Mexico just proved it can park 38,000 trucks and almost run out of milk. Has your co‑op ever shown you that risk map?

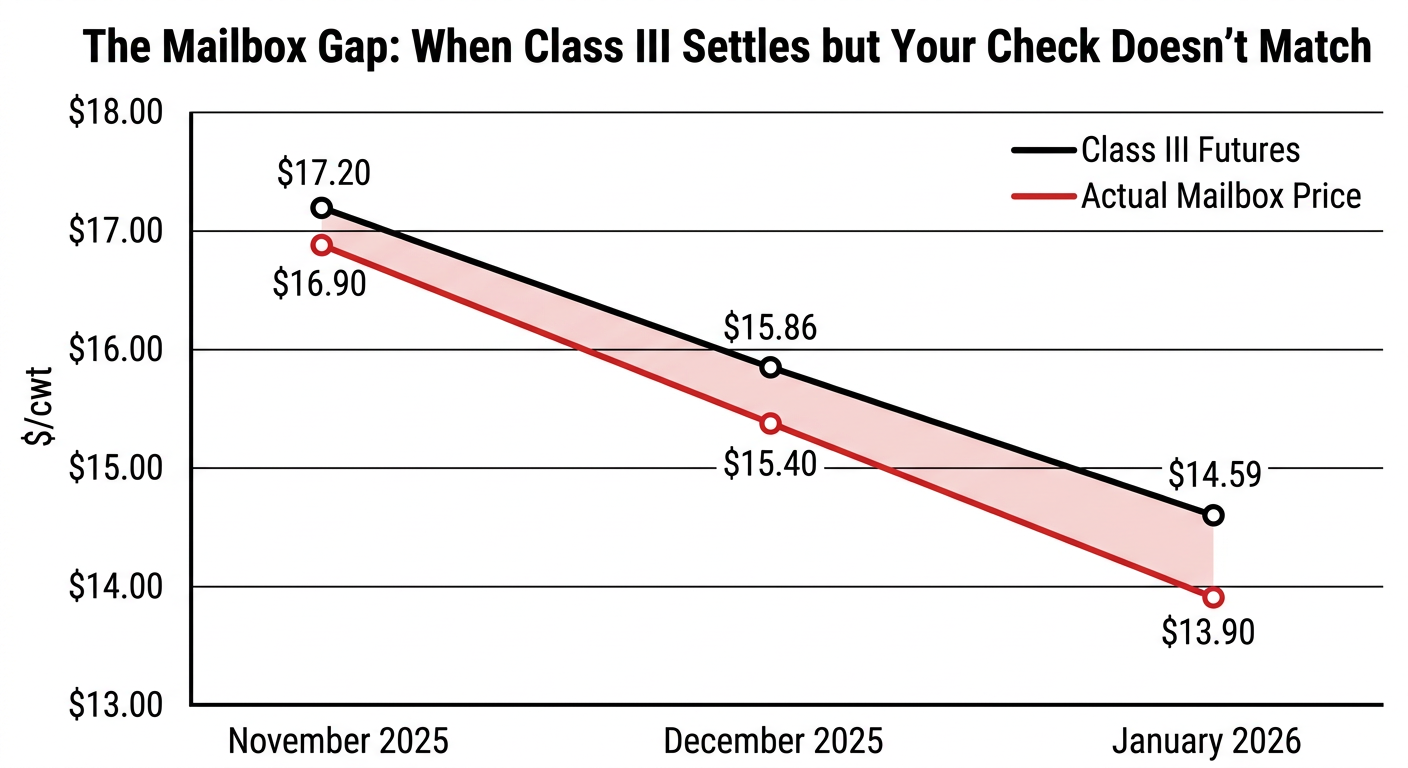

December Class III settled at $15.86/cwt. January dropped to $14.59 — the lowest since July 2023, according to Dairy Star. Those are price moves your hedge is built to handle. But if your co‑op sells heavily into Mexico, your mailbox came in shorter than even those numbers explain. And nothing on the futures screen told you why.

The answer was 1,500 miles south, stuck in traffic at Ciudad Juárez.

