6% calf mortality = $350K annual loss. New genomics launching April 2026. Your cost? Maybe nothing if you’re already genomic testing, up to $40K if starting fresh.

You know that sinking feeling when you walk into the calf barn and spot another one with scours? And these days—with replacement heifers running $3,000 to $4,000 according to the latest USDA market reports—every sick calf feels like watching money evaporate.

Here’s what’s got my attention: we’re still losing about 6% of our calves before weaning, at least according to the last comprehensive USDA survey from 2014. Canadian research from just a couple years back shows similar numbers, which tells me we haven’t made much progress despite all our management improvements. It’s frustrating, honestly.

So when I heard about the April 2026 launch of national genomic evaluations for calf health traits at the CDCB meeting on October 1st in Rosemont, I had to dig deeper. The Council on Dairy Cattle Breeding and USDA’s genetics lab have been working on this for years, and they’re targeting exactly what’s killing our calves—scours and respiratory disease. Those two culprits are responsible for about 75% of our pre-weaning deaths, based on research published in the Journal of Dairy Science (Urie et al., 2018).

What I’ve found is that for many of us running typical 1,000-cow operations, the economics of calf losses are worse than we probably realize. When you do the math—and I’ll walk through this with you—we’re looking at significant potential here. But there’s also a lot to consider before jumping in.

Click the link to view the presentation.

Genetic Tools for Healthier Calves

John Cole, Ph.D., CDCB Chief Research and Development Officer

Slides

What They’re Actually Measuring (And Why It Matters)

Let me be clear about something: these aren’t treatment protocols or management recommendations we’re talking about. These are genetic predictions—basically, which bloodlines tend to produce calves that stay healthier.

The data foundation is pretty impressive. CDCB researchers analyzed over 200,000 diarrhea records and nearly 700,000 respiratory disease records spanning the last decade. That’s a lot of sick calves, unfortunately. What’s interesting is how the breeds compare—Holstein calves made up about 80% of the dataset, with Jerseys at 17%. And here’s something worth noting: Jersey calves in this dataset showed slightly higher disease rates. We’re talking 17.8% for scours and 23.7% for respiratory disease, compared to 13.5% and 14.5% for Holsteins.

Now, the heritability numbers—2.6 for diarrhea resistance and 2.2 for respiratory disease resistance—those might seem pretty low if you’re used to seeing 30 or 40 percent for production traits. But as Dr. John Cole from CDCB pointed out at the October meeting, you can’t really compare them that way. He basically said, “Don’t worry about the lower heritability—it’s about getting started and making progress where we can.”

What really piques my interest, though, is that these calf health traits appear to be genetically independent from the other stuff we select for. The correlations with production, fertility, and longevity are hovering near zero based on the preliminary research. If that holds up—and it’s still early days—we might not face those painful trade-offs we’ve dealt with before. You know, like what happened with milk yield and fertility over the past few decades.

Let’s Talk Real Economics (The Cost Depends on You)

So here’s where it gets interesting—and more nuanced than you might think. Based on current market conditions and what we’ve seen in other countries, your actual investment could range from zero to $40,000.

First, the losses we’re all facing. For a typical 1,000-cow dairy, you’re probably losing around 54 calves annually at current mortality rates. That’s roughly $189,000 just in replacement value at today’s prices. Then you’ve got what you already invested in those calves before they died—feed, labor, vet care—probably another $15,000 to $20,000 based on typical rearing costs through weaning.

And that’s just the ones that die.

The survivors that got sick? They’re costing you too. Research from the University of Guelph (Winder et al., 2022, Journal of Dairy Science) shows these calves produce significantly less milk in their first lactation—we’re talking over 700 kilograms less. Plus, they tend to calve later and leave the herd earlier. Add it all up, and the total annual hit from calf health problems could easily exceed $350,000 for a 1,000-cow operation.

Your Investment Options – Quick Cost Breakdown

| Your Current Situation | Your Cost for Calf Health Evaluations |

| Already genomic testing | $0 (Free on existing tests) |

| Never tested – heifers only | $18,000 (450 animals) |

| Never tested – full herd | $40,000 (1,000 animals) |

| Gradual approach | $4,000-6,000 per year |

Now, here’s where it gets interesting on the investment side. Your costs depend entirely on your current genomic testing status:

If you’re already genomic testing: Based on what happened in Canada, Australia, and other countries when new traits were added, you’ll likely get these calf health evaluations for free on all previously tested animals. That’s potentially thousands of animals with zero additional cost. You’d only pay for new animals going forward, and even then, the per-test cost shouldn’t increase.

