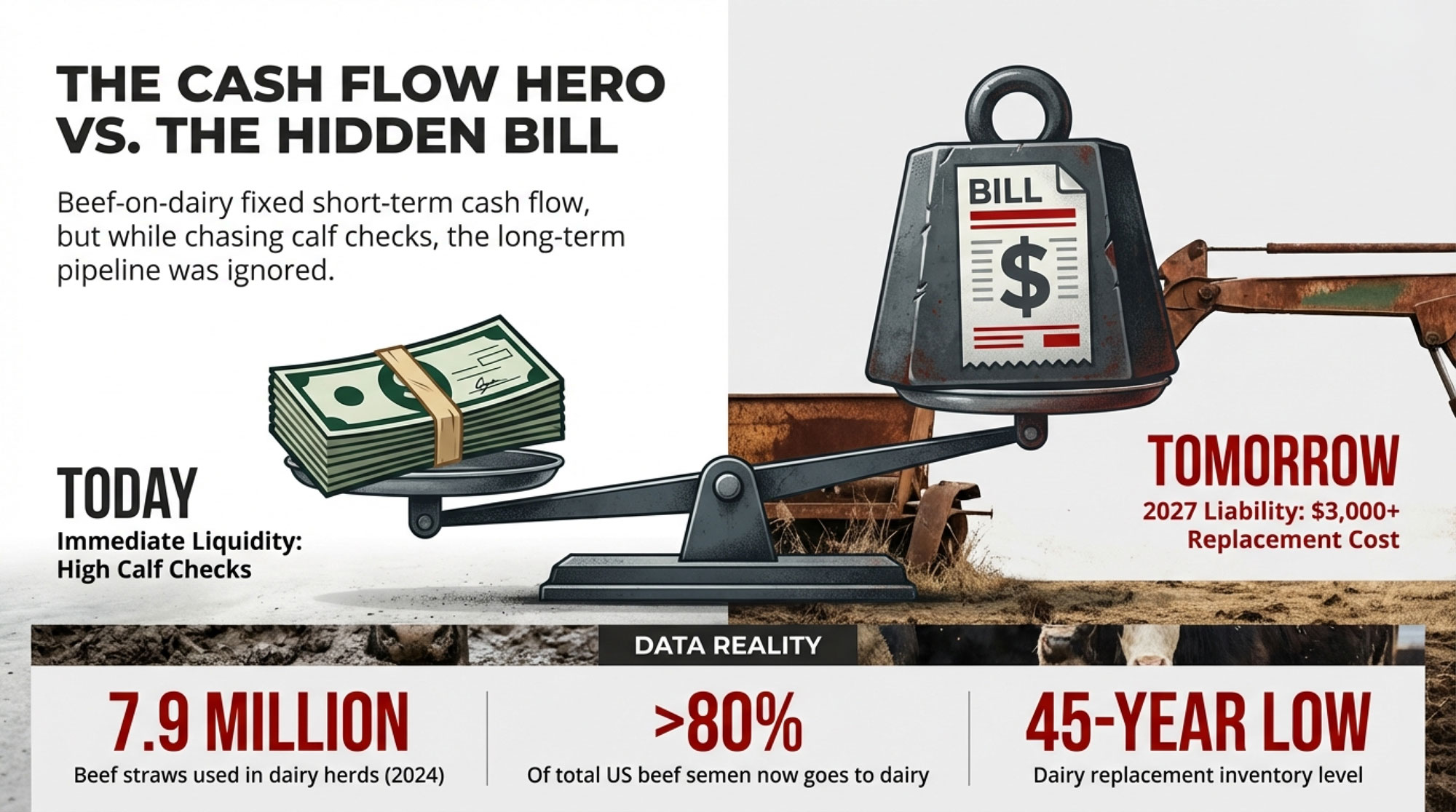

If your only beef-on-dairy metric is today’s calf cheque, you’re ignoring the $3,000 heifer bill with your name on it.

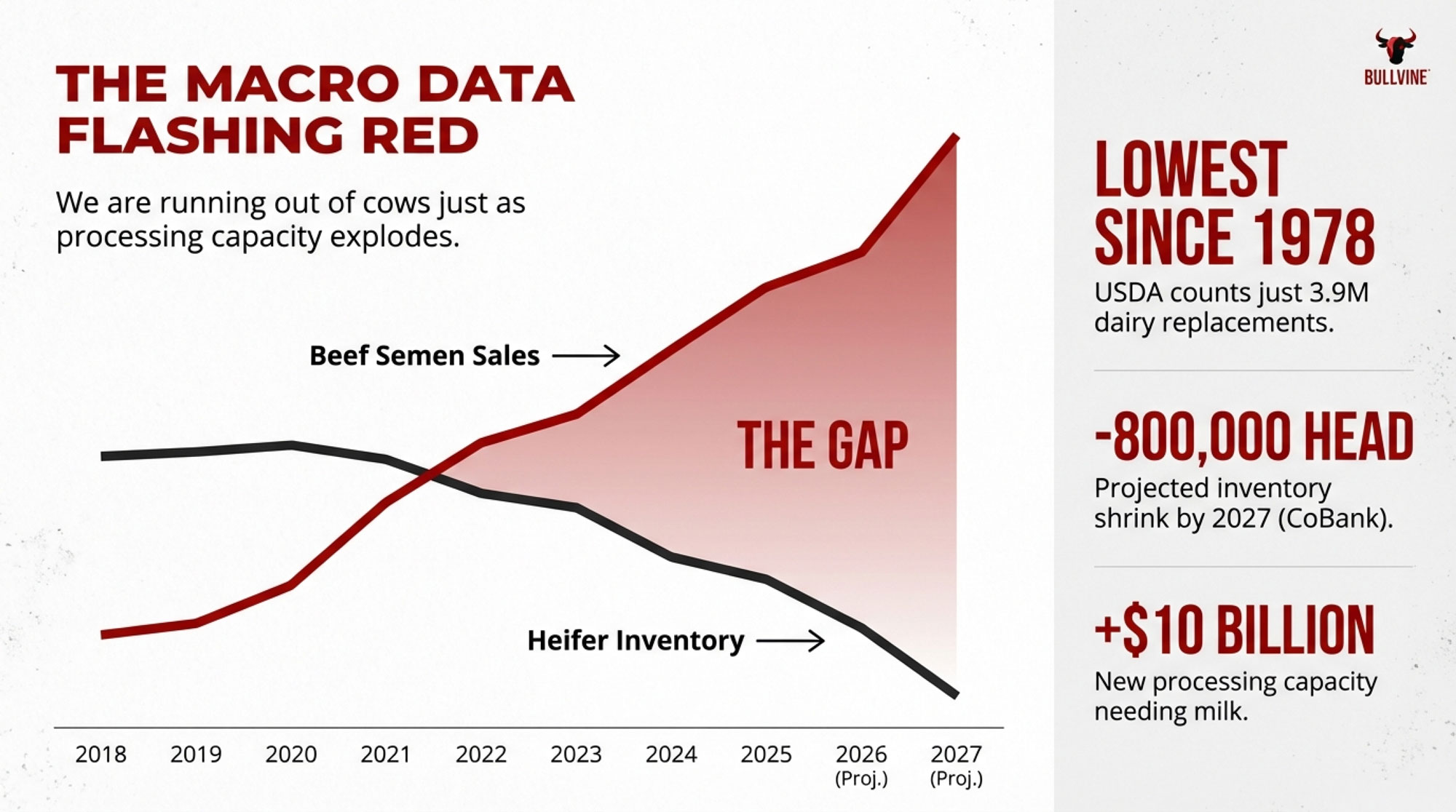

EXECUTIVE SUMMARY: Beef‑on‑dairy has been a cash‑flow hero for many herds, but the big math now flashing red is hard to ignore: 7.9 million beef straws into dairy cows, 800,000 fewer heifers ahead, and replacement prices already north of US$3,000 in many regions. USDA counts just 3.914 million dairy replacements as of January 1, 2025—the lowest since 1978—while CoBank projects inventories will shrink by about 800,000 head before recovering near 2027, right as roughly US$10 billion in new processing capacity comes online and needs milk. What’s interesting here is that the article shows reproduction, not semen color, is the real gatekeeper: herds under roughly 20% 21‑day PR that breed heavily to beef aren’t just “cashing in,” they’re effectively scheduling a heifer shortage and future cheques for someone else’s US$3,000 heifers. Drawing on economic modeling from Albert De Vries, PhD (University of Florida), and sector work by Jan Hulshof, PhD (Wageningen), it outlines practical “guard rails” for how much beef‑on‑dairy a herd can safely run at different PR levels, especially when combined with genomics and sexed semen on the top genetics. A five‑question framework then helps producers stress‑test their own program—repro, heifer pipeline, genomic use, calf/transition management, and calf marketing—so they can see whether they’re building a sustainable strategy or quietly writing a US$30,000–60,000‑a‑year heifer bill for 2027 and beyond. The takeaway is simple but not always comfortable: beef‑on‑dairy is a powerful profitability tool, but only when it sits on top of strong reproduction and disciplined heifer planning instead of short‑term calf prices.

