USDA forecasts rising milk production and changing export patterns through 2026. What’s driving the $21.60 milk price, and why might it drop? Find out now.

EXECUTIVE SUMMARY: The latest USDA Supply and Demand report signals significant shifts ahead for dairy markets, with expanding U.S. milk production expected to continue through 2026 despite slightly lower projected prices. While strong export demand is currently offsetting supply growth and supporting a $21.60/cwt all-milk price for 2025, farmers should prepare for potential challenges as fat-basis exports decline and imports rise in 2026, pushing prices down to $21.15/cwt. The double impact of growing dairy herds and increasing per-cow productivity creates a compounding effect on total milk supply that will fundamentally shape market conditions over the next two years, requiring strategic planning and robust risk management from producers looking to maintain profitability.

KEY TAKEAWAYS

Window of opportunity: Strong prices projected for 2025 ($21.60/cwt) provide a chance to strengthen financial position before potentially softer markets arrive in 2026 ($21.15/cwt)

Export dependency increasing: Current price strength is heavily supported by international demand for butter, cheese, and whey products, making your operation more vulnerable to global market shifts

Domestic consumption growth: Increasing U.S. consumption for both fat and skim-solids components provide a stable foundation even as international markets fluctuate

Component value divergence: Different export patterns for fat versus protein products mean optimizing your herd for higher components could provide advantages as markets evolve

Risk management critical: With expanding U.S. production meeting evolving international markets, implementing forward contracts and other protection strategies now could safeguard your operation from the volatility ahead

According to the USDA’s latest Supply and Demand report released yesterday, U.S. dairy farmers can expect expanding milk production, export growth, and moderate price declines by 2026. The May 12th update confirms the trend of growing dairy herds and increasing per-cow productivity, setting the stage for significant market developments over the next two years.

The USDA projects the all-milk price for 2025 at $21.60 per hundredweight (cwt), with a slight dip to $21.15 per cwt in 2026 as increased supply weighs on markets despite growing domestic and export demand.

Production Expansion Continues

U.S. dairy herds are growing, and that’s not slowing down anytime soon. The May report confirms what many producers have observed firsthand – more cows are entering production, and each cow is giving more milk.

This double-whammy of larger herds and better productivity creates a compounding effect on total milk supply, shaping market dynamics through 2026.

For producers making expansion decisions, this trend signals the need for caution. While prices remain relatively strong in the near term, the growing national herd suggests increased competition is coming.

Export Markets Providing Short-Term Support

International demand is currently the dairy industry’s best friend. The USDA has raised its forecast for exports fatally, pointing specifically to “competitively priced butter and cheese” driving international sales.

Exports of whey products, lactose, and cheese are all projected to increase, providing crucial market support that’s helping offset the production increases.

This export strength explains why the USDA raised its price forecasts for butter, cheese, nonfat dry milk (NDM), and whey from last month’s projections – international buyers are absorbing much of the additional production.

Long-Term Price Pressures Building

Looking ahead to 2026, the picture becomes more complex. Fat-basis exports are expected to decline compared to 2025, potentially adding pressure to butter and cheese markets.

Meanwhile, imports are projected to rise, with more butter and skim solids entering the U.S. market. Reduced exports and increased imports could create more challenging market conditions.

The forecasted milk price drop from $21.60 to $21.15 per cwt between 2025 and 2026 reflects this building pressure, though strong domestic consumption should prevent more dramatic declines.

Domestic Consumption Provides Foundation

A key bright spot in the report is the projection for domestic dairy consumption, which is expected to increase for both fat and skim-solids in 2026.

This growth in home market demand creates a more stable foundation for the industry even as international markets fluctuate. American consumers continue embracing dairy products across multiple categories, providing a reliable customer base.

For farmers concerned about market volatility, this domestic growth represents perhaps the most sustainable pillar of long-term demand.

What This Means for Your Operation

If you’re making plans for your dairy operation, the USDA report suggests a window of opportunity now, with potential challenges ahead.

The current price strength for 2025 offers a chance to strengthen your financial position before the projected softer markets 2026 arrive. Smart producers will use this period to reduce debt, invest in efficiency improvements, or build cash reserves.

Component values will likely increase divergence as different export markets favor fat versus protein products. Farms that optimize production for higher components may find advantages in this environment.

