Did you know India produces 69% of the world’s buffalo milk—nearly double US cow production? Imagine the untapped profit potential!

EXECUTIVE SUMMARY: Here’s the thing—India’s buffalo dairy sector controls nearly 70% of global buffalo milk, pumping out over 104 billion kilos a year, while exporting just $1.5 million. The gap is huge. Buffalo milk commands a fat-driven premium of around 90 cents per liter, compared to 60 cents for cow’s. What’s new? AI-driven breeding tech is making waves, boosting milk yields by over 500 kg per lactation and adding roughly $570 income per buffalo (source: IJAS 2025). Yet sensor adoption is still under 5%, so the upside is massive. Farmers in Punjab report AI daughters with better yields and creamier quality, though success rates trail those of cattle. Global demand, especially in Asia, is booming, pushing exports higher. If you want new profit streams, it’s time to rethink buffalos, not just cows, and invest in precision breeding technologies.

KEY TAKEAWAYS:

Boost milk by 525+ kg/lactation with AI breeding tech—potentially add $570 revenue per buffalo. Start with heat detection accuracy improvements and reproductive management programs (source: IJAS, 2025).

Tap into premium buffalo milk pricing at 90 cents/liter, nearly 50% higher than cow’s milk, by focusing on butterfat-rich genetics and strategic herd nutrition (source: Dairy Market Reports, 2025).

Leverage digital tools like rumen sensors and remote vet platforms to cut health costs and improve reproductive success—MoooFarm already connects 15,000 farmers (source: Dairy Global, 2024).

Prepare your export game now: Asia’s dairy import demand is massive, but cold chain compliance and traceability tech (think blockchain pilots) are essential to compete (sources: FAO, Dairy Global).

Recognize buffalo’s ecological edge with 30% lower emissions per liter than cows—position your operation for future carbon regulations and sustainability premiums (source: Indian Ag Research, EPA).

I was with a farmer in Haryana at dawn recently. He pulled up his phone and said, “Priya’s ready for AI breeding in six hours.” Not guesswork—this little rumen bolus sensor tucked in her first stomach was telling him exactly when she was at her peak heat.

Priya’s a Murrah, India’s superstar breed, kind of like the Holstein but with butterfat that’s nearly double: 7 to 8 percent. This farmer runs his operation at roughly half the cost of many North American dairy operations.

What’s fascinating is that this kind of tech isn’t just staying on the big farms—it’s creeping into the smaller outfits too, shaking up the entire Indian dairy scene.

Buffalo milk commands around 90 cents per liter in the market here—nearly 50% more than cow’s milk prices, which hover near 60 cents a liter. Yet, exports of buffalo milk products linger near $1.5 million annually, tiny compared to the size of the domestic market.

Technology Bridges the Gap

Take a startup like MoooFarm. They’ve connected 15,000 farmers with vets through smartphones—meaning more than two-thirds of herd health issues get managed remotely before they balloon into bigger problems.

Then there’s the real star: CIRB’s rumen bolus sensors quietly gathering data inside the buffalo’s rumen, tracking temperature and gut health, helping farmers catch heat and health issues earlier than ever.

Here’s how that scales in numbers:

Breed

Butterfat %

Daily Milk (Liters)

Cost per cwt (USD)

Murrah Buffalo

7.5 – 8.0

8 – 12

16 – 20*

US Holstein

3.6 – 3.8

28 – 35

18 – 22

European Mix

4.0 – 4.2

20 – 25

20 – 25

NZ Friesian

4.5 – 4.8

15 – 18

15 – 19

*Note: Indian cost data focuses primarily on feed costs; full farm costs are still being analyzed.

Source: Compiled from Tridge, USDA, and industry data.

Hot Weather, Dry Feed, and Patchy Signals

Farmers in Gujarat know the hit that summer delivers: milk production can dip by up to 25% as green feed dries up pre-monsoon. Meanwhile, internet cuts in Rajasthan make it challenging to get timely vet advice.

But innovation clicks in: a farmer near Mysore invested $50,000 in solar-powered cooling, slashing milk spoilage and paying off the system in under a year.

Buffalo dairy exports are small right now, but don’t overlook Asia’s massive dairy demand—with imports from China, Indonesia, and the Philippines in the billions.

Export challenges? Strict cold chain and food safety standards are a real barrier.

Technologies like blockchain might be the solution—but they’re still in early pilot stages.

Case studies from Punjab Agricultural University’s extension programs document that some cooperative farmers with larger buffalo operations (10+ head) achieve positive returns within 6-12 months, although results vary significantly based on local conditions, management quality, and infrastructure availability.

Add to that, buffalo heat signs are subtle and slip away fast—lasting 12-18 hours versus cows’ 18-24. That sensor tech is the real lifesaver in accurately timing AI.

This isn’t just a feel-good stat—it’s becoming a trade reality.

The Bottom Line

The tech is real, and producers are already seeing returns—though it all depends on local conditions, infrastructure, and how well you manage the basics.

If you’re eyeing exports: competing on price is no longer enough. Brand trust and supply chain transparency are the new currency.

For innovators and investors: this is an opening you can’t afford to miss in a market hungry for buffalo-specific solutions.

The buffalo revolution isn’t coming—it’s here. Dairy leaders can’t afford to ignore this shift.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Making Sense of Your Herd’s Data – This article provides a tactical guide for turning sensor data into profitable decisions. It reveals practical methods for interpreting health and reproduction alerts, helping you implement the same kind of precision monitoring discussed in the main piece on your own operation.

The Global Dairy Market: Are You A Player Or A Spectator? – While the main article highlights India as an emerging competitor, this piece offers a broader strategic view of global market dynamics. It outlines key economic trends and forces you to consider your farm’s position in the international dairy trade.

The Genomic Revolution: Are You Breeding for the Future or Just for Today? – Moving beyond the AI breeding discussed in India, this article explores the next frontier: genomics. It demonstrates how to leverage advanced genetic data to build a more resilient, efficient, and profitable herd for future market and environmental challenges.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

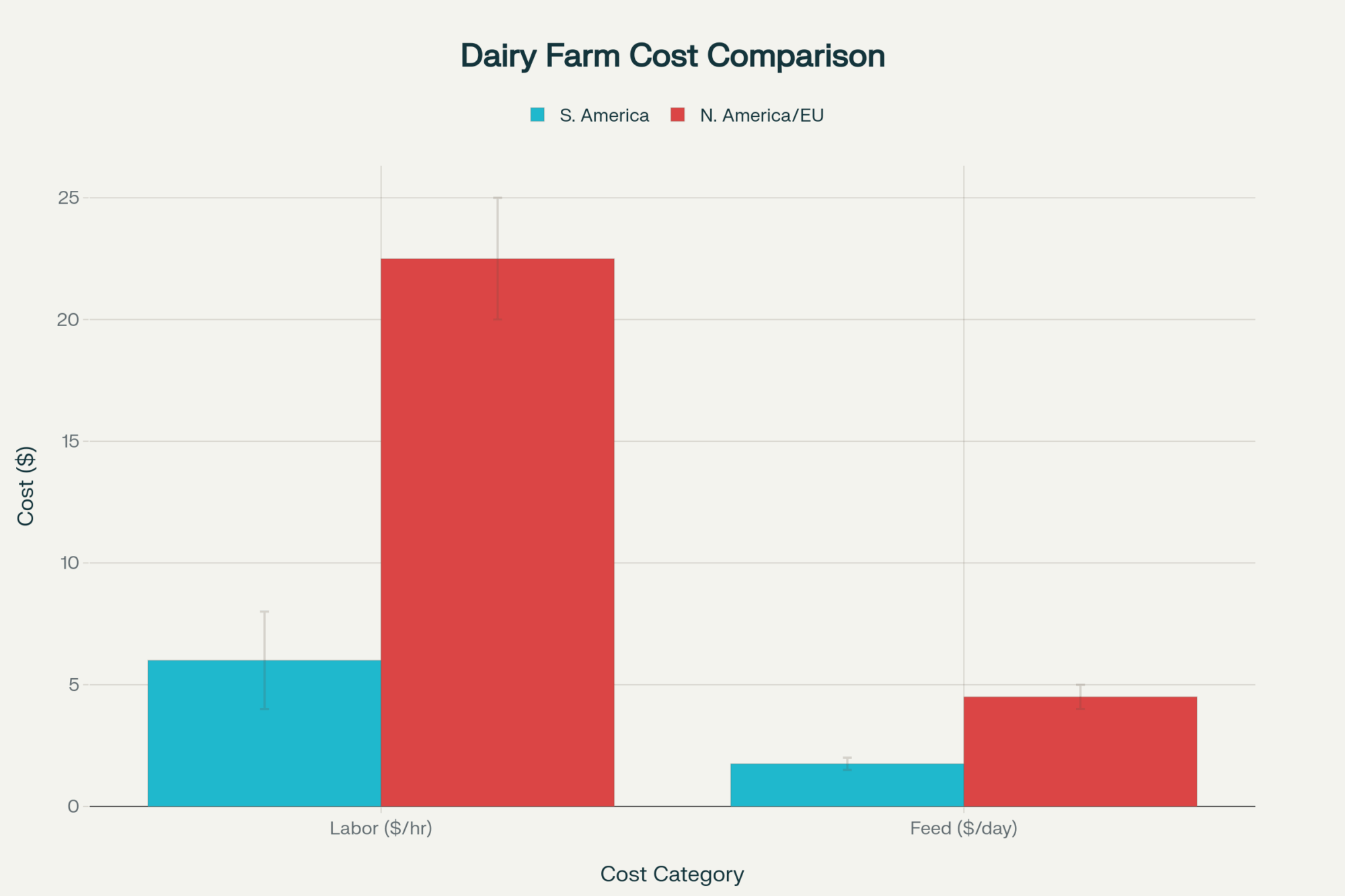

Argentina now ships dairy products to over 80 countries, despite labor costs ranging from $ 4 to $8 per hour. We’re paying $20-25/hr. Something’s gotta give.