If you sit down with dairy folks this winter—from big freestalls in Wisconsin to tie‑stalls in Ontario to those dry lot systems in the Texas Panhandle—you’ll hear a familiar line: “Beef‑on‑dairy really helped our cash flow… and now we’re wondering where the heifers went.”

What’s interesting is that this isn’t just coffee‑shop talk. The national numbers are telling the same story a lot of you are seeing when you walk past your heifer pens—and now we’re staring at US$3,000‑plus heifer tags when it comes time to fill the gaps.

The latest Regular Members Semen Sales Report from the National Association of Animal Breeders (NAAB) shows that in 2024, U.S. producers bought about 9.7 million units of beef semen, and roughly 7.9 million of those units were used in dairy herds, not beef herds. Industry reports indicate that more than 4 out of 5 beef straws in the U.S. now go into dairy cows.

At the same time, USDA’s January 1, 2025, cattle inventory report put the U.S. beef cow herd at about 27.86 million head. Analysts at Angus Journal and university extension have highlighted that the smallest U.S. beef cow herd since the early 1960s is down several million head from where it sat in 2019. So we’ve got record beef semen use in dairies sitting on top of the tightest beef cow numbers in more than half a century.

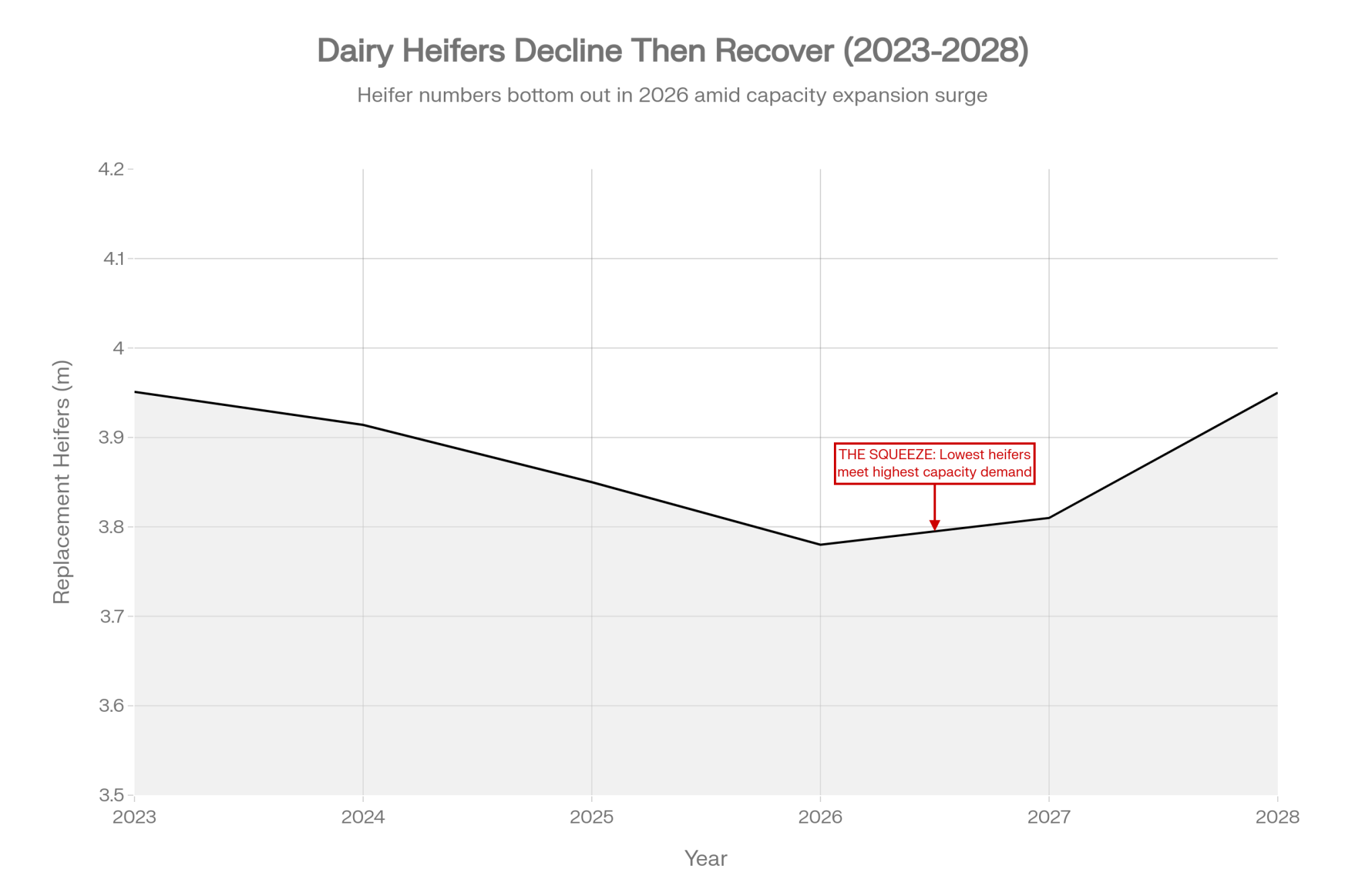

And here’s where the conversation really sharpens. CoBank’s dairy team, led by Corey Geiger, MBA, released a 2025 analysis showing that U.S. dairy replacement heifer inventories are already at about a 20‑year low and could shrink by an estimated 800,000 head over the next two years before starting to rebound closer to 2027. That same CoBank work highlights that roughly 10 billion dollars in new dairy processing capacity, much of it cheese and ingredient plants that live on butterfat performance and protein, is scheduled to be online by 2027. Those plants will need milk, and milk needs cows.

| Year | Replacement Heifers (M) | New Capacity Online (USD B) |

|---|---|---|

| 2023 | 3.951 | $2.1 |

| 2024 | 3.914 | $4.2 |

| 2025 | 3.85 (proj) | $6.8 |

| 2026 | 3.78 (proj) | $8.9 |

| 2027 | 3.81 (recovery begins) | $10.2 (peak) |

| 2028 | 3.95 | $10.2+ (operational) |

So the real question isn’t just “Is beef‑on‑dairy a good idea?” It’s “Given where milk, beef, and heifer supplies are heading, is the way we’re using beef‑on‑dairy going to build our business—or back us into buying very expensive heifers a couple of years from now?”

Let’s walk through that together, the way we’d talk it through over coffee at the kitchen table.

How We Got Here: Three Big Shifts That Opened the Door

Looking at this trend, three big changes really opened the gate for beef‑on‑dairy: sexed semen that finally works well enough to plan around, genomics that actually drive decisions, and a beef cow herd that’s the smallest it’s been in decades.

1. Sexed semen finally got reliable enough to plan around

You probably remember the early days of sexed semen. Back in the late 2000s and early 2010s, university trials and extension bulletins regularly reported conception rates 25–30 percent lower than conventional semen in many herds, and that matched what plenty of us saw in our own breeding records. It was great when it worked, but too many repeats and open cows made it a tough sell outside a handful of show heifers or elite donors.

Over the last decade, that story has shifted. With improved sorting technology, better extenders, and higher sperm numbers per straw, modern sexed semen has narrowed the gap. Extension educators and field data now suggest that in well‑managed heifer programs, sexed semen often delivers conception rates in the mid‑40 percent range, sometimes approaching 50 percent in top herds, while conventional semen on the same heifers tends to run about 5–10 points higher. In cows, the difference is often similar or slightly wider, and it’s more sensitive to fresh-cow management and heat detection.

So in real‑world terms, what farmers are finding in solid heifer programs is that sexed semen now runs roughly 75–85 percent of conventional conception rates, with a few very dialed‑in herds creeping up closer to 90 percent. That aligns with the research summaries from land‑grant universities and industry meetings. It still demands good transition‑period care, sharp heat detection, and careful semen handling, but it’s finally good enough to build a replacement strategy around instead of just dabbling.

2. Genomics went from “nice‑to‑have” to “we actually use this”

The second big shift is genomics. Ten or twelve years ago, genotyping felt like something that happened in AI stud offices and a few elite Holstein barns. Today, millions of animals are genotyped, and research from USDA’s Agricultural Research Service (ARS) and the Council on Dairy Cattle Breeding (CDCB) shows that genomic evaluations for young heifers deliver substantially higher reliability than old‑style parent averages for traits like milk, fat, protein, daughter pregnancy rate, and some health traits.

What I’ve noticed, especially in Midwest and Ontario herds that are leaning into this, is that once producers start using genomic rankings, it changes the conversation around both beef‑on‑dairy and replacement rearing:

- Heifer calves get genotyped through CDCB‑approved programs.

- The herd ranks them on Net Merit, Pro$, or a custom index that weights production, components, fertility, mastitis resistance, and longevity in line with how their milk is priced.

- The best group becomes the “sexed semen group,” a middle group is flexible, and a lower‑merit group is deliberately steered toward beef semen or not raised at all.

