Every ‘solution’ that claims to save dairy farms was never designed to fix anything — it was built to extract you, one milk check at a time.

You know the line by now. Every time milk prices crash, every time a farm auction makes the local news, somebody shows up with a binder and a slogan. “Efficiency will save you.” “Diversify into organics.” “Join a co-op — strength in numbers.”

I mean, I’ve heard them all. You probably have too. But here’s the thing that nobody in those meetings will ever say out loud — the system isn’t broken. It’s working exactly the way it was built. It just wasn’t built for you.

The math nobody wants to admit

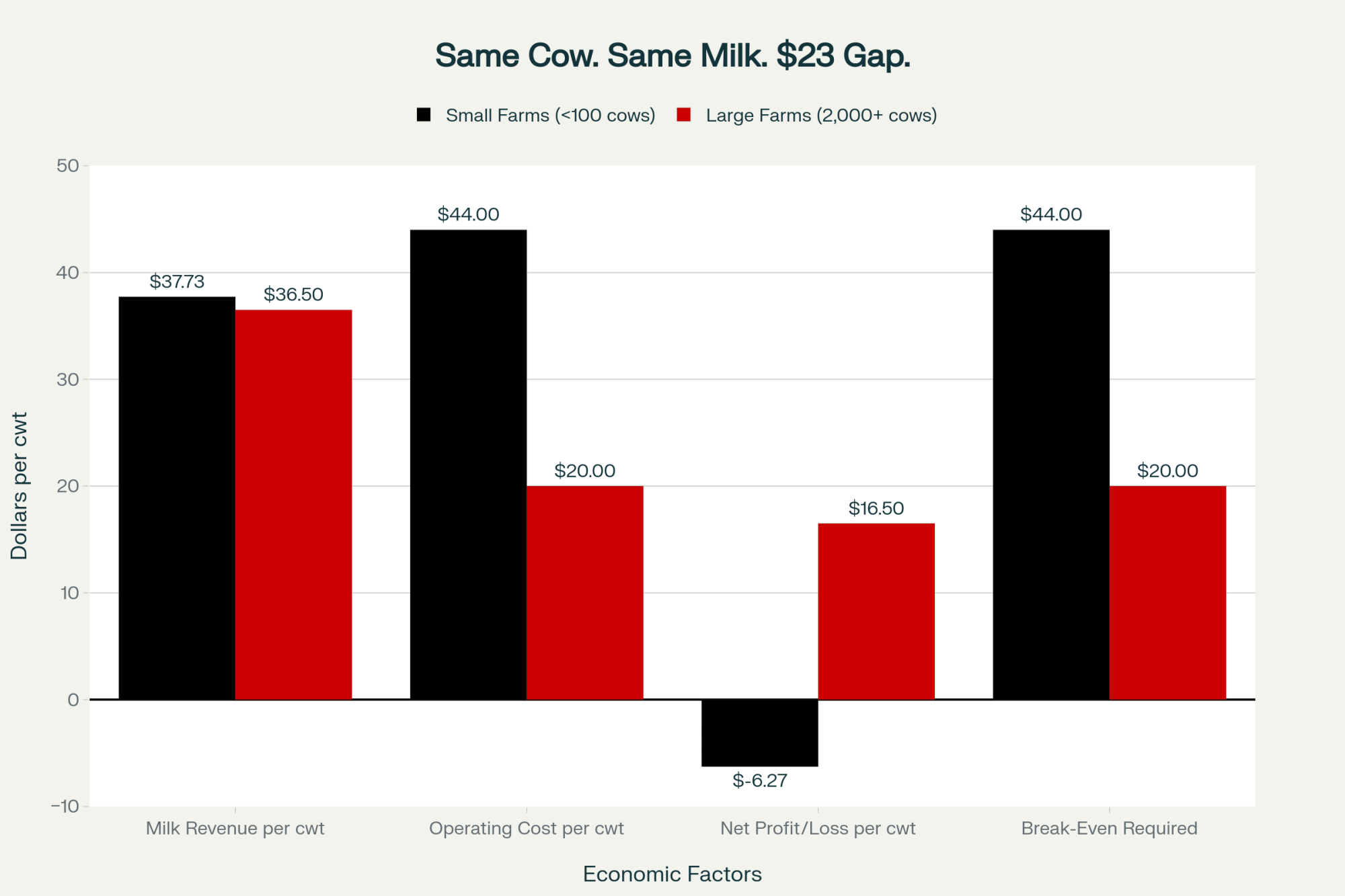

Small dairies lose $6.27 per hundredweight while large operations profit $16.50 on the same product—a $23 gap that exposes the system’s built-in preference for scale over sustainability

Down in Wisconsin, the USDA’s Economic Research Service has been crunching the same numbers for years. Small herds — fewer than 100 cows — produce milk at $42 to $44 per hundredweight. Large herds — 2,000 cows and up — come in at $19 to $20.

That’s a $23 gap that no efficiency app, no robotic milker, and no “farm family tradition” can erase.

I was at a producer meeting in Madison when one co-op board member leaned back and said it plain: “Small dairies are emotionally important, but economically irrelevant.” Brutal. True. That’s the level of quiet truth people at the top already understand but never put in print.

And that’s the problem — your loss is their model.

Where the money actually goes

Let’s put real numbers to this thing.

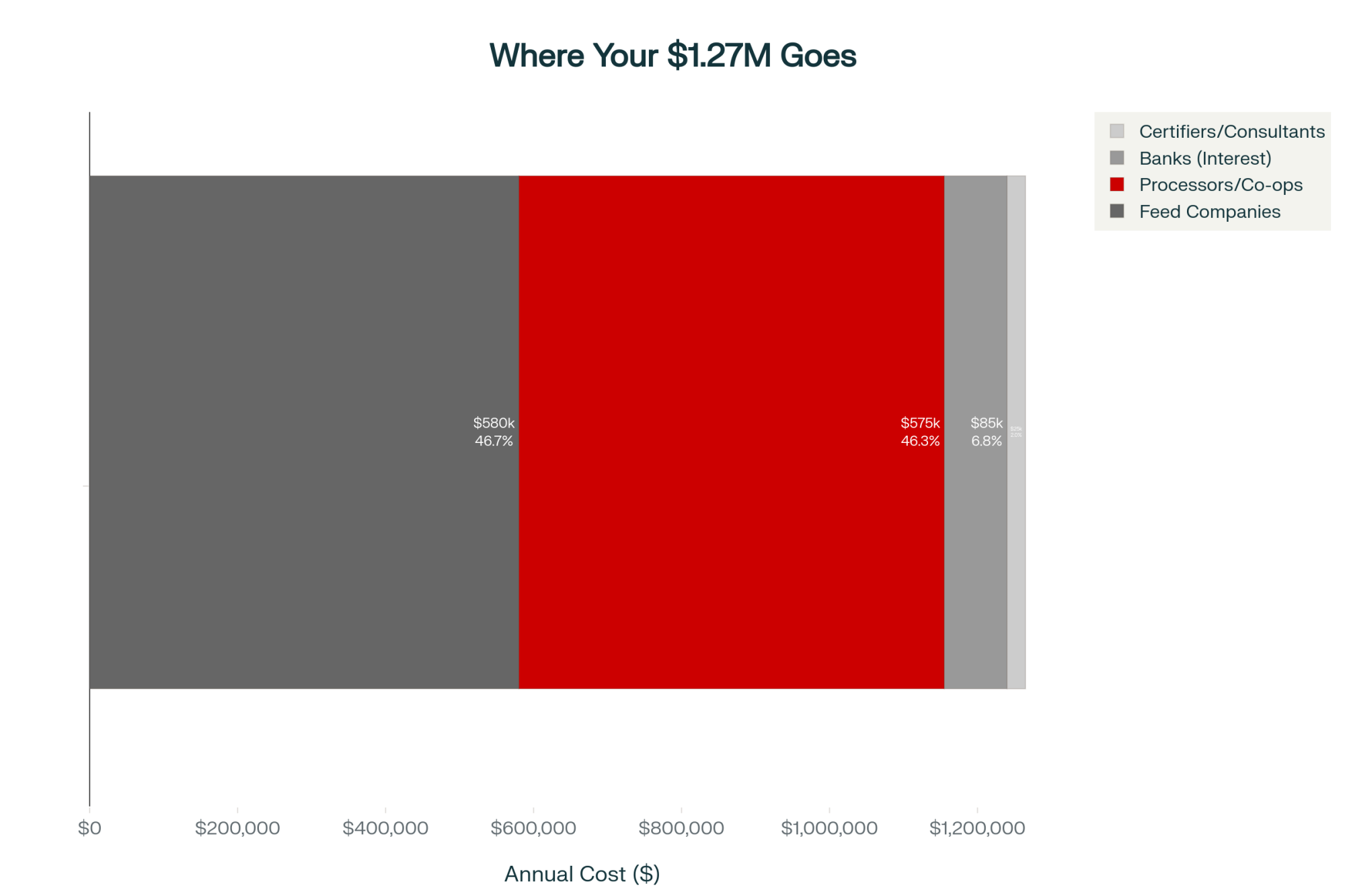

A 250-cow dairy feeding 50 pounds per head per day spends roughly 0,000 a year on feed, per USDA feed cost indices. Feed companies take 8–12% margins on that. That’s $175,000 to $240,000 every three years transferred out of your pocket before you even pay labor.

Add the bank. The Farm Credit System’s nationwide reports list operating and mortgage interest averaging around 6.8%. On a $900,000 land note and a $300,000 operating loan, that’s about $85,000 a year in interest.

Then your co-op or processor adds another chunk. According to Rabobank’s 2025 Dairy Outlook, most processors net around $3.50 per hundredweight after hauling and processing — that’s $575,000 from your production.

A 250-cow dairy operation sends $1.27 million annually to feed companies, processors, banks, and consultants before the farmer pays for labor or takes home a single dollar—revealing the extraction system that profits from farm losses

So the next time someone says, “You just need to manage costs better,” tell them your losses financed someone else’s record quarter.