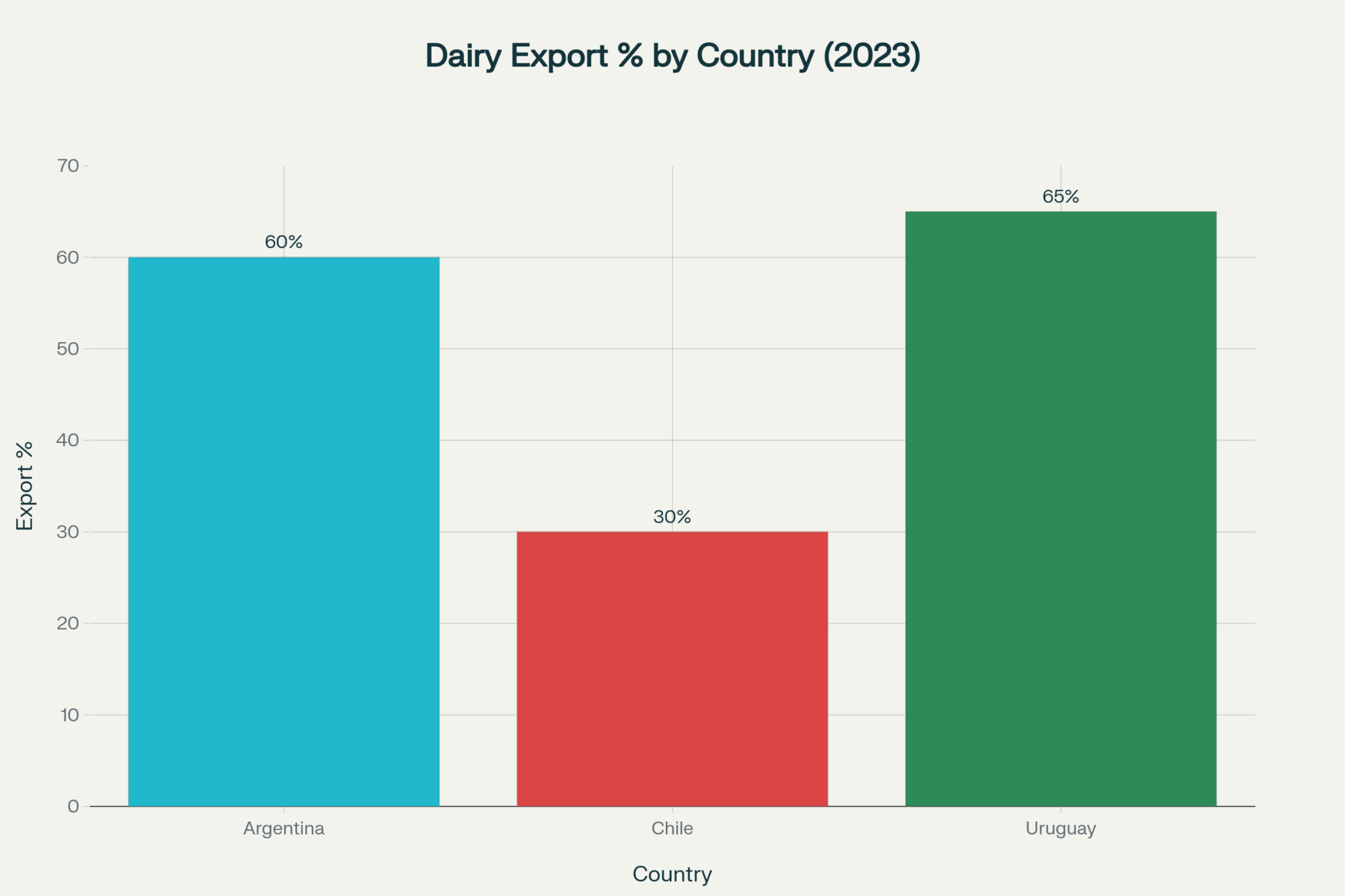

EXECUTIVE SUMMARY: You know that feeling when you realize everyone else figured out something you missed? That’s what’s happening with South American dairy right now. While we’re fighting $25/hour labor and massive cooling bills, Argentina’s running 150-200 cow herds at $4-8/hour labor costs, and Chile’s hitting record production with GPS-guided grazing. The numbers don’t lie—their feed costs about 50% of what we pay, land rent is $200-400/hectare versus our $1,000-2,000, and they’re shipping to 80+ countries because their cost structure allows them to compete anywhere. Uruguay exports 65% of its milk, despite being smaller than most countries, demonstrating that efficiency often outweighs size. After Argentina’s production dropped 22% early this year, they’re bouncing back through exports, while we’re still fighting the same old cost pressures. Here’s the thing—their tech adoption is smart, not expensive, and it’s working with their natural advantages instead of against them. Maybe it’s time we stopped thinking bigger is always better and started thinking smarter.

KEY TAKEAWAYS

Labor advantage that changes everything: Argentine dairy workers cost $4-8/hour while ours run $20-25/hour—that’s a $30,000+ annual savings per worker that goes straight to your bottom line. Start benchmarking your labor costs per cow against these numbers.

Feed costs are cut in half through pasture optimization: South American operations spend $1.50-$2.00 per day per cow on feed, versus our $4-$5 per day average—GPS-guided rotational grazing and extended seasons make the difference. Calculate what a 40-50% feed cost reduction would mean for your operation.

Technology that fits your system, not fights it: Automated gates and pasture sensors are paying back in 12-18 months without forcing system overhauls—Chilean producers are proving precision ag works for grass-based operations. Evaluate tech investments that enhance your natural advantages instead of replacing them.

Export diversification fosters market stability: Argentina reached 80+ countries in 2023, whereas we’re often limited to 2-3 buyers—their cost structure provides pricing flexibility that we can’t match. Start monitoring global milk flows through USDA FAS reports to understand your competitive position.

Climate advantages worth $100-300/cow/year: Natural cooling eliminates massive infrastructure costs while 7-8 month grazing seasons reduce purchased feed dependence—these aren’t temporary benefits, they’re permanent structural advantages. Assess your climate-related costs and identify where efficiency improvements could be beneficial.

I just wrapped up a call with a buddy who tracks global milk flows for a living. “Argentina’s now shipping dairy to over 80 countries,” he told me. “And their growth isn’t slowing.”

That caught me off guard. While we’re busy watching Wisconsin weather and New Zealand production reports, something massive is happening down south.

Argentina: From Crisis to Competition

Out in the Pampas—Argentina’s dairy heartland—most operations run 150-200 cows, rotating paddocks every 28-35 days. Those cows are producing 20-24 liters of milk daily during peak lactation.

The real story? Cost structure. Land and labor run a fraction of what we pay up north.

The turnaround has been dramatic. Following severe droughts and economic pressures, which led to a nearly 22% decline in milk production from January to February 2024 compared to the same period in the previous year, the industry is relying on exports for recovery.

A key catalyst was the removal of export tariffs (retenciones) on dairy products. This policy, initially implemented by the previous government, was made permanent by President Javier Milei’s administration in late 2023, signaling a major shift toward promoting exports.

According to export data monitored by OCLA, around 60% of dairy products, mainly milk powders, were destined for export in 2023—not the entire milk volume.

Juan Diaz of El Rosario Farm near Santa Fe notes, “Opening up export routes has transformed our cash flow and outlook.”

Chile: Where Precision Meets Pasture

Chile’s dairy production is concentrated in Los Ríos and Los Lagos, contributing 83.6% of the national milk output. Average farm sizes range between 120 and 150 head.

Despite periodic droughts, these regions produced approximately 2.23 billion liters of milk in 2023.

Dairy tech advisors in the Temuco region observe that the most competitive producers are those blending technology—including GPS-guided pasture management and automated water systems—with a deep respect for their pasture-based heritage.

Uruguay: Small But Mighty Dairy Exporter

Uruguay, home to less than 4 million people, exports about 65% of its dairy production. Herd sizes commonly range from 120 to 160 cows.

Export volumes increased by roughly 10% in 2023, despite price volatility.

A producer near Montevideo, Lucia, points out, “Our steady climate and reliable supply are major drivers behind buyer loyalty.”

South America’s Unbeatable Cost Structure

USDA data highlights a stark contrast: Labor costs in Argentina average $4-$8 per hour, while in the US, they average $20-$25. Likewise, feed costs for pasture-based systems are typically half the price of those for confinement systems.

Cost Category

Pasture-Based (S. America)

Confinement (US/EU)

Labor Cost

$4-$8/hr

$20-$25/hr

Feed Cost

$1.50-$2.00/day per cow

$4.00-$5.00/day

Land Rent

$200-$400/ha

$1,000-$2,000/ha

Cooling Costs

Minimal

$100-$300/year/cow

These savings add up fast, helping producers maintain stronger margins.

Tech That Works with Your System

Technology is no longer confined to large-scale dairy operations. Automated gates, pasture sensors, and robotic milkers are well-suited for pasture-focused operations.

Ana Gómez, a veterinary technician and farm manager in Uruguay, said, “We installed automated waterers last season. It helped reduce labor without changing how we run our farm.”