In an economic simulation published in JDS Communications, Albert De Vries, PhD, at the University of Florida, and colleagues modeled this kind of strategy—sexed semen on the top end, beef semen on the bottom, genomics guiding who’s who—and found that income from calves over semen and rearing costs improved compared with a simple “all dairy semen” approach. That finding lines up with what many progressive herds report: they raise fewer marginal heifers, capture more value from beef‑on‑dairy calves that never belonged in the milking string, and keep their replacement pipeline more intentional.

3. The beef cow herd shrank—and it’s not bouncing back quickly

The third piece is beef. USDA’s cattle inventory reports show the U.S. beef cow herd has dropped from around 31.7 million head in 2019 to 27.86 million as of January 1, 2025. Extension economists note this is the smallest beef cow herd the U.S. has seen since the early 1960s, driven by multi‑year drought in the Plains and West, high feed costs, and an aging rancher base that hasn’t rushed to rebuild.

Rabobank’s beef team analyzed cow–calf returns over the last decade and found that from 2013 to 2017, U.S. cow–calf operations averaged about 153 U.S. dollars per cow per year. From 2018 through 2022, those returns flipped negative, averaging roughly minus 21 dollars per head per year when revenue was stacked up against operating costs, labor, taxes, and insurance. When you put drought risk on top of that, it’s not surprising that a lot of ranchers were slow to restock.

On the dairy side, CoBank points out that U.S. dairy is in the midst of an historic processing build‑out—about $ 10 billion in new or expanded plants, largely focused on cheese and ingredients that reward butterfat and protein. Those plants will want milk, and they’ll want it relatively quickly over the next couple of years.

Meanwhile, industry sales data using CattleFax estimates show beef‑on‑dairy calves going from about 410,000 head in 2018 to around 2.6 million in 2022. An American Association of Bovine Practitioners (AABP) paper titled “The future of dairy‑beef in cattle production,” led by Daniel Grooms, DVM, PhD, at Michigan State University, projects that with widespread use of sexed semen, more than 3.5 million beef‑on‑dairy animals could be entering the U.S. fed beef supply annually in some scenarios.

So this development suggests a pretty clear story: fewer native beef calves, more dairy cows bred to beef, tight heifer numbers, and big new processors coming online. Beef‑on‑dairy has moved from side‑gig to structural pillar in a hurry.

Two Ways Herds Are Using Beef‑on‑Dairy—and Why the Outcomes Look So Different

Once you accept that the big‑picture economics support beef‑on‑dairy, the real question becomes: “How are we using it on our farm?” That’s where you start to see two very different paths.

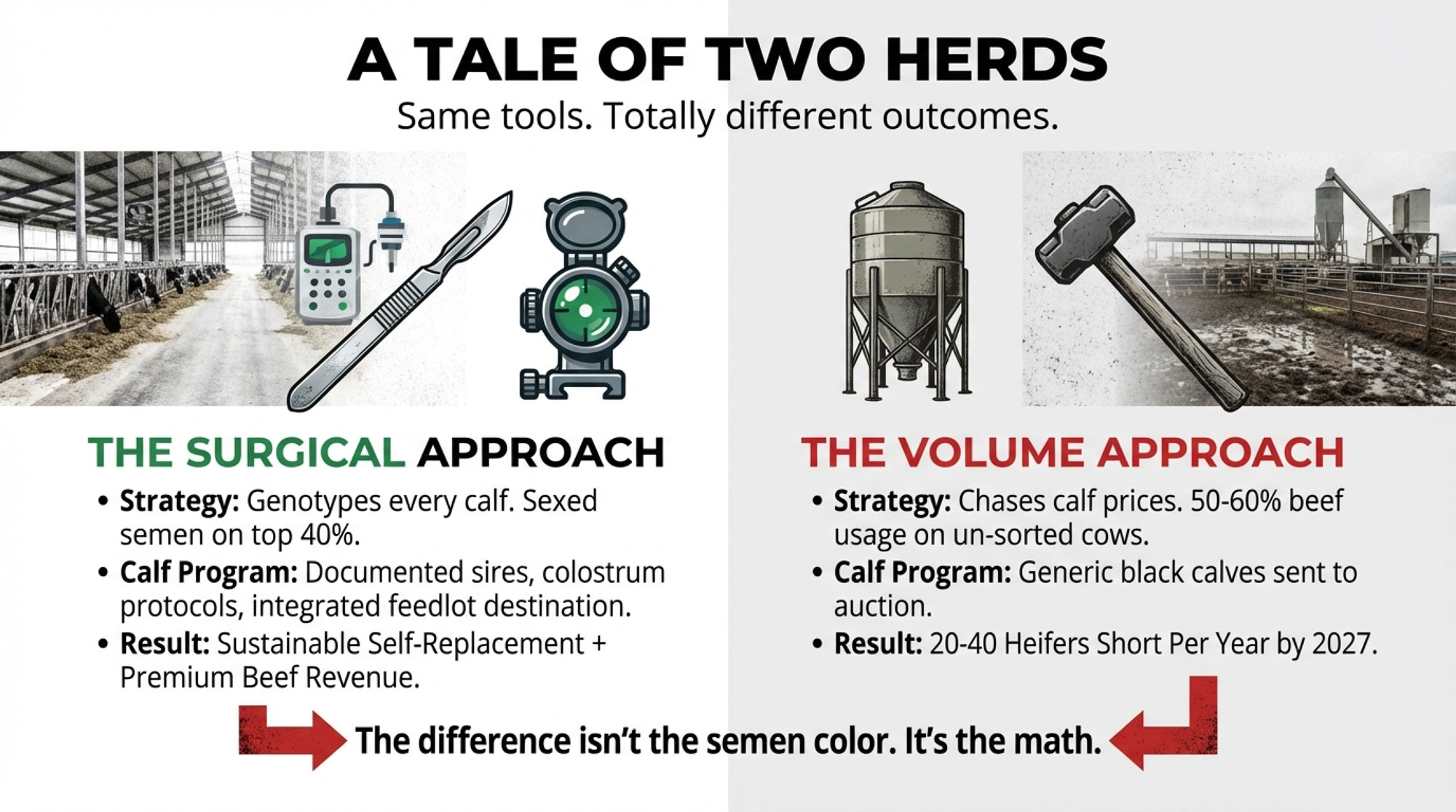

The “surgical” approach: disciplined, data‑driven, and usually well‑rewarded

Picture a 750‑cow Holstein freestall in eastern Wisconsin or a 1,200‑cow dry lot herd in California’s Central Valley. They’re working with a herd veterinarian, a PhD nutritionist who lives in the fresh cow data, and a genetics adviser who knows their goals cold.

What farmers are finding in operations like this is that beef‑on‑dairy is treated like a scalpel, not a sledgehammer:

- Almost every heifer calf is genotyped within 60 days of birth.

- Twice a year, cows and heifers are ranked on a profit‑focused index (Net Merit, Pro$, or a custom index using CDCB and herd data).

- Breeding decisions follow that ranking very closely:

- Top 35–40 percent get sexed dairy semen on first service and often second.

- A middle 20–30 percent is a “swing group” that may get sexed, conventional, or beef, depending on projected heifer needs.

- The bottom 30–35 percent get beef semen exclusively.

On the beef side, they’re using bulls from programs built for beef‑on‑dairy—high calving ease, strong marbling and ribeye EPDs, moderate mature size, and documented performance on dairy crosses, drawing from Beef Improvement Federation guidelines and AI stud beef‑on‑dairy sire lists. They’re not just chasing black hides; they’re aiming for cattle that will grow, grade, and hang a carcass the packer wants.

Those calves usually aren’t disappearing into the local sale barn. Many go into integrated dairy‑beef programs in Nebraska, Kansas, and the High Plains. These programs typically require:

- Recorded sire IDs and, ideally, dam information.

- Colostrum measured by Brix refractometer, with documented volumes and timing.

- Specific vaccination and weaning protocols.

- Consistent shipping ages and weights.

In return, feedlots and packers share performance and carcass data, including average daily gain, health outcomes, liver scores, dressing percentage, quality, and yield grades. National Beef Quality Audit (NBQA) reports show that marbling scores and the share of carcasses grading Choice and Prime are at or near record highs, and dairy‑influenced cattle contribute to that when they’re managed appropriately. Research from Texas Tech and other universities has shown that when marbling levels and cooking conditions are matched, consumers generally rate steaks from dairy‑influenced cattle as comparable in tenderness and flavor to those from conventional beef breeds.

