Your yogurt or formula plant adds ‘low‑risk’ ingredients after pasteurization. The last time it went wrong, it ended up at €134M. What’s your plan?

Executive Summary: A single “low‑risk” ingredient has just turned into a high‑stakes stress test for dairy’s whole value chain. Cereulide‑contaminated ARA oil from Cabio Biotech forced Nestlé, Danone, Lactalis, and Hochdorf into recalls across 60+ countries and pushed EFSA to set the first‑ever toxin limits for infant formula. For producers, the clearest warning sign is still the Fonterra–Danone case, where a precautionary recall that never sickened anyone ended in roughly €134 million in damages and a hit to earnings, even as the co‑op insisted the farmgate milk price was unchanged. This time, the contamination is real, regulators are reacting in real time, and processors face higher verification and compliance costs that can squeeze plant investment, premiums, and long‑term contract terms. Herds whose milk feeds yogurt, fortified milk, and formula lines are most exposed, because those products depend on post‑pasteurization ingredients like oils, cultures, and vitamin blends supplied by a small group of global players. The article lays out five concrete moves to cut ingredient and recall risk — plus specific questions you can take to your co‑op manager or field rep to understand how much of your milk cheque depends on what happens after pasteurization.

If you’re supplying milk to any plant that makes yogurt, specialty cheese, fortified fluid milk, or export‑grade powder, the 2025–26 infant formula crisis isn’t just someone else’s problem. It’s a live stress test of the ingredient supply chain your milk flows through — and the contracts your revenue depends on.

Since late November 2025, four major manufacturers — Nestlé, Danone, Lactalis, and Hochdorf — have pulled infant formula off shelves in more than 60 countries after cereulide, a heat‑stable toxin produced by certain Bacillus cereusstrains, was detected in ARA oil traced to Cabio Biotech, a Wuhan‑based supplier. The French Agriculture Ministry identified Cabio as the producer of the contaminated ARA oil, though the company has said it sent products for independent testing and plans to publish the results. Hochdorf Swiss Nutrition AG recalled 10,000 packs of a Bimbosan goat milk product on January 13, 2026, as a precautionary measure after confirming that ARA oil from the same supplier had been processed in small quantities at its facility.