Shift in Global Markets

Argentina expanded exports to over 80 countries in 2023, diversifying product lines and markets.

Chile’s growing domestic production is actively displacing imports worth millions annually.

Uruguay reported a 10% growth in dairy exports in 2023, expanding reach into Africa and Asia.

Watch the Risks

While Argentina’s 2023 tariff reforms under President Milei have boosted exports, currency swings and political volatility remain concerns.

Infrastructure issues, including inadequate transportation and cold storage systems, also hinder growth and market access.

What You Can Do Next

Understand your full cost structure, especially feed, labor, and climate-related costs.

Monitor global market flow and emerging buyer preferences.

Evaluate technology that complements your production system, not forces it.

Plan for currency, political, and environmental risks.

The global dairy market is shifting, and South America’s rise demands your attention.

The fundamentals of global dairy are shifting under our feet. South America’s structural advantages in cost and climate aren’t a temporary trend—they represent a new competitive reality. Smart operators aren’t just watching this change; they’re analyzing their own operations against it. The question isn’t if this will affect your business, but how you’ll prepare for it.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Why 70-Hour Weeks Are Killing Your Dairy Profits – This article provides tactical strategies to optimize labor efficiency. It uses data to prove that working smarter, not harder, is the key to profitability, directly complementing the main article’s focus on South America’s labor cost advantage.

5 Technologies That Will Make or Break Your Dairy Farm in 2025 – This forward-looking article explores the innovative tools available to compete. It demonstrates how to leverage precision technology, from sensors to feeding systems, to boost efficiency and close the competitive gap with lower-cost regions.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Pakistan’s hitting 470 gBPI scores while we’re stuck at 267. Time to rethink what’s possible with genomic testing.

EXECUTIVE SUMMARY: Okay, here’s what’s got me fired up about Pakistan’s dairy scene. They’re producing 63 million tonnes annually with herds hitting genomic scores that embarrass some of our best operations. We’re talking 470 gBPI when top 1% globally barely cracks 267. Their corporate farms are deploying the same elite genetics we use, but with $0.15/lb lower feed costs and 30% better heat stress management. One operation went from crossbred mediocrity to world-class daughters in just three years using Australian genomics and Zoetis testing. With export markets exploding and their 55% productivity gap closing fast, this isn’t just an overseas story anymore. If you’re not watching what Pakistan’s doing with TMR optimization and reproductive tech, you’re missing the next wave of dairy efficiency.

KEY TAKEAWAYS:

Boost genetic progress 2.5x faster with genomic testing like Pakistan’s elite farms—talk to your breeding consultant about implementing daughter evaluations this fall before breeding season

Save $0.15 per pound on feed costs through precision TMR formulations and heat-adapted rations—work with your nutritionist to optimize for 2025’s volatile ingredient markets

Cut reproductive failures by 20% using advanced heat detection tech that’s solving Pakistan’s “silent heat” problems—especially critical as summer heat stress increases

Slash milk spoilage losses 15-20% with cooperative chilling stations like Pakistan’s World Bank program—explore shared cooling infrastructure with neighboring farms

Tap export premium markets worth billions through halal certification and international partnerships—diversify your income streams while global dairy demand surges

You know those moments at a conference when someone drops information that completely shifts your perspective? Had one of those recently while chatting over coffee with a geneticist who’d just returned from Pakistan. What he told me about what’s happening there… well, it’s got me thinking we all need to pay closer attention.

Here’s the thing most of us don’t fully grasp about Pakistan: they’re not just another developing market dabbling in dairy. We’re talking about the world’s fifth-largest population — over 255 million people — and a dairy sector that’s exploding. Their livestock sector now includes 57.5 million cattle plus 46.3 million buffalo, creating one of the world’s largest dairy herds.

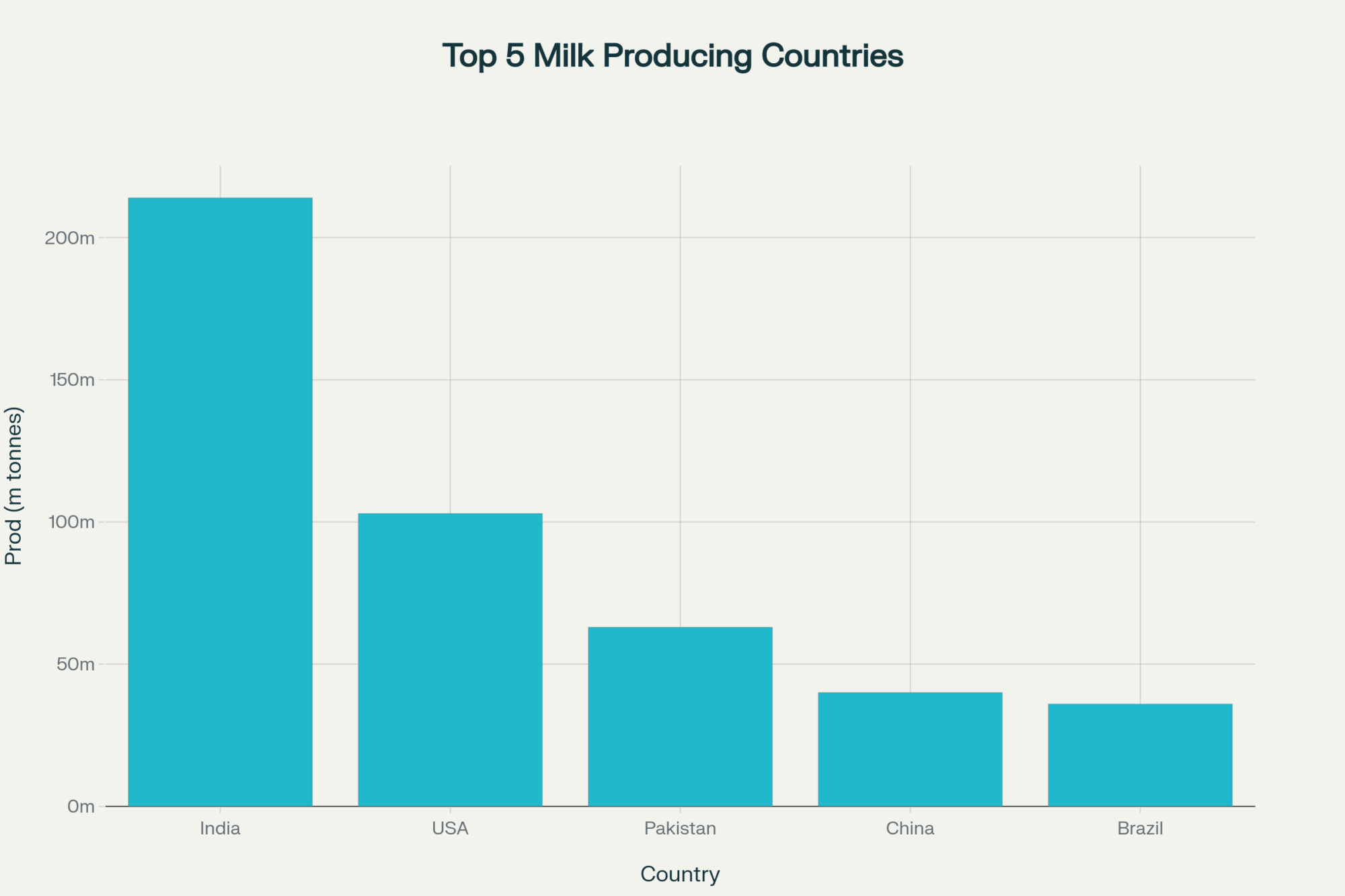

Milk production of top 5 countries in 2022 showing Pakistan’s rank

Think about that for a second. That’s more dairy animals than our entire North American inventory, and they’re producing around 64.3 million tons of milk annually, according to FAO’s latest data. That puts them third globally — behind India and the US, ahead of China and Brazil.

However, here’s where it gets interesting —and perhaps a little concerning for those of us considering long-term competition.

The Tale of Two Completely Different Dairy Worlds

What strikes me about Pakistan’s setup is how it’s basically two industries running side by side. You’ve got this massive traditional sector — we’re talking 80% of production coming from smallholder farms with just 2-5 animals each. Picture motorcycles weaving through traffic, loaded with twin milk cans, delivering fresh milk directly to consumers. That’s the reality for most of their supply chain.

Then there’s this other world emerging… and it’s impressive. Around 80 corporate mega-dairies ranging from 1,000 to 6,000 cows, with facilities that — I’m not exaggerating here — would make some of our operations take notice.

Take Interloop Dairies, recognized as Pakistan’s largest corporate dairy farm. They’re running over 10,000 Holstein Friesians with advanced milking parlors from GEA, producing export-quality mozzarella using Individual Quick Freezing technology. That’s not your typical developing market operation.

What’s fascinating is their cost structure. Abundant high-quality groundwater in Punjab province (think about that in our water-stressed environment), cheap labor, and the ability to grow corn and forages on incredibly fertile soils. Research shows that their commercial farms average 844 liters per cow daily for water usage during the summer — that’s a lot of water, but it’s available.

That combination should get anyone’s attention.

The Indigenous Foundation: Asset and Challenge

Here’s where breeding gets interesting. Pakistan’s traditional foundation is built on indigenous breeds that are perfectly adapted to local conditions, yet possess unique characteristics.

The Nili-Ravi buffalo dominates smallholder farms, and get this — recent research shows they’re producing milk with around 6.8% fat content. These animals are tough as nails — they have to be in that climate — but their genetic ceiling creates interesting dynamics. Then you have heat-tolerant Zebu cattle, such as the Sahiwal and Red Sindhi, which have evolved specifically for those conditions.