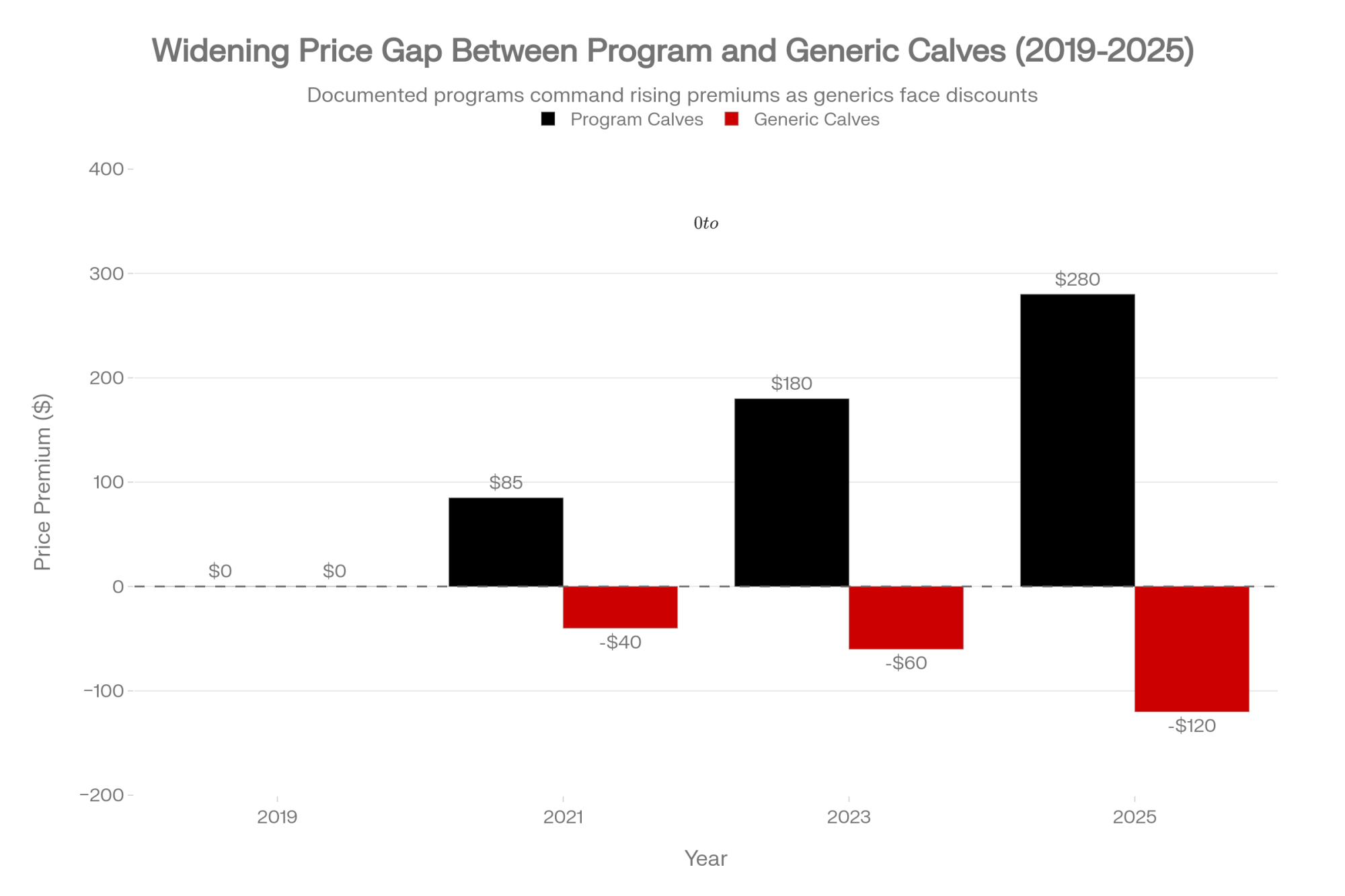

That’s why well‑documented dairy‑beef calves from known programs are often bringing a clear premium over generic calves at similar weights in recent sale reports. In herds that follow this “surgical” approach, beef‑on‑dairy fits cleanly into a bigger system: repro, genetics, calf care, and marketing all point in the same direction.

The “volume” approach: chasing calf prices, then feeling the heifer pinch

Now let’s think about a more typical picture for a lot of farms in the Northeast, Great Lakes, and Ontario: a 250‑ to 400‑cow herd, solid people, busy days, plenty going on.

In 2022 and 2023, many of these barns saw local auction reports and buyer bids showing very strong prices for crossbred beef‑on‑dairy calves—often several hundred U.S. dollars higher than straight Holstein bull calves of similar weight. In some U.S. regions and Canadian sales, top‑end dairy‑beef calves were creeping into the upper hundreds of dollars and, at times, flirting with four‑figure prices if they were the right type at the right time.

So they did what any rational business would do in that moment: they leaned into beef semen.

- Maybe 50–60 percent of cows got bred to beef, often targeting older or softer cows, but usually without genomic data to define “bottom end.”

- Heifers saw some sexed semen, more to “make sure we have enough heifers” than as part of a tightly modeled plan.

- Calves were sold through local barns as beef crosses, with basic colostrum and vaccinations, but few records following them, and no integrated program specs.

For a year or two, those calf cheques looked great. Pens were busy. It felt like the right move.

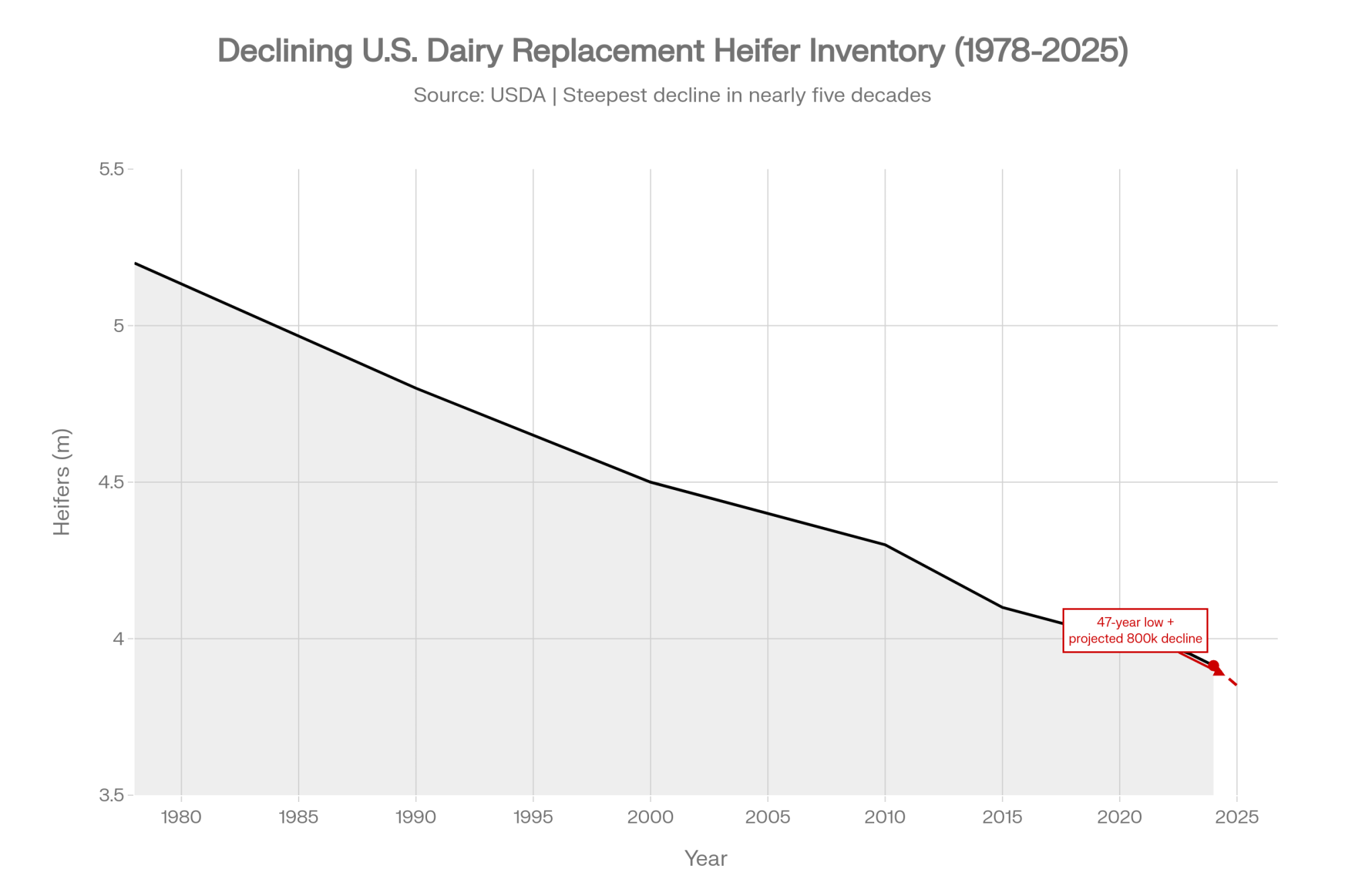

Then, USDA and CoBank put some harder numbers to the national heifer picture. They highlighted that on January 1, 2025, the U.S. had just 3.914 million dairy replacement heifers—down from 3.951 million the year before and the lowest since 1978. CoBank’s report projected that inventories could shrink by around 800,000 head over the next two years before recovering in 2027, and that high‑quality heifers were already bringing record prices with potential to go “well above $3,000 per head” in many regions.

