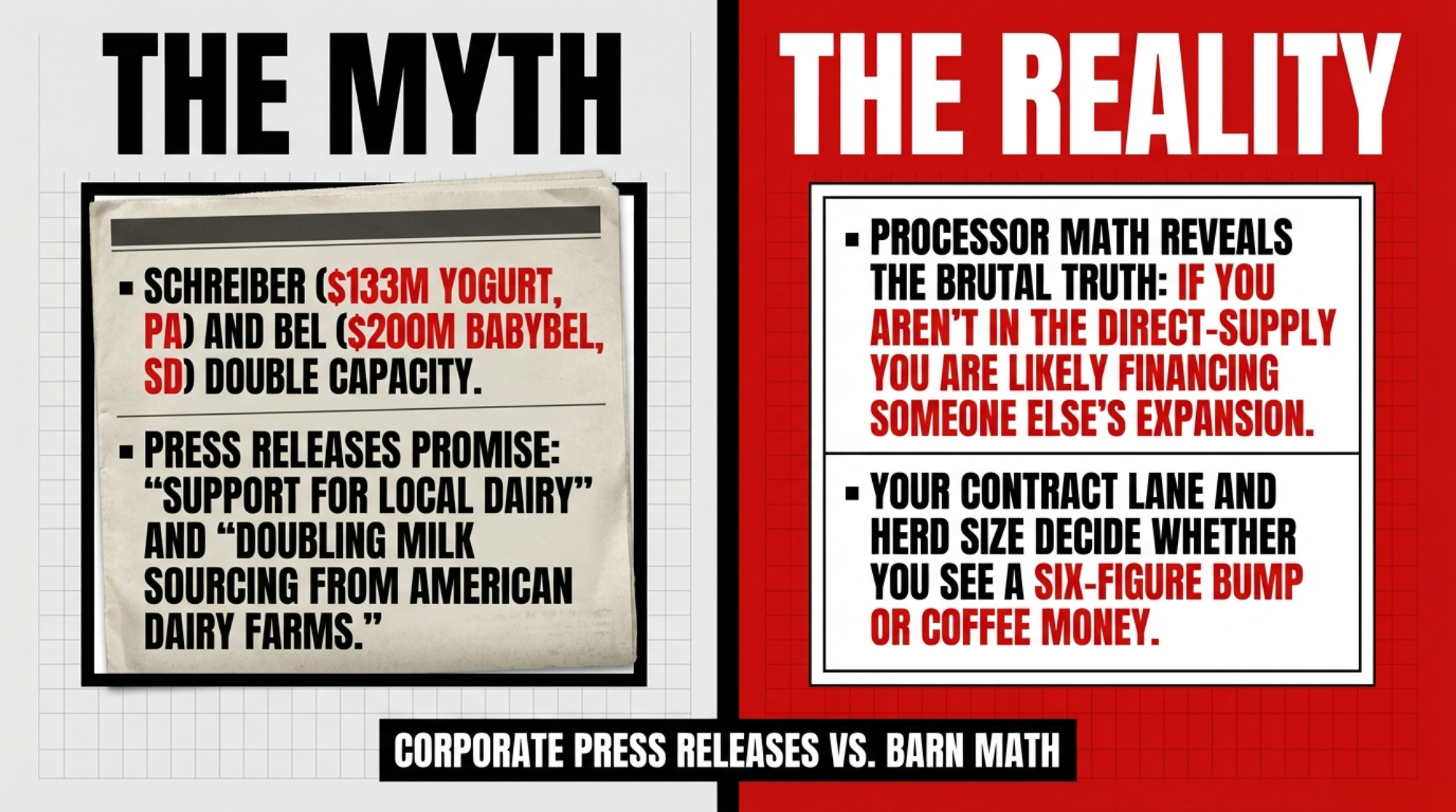

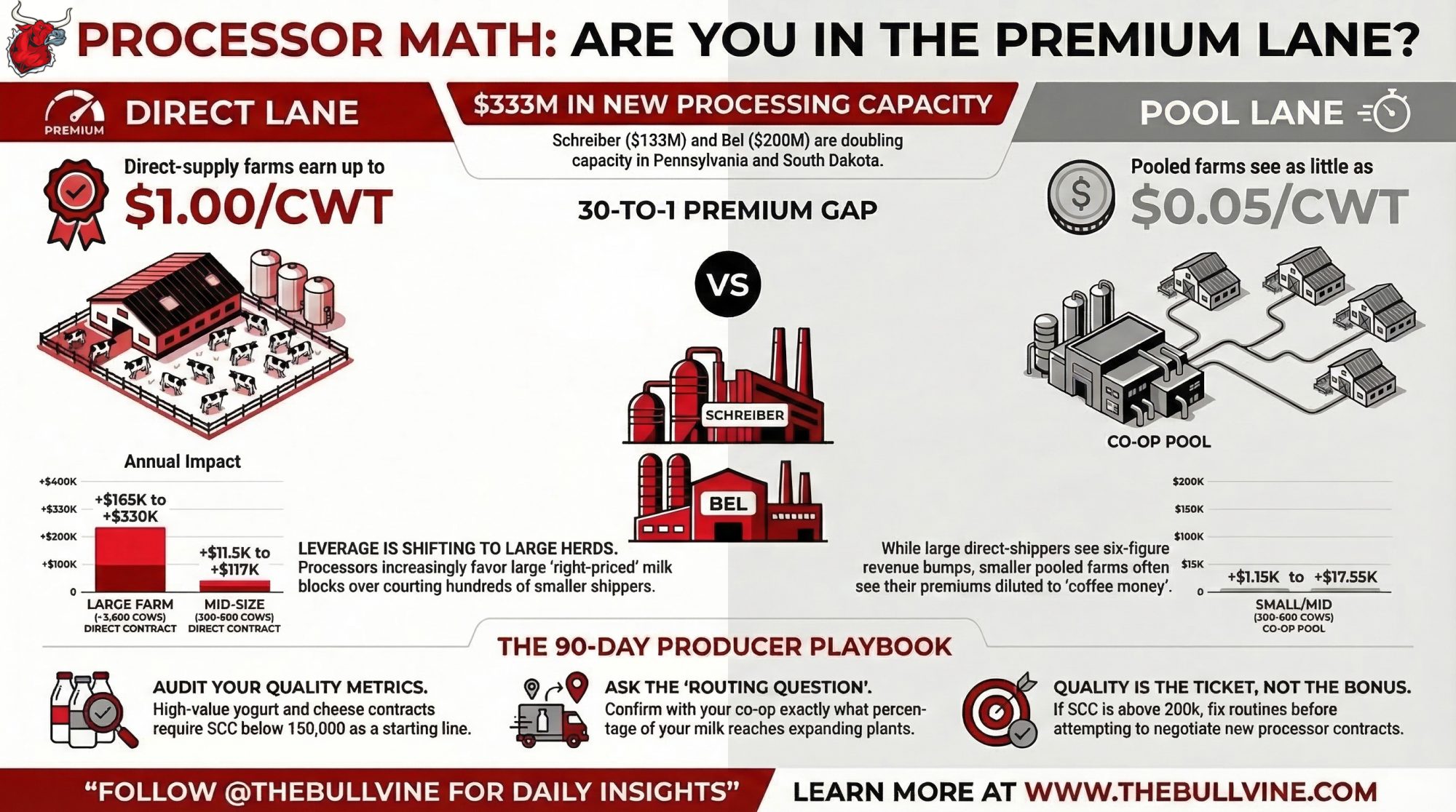

Processor math reveals the brutal truth: If you aren’t in the direct-supply lane, you’re likely financing someone else’s expansion.

Executive Summary: $333M processor rush: Schreiber ($133M yogurt) and Bel ($200M Babybel) double capacity in PA/SD. Rod Hissong’s $5M Schreiber contract gains $165K–$330K/year. 200‑cow pool farms get $1K–$7K. 30‑to‑1 premium gap. PA’s 490 farm exits flip leverage to herds like Mercer Vu. FO30 down $5.42/cwt. Run your numbers: co‑op routing % + SCC <150K? +$0.50/cwt floor to switch lanes. Processor Math asks: where’s your share?”

