The T.C. Jacoby Weekly Market Report Week Ending April 30, 2021

The bulls continued their leisurely stroll through the dairy pits this week and the milk markets moved higher.

The bulls continued their leisurely stroll through the dairy pits this week and the milk markets moved higher. Class III futures posted sizeable gains. Summer contracts added a half-dollar or more, which lifted them well above $19 per cwt. June through October Class IV contracts added 30ȼ to 40ȼ. May Class IV settled at $16.21, and the other contracts all topped $17, a welcome sight for dairy producers who don’t get the full benefit of the sky-high Class III market.

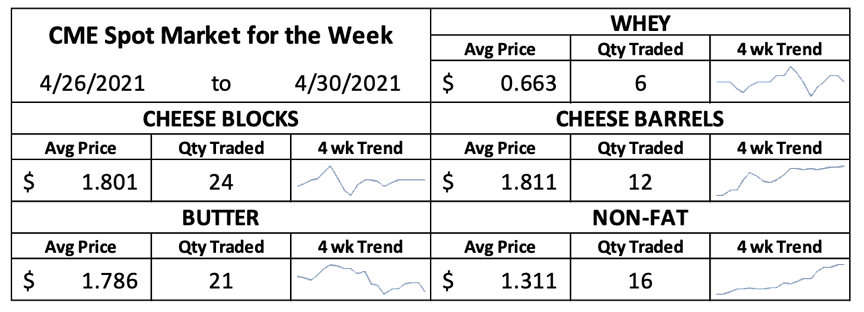

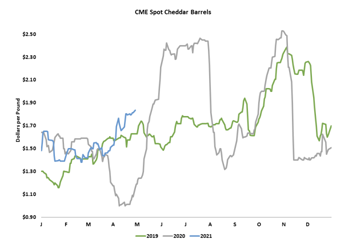

It’s been a big month for barrels. They closed today at $1.835 per pound, up 3ȼ since last Friday and up an impressive 35.25ȼ since the end of March. CME spot Cheddar blocks added a more modest 0.75ȼ this week and were up 6.25ȼ for the month. Cheesemakers tell USDA’s Dairy Market News that sales have plateaued, as restaurants have largely restocked.

It’s been a big month for barrels. They closed today at $1.835 per pound, up 3ȼ since last Friday and up an impressive 35.25ȼ since the end of March. CME spot Cheddar blocks added a more modest 0.75ȼ this week and were up 6.25ȼ for the month. Cheesemakers tell USDA’s Dairy Market News that sales have plateaued, as restaurants have largely restocked.

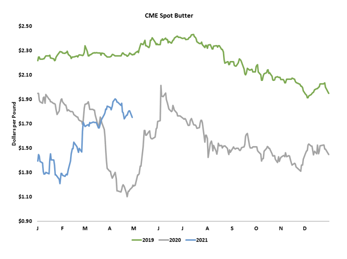

Butter sales are starting to slip. Dairy Market News notes that foodservice orders have ebbed and retail requests are “lackluster.” Uninspiring demand dragged prices lower. CME spot butter fell 1.75ȼ this week to $1.7525. Butter closed out the month 6.5ȼ lower than where it began.

Cream is plentiful in the West, and churns there are running hard, as befits the season. Supplies are tighter in the Midwest and the Northeast, and the shortage of trucks and drivers has exacerbated the regional imbalance. Logistical headaches are rippling through the dairy supply chain, preventing milk and cream from flowing smoothly to its most profitable outlet.

Cream is plentiful in the West, and churns there are running hard, as befits the season. Supplies are tighter in the Midwest and the Northeast, and the shortage of trucks and drivers has exacerbated the regional imbalance. Logistical headaches are rippling through the dairy supply chain, preventing milk and cream from flowing smoothly to its most profitable outlet.