When these “volume” beef‑on‑dairy herds sat down with their advisors and laid out heifer inventories by age—0–6, 6–12, 12–18, 18–24 months—and rolled those forward against their normal cull rate, some discovered they were on track to be 20–40 heifers short of their usual replacement needs for 2026–2027. In the same breath, market reports in the U.S. and Canada showed quality replacements bringing about US$3,000 or more in tight U.S. areas and C$4,000–5,000 at special sales in parts of Ontario and Western Canada.

So the narrative quietly shifted from “Beef‑on‑dairy saved our cash flow” to “We might have to buy a truckload of very expensive heifers because we got ahead of our repro and replacement planning.”

On top of that, feedlots and packers have been vocal—through AABP sessions, NBQA debriefs, and trade press—about preferring calves from known herds with documented genetics and health histories, and discounting anonymous calves where they don’t know what they’re getting. That gap in value between “program calves” and “generic black calves” has widened as more dairy‑beef cattle hit the system.

Same toolbox: sexed semen, beef semen, genomics. Very different outcomes.

What Packers and Feedlots Are Really Saying About Dairy‑Beef

When you listen closely to packer reps and feedlot managers at meetings or in interviews, they’re not out to shut down dairy‑beef. What they want is cattle that work on their end of the ledger.

The good news: they like how it eats

From a meat‑quality standpoint, dairy‑influenced cattle can be a real asset:

- The 2022 National Beef Quality Audit reported that marbling scores were the highest ever recorded in the NBQA series, with a larger share of carcasses grading Choice and Prime than in previous audits. Dairy‑influenced cattle, both Holstein and beef‑on‑dairy crosses, contribute to those marbling numbers when they’re fed and managed well.

- Research at Texas Tech and other universities, summarized in dairy and beef industry media, has shown that when marbling and cooking conditions are similar, consumer taste panels often rate steaks from dairy‑cross and conventional beef cattle similarly for tenderness and flavor.

So from the consumer’s perspective—knife and fork in hand—well‑finished dairy‑beef can perform just fine.

The pain points: health, conformation, and dressing percentage

Where the challenges show up is in three familiar areas:

- Liver health. NBQA findings and packer feedback point to liver abscesses as a persistent and costly issue, particularly in some high‑grain finishing programs, and the AABP dairy‑beef paper flags liver abscess rates as a key concern in some dairy‑beef pens. Each condemned liver is lost value and is usually a sign that subclinical health issues have already trimmed average daily gain.

- Carcass conformation. Holsteins and many dairy crosses tend to be narrower and more framey than traditional beef steers at a given weight. Board‑invited reviews in Translational Animal Science have noted that this can make it harder to hit certain boxed beef and steak‑size specs, especially for programs that want a consistent ribeye size or steak portion.

- Dressing percentage. Those same reviews and multiple feedlot trials show dairy‑influenced cattle generally dress lower than conventional beef steers. Even a couple of points difference in dressing percentage can mean a meaningful shift in dollars per head on most grids.

What’s encouraging is that none of this is a deal‑breaker. The AABP paper and extension work on dairy‑beef and surplus calf management emphasize that strong colostrum programs, consistent calf rearing, thoughtful step‑up rations, and smart sire selection can make dairy‑beef cattle very competitive. The key is whether those calves show up as part of a system that’s designed for that, or as random calves with unknown histories.

The 2026 Heifer Squeeze: A Lagging Result of 2023–2024 Choices

Now let’s swing back to replacements, because that’s where this all lands for most herds.

You already know the biology, but it helps to line it up with the calendar:

- Breed a cow today, and if she settles, you get a calf in about nine months.

- If that calf is a heifer and you raise her, she’ll freshen roughly 22–24 months later, depending on your heifer program.

So the heifers freshening in 2026 are mostly the product of what you bred in 2023 and early 2024—the exact period when beef‑on‑dairy semen use really spiked.

NAAB’s semen data shows that domestic beef semen sales hit new highs in 2023 and 2024, with about 9.7 million beef units sold in 2024 and 7.9 million of those going into dairy herds. USDA’s January 2025 cattle report pegged dairy replacement heifers at 3.914 million head, down from 3.951 million a year earlier and the lowest since 1978.

CoBank’s 2025 heifer report took those numbers, combined them with typical calving and culling patterns, and concluded that total replacement heifer inventories are likely to shrink by around 800,000 head over the next two years before starting to rebound near 2027. They also noted that high‑quality heifers have already reached record values—well above US$3,000 per head in some U.S. regions—and could move higher if supplies tighten as expected.

So if you’re looking at your heifer pens this winter and thinking, “This feels thinner than it should be,” you’re not alone—and you’re not imagining it. Part of that is the national picture. Part of it traces straight back to how aggressively you used beef semen in 2023–2024 relative to your reproduction and heifer‑raising performance.

How Much Beef‑on‑Dairy Can Your Herd Really Support?

Here’s where fresh cow management and reproduction quietly decide how far you can safely push beef‑on‑dairy.

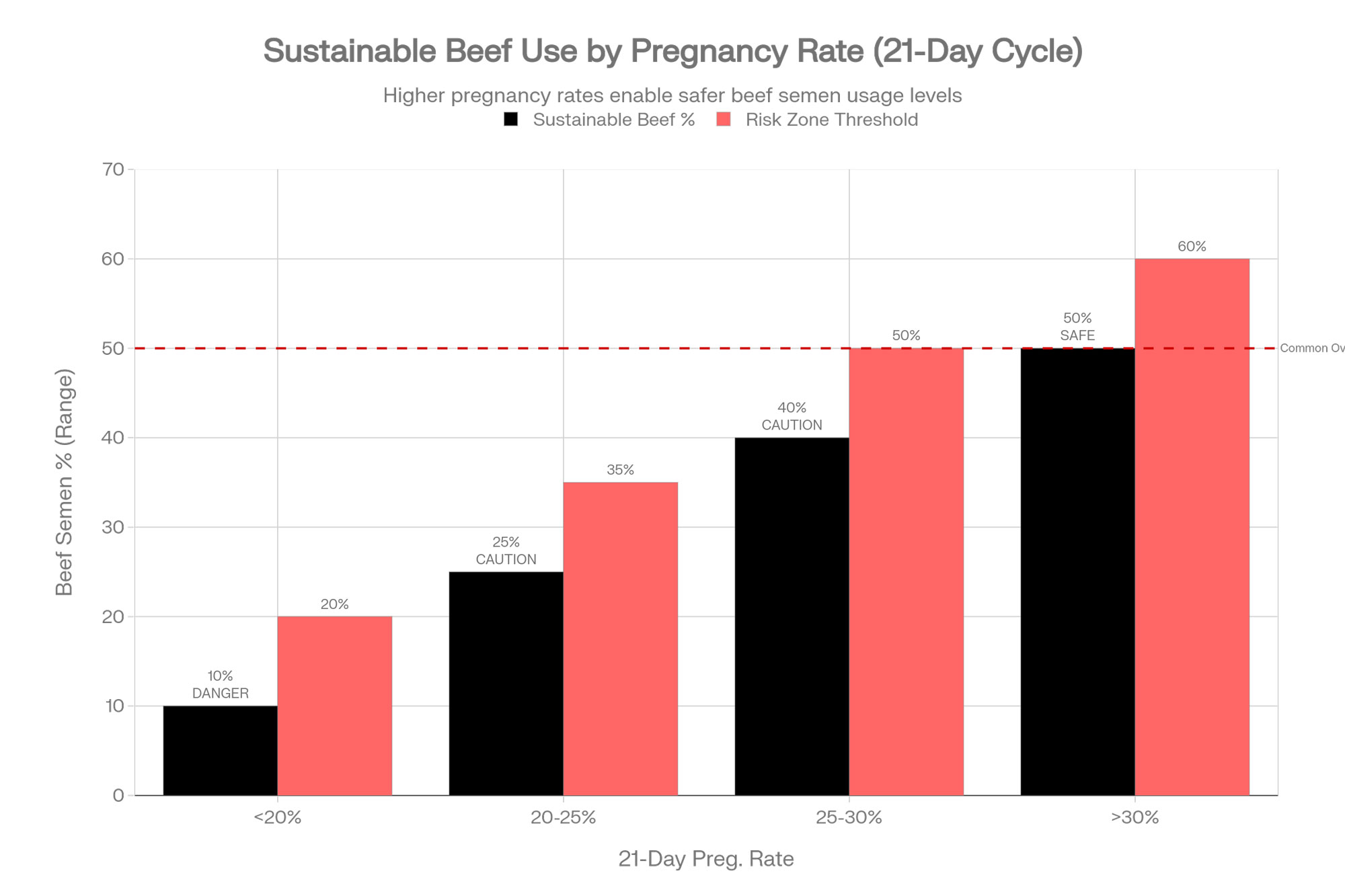

Looking at this trend, the consistent message out of economic modeling and extension work is that the 21‑day pregnancy rate is the key gatekeeper. In a series of papers, De Vries and co‑authors showed that the higher the 21‑day PR, the more room a herd has to use beef semen without starving itself for replacements, especially when using sexed semen on the top genetics.

