Europe’s milk moves could flood your mailbox. Is your dairy ready for the next wave?

EXECUTIVE SUMMARY: European milk production swings are making an outsized impact on North American dairy margins this season. As the EU, U.S., and New Zealand jostle for global export leadership, every volume shift and new regulation from Brussels lands directly on U.S. farm income and risk. From compliance costs to feed volatility, today’s market noise looks more like a set of fast-moving waves than the predictable old cycles. That’s why top producers are leaning into real-time break-even tracking, component-driven strategies, and flexible risk coverage. This article gets practical—highlighting lessons from the 2015 quota flood, the importance of managing debt and working capital, and exactly which steps farmers are taking to lock in resilience. If staying afloat—and ahead—in this new dairy world is your goal, the toolbox outlined here belongs in every barn.

You know, sometimes it feels like the global milk market is just one noisy, unpredictable stock tank. I’ve had a dozen conversations this harvest about how a seemingly small regulatory change in Brussels or a surge in Irish production leaves folks scratching their heads when the mailbox check or feed bill shows up in Wisconsin or Idaho. So let’s break down what’s actually factual, what matters for North America right now, and the smart steps farms are taking to stay steady in choppy global waters.

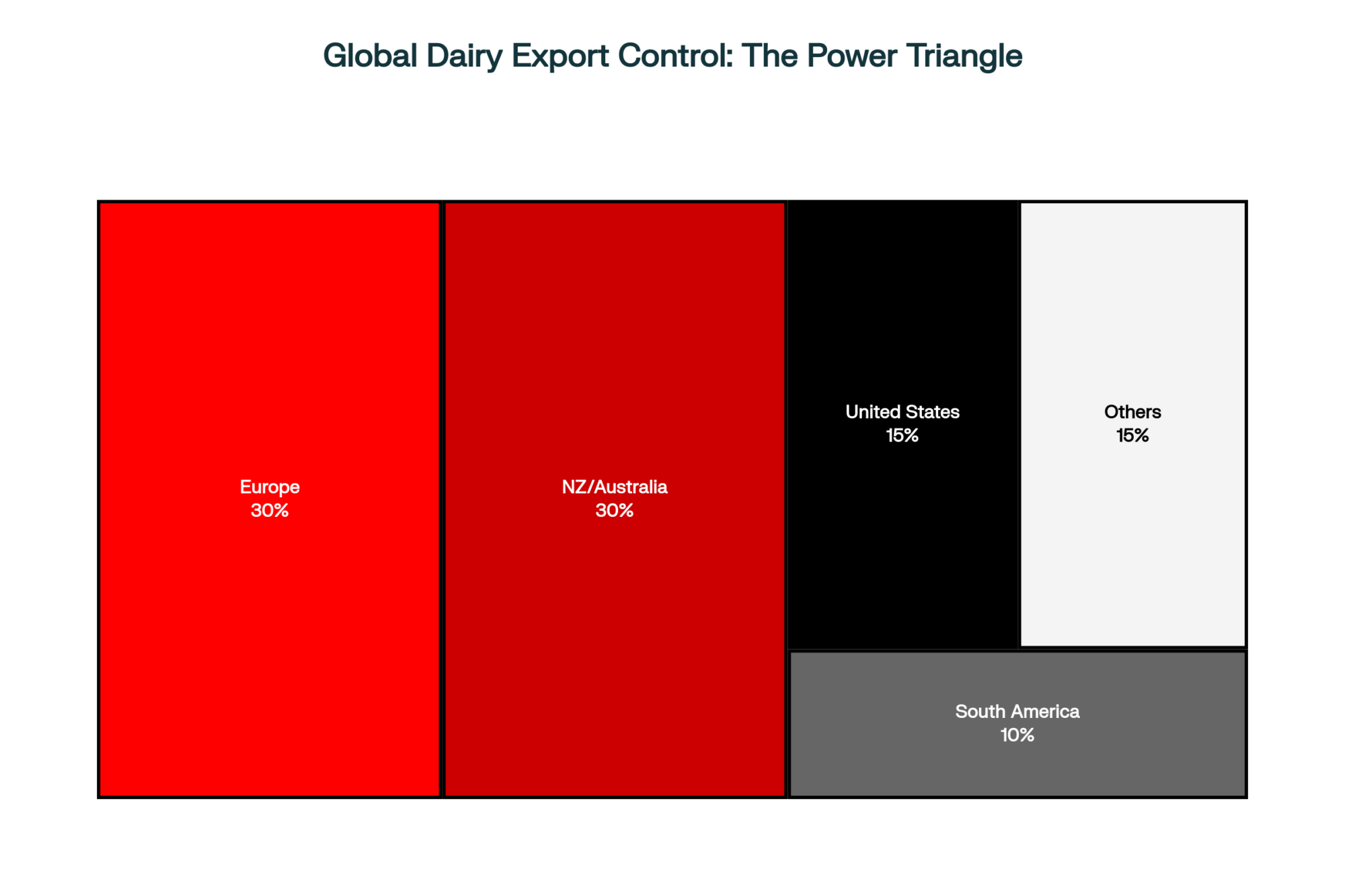

Europe’s Ripple Effect—Bigger Than Ever

Looking at data from the FAO and European Commission this season, Europe’s share of global dairy exports is as high as any region in the world—routinely neck-and-neck with New Zealand and the U.S. USDA FAS trade briefs and figures from the International Dairy Federation confirm that EU policy, volume, and even local weather matter for price benchmarks in every major importing region, from China to Algeria and Saudi Arabia [FAO Dairy Market Review 2024; European Commission Milk Market Observatory 2025; USDA Dairy: World Markets and Trade 2025].