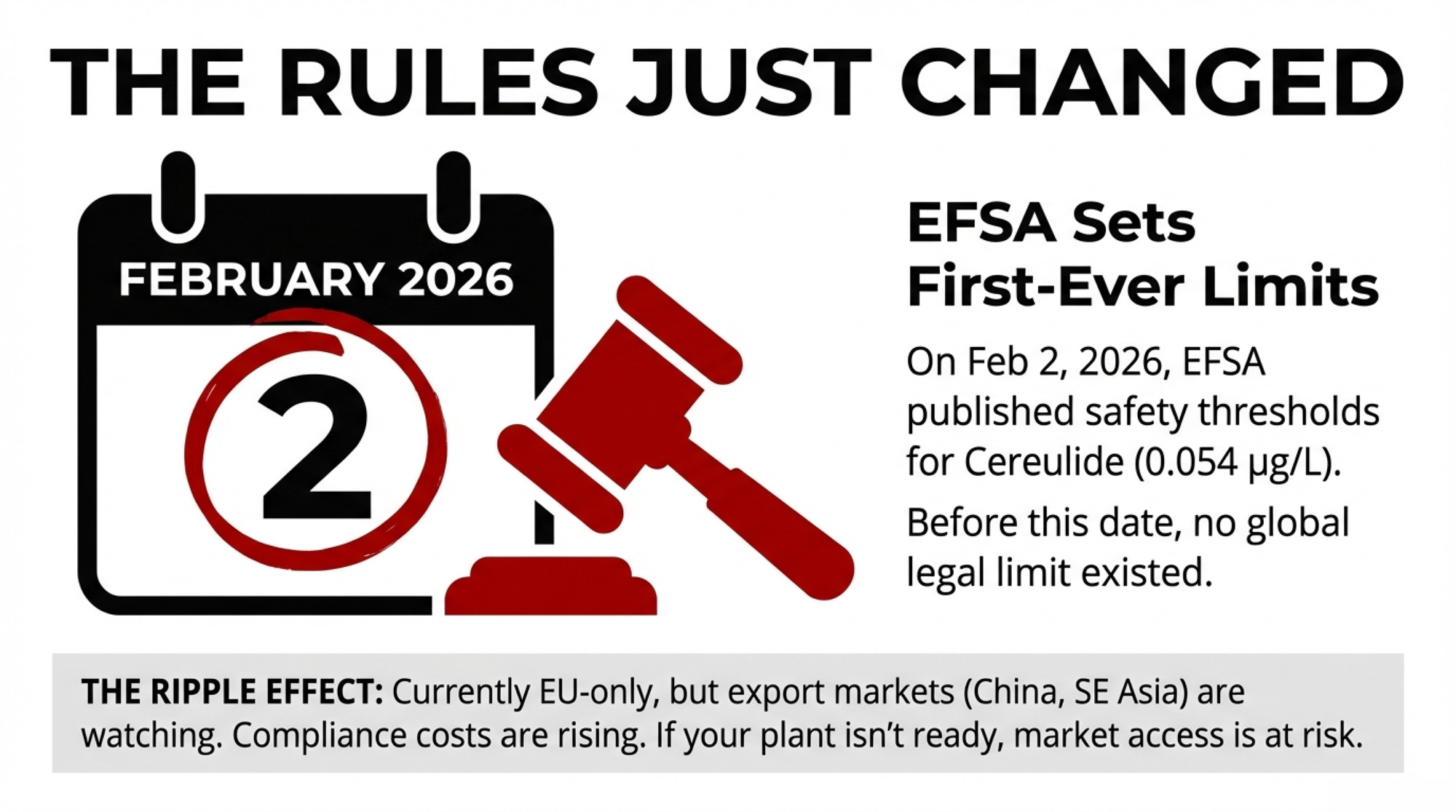

France has opened investigations into two infant deaths, though authorities have stressed that no causal link to the recalled formula has been scientifically established. Danone shares dropped as much as 12% intraday during the worst of the late‑January sell‑off, with cumulative declines of roughly 8–10% over the week the news broke. And on February 2, 2026, EFSA published the first‑ever safety thresholds for cereulide in infant formula — 0.054 μg/L for standard formula and 0.1 μg/L for follow‑on — because until that moment, no legal limit existed anywhere.

Nestlé said recalled batches represent less than 0.5% of its annual group sales. That sounds small — until you remember the Fonterra precedent.

