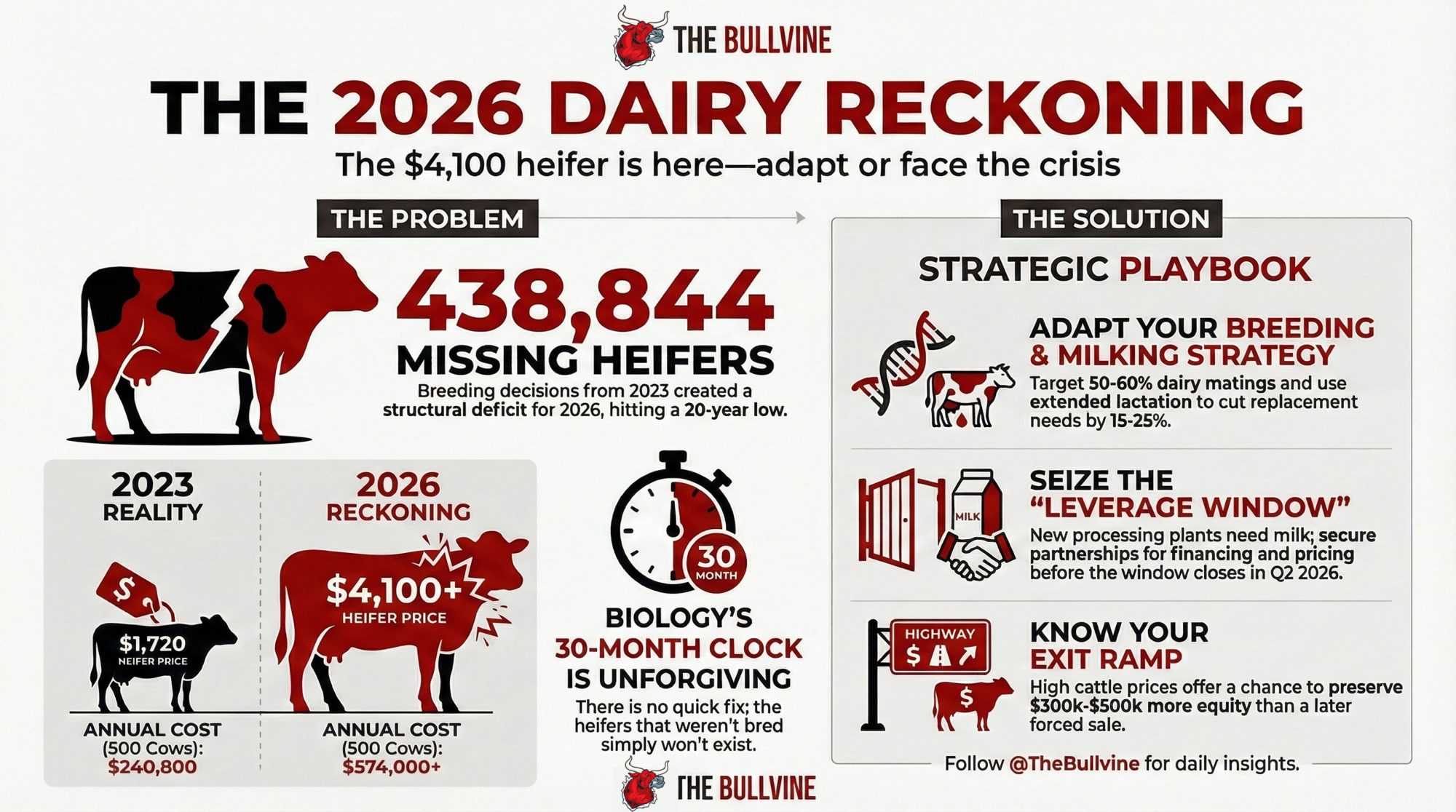

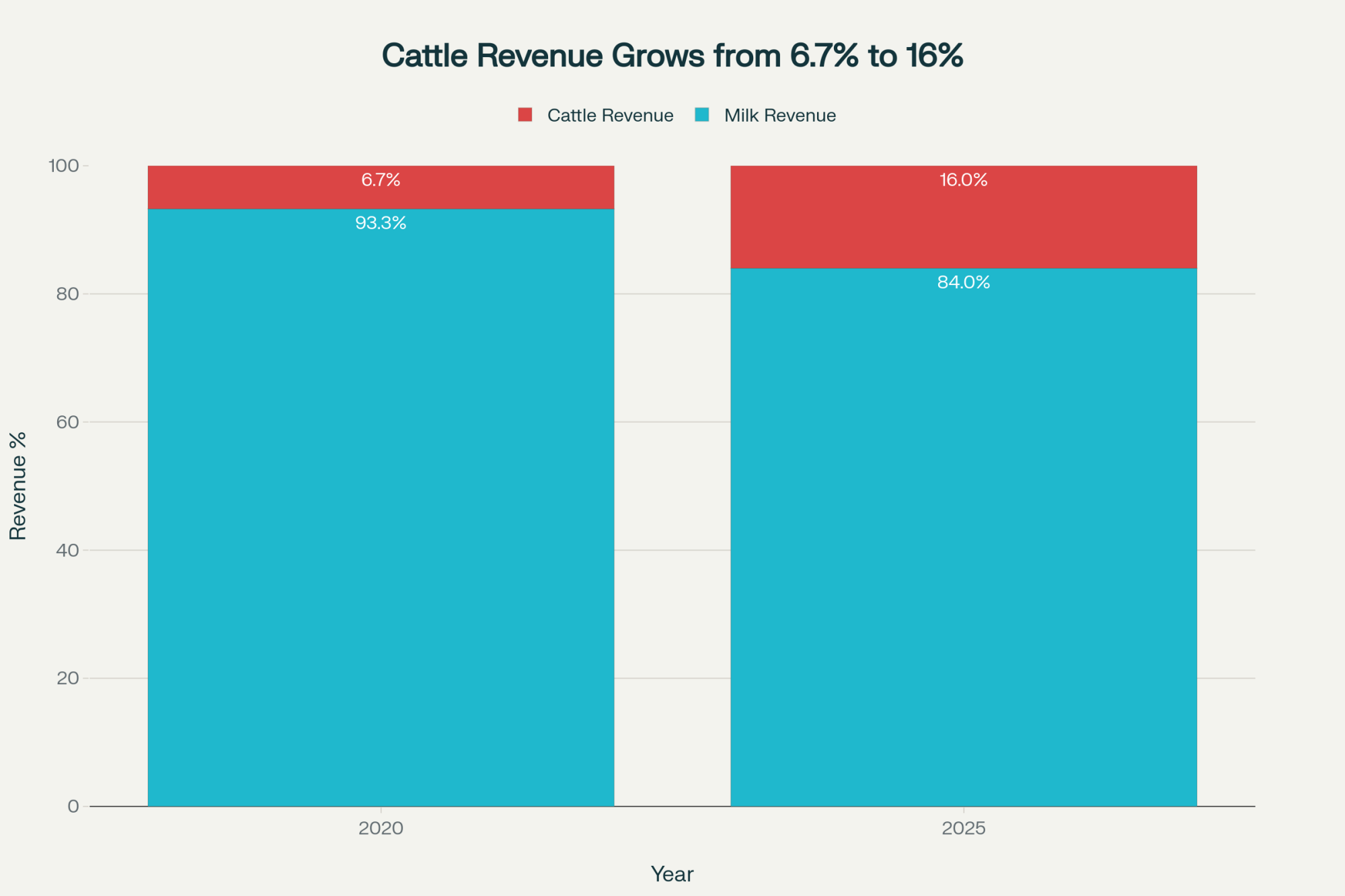

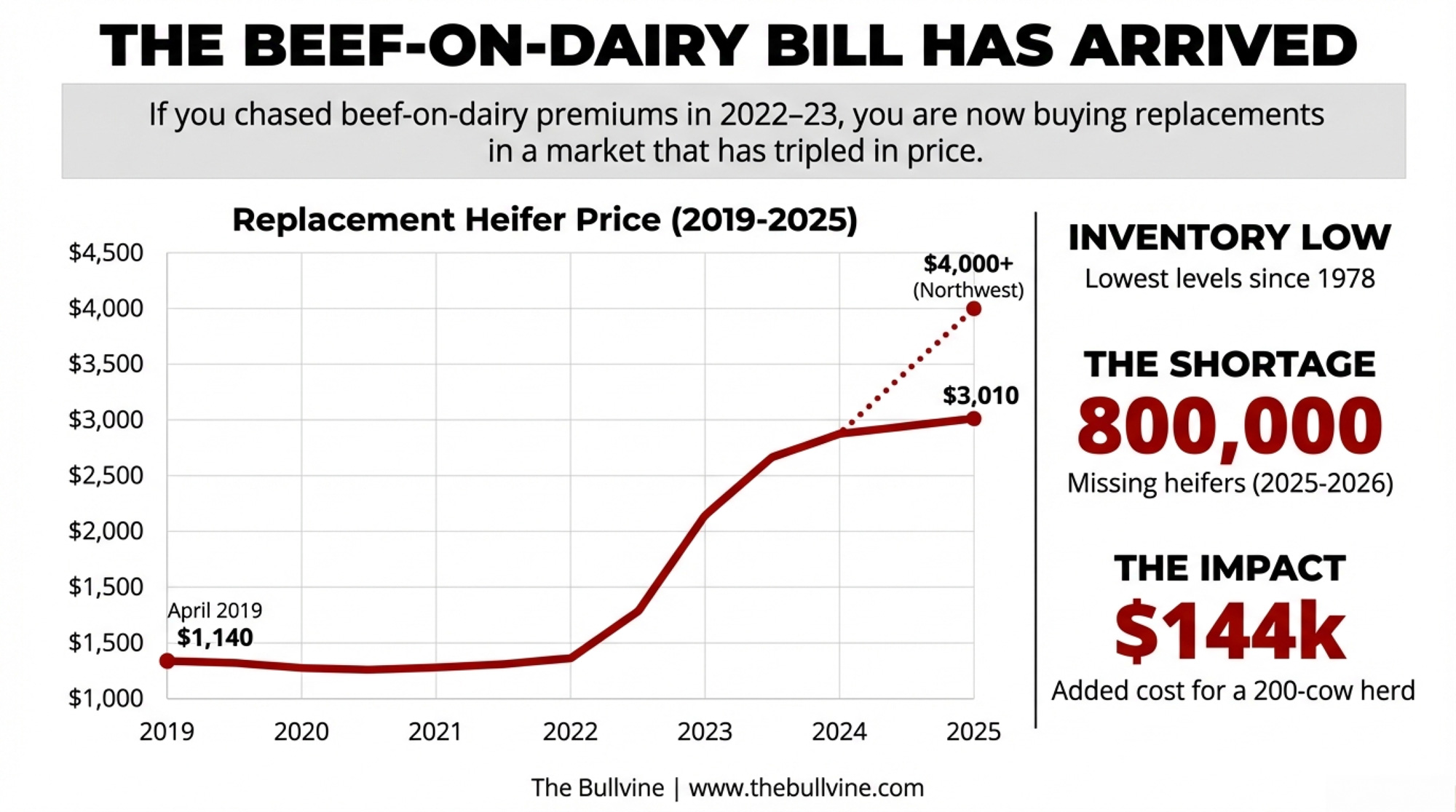

3 out of 4 dairies bred beef-on-dairy. Now 800,000 heifers are missing, and replacements are $3,010 a head. Where does your herd sit in that math?

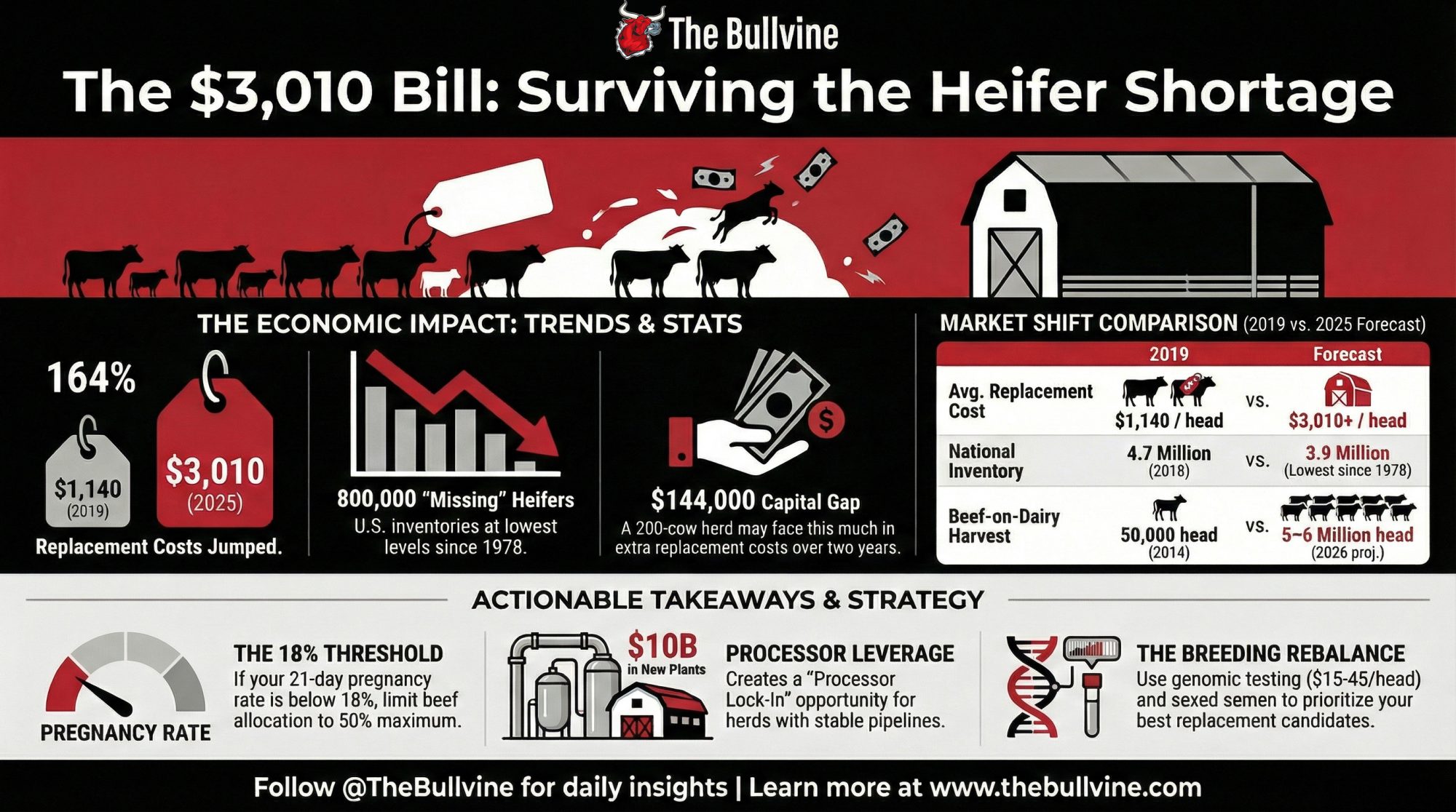

Executive Summary: If you chased beef‑on‑dairy premiums in 2022–23, you’re now buying replacements in a world where heifer prices jumped from $1,140 in 2019 to $3,010 in mid‑2025 and often top $4,000 in high‑demand regions. At the same time, U.S. replacement inventories have dropped to their lowest level since 1978, leaving roughly 800,000 “missing” heifers across 2025–2026 and making it harder—and more expensive—to keep herds at size. For a 200‑cow herd turning over 35–38% per year, that shift alone can mean an extra $126,000–$144,000 in replacement capital over the next two years if you have to buy those animals instead of calving them in. This piece breaks your options into four concrete paths—breeding rebalance, reduced culling, strategic exit, and processor lock‑in—and spells out where each helps, where it backfires, and the thresholds (like an 18% pregnancy rate or culling below 30%) that should force a rethink. It also links your barn‑level math to the bigger picture: beef‑on‑dairy calves now account for 12–15% of fed beef harvests, and roughly $10 billion in new dairy plants are scheduled to come online by 2027, keeping processor demand for reliable milk flows high even as replacements stay tight. The goal is simple: give you enough numbers and clear decision rules to decide whether your 2026 breeding sheet keeps you in the group processors treat as long‑term partners—or in the group scrambling for $3,000+ heifers with everyone else.

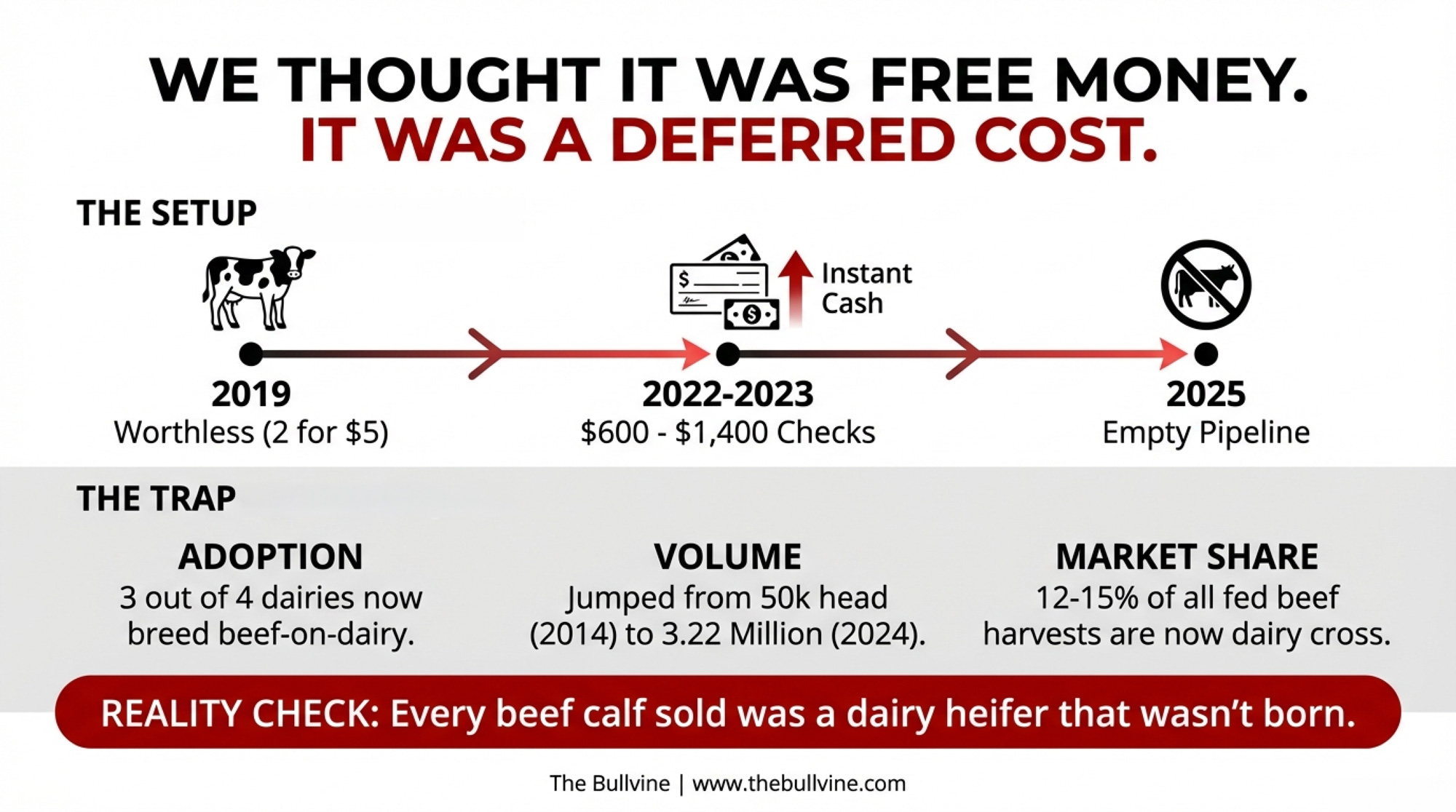

Ken McCarty of McCarty Family Farms still remembers trying to sell Holstein bull calves: “Two for $5″—with no takers. That painful baseline explains why dairy producers didn’t hesitate when beef-on-dairy calves started bringing $600, then $1,000, then $1,400 per head. The math seemed obvious. The check was immediate.

But it wasn’t free money. It was a deferred bill. And that bill has arrived.

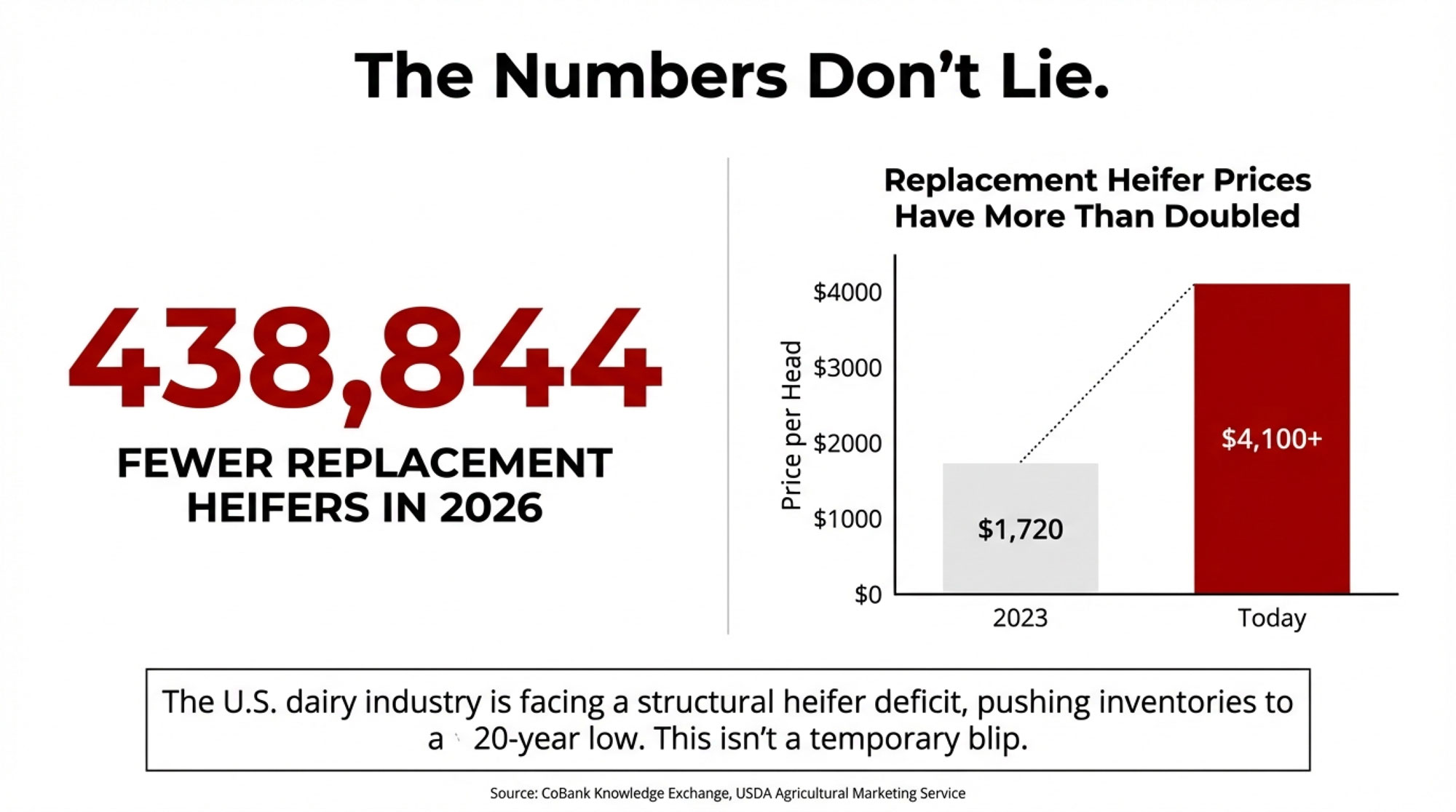

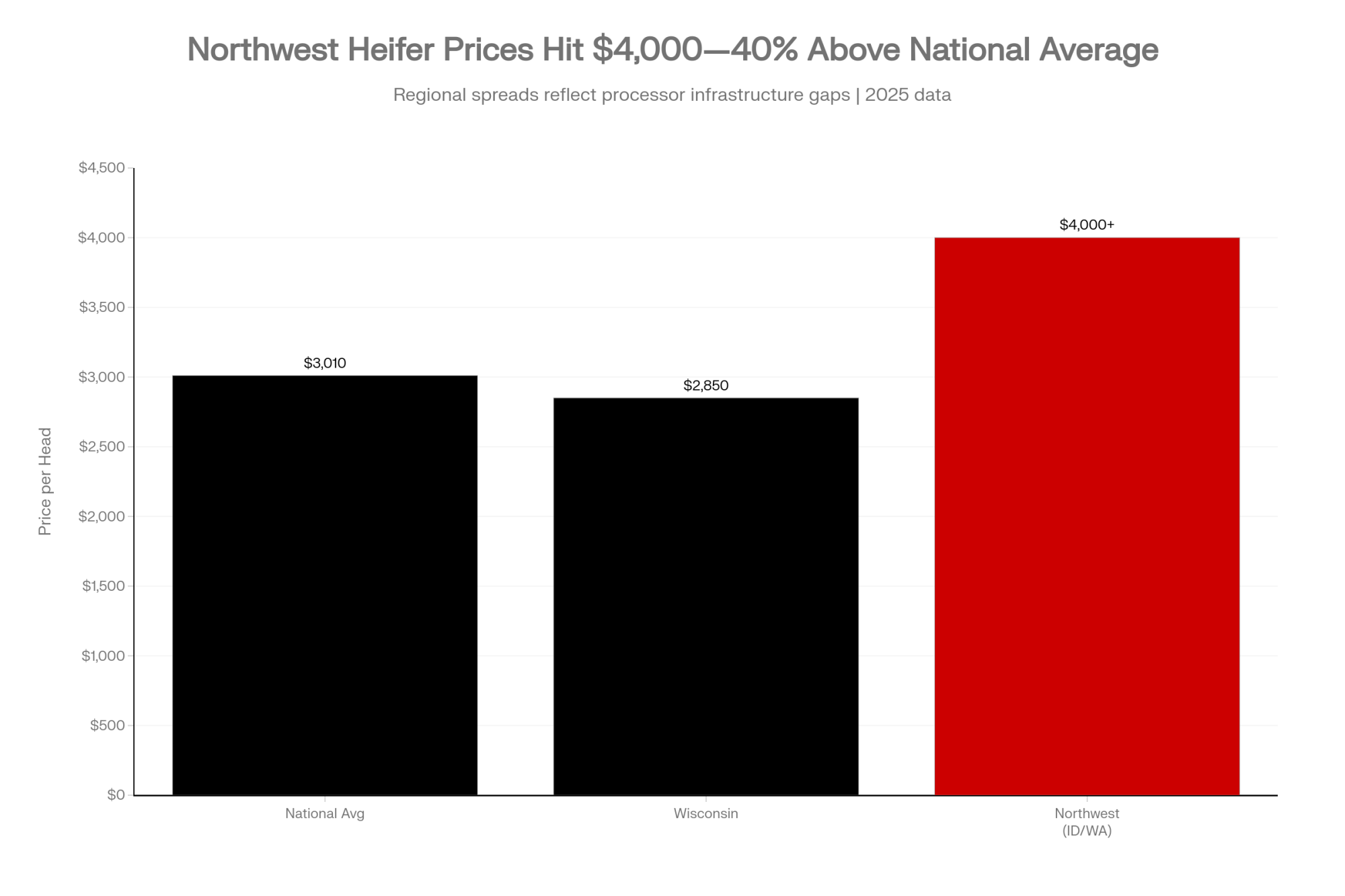

CoBank data shows replacement heifer prices climbed from $1,140 per head in April 2019 to $3,010 by July 2025—with top-quality animals in California and Minnesota auction barns commanding $4,000 or more. USDA’s January 30, 2026, cattle inventory report confirmed the national herd continues to contract. For operations that bred heavily to beef in 2022 and 2023, the pipeline is now empty. For those who maintained balance, a window is opening.

