Farms using AI are banking an extra $400 per cow annually. That’s real money, not hype.

EXECUTIVE SUMMARY: Look, I’ve been watching this AI thing roll through dairy country for a while now, and here’s what’s actually happening out there. Farms leveraging AI are pulling in around $400 extra per cow each year — that’s not some pie-in-the-sky number, that’s documented profit. Now, where you farm matters big time: Wisconsin guys are seeing $380-420 per cow, but head west to California, where labor’s expensive and heat stress is brutal? Some dairies are hitting $500 per cow. Meanwhile, Europe’s way ahead of us — the Dutch have 67% adoption, Australia’s at 40%, and we’re… well, we’re playing catch-up because half our rural areas can’t even get decent internet. Here’s the thing, though — you don’t need to drop a fortune or revolutionize everything overnight. Start with health monitoring, get your feet wet, and build from there. The farms making moves now? They’re the ones who’ll be writing checks while others are still debating.

KEY TAKEAWAYS

Add $400 per cow to your bottom line by starting with health monitoring systems — fastest ROI you’ll see, especially if you’re dealing with winter stress in the Midwest or heat challenges down south

Get your internet sorted first — you need at least 25 Mbps to make AI worth a damn, and too many US dairy regions are still stuck in the stone age connectivity-wise

Invest $8-12K in training your key people — all that fancy data’s worthless if your team can’t read it or act on it when a cow’s in trouble at 3 AM

Lock down your data ownership rights — negotiate clear contracts so your farm’s valuable information doesn’t end up helping commodity traders make money off your back

Pick partners who’ll stick around — go with vendors tied to university research or proven track records, because that shiny startup might disappear right when you need support most

Look, I’ve been watching this AI wave roll through dairy farms for a couple of years now, and the truth? Those 3 AM alerts — yeah, the ones you dread — they’re saving lives.

Take Amber Horn up in Wisconsin. She’s got 2,100 cows, and one night, her phone buzzed — not some random call, but a sensor picking up a fever in cow #287 before you could see any signs.

That alert, thanks to the smaXtec system, helped Amber’s dairy dodge nearly half a million in losses and deliver a jaw-dropping 7.8x ROI last year.

And Amber isn’t alone.

Decoding the ROI

Dairies using AI tech bump their bottom line by about $400 extra per cow annually, but geography matters:

$380–420 in Wisconsin confinement barns — think harsh winters and steady, demanding labor

$290–350 in Texas heat-stressed herds — battling scorching days

$450–500 in California dairies — where labor’s pricey and heat stress bites deeper

The numbers? Sound, backed by multiple solid sources.

Joe, just nearby Amber, put it bluntly:

“That sensor paid for itself the first time it flagged a cow before I even saw she was sick. Saved me $2,000 in vet bills and kept her in the string.”

Beyond the Hype

The University of Wisconsin’s Dairy Brain project? Not some lab toy. They’re managing data for over 4,000 cows — spotting health issues faster than even the best vet — but the barn is no lab: frozen pipes and spotty internet threaten even the best tech.

Fortunately, Brazil’s innovators have developed AI that works offline, syncing when the internet is restored—a vital feature for far-flung farms.

Global Snapshot

Europe leads, with 67% of Dutch dairies digitally monitoring, but only 25% deeply utilizing AI.

Australia’s dancing to a different tune — 40% adoption focused on pasture and breeding.

America? Split in two:

37% adoption among big dairies (500+ cows)

Less than 20% among smaller operations

Much of this is held back by lagging broadband — only 39% of dairy regions can hit the 25 Mbps needed for AI.

An Aussie consultant said it best:

“We’ve cut feed costs by over 30% with AI. That’s the difference between winning and falling behind.”

Crunching the Numbers

Expect costs of about $75,000 upfront and $12,000 yearly maintenance for an AI system.

Payback is about 15 months on average, with a 30% risk buffer accounting for tech glitches, staffing changes, and market shifts.

Smaller farms often see quicker returns by dumping manual checks altogether.

Guard Your Data

Current laws don’t protect your data rights well — your farm’s info can be sold or shared without your say-so.

States like Vermont and California try to help, but most of us are still in the wild west.

Your Playbook to Win

Start simple: Begin with health monitoring — lowest hanging fruit, fastest payback

Build your base: Secure reliable internet — no speed, no smart tech

Train your team: Data’s useless if no one understands it

Protect your data: Don’t sign away your farm’s story

Choose partners for the long haul: Pick vendors tied to universities or proven track records — those who will still be around in five years. AI isn’t coming to dairy farming—it’s here, it’s profitable, and it’s creating competitive gaps that widen every month. Operations implementing comprehensive AI systems achieve documented 10-20% production increases while reducing costs 15-25%, with payback periods as short as 15 months.

Your competitive position depends on action, not analysis. The producers winning this transition aren’t waiting for perfect solutions—they’re implementing effective ones and improving as they learn.

The choice is stark: embrace the technology and its challenges now, or risk falling behind operations that started today.

Bottom line? The 2025 dairy landscape is separating into winners and everyone else. Time to choose which side you’re on.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Stop Dreading the Vet Check: How Proactive Health Monitoring is Changing the Game – This piece offers tactical advice on shifting from reactive treatment to proactive health management using sensor data. It provides practical strategies for interpreting alerts to reduce vet costs and improve herd longevity, complementing the main article’s ROI discussion.

The Great Divide: Is Your Dairy Built for the Future or Stuck in the Past? – This strategic analysis explores the economic trends forcing dairies to modernize. It reveals the financial mindset and investment strategies of top-performing operations, providing the market context for why the $400/cow AI advantage is becoming a competitive necessity.

Beyond the Bull Book: How AI is Unlocking the True Potential of Dairy Genomics – Looking beyond health monitoring, this article explores the next frontier: AI-driven genomics. It demonstrates how machine learning is creating more reliable breeding values and customized genetic plans, offering a glimpse into the future of data-driven herd improvement.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

What if cutting your worst 40 cows could boost your milk check by $8600/month? One Bavarian farmer found out.