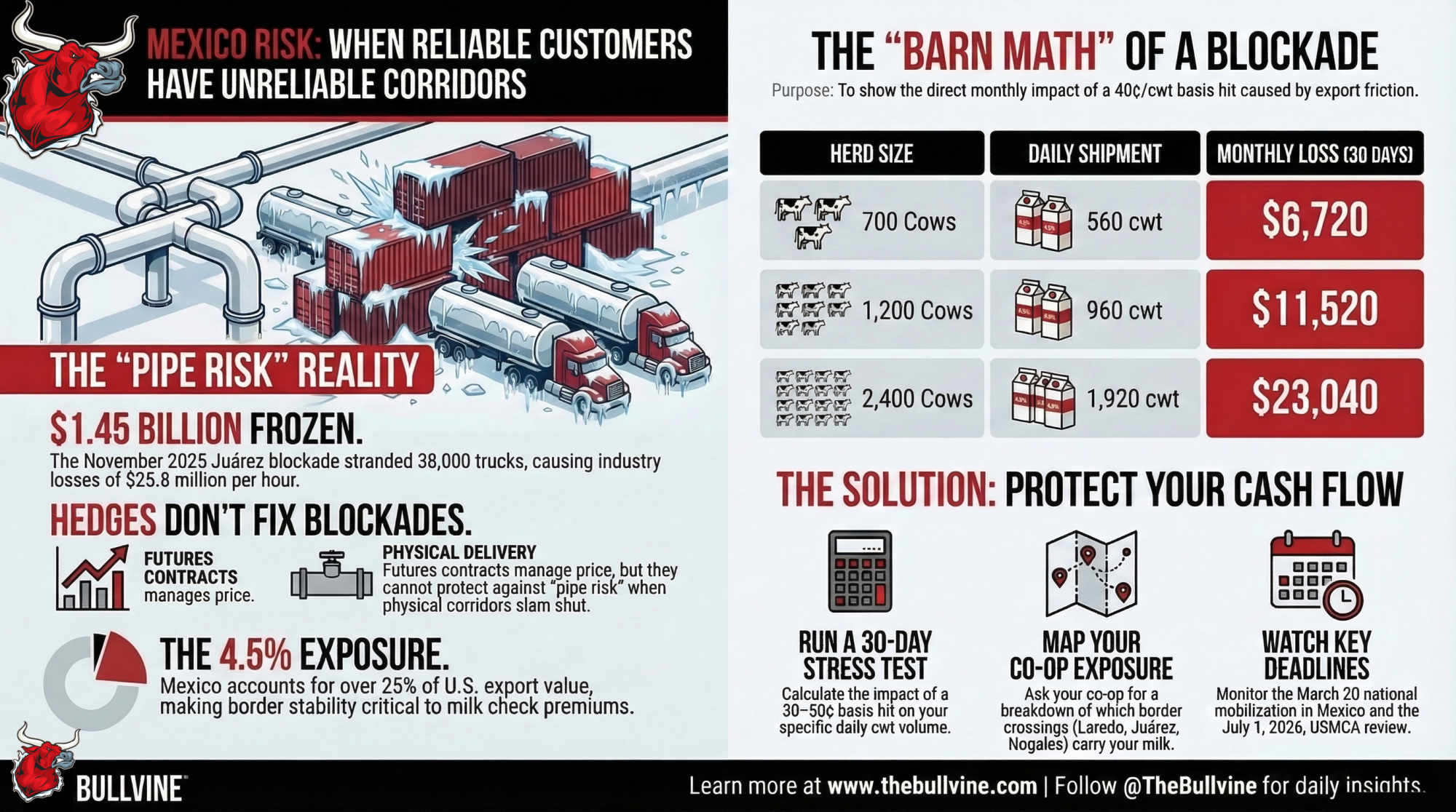

In late November 2025, farmer and trucker groups across Mexico launched what they called a “megablockade” — shutting highways and occupying customs facilities in at least 17 states. The National Front for the Rescue of Mexican Farmland (FNRCM), the National Association of Carriers (ANTAC), and the Movimiento Agrícola Campesino (MAC) targeted corridors in Chihuahua, Sinaloa, and Zacatecas, as well as routes radiating from Mexico City. At the Ciudad Juárez–El Paso crossing — Mexico’s busiest commercial border zone — FreightWaves reported roughly 38,000 trucks stranded, delaying about US$1.45 billion in exports and causing industry losses of around US$25.8 million per hour.