The Scale Nobody Predicted

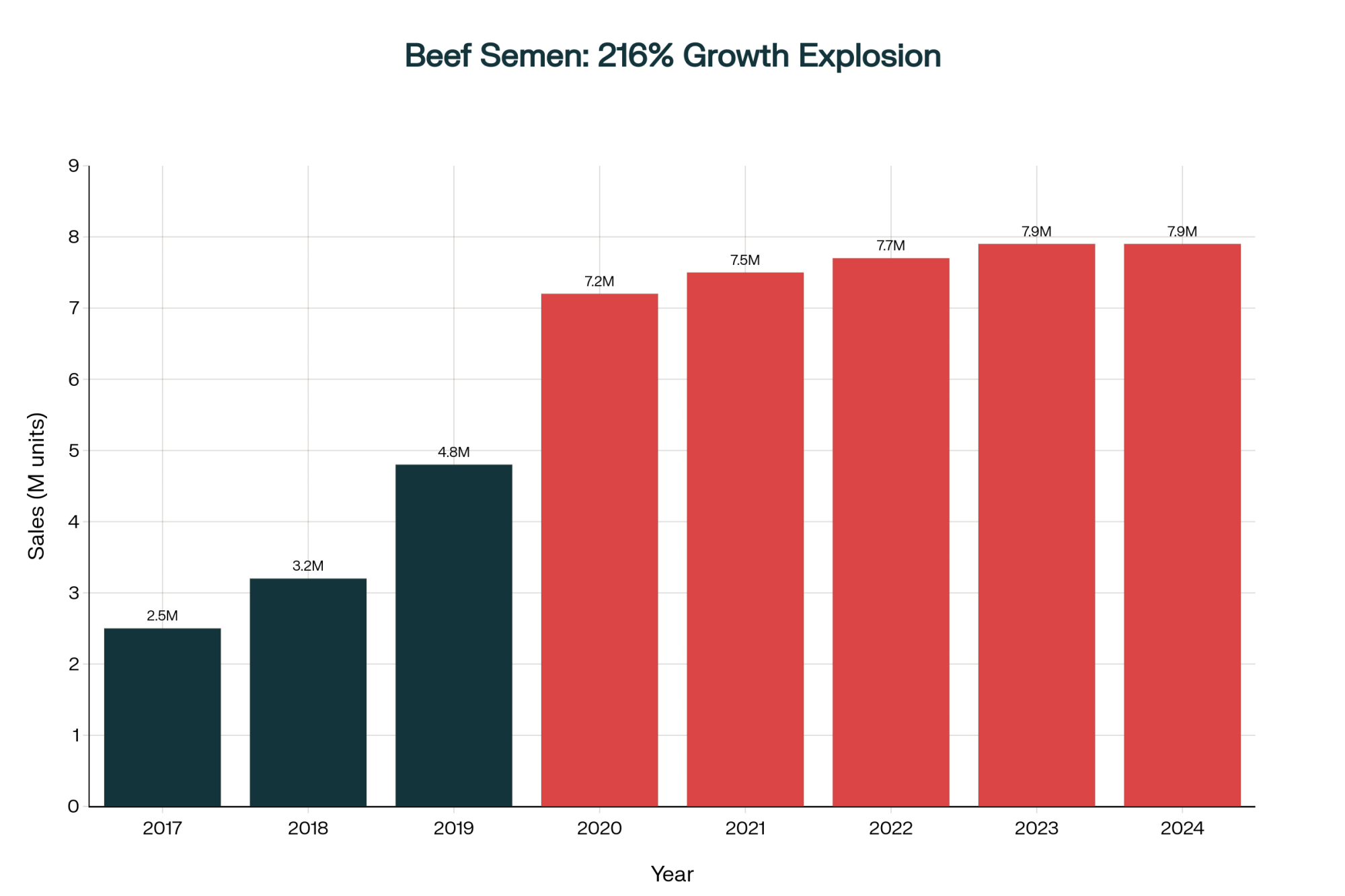

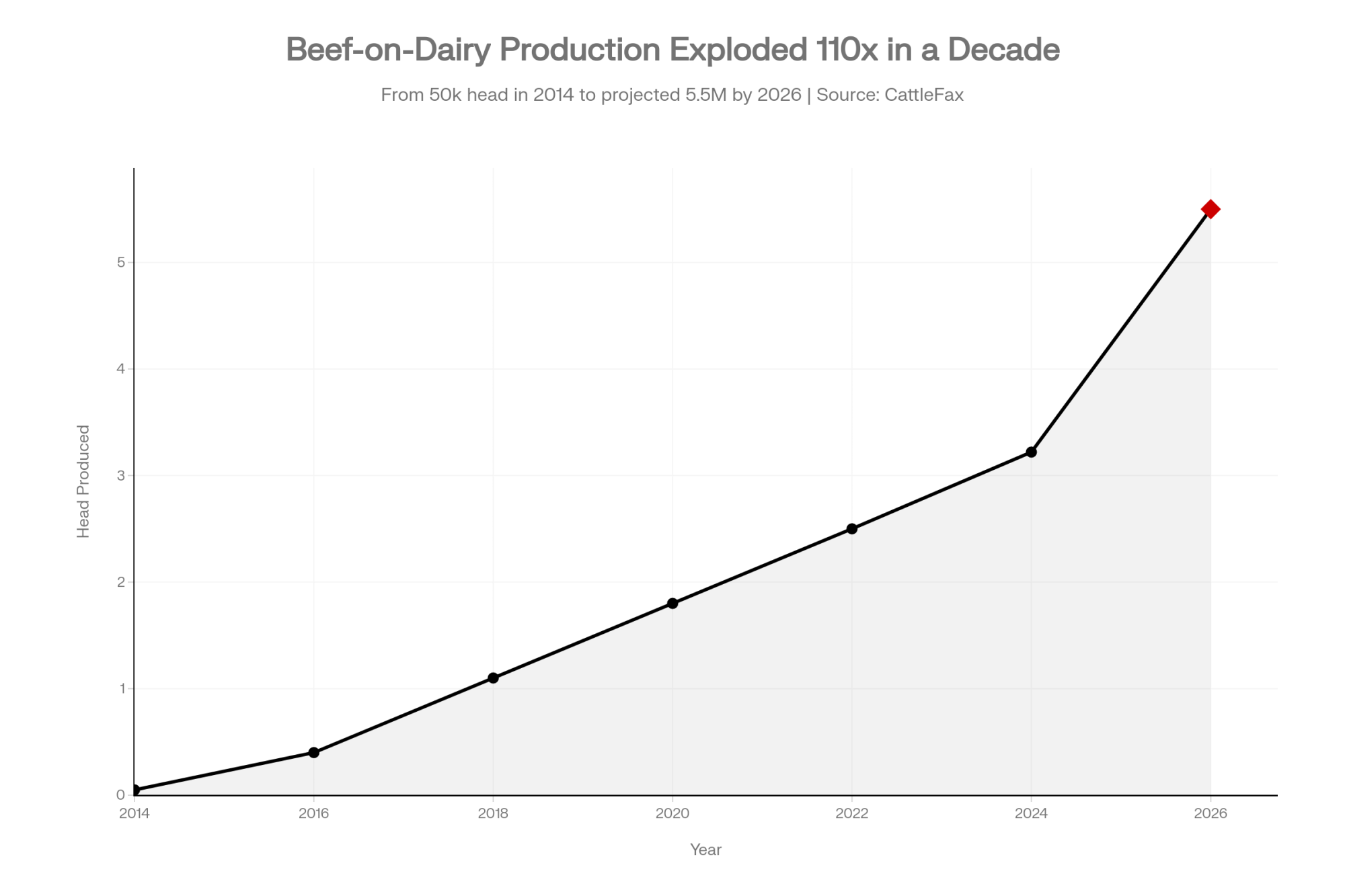

The adoption curve was staggering. Beef semen sales into dairy herds grew from 1.2 million units in 2010 to 9.4 million units by 2023—roughly 84% of which went into dairy cows, according to a 2024 Purina survey. That same survey found almost three-fourths of U.S. dairy farmers are now actively crossbreeding using beef genetics, with another 16% considering it.

CattleFax puts the production numbers in starker terms: beef-on-dairy calf production jumped from 50,000 head in 2014 to 3.22 million in 2024, with projections reaching 5–6 million head by 2026. These crossbred cattle now account for 12–15% of fed beef harvests.

Every one of those calves was a dairy heifer that wasn’t born.

The Pipeline Math That’s Already Locked In

Sarina Sharp at the Daily Dairy Report flagged in early 2024 that dairy heifer inventories had declined for six consecutive years. USDA’s January 2025 snapshot put milk replacement heifers at 3.914 million head—the lowest since 1978, a full 18% below 2018 levels.

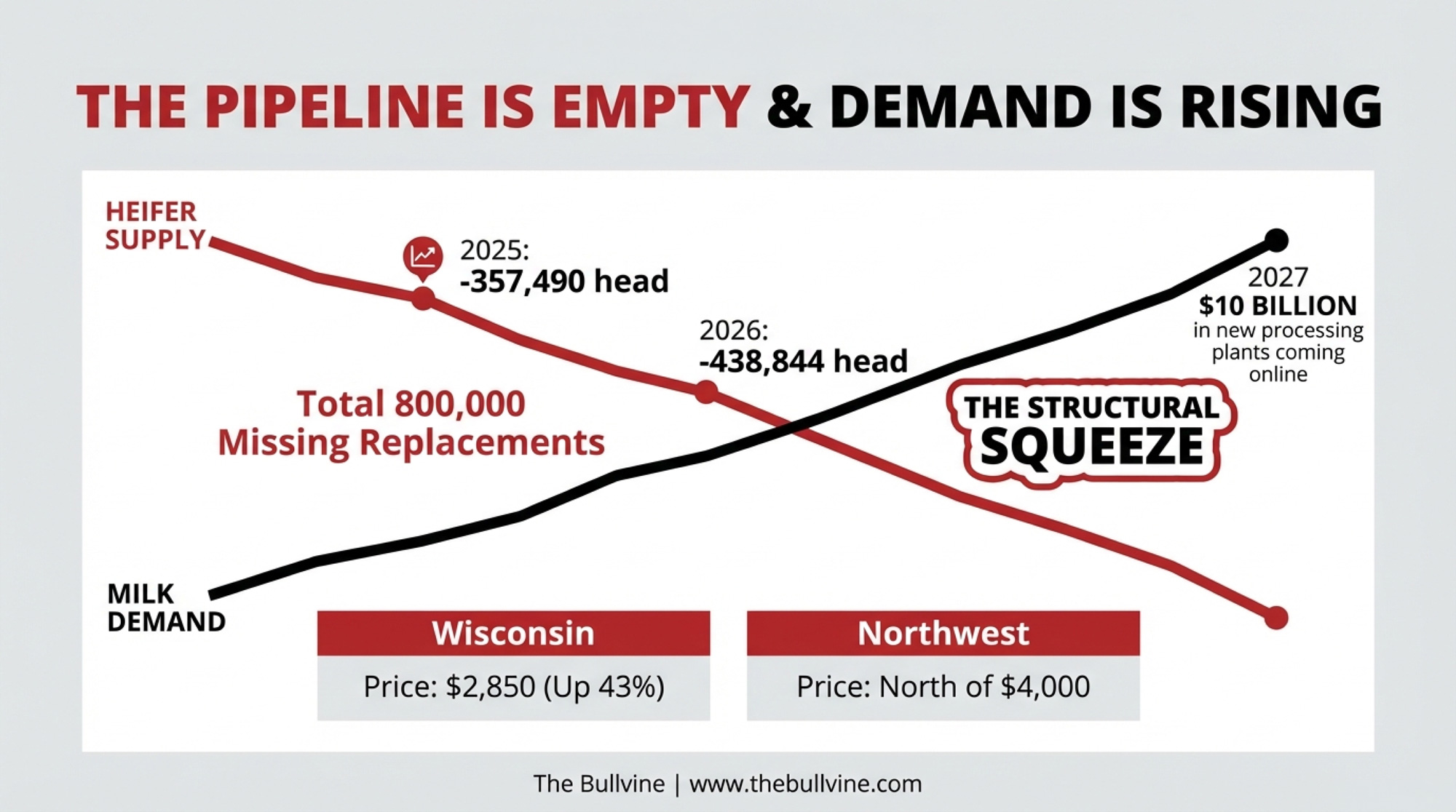

CoBank economist Corey Geiger quantified the gap in an August 2025 report: 357,490 fewer dairy heifers available in 2025, then 438,844 fewer in 2026. Add those up. That’s roughly 800,000 missing replacements across a two-year window. And as Geiger commented: “We don’t see a rebound until 2027, and that will be up 285-thousand, but you’ve got to remember, that’s going to be after 800-thousand fewer heifers”.

Regional variation tells its own story. Wisconsin replacement values jumped 43% year-over-year between October 2023 ($1,990) and October 2024 ($2,850), according to USDA data. Yet Wisconsin actually gained 10,000 heifers while Texas lost 10,000 head. “Watch” on the Northwest (Idaho/Washington), where prices have reportedly hit that $4,000+ “north of the border” threshold. That divergence comes down to processor relationships and infrastructure, not just breeding decisions.

The Beef-on-Dairy Miscalculation

Here’s what producers believed: beef-on-dairy premiums were an additive income. Extra revenue layered on top of normal operations without meaningful trade-offs.

Here’s what actually happened.

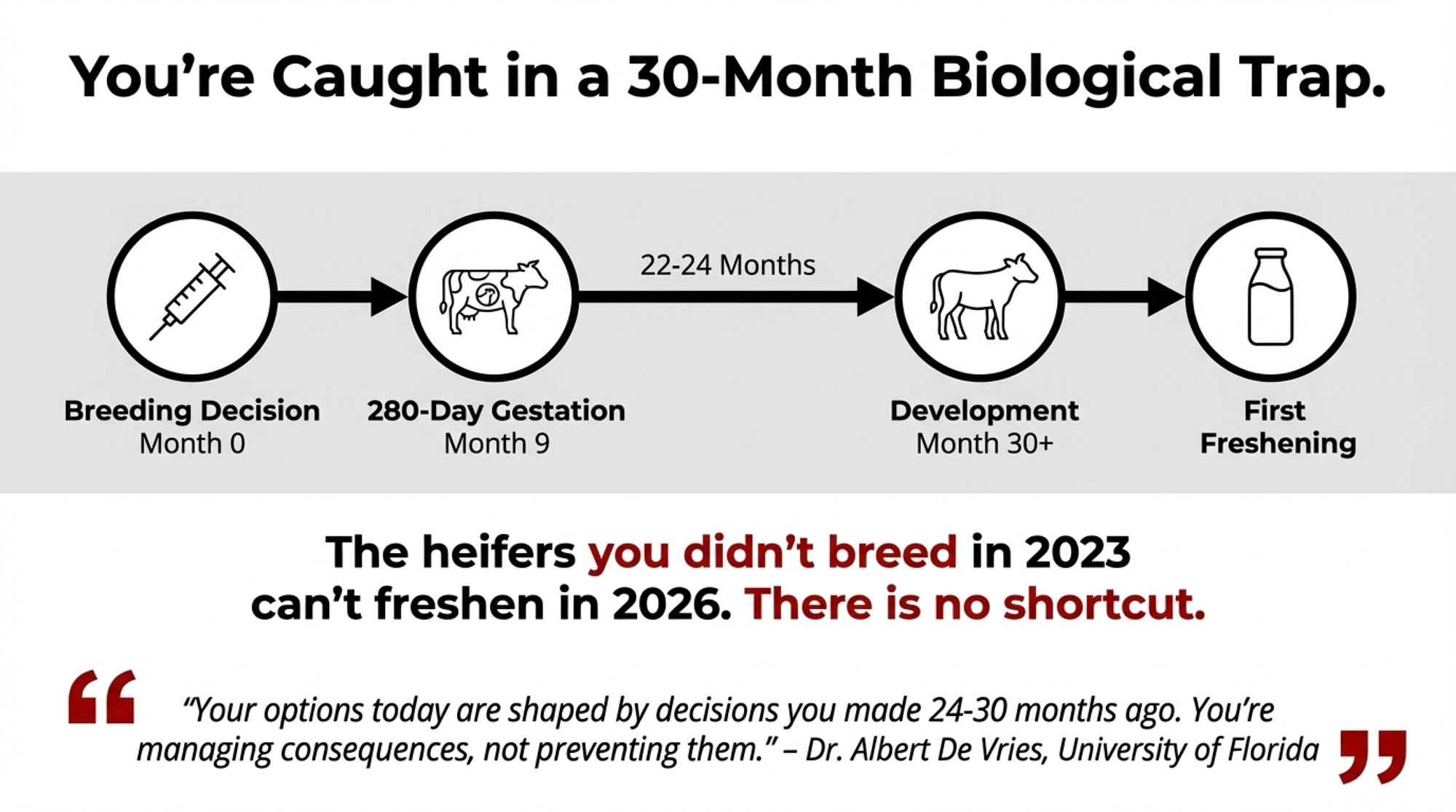

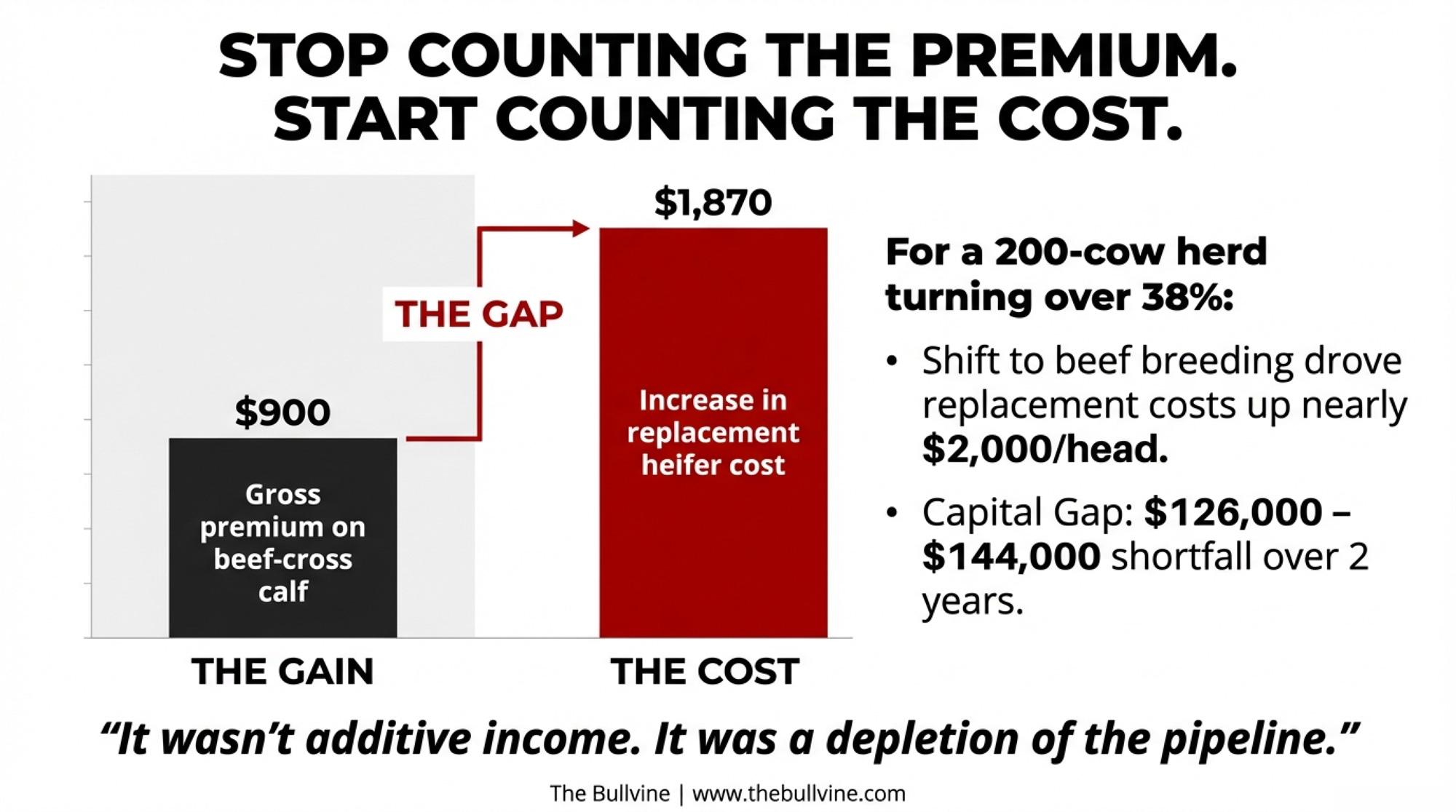

When beef-on-dairy calves climbed toward the $1,400 average that Purina’s Laurence Williams cited by 2024-2025, producers weren’t making a one-time decision. They were depleting a pipeline that takes three-plus years to rebuild. Every beef breeding looked like a $900 gain. What nobody penciled in was the replacement heifer that wouldn’t exist three years later—an animal that now costs $1,870 more than it did in 2019.

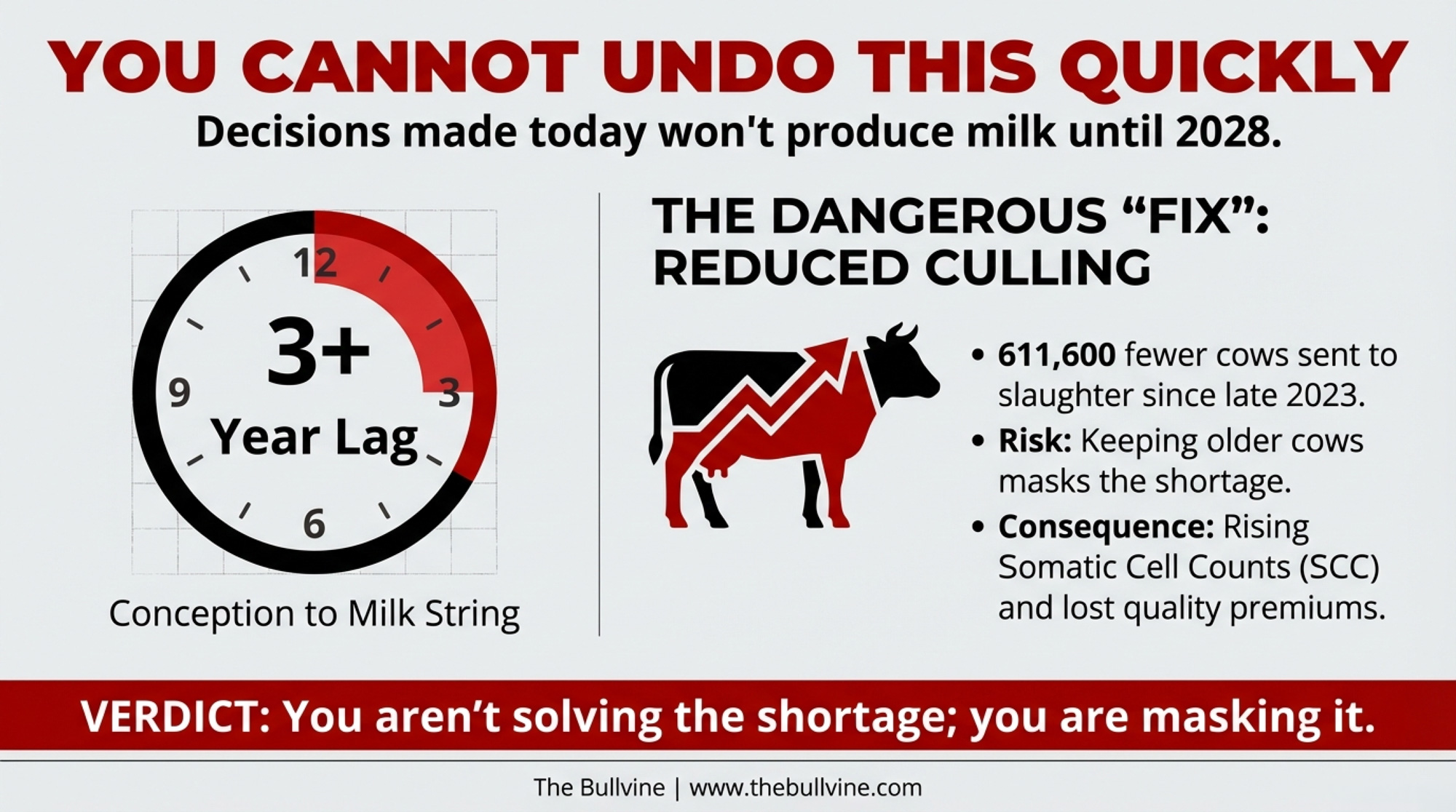

CoBank’s analysis is blunt: from conception to a cow in the milk string is a “three-plus year proposition”. You can’t undo aggressive beef breeding quickly.