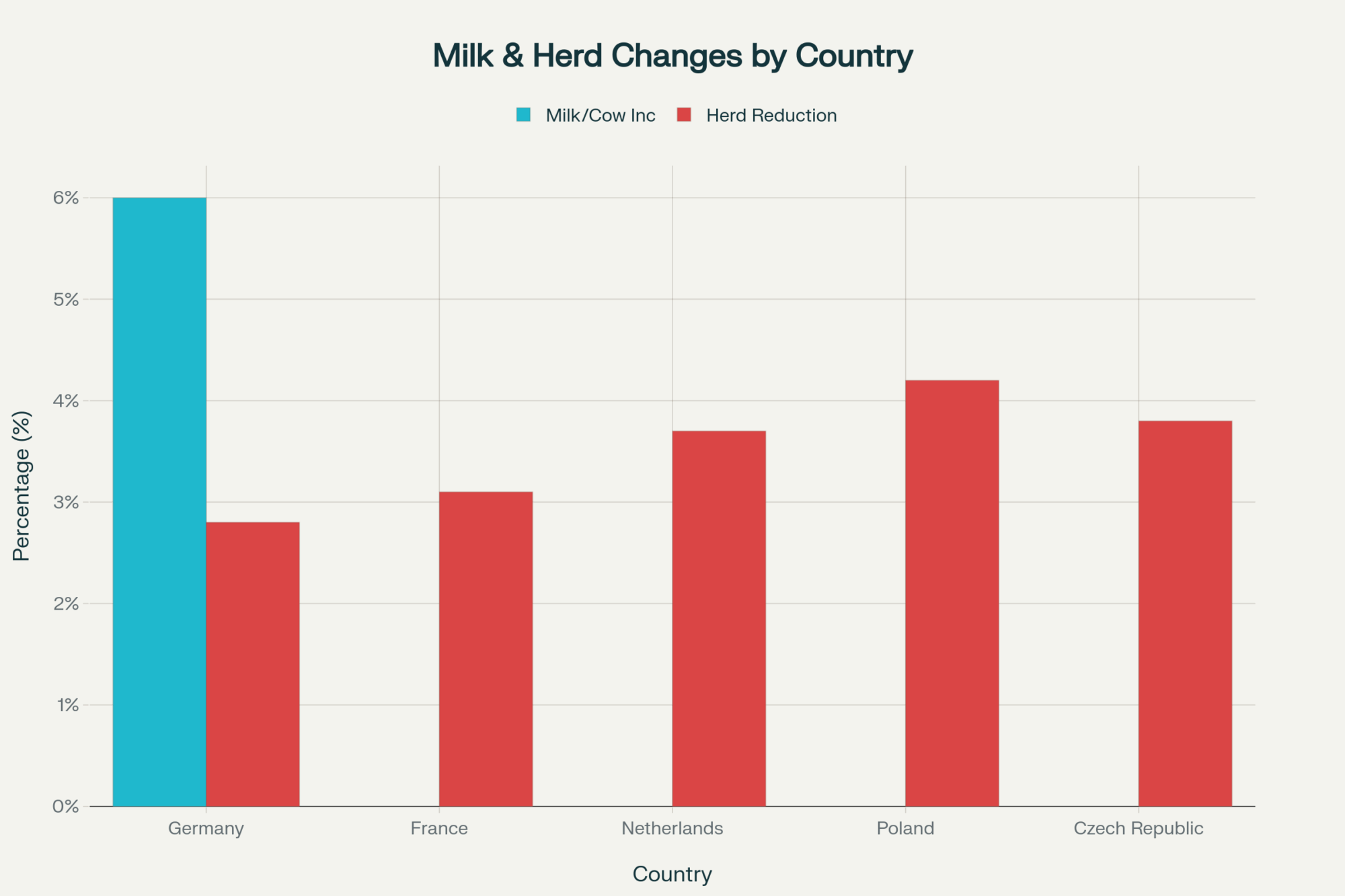

EXECUTIVE SUMMARY: While American producers keep adding cows, European dairy operations just cracked the code on strategic contraction—deliberately cutting herd sizes to boost per-cow profitability. German farms that reduced their herds by 2.8% saw a 6% increase in milk production per cow, with some operations saving €800 monthly on feed costs while also increasing quality bonuses by 40%. The numbers don’t lie: precision culling combined with component optimization is generating 25-30% price premiums across Europe, proving that smart management beats scale every time. From Bavaria to the Netherlands, dairy producers are discovering that fewer cows can mean fatter margins—especially when you pair strategic cuts with precision technology. This is no longer just a European trend. The playbook works anywhere you have the guts to cull smartly instead of expanding blindly.

KEY TAKEAWAYS

Cut strategically, profit immediately: German operations reduced feed costs by €800/month ($860 USD) per farm while boosting quality bonuses 40% through selective culling—start by identifying your 10 lowest-producing cows this week

Precision tech pays when done right: Danish precision feeding systems deliver 18-36 month payback periods with annual savings of €20,000 ($21,600 USD), but only if you invest in proper training first—budget 6 months for the learning curve

Premium positioning captures outsized value: European premium dairy represents just 12% of volume but grabs 22% of export revenue through component optimization—negotiate quality bonuses with your processor using individual cow data

Environmental compliance = competitive advantage: Dutch nitrogen regulations forced €120,000 investments that now generate €22,000 annual savings ($23,800 USD) through improved efficiency—turn regulatory pressure into a profit opportunity

Strategic contraction beats volume expansion: While US operations added 58,000 cows chasing scale, European farms cut 687,000 head and watched profit margins soar 25-30% above historical averages—optimize what you have instead of expanding what you manage

You know that moment when everything you thought you knew about dairy gets flipped upside down? That’s what happened when I started hearing stories like this one from Bavaria. A dairy producer—let’s call him Klaus, representing dozens of similar cases across Germany—told his banker he was cutting 40 cows from his 320-head operation. Fast-forward to this fall, and that same banker was buying him drinks after the October milk check came in 22% higher—all while those extra mouths were gone and daily chores were lighter.

Klaus isn’t alone. Across Europe, dairy folks have caught onto something that challenges everything we learned at dairy short courses: sometimes less really is more, especially if you know which cows to keep and which ones get a ride on the truck.

Raw milk prices tell the story. German producers have been commanding premium pricing in 2025, tracking 25-30% above recent historical averages, with French operations following suit. But the secret isn’t just about cutting numbers; it’s about making each remaining cow work harder and smarter.

Europe’s Contraction: A Country-by-Country Playbook

The data shows one thing crystal clear: just slashing herd numbers won’t guarantee success. Real gains come when you pair fewer cows with significantly higher per-cow productivity.

Germany: Culling Smart, Not Just Hard

German operations reduced herd sizes while improving management, focusing on selective culling and quality optimization. The results speak for themselves—milk output per cow increased substantially while feed costs per liter dropped.