The Fonterra Precedent: Recalls Cost Real Money

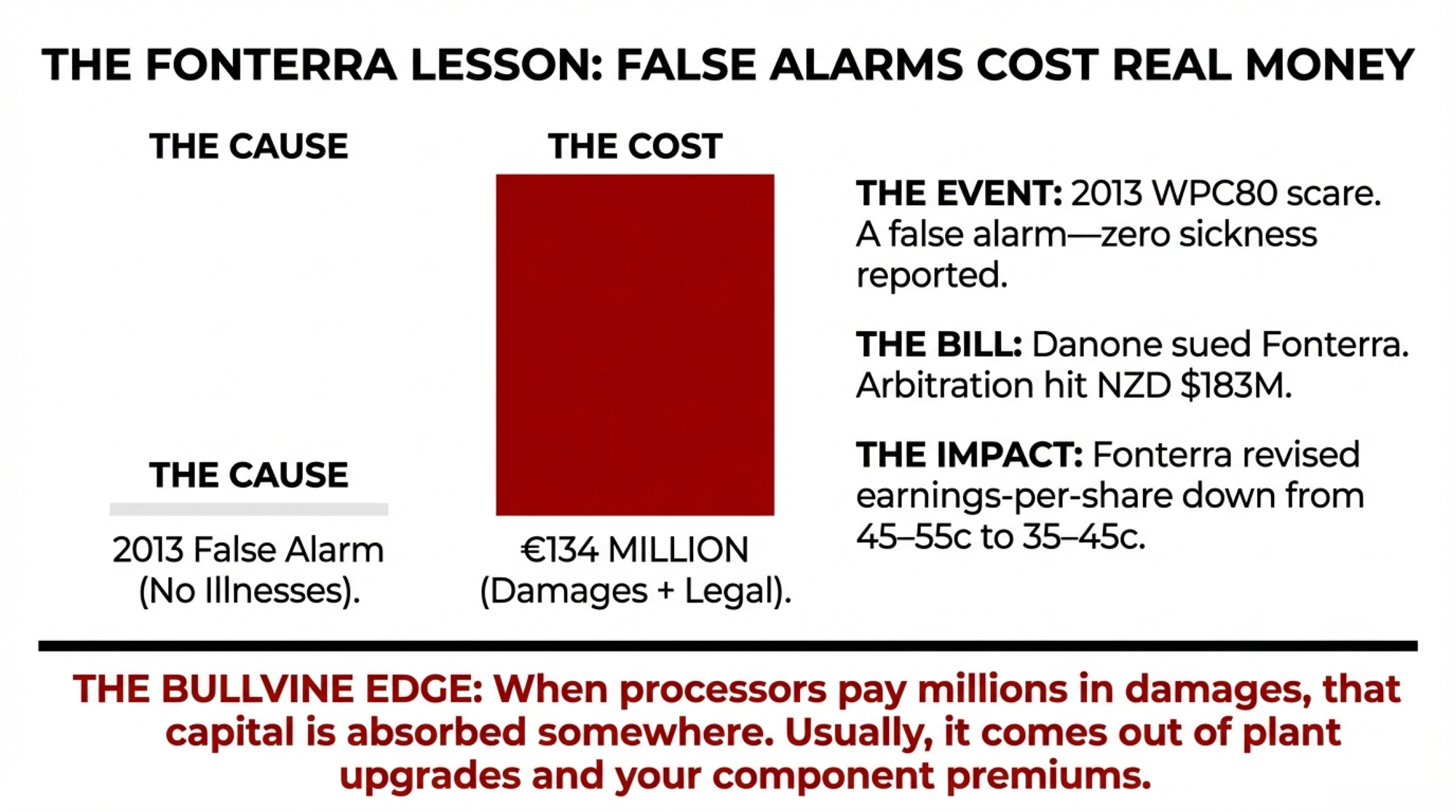

In August 2013, Fonterra issued a precautionary recall of its WPC80 whey protein concentrate due to suspected contamination with Clostridium botulinum. The fear turned out to be unfounded. No one got sick. But Danone, which used WPC80 in its Nutricia baby formula plants across Asia, pulled the product from eight markets and sued.

Danone sought hundreds of millions in damages, with claims reported at various stages ranging from €200 million to €370 million. The arbitration tribunal in Singapore ruled in November 2017 that Fonterra must pay NZD $183 millionin recall costs. Danone’s counsel, Simpson Thacher, later stated that the total, including interest and legal costs, reached €134 million — roughly US$165 million.

Fonterra told the market the decision had “no impact on the forecast Farmgate Milk Price”. But it also revised its FY17/18 earnings‑per‑share forecast downward — from 45–55 cents to 35–45 cents — partly citing the arbitration. That capital is absorbed somewhere. Plant upgrades deferred. Component premiums that could have been more competitive.

CEO Theo Spierings said the co‑op was “disappointed that the arbitration tribunal did not fully recognise the terms of our supply agreement with Danone, including the agreed limitations of liability”.

That was for a scare that turned out to be nothing. The current cereulide situation involves real toxin detections, confirmed product contamination at multiple manufacturers, active government investigations, and a named supplier — Cabio Biotech — at the center of a root‑cause analysis still underway.

