Tariffs are reshaping dairy demand—discover which products thrive or die in the trade war crossfire.

EXECUTIVE SUMMARY:

Tariffs are fracturing global dairy markets, with butterfat exports surging due to global shortages while whey and lactose face collapse from Chinese retaliation. The U.S.-China trade war triggered a $6B profit loss for dairy farmers, exposing vulnerabilities in export-dependent sectors. Price elasticity dictates outcomes: butter’s global price gap buffers tariffs, but high-elasticity products like cheese face demand destruction. Retaliatory measures and TRQ administration amplify risks, forcing farmers to diversify markets, differentiate products, or risk consolidation. Adaptation isn’t optional—it’s survival.

KEY TAKEAWAYS:

- Whey/lactose demand has cratered (23% prices) due to China’s 125% tariffs, with no quick fixes for glutted markets.

- Butter exports defy tariffs, up 224% YoY, fueled by a $1.10/lb global price gap—proof fundamentals trump politics.

- Retaliation risks outweigh protection: Losing China’s market took years; regaining it may be impossible amid shifting global supply chains.

- Diversify or die: Farms reliant on single products/markets face extinction; value-added dairy and Southeast Asia exports offer lifelines.

- TRQ loopholes matter: Canada’s “processor-only” quotas show nominal trade access ≠ to real market share—read the fine print.

The global dairy market is facing unprecedented disruption as tariff battles escalate. While politicians claim to protect domestic industries, the reality for dairy farmers is far more complex – and potentially devastating. This analysis cuts through the political BS to reveal how tariffs are reshaping dairy demand patterns, creating unexpected winners and losers, and why your operation needs to prepare now for the ripple effects that could make or break your future.

The Tariff Time Bomb: Dairy’s New Reality

The first quarter of 2025 has unleashed a perfect storm of trade tensions fundamentally reshaping global dairy markets. What began as modest tariff posturing has morphed into potentially market-destroying trade barriers threatening to upend decades of established trade relationships.

Let’s be brutally honest about where we stand: The escalation has been breathtaking in speed and scope. On February 4, the US reinstated a 10% tariff on Chinese imports. By March 4, this jumped to 20%. China wasted no time responding, slapping 10% retaliatory tariffs on US dairy products by March 10. Then came the hammer blow – on April 3, the US imposed an additional 34% tariff on Chinese imports, prompting China to retaliate with an 84% tariff on US goods, later increasing to a staggering 125%.

And this isn’t just a US-China problem. The US has simultaneously imposed 25% tariffs on imports from Mexico and Canada – two of our most critical dairy trading partners. Despite a 90-day pause on some global tariffs, the restrictions affecting America’s three largest dairy export markets remain firmly in place.

The consequences? Analysts project these combined tariffs could inflict a billion loss in profit for dairy farmers over the next four years. For context, previous retaliatory tariffs from China alone resulted in approximately .6 billion in lost revenues for US dairy farms from 2019 to 2021.

Are you paying attention yet? This trade war is about to hit your milk check-in ways.

Why Tariffs Hit Dairy Differently: The Economics You Need to Understand

To protect your operation, understand how tariffs fundamentally reshape dairy economics. Tariffs aren’t just political tools – they’re taxes on imported products that increase their effective price to importers and consumers.

The Price Elasticity Factor

The demand response to tariff-induced price increases varies dramatically across dairy products due to differences in price elasticity. This isn’t theoretical – it directly impacts which products face demand collapse and which might weather the storm:

- Fluid Milk: Often shows inelastic demand, particularly for conventional milk – much like how your high-producing Holsteins keep pumping regardless of minor management changes

- Specialty Cheeses: Demonstrate significantly higher price elasticity (around -1.73 for natural cheese) – think of how quickly your heifers respond to even small changes in their ration

- Butter: Research shows mixed elasticity, with some studies finding highly elastic demand (-1.87) – like how butterfat responds dramatically to even minor feed adjustments

- Yogurt: Generally elastic demand across product types – comparable to how quickly somatic cell counts can spike with even minor lapses in milking hygiene

- Dairy Ingredients: Whey and lactose show highly elastic derived demand from food manufacturers – like how quickly your milk truck will pass by if you miss quality parameters by even a small margin

This elasticity differential explains why certain products experience more dramatic demand destruction when hit with tariffs. The proliferation of plant-based alternatives has further increased the elasticity of traditional dairy products, making them more vulnerable to tariff impacts than in previous decades.