If you’ve never genomic tested: That’s where the $40,000 figure comes from—testing your entire cow herd plus replacement heifers (roughly $40 per test for 1,000 animals), plus the premium for genetically superior semen (maybe $10-15 more per unit), and getting your data systems up to speed.

The smart middle ground: Start with just your replacement heifers. That’s maybe 450 animals at $40 each—$18,000instead of $40,000. You’ll still get valuable information for breeding decisions while keeping costs manageable.

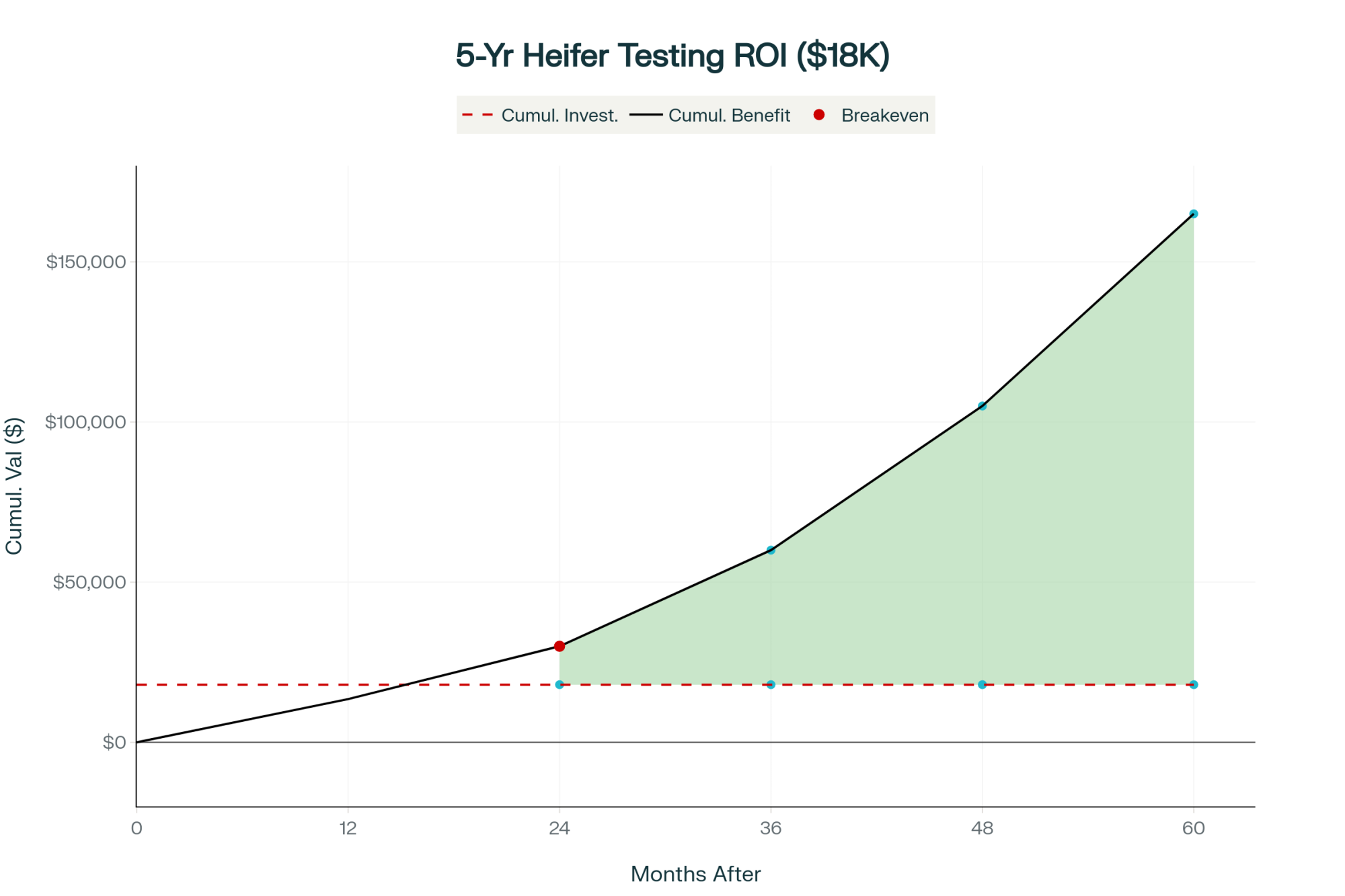

Here’s the reality check, though—and this is important—the first-year returns are modest regardless of your testing approach. Maybe $12,000 to $15,000 in reduced mortality and morbidity. You’re not breaking even until somewhere between 24 and 30 months if everything goes right. By year five, though, the modeling suggests annual benefits of around $60,000 with a pretty decent return on investment.

But—and this is a big but—these projections assume you’re already doing a decent job with management. If you’re at 3-4% mortality through solid protocols, genetic improvement might push you toward that elite 1-2% range. If you’re struggling at 8-10% mortality? Fix your management first. The genetics won’t overcome broken systems.

Smart Entry Strategies (You Don’t Need to Go All-In)

Here’s what many producers don’t realize: you have options beyond the all-or-nothing approach.

Option 1: The Free Ride

If you’ve been genomic testing for years, you’re sitting pretty. When April 2026 rolls around, all your historical data should automatically get calf health evaluations. No additional investment needed.

Option 2: Heifer-Only Testing

Never tested before? Start with your 450 replacement heifers. At $40 each, that’s $18,000—less than half the full-herd cost. You’ll get genetic information on your future cows and can make smarter sire selection decisions immediately.

Option 3: The Gradual Build

Test 100-150 animals per year. Spread the cost over 3-4 years while you validate whether the technology works in your herd. This approach costs $4,000-6,000 annually—much more manageable.

Option 4: Bulls Only

Just focus on selecting better sires using the published evaluations. Zero testing cost, though you won’t know which of your cows to breed to which bulls for optimal results.

The Zoetis Factor (Competition Already Exists)

Here’s something many producers don’t realize: we’re not waiting in a vacuum for CDCB’s launch. Zoetis has been selling wellness trait evaluations since 2016. Nearly a decade head start.