And the 2024 NAAB semen sales data reveals how producers tried to have it both ways. Gender-sorted dairy semen surged 17.9%—an additional 1.5 million units. But beef semen held steady at 7.9 million units. No retreat.

How This Lands on Real Operations

When Mike North of Ever.Ag started seeing two-to-three-day-old beef-cross calves bringing $1,000, his framing captured the logic perfectly: “Why feed an animal for 18 months when the money’s sitting there at day three?”

But North also flagged the inflection point when the math flipped: “Some animals moving in the northwest last week were north of $4,000 an animal. That’s a pretty tall price, and so now, guess what? We’re seeing people starting to switch some of their breeding back to that replacement animal”.

One Minnesota producer’s current allocation illustrates the hedging strategy most operations have adopted: 10% of cows bred to sexed semen, while the rest go to beef; for heifers, 50% bred to sexed semen, while the other half go to beef. That’s not a correction—it’s a bet that partial measures will thread the needle.

Meanwhile, culling rates have collapsed. Dairy farmers have sent 611,600 fewer cows to slaughter since Labor Day 2023, according to CoBank’s analysis of USDA data. That keeps milk flowing but ages the herd.

Running the Numbers: Gross Premium vs. Net Replacement Cost

Here’s the full picture for a typical 200-cow Holstein operation in the Upper Midwest:

The spread:

Beef-cross premium over Holstein bull: ~$750-$1,200/head (2024-2025 market)

Incremental heifer cost increase (2019 vs 2025): ~$1,870/head at national averages

The math: If your replacement ratio means 1.5-2 beef breedings per “lost” heifer, and premiums average $900, you’ve captured $1,350-$1,800 in gross premium. But across the industry, the collective shift toward beef breeding drove replacement heifer costs up $1,870 per head. For a 200-cow operation needing 70-80 replacements annually (35-38% turnover), that gap represents $126,000-$144,000 in additional replacement capital over 24 months—if you can find animals to buy at all.

Metric

Value

Notes

Herd Size

200 cows

Typical Upper Midwest operation

Annual Replacement Rate

35-38%

70-76 replacements needed yearly

Beef-Cross Premium (2024-25)

$750-$1,200/head

Average $900 across regions

Gross Premium Captured

$1,575/replacement

Assumes 1.75 breedings per heifer @ $900

Heifer Cost Increase (2019-2025)

+$1,870/head

From $1,140 to $3,010 national average

Net Gap per Replacement

-$295/head

Premium didn’t cover cost inflation

Total Additional Capital (24 months)

$126,000-$144,000

For 140-152 replacements over 2 years

Critical Time Horizon

2026-2027

When depleted 2022-23 pipeline hits

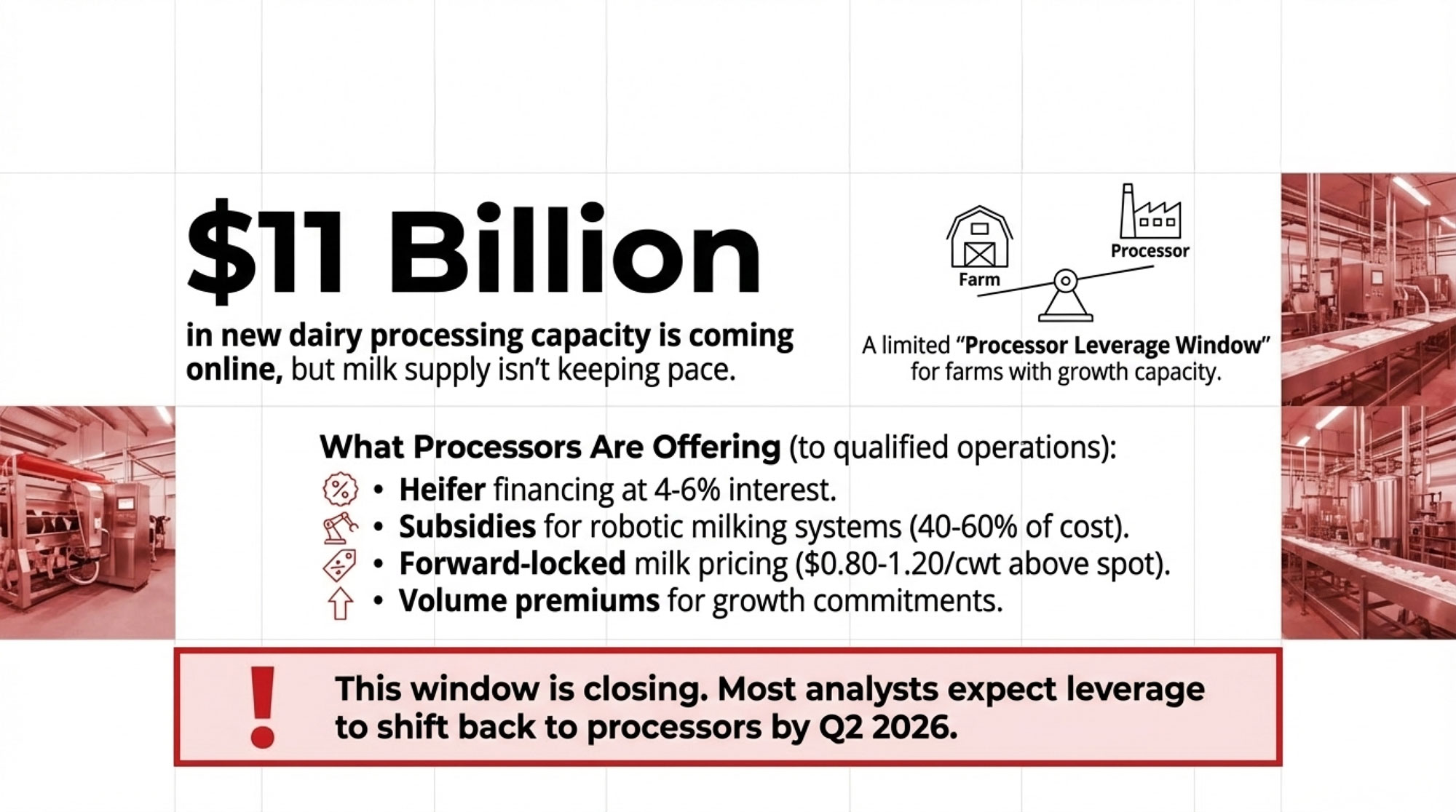

And here’s the kicker: The $10 billion in new dairy plants are set to come online through 2027, meaning processor demand for milk will keep climbing even as replacement supply stays pinched.

Four Paths Forward—And Where Each Can Backfire

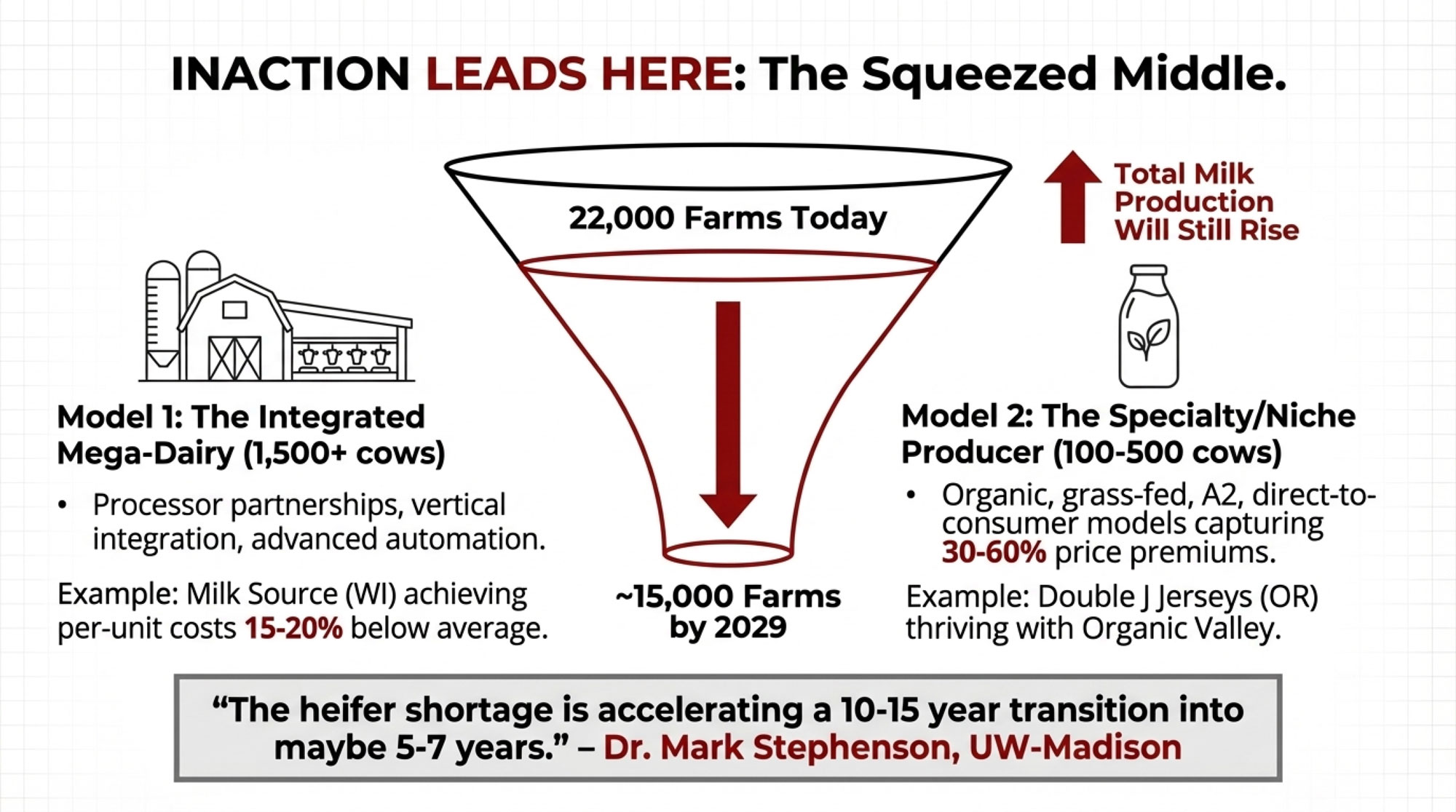

Chris Wolf’s Michigan State analysis of 14,824 farm records found that performance variation among small farms is 38% farm-related compared to only 15% for large farms. Your response to this crisis matters more at 200 cows than at 2,000.

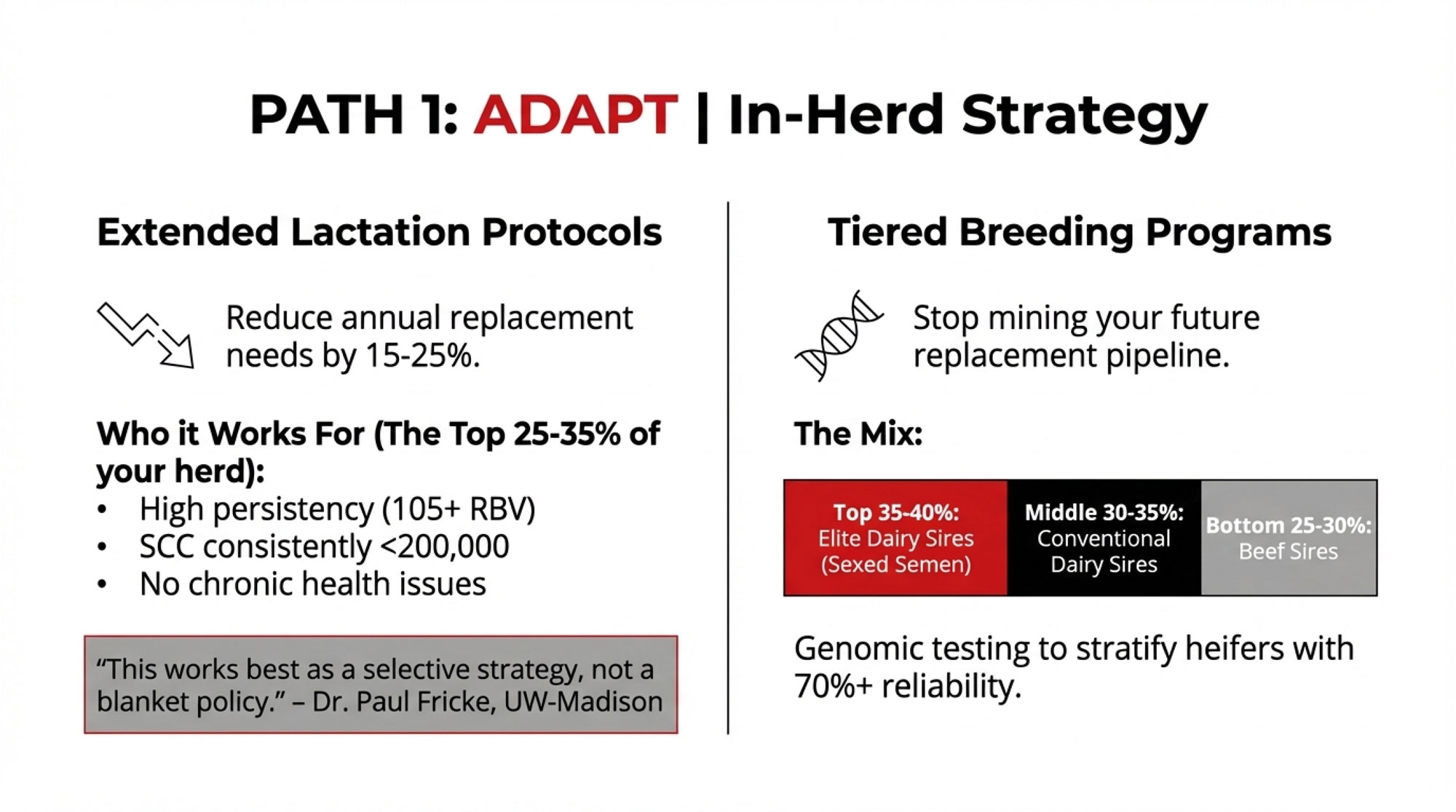

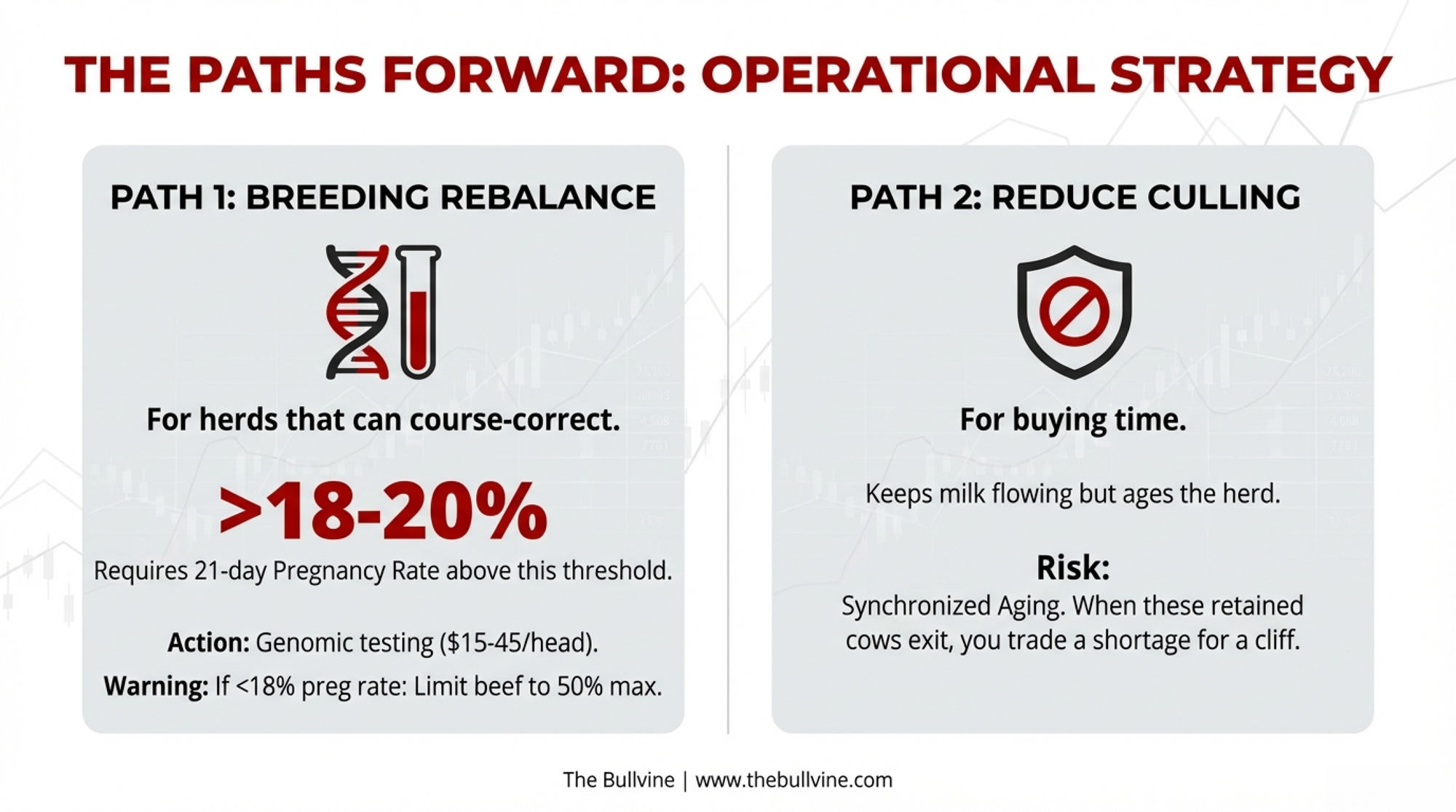

Path 1: Breeding Rebalance

Path 2: Reduce Culling

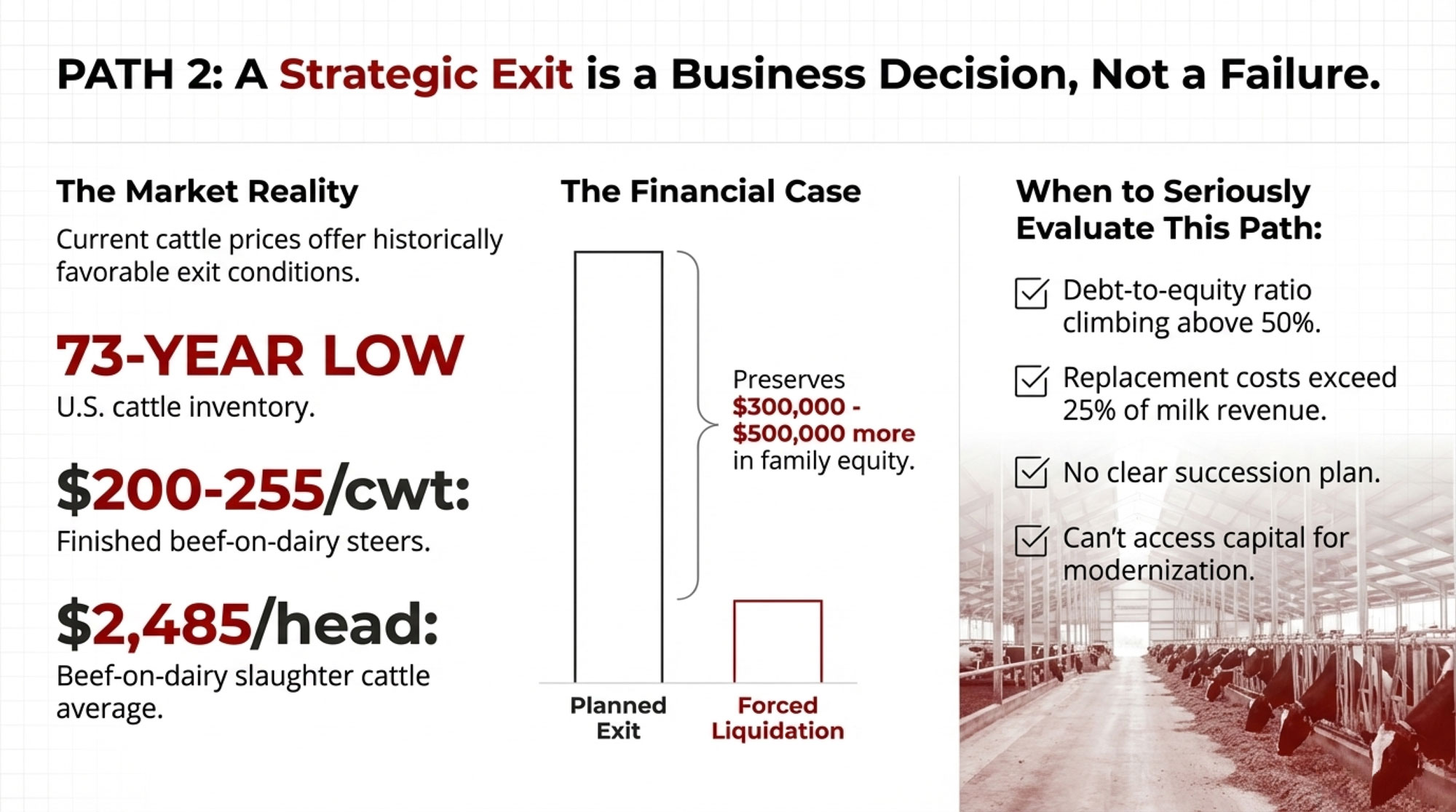

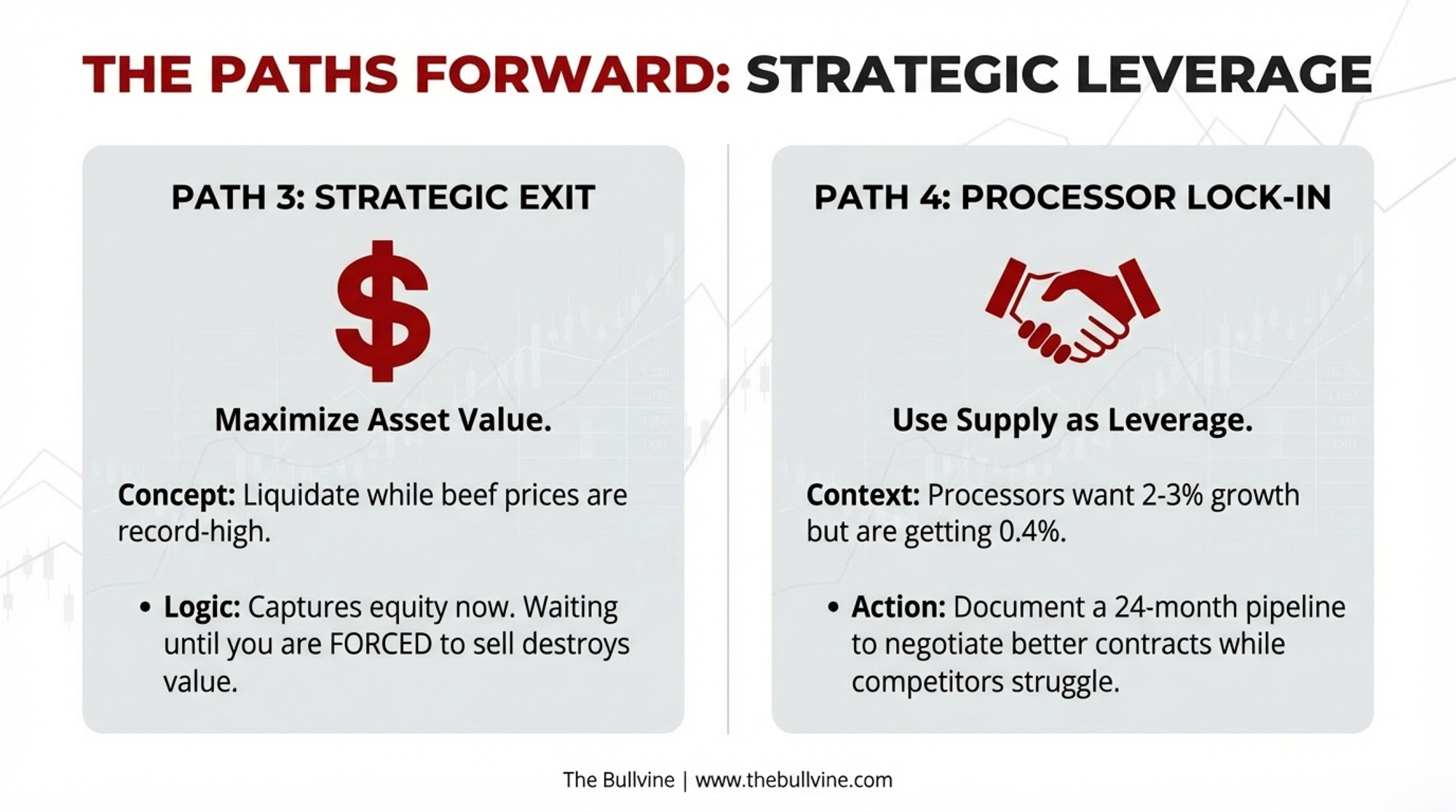

Path 3: Strategic Exit

Path 4: Processor Lock-In

Best for

Herds that can still course-correct the pipeline

Healthy older cows; buys time

Monthly losses; owners near retirement

Stable herds that can prove supply

Requires

Genomic testing ($15-45/head); sexed dairy on top 35-40%

Transition management; accept lower avg production

Honest market assessment before values erode

Documented 24-month replacement pipeline

⚠️ Backfire risk

Below 18% pregnancy rate, can’t maintain pipeline AND premiums

Failing to deliver on the supply commitment damages the relationship

Key threshold

21-day pregnancy rate ≥20% for optimal beef allocation

Monitor herd age distribution and SCC quarterly

Compare current liquidation value vs. projected 2027 value

Can you document pipeline sustainability?