Dairy was the first product to run short. Iván Pérez Ruiz, president of the Juárez Chamber of Commerce, told news reporters that previous blockades “nearly resulted in a complete shortage of dairy products, with milk and cheese being the most impacted.” María Teresa Delgado Zárate of Index Juárez estimated daily export losses at $250 million. Manuel Sotelo Suárez of CANACAR warned the city was “very close to running out of supplies.”

That’s the heart of this story. You hedge prices like an adult. But the Mexico border isn’t a permanent green light — it’s a high‑beta pipeline that can slam shut with one national protest call. The risk hiding in your milk check isn’t about what Class III settles at. It’s about what happens between that settlement and your mailbox when the road closes.

CoBank Called Mexico “Reliable.” Three Weeks Later, Juárez Froze.

In December 2024, CoBank published a report called “Mexico Has Become America’s Most Reliable Dairy Customer.” Lead dairy economist Corey Geiger laid out the numbers: Mexico accounts for more than one‑fourth of total U.S. dairy export value and buys roughly 4.5% of U.S. milk production. In 2023, U.S. dairy exports to Mexico hit 1.38 billion pounds on a milk‑solids basis — a 42% increase over the prior decade. Mexico’s per-capita dairy consumption has grown about 50 pounds since 2011, and U.S. exports now cover more than 80% of Mexico’s dairy deficit. CoBank estimates one in six tanker loads of U.S. milk ends up overseas, and processors have committed around US$8 billion in new capacity coming online soon.

From a demand standpoint, Mexico really has behaved like an anchor customer. The pipes getting product there are another story.

On November 23–24, 2025, ANTAC, FNRCM, and MAC rolled out coordinated blockades before dawn. Mexico News Daily reported on November 27 that “mega-blockades” were in their fourth day, choking truck access to U.S. ports of entry. Maquiladora plants went into technical stoppages. Around 30,000 workers sat on downtime. Shippers were told to expect 10 or more days of delays even after protesters cleared the roads. News outlets reported the dairy sector faced “operational paralysis,” and by the time a third blockade was announced in December, the backlog from earlier rounds still hadn’t cleared.

Interior Minister Rosa Icela Rodríguez announced a deal on November 27 — working groups in exchange for suspending the blockades. FNRCM and ANTAC called it a truce, not a surrender. They’ve already circled the next date.

On March 3, 2026, UnoTV reported that FNRCM and ANTAC called a national mobilization for March 20 — two weeks from today — including highway blockades and actions in Mexico City. The CNTE teachers’ union announced a national strike for March 18–20, which will overlap with other strikes. MexicoBusiness.news confirmed the call on February 27. Mexico Solidarity described it as a mobilization for “food sovereignty and agricultural transformation,” with farmers demanding that basic grains be removed from the USMCA.

That’s a planned action, not a historical event. But it tells you blockades are a deliberate political tool now — not a one‑off tantrum. And the people who really control your milk check aren’t all sitting at your co‑op’s head office.

How Does This Actually Hit Your Milk Check?

The broader numbers were already ugly before the blockades started. October 2025’s U.S. average mailbox dropped 85¢ in a single month to $18.70/cwt — $5.58 below the same month a year earlier, according to USDA NASS data. Upper Midwest producers on FMMO 30 held up better, averaging $19.74 in September and roughly $19.25 in October. But reports already documented a $1.30/cwt gap nationally between the statistical all‑milk price and what farmers actually received, driven by depooling, component math, and co‑op deductions.

For co‑ops whose Mexico-bound product was stuck at Juárez, that gap had one more driver the data didn’t itemize.

Here’s the sequence: bridges close or crawl for days. Even after protesters leave, backlogs add another 10 days of friction. Plants scramble — rerouting loads through Nogales or Nuevo Laredo, shoving product into lower‑value domestic channels, piling inventory, and hoping buyers wait. Class III still settles where it settles. Your hedge does what it’s supposed to on that screen. But the gap opens in the co‑op’s margin. And when that margin gets squeezed, the co‑op pulls the levers it controls: export premiums, quality incentives, over‑base pricing, intake policies.

The basis risk lands on you.