Putting it into everyday terms—and blending what the models say with what consultants see—these “guard rails” keep popping up:

- 21‑day PR under about 20 percent. For most herds in this band, it’s hard enough just to make enough replacement heifers with mostly dairy semen. Modeling and field experience suggest that if you’re in this range and breeding a big chunk of the herd to beef, you’re almost certainly scheduling a heifer shortage and future heifer purchases.

- 21‑day PR in the 20–25 percent range. At this level, there’s usually room for some beef‑on‑dairy—often something like 20–30 percent of matings—if you’re using sexed semen on your best cows and heifers and actually tracking your heifer pipeline by age group. But there’s not much slack for a spike in culls or a health event in the heifer program.

- 21‑day PR in the 25–30 percent range. Here, the economics and the farm‑level stories line up: many herds can support roughly 35–45 percent of breedings to beef semen and stay self‑replacing, provided they keep heifer losses modest and stick to a genomic or performance‑based ranking for who gets sexed semen.

- 21‑day PR consistently above 30 percent. Once herds reach 30 percent 21‑day PR, with solid transition performance and steady culling, they often have substantial flexibility. These herds can frequently breed around half—or a bit more—of their cows to beef semen and still maintain or even grow herd size, as long as they’re disciplined about using sexed semen on the right animals.

That 2023 Animals paper from Wageningen University & Research, led by Jan Hulshof, PhD, reached a similar conclusion in European modeling: beef‑on‑dairy improves efficiency and profitability when combined with sexed semen and strong reproduction, but it creates pressure on replacements and can raise welfare issues if used mainly to chase high calf prices without that foundation.

If you want the blunt version of what’s hiding in those graphs, it’s this: if your 21‑day PR is under 20 percent and roughly half your services are to beef, in most herds you don’t have a beef‑on‑dairy strategy—you have a scheduled heifer problem.

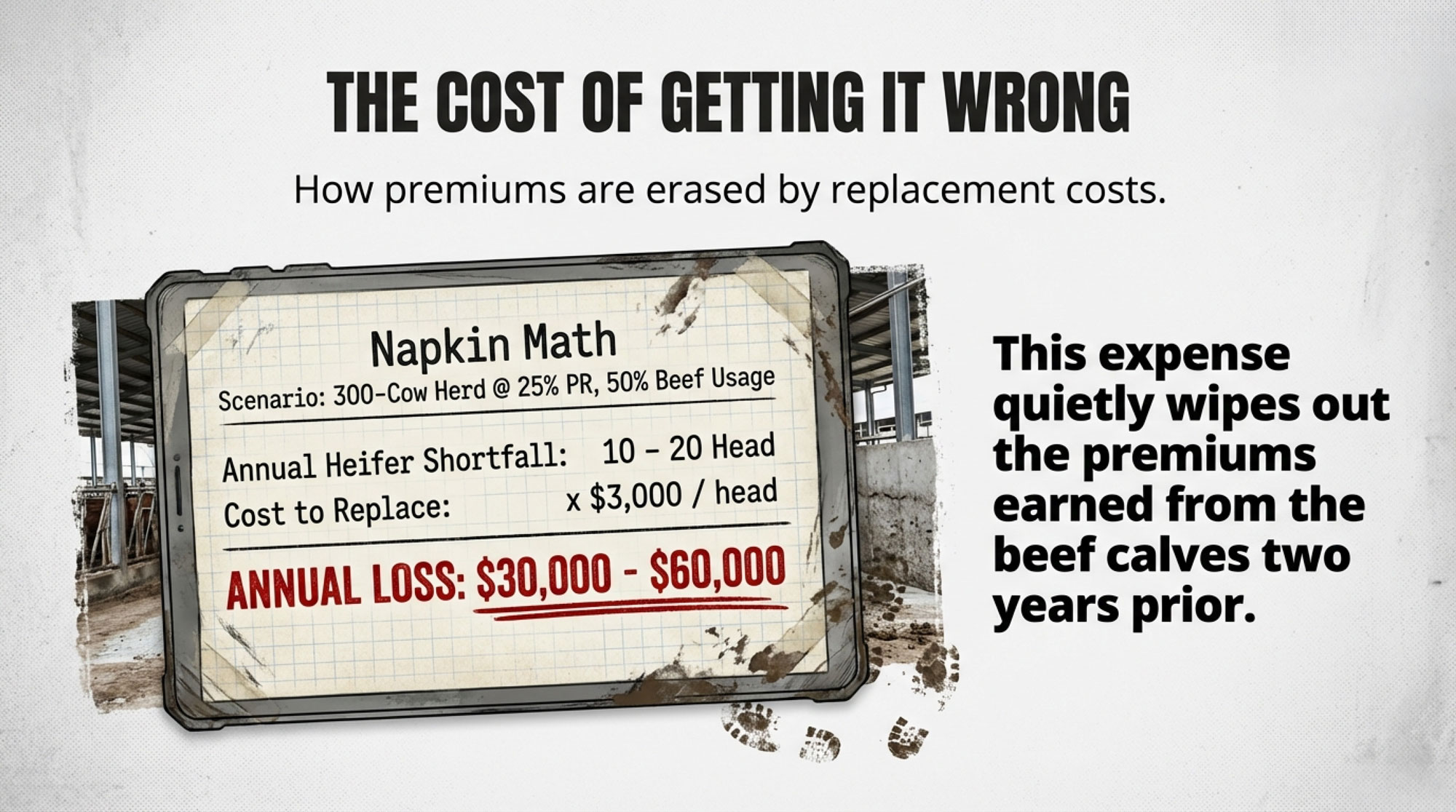

To make this more concrete, let’s run a quick example.

Say you run a 300‑cow herd with a 32 percent annual cull rate. That means you need about 96 replacement heifers freshening each year just to hold steady.

At 25 percent 21‑day PR, using a mix of dairy and sexed semen, you might reasonably expect to produce enough heifers to replace those 96 cows and keep a small buffer, as long as calf and heifer losses are modest. If 30 percent of your breedings are to beef semen, you’ll likely still be self‑replacing.

But if you push beef to 50 percent of services at that same 25 percent PR, simple spreadsheet math often shows a shortfall—maybe 10–20 heifers per year—that you’ll need to cover with purchases. At US$3,000 per head, that’s US$30,000–60,000 a year in heifer purchases that quietly offset a lot of those earlier calf cheques.

Now imagine that same herd at 30 percent 21‑day PR. With stronger repro and the same cull rate, the modeling and real‑world experience suggest you can often support 40–50 percent of matings to beef and still have enough heifers coming, especially if you’re steering sexed semen toward your best genetics and managing heifer losses tightly. That’s where beef‑on‑dairy becomes a sustainable part of the business rather than a short‑term cash grab.

For Canadian quota herds, where expansion room is limited, and every cow slot carries its own capital cost, this math gets even tighter. You can’t just “buy more quota” to cover a heifer shortfall the way a U.S. herd might buy more cows. Getting the beef‑on‑dairy balance wrong means either paying top dollar for scarce heifers or watching your production rights sit underutilized while you wait for replacements to catch up.