Their system draws from hundreds of thousands of health records and genotyped animals, based on research they’ve published in JDS (Vukasinovic et al., 2019). And from what I’m hearing from producers who use it—especially those larger operations in California and the upper Midwest—it works reasonably well. The wellness traits are already integrated into most AI stud catalogs, and the genomic prediction reliabilities are pretty solid for young animals.

Rosy Lane Holsteins 12-Month Study

| Health Metric | Bottom 25% Genetics | Top 25% Genetics | Improvement |

| Scours Cases (per 100 calves) | 28 cases | 14 cases | 50% reduction |

| Pneumonia Cases (per 100 calves) | 44 cases | 30 cases | 32% reduction |

| Treatment Costs (per 100 calves) | $4,200 | $2,100 | $2,100 saved |

| Overall Calf Mortality | 6.5% | 4.0% | 38% reduction |

Based on Zoetis Calf Wellness Index data (similar methodology to CDCB)

So, where might CDCB have advantages? Well, they’re drawing from a broader population through the national database—we’re talking millions of genotypes from over 15,000 DHI herds. The methodology is transparent and peer-reviewed. And if you’re already on DHI, there’s no premium pricing.

Something that’s puzzling folks is the difference in heritability. Zoetis reports about 4.5 for scours, while CDCB shows 2.6. That’s not necessarily a contradiction—different statistical approaches, different populations, different ways of measuring. Both might work fine; they’re just looking through different lenses.

My guess? Both systems will coexist. Smart producers will probably compare them once CDCB launches. If the bull rankings correlate strongly, they’re telling you the same thing. If not… well, that’s when it gets interesting.

The Data Challenge Nobody Wants to Talk About

Here’s what really concerns me, and it’s barely mentioned: only about 12% of dairy farms systematically record calf health data, according to Canadian research (Renaud et al., 2023) that probably reflects our situation too. And those 12%? They tend to be the larger, better-managed operations that already have lower mortality.

This creates what’s called selection bias. The genetic evaluations end up being optimized for farms that look like the ones contributing data. So if you’re running a large operation with dedicated calf managers and automated systems, these predictions will probably work great. But what about smaller operations with different management styles? Or those grazing operations in Vermont compared to the freestall operations in Idaho?