After the big quota-lift in 2015, history proved these ripple effects: Europe’s open floodgates sent milk downstream to world markets, dropping global prices and shrinking margins back home. This dynamic (and similar cycles since) is widely documented by USDA’s Economic Research Service and industry analyses [USDA ERS 2016 Dairy Outlook]. These aren’t hypothetical models—they’re what producers are still living through, every time a big EU volume shift combines with U.S. or Oceania constraints or demand spasms in China.

Market Moves: When Data and Intuition Don’t Always Match

What’s interesting right now, reading updates from USDA Dairy Market News and IDF, is how export punches keep rolling—U.S. butter and nonfat dry milk exports are at multi-year highs as of August and September. Yet the same sources, and public updates from major global processors, flag that key importers (especially in Asia) are warming only slowly after a soft patch. Price is now set at the intersection of commodities, shipping, trade policy (yes, tariffs still sting), and shifts in government intervention or environmental regulation.

And here’s the farmer’s perspective: global milk prices don’t just bounce up and down like a ball. With international markets more closely linked than ever, a wave in Europe or Oceania can hit North American producers’ returns like the surge on a big tidal pond: unpredictable and fast.

Debt, Leverage, and Reluctance to Slow Down

I’ve noticed most extension meetings address debt and capital structure more than ever, thanks to USDA and Farm Credit reporting higher average borrowing in new builds—and Wageningen and Thünen Institutes in Europe showing similar trends in Dutch and German herds [USDA ERS 2025; Wageningen University 2024 Dairy Finance; Thünen Institute German Survey 2024]. The same stubborn reality: high fixed payments don’t let a producer ramp down milk flow very quickly, even if the next three months look ugly on paper. Most of us end up chasing volume, not conservation, because loan payments wait for nobody.

Feed: The Margin Maker (or Breaker)

The data from Penn State, UW-Madison, and Cornell extension budgets for 2024 are crystal clear: feed claims 50–60% of the average conventional herd’s cost structure—a number that climbs higher if you’re buying more feed than you grow [PSU Dairy Budgets 2024; UW Center for Dairy Profitability 2025]. USDA Ag Marketing Service had corn in the low $4s throughout harvest, but soybean meal swings and local hay shortages have kept feed volatility front and center.

What producers increasingly do—across regions and herd sizes—is double down on feed testing, fresh cow management, and ration tweaking. Historical data from the bleakest periods (2014, 2022) show that a tenth of a point of feed efficiency or improvement in butterfat performance can move a break-even from the red to the black. Industry extension sources all show more hands adjusting the TMR mixer and paying closer attention to transition period protocols and dry matter intake trends.

When Regulators Call the Tune

Complying with environmental mandates is no longer just a box for the processor or CAFO paperwork. UC Davis and multiple extension sources consistently estimate new California methane and nutrient regulations cost up to $0.40–0.55/cwt once all’s accounted for [UC Davis Agricultural Economics Policy Update, 2025]. That mirrors regulatory costs now rolling out in European dairies—Denmark, the Netherlands, and Germany are all adding, not subtracting, layers of compliance spending [European Commission Dairy Policy Fact Sheet 2025].

For Northern and Eastern U.S. producers near sensitive watersheds, budgets frequently flag compliance costs of $50–$70 per cow annually just for nutrient handling [Cornell Pro-Dairy Water Quality 2024; Wisconsin DATCP CAFO reports]. It’s a new line item in every cost calculation—something more farms are integrating into regular budget reviews.