An accountant friend of mine told me over lunch, “For every dollar a farm burns in equity, someone up the chain makes six.” That right there should stop the room cold.

Starting with $1,000 in milk value, farmers watch $573 get extracted by feed companies, banks, processors, and consultants—keeping only $427 while upstream stakeholders profit $6 for every $1 of farm equity burned

The organic trap: paying to play

Here’s another shiny “fix” that just doesn’t add up.

Per the USDA’s National Organic Program, converting a farm means running the land chemical-free for 36 months, and feeding cattle organic rations for 12 months before certification. According to Cornell’s 2024 Organic Dairy Cost study, feed costs jump 30–40%, while tank weights drop 8%.

That’s an extra $180,000 in feed, $10,000 in certifications, and about $40,000 in lost yield a year before you even cash a single “organic premium” check.

Dan Richter, milking 220 cows out in Cashton, said it best: “We made it to certification, but we were broke before the first organic load hit the plant.” He’s not alone — Cornell data shows two-thirds of organic transitions never reach sustainable profitability.

What strikes me most? The programs keep rolling anyway. Because suppliers, certifiers, and consultants still make their margin, no matter what happens to the farm.

Equipment-sharing: good on paper, chaos in practice

You hear it at winter extension meetings — “Form an equipment co-op, cut your costs!”

But University of Minnesota Extension found that those shared projects shave about 10% off upfront ownership costs, while downtime climbs 20% and repair expenses eat another 7%.

A producer from Viroqua told me, “We spent more time arguing over whose turn it was to use the chopper than actually chopping.”

And look, that’s not laziness. That’s just how weather and manure work. You can’t partition urgency. The only folks winning from that plan are the sales reps who sold the machinery in the first place.

Processors love to brag about “protein incentives.” USDA Dairy Market News says the average premium sits around $1.25 per hundredweight.

The trouble is… that extra protein costs money. Cornell dairy nutritionists peg the annual ration bump at roughly $75,000, plus $15,000 for consultant fees and testing programs.

Best case — you net maybe $20,000.

Meanwhile, processors get exactly what they want — uniform, high-solids milk without buying a pound of extra grain.

Like one New York nutritionist told me quietly at a conference this year: “Protein bonuses aren’t a windfall. They’re a management leash.”

Co-ops: from shields to siphons

People forget the history — co-ops were started to protect producers from predatory processors. But the GAO’s 2024 Cooperative Governance Report revealed that 78% of major U.S. co-ops now use milk-volume voting.

One member equals one vote? Not anymore. It’s cubic tons of milk per vote now.

A 300-cow operator from Brookings County told me, “My co-op makes more on hauling my milk than I make milking the cows.” The sad thing? That’s not hyperbole.

Even the GAO data shows that cooperative processing divisions now generate more operational profit than they do from member payments. Somewhere along the line, the idea of “member-first” flipped to “margin-first.”

The big picture — and it’s not pretty

The USDA’s Agricultural Projections to 2034 project the U.S. will have 12,000–15,000 dairies left by 2030. We’re sitting around 26,000 now.

Rabobank’s forecast says six processors will control 80% of total U.S. milk flow, while the Council on Dairy Cattle Breeding (2025) reports five Holstein sires now sire 82% of all replacements.

Think about that — market and genetics bottlenecked into half a dozen corporate hands.

And what happens locally? UW–Madison economists calculated that each 100-cow farm loss strips $500,000 from regional rural economies — vet clinics, feed stores, mechanics, and local schools. Drive from Antigo to Arcadia this fall, and you’ll see them: boarded barns, “auction today” signs, and co-ops consolidating routes that used to serve three farms per mile.

That’s not bad luck. That’s a business plan.

“Just one more year…”

You can tell when somebody’s gone from hopeful to cornered — they start saying it. “If we can just make it one more year.”

You know who wants you to “hang on”? The people who profit from delay: bankers, feed mills, processors. Tom Greene calls it “equity farming for other people.”

Every year, small dairies run at a loss, but the rest of the chain keeps cashing checks on time.

That’s the hidden cost of loyalty — the longer you stay, the more they gain.

What you can actually do about it

This part matters because nobody else is going to say it straight.

Call your accountant, not your lender. The bank lives on time. The accountant lives on truth. Ask them to run your net after unpaid family labor and true depreciation.

Get a land appraisal. The American Society of Farm Managers and Rural Appraisers says Midwest farmland finally plateaued in 2025 after years of inflation. If you’re considering an exit, waiting means losing margin.

Run two lists. Stay and lose $100K in equity per year. Exit, keep $2.5 million clean. Math doesn’t lie — it just hurts.

Make the family meeting happen. Don’t wait until the next refinance or co-op contract cycle. This isn’t quitting; it’s protecting what generations built.

If that sounds heavy, that’s because it is. But so is the weight of hope that never pays off.

The inconvenient truth

The real betrayal here isn’t that the system failed small dairy. It’s that it pretended to save it while quietly making money off every stage of its decline.

This whole setup isn’t chaos — it’s choreography. And it plays out just as designed: the smaller farms provide the illusion of diversity, the mid-tier keeps the supply chain full, and the megas consolidate control.

So tomorrow morning, when you’re tightening hoses or scraping the feed alley, stop and look at your milk check before you start another year of “hanging on.” Ask yourself:

“If everyone else is making money off my losses, how long am I willing to play the game?”

Because the truth is — this system isn’t failing. It’s succeeding exactly the way it was designed to. And that’s the part nobody in a suit will ever say out loud.

KEY TAKEAWAYS

The dairy system isn’t “broken” — it’s performing exactly as designed. Farmers lose; everyone else wins.

The economics are brutal: small farms spend twice what megas do to produce the same milk. Passion doesn’t pay bills.

Every so‑called “solution” — co‑ops, consultants, organic programs — is just a polite way to harvest your last dollars.

For every dollar of farm equity burned, six show up elsewhere — in feed, finance, or processing profits.

The smartest play isn’t hope. It’s strategy: scale, specialize, or sell before the system cashes you out.

EXECUTIVE SUMMARY

The small dairy crisis isn’t some tragic accident — it’s the business model. The USDA’s data shows that small farms make milk for $44/cwt, while megas do it for $20. That’s not competition; that’s a setup. Meanwhile, every “solution” — organic transitions, efficiency programs, co-op loyalty — just keeps you milking long enough for everyone else to get paid. Cornell, Rabobank, and GAO reports show how feed dealers, banks, and processors profit from your losses. For every dollar of farm equity burned, six appear upstream. The system isn’t failing; it’s extracting. So if you’re still hanging on, here’s the real math: scale up, specialize, or get out while there’s still something left to save.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Decide or Decline: 2025 and the Future of Mid-Size Dairies – Analyzes the specific “mid-size squeeze” wiping out 700-1,200 cow herds and outlines the three rigid paths—expansion, specialization, or exit—remaining for operations caught in the scale gap.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Your banker knows. Your co-op won’t say it. China’s birth crisis means your 300-cow dairy has 90 days to decide its fate. Here’s how.

EXECUTIVE SUMMARY: China’s 42 million tonne milk mountain isn’t temporary—it’s the product of a 48% birth rate collapse that permanently eliminates demand for 5% of global milk production. If you’re running a 200-500 cow dairy, this structural shift means you’re losing $359,609 annually compared to 2,000-cow operations, a gap that superior management cannot close. With milk prices locked at $16.50-18.00/cwt through 2027, you have exactly three viable options: borrow $8-15 million to scale beyond 1,500 cows, pivot to premium markets with guaranteed contracts (organic, A2, grass-fed), or execute a strategic exit that preserves your equity. The difference between acting now and waiting is stark—strategic exit today nets 70-85% of equity ($1.5M), while forced liquidation in 12 months recovers just 30-50% ($700K). Every month of indecision bleeds $23,000-55,000 through operating losses and accelerating asset depreciation. Your Q1 2026 decision isn’t about whether you’re a good farmer—it’s about whether you’ll control your family’s financial future or let market forces decide for you.

Let me share something that’s been on my mind lately—and I think it deserves careful attention from every dairy farmer reading this. China’s sitting on 42 million tonnes of surplus milk, based on their agriculture ministry’s September reports. That’s roughly 5% of global production, just… sitting there. And here’s what’s interesting: this isn’t your typical market cycle that we’ve all weathered before.

You know, I’ve been digging through the data, talking with economists at Cornell and Wisconsin’s dairy programs, and what’s emerging is a picture that’s fundamentally different from anything we’ve navigated since—well, probably since we all switched from hand milking to mechanical systems. Understanding why this time really is different —and knowing what steps to take right now —could make all the difference for your operation over the next 24 months.

Why This Crisis Breaks All the Old Patterns

So I was looking back at my notes from the 2009 downturn the other day. Remember that one? USDA data shows all-milk prices bottomed out at $11.30 per hundredweight in July 2009, then bounced right back within 12 months. The 2016 slump—you remember, when Russia imposed an embargo and the EU eliminated quotas—that stabilized within 18-24 months, according to the dairy network analysis I’ve been reviewing. Even COVID, for all its disruption, saw our sector adapt remarkably well within months. There’s actually some fascinating research in the Journal of Dairy Science from 2021 documenting how quickly we pivoted.

But China? This is something else entirely.

What farmers are discovering—and China’s National Bureau of Statistics backs this—is that we’re dealing with a demographic reality nobody can fix. Their birth rate collapsed from 12.43 per 1,000 people in 2016 to just 6.39 in 2023. That’s a 48% decline, folks. The population of kids aged 0-3… you know, the ones drinking all that infant formula? Down from 47 million to 28 million in just five years. Those babies don’t exist and won’t magically appear if milk prices recover.

The numbers don’t lie: China lost 19 million formula consumers (40% decline) while birth rates crashed 48%. This isn’t a cycle—it’s permanent demand destruction that eliminates 5% of global milk consumption. Your 2027 milk price depends on markets that will never return.