Path 1 is where the Journal of Dairy Science analysis matters most: beef semen becomes economically optimal when crossbred calf price hits at least 2x dairy calf price, AND herd achieves ~20% 21-day pregnancy rate. ⚠️ Below 18%, limit beef allocation to 50% maximum. Only about 10% of Florida producers use genomic testing, per University of Florida estimates—adoption rates vary significantly by region.

Path 2 carries a hidden cost. Retaining older cows often means rising somatic cell counts, which can erode quality premiums from your processor—compounding financial strain at exactly the wrong time. Worse, when a wave of retained cows exits simultaneously, you’ve traded a gradual shortage for a cliff.

Path 3 isn’t a failure. With beef cattle prices at record highs, liquidating today captures significantly more equity than waiting until the shortage resolves. ⚠️ Waiting preserves optionality but erodes equity if exit becomes forced rather than chosen.

Path 4 is the angle most producers haven’t considered. Strong signals suggest processors expecting 2-3% milk supply growth and getting 0.4% are becoming choosy about who they keep. If you can document pipeline sustainability, you may find yourself first in line for favorable contract terms as competitors struggle to guarantee supply.

Signals to Watch

Heifer inventory trajectory. CoBank projects inventories won’t normalize until 2027 at the earliest. Watch USDA semi-annual reports for evidence that national heifer numbers have stopped declining.

Regional price spreads. The gap between Wisconsin’s $2,850 and Northwest prices “north of $4,000” reflects infrastructure differences, not just supply. Where does your region sit?

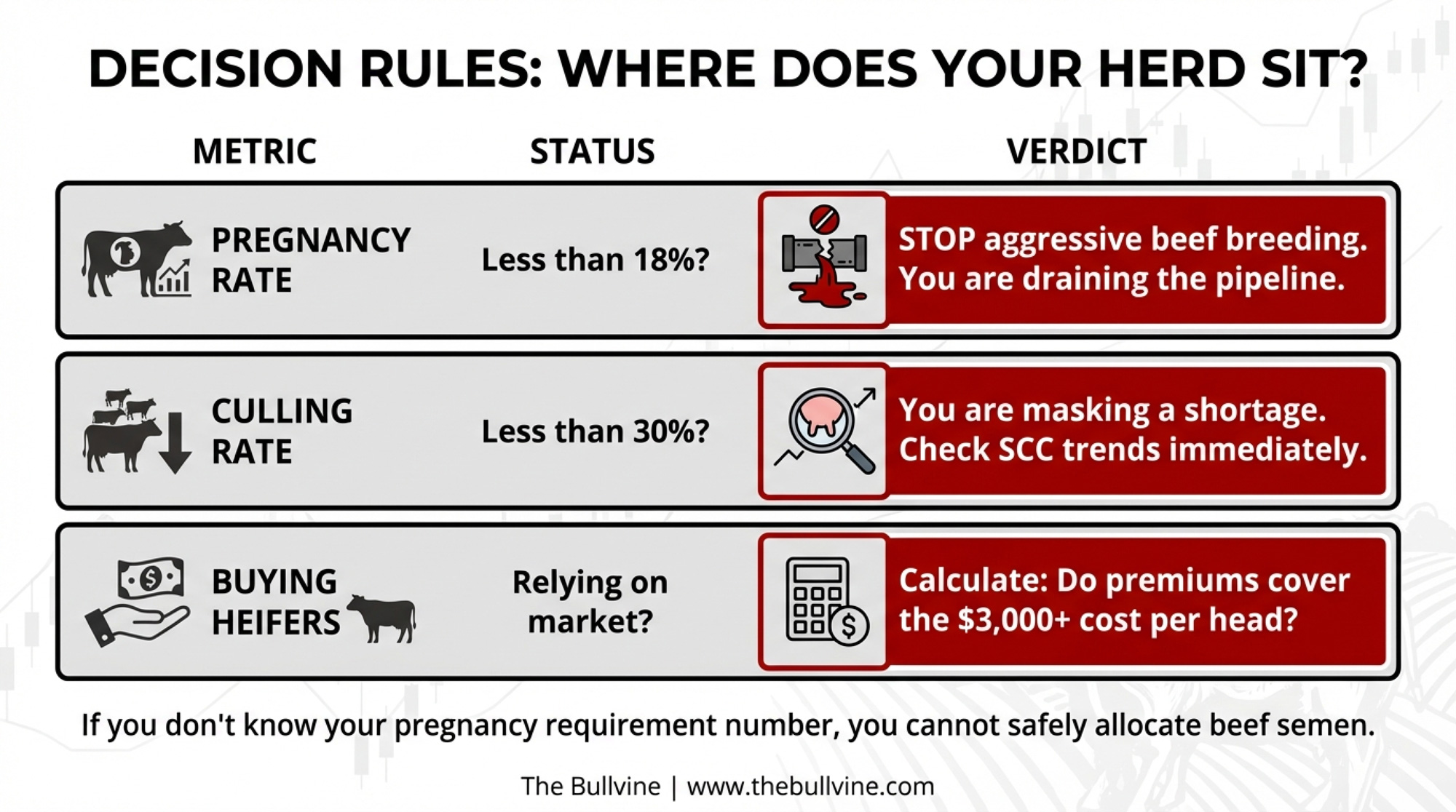

Your own replacement math. How many dairy heifer pregnancies must you generate annually to maintain herd size at the target age structure? If you don’t know that number, you can’t evaluate your breeding allocation.

What This Means for Your Operation

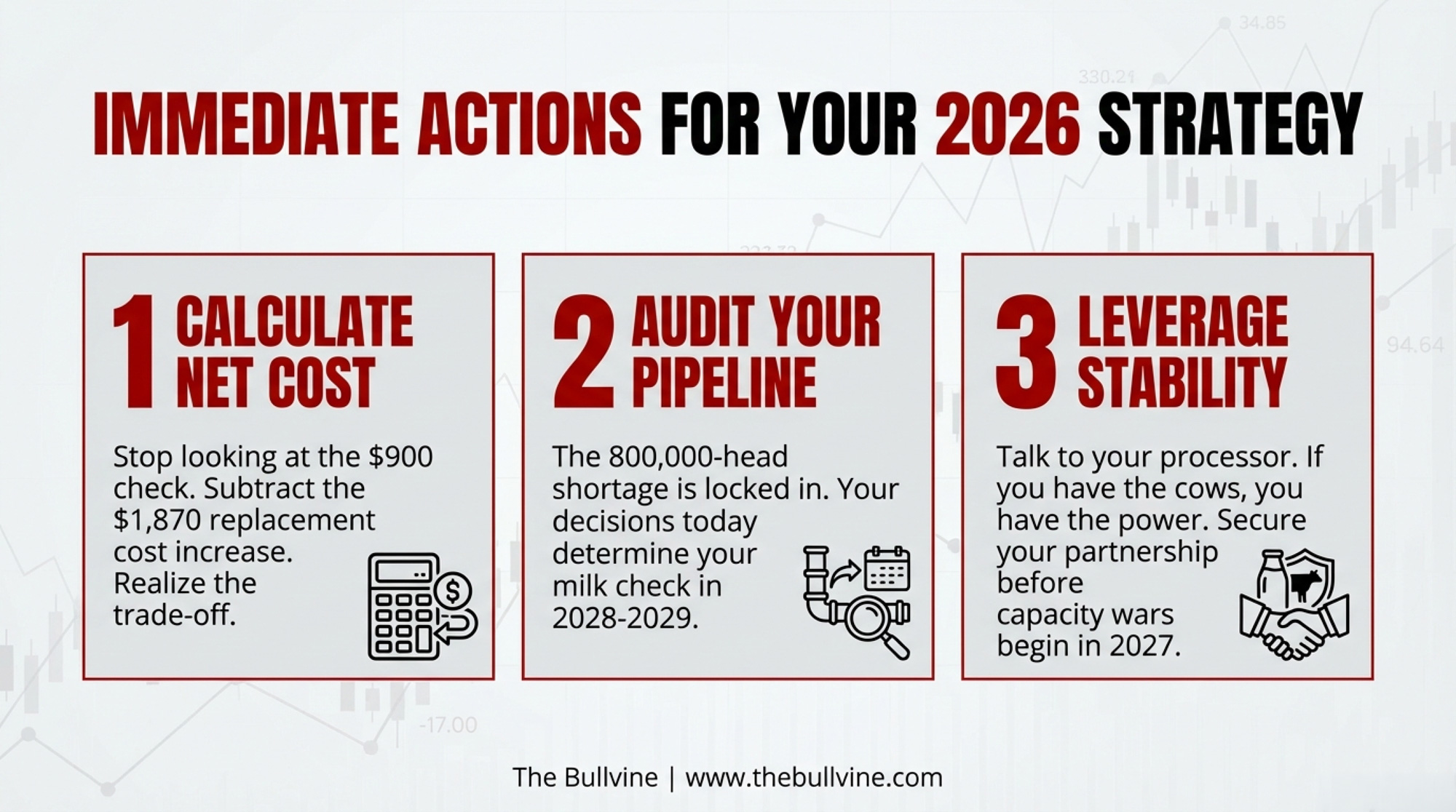

Calculate the real cost, not the gross premium. The $900 beef-cross check was real income—but if replacement costs have jumped $1,500+ per head since 2022, determine whether premiums actually offset that increase or simply deferred it

Run your replacement pipeline projection: at current breeding allocation and reproductive performance, will you have the heifers you need in 2028?

If “hard to breed” or “lower producing” remain your primary beef allocation criteria, the room for instinct-based allocation has narrowed sharply

Check your culling rate—if you’ve dropped below 30%, you’re likely masking a shortage rather than solving it—and check your SCC trends while you’re at it

Ask your processor what they value. If you can demonstrate a documented 24-month replacement pipeline, you may be in a stronger negotiating position than you realize

Opportunity signal: Balanced breeding programs with adequate heifer inventory could mean more favorable processor contracts as competitors struggle to guarantee supply

Key Takeaways

The 800,000-head shortage is locked in through 2026. Breeding decisions made today won’t produce milking cows until 2028-2029. The next 18 months are about managing what’s already baked in.

Don’t confuse gross premium with replacement reality. Across the industry, the collective shift drove replacement costs up $1,870 per head. For operations now buying replacements, the premium captured doesn’t come close to covering the increase in costs.

The 18% pregnancy rate threshold matters. Below that level, aggressive beef allocation creates unavoidable replacement shortfalls regardless of premium levels.

$10 billion in new dairy plants through 2027 means processor demand for milk keeps climbing while replacement supply stays pinched. Processors are likely choosing partners rather than just buying milk.

The Bottom Line

The operations that survive this won’t be those who avoided beef-on-dairy—many of the largest, most sophisticated dairies bred heavily to beef. They’ll be the ones who tracked replacement pipeline math while capturing premiums, rather than assuming the check today wouldn’t create a bill tomorrow.

Where does your operation sit on that spectrum—and what does your 2026 breeding sheet say about the answer?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

High-Value Crosses: The Next Phase of the Beef-on-Dairy Revolution – Breaks down advanced terminal crossbreeding strategies that maximize carcass value without sacrificing your herd’s future. It delivers the blueprints for “Elite Beef” programs that command significantly higher premiums than standard auction barn crosses.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

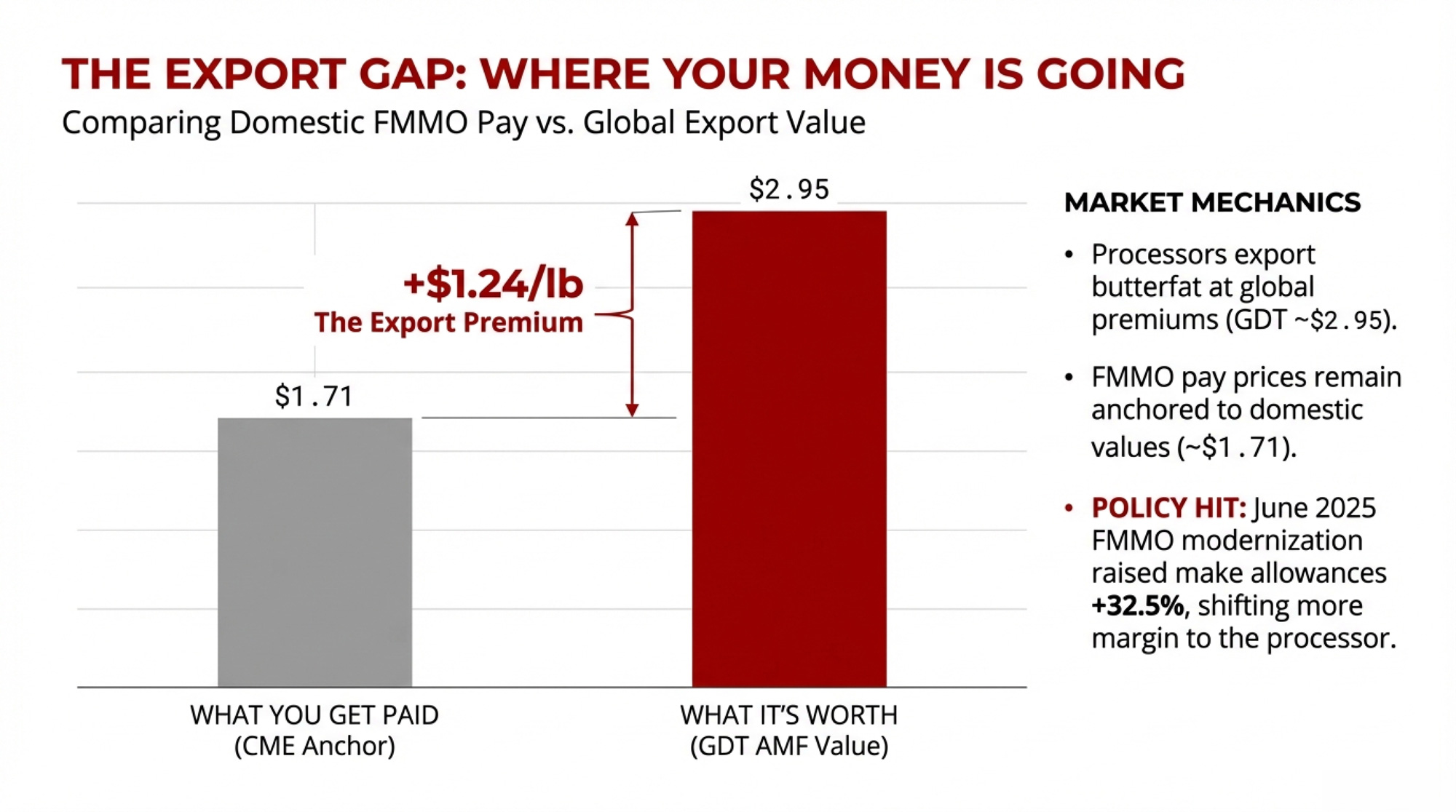

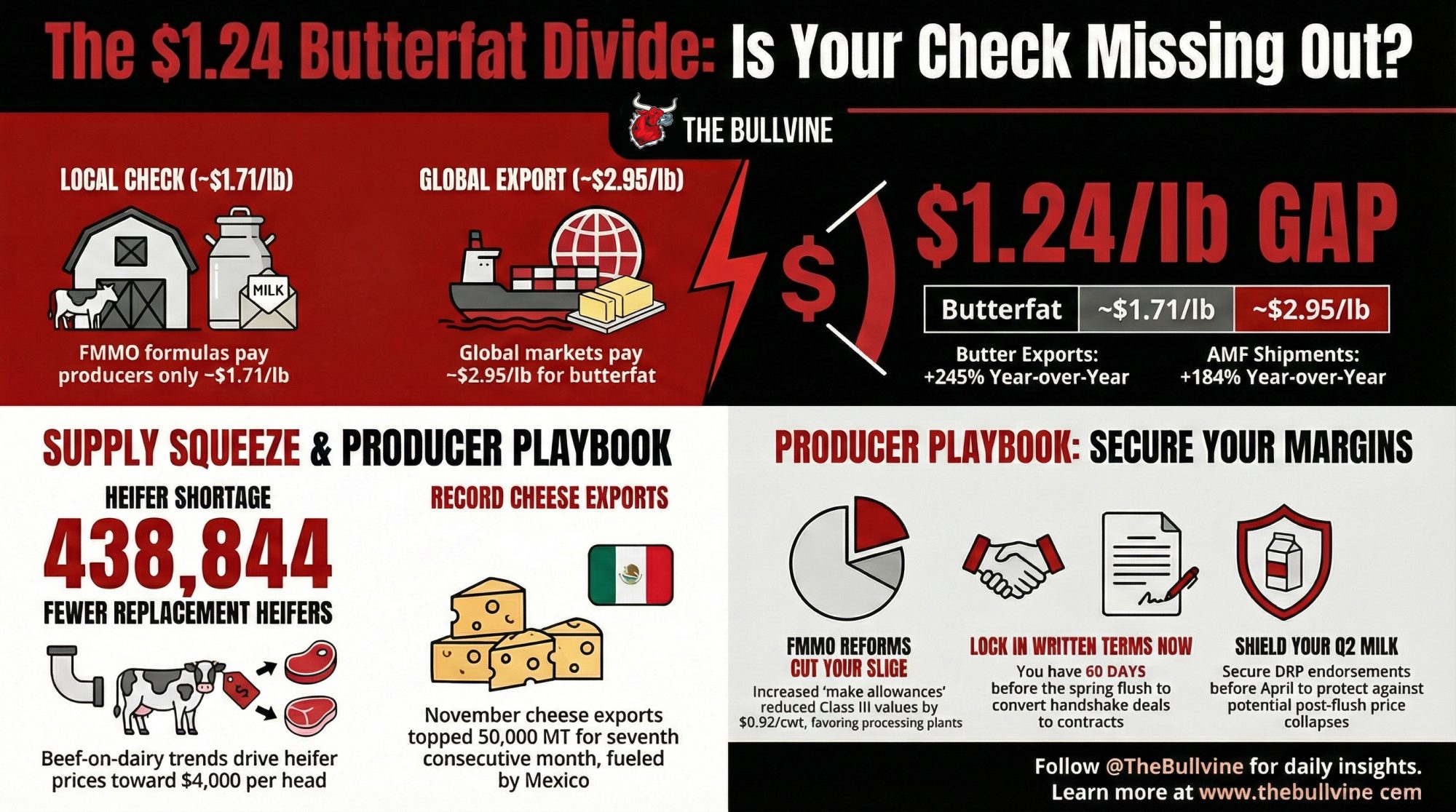

Processors are exporting your butterfat at roughly $2.95/lb while the FMMO pays you based on ~$1.71. Here’s how that gap formed — and what you need to lock in before spring flush closes the window.

EXECUTIVE SUMMARY: Your butterfat is worth $2.95/lb on the global market. The FMMO pays you based on $1.71. That $1.24/lb gap — exposed in USDA’s December 2025 report — flows to processors exporting record butter and AMF volumes, not to the producers making the components. June’s FMMO modernization widened the divide: raised make allowances cut Class III by $0.92/cwt handing plants a bigger slice while yours shrank. Supply pressure is building from the other direction — CoBank projects 438,844 fewer replacement heifers by 2026, with prices at $3,010–$4,000/head, just as $10 billion in new processing capacity needs milk. Component-focused operations in deficit regions have roughly 60 days before the spring flush to convert handshake deals into written terms. After that, the leverage shifts.

Cheese blew past expectations. Butter missed — again. NFDM production fell, but stocks climbed anyway. When USDA dropped the December 2025 Dairy Products report on February 5, 2026, futures barely flinched. Everything traded flat except powder, which caught immediate sell-side pressure.

The headline numbers look simple enough: total cheese at 1.28 billion pounds (+6.7% year over year), butter at 204 million pounds (+2.0%), nonfat dry milk at 127 million pounds (down 2.7%), per USDA NASS. But underneath those percentages sits a widening disconnect between the global value of your components and what actually shows up on your milk check — a gap that should be front-of-mind for every component-focused operation heading into spring 2026.

For the component-focused operations tracking their butterfat premium against the blend, December’s milk check told a familiar story: the premium was up, but not nearly as much as the export math suggested it should be. The rest of the value? It left the country.

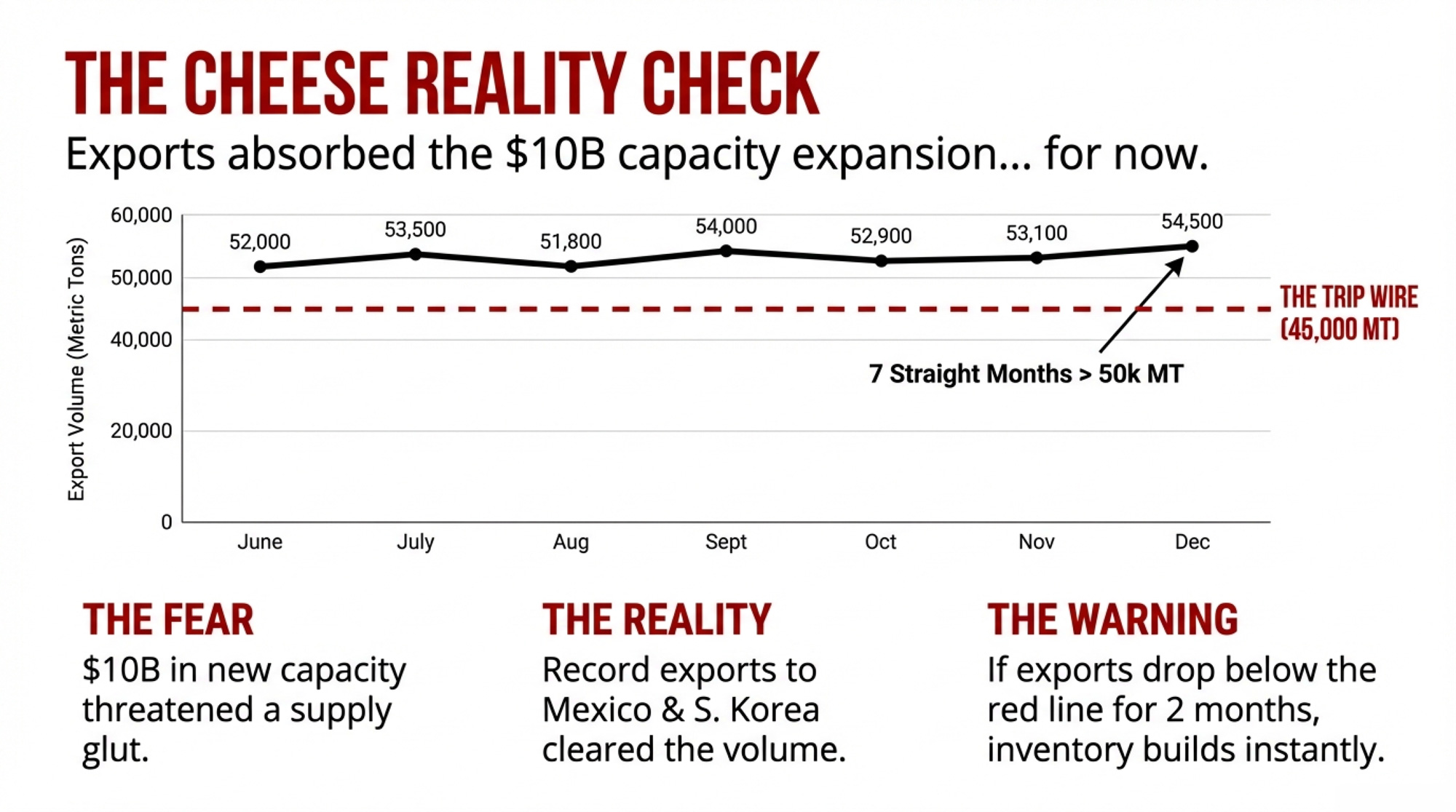

Cheese: $10 Billion in Capacity, and the Export Machine Is Absorbing It

Cheddar alone hit 340,350 thousand pounds in December — up 9.0% from a year ago. Not a one-month blip. Full-year 2025 cheddar finished 5.3% above 2024, and total cheese came in 2.9% higher. Italian types weren’t far behind: mozzarella up 5.9%, Parmesan up a striking 22.9%.

Announced U.S. dairy processing investments total roughly $10 billion through 2027, according to CoBank. The industry braced for a glut that would crush the board.

It hasn’t happened — because export demand ate through the extra volume. USDEC’s January 2026 trade summary puts November 2025 cheese exports at 50,775 metric tons, up 28% year over year. That’s the seventh consecutive month above 50,000 MT — a threshold never breached before 2025. Volume rose significantly to Mexico and South Korea, which USDEC says is “poised to set an annual record for U.S. cheese purchasing.” Southeast Asia cheese exports surged 92%.

Month

U.S. Cheese Exports (MT)

YoY Change (%)

Status vs. 50k MT Threshold

May 2025

51,240

+18%

✓ Above

June 2025

52,890

+22%

✓ Above

July 2025

53,470

+24%

✓ Above

Aug 2025

51,920

+21%

✓ Above

Sept 2025

54,110

+26%

✓ Above

Oct 2025

52,650

+23%

✓ Above

Nov 2025

50,775

+28%

✓ Above

But 28% export growth isn’t a number you can bank on forever. Here’s the threshold worth watching: if monthly cheese exports drop below 45,000 MT for two consecutive months while new plants keep ramping, domestic inventories will build faster than the market can clear. That’s not a prediction. It’s a trip wire.