Here’s the barn math. A 1,200‑cow herd at 80 lb/day ships 960 cwt/day. If the co‑op’s effective pay price runs 40¢/cwtbelow your hedge‑implied price for 30 days, that’s 960 × $0.40 × 30 = US$11,520. A 700‑cow herd shipping 560 cwt/day at the same gap: US$6,720. At 2,400 cows, closer to US$23,000. Plug in your own daily cwt and see where you land.

Those aren’t predictions. They’re scenarios built off the scale you just watched at Juárez — where Delgado Zárate estimated $250 million a day in export losses and Pérez Ruiz said dairy nearly ran out. The kind of surprises that show up in the mailbox, not on the futures app. With dairy economist Bill Brooks of Stoneheart Consulting estimating 2026 income over feed costs at $10.14/cwt — down $2.30 from 2025, per Dairy Star — there’s not much cushion between a rough month and the 2026 margin math that makes every basis surprise harder to absorb.

Why Can’t Your Price Hedge See a Blockade Coming?

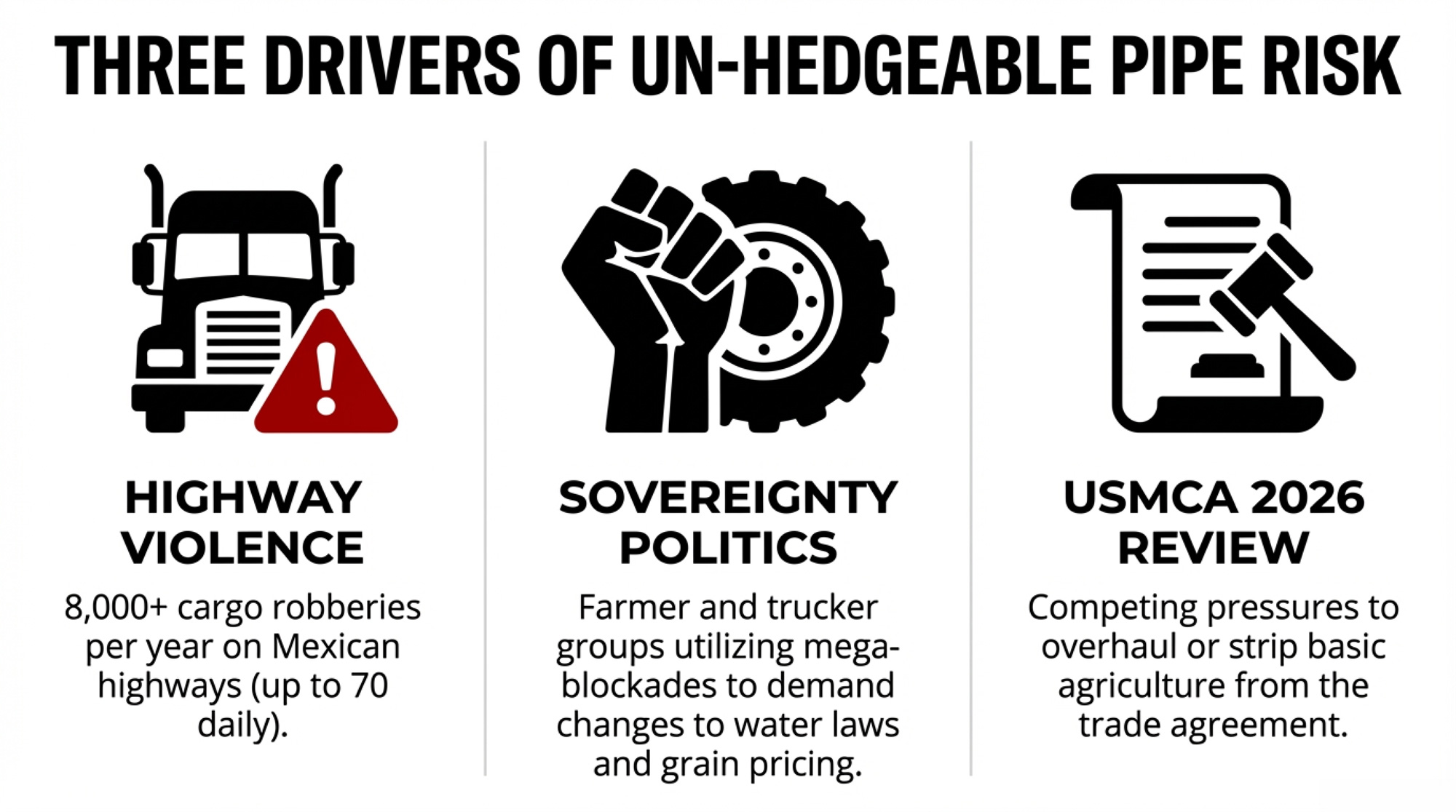

Hedging tools handle price risk. There’s no ticker for “pipe” risk — no DRP endorsement that covers Juárez running at half capacity or 8,000 cargo robberies a year on Mexican highways.