Why Cereulide Sits Outside Most HACCP Plans

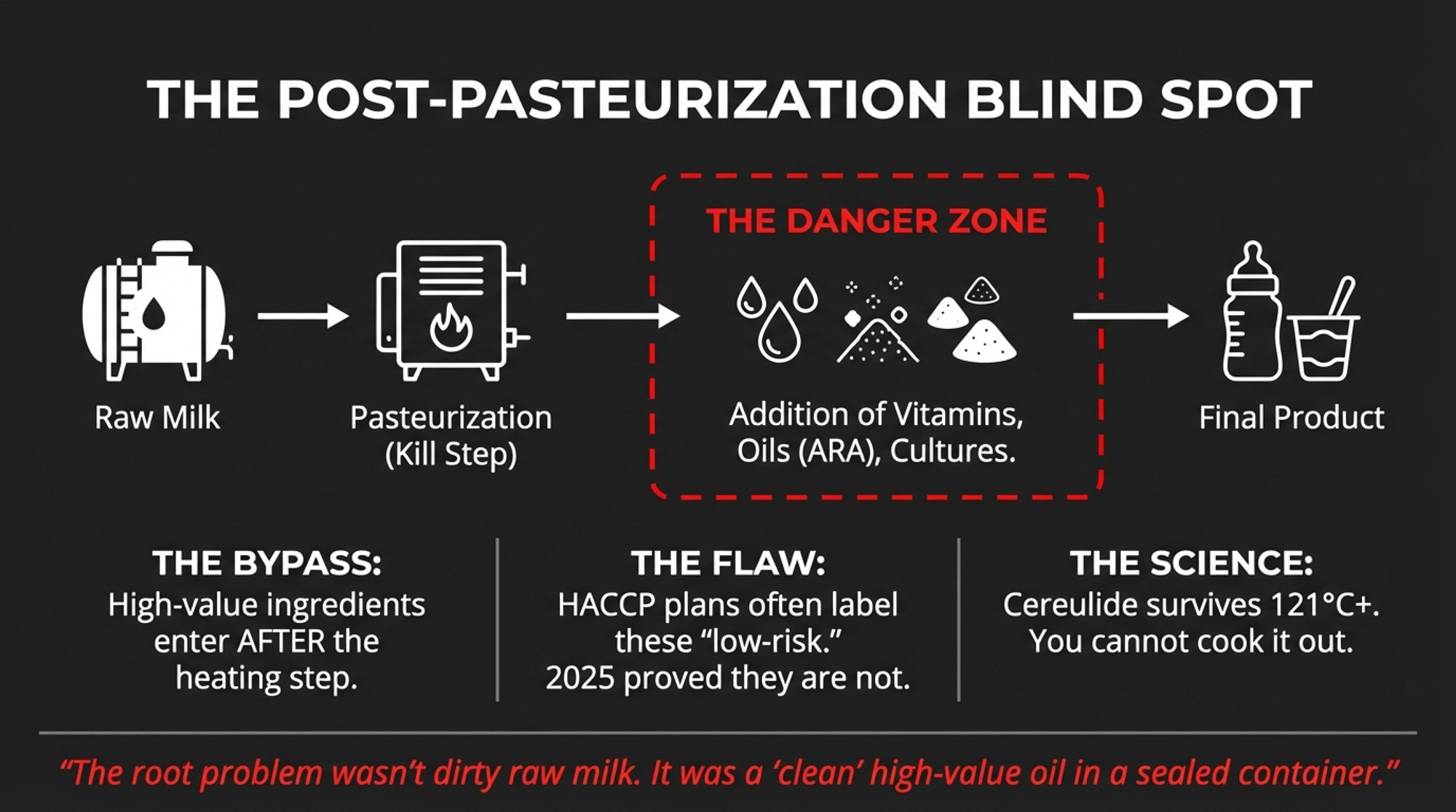

The root problem wasn’t dirty raw milk or a failed pasteurizer. It was a “clean,” high‑value oil ingredient in sealed containers, classified as low‑risk in standard HACCP protocols, and added after the main heat step. Industry experts are already recommending that ARA oil be upgraded from “low‑risk” to “high‑risk” to intensify scrutiny.

Cereulide is extremely heat‑stable. A 2024 technical brief from the Food Research Institute at the University of Wisconsin–Madison documents that it can withstand temperatures around 121–126°C in oily matrices — well above standard pasteurization and many UHT processes. A 2021 Applied and Environmental Microbiology study by Walser and colleagues showed that when cow’s milk fat content rose from 0.5% to 50%, the proportion of cereulide in the lipid phase climbed from 13.3% to 78.6%. It concentrates in fat, and there’s no practical way to remove it once it’s there.

Professor Monika Ehling‑Schulz of the University of Vienna, who co‑developed the ISO detection method, shared that the core problem is the absence of established reference doses — “Nobody knows what this ‘low’ concentration actually means, because the limit has not been defined yet”. Marcel Zwietering, professor of food microbiology at Wageningen University, told the same outlet that the most likely scenario is B. cereus growing and producing cereulide during or before oil production, not in the oil itself — meaning the contamination occurs upstream and hitches a ride into the dairy plant.