Here’s what happened: After that horrific 2008 melamine scandal—six babies died, 300,000 were hospitalized according to World Health Organization reports—Beijing went all-in on dairy self-sufficiency. The Chinese began importing hundreds of thousands of Holstein cattle in 2019, according to the customs data I’ve been reviewing. Average herd sizes grew 40% year-over-year through late 2023, if you can believe it. They hit 85% self-sufficiency, up from about 70%—exactly what they wanted. Problem is, they built all this capacity assuming demand would keep growing.

Now here’s where it gets really unusual. Chinese raw milk prices have been underwater for over two years—sitting at 2.6 yuan per kilogram against production costs of 3.8 yuan, based on China Dairy Industry Association data from October. Farmers there are literally paying to produce milk. Yet production continues, propped up by government subsidies, soft loans from state banks, and political imperatives that… well, they just don’t follow normal market rules.

The Hard Math Behind Mid-Size Dairy Challenges

USDA’s Agricultural Resource Management Survey data reveal a stark cost differential across farm sizes. And this isn’t about who’s a better farmer—it’s about structural economics that management alone can’t overcome.

Looking at production costs per hundredweight from the USDA’s dairy cost and returns estimates:

Farms with fewer than 200 cows: generally running $23.68-33.54/cwt

200-499 cows: around $20.85/cwt

500-999 cows: typically $18.93/cwt

1,000-1,999 cows: averaging $17.39/cwt

2,000+ cows: down to $16.16/cwt

The brutal economics of scale: Mid-size operations face an automatic $4.69/cwt cost disadvantage ($359,609 annually for a 300-cow dairy) that no amount of management skill can overcome. Market prices lock them into structural losses through 2027.

With USDA’s World Agricultural Supply and Demand Estimates showing milk prices at $16.50-18.00/cwt through 2026-2027, you can see the problem pretty clearly. A 300-cow operation faces production costs about $4.69/cwt higherthan a 2,000-cow operation. On annual production of, say, 76,650 cwt, that’s a $359,609 competitive disadvantagebefore you even wake up in the morning.

What’s really interesting is research by agricultural economists at Wisconsin showing that management quality accounts for only about 22% of the variance in profitability. The other 78%? That comes from herd size and the resulting cost structure. Labor costs alone create roughly a $2.60/cwt difference between mid-size and large operations. Fixed overhead adds another $3.33/cwt disadvantage. Even feed costs—where you’d think everyone’s buying the same corn—show about a $1.40/cwt advantage for large operations through volume purchasing and precision nutrition programs.

You just can’t manage your way out of that kind of structural disadvantage, no matter how good you are. And believe me, I’ve seen some excellent managers struggle with this reality.

Three Paths Forward: Finding Your Best Option

After talking with farm management specialists at Penn State Extension and Farm Credit consultants across the Midwest, three viable paths keep emerging for dairy operations facing this transformation. Each has specific requirements that need honest evaluation.

Path 1: Scale to Competitive Size (1,500-2,500+ cows)

I’ve noticed that farmers considering expansion need to tick quite a few boxes before this makes sense. Agricultural lenders at CoBank and Farm Credit are generally looking for:

Debt-to-asset ratio below 40% before you even start

At least $300,000-600,000 in working capital reserves (expansion disrupts cash flow for 12-24 months, as many of us have learned the hard way)

Access to $8-15 million in financing

Another 500-800 acres of land are available

Confirmation from your processor that they can handle the additional volume

As consultants like Tom Villenga in Wisconsin often explain, it typically takes 18-24 months from groundbreaking to positive cash flow. And farmers need to understand—you’re not really farming at that scale anymore. You’re managing 8-15 employees and running a business. It’s a completely different skill set.

Path 2: Pivot to Premium Markets

This development suggests a real opportunity for the right operations. Organic milk premiums are running $8-12/cwt over conventional, based on CROPP Cooperative’s October market reports. But location matters enormously here.

Economists at Cornell’s Dyson School have documented that you need to be within 75 miles of a metro area with a population of 250,000+ to make premium markets work. The affluent consumers who pay those premiums are concentrated in specific geographic areas—that’s just the reality of it.

What farmers are finding crucial: secure your premium buyer contracts before beginning any conversion. I keep hearing stories—you probably have too—of operations that completed expensive organic transitions only to discover no premium buyers existed in their region. That’s a tough spot to be in.

The conversion timeline’s no joke either. It’s a full three years before you see those organic premiums, based on USDA’s National Organic Program guidelines. During that time, you’re incurring organic costs while still selling at conventional prices. Budget $50,000-100,000 for a 300-cow operation to make that transition, based on case studies from Vermont’s sustainable agriculture program.

Path 3: Strategic Exit While Preserving Equity

Nobody likes talking about this option, but sometimes it’s the smartest move. Industry consultants like Gary Sipiorski at Vita Plus, who’s been working with dairy operations for decades, often point out that strategic exit while you’re solvent preserves 70-85% of equity. Forced liquidation after covenant violations? You’re looking at 30-50% if you’re lucky.

Here’s something most farmers don’t know about: Section 1232 of the bankruptcy code can save substantial capital gains taxes for farmers with highly appreciated land. Agricultural bankruptcy attorneys who specialize in this area explain that if appropriately executed before selling assets, farmers can save $200,000-500,000 in capital gains taxes through a strategic Chapter 12 filing. It’s worth understanding these provisions even if you hope never to use them.

The indicators suggesting this path include working capital trending below 6 months of operating expenses, being 55+ without a committed next generation, or simply having no viable path to profitability at forecast milk prices.

The Asset Value Reality Nobody Discusses

What’s particularly concerning—and I don’t hear this discussed nearly enough at co-op meetings—is how quickly farm asset values deteriorate when a region’s dairy sector struggles.

Mark Stephenson at Wisconsin’s Center for Dairy Profitability has done extensive work on this. When dairy becomes structurally unprofitable in a region and multiple farms exit simultaneously, those anticipated liquidation values farmers count on for retirement… they simply evaporate.

Think about it. Land you believe is worth $9,000 per acre based on that sale down the road last year? When 8-12 dairy farms in your county hit the market simultaneously with no qualified buyers, you might see $6,000-6,500. I’ve watched it happen in several Wisconsin counties over the past three years, and it’s heartbreaking.

Equipment values face the same compression. That 2018 John Deere you figure is worth $75,000? When six similar tractors are at auction within 50 miles, you might get $48,000. And dairy-specific infrastructure—milking parlors, freestall barns—they become nearly worthless without other dairy farmers to buy them.

Based on Farm Financial Standards Council accounting principles, farms in declining dairy regions face combined monthly wealth destruction of $23,000- $ 55,000 from operating losses and asset depreciation. Your farm’s value isn’t static—it’s changing every month based on regional dynamics.

Time destroys wealth faster than you think. A 300-cow operation valued at $1.5M today becomes $322K in 12 months—78% wealth destruction. Strategic exit today preserves $1.16M (77.5%). Forced liquidation after covenant violations leaves you with $323K (21.5%). That’s a $839,700 difference for waiting one year.

What Co-ops Are Saying vs. Market Reality

Comparing cooperative messaging against actual market data reveals… well, let’s call it a disconnect.

When co-ops say “market conditions will stabilize by late 2026,” they’re technically correct—USDA projects Class III prices around $18-19/cwt. But here’s what they’re not emphasizing: that’s still below breakeven for operations under 1,000 cows while remaining profitable for 2,000+ cow operations. In other words, “stabilization” actually accelerates consolidation rather than providing relief.

This disconnect partly stems from structural conflicts within the cooperative model itself. Market analysts like Phil Plourd at Blimling and Associates have documented how co-ops need maximum milk volume to spread fixed processing costs. They have an incentive to keep members producing, even at a loss—it’s just the nature of the cooperative structure.

What really caught my attention was data from the National Milk Producers Federation showing that DFA lost over 500 member farms in 2023. They’re anticipating shrinking from current levels to around 5,100 farms by 2030. That’s roughly a 9-10% annual attrition rate among their membership. If co-ops are successfully supporting family farms, why are 280+ farms leaving each year?

Looking Ahead: The 2028 Dairy Landscape

Based on consolidation trends documented by Rabobank’s dairy research group and factoring in China’s sustained market pressure, here’s what I think we’re looking at:

Total U.S. dairy farms will likely decline from today’s roughly 31,000 to somewhere around 20,000-22,000 by 2028—that’s a 29-35% reduction. But the distribution shift is even more dramatic.

Operations with 2,000+ cows, currently about 800 farms producing 46% of U.S. milk, will probably expand to 1,200-1,400 farms producing 60-65%. Meanwhile, that middle tier—200-999 cow operations in commodity production—faces a 75-85% reduction. It’s stark, but that’s what the data suggests.

What’s emerging are essentially three viable farm types:

Industrial-scale operations (2,000-5,000+ cows) competing on efficiency

Lifestyle farms (<100 cows) subsidized by off-farm income

The middle? It’s disappearing. And that’s a huge change for our industry.

Your Action Plan: Practical Steps for Right Now

For farmers reading this in late 2025, your window for strategic decision-making is measured in months, not years. Here’s what I’d suggest doing immediately:

This week: Calculate your true working capital per cow. Take current assets minus current liabilities, divide by cow count. If you’re below $800 per cow, you need to act fast.

Schedule a frank conversation with your banker about exactly where you stand relative to loan covenants. Don’t wait for them to call you—be proactive about it.

Have an honest family discussion about the farm’s actual financial position. I know these conversations are tough, but they’re essential.

And listen, if stress is affecting your sleep, relationships, or wellbeing, please reach out for help. The National Suicide Prevention Lifeline at 988, Farm Aid at 1-800-FARM-AID, and Iowa Concern at 1-800-447-1985 all have counselors who understand what you’re going through. There’s no shame in needing support—we all do sometimes.

Within 30 days: Engage an independent agricultural consultant—not your co-op field rep—for an honest viability assessment. Yes, it’ll cost $2,000-5,000, but it could save you hundreds of thousands in the long run.