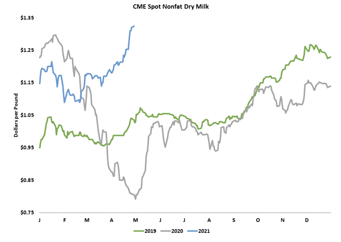

The powders remain strong. CME spot dry whey finished the month right where it started, at 66ȼ per pound. That was up 4ȼ from last Friday. Spot nonfat dry milk (NDM) jumped 7.25ȼ to $1.325, the highest spot value since October 2014. Thanks to strong foreign demand, spot NDM rallied 14ȼ this month, a 12% increase. U.S. milk powder is priced to move, and Mexico is finally stepping up purchases. Europe has very little SMP available for sale, and most milk powder in Australia and New Zealand is already committed to buyers in Southeast Asia. That leaves the United States and South America to capture new orders.

The powders remain strong. CME spot dry whey finished the month right where it started, at 66ȼ per pound. That was up 4ȼ from last Friday. Spot nonfat dry milk (NDM) jumped 7.25ȼ to $1.325, the highest spot value since October 2014. Thanks to strong foreign demand, spot NDM rallied 14ȼ this month, a 12% increase. U.S. milk powder is priced to move, and Mexico is finally stepping up purchases. Europe has very little SMP available for sale, and most milk powder in Australia and New Zealand is already committed to buyers in Southeast Asia. That leaves the United States and South America to capture new orders.

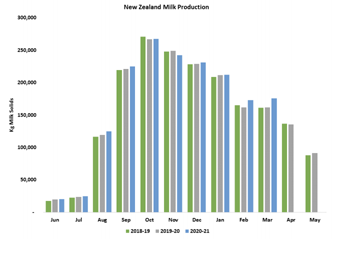

Milk output was very strong in New Zealand in March. Collections jumped 9.8% from the prior year, bringing season-to-date collections to the highest June to March tally on record, up 2.1% from last year. Timely rains in February and early March promoted grass growth and lifted milk output last month. But the rains have slowed, which could make for slower growth in the final two months of the 2020- 21 season.

Milk output was very strong in New Zealand in March. Collections jumped 9.8% from the prior year, bringing season-to-date collections to the highest June to March tally on record, up 2.1% from last year. Timely rains in February and early March promoted grass growth and lifted milk output last month. But the rains have slowed, which could make for slower growth in the final two months of the 2020- 21 season.

In Australia, milk output improved in February but faltered in March. For the season to date, Aussie milk collections are 1% greater than the very low volumes of last year. After several years of drought, Australian dairy producers are grateful for much greener pastures. But they face new hurdles. The island has been extremely isolated. That’s kept the pandemic largely at bay, but it’s also reduced the labor pool, and many producers can’t find enough help. Now that Australia and New Zealand have agreed to merge their travel bubbles, Australia is seeking farmworkers in New Zealand, promising airfare and good wages. In response, kiwi producers are stepping up efforts to retain experienced farmhands.

In the United States, the flush is in full swing and milk is plentiful. The weak dollar and tight global inventories for milk powder are helping to lift Class IV values despite domestic abundance and all the headaches of global trade.

In the United States, the flush is in full swing and milk is plentiful. The weak dollar and tight global inventories for milk powder are helping to lift Class IV values despite domestic abundance and all the headaches of global trade.

The corn market just keeps climbing. May corn futures jumped 38ȼ today as traders who were caught short rushed to buy back their positions before they were obligated to deliver corn to Chicago. May corn settled at a sevenyear high of $7.40 per bushel, up more than $1.75 this month. July corn closed at $6.7325, up 41ȼ this week. The U.S. has

exported huge volumes of corn and there is no sign of a slowdown. Brazil’s corn crop is withering and there is little rain in the forecast. In the Corn Belt, planters are rolling. Farmers and feed-buyers are hoping for big yields, but there is a lot of weather between now and harvest.

Soybeans followed corn higher. July soybeans closed at $15.3425, up 18.25ȼ from last Friday. July soybean meal closed at $426.10 per ton, up 30ȼ. Feed costs are rising quickly.

Source: Jacoby