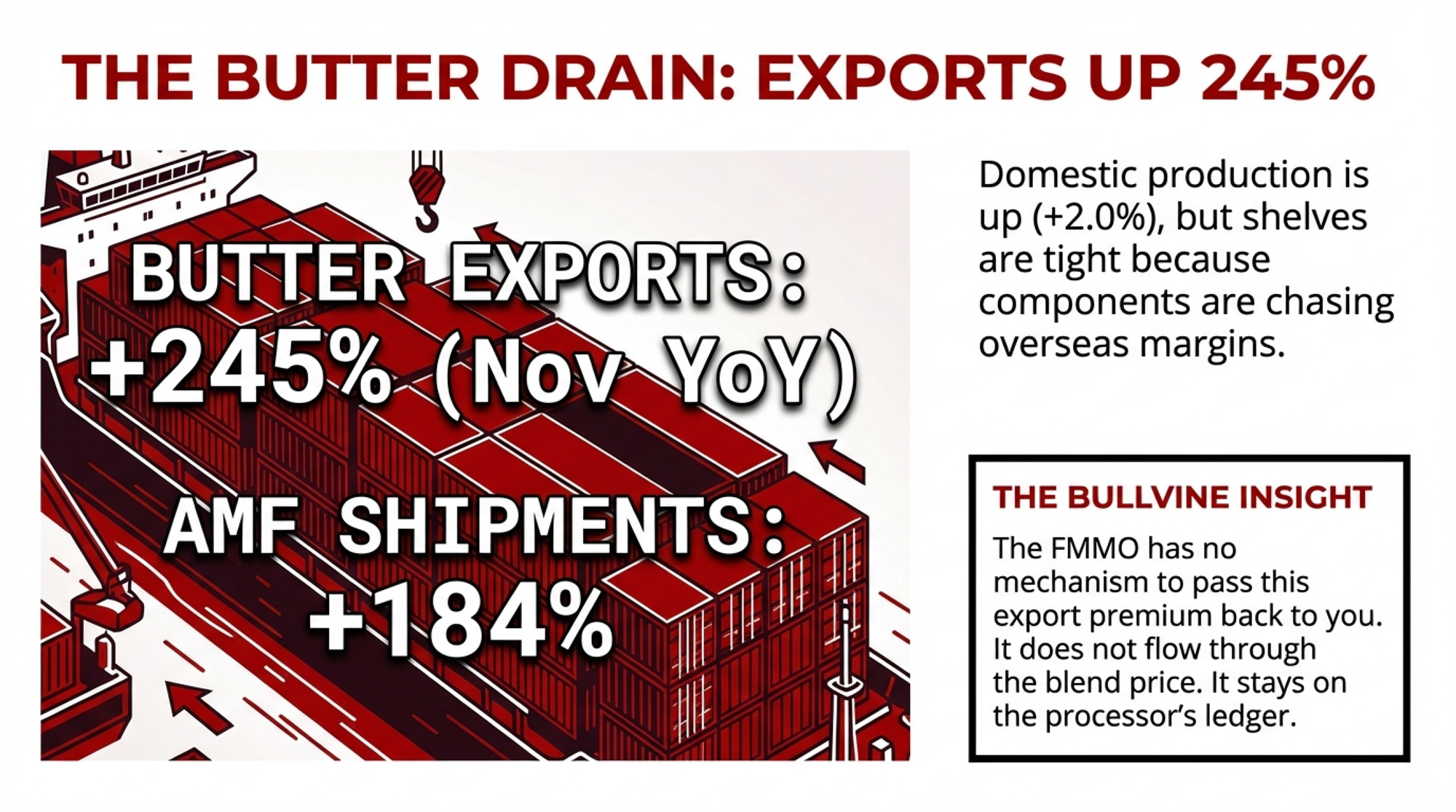

Butter: Your Fat Leaves the Country at ~$2.95. Your Check Reflects ~$1.71.

Butter production came in at 203,848 thousand pounds, just 2.0% above December 2024. Full-year 2025 butter was up 5.7% — not a collapse — but December fell well short of private forecasts for the second straight month. USDA’s January 23 Milk Production report showed December output in the 24 major states at 18.8 billion pounds, up 4.6%year over year, with 222,000 more cows and 42 more pounds per cow generating plenty of cream.

So where’d all the butter go? Overseas. Where the margins are.

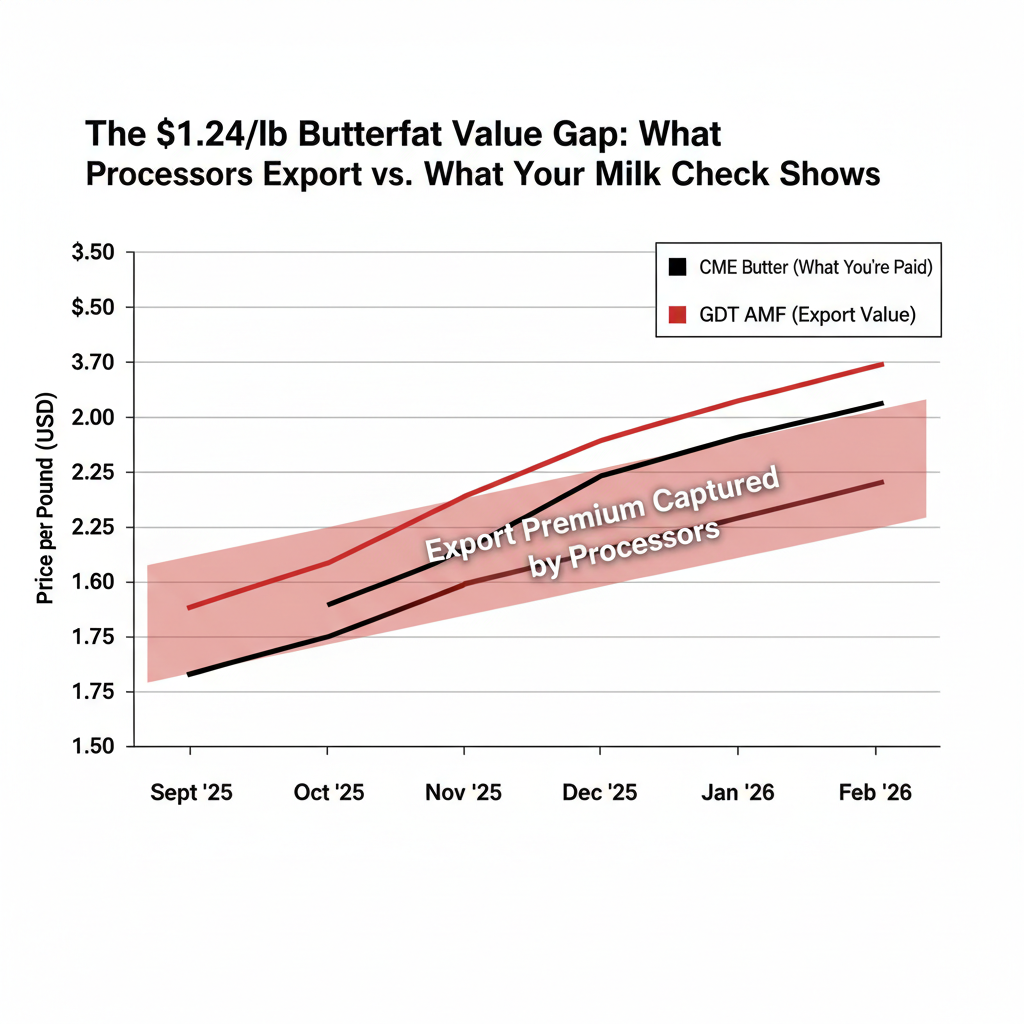

Per the CME cash dairy trade the week of February 3 (prices as of February 5, 2026), spot butter closed at approximately $1.71/lb, up from around $1.58 earlier in the week. GDT futures for February 2026 delivery had butter at roughly $2.64/lb and anhydrous milk fat at roughly $2.95/lb, per the Daily Dairy Report. That’s a spread of about $0.93/lb between CME and GDT butter — and $1.24/lb between CME butter and GDT AMF.

USDEC confirms processors are leaning hard into that spread. November butter exports surged 245% year over year. AMF shipments jumped 184%. USDEC called it the highest single month on a milk-fat basis for U.S. dairy exports — total butterfat exports reached 15,308 metric tons.

Now stack FMMO math on top. The June 2025 Federal Order modernization raised the butter make allowance from $0.1715/lb to $0.2272/lb — a 32.5% increase, per the USDA final rule published January 17, 2025. The changes “lowered the value of producer milk,” with the new cheese make allowances alone reducing the Class III price by $0.92/cwt.

The formula changes gave plants a bigger slice of the value pie. Your slice got smaller.

You produce the butterfat. Your plant converts it to 82% butter or AMF and sells it into an export channel, priced off GDT. Your milk check stays anchored to CME butter minus a bigger make allowance. The FMMO has no mechanism to pass that export premium back to you. Not through your blend price. Not through your component premium.

Product / Metric

CME Price ($/lb)

GDT Price ($/lb)

Spread ($/lb)

Value Gap per Tanker

Butter (82% fat)

$1.71

$2.64

+$0.93

~$5,580

Anhydrous Milk Fat

$1.71*

$2.95

+$1.24

~$7,440

Your Butterfat (3.7% test)

Based on $1.71 CME

Actual export value $2.95

+$1.24

~$7,440

Per Cwt Impact (80 lb/cwt @ 3.7% BF)

Paid ~$5.06/cwt BF

Worth ~$8.74/cwt BF

-$3.68/cwt

-$221/tanker

One partial exception worth investigating: if you’re a co-op member, your cooperative may return a share of export value through patronage dividends or retained earnings. Pull your co-op’s annual financial statement. Ask the question directly at your next member meeting. You might not like the answer — but you deserve to know it.

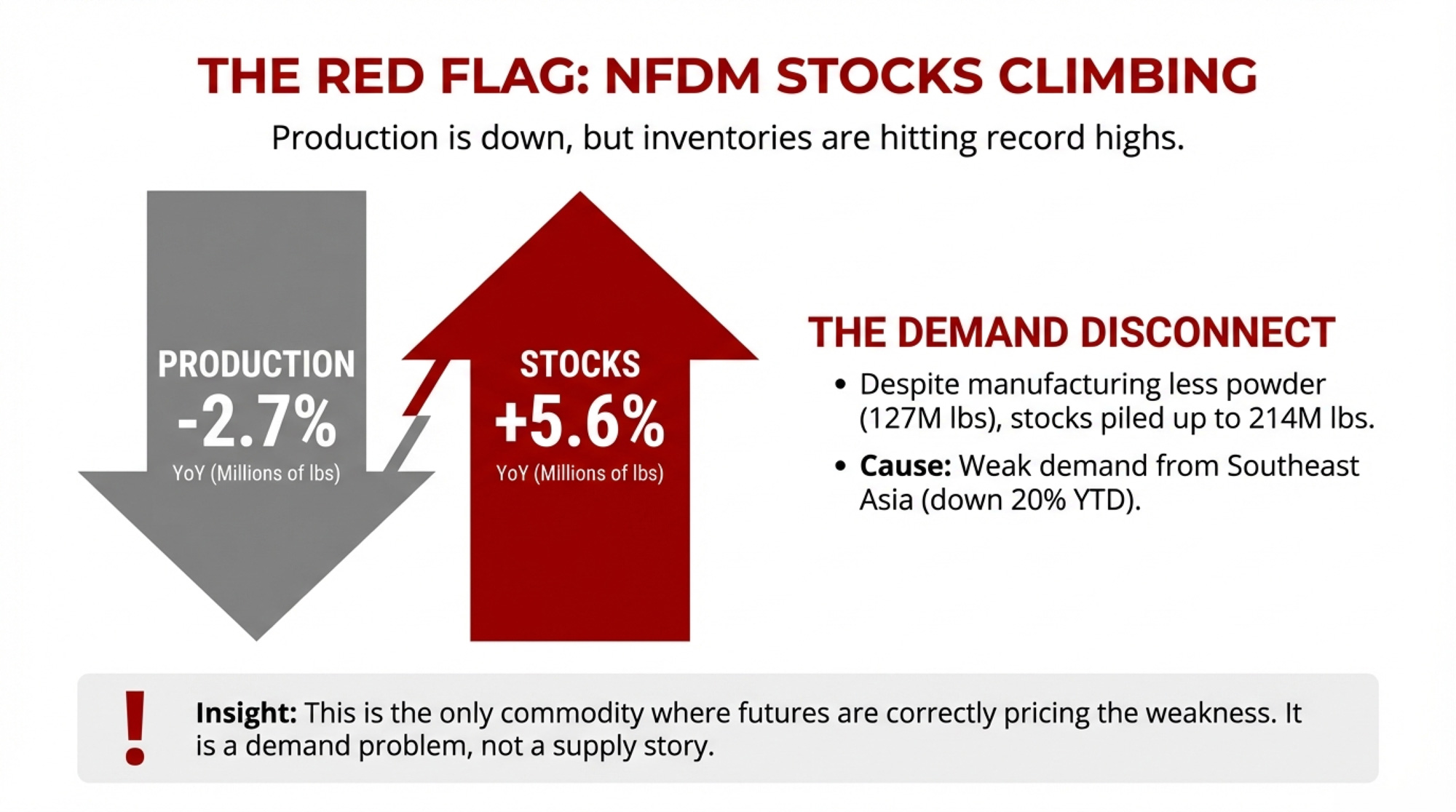

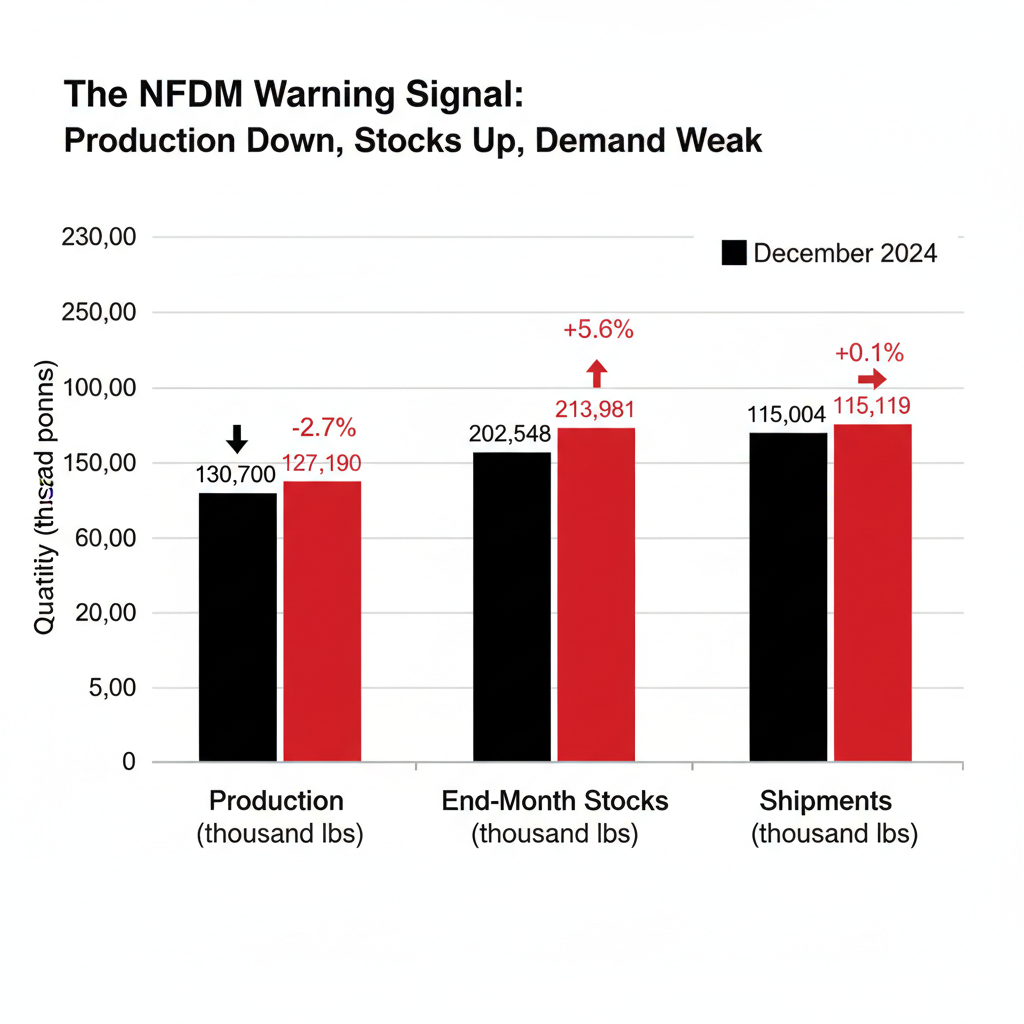

NFDM: Production Down, Stocks Up — Powder Took the Only Futures Hit

This is where the December report sent its clearest signal, and the one place futures actually listened.

December NFDM production came in at 127,190 thousand pounds, down 2.7% year over year. Skim milk powder dropped even harder — down 15.2%. If you only saw the production side, you’d assume a tightening powder complex.

Category

Dec 2024

Dec 2025

Change

Production

130,700

127,190

-2.7% ↓

End-Month Stocks

202,548

213,981

+5.6% ↑

Shipments

115,004

115,119

+0.1% →

End-of-month manufacturer stocks told a different story: 213,981 thousand pounds, up 5.6% from 202,548 a year ago. NFDM shipments were essentially flat at 115,119 thousand pounds (+0.1%). USDEC’s trade data through three quarters showed total export volume up only 1.7% through September, while powder shipments to Mexico and Southeast Asia posted year-over-year declines. USDEC directly noted that “a decline in exportable supplies of milk powder from the U.S., combined with tepid demand from SEA, has caused volumes into the region to fall.”

November did bring a rebound in Southeast Asian powder shipments — NFDM/SMP to the region jumped 23%, driven almost entirely by Indonesia — but year-to-date milk powder exports to Southeast Asia were still down 20% through November.

Falling production. Rising stocks. Flat-to-weak exports. That’s a demand problem, not a supply story.

The Quiet Whey Shift: Putting a Floor Under Class III

One number buried in this report deserves your attention. Whey protein isolate production jumped 11.7% year over year to 20,644 thousand pounds, while WPI stocks fell 5.4%. Consumer demand for high-protein products is pulling whey streams into higher-value WPI — human dry whey was up only 4.0% despite 6.7% more cheese generating more liquid whey.

Because dry whey feeds the Class III formula, that structural pull is quietly supporting one of the inputs that determines your Class III price. If you’re on Class III, your dry whey component isn’t eroding the way the powder side is. Small bright spot in a complicated picture.

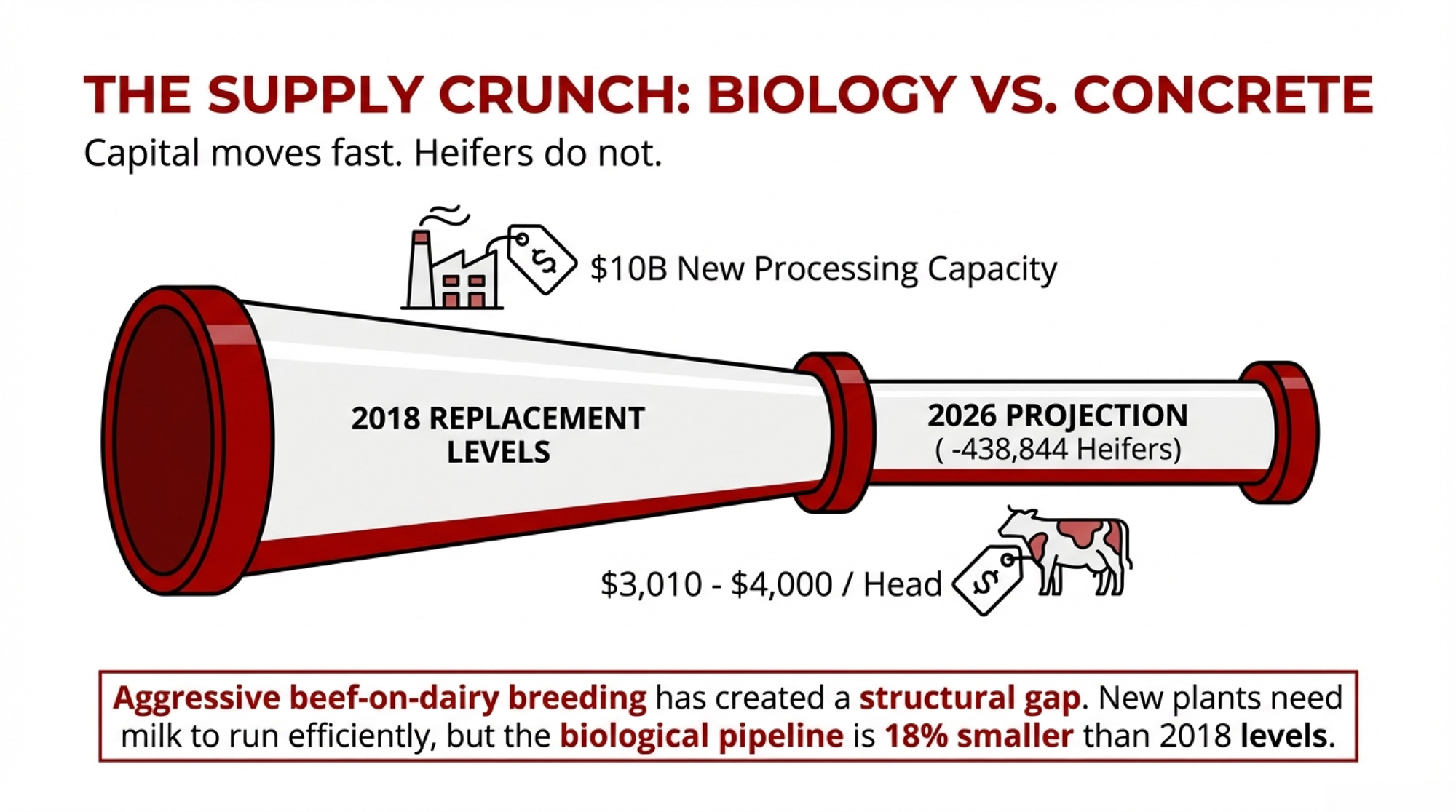

438,000 Fewer Heifers vs. $10 Billion in Hungry Plants

Every capacity story runs into the same wall. Biology doesn’t move at the speed of capital.

CoBank’s Corey Geiger projected in August 2025 that U.S. dairy heifer inventories would shrink by 438,844 head between 2025 and 2026, driven by beef-on-dairy breeding decisions that sent skyrocketing volumes of beef semen into dairy herds — 7.9 million units in 2024 alone, per NAAB data. Over two years, CoBank estimates the total decline could reach roughly 800,000 fewer replacement heifers, with a rebound starting in 2027. USDA’s January 2025 Cattle report showed 3.914 million dairy replacements — 18% fewer than in 2018.

Year

Heifer Inventory (million)

Cumulative Capacity Investment ($B)

2024

3.91

$2.5

2025

3.69

$5.8

2026

3.47

$8.5

2027

3.58 (projected rebound starts)

$10.0

December 2025 milk production still looked strong — up 4.6% in the 24 major states with 222,000 more cows and 42 more pounds per cow. But USDA’s January 2026 WASDE pegs 2026 production at 234.3 billion pounds, up roughly 1.4% from 2025, as a thinning replacement pipeline starts to constrain herd expansion.

Geiger didn’t sugarcoat it: “The short answer is that it will be tight. Those dairy plants will require more annual milk and component production, largely butterfat and protein. And it will take many more dairy heifer calves in future years to bring the national herd back to historic levels.”

Heifer prices already reflect the squeeze, from $1,720/head in April 2023 to roughly $3,010 by mid-2025 per the USDA’s July 2025 Agricultural Prices report. Top dairy heifers in California and Minnesota auction barns were bringing upwards of $4,000 per head by mid-year 2025, according to CoBank.

Why Flat Futures Don’t Mean the Fundamentals Are Wrong

If all this tension is real, why did cheese and butter futures trade flat on report day?

Near-term data wasn’t wildly off expectations. Cheese was already strong in November. Butter’s miss fit the ongoing “tight but not panicked” narrative. NFDM was the exception because rising stocks directly contradicted the bullish price story—a signal even a thin market could quickly process.

The deeper issue is structural. Dairy futures trade at a fraction of the open interest depth seen in cattle or hog contracts. That’s not a market that can efficiently price a two-year heifer decline or a multi-year butterfat export arbitrage. The flat response isn’t the market disagreeing with the fundamentals. It’s the market admitting it can’t fully express them.

And that gap between what futures say and what the fundamentals show? That’s where the opportunity sits for producers paying close attention.

What This Means for Your Operation

Your butterfat is underpriced relative to global value. As of February 5, 2026: GDT AMF at roughly $2.95/lb; CME butter at approximately $1.71/lb. Your Class IV price is anchored to CME plus a bigger make allowance. Component optimization still pays inside the system, but the extra export margin sits on the processor’s ledger. The spread to watch: if CME stays below $1.80 while GDT holds above $2.50, processors have no incentive to redirect cream to domestic channels, and your Class IV component value stays compressed. Pull your last three milk checks. Compare your butterfat premium per hundredweight to the CME butter price on those settlement dates. The gap between what you’re getting and what GDT says your fat is worth — that’s the number this article is about.