Meet with an agricultural attorney who understands Section 1232 provisions and strategic options. Get real liquidation values for your assets from agricultural appraisers, not optimistic book values.

Develop three scenarios with your family: scale up, premium pivot, or strategic exit. Run the numbers on each. Be honest about what’s realistic for your situation.

The Success Story: Learning from Those Who’ve Navigated Change

Let me share a story about a family I’ll call the Johnsons—they represent what I’m seeing across eastern Iowa and similar situations throughout the Midwest. Third-generation dairy farmers with 380 cows faced this exact decision in early 2024, when working capital started to dwindle.

After careful analysis with their consultant, they executed a strategic exit in May 2024, using Section 1232 provisions to preserve an additional $180,000 in capital gains taxes. Today? They’re debt-free. The husband works as a herd manager for a 2,500-cow operation nearby. They kept their house and 40 acres. Their adult daughter started veterinary school this fall.

But let me be honest about something—when he talked with me about it, he said it was the hardest year of his life. “Watching that auction… seeing our cows loaded on someone else’s trailer… I couldn’t watch. Had to walk away.” His voice caught a bit. “Four generations of Johnsons milked those cows. Four generations.”

The identity crisis is real. The sense of failure—even when you’re making the smart financial decision—it’s overwhelming. He told me he didn’t go to the coffee shop for three months because he couldn’t face the questions. Couldn’t face being “the Johnson who lost the farm,” even though he’d actually saved his family’s financial future.

“But you know what?” he continued, “Looking at our grandkids playing in the yard, knowing they’ll have college funds, knowing we can sleep at night without worrying about milk prices… we made the right call. Hardest thing I ever did. Also, the smartest.”

That’s the kind of brutal honesty we need right now. Strategic exit isn’t failure—it’s protecting what matters most. But that doesn’t make it easy.

Key Takeaways for Your Decision

What this all boils down to is understanding that we’re experiencing a structural transformation, not a typical cyclical downturn. China’s demographic shift and production surplus represent permanent changes to global dairy demand—at least for the foreseeable future.

The $3-5/cwt cost advantage that 2,000+ cow operations enjoy over 200-500 cow farms simply can’t be overcome through better management. It’s structural, and we need to accept that reality.

Every month of delay in stressed markets costs not just operating losses but also substantial asset-value deterioration—that hidden wealth destruction that nobody talks about at the coffee shop.

Three paths remain viable for most operations: scaling to 1,500+ cows if you have the resources, pivoting to premium markets with guaranteed contracts, or executing a strategic exit while preserving equity.

The window for making these decisions strategically rather than under duress is closing. Industry dynamics suggest farmers need to commit to their chosen path by the end of Q1 2026.

And please, remember this: with farmer suicide rates running 3.5 times the national average according to CDC data, no amount of farm equity is worth sacrificing your wellbeing or family relationships. Your family needs you more than they need the farm.

The dairy industry’s undergoing its most significant transformation in generations. Like that shift from hand milking to mechanical systems, this change will determine which farms exist in 2028 and which become memories. The farmers who acknowledge this reality and act decisively—whether scaling up, pivoting to premium, or strategically exiting—will be the ones sharing stories of resilience rather than regret.

The choice, and the timeline, are yours. But that window for making the choice? It’s closing faster than most of us realize. What matters now is making an informed decision while you still have options.

KEY TAKEAWAYS:

This is structural, not cyclical: China’s 42 million tonne surplus reflects permanent demand loss from a 48% birth rate collapse—recovery isn’t coming

Your management can’t fix physics: 300-cow dairies face an automatic $359,609 annual disadvantage versus 2,000-cow operations at any skill level

Three paths remain viable: Scale past 1,500 cows ($8-15M investment), pivot to premium markets with secured contracts, or execute strategic exit today at 70-85% equity (vs. 30-50% in forced liquidation)

Every month costs $23,000-55,000: Operating losses plus hidden asset depreciation are turning $1.5M farms into $700K distressed sales

Control your exit or it controls you: Make your decision by Q1 2026 while you have options—after that, loan covenants decide your fate

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Half of U.S. dairy farms will vanish by 2030. The survivors? They’re making one decision differently.

EXECUTIVE SUMMARY: The math stopped working when milk prices crept up 16% but diesel doubled and feed jumped 40%—that’s why 2,800 dairy farms close annually and milk checks now arrive with crisis hotline cards. Most producers don’t realize they have just 18 months from first losses to forced decisions, and waiting those extra six months costs families $380,000 in preserved equity. Strategic exits at month 8-10 save $400,000-$680,000; forced liquidations leave $100,000-$200,000. With half of America’s 26,000 dairy farms vanishing by 2030 and kids as young as 14 running milking shifts, this isn’t about failure—it’s about timing. This article provides the exact month-by-month timeline, real alternatives that work (partnerships, robotics, organic), and the framework to make informed decisions while you still have choices. Because sometimes the bravest thing you can do is preserve what three generations built before it’s too late.

So I was talking with a producer last week—you know how these conversations go, catching up at the feed store or after a meeting—and he mentioned something that really stuck with me. His milk check came with a little card tucked in. Mental health resources, crisis hotline numbers.

After thirty years in this business, that’s…well, that’s something new.

And it got me thinking about what we’re all seeing out there. The combination of labor challenges, these heat waves that seem to hit harder every year, and margins that just don’t pencil out anymore—especially for those 200 to 400 cow operations that used to be the heart of rural communities. You know the ones I’m talking about. Maybe it’s your operation.

Here’s what’s keeping me up at night: Industry projections from Rabobank show we’re losing about 2,800 farms every year now—that’s 7 to 9% of all U.S. dairy operations annually. The economists I trust—folks at Cornell PRO-DAIRY, Wisconsin’s Center for Dairy Profitability, the people who really understand our business—they keep talking about this 12 to 18 month window. That’s what you’ve got when things start going sideways. And what do you do in those months? The difference can be hundreds of thousands of dollars. I’m not exaggerating. We’re talking about preserving what your family built versus watching it disappear.

What’s Really Different in the Barn These Days

You probably know this already, but walk into any mid-sized dairy operation today, and it feels different than it did five years ago. Can’t quite put your finger on it at first, but then you realize—it’s quieter. Not the good kind of quiet either.

Five years back, you’d hear workers talking during morning milking —maybe some Spanish conversation —and teenagers grumbling about the early start (though secretly learning the trade). Now? Often, it’s just the owners — usually in their fifties, maybe early sixties — doing the work of four or five people. And they look exhausted.

What’s interesting is how the numbers back up what we’re feeling. The National Milk Producers Federation’s 2025 workforce data shows that immigrant workers make up about 51% of our workforce, but here’s the kicker—they produce 79% of the milk. Think about that for a second. And these folks, they’re operating under a kind of stress that wasn’t there before. I see it myself. Unfamiliar truck pulls up? Conversations stop. Workers keep phone numbers in their pockets now—family contacts, immigration attorneys. That’s become normal, and it shouldn’t be.

The age thing is really something else. Was talking to a Wisconsin producer recently who’s got two helpers, both in their seventies. “There’s just no pipeline of younger workers,” he told me. And he’s right—USDA’s Economic Research Service documented that agricultural employment dropped by 155,000 workers between March and July this year. That’s 7% of our workforce, gone in four months.

But here’s what really gets me—and I hate even saying this—we’ve got fourteen-, fifteen-year-old kids running full milking shifts. Not helping out, not learning from Dad or Grandpa. Running the shift. Because there’s literally nobody else. That’s not how it’s supposed to work.

When Everything Comes at You at Once

The Labor Situation Can Change Overnight

Let me tell you about what happened in Lovington, New Mexico, this past June. Shows you how fast things can go south.

Isaak Bos was running his operation like any other day when Homeland Security showed up. Full enforcement action, armed agents, the whole thing. By the time they left? Sixty-four percent of his workforce was gone. Eleven were arrested on the spot, and another twenty-four were let go when their papers didn’t check out. The Albuquerque Journal covered it extensively—this isn’t hearsay, it’s a documented fact.

“Milk production had effectively ceased,” Bos told reporters. “We’re barely able to keep going.”

Here’s what really opened my eyes—UC Davis agricultural economists have been tracking this, and their 2025 research found that when raids happen, farms that haven’t even been touched lose 25 to 45% of their workers. They just stop showing up. Can’t blame them, really. Word travels fast in these communities. One raid in Vermont affects operations in Wisconsin, Idaho, and California. Everyone’s on edge.

Heat Stress Is Getting More Expensive Every Year

While we’re scrambling for workers, the heat’s becoming a bigger problem than most people realize. And I mean, we all feel it, right? But the numbers are sobering.

This study from Science Advances—Dr. Nathaniel Mueller and his team published it this year—found that one day of extreme heat cuts milk production by up to 10%. And here’s the kicker: those effects stick around for more than ten days. Small farms, the ones under 100 cows? According to the University of Illinois farmdoc daily analysis from March, they’re losing 1.6% of production annually just to heat stress. That’s nearly 60% worse than bigger operations that can afford better cooling.

Let me put this in real terms. If you’re running a small operation, maybe clearing $60 to $175 per cow annually (and that’s being optimistic these days), Texas A&M and Florida extension economists calculate you’re looking at heat stress losses of $400 to $700 per cow. Even up here in the Midwest, we’re seeing impact. Pennsylvania operations are reporting similar challenges. California producers? They’re dealing with both heat and water restrictions—double whammy.

Now, the extension folks—and they mean well—they recommend cooling systems. Tunnel ventilation, evaporative cooling, all that. Penn State, Wisconsin, and Cornell all cite $70,000 to $85,000 for a 200-cow operation. But here’s the thing nobody wants to say out loud: if you’re already losing sixty, seventy thousand a year, where’s that money coming from? Banks aren’t lending for improvements when you can’t show positive cash flow.

