The official start of spring is right around the corner and milk volumes are responding accordingly. Output is steady to higher in most parts of the country as the spring flush rolls in.

The official start of spring is right around the corner and milk volumes are responding accordingly. Output is steady to higher in most parts of the country as the spring flush rolls in. Bouts of extreme weather have popped up across the nation and are challenging the production and transportation of milk. Producers in parts of the northeast are digging themselves out from under several feet of snow while those in California slog through seemingly unending rain. Flooding is causing cow comfort and animal health concerns and, in the most severe cases, is forcing producers to evacuate their herds to higher ground. With more rain expected to fall, fears are mounting that critical infrastructure such as levees will fail, further exacerbating the situation. While increased precipitation has helped to refill reservoirs and could provide some relief to California’s water crisis, for the moment attention is focused on dealing with the immediate impacts of the flooding.

The official start of spring is right around the corner and milk volumes are responding accordingly. Output is steady to higher in most parts of the country as the spring flush rolls in. Bouts of extreme weather have popped up across the nation and are challenging the production and transportation of milk. Producers in parts of the northeast are digging themselves out from under several feet of snow while those in California slog through seemingly unending rain. Flooding is causing cow comfort and animal health concerns and, in the most severe cases, is forcing producers to evacuate their herds to higher ground. With more rain expected to fall, fears are mounting that critical infrastructure such as levees will fail, further exacerbating the situation. While increased precipitation has helped to refill reservoirs and could provide some relief to California’s water crisis, for the moment attention is focused on dealing with the immediate impacts of the flooding.

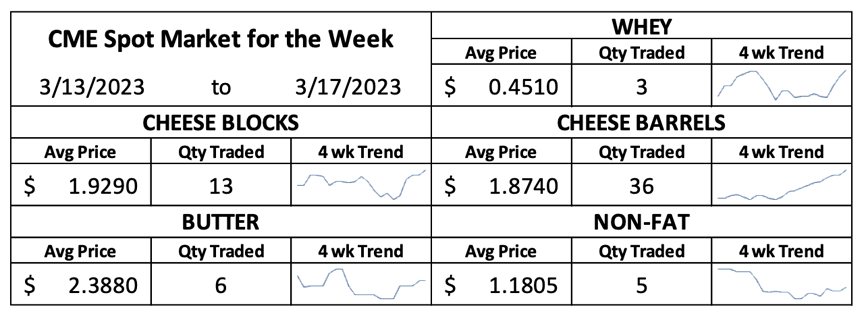

As students excitedly look forward to their spring breaks, demand from bottlers has softened. This has freed up even more milk for manufacturing uses, which was already oversubscribed. Balancing operations are stepping up milk intake where possible, but they remain constrained by a variety of factors including labor complications. As a result, spot milk can be obtained at extreme discounts. Dairy Market News once again reported that in the Central region, spot milk can be picked up for as little as $12 under Class III pricing. Meanwhile, milk futures followed the commodity markets upward this week. On Friday, every 2023 Class III contract except MAR23 and MAY23 settled above $19/cwt. Nearby Class IV contracts fell slightly over the course of the week.

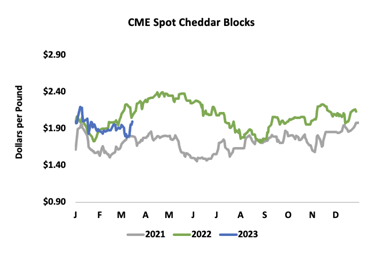

The spot market found surprising traction this week as every commodity ended Friday’s trade at a higher price than at the end of Monday’s session. The Cheddar markets, in particular, vaulted higher. Except for a .75¢ decline on Thursday, Cheddar blocks saw the price move upward each day, including a 11.5¢ leap on Tuesday. Ultimately, blocks ended the week at $1.9975/lb., an increase of 21.75¢ compared to last Friday’s close. Not to be left behind, barrels staged their own comeback this week, including a 7.25¢ jump on Friday as 16 loads traded hangs. Barrels ended the week at $1.96/lb., an increase of 19¢ compared to last week and bringing the block-barrel spread to 3.75¢.

With cheap milk readily available, cheese vats have been full across the country. Market participants indicate that inventories have been steady. Even so, demand appears to be strong enough to at least provide some lift to Cheddar prices, as witnessed in the market this week. Demand from both retail and foodservice channels has been perky with demand for barrels especially pronounced. The pull from the export market has been mixed as some traders report keen interest from global buyers while others emphasize that U.S. product has lost competitiveness compared to other international sources.

The spot dry whey market gave up a quarter of a cent on each Monday and Tuesday before more than compensating with a 1.25¢ and 1¢ gain on Wednesday and Thursday, respectively. After remaining unchanged on Friday the market closed out the week at 46¢ per pound, an increase of 1.75¢ compared to last Friday. Heavy cheese production has kept a steady whey stream available for processors. Price signals are pulling the whey stream toward the production of dry whey at the expense of higher protein products. Even so, demand is reportedly mixed. While interest has improved from some international buyers, product from alternative supply regions, especially Europe, is very competitively priced.

Cream availability varies across the country. In the Western states cream supplies remain long while Dairy Market News reports that the market is significantly tighter in the Eastern states. Despite the regional differences, the overarching message is that churns continue to run busy schedules. Butter inventories are healthy and some of the butter being produced today is being immediately frozen for later use. With the spring holidays rapidly approaching, demand for butter and other Class II products has increased considerably which should keep tension in the markets in the coming weeks.

The spot butter market rose in fits and starts this week. After kicking off the week with a 4.75¢ increase on Monday, the spot price remained unchanged on Tuesday and Wednesday. Another two penny increase on Thursday lifted the price to $2.40/lb. where it remained during Friday’s session. A total of six loads of butter traded hands during the week.

On the other side of the Class IV complex, market movements were more mixed. The spot nonfat dry milk (NDM) price kicked off the week with a half penny loss on Monday, followed by another dip on Wednesday. These declines were countered by a 1.5¢ gain on Tuesday and another .75¢ increase on Friday. When the dust settled, the NDM market ended the week at $1.1875/lb., up 1.25¢ compared to last Friday. Ample milk supplies are keeping dryers working hard and supplies are reported to be readily available. Meanwhile, demand is mixed on both the international and domestic fronts. Mexican buyers appear intermittently while some domestic buyers are swapping NDM out for WPC34 as prices in that market fall.

Elevated feed prices seem poised to continue negatively impacting producer profitability. The corn markets rose this week with the MAY23 contract settling on Friday at $6.3450/bu. Concerns about global supplies persist, especially given intensifying heat and drought in Argentina. Meanwhile soybean meal prices slipped with the MAY23 contract settling on Friday at $466/ton. In USDA’s North American Grain and Oilseed Crushing Summary published on Monday, the agency estimated that U.S. soybean crushing was up 2.6% in 2022 to 65.856 million tons.

Original Report At: https://www.jacoby.com/market-report/the-spring-flush-rolls-in/

{kind=link}