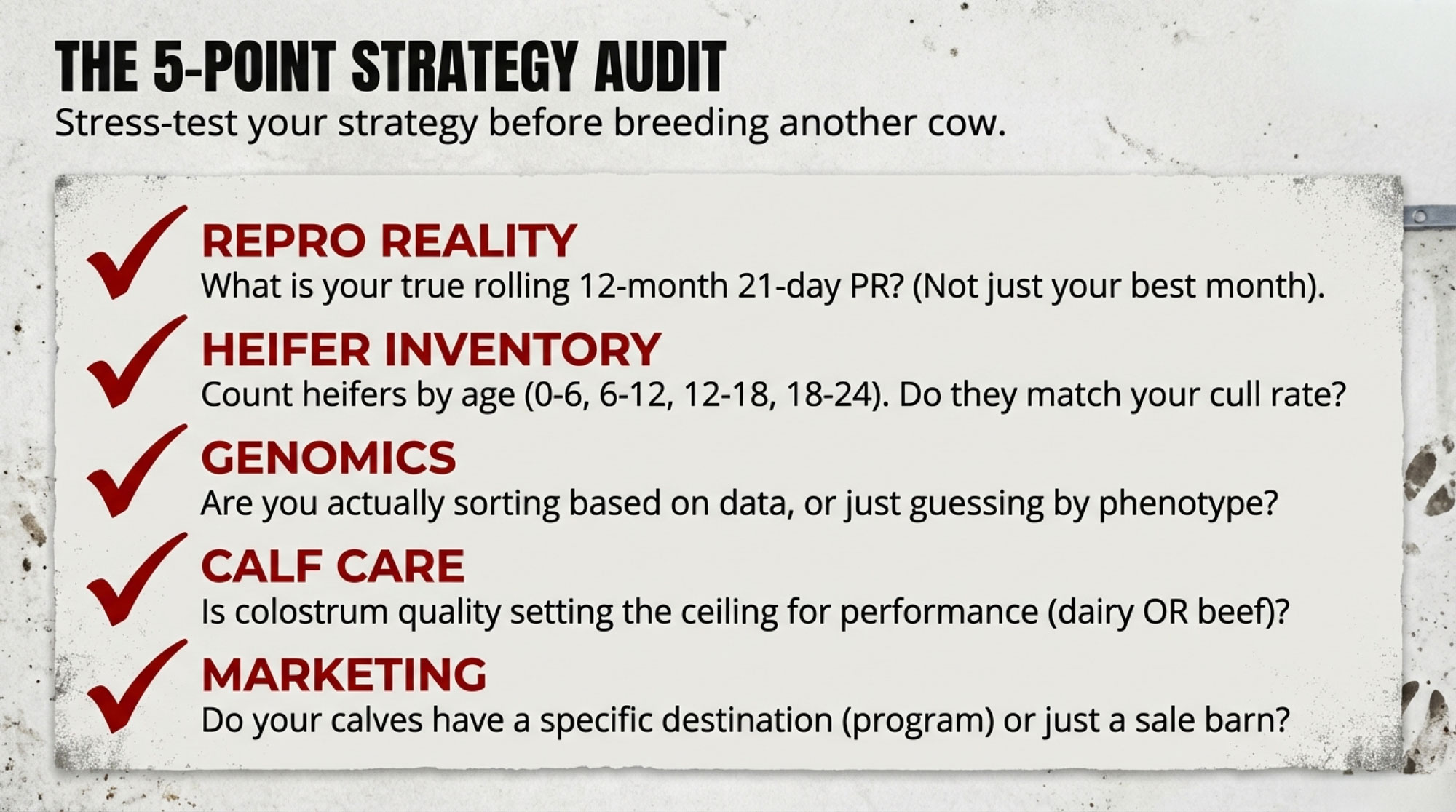

A Simple “Over‑Coffee” Framework to Check Your Own Program

When this topic comes up at winter meetings or around kitchen tables, we often end up sketching the same handful of questions on a napkin. Here’s a simple framework you can walk through with your own team.

| Metric | Scenario A: Disciplined (30% Beef) | Scenario B: Aggressive (50% Beef) | Year-Over-Year Impact |

| Herd Size | 300 cows | 300 cows | — |

| 21-Day PR | 25% | 25% | — |

| Annual Culls (32% rate) | 96 cows | 96 cows | — |

| Heifers Needed (replacement buffer) | 96–100 | 96–100 | — |

| Beef Semen % | 30% | 50% | — |

| Female Calves Born (annual) | ~1,200 | ~1,200 | — |

| Expected Dairy Heifer Calves | ~588 | ~588 | — |

| Heifers Raised to 24m | ~540 (with 8% loss) | ~540 (with 8% loss) | — |

| Heifers Freshening Annually | ~102 | ~96 | Shortage: 6 heifers |

| Cumulative 2-Year Shortage | 0 (self-replacing) | 16–20 heifers | — |

| Replacement Heifer Cost (2026–2027) | $0 (self-replacing) | $48,000–60,000 (at $3,000/head) | +$50,000/2 years |

| Avg. Annual Beef Calf Premium (2023–24) | $180/calf × 360 calves = $64,800 | $220/calf × 600 calves = $132,000 | +$67,200 gross |

| Premium Over 2 Years (2024–2025) | $129,600 | $264,000 | +$134,400 |

| Less: Heifer Purchase Bill (2026–2027) | $0 | –$54,000 | –$54,000 |

| Less: Heifer Management Opportunity Cost | ~$12,000 | ~$18,000 | –$6,000 |

| Net Advantage After 3-Year Cycle | $129,600 cumulative | $186,400 cumulative | +$56,800 |

| BUT: Scenario B at Risk If PR Drops or Culls Rise | Stable | Deficit grows fast | Vulnerable |

1. Where’s your reproduction really at?

Start here, every time:

- What’s your true rolling 12‑month 21‑day pregnancy rate—not just your best month last summer?

- Are transition‑period problems like metritis, ketosis, and displaced abomasum dragging that number down more than semen choice is?

- When did you last review voluntary waiting period, heat detection (visual plus activity systems), and AI timing with your vet or repro consultant?

Land‑grant extension programs from places like the University of Wisconsin, Penn State, and Cornell keep showing that investments in cow comfort, fresh cow management, and heat detection often deliver some of the strongest returns in dairy herds. Without that foundation, changing semen color won’t fix the underlying issue.

2. Do you truly know your heifer pipeline?

What farmers are finding is that a simple age‑structured heifer count is one of the most eye‑opening tools you can use:

- How many heifers do you have today in each age band: 0–6, 6–12, 12–18, 18–24 months?

- If you project those forward and apply your typical cull rate and target herd size, will you have enough first‑lactation cows to hold or grow your herd in 2027 and 2028?

- If you assume you won’t buy heifers, what does your herd size look like three years out?

CoBank did this math on the national herd and came up with that projected 800,000‑head shortfall. Doing it on your own numbers will tell you very quickly whether your current beef‑on‑dairy level makes sense—or whether it’s quietly eating tomorrow’s replacements.

3. Is genomics actually changing your decisions?

Genomics is only worth paying for if it changes what you do:

- Are genomic results directly influencing which animals get sexed semen, which get beef, and which aren’t raised?

- Are there heifers that look “good” to the eye but that the genomic numbers clearly put at the bottom of the list, that you’re still raising?

CDCB, USDA‑ARS, and university researchers have shown that many herds raise more heifers than they truly need, and often not the right ones, when decisions are based only on pedigree and appearance. Using genomics to sort those heifers can free up dollars and space to focus on the replacements that will actually drive your herd forward.

4. How strong is your calf and transition program?

We can talk about semen and proofs all day, but colostrum and fresh cow management still set the ceiling:

- Are you routinely checking colostrum quality with a Brix refractometer and ensuring the right volume is delivered to calves within the recommended timeframe?

- Do your calf facilities provide the drainage, bedding, and ventilation that your vet and extension resources recommend, even when it’s cold, wet, or windy?

- On the cow side, are your close‑up and fresh pens hitting targets for stocking density, bunk space, and stall design, or do those pens get crowded when you’re short on beds?

Research summarized in the Journal of Dairy Science and in calf‑raising guides from Penn State and UC Davis shows that calves with strong colostrum and early‑life care have lower morbidity, better growth, and better performance later in life—whether they end up as dairy cows or dairy‑beef cattle.

5. Where do your beef‑on‑dairy calves actually go?

Finally, follow the calf beyond your driveway:

- Are you selling into a structured dairy‑beef program or to a regular buyer who lays out expectations and occasionally shares feedback on performance?

- Or are most of your calves going through local sale barns as anonymous black calves with little information attached?

AABP’s dairy‑beef work and reports from feedlots in Kansas, Nebraska, and Texas suggest that as beef‑on‑dairy numbers grow, feedlots and packers are increasingly willing to pay premiums for calves with known backgrounds—from herds they trust—and are more cautious on price with unknown cattle. It’s worth noting that those premiums depend on meeting specific contract specs that can change quickly, so there’s some marketing risk to manage along with the opportunity.

If your only metric for beef‑on‑dairy success is this month’s calf cheque, you’re missing half the story.

Where This All Seems to Be Heading

When you stack up the NAAB semen trends, USDA herd numbers, CoBank’s heifer modeling, the beef‑on‑dairy research, and what vets and consultants are seeing across barns, a few patterns start to show through the noise.

In larger freestall and dry lot herds in the Upper Midwest, West, and Southwest, beef‑on‑dairy is quickly becoming part of the core business model. These herds are tying beef‑on‑dairy into their genetic strategy, fresh cow management, heifer planning, and marketing. They’re monitoring butterfat performance and components for the milk cheque, and calf contracts and feedlot relationships on the beef side.

In mid‑sized herds across the Northeast, Great Lakes, and Ontario, there’s a lot of recalibrating going on. Many of these farms enjoyed the bump from beef‑on‑dairy calf prices in 2022–2023, but they’re now staring at tighter heifer numbers and higher replacement costs. They’re asking tougher questions about how far to push beef semen, where to invest next—reproduction, genomics, heifer housing, or structured calf marketing—and how to balance short‑term cash flow with long‑term herd stability.

In smaller tie‑stall and grazing systems—from Vermont to Quebec to the Prairies—beef‑on‑dairy is often being used more selectively: beef semen on clearly lower‑merit cows, while day‑to‑day focus stays on forage quality, butterfat performance, cow longevity, and labor efficiency. Some of these farms are teaming up with a few trusted calf buyers or dairy‑beef programs so they can capture better value for calves without taking on all the logistics themselves.

The Wageningen University Animals paper and other sector‑level analyses in Europe and New Zealand point the same direction as what we’re seeing here: beef‑on‑dairy can be a powerful tool to improve profitability and resource use when it’s built on strong reproduction, sexed semen, and careful replacement planning, but it can create pressure on replacements and welfare if it’s used mainly as a way to ride high calf prices for a season or two.

The Bottom Line

What I’ve noticed, walking freestalls in Wisconsin, parlors in New York, dry lots in the High Plains, and tie‑stalls in Ontario, is that beef‑on‑dairy doesn’t really change what it takes to run a strong dairy. It just makes the strengths—and the cracks—a lot more visible.