“We used to keep every cow that could stand up and give milk,” explains a Lower Saxony producer representative of this trend. “Now we only keep cows that can pay their way. Cut about 80 head last year, but got more milk per cow overall. The feed bill dropped by around €800 a month (roughly $860 USD / C$1,180), and our quality bonuses increased by 40%. But here’s the thing—it took us nearly two years to get the culling protocols right. Plenty of neighbors tried the same approach and didn’t see results.”

France: Turning Regulatory Pressure into Cheese Gold

French dairy operations reduced herd sizes largely in response to nitrate reduction requirements in sensitive watersheds. But instead of just shrinking, many invested heavily in precision nutrition systems and premium product development.

The payoff? French cheese exports increased in value, despite lower overall milk volumes, as artisan and specialty cheese production captured premium pricing that more than offset the volume reduction.

“We’re not just selling milk—we’re selling stories, tradition, and quality,” says a representative cheese producer from the French Alps. “The market rewards that approach when you execute it properly.”

Netherlands: How Environmental Pressure Created Profit

Dutch producers faced some of the toughest environmental regulations, with nitrogen emission limits requiring substantial investments in new technology and management practices. Many operations invested six-figure amounts in compliance systems—everything from precision feeding to advanced manure management.

“First two years were brutal,” admits a Utrecht-area producer representing this experience. “Spent over €85,000 (about $92,000 USD / C$126,000) on new tech, including digesters and feeding systems. Thought about quitting more than once. However, by year three, I was saving around €18,000 ($19,400 USD / C$26,600) annually on feed while meeting all environmental targets. My cows are healthier, margins are better, and I sleep through the night again.”

Another operation in Groningen invested over €110,000 (roughly $120,000 USD / C$163,000) in compliance technology and now generates an extra €22,000 per year ($23,800 USD / C$32,600) in savings and environmental bonuses.

The Reality Nobody Talks About

However, here’s what the equipment dealers won’t mention upfront: research indicates that a significant percentage of operations attempting precision systems fail to achieve positive returns on investment, primarily due to management challenges or poor implementation.

Success isn’t guaranteed. It depends entirely on your willingness to learn new management skills and adapt your operation to make the technology actually work.

The survivors, however, achieved remarkable efficiency gains through scale optimization and the adoption of smart technology.

The Million-Dollar Mistake: Why Tech Alone Won’t Save You

Denmark leads Europe in precision dairy adoption, but their experience teaches an important lesson: management matters just as much as machinery.

Studies of Danish precision feeding adoption show payback times ranging from 18 to 36 months, with considerable variation based on the quality of management. Some operations never achieve positive returns.

A Jutland producer invested €45,000 (about $48,600 USD / C$66,600) in individual feeding and monitoring technology for his 240-cow operation. “Took me 18 months to see my money back, and that’s because I spent the first six months just learning how to use the systems properly,” he explains. “The dealer training was worthless. Had to learn from other farmers who’d made it work.”

The Bottom Line on Tech Investments

Research shows precision nutrition systems typically cost €50,000-€80,000 ($54,000-$86,000 USD / C$74,000-$119,000), with successful adopters seeing annual savings in the €15,000-€25,000 range ($16,000-$27,000 USD / C$22,000-$37,000). However, significant farm-level variation exists, and the risk of no return is a real concern.

Start with component testing. Train yourself and your team properly. Add technology gradually. Track progress monthly. That’s how you avoid becoming another cautionary tale.

Premium Markets: Small Pond, Deep Water

European premium positioning works, but understanding the scale limitations is crucial for realistic expectations.

Premium dairy represents a small but valuable market segment—roughly 10-15% of production volume, yet capturing a disproportionate share of export value through higher pricing. That gap explains why strategic positioning works for some operations while remaining inaccessible to others.

French artisanal cheese operations fetch premiums of 45-65% over commodity pricing, but these markets have strict volume and quality requirements. You need consistent fat content above 3.8%, somatic cell counts under 150,000, and management protocols that meet processor specifications.

“Premium means hitting the grade every single time,” emphasizes a French cheese producer. “Fat, proteins, cells, handling—everything has to be perfect, or you’re out.”

Global Competition: Different Strategies, Different Results

Europeans optimize for value; North Americans chase volume. Both approaches work within their respective market structures, but the trends are diverging.

German operations reduced herd sizes while substantially improving per-cow productivity. US dairy production grew through herd expansion and genetic improvements. New Zealand producers reduced cow numbers but maintained milk solids through genetic selection and precision feeding.

Region

Herd Strategy

Productivity Focus

Market Approach

Germany

Strategic reduction

Per-cow optimization

Quality premiums

New Zealand

Efficiency-driven cuts

Genetic improvement

Export efficiency

United States

Continued expansion

Scale and technology

Volume growth

Australia

Regional variation

Mixed approaches

Niche markets

Sources: National agricultural statistics, industry reports

North American Implementation: What Actually Works Here

So what does Bavarian success mean for a farm in Michigan or Ontario? More than you might think—if you understand the management requirements.

An Ontario producer credits supply management stability for enabling his C$75,000 ($55,000 USD) investment in technology. “Stable milk prices let me focus on managing better rather than just milking more cows. But I spent six months learning the systems before seeing real results.”

A Michigan producer started with basic component testing, which eventually led her cooperative to offer quality bonuses. “The data made a huge difference, but you’ve got to know how to interpret the reports and make meaningful changes.”

Your Implementation Roadmap

Phase 1: Foundation Building (Months 1-6) Install component testing systems, begin individual cow monitoring, and establish baseline performance metrics. Don’t expect immediate results—focus on understanding your herd’s actual performance. Investment: $15,000-30,000 USD

Phase 2: Precision Systems (Months 6-18) Gradually implement precision feeding for high-producing groups, add automated health monitoring, and optimize rations based on individual cow data. Budget time for the learning curve. Investment: $40,000-80,000 USD

Phase 3: Premium Positioning (Months 18-36) Build processor relationships for quality bonuses, implement environmental monitoring for certifications, and explore direct marketing opportunities where feasible. Investment: $25,000-50,000 USD

Your Next Steps: The European Lesson for North America

The European transformation didn’t happen because producers got lucky with market timing. It happened because they used better data to make informed decisions about which cows to feed and which ones to sell—but it required developing new management skills to ensure the technology actually delivered results.

Start with component testing. Understand your herd’s real performance variations. Invest in training—both for yourself and your team. Build relationships with processors and buyers who value quality over quantity.