Risk Management Becomes Critical

Price volatility is almost guaranteed with expanding U.S. production, growing but uneven export markets, and changing import patterns. Now is the time to evaluate your risk management strategy.

Forward contracting, futures markets, and government programs should all be on the table as you plan for the next 24 months. The relatively strong prices projected for 2025 provide an opportunity to lock in margins while they’re available.

Remember that the entire industry sees these same projections, which means many producers may be expanding simultaneously, accelerating the supply growth beyond the forecast.

The Bottom Line

The dairy landscape is shifting beneath our feet. Growing U.S. production will meet evolving international markets and steady domestic consumption, creating opportunities and challenges.

Near-term price strength masks the pressure of expanding supply, giving smart producers a window to prepare. Those who understand these market dynamics and position their operations accordingly will navigate the coming changes most successfully.

What’s your plan for capitalizing on stronger 2025 prices while preparing for potential softening in 2026? Share your thoughts in the comments or contact our market analysts for personalized guidance.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Cheese prices crash 6¢ on surplus milk, butter dips as NDM defies trend with export-driven gains in mixed dairy markets.

EXECUTIVE SUMMARY: The CME dairy markets saw sharp divergences on April 21, with cheddar blocks plummeting 6¢ to $1.7750/lb amid abundant Midwest milk supplies and sluggish post-Easter demand, while barrels fell 3.25¢ despite higher trading activity. Butter slipped 2.25¢ on thin trading, reflecting ample inventories, but Nonfat Dry Milk (NDM) gained 1¢ due to strong export orders from Southeast Asia and Mexico. Global dynamics intensified the split: EU and New Zealand production pressured cheese/butter prices, while NDM capitalized on tight international powder markets. Trading volumes remained low in cheese blocks and butter, raising volatility concerns, as producers were urged to hedge against milk price swings and monitor feed costs. Market sentiment leaned bearish for cheese but cautiously optimistic for NDM’s export potential.

KEY TAKEAWAYS:

Cheese Collapse: Blocks hit $1.7750/lb (-6¢) on surplus milk and weak demand, with barrels inverting to trade higher at $1.8075/lb despite a 3.25¢ drop.

Butter Stability Test: Prices eased to $2.3200/lb (-2.25¢) amid light trading, signaling buyer patience despite historically high levels.

NDM Resilience: Rose 1¢ to $1.1825/lb on robust global demand, contrasting with milkfat weakness.

Global Split: EU/NZ milk output pressures cheese/butter, while U.S. NDM gains export traction.

Risk Alert: Producers advised to hedge amid volatile Class III prices and rising soybean meal costs.

Cheese prices plunged on the CME cash market today amid signs of ample supply and hesitant demand, with blocks dropping 6 cents and barrels falling 3.25 cents. Butter also weakened as limited trading activity suggested comfortable inventory levels, while Nonfat Dry Milk bucked the trend with modest gains, supported by solid export demand. This divergence highlights the current split market conditions, with protein components showing strength against weakness in the milkfat complex.

Cheese: Cheddar cheese prices dropped substantially today, with blocks leading the decline. The 6-cent plunge in blocks to $1.7750 per pound coincided with reports of readily available milk supplies in key Midwestern production regions directed to cheese vats, potentially boosting near-term supply. Post-Easter retail restocking appears less robust than anticipated, while food service demand remains tentative despite higher trading activity in barrels. The unusual price inversion, with barrels ($1.8075) trading above blocks ($1.7750), likely reflects the thin block trading rather than a fundamental shift in market dynamics.

Butter: Prices eased by 2.25 cents to $2.3200 per pound on minimal trading. This movement suggests the market balances comfortable inventory levels against steady but not aggressive demand. Recent USDA Cold Storage data may indicate sufficient butter stocks nationally, reducing buyer urgency in the spot market. While prices remain historically elevated, today’s lack of buying interest points to a potential near-term ceiling.

Nonfat Dry Milk: Unlike other commodities, NDM gained 1 cent to settle at $1.1825 per pound. This strength likely stems from firm international skim milk powder prices and continued solid export demand, particularly from Mexico and Southeast Asian markets. Domestic demand for high-protein ingredients also remains supportive.