However, here’s the breeding challenge that most people don’t realize: those Nili-Ravi buffalo are prone to “silent heats,” making heat detection a significant challenge for AI adoption. From a competitive standpoint, this creates a moat around the traditional sector. You can’t just gradually upgrade these operations with better genetics — the biology doesn’t work that way.

That’s exactly why the corporate farms are going all-in on imported Holstein genetics. It’s not just about higher yields; it’s about building systems where modern breeding tech actually functions.

The Genetics Revolution Nobody Saw Coming

This development fascinates me more than anything else… Pakistan has quietly become a major destination for the same elite genetics driving productivity from Wisconsin to New Zealand.

The story that really captures what’s happening: a Pakistani veterinarian got stranded in Australia during COVID. Instead of sitting around, he worked on several high-tech Australian dairy farms and saw firsthand what elite genetics could do. When he returned home, he and two colleagues set up a dairy operation using imported, genomically tested Australian heifers.

This is where it gets impressive. HRM Dairies now genotypes all heifers with Zoetis and has produced daughters of Carenda Pilbara ranging between 348 and 470 gBPI. For context, the top 1% in Australia has an average wealth of over 267 gBPI. These aren’t just good numbers for Pakistan — these are elite numbers by any standard.

The Pakistani government has committed Rs40 billion toward genetic improvement programs. That’s transformational money.

Here’s what this means for competitive positioning: Research on 600 dairy farms in Punjab shows genomic selection could close a 55% productivity gap that currently exists. If they achieve even half those gains across their massive animal base…

Think about the implications… If a major milk-producing region can accelerate genetic progress by that magnitude, how does it change global market dynamics within a decade?

Corporate Farms That Would Impress Anyone

I’ll be honest — some of these operations are more sophisticated than farms I’ve visited in established dairy regions.

Dairyland was established with imported Australian Holstein heifers and now operates a complete “grass-to-glass” vertical integration, featuring hormone-free production and rigorous microbiological testing.

FrieslandCampina Engro’s Nara Dairy Farm spans 220 acres, housing over 6,000 animals that adhere to international health and safety standards. They’ve been pioneering corporate dairy farming since 2006, with flagship brands like Olper’s and Tarang as household names.

Everfresh Farms focuses on exceptionally high-quality fresh milk, consistently achieving low Total Plate Counts — a critical measure of milk hygiene. They’re using sophisticated milking parlors from GEA WESTFALIA Surge.

What caught my attention is the technology adoption. These aren’t scaled-up traditional operations — they’re deploying automated milking systems, climate-controlled barns with misting (essential at 50°C), TMR wagons for scientifically balanced feeding, and substantial solar installations.

What strikes me about these operations is how they’re integrating sustainability from day one. Water conservation, renewable energy, waste-to-biogas systems — they’re building climate-smart dairying into their DNA rather than retrofitting later.

The Infrastructure Reality That’s Finally Changing

Let’s talk about the elephant in the room — the cold chain that’s finally being built.

Anyone dealing with milk in extreme heat knows temperature control isn’t optional. In Pakistan’s climate, where summer temps hit 50°C (122°F), loose milk without refrigeration… well, you can imagine.

The numbers: Historically, 15-20% of milk wastage occurs due to spoilage before reaching consumers. For context, that’s equivalent to discarding the entire annual production of a mid-sized US state.

What’s interesting, though, is how targeted interventions prove this isn’t insurmountable. The World Bank’s Sindh Agriculture Growth Project provided milk chillers to producer groups, yielding immediate results: reduced waste, increased farmer incomes, and improved quality control.

Corporate farms are deploying full cold chain infrastructure alongside their advanced systems. They’re building modern dairy infrastructure from scratch, without the legacy constraints that many of us face.

For producers watching from afar: These infrastructure investments create templates that work in challenging climates. Some cooling and logistics solutions being developed could apply to southern US operations dealing with increasing heat stress.

The Productivity Gap That’s Actually an Opportunity

Here’s where numbers get really interesting. Recent research on 600 dairy farms in Punjab indicates that the average farm has a 55% yield improvement potential. By closing that gap, average operations could increase yearly fat-corrected milk production by 120,036 kg and the non-milking herd for meat by 25 head.

What strikes me is that we’re not talking about theoretical improvements. These are achievable gains based on existing technology and management practices that have already been demonstrated on corporate farms.

The study found that small farms (under 25 head) are actually more technically efficient than medium and large farms — suggesting room for improvement across all scales. Clear evidence shows that keeping higher shares of exotic cows versus local breeds, along with higher farm-gate milk prices, triggers significant efficiency gains.

That’s the productivity trajectory that could fundamentally alter global supply dynamics if it scales across their 30-million-head base.

The Export Opportunity That Changes Everything

Here’s where strategic implications become clear. Pakistan’s milk exports reached $5.47 million in 2023, primarily to Saudi Arabia ($2.78 million), the UAE ($1 million), and Somalia ($ 572,000). It might not sound like much, but industry analysts discuss export potential reaching billions.

The strategy involves utilizing buffalo milk for domestic consumption while targeting cow milk-based products for export, such as cheese, butter, and ghee. This leverages the growing base of high-yield Holstein and Jersey cows while maximizing value from different milk types.

China represents the primary target, with agreements already in place for companies like Fauji Foods Limited to begin exporting buffalo milk to China’s Royal Group. Given China’s dairy deficit and Pakistan’s geographic proximity, this could scale rapidly.

Middle East and North Africa markets offer additional opportunities, particularly for Halal-certified products, where Pakistan has natural competitive advantages.

What’s interesting from a competitive standpoint is the strategic focus on products. Rather than competing directly in commodity milk, they’re targeting value-added products where margins are higher and technical barriers create natural protection.

The Policy Wild Card Everyone’s Watching

Here’s where things get complicated… and why timing matters more than most realize.

Current policy includes an 18% sales tax on packaged milk, which has caused a 20% decline in formal sector volumes, effectively subsidizing the informal loose milk market while penalizing companies that invest in food safety and modern infrastructure.

But change is coming. The Pakistan Dairy Association proposed reducing that tax from 18% to 5%, projecting it could boost volumes by 20% and increase government revenue by 22% year-on-year. Government officials confirmed they’re reviewing this policy.

As Dr. Shehzad Amin from Pakistan Dairy Association put it: “No country taxes milk at 18% — the highest global rate is 9%. Safe milk is not a luxury, it’s a right.”

The competitive implications become clear when you consider that policy alignment could accelerate the timeline for Pakistani dairy reaching export competitiveness by several years.

Technology Adoption That’s Actually Impressive

What gets my attention is how quickly leading operations are adopting advanced technology.

Corporate farms aren’t just buying better cows — they’re deploying the full suite of modern dairy technology. Automated milking, climate-controlled housing, precision feeding, genomic testing, reproductive management software… the works.

HRM Dairies distinguished itself as the only farm in Pakistan currently conducting genomic testing. They’re not just importing genetics; they’re utilizing the same scientific selection tools that drive productivity on the most advanced farms globally.

Their genomic testing capability generates daughters that are performance-proven under Pakistani conditions. According to management, 97% of their herd achieved pregnancy last year, with low mortality and production averaging over 12,000 liters per cow. That’s world-class performance.

This trend suggests that we’re seeing “demonstration farms” — operations that prove elite genetics work under local conditions and serve as showcases for wider adoption.

Climate Innovation with Global Applications

Pakistan’s extreme climate forces innovations that could benefit dairy operations worldwide.

Research shows increasing cooling sessions to five times daily improved milk yield by 3.2 kg per day in Nili Ravi buffaloes. Studies indicate that a 1°C temperature increase reduces milk yields by 1.72 liters per month, while humidity increases further suppress yields.

These pressures drive the development of heat stress management systems with automated cooling cycles, feed adjustment protocols optimized for high-temperature periods, and water management systems designed for extreme conditions.

Technology adaptation opportunities are significant. Sprinkler cooling systems, climate-controlled housing designs, and feed formulation strategies developed for 50°C conditions could provide competitive advantages in other regions facing similar challenges — such as Texas, Arizona, or anywhere heat stress is becoming a bigger issue.

The Human Element That Makes It Real

Behind all these numbers and technology stories are people making it happen.

What resonates with me is how these operators think systemically about profitability, animal health, and long-term sustainability rather than just chasing production numbers.

The Pakistani veterinarian stranded in Australia perfectly captures how knowledge transfer happens in modern dairy. He didn’t just bring back genetics — he brought back an entire approach to dairy management that’s now influencing operations across Pakistan.

I was impressed by conversations with Muddassar Hassan from HRM Dairies, who played a key role in introducing Australian genetics to Pakistan. His background includes importing heifers from leading Australian breeders, seeing firsthand how these animals perform under local conditions.

“Profit isn’t just about milk production; it’s also about lower expenses. If your cow is producing 12,000 litres but gets mastitis twice and takes four services to get pregnant, you aren’t making much profit. But if she’s producing 8,000-9,000 litres while getting pregnant easily and staying healthy, she’s almost certainly more profitable,” he explained.

That’s practical wisdom that transcends geographic boundaries.

Regional Lessons for North American Producers

Several developments in Pakistan offer insights for producers dealing with similar challenges:

Heat stress management: Climate-controlled barn designs and cooling protocols developed for extreme conditions could benefit operations in southern US regions where summer temperatures are increasingly problematic.

