiple groceries, cafés, and farm stands across the Catskills, Clark was clearly operating on that logistics side of the line.

There’s nothing wrong with that if it’s what you want. MOO‑ville runs multiple delivery trucks and has staff just for routes and retail. Ronnybrook built those NYC market runs into its identity from the start. But you want to choose to become a logistics business, not wake up in one by accident.

Why Clark Could Hit Pause and Keep Milking

Here’s a part of Clark’s story that deserves as much airtime as the shutdown: they could step off the creamery treadmill and keep the dairy running.

Look at a few structural choices they made:

- They never processed all their milk. In 2022, about 25% went through the plant, while the rest still shipped as bulk. When they shut the creamery, they had somewhere to send that milk.

- They leaned into used, movable stainless. Scribner Hollow describes Kyle sourcing used pasteurizers, tanks, and other equipment from all over, rather than pouring everything into custom, immovable installations. That kept sunk costs lower and resale or repurposing options open.

- They didn’t strap the entire farm to the plant’s fortunes. We don’t see their loan documents, but the fact that the dairy stayed standing tells you the creamery wasn’t financed in a way that automatically dragged land and cows down when they hit pause.

When WBNG shared the closure, locals piled into the comments talking about buying the last pints of milk and cream cheese and thanking the family for years of product. Another nearby business posted, “Sad news from our friends over at Clark’s farms! We’re wishing them the best and hoping to hear they re open in the future!” It read more like a community send‑off than a failure.

That’s what an off‑ramp looks like when you actually need it. You don’t build it because you’re aiming to quit. You build it because you respect your dairy enough not to let one project drag the whole place down if the numbers or the hours stop lining up.

Legacy Changes the Risk Math

None of that math happens in a vacuum. Legacy sits right in the middle of it.

If you’re first‑generation with no clear successor, a creamery can feel like one more business shot. If it doesn’t work, you sell what you can, pay who you can, and move on. Ugly, but simple.

On a five‑generation place like Clark’s, the stakes hit different.

That 1907 barn overlooking Delhi was built by Kyle’s great‑great‑grandfather. By the time Scribner Hollow profiled the farm in 2022, they were already 114 years into the family dairy story. When the creamery pause hit social media, locals weren’t piling on—they were saying “thank you” and wishing the family well.

Academics call it socioemotional wealth—all the non‑financial value tied up in keeping your farm in the family, protecting your name, and handing something real to the next generation. Put simply: how sick you’d feel being the one who lost the place.

If you’re in Kyle’s boots, you’re not just asking, “Does this creamery cash flow in 2025?” You’re also asking, “If this ever pulls the dairy down, am I the one who ends 100‑plus years of work on this hill?”

That question doesn’t show up on your cost‑of‑production sheet. But it does show up when you decide whether to grind through another year of 140‑hour weeks or step back and protect the core dairy. Clark chose to protect the dairy. A lot of Bullvine readers would, too.