Dry Whey: Prices dipped slightly by 0.50 cents to $0.4775 per pound, suggesting a relatively balanced market. Whey supplies remain generally available, given robust cheese production rates. At the same time, demand from both domestic food processing and animal feed sectors appears stable but not strong enough to drive significant price increases.

Volume and Trading Activity

Trading activity varied significantly across dairy products today, with overall volume relatively light, particularly in butter and block cheese markets.

Butter: Activity was minimal, with only one load trading hands. Two bids and one offer were on the board at the close, indicating minimal market depth and participation. This thin trading environment makes the price discovery process less reliable and potentially more volatile.

Cheddar Blocks: Only one load traded today. Notably, no bids were registered at the close, while two offers remained unfilled, clearly signaling the selling pressure that drove prices sharply lower. This imbalance reflects significant buyer hesitancy at current price levels.

Cheddar Barrels: This market saw the most activity among dairy products, with five loads trading. However, unlike blocks, no bids were present at the close against two unfilled offers, reinforcing the overall weak tone in the cheese complex despite the higher volume.

NDM Grade A: Moderate activity was observed with four loads trading. The market appeared more balanced, with four bids and three offers posted at the close, suggesting more two-sided interest than the cheese markets. This balanced bid/ask picture lends credibility to today’s price increase.

Dry Whey: Activity was moderate, with three loads trading. At the close, one bid remained on the board, with no offers present, indicating some underlying support but a lack of aggressive selling interest at current levels.

The low volume in butter and blocks suggests today’s price discovery was based on limited participation, potentially making these price points less representative of broader market sentiment and subject to revision with increased activity in coming sessions.

Global Context

International dairy market dynamics are exerting mixed influences on U.S. prices. Production trends in major exporting regions like the European Union and New Zealand appear stable, slightly increasing as they progress through their respective seasonal cycles. This increased global milk supply, particularly if channeled into butter and cheese production in the EU, could contribute to a more competitive international market for these products, potentially capping U.S. export opportunities and adding downward pressure to domestic prices.

Conversely, the global market for milk powders, particularly skim milk powder (SMP, the international equivalent of NDM), seems to be on firmer footing. Steady import demand from key regions like Southeast Asia and the Middle East/North Africa (MENA), potentially coupled with less aggressive European export positioning, appears to support global powder prices. Today’s rise in CME NDM prices, despite domestic cheese/butter weakness, suggests that U.S. NDM remains competitive globally and is benefiting from this international demand-pull.

At current price levels, U.S. butter ($2.3200/lb) and cheese ($1.7750-$1.8075/lb) may face stiffer competition on the world market if international prices are softer. Market participants should continue monitoring exchange rates and competitor pricing to assess U.S. export competitiveness across the dairy complex.

Forecasts and Analysis

Today’s CME Class III futures settlement for May was $18.08/cwt, while the May Class IV settlement was $18.37/cwt. The significant weakness in today’s cash cheese market puts immediate downward pressure on the Class III complex, potentially challenging the $18.08 futures level if this cash weakness persists. Conversely, the strength of NDM supports the Class IV price.

Feed costs remain a critical variable for producer profitability. Today’s CME futures settlements show May Corn at $4.82/bushel and December Corn at $4.64/bushel. May Soybean Meal settled at $292.90/ton, with December Meal at $306.40/ton. While near-term corn prices are relatively stable, deferred soybean meal prices show an increase, suggesting potentially rising protein feed costs later in the year. This outlook, combined with potentially volatile milk prices indicated by today’s spot market action, underscores the importance of risk management for dairy producers.

Calculating the milk-feed price ratio based on current futures would provide essential insights into anticipated margin pressure or relief. Producers should closely monitor cheese market developments due to their significant impact on Class III prices and evaluate hedging strategies for milk output and feed inputs. Traders might anticipate continued volatility, particularly in the cheese complex, and watch for confirmation of trends in upcoming sessions and key data releases like Cold Storage and Milk Production reports.

Market Sentiment

Today’s prevailing sentiment in dairy markets appears decidedly mixed, reflecting the divergent price action across commodities. The sharp sell-off in cheese has generated a cautious, if not outright bearish, tone in that segment. The market commentary reflects growing unease about the balance between robust cheese production and potentially softening demand. One analyst might note, “Buyers seem hesitant to build inventory at current cheese prices, waiting for clearer demand signals or further price concessions.” The lack of bids on the CME board lends credence to this view.