The Math Just Doesn’t Work Anymore

November’s milk price came in at $21.55 per hundredweight. But you know how it is—after co-op deductions, quality adjustments, hauling…you’re seeing less. Sometimes a lot less.

Here’s what’s interesting—and I really wish I could draw you a picture here because it’s striking when you see it laid out. I was looking at the cost changes since 2020, and the spread is just brutal. Let me walk you through what I mean:

Back in 2020, we had milk at about $18.50 per hundredweight. Your basic feed costs, let’s index them at 100 to make it simple. Labor was running around $16 an hour if you could find it. Diesel? About $2.20 a gallon.

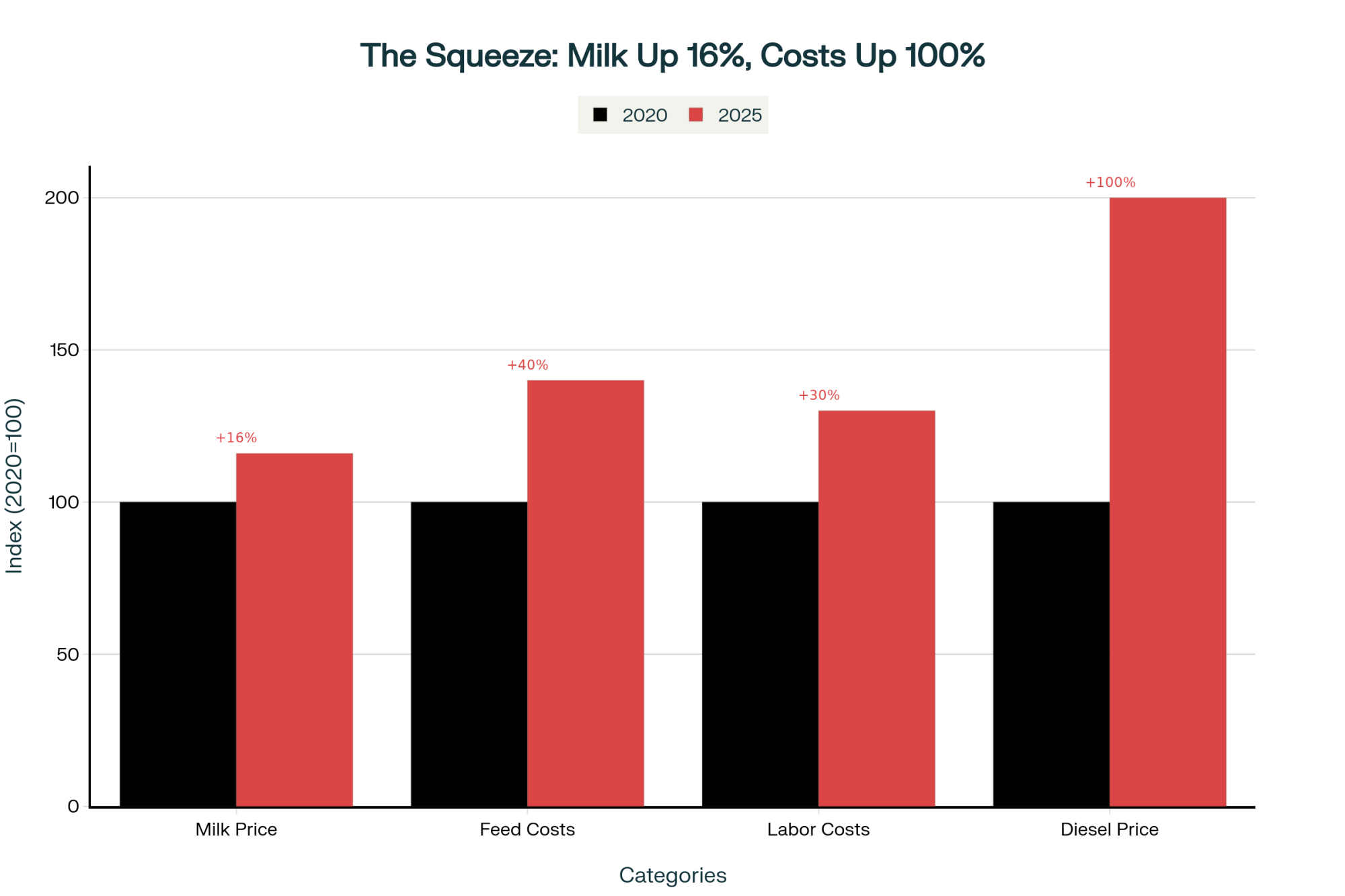

Fast forward to now, 2025. Milk’s up to $21.55—hey, that’s 16% better, right? But look at everything else. Feed costs have jumped 40% from that baseline. Labor—if you can even find workers—is running $20 to $21 an hour, up 30%. And diesel? Don’t get me started. We’re looking at $4.40 a gallon in many areas. That’s doubled.

While milk prices crawled up 16% since 2020, diesel doubled, feed jumped 40%, and labor climbed 30%—creating an unsustainable cost structure that explains why 2,800 dairies close annually

So you’ve got milk prices creeping up by 16% while your inputs shoot up by 30%, 40%, or even 100%. That gap between what you’re getting paid and what you’re paying out? That’s where your equity bleeds away, month after month. When the milk check doesn’t cover the feed bill, you’re basically robbing Peter to pay Paul.

The bankruptcy numbers tell the same story—259 dairy farms filed Chapter 12 between April 2024 and March 2025. That’s a 55% jump from the year before. But here’s what that doesn’t capture—for every farm that files, there’s probably another one or two quietly selling off equipment, maybe some land, trying to restructure without the paperwork. The stigma’s real, you know?

Small and mid-size dairies hemorrhaged 42% of operations while mega-farms grew 16.8%, now controlling nearly half of all U.S. milk production—proving economies of scale aren’t optional anymore

Understanding That 12 to 18 Month Timeline

When the economists at Cornell and Wisconsin talk about this 12- to 18-month window, they’re not being dramatic. Let me walk you through what this looks like, based on what I’m seeing across multiple operations. Think of it as a composite—no single farm, but patterns I see repeatedly.

Months 1 Through 6: The Slow Bleed

You start drawing more heavily on your operating line. Maybe go from $140,000 to $165,000 over a quarter. It feels manageable because you’ve still got credit available.

You start making small compromises. Put off that gutter cleaner repair—sure, it means 90 minutes of manual scraping every day, but you save $3,200. You match a wage offer you can’t really afford because if that last good employee leaves, you’re done.

The bank might restructure some debt and convert short-term debt to long-term debt. Feels like breathing room, right? But you’re just locking in obligations you probably can’t meet long-term.

Months 7 Through 12: Options Starting to Close

Your credit line’s getting close to maxed out. The lender—and these are good people who want to help—they start asking for monthly financials instead of quarterly. That’s never a good sign, as you probably know.

You can’t defer maintenance anymore, but you can’t afford it either. You’re one major breakdown away from crisis. One bad bout of mastitis in the fresh cow group. One compressor failure.

This is when those hard conversations happen. I know a couple in Vermont who have been farming for 40 years. She found him in the barn at 2 AM, just standing there. “We need to talk about what we’re doing,” she said. But they convinced themselves spring prices would turn things around. In my experience…they rarely do.

Months 13 Through 18: Decision Time

Banks lose confidence. You’ve violated debt covenants—maybe debt-to-asset ratio, maybe working capital requirements. Your options are bankruptcy or a forced sale. Any equity you’ve got left needs immediate action if you want to preserve it.

By now, that window for a strategic exit? It’s mostly closed. Operations that could’ve preserved $400,000 to $600,000 in family wealth six months earlier are looking at scenarios where keeping $100,000 to $200,000 feels like a win.

The Conversation Nobody Wants to Have

Here’s something we need to be honest about, even though it’s uncomfortable: strategic exits made early preserve dramatically more wealth than waiting for the bank to force your hand.