The Substitution Myth

Politicians love to claim tariffs will simply shift demand to domestic producers. The reality? That’s complete bullshit. This substitution is neither automatic nor complete:

- Effectiveness depends on whether domestic products match the quality and characteristics of imports – just like how you can’t simply swap a high-genetic-merit Holstein for a commercial Jersey and expect the same components

- If imported products possess unique attributes not easily replicated domestically, substitution may be limited – like how no amount of TMR adjustments can make up for poor-quality forage

- The domestic industry must have sufficient capacity and competitive cost structures to capitalize on the opportunity – just as your parlor throughput can’t suddenly double without significant infrastructure investment

When was the last time you saw politicians understand how dairy markets work? These are the same people who can’t tell the difference between a Holstein and an Angus.

The Product Battlefield: Winners and Losers in the Tariff War

The dairy portfolio is experiencing wildly divergent tariff impacts, with some products flourishing despite trade barriers while others face devastating demand destruction.

Whey and Lactose: The Casualties

The impact on whey and lactose markets has been particularly severe:

- US exports of these products to China have plummeted as tariffs escalated

- Dry whey prices crashed 23% between February and April 2025

- Lactose prices fell 21% during the same period

- China represents 42% of US whey exports and 43% of US lactose exports

- Inventories of these products have ballooned by 57% as export channels close

The magnitude of this demand destruction stems from China’s dominant position in these markets and the products’ high price elasticity. The outlook for producers heavily invested in these products is grim unless alternative markets can be developed rapidly.

Butter: The Surprising Survivor

In stark contrast to whey markets, butter demand shows remarkable resilience despite the tariff environment:

- Global butter supply shortages have driven up international prices substantially

- European Union butter prices have surged 47% compared to 2023

- The average Global Dairy Trade auction price for butter reached $3.45 per pound in recent trading

- US butter prices ($2.3475/lb as of April 11) sit well below international levels

- This price gap provides a substantial buffer against tariff impacts

US butterfat exports increased dramatically by 224.5% in February 2025 compared to the previous year, totaling 8,642 metric tons—the largest monthly export volume since April 2014. This growth persists despite the challenging tariff environment precisely because the global price premium exceeds the tariff costs for many markets.

Cheese: The Mixed Bag

Cheese markets demonstrate a nuanced response to tariffs:

- Mexican retaliatory tariffs (20-25%) in 2018-2019 reduced US cheese exports by about 12%

- However, recent data shows US dairy exports to Mexico rose 8% in value terms in February 2025

- Canada has included cheese among products subject to 25% retaliatory tariffs

- Global Dairy Trade auction results show Cheddar prices increased 8% to $4,257/MT in recent trading

This mixed picture reflects varying price elasticities across cheese types and the complex interplay between tariffs, supply constraints, and shifting consumer preferences.

Global Market Reshuffling: The New Trade Reality

The tariff environment fundamentally restates global dairy trade patterns with potentially long-lasting consequences for demand.

Market Share Redistribution

As US products face prohibitive tariffs in key markets like China, competitors are rapidly filling the void:

- “We’re seeing a shift toward European and New Zealand suppliers to fill the gap,” noted Maria Chen, a Beijing-based dairy analyst

- New Zealand is ramping up shipments to China, with exports projected to grow by 15% this year

- European dairy exporters are positioned to benefit, though they maintain caution about potential supply constraints

This redistribution of market share can have permanent effects even if tariffs are eventually removed, as suppliers establish new relationships and supply chains adapt. Once you lose market position, regaining it can take years – if it happens at all. It’s like trying to get your milk quality premium back after losing it – the processor has already found another farm to fill that high-quality slot.