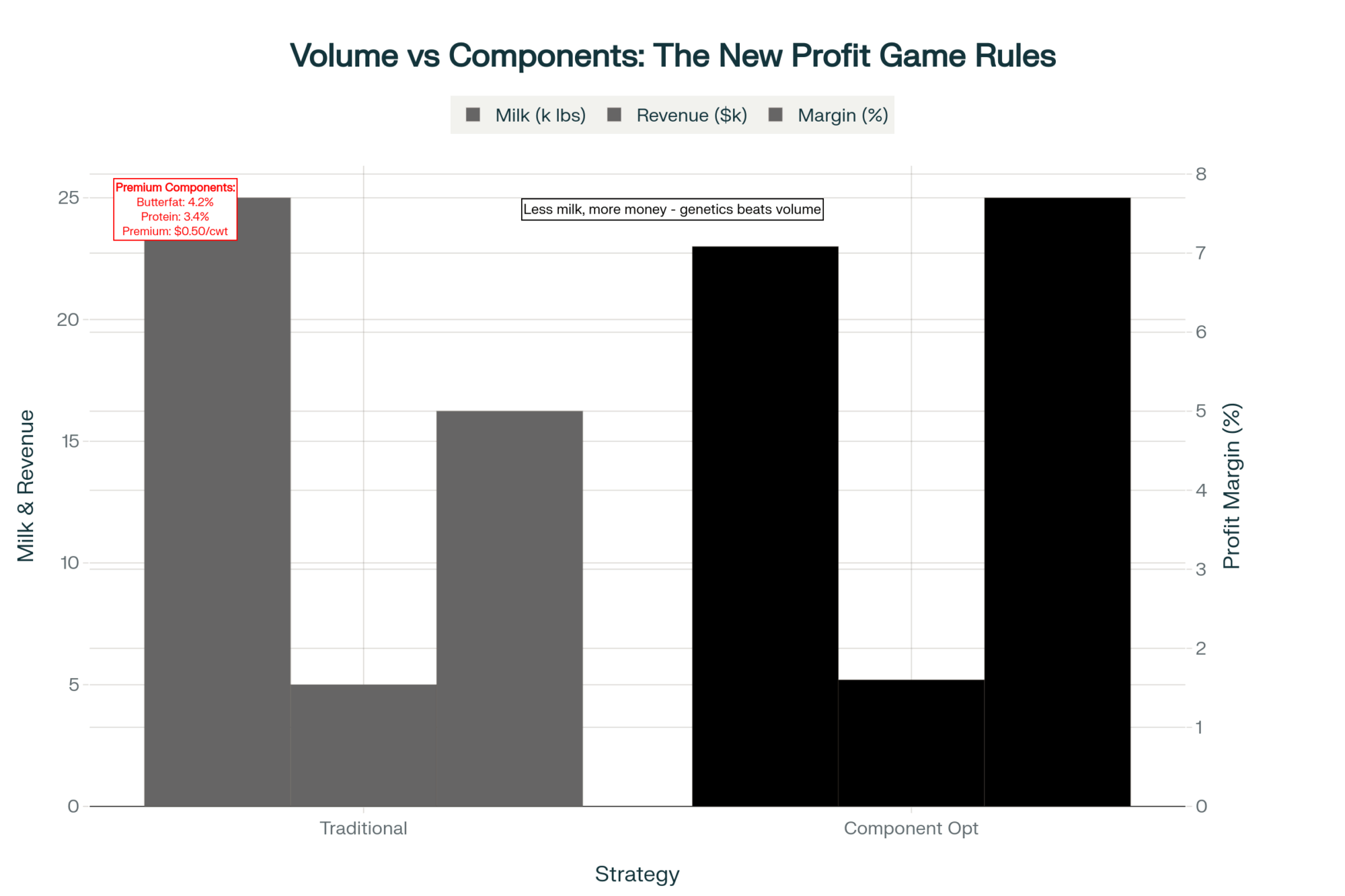

Price Spreads, Component Value, and Dairy Resilience

USDA Reporter summaries and CME data from early October confirm that Class III/IV spreads topped $2/cwt—meaning the farm’s product mix, from cheese to butterfat, is increasingly make-or-break for winter cash flow. Extension and IDF bulletins show that maximized component programs (think protein-by-breed planning or butterfat levels targeting cooperative premiums) are paying out ever higher.

The data (and plenty of farmer experience) say it’s wise to keep chasing component optimization with genetic selection, ration shifts, and milk quality focus—not only for incentive programs but also for the buffer against commodity price swings. Farms that get complacent here risk losing the best margin lifelines left in a volatile pricing world.

Farmer Risk Playbooks: Layering and Learning

Here’s a theme that runs through nearly every 2025 extension update and peer group panel: those who spread risk, keep cash reserves, and use partial hedging (from Dairy Margin Coverage to LGM or local processor contracts) are the ones telling positive stories at year’s end. Across the Corn Belt, into the Northeast and West, budgeting tools and farm management software are being used daily to run break-evens, test expansion math, and keep track of every feed load and market move.

Risk Tool

Survival %

Annual Cost

Rating

Dairy Margin Coverage

78%

$100–300

Essential

LGM Insurance

65%

$200–500

Strong

Cash Reserves (90 days)

85%

Opportunity cost

Critical

Feed Hedging

70%

1–3% of feed

Important

Processor Contracts

60%

Price discount

Useful

No Risk Management

35%

$0

Dangerous

Extension groups are now coaching herds to treat working capital as “production insurance” and to see budgeting and risk review as ongoing—not just annual—events. It’s a practice that’s proving the difference between being able to row to safe harbor in a market storm…or simply getting swept along for the ride.

Past Lessons, Forward Momentum

There’s universal agreement—whether it’s coming from a Missouri discussion group or New England’s latest fact sheets: flexibility beats size or even efficiency alone, especially once margins start to tighten. Farms that survived 2014 or the sudden whiplash of 2022 put working capital on par with any weekly milk check and made their lender and nutritionist partners, not just vendors.