Strong reproduction and fresh cow management buy you the freedom to use beef semen without starving your heifer pipeline. Genomics and thoughtful sire selection help you decide which animals should build your next generation of cows and which should produce high‑value beef calves. Good colostrum and calf care protect the value built into every pregnancy. And clear relationships with buyers and feedlots help turn those calves from “generic black crosses” into predictable, valued cattle in somebody’s beef chain.

So maybe the most useful question to bring back to your own kitchen table is this:

Are we using beef‑on‑dairy in a way that builds on the real strengths of our herd—reproduction, genetics, fresh cow and calf management, marketing—or are we leaning a bit too hard on strong calf prices to cover for things we already know we should fix?

If the honest answer is “a bit of both,” that’s actually a good place to start. It means you’ve already identified where your next management dollar is most likely to pay you back—in heifers you don’t have to buy, in calves that earn a premium instead of a discount, and in a herd that’s ready for whatever milk and beef markets throw at it between now and that 2027 wave of new processing capacity.

| Diagnostic Criteria | ✅ Sustainable Beef-on-Dairy | 🔴 Scheduled Crisis (Hidden Bill Coming) |

| 21-Day PR | 25–30%+ (rolling 12-month average) | <20% or volatile 15–22% |

| Reliable base for 30–45% beef semen | Inadequate base; even 40% beef starves replacements | |

| Heifer Pipeline Visibility | Age-structured count (0–6m, 6–12m, 12–18m, 18–24m); modeled forward vs. cull rate | No systematic count; heifer pens “look OK” but no forward projection |

| Know if self-replacing through 2027–2028 | Blind to shortage until it hits; then scrambling to buy | |

| Genomic Decision-Making | Genotyping 90%+ of heifer calves; genomic ranking directly drives sexed vs. beef semen assignment; culling non-merit animals early | Minimal genotyping; sexed semen and beef assigned by “gut feel” or herd appearance; raising marginal heifers anyway |

| Raising the RIGHT heifers | Raising MORE heifers, not necessarily better ones | |

| Calf & Transition Program | Colostrum quality checked with Brix; consistent volumes/timing; calf facility meets vet/extension standards (drainage, bedding, ventilation) | Basic colostrum; calf housing crowded or inconsistent; transition pens cramped when volume spikes |

| Strong colostrum sets all calves (dairy or beef) up for performance | Weak colostrum and housing drag down heifer health/growth | |

| Beef Calf Marketing | Documented program: sire ID, dam info, colostrum, vaccination, weaning protocols; partner with known feedlot/dairy-beef program; receive performance/carcass feedback | Anonymous sale barn sales; minimal traceability; generic “black calf” pricing; no feedback loop |

| Earn $280–400/head premium over commodity; build brand | Leave $3,000–4,000 per truckload on the table; buyers discount unknown cattle | |

| Overall Herd Status | Multi-year plan in place; beef-on-dairy as one tool, not the solution | Riding high calf prices now; financing 2027 heifer crisis later |

| Action This Week | Fine-tune; confirm heifer counts; adjust sexed % if needed | STOP; audit repro; model heifer shortage; plan heifer purchasing or pivot beef % down |

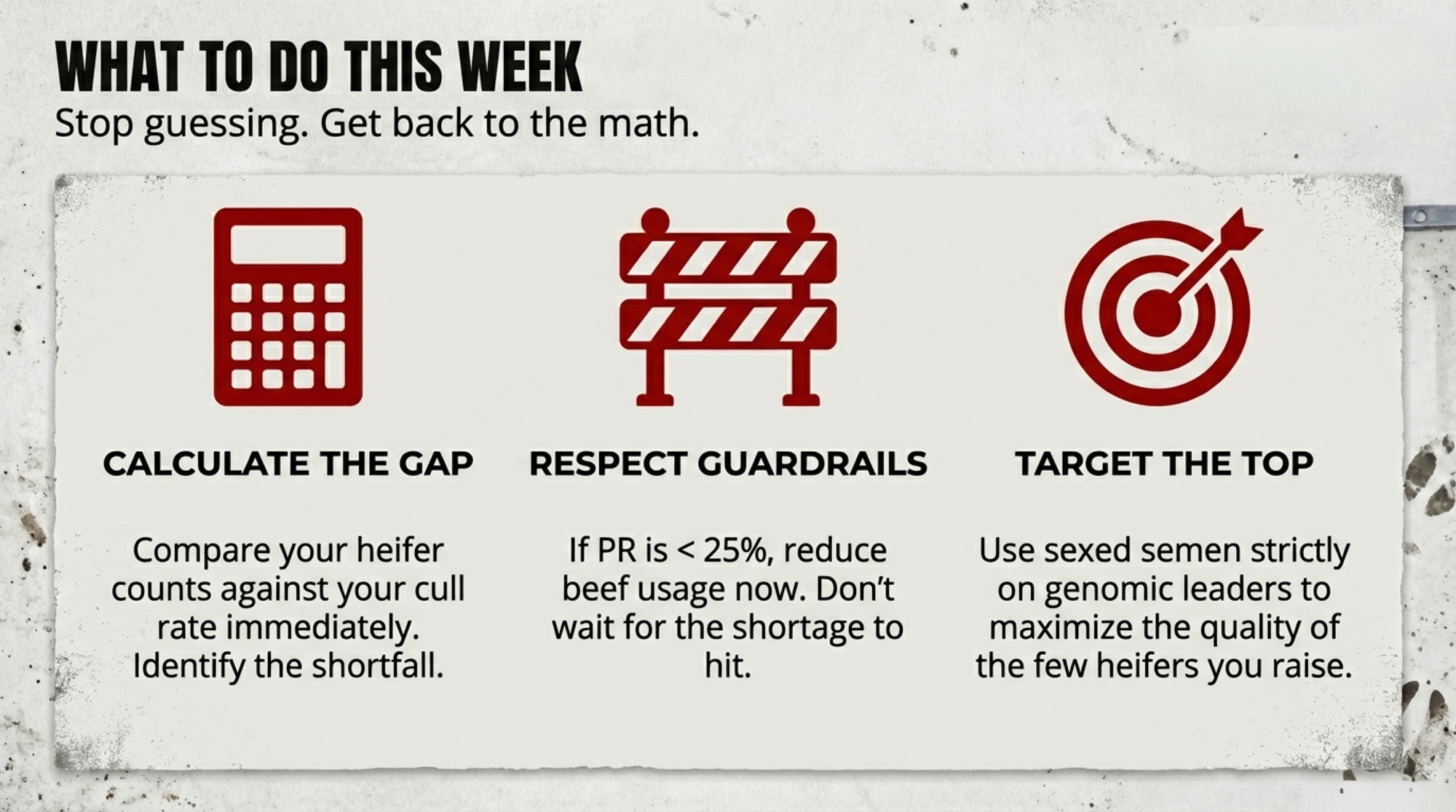

This week, before you get too far into spring breeding decisions:

- Check your 12‑month 21‑day PR.

- Lay out your heifers by age band and run them against your cull rate.

- Decide which cows truly deserve sexed semen—and which calves truly deserve a beef premium.

That’s the math that will tell you whether beef‑on‑dairy is working for your herd, or whether you’re quietly writing yourself a very expensive heifer cheque for 2027.

KEY TAKEAWAYS

- The beef-on-dairy math has flipped. 7.9 million beef straws went into U.S. dairy herds in 2024, but USDA counts just 3.914 million replacement heifers—the lowest since 1978—and CoBank projects another 800,000-head shrink before inventories recover near 2027.

- Reproduction is the gatekeeper, not semen color. Herds under 20% 21-day PR breeding heavily to beef aren’t cashing in—they’re scheduling a heifer shortage. Above 30% PR, many herds can safely run 40–50% beef and stay self-replacing.

- The hidden bill adds up fast. A 300-cow herd at 25% PR pushing 50% beef could come up 10–20 heifers short annually. At US$3,000+ each, that’s US$30,000–60,000 per year quietly erasing those 2023 calf premiums.

- Program calves earn premiums; anonymous calves get discounted. Feedlots and packers increasingly separate documented dairy-beef calves from generic “black calves” on price—and that gap is widening.

- Your move this week: Check your 12-month 21-day PR, map heifers by age against your cull rate, and decide which cows truly deserve sexed semen. That math tells you whether beef-on-dairy is building your herd—or billing it.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – Stop the guesswork and find your profit tier. This guide breaks down the specific reproductive “guard rails” that separate top-tier earners from those losing ground, providing a Monday-morning blueprint for maximizing monthly revenue.

- 438,000 Missing Heifers. $4,100 Price Tags. Beef-on-Dairy’s Reckoning Has Arrived. – Position your dairy for a structural reset. This analysis exposes the 2026-2027 heifer inventory gap, arming you with the market intelligence to navigate $4,100 price tags and secure elusive processor partnerships before the window closes.

- The Next Frontier: What’s Really Coming for Dairy Cattle Breeding (2025-2030) – Unlock the next decade of genetic advantage. This feature reveals how breakthroughs in casein selection and AI-driven health markers can generate an extra $5,000 per cow, transforming your breeding program into a high-value protein factory.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.