Do you think Chinese buyers will return to US suppliers once they’ve established relationships with European and New Zealand producers? Not a chance.

The China Paradox

A particularly interesting dynamic is emerging in China:

- China’s milk production dropped 9.2% in early 2025

- Despite this domestic production decline, tariffs are blocking affordable US supplies

- This forces Chinese buyers to source from more expensive alternative suppliers or reduce consumption

What This Means for Your Operation

The current tariff situation has several important implications for dairy operations of all sizes:

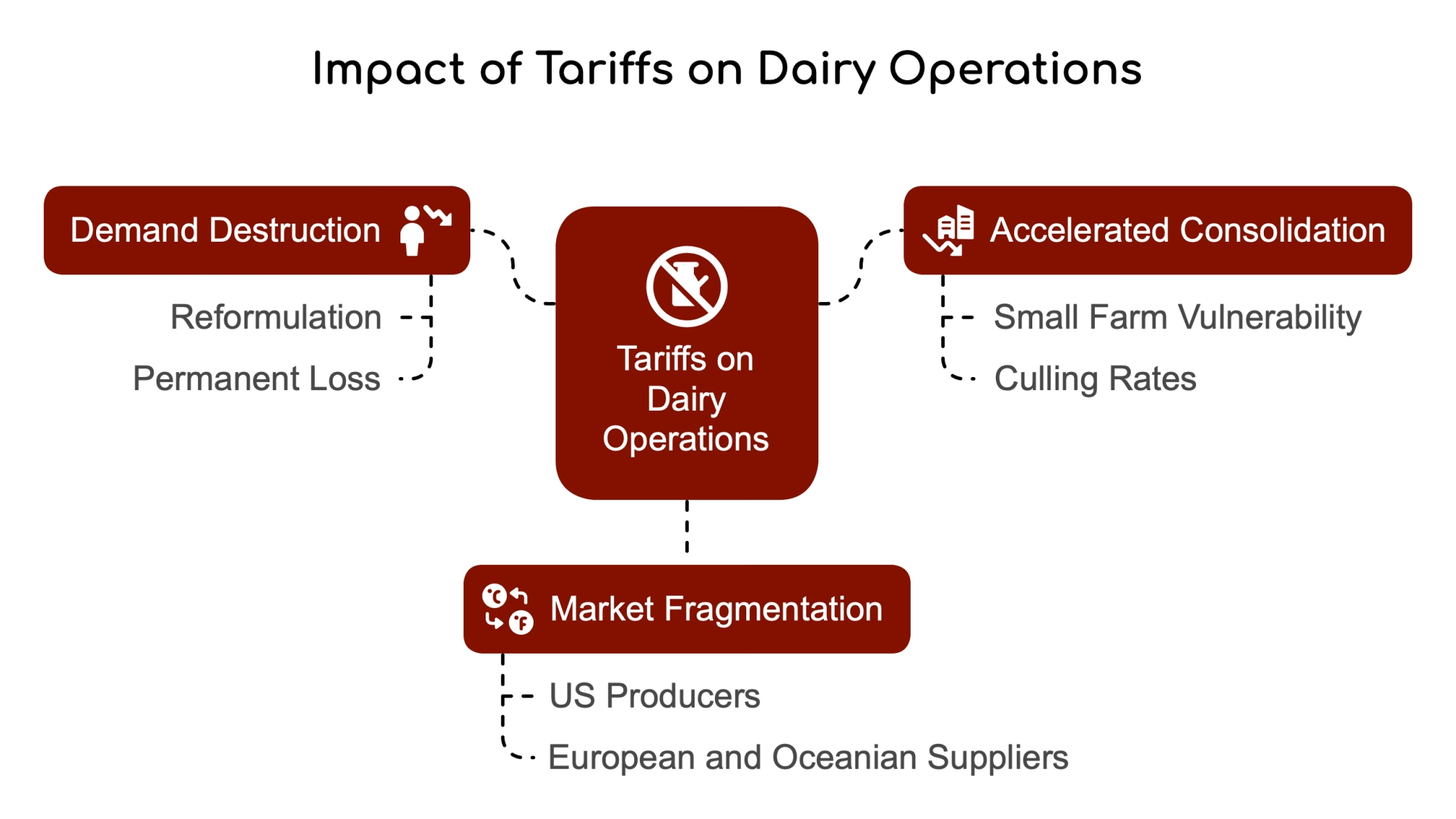

Demand Destruction vs. Diversion

For products with high tariffs, like whey and lactose, the primary effect is not merely demanding diversion but potential demand destruction:

- Prohibitive tariffs can force manufacturers to reformulate products to use less of the affected ingredients – like how feed companies reformulate when a specific ingredient becomes too expensive

- Once reformulation occurs, demand may not return even if tariffs are removed – just as cows don’t immediately return to peak production after a bout of acidosis

- This represents a permanent loss of market share rather than a temporary disruption

Accelerated Consolidation

The financial pressure from tariff-related market disruptions will likely accelerate industry consolidation:

- Small farms face particular vulnerability as margins compress

- The current low culling rates (down 30% in June) may reverse as financial pressures mount – much like how you might have held onto marginal cows during high milk prices but must make harder decisions when the milk check shrinks

- Farms without diversified markets or substantial risk management tools will face the greatest pressure

Let’s face it – the industry was already consolidating. These tariffs are like pouring gasoline on that fire. Are you prepared to be one of the survivors, or will you be another statistic in the ongoing decline of dairy farm numbers?

Market Fragmentation

The global dairy market is fragmenting along geopolitical lines:

- US producers are pivoting to Mexico and Southeast Asia as China’s access diminishes

- European and Oceanian suppliers are strengthening positions in China

- This reorganization of trade flows will create new demand patterns that outlast specific tariffs

Strategic Responses: Protecting Your Operation

Diversify Your Product Mix