EFSA’s new acute reference dose of 0.014 μg/kg body weight for infants is the first regulatory benchmark anywhere. But it applies only within the EU, and only to infant formula for now. Cereulide remains “largely unregulated outside the bloc”. No equivalent limits exist for yogurt, enriched milk, or any other dairy category in any market.

Your Plant’s Post‑Pasteurization Blind Spot

Bring this into your plant. Whether it’s a yogurt operation in Wisconsin, a drinking‑yogurt line in Ontario, a Lactalis UHT facility in Brazil, an enriched‑milk plant in Western Europe, or a powder site on New Zealand’s South Island, the pattern looks the same.

Raw milk gets standardized, pasteurized, and cooled. Then a stack of ingredients is added after the kill step: starter cultures, probiotic blends, vitamin premixes, microencapsulated oils such as DHA and ARA, fruit preparations, flavours, stabilizers, and bioprotective cultures. Every one of those additions jumps past pasteurization. And most HACCP plans classify them as low‑risk — exactly how ARA oil was classified before this crisis blew up.

| Ingredient category | Typical use in dairy lines | Contamination impact if compromised | Overall recall & contract risk* |

|---|---|---|---|

| Microencapsulated oils (ARA/DHA) | Infant formula, enriched milk, yogurt drinks | Systemic recall across brands and countries | Very High |

| Vitamin & mineral premixes | Fortified milk, pediatric formulas | Wide lot‑to‑lot spread, hard to detect in plant | High |

| Starter & probiotic cultures | Yogurt, cheese, fermented drinks | Product spoilage, off‑flavours, some safety risk | Medium |

| Fruit preparations & flavours | Yogurt, desserts, drinking yogurts | Localized recalls, limited to flavoured SKUs | Low–Medium |

One contaminated ingredient from one supplier — Cabio Biotech — cascaded through four multinational manufacturers and 60+ countries in weeks. If your plant’s cultured or fortified lines depend on similar post‑pasteurization ingredients sourced from the same small pool of global suppliers, you’re exposed to the same structural risk across different product categories. That’s true whether your milk ships to a Fonterra site in Canterbury or a Conaprole plant in Uruguay.