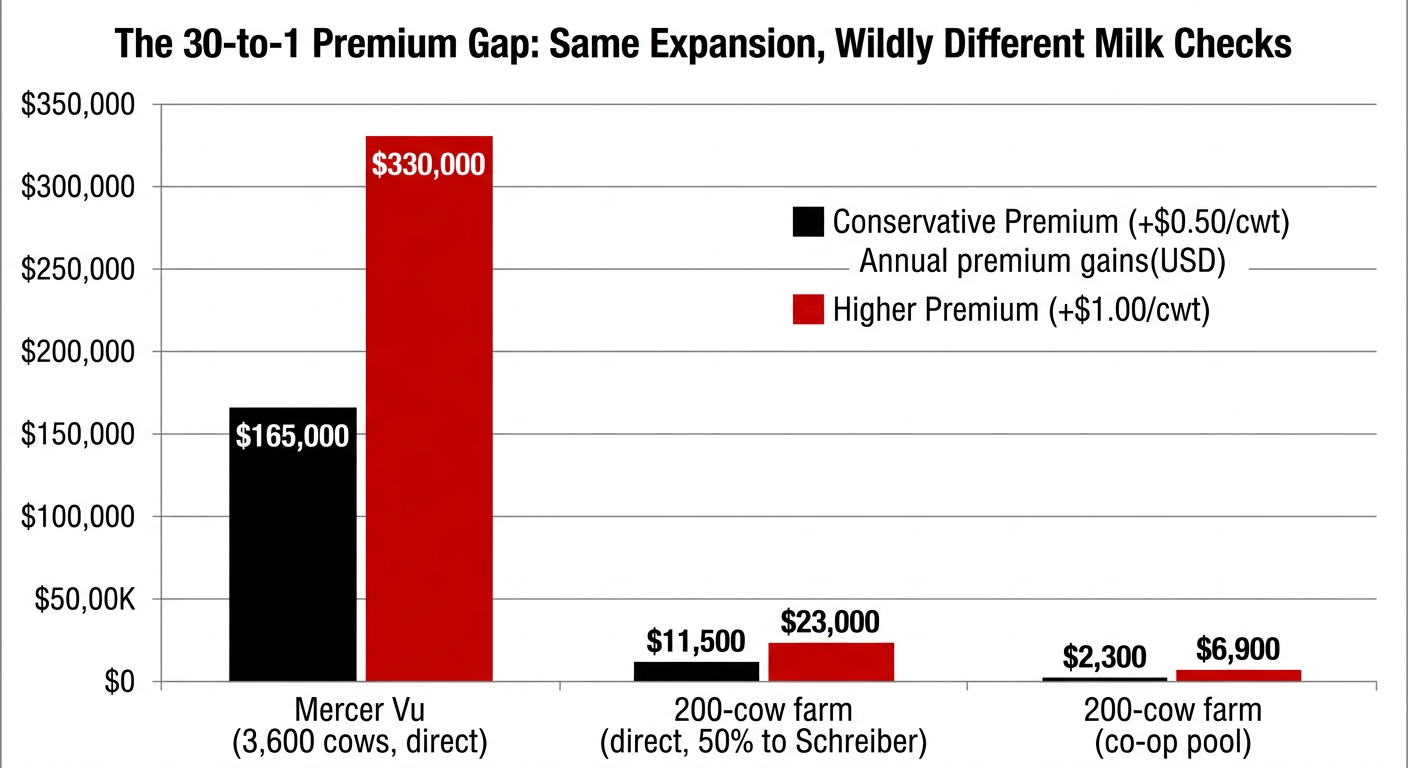

Rod Hissong ships 33 million pounds of milk a year to Schreiber Foods’ Shippensburg, Pennsylvania, plant — at least $5.06 million in annual revenue from that one relationship, using the Federal Order Class II minimum of $15.34/cwt(USDA, February 2026) as a floor. When Schreiber’s new yogurt line hits full stride, that same expansion could add $165,000–$330,000/year to his milk check, while a 200‑cow co‑op farm in the same sourcing zone might only see $1,150–$6,900 from the same announcement — depending on how premiums wash through the pool.