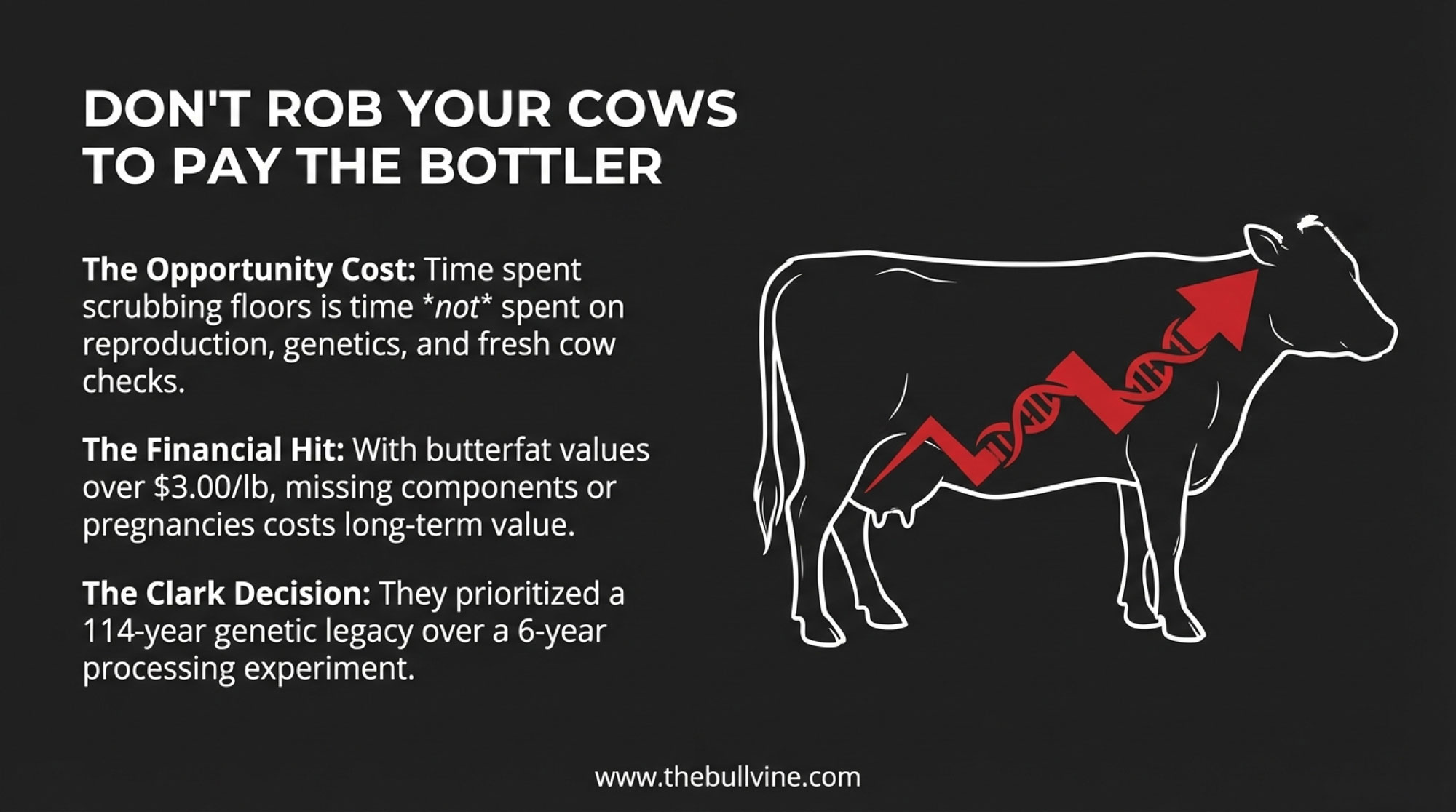

Don’t Forget the Herd: Genetics, Components, and Long‑Term Value

There’s another engine running through this story that’s easy to overlook when you’re staring at stainless: your herd.

If you’ve spent years breeding for Fat, Protein, fertility, and health, that’s not just hobby genetics. It’s a big piece of your risk and return.

- Milk cheques. In component‑priced systems, FMMO and co‑op schedules have been paying strong money for butterfat and Protein. When butterfat values in the Northeast climb above $3.00/lb, a herd running just a few tenths higher in components than the blend can easily see $2–$4/cwt more than average herds shipping the same volume. That shows up whether your milk goes into your own bottle or someone else’s cheese.

- Replacement pressure. Better fertility, health, and livability mean fewer heifers needed to maintain herd size. Analysts talking about the “processing gap” have also flagged tight heifer supplies and higher replacement prices, especially as more calves go beef‑on‑dairy. That makes every genomic and mating decision more expensive to mess up.

- Reputation and options. Strong cow families with performance and type give you options—embryos, breeding stock, bulls in AI, or simply better conversations with lenders and partners who know you’ve built something with resale value.

If a creamery forces you to rob time from fresh‑cow checks, repro, and data review, you’re not just putting this year’s processing margin at risk. You’re putting the next decade of herd progress at risk, too.

When Clark stepped away from the creamery while keeping the dairy, they didn’t just protect cash flow. They protected a herd and a genetic trajectory, they’ve built one generation at a time. If you’re serious about breeding and components, that needs to sit right beside any stainless quote you’re considering.

What This Means for Your Operation

Here’s where you stop looking at Delaware County and start looking at your own kitchen table.

1. Start with the One Question You Can’t Dodge

Before you chase a grant or sign a creamery loan, ask this out loud:

Who will milk the cows while I’m bottling the milk?

If your answer is “We’ll just work harder” or “We’ll figure it out,” you don’t have a plan. You’ve got a hope.

A real answer sounds like:

“I’ll run the plant from 9 to 3, my parents stay on both milkings for now, we hire a part‑time milker for two evenings, and if someone’s sick, we cancel one processing day and roll that product into the next run.”

If you can’t write down that level of detail—with names, hours, and backups—you’re not ready to buy stainless. You’re ready to go back to the whiteboard.

| Factor | Bulk Milk (No Processing) | On-Farm Creamery (25% Processed) |

|---|---|---|

| Revenue per gallon | $1.85 (blend/pool price) | $1.85 (bulk) + $5.50 (processed, 25% of volume) |

| Net margin per processed gallon | n/a | $1.15–$2.15 (after processing + delivery costs) |

| Extra weekly margin (3,000 gal) | $0 | $3,450–$6,450 |

| Weekly labor (family) | 50–70 hours (dairy only) | 120–160 hours (dairy + plant + delivery) |

| Effective hourly rate for extra work | n/a | $35–$85/hour (before equipment ROI) |

| Capital investment | Minimal (routine dairy equipment) | $150,000–$500,000+ (plant, truck, cold storage) |

| Flexibility to scale down | High—adjust herd size, cull strategically | Low—fixed plant overhead, route commitments, debt service |

| Risk to core dairy | Low—focus stays on cows and crops | High—time/capital diverted; plant failure can drag dairy down |

| Exit options if stressed | Steady—co-op/processor always needs milk | Limited—selling used stainless at discount, breaking customer commitments |

| Best fit for… | Farms prioritizing herd genetics, land base, simplicity, or nearing succession | Farms with committed next-gen, dedicated staff, dense local market, long runway |

2. Put Your Week on Paper

Do this with the people who’ll actually be working it.