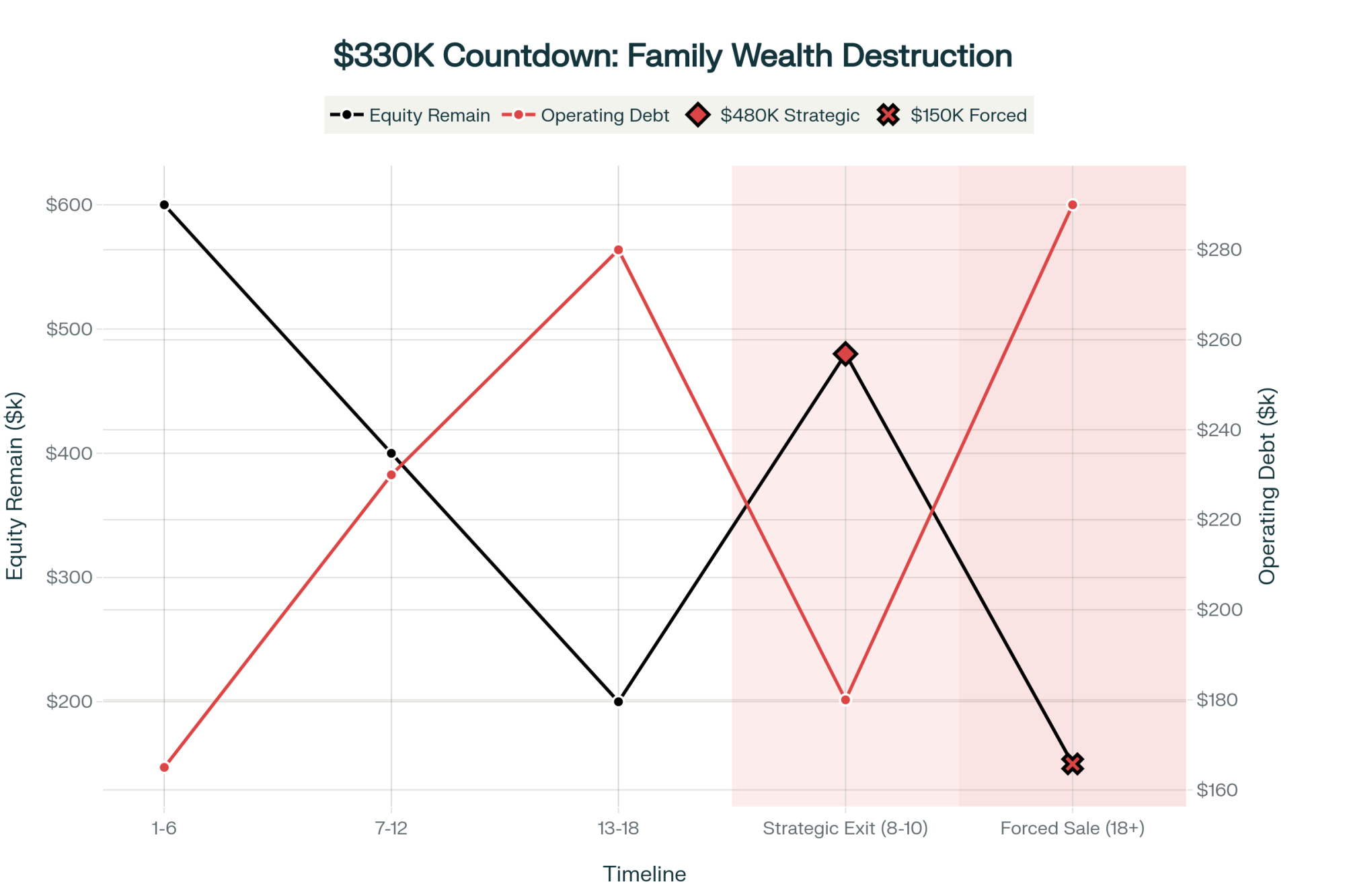

The brutal math of waiting: Strategic exits at month 8-10 preserve $480,000 in family wealth, while forced liquidations at month 18+ leave just $150,000—a $330,000 penalty for six months of denial

Let me break down what I’ve seen happen, based on actual auction results and sale data from 2025:

Strategic Exit (while you’ve still got 7-9 months of runway):

Sell your herd voluntarily, maybe get $1,850 per good cow

Equipment goes through a proper auction with time to market it right

Real estate gets listed properly, not fire-sold

Families walk away with $400,000 to $680,000

Forced Liquidation (month 18 and beyond):

Distressed sale, maybe $1,400 per cow if you’re lucky

Equipment auction under pressure, buyers know you’re desperate

Real estate sells fast and cheap

Families keep $100,000 to $200,000

That three to five hundred thousand dollar difference? That’s college funds. That’s retirement. That’s the chance to start over without crushing debt. And the only variable is timing.

As a Pennsylvania dairyman who went through this last year told me: “The hardest part was admitting we needed to exit. Once we did, we realized we should’ve made the decision six months earlier. Would’ve kept another $200,000.”

What Producers Are Actually Doing

Making Do with What They’ve Got

Was talking to a reproductive specialist in Florida last week—smart guy, been around—and he told me about a client who couldn’t afford a proper cooling system. Five thousand for misters was out of reach. So this producer rigged up a garden sprinkler on a fence post in the holding pen.

“It kept cows from dropping 10 to 20 pounds of production per day,” he said. “Bought him a month to generate some cash flow for proper cooling.”

That’s the reality for a lot of us, isn’t it? Hardware store solutions. Making do. It’s not ideal, but it keeps you going another day.

Partnerships—Sometimes They Work

Three neighbors in Idaho pooled their operations last year. Formed an LLC, consolidated everything. Individually, they were all questionable. Together? They’re actually competitive now.

But finding the right partners is tough. You need compatible management styles, similar work ethics, and—here’s the kicker—about $75,000 to $150,000 just for legal setup and restructuring. Folks who track these things estimate that maybe one in four or five partnership attempts actually succeeds long-term. The rest fall apart, usually over management disputes, within eighteen months. The Milk Producers Council has been documenting these partnerships, and the success stories all have one thing in common: clear, written agreements about everything from work schedules to exit strategies.

Some Folks Are Finding New Paths

It’s not all doom and gloom, and I want to be clear about that. Some operations are finding ways forward that work.

Several Vermont farms I know of are transitioning to organic. USDA’s organic price reports show a $38 per hundredweight price, compared with the $21.55 conventional price. But it’s brutal—the Northeast Organic Dairy Producers Alliance documents that it takes years and costs hundreds of thousands, while your revenues drop during the transition. You need deep pockets to weather that storm.

There are operations near Philadelphia, Boston, places like that, doing on-farm processing. Selling direct at $12 per gallon to customers who want the “farm experience.” One New York operation I visited invested $380,000 in processing facilities and visitor infrastructure. It’s working for them, but you need the right location and wealthy suburban customers nearby.

In Ohio, the Johnsons invested $800,000 in robotic milkers—but only after selling 60 acres to raise capital. Three years later, they’re viable with 300 cows and two full-time people. Not everyone has 60 acres to sell, but for those who do, technology might be an option. Just remember, the payback period is typically 7-10 years if everything goes right.

And here’s something interesting—completely legal, but not widely known—strategic bankruptcy under Section 1232 of the tax code can actually preserve more wealth than conventional sales in certain circumstances. The provision treats specific capital gains as dischargeable debt. You need a good attorney who understands agriculture, but it’s an option worth knowing about.

The Human Cost Nobody Talks About

We focus so much on the financial side, but the human toll…that’s what really matters, isn’t it?

The CDC found that farmers are 3.5 times more likely to die by suicide than the general population. Dr. Andria Jones-Bitton’s research at the University of Guelph documented that 68% of farmers experience chronic stress. Nearly half meet clinical definitions for anxiety. About 35% for depression.

Think about what this means for families. Farm wives who’ve managed the books and fed calves for twenty-five years suddenly need to find outside employment at fifty with no traditional work history. Kids who worked adult hours on the farm, watching it fail, wondering if it was somehow their fault. The weight of being the generation that “lost the farm”—that stays with people.

A dairy wife from Minnesota shared something that really stuck with me: “Being married to a farmer means putting everything else on hold from April to October, just trying to keep your husband from breaking.” Another described herself as essentially a single parent because her husband’s always in the barn, always stressed, never really present even when he’s physically there.

Where This Is All Heading

Small and mid-size dairies hemorrhaged 42% of operations while mega-farms grew 16.8%, now controlling nearly half of all U.S. milk production—proving economies of scale aren’t optional anymore

Industry projections are sobering—we’ll lose 7 to 9% of operations annually through 2027. Let me put that in real numbers so you can picture what’s happening:

The Decline We’re Looking At:

2020: We had 31,657 dairy operations according to the Census of Agriculture

2022: Down to 28,900

2024: About 26,400 (estimated)

Right now, 2025: Around 26,000 operations

Now, if we keep losing 7% a year like the projections suggest:

2026: We’re looking at 24,180 operations

2027: Down to 22,487

2028: About 20,893

2029: Roughly 19,430

2030: Somewhere between 13,000 and 18,000 operations

From 31,657 farms in 2020 to a projected 18,000 by 2030—this isn’t gradual evolution, it’s an industry extinction event claiming nearly 8 farms per day for the next five years

Some folks think consolidation could accelerate in those final years—once you hit certain thresholds with processing capacity and infrastructure, things can snowball. That’s why some projections go as low as 12,000 to 14,000 farms by 2030.

Picture that trend line…it’s not a gentle slope. We’re talking about losing half—maybe more—of all U.S. dairy farms in just five years. Each of those data points? That’s hundreds of families making the decision we’ve been talking about.

If this keeps up—and honestly, I don’t see what would change it—by 2030, we’re looking at:

Going from today’s 26,000 farms down to maybe 13,000 to 18,000 (could be even lower if things accelerate)

Operations with over 1,000 cows controlling 65 to 72% of all production

Production moving to Idaho, New Mexico, Texas—where those economies of scale work better

Traditional dairy states—Wisconsin, Vermont, upstate New York, and Pennsylvania Dutch Country—are losing half to two-thirds of their farms

You know, this consolidation might create certain efficiencies. Sure. But it reduces resilience. When 65% of your milk comes from fewer, larger operations, any disruption—such as a disease outbreak, a weather event, or another immigration raid—has massive impacts. We got a taste of this during COVID. Next time? It’ll be worse.

What You Need to Know Right Now

If Your Operation’s Losing Money

First thing—and I mean this week—sit down and calculate your actual runway. How many months can you really keep going at current burn rates? Be honest with yourself. This isn’t the time for optimism.

Get a confidential consultation with someone who understands agricultural transitions. Your state extension service can usually connect you. Do it now while you still have options. Every month you operate at a loss, you’re converting twenty to thirty thousand dollars in family wealth into expenses you’ll never recover. That’s real money that could be in your pocket.

Look at all your options. Strategic exit while you’ve got equity to preserve. Partnerships, if you’ve got the right neighbors and the relationship to make it work. Maybe pivoting to specialty markets if you’re positioned for it—A2 milk premiums, grass-fed certification, direct marketing if you’re near population centers. Scaling up if—and this is rare—you somehow have capital access.

But here’s what matters most: your family’s wellbeing trumps everything else. Your mental health, your marriage, your relationship with your kids—all of that matters infinitely more than what the neighbors think.

For the Lenders and Consultants

I know you’re reading this too. If you’re working with struggling operations, please—have honest conversations about strategic exits before all the equity’s gone. Stop promoting solutions that require capital these farms don’t have. That robotic milking system might be amazing technology, but not if the farm goes bankrupt before the ROI shows up.

Communities need to start planning for transitions. I know it’s hard to accept, but pretending family dairy’s going to reverse these trends somehow…that’s not helping anyone.

Making the Tough Call

I keep thinking about this Wisconsin family I know—real people, not a composite. They made their exit decision with about 8 to 10 months left in their viability window. Walked away with $482,000 in preserved equity. If they’d waited until the bank forced their hand? They’d have kept less than $200,000.