What’s particularly heartening is more farms are now proactively putting reserves away in the “good” quarters rather than waiting for the next price crash. That shift, widely endorsed in current university and co-op extension workshops, means more businesses are poised to adapt to whatever moves Europe or world trade throws their way.

Looking at Winter—and the Year Ahead

If you’re looking for actionable steps, this year’s most robust takeaways from across the government, extension, and industry space are these:

Know your cost structure cold and react quickly to any break-even changes.

Prioritize fresh cow and transition period management for best margin protection.

Maximize component herd strategies (and renegotiate for best premiums).

Plan for regulatory compliance costs as a “normal” budget item.

Treat cash reserves and budgeting as production tools, not afterthoughts.

Layer your risk with multiple tools and update your mix every season.

And perhaps the most important advice? Stay curious and connected. Use every extension, processor, and peer resource out there—and keep agile enough to pivot when new global “waves” come across the Atlantic.

In this interconnected dairy world, the best producers aren’t fortune tellers—they’re steady captains, always ready to adjust sail.

Key Takeaways:

European market shifts can hit milk checks fast—stay alert to global supply changes.

Update break-evens often; real-time cost tracking is your strongest defense.

Feed and component management are difference-makers for net margins.

Build regulatory compliance into your core business plan, not just for inspection day.

Use layered risk tools—insurance, contracts, and liquidity—to position your farm for any market weather.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Protect Your Dairy Operations from America’s 1,000-Fold Subsidy Advantage – This action-oriented guide details a 3-phase plan for achieving component targets (4.2% fat, 3.3% protein) and optimizing feed conversion above 1.75:1. It provides concrete ROI calculations to show how operational excellence creates a competitive advantage that can neutralize market disadvantages.

Dykman Dairy’s $75 Million Debt Crisis: Mismanagement or Misfortune? – This cautionary case study offers a deep dive into the devastating strategic risks of unchecked leverage and rapid expansion. It provides five vital tips on debt revision, diversification, and strengthening lender relations to help you proactively manage financial flexibility against global market shocks.

The $500000 Precision Dairy Gamble: Why Most Farms Are Being Sold a False Promise – This strategic technology evaluation challenges the high-cost automation pitch, revealing how optimizing fundamental protocols (like transition cow health) offers a better, lower-cost ROI than relying solely on expensive sensors and robotics. Use this to filter smart capital investments.

Join the Revolution!

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Dairy feed prices dropping while milk values rise—discover how to capitalize on this rare profit window before market conditions shift again.

EXECUTIVE SUMMARY: As we move through 2025, North American dairy producers face a unique economic opportunity with feed costs projected to decrease by 10.1% while dairy prices stand nearly 20% higher than last year, creating an exceptional profit environment. The article provides a comprehensive roadmap for navigating this landscape, covering everything from strategic procurement of corn below $4.60/bushel and soybean meal under $300/ton to implementing advanced feed efficiency strategies that can save up to $470/cow/year. With USDA forecasting potentially record corn production around 15.58 billion bushels and improved forage availability, producers who implement the article’s recommendations on forage quality management, alternative feed ingredients, and precision nutrition can significantly enhance their margins while preparing for future volatility through strategic hedging and forward contracting approaches.

KEY TAKEAWAYS

Timing is critical: Current market conditions present a rare window where input costs are declining while milk prices remain strong—USDA projects milk receipts to increase by 2.7% to reach $51.1 billion in 2025.

Feed efficiency drives profitability: Each percentage point increase in forage NDF digestibility can boost milk production by 0.55 pounds per day, with top herds achieving feed efficiency ratios of 1.5-1.8 pounds milk per pound DMI.

Strategic procurement matters: Forward contracting 60-70% of feed needs (particularly with corn below $4.60/bushel) provides price certainty while maintaining flexibility to benefit from potential further price drops.

Alternative ingredients offer savings: Properly evaluated co-products like distillers grains, canola meal, and beet pulp can significantly reduce ration costs without compromising production when incorporated strategically.

Technology adoption pays: Precision feeding systems and individual cow monitoring technologies demonstrate ROI through labor savings of $32,850-$45,000 annually per robot and production increases of 3-15%.

So I’ve been diving deep into what’s happening with feed costs for 2025, and let me tell you – it’s quite the mixed bag. The dairy feed landscape looks complex, but there are some real opportunities if you know where to look.

The good news? We’re seeing some moderation from those crazy record prices we’ve been dealing with. But don’t pop the champagne just yet – there’s still plenty of volatility to navigate. Let’s break down what’s happening and how the smartest producers stay ahead.

Current Feed Market Landscape: What’s Happening

The Hard Numbers: 2025 Price Projections You Can Trust

So here’s the deal – USDA is forecasting a potential record corn production of around 15.58 billion bushels for 2025. They expect farmers to plant about 94 million acres (up 3.7% from last year) with around 181 bushels per acre yields. This should push ending stocks to nearly 2 billion bushels – about 425 million more than in 2024. All this points to some downward pressure on prices, precisely what we need.