- List every dairy job you do now with honest hours: milking, scraping, feed mixing, bedding, calves, breeding decisions, cropping, breakdowns, and paperwork.

- List every processing job you’re adding: receiving, batching, pasteurizing, cooling, bottling, labeling, stacking, cleaning, swabbing, record‑keeping, and inspector visits.

- List every distribution job: loading, driving, unloading, stocking, talking with buyers, invoicing, chasing cheques.

Add up those hours against the people you actually have—not the extra hire you “hope” will show up. If your plan needs any core person over 60–65 hours/week beyond a short start‑up push, be honest: you’re designing a burnout schedule, not a sustainable business.

3. Decide When You’re Willing to Become a Logistics Business

Draw this line before you start adding accounts.

Write down:

- The maximum number of wholesale accounts you’ll serve before you cost out a dedicated driver or route person—maybe that’s 12, maybe 18, but write a number.

- The minimum drop size that makes a stop worth it—how many cases have to come off the truck to justify the fuel and time.

- Which types of accounts you’re willing to walk away from if your route starts looking like spaghetti and you’re spending more time behind a café than behind a cow.

If you don’t set those rules now, your route will quietly run you.

4. Build the Off‑Ramp While You’re Pouring Concrete

If you go ahead, don’t wait until you’re exhausted to think about exit options.

- Keep your co‑op or processor relationship alive, even if you’re shipping less. You want a place to send milk if you need to dial the creamery back.

- Work with your accountant and lender, so the creamery debt doesn’t automatically drag land and cows into the fire if the plant has a bad year.

- Favor used or modular stainless steel, you could realistically sell if you change course.

- Set “stop rules” now: for example, “If after three years the creamery isn’t generating at least $X/month in net cash and our average weekly hours are still above Y, we pause and reassess.” Adjust X and Y to your reality—but don’t ignore them later.

5. Check Processing Against Your Herd Strategy

Your creamery plan shouldn’t be in a separate binder from your breeding plan. It should sit on top of it.

Ask yourself:

- “Does this creamery help us capture more value from the components and health traits we’ve been selecting for, or does it risk pulling attention away from managing them?”

- “If cash gets tight, do we cut repro and replacement investment first, or do we slow down creamery expansion and marketing?”

If the honest answer is “we’d sacrifice herd investment to keep the plant going,” you’re trading long‑term herd value for short‑term plant cashflow. That might be the right call in a specific situation. Just make sure it’s a conscious choice, not something you stumble into.

Key Takeaways

- The on‑farm creamery premium is real—but it isn’t free. Processing a 25% slice of your milk might add several thousand dollars a week in margin, but you usually buy it with 70–90 extra hours of processing and delivery piled on top of a full dairy week.

- Once you’re past roughly 15–20 accounts, you’re running a logistics business. At that point, route density, drop size, and store delivery windows matter as much as butterfat tests.

- The farms that make processing work long‑term add people, not just stainless. MOO‑ville, Ronnybrook, and Hudson Valley Fresh all spread the load across family, staff, or co‑ops instead of forcing one family to carry everything.

- A well‑built off‑ramp is a form of insurance. Clark Farms could pause the creamery and keep milking because they never welded the farm’s survival to the plant’s success.

- Your herd and land are still the backbone. A strong Holstein herd on owned ground will outlast any value‑added project that only works if you live a 143‑hour week.

- The right time to discover your breaking point is on paper—not at 11 p.m. in the plant. If your creamery plan only works with everyone running at 110% forever, it doesn’t actually work.

- The first real due‑diligence question is simple. “Who will milk the cows while I’m bottling the milk?” If you can’t answer that clearly, you’ve already learned something important from Clark Farms’ experience.

The Bottom Line

Clark Farms didn’t fail at diversification. They ran a full‑scale, real‑world trial of on‑farm processing under today’s economics, then listened when the premium and the hours stopped lining up. They made the hard call to protect the dairy that’s been there since 1907, honour their family’s work, and leave the door open for whatever comes next.

If you’re weighing a creamery of your own—or you’re already living a week that feels a little too close to 143 hours—the real question isn’t just “Can this make money?” It’s “What does this do to our time, our cows, and our ability to hand something solid to whoever comes next?”

That’s the answer you want in hand before the stainless rolls into your yard.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Arm your operation with a cold-eyed look at the $250,000 margin gap threatening mid-size dairies today. It delivers a tactical 90-day liquidity plan and exposes why calculating your $17 milk breakeven is Monday’s top priority.

- Beyond Efficiency: Three Dairy Models Built to Survive $14 Milk in 2026 – Gain a strategic roadmap for the “end of the middle” by identifying which structural model fits your region. It reveals the long-term positioning required to survive $14 milk and helps you choose between scale or branding.

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – Secure a competitive advantage by exposing how beef-on-dairy premiums are masking structural unprofitability. It breaks down the disruptive “27:100” heifer ratio and reveals why breeding for protein is the key to outlasting the 2026 reset.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.