That $280,000 difference came down to one thing: having the courage to make a strategic decision while they still had choices.

For all of us looking at that 12 to 18 month countdown—and you know who you are—the question isn’t whether the farm continues. We can read the economics. The question is whether you preserve the wealth you’ve built through strategic action or lose it through delay.

Getting Help

If you’re struggling—financially, mentally, or both—please reach out. There’s no shame in it.

Mental Health Support:

National Suicide Prevention Lifeline: 988

Farm Aid Hotline: 1-800-FARM-AID

AgriStress Helpline: 1-833-897-2474

Financial Planning:

Your state extension service has transition specialists

Wisconsin Farm Center: 1-800-942-2474

Pennsylvania Center for Dairy Excellence: 1-888-373-7232

Cornell PRO-DAIRY programs

Michigan State Extension: 1-888-678-3464

Look, the clock’s ticking on thousands of operations. Understanding the timeline, recognizing your options, and—this is the hard part—acting while you still have choices…that’s what determines whether you preserve what three generations built or watch it disappear.

The decision’s incredibly difficult. I get that. But the math? The math is becoming clearer every day.

And if you’re reading this thinking, “he’s describing my farm”… maybe it’s time for that conversation you’ve been avoiding. Better to have it now, on your terms, than later on someone else’s.

We’re all in this together, even when it feels like we’re alone. And sometimes the bravest thing you can do is know when it’s time to preserve what you can and move forward.

KEY TAKEAWAYS

Your 18-month countdown starts the day you can’t pay all bills on time—most farmers don’t realize until month 12, when half their equity is already gone

The $380,000 decision: Exit strategically at month 8-10, keeping $480K, or wait for forced liquidation at month 18, keeping $100K (real Wisconsin example)

Red flags demanding immediate action: Bank requests monthly financials, your 14-year-old runs milking shifts, you’re choosing between feed bills and diesel

Three viable options remain: Strategic exit (preserves family wealth), partnerships with neighbors (1 in 4 succeed with $75-150K legal costs), or technology pivot (requires $800K+ capital)

This week’s action: Call your state extension service for confidential consultation—it’s free, and waiting another month costs you $20-30K in family wealth that’s gone forever

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Why 2025 Could Be the Most Profitable Year for Dairy Farmers Yet! – This piece provides a counter-strategy to the exit-focused mindset, demonstrating how to leverage lower input costs, nutritional science, and smart herd management to build a stronger, more profitable bottom line in the current climate.

Global Dairy Market Recap: Mixed Signals and Opportunities – January 20, 2025 – Understand the “why” behind your milk check. This article decodes the complex global signals, from European price drops to SGX futures, helping you make smarter strategic decisions by seeing the macro-trends before they hit your farm.

Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.

Trump kills Canada dairy trade. You have 9 months until USMCA review. 3 paths: Scale to 2,500 cows, diversify income, or exit with 95% value.

Executive Summary: Trump terminated Canada trade talks this week, but dairy’s real crisis started long before—we’ve lost 15,866 farms while exports hit record highs that never reached farmers’ bank accounts. With just 9 months until the USMCA review that could reshape North American dairy, producers face three proven paths: scale to 2,500+ cows with deep pockets and $260,000 working capital, build a 300-cow diversified operation where beef-on-dairy and renewable energy generate 60% of revenue, or exit strategically while you can still recover 85-95% of assets. The traditional 500-800 cow dairy is already extinct—those operations are burning $75,000 yearly just hoping things improve. Whether it’s through mega-scale efficiency, diversified resilience, or wealth preservation, the winners have one thing in common: they’re making their move now, not waiting for political rescue.

When President Trump terminated trade talks with Canada this week after Ontario’s Reagan ad escalated tensions, it wasn’t really a surprise to anyone paying attention. But for dairy farmers already dealing with razor-thin margins and export dependency, it was the wake-up call we probably needed.

You know how it is at co-op meetings lately. The conversations have really shifted. Instead of everyone comparing notes on new parlor expansions, folks are quietly discussing beef-on-dairy premiums and asking each other about working capital reserves. And yeah, there’s definitely a lot more kitchen table discussions happening about what this whole dairy farming thing actually means for the next generation.

What’s interesting is how Trump’s latest trade disruption—combined with the USMCA review looming and both sides taking increasingly hard positions on dairy—has become the moment when something we’ve all sensed for years finally became impossible to ignore. Here’s the thing though…this wasn’t really about any single political announcement, was it?

This was just when we had to face facts: the way we’ve been thinking about dairy growth for the last two decades? It’s not working anymore.

Farm bankruptcies surged 55% in 2024 and continued climbing into 2025, signaling the most severe financial crisis for American agriculture since the pre-pandemic peak. The dramatic upturn from the 2023 low of 139 filings exposes how quickly market conditions deteriorated once government support ended.

The Stark Reality in Numbers

The data’s pretty stark when you look at it. The 2022 USDA Agricultural Census shows we lost 15,866 dairy farmsbetween 2017 and 2022. That’s around 8.8% fewer farms every single year, and it’s actually picking up speed.

Federal bankruptcy court records through July show Chapter 12 farm bankruptcies are up 55% from last year. Think about that for a second.

Up in Canada—and you probably know this already—industry reports suggest they could lose half their remaining dairy farms by 2030. And that’s with supply management protecting incomes!

But here’s what I find really encouraging, honestly. While everyone’s focused on the political drama, something pretty remarkable is happening on actual farms. The smartest producers I talk to—and I bet you know a few like this—they aren’t waiting around for Washington or Ottawa to fix things. They’re completely rethinking their operations.

The Export Story We Need to Face

So here’s something we probably need to be honest about. When the U.S. Dairy Export Council reported dairy exports hit $4.72 billion through June—up 15% from last year—we all celebrated, right?

I mean, strong cheese and butterfat export performance, Mexico and Canada buying 44% of everything we ship overseas…sounds great on paper.

But here’s what most of us didn’t want to admit…

Remember that big export surge in July? Up 53% year-over-year according to USDEC? Well, most farms I know actually saw their margins shrink. As University of Minnesota economists have been pointing out—and this really gets me—we’re basically moving product at whatever price it takes to keep the volume flowing.

The gap between export growth and what actually shows up in the milk check? That’s not temporary anymore. It’s built into the system.

And the real kicker? We’ve built our whole growth strategy on markets we can’t control. Mexico’s trade ministry has threatened tariffs three times since February. Canada literally passed Bill C-202 in June making dairy concessions legally impossible. China’s domestic oversupply situation has cut their imports 12% according to Rabobank’s September report.

With the USMCA six-year review coming July 1, 2026—that’s just 9 months away, folks—this whole export dependency thing is about to get really tested.

What Expansion Really Costs

You want to know what really gets me about expansion economics? It’s not the numbers you see in the business plan—it’s everything else that happens underneath.

Recent university expansion modeling studies show that your typical 250-to-500 cow expansion? We’re talking $5 million, give or take.

The equipment companies get $800,000 to $1.2 million right off the bat. Construction crews take another $600,000 to $900,000. Genetics companies collect their $400,000 to $600,000.

And your lender? Farm Credit Services analysis shows they’ll make roughly $1.5 million in interest over a typical 15-year term at current rates.

So before you’ve even milked one extra cow—think about this—the supply chain’s already captured $3.6 to $4.6 million. Meanwhile, if everything goes perfectly—and when does that ever happen in dairy?—Wisconsin Extension’s financial analysis suggests you might clear $3.6 million over 10 years. That’s about 3.7% annually on your equity.

The rest of the industry captured three times what you did, and they didn’t take any of the operational risk. As Corey Geiger, economist over at CoBank, mentioned in their October outlook, after almost a decade of butterfat driving milk checks, protein’s taking over as the primary value driver. And I’ll be honest, a lot of farms haven’t adjusted their feeding programs for that shift yet.

Before you’ve milked a single extra cow from that $5 million expansion, the supply chain has already captured $3.75 million—equipment dealers, contractors, genetics companies, and your lender. Meanwhile, if everything goes perfectly for a decade, you might net $3.6 million at a 3.7% annual return… while carrying 100% of the operational risk. No wonder University Extension analysts are warning farmers: the math hasn’t worked for years.

Three Ways Forward That Actually Work

The diversified 300-cow model spreads risk across six revenue streams, insulating farms from milk price volatility that’s killing traditional operations. With 55% of income from non-milk sources including beef-on-dairy premiums and renewable energy, these farms saw only 8-9% revenue drops during severe milk price crashes—versus catastrophic losses for single-stream dairies burning $75,000 annually.

Building Something Different

What’s really fascinating—and I’ve been watching this closely—is how these smaller operations with 200 to 400 cows are completely reimagining what a dairy farm can be. I’ve been looking at several Wisconsin operations that are really opening eyes.

Consider what a typical 300-cow operation in the Midwest is doing now. They’re deliberately capping herd size. Not because they can’t handle more, but because that’s the sweet spot where family labor plus two employees can run things efficiently. No dependency on visa workers or…well, you know how hard it is to find reliable help these days.

Here’s how the revenue typically breaks down on these diversified operations—this comes from Wisconsin Extension’s 2025 farm financial modeling:

Milk to the co-op: around 40-45% of revenue

Beef-on-dairy programs: 15-20%

Renewable energy (digesters, solar): 10-15%

Agritourism or direct sales: 5-10%

Custom services for neighbors: 5-10%

High-value genetics or embryos: 5-10%

When milk prices have dropped significantly—which has happened multiple times in recent years according to USDA pricing data—their total revenue only falls about 8-9%. Yeah, it hurts. But it doesn’t kill them.

Now, managing all those different income streams? That’s the challenge, honestly. As one producer told me at World Dairy Expo, “Some days I feel more like a business manager than a dairy farmer.” Learning renewable energy contracts alone can take months. But here’s the thing—that complexity gives them options their single-stream neighbors don’t have.