Two days after that Schreiber news, Bel Group broke ground on a $200 million expansion in Brookings, South Dakota, to double Babybel production from 10,000 to 20,000 tons per year and double its milk intake from American farms, primarily in South Dakota and neighboring states. Together, those two projects add $333 million in dairy processing capacity to regions where milk is already concentrating into fewer, larger herds — and where contract structure quietly decides who actually gets paid.

The Massive Premium Dilution Nobody Mentions

Press releases promise “support for local dairy.” The barn math says your contract lane and herd size decide whether you see a six‑figure bump or coffee money.

Mercer Vu Farms — Hissong’s operation in Mercersburg, PA — milks about 3,600 mature cows, farms 5,500 acres, and produces roughly 100 million pounds annually. Glenn and Mae Hissong started that herd with 7 cows in 1949; today, about one‑third of Mercer Vu’s production, around 33 million lbs/year, goes straight to Schreiber. The rest moves through Land O’Lakes.

The “average” Schreiber‑zone producer looks very different. The Center for Dairy Excellence’s 2025 survey pegs average responding herd size at 152 cows, while the USDA puts the statewide Pennsylvania average closer to 106 cows. Even using 152, that’s roughly 3.5 million lbs/year per farm — about a tenth of Mercer Vu’s Schreiber volume.

Schreiber’s 109,000 lbs/day: Same Expansion, Very Different Milk Checks

Governor Shapiro’s office says Schreiber’s Shippensburg project will add 109,000 lbs of raw milk processing per day, or about 39.8 million lbs/year, across 165 farms in 11 counties. Under realistic premium scenarios, that looks like this:

| Farm Profile | Annual Schreiber Volume | Premium Scenario | Annual Impact (barn math) |

| Mercer Vu (~3,600 cows, direct) | ~33M lbs | +$0.50/cwt | +$165,000 (33,000 cwt × $0.50) |

| +$1.00/cwt | +$330,000 (33,000 cwt × $1.00) | ||

| 200‑cow farm (direct, 50% to Schreiber) | ~2.3M lbs | +$0.50/cwt | +$11,500 (23,000 cwt × $0.50) |

| +$1.00/cwt | +$23,000 (23,000 cwt × $1.00) | ||

| 200‑cow farm (co‑op pool, indirect) | Pooled | +$0.05–$0.15/cwt (diluted) | +$1,150–$3,450 (23,000 cwt × $0.05–$0.15) |