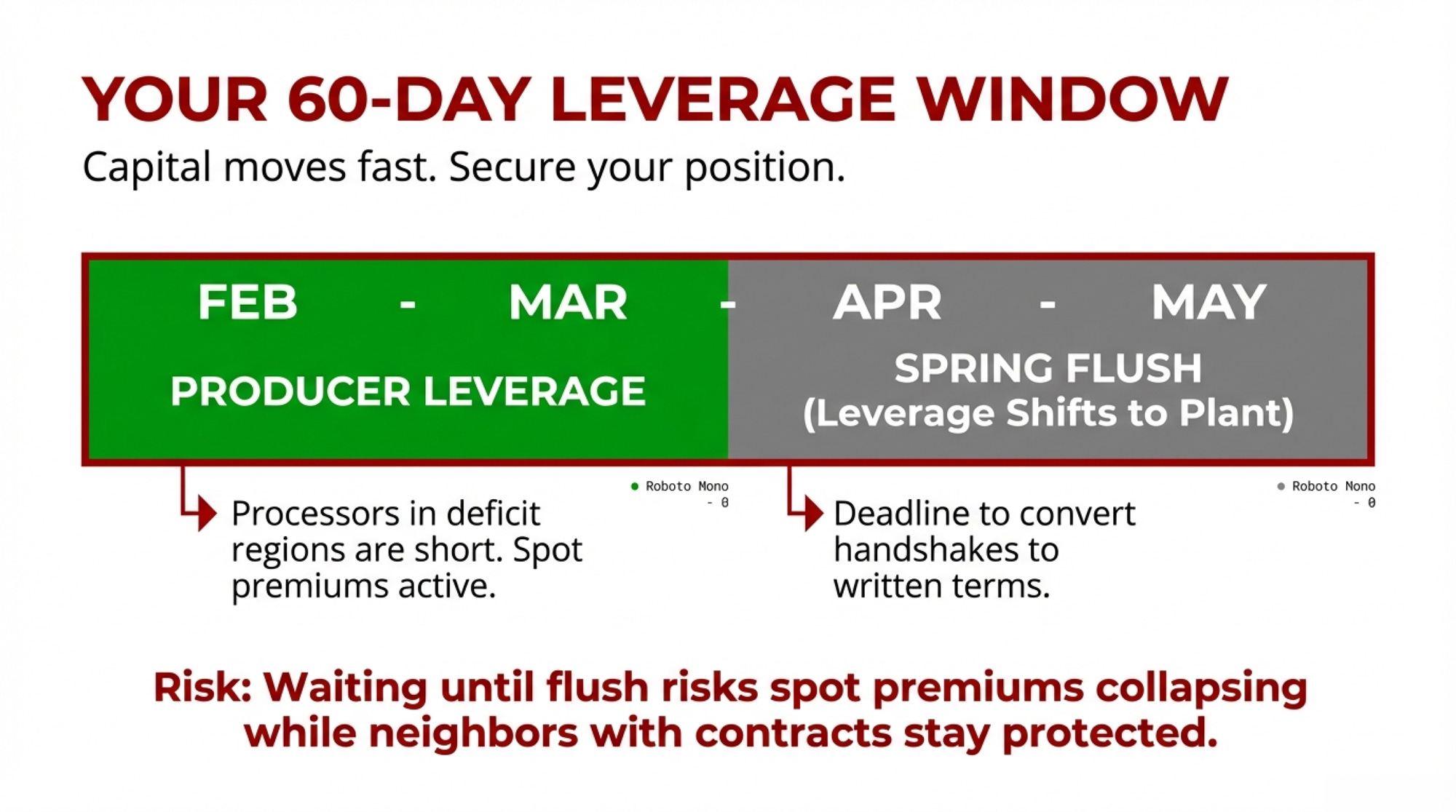

If you’re in a deficit region, your leverage is real — but it has a shelf life. Processors in short areas are paying to secure a supply right now. That urgency fades as cooperatives formalize long-haul logistics and spring flush arrives in April–May. The most important move in the next 60 days isn’t a hedge — it’s getting written terms on component premiums, hauling, and volume commitments while plants still feel short. Twelve-to eighteen-month agreements balance security with flexibility. The trade-off: if spot premiums spike higher than your locked rate during peak shortage, you’ll watch neighbors on handshake deals get paid more. But you’ll also sleep through the months when premiums collapse post-flush.

Watch NFDM stocks, not price. If manufacturer stocks hold above 210 million pounds through the March report while exports stay flat, that’s your signal to layer in Class IV put protection before spring flush. DRP Q2 2026 endorsements (April–June milk) are mostly written in the late-January to March window, outside of USDA report release days when sales are suspended. You want protection in place before April, not after.

Run the heifer math before you bid. At $3,500/head (midpoint of the $3,010–$4,000 range CoBank reported) and current carrying costs — Penn State Extension’s most recent data puts total rearing costs at roughly $1.60–$2.82 per head per day depending on operation type and region — a heifer needs to enter your string within about 24 months to break even against buying a fresh cow. But retaining heifers ties up capital and bunk space for 22+ months before they generate a dollar of milk revenue. Buying springers costs more per head but puts milk in the tank within weeks. Your cash flow position — not just the per-head price — should drive this call.

Check your Federal Order’s Class IV exposure. If you’re in Order 5 (Appalachian) running high Class I utilization, the differential increases from the June 2025 reforms may partially offset the make allowance pain — analysis found Orders 1, 5, 7, and 33 gained value under the new structure, while Order 30 (Upper Midwest) lost value. Run your margin-over-feed calculation against current component values to see where your breakeven actually sits under the new formulas.

Federal Milk Marketing Order

Order #

Value Impact

Primary Driver

Northeast

1

Gained Value

Higher Class I differentials offset make allowance increases

Appalachian

5

Gained Value

High Class I utilization + differential increases

Southeast

7

Gained Value

Class I differential structure favorable

Upper Midwest

30

Lost Value

Heavy Class III/IV exposure + make allowance cuts hit hard

Mideast

33

Gained Value

Class I differential gains exceeded component losses

Key Takeaways

Cheese is running hot but roughly in balance thanks to record exports — November was the seventh straight month above 50,000 MT. The risk trigger: monthly exports below 45,000 MT for 2 consecutive months while new plants keep coming online.

Butterfat is where the value gap is widest. CME butter at ~$1.71/lb vs. GDT AMF at ~$2.95/lb as of February 5, 2026, represents a $1.24/lb spread that FMMO pricing doesn’t capture for producers. Co-op members: ask what share, if any, flows back through patronage.

NFDM sent the clearest warning in this report. Stocks up 5.6% while production fell 2.7%, and year-to-date powder exports to Southeast Asia were down 20% through November — that’s the pattern that precedes price weakness, not strength.

The heifer shortage is real and has come at a bad time. It won’t choke production in 2026, but by 2027 — when new plants need to run full — the math stops working without more replacements than the pipeline can deliver.

Check your DRP windows. Q2 2026 endorsements are mostly written in the late-January to March window. If NFDM stocks stay elevated and spring flush hits Class IV values, you want coverage locked before April.

The Bottom Line

The next two months aren’t about whether exports stay strong or heifers tick up another $200. They’re about whether you’ll have written terms — or still be on a handshake — when your plant decides who to lock in for the next cycle. And whether the terms you’re milking under today reflect even a fraction of what your components are actually worth on the global market.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

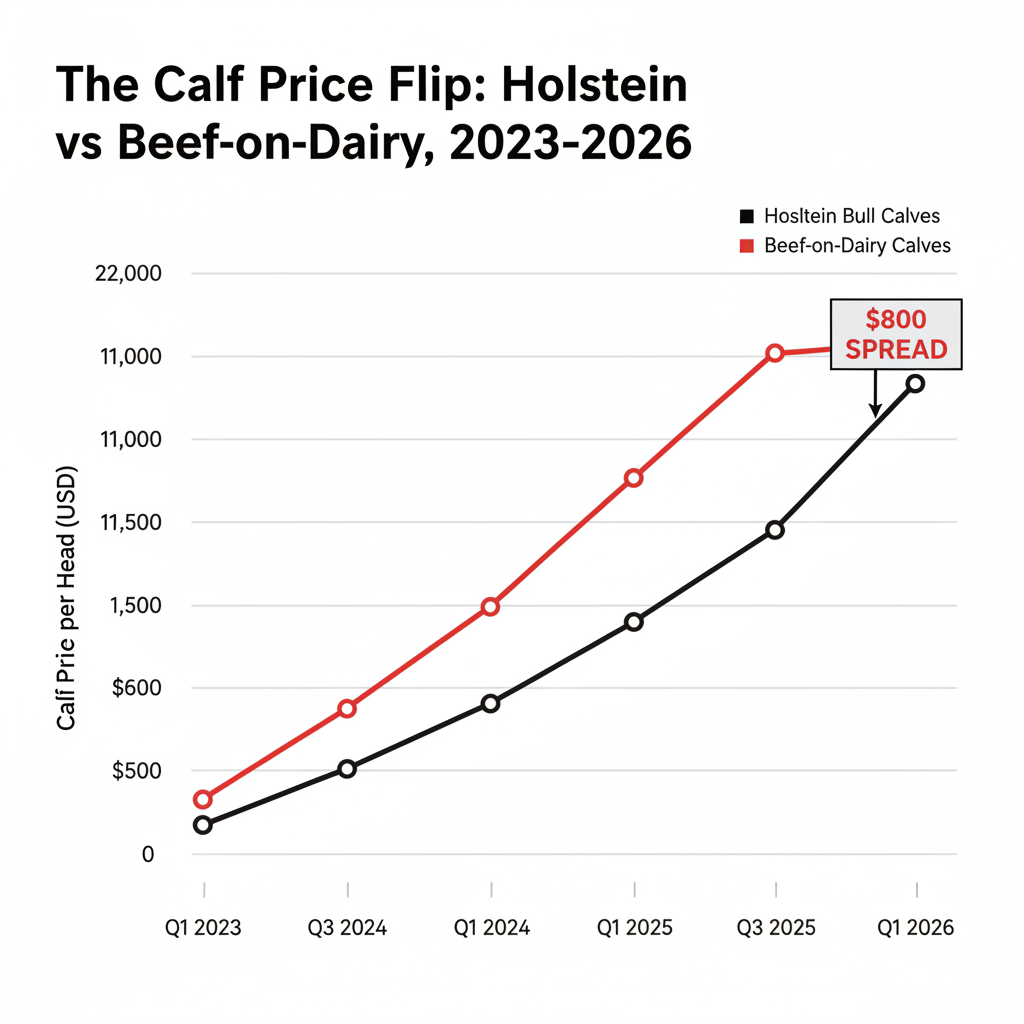

Holstein bulls at $800. Beef‑on‑dairy at $1,750. Same cow, same calving—double the cheque. Why are you still breeding everything Holstein?

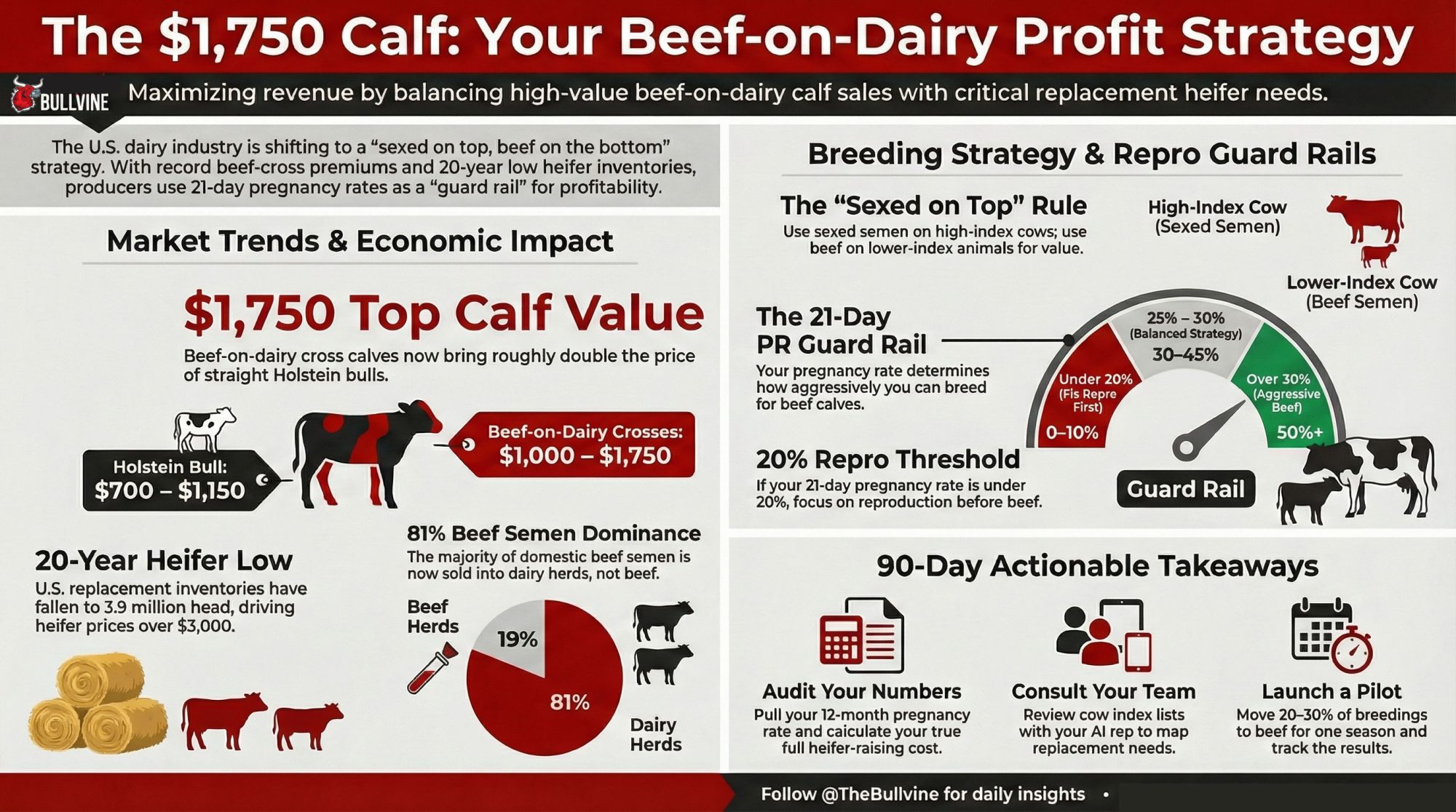

EXECUTIVE SUMMARY: In many U.S. sale barns today, Holstein bull calves that once brought $300–$450 are now commonly in the $700–$1,000 range in stronger markets, while well‑bred beef‑on‑dairy calves are cashing cheques up to about $1,750 in some auctions. At the same time, U.S. replacement heifer inventories have fallen to a 20‑year low near 3.9 million head as processors invest roughly $10 billion in new and expanded plants that will need milk to run. That combination has pushed 81% of domestic beef semen sales into dairy herds and made the “sexed on top, beef on the bottom” strategy hard to ignore. The catch is that it only pays long‑term if your 21‑day pregnancy rate stays above about 20% and you have heifers to spare, with herds in the 30–40% band able to run 50% or more of their breedings to beef while herds under 25% are usually better off fixing repro first. Three Wisconsin families—Hillview, Hiemstra, and Dornacker—show how registered Holsteins, a soil‑driven 170‑cow system, and a ProCROSS robot herd are all turning those same numbers into very different but profitable plans. By the end, you’ll know which of three breeding “paths” your own numbers put you in and what to do over the next 90 days to match sexed and beef semen to your repro, heifer, and calf markets.

In strong Wisconsin markets, beef‑on‑dairy calves are bringing up to about $1,750 a head and Holstein bull calves are often in the $800–$1,000 range, with top sales in other regions breaking the $1,000 mark as well. U.S. milk replacement heifer inventories are down to roughly 3.9 million head as of January 1, 2026—a 20‑year low—with CoBank warning they could shrink another 800,000 head before 2027. At the same time, 81% of domestic beef semen now goes into dairy cows, not beef herds. If you’re breeding cows, managing heifers, or signing milk and cattle contracts in 2026, that mix isn’t background noise. It’s the math that decides whether your breeding program keeps you ahead of the curve or leaves you short of replacements when the processor wants more milk.

Quarter

Holstein Bull Calf Price (USD)

Beef-on-Dairy Calf Price (USD)

Spread (USD)

Q1 2023

$350

$800

$450

Q3 2023

$450

$1,100

$650

Q1 2024

$600

$1,350

$750

Q3 2024

$750

$1,500

$750

Q1 2025

$850

$1,600

$750

Q3 2025

$900

$1,700

$800

Q1 2026

$950

$1,750

$800

If you’re already selling calves, buying semen, and watching heifer checks climb, this is aimed squarely at you. The question isn’t “Should I try beef‑on‑dairy?” anymore. It’s: given your repro numbers and heifer pipeline, how hard can you lean into beef‑on‑dairy without blowing a hole in your future fresh pen?

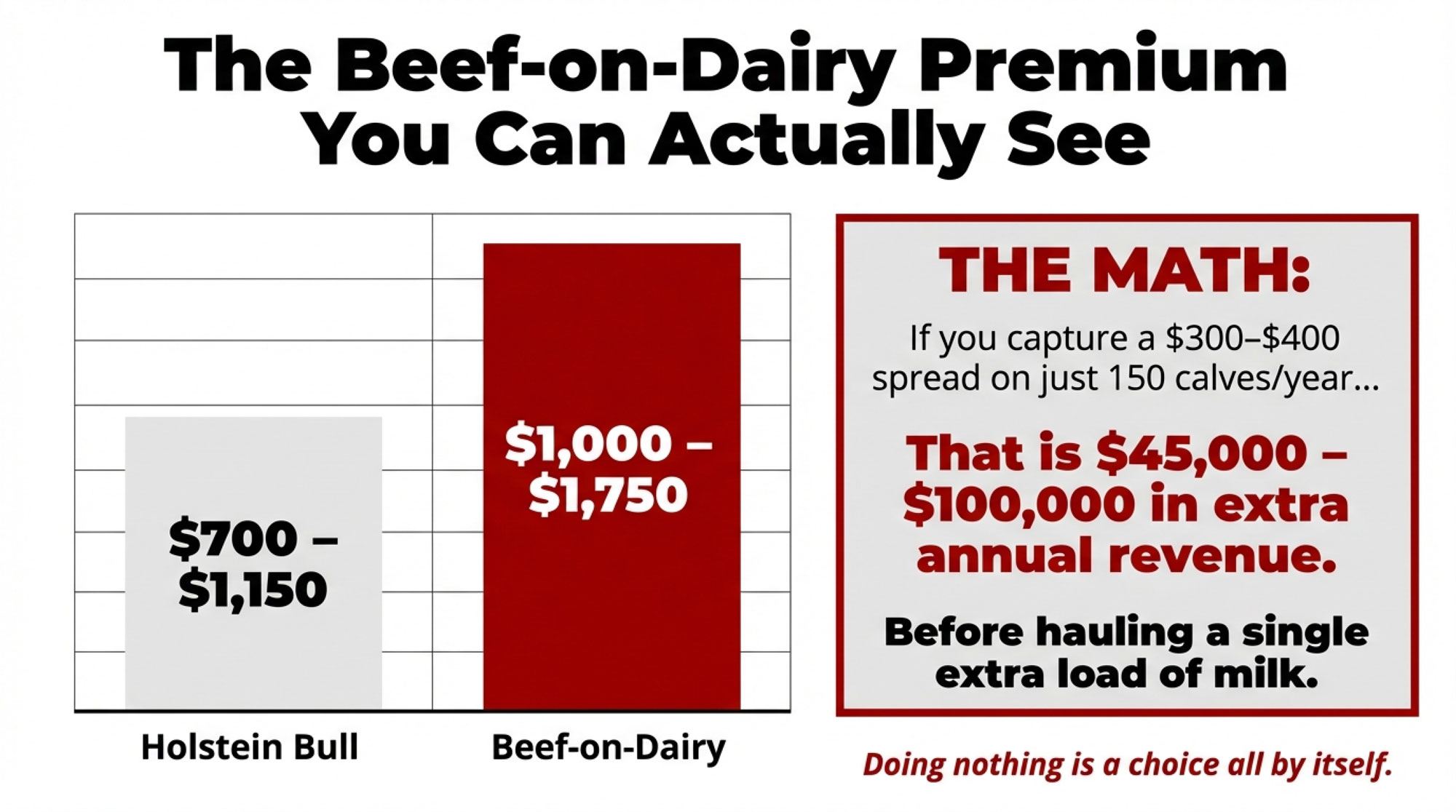

The Beef‑on‑Dairy Premium You Can Actually See

For years, bull calves were the side hustle. They helped pay a bill or two but didn’t change your year.

That flipped in late 2023 and into 2024. In sale barns across Wisconsin and Pennsylvania, newborn Holstein steer calves were bringing about $300–$450 per head, while beef‑cross calves hit as high as $1,750. Since then, a string of 2024–2025 market reports has pushed both numbers higher, with 2025 coverage noting newborn beef‑cross calves topping $1,500–$1,600 in Wisconsin and Premier’s January 2026 report listing beef‑dairy cross calves at $1,000–$1,750 and most Holstein bulls at $700–$1,150.

Sale reports from central U.S. barns tell a similar story. At South Central Livestock Exchange in 2024, “baby calf” reports—a mix of dairy and dairy‑beef—showed ranges like $175–$875 and $200–$780 per head depending on quality and condition. You don’t even need a breed column to see the pattern: the top calves bring several hundred dollars more than the bottom tier.

Since those 2023–2024 reports, national summaries from CattleFax‑linked analyses have pegged average day‑old beef‑on‑dairy calves around $1,400 in some U.S. markets, more than double levels from just a few years ago, while Holstein bull calves have also climbed. Exact numbers depend on your barn, your buyer, and this week’s market. The important part is the spread between plain Holsteins and well‑sired beef‑on‑dairy calves—and that spread has stayed real.

Run that against your own numbers. If you can consistently capture even a $300–$400 per‑head spread on 150–250 calves a year by shifting from commodity Holstein bulls to well‑managed beef‑on‑dairy crosses, you’re talking roughly $45,000–$100,000 in extra annual revenue before you haul one extra load of milk. Your math will be different, but the dollars are big enough that “doing nothing” is a choice all by itself.

How Hillview Turned Beef‑on‑Dairy Into a Revenue Engine

Jauquet’s Hillview Dairy in Luxemburg, Wisconsin, is the kind of place semen companies like to put on a brochure. They milk about 650 registered Holsteins in a cross‑ventilated freestall and have already been profiled for comfort, repro, and genetics.

Herds like Hillview didn’t jump into beef‑on‑dairy for the novelty. They moved because the economics said they could get more per pregnancy. Their breeding pattern now looks a lot like what the economists have been running in their models:

Sexed Holstein semen on the top of the herd—your highest‑index cows and heifers—to generate just the replacements you actually need.

Beef semen on lower‑index cows and groups where making another heifer mostly adds cost, not value.

A structured repro program (timed AI, close fresh‑cow work, and consistent heat detection) so expensive straws aren’t wasted on sloppy timing.

An October 2021 paper in JDS Communications (“Economics of using beef semen on dairy herds”) found that once your 21‑day pregnancy rate hits roughly 20% or better, and once beef‑on‑dairy calves bring at least about 2x the price of straight Holstein bull calves, this “sexed on top, beef on the bottom” approach maximizes income from calves over semen cost—even when sexed semen is more than twice the price of conventional or beef semen.

If your current repro and local calf markets look anything like that, you’re playing in the same lane as Hillview, whether you’ve admitted it yet or not.

Josh Hiemstra: Beef‑on‑Dairy as a Whole‑Farm System

Not every story here is about a big registered Holstein herd. Some are about getting every acre to pull its weight.

Hiemstra Dairy in Brandon, Wisconsin, milks about 170 cows and farms roughly 790 acres of owned and rented land in western Fond du Lac County. Josh Hiemstra farms with his family and has been profiled for his cover crops and soil‑health focus; he thinks in rotations and roots as much as in pounds and litres.

In a 2024 Farm Progress feature, Josh laid out how beef‑on‑dairy fits his plan. He’d just sold a load of beef‑on‑dairy steers and heifers that averaged 1,400 pounds and brought $1.75 per pound—about $2,450 per head. Then came the line that stuck with a lot of dairymen:

“I could have been smart and sold them as baby calves,” he admits.

He didn’t, because on his farm:

He can push more corn through finishing cattle than through the milking herd.

Older infrastructure—tower silos, a conventional parlor—fits a mixed dairy‑plus‑beef setup just fine.

Cover crops and “odd” forages that don’t slot neatly into a high‑producing TMR fit nicely into beef rations.

For Hiemstra, beef‑on‑dairy isn’t a side hustle bolted onto a dairy. It’s part of a whole‑farm plan to make soil, feed, facilities, and cattle all pull in the same direction.

Heifers at a 20‑Year Low and a $10 Billion Stainless Build‑Out

Calf cheques feel good. Realizing you’ve starved your heifer pipeline does not.

CoBank’s August 2025 report “Dairy Heifer Inventories to Shrink Further Before Rebounding in 2027” pegs U.S. dairy replacement heifer inventories at a 20‑year low and projects they’ll shrink by another 800,000 head before they regain ground in 2027. USDA’s January 1, 2026, cattle report backs that up, putting milk replacement heifers at about 3.9 million head.

At the same time, CoBank highlights a “historic $10 billion” wave of new and expanded dairy processing capacity—cheese plants, ingredient plants, and value‑added facilities—set to come online through 2027. That’s a lot of new stainless chasing milk from a smaller pool of replacements.

On prices, CoBank’s Corey Geiger notes that heifer values “have reached record highs and could climb well above $3,000 per head.” Brownfield’s read on Wisconsin data shows replacement dairy animals jumping 69% in a year—from $1,990 in October 2023 to $2,850 in October 2024—with some Northwest sales “north of $4,000 per head.” Other 2025 coverage points to bred dairy heifers in many U.S. markets trading north of $3,000, with top strings clearing $4,000.

Every heifer you raise—or decide not to—now drags a much bigger number behind her than she did just a few years ago.

What Heifers Really Cost You

None of that means the right answer is to quit raising heifers. It does mean you should know, cold, what yours cost.

A 2019 economic analysis of pre‑weaning strategies found that:

Feed typically accounts for about 46% of heifer‑raising costs.

Pre‑weaning costs alone can range from roughly $259 to $583 per calf, depending on housing, milk program, and labour.

Once that calf gets to freshening, many 2024–2025 North American budgets put full heifer‑raising costs in the low‑to‑mid $2,000s per head, once you count feed, labour, interest, facilities, and death loss.

On the market side, CoBank and regional reports point to bred heifers trading around and above $3,000 per head, with special sales and select strings in some regions bringing over $4,000.

If your true cost to raise a heifer is running $2,300–$2,600, and local bred heifers are selling for $2,800–$3,200 or more, it’s perfectly rational to question the old “raise everything” reflex.

A simple rule of thumb: if your full heifer cost is consistently more than about 10–15% above the going price for solid bred heifers in your region, it’s time to pressure‑test a buy‑vs‑raise strategy with your adviser or lender instead of assuming raising is always the cheaper, safer play.