Your Action Checklist:

✓ Test milk components this week—establish your performance baseline ✓ Calculate individual cow profitability—identify your best and worst performers ✓ Contact your processor—explore quality bonus programs and requirements ✓ Budget for training time—technology without management skills consistently fails ✓ Start small and prove concepts—before making major capital investments

Will you optimize the cows you have, or just keep adding more mouths to feed?

You don’t need to be European to implement smart dairy management, but you do need to think like them—and invest the time to develop management skills that make precision systems deliver real results instead of just looking impressive in the barn.

The choice is yours, but don’t wait too long. European producers started this transformation five years ago, while others debated whether change was necessary. Now they’re capturing premium pricing while commodity markets squeeze margins.

Your turn.

Currency conversions based on approximate rates: 1 € = 1.08 USD, 1 € = 1.48 CAD

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Unlock Higher Milk Prices: The Ultimate Guide to Improving Milk Components – This guide provides actionable strategies for boosting butterfat and protein. It details proven methods for adjusting rations and management protocols to capture the quality premiums discussed in the main article, directly impacting your milk check.

The Dairy Industry’s Great Consolidation: What It Means For Your Farm’s Future – This analysis explores the economic forces reshaping the dairy landscape. It demonstrates how market consolidation puts pressure on producers, reinforcing why the efficiency gains from strategic contraction are becoming essential for long-term survival and profitability.

The Robots are Here: Is Dairy Farm Automation a Fad or the Future? – Going beyond the hype, this article offers a critical look at the real-world ROI of dairy automation. It helps you assess if new tech is a smart investment or a costly distraction, expanding on this article’s warnings about tech failing without proper management.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

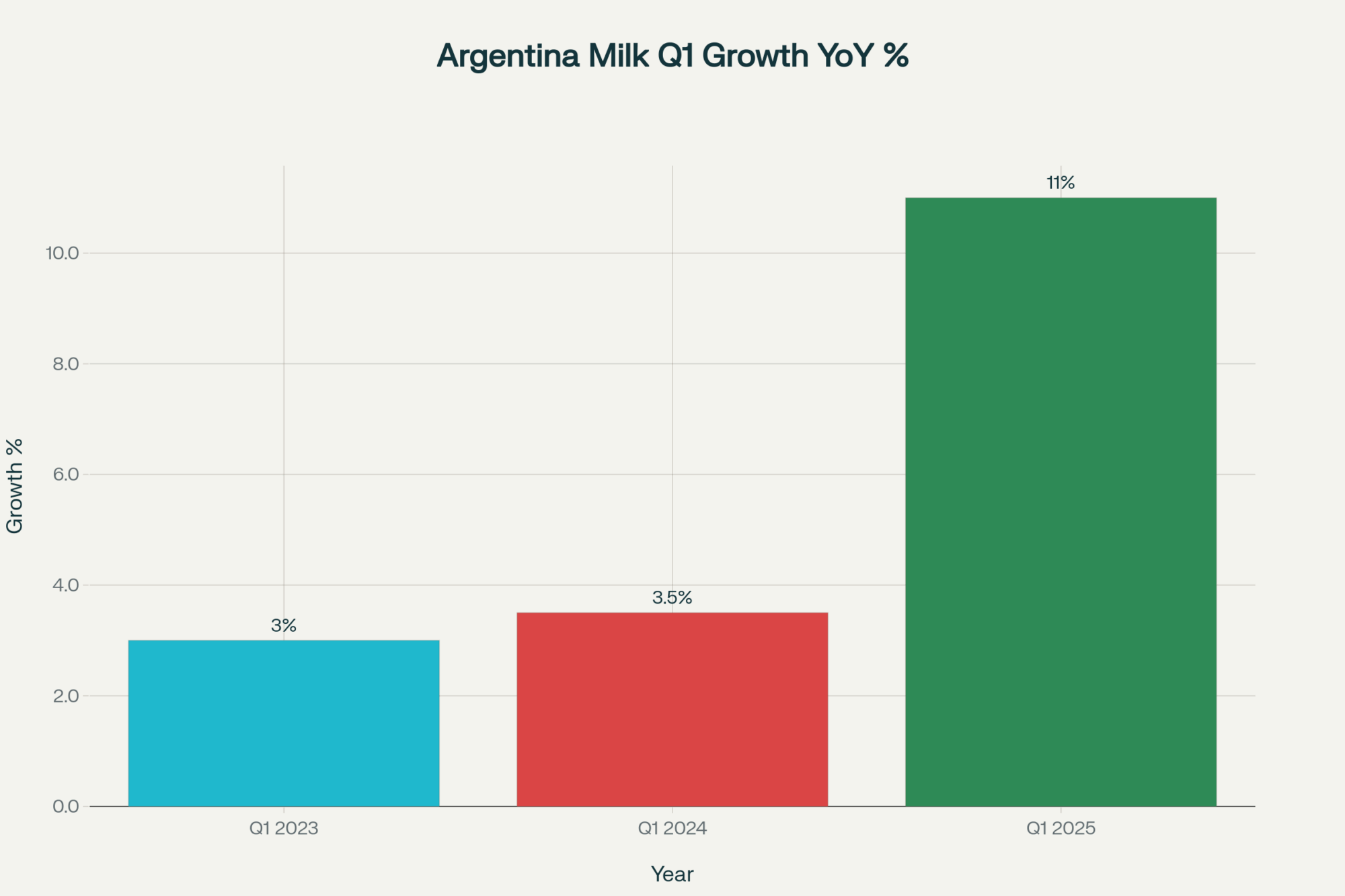

Argentina’s milk output jumped 11% in Q1—that’s reshaping global dairy prices faster than you think.