| +$0.10–$0.30/cwt (diluted) | +$2,300–$6,900 (23,000 cwt × $0.10–$0.30) |

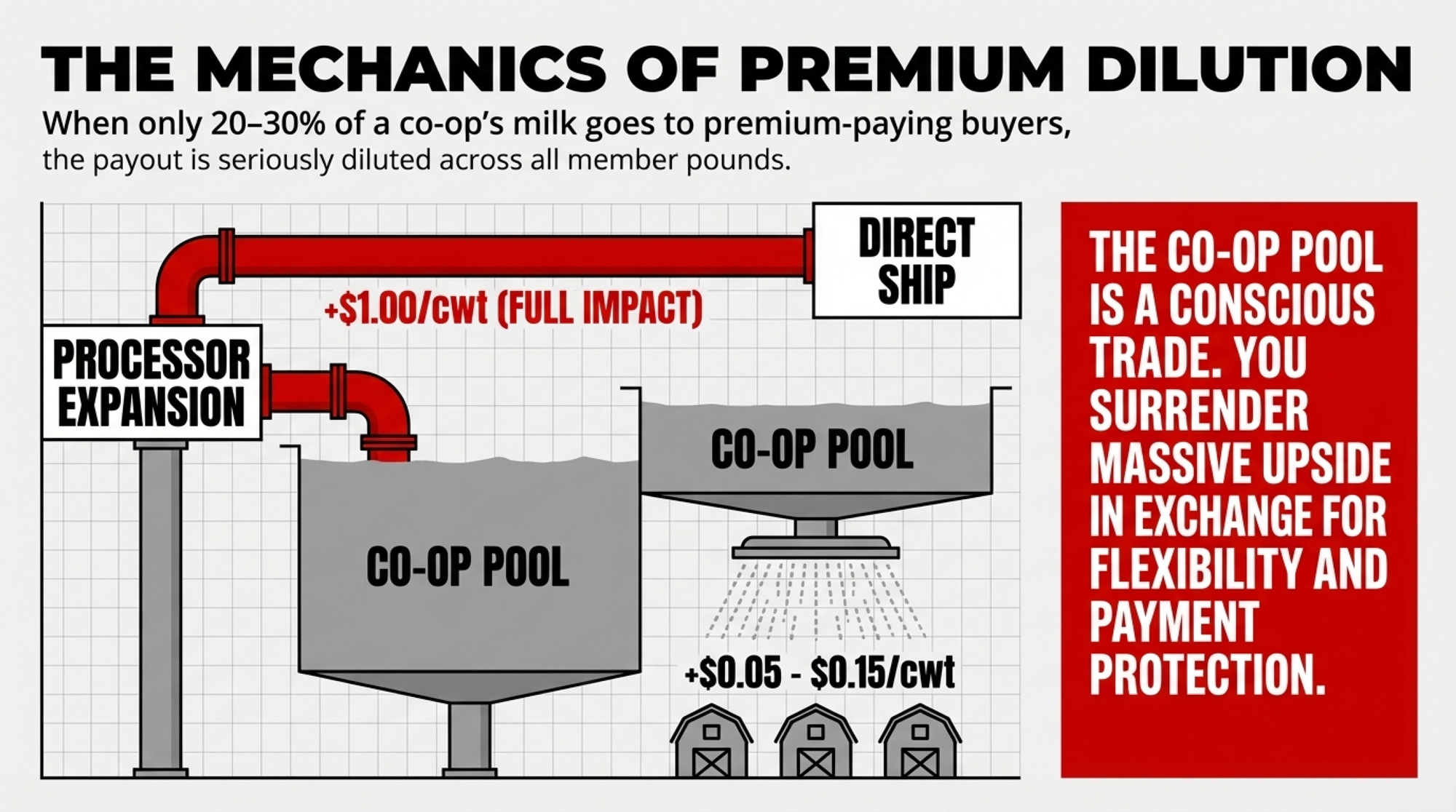

Those premium bands line up with historical $0.25–$1.00/cwt over‑order and contract premiums discussed by agricultural economist John Janzen in Progressive Dairy, and with the pooling math laid out by Mark Stephenson and Andrew Novakovic for the Center for Dairy Excellence. Their work shows that when only 20–30% of a co‑op’s milk goes to premium‑paying buyers, those premiums are “seriously diluted” across all member pounds.

Same expansion. Same counties. A difference that can approach 30‑to‑1 between the top and bottom rows.

| Farm Profile | Conservative Premium (+$0.50 or +$0.10 pooled) | Higher Premium (+$1.00 or +$0.30 pooled) |

|---|---|---|

| Mercer Vu (3,600 cows, direct) | $165,000 | $330,000 |

| 200-cow farm (direct, 50% to Schreiber) | $11,500 | $23,000 |

| 200-cow farm (co-op pool) | $2,300 | $6,900 |

If your milk only reaches an expanding plant through a pool, you’re living in that bottom row — even if the press release name‑checks your state.

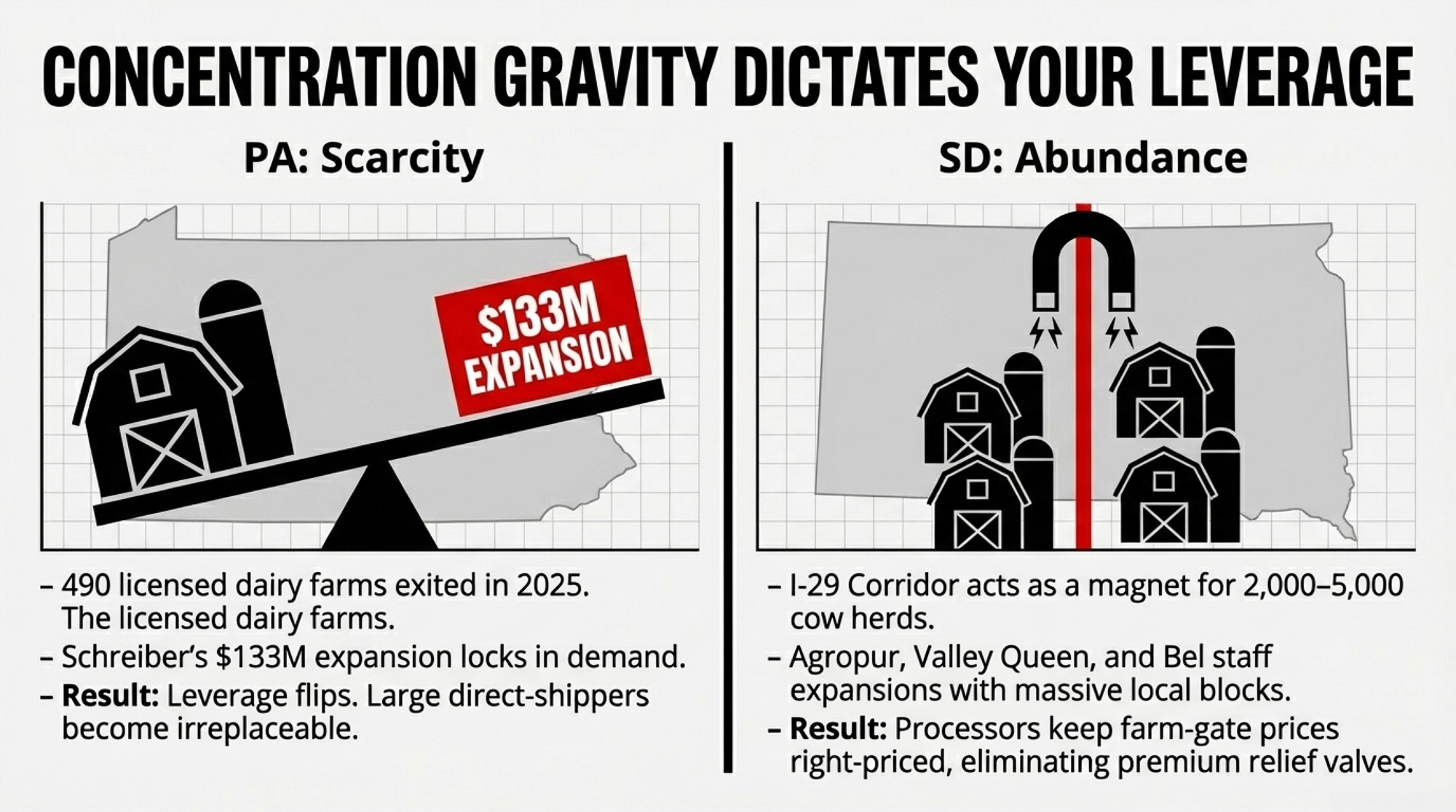

Concentration Gravity: From Shippensburg to Brookings

What’s happening in south‑central Pennsylvania is part of a broader concentration gravity: processor capital chasing large, “right‑priced” milk blocks.