We’re looking at fewer planted acres for soybeans – about 84 million (down 3.8% from 2024) as farmers shift some land to corn. However, with slightly better yields expected, production should stay fairly stable at around 4.37 billion bushels. The projected price hovers around $9.95-$10.00 per bushel – way better than the $14.20 average in 2022/23. And for dairy rations specifically, soybean meal prices are expected to average $300-$310 per short ton.

The forage situation is improving, too. On-farm hay stocks are up about 6% from last year, hitting about 81.5 million tons as of December 1, 2024. This has helped drive hay prices down significantly through late 2024.

REALITY CHECK: I talked with a nutritionist friend in Iowa last week, and she’s concerned about those early planting challenges we’re seeing – drought in the Western Corn Belt and too much rain in the East. These could threaten a big chunk of US corn production. The smart producers aren’t banking on these favorable forecasts – they’re developing Plan B scenarios just in case.

The Volatility Trap: Why “Average” Prices Are Misleading

You know how averages can be deceiving, right? Despite these lower projected prices, volatility remains a considerable concern. Several factors are keeping us on our toes:

Weather Extremes: Remember those excessive spring rains last year? Weather remains the wild card that can flip the script overnight.

Geopolitical Wildcards: Those ongoing conflicts continue disrupting production and trade. And don’t get me started on potential trade disputes with Mexico and Canada – those could shake up our export markets.

Energy Price Fluctuations: Every time energy costs jump, we feel it in fertilizer prices, transportation costs, and overall farm expenses.

Biofuel Policy Shifts: The ethanol and renewable diesel mandates influence corn and soybean oil usage, which ripples our feed costs.

Economic Pressures: Inflation, interest rates, currency exchange – all these broader economic factors affect what we pay for inputs and what we get for our milk.

This volatility means we can’t just set and forget our feed strategy. We need robust risk management and flexible feeding approaches to protect our margins.

Game-Changing Feed Efficiency Strategies from Top Performers

Forage Quality Revolution: The Foundation of Profitability

Do you know what I’ve been noticing on the most profitable farms? They’re obsessed with forage quality. For good reason, the research shows that increasing forage NDF digestibility by just one percentage point can boost dry matter intake by about 0.37 pounds and increase 4% fat-corrected milk production by 0.55 pounds per day.

THE HARD TRUTH: Every time you settle for mediocre forage quality, you’re writing a check to your feed supplier. Each percentage point drop in NDF digestibility costs real money in lost production and forces you to buy more concentrate.

The top operations I’ve visited are focusing on several key strategies:

Strategic Variety Selection: They choose forage varieties bred explicitly for higher digestibility and yield potential.

Precision Harvest Timing: They’re fanatical about harvesting at the optimal stage of maturity. I saw one operation using alfalfa quality sticks to determine the perfect cutting time based on NDF targets.

Advanced Harvesting Techniques: Wide swathing proper conditioning – these techniques accelerate drying time, reducing respiration losses and preserving nutrients.

Silage Management Excellence: They’re obsessive about rapid filling, proper packing, effective sealing with high-quality plastic and oxygen-barrier films, and using proven bacterial inoculants.

INNOVATION SPOTLIGHT: I visited a farm in Wisconsin trying intercropping – they’re feeding pea-wheat intercrop silage instead of traditional monocultures. They’ve reduced concentrate requirements by 60% without affecting milk yield or quality. Pretty impressive stuff!

Rumen Function Optimization: The Hidden Efficiency Engine

A healthy rumen is like a well-tuned engine – essential for efficient digestion and nutrient utilization. Maintaining optimal rumen pH (above 5.8) is critical, as low pH impairs fiber digestion, reduces microbial protein synthesis, and can tank feed intake.

The leading operations I’ve studied implement several strategies to promote rumen health:

Strategic Fiber Management: They provide sufficient physically effective NDF from forages to stimulate chewing and saliva production.

Controlled Starch Fermentation: They carefully manage digestion rates through grain selection and processing methods.

Feeding Consistency: They deliver a consistent TMR at the exact times each day to stabilize the rumen environment.

Microbial Protein Maximization: They synchronize the availability of fermentable carbohydrates and degradable protein sources.

Amino Acid Precision: They formulate rations to meet specific requirements for essential amino acids, particularly methionine and lysine.

Technology ROI: Data-Driven Decisions That Pay

The tech revolution is changing the game. Have you seen those systems that measure individual cow feed intake? Combining intake data with milk production records, these systems calculate individual cow feed efficiency and income over feed cost. This allows for more precise culling decisions and provides data for selecting more efficient animals.

Other high-impact technologies include:

Robotic Milking Systems: These integrate automated feeding components and collect vast amounts of data on individual cow visits, intake, and production. The North American robotic milking market is projected to grow from $641.9 million this year to over $1 billion by 2032.

Feed Analysis Technology: Regular NIR or wet chemistry analysis for all feed ingredients is crucial for accurate ration formulation.