What farmers are finding in states like Iowa and South Dakota is that their management systems—often smaller herds with different housing approaches—might not match what’s in the database. That’s a real concern.

What’s more, you need to actively authorize your Dairy Records Processing Center to transmit health data to CDCB using Format 6. No permission, no data contribution. And if farms like yours aren’t contributing data, the evaluations might not predict well in your environment. It’s a bit of a catch-22.

From conversations with DRPC folks, participation is growing but still lower than ideal. We need more farms sharing data before these evaluations become truly representative of the industry as a whole.

How to Know If It’s Actually Working

If you’re thinking about jumping in, you need concrete checkpoints. Here’s what I’d be watching:

Around 12-18 months after you start (late 2027), compare disease rates between calves from your top genetic sires versus your average ones. You should see the better genetics showing noticeably lower disease—maybe 20-30% lower—once you’ve got enough calves to compare. If you don’t see that difference, the evaluations aren’t predicting right in your barn.

At 24-30 months, check your financials. If you’re still deep in the red, it might be time to reconsider. Also, watch for unexpected issues—are those “healthier” calves growing slower? Birth weights creeping up? I’ve seen this with other traits where unexpected correlations pop up after a few generations.

By 36-42 months, your first heifers from high-health sires are entering the milking string. If their production is way below genetic predictions or fertility is tanking, you might be seeing those dreaded antagonistic correlations emerging.

The kicker is that all this requires obsessive record keeping. If you can’t document every health event consistently—including the healthy calves—you’ll never know if it’s working. And let’s be honest, that’s a challenge for a lot of us.

A Practical Approach to Implementation

Based on what I’ve learned from producers who’ve adopted genomics for other traits, here’s what makes sense:

Right now, through April 2026, take an honest look at your situation. Can your team consistently record health data? Is management or genetics your bigger constraint? Either way, start recording health data now—you’ll need that baseline. And call your DRPC to get the Format 6 data transmission authorized. Ask specifically about fields like “calf health event,” “treatment date,” and “disease code”—those are the critical ones.

If you’re already genomic testing: Relax. You’re likely getting these evaluations for free on all your tested animals. Focus on understanding how to use the new information effectively.

If you’ve never tested: Consider starting with just your heifers. It’s a $18,000 investment instead of $40,000, and you’ll learn whether this technology works for you before going all-in.

When April 2026 rolls around, don’t go all-in with your breeding decisions either. Start with maybe 20-30% of your breedings using top calf health sires. Keep detailed records. See if performance matches predictions. And stick with proven bulls with decent reliabilities—this isn’t the time to gamble on unproven young sires with reliabilities under 50%.

By the end of 2027, you’ll have enough data to make a decision. Seeing good improvement and approaching breakeven? Expand to more of your breedings. Mixed results? Stay conservative. No improvement or weird trade-offs? Maybe redirect that investment to management improvements.

The Bigger Industry Picture

What we’re seeing goes beyond just another trait to select for. Based on how genetic trends have evolved since genomic selection became available in 2009, this technology might widen the gap between large and small operations.

Research tracking genetic progress over the past couple of decades shows that large herds (over 500 cows) have achieved significantly faster improvement than small herds (under 100 cows) since the advent of genomics. The genetic merit gap has actually widened, not narrowed.

The same dynamics will probably play out here. Operations in Wisconsin’s Central Sands region, with their large-scale calf-raising facilities, will likely benefit more than small grazing operations in Vermont’s Northeast Kingdom. Down in Texas and New Mexico, those big dairies with automated calf feeding systems are positioned differently than the traditional tie-stall barns still common in parts of Pennsylvania and New York’s North Country.

Looking at this trend more broadly, what’s happening in the Midwest—particularly in states like Michigan and Ohio, where you’ve got a mix of farm sizes—might be most telling. The mid-sized operations (300-800 cows) are the ones really wrestling with whether this technology makes sense for them.

It’s not that the technology is biased—it’s that successful implementation requires resources that aren’t equally distributed. But here’s the silver lining: if you’re already genomic testing, you’re not at a resource disadvantage for this new trait.