Genomic acceleration: The Pakistani experience demonstrates how quickly genetic progress can be achieved when genomic testing combines with elite genetics and proper management — they’re compressing timelines that we thought would take decades.

Cooperative infrastructure: The Success of programs like the World Bank’s milk chiller project demonstrates how shared infrastructure enables smaller operations to access technology that would be uneconomical for them individually. Applications for producer cooperatives dealing with processing or cooling challenges.

Sustainability integration: Building renewable energy and resource conservation into operations from the ground up rather than retrofitting later. Their solar installations and water recycling systems are impressive.

What This Means for Global Markets (And Why You Should Care)

Implications here are bigger than most of us think. Pakistan isn’t just scaling up dairy production — it’s building an entirely different cost structure while deploying the same elite genetics that drive productivity in developed markets.

Consider the math: if these corporate operations achieve even moderate success in raising the productivity of that 30-million-head base while maintaining cost advantages, we’re potentially looking at fundamental shifts in global dairy competitiveness within the next decade.

Traditional bottlenecks — such as heat stress management, breeding efficiency, and feed quality — are being systematically addressed by operations with capital and technical sophistication, enabling the implementation of effective solutions.

And here’s the kicker: they’re doing it with labor cost structures and feed production capabilities most Western operations can’t match.

Looking Forward: What to Watch

The timeline for Pakistani dairy becoming a significant global competitor is compressing. Several factors suggest major impacts within 5-7 years:

Policy reforms that reduce tax barriers and improve regulatory consistency could accelerate the formalization of milk supply. That 18% to 5% tax reduction alone could be transformational.

Infrastructure investments in cold chain and processing capacity create the backbone for scaled operations. Once that cold chain is built, everything changes.

Genetic improvements are already yielding measurable results at leading farms and will continue to compound over time. Starting with a 55% productivity gap, there’s tremendous upside potential.

Export market development provides economic incentives for continued investment and modernization. Those Chinese contracts could be just the beginning.

The productivity improvement potential identified in recent research isn’t theoretical — it’s achievable with existing technology and management practices. If that scales across their massive animal base…

The question for North American producers isn’t whether Pakistan will become a significant dairy competitor, but when and how to position for that reality.

The Strategic Questions We Should Be Asking

This development raises fundamental questions about future global dairy competition:

Are we ready for this level of competition? When you combine scale, low costs, modern technology, and elite genetics, you get a formidable competitor.

What’s our competitive advantage moving forward? If they can deploy the same genetics and technology we use, what differentiates us?

How do we adapt our heat stress management? As climate change affects traditional dairy regions, innovations being developed for 50°C conditions could become essential.

What about our feed efficiency? Their necessity to optimize every production aspect might drive innovations we should watch.

The Bottom Line for Your Operation

So where does this leave us? Several practical takeaways:

Stay informed about global developments — what happens in Pakistan won’t stay in Pakistan. Global dairy markets are more interconnected than ever, and genetics companies, equipment manufacturers, and consultants are already active in this space.

Consider climate adaptation technologies — if heat stress is becoming a more significant issue for your operation, examine what’s being developed for extreme conditions. Some solutions might be applicable sooner than you think.

Don’t underestimate the power of genomics — the Pakistani experience shows how quickly genetic progress can accelerate with the right tools and commitment. Are you maximizing your genetic potential?

Think about your competitive advantages — what makes your operation unique in an increasingly competitive global market? Quality? Efficiency? Sustainability? Location advantages?

Watch policy developments — government decisions on taxes, trade, and regulations can dramatically shift competitive dynamics. Sometimes, policy changes matter more than technology.

The dairy industry has always been about adapting to change. The question is whether we’re adapting fast enough to stay competitive in a rapidly evolving global marketplace.

This sleeping giant is waking up fast. The combination of scale, modern technology, elite genetics, and cost advantages they’re building is unlike anything we’ve seen before in the dairy industry.

The Competitive Reality Check

Here’s what I keep coming back to: Pakistan represents a distinct model of dairy development that we haven’t seen before. Instead of gradually modernizing existing systems, they’re essentially building a parallel, modern industry alongside traditional operations.

If successful — and early indicators suggest they might be — this creates a producer with significant scale, low costs, and increasingly sophisticated genetics and management. That’s not a combination global dairy markets have had to contend with before.

For North American producers, this isn’t necessarily a crisis, but it’s definitely something to monitor. The same genetics companies we work with, the same technology providers, the same management consultants — they’re all active in Pakistan now. The knowledge and tools that give us a competitive advantage are no longer exclusive.

The question isn’t whether Pakistan’s dairy industry will continue to grow and modernize. Based on what I’m seeing, that trajectory is pretty well established. The question is how quickly they can scale their modern sector and what impact that has on global supply dynamics.

We might be looking at a new major player in global dairy markets within the next 5-10 years. Unlike some other emerging producers, they’re building on a foundation of modern technology and elite genetics from day one.

What are your thoughts? Are you seeing similar developments in other markets? How are you positioning your operation to compete in this global market?

Because one thing’s becoming clear: the global dairy industry is getting more competitive, not less. Producers who think strategically about these shifts — whether adapting climate technologies, maximizing genetic potential, or developing their own competitive advantages — will be the ones who thrive in the years ahead.

The real question isn’t whether Pakistan will become a major player in global dairy markets. Based on what I’m seeing, that trajectory is established. The question is: are we ready?

The bottom line? Pakistan’s combining our genetics with their innovation to create something we haven’t seen before. Time to steal their playbook.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

5 Technologies That Will Make or Break Your Dairy Farm in 2025 – Learn about the same cutting-edge technologies Pakistan’s mega-dairies are deploying—from robotic milking to precision feeding—and how to implement them for immediate productivity gains.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Fair dairy competition is dead. While you chase 0.1% feed efficiency gains, competitors bank $25,000+ per cow in government support.

Here’s an uncomfortable truth the dairy industry won’t tell you: Pure market competition in global dairy died years ago, and pretending otherwise is bankrupting American farmers. While you’re optimizing feed conversion ratios and investing in genomic testing to squeeze out marginal gains, your government-backed competitors are literally printing money. Russia just allocated $880 million in direct dairy support for 2025—a 50% increase from 2024. Norwegian farmers pocket subsidies worth 30% of their total revenue. Swiss producers receive support that’s “more than twice what farmers in other countries get.”

The brutal reality? You’re not competing against other farmers anymore. You’re competing against entire national treasuries.

Stop Believing the Free Market Fairy Tale

Let’s destroy the most dangerous myth in American dairy: that we compete in a “free market.”

Global direct dairy subsidies reveal massive competitive disparities, with Russian farms receiving $100,000 per farm compared to just $3,400 for U.S. operations. Note these are direct dairy subsidies and trade compensation only.

Here’s what the numbers actually show:

Canada: $3.2 billion in trade compensation

Russia: $880 million for 2025 alone (50% increase)

Norway: 30% of farm revenue from government subsidies

U.S.: $68 million in Dairy Margin Coverage payments

Translation: While American dairy farmers get $3.40 per cow in direct targeted support, subsidized competitors are banking tens of thousands per cow annually. That’s not competition—that’s economic warfare.

The Subsidy Arms Race Is Accelerating (And You’re Losing)

The uncomfortable question: How do you compete when your feed costs $400 per cow annually while subsidized competitors get that covered by their government?

Critical Analysis: The Efficiency Myth Exposed

Cambridge University research reveals the dirty secret about agricultural subsidies: Coupled subsidies actually reduce technical inefficiency in dairy farms, while environmental subsidies improve efficiency. This destroys the conventional wisdom that subsidies make farmers lazy.

What this means for your operation: Those heavily subsidized European farms receiving environmental payments aren’t just getting financial support and becoming more efficient competitors. Meanwhile, you’re investing your own money in sustainability improvements, and they get paid to implement them.

The Genetic Defense Strategy: Building Unsubsidizable Advantages

The one competitive advantage that no government subsidy can replicate is genetic merit that compounds annually.

Comprehensive genomic testing delivers $96,000 annual genetic gains for a 1,000-cow herd, providing 2.4x return on investment compared to $40,000 annual testing costs

The UK Genomic Revolution: Real Numbers, Real Results

Agriculture and Horticulture Development Board (AHDB) data from 2024 reveals the genetic gap that’s reshaping competitive dynamics:

£193 per animal difference in lifetime profitability between farms using full genomic testing versus partial implementation

£430 average PLI for calves in herds with comprehensive genomic programs

£237 average PLI for herds testing only portions of their animals

Translation: While subsidized competitors get temporary financial advantages, genomic-driven operations build permanent genetic improvements that accumulate over generations.