Sentiment surrounding butter also appears cautious, influenced by ample inventories capping upside potential, though the historically high price level prevents deep bearishness. A broker might observe that the “butter market feels well-supplied; buyers are patient.”

In stark contrast, sentiment regarding NDM is more optimistic. Positive export expectations likely fuel the price strength. A trader might comment: “We continue to see consistent inquiries for NDM from Southeast Asian buyers, keeping the export pipeline active and supporting domestic prices.”

Overall, the market mood is fragmented. While concerns about milkfat and cheese values dominate discussions following today’s session, the underlying support for milk powders provides a counterpoint. Uncertainty regarding the strength of domestic demand heading into late spring and summer, coupled with evolving global market conditions, contributes to a cautious outlook despite pockets of optimism in the powder complex.

Closing Summary & Recommendations

In summary, today’s CME dairy markets were characterized by significant weakness in cheese and butter prices, driven by ample domestic supplies and cautious buyer sentiment. Nonfat Dry Milk provided a notable exception, strengthening on the back of positive export expectations and firmer global powder markets. Trading volume was light in butter and blocks, adding uncertainty to those price declines, while NDM saw more active, two-sided trade.

Based on today’s activity and broader market context, stakeholders should consider the following:

For Producers:

Closely monitor the trajectory of cash cheese prices, as continued weakness could pressure Class III milk prices further

Evaluate risk management strategies, paying attention to both milk price volatility and feed cost trends indicated by corn and soybean meal futures

Consider that the relative strength in NDM offers some support to Class IV values, which may provide a more stable pricing option in the near term

For Traders:

Recognize the current divergence between cheese/butter and NDM markets

Look for confirmation of trends in subsequent trading sessions and upcoming fundamental reports (e.g., USDA Cold Storage, Milk Production)

Be mindful of the low liquidity observed in butter and blocks, which could lead to heightened volatility

Continue monitoring global market developments and export demand as key factors influencing price direction

The outlook suggests a market grappling with potentially heavy cheese and butter supplies against stronger fundamentals for milk powders, driven largely by export dynamics. Near-term price direction will likely hinge on evolving domestic demand, U.S. export competitiveness, and global milk production trends.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Tariffs are reshaping dairy demand—discover which products thrive or die in the trade war crossfire.

EXECUTIVE SUMMARY:

Tariffs are fracturing global dairy markets, with butterfat exports surging due to global shortages while whey and lactose face collapse from Chinese retaliation. The U.S.-China trade war triggered a $6B profit loss for dairy farmers, exposing vulnerabilities in export-dependent sectors. Price elasticity dictates outcomes: butter’s global price gap buffers tariffs, but high-elasticity products like cheese face demand destruction. Retaliatory measures and TRQ administration amplify risks, forcing farmers to diversify markets, differentiate products, or risk consolidation. Adaptation isn’t optional—it’s survival.

KEY TAKEAWAYS:

Whey/lactose demand has cratered (23% prices) due to China’s 125% tariffs, with no quick fixes for glutted markets.

Butter exports defy tariffs, up 224% YoY, fueled by a $1.10/lb global price gap—proof fundamentals trump politics.

Retaliation risks outweigh protection: Losing China’s market took years; regaining it may be impossible amid shifting global supply chains.

Diversify or die: Farms reliant on single products/markets face extinction; value-added dairy and Southeast Asia exports offer lifelines.

TRQ loopholes matter: Canada’s “processor-only” quotas show nominal trade access ≠ to real market share—read the fine print.

The global dairy market is facing unprecedented disruption as tariff battles escalate. While politicians claim to protect domestic industries, the reality for dairy farmers is far more complex – and potentially devastating. This analysis cuts through the political BS to reveal how tariffs are reshaping dairy demand patterns, creating unexpected winners and losers, and why your operation needs to prepare now for the ripple effects that could make or break your future.