What EFSA’s Outbreak Data Add to the Picture

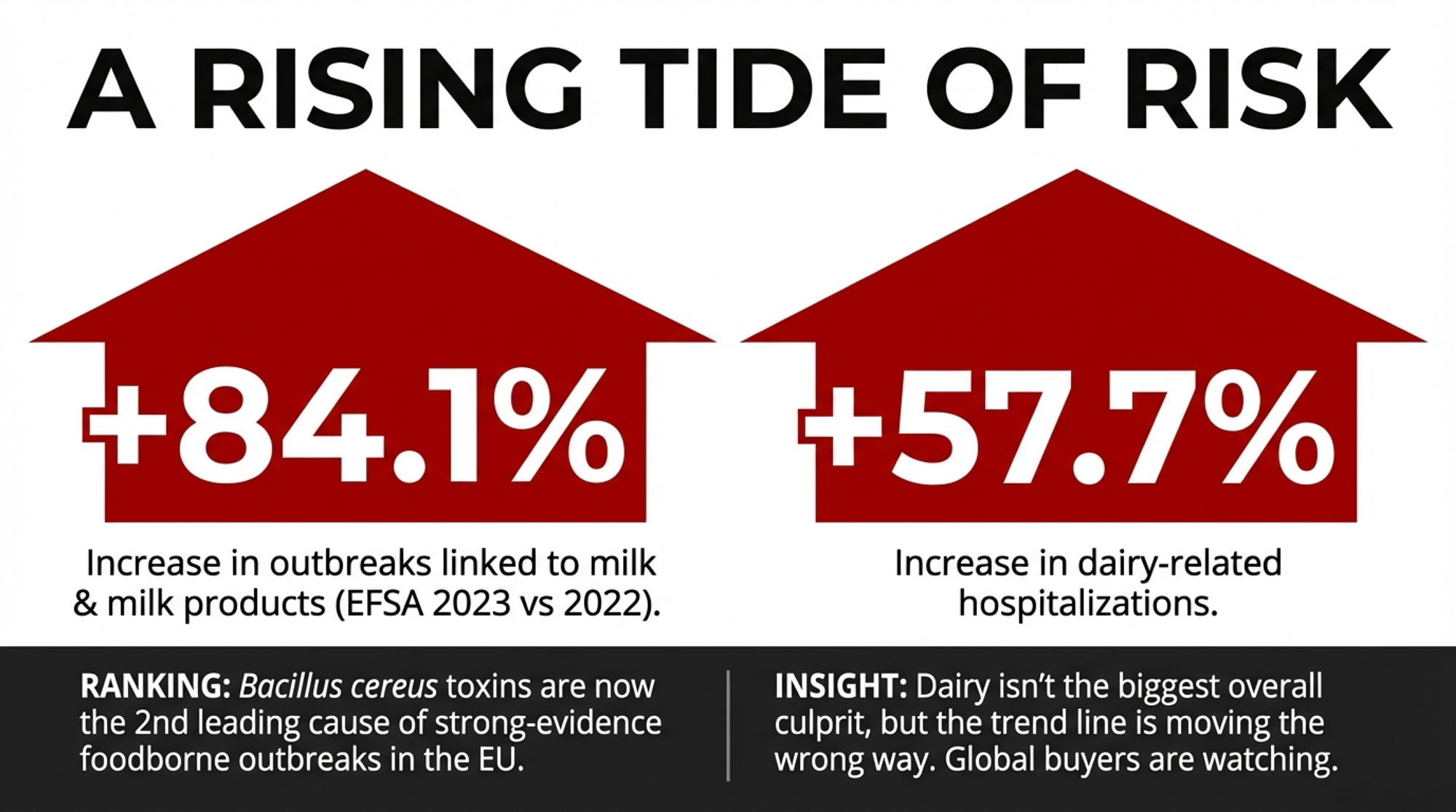

There’s a broader signal worth watching. EFSA’s 2023 foodborne outbreak report showed that cases linked to the “milk and milk products” food group increased by 392 compared to 2022 — an 84.1% jump. Hospitalizations rose by 30, up 57.7% year‑over‑year.

One large norovirus outbreak in Germany involving dairy desserts drove most of that spike — 538 of 858 strong‑evidence cases in this food group. Dairy was far from the biggest overall source of foodborne illness in 2023; multi‑ingredient foods, meat, eggs, and fish still dominated. But Bacillus cereus toxins ranked second among the leading causes of strong‑evidence foodborne outbreaks across all EU foods that year. And EU outbreak numbers influence how global buyers and retailers think about dairy risk everywhere — including your export markets.

Dairy may not be the biggest culprit in the outbreak data. But the trend line is moving in the wrong direction, which makes the following steps table-stakes for any operation shipping into high‑value or export‑facing lines.

5 Moves to Cut Dairy Ingredient and Recall Risk

You’re not going to solve global toxicology from the parlour. But there are concrete steps that shift the math.

- Reclassify post‑pasteurization ingredients as high‑risk by default. If an ingredient is fermentation‑derived and added after the last heat step, it belongs in your hazard analysis as a distinct, high‑scrutiny line item — not buried under “low‑risk dry ingredients.” Industry experts are already recommending this for ARA oil specifically.