The Beef-on-Dairy Strategic Shift

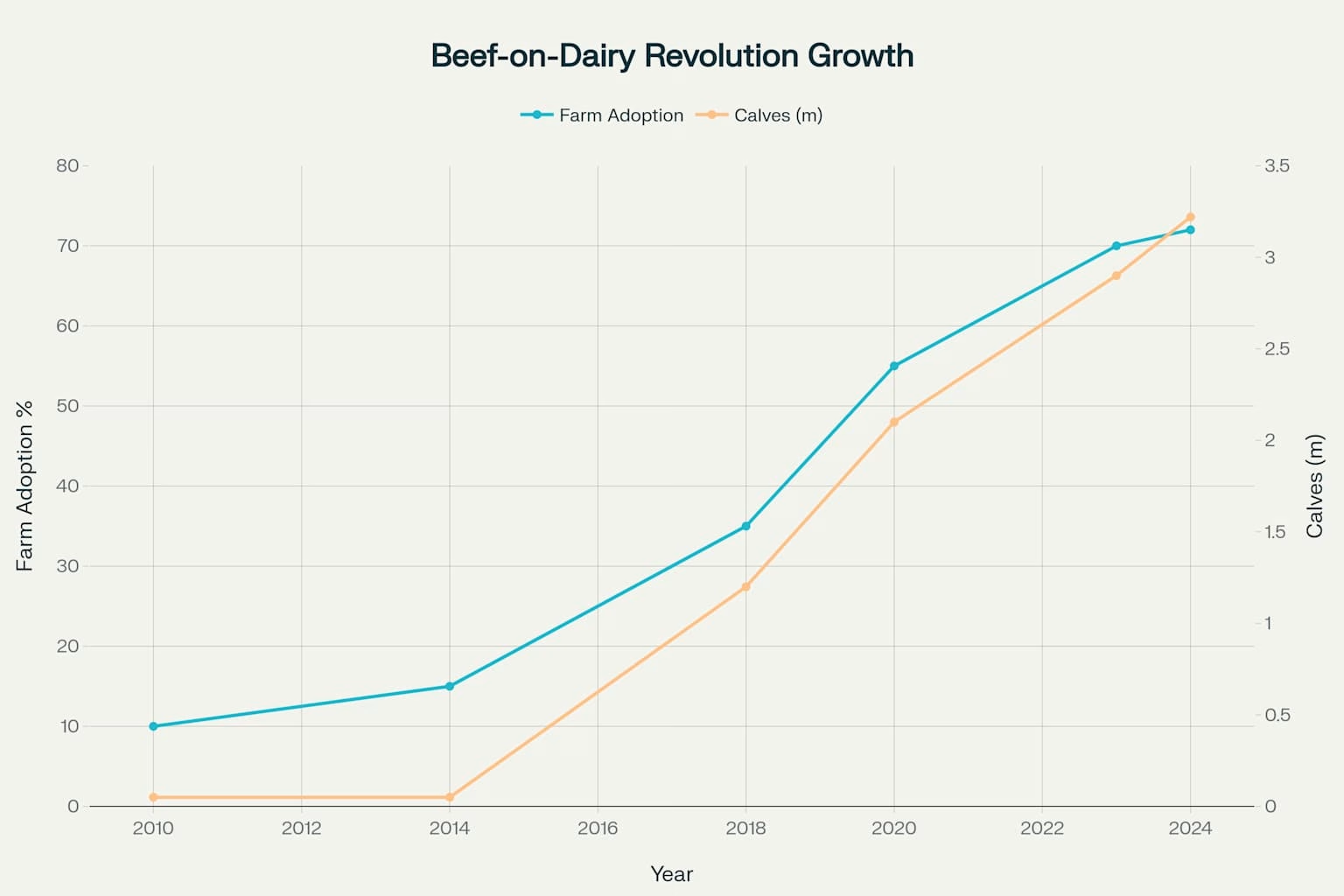

Beef-on-dairy crossbreeding has exploded from 10% farm adoption in 2010 to 72% in 2024, producing 3.22 million crossbred calves annually worth $525 premium each

California dairy data exposes a breeding revolution that’s creating new profit centers:

81% of operations now use beef semen on dairy cows, with 78% citing extra profit as the primary advantage

34% of farms breed more than 30% of eligible cows with beef semen, fundamentally altering their business model

Angus dominates at 89% usage, followed by Limousin (12%) and Wagyu (10%)

The strategic insight: While subsidized competitors focus on volume production, smart American operators are diversifying revenue streams through strategic breeding that creates premium calf markets subsidies cannot penetrate.

Elite Operation Case Study: Precision Genetics Beats Government Support

Consider this real-world competitive scenario: A Wisconsin operation implementing comprehensive genomic selection generates £193 (USD 240) additional lifetime value per animal compared to traditional breeding approaches. A 1,000-cow herd with 400 annual replacements represents $96,000 in additional annual genetic gain—nearly 30 times the DMC program’s per-cow support.

The genomic multiplier effect: Unlike subsidies that provide temporary financial relief, genetic improvements compound annually. A 2% improvement in component yield achieved through genomic selection continues paying dividends for the animal’s entire productive life and transfers to offspring.

The Three Subsidy Models Reshaping Global Competition

Model 1: The Fortress Strategy (Canada)

The System: Production quotas + guaranteed cost-plus pricing + 245% import tariffs The Reality: Quota holders operate in an artificially protected system where production rights create guaranteed value regardless of market efficiency Your Challenge: Canadian milk rarely competes in global markets, but their protected domestic market represents $9.15 billion in lost export opportunities

Model 2: The War Economy (Russia)

The System: 1.5x increase in dairy support + 8.3% concessional loans + 42% cost reimbursement The Goal: Boost production from 34 to 38.5 million tonnes by 2030 Your Threat: $4.8 billion in additional subsidized milk hitting global markets

Model 3: The Green Shield (EU)

The System: €400 million annually + 25% eco-scheme requirements + CAP protection The Advantage: Getting paid for environmental practices you must implement at your own cost The Impact: Dutch farmers allocate 32% of payments to environmental initiatives you fund privately

The Technology Investment Trap

Here’s the precision agriculture paradox killing American competitiveness:

You invest $150,000 in robotic milking systems to boost 15-20% efficiency. Meanwhile, subsidized competitors receive $200,000+ in government grants for identical technology. Frontiers in Animal Science research shows precision dairy farming increases milk yield by 30%, cuts feed costs by 25%, and reduces environmental impact by 20%—but these gains become meaningless when competitors get the technology free.

Your technology investments have shifted from competitive advantages to survival necessities.

The Genomic Competitive Response

Smart operations are turning to genetics-based competitive strategies that subsidies cannot replicate:

Component-Focused Breeding Programs:

Target 4.2% butterfat and 3.3% protein content through systematic genomic selection

Generate $15,000-20,000 additional annual revenue per 100-cow herd through premium pricing

Create defensible market positions that commodity imports cannot easily penetrate

Crossbreeding Revenue Diversification:

Implement strategic beef-on-dairy programs using high-value breeds (Wagyu, premium Angus)

Generate additional revenue streams through premium calf markets

Reduce dependency on fluid milk pricing volatility

Genomic Acceleration Strategies:

DNA test 100% of replacement heifers rather than partial herd sampling

Focus selection on economically relevant traits (components, fertility, health)

Build genetic merit advantages that compound over generations

Challenging Industry Orthodoxy: The Breeding Association Conspiracy of Silence

Here’s the controversial truth that major breeding organizations won’t acknowledge: Traditional breeding approaches used by most American dairies are systematically inferior to comprehensive genomic programs, yet industry associations continue promoting outdated evaluation methods that favor large, established operations over innovation.

The data is devastating for conventional wisdom:

Holstein Association registration programs still emphasize visual appraisal and pedigree analysis that genomic research has proven inferior for economic traits

AI organizations report ≤80% of beef bull collections qualify for sale versus >90% for Holstein bulls based on advanced semen quality assessments, yet Sire Conception Rates for Angus bulls (33.8%) nearly match Holstein bulls (34.3%) on dairy cows, proving collection qualification standards may not reflect actual fertility performance

The uncomfortable question for industry leaders: Why do breeding associations continue promoting evaluation systems that genomic research has proven less effective than DNA-based selection?

The Environmental Subsidy Revolution: Game Over for Unsubsidized Farms

WWF-UK research proves regenerative dairy systems deliver financial returns—but only when you don’t compete against farmers getting paid to implement them.

The Green Subsidy Advantage Gap

Environmental Investment

Your Cost

Subsidized Competitor Cost

Disadvantage

Methane reduction technology

$25/cow/year

Government funded + carbon credits

$25/cow

Precision feeding systems

$15,000 setup

€4,500 EU eco-scheme payment

$19,500

Genomic testing program

$40/test

Included in development subsidies

$40/test

The brutal math: Environmental subsidies aren’t just supporting competitors—they’re creating permanent cost advantages you can never overcome through efficiency alone.

The Genetic Environmental Solution

Smart operators are using genomic selection to build environmental advantages that create both cost savings and revenue opportunities:

Methane-Efficient Genetics:

Select for feed efficiency traits that reduce methane output per unit of milk

Target feed conversion ratios of 1.75:1 or better through genomic selection

Generate $25,000-50,000 annual cost savings on 100-cow operations

Component-Environment Integration:

Breed for higher component yields that reduce environmental impact per unit of saleable product

Focus on fertility traits that reduce replacement rates and associated environmental costs

Build genetic profiles that qualify for emerging carbon credit programs

What Smart Operators Are Actually Doing (Beyond Hope and Prayer)

Immediate Defensive Strategies (Next 30 Days)

Stop playing by broken rules. Start thinking like a genetic strategist:

Comprehensive Genomic Audit

DNA test 100% of replacement heifers, not just elite animals

Focus selection on economic traits: components, fertility, health resistance

Eliminate visual appraisal bias that favors appearance over performance

Component Revolution Implementation

Target 4.2% butterfat and 3.3% protein through systematic genetic selection

Prioritize component premiums over volume in breeding decisions

Build genetic profiles that command premium pricing

Beef-on-Dairy Revenue Diversification

Implement strategic crossbreeding on 25-30% of eligible animals

Focus on high-value beef breeds: Wagyu, premium Angus lines

Develop direct marketing relationships for premium crossbred calves

Develop premium component milk contracts that reward genetic superiority

Target processor relationships that value consistent, high-quality genetics

Build direct-to-consumer channels for products from genetically superior animals

The Uncomfortable Truth About New Zealand’s “Miracle”

Here’s the fact that destroys every subsidy defender’s argument: New Zealand abolished all farm subsidies in 1984 and remains a dominant global dairy exporter. Wouldn’t New Zealand have collapsed decades ago if subsidies truly enhanced competitiveness?