81% of Beef Semen Now Goes Into Dairy Cows

If you still think beef‑on‑dairy is a niche play for a few “progressive” herds, the semen market disagrees.

NAAB’s 2024 data shows 81% of all domestic beef semen sales now go onto dairy cows and heifers. Sexed dairy units keep climbing. Conventional dairy semen is getting squeezed from both sides.

The 2021 JDS Communications economics work predicts exactly that pattern. In its most profitable scenarios, herds:

Use sexed Holstein semen on the top‑ranked cows and heifers to generate replacements with the genetics they want.

Use beef semen on lower‑ranked or surplus animals, assuming beef‑on‑dairy calves bring at least about 2x the price of straight Holstein bull calves.

In other words, the semen sales chart already looks a lot like the recommended playbook: sexed for replacements, beef for value‑added calves, and conventional dairy semen steadily losing ground.

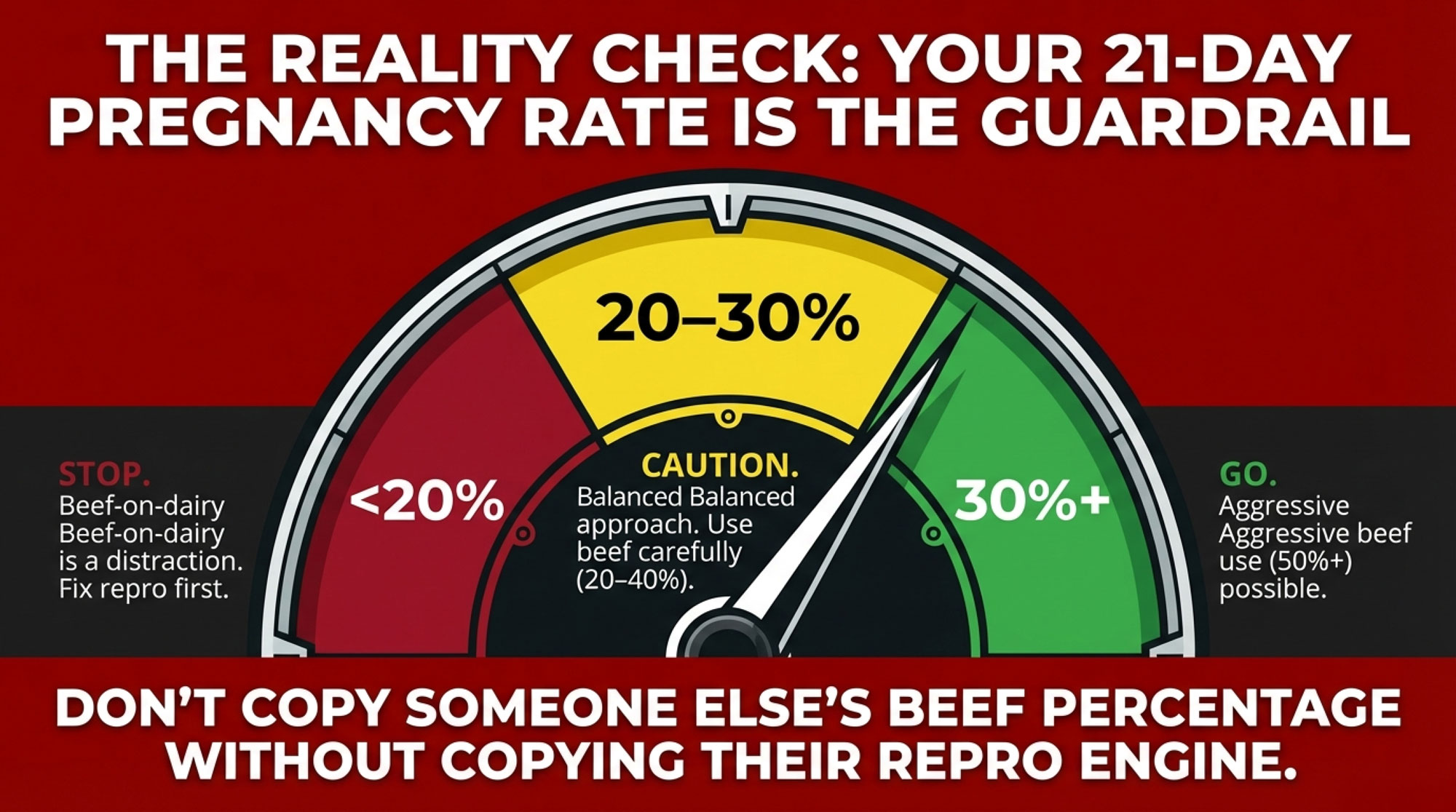

Your 21‑Day Pregnancy Rate Is the Guard Rail

Here’s where good herds quietly get themselves into trouble: copying someone else’s beef‑semen percentage without copying their repro engine.

UW–Extension work and the JDS Communications paper both land on the same idea: beef‑on‑dairy is a “spare pregnancy” business. You use pregnancies you don’t need for replacements to make higher‑value beef‑on‑dairy calves. If you’re short on pregnancies or short on heifers, chasing beef premiums can saw through your replacement pipeline fast.

High‑performing herds recognized by the Dairy Cattle Reproduction Council (DCRC) often run 21‑day pregnancy rates in the mid‑30s to low‑40s. Those herds have room to be aggressive with beef semen and still sleep at night about replacements.

If your 21‑day pregnancy rate is in the teens or low‑20s, you’re running a different race.

Here’s a simple frame based on the modelling and what the top repro herds actually do—not a law, but a practical starting point:

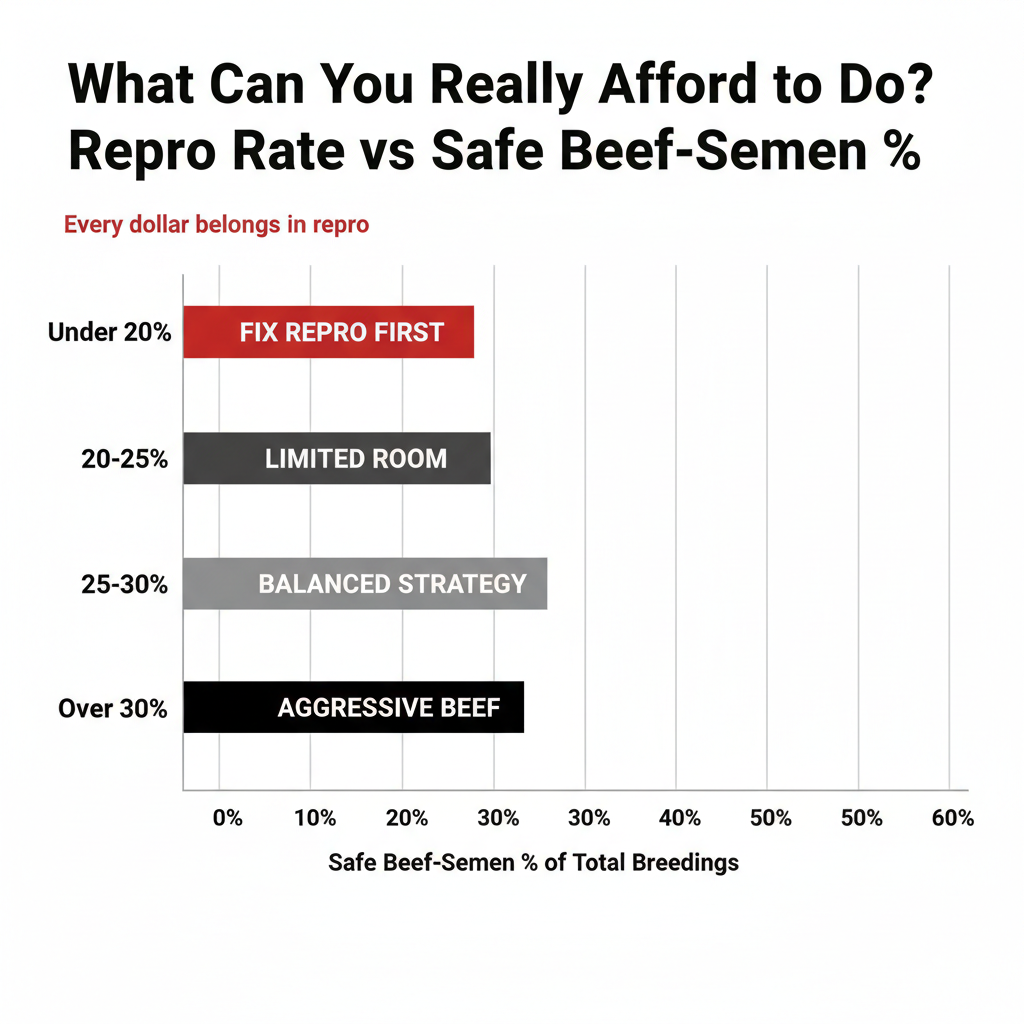

21‑Day Pregnancy Rate

Suggested Beef % of Breedings

What That Really Means

Under 20%

0–10%

Beef‑on‑dairy is a distraction; every dollar belongs in repro first.

20–25%

20–30%

Limited room; focus on sexed semen on top cows; use beef carefully.

25–30%

30–45%

A balanced “both/and” beef‑plus‑sexed strategy is realistic.

Over 30%

50%+

Aggressive beef use can work if you tightly manage the heifer inventory.

Those ranges line up with what the JDS Communications paper found and what DCRC‑type herds live every day. They’re guard rails, not commandments—but if your 21‑day PR is in the teens, cranking beef semen to 60% isn’t a bold strategy. It’s rolling the dice on your own replacement line.

Sexed Semen: The Old Knock vs the New Data

A lot of producers formed their opinions about sexed semen back when the technology was taking a 20‑point hit on conception. 2010 called. It wants those assumptions back.

A 2023 review in Animals pulled together results from multiple European and Irish studies on beef‑on‑dairy strategies. It found that modern sexed semen often hits 80–90% of conventional semen’s conception rates under good management, especially in heifers, not the steep penalty many people still quote from memory.

Both that review and the 2021 JDS Communications economics paper land on the same play:

Use sexed semen on higher‑index animals so more of your replacements come from the top of the herd.

Use beef semen on lower‑index animals to turn surplus pregnancies into calves with a better paycheque.

You may still see a few points lower conception with sexed vs conventional, depending on your handling and cow group. But if sexed semen lets you trim your heifer pipeline back to what you truly need—and frees up more pregnancies for beef‑on‑dairy calves that bring roughly double the Holstein price—the total calf‑plus‑semen line on your P&L can still climb.

So the real question isn’t “Is sexed semen good or bad?” It’s: what’s your actual cost per pregnancy with sexed, conventional, and beef semen, using your own conception rates and prices?

The Dornacker Plan: Crossbreeding, Robots, and Beef‑Ready Cows

Not every future‑proof herd is pure Holstein or built around banners.

Dornacker Prairies in Wisconsin is a fifth‑generation dairy with about 360 cows on roughly 1,000 acres, and about 90% of those acres are used to feed their own herd. Allen and Nancy Dornacker farm alongside Allen’s parents, Ralph and Arlene, and their four kids. They’ve been profiled internationally for blending robots, crossbreeding, and composting into a single system that works for their land and family.

Over the last decade, they’ve:

Installed Lely A5 robots starting in 2018, expanding from three units to six, with room for nine.

Adopted ProCROSS crossbreeding (Holstein × VikingRed × Montbéliarde) beginning in 2016 to improve fertility, health, and longevity.

Implemented composting that’s cut fertilizer purchases by about 80%.

Their crossbred herd averages around 9,200 kg of milk per cow per year (about 20,000 lb), with components near 4.6% fat and 3.6% protein—numbers that stack up nicely on a component‑based paycheque.

In a herd like that, beef‑on‑dairy is one more lever, not the whole story. Crossbred cows with stronger fertility give you more room to decide which lactations get beef vs sexed dairy semen. Moderate‑sized, robot‑friendly cows fit tighter breeding programs. Beef‑on‑dairy calf revenue stacks on top of genetics and facilities built around long‑term family ownership, not just next month’s cash flow.

If your focus is banners and purebred marketing, this path comes with trade‑offs. If your focus is a resilient commercial herd your kids might actually want to run, it’s worth a serious look.

Cover crops + “odd” forages fit beef rations; old infrastructure = low overhead

Robot-friendly moderate-frame cows; strong fertility (crossbreeding); family succession plan

Main Constraint They Manage

Heifer inventory—must keep sexed-semen conception high

Land base & feed logistics (790 acres, finishing cattle on-site)

Balancing milk components (4.6% fat, 3.6% protein) with beef-calf revenue

The Beef‑on‑Dairy Gold Rush Has a Downside

It’s easy to get starry‑eyed about $1,400 calf stories. Here’s the part that keeps you out of trouble.

The same 2023 Animals review that highlights beef‑on‑dairy’s upside also flags real risks when beef sires get sprayed across dairy cows without enough planning:

Longer gestation with some beef breeds, stretching calving intervals, and tying up stalls.

Higher dystocia and stillbirth rates in certain beef × Holstein crosses when calving ease isn’t prioritized.

Welfare and marketing problems occur when calves don’t meet buyer expectations on growth, muscling, or carcass traits.

On the fed‑cattle side, Kansas State’s grid‑pricing work shows that cattle outside packer specs on weight, yield, or quality take meaningful discounts. Poorly planned beef‑on‑dairy crosses—wrong frame, wrong fat cover, wrong muscling—are more likely to land in those discounted buckets.

If you:

Chase beef‑on‑dairy premiums with sires that add too much birthweight or gestation,

Ignore calving‑ease and carcass traits when picking beef bulls for dairy cows, and

Don’t align your calves with what your buyer, feedlot, or packer actually wants,

you can watch the “gold rush” vanish into dead calves, extra days open, and grid deductions.

The herds that will still be glad they leaned into beef‑on‑dairy five years from now are already:

Using calving‑ease beef sires validated on dairy crosses.

Matching sires to specific buyer or grid specs, not just grabbing “any Angus” off the sheet.

Tracking calf health, growth, and sale prices in their own records instead of assuming every beef‑cross calf lands at the top of the market.

What This Means for Your Operation

Beef‑on‑dairy is not a yes‑or‑no question. It’s a strategy that has to fit your repro, heifers, feed base, and markets.

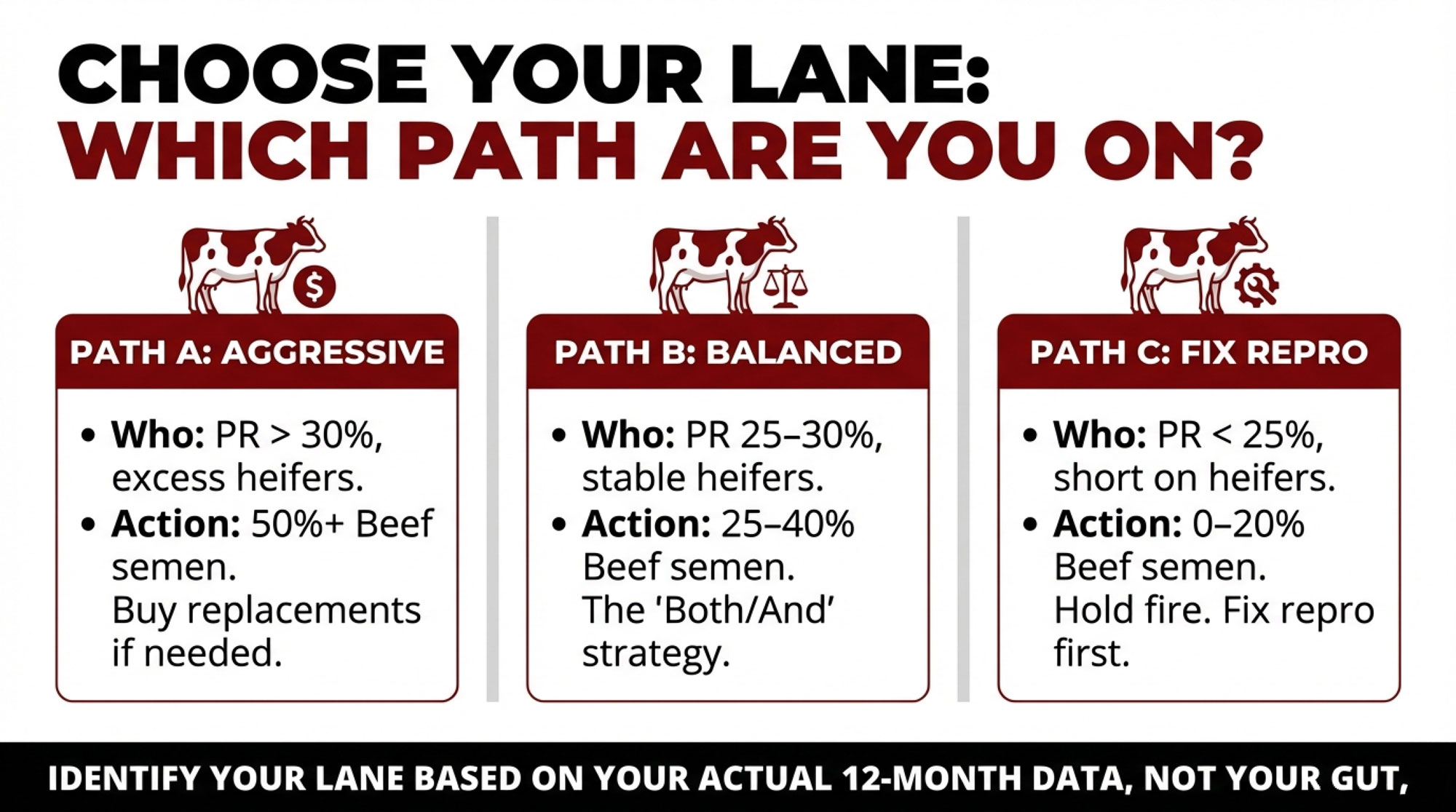

Most herds will land in one of three lanes.

Path A: Aggressive Beef (50%+ of Breedings)

You’re here if:

Your 21‑day pregnancy rate runs around 30% or higher.

You’ve consistently had more heifers than you truly need.

You have reliable outlets for beef‑on‑dairy calves or your own finishing capacity.

What it looks like:

The top 20–30% of cows and most heifers get sexed Holstein semen, selected on Net Merit, DWP$, or your index of choice.

The bottom 50–70% of cows receive beef semen from calving‑ease, dairy‑tested sires that meet buyer specs.

You’re willing to buy replacements when the heifer market says that beats raising every last one yourself.

Path B: Balanced Strategy (25–40% Beef)

You’re here if:

Your 21‑day pregnancy rate sits in the 25–30% band.

You’re mostly okay on heifers—short in some years, long in others.

You have decent calf markets but no locked‑in premium contract.

What it looks like:

The top 30–40% of cows and heifers get sexed dairy semen.

The bottom 25–40% of cows go to beef.

Conventional dairy semen still has a role where it wins on cost per pregnancy.

A lot of 300–800‑cow herds are going to live here for a while as they keep nudging repro higher.

Path C: Fix Repro First (0–20% Beef)

You’re here if:

Your 21‑day pregnancy rate is under about 25%.

You’re short on heifers and stretching days‑in‑milk.

Your risk budget feels pretty thin.

What it looks like:

Beef semen is used sparingly—older cows, obvious genetic culls, maybe a small test group.

Most of your cash goes into repro and cow performance: transition, heat detection, cow comfort, and vet work.

If you’re in Path C, the smartest beef‑on‑dairy move may be to hold your fire. Get your repro into the mid‑20s or 30s first. The beef premiums will still be there when you’ve actually got pregnancies to spare.

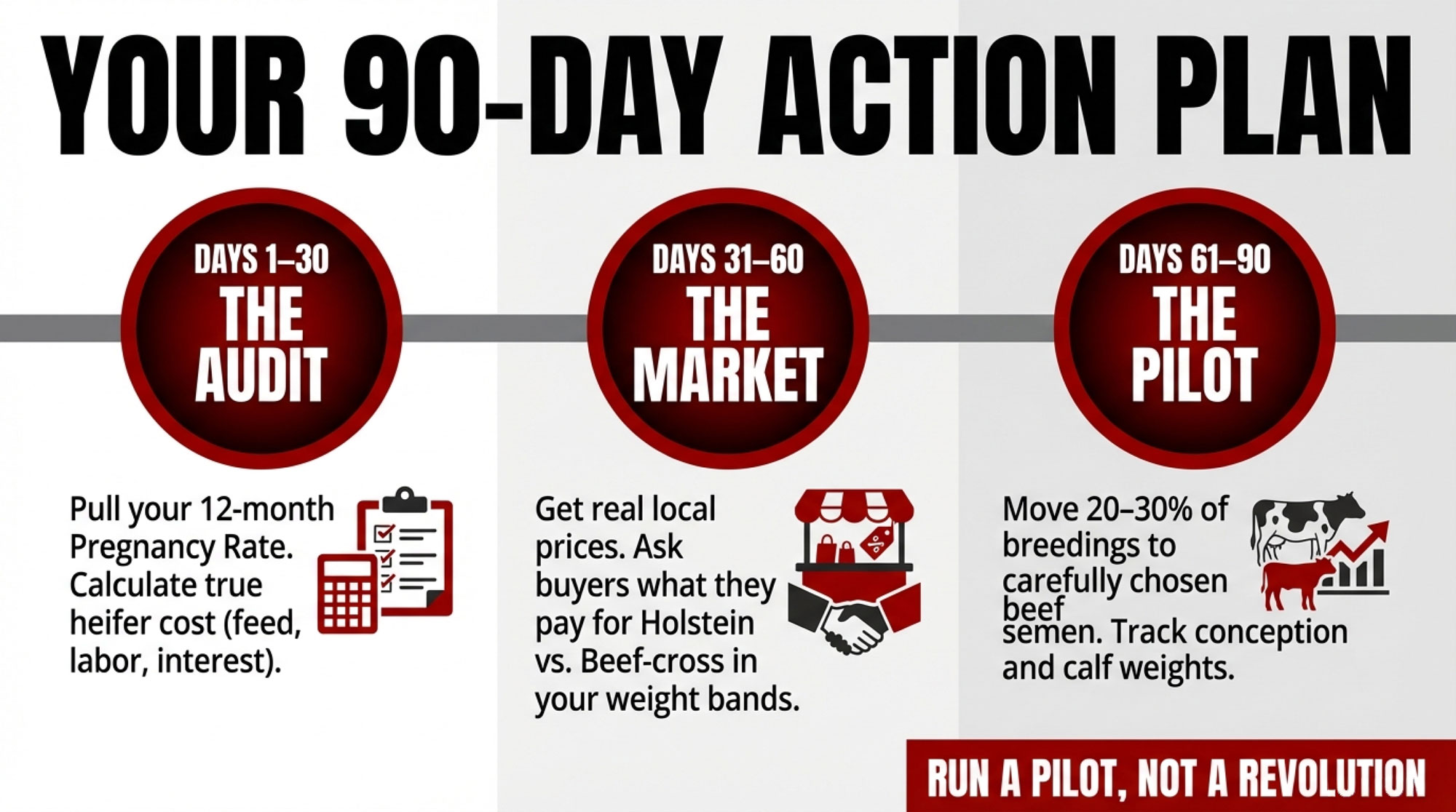

Your 90‑Day Action Plan

Here’s how you turn this from a good read into a working plan on your farm.

Next 30 days

Pull your 12‑month 21‑day pregnancy rate. Use your herd software or DHI reports, not a guess. That number tells you if Path A, B, or C is even on the table.

Calculate your full heifer cost. Use your 2024 books—feed, labour, interest, bedding, facilities, and death loss. If you need a framework, start from a university heifer‑raising budget or sit down with your lender and walk through your numbers line by line.

Next 60 days

Get real local calf price ranges. Talk directly to your sale barn or calf buyer. Ask what they’ve actually been paying for Holstein bull calves vs beef‑on‑dairy calves in your weight bands over the last 60–90 days. Use that spread—not coffee‑shop talk—as your baseline.

Sit down with your AI and genetics rep. Bring cow and heifer index lists, cull data, and heifer counts. Map how many replacements you truly need, and which animals can shift to beef semen without starving your fresh pen 18–24 months from now.

Next 90 days

Run a pilot, not a revolution. If your repro supports it, move 20–30% of breedings to carefully chosen beef semen for one breeding season. Track breedings, conceptions, calvings, calf weights, and sale prices. Let your own numbers, not somebody else’s story, tell you whether to ramp up or back off.

Check your risk tools. USDA’s Livestock Risk Protection (LRP) program has expanded coverage options in recent years, including coverage tied to feeder cattle and calf prices in general. Talk with your insurance agent or extension specialist about whether any current LRP products fit the kind of calves you’re producing and how you market them.

While you’re at it, read your milk cheque and the fine print of your contract. If your processor is paying for components, animal care, or specific beef‑on‑dairy traits, those lines belong in the same spreadsheet as semen prices and calf bids.

Timeline

Action Step

What to Calculate or Ask

Why It Matters

Next 30 Days(Step 1)

Pull your 21-day pregnancy rate

Use herd software or DHI—12-month rolling average, not a guess

Tells you if Path A, B, or C is even on the table; this number is your beef-semen budget

Next 30 Days(Step 2)

Calculate your full heifer cost

Feed + labor + interest + facilities + death loss from 2024 books

If your cost is >10–15% above local bred-heifer prices, raising every heifer is leaving money on the table

Next 60 Days(Step 3)

Get real local calf prices

Call sale barn or buyer: What did Holstein bulls vs beef-cross calves actually bring in last 60–90 days?