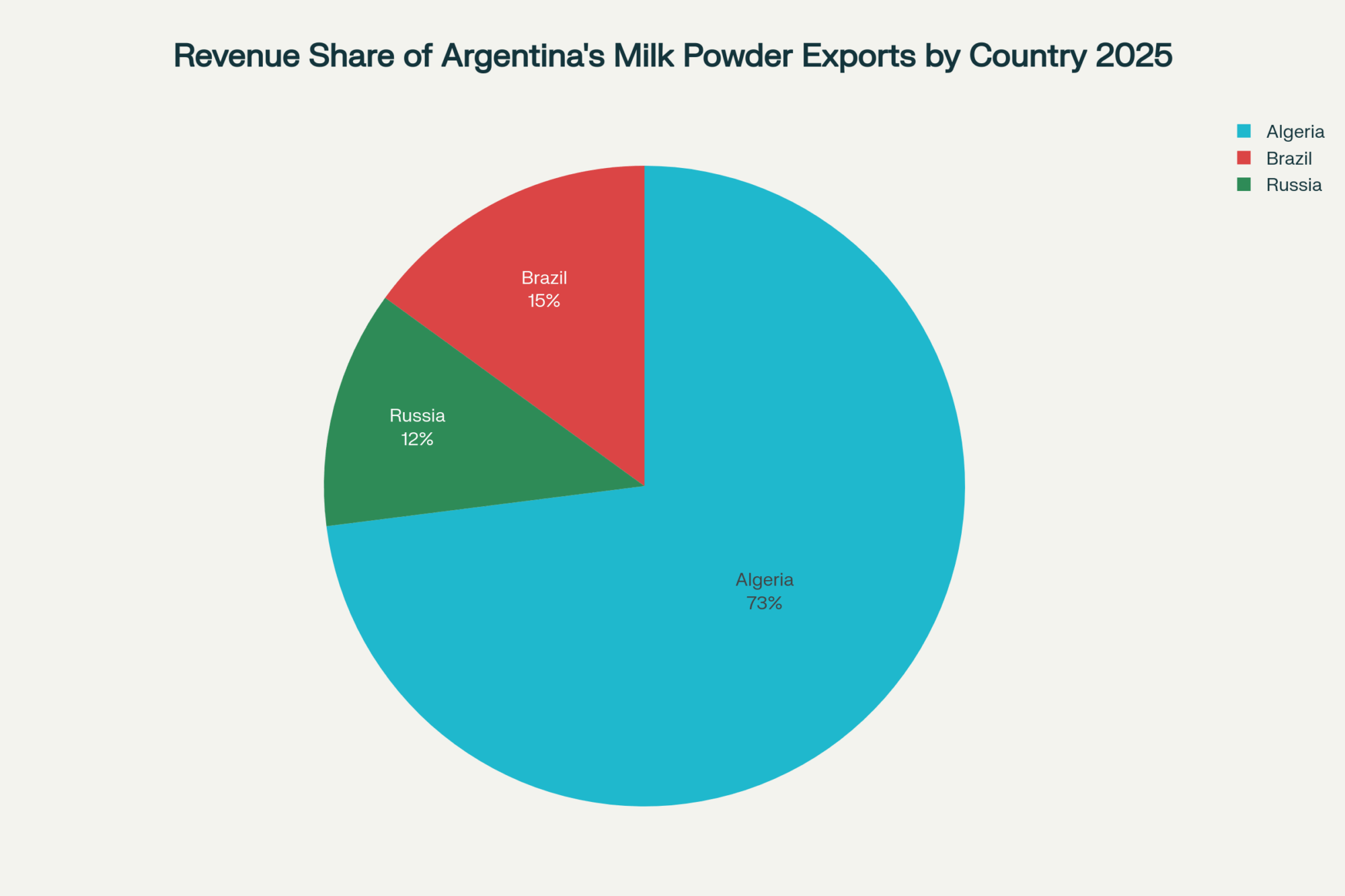

EXECUTIVE SUMMARY: Here’s what’s really goig on: Argentina just became the world’s fastest-growing major dairy producer with 11% growth in Q1 2025—and that’s going to hit your bottom line whether you like it or not. They scrapped those 9% export duties last August, making their milk powder suddenly way more competitive on global markets. We’re talking about 11.2 billion liters projected for this year, with 73% of their powder heading to Algeria alone. The thing is, while EU and U.S. production stays flat due to environmental regs and costs, Argentina’s ramping up fast with smart tech adoption. If you’re not watching milk powder futures and thinking about your operational efficiency right now, you’re missing the boat. This isn’t just another recovery story—it’s a complete reshuffling of who’s calling the shots in global dairy.

KEY TAKEAWAYS

Monitor your commodity exposure now—Argentina’s supply surge could drop global milk powder prices by 5-10%, directly impacting your marketing strategy and contract timing.

Audit your feed efficiency immediately—With new global competition, farms achieving 5-8% efficiency gains through precision monitoring (like Argentina’s Grupo Chiavassa) will separate winners from losers.

Review your supply chain positioning—Argentina’s export growth into Algeria, Brazil, and Russia could create opportunities or headaches depending on where your milk goes and what you buy.

Consider technology investments that boost margins—Argentine producers are using rumination collars and automated health systems to stay competitive; falling behind on farm tech isn’t an option anymore.

Prepare for price volatility through 2025—With traditional powerhouses struggling and Argentina surging, expect more market swings and plan your risk management accordingly.

Look, the bottom line? Argentina went from crisis to global growth leader in 18 months. That kind of speed should wake us all up about how fast things can change in this business. Whether this creates opportunity or problems for your operation depends entirely on how quickly you adapt to the new reality.

Argentina’s dairy industry is sprinting ahead, reshaping the global market in a way that demands serious attention. Production gains reached nearly 11% in the first quarter of 2025, with forecasts suggesting total output close to 11.2 billion liters this year. This rapid expansion signals a significant market shift that could affect operations worldwide.

Argentina’s production surge isn’t just numbers on a chart. It’s a structural recovery driven by policy reforms and operational improvements that will influence global milk flows and pricing. This is critical for producers worldwide.

Farm-level optimism is notable, even if expressed cautiously in public. Many producers are reinvesting in their herds. Grupo Chiavassa, a leading dairy in Santa Fe, uses rumination collars and health monitoring tech from Allflex to enhance productivity and animal health. Though exact 2025 numbers aren’t published yet, previous data confirms technology adoption is delivering real benefits.

Weather remains unpredictable. The La Niña pattern caused pasture challenges in southern provinces, but the Pampas largely received adequate rainfall to support production growth.

Argentina’s dairy surge is changing global markets. Learn how 11% Q1 growth impacts your farm’s profitability and how to adapt your strategy for a competitive edge

Key facts worth noting:

Production growth near 11% in Q1 2025

Total milk volume projected near 11.2 billion liters for 2025

Algeria absorbs about 73% of Argentina’s whole milk powder exports, with Brazil and Russia also major markets

Export duties permanently eliminated in August 2024

Some recent chatter has centered on Nestlé’s Villa Nueva plant, but the major capacity expansion there took place in 2019. The real bottleneck today, as the Argentine Dairy Observatory highlights, is the need for broad upgrades to processing and cold-storage infrastructure across the country.

Farm gate prices have nudged higher, but increasing feed, fertilizer, and land rent costs mean margins remain tight despite growing volumes.