COST-BENEFIT REALITY: Yes, these robotic systems require substantial upfront investment ($150,000-$200,000 per robot), but they can generate annual labor savings of $32,850-$45,000 per robot and production increases of 3-15%, with typical payback periods of 4-7 years. Last month, I visited a farm in Pennsylvania that’s seeing ROI in just under 5 years on their robots.

2025 Feed Price Projections & Volatility Factors

Ingredient

2025 Price Forecast

2024 Price

Key Supply/Demand Drivers

Top Volatility Risks

Corn

$4.20–$4.39/bu

$6.54/bu (2023)

Record production (15.58B bu), ethanol demand

Drought in the Western Corn Belt

Soybean Meal

$300–$310/ton

$420+/ton (2023)

Biofuel-driven crush demand, global surpluses

South American drought recurrence

Alfalfa Hay

$170–$180/ton

$280+/ton (2023)

Improved stocks (+6% YoY), regional quality gaps

Transportation cost spikes

Alternative Feed Strategies: Beyond Conventional Ingredients

Before you jump into any non-traditional feedstuff, you need a systematic evaluation. Here’s what I look for:

Nutrient Profile Analysis: What’s the actual content of energy, protein, fiber fractions, fat, and minerals? And remember – you need to analyze the specific batch you’re considering, as these alternatives can vary wildly.

True Cost Calculation: What’s the cost per pound of crude protein or Mcal of NEL compared to traditional ingredients? Don’t forget to include transportation, storage, and handling fees.

Whole-Ration Impact: How does it fit into your TMR? Consider effects on diet balance, palatability, DMI, milk yield, components, rumen function, and manure characteristics.

Supply Chain Reliability: Can you consistently get the quantities you need? How much variation exists between loads or batches?

Practical Handling Considerations: How will you store and handle it on your farm? Wet feeds need different storage and have shorter shelf lives.

High-Value Co-Products: Proven Performers

Several co-products have proven their worth in dairy rations:

Distillers Grains (DDGs): A great source of protein (25-33% CP) and energy, with relatively high fat (5-12%) and phosphorus. Watch the variability between sources and keep inclusion around 20-30% of ration DM.

Canola Meal: Valued for its high protein content (~36% CP) and favorable amino acid profile. Some research shows that it can support higher milk production than diets with cottonseed meals.

Cottonseed Products: Whole cottonseed gives you that unique protein, fiber, and fat combination. Just watch the gossypol levels, especially with young animals.

Wheat Middlings (“Midds”): Offer moderate protein and high energy (about 92% of corn). They’re palatable but ferment rapidly, so limit inclusion to 15-20% of TMR dry matter.

Soy Hulls: High in digestible fiber and can effectively replace some forage fiber or grain starch.

Beet Pulp: Another great source of digestible fiber and energy, often used to replace grain or supplement forage.

Alternative Feed Cost-Benefit Analysis

Feedstuff

Cost ($/ton)

CP (%)

NE_L (Mcal/lb)

Max Inclusion

Pros

Cons/Risks

Corn DDGs

$240

28

0.85

30%

High energy, fiber

Variability, milk fat drop

Canola Meal

$380

36

0.78

20%

Methionine-rich, sustainable

Regional availability

Beet Pulp

$210

8

0.72

15%

Digestible fiber, palatable

Dust issues, storage

Emerging Feed Innovations: What’s Working Now

Some interesting research is happening with less conventional feed sources:

Crop Residues: Corn stover and corncobs are abundant but low in protein and energy and have poor digestibility. If treated with alkaline agents, they can replace some forage, but watch for reduced energy density.

Algae (Seaweeds): Contains valuable proteins, polysaccharides, fatty acids, minerals, and bioactive compounds. Some red seaweeds also show promise for reducing methane emissions.

Field Peas: Research shows they can effectively replace corn grain and soybean meal portions. One study found substituting up to 60% of traditional protein and energy sources maintained milk production and composition.

Hydroponic Sprouts: Systems producing fresh barley sprouts can replace portions of corn and soybean meal in heifer and mid-lactation cow diets.

REGIONAL INNOVATION ALERT: I was talking with a producer from Quebec who’s having success with kelp-based rations. They’re seeing both production benefits and reduced environmental impact through methane reduction.

Feed Efficiency Benchmarks for Top Herds

Metric

Target Range

Impact on Profitability

Management Levers

Feed Efficiency (lbs milk/lb DMI)

1.5–1.8

+$470/cow/year at 1.55→1.75

Rumen health, forage digestibility

Silage DM Loss

<10% (vs. 25% in bunkers)

Saves $280/cow/year

Oxygen-barrier films, packing density

TMR Refusal Rate

2–3%

Prevents $18K/year waste

Accurate dry matter testing, mixing

Strategic Procurement: Locking in Profits, Not Just Prices

Forward Contracting: Beyond Basic Buying

A forward contract locks in a specific quantity and feed quality for future delivery at an agreed-upon price today.

Pros: Price certainty is the big one. You’re protected against future market increases, which helps with budgeting and financial planning. It can also help secure physical supply during tight periods.