On the PA side, Schreiber can pick up its extra 39.8 million lbs/year largely by deepening commitments with a handful of big direct shippers like Mercer Vu and adding a smaller number of mid‑size farms that can meet yogurt‑grade quality. Janzen’s line — “it’s much easier to sign up 10 2,000‑cow farms than 100 200‑cow farms” — is the procurement cheat code.

On the SD side, that same gravity is even stronger:

- Valley Queen’s 2025 profile highlights 39 farms milking around 95,000 cows — about 2,400 cows per farm, all within reasonable hauling distance.

- South Dakota has been one of the fastest‑growing milk states in the U.S., while national herd numbers slowly shrink.

- Agropur (Lake Norden), Valley Queen (Milbank), and Bel (Brookings) now form a cheese/snack corridor that can staff expansions with local 2,000‑ to 5,000‑cow herds instead of courting hundreds of smaller shippers.

Bel’s press release says Brookings currently produces 10,000 tons/year of Babybel and will double to 20,000 tons, “doubling milk sourcing from American dairy farms, primarily in South Dakota and neighboring states.” Earlier coverage around the original Brookings plant pegged its draw at about 15,000 cows; doubling production implies a similar additional draw.

The more easily Bel, Agropur, and Valley Queen can fill new vats with I‑29 corridor milk, the fewer basis‑premium “relief valves” remain for smaller herds shipping in from border states. That shows up later as weaker premiums and fewer calls when plants are short.

What Does Bel’s Expansion Really Mean for a 500‑Cow SD Herd?

South Dakota’s starting price floor is very different from Pennsylvania’s.

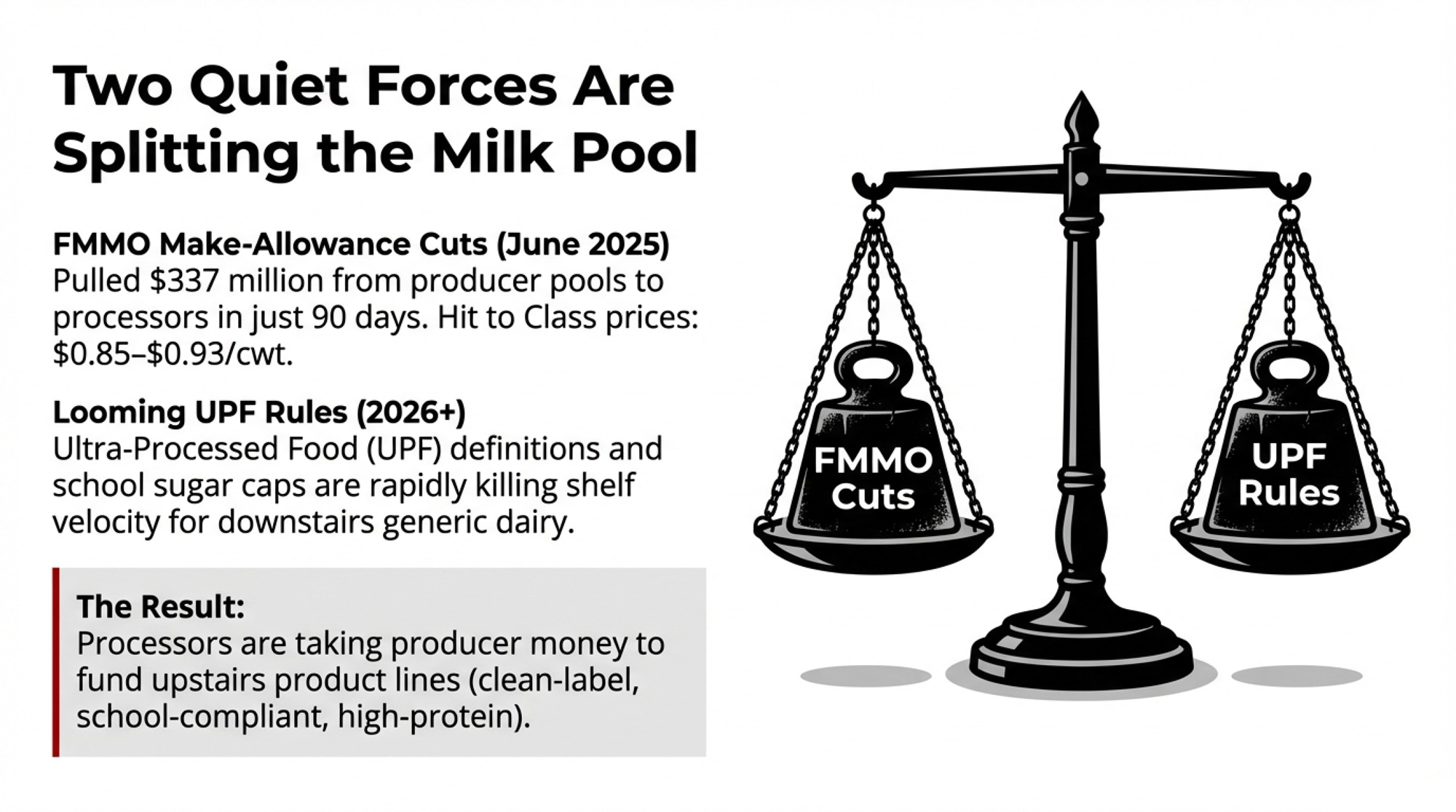

Federal Order 30 data show an Upper Midwest Statistical Uniform Price of $15.05/cwt in January 2026, down $5.42 from $20.47/cwt in January 2025, and among the lowest uniform prices across the FMMOs at that point. American Farm Bureau’s analysis of the June 2025 FMMO changes estimates that, in the first three months, higher allowances alone will result in about $64 million in lost revenue to the Upper Midwest pool.

A 500‑cow SD herd producing roughly 11.7 million lbs/year sits at about $1.76 million of gross milk revenue at $15.05/cwt.