Instead, they’ve maintained market leadership through operational efficiency and genetic innovation—exactly what economic theory predicts.

The genomic insight: New Zealand’s continued success demonstrates that genetic merit, operational efficiency, and market positioning create more sustainable competitive advantages than government financial support.

The question this raises: Are subsidized dairy sectors building genuine competitive advantages or dangerous dependencies that will collapse when government support inevitably changes?

Market Intelligence: The Data That Changes Everything

Global Genetic Competitiveness Analysis

Genetic Strategy

Implementation Cost

Annual Genetic Gain

10-Year Advantage

Comprehensive genomic testing

$40,000 (1,000 cows)

£193 per animal

$600,000+ herd value

Partial genetic evaluation

$15,000 (1,000 cows)

£37 per animal

$115,000 herd value

Traditional breeding

$5,000 (1,000 cows)

£0 per animal

No genetic progress

Strategic crossbreeding

$25,000 setup cost

$150 per calf

$400,000+ revenue stream

Strategic insight: Genetic improvements provide the only competitive advantage that compounds annually and cannot be replicated through government intervention.

The Bottom Line: Your Genetic Survival Playbook

Remember that $880 million Russian investment? It’s not just money—it’s a declaration that global dairy competition is now state-sponsored economic warfare.

The myth of “fair competition” in dairy markets isn’t just wrong—it’s dangerous. Operating under this illusion while competitors receive massive government backing is a recipe for slow-motion bankruptcy.

Here’s what separates genetic survivors from subsidy casualties:

First, stop hoping for fairness and start building genetic advantages. Environmental sustainability isn’t just good farming—it’s positioning for premium markets and future carbon credit opportunities while current competitors get paid for practices you’re implementing at cost.

Second, genomic selection provides the only sustainable competitive advantage against unlimited government support. Component yield improvements and breeding efficiency gains compound annually, creating permanent advantages that subsidies cannot replicate.

Third, traditional breeding approaches promoted by industry associations are systematically inferior to comprehensive genomic programs. Challenge conventional wisdom about visual appraisal and pedigree analysis that genomic research has proven less effective for economic traits.

The genetic action plan for the next 12 months:

Immediate Implementation (30 days):

DNA test 100% of replacement heifers, focusing on component traits and reproductive efficiency

Audit current genetic progress using economically relevant metrics, not show ring standards

Implement strategic beef-on-dairy crossbreeding on 25-30% of eligible animals

Genetic Acceleration (3-6 months):

Partner with AI organizations for access to highest-genomic bulls regardless of traditional popularity

Develop herd-specific breeding strategies that maximize genetic progress within facility constraints

Establish 10-year genetic improvement plans with specific component yield and efficiency targets

Create elite cow families within herds for maximum genetic progress acceleration

Develop premium market relationships that reward genetic superiority over commodity volume

Your immediate next step: Calculate your herd’s current genetic merit using genomic evaluations, not traditional breeding methods. Suppose your genomic PLI averages below £400 per animal, or you’re not implementing comprehensive DNA testing. In that case, you’ve identified your biggest strategic vulnerability—and your most important competitive opportunity for building subsidy-proof advantages.

The provocative challenge that should keep every breeding manager awake tonight: If comprehensive genomic selection generates £193 additional lifetime value per animal compared to traditional methods, why are major breed associations still promoting visual appraisal and pedigree analysis that genetic research has proven inferior? The answer reveals an industry more interested in protecting established hierarchies than advancing genetic progress—exactly the kind of conventional thinking subsidized competitors use to their advantage.

The dairy industry’s future belongs to operations that build measurable genetic advantages through DNA-driven selection, not those that hope for favorable trade policies or cling to outdated breeding traditions. The genetic tools exist today to build competitive advantages that no subsidy can replicate. The question is whether you’ll use them.

KEY TAKEAWAYS

Genomic Selection ROI Advantage: Comprehensive DNA testing across 100% of replacement heifers generates £193 additional lifetime value per animal versus traditional methods—creating $96,000 annual genetic gain on 1,000-cow herds that compounds over generations

Beef-on-Dairy Revenue Diversification: Strategic crossbreeding with premium breeds (Wagyu, Angus) on 25-30% of eligible animals creates additional revenue streams worth $150+ per calf while reducing dependency on volatile fluid milk pricing

Component-Focused Competitive Strategy: Target 4.2% butterfat and 3.3% protein through systematic genetic selection to generate $15,000-20,000 additional annual revenue per 100-cow herd through premium component pricing that commodity imports cannot penetrate

Environmental Technology Investment Defense: While subsidized competitors receive government funding for methane reduction technology, genomic selection for feed efficiency traits reduces environmental impact per unit of milk while building genetic merit that accumulates annually

Risk Management Portfolio Enhancement: Layer comprehensive genomic testing ($40,000 investment protecting $600,000+ herd value over 10 years) with strategic component hedging and margin insurance to compete against unlimited government backing through measurable genetic progress

EXECUTIVE SUMMARY

The “free market” fairy tale in global dairy just cost American farmers their competitive edge—here’s your genomic defense strategy. While U.S. producers optimize feed conversion ratios for marginal gains, Russia allocated $880 million in dairy support for 2025 alone, Norwegian farmers pocket subsidies worth 30% of revenue, and Canadian operations receive $328,000 per farm in trade compensation. New research reveals that comprehensive genomic testing generates £193 ($240 USD) additional lifetime value per animal compared to traditional breeding—nearly 30 times the DMC program’s per-cow support. The brutal math: environmental subsidies aren’t just supporting competitors, they’re creating permanent cost advantages you can never overcome through efficiency alone. Smart operators are abandoning hope for “level playing fields” and building genetic advantages that no government subsidy can replicate through strategic genomic selection, beef-on-dairy crossbreeding, and component-focused breeding programs.Stop waiting for trade policy fixes and start building competitive advantages that survive regardless of subsidy policies.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

A Comprehensive Guide to Enhanced Genetic Selection – Reveals specific tools and deterministic models for implementing genomic selection in your breeding program, demonstrating how to achieve balanced genetic gains for fertility and production traits that create sustainable competitive advantages.

Protect Your Dairy Operations from America’s 1000-fold Subsidy Advantage – Demonstrates how component optimization and feed efficiency strategies can neutralize massive subsidy disparities, providing tactical methods to achieve $15,000-20,000 additional annual revenue through premium positioning and operational excellence.

5 Technologies That Will Make or Break Your Dairy Farm in 2025 – Exposes which precision agriculture investments deliver genuine ROI versus expensive distractions, revealing how smart calf sensors and AI analytics can slash mortality 40% and boost yields 20% while competing against subsidized operations.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Discover CME dairy market trends. Global cheese and butter prices affect your business. Check our expert analysis to stay ahead.

Summary:

As we delve into the CME Dairy Reports for October 23rd, 2024, a blend of optimism and caution greets dairy farmers and industry experts. Class III and Cheese futures find new traction, with over 2,500 Class III and nearly 700 Cheese futures trading, signaling a resurgence amidst fluctuating demand and global price disparities. The cheese market balances bearish perceptions with signs of domestic and international demand recovery. Simultaneously, the butter market grapples with equilibrium, encountering price swings, yet suggests global comparisons reveal striking price differences, with U.S. cheese at $1.90 per pound versus Europe’s $2.48 and New Zealand’s $2.13. Butter prices range from $2.69 in the U.S. to $3.74 in Europe, navigating complex factors domestically and abroad. Meanwhile, the NFDM market remains stable, though the California bird flu epidemic poses a potential disruption, with soft demand tempering market shifts, ultimately inviting deeper analysis and strategic consideration.

Key Takeaways:

Class III and Cheese futures show a positive shift despite bearish market sentiments, with significant trading volumes indicating increased investor interest.

The spot cheese market has reached a new equilibrium of around $1.90, balancing perceived price vulnerability and actual market demands.

Cheese market exports suggest improving demand despite non-competitive US pricing on a global scale.

The butter market seeks equilibrium, experiencing variability amidst ample cream supplies and fluctuating domestic and international demand.

The NFDM market remains stable yet vulnerably supported by underlying production impacts like the Bird Flu epidemic in California.

Global dairy price discrepancies highlight varied competitive positions. US pricing is more favorable in the cheese and milk powder markets, contrasted by higher butter costs.

Strategic flexibility, coupled with proactive engagement in market trends and network building, is paramount for dairy farmers and industry professionals to navigate market shifts.

On this sunny October morning, as we look at the CME dairy market, something interesting is brewing. Spot cheese and butter prices are dancing to a new tune, underscoring their pivotal role amid fierce global competition. But what does this mean for those immersed in the dairy world, where every penny counts? As a dairy farmer or an industry professional, have you ever wondered how these price shifts might shape the future of your operations?

In today’s interconnected markets, every dollar and cent in price fluctuation could be the difference between profit and peril. However, in the cheese market, these fluctuations also present profit opportunities, adding optimism to the market dynamics.

The U.S. spot cheese market stabilized at around $1.90 per pound.

European cheese prices are $2.48, with New Zealand trailing at $2.13.

Butter prices range widely across regions, from $2.69 in the U.S. to $3.74 in Europe.

Our journey into the recent CME dairy reports begins with a look at the latest numbers impacting the industry. Let’s dive into the data driving today’s insights.