Cons: You lose the opportunity to benefit if market prices fall after you contract. You must deliver at the agreed price, even if spot market prices drop.

Strategic Approach: Rather than simultaneously contracting 100% of your needs, consider incremental purchasing – lock in portions of your requirements over time. Maybe secure 60-70% before anticipated seasonal price increases. This helps average out prices while retaining some flexibility.

Hedging Tools: Sophisticated Risk Management

Hedging uses financial instruments to offset price risk associated with physical commodities.

Futures Contracts: These are standardized agreements to buy or sell a commodity at a predetermined price on a future date. If you anticipate buying corn or soybean meal in the future, you can buy futures contracts today. If cash prices rise by the time you need to purchase, your futures contract position will likely increase in value, offsetting the higher cash price.

Options on Futures Contracts: These give you the right, but not the obligation, to buy or sell a futures contract at a specific price. You can buy call options on corn or soybean meal futures to protect against rising feed costs while retaining the ability to benefit from falling prices.

EXPERT ADVICE: Last week, I talked with a risk management consultant who said, “Don’t lock it all in. Set a minimum and maximum volume to contract each month. If you’re new to contracting or have low debt, consider less than 50 percent of monthly production. If you’re more experienced or highly leveraged, maybe reach 60-80 percent.”

Building Resilient Supplier Relationships: The Human Factor

Beyond formal contracts and hedging, cultivating strong relationships with feed suppliers, nutritionists, and neighboring crop producers can be incredibly valuable. These relationships can yield better market intelligence, more reliable supply during tight periods, potentially more favorable payment terms, and quicker access to solutions when needed.

Practical Ration Adjustments: Balancing Cost and Performance

Fine-Tuning Nutrition Without Sacrificing Production

Optimizing rations while controlling costs is an ongoing process:

Forage Foundation: High-quality forage should always be the cornerstone. Maximize its inclusion when quality permits – it’s often the most cost-effective source of nutrients.

Comprehensive Analysis: Regularly test all feed ingredients, especially forages and variable byproducts. Accurate nutrient values are non-negotiable for precise balancing.

Leverage Formulation Tools: Work closely with a nutritionist using modern ration software to evaluate complex nutrient interactions and find cost-effective combinations.

Strategic Alternative Evaluation: When considering alternatives, assess them based on the cost per unit of key nutrients compared to what they’re replacing.

Gradual Implementation: Avoid abrupt shifts in ration composition. Introduce new ingredients slowly over several days or weeks to allow the rumen microbes to adapt.

Performance Monitoring: Closely observe cows for changes in DMI, milk yield, components, manure consistency, body condition, chewing activity, and overall health.

Critical Nutrient Considerations in Cost-Constrained Scenarios

When adjusting rations to manage costs, maintaining the proper nutrient balance is paramount:

Energy Balance: Meeting the Net Energy for Lactation requirement is fundamental—balance sources like starch, digestible fiber, and fat. Avoid excessive rapidly fermentable carbs that can lead to acidosis.

Protein Efficiency: Focus on Metabolizable Protein requirements, accounting for both rumen degradable protein for microbes and bypass protein. Pay attention to lysine and methionine to improve protein efficiency and component yield.

Fiber Requirements: Adequate fiber is crucial for rumen health. The target minimum ration NDF is around 28% dry matter, with ADF at 18-20% or higher. Ensure sufficient physically effective NDF from longer forage particles.

Mineral and Vitamin Precision: Meet requirements without significant over-supplementation, which adds unnecessary cost and can sometimes cause antagonisms.

COMPONENT FOCUS: Component values will shift with the federal order pricing formula changes coming on June 1, 2025. Ensure your ration strategy maximizes the most valuable components under the new structure.

Grow vs. Buy: Strategic Decision Framework

Economic Analysis: The Complete Cost Picture

A thorough economic analysis is essential for making an informed grow-versus-buy decision:

Costs of Growing include:

Land Costs: Either cash rent or opportunity cost of owned land

Field Operations: Fuel, labor, machinery costs for tillage, planting, spraying, harvesting

Machinery Costs: Ownership costs (depreciation, interest, insurance) and operating costs

Storage Costs: Including estimated storage losses

Yield Risk: The financial impact of potential yield variability

Costs of Buying include:

Purchase Price: The price per ton paid to the supplier

Transportation: Hauling costs, if not included in the purchase price

Storage Costs: On-farm storage, if not used immediately

Quality Risk: Potential variability in nutrient content and quality

Supply Risk: The risk of not being able to source the required quantity or quality

Operational Fit Assessment: Beyond the Numbers

The decision extends beyond pure economics:

Resource Availability: Do you have suitable land, adequate labor with cropping skills, and necessary capital for machinery?

Management Focus: Do you have the expertise, time, and interest to manage cropping alongside the dairy herd effectively?

Quality Control: Growing your feed offers greater control over forage quality through timely harvest and handling. Buying introduces reliance on supplier quality standards.