The varying impact of tariffs across product categories creates both risks and opportunities:

- Farms heavily dependent on whey and lactose revenue streams face the greatest exposure

- Operations with the flexibility to shift toward butter production may benefit from continued strong export demand

- Cheese producers should evaluate their specific varieties and target markets for vulnerability

Explore Alternative Markets

As traditional export channels face disruption, forward-thinking producers are exploring new opportunities:

- Southeast Asian markets (Vietnam, Philippines, Indonesia) show growing dairy demand and fewer trade restrictions

- Middle Eastern markets continue to expand dairy imports with less political volatility

- Domestic specialty markets may offer premium opportunities as imports face tariff-induced price increases

When was the last time you looked beyond your current milk market? The days of passive milk marketing are over. Your future depends on actively seeking new opportunities before your current ones disappear.

Invest in Product Differentiation

Generic commodity products face the greatest vulnerability to tariff-induced substitution:

- Specialty products with unique characteristics face less substitution pressure – just like how your registered Holsteins with superior genetics command premium prices compared to commercial animals

- Value-added processing can create products less vulnerable to commodity market swings – like how farms with on-site processing can capture more of the consumer dollar

- Sustainability certifications may provide access to premium markets less sensitive to price – much like how organic certification provides a buffer against conventional milk price volatility

Implement Robust Risk Management

The tariff environment demands more sophisticated risk management approaches:

- Traditional hedging strategies may be insufficient in rapidly changing trade environments

- Forward contracts with domestic processors provide greater certainty as export markets fluctuate

- Maintaining financial reserves becomes increasingly critical as market volatility increases

Are you still managing risk like it’s 2010? Because the market has fundamentally changed, and your approach needs to change with it.

The Tariff Endgame: What Happens Next?

The current tariff situation represents a fundamental shift in global trade patterns rather than a temporary disruption. While specific tariff rates may change, the era of relatively frictionless global dairy trade appears to be ending.