Three Key Questions for Your DRPC

Before making any decisions, here’s what to ask at your next DRPC meeting:

First, what percentage of herds in your region are contributing health data? If it’s below 20%, the evaluations might not accurately reflect your management system.

Second, can they show you how CDCB and Zoetis rankings compare for bulls you’re currently using? This tells you whether the systems agree or if you’re looking at conflicting information.

Third, what’s the actual process and cost for setting up data transmission from your herd management software? Some systems need upgrades—better to know upfront. DairyComp 305 users might need different modules than PCDART folks, for instance.

And here’s the new critical question: If I’m already genomic testing, will my historical tests automatically get calf health evaluations in April 2026? Get this in writing.

The Bottom Line for Your Operation

After digging through all this, here’s my take:

If your mortality is over 5%, focus on management first. Whether genomic testing costs you nothing or $40,000, it won’t fix broken protocols.

If you’re at 3-4% mortality, you’re in the sweet spot. If you’re already genomic testing, you’ll get free evaluations to work with. If not, start with heifer testing at $18,000 to validate the technology.

If you’re already under 3%, you’re bumping against biological limits. These evaluations might be exactly what you need to get to that elite level—and if you’re already testing, it’s free value.

What concerns me is how much your success depends on other producers’ data. It’s a collective challenge that individual farms can’t solve alone. And remember—genetic selection and good management work together. They’re not either/or propositions.

At current replacement prices, we can’t afford historical mortality rates. These genomic tools offer one path forward, but only for operations positioned to use them effectively. The technology is real. Whether it revolutionizes your operation depends on matching these tools to your specific situation—and your cost of entry might be much lower than you think.

The economics are compelling if you get it right. But genomic selection can create problems as easily as it solves them if applied incorrectly. Take your time, validate carefully, and don’t let anyone convince you there’s a one-size-fits-all solution to something as complex as calf health.

What’s your take on all this? Are you planning to jump in early, or taking more of a wait-and-see approach? I’d be interested to hear what other producers are thinking as we head toward this launch. Send your thoughts to editorial@thebullvine.com—these conversations help us all make better decisions.

Key Takeaways

- Your mortality rate dictates your path: Under 3% = invest in genomics | 3-4% = test cautiously | Over 5% = fix management first—any investment is wasted on broken basics

- The real cost varies wildly: Free for existing genomic testers based on international precedent | $18,000 for heifer-only testing | Up to $40,000 for full-herd startup

- Data bias could sink you: Only 12% of farms (mostly large operations) contribute health data, meaning these predictions might fail in your specific environment

- Start smart, not big: Test heifers only ($18,000) or use free evaluations on existing tests, validate for 18 months, then decide whether to expand

Executive Summary:

Your sick calves drain $350,000 annually, but April 2026’s genomic fix isn’t a silver bullet. CDCB’s new calf health evaluations could cost you nothing if you’re already genomic testing (based on precedent from other countries), or up to $40,000 if starting from scratch—farms above 5% mortality should invest in basics first regardless. The genetics target scours and respiratory disease with modest heritabilities of 2.6 percent and 2.2 percent, meaning gradual multi-generational progress, not instant transformation. Here’s the catch: only 12% of farms share health data, so predictions favor large operations and may not work for your specific system. With Zoetis already dominating this space since 2016, producers must choose between competing evaluations while validating what actually works in their barns. Bottom line: this technology amplifies excellent management but won’t salvage broken protocols—know which category you’re in before writing any check.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- The Ultimate Colostrum Management Checklist: Are You Missing These 5 Critical Steps? – This article provides a critical hands-on guide for perfecting your ‘day one’ colostrum protocols. It delivers actionable strategies for building the immunity that genetics can only supplement, directly addressing the “management first” advice for reducing early calf mortality.

- Heifer Economics in 2025: Are You Raising a $3,000 Problem or a $5,000 Asset? – This piece breaks down the volatile economics of replacement heifers mentioned in the article. It provides a strategic framework for using your current genomic data to decide which animals are worth the $3,500 investment, ensuring you’re not just raising healthier calves, but profitable ones.

- Beyond the Clipboard: How Automated Calf Monitoring Systems Are Finally Paying Off – This report spotlights the technology that solves the “12% data problem” mentioned in the article. It demonstrates how automated monitoring and smart feeders capture the exact health data required to validate your genetic selections and prove if new traits are actually working in your barn.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.