Use that spread—not coffee-shop gossip—as your baseline; if spread is <$300/head, beef-on-dairy math gets harder

Next 60 Days(Step 4)

Sit down with AI/genetics rep

Bring cow index lists, cull data, heifer counts; map how many replacements you truly need

Prevents the classic mistake: copying someone else’s beef-% when their repro and heifer pipeline are 20 points stronger than yours

Next 90 Days(Step 5)

Run a pilot, not a revolution

Move 20–30% of breedings to beef semen for one breeding season; track breedings, conceptions, calvings, calf weights, sale prices

Let your numbers tell you whether to ramp up or back off—not somebody else’s story at the sale barn

Next 90 Days(Step 6)

Check your risk tools

Talk to insurance agent about USDA Livestock Risk Protection (LRP) for feeder cattle/calf price coverage; read milk contract fine print for component or beef-calf incentives

If your processor pays for specific traits or your calf market swings hard, these lines belong in the same spreadsheet as semen prices

Key Takeaways

Beef‑on‑dairy calves are bringing several hundred dollars more per head than Holsteins in many U.S. markets—Holstein calves that used to bring $300–$450 are now commonly $700–$1,000 in strong markets, while beef‑cross calves are topping $1,500–$1,750 in parts of Wisconsin and over $1,000 in Pennsylvania and other key regions.

Heifer economics have flipped fast. CoBank says inventories could shrink by another 800,000 head before 2027, while Wisconsin replacement values jumped 69% in a year, and many U.S.-bred heifers now sell north of $3,000, with some lots over $4,000.

Beef‑on‑dairy works best long‑term when repro and heifer numbers are strong. Modelling shows the math starts to work above roughly 20% 21‑day PR and 2x calf price, with herds in the 30–40% band having the most flexibility.

There’s a real downside if you pick the wrong beef sires or ignore carcass specs. Longer gestations, harder calvings, and packer grid discounts can erase calf‑price gains very quickly.

The herds that will still be happy with beef‑on‑dairy in five years are matching sexed and beef semen to their own numbers—pregnancy rate, heifer needs, feed base, and actual buyers—not to the latest rumour at the sale barn.

The Bottom Line

You don’t have to milk 650 cows in Luxemburg or farm 790 acres in Fond du Lac County to make this work. But, like those families, you do have to pick a lane and live with the math that comes with it.

So when you look back on 2026, a year from now, do you want to say, “We finally lined up our breeding plan with our numbers,” or still be loading $700 Holstein bull calves while your buyer’s paying a lot more for the right beef‑on‑dairy cross?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Building a Beef-on-Dairy System: Capturing $360,000 in Annual Farm Profit – Stop leaving money on the table and start building a profit-driven pipeline. This breakdown delivers the exact ROI calculations and management shifts needed to capture massive annual revenue gains by aligning your breeding with real-world demand.

The ProCROSS Payoff: Is It Time to Cross the Line? – Breaks down the University of Minnesota’s findings on how crossbreeding delivers a 9-13% boost in daily profit. This unconventional approach reveals how improving health and fertility traits secures your competitive advantage in a high-cost environment.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Sick calves can drain $27,000/year from your herd. By 2026, genomics will let you stop breeding them. Here’s the playbook.

EXECUTIVE SUMMARY: USDA research now confirms what many producers have long suspected: calf scours and respiratory disease are partly genetic—and by 2026, you’ll be able to select against them. The numbers are hard to ignore. Sick calves can drain $27,000 a year from a 1,000-cow herd, while wrong breeding calls leave another $30,000-plus on the table in missed beef-on-dairy premiums and wasted heifer slots. With replacements at a 20-year low, beef-cross calves topping $1,000, and heifers costing north of $2,500 to raise, every semen straw now carries real economic weight. This article lays out a five-step breeding playbook—genomic testing, rule-based beef-versus-dairy decisions, calf-health sire screening, calving-pressure management, and ongoing market adjustments—that forward-thinking herds are already putting to work. Producers who start now can realistically expect to shift $50,000 or more in annual herd economics within 18-24 months.

You know how the talk goes once the parlor’s washed down and the coffee’s on. Somebody mentions a nasty run of scours or a bunch of calves that just won’t quit coughing in the group pen, and five minutes later, you’re into genomics, beef‑on‑dairy, heifer prices, and whether some cows should ever see a dairy straw again. That’s not small talk anymore. That’s survival planning.

What’s interesting right now is that the genetics and the economics are finally lining up with what a lot of you have been seeing in your own hutches. Some cow families just throw tougher calves. Others seem to live in the treatment book every winter. And those sick calves quietly eat money long before they get a chance to show what they can really do on butterfat performance, fertility, or longevity.

At the same time, beef‑on‑dairy has turned into serious money in a lot of sale barns and contract deals, right when replacement heifers have slid to the lowest levels we’ve seen in about 20 years and gotten expensive to either raise or buy. A 2025 CoBank report describes US dairy heifer inventories as sitting at roughly a 20‑year low and projects they could tighten by as much as 800,000 head before gradually rebounding after 2027 as roughly 10 billion dollars of new processing capacity comes online and needs milk. Analysts used USDA Cattle Inventory data to show that the number of dairy heifers over 500 pounds dropped from about 4.76 million in 2018 to roughly 4.06 million by early 2024—almost a 15% decline in the pool of future milkers.

Put all of that together, and the question changes from “How do we get fewer sick calves?” to something a lot sharper:

Which calves do you actually want to be making in 2026—and which ones are you better off never creating in the first place?

Let’s walk through what the newest science says about calf‑health genetics, how it connects to beef‑on‑dairy money and replacement economics, and what a practical breeding plan looks like on real dairies.

Looking at This Trend: What the New Calf‑Health Genetics Actually Show

If you’re going to let genetics influence how you think about scours and pneumonia, the first question is simple: are these traits heritable enough to move the needle?

A 2025 paper in the Journal of Dairy Science from USDA’s Animal Genomics and Improvement Laboratory went straight at that. The team led by geneticists Babu Neupane, PhD, and John B. Cole, PhD, pulled producer‑recorded calf health data from the National Cooperator Database and built what’s probably the most comprehensive calf‑health dataset we’ve ever seen for North American Holsteins and Jerseys.

Here’s what they worked with:

207,602 calf records for diarrhea between 3 and 60 days of age.

681,741 records for respiratory disease between 3 and 365 days.

Calves born from 2013 to 2024, with about 97.5% of the data coming from Holsteins and Jerseys.

When they summarized those records, they found that 14.46% of calves had a recorded case of diarrhea in that 3‑ to 60‑day window, and 16.05% had a recorded respiratory case between 3 and 365 days. If you’ve ever watched a damp March wind whistle through hutches in Wisconsin or Ontario, those numbers probably sound about right. Scours tends to bully the youngest calves; as they get older, respiratory problems slowly take over.

On the genetic side, they estimated heritabilities of 0.026 (2.6%) for resistance to diarrhea and 0.022 (2.2%) for resistance to respiratory disease. That’s modest, but it’s right in line with what’s been reported for cow‑health traits like clinical mastitis, metritis, and ketosis that we already include in Net Merit, Pro$, and other indexes. In plain language: calf‑health traits behave like other health traits we’re already comfortable breeding for.

Trait

Heritability

Similar Industry Trait

Top 5% Sires (% Healthy Calves)

Bottom 5% Sires (% Healthy Calves)

Practical Implication

Diarrhea Resistance

2.6%

Clinical Mastitis (1.5%–3%)

88%

71%

17 percentage-point spread; top sires prevent ~200+ sick-calf events per 1,000 calves born

Respiratory Resistance

2.2%

Ketosis (1–2%)

88%

70%

Same order of magnitude; respiratory RBV predicts > 1 fewer pneumonia case per 10–12 calves

Cow Mastitis

1.5%–3%

Industry standard

~85%

~72%

Calf-health heritability is comparable to traits we’ve been selecting on for 20+ years

Genetic Correlations

0.0 to -0.1

Low cross-trait pull

N/A

N/A

Improving calf health does not sacrifice milk, fat, protein, or fertility gains

What’s encouraging is that when USDA‑AGIL ran genomic evaluations for these traits, the genomic predictions were noticeably more reliable than simple parent averages, particularly for young bulls with no daughter data yet. They also found that genetic correlations between calf‑health traits and most other traits—production, fertility, cow health—were low, with only a modest link between diarrhea and respiratory resistance and very little pull against milk or component traits. That matters. It means you can add calf‑health traits into a balanced index without giving up the gains you’re making in milk, fat, protein, or cow fitness.

USDA‑ARS and the Council on Dairy Cattle Breeding (CDCB) have been presenting this work through ICAR and industry meetings. The consistent message has been that these calf‑health traits are ready for inclusion in US national genetic evaluations for Holsteins and Jerseys as soon as data quality and validation milestones are met, with 2026 targeted as the window for implementation. The exact month depends on final testing and governance, but the direction is clear.

So, from a genetics point of view, we’re not talking about “maybe someday” anymore. These are real traits with real proofs coming.

What Sick Calves Really Cost: From $25 Per Case to $27,000 Per Year

You probably don’t need a scientist to tell you that sick calves are expensive, but it helps to put some hard numbers behind your gut feel.

A 2023 study in JDS Communications examined health costs at 16 certified organic Holstein dairies in the US. The researchers, including Laura C. Hardie, MSc, used on‑farm treatment records and standardized cost estimates for veterinarian time, medications, and producer labor.

On the calf side, they found average direct costs of:

25.21 dollars per case of scours.

56.37 dollars per case of respiratory disease.

Those figures are just what you can see on the invoice—vet visits, drugs, and some labor. They don’t include slower growth, extra days on milk replacer or starter, extra days to breeding, or the way a rough start can nibble away at first‑lactation milk and component performance. Reviews on calf health and heifer rearing, along with herd‑level calf‑health investigations, keep showing what many of you have already noticed: calves that get hammered early often lag behind, even when they survive and make it into the milk string.

So it’s reasonable—based on those cost estimates and the documented performance impacts—to say that a serious pre‑weaning disease episode can trim a few hundred dollars off a heifer’s lifetime economic value on many farms once you add up treatment, extra rearing time, and lost milk later on. The exact figure will move with your feed costs, labor rate, housing system, and milk price, but the order of magnitude is real.

If you want to see how that plays out across a herd, let’s do some simple math. Picture a 1,000‑cow dairy calving about 900 heifers a year. Say 15% of those calves—135 animals—have a significant scours or respiratory event. If you assign a conservative 200‑dollar economic hit per case, combining Hardie’s direct treatment costs with some allowance for long‑term performance losses, you end up at:

135 calves × 200 dollars ≈ 27,000 dollars per year in calf‑health‑related losses.

Cost Component

Amount (USD)

Percentage of Total

Direct Vet & Drug Costs

5,100

19%

Producer Labor (extra time)

4,050

15%

Slow Growth & Extended Rearing

8,100

30%

Lost First-Lactation Milk/Components

9,750

36%

Total

$27,000

100%

That’s not a published national average—it’s a realistic illustrative example built from current cost data and what we know about early‑life disease. On herds with higher disease burden, more expensive inputs, or longer rearing periods, that number can easily climb into the higher tens of thousands.

And that’s before you count the extra time and stress your team spends on repeated treatments and nursing fragile calves through bad weather.

So when we say calf health isn’t a “minor line item,” that it’s a major factor in your annual profit and loss, that’s the level of math we’re talking about.

Beef‑on‑Dairy and Tight Heifer Numbers: Why Every Calf Turned Strategic

Now layer the beef‑on‑dairy story and the heifer shortage on top of that.

On the beef side, you’ve watched this play out: the US beef cow herd has been slow to rebuild, and beef supplies have been tight enough that packers and feedlots are looking harder at dairy‑origin cattle, especially high‑health dairy‑beef cross calves. At the same time, dairy herds have become much more consistent with reproduction—timed AI, sexed semen, improved fresh cow management through the transition period—so you have more control over whether a given pregnancy is a “dairy heifer” or a “beef‑on‑dairy” calf.

Economists who work with both dairy and beef have been frank about the impact. In a 2025 interview, Mike North, an economist and risk‑management advisor with Ever.Ag, who works with many Midwest dairies, explained that beef‑on‑dairy breeding programs are generating “upwards of two and a half dollars per hundredweight in revenue back to the farm just in beef breeding” on some operations. In that same segment, he pointed out that in the current market environment, it’s not unusual to see a well‑bred, three‑day‑old dairy‑beef cross calf bring more than 1,000 dollars at certain sales, which really changes how that calf looks compared to a straight Holstein bull calf.

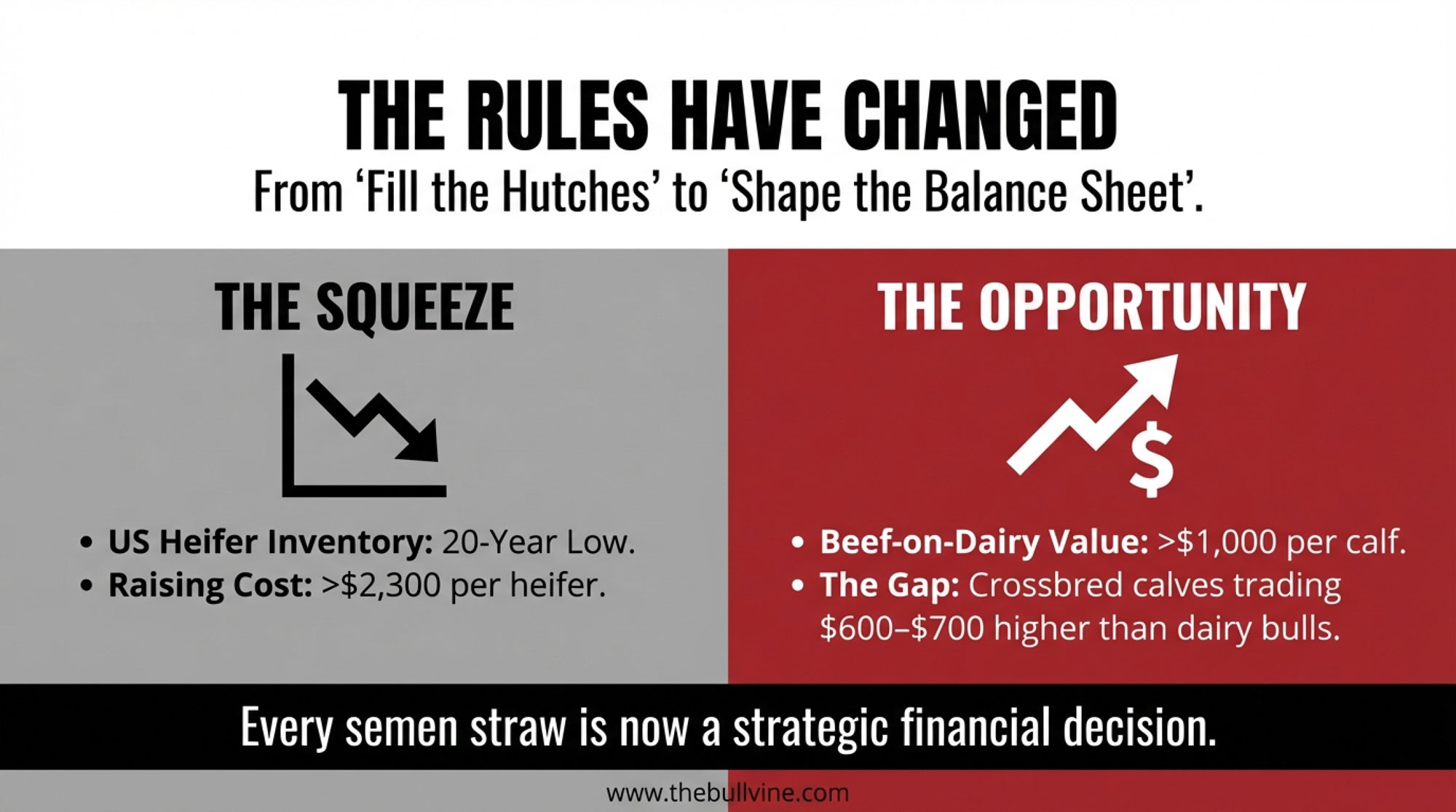

On the replacement side, CoBank’s 2025 heifer‑inventory analysis describes a sector at a “unique inflection point,” with dairy heifer numbers already at a 20‑year low and not expected to rebound until around 2027, as new processing plants draw more milk and heifer demand slowly pulls numbers up again. USDA Cattle Inventory reports shows that heifers over 500 pounds dropped from roughly 4.76 million in 2018 to 4.06 million in early 2024, while noting that stronger milk prices and processing expansion could drive replacement values higher. At the same time extension economists have pointed out that the total cost to raise a replacement heifer—from birth to first calving—often sits somewhere between 1,600 and 2,400 dollars under pre‑inflation conditions, with more recent budgets and Canadian/US benchmarking suggesting that on many units today, full economic rearing cost runs in the 2,300–3,000‑dollar range per head once you factor in feed, labor, housing, and overhead.

So across North America right now:

Dairy‑beef cross calves commonly bring a few hundred dollars more than straight Holstein bull calves at auction, with recent reports showing crossbred calves trading around 600–700 dollars in some Midwest sales while conventional bull calves lag behind.

In certain barns and weeks, especially in strong markets, three‑day‑old beef‑on‑dairy calves have topped 1,000 dollars.

Replacement heifers are scarce and expensive by historic standards, with multiple analyses pointing to rearing costs comfortably north of 2,000 dollars per head and market values for springers often pushing into the upper‑2,000 to 3,000‑dollar range in tight regions.

This development suggests that calves have shifted from “fill the hutches” to “shape the balance sheet.” Whether a pregnancy produces a dairy heifer or a dairy‑beef calf now has a direct and significant impact on both your future herd and your short‑term cash flow.

What Farmers Are Finding: A Five‑Step Breeding Framework That Actually Works

Looking at this trend across herds in Ontario, Wisconsin, California, and the Northeast, what I’ve noticed is that the operations making this work aren’t doing anything mystical. They’re just being very deliberate and consistent.

Most of them follow some version of a five‑step framework:

Use genomics to see which cow families are truly driving your herd.

Make a clear, rule‑based beef‑versus‑dairy decision for each breeding.

For dairy matings, add calf‑health genetics to your sire criteria as those proofs become available.

Factor in gestation length and calving pressure so you don’t overload high‑stress windows.

Re‑run the economics regularly as calf prices, heifer values, and milk markets move.

Let’s unpack that in barn‑level terms.

Step 1: Use Genomics to See Which Families to Grow—and Which to Let Go

Most herds that are serious about this are genomic‑testing their heifer calves, and some have also done a one‑time pass on younger cows to avoid missing high‑value animals that might be hiding behind older genetics.

A good real‑world example comes from a 5,000‑cow Holstein herd in the western US profile in 2024. The dairy, managed by veterinarian and producer Dr. Sergio Lopes, began genomic testing heifers in 2016 when they realized they were simply overrun with replacements and needed a better way to decide which heifers were truly worth raising.

Genomic results showed them a few things very quickly:

Some cows they had always considered “average” based on current production actually had very strong genetic merit.

Some of their highest‑producing cows were benefiting more from management and environment than genetics.

There were identification problems—wrong semen recorded, calves linked to the wrong dams—that genomics helped uncover and correct.

After a couple of years of working with the data, Lopes said they were confident enough to change their breeding strategy completely. They dropped conventional semen, used sexed dairy semen only on their best families, and bred the rest to beef. Today, they have a background of roughly 12,000 dairy‑beef cross animals tied to their 5,000‑cow dairy and partner herds, with beef calves and fed cattle now a major income stream alongside milk.

On a 300‑ to 600‑cow family herd—say a free‑stall in Wisconsin or a tie‑stall in Ontario—the same pattern shows up on a smaller scale. Producers genomic‑test their heifer calves, rank them on the index that matters most—Net Merit, TPI, Pro$, LPI, maybe with extra weight on health—and discover they have:

A top group, often the top 20–30%, they absolutely want to build daughters and granddaughters from.

A middle group they can flex up or down based on heifer inventory and cash flow.

A bottom group that’s tough to justify raising to calving when replacements are expensive, and barn space is tight.

Once you see your herd laid out like that, it becomes a lot easier to say, “These families deserve sexed semen and more daughters,” and “These cows can contribute better through beef‑cross calves than through more low‑merit heifers.”

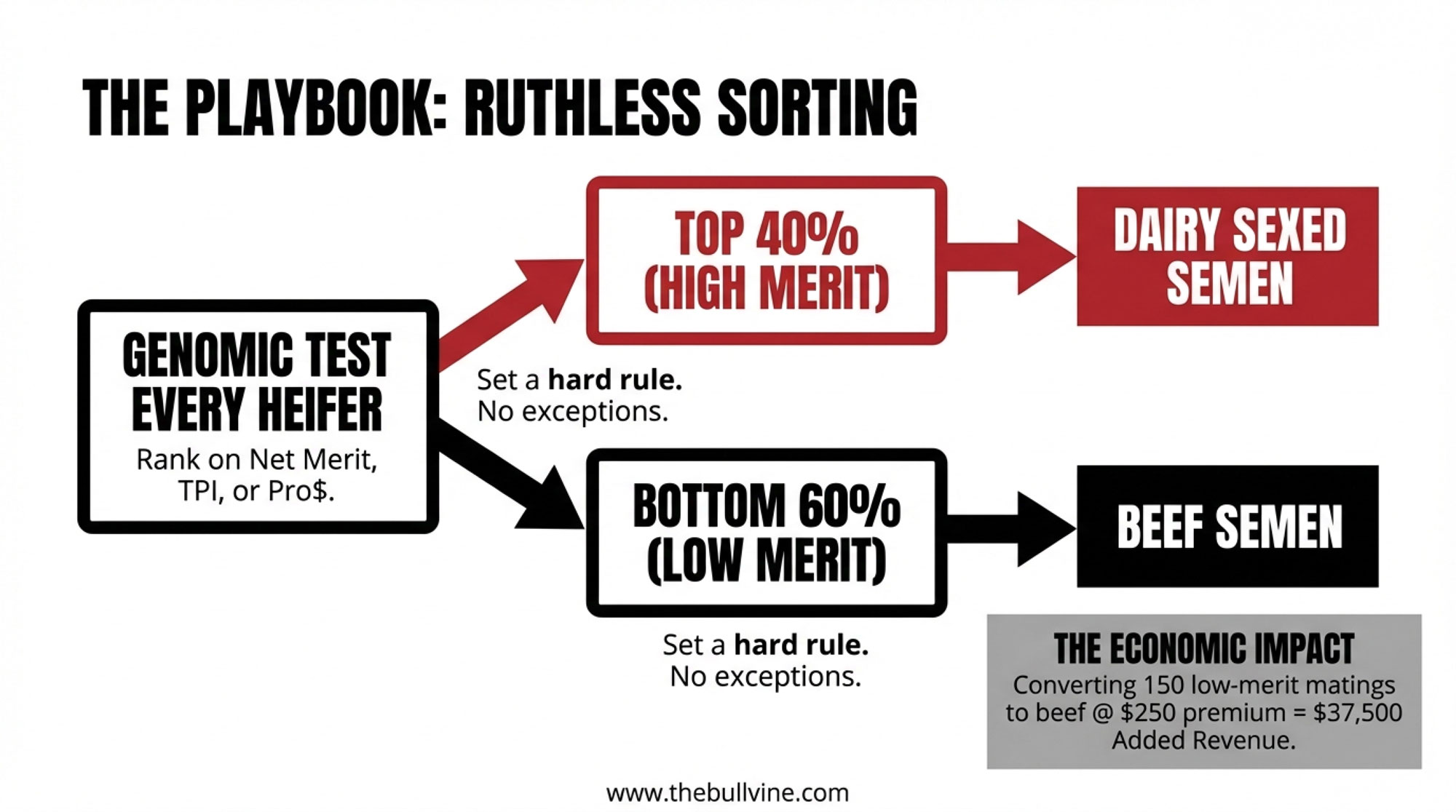

Step 2: Make Beef‑Versus‑Dairy Decisions Simple and Rule‑Based

Once you’ve got a handle on your cow families, the next step is to stop making beef‑versus‑dairy calls on the fly in the parlor and start following a simple rule you can execute every week.

A rule that’s working on a lot of herds looks something like this:

First‑ and second‑lactation cows whose most recent heifer ranks in the top 40% of your genomic list get bred to dairy semen, often sexed.

Cows whose daughters fall below that line, plus older cows without strong family backing, get bred to beef.

When herds stick to that for a full year, they usually end up with roughly 30–40% of cows getting dairy semen and 60–70% getting beef. That mix often covers replacement needs—because dairy semen is concentrated on the right cows—while generating a steady stream of well‑bred dairy‑beef calves.

Here’s where the big math starts to bite in your favor. In many Midwestern markets right now, it’s common to see a beef‑on‑dairy calf sell for a few hundred dollars more than a straight Holstein bull calf. For example, in early 2024, it was reported that crossbred calves were selling for around 675 dollars per head in some US sales, while conventional Holstein bull calves lagged far behind, and noted that “beef on dairy” was becoming a “big money” factor in the heifer shortage conversation. If you take 150 matings that would have produced low‑merit dairy calves and, instead, flip them to beef‑on‑dairy matings with a 250‑dollar average premium, you’re looking at:

Even if you trim that for calf‑price volatility or the occasional calf that doesn’t quite hit the premium, you’re still talking about tens of thousands of dollars per year from one simple change in breeding policy.

And on the cost side, you’re not spending all the feed, bedding, labor, and barn space to raise heifers from those bottom families. Long‑term work out of places like Cornell, Penn State, and western Canadian benchmarking suggests that when you spread all the costs out, total rearing cost per dairy heifer—from birth to first calving—often sits in the 2,000–3,000‑dollar range once you include feed, bedding, labor, health, and overhead, with the exact figure depending on system (confinement, pasture, dry lot) and region. So not raising heifers that were never likely to pay you back is a big part of this story, too.

Step 3: Add Calf‑Health Genetics to Your Dairy Sire List

Now bring calf‑health genetics back into the picture.

We’ve already seen that calf diarrhea and respiratory disease are heritable and can be evaluated genomically. Canada gives us a clear preview of how those traits can look in practice.

In August 2025, Lactanet—the national genetics and data organization for Canadian dairy producers—launched a Holstein calf‑health genetic evaluation that combines recorded cases of respiratory disease from birth to 180 days and diarrhea from birth to 60 days. The new trait is expressed as a Relative Breeding Value (RBV) centered at 100 with a standard deviation of 5. Higher RBVs indicate sires whose daughters are more likely to stay free of recorded calf‑health events in that early‑life window.