Risk Profile: Growing exposes you to production risks (weather, pests, yield variability), while buying exposes you primarily to price and supply availability risks.

Future Preparedness: Beyond 2025

Anticipating Long-Term Market Trends

Long-term agricultural baseline projections provide valuable insights into potential future market directions:

Moderation in Crop Prices: Following the volatility and peaks of recent years, projections indicate a return to more moderate price levels for significant feed grains and oilseeds over the next decade, potentially settling near plateaus established before the recent surge. However, significant annual fluctuations due to weather and other factors are still expected.

Livestock Cycles: Cattle prices, currently high due to herd contraction, are projected to eventually decline as the industry rebuilds inventories in response to favorable margins.

Food Price Inflation: After the rapid increases in 2022 and 2023, overall consumer food price inflation is projected to slow and stabilize closer to historical averages beyond 2025.

Evolving Dairy Consumption: While overall demand for dairy protein remains strong globally, consumption patterns within North America are shifting. There is growing demand for specific product types like high-fat dairy, specialty cheeses, organic milk, and functional dairy products, alongside the continued rise of plant-based dairy alternatives.

Preparing for Key Challenges

Dairy producers must prepare for several significant challenges that will likely shape the feed and dairy markets in the coming years:

Sustainability Pressures: Environmental scrutiny of livestock agriculture is intensifying. Focus areas include greenhouse gas emissions, manure management, water quality and usage, and land use efficiency.

Regulatory Landscape: The policy environment is dynamic. Potential changes include stricter environmental regulations, evolving animal welfare standards, tighter rules on antibiotic use, modifications to farm support programs, and shifts in international trade agreements that could disrupt key export markets.

Consumer Shifts & Market Access: The rise of dairy alternatives continues, driven by factors like lactose intolerance, veganism, and health/environmental concerns. Consumers also increasingly demand transparency regarding production methods and specific attributes like organic, non-GMO, or grass-fed.

Input Cost Volatility: While feed prices may moderate on average, volatility in feed ingredients, energy, fertilizer, labor, and other inputs will likely remain a persistent challenge.

Climate Change Impacts: Increasing frequency and severity of extreme weather events pose risks to crop production and animal productivity.

Identifying Future Opportunities

Amidst the challenges, numerous opportunities exist for forward-thinking dairy operations:

Technology Adoption: Continued advancements in precision agriculture offer significant potential, including precision feeding systems, individual cow monitoring for health and efficiency, robotic automation to address labor challenges, advanced data analytics for decision support, and ongoing genetic selection for improved feed efficiency.

Novel Feed Ingredients: Research and development into alternative and sustainable feed sources like algae, insect protein, single-cell proteins, and improved co-products may yield scalable and cost-effective options in the future.

Value-Added & Niche Markets: Capitalizing on consumer trends by producing for specific markets such as organic, grass-fed, and A2 milk or developing on-farm processing or direct marketing channels can capture higher margins.

Sustainability as a Value Proposition: Demonstrating strong environmental stewardship can enhance brand image and potentially open doors to premium markets or participation in emerging ecosystem services markets, such as carbon credits.

Diversification: Integrating complementary enterprises, such as raising high-value beef-on-dairy crossbred calves, can provide additional revenue streams and buffer against dairy market volatility.

The Bottom Line

Navigating the complexities of the 2025 feed economic landscape requires a proactive, informed, and integrated approach. While challenges related to cost volatility and margin pressures persist, opportunities exist for dairy producers who strategically manage their resources and adapt to market dynamics.

The key to success lies in implementing a balanced strategy that includes astute market awareness and risk management, maximizing on-farm feed efficiency, making strategic ingredient selections and ration formulations, making informed sourcing decisions, and preparing for future trends. Dairy operations can successfully navigate the current landscape and build a foundation for sustained production excellence and profitability by focusing on these areas.

Remember that these strategies are interconnected. Procurement decisions impact ration formulation options; forage quality influences feed efficiency; feed efficiency affects overall profitability and sustainability metrics. Success requires a holistic management approach where decisions in one area consider the implications for others, with open communication between farm owners, herd managers, nutritionists, veterinarians, and financial advisors.

The feed cost challenges facing North American dairy producers in 2025 demand more than incremental adjustments. While the market may offer some relief from recent price peaks, volatility, and margin pressure necessitate a strategic, proactive, and adaptable management style to outmaneuver sky-high costs while maintaining production excellence.

Learn more:

Strategies to Boost Cash Flow on Your Dairy Farm – Explores multiple approaches to improving farm finances, including feed management optimization as a key strategy for controlling costs while maintaining production.

Join over 30,000 successful dairy professionals who rely on Bullvine Daily for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we and our partners use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us and our partners to process personal data such as browsing behavior or unique IDs on this site and show (non-) personalized ads. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Click below to consent to the above or make granular choices. Your choices will be applied to this site only. You can change your settings at any time, including withdrawing your consent, by using the toggles on the Cookie Policy, or by clicking on the manage consent button at the bottom of the screen.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Join the Revolution!

Join the Revolution! Join the Revolution!

Join the Revolution!