Scenario Planning

Forward-thinking dairy operations should prepare for multiple potential scenarios:

Scenario 1: Prolonged Tariff War

- China and US maintain high retaliatory tariffs for 2+ years

- Permanent loss of US market share in China for whey, lactose

- Continued strong butter exports due to global supply shortages

- Accelerated consolidation of smaller dairy operations

Scenario 2: Partial Resolution

- Targeted tariff reductions in specific product categories

- The gradual recovery of some export volumes but at a lower market share

- Continued market fragmentation along geopolitical lines

- Persistent price volatility as markets adjust to new trade patterns

Scenario 3: New Trade Framework

- Comprehensive trade agreement replacing tariffs with managed trade

- Establishment of product-specific quotas and market access provisions

- Increased regulatory barriers replacing tariff barriers

- Greater government intervention in agricultural markets globally

The Bottom Line

Will tariffs impact dairy demand? The evidence overwhelmingly suggests they will—and already are—have significant effects. However, these impacts vary dramatically across products, markets, and time horizons.

For products like whey and lactose, prohibitive Chinese tariffs have collapsed demand, creating domestic surpluses and price depression. Meanwhile, butter exports surged despite the tariff environment due to global shortages and substantial price differentials.

The dairy industry faces a period of profound readjustment as trade flows reorganize, market shares shift, and supply chains adapt to the new tariff reality. While temporary tariff suspensions may provide brief relief, the fundamental uncertainty introduced by weaponized trade policy will continue to reshape dairy demand patterns for years.

The resilience of butterfat exports amid this turbulence demonstrates that market fundamentals like global supply shortages can sometimes overcome tariff barriers. However, tariffs represent a significant and potentially permanent disruption to established demand patterns for most dairy products.

The operations that will thrive in this new environment will be those that:

- Understand the specific tariff impacts on their product mix

- Diversify their market exposure beyond vulnerable export channels

- Invest in product differentiation to reduce substitution pressure

- Implement robust risk management strategies

- Maintain financial flexibility to weather market disruptions

The era of predictable global dairy trade is ending. The question isn’t whether tariffs will impact dairy demand—it’s how effectively your operation can adapt to the new reality.

What’s Your Tariff Exposure?

Take a hard look at your operation’s vulnerability to tariff-induced market disruptions:

- What percentage of your milk goes into products that are heavily dependent on export markets?

- How diversified are your processor relationships and their end markets?

- What financial reserves do you maintain to weather market volatility?

- What risk management tools are you currently employing?

- How quickly could you adapt your production mix if market conditions change dramatically?

The answers to these questions will determine whether your operation becomes a casualty or a survivor in the new tariff warfare reshaping global dairy markets. As the old farm saying goes, “Don’t put all your eggs in one basket” – or in this case, don’t stake your dairy’s future on a single export market that could vanish overnight with the stroke of a politician’s pen.

It’s time to stop pretending these trade wars are someone else’s problem. They’re your problem now. The question is: what are you going to do about it?

Take action today: Contact your processor to understand exactly where your milk ends up and which markets it serves. Review your risk management strategy with your financial advisor. Join forces with other producers to explore new market opportunities. The dairy industry has survived countless challenges, but only those who adapt will thrive in this new tariff reality.

Learn more:

- Trump’s Liberation Day Tariffs: A $8.2B Gamble for Dairy Farmers

Dive into how retaliatory tariffs from Canada and China threaten $8.2 billion in U.S. dairy exports, and what farmers can do to protect their bottom line. - How Trump’s Tariffs Threaten Your Herd’s Bottom Line

Explore the real-world impact of new tariffs on milk prices, export markets, and daily farm profitability—straight from the barns and boardrooms. - Trump’s Tariff Gambit: Will Dairy Farmers Win or Lose in Global Trade Showdown?

Unpack the sector’s divided response to tariffs, the risks of permanent market loss, and why trade negotiations could reshape dairy’s future.

Join the Revolution!

Join the Revolution!

Join the Revolution!

Join the Revolution!Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.