Globally, with growth stalling in the EU and U.S. due to environmental regulations and rising costs, Argentina’s rapid rise creates new competitive dynamics that affect everyone in dairy.

What This Means for Your Operation

Watch milk powder futures closely—Argentina’s rising supply could push prices downward, affecting your margin planning. Audit your operational efficiencies and consider tech investments that might help you stay competitive. If you’re part of a supply chain, whether trading or processing, identify how Argentina’s expanding exports might overlap with your operations.

According to recent Extension work from the University of Minnesota, farms implementing precision monitoring systems are seeing 5-8% improvements in feed efficiency. That’s the kind of edge that matters when global competition intensifies.

What strikes me about Argentina’s transformation is the speed and scale of change. Two years ago, they were struggling with crisis-level inflation and production declines. Now they’re leading global growth and grabbing market share. It’s a powerful reminder that in dairy, staying nimble and informed isn’t just smart—it’s essential for survival.

Argentina’s back, they’re competitive, and they’re rewriting the rules for global dairy markets. Whether that creates opportunity or challenges for your operation depends entirely on how quickly you adapt to this new reality.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The Robotics Revolution: Embracing Technology to Save the Family Dairy Farm – This deep dive into robotic milking systems provides actionable insights on the ROI, labor savings, and production gains of implementing cutting-edge technology. Learn how to evaluate if this investment can boost your farm’s efficiency and competitiveness.

How to Attract and Retain Exceptional Labor for Your Dairy Farm – A strong team is your ultimate competitive advantage. This guide offers practical strategies for improving employee retention, using technology to simplify scheduling and communication, and building a farm culture that supports long-term profitability.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

New Zealand pivoted 40% of dairy exports in 18 months while US operations wait for government bailouts. Market agility beats scale—here’s the proof.

EXECUTIVE SUMMARY: Most North American dairy operations are structured like single-bull breeding programs—impressive in one area, catastrophically vulnerable everywhere else. New Zealand just proved why market concentration kills: while 40% of U.S. dairy exports flow to just three countries now embroiled in trade wars, Kiwi farmers executed an $25.7 billion strategic pivot that captured 46% of China’s dairy import market in under six months. Fonterra’s unified structure—processing 80% of national milk supply—enables coordinated market strategy impossible in America’s fragmented industry where thousands of processors chase quarterly profits instead of long-term positioning. The research reveals that operations scoring below 20 on the included 7-point Market Agility Assessment face crisis-level vulnerability to trade disruption, with potential income losses of $22,800 annually for a typical 500-cow operation during tariff retaliation. Progressive farms implementing genomic testing (targeting £400+ PLI), precision feeding systems (achieving 1.3-1.5 feed conversion ratios), and component optimization strategies are building the structural flexibility that turns trade chaos into competitive advantage. The era of stable, proximate markets is over—survival requires the same strategic evolution that transformed New Zealand dairy from commodity supplier to indispensable B2B partner.

KEY TAKEAWAYS

Market Diversification Strategy: Reduce top-3-market dependence below 60% within 24 months to avoid the $1.90/cwt price reduction and potential 8% production decline that tariff retaliation could trigger—equivalent to losing 960,000 pounds annually for a 1,000-cow operation.

Component Optimization Implementation: Target 3.8%+ butterfat and 3.3%+ protein through precision feeding systems and genomic selection (achieving £400+ PLI performance) to capture Asian market premiums where specific component profiles command substantially higher prices than commodity sales.

Technology Infrastructure Investment: Deploy automated monitoring systems and precision dairy technologies within 18 months to enable individual cow management and rapid production adjustments—New Zealand’s 2-3 year genetic improvement cycles versus traditional 5-7 year programs demonstrate the competitive advantage of data-driven agility.

Strategic Coordination Development: Participate in unified market development initiatives and export consortiums to overcome North America’s structural fragmentation disadvantage—while Fonterra coordinates national strategy, U.S. dairy remains trapped in reactive, individual company scrambling that surrenders market opportunities to more organized competitors.

Financial Resilience Building: Establish reserves sufficient for 12-month operations at 85% of current milk prices and complete the included Market Agility Assessment to identify vulnerability gaps—operations scoring below 20 face fundamental restructuring needs before the next trade disruption.

Picture this: You’re managing a 500-cow Holstein operation averaging 28,000 pounds per cow annually at 3.8% butterfat and 3.2% protein. Suddenly, your biggest milk buyer—representing 40% of your volume—slaps you overnight with a 30% price cut. Most North American operations would scramble for government support or accept devastating losses. New Zealand farmers just pulled off the dairy equivalent of switching feed systems mid-lactation while boosting milk solids production in the process.

The global dairy trade landscape exploded in April 2025 when sweeping U.S. tariffs should have decimated exporters worldwide. Instead, it became the catalyst for the most decisive strategic pivot in modern dairy history. While American and European producers filed WTO complaints and waited for Dairy Margin Coverage payments, New Zealand executed a masterclass in market agility that’s rewriting the playbook for dairy trade strategy.

This isn’t just another trade war story—it’s a live demonstration of why structural agility beats scale when markets fracture, and why the era of predictable, proximate markets just ended for good.

Challenging the Sacred Cow: Why Market Concentration Is Killing North American Dairy

Let’s address the elephant in the milking parlor that nobody wants to discuss: North American dairy’s dangerous addiction to geographic market concentration is a structural weakness masquerading as efficiency.

According to the American Farm Bureau Federation’s latest analysis, over 40% of U.S. dairy exports flow to just three countries—Mexico, Canada, and China—all now embroiled in trade tensions. This isn’t diversification; it’s putting all your genetic material in one AI tank and hoping nothing goes wrong.

Research from the University of Wisconsin quantifies this vulnerability starkly: retaliatory tariffs could reduce all-milk prices by $1.90 per hundredweight, with Class III milk prices declining by $2.86 under full retaliation scenarios. For a 500-cow operation averaging 24,000 pounds per cow annually, that’s a $22,800 annual income loss—equivalent to losing your entire replacement heifer budget.

Why do we accept this risk? Because the industry confuses proximity with security. Just as progressive farms abandoned the practice of breeding every cow to the same bull regardless of genetic merit, we must abandon the illusion that neighboring markets guarantee stability.

The Tariff Tsunami: Deconstructing Economic Warfare

The April 2, 2025, trade offensive wasn’t a policy adjustment—it was calculated economic restructuring designed to fracture competitive alliances. On April 2, 2025, the U.S. President declared a national emergency under Section 232 of the Trade Expansion Act of 1962, citing foreign trade practices that were allegedly “undermining the US economy and national security”.