Three forces are driving the border risk your hedge account can’t touch.

Cargo theft and highway violence. El País reported in December 2025 that cargo trucks in Mexico suffer at least 8,000 robberies per year — 21 a day — and more than 80% involve violence against the driver. ANTAC says the real figure is 54 to 70 thefts daily because most go unreported. Concamin estimates cargo theft costs around 15 million pesos per day.

Water, grain, and food sovereignty politics. In October 2025, FNRCM paralyzed highways and rail lines in 17 states, demanding higher grain prices and opposing changes to Mexico’s General Water Law. FNRCM leader Marco Antonio Ortiz Salas publicly alleged that the CME and transnational grain companies were “manipulating markets.” No evidence supported that specific claim — but the grievances are real enough to park tractors on bridges, and they’re at the core of the March 20 call.

The 2026 USMCA review. Under Article 34.7, the USMCA must undergo a joint review by July 1, 2026. On January 5, the National Milk Producers Federation said it and the U.S. Dairy Export Council are “advancing a coordinated strategy to ensure the agreement delivers on its promises to U.S. dairy producers.” More than 120 U.S. agricultural groups want an extension with minimal changes. Mexican farm movements want the opposite — basic grains removed from the agreement entirely.

Your hedge locks in a price. The fact that Mexico is both your co‑op’s most “reliable” customer and one of its riskiest corridors — that’s what you have to decide what to do with.

What Should You Ask Your Co‑op Before March 20?

You can’t control FNRCM or ANTAC. You can control how blindly you’re exposed to them.

Start with the exposure question. Ask for a simple 12‑month breakdown: what percent of total solids are exported, what percent goes to Mexico, and how much of that moves through Pharr, Laredo, Ciudad Juárez, or Nogales. CoBank’s data show that Mexico buys more than a quarter of the U.S. dairy export value. If your co‑op can’t ballpark which bridges carry your milk, that’s worth raising at the next member meeting.

Then make them walk through a scenario. Say Juárez runs at half capacity for 30 days, including backlog time. Which plants pull back intake first? Which products get priority for limited export slots? In what order do they adjust premiums, quality incentives, and over‑base pricing? You’re not asking them to predict the future. You’re asking whether they’ve done the same “what if?” work you do before locking in feed.

The USMCA review adds a harder edge. NMPF confirmed in January that it’s pushing for stronger enforcement of market‑access commitments. Mexican farm movements are treating July 1 as a pressure point. Ask your board what assumptions they’re making about Mexico volumes through 2027 — and how those interact with the $8 billion in new processing capacity CoBank flagged.

If the only chart they show you is “exports up and to the right,” ask what happens when the road under that chart closes for a few weeks. For the families who’ve already decided the farm is worth fighting for, the answer matters.

How Does This Change What You Do on the Farm?

Macro risk is interesting. The bank and the feed mill still want their money on time.

Cash flow isn’t just about price anymore. With 2026 income over feed at $10.14/cwt, a surprise basis hit is the difference between a month you ride out, and a month you’re juggling which bill to delay. Within the next 30 days, pull your last 12 months of milk checks, calculate your average daily cwt shipped, and model what happens if your mailbox comes in 30¢/cwt worse than your hedge implied for 30 days. Then do the same at 50¢/cwt. Turn each into a dollar number and ask: could we ride this without breaking covenants?

If the answer makes your stomach tighten, sit down with your lender before March 20. Say: “Here’s what these scenarios look like for us. If something like this happens because of a border event, what would you want to see from us?” That’s not panic. That’s the conversation a lender expects to have before trouble arrives, not after.