Let’s be brutally honest about where we stand: The escalation has been breathtaking in speed and scope. On February 4, the US reinstated a 10% tariff on Chinese imports. By March 4, this jumped to 20%. China wasted no time responding, slapping 10% retaliatory tariffs on US dairy products by March 10. Then came the hammer blow – on April 3, the US imposed an additional 34% tariff on Chinese imports, prompting China to retaliate with an 84% tariff on US goods, later increasing to a staggering 125%.

And this isn’t just a US-China problem. The US has simultaneously imposed 25% tariffs on imports from Mexico and Canada – two of our most critical dairy trading partners. Despite a 90-day pause on some global tariffs, the restrictions affecting America’s three largest dairy export markets remain firmly in place.

Are you paying attention yet? This trade war is about to hit your milk check-in ways.

Why Tariffs Hit Dairy Differently: The Economics You Need to Understand

To protect your operation, understand how tariffs fundamentally reshape dairy economics. Tariffs aren’t just political tools – they’re taxes on imported products that increase their effective price to importers and consumers.

The Price Elasticity Factor

The demand response to tariff-induced price increases varies dramatically across dairy products due to differences in price elasticity. This isn’t theoretical – it directly impacts which products face demand collapse and which might weather the storm:

Fluid Milk: Often shows inelastic demand, particularly for conventional milk – much like how your high-producing Holsteins keep pumping regardless of minor management changes

Specialty Cheeses: Demonstrate significantly higher price elasticity (around -1.73 for natural cheese) – think of how quickly your heifers respond to even small changes in their ration

Butter: Research shows mixed elasticity, with some studies finding highly elastic demand (-1.87) – like how butterfat responds dramatically to even minor feed adjustments

Yogurt: Generally elastic demand across product types – comparable to how quickly somatic cell counts can spike with even minor lapses in milking hygiene

Dairy Ingredients: Whey and lactose show highly elastic derived demand from food manufacturers – like how quickly your milk truck will pass by if you miss quality parameters by even a small margin

This elasticity differential explains why certain products experience more dramatic demand destruction when hit with tariffs. The proliferation of plant-based alternatives has further increased the elasticity of traditional dairy products, making them more vulnerable to tariff impacts than in previous decades.

The Substitution Myth

Politicians love to claim tariffs will simply shift demand to domestic producers. The reality? That’s complete bullshit. This substitution is neither automatic nor complete:

Effectiveness depends on whether domestic products match the quality and characteristics of imports – just like how you can’t simply swap a high-genetic-merit Holstein for a commercial Jersey and expect the same components

If imported products possess unique attributes not easily replicated domestically, substitution may be limited – like how no amount of TMR adjustments can make up for poor-quality forage

The domestic industry must have sufficient capacity and competitive cost structures to capitalize on the opportunity – just as your parlor throughput can’t suddenly double without significant infrastructure investment

When was the last time you saw politicians understand how dairy markets work? These are the same people who can’t tell the difference between a Holstein and an Angus.

The Product Battlefield: Winners and Losers in the Tariff War

The dairy portfolio is experiencing wildly divergent tariff impacts, with some products flourishing despite trade barriers while others face devastating demand destruction.

Whey and Lactose: The Casualties

The impact on whey and lactose markets has been particularly severe:

US exports of these products to China have plummeted as tariffs escalated

Dry whey prices crashed 23% between February and April 2025

Lactose prices fell 21% during the same period

China represents 42% of US whey exports and 43% of US lactose exports

Inventories of these products have ballooned by 57% as export channels close

The magnitude of this demand destruction stems from China’s dominant position in these markets and the products’ high price elasticity. The outlook for producers heavily invested in these products is grim unless alternative markets can be developed rapidly.

Butter: The Surprising Survivor

In stark contrast to whey markets, butter demand shows remarkable resilience despite the tariff environment:

Global butter supply shortages have driven up international prices substantially

European Union butter prices have surged 47% compared to 2023

The average Global Dairy Trade auction price for butter reached $3.45 per pound in recent trading

US butter prices ($2.3475/lb as of April 11) sit well below international levels

This price gap provides a substantial buffer against tariff impacts

US butterfat exports increased dramatically by 224.5% in February 2025 compared to the previous year, totaling 8,642 metric tons—the largest monthly export volume since April 2014. This growth persists despite the challenging tariff environment precisely because the global price premium exceeds the tariff costs for many markets.