Bel’s expansion doubles Babybeladd’s output to 20,000 tons and puts another $200 million into the Brookings site. Translate that into barn‑math scenarios for a 500‑cow herd:

| Factor | Direct Contract | Co-op Pool |

| Premium Potential (500-cow herd, SD example) | +$58,500–$117,000/year ($0.50–$1.00/cwt over FMMO) | +$5,850–$17,550/year (diluted +$0.05–$0.15/cwt across all pool lbs) |

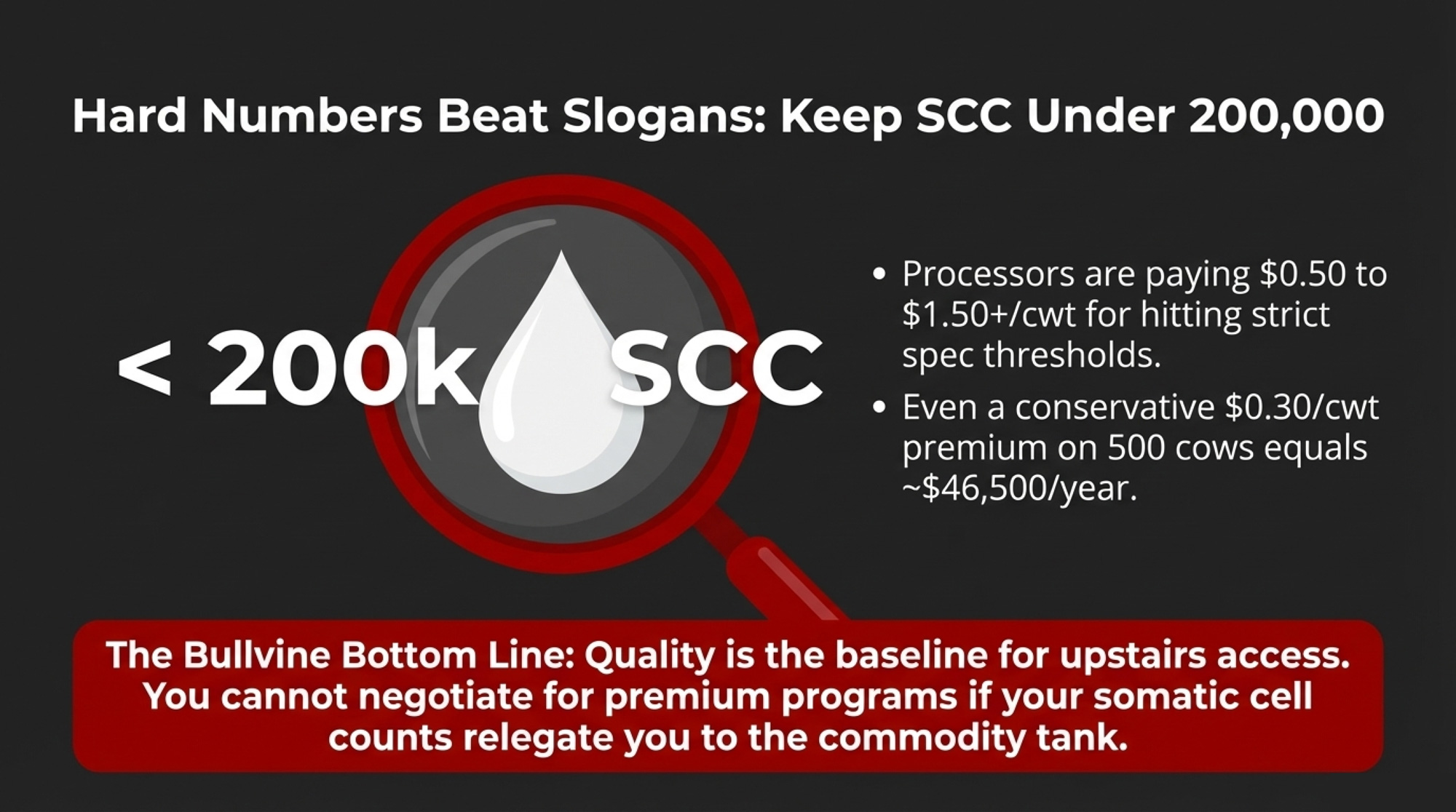

| Quality Threshold | SCC <150K (target <100K); strict bacteria/temp audits; failures can trigger termination | More flexibility on month-to-month quality variance; still need to meet minimum FMMO standards |

| Volume Commitment | 3–5 year agreement typical; specified daily/monthly minimums; limited flexibility to expand/shrink without renegotiation | Ship what you produce; flexibility to grow/contract herd size without contract amendments |

| Payment Protection | Termination risk if plant closes, finds cheaper supply, or cites quality “for cause” | Federal Order payment security; pool guarantees you get paid even if processor fails |

| Upside Capture | You get full premium when processor wins (e.g., +$0.50–$1.00/cwt for specialty cheese/yogurt) | Premium dilution: your milk subsidizes pool members farther from premium plants |

Exact over‑order numbers are contract‑specific and not public, but these ranges reflect real SD “right‑price” conversations and are consistent with historical premium levels along the corridor.

| Scenario | Volume & Price | Annual Impact (barn math) |

| Base case (pool only) | 11.7M lbs at $15.05/cwt | $1.76M (117,000 cwt × $15.05) |

| Direct lane, +$0.50/cwt | 11.7M lbs at $15.55/cwt | +$58,500 (117,000 cwt × $0.50) |

| Direct lane, +$1.00/cwt | 11.7M lbs at $16.05/cwt | +$117,000 (117,000 cwt × $1.00) |

| Pool farm, diluted +$0.05–$0.15/cwt corridor lift | 11.7M lbs at $15.10–$15.20/cwt | +$5,850–$17,550 (117,000 cwt × $0.05–$0.15) |

Lynn Boadwine — who milks more than 2,000 cows near Baltic and has been a visible voice for SD dairy recruitment — summed up the processor logic bluntly: “You don’t want to have the highest price raw material for those folks, so they’re not going to move here. We’ve got to be right-priced to attract a processor.”