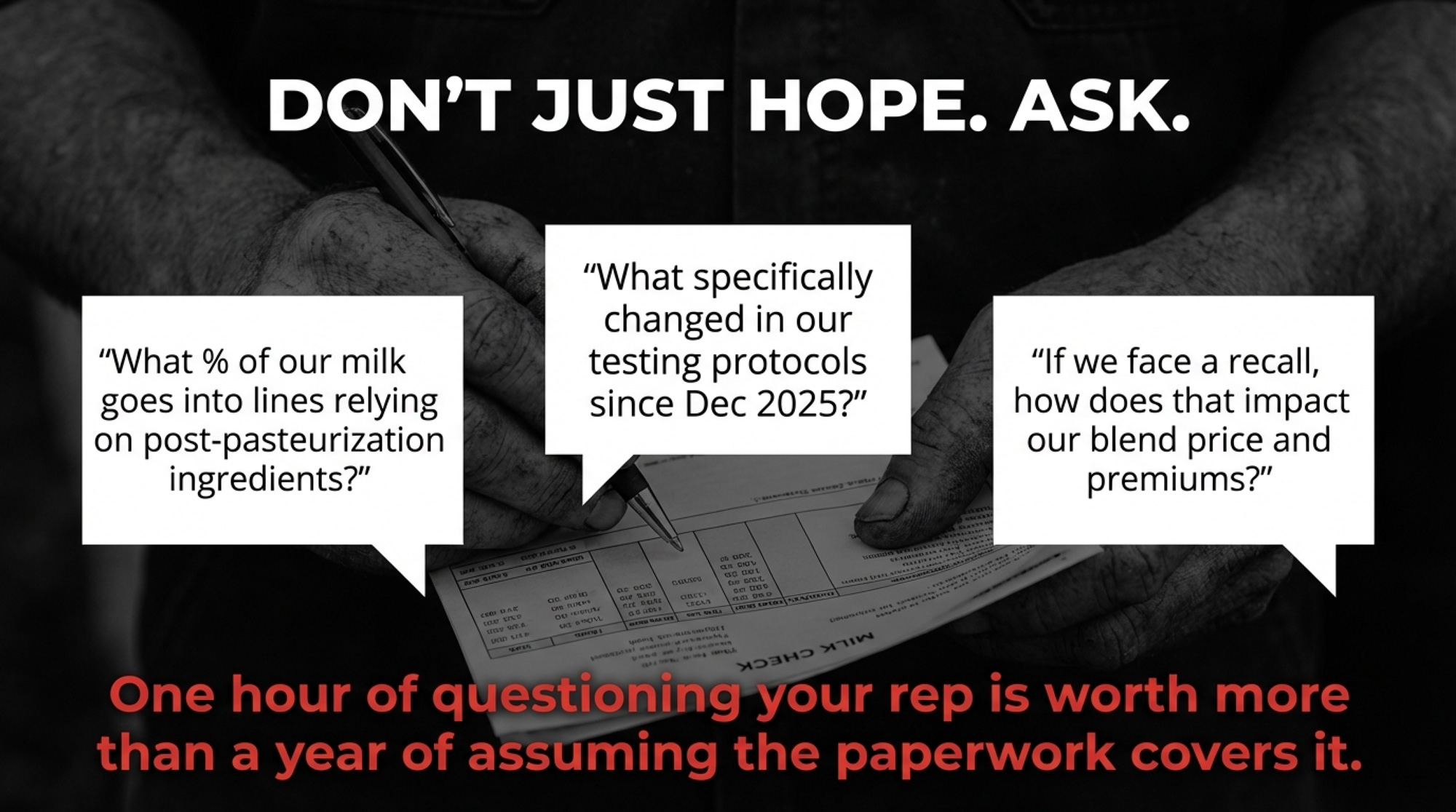

- Ask your suppliers harder questions. “Are you GFSI‑certified?” is table stakes. What matters now: “Do you test finished lots for emetic B. cereus or cereulide? Which methods? What changed in your program after the 2025–26 recalls?” If you’re on a co‑op board, this is a fair question for your plant management team.

- Write change‑notification clauses into specs and contracts. Require suppliers to notify you before shifting production to a different facility, changing a critical raw‑material source, or receiving a regulatory finding. That won’t prevent contamination, but it gives you a window to ratchet up verification before a lot of high‑value milk gets committed.

- Build in independent verification testing where margins justify it. Certificates of analysis show you what the supplier tested for. For post‑pasteurization ingredients that support a big share of your premium lines, periodic independent testing — especially when onboarding a new supplier — adds a layer that COAs don’t. The FDA’s October 2024 BAM method for quantitative cereulide analysis gives labs a standardized protocol.

- Avoid putting all your ingredient risk on one supplier. This crisis traces to a single ARA oil supplier — Cabio Biotech — that fed four multinational manufacturers. Qualifying at least two sources for each critical post‑pasteurization ingredient costs some volume discount and logistics simplicity — but eliminates the single point of failure. Most serious herds already think this way about forage and semen. Apply the same logic upstream.

What This Means for Your Operation

- Ask your co‑op manager, field rep, or dairy company liaison — whatever the title is in your market — one question first: “What proportion of our milk goes into lines that rely on ingredients added after pasteurization?” Whether you’re supplying a processor in Ontario, shipping into a facility in southern Brazil, or delivering to a Fonterra collection point in the Waikato, this is the starting point. If you don’t know the answer, that’s the first gap to close.