Here’s the brutal timeline that reshaped global dairy competition:

April 2: National emergency declared, “Liberation Day” for American industry announced

April 5: Universal 10% tariff effective 12:01 AM EDT on most imports, including New Zealand dairy

April 9: Escalation reached 125% on both sides between the U.S. and China

April 10: Full tariff war implementation

The strategic genius wasn’t in the tariff rates but in their differential application. While New Zealand faced a 10% baseline, the European Union was hit with 20% tariffs, and China faced rates escalating to 125%. According to Sense Partners’ research, New Zealand dairy, which already faced an average tariff rate of 19.6%, created combined barriers approaching 30%, transforming the U.S. from a premium, growing market into a high-cost, high-risk proposition overnight.

The justification was immediately challenged. Trade Minister Todd McClay clarified that New Zealand’s average tariff on U.S. goods is a mere 1.8%, not the 20% claimed by the U.S. administration. Kimberly Crewther, Executive Director of the Dairy Companies Association of New Zealand (DCANZ), characterized the tariffs as both “unjustified and discriminatory,” highlighting the “chilling effect on trade”.

The Great Rebalancing: $25.7 Billion in Strategic Motion

While competitors defaulted to defensive lobbying, New Zealand executed what can only be described as the dairy equivalent of switching from a 2X to a 3X milking schedule while simultaneously optimizing the entire herd for component production.

The numbers from The Bullvine’s research demonstrate surgical precision:

Before Tariff Implementation:

The U.S. was New Zealand’s fastest-growing major market, with 16% export growth in 2023

Total U.S. export value reached NZ$1.2+ billion and is climbing

U.S. had surpassed Australia as second-largest destination by March 2024, with a total value of NZ$14.6 billion

After Strategic Pivot:

New Zealand captured an astonishing 46% of China’s total dairy import market, equivalent to cornering nearly half of all genetic merit in a breed

Complete duty-free access to China through FTA, while U.S. dairy faced 125% tariffs

Southeast Asia is designated as the next major growth engine with 8.3% import growth in the 12 months to June 2024

The scale of this reallocation is staggering: New Zealand’s total dairy exports reached NZ$25.7 billion in 2024, representing a 7.7% increase despite global trade tensions.

The Asian Opportunity Matrix: Technical Specifications

Market

Strategic Advantage

Technical Requirements

Performance Metrics

China

Duty-free vs. 125% U.S. tariffs

SCC 3.3%

46% market share captured

Southeast Asia

8.3% import growth, café boom

UHT processing capability

Next major growth engine

Japan

Premium aging demographics

Functional protein delivery

Top-five market status

Why This Matters for Your Operation: This market reallocation is like watching a top genetic sire go from 500 units of semen per year to 50,000 units while maintaining conception rates. The scale and speed of this pivot would be impossible without the structural advantages New Zealand has built over the decades.

The Fonterra Factor: Unified Genetic Program at National Scale

Here’s where conventional wisdom gets shattered: New Zealand’s “cooperative socialism” actually delivers superior market capitalism results.

Fonterra processes over 80% of New Zealand’s milk supply, functioning as a de facto national champion that can execute a unified, long-term strategy impossible in a fragmented industry. Think of Fonterra as having every Holstein breeder in North America coordinate through a single genetic program with unified goals.

Compare this to North American fragmentation:

U.S. dairy includes thousands of independent processors with competing short-term interests

No single entity has the scale to execute a coordinated market strategy

Individual companies chase quarterly profits instead of long-term market positioning

The B2B Masterstroke: From Consumer Brands to Value Chain Integration

In May 2024, Fonterra announced it was exploring divesting its entire global portfolio of consumer brands, including iconic names like Anchor and Mainland. This bold move shed assets, utilizing approximately 15% of the co-op’s milk solids to double down on higher-margin Ingredients and Foodservice channels.

The strategy is paying off spectacularly. The research shows this B2B focus perfectly aligns with Asian market opportunities, transforming Fonterra from a potential competitor on foreign supermarket shelves into an indispensable partner for local food companies.

Technical Implementation:

Southeast Asia’s booming foodservice sector requires sophisticated UHT creams, specialty butters, and functional proteins for the proliferation of specialty bakeries and lifestyle cafés

China’s food processing expansion demands specialized milk protein concentrates and advanced whey fractions

Japan’s aging population pays premiums for functional dairy proteins targeting health outcomes

This strategic pivot is like switching from selling commodity milk to becoming the exclusive supplier of high-protein milk for specialty cheese production. The margins improve, the relationship deepens, and substitution becomes costly for your customer.

New Zealand’s pivot success wasn’t just structural—it was enabled by precision dairy technologies that allow rapid optimization for different market requirements.

The Uncomfortable Truth About Lameness and Market Flexibility

Here’s a controversial reality check that connects directly to market agility: 22% of U.S. dairy cows walk around farms with noticeable limps, yet we obsess over feed efficiency while ignoring mobility efficiency.

Research reveals lameness costs range from $76 to $336 per case, with the problem significantly under-reported on dairy farms. More critically, overstocking—common in operations running 1.3-1.5 cows per stall—compromises lying time and creates long-term lameness issues that cripple operational flexibility.

The Connection to Market Agility: Chronic lameness problems reflect the same systematic thinking that creates market concentration problems. Just as we crowd more cows into facilities designed for smaller animals, we crowd more risk into fewer markets. Both strategies sacrifice long-term resilience for short-term productivity gains.

The Evidence-Based Alternative: Research demonstrates that cows should spend no more than 3-3.5 hours daily out of stalls to maintain 11.5-12.5 hours of lying time. Operations exceeding these thresholds—like export strategies concentrated in too few markets—eventually face systemic breakdowns that are expensive to remedy.

North American Vulnerability: The Fragmentation Problem

The contrast with New Zealand’s agility exposes critical structural weaknesses in North American dairy. Consider this operational analogy: North American dairy is like running 50 separate breeding programs with different objectives, while New Zealand runs one coordinated program with unified goals.

The Data Tells the Story

Current North American performance metrics from USDA sources:

U.S. milk production reached 227.8 billion pounds in 2025, with a forecast dairy herd of 9.420 million head

Average milk yield per cow forecast at 24,185 pounds annually—up 30 pounds from previous projections

Production per cow averaged 2,125 pounds in major producing states in May 2025

However, these production gains mask serious vulnerabilities. The American Farm Bureau Federation confirms that over half of all U.S. agricultural exports went to just three countries: Mexico, Canada, and China in 2024, all now facing trade tensions.