Cheese: The Mixed Bag

Cheese markets demonstrate a nuanced response to tariffs:

Mexican retaliatory tariffs (20-25%) in 2018-2019 reduced US cheese exports by about 12%

However, recent data shows US dairy exports to Mexico rose 8% in value terms in February 2025

Canada has included cheese among products subject to 25% retaliatory tariffs

Global Dairy Trade auction results show Cheddar prices increased 8% to $4,257/MT in recent trading

This mixed picture reflects varying price elasticities across cheese types and the complex interplay between tariffs, supply constraints, and shifting consumer preferences.

Global Market Reshuffling: The New Trade Reality

The tariff environment fundamentally restates global dairy trade patterns with potentially long-lasting consequences for demand.

Market Share Redistribution

As US products face prohibitive tariffs in key markets like China, competitors are rapidly filling the void:

“We’re seeing a shift toward European and New Zealand suppliers to fill the gap,” noted Maria Chen, a Beijing-based dairy analyst

New Zealand is ramping up shipments to China, with exports projected to grow by 15% this year

European dairy exporters are positioned to benefit, though they maintain caution about potential supply constraints

This redistribution of market share can have permanent effects even if tariffs are eventually removed, as suppliers establish new relationships and supply chains adapt. Once you lose market position, regaining it can take years – if it happens at all. It’s like trying to get your milk quality premium back after losing it – the processor has already found another farm to fill that high-quality slot.

Do you think Chinese buyers will return to US suppliers once they’ve established relationships with European and New Zealand producers? Not a chance.

The China Paradox

A particularly interesting dynamic is emerging in China:

China’s milk production dropped 9.2% in early 2025

Despite this domestic production decline, tariffs are blocking affordable US supplies

This forces Chinese buyers to source from more expensive alternative suppliers or reduce consumption

What This Means for Your Operation

The current tariff situation has several important implications for dairy operations of all sizes:

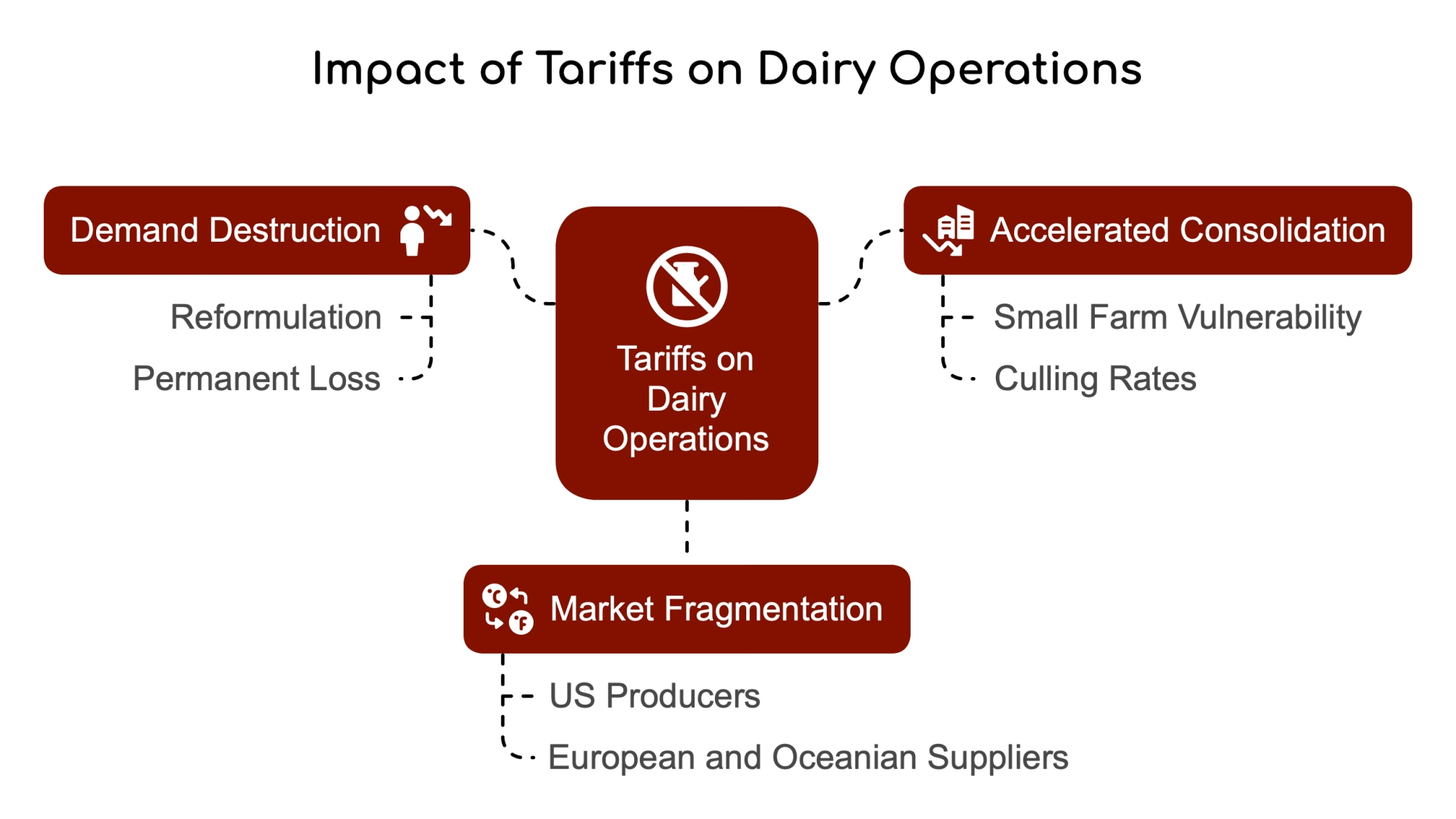

Demand Destruction vs. Diversion

For products with high tariffs, like whey and lactose, the primary effect is not merely demanding diversion but potential demand destruction:

Prohibitive tariffs can force manufacturers to reformulate products to use less of the affected ingredients – like how feed companies reformulate when a specific ingredient becomes too expensive

Once reformulation occurs, demand may not return even if tariffs are removed – just as cows don’t immediately return to peak production after a bout of acidosis

This represents a permanent loss of market share rather than a temporary disruption

Accelerated Consolidation

The financial pressure from tariff-related market disruptions will likely accelerate industry consolidation:

Small farms face particular vulnerability as margins compress

The current low culling rates (down 30% in June) may reverse as financial pressures mount – much like how you might have held onto marginal cows during high milk prices but must make harder decisions when the milk check shrinks

Farms without diversified markets or substantial risk management tools will face the greatest pressure

Let’s face it – the industry was already consolidating. These tariffs are like pouring gasoline on that fire. Are you prepared to be one of the survivors, or will you be another statistic in the ongoing decline of dairy farm numbers?

Market Fragmentation

The global dairy market is fragmenting along geopolitical lines:

US producers are pivoting to Mexico and Southeast Asia as China’s access diminishes

European and Oceanian suppliers are strengthening positions in China

This reorganization of trade flows will create new demand patterns that outlast specific tariffs

Strategic Responses: Protecting Your Operation

Diversify Your Product Mix

The varying impact of tariffs across product categories creates both risks and opportunities:

Farms heavily dependent on whey and lactose revenue streams face the greatest exposure

Operations with the flexibility to shift toward butter production may benefit from continued strong export demand

Cheese producers should evaluate their specific varieties and target markets for vulnerability

Explore Alternative Markets

As traditional export channels face disruption, forward-thinking producers are exploring new opportunities:

Southeast Asian markets (Vietnam, Philippines, Indonesia) show growing dairy demand and fewer trade restrictions

Middle Eastern markets continue to expand dairy imports with less political volatility

Domestic specialty markets may offer premium opportunities as imports face tariff-induced price increases

When was the last time you looked beyond your current milk market? The days of passive milk marketing are over. Your future depends on actively seeking new opportunities before your current ones disappear.