What I’ve noticed is many of these operations are running crossbred cows—Holstein-Jersey or three-way crosses with Swedish Red or Norwegian Red genetics. The cows average about 1,250 pounds instead of the big 1,450-pound Holsteins. Lower production per cow, sure—maybe 22,000 pounds annually versus 26,000.

But—and this is what’s interesting—University of Wisconsin research shows they’re seeing 15% better feed efficiency, $700 less per replacement based on current heifer prices, and the cows last almost five lactations instead of the 2.9 lactation national average USDA reports. The lifetime daily production actually beats the bigger cows. Go figure.

Going Really Big

Now if you’ve got deep pockets and nerves of steel, there’s another way. The 2022 USDA Census shows farms with 2,500+ cows grew from 714 to 834 operations between 2017 and 2022. They’re producing 46% of America’s milknow.

These mega-dairies—and I’ve talked to several managers recently—are running on completely different economics. They typically need debt-to-asset ratios below 40% according to what lenders are telling them. Working capital needs to be at least 15% of gross revenue.

They ship to multiple processors—you never want all your eggs in one basket, right? And you need geographic advantages for growing feed that not everyone has, especially in the Northeast.

Most important though? You need serious fortitude. When margins compress severely—which has happened multiple times in recent years according to USDA price reports—these operations are carrying $150,000 to $200,000 in monthly fixed costs regardless.

As one large-herd manager in California told me, “Scale works, but only if you can survive the valleys. We’ve restructured debt twice since 2019.”

Down in Florida, it’s even tougher. Heat stress management alone adds 15-20% to operating costs compared to northern states. But those operations are capturing fluid milk premiums that make it work—sometimes. Out in Idaho and the Mountain West, water rights are becoming the limiting factor. You can have all the cows you want, but if you can’t irrigate feed…well, you get the picture.

The Strategic Move: Preserving Equity and Wealth

This is tough to say, but for maybe 20-30% of producers, the smartest financial move might be protecting the wealth they’ve already built while they still can do it on their terms.

Paul Mitchell, an economist from Wisconsin Extension, published an analysis in January that really drives this home. If you’re losing $75,000 a year after family living expenses—and Farm Business Farm Management data suggests that describes a lot of 500-cow operations right now—you’re burning through $375,000 in retirement wealth over five years just hoping things improve.

The USMCA review hits July 2026—just 9 months away. If you’re losing $75,000 annually (typical for 500-cow operations per Farm Business data), you’ll burn through $56,000 before that trade negotiation even starts. Wait five years hoping for political rescue? You’ve incinerated $375,000 in retirement wealth. Exit now with $1.5M in equity, invest conservatively at 4%, and you’re generating $60,000 annually for life—without the stress, without the risk.

Think about this: Exit now with $1.5 million in equity, invest it conservatively at 4%—which is what most financial advisors are suggesting these days—and you’re looking at $60,000 in annual income. Wait five years? That drops to $45,000. That’s $15,000 less every year for the rest of your life.

And here’s the real kicker from Farm Credit Services of America data: farms that exit voluntarily recover 85-95% of their asset value. Forced liquidations through bankruptcy? You’re lucky to get 50-65% according to Chapter 12 trustee reports. On a $2.5 million operation, that’s a $750,000 difference.

I know producers who’ve made this strategic choice recently to preserve their retirement wealth. They’re 58, 59 years old, still healthy, and they’ve got their equity protected. Meanwhile—and this is hard to watch—their neighbors who are trying to tough it out have watched equity evaporate as milk prices stayed below production costs.

Factor

Mega-Scale (2,500+ Cows)

Diversified (300 Cows)

Traditional (500-800 Cows)

Strategic Exit

Herd Size

2,500+ head

300 head

500-800 head

Sold/leased

Working Capital Required

$260,000 (15% of revenue)

$100,000

$150,000

$1.5M preserved equity

Annual Financial Performance

+$50,000 net income

+$30,000 net income

-$75,000 annual loss

$60,000 annual (4% return)

Milk Revenue %

95%

42.5%

90%

0%

Non-Milk Revenue %

5%

57.5%

10%

100% (investment income)

Risk Level

High debt, high volume risk

Moderate, spread across streams

Critical – burning equity

Very low

Key Advantage

Economies of scale, processor leverage

Income resilience, 8-9% revenue drop in crashes

None remaining

Wealth preserved, stress eliminated

Major Disadvantage

$150K-$200K monthly fixed costs

Complex management, 6+ revenue streams

Single income stream, no buffers

Leaving the industry, emotional cost

Survival Probability

High (if capitalized)

High

Low – Already extinct

Wealth Protected

Best For

Deep pockets, Western geography

Family operations, adaptable managers

Nobody – this model is dead

Ages 55-62, declining profit farms

What Smart Producers Are Doing Right Now

Building a Real Safety Net

The farms that’ll make it through what’s coming—and I really believe this—have at least 20% of gross revenue as working capital. That’s what both Farm Credit Services and CoBank are recommending now.

For a typical 250-cow dairy bringing in $1.3 million, that means $260,000 in cash or credit you can access quickly.

Sounds like a lot, I know. But when processors delay payments—which has happened with several co-ops in recent months—you need substantial liquidity just to keep buying feed and paying people. Without that cushion, feed suppliers put you on cash-only terms fast. And then…well, you’re in real trouble.

Making the Most of Beef-on-Dairy

According to recent market reports, beef-cross dairy calves are bringing strong premiums at auction barns everywhere from California to Pennsylvania. That’s up significantly from just a few years ago. Pretty incredible, right?

Smart producers are breeding 35-40% of their cows to beef bulls—mostly Angus or Simmental genetics from the major AI companies. On a 250-cow dairy, breeding 44 cows to beef can add substantial annual revenue based on current premiums. That’s becoming 6-9% of total farm income for folks doing it right.

Even when premiums normalize to more sustainable levels in the coming years, you’re still way ahead of straight Holstein bull calves.

Beef-on-dairy calf prices exploded 115% from 2022 to 2025, hitting $1,400 per head as U.S. beef herds dropped to 64-year lows. Smart producers breeding 40% of their 300-cow herds to beef bulls are banking $21,000 annually—6-9% of total farm income. But here’s the catch: heifer replacement costs jumped 43% to $2,850 in the same period. Wisconsin operations now face a strategic dilemma: cash in on record calf prices or maintain herd genetics for the long game?

The catch? Documentation matters. Major packers are telling producers they need complete records—genetics, health protocols, everything. Can’t pay premiums without proper paperwork for their retail customers who are demanding traceability. You probably already know this, but it’s worth emphasizing.

Getting Paid for Components

With $11 billion in new processing capacity coming online through 2028 according to International Dairy Foods Association reports, processors really need consistent, high-component milk.

Several major yogurt and cheese plants in the Northeast are paying 50 cents to $1.50 per hundredweight extra for milk that’s consistently above 3.25% protein with minimal daily variation.

What surprised me when talking to procurement managers is what they really value. They’d rather have steady 3.15% protein than variable 3.25%. Their production lines need consistency more than peak levels—they can standardize up, but variation causes real problems in their processes.

Regional differences matter too. Texas and Southwest processors are more focused on butterfat consistency for ice cream production, while Upper Midwest cheese plants prioritize protein levels. But the principle’s the same everywhere—consistency pays.

On 6 million pounds annually from a 250-cow herd, a dollar premium means $60,000 more per year. That’s real money for managing what you’re already producing.

The Mindset That Makes the Difference

You know what really separates the farms that’ll make it from those that won’t? It’s what researchers at Purdue’s Center for Commercial Agriculture call “strategic clarity”—recognizing that staying in dairy when the math doesn’t work isn’t being tough or noble. It’s just expensive.

Look, everyone in the industry—your co-op field rep, banker, equipment dealer, nutritionist—they all benefit when you keep going. They make money when you borrow, produce, expand, buy inputs. They even make money at the liquidation auction if things go south. That’s not being cynical, it’s just…well, it’s how the system works.

What they don’t make money on? You deciding your wealth might grow faster outside dairy than in it. And that’s fine—it’s not their call to make. It’s yours.

What’s Coming in 2026

The USMCA six-year review starts July 1, 2026. Canada’s Parliament already passed Bill C-202 blocking dairy concessions. Mexico’s Economy Secretary has threatened retaliation multiple times this year. The export markets that looked rock-solid when Class III milk was $25 per hundredweight in 2022? Not so much anymore.

The producers who’ll do well aren’t waiting to see how this plays out. Whether it’s building multiple revenue streams like those diversified Wisconsin operations, scaling up like the Western mega-dairies, or preserving wealth through a strategic exit—the window for making these decisions on your terms is getting pretty narrow.

What I’m seeing from coast to coast—and the data backs this up—is that middle ground of 500-800 cow dairies that were supposed to be the sweet spot? That’s disappearing fast.

CoBank and Rabobank projections suggest by 2030 we’ll have huge operations milking thousands and smaller diversified farms milking a few hundred. The traditional 600-cow family dairy as we’ve known it? That model’s already becoming history.

The Choice That Matters

When you look at everything happening—Trump’s trade disruptions, farms disappearing at nearly 9% per year according to USDA data, the complete restructuring of global dairy markets that OECD-FAO documented in their 2025 Agricultural Outlook—there’s really just one question: Are you building something that can handle what’s coming, or hoping things go back to how they were?

Because hoping things get better…well, that isn’t a business strategy. It’s just an expensive way to put off hard decisions.

The producers who thrive through 2030 won’t necessarily be the ones still milking cows. Some will build these amazing multi-revenue operations generating income from six or seven different streams. Others will scale up to where the economies actually work at 3,000+ head. And yes, some will strategically preserve their wealth, keeping what they’ve built instead of watching it disappear over the next few years.

Trump terminating those trade talks this week? That didn’t cause dairy’s problems. But it sure made them impossible to ignore anymore.

For producers willing to look past the political drama and see what’s really happening, this moment of clarity—uncomfortable as it might be—gives you the chance to make good decisions while you still have meaningful options.