Global Competitors: A Tale of Reactive Dysfunction

The 2025 tariff shock threw the world’s major dairy exporters into disarray. According to the research analysis, their responses have been markedly different, dictated by their unique industrial structures and strategic constraints.

The U.S. on the Back Foot: Reactive and Fragmented

Hit with retaliatory tariffs climbing as high as 125%, U.S. exports of whey and lactose products for which China was the primary global market, collapsed. Dr. Michael Harvey of Rabobank described this not as a “temporary trade hiccup” but a “fundamental realignment of global dairy flows”.

The U.S. response has been characterized by fragmentation and political dependence. Individual firms and industry groups like the International Dairy Foods Association (IDFA) and National Milk Producers Federation (NMPF) have urged the administration to resolve disputes and lobbied for government support through programs like the USDA’s Emergency Commodity Assistance Program.

Furthermore, the U.S. has struggled to leverage its own regional trade agreement, the USMCA. Ongoing disputes with Canada over dairy Tariff-Rate Quotas have seen the U.S. file multiple dispute settlement cases, arguing that Canada’s system unfairly locks out American exporters.

The EU Under Siege: Besieged and Bureaucratic

The European Union finds itself caught in a multi-front trade war. Facing 20% U.S. tariffs on one side, the EU is now the target of a Chinese anti-subsidy investigation threatening over USD $570 million in EU dairy exports.

The EU’s response has been characteristically institutional and defensive, launching formal WTO challenges, issuing official condemnations, and relying on Common Agricultural Policy safety nets. While EU exporters seek to diversify to emerging markets, their highly regulated, subsidy-dependent system makes them less nimble than their Kiwi counterparts.

The Sustainability Weapon: Environmental Performance as Market Access

Another sacred cow that needs challenging is treating sustainability as a compliance burden instead of a competitive weapon.

New Zealand’s environmental performance demonstrates a strategic advantage. Operating completely unsubsidized in a fully deregulated market, New Zealand farmers have been forced to optimize for efficiency and sustainability simultaneously. This isn’t environmental virtue signaling—it’s commercial survival that happens to align with consumer preferences.

The Bottom Line for Your Operation: Just as somatic cell count became a non-negotiable milk quality benchmark, sustainability metrics are becoming market access requirements, not voluntary exercises. Operations that integrate this reality into strategic planning will capture premium opportunities; those that treat it as compliance overhead will find themselves excluded from high-value markets.

Below 20: Crisis Risk—fundamental restructuring needed before next trade disruption

The Uncomfortable Truth About Labor and Structural Paralysis

Here’s a conversation the industry avoids: 70% of hired labor on U.S. dairy farms faces documentation challenges, yet we plan market strategies assuming stable workforce availability.

The New Zealand Contrast: Operating with stable workforce structures and regulatory certainty, New Zealand dairy operations can make strategic decisions based on market opportunities rather than regulatory uncertainty. This operational stability is another structural advantage that enables rapid market pivots.

Evidence-Based Solutions: Research suggests that farms investing in automation and precision technologies reduce labor dependency while improving flexibility. Automated systems create operational resilience that enables strategic pivoting when market opportunities arise.

The Bottom Line: Structural Reform or Strategic Irrelevance

New Zealand’s $25.7 billion pivot proves a fundamental truth: In fragmented global markets, the ability to reallocate resources rapidly trumps raw production capacity. While North American dairy focused on optimizing for stable, nearby markets, New Zealand built the structural flexibility to thrive in chaos.

The lessons are clear and urgent:

Immediate Action Items for North American Operations:

Market Diversification Strategy: Begin aggressive pursuit of radical market diversification with a specific focus on Southeast Asia, the Middle East, and Africa. Target: Reduce top-3-market dependence below 60% within 24 months.

Component Strategy Implementation: Using verified precision feeding systems, begin optimizing for butterfat and protein percentages that command premiums in diversified markets. Target: 3.8%+ butterfat, 3.3%+ protein within 12 months with documented progress tracking.

Technology Infrastructure Development: Implement precision dairy systems enabling individual animal management. Target: Deploy automated monitoring systems within 18 months with documented ROI analysis.

Strategic Coordination Enhancement: Develop collaborative relationships enabling unified market development efforts through established industry networks. Target: Participate in at least one coordinated export initiative annually with measurable outcomes.

Financial Resilience Building: Establish financial buffers capable of withstanding major market disruptions. Target: Build reserves sufficient for 12-month operations at 85% of the current milk price.

The Strategic Reality Check:

Your current structure probably can’t deliver New Zealand-level agility. The fragmentation that seemed like healthy competition is now a strategic vulnerability. The government safety nets that provided security are now agility anchors.

But here’s the opportunity: Every structural disadvantage can become a competitive advantage for operations willing to challenge conventional practices and implement evidence-based alternatives.

Market agility isn’t longer a competitive advantage—it’s a survival requirement when trade wars become standard operating procedures. New Zealand proved that nimble beats big when markets fracture. The only question now is whether North American dairy is ready to learn from the masters—or get left behind watching their exports disappear.

Your Next Steps:

Complete the Market Agility Assessment above using actual data from your operation, not estimates

Identify your three lowest scores and develop 90-day improvement plans with external expert consultation

Establish market intelligence sources beyond local co-op communications and regional publications

Connect with precision technology vendors to assess infrastructure gaps and investment requirements

Engage with industry coordination efforts through organizations like USDEC or regional dairy associations

The harsh reality: Waiting for government solutions or market stability to return is a strategy that guarantees irrelevance. The operations that will thrive in the next decade are already building the structural agility that New Zealand demonstrated is possible.

In dairy farming, just like in genetics, diversity and adaptability beat raw numbers every time. New Zealand farmers built their industry like a balanced breeding program—multiple strengths, rapid response capability, and the discipline to make hard decisions quickly. North American dairy needs the same strategic evolution, or risk becoming the genetic equivalent of a single-trait selection program—impressive in one area, vulnerable everywhere else.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we and our partners use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us and our partners to process personal data such as browsing behavior or unique IDs on this site and show (non-) personalized ads. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Click below to consent to the above or make granular choices. Your choices will be applied to this site only. You can change your settings at any time, including withdrawing your consent, by using the toggles on the Cookie Policy, or by clicking on the manage consent button at the bottom of the screen.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Join the Revolution!

Join the Revolution! Join the Revolution!

Join the Revolution!