Commodity

Spot Price (USD)

Change (USD)

Futures Price (Dec)

Global Comparison (EU/NZ)

Class III Milk

$20.58/hwt

+0.14

$20.58

—

Cheese (Blocks)

$1.92/lb

+0.03

$1.94

EU: $2.48, NZ: $2.13

Cheese (Barrels)

$1.9075/lb

-0.0025

$1.94

EU: $2.48, NZ: $2.13

Butter

$2.655/lb

-0.0225

$2.71

EU: $3.74, NZ: $2.87

NFDM

$1.36/lb

—

—

EU: $0.41, NZ: $0.51

Trading Surge Defies Bearish Trends in Class III and Cheese Futures

The current market dynamics for Class III and cheese futures show a noticeable uptick in trading volume, with over 2,500 Class III and nearly 700 cheese futures being exchanged. This increase highlights a rising interest from market players despite the lingering bearish sentiment. As prices in nearby futures have dipped, new buyers see this as an entry point. Open interest reflects this renewed engagement, although November Class III futures remain an exception.

While the market buzzes with the perception of vulnerability due to recent price weaknesses, the underlying reality suggests stability near the $1.90 cheese spot price. Although prices have dropped significantly since early September, demand restrains from a bullish swing. This consolidation suggests that the market willingly clears products at this level, waiting for a justifiable need—quick cash conversion or fulfilling the last cheese requirement.

Spot Cheese Market: A Balancing Act Between Perception and Reality

When examining the recent dynamics of the spot cheese market, it becomes evident that trading patterns have predominantly hovered around the $1.90 mark. This level isn’t just a figure on the trading charts; it represents a historical anchor, reflecting the extensive market memory associated with this pricing tier. The fluctuations around this price point highlight a broader narrative of cautious optimism tempered by market realities. This $1.90 mark is significant, representing a balance point where the market has historically found stability.

The release of the September Milk Production report injected a fresh wave of bearish sentiment into the market ecosystem. With milk production figures surpassing expectations, market participants have recalibrated their outlooks, assessing potential vulnerabilities in cheese pricing. The report casts a shadow over the perceived stability, with many traders anticipating further price declines if surplus conditions persist. The report’s findings have led to a shift in market sentiment, with many now expecting a downward price trend if surplus conditions continue.

Despite the perceptions fueled by the September Milk Production report, the cheese market is resilient. This resilience should reassure stakeholders about the market’s ability to weather potential challenges and maintain stability.

Cheese Market: A Delicate Balance Between Optimism and Caution

For the cheese market, sentiment is a nuanced dance between optimism and cautious watchfulness. As prices hang around the $1.90 mark, which many have recognized as a comfortable familiarity, there’s a growing belief that this stability is less about chance and more about a complex interplay of factors.

One pivotal element in maintaining this equilibrium is rising domestic demand. As we approach the cooler months, a predictable uptick in consumption—think festive gatherings and comfort foods—naturally drives cheese sales. These seasonal trends subtly nudge domestic buyers to restock their shelves, hinting at a potential price uplift and instilling hope in the market’s future.

Meanwhile, export markets are starting to regain relevance. Despite past challenges in international price competitiveness, anecdotal insights suggest a refreshing vigor in overseas demand. U.S. cheese is finding its place on foreign plates more than in recent months, perhaps prompted by strategic pricing or a revival in global appetite.

Adding another layer to this steady landscape are the lighter inventories. Current stock levels are not overwhelming, providing a natural cushion against excessive price declines. ‘Lighter inventories’ refer to the current stock levels that are not excessive, which helps prevent a significant drop in prices due to oversupply. This reduced inventory is a subtle price support, ensuring that prices can maintain their current levels without the looming threat of oversupply.

However, as we know, stability in commodity markets can be as fragile as a cheese souffle. A sudden surge in demand, whether domestic or international or any disruption in milk production could rapidly tilt the balance. This leaves us wondering: Is the cheese market on the verge of a stealth rally, or will it sustain this steady path into the new year?

The Butter Market: Finding Its Feet in a Turbulent Dance

When we examine the butter market, we see a dance of search and equilibrium reminiscent of Wall Street’s volatile swings. Wednesday’s trading lull among butter buyers triggered a notable decline in the cash price, which fell by 2.25 cents. Yet despite this drop, we’re still hovering above the previous low of $2.61. So, what’s going on here? The market is in flux, seeking a level where buyers and sellers can comfortably meet once more.

Now, here’s where it gets interesting. The market is feeling heavy, echoing a sentiment that it’s close to bottom. Fluctuations are expected to continue as the market tries to find its footing. Some domestic factors impacting this are ample cream supplies and the whisper of light demand, which has kept the market tentatively moving upward. Given these dynamics, the butter market is in a holding pattern, waiting, watching, and ready to pivot.

Despite these domestic pressures, the international scene offers a glimmer of opportunity. U.S. butter prices could stir some export activity, albeit modestly. Although the U.S. isn’t light on global butter exports like cheese or NFDM, our prices could entice international buyers seeking alternatives to the pricier European options. With U.S. butter priced at $2.69 per pound, compared to Europe’s lofty $3.74, there’s room to grow U.S. exports if demand elsewhere tightens.

The butter market’s dance is far from over. While domestic demand stays tepid, the string-pulling of international trade dynamics could lead to interesting, albeit cautious, moves in the coming weeks. As dairy professionals, watching domestic cream supplies and global price disparities could provide strategic insights for betting on the following market turns.

NFDM Market: Stability With a Side of Uncertainty

The NFDM market continues to exhibit a noteworthy level of stability, with the week’s trading activity reflecting a steady environment. Recent trades saw 11 spot loads maintaining a consistent price of $1.3600 per pound, illustrating the market’s resilience amidst fluctuating commodities. Despite a tapering of futures volume to 153 contracts, the patterns remained mixed, though mainly trending upwards, suggesting an undercurrent of cautious optimism.

However, the bird flu epidemic in California has introduced a potential disruptor, now quietly acting as an underlying influence in the market. While the immediate repercussions haven’t triggered a dramatic shift, the epidemic’s interference with milk production could prime the market for volatility. California’s impact is significant, given that approximately 50% of U.S. NFDM/SMP originates from there.

The persistent issue of soft or spotty demand also presents formidable obstacles. This demand slump counterbalances potential price hikes that might result from production stresses. Soft demand remains a headwind, keeping price escalation and substantial market shifts in check, at least for the moment.

Yet, this unique juxtaposition—steady prices, looming competitive pressure from lower-cost international markets, notably Europe and New Zealand, and domestic production challenges—poses a pending puzzle for market participants. As these elements collide, will the NFDM market remain tethered by its stability, or are we on the brink of an imminent shift?

The Price Puzzle: Navigating Global Discrepancies in Dairy Commodities

Regarding global competition, the prices of cheese and butter in the U.S., Europe, and New Zealand showcase stark differences that directly influence market dynamics. European cheese commands the highest price, $2.48 per pound, a significant lead over the U.S. price of $1.94 per pound and New Zealand’s at $2.13. This price disparity gives U.S. cheese a competitive edge in international trade, potentially driving up export demand as it becomes more attractive for global buyers seeking cost-effective solutions.

Similarly, the butter market reveals intriguing contrasts. Europe maintains hefty butter prices at $3.74 per pound, leading the global stage, followed by New Zealand at $2.87 and the U.S. at $2.69. This positioning suggests that, while U.S. butter prices remain lower than Europe’s, they still present a strategic advantage against New Zealand, positioning American butter producers well to capitalize on price-sensitive markets.

Turning to milk powder, the dynamics shift dramatically. U.S. nonfat dry milk (NDM) and skim milk powder (SMP) hold their ground at $0.60 per pound but face fierce competition from New Zealand, priced at $0.51, and Europe at the most competitive rate of $0.41. These variations in pricing potentially inhibit U.S. market share in Asia and other vital regions where price competitiveness is paramount. Consequently, American producers may need to explore value-added strategies or niche markets to sustain international appeal amidst these pricing challenges.

Understanding these price discrepancies is essential for U.S. dairy farmers and professionals navigating a landscape teeming with opportunities and threats. The global marketplace is ever-evolving, and staying competitive requires astute awareness and strategic adaptation.

The Bottom Line

The volatility seen in Class III and Cheese futures this week underscores the complexities and uncertainties prevailing in the global dairy market. Our discussion highlighted the tug-of-war between bullish perceptions and bearish realities within the U.S. cheese sector and a balancing act influenced by domestic and export demands. For butter, we observed a challenging pursuit of equilibrium amidst fluctuating prices, with ample cream supplies posing a persistent obstacle. Meanwhile, the NFDM market remains stable yet is subtly affected by factors like California’s Bird Flu epidemic, illustrating the intricate web of causes and effects that define dairy trading today.

Furthermore, the stark price discrepancies among international players like Europe, the U.S., and New Zealand reaffirm the interconnected nature of global dairy markets, which pose opportunities and hurdles for U.S. producers. Such dynamics compel us to ask: Are we ready to adapt to these global pricing puzzles?

The future holds possibilities for growth and resilience, but only if we remain attentive to these market currents. What are your thoughts on these developments? Do you see similar patterns in your operations or local markets? Let’s delve deeper into this discussion—share your insights in the comments below or with your network. Your perspectives are invaluable in navigating the ever-shifting landscape of dairy commodities.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we and our partners use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us and our partners to process personal data such as browsing behavior or unique IDs on this site and show (non-) personalized ads. Not consenting or withdrawing consent, may adversely affect certain features and functions.