Your hedge strategy may need one more trigger. You probably adjust coverage when futures move sharply, or big USDA reports drop. Consider adding one more: the gap between your hedge‑implied price and the actual mailbox. If that gap widens beyond 30–50¢/cwt for two consecutive checks, it doesn’t automatically mean “Mexico.” But it’s a red flag to ask your co‑op whether pipeline issues are in the mix and to re‑check your cash‑flow plan for the next 60–90 days.

Expansion decisions carry new questions. If you’re adding cows or signing a longer‑term supply deal, ask how those decisions tie into Mexico exposure. “How dependent is this plant on exports through Juárez?” and “What exactly did you do on premiums during the November 2025 blockades?” won’t make every marketer smile. But they’re the questions a lender would ask if they were sitting where you are.

Options and Trade‑Offs for Farmers

You don’t get to vote on Mexico’s water law or who parks a tractor on a bridge. You do get to choose how much of that volatility you carry.

Path 1: Treat Mexico as a high‑beta outlet — and price it in. This makes sense if your co‑op is genuinely good at export business and you have enough financial cushion for occasional rough patches. It requires knowing how much of your co‑op’s volume goes to Mexico and building a realistic risk haircut into long‑range margin expectations. You still get stung in bad years. If blockades become seasonal, the “occasional rough patch” becomes a pattern.

Path 2: Run a 30‑day border stress test — this month, before March 20. This is the move if you’re mid-size, have real debt, and have limited shock absorbers. Use your actual daily cwt and run two scenarios — basis 30¢/cwt and 50¢/cwt worse for 30 days. Put those dollar numbers next to your cash‑flow plan and covenants. Book a conversation with your lender this week.

Path 3: Push for a written co‑op border playbook. If you’re committed to your co‑op and want fewer surprises, ask the exposure questions in member meetings, where they’re recorded. Push for a border‑risk section in the annual business update: exposure by crossing, disruption scenarios, and the order in which premiums change. If Pérez Ruiz can tell the media that dairy nearly ran out at his city’s crossing, your co‑op can tell you how much of your milk was heading there. The USMCA review deadline — July 1, 2026 — makes this more urgent, not less.

Path 4: Align your risk advisors around pipes, not just prices. In your next risk call, say: “Let’s talk specifically about basis moves when pipelines jam — blockades, plant outages — and what that looks like in our numbers.” In your next lender meeting: “Are you factoring Mexico corridor risk into how you look at our credit?”

Key Takeaways

- If your co‑op sells a meaningful share of solids into Mexico through one or two crossings, treat border risk as its own line on your 2027 plan — not just “export.”

- If your mailbox comes in 30–50¢/cwt below what your hedge implied for two consecutive checks, call your co‑op and ask whether pipeline issues are in the mix.

- If your co‑op can’t tell you what share of its Mexico volume flows through Pharr, Laredo, Juárez, or Nogales, push for that exposure map before you sign a major expansion or supply contract.

- If a 30‑day stress test at 40¢/cwt basis hit would strain your cash flow or covenants, talk to your lender now — not after March 20.

The Bottom Line

Your hedge account sees the price side of your risk. The Mexico border has quietly become one of the most important pipe risks in North American dairy, concentrated in a handful of crossings where organized groups have already proved they can park 38,000 trucks and push dairy to the brink of shortage in days.

The question isn’t whether somebody will line up on those crossings again. They’ve already circled March 20. Whether you find out how exposed you are from a slide at a co‑op meeting, a conversation with your lender, or the next milk check that doesn’t match what you modeled — that part is up to you.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $4/cwt Your Milk Check Is Missing – And What’s Actually Working to Get It Back – Stop the bleeding in your mailbox price by identifying the structural make-allowance hits and regional deductions currently scalping your margin. It delivers a hard-nosed checklist to recover value through component gold-rushes and smarter beef-sire selection.

- USMCA 2026: The $200M Question – Why Only 42% of U.S. Dairy Access to Canada Gets Used – Exposes the paper-access trap of the USMCA before the 2026 review reshapes the trade table again. It reveals why promised quotas fail to deliver and arms your operation with the strategic positioning required to survive the coming horse-trading.

- The Texas ESL Boom: How Smart Producers Are Turning Consistency into Contract Power – Reveals how the ESL boom is weaponizing milk quality data into contract leverage, shifting the profit center from bulk volume to 90-day shelf-life predictability. It identifies the high-tech supply chains that will dominate the landscape through 2030.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.