When a region can keep landing plants and keep farm‑gate prices “right‑priced” for processors, it’s not just growing local capacity. It’s slowly shifting where processors feel comfortable cutting bigger checks.

490 Pennsylvania Farms Gone — and Why That Flips the Leverage

Now flip back to Pennsylvania, because Hissong’s leverage sits on top of a changing supply base.

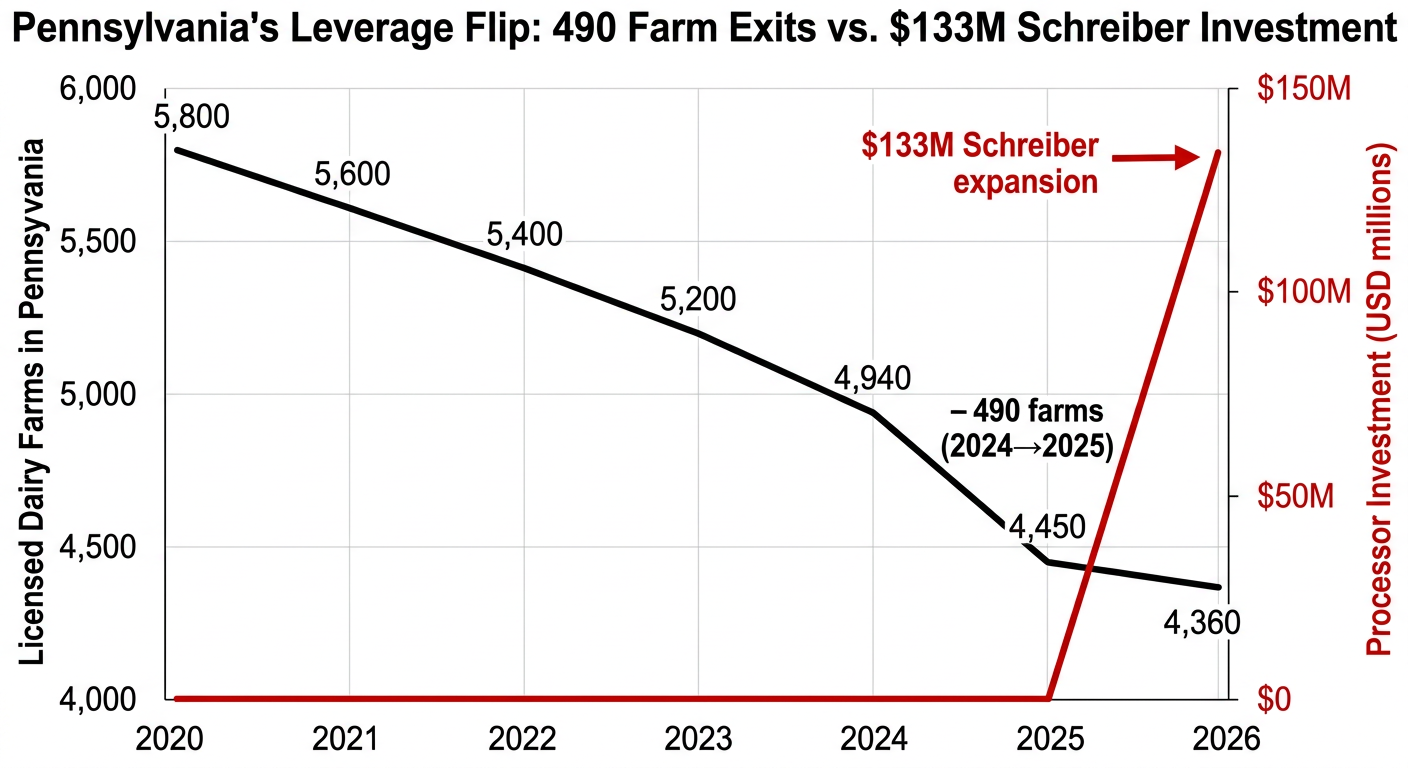

Looking at the USDA’s Milk Production report, notes that Pennsylvania lost 490 licensed dairy farms in 2025, dropping from 4,940 to 4,360 dairies — an 11.7% decline and about 41% of all U.S. dairy farm exits that year. Cow numbers fell by around 4,000 head to roughly 465,000, and state milk volume slipped 0.5% while national production rose 3.4%.

Schreiber has operated its Shippensburg plant since 2002. By locking in a $132.9 million expansion and 47 new jobs there, the company is effectively tethering more of its future yogurt strategy to south‑central PA.

Put that together:

- Fewer herds.

- Slightly fewer cows.

- More processing demand backed by fresh capital.

For a large, proven direct‑ship supplier like Mercer Vu, that’s the moment the math flips. He’s no longer just one more shipper in a crowded market; he’s one of the relatively few large herds Schreiber can’t easily replace.

For a 200‑cow farm shipping into a co‑op pool, it raises the stakes on whether your co‑op is at the Schreiber table or repositioning milk into lower‑value outlets.

When Hissong said it’s “exciting and commendable for Schreiber Foods to continue investing in this plant” rather than chasing expansion “in West Texas, New York and other areas,” he was also naming the alternative: that $133 million could’ve gone somewhere else. pa

Trevor Farrell, Schreiber’s president, underlined that intent: “This expansion reinforces our long-term commitment to this area.”

Big capital decisions like this lock in procurement patterns and premium maps for years. If your region isn’t seeing those announcements — or if you’re not inside the sourcing radius — you’re playing a different premium game than your peers in PA or SD.

The 90‑Day Playbook Before the Premium Window Closes

Processors usually build their supply base 12–18 months before an expansion line hits full utilization. After that, they mostly manage what they’ve signed.

If you’re anywhere near Brookings or Shippensburg, the next 90 days matter.