- Ask what changed post‑recall: “Since the cereulide infant formula situation, what concrete changes have we made in how we qualify and monitor ingredient suppliers?” If the answer is “nothing yet,” that’s a signal — and it applies equally to a plant in Idaho and one in Minas Gerais or Victoria.

- Understand your contract exposure. Fonterra’s arbitration payout — ultimately reaching an estimated €134 million, including interest and costs — stemmed from an unfounded scare. If your processor absorbs a real recall, what happens to plant investment, premium payments, and long‑term contract terms? Run the question out loud at your next producer meeting — whether that’s a DFC town hall, a Fonterra supplier session, or a co‑op AGM in Latin America.

- If your milk mainly feeds commodity powder and cheddar, the exposure is different but not zero. Plants with large value‑added sidelines can see margin pressure from those lines spill over into the commodity pool. Ask: “If our premium lines paused for a quarter, what would that do to our blend price?”

- Watch the regulatory calendar. EFSA’s new cereulide thresholds are EU‑only and infant‑formula‑only for now. But when EU regulators move, export markets take notice — including the buyers that Argentina, Uruguay, New Zealand, and Australia depend on in North Africa, Southeast Asia, and China. If similar limits expand to other dairy categories, compliance and testing costs fall on processors and, eventually, on milk prices. Worth tracking wherever you farm.

| Herd profile & milk destination | Share of milk in value‑added lines (%) | Baseline blend price (CAD/hl) | Estimated impact on blend price if premium lines pause 1 quarter (CAD/hl) | Margin impact per cow per quarter (CAD, 40 L/cow/day) |

|---|---|---|---|---|

| High‑value herd – yogurt, formula, enriched milk heavy | 70 | 90 | ‑7.50 | ‑225 |

| Mixed herd – cheese, powder, some cultured & fortified lines | 40 | 80 | ‑3.00 | ‑90 |

| Commodity‑leaning herd – powder & cheddar focus | 15 | 72 | ‑1.00 | ‑30 |

| Export‑exposed herd – strong infant formula & UHT linkages | 60 | 88 | ‑6.00 | ‑180 |

Key Takeaways

- The 2025–26 infant formula crisis exposed a structural gap — post‑pasteurization ingredients classified as low‑risk — that exists in yogurt, enriched milk, and cultured‑product plants through which your milk flows. ARA oil from one supplier, Cabio Biotech, cascaded through four manufacturers and 60+ countries.

- The Fonterra–Danone precedent shows the real financial cost: an estimated €134 million in total recall damages from a scare that turned out to be nothing. The current situation involves real contamination, real regulatory action, and active investigations.

- EFSA’s February 2, 2026, cereulide thresholds are the first legal benchmark anywhere in the world. More categories and more jurisdictions may follow. Your processor’s readiness for that shift affects your pay price, your premiums, and your long‑term contract stability.

- The single most useful thing you can do right now: find out what share of your milk goes into lines that depend on post‑pasteurization ingredients, and ask what your plant changed in its ingredient qualification program since December 2025.

The Bottom Line

The producers who come through shocks like this in decent shape are the ones who asked the uncomfortable questions before the answers showed up on a recall notice. That’s true on a 200‑cow operation in Quebec, a 2,000‑cow dry lot in the San Joaquin Valley, a pastoral herd in the Waikato, or a growing operation in Buenos Aires province. One hour at the kitchen table with your milk cheque and a few pointed questions is worth more than another year of assuming the paperwork has it covered.

Learn More

- The 3.5-Hour Cow Rule: How Time Out of the Pen Quietly Erases Over $300,000 from Some Milk Cheques – Capture a massive margin boost by mastering the strict 3.5-hour rule for cow handling. This operational guide exposes how hidden rest-time leaks quietly strip six-figure revenue from your cheque, providing immediate methods to protect your farm’s bottom line.

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – Secure your 2026 survival by decoding the structural reset currently upending traditional dairy economics. This strategic analysis arms you with the math to navigate beef-on-dairy traps and replacement shortages that threaten your long-term contract stability and equity.

- Lab-Grown Milk Has Arrived: The Dairy Innovation Farmers Can’t Ignore – Lead the next dairy revolution by understanding the “molecularly identical” threat and opportunity of lab-grown whole milk. This disruptor report reveals how mammalian cell technology is moving toward market pilots, reshaping global competition and redefining future dairy value.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.