Invest in Product Differentiation

Generic commodity products face the greatest vulnerability to tariff-induced substitution:

Specialty products with unique characteristics face less substitution pressure – just like how your registered Holsteins with superior genetics command premium prices compared to commercial animals

Value-added processing can create products less vulnerable to commodity market swings – like how farms with on-site processing can capture more of the consumer dollar

Sustainability certifications may provide access to premium markets less sensitive to price – much like how organic certification provides a buffer against conventional milk price volatility

Implement Robust Risk Management

The tariff environment demands more sophisticated risk management approaches:

Traditional hedging strategies may be insufficient in rapidly changing trade environments

Forward contracts with domestic processors provide greater certainty as export markets fluctuate

Maintaining financial reserves becomes increasingly critical as market volatility increases

Are you still managing risk like it’s 2010? Because the market has fundamentally changed, and your approach needs to change with it.

The Tariff Endgame: What Happens Next?

The current tariff situation represents a fundamental shift in global trade patterns rather than a temporary disruption. While specific tariff rates may change, the era of relatively frictionless global dairy trade appears to be ending.

Scenario Planning

Forward-thinking dairy operations should prepare for multiple potential scenarios:

Scenario 1: Prolonged Tariff War

China and US maintain high retaliatory tariffs for 2+ years

Permanent loss of US market share in China for whey, lactose

Continued strong butter exports due to global supply shortages

Accelerated consolidation of smaller dairy operations

Scenario 2: Partial Resolution

Targeted tariff reductions in specific product categories

The gradual recovery of some export volumes but at a lower market share

Continued market fragmentation along geopolitical lines

Persistent price volatility as markets adjust to new trade patterns

Scenario 3: New Trade Framework

Comprehensive trade agreement replacing tariffs with managed trade

Establishment of product-specific quotas and market access provisions

Greater government intervention in agricultural markets globally

The Bottom Line

Will tariffs impact dairy demand? The evidence overwhelmingly suggests they will—and already are—have significant effects. However, these impacts vary dramatically across products, markets, and time horizons.

For products like whey and lactose, prohibitive Chinese tariffs have collapsed demand, creating domestic surpluses and price depression. Meanwhile, butter exports surged despite the tariff environment due to global shortages and substantial price differentials.

The dairy industry faces a period of profound readjustment as trade flows reorganize, market shares shift, and supply chains adapt to the new tariff reality. While temporary tariff suspensions may provide brief relief, the fundamental uncertainty introduced by weaponized trade policy will continue to reshape dairy demand patterns for years.

The resilience of butterfat exports amid this turbulence demonstrates that market fundamentals like global supply shortages can sometimes overcome tariff barriers. However, tariffs represent a significant and potentially permanent disruption to established demand patterns for most dairy products.

The operations that will thrive in this new environment will be those that:

Understand the specific tariff impacts on their product mix

Diversify their market exposure beyond vulnerable export channels

Invest in product differentiation to reduce substitution pressure

Implement robust risk management strategies

Maintain financial flexibility to weather market disruptions

The era of predictable global dairy trade is ending. The question isn’t whether tariffs will impact dairy demand—it’s how effectively your operation can adapt to the new reality.

What’s Your Tariff Exposure?

Take a hard look at your operation’s vulnerability to tariff-induced market disruptions:

What percentage of your milk goes into products that are heavily dependent on export markets?

How diversified are your processor relationships and their end markets?

What financial reserves do you maintain to weather market volatility?

What risk management tools are you currently employing?

How quickly could you adapt your production mix if market conditions change dramatically?

The answers to these questions will determine whether your operation becomes a casualty or a survivor in the new tariff warfare reshaping global dairy markets. As the old farm saying goes, “Don’t put all your eggs in one basket” – or in this case, don’t stake your dairy’s future on a single export market that could vanish overnight with the stroke of a politician’s pen.

It’s time to stop pretending these trade wars are someone else’s problem. They’re your problem now. The question is: what are you going to do about it?

Take action today: Contact your processor to understand exactly where your milk ends up and which markets it serves. Review your risk management strategy with your financial advisor. Join forces with other producers to explore new market opportunities. The dairy industry has survived countless challenges, but only those who adapt will thrive in this new tariff reality.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we and our partners use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us and our partners to process personal data such as browsing behavior or unique IDs on this site and show (non-) personalized ads. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Click below to consent to the above or make granular choices. Your choices will be applied to this site only. You can change your settings at any time, including withdrawing your consent, by using the toggles on the Cookie Policy, or by clicking on the manage consent button at the bottom of the screen.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Join the Revolution!

Join the Revolution! Join the Revolution!

Join the Revolution!