If You’re a 500‑Cow SD Herd in the Pool

In the next 30 days:

- Pull your last 12 months of DHIA records. Write down the average SCC, bacteria count, fat %, and protein %.

- If SCC is over 200,000 or SPC/bacteria over 20,000 cfu/mL, fix that first. That kind of quality noise kills a procurement conversation before it starts.

- Call your co‑op field rep and ask three precise questions:

- “Do we currently supply Bel Brookings, Agropur Lake Norden, or Valley Queen Milbank?”

- “Roughly what share of my milk routes to each?”

- “Are there any volume commitments tied to those plants I should know about?”

By 90 days out:

- Ask SDSU Extension or SD dairy groups for named contacts in Bel, Agropur, and Valley Queen procurement. Don’t sit back and hope they find you.

- Fix any bulk tank cooling problems — recorded temps above 40°F at two hours are a red flag for most audits.

- Decide your minimum acceptable premium before you sit down. If Bel or a handler can’t clear your current blend by at least +$0.50/cwt on all lbs, your default assumption should be that staying in the pool is the safer play.

If You’re a 200‑Cow PA Farm in Schreiber’s Zone

This month:

- Pull DHIA and tighten your own bar: for Class II yogurt, aim for SCC below 150,000, with <100,000 as the “best shot at premiums” goal.

- If you’re at 180,000, that’s a 60–90 day barn‑level fix (dry‑cow program, milking routine, towels, prep).

- Ask your co‑op explicitly: “Do we have a direct supply agreement with Schreiber Shippensburg? If yes, how much of that volume comes from farms my size?”

Then set your walk‑away number:

- If your current blend is $15.05–$15.34/cwt, you probably need at least +$0.35–$0.50/cwt to justify a direct contract with tighter QA and termination clauses.

- On 2.3M lbs, that’s about $8,050–$11,500/year. A +$0.25/cwt offer (~$5,750) may not be worth the extra risk when you can often find similar gains by tightening components and SCC inside the pool.

If You’re a 400–600‑Cow Herd Stuck in “We Should Talk.”

This week:

- Call your actual processor contact — not the plant’s main line. If you don’t have a name and a number, that’s job one.

- Prepare a one‑page supply proposal:

- Average daily lbs.

- 12‑month quality stats.

- Hauling logistics.

- A specific offer like: “We can deliver 8 million lbs/year on a 3‑year agreement with 6‑month mutual termination.”

Then get a contract review. Janzen’s work on milk contracts points to “market conditions,” “quality failures,” and “termination for cause” clauses that quietly shift risk to the producer. A $500 legal review on a $2M/year contract is inexpensive risk insurance.

If you don’t have at least a term sheet by fall 2026, assume this specific Bel/Schreiber expansion wave is largely spoken for. You’ll still move milk. You may not be in the first row of premium seats.

What This Means for Your Operation

- Your contract lane matters more than your ZIP code. A 500‑cow herd inside Bel’s or Schreiber’s direct‑supply lane can see $58,500–$117,000/year from a $0.50–$1.00/cwt premium. A similar herd shipping through a pool might see $5,850–$17,550 — or nothing direct.

- Quality is the ticket, not the bonus. For higher‑value Class II and branded cheese, <150,000 SCC is the starting line, and <100,000 is the target for serious premium conversations. If you’re above that, your first processor‑math project is fixing cows and routines, not chasing contracts.

- The co‑op pool is a conscious trade, not a default. You give up some upside — maybe $29,000–$58,500/yearon a 500‑cow SD herd — in exchange for flexibility and regulatory payment protections. For small and mid‑size herds, that can be the smart play if you’re choosing it with eyes open.

- Expansion somewhere shifts leverage everywhere. When corridor states like SD keep landing plants and keeping milk “right‑priced” for processors, it slowly nudges leverage away from regions that aren’t seeing those investments. That shows up later as weaker over‑order premiums and tighter contract terms.

- 30‑day homework: Print your last 12 milk checks and DHIA summary. On one page, answer:

- What % of your milk currently routes to a plant with announced expansion?

- How many $/cwt above FMMO minimum are you actually getting?

- How much of that spread is due to components/quality vs. processor premiums?

If you can’t answer those three without making a call, that’s your signal that the real story isn’t in Bel’s or Schreiber’s press release — it’s in the fine print of your own milk check.

Key Takeaways

- If more than half your milk already ships to an expanding plant, you’re in the leverage band this article describes. Your decisions over the next 12–18 months are about terms and floors, not just having a home for your milk.

- If all of your milk is pooled and none of it routes to an expanding plant, you’re probably subsidizing someone else’s premium. Your paths are: get into a sourcing radius, get into a different pool, or squeeze more out of components and costs where you are.

- If you’re in that 300–500‑cow middle, you’re big enough that a good contract moves the needle, but small enough that you’re not the first call. Your edge is quality plus relationships — not waiting by the phone.

The Bottom Line

Whether you’re sitting in Franklin County or three states away, the practical question is simple: are you close enough — on paper and on quality — to be inside a processor’s premium lane, or are you quietly financing someone else’s expansion?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $212,000 Bulk Tank Lie Hitting Upper Midwest Dairies – Gain immediate margin by escaping the “test percentage” trap. This breakdown delivers a four-point playbook to rebuild culling and nutrition around the component pounds that actually drive your 2026 milk check, potentially recovering six figures in lost revenue.

- The $100 Springer Gap: Dairy Farm Relocation Is Moving America’s Milk Map to I-29 – Exposes the structural “gravity wells” reshaping the American milk map. You’ll gain a strategic framework to evaluate relocation versus adaptation, arming your operation with the long-term positioning required to survive as processing capacity concentrates into specific growth corridors.

- The $1750 Calf: Is Your 2026 Breeding Plan Leaving $800 a Head on the Table? – Reveals how to transform your breeding program into a high-margin revenue engine. This guide breaks down the precise genetic math needed to solve the heifer shortage while capturing massive calf premiums that finally offset